Generalized Dynamic Factor Models and Volatilities:

Consistency, Rates, and Prediction Intervals

Abstract

Volatilities, in high-dimensional panels of economic time series with a dynamic factor structure on the levels or returns,

typically also admit a dynamic factor decomposition. We consider a two-stage dynamic factor model method recovering the common and idiosyncratic components of both levels and log-volatilities. Specifically, in a first estimation step, we extract the common and idiosyncratic shocks for the levels, from which a log-volatility proxy is computed. In a second step, we estimate a dynamic factor model, which is equivalent to a multiplicative factor structure for volatilities, for the log-volatility panel. By exploiting this two-stage factor approach, we build one-step-ahead conditional prediction intervals for large panels of returns. Those intervals are based on empirical quantiles, not on conditional variances; they can be either equal- or unequal-tailed. We provide uniform consistency and consistency rates results for the proposed estimators as both and tend to infinity. We study the finite-sample properties of our estimators by means of Monte Carlo simulations. Finally, we apply our methodology to a panel of asset returns belonging to the S&P100 index in order to compute one-step-ahead conditional prediction intervals for the period 2006-2013. A comparison with the componentwise GARCH benchmark (which does not take advantage of cross-sectional information) demonstrates the superiority of our approach, which is genuinely multivariate (and high-dimensional), nonparametric, and model-free.

JEL Classification: C32, C38, C58.

Keywords: Volatility, Dynamic Factor Models, Prediction intervals, GARCH.

We thank Christian Brownlees, Christian Francq, and Haeran Cho for helpful comments. This paper was also presented at: “Panel Data Forecasting Conference”, University of Southern California, Dornsife, Los Angeles, April, 2019; the “6th Rimini Centre for Economic Analysis (RCEA) Time Series Econometrics Workshop”, University of Cyprus, Larnaca, June 2019, the “International Association for Applied Econometrics (IAAE) 2019 Annual Conference”, University of Cyprus, Nicosia, June 2019, and the “Workshop on High-Dimensional Data Analysis”, Durham University, June 2019.

1 Introduction

Data in high dimension unquestionably constitute one of the main challenges of contemporary statistics/econometrics, and have become pervasive in most domains related with data sciences. Time series have not escaped that evolution, and the analysis of high-dimensional time series—equivalently, large cross-sections of univariate time series or panels—today ranks among the most active topics in theoretical and applied econometrics.

The most successful methods so far in the analysis and prediction of high-dimensional time series are based on the so-called factor model approach. That approach, under its various forms, is based on a (non-observed) decomposition of the observation (a large cross-section of time series with complex interrelations) into the sum of two mutually orthogonal (all leads, all lags) components: the common component, driven by a small number of factors or common shocks, and an idiosyncratic component, with some variations in the definitions of “common” and “idiosyncratic,” and the assumptions made. Regardless of the definition adopted, the common and idiosyncratic components typically are disentangled by means of adequate cross-sectional and/or temporal aggregation of the observed time series.

Those aggregation and factor model approaches are strongly rooted in the multivariate time-series methods developed in the eighties and nineties, of which George Tiao and his collaborators have been most influential and unremittable pioneers: see, for instance, Tiao, (1972), Tiao and Hillmer, (1978), Tiao and Guttman, (1980), Tiao and Box, (1981), Tsay and Tiao, (1985), Peña and Box, (1987), and Tiao and Tsay, (1989).

The type of factor model we are considering here is the General or Generalized Dynamic Factor Model (GDFM) introduced by Forni et al., (2000), which, by taking into account all leading and lagging linear dependencies among the data, encompasses most other models, as e.g. the static factor approaches by Bai and Ng, (2002), Stock and Watson, (2002), and Fan et al., (2013). Moreover, as emphasised in Forni and Lippi, (2001) and Hallin and Lippi, (2013), beyond the usual assumptions of second-order stationarity and existence of spectral densities, the GDFM decomposition into a common and an idiosyncratic component basically does not place any structural constraints on the data-generating process. In this sense, contrary to static factor approaches, it is canonical, nonparametric and model-free. In this paper, we consider the one-sided GDFM estimation method recently described in Forni et al., (2015, 2017).

Prediction, in classical univariate and moderately multivariate time series analysis, is an obvious and natural objective; it is certainly no less crucial in high dimension. Efficient prediction, however, should exploit the amount of information available, due to the complex cross-dependencies among the many cross-sectional components, in the present and lagged values of the whole cross-section; the larger the cross-section (i.e., the higher the dimension), the more crucial the role of that information, and the more delicate its recovering. Factor models naturally have been used in the construction of point-predictors, and quite successfully so: see, e.g., Stock and Watson, (2002), Bai and Ng, (2008), Forni et al., (2018), to quote only a very few. Those authors, however, are dealing, mostly, with macroeconomic data, while less attention has been given to factor model methods in the analysis and prediction of financial returns: see, e.g. Chamberlain and Rothschild, (1983), Connor and Korajczyk, (1993), or Aït-Sahalia and Xiu, (2017). In particular, when dealing with returns, due to the presence of conditional distribution heterogeneity (of which conditional heteroskedasticity is only a very particular case), conditional volatility phenomenons are essential, and definitely should be taken into account when building conditional prediction limits or conditional prediction intervals.

Most multivariate methods available in the literature for the analysis of conditional heterogeneity are restricted to the study of conditional heteroskedasticity, and rely on parametrisations of the ARCH-GARCH or Stochastic Volatility type: see, for instance, the reviews by Bauwens et al., (2006) and Asai et al., (2006). Because of the curse of dimensionality, however, only the very simplest models can be considered in high-dimensional panels, possibly inducing a nonnegligible loss of efficiency. Among those, the factor GARCH approach is the most popular, see e.g. Diebold and Nerlove, (1989), Ng et al., (1992), Harvey et al., (1992), and Sentana et al., (2008). Static factor models directly based on volatilities have also been considered, but these fail to exploit the information contained in the idiosyncratic components of returns, see e.g. Connor et al., (2006) and Fan et al., (2015). For these reasons, Barigozzi and Hallin, (2016) introduce a two-step GDFM approach by which the nonparametric and model-free virtues of factor models are used in a joint analysis of returns and volatilities. In Barigozzi and Hallin, 2017a , that two-step GDFM is combined with a GARCH strategy in order to produce point-forecasts for volatilities (see also Trucíos et al., , 2019 for a recent example), while Barigozzi and Hallin, 2017b and Barigozzi et al., (2018) apply the same methodology in a study of the dynamic interdependencies of US and international financial markets. A two-stage factor approach similar to ours but in a static factor model setting is proposed in Chicheportiche and Bouchaud, (2015).

The objective of this paper is to combine the same two-step GDFM approach with a quantile-based construction of conditional confidence limits producing conditional interval predictions rather than point-forecasts for returns. That objective requires nontrivial consistency results on the two-step GDFM estimation method, which are not provided in Barigozzi and Hallin, (2016); Barigozzi and Hallin, 2017a ; Barigozzi and Hallin, 2017b . The first part of this paper, therefore, is devoted to a careful asymptotic analysis of the two-step GDFM. We then describe the quantile-based construction of conditional confidence limits, which we apply to a dataset of S&P100 daily returns.

The paper is organised as follows. In Section 2, we present the GDFM model for the stochastic processes of returns (levels) and log-volatilities, and give sufficient conditions for its existence and identification. Section 3.1 describes the estimation of the model, and Section 3.2 establishes the consistency properties (with rates) of the proposed estimators. In Section 4, we define the one-step-ahead conditional prediction confidence limits and intervals. In Section 5, we study the finite-sample properties of our estimators via simulations. Section 6 applies our methodology to a panel of daily returns of stocks listed in the S&P100 index and investigates the resulting coverage performance. In Section 7, we conclude. Proofs are postponed to an Appendix.

Notation

The sub-exponential norm of a scalar random variable is defined as (see e.g. Definition 5.13 in Vershynin, , 2012). The transposed complex conjugate of a complex vector is denoted as and . For an hermitian complex matrix with generic entry and largest (in modulus) eigenvalue , let and . As usual, stands for the lag operator, such that, given a stochastic vector process , for any integer and any . Last, we denote by the indicator function of an event .

2 A General Dynamic Factor Model for levels and volatilities

We throughout assume that all stochastic variables in this paper belong to the Hilbert space , where is some common probability space. We study double-indexed stochastic processes of theform , with -dimensional sub-processes , . In practice, we deal with the finite observed realisation

of . In the empirical application of Section 6, the ’s are observed values of daily stock returns, and we therefore call the “levels” process. The assumptions in Section 2.1 are mainly taken from Forni et al., (2017), with some modifications, mostly concerning the idiosyncratic components. On the other hand, the assumptions in Section 2.2 are new and are related to the log-volatility proxies originally introduced in Barigozzi and Hallin, (2016); Barigozzi and Hallin, 2017a .

2.1 Model and assumptions for levels

The Generalized Dynamic Factor Model (GDFM) for the levels process is a decomposition of into

| (2.1) |

with

| (2.2) |

where stands for the expected value of and the processes and are mutually orthogonal (at all leads and lags) - and -dimensional white noises, respectively. Call the process of common factors or common shocks and the process of idiosyncratic shocks; and are ’s common and idiosyncratic components, respectively.

Assumption (L1).

-

(i)

the dimension of does not depend on ; the process is second-order white noise, with mean and diagonal positive definite covariance ;

-

(ii)

writing for the coefficient of in , there exists a constant such that for all ;

-

(iii)

the process is second-order white noise, with mean and positive definite covariance ; moreover, for all and such that ;

-

(iv)

there exists a constant such that for all ;

-

(v)

there exists a constant such that for all ;

-

(vi)

for all , , and ;

-

(vii)

there exists a constant such that for all ;

-

(viii)

there exists a constant such that for all.

These assumptions are standard in the literature with the exception of part (iv) which imposes a mild form of sparsity on the covariance matrix of the idiosyncratic innovations. A similar condition can be found in Fan et al., (2013) and is empirically verified by Boivin and Ng, (2006) and Bai and Ng, (2008) for US macroeconomic data, and by Barigozzi and Hallin, 2017b for stock returns. As a consequence of parts (iv) and (v), the idiosyncratic components are allowed to be serially autocorrelated and mildly cross-correlated (see also Lemma 1 below). Moreover, it is easy to check that such assumption is nesting other typical conditions on the cross-sectional dependence of idiosyncratic components (see e.g. Bai and Ng, , 2002, and Stock and Watson, , 2002, in the static factor model case). Parts (ii) and (v) imply absolute summability of the autocovariances and therefore the existence of a purely continuous spectral density. Moreover these assumptions and existence of fourth-order moments in parts (vii) and (viii) are classical requirements for consistent estimation of the autocovariances and the spectral density (see e.g. Chapter IV, Theorem 6, in Hannan, , 1970, for the autocovariances, and the results in Section 6.2 in Priestley, , 2001, and Theorem 5A in Parzen, , 1957, for the spectral density). Last, in part (iii) we also make the typical assumption of martingale difference innovations used in the GARCH literature (see e.g. Definition 2.1 in Francq and Zakoian, , 2011).

It should be insisted, however, that the GDFM is not a statistical model in the usual sense, inasmuch as, beyond the requirement of second-order stationarity, the existence of a finite (but unspecified) , and the existence of a spectrum, it does not really impose any restrictions on the data-generating process: as argued by Forni and Lippi, (2001) and Hallin and Lippi, (2013), (2.1)-(2.2) indeed constitute a representation result rather than a model equation.

On the filters and we furthermore impose the following assumptions:

Assumption (L2).

-

(i)

has rational entries, i.e. , where and , for all and , are finite-order polynomials;

-

(ii)

there exists a constant such that for all , all , and all such that ;

-

(iii)

the coefficients of are such that for some positive constant , all , all , and ;

-

(iv)

is of the form where , for all , is a finite-order polynomial, and for all such that .

This latter assumption is not strictly needed and could be easily relaxed to allow for infinite order autoregressive dynamics—at the expense, however, of heavier notation and longer proofs; see also Section 3.2 for a short discussion. This assumption implies that both the common and idiosyncratic components have a rational spectral density. Rational filters for the common component are also assumed in Forni et al., (2017), while here we also assume that the idiosyncratic component admits a finite autoregressive representation. In particular, using part (iv), we can rewrite the second equation in (2.2) as

| (2.4) |

Let , and , , be the spectral density matrices of the observed panel, the common, and the idiosyncratic components, respectively; the existence of those spectral densities is guaranteed by Assumption (L1). Denote by , , and their respective -th largest eigenvalues—the panel, common, and idiosyncratic dynamic eigenvalues, on which we assume the following. Hereafter, “forall ” or “” is to be understood as “for all but over a subset of values included in a set with Lebesgue measure zero.” Similarly, in the sequel is an essential , etc.

Assumption (L3).

There exist a positive integer and continuous functions and from to , , independent of , and such that

Under this assumption, the first common dynamic eigenvalues, irrespective of the frequency (except possibly over a set of measure zero), are diverging linearly as . The following results then hold for the idiosyncratic dynamic eigenvalues and those of the panel.

Lemma 1.

Under Assumptions (L1) and (L3),

-

(i)

there exists a constant such that for all ;

-

(ii)

there exist a positive integer and continuous functions and from to ,, independent of and such that , -a.e. in , all , and all ;

-

(iii)

there exists a constant such that for all .

As a consequence of Lemma 1, identification of the model, i.e., consistently disentangling the unobserved common and idiosyncratic components, is possible, under the assumptions made in the limit, as , thanks to the behaviour of the dynamic eigenvalues.

Based on results by Anderson and Deistler, (2008) for singular vector processes with a rational spectrum, Forni and Lippi, (2011) and Forni et al., (2015) prove that, for generic values of the coefficients of the filters as defined in Assumption (L2), the space spanned by for and is the same as the space spanned by any -dimensional subvector of and its lags; moreover, those subvectors admit an autoregressive representation driven by the common shocks .

More precisely, any -dimensional subvector of admits an autoregressive representation of the form

| (2.5) |

where is a finite-order VAR operator such that , is the vector of common shocks in (2.3), and an appropriate matrix. On that representation, we make the following assumptions.

Assumption (L4).

Let be an arbitrary -dimensional subvector of : the autoregressive representation (2.5) is such that

-

(i)

is uniquely defined;

-

(ii)

the degree of is uniformly bounded, that is, for some integer independent of and the choice of the subvector ;

-

(iii)

for all such that ;

-

(iv)

is , with full rank ;

-

(v)

denoting by the lag- autocovariances of and defining

, where is independent of the choice of the subvector .

This assumption allows us to derive an alternative representation of the GDFM (2.2) which is particularly useful for estimation and for the construction, in Section 2.2 below, of a further GDFM for log-volatilities. Without loss of generality, let factorise into for some positive integer , so that we can partition into subprocesses, each of dimension , of the form , , with superscript (k) substituted for ‡. Each satisfies (2.5) and Assumption (L4). Defining the matrix , we thus have the VAR representation

| (2.6) |

where is block-diagonal with diagonal blocks . Moreover, in view of (2.3), we have (see Proposition 3 in Forni et al., , 2017). Then, the following alternative and equivalent representation of the GDFM holds:

| (2.7) |

The advantage of this representation is that it is “static” in the sense that the common shocks now are loaded only contemporaneously and not via filters as in (2.3).

To conclude with, note that the Yule-Walker equations

| (2.8) |

characterising the matrix coefficients of in (2.14) are well defined in view of part (v) of Assumption (L4); the same conclusion holds, blockwise, for the -dimensional VAR (2.6).

For ease of notation, define the filtered processes

with traditional (static) covariance eigenvalues , , and , respectively. Since (2.7) is a static factor model, it is natural to make the following assumption on the eigenvalues of the covariance of (see Assumption 4 in Forni et al., , 2009 or Assumption 6 in Forni et al., , 2017). Unless , indeed, it does not even follow from Assumption (L3) that has rank .

Assumption (L5).

There exist a positive integer and constants , , independent of such that for all and all .

The following results then hold for the eigenvalues and of the covariance matrices of and , respectively.

Lemma 2.

Under Assumptions (L1), (L3), (L4), and (L5),

-

(i)

there exists a constant such that for all ;

-

(ii)

there exist a positive integer and constants , , independent of such that for all and all ;

-

(iii)

there exists a constant such that for all .

2.2 Model and assumptions for volatilities

We define the vector of common innovations (at time ) as the -dimensional vector

for , the processes , clearly are singular. Then, letting , our log-volatility proxy is

| (2.9) |

yielding the double-indexed stochastic process , with -dimensional sub-processes . We call the “log-volatilities” process. Similar definitions are used in Engle and Marcucci, (2006) and our previous work (Barigozzi and Hallin, , 2016; Barigozzi and Hallin, 2017a, ; Barigozzi and Hallin, 2017b, , and Barigozzi et al., , 2018). In order for such processes to be well defined we make the following assumption.

Assumption (V0).

For all and , almost surely.

This assumption makes sure that no cancellation can happen between common and idiosyncratic innovations; it is required, since and , although mutually orthogonal by Assumption (L1.vi), need not be mutually independent (assuming, for instance, that and are absolutely continuous is not sufficient).

Assuming a GDFM with factors for the log-volatilities, we obtain

| (2.10) | ||||

| with | (2.11) |

where is ’s expected value, and are ’s common and idiosyncratic components, and the processes and , are mutually orthogonal (at all leads and lags) - and -dimensional white noise, respectively. Note that a GDFM for log-volatilities implies a multiplicative GDFM representation

for the volatilities themselves. Letting

equations (2.11) in vector notation take the form

| (2.12) |

with and .

The following assumptions then are the analogues, for log-volatilities and (2.10)-(2.11) , of Assumption (L1).

Assumption (V1).

-

(i)

The dimension of does not depend on ; the process is second-order white noise, with mean and diagonal positive definite covariance ;

-

(ii)

writing for the coefficient of in , there exists a constant such that for all ;

-

(iii)

the process is second-order white noise, with mean and positive definite covariance ; moreover, for all and and such that ;

-

(iv)

there exists a constant such that for all ;

-

(v)

there exists a constant such that for all ;

-

(vi)

for all , , and ;

-

(vii)

there exists a constant such that for all ;

-

(viii)

there exists a constant such that for all .

The same comments made for Assumption (L1) apply here. Moreover, note that all moments of log-transforms of heavy-tailed variables exist and are finite, even for stable distributions (see e.g. Theorem 5.8.1 in Uchaikin and Zolotarev, , 2011). Pursuing with assumptions, the following one is the log-volatility counterpart of (L2).

Assumption (V2).

-

(i)

has rational entries , where and , for all and , are finite-order polynomials;

-

(ii)

there exists a constant such that for all , all , and all such that ;

-

(iii)

the coefficients of are such that for some constant and all ,, and ;

-

(iv)

is of the form where , for all , is a finite-order polynomial, and for all such that .

Assumptions (V2.iv) implies that we can rewrite (2.11) also as

| (2.13) |

As in the case of levels, this assumption could be relaxed to allow for an infinite autoregressive order.

Let , , and , denote the spectral density matrices of , its common and its idiosyncratic components, with -th largest eigenvalues , and , respectively. As in (L3), we assume the following.

Assumption (V3).

There exist a positive integer and continuous functions and from to , , such that , -a.e. in , all , and all .

Finally, the analogue (V4) of (L4) again is based on the representation results in Forni et al., (2015): any - dimensional subvector of admits an autoregressive representation of the form

| (2.14) |

where is a finite-order VAR operator such that , is the vector of common shocks in (2.12), and an appropriate matrix. On that representation, we make the following assumptions:

Assumption (V4).

-

(i)

is uniquely defined;

-

(ii)

the degree of is uniformly bounded, that is, for some integer independent of and the choice of the subvector ;

-

(iii)

for all such that .

-

(iv)

the matrix has full rank ;

-

(v)

denoting by the lag- autocovariances of and defining analogously to in (L4), , where is independent of the choice of the subvector .

Now, Assumption (V4) implies , so that, assuming without loss of generality that (with if ) and defining a block-diagonal autoregressive operator the way we defined in the previous section, we can rewrite the GDFM for log-volatilities under the static form

| (2.15) |

After defining, with obvious notation, the filtered processes , , and , with (static) spectral eigenvalues , , and , we conclude with the analogues of (L5) and Lemmas 1 and 2 for the log-volatility panels.

Assumption (V5).

There exist a positive integer and constants , , independent of such that for all and all .

We then have the following.

Lemma 3.

Under Assumptions (V0), (V1), (V3), (V4), and (V5),

-

(i)

there exists a constant such that for all ;

-

(ii)

there exist a positive integer and continuous functions and from to , , independent of and such that , -a.e. in , all , and all ;

-

(iii)

there exists a constant such that for all ;

-

(iv)

there exists a constant such that for all ;

-

(v)

there exist a positive integer and constants , , independent of such that , for all and all ;

-

(vi)

there exists a constant such that for all .

3 Estimation, consistency, and rates

Hereafter, the terminology “estimation”, “estimator”, etc. is used, in an orthodox way, for data-driven quantities attempting at evaluating parameters (covariances, spectra, loadings, …) but also, with a slight abuse, for data-driven quantities attempting at reconstructing unobserved variables (such as common factors, common and idiosyncratic components, …). All those “estimators”, which are -measurable random variables (hence depend both on and ) are carrying “hats”.

3.1 Summary of estimation

Estimation proceeds in two parts. The first part deals with the observed panel of levels, and follows along similar lines as in Forni et al., (2017), yielding estimated log-volatility proxies; the second part consists in repeating the same estimation steps, now based on those estimated log-volatility quantities. Global consistency of the procedure is discussed in the next section, along with further necessary conditions.

To start with, we assume that and are known—an assumption we are relaxing later on. For simplicity of notation, we also assume and to be centred, i.e., to have zero mean; in practice, sample means are to be subtracted in order to obtain centred variables—which has no impact on consistency nor consistency rates.

Here is a detailed list of the steps required for estimation. Further comments on the choice of the quantities needed for estimation and a schematic description of the procedure are given at the end of this section (see also Algorithms 1 and 2).

-

(L.i)

To start with, compute the lag-window estimator

of the spectral density matrix of returns, where is the usual lag- sample autocovariance matrix of levels and is a suitable kernel with bandwidth . We here adopt the common choice of a Bartlett kernel

but other classical kernels are also possible.

-

(L.ii)

Collect the normalised column eigenvectors associated with ’s largest eigenvalues into the matrix , and collect the corresponding eigenvalues into the diagonal matrix . Take

as an estimate of the spectral density matrix of the level-common component process .

-

(L.iii)

By inverse Fourier transform of , estimate the autocovariance matrices of :

-

(L.iv)

Assuming, for simplicity, 111In practice, the last cross-sectional items can be added to the last block in the analysis which will then have size larger than . Since the arguments in Forni et al., (2017) used in the next section apply to any partition of blocks of size or larger, nothing changes in what follows. that , consider the diagonal blocks of the ’s. For each block, estimate, via Yule-Walker methods, the coefficients of a -dimensional VAR model (order determined via AIC or BIC). In other words, compute the sample analogue of (2.8). This yields, for the -th diagonal block, an estimator of the autoregressive filter appearing in Assumption (L4), hence an estimator of the VAR filter . The resulting estimated filtered process and its estimated covariance matrix are and , respectively.

-

(L.v)

Collect the normalised (column) eigenvectors corresponding to ’s largest eigenvalues into the matrix . Projecting onto the space spanned by the columns of provides an estimate of the innovation process . Taking into account the set of identifying restrictions described in Assumption (I) below, we obtain the estimators

Our estimator of the dynamic loadings then is , where we truncate the filter at some finite lag . From this we obtain an estimator of the common component.

-

(L.vi)

The resulting estimator of the idiosyncratic component is . Fitting a univariate AR model (order determined via AIC or BIC), either by least squares or via Yule-Walker methods, to each of the components of yields estimators of the residuals and of the diagonal matrix of coefficients from which we also obtain with truncated at some finite lag .

-

(R)

For all and , let and define the estimated log-volatility proxies as capped values of :

where is a sequence of constants to be chosen in order to make our proxy robust to the log-transform. Note that consistency of our estimation procedure requires an adaptive choice of , depending on the sample size as explained in Assumption (R) below. In particular, must be strictly positive for consistency to hold.

-

(V.i)

Denote by , the -dimensional vector of log-volatility proxies and compute the lag-window estimator

of its spectral density matrix, where is the lag- sample autocovariance matrix of estimated log-volatilities. Here again we adopt the Bartlett kernel, with bandwidth , which could be different from in step (L.i).

-

(V.ii)-(V.vi)

Repeat steps (L.ii)-(L.vi) for . In particular, steps (V.ii)-(V.v) yield the estimators and , from which we compute

while from (V.vi) we obtain and , hence . As before, and are truncated at finite lags and .

An important remark needs to be made here. The cross-sectional ordering of the panel has an impact on the selection of the diagonal blocks in steps (L.iv) and (V.iv). Each cross-sectional permutation of the panel, thus, would lead to distinct estimators—all sharing the same asymptotic properties. A Rao-Blackwell argument (see Forni et al., , 2017 for details) suggests aggregating these estimators into a unique one by simple averaging (after obvious reordering of the cross-section) of the resulting estimated shocks. Although averaging over all permutations is clearly unfeasible, as stressed by Forni et al., (2017) and verified empirically also in Forni et al., (2018), a few of them are enough, in practice, to deliver stable averages (which therefore are matching the infeasible average over all permutations).

Implementation of the above estimation steps is described in Algorithms 1 and 2. Those algorithms require setting bandwidths and for the estimation of the spectral densities, a capping constant , and the number of factors and . Concerning the bandwidths and the capping constant, we refer to Section 3.2 for the required asymptotic properties (see Assumptions (K) and (R), respectively), while a numerical assessment of the impact of these quantities is provided in Section 5 on simulated data (see also the results in Appendix D) and in Section 6 on real data. Overall, our numerical analysis shows that low levels of capping or even no capping at all are preferable, as they avoid inducing too much bias in the log-volatility distributions. As for the bandwidths, large values of are required to construct reliable estimates, since they allow setting large enough to capture the high persistence of log-volatility series. Our results are quite insensitive to the choice of , due to the fact that financial returns typically are only weakly autocorrelated.

Finally, we can determine the numbers and of common shocks by means of the information criteria proposed by Hallin and Liška, (2007) and applied on the panels and , respectively. The resulting data-driven estimators and converge in probability to and , respectively. Since and are integers, this means that, for any , there exist and such that, for all and , and with probability larger than . Hence, in Section 3.2 below, we safely can assume that and are known.

3.2 Consistency and rates

Consistency of the estimators of the GDFM model for levels is proved in Forni et al., (2017). Some differences exist, though, between their approach and ours. First, Forni et al., (2017) make slightly weaker assumptions on idiosyncratic serial dependence and, by exploiting results in Wu and Zaffaroni, (2018) on spectral density estimation, they derive their consistency results under the constraint that as . A more classical approach is adopted here, based on Assumptions (L1) and (V1), which as a consequence requires mildly stronger constraints on the range of admissible values for the bandwidths and . Specifically, we require the following.

Assumption (K).

As , and .

Note that for as in our empirical study, the range of admissible bandwidths is still such that most of the serial dependence in the data is captured when estimating the spectral density (see Section 6 for more details on the choice of the bandwidths).

Second, the results in Forni et al., (2017) hold pointwise in , which is not sufficient for our needs when it comes to prove consistency in the second part of the estimation procedure. Indeed, we need uniform (over all ) consistency of the estimators of the common and idiosyncratic components. For this reason, we make additional assumptions on the distribution of common and idiosyncratic components.

Assumption (T).

There exist constants , , , and , such that, for any ,

-

(i)

;

-

(ii)

;

-

(iii)

, for all ;

-

(iv)

, for all .

This assumption is equivalent to an assumption of sub-exponential tails of the common factors and the normed linear combinations of idiosyncratic components. Specifically, it can be shown that (Ti) is equivalent to requiring for any , that for any and some finite (see also Vershynin, , 2012, and Appendix A.3 for details). The same holds also for (Tii), (Tiii), and (Tiv). See Remark 1 at the end of this section for a discussion of the implications and possible relaxations of this assumption.

Two remarks on (Tiii) and (Tiv) are in order here (see Sections 5.2.4 and 5.2.5 in Vershynin, , 2012 for details). First, note that by letting , with for a given , those assumptions imply that each idiosyncratic component has marginal sub-exponential distribution. Second, an implication of Lemmas 2 and 3 is that vectors of the form and have finite variance for all , a necessary condition for pointwise consistency. However, (Tiii) and (Tiv) are stricter on idiosyncratic cross-sectional dependence, since they control all moments of normed linear combinations of idiosyncratic components. Indeed, since the common components and are recovered by aggregation across the elements of and , respectively, uniform consistency requires limiting the contribution of the tails of the distribution of cross-sectional averages of idiosyncratic components.

Finally, since factors and factor loadings are not separately identified, we can, without loss of generality, impose the following assumptions, which are just identification constraints (see Forni et al., , 2009 for similar conditions).

Assumption (I).

-

(i)

Denoting by the matrix of normalized column eigenvectors corresponding to the largest eigenvalues of the covariance matrix of , put and ;

-

(ii)

denoting by the matrix of normalized eigenvectors corresponding to the largest eigenvalues of the covariance matrix of , put and .

In other words, Assumption (I) requires the common factors () to be the (non-normalised) principal components of (). Note that, under Assumption (I), both the factors and their loadings depend on ; their product, however, does not, which is particularly convenient and simplifies the proofs. Other identification constraints are commonly used in principal component analysis (see e.g. Fan et al., , 2013); they do not affect the results below, but lead to much heavier notation.

The consistency properties of the estimated GDFM for the levels as described in steps (L.i)-(L.vi) are as follows.

Proposition 1.

Let . Then, under Assumptions (L1)-(L5), (K), (T), and (I), there exists a diagonal matrix with entries such that

-

(a)

, for all ;

-

(b)

;

-

(c)

, for all ;

-

(d)

.

The proof of parts (a) and (b) of Proposition 1 follows directly from Forni et al., (2017) together with Assumptions (Ti) and (Tiii). However, parts (c) and (d) concerning the idiosyncratic components are new results and provide uniform consistency over both time and the cross-section (see also Remark 1 below). In particular, notice that parts (c) and (d) of Proposition 1 are proved under Assumption (L2iv) of a finite-order autoregressive representation for the idiosyncratic component. Relaxing that assumption into possibly infinite-order autoregressive repressentations would require addressing, in the proofs of parts (c) and (d), the issue of truncation errors related to finite-order AR fitting. Consistency still could be proved, but with rates depending on the rate of decay of the autocovariances of idiosyncratic components, as shown, for example, in den Haan and Levin, (1997). For simplicity, we do not consider this here.

As for the global consistency properties (after the second estimation step), we need a final condition on the choice of the capping sequence in step (R).

Assumption (R).

The sequence is such that the sets satisfy uniformly in as . Moreover, there exist a positive integer and constants and , independent of , such that for all .

The intuition behind this assumption is as follows. As shown in Appendix A.4, an immediate consequence of Proposition 1 is that the volatility proxies are consistently estimated, namely,

Now, setting in step (R), then, due to the log-transform, uniform consistency of becomes problematic when gets “close to zero”. For this reason, we need . The set is that of all time points at which is close to zero, and uniform consistency of for straightforwardly follows from uniform consistency of . On the other hand, the sets should not contain too many time points, and have cardinality going to zero at appropriate rate—whence Assumption (R). In particular, we suggest to choose of the order of for all . Although we do not have theoretical results justifying this choice of in practice, simulation-based results (see Appendix B) indicate that, the condition on the cardinality of the sets is indeed satisfied for decreasing logarithmically in .

Consistency of the estimated GDFM for log-volatilities as described in steps (R) and (V.i)-(V.vi) then follows.

Proposition 2.

Let and assume that for some finite . Then, under Assumptions (L1)-(L5), (V1)-(V5), (K), (T), (I), and (R), there exists a diagonal matrix with entries such that

-

(a)

for all ;

-

(b)

;

-

(c)

for all ;

-

(d)

.

This result, which is new, provides the theoretical foundation for the consistency of the estimators used in Barigozzi and Hallin, (2016); Barigozzi and Hallin, 2017a ; Barigozzi and Hallin, 2017b and in this paper. Note that parts (c) and (d), just as parts (c) and (d) of Proposition 1, are proved under Assumption (V2iv) of a finite-order autoregressive representation for the idiosyncratic components; the same comments as for Proposition 1 apply.

Our results show that, up to logarithmic factors and the bandwidth-related ones, the rates of consistency of our estimators are of order as in classical one-step factor models. The following three technical remarks discuss how our assumptions, in particular Assumptions (T) and (K), affect the consistency rates, and how the effect of those logarithmic and bandwidth-related factors could be controlled further if we were willing to make additional assumptions.

Remark 1 (Serial dependence of idiosyncratic components).

Inspection of the proof of part (c) of Proposition 1 shows that the extra (with respect to part (b)) factor there is due to terms of the type . Now, while the cross-sectional dependence of idiosyncratic components is controlled via Assumption (Tiii), we do not impose (beyond weak stationarity) any specific assumption on their serial dependence. However, it is worth noting that, if we made some mild additional mixing assumption controlling that serial dependence, then those terms could be bounded by a Bernstein-type inequality, as for example in Theorem 1 by Merlevède et al., (2011). Similar comments apply to Proposition 2 and bounds on the idiosyncratic sums . If such additional assumptions were made, the rates in Proposition 1 parts (c) and (d) would change to , those in Proposition 2 part (a) to , those in part (b) to , and those in parts (c) and (d) to .

Remark 2 (Tail behavior).

In Section 6, we analyze a panel of stock returns, and it is therefore worth discussing how our assumptions relate to the distributional properties of financial data. First, let us stress that it is common, in the financial econometrics literature, to assume Gaussianity of log-volatility proxies (see e.g. Alizadeh et al., , 2002). This is in agreement with the tail Assumptions (Tii) and (Tiv) since sub-Gaussians tails are lighter than sub-exponentials. In the Gaussian case, the rates in Proposition 2 part (a) would change to , those in part (b) to , and those in parts (c), and (d) to .

Second, Assumption (Ti) straightforwardly generalizes to more general classes of distributions such that, for some finite constants , , and , for any and ; (Tiii) can be generalized similarly for level idiosyncratic components. These distributions are studied in the literature under the name of sub-Weibull distributions (Kuchibhotla and Chakrabortty, , 2018, and Vladimirova and Arbel, , 2019) or semi-exponential (Borovkov, , 2000).222Note that the assumption of a sub-Weibull tail decay is equivalent to the moment condition for all and some finite (see Vladimirova and Arbel, , 2019, Theorem 2.1); fourth-order moments in that case always exist. By letting , we could allow for tails, which, although still exponentially decaying, could be heavier than assumed in Assumption (T), thus accounting for moderately extreme events. Following the same steps as in Appendix A.3, it is easily seen that in this case the rates in Proposition 1 part (b) would change to and those in parts (c) and (d)) to . As for Proposition 2, would we assume a sub-Weibull distribution also in (Tii) and (Tiv) (with the same value of ), then rates would change to in part (a), to in part (b), and to in parts (c) and (d). To conclude, assuming sub-Gaussian tails in (Tii) and (Tiv) modifies the rates in part (a) of Proposition 2 into , those in part (b) into , and those in parts (c) and (d) into .

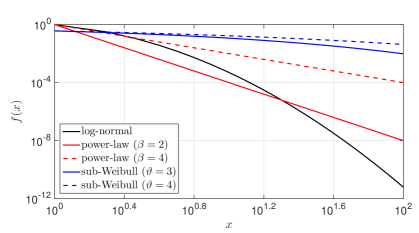

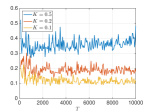

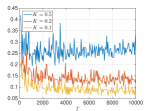

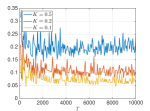

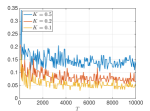

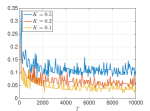

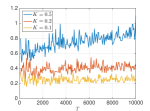

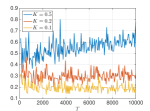

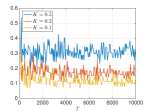

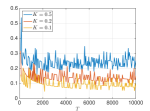

Finally, in principle, we also could assume power-law decay—that is, the existence of finite constants and such that for any and ; we similarly could generalize (Tiii) for level idiosyncratic components. We do not explore this possibility in detail, but we notice that , in order to have consistency under this setting, we would need at least ; moreover, the smaller , the smaller the range of admissible choices for the bandwidths and . Notice however that, in practice, determining the actual values of and is very tricky, and that small values of can generate a tail behavior which is comparable to the power-law behavior (see Figure 1).

|

Remark 3 (Bandwidths and estimation of spectral densities).

The results in Propositions 1 and 2 require uniform consistency of the estimated spectral density over all frequencies. For this reason, we have stronger than usual asymptotic constraints on the bandwidths. These could be relaxed if we made stronger assumptions on the shocks. First, notice that in our setting the level shocks are just uncorrelated (see Assumptions (L1i) and (L1iii)), and are by no means independent. However, if we are willing to assume the existence, for level shocks, of moments of all orders, then we could apply Theorem 7.7.4 in Brillinger, (2001), which would allow us to replace with for any in the definition of in Proposition 1. Second, we could, in principle, allow for independent shocks on log-volatilities (e.g. assuming Gaussianity, see Remark 1) and therefore make use of Theorem 4 and Section 4.2 in Wu and Zaffaroni, (2018), which would allow us to replace with in the definition of in Proposition 2.

4 Conditional prediction intervals

Before describing our prediction intervals, let us summarise here the main notation developed in the previous sections. Given an observed dataset of size , we have, for the levels,

| (4.1) | ||||

where because of (2.4) and, for the log-volatilities,

| (4.2) | ||||

where because of (2.13).

The optimal one-step-ahead linear predictors of level and log-volatility are thus

| (4.3) |

with innovations and , respectively. As a consequence, the level innovations are

We therefore define a one-step-ahead predictor of the volatilities as

with associated “multiplicative innovations”

Note, however, that, due to the nonlinear nature of the exponential transformation from to , this multiplicative decomposition of volatilities into a predictor and an “innovation” does not enjoy (in the space of volatilities) the traditional optimality properties, which only hold for their logarithms (in the space of log-volatilities). This, however, will not be a concern in the quantile-based construction we now describe, due to the fact that the coverage probabilities of a interquantile interval are invariant under continuous monotone transformations: the quantile of .

Denoting by the (unconditional) -quantile of , (which, by stationarity, does not depend on ), theoretical lower and upper prediction bounds with confidence level and are

| (4.4) |

respectively. Note that lies above for and lies below for . Prediction intervals with coverage probability can be constructed as

| (4.5) |

with and , covering (see (4.8)) provided that

| (4.6) |

Clearly, the lower bound provides a measure of the Value-at-Risk of level at time , which we denote as (see Section 12.3.1 in Francq and Zakoian, , 2011 for a review).333Usually, a Value-at-Risk is reported as a positive quantity. That will be the case with for small enough. Positive values of are possible, though: in such cases, is defined to be zero by convention (see Francq and Zakoian, , 2011, Definition 12.1).

The advantage of quantile-based prediction intervals of the form (4.5) over their conditional heteroskedasticity-based competitors stems from the fact that, irrespective of the way has been obtained, the conditional -quantiles of (conditional on ) are of the form (4.4). This quantile-based approach moreover allows for unequal tails ( in (4.6)—hence, distinct attitudes towards losses and gains) and automatically takes into account the typical skewness of financial data distributions.

In practice, the model is estimated from a observed panel; the empirical counterparts of and for are

and

and we accordingly define ; based on the estimates and of and , let .

For any , denote by the order statistic of ; the empirical quantile then can be used as an estimator of . Empirical versions of the prediction limits and intervals (4.4) and (4.5) are

and

| (4.7) |

with and . A schematic description of this procedure is given in Algorithm 3.

If the ’s were i.i.d. instead of weak white noise, the convergence (for given and , without rates) of (4.7) to (4.5) would follow from the fact that, as a consequence of the consistent estimation of the GDFMs for levels and volatilities, for any and , converges to zero as and tend to infinity.

Then, the difference between the empirical quantile of order computed from and the empirical quantile of order computed from the unobservable is for given as and tend to infinity. Now, for given , were the ’s i.i.d., the empirical -quantile computed from is, for large enough, arbitrarily close to its theoretical counterpart with probability arbitrarily close to one. The same conclusion extends to the present case where the ’s are stationary and uncorrelated provided that they satisfy some additional mild ergodicity or mixing assumption. The literature on Glivenko-Cantelli and quantile consistency under ergodicity and mixing is abundant, and we will not proceed with imposing any specific mixing conditions here which anyway hardly can be checked from the data. The reader may like to refer to Theorem 3.1 in Francq and Zakoian, (2019) for details.

Once prediction regions have been constructed, it is important to evaluate their actual coverage performance. For this, it is useful to define the conditional coverage indicators—namely, for prediction intervals ,

| (4.8) |

For a given , we say that provides the correct coverage if

which is equivalent (see e.g. Lemma 1 in Christoffersen, , 1998) to the hypothesis that

| (4.9) |

That hypothesis can be tested against alternatives of insufficient coverage probability values, against non-sharp prediction limits, or against alternatives of serial dependence. We refer to Section 6.3 for details and implementation.

5 Simulation study

5.1 Setup

To study the performance of our estimator on finite samples, we simulate data ( replications) according to the model described in (4.1)-(4.2).

For each Monte Carlo replication and for given values of , and , we first simulate a multiplicative factor model for the volatilities which in turn implies a factor structure also for the levels. The common component of the log-volatilities is generated as

where , is with entries and rescaled such that ,and where the coefficients are diagonal matrices with entries and rescaled in such a way that for .444In particular, when looking at simulated data 25% of the total roots are found to be in the range , thus accounting for high persistence in log-volatilities, see also Table 1 below. Then, we generate the process

where , with a Toeplitz matrix with entries , if and zero otherwise, and generated in the same way as . Denoting by the th element of , we rescale it into so that the signal-to-noise ratio is 2.

Define

where with equal probabilities 0.5 and is the th element of . The volatility and log-volatility proxies then are

from which we see that, since each is driven by the -dimensional vector of shocks , it has the role of common log-volatility, while the shocks have only an idiosyncratic role.

Letting be the normalized eigenvectors corresponding to the largest eigenvalues of the sample covariance of the vector , we build the level shocks as

where is such that , and . Note that, by construction, the elements and of the vectors and are such that : therefore, we can also write .

Finally, we generate the vectors of common and idiosyncratic components of the levels as

where is a diagonal matrix with entries , and is generated in the same way but with entries from a uniform distribution over ; since these matrices are diagonal, the autoregressive models for and are causal. The panel of levels then is generated as .

In our numerical study, we let , , and either and , and (as in the empirical application of the next section), or and . For each configuration considered, we simulate and estimate the model times.

It has to be noticed that the data-generating process we are considering is similar to a stochastic volatility model. To illustrate the properties of the generated data, we report in Table 1 the autocorrelations up to lag 10 of , , , , , , , , , and , averaged over all replications and over all series, and when , . It can be seen that log-volatilities and volatilities have high persistence, while, due to the way they are generated, the shocks and display no linear serial dependence, i.e. are weak white noises. Turning to the kurtosis of the level shocks reported in the left panel of Table 2, these display heavy tails (especially the common ones) for the case and , while the kurtosis tends to decrease when increasing , possibly due to the aggregation of shocks in generating the common components of the log-volatility . Similar comments apply to the absolute values of skewness reported in the right panel of Table 2: especially in the case and , the common shocks display a high degree of asymmetry. Because of these features of the simulated data the case and is particularly interesting to study to assess the performance of our estimators when dealing with heavy-tailed and skewed data.

| lag | ||||||

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 6 | |

| 0.2967* | 0.2856* | 0.1178* | 0.1691* | 0.0528 | 0.1142* | |

| 0.3082* | 0.2743* | 0.1201* | 0.1426* | 0.0552 | 0.0758* | |

| -0.0378 | 0.0696* | -0.0565 | 0.0089 | -0.0099 | -0.0283 | |

| 0.0326 | 0.0495 | 0.0020 | 0.0035 | 0.0031 | 0.0042 | |

| -0.0023 | -0.0017 | -0.0035 | 0.0005 | -0.0015 | -0.0028 | |

| 0.2961* | 0.2674* | 0.1196* | 0.1445* | 0.0565 | 0.0771* | |

| 0.1753* | 0.1770* | 0.0096 | 0.0302 | -0.0032 | -0.0262 | |

| 0.0989* | 0.0791* | 0.0068 | 0.0023 | 0.0016 | -0.0037 | |

| 0.0020 | 0.0783* | -0.0033 | 0.0118 | -0.0018 | -0.0002 | |

| 0.2877* | 0.2260* | 0.1054* | 0.1200* | 0.0522 | 0.0622* | |

| 0.1174* | 0.1439* | 0.0051 | 0.0219 | -0.0031 | -0.0172 | |

| 0.0994* | 0.0798* | 0.0073 | 0.0023 | 0.0018 | 0.0029 | |

| lag | ||||||

| 1 | 2 | 3 | 4 | 5 | 6 | |

| 0.2654* | 0.2826* | 0.1183* | 0.1611* | 0.0508 | 0.1272* | |

| 0.2757* | 0.2607* | 0.1237* | 0.1305* | 0.0511 | 0.0913* | |

| -0.0089 | -0.0690* | -0.0028 | 0.0304 | -0.0353 | -0.0071 | |

| 0.1939* | 0.0721* | 0.0034 | 0.0166 | 0.0077 | 0.0113 | |

| -0.0010 | -0.0011 | -0.0030 | 0.0002 | -0.0038 | -0.0030 | |

| 0.2635* | 0.2515* | 0.1212* | 0.1283* | 0.0503 | 0.0907* | |

| 0.1977* | 0.0592 | 0.0465 | 0.0492 | -0.0142 | 0.0002 | |

| 0.2545* | 0.0822* | 0.0161 | 0.0222 | 0.0073 | 0.0101 | |

| -0.0172 | 0.0814* | -0.0052 | 0.0119 | -0.0045 | -0.0013 | |

| 0.2708* | 0.2133* | 0.1076* | 0.1059* | 0.0502 | 0.0764* | |

| 0.1227* | 0.0671* | 0.0285 | 0.0374 | -0.0123 | -0.0003 | |

| 0.2166* | 0.0909* | 0.0237 | 0.0242 | 0.0079 | 0.0009 | |

| lag | ||||||

| 1 | 2 | 3 | 4 | 5 | 6 | |

| 0.2730* | 0.2692* | 0.1254* | 0.1717* | 0.0494 | 0.1293* | |

| 0.2375* | 0.2348* | 0.1036* | 0.1481* | 0.0238 | 0.0885* | |

| -0.0221 | 0.0127 | -0.0204 | -0.0001 | -0.0071 | -0.0067 | |

| 0.0025 | 0.0640* | 0.0222 | 0.0616 | 0.0001 | 0.0134 | |

| -0.0026 | -0.0002 | 0.0000 | 0.0026 | -0.0011 | -0.0035 | |

| 0.2330* | 0.2313* | 0.1015* | 0.1456* | 0.0229 | 0.0879* | |

| 0.1835* | 0.1254* | 0.0364 | 0.0277 | 0.0079 | 0.0008 | |

| 0.1159* | 0.1020* | 0.0388 | 0.0377 | 0.0131 | 0.0057 | |

| 0.0317 | 0.0872* | 0.0032 | 0.0156 | -0.0008 | -0.0007 | |

| 0.2509* | 0.1918* | 0.0969* | 0.1227* | 0.0293 | 0.0711* | |

| 0.1313* | 0.1121* | 0.0253 | 0.0220 | 0.0040 | 0.0012 | |

| 0.1047* | 0.0869* | 0.0426 | 0.0425 | 0.0043 | 0.0133 | |

| kurtosis | skewness | |||||||||||

| , | , | , | , | , | , | |||||||

| max. | aver. | max. | aver. | max. | aver. | max. | aver. | max. | aver. | max. | aver. | |

| 161.40 | 83.53 | 67.60 | 10.94 | 31.86 | 5.60 | 7.88 | 0.28 | 4.08 | 0.03 | 2.53 | 0.02 | |

| 15.03 | 3.02 | 12.68 | 3.02 | 9.36 | 3.01 | 1.14 | 0.01 | 1.07 | 0.01 | 0.85 | 0.01 | |

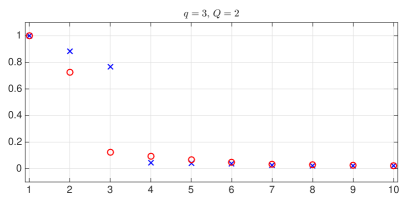

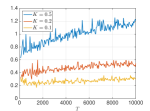

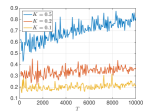

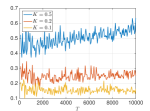

Furthermore, notice that , by construction, is a singular vector (as it should be) and has the role of a common level innovation. Moreover, the elements of , in general, are cross-sectionally dependent. As a consequence, both and have an approximate dynamic factor structure. In Figure 2 we show scree-plots with the ten largest eigenvalues of the zero-frequency sample spectral density matrices of (blue crosses), and (red circles), normalized by the largest zero-frequency eigenvalue, averaged over all realisations, when , , , and .

|

5.2 Results

For each replication, we estimate the model as described in Section 3. The capping constants and the bandwidths and involved in the estimation of the spectral density are chosen as in the empirical analysis of the next section. Specifically, we let , while the bandwidths values are and for , and for , and for (see Appendix D for results based on other values). Once we obtain estimated common components for the levels and for the log-volatilities, we compute the global error measures

and the maximal errors over all realizations:

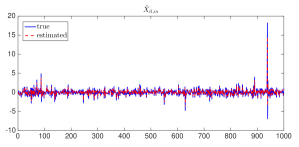

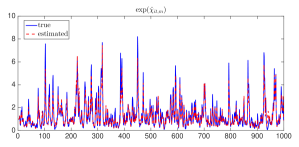

Notice that the error in the estimation of the common component of the levels (first step of the estimation procedure) has already been studied in Forni et al., (2017) and Forni et al., (2018). We therefore consider it as the benchmark error with respect to which the performance of the second estimation step, which is the novelty of this paper, is to be compared. Results are provided in Table 3. We note that MSE and MAD in the second step tend to be about 1.5 times higher than in the first step, which is not unexpected as first- and second- step errors typically cumulate in a two-stage procedure. However, when turning to MAX, this is no longer the case, since levels in our data-generating process display heavier tails than log-volatilities—in line with the typical behavior of daily stock returns and their volatilities. Increasing and improves the performance of all estimators; the role of , in that respect, seems to be the main one—a manifestation of the “blessing of dimensionality". On the other hand increasing the number of common log-volatility shocks, tends to make estimation of the second step harder, but still results are in line with the case . Capping has an effect in controlling the maximum error but does not affect the MSE and MAD results much. To illustrate the good performances of our method, in Figure 3 we show, for one replication, the estimated (in red) and simulated (in blue) common components of levels, and of volatilities, respectively, for , , , and (which is the case exhibiting the heaviest tails), setting . The choice of bandwidths adopted seems to work quite well, and, comparing to alternative choices considered in Appendix D, it can be shown that must be large enough to capture the persistence in log-volatilities, while lower values of are enough for levels and do not affect much the second step of estimation.

| , | |||||||

|---|---|---|---|---|---|---|---|

| 0.215 | 0.219 | 0.168 | 0.164 | 0.125 | 0.154 | ||

| 0.368 | 0.321 | 0.302 | 0.247 | 0.251 | 0.241 | ||

| 0.369 | 0.324 | 0.276 | 0.247 | 0.240 | 0.230 | ||

| 0.377 | 0.334 | 0.279 | 0.238 | 0.238 | 0.230 | ||

| 0.278 | 0.245 | 0.255 | 0.226 | 0.234 | 0.228 | ||

| 0.442 | 0.401 | 0.394 | 0.346 | 0.360 | 0.342 | ||

| 0.436 | 0.395 | 0.367 | 0.346 | 0.344 | 0.323 | ||

| 0.437 | 0.397 | 0.364 | 0.324 | 0.337 | 0.317 | ||

| 10.797 | 13.560 | 17.113 | 16.352 | 14.405 | 19.757 | ||

| 6.587 | 6.709 | 8.996 | 6.270 | 7.462 | 7.912 | ||

| 8.259 | 7.247 | 7.967 | 6.270 | 9.328 | 8.431 | ||

| 8.987 | 8.402 | 8.295 | 10.223 | 9.821 | 8.960 | ||

| , | |||||||

| 0.143 | 0.155 | 0.101 | 0.112 | 0.086 | 0.085 | ||

| 0.291 | 0.284 | 0.237 | 0.216 | 0.209 | 0.185 | ||

| 0.262 | 0.261 | 0.197 | 0.199 | 0.179 | 0.163 | ||

| 0.250 | 0.252 | 0.182 | 0.176 | 0.162 | 0.141 | ||

| 0.265 | 0.261 | 0.227 | 0.228 | 0.210 | 0.205 | ||

| 0.412 | 0.402 | 0.370 | 0.348 | 0.346 | 0.322 | ||

| 0.389 | 0.381 | 0.336 | 0.327 | 0.317 | 0.299 | ||

| 0.378 | 0.372 | 0.321 | 0.307 | 0.300 | 0.275 | ||

| 6.634 | 8.693 | 9.682 | 12.606 | 10.943 | 19.277 | ||

| 5.532 | 5.624 | 5.128 | 6.725 | 4.488 | 5.209 | ||

| 5.688 | 5.800 | 5.561 | 6.204 | 4.813 | 4.675 | ||

| 5.713 | 6.180 | 5.630 | 7.317 | 4.978 | 5.235 | ||

| , | |||||||

| 0.151 | 0.161 | 0.112 | 0.129 | 0.082 | 0.085 | ||

| 0.356 | 0.323 | 0.290 | 0.277 | 0.247 | 0.224 | ||

| 0.324 | 0.299 | 0.259 | 0.247 | 0.210 | 0.190 | ||

| 0.311 | 0.287 | 0.248 | 0.231 | 0.193 | 0.173 | ||

| 0.279 | 0.271 | 0.241 | 0.248 | 0.212 | 0.213 | ||

| 0.461 | 0.434 | 0.414 | 0.398 | 0.382 | 0.360 | ||

| 0.437 | 0.415 | 0.387 | 0.372 | 0.350 | 0.327 | ||

| 0.426 | 0.404 | 0.376 | 0.356 | 0.334 | 0.311 | ||

| 5.395 | 9.180 | 5.900 | 8.936 | 6.210 | 11.411 | ||

| 4.833 | 5.066 | 5.009 | 5.654 | 5.111 | 5.571 | ||

| 4.988 | 5.325 | 5.269 | 5.998 | 5.355 | 5.654 | ||

| 5.058 | 5.748 | 5.660 | 6.208 | 5.599 | 5.413 | ||

|

|

Finally, for , we estimated the model using the first 900 observations, then ran a recursive pseudo-out-of-sample forecasting exercise constructing one-step-ahead prediction intervals for the remaining observations (from to ), as described in Section 4. The -upper and -lower bounds and of prediction intervals with coverage probability are then computed for each series and replication and each out-of-sample observation. From the latter, we compute the observed coverage frequencies across all series and replications

and the proportions of coverage violations in the upper and lower tails,

and

respectively. Results are shown in Table 4. Overall performances look reasonably good—the larger and , the better. We note that capping has a clear effect on the empirical coverage; too much capping seems to affect mostly the cases in which and . No capping at all works quite well in practice, despite the fact that theoretical results require . Moreover, the same comments apply to empirical coverage as for the choice of bandwidths, with the additional finding that higher values of yield more reliable prediction performances (see Appendix D).

| , | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.32 | 0.2 | 0.1 | 0.05 | 0.01 | 0.32 | 0.2 | 0.1 | 0.05 | 0.01 | ||

| 0.6409 | 0.7637 | 0.8667 | 0.9312 | 0.9869 | 0.6765 | 0.7992 | 0.9082 | 0.9573 | 0.9926 | ||

| 0.1810 | 0.1195 | 0.0674 | 0.0342 | 0.0057 | 0.1635 | 0.1026 | 0.0470 | 0.0221 | 0.0040 | ||

| 0.1781 | 0.1168 | 0.0659 | 0.0346 | 0.0074 | 0.1601 | 0.0983 | 0.0449 | 0.0206 | 0.0035 | ||

| 0.6691 | 0.7769 | 0.8685 | 0.9197 | 0.9681 | 0.7201 | 0.8285 | 0.9226 | 0.9628 | 0.9934 | ||

| 0.1636 | 0.1124 | 0.0682 | 0.0403 | 0.0153 | 0.1422 | 0.0876 | 0.0392 | 0.0194 | 0.0034 | ||

| 0.1673 | 0.1107 | 0.0633 | 0.0400 | 0.0166 | 0.1378 | 0.0840 | 0.0383 | 0.0179 | 0.0033 | ||

| 0.7072 | 0.7987 | 0.8799 | 0.9238 | 0.9699 | 0.7119 | 0.7957 | 0.8763 | 0.9257 | 0.9703 | ||

| 0.1453 | 0.1023 | 0.0617 | 0.0384 | 0.0145 | 0.1429 | 0.1007 | 0.0600 | 0.0360 | 0.0150 | ||

| 0.1475 | 0.0990 | 0.0584 | 0.0378 | 0.0156 | 0.1453 | 0.1037 | 0.0638 | 0.0383 | 0.0147 | ||

| , | |||||||||||

| 0.32 | 0.2 | 0.1 | 0.05 | 0.01 | 0.32 | 0.2 | 0.1 | 0.05 | 0.01 | ||

| 0.6350 | 0.7523 | 0.8543 | 0.9131 | 0.9688 | 0.6718 | 0.7917 | 0.8929 | 0.9457 | 0.9895 | ||

| 0.1810 | 0.1252 | 0.0749 | 0.0449 | 0.0157 | 0.1619 | 0.1037 | 0.0530 | 0.0277 | 0.0053 | ||

| 0.1840 | 0.1225 | 0.0708 | 0.0420 | 0.0155 | 0.1664 | 0.1047 | 0.0542 | 0.0266 | 0.0053 | ||

| 0.6767 | 0.7775 | 0.8665 | 0.9206 | 0.9701 | 0.7031 | 0.8081 | 0.8986 | 0.9469 | 0.9916 | ||

| 0.1601 | 0.1145 | 0.0691 | 0.0422 | 0.0162 | 0.1458 | 0.0935 | 0.0503 | 0.0250 | 0.0039 | ||

| 0.1632 | 0.1080 | 0.0644 | 0.0372 | 0.0137 | 0.1512 | 0.0985 | 0.0512 | 0.0282 | 0.0046 | ||

| 0.7129 | 0.7993 | 0.8803 | 0.9267 | 0.9724 | 0.7565 | 0.8447 | 0.9222 | 0.9610 | 0.9923 | ||

| 0.1445 | 0.1033 | 0.0614 | 0.0384 | 0.0147 | 0.1209 | 0.0780 | 0.0382 | 0.0196 | 0.0043 | ||

| 0.1426 | 0.09740 | 0.0583 | 0.0349 | 0.0129 | 0.1227 | 0.0774 | 0.0397 | 0.0195 | 0.0035 | ||

| , | |||||||||||

| 0.32 | 0.2 | 0.1 | 0.05 | 0.01 | 0.32 | 0.2 | 0.1 | 0.05 | 0.01 | ||

| 0.6888 | 0.8045 | 0.8981 | 0.9500 | 0.9874 | 0.6391 | 0.7563 | 0.8623 | 0.9215 | 0.9784 | ||

| 0.1568 | 0.0995 | 0.0527 | 0.0258 | 0.0065 | 0.1786 | 0.1212 | 0.0678 | 0.0387 | 0.0107 | ||

| 0.1544 | 0.0960 | 0.0492 | 0.0242 | 0.0061 | 0.1824 | 0.1226 | 0.0700 | 0.0399 | 0.0110 | ||

| 0.7335 | 0.8290 | 0.9105 | 0.9539 | 0.9890 | 0.6770 | 0.7814 | 0.8752 | 0.9277 | 0.9791 | ||

| 0.1345 | 0.0863 | 0.0459 | 0.0239 | 0.0056 | 0.1602 | 0.1077 | 0.0613 | 0.0355 | 0.0103 | ||

| 0.1320 | 0.0847 | 0.0436 | 0.0222 | 0.0054 | 0.1629 | 0.1110 | 0.0636 | 0.0368 | 0.0106 | ||

| 0.7733 | 0.8539 | 0.9213 | 0.9595 | 0.9898 | 0.7167 | 0.8066 | 0.8879 | 0.9352 | 0.9809 | ||

| 0.1154 | 0.0747 | 0.0408 | 0.0207 | 0.0055 | 0.1395 | 0.0953 | 0.0551 | 0.0326 | 0.0093 | ||

| 0.1113 | 0.0714 | 0.0379 | 0.0198 | 0.0047 | 0.1439 | 0.0981 | 0.0570 | 0.0322 | 0.0099 | ||

6 Interval prediction for S&P100 returns

In this section, we apply our methodology to a panel of daily returns of stocks from the Standard & Poor’s 100 Index. Data are observed from January 4, 2000 through September 30, 2013, for a total of observations. We run a pseudo-out-of-sample forecasting exercise by estimating the model using data over the period , with and , corresponding to an evaluation period running from January 3, 2006 through September 27, 2013. For each value of , we estimate the one-step-ahead prediction intervals as defined in (4.7). The data cover the following sectors (in parentheses, the number of series in each sector): Consumer Discretionary (11), Consumer Staples (10), Energy (12), Financials (13), Health Care (11), Industrials (14), Information Technology (12), Materials (3), Telecommunications Services (2), Utilities (2) (see Appendix C for the names of individual stocks).

Although we should, in principle, fully re-estimate the whole model at each of the iterations, some quantities were kept fixed throughout the exercise. In particular, when applied to the full panel, the Hallin and Liška, (2007) criterion returns common factors for the level panel and common factors for log-volatility panel: those values are used in all subsequent analyzes. We also choose the bandwidths by minimizing, over a grid of possible bandwidth values, the mean-squared errors

respectively, leading to possibly distinct bandwidths for and . More precisely, we first determine and then determine using the chosen to compute . As a result we throughout use and . The VAR orders and the orders of their truncated inverse MA representations needed to compute impulse responses are set as follows: (i) , with inverse MA truncated at lag ; (ii) , with inverse MA truncated at lag ; (iii) , with inverse MA truncated at lag ; (iv) , with inverse MA truncated at lag . The estimation of the GDFM is based on 10 cross-sectional permutations, as explained at the end of Section 3.1. Finally, regarding the choice of the capping constant , we choose irrespective of ; note that, with reference to Assumption (R), we have . Also note that, on the average across the iterations, 6%, out of the total observations, are capped when , 14% when , and 27% when .

For any given sample size , we compute the quantiles of using , where weset , hence using either the past six months, one year, or two years of available data, or using all available past observations. Denoting by the vector of the most recent observations (so that coincides with ), for levels and window sizes , and for , we obtain the estimates

6.1 Coverage performance: qualitative analysis

For each of the series considered we compute the coverage frequency

the proportions

of coverage violations in the upper and lower tails, and the average interval length

Table 5 reports, for with (corresponding to coverage levels 68%, 80%, 90%, 95% and 99%) and , the cross-sectional average of the empirical coverage frequencies , the cross-sectional averages and of the proportions of coverage violations and , and the cross-sectional average of the average interval lengths .

| 0.32 | 0.2 | 0.1 | 0.05 | 0.01 | 0.32 | 0.2 | 0.1 | 0.05 | 0.01 | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0.6709 | 0.7894 | 0.8887 | 0.9400 | 0.9812 | 0.6874 | 0.7985 | 0.8931 | 0.9416 | 0.9813 | |

| 0.1641 | 0.1048 | 0.0552 | 0.0299 | 0.0094 | 0.1559 | 0.1002 | 0.0533 | 0.0291 | 0.0095 | |

| 0.1650 | 0.1058 | 0.0561 | 0.0301 | 0.0094 | 0.1566 | 0.1013 | 0.0536 | 0.0292 | 0.0091 | |

| 3.3934 | 4.5156 | 6.1305 | 7.7681 | 12.4174 | 3.4726 | 4.5726 | 6.1553 | 7.7698 | 12.3130 | |

| 0.6708 | 0.7903 | 0.8902 | 0.9415 | 0.9848 | 0.6882 | 0.7999 | 0.8940 | 0.9424 | 0.9846 | |

| 0.1647 | 0.1044 | 0.0544 | 0.0289 | 0.0077 | 0.1560 | 0.0998 | 0.0526 | 0.0287 | 0.0078 | |

| 0.1644 | 0.1053 | 0.0554 | 0.0296 | 0.0075 | 0.1558 | 0.1003 | 0.0534 | 0.0289 | 0.0076 | |

| 3.3621 | 4.4794 | 6.0949 | 7.7240 | 12.5008 | 3.4351 | 4.5290 | 6.1078 | 7.7074 | 12.3767 | |

| 0.6711 | 0.7895 | 0.8895 | 0.9412 | 0.9846 | 0.6886 | 0.7995 | 0.8929 | 0.9419 | 0.9843 | |

| 0.1651 | 0.1057 | 0.0551 | 0.0290 | 0.0078 | 0.1561 | 0.1005 | 0.0536 | 0.0288 | 0.0081 | |

| 0.1638 | 0.1047 | 0.0554 | 0.0298 | 0.0076 | 0.1553 | 0.1000 | 0.0535 | 0.0292 | 0.0076 | |

| 3.3034 | 4.4179 | 6.0266 | 7.6643 | 12.1190 | 3.3786 | 4.4708 | 6.0439 | 7.6539 | 12.0462 | |

| 0.7010 | 0.8142 | 0.9049 | 0.9506 | 0.9881 | 0.7187 | 0.8244 | 0.9096 | 0.9523 | 0.9881 | |

| 0.1516 | 0.0933 | 0.0474 | 0.0247 | 0.0061 | 0.1424 | 0.0879 | 0.0452 | 0.0237 | 0.0062 | |

| 0.1474 | 0.0925 | 0.0477 | 0.0248 | 0.0058 | 0.1389 | 0.0877 | 0.0452 | 0.0239 | 0.0057 | |

| 3.4523 | 4.6632 | 6.4305 | 8.2802 | 13.3895 | 3.5562 | 4.7560 | 6.5201 | 8.3747 | 13.5115 | |

| 0.32 | 0.2 | 0.1 | 0.05 | 0.01 | 0.32 | 0.2 | 0.1 | 0.05 | 0.01 | |

| 0.7126 | 0.8141 | 0.8997 | 0.9452 | 0.9821 | 0.7552 | 0.8391 | 0.9119 | 0.9507 | 0.9836 | |

| 0.1435 | 0.0926 | 0.0500 | 0.0274 | 0.0091 | 0.1222 | 0.0800 | 0.0436 | 0.0243 | 0.0082 | |

| 0.1439 | 0.0932 | 0.0504 | 0.0274 | 0.0088 | 0.1226 | 0.0809 | 0.0446 | 0.0251 | 0.0081 | |

| 3.6203 | 4.6949 | 6.2419 | 7.8371 | 12.3547 | 3.9076 | 4.9426 | 6.4443 | 8.0189 | 12.5330 | |

| 0.7138 | 0.8143 | 0.9009 | 0.9452 | 0.9851 | 0.7556 | 0.8398 | 0.9127 | 0.9512 | 0.9866 | |

| 0.1433 | 0.0928 | 0.0491 | 0.0271 | 0.0077 | 0.1224 | 0.0798 | 0.0432 | 0.0242 | 0.0069 | |

| 0.1428 | 0.0929 | 0.0500 | 0.0277 | 0.0072 | 0.1219 | 0.0804 | 0.0440 | 0.0246 | 0.0065 | |

| 3.5796 | 4.6500 | 6.1923 | 7.7700 | 12.4405 | 3.8737 | 4.9105 | 6.4108 | 7.9706 | 12.7086 | |

| 0.7149 | 0.8150 | 0.9002 | 0.9449 | 0.9846 | 0.7588 | 0.8422 | 0.9132 | 0.9514 | 0.9861 | |

| 0.1430 | 0.0927 | 0.0495 | 0.0274 | 0.0080 | 0.1204 | 0.0782 | 0.0426 | 0.0236 | 0.0072 | |

| 0.1420 | 0.0923 | 0.0502 | 0.0277 | 0.0074 | 0.1208 | 0.0795 | 0.0442 | 0.0250 | 0.0067 | |

| 3.5336 | 4.6035 | 6.1513 | 7.7434 | 12.1898 | 3.8584 | 4.9070 | 6.4371 | 8.0357 | 12.6302 | |

| 0.7430 | 0.8387 | 0.9162 | 0.9551 | 0.9886 | 0.7824 | 0.8633 | 0.9283 | 0.9613 | 0.9900 | |

| 0.1301 | 0.0808 | 0.0415 | 0.0221 | 0.0061 | 0.1091 | 0.0680 | 0.0351 | 0.0189 | 0.0053 | |

| 0.1269 | 0.0805 | 0.0422 | 0.0228 | 0.0054 | 0.1085 | 0.0687 | 0.0366 | 0.0198 | 0.0047 | |

| 3.7420 | 4.9317 | 6.6982 | 8.5677 | 13.7991 | 4.1045 | 5.2913 | 7.0734 | 8.9901 | 14.4295 | |

Inspection of the table reveals that and , which is a qualitative confirmation of the validity of our methodology (see Section 6.3 for more formal validation). Three remarks emerge from these results. First, regarding the sensitivity of our procedure to capping, lower values of , in general, provide better results when is higher, while larger values of provide better results for lower values of ; in all cases, yields a mostly conservative coverage frequency higher than . In particular, note that the choice of (no capping at all), although ruled out by Assumption (R), still provides very good results. Second, setting , that is, considering the entire past history to compute quantiles apparently is not the best strategy, and shorter horizons seem preferable. This finding is possibly related to some time variation in the distribution of the innovations of log-volatilities at horizons longer than one year. Third, for any given , shorter intervals are obtained when setting or regardless of the choice of . Overall, choosing and or works best for and , while and or works best for , and .

|

|

|

|

|

|

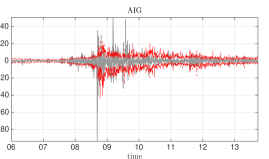

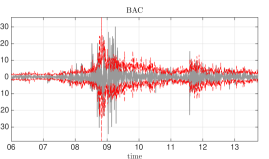

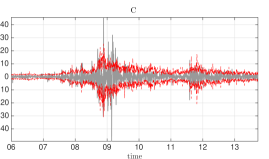

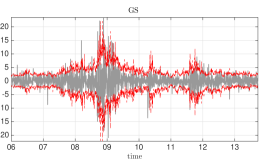

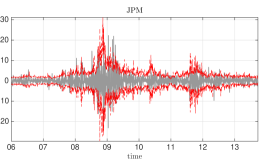

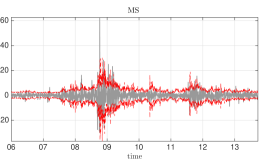

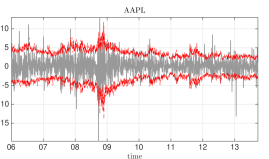

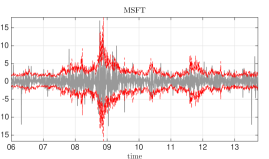

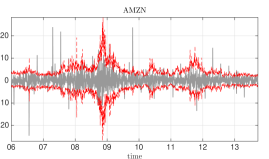

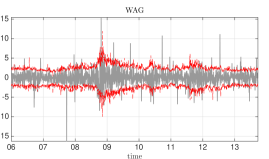

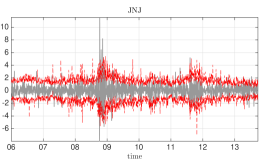

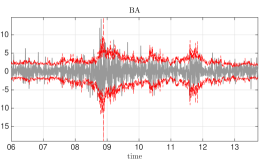

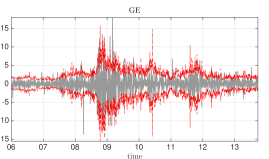

In Figures 4 and 5, we set and and we show (in grey) for some selected individual stocks, together with (in red) the estimated upper and lower bounds of the 90% one-step-ahead prediction interval, i.e. and , respectively. Figure 4 shows results for six of the most volatiles stocks in our dataset, all belonging to the financial sector: America International Group (AIG), Bank of America (BAC), Citigroup (C), Goldman Sachs (GS), JPMorgan Chase (JPM), Morgan Stanley (MS). Figure 5 provides the same results for eight relevant non-financial stocks: Apple (AAPL), Microsoft (MSFT), Amazon (AMZN), Wallgreens (WAG), Exxon Mobil (XOM), Johnson & Johnson (JNJ), Boeing (BA), General Electric (GE). Volatilities, in those series, which were the most seriously affected by the great financial crisis, are notoriously hard to predict.

|

|

|

|

|

|

|

|

6.2 Coverage: comparison with GARCH

The novelty of our prediction intervals is that they are exploiting the information contained in the available cross-section of stocks. This is in sharp contrast with the usual GARCH approach, which is strongly univariate, and disregards cross-sectional information by analyzing the series one by one. Moreover, estimating 90 univariate GARCH models requires much more computing time than estimating our model. GARCH nevertheless constitute the more common practice in this context, and serves as a natural benchmark.

We therefore compare our prediction intervals with those obtained by fitting, via quasi-maximum likelihood, univariate GARCH(1,1) models to all series in our panel. Specifically, for each series , we estimate the model

For given , we obtain estimated parameters and , from which we compute the estimated volatilities and the innovation values , . Innovation quantiles are computed from , where as before we set . Then, for any given level and window size , and for , given the one-step-ahead volatility pre- dictor , we compute the the upper and lower confidence bounds

yielding the one-step-ahead prediction intervals

and the indicators of correct interval prediction . Based on these quantities, we then compute, for , the empirical coverage frequency, denoted as , the proportions of coverage violations in the upper and lower tail, denoted as and , respectively, and the average interval length, denoted as . Averages of these quantities over the series under study are shown in Table 6. Inspection of this table reveals that the GDFM performances are slightly better than the GARCH ones in terms of coverage frequencies, based on similar interval lengths. This, however, is mainly a descriptive and, due to cross-sectional dependence, somewhat misleading assessment, which ideally should be reinforced into a more formal testing analysis.

| 0.32 | 0.2 | 0.1 | 0.05 | 0.01 | |

|---|---|---|---|---|---|

| 0.6755 | 0.7947 | 0.8933 | 0.9429 | 0.9834 | |

| 0.1576 | 0.0991 | 0.0507 | 0.0267 | 0.0076 | |

| 0.1669 | 0.1062 | 0.0560 | 0.0304 | 0.0090 | |

| 3.4401 | 4.5562 | 6.1207 | 7.7282 | 12.3986 | |

| 0.6786 | 0.7981 | 0.8968 | 0.9460 | 0.9871 | |

| 0.1567 | 0.0978 | 0.0491 | 0.0255 | 0.0060 | |

| 0.1647 | 0.1041 | 0.0541 | 0.0285 | 0.0069 | |

| 3.4142 | 4.5235 | 6.0755 | 7.6329 | 12.2536 | |

| 0.6807 | 0.7994 | 0.8983 | 0.9479 | 0.9878 | |

| 0.1560 | 0.0975 | 0.0488 | 0.0248 | 0.0056 | |

| 0.1633 | 0.1031 | 0.0529 | 0.0274 | 0.0066 | |

| 3.3822 | 4.4801 | 6.0220 | 7.5581 | 11.7469 | |

| 0.6920 | 0.8077 | 0.9036 | 0.9510 | 0.9897 | |

| 0.1520 | 0.0935 | 0.0458 | 0.0228 | 0.0048 | |

| 0.1560 | 0.0988 | 0.0505 | 0.0262 | 0.0055 | |

| 3.4139 | 4.4942 | 6.0156 | 7.5369 | 11.6268 | |

A formal comparison between the GDFM and GARCH(1,1) coverage performances should take into account the fact that the coverage results of the two methods, for given and , are not independent. The situation is quite similar to that of comparing paired proportions, where tests are to be carried out on the basis of the traditional McNemar, (1947) test. For given and , consider, for all , the events (discordant GDFM and GARCH coverage results)

and define

Consider the null hypothesis under which the indicators of a successful interval prediction in both methods are i.i.d. Bernoulli, with identical (but otherwise unspecified) coverage probabilities. The McNemar test of that hypothesis is conditioning on the sum of discordant coverage results: concordant results indeed carry no information on a difference between coverage probabilities. Conditional on , the null distribution of is binomial Bin. At probability level , the test rejects in favour of a better GDFM coverage for “large values” of , in favour of a better GARCH coverage for “small values” of the same (equivalently, “large values” of ), with critical values the and binomial quantiles, respectively.

Table 7 reports the McNemar empirical rejection frequencies (over the series)—in favour of a better GDFM coverage in the left-hand panel, in favour of a better GARCH coverage in the right-hand one. We consider the cases in which or , or , (for the GDFM); testing was performed at significance levels , , and . Irrespective of and , the GDFM approach appears to outperform, quite consistently and significantly, the GARCH one.