∎

China University of Petroleum, China

2. Key Laboratory of Electronics and Information Technology for Space Systems

National Space Science Center, CAS

33institutetext: Jundong Li 44institutetext: Computer Science and Engineering

Arizona State University, USA 55institutetext: Yunquan Song 66institutetext: Xijun Liang 77institutetext: College of Science

China University of Petroleum, China 88institutetext: Ling Jian 99institutetext: School of Economics and Management

China University of Petroleum, China

99email: bebetter@upc.edu.cn 1010institutetext: Huan Liu 1111institutetext: Computer Science and Engineering

Arizona State University, USA

Online Newton Step Algorithm with Estimated Gradient

Abstract

Online learning with limited information feedback (bandit) tries to solve the problem where an online learner receives partial feedback information from the environment in the course of learning. Under this setting, Flaxman et al. Flaxman2005Online extended Zinkevich’s classical Online Gradient Descent (OGD) algorithm Zinkevich2003Online by proposing the Online Gradient Descent with Expected Gradient (OGDEG) algorithm. Specifically, it uses a simple trick to approximate the gradient of the loss function by evaluating it at a single point and bounds the expected regret as Flaxman2005Online , where the number of rounds is . Meanwhile, past research efforts have shown that compared with the first-order algorithms, second-order online learning algorithms such as Online Newton Step (ONS) Hazan2007Logarithmic can significantly accelerate the convergence rate of traditional online learning algorithms. Motivated by this, this paper aims to exploit the second-order information to speed up the convergence of the OGDEG algorithm. In particular, we extend the ONS algorithm with the trick of expected gradient and develop a novel second-order online learning algorithm, i.e., Online Newton Step with Expected Gradient (ONSEG). Theoretically, we show that the proposed ONSEG algorithm significantly reduces the expected regret of OGDEG algorithm from to in the bandit feedback scenario. Empirically, we further demonstrate the advantages of the proposed algorithm on multiple real-world datasets.

1 Introduction

Online learning algorithms differ from conventional learning paradigms as they targeted at learning the model incrementally from data in a sequential manner given the knowledge (could be partial) of answers pertaining to previously made decisions. They have shown to be effective in handling large-scale and high-velocity streaming data and emerged to become popular in the big data era Hoi2018Online ; Hoi2014LIBOL . In recent years, a number of effective online learning algorithms have been investigated and applied in a variety of high-impact domains, ranging from game theory, information theory, to machine learning and data mining Ding2017Large ; Shai2011Online ; Wang2003Mining . Most previously proposed online learning algorithms fall into the well-established framework of online convex optimization Gordon1999Regret ; Zinkevich2003Online .

In terms of the optimization algorithms, online learning algorithms can be broadly divided into the following categories: (i) first-order algorithms which aim to optimize the objective function using the first-order (sub) gradient such as the well-known OGD algorithm Zinkevich2003Online ; and (ii) second-order algorithms which aim to exploit second-order information to speed up the convergence rate of the optimization process, such as the ONS algorithm Hazan2007Logarithmic . In online convex optimization, previous approaches are mainly based on the first-order optimization, i.e., optimization using the first-order derivative of the cost function. The regret bound achieved by these algorithms is often considered to be proportional to the polynomial of the number of rounds . For example, Zinkevich2003Online showed that with the simple OGD algorithm, we can achieve the regret bound of . Later on, Hazan2007Logarithmic introduced a new algorithm with ONS by exploiting the second-order derivative of the cost function, which can be regarded as an online analogy of the Newton-Raphson method Ypma1995Historical in the offline learning. Although the time complexity of ONS is higher than that of OGD ( denotes the number of features) per iteration, it guarantees a logarithmic regret bound with a warm assumption of the cost function.

Additionally, according to the forms of feedback information of the prediction, existing online convex optimization algorithms can be broadly classified into two categories Abernethy2012Interior : (i) online learning with full information feedback; and (ii) online learning with limited feedback (or bandit feedback) Dani2007The ; Hazan2016An ; Mcmahan2004Online ; Neu2013An . In the former scenario, full information feedback of the prediction is always revealed to the learner at the end of each round; while in the latter scenario, the learner only receives partial information feedback from the environment of the prediction. In many real-world applications, the full information feedback is often difficult to acquire while the cost of obtaining bandit feedback is often much lower. For example, in many e-commerce websites, users only provide positive feedback (e.g., clicks or purchasing behaviors) Suhara2013Robust ; Zoghi2017Online but do not necessarily disclose the full information feedback (e.g., fine-grained preferences). In this regard, online convex optimization with bandit feedback has motivated a surge of research interests in recent years. For example, Flaxman2005Online extended the OGD algorithm to the bandit setting, where the learner only knows the value of the cost function at the current prediction point while the cost function value at other points remains opaque. In particular, it uses a simple approximation of the gradient of the cost function at the current point , and bounds the expected regret (against an oblivious adversary) as .

As second-order algorithms such as ONS often lead to lower regret bound than the first-order methods when full information feedback is available, one natural question to ask is whether the success can be shifted to the bandit feedback scenario. To answer this question, in this paper, we make the initial investigation of the ONS algorithm when only partial feedback is available. Our main contribution is the development of a novel second-order online convex optimization algorithm which can reduce the regret bound from Flaxman2005Online to . Furthermore, if the cost function is -Lipschitz, we can further bound the regret as which is often desired in practical usage.

The remainder of this paper is organized as follows. In Section 2, we summarize some symbols used throughout this paper and present the preliminaries of the bandit convex optimization problem. In Section 3, we introduce the proposed Online Newton Step algorithm with Estimated Gradient in details. In Section 4, empirical evaluations on benchmark datasets are given to show the superiority of the proposed algorithm. In Section 5, we briefly review related work on bandit convex learning. The conclusion is presented in Section 6.

2 Preliminaries

In this section, we first present the notations and symbols used in the paper and then formally define the problem of bandit convex optimization.

2.1 Notations and Symbols

Table 1 lists the main notations and symbols used in this paper. We use bold lowercase characters to denote vectors (e.g., a), bold upper case characters to denote matrices (e.g., A), and to denote the transpose of A. For a positive definite matrix A, we use to denote the Mahalanobis norm of vector x with respect to A.

denotes the gradient operator. denotes a random variable that is distributed uniformly over . Under the bandit feedback setting, we use to denote the conditional expectation given the observations up to time .

| Notations | Definitions |

|---|---|

| convex feasible set | |

| the generalized projection of onto | |

| loss function of the iteration | |

| upper bound of on | |

| parameter of | |

| parameter of the -nice function |

2.2 Bandit Convex Optimization

Bandit convex optimization (BCO) are often performed for a sequence of consecutive rounds. In particular at each round , the online learner picks a data sample from a convex set . After the data sample is picked and used to make the prediction, a convex cost function is revealed, then the online learner suffers from an instantaneous loss . Under the online convex optimization framework, we assume that the sequence of loss functions are fixed in advance. And the goal of the online learner is to choose a sequence of predictions such that the regret defined as is minimized, where denotes the cumulative error across all rounds while denotes the cumulative error resulted from the optimal decisions in hindsight. In the full information feedback setting, the learner has access to the gradient of the loss function at any point in the feasible set . Conversely, in the BCO setting the given feedback is , which is the value of the loss function at the point it chooses.

In this paper, we assume that origin is contained in the feasible set with as diameter, so . Meanwhile, the loss functions are -nice function (see Hazan2016Graduated ) and bounded by (i.e. ).

3 The Proposed Online Newton Step Algorithm with Estimated Gradient

As mentioned previously, this paper focuses on the online learning problem with partial information feedback - the bandit setting. For example, in the multi-armed bandit problem (MAB) Salehi2017Stochastic ; Tekin2010Online : there are different arms, and on each round the learner chooses one of the arms which is denoted by a basic unit vector (indicate which arm is pulled). Then the learner receives a cost of choosing this arm, . The vector associates a cost for each arm, but the learner only has access to the cost of the arm she/he pulls.

In this setting, the functions change adversarially over time and we can only evaluate each function once and cannot access the gradient of directly for gradient descent. To tackle this issue, Flaxman2005Online proposed to use one-point estimate of the gradient. Specifically, for a uniformly random unit vector , we have 111The equation holds for . Theoretically, the vector is an estimate of the gradient with low bias, and thus it is an approximation of the gradient. In fact, is an unbiased estimator of the gradient of a smoothed version of , which can be mathematically formulated as As shown by Flaxman et al. Flaxman2005Online , the advantage of is that it is differentiable and we can estimate its gradient with a single call since (see LEMMA 2.1 in Flaxman2005Online for details). One should note that under the assumption of is bounded () and -nice222Hazan et al. show that these functions are rich enough to capture non-convex structure that exists in natural data. Hazan2016Graduated , we can prove that is -exp-concave function (when ) Hazan2007Logarithmic , which is a key property in the proof of Theorem 1.

Based on the merit of the equation , we extend the ONS to the setting of limited feedback and propose a novel second-order online learning method - Online Newton Step algorithm with Estimated Gradient algorithm (ONSEG). The proposed ONSEG algorithm is summarized as follows:

In the following, we give the regret analysis of the proposed Online Newton Step Algorithm with Estimated Gradient (ONSEG).

Theorem 3.1

Assume that for all t, function is -nice function (see Hazan2016Graduated ). For all in , , with the notation of , we have For , , and ONSEG gives the following guarantee on the expected regret bound:

: For any , OBSERVATION 3.2 in Flaxman2005Online shows that with a proper setting of the parameters , the picked points . Suppose we run the ONS algorithm on the functions (i.e., the smoothed function of ) on the feasible set . Let , then LEMMA 2.1 in Flaxman2005Online shows that . For convenience, we denote as in the following context. We first show that the following formulation provides an upper bound of the expected regret:

Let denotes the best chosen with the benefit of hindsight. By Lemma 3 Hazan2007Logarithmic , we have:

for For convenience, we can define according to the update rule of In this way, by the definition of , we have:

| (2) |

| (3) |

Multiplying the transpose of Eq.(2) by Eq.(3) we get:

Since is the projection of in the norm that can be induced by , we can obtain that (See Lemma 8 Hazan2007Logarithmic ):

This inequality justifies the reason of using the generalized projections rather than the standard projections. This fact together with Eq.(3) gives:

Now, by summing up over from to , it leads to the following inequality:

It should be noted that we use the fact that in the last inequality. By moving the term to the LHS, it leads to the expression for

Using the facts that and , and the choice of we get:

Taking expectation, and using the fact that , we obtain:

| (4) |

According to Lemma 11 in Hazan2007Logarithmic , Eq.(4) can be bounded by , via the setting of , , and . Now since , and , we have and . Then we get:

Let be as given in OBSERVATION 3.3 Flaxman2005Online . For any , as is the average of within , OBSERVATION 3.3 in Flaxman2005Online shows that . According to OBSERVATION 3.1 in Flaxman2005Online , we have . With these above observations, we can obtain the expectation regret upper bound of ONSEG as:

| (5) | |||||

By plugging in , we get the expression of the form , where , and . Setting and gives a value of . This gives the stated expected regret bound.

Theorem 3.2

In the proposed Online Newton Step Algorithm with Estimated Gradient, if each function is -Lipschitz, then for and , we have:

4 Empirical Evaluations

| Dataset | type | ||

|---|---|---|---|

| abalone | 4177 | 7 | regression |

| kin | 3000 | 8 | regression |

| ionosphere | 351 | 33 | classification |

| cancer | 683 | 9 | classification |

| SSE 180 | 680 | 94 | portfolio |

Empirical evaluations of the proposed method was performed on two regression datasets, two classification datasets, and one stock dataset, they are abalone, kin, ionosphere, cancer, and SSE 180. All datasets can be download from the libSVM repository333https://www.csie.ntu.edu.tw/\~cjlin/libsvmtools/datasets/ and EastMoney444http://choice.eastmoney.com/ (see Table 1 for details of each dataset). We compare the proposed second-order bandit learning algorithm ONSEG with the first-order bandit learning algorithm OGDEG Flaxman2005Online . In addition, in the scenario of online regression and online classification problems, OGD and ONS are baseline methods with the full information feedback. To accelerate the computational efficiency, ONSEG and ONS employ Sherman-Morrson-Woodbury formula Brookes2011The

to compute in time using only matrix-vector and vector-vector products after given and . All experiments are performed in MATLAB 7.14 environment on a single computer with 3.4 GHz Intel Core i5 processors and 8G RODRAM running under the Windows 10 operating system. The source code of the proposed ONSEG algorithm will be released upon the acceptance of the manuscript.

Online Regression

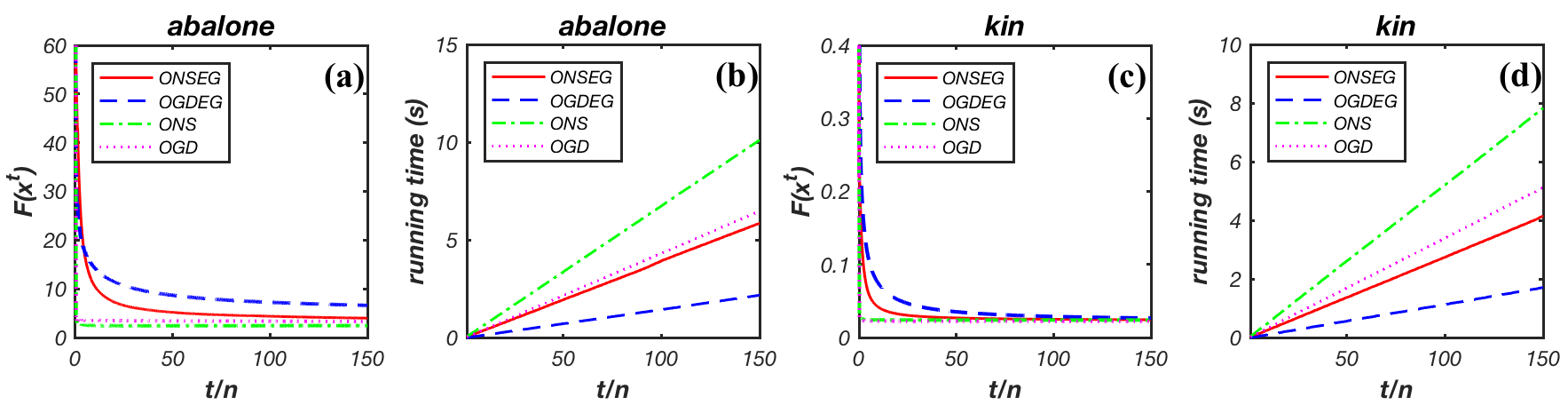

We first evaluate different methods in terms of regression on the abalone and kin datasets. We select the least square loss as the loss function, and use the mean squared error as the metric to evaluate different online learning algorithms, i.e., ONSEG, ONS, OGDEG, and OGD. Parameter settings of all the compared methods are as follows: OGD sets the step size , which changes with the increase of Hazan2006Efficient . Similarly, OGDEG sets the step size Flaxman2005Online . For ONS, we estimate for the abalone dataset and for the kin dataset according to Hazan2007Logarithmic . And in ONSEG, the smoothed parameter is set as Theorem 1 and the reciprocal of the step size, i.e. , is estimated to be for abalone and for kin. The experiments are performed over iterations and the results are depicted in Figure 1. reports the mean squared error of different algorithms w.r.t. number of iterations . As expected, the proposed ONSEG outperforms OGDEG, showing it converges faster. And also, in terms of the running time, we can also find that the proposed ONSEG is much more efficient than methods that require gradient such as ONS and OGD.

Online Classification

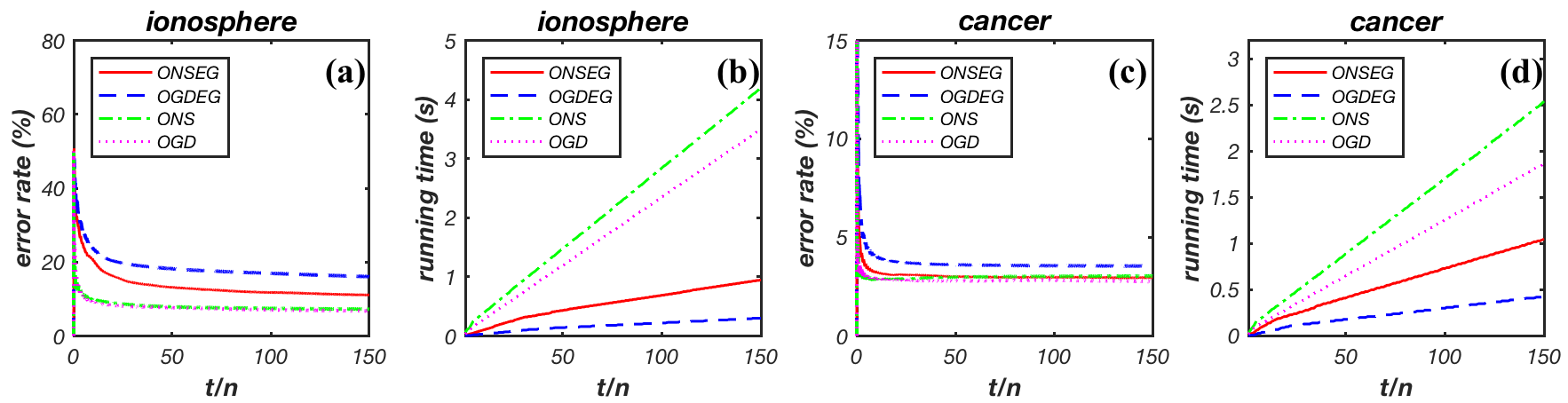

We evaluate different online learning methods in terms of the classification task. We select the logistic regression as the classifier, i.e., . According to the maximum likelihood estimation principle, we define the loss function as , where . Furthermore, the mean error rate is selected as the metric to evaluate different online learning algorithms. In this experiment, parameter settings are similar to the last subsection. OGD sets the step size . OGDEG sets the step size . For ONS, we estimate for ionosphere and for cancer according to Hazan2007Logarithmic . And in ONSEG, the smoothed parameter is set as Theorem 1, the reciprocal of the step size, i.e., is set to be for ionosphere and for cancer. Similarly, we run the experiments over iterations. The empirical results are shown in Figure 2. Generally, we have all the similar observations as the regression task.

Online Portfolio

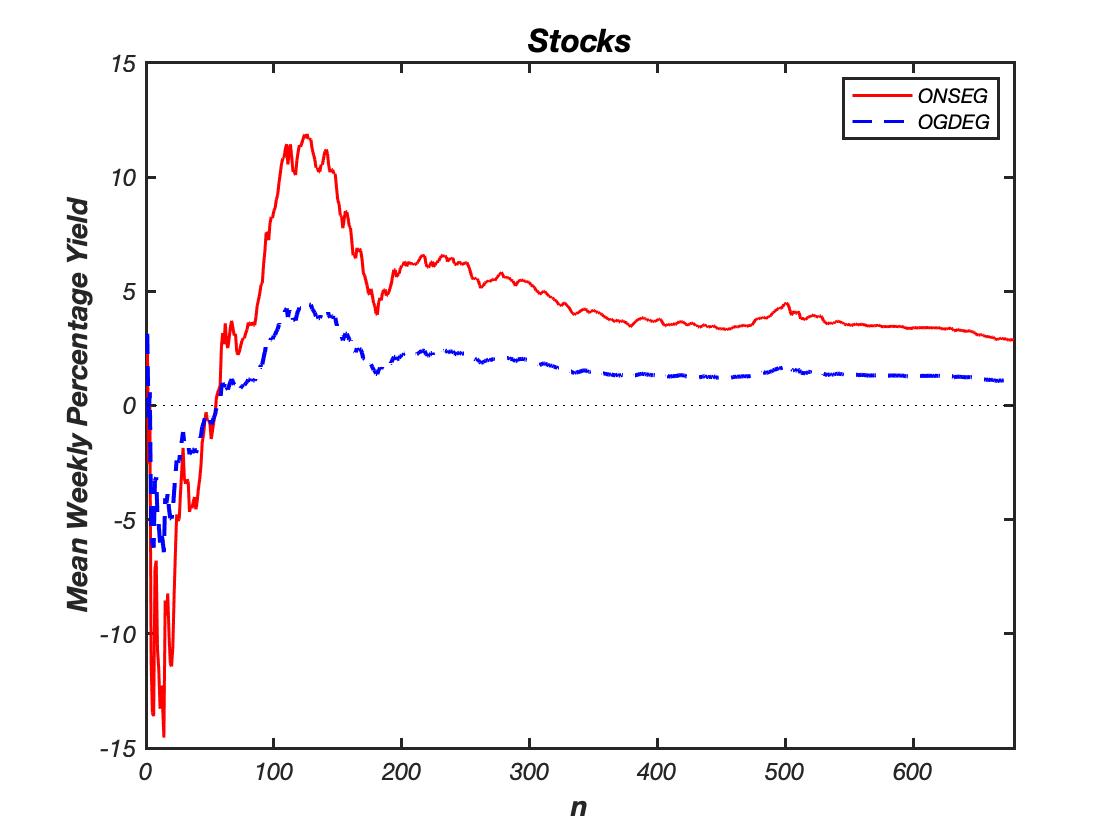

We finally evaluate different bandit online learning methods in terms of the portfolio task Hazan2006Efficient . In this experiment, we use stock market data (94 stokes selected from stock index of Shanghai Stock Exchange) date from Feb 6th, 2005 to Jan 31th, 2019 (weekly data) to simulate the portfolio task, which is a limited information feedback scenario. ONS and OGD are no longer applicable due to the absence of gradient information. Hence, we only compare two bandit online learning algorithms here, i.e., OGDEG and ONSEG. We select the return rate function as the objective function where satisfying stands for the weighted vector of the portfolio, denotes the vector of return rate corresponding to the current portfolio. The mean return rate (mean weekly percentage yield) is selected as the metric to evaluate different bandit online learning algorithms. Parameter settings of ONSEG and OGDEG are as follows: OGDEG sets the step size ; ONSEG sets the smoothed parameter as Theorem 1, the reciprocal of the step size, i.e., as . We report the average return rate (over 100 trials of 94 random stocks from the SSE 180) of the algorithms in Figure 3. As expected, the proposed ONSEG with 2.88% mean weekly percentage yields outperforms OGDEG with 1.02% return rate, showing that the proposed ONSEG is more efficient than OGDEG in the limited feedback information situation.

As a summary, expected gradient algorithms such as the proposed ONSEG are faster than the gradient algorithms such as ONS and OGD. In addition, the proposed second-order online learning method ONSEG converges faster than the first-order method OGDEG in the bandit feedback scenario. Hence, ONSEG provides a principled way to deal with large-scale bandit learning problems.

5 Related Work

In this section, we briefly review related work on bandit convex optimization algorithms which are closely related to the proposed ONSEG algorithm. The recent studies of bandit convex optimization were largely pioneered by Kleinberg2004Nearly and Flaxman2005Online . In particular, Flaxman2005Online proposed to use a simple trick to approximate the gradient of a function with a single data sample. Meanwhile, the authors provided an intuitive understanding of the approximation through the gradient of a smoothed function and proved that the proposed algorithm with a one-point estimate of the gradient achieve an expected regret bound as for convex bounded loss. For the setting of Lipschitz-continuous convex loss, a bound of were obtained by Kleinberg2004Nearly and Flaxman2005Online . To improve the regret bound of bandit online learning, numerous learning algorithms have been proposed. Among them, Dani2007The proposed the Geometric Hedge algorithm that results in an optimal regret bound of for linear loss functions. Motivated by the interior point methods, Abernethy2008Competing proposed a new algorithm that achieves the same nearly-optimal regret bound for the linear optimization problem in bandit scenario.

For some specifical classes of nonlinear convex losses, several methods have been proposed Saha2011Improved ; Bubeck2017Kernel ; Yang2016Optimistic ; Hazan2016Graduated ; Hazan2014Bandit . Under the assumption of strongly convex loss, Agarwal2010Optimal obtained an upper bound of . The follow-up work Saha2011Improved showed that for convex and smooth loss functions, we can make use of FTRL with a self-concordant barrier as regularization and attain a regret bound of by sampling around the Dikin ellipsoid. In a recent paper, Hazan and Levy Hazan2014Bandit investigated the bandit convex optimization problem. Specifically, they assumed that the adversary is limited to choose strongly convex and smooth loss functions while the player have options to choose points from a constrained set. In this setting, they developed an algorithm that achieves a regret bound of . While a recent paper by Shamir2013On shows that the lower bound of regret has to be even with the strongly convex and smooth assumptions.

6 Conclusions

In this paper, we propose a novel second-order online learning algorithm by extending the ONS algorithm to the bandit feedback scenario where we do not have access to the gradient of the loss function. Specifically, we present a simple trick to approximate the gradient of instantaneous loss function by evaluating the function at a single point. Theoretically, we bound the expected regret as which is superior to the existing first-order online bandit learning algorithms as they only achieved an expected regret bound of under mild assumptions of the loss functions. Under the further -Lipschitz continuous assumption of the loss function , we can tighten the regret upper bound as which is often desired in practical usage. Empirically, we also show that the proposed ONSEG algorithm results in a significant improvement over: (1) first-order bandit online learning algorithm OGDEG in terms of convergence rate; and (2) online learning methods that require gradient in terms of running time.

References

- (1) Abernethy, J., Hazan, E., Rakhlin, A.: Competing in the dark: An efficient algorithm for bandit linear optimization. In: Conference on Learning Theory, pp. 263–274 (2008)

- (2) Abernethy, J., Hazan, E., Rakhlin, A.: Interior-point methods for full-information and bandit online learning. IEEE Transactions on Information Theory 58(7), 4164–4175 (2012)

- (3) Agarwal, A., Dekel, O., Xiao, L.: Optimal algorithms for online convex optimization with multi-point bandit feedback. In: Conference on Learning Theory, pp. 28–40 (2010)

-

(4)

Brookes, M.: The matrix reference manual.

www.ee.ic.ac.uk/hp/staff/dmb/matrix/intro.

html (2011) - (5) Bubeck, S., Lee, Y.T., Eldan, R.: Kernel-based methods for bandit convex optimization. In: Proceedings of the 49th Annual ACM SIGACT Symposium on Theory of Computing, pp. 72–85. ACM (2017)

- (6) Dani, V., Hayes, T.P., Kakade, S.: The price of bandit information for online optimization. In: Conference on Neural Information Processing Systems, Vancouver, British Columbia, Canada, December, pp. 19–28 (2007)

- (7) Ding, Y., Liu, C., Zhao, P., Hoi, S.C.H.: Large scale kernel methods for online auc maximization. In: IEEE International Conference on Data Mining, pp. 91–100 (2017)

- (8) Flaxman, A.D., Kalai, A.T., Mcmahan, H.B.: Online convex optimization in the bandit setting: gradient descent without a gradient. In: Proceedings of the 16th Annual ACM-SIAM Symposium on Discrete Algorithms, pp. 385–394 (2005)

- (9) Gordon, G.J.: Regret bounds for prediction problems. In: 12th Conference on Computational Learning Theory, pp. 29–40 (1999)

- (10) Hazan, E.: Efficient Algorithms for Online Convex Optimization and Their Applications. Princeton University (2006)

- (11) Hazan, E., Agarwal, A., Kale, S.: Logarithmic regret algorithms for online convex optimization. Machine Learning 69(2-3), 169–192 (2007)

- (12) Hazan, E., Levy, K.: Bandit convex optimization: Towards tight bounds. In: Proceedings of the 28th Annual Conference on Advances in Neural Information Processing Systems, pp. 784–792 (2014)

- (13) Hazan, E., Levy, K.Y., Shalev-Shwartz, S.: On graduated optimization for stochastic non-convex problems. In: Proceedings of the 33th International Conference on Machine Learning, pp. 1833–1841 (2016)

- (14) Hazan, E., Li, Y.: An optimal algorithm for bandit convex optimization. arXiv:1603.04350 (2016)

- (15) Hoi, S.C.H., Sahoo, D., Lu, J., Zhao, P.: Online learning: A comprehensive survey. arXiv:1802.02871 (2018)

- (16) Hoi, S.C.H., Wang, J., Zhao, P.: Libol: A library for online learning algorithms. Journal of Machine Learning Research 15, 495–499 (2014)

- (17) Kleinberg, R.D.: Nearly tight bounds for the continuum-armed bandit problem. Advances in Neural Information Processing Systems pp. 697–704 (2004)

- (18) Mcmahan, H.B., Blum, A.: Online Geometric Optimization in the Bandit Setting Against an Adaptive Adversary. Springer Berlin Heidelberg (2004)

- (19) Neu, G., Bartók, G.: An efficient algorithm for learning with semi-bandit feedback. In: Algorithmic Learning Theory

- (20) Saha, A., Tewari, A.: Improved regret guarantees for online smooth convex optimization with bandit feedback. In: Proceedings of the 14th International Conference on Artificial Intelligence and Statistics, pp. 636–642 (2011)

- (21) Salehi, F., Celis, L.E., Thiran, P.: Stochastic optimization with bandit sampling. arXiv:1708.02544v2 (2017)

- (22) Shalev-Shwartz, S.: Online learning and online convex optimization. Foundations & Trends in Machine Learning 4(2), 107–194 (2011)

- (23) Shamir, O.: On the complexity of bandit and derivative-free stochastic convex optimization. Journal of Machine Learning Research 30, 3–24 (2013)

- (24) Suhara, Y., Suzuki, J., Kataoka, R.: Robust online learning to rank via selective pairwise approach based on evaluation measures. IMT 28(1), 22–33 (2013)

- (25) Tekin, C., Liu, M.: Online algorithms for the multi-armed bandit problem with markovian rewards. In: Communication, Control, and Computing, pp. 1675–1682 (2010)

- (26) Wang, H., Fan, W., Yu, P.S., Han, J.: Mining concept-drifting data streams using ensemble classifiers. In: ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pp. 226–235 (2003)

- (27) Yang, S., Mohri, M.: Optimistic bandit convex optimization. In: Proceedings of the 30th Annual Conference on Advances in Neural Information Processing Systems, pp. 2297–2305 (2016)

- (28) Ypma, Tjalling, J.: Historical development of the newton-raphson method. Siam Review 37(4), 531–551 (1995)

- (29) Zinkevich, M.: Online convex programming and generalized infinitesimal gradient ascent. In: Proceedings of the 20th International Conference on Machine Learning, pp. 928–936. AAAI Press (2003)

- (30) Zoghi, M., Tunys, T., Ghavamzadeh, M., Kveton, B., Szepesvari, C., Wen, Z.: Online learning to rank in stochastic click models. In: Proceedings of the 34th International Conference on Machine Learning, pp. 4199–4208 (2017)