High-Dimensional Robust Mean Estimation in Nearly-Linear Time

Abstract

We study the fundamental problem of high-dimensional mean estimation in a robust model where a constant fraction of the samples are adversarially corrupted. Recent work gave the first polynomial time algorithms for this problem with dimension-independent error guarantees for several families of structured distributions.

In this work, we give the first nearly-linear time algorithms for high-dimensional robust mean estimation. Specifically, we focus on distributions with (i) known covariance and sub-gaussian tails, and (ii) unknown bounded covariance. Given samples on , an -fraction of which may be arbitrarily corrupted, our algorithms run in time and approximate the true mean within the information-theoretically optimal error, up to constant factors. Previous robust algorithms with comparable error guarantees have running times , for .

Our algorithms rely on a natural family of SDPs parameterized by our current guess for the unknown mean . We give a win-win analysis establishing the following: either a near-optimal solution to the primal SDP yields a good candidate for — independent of our current guess — or a near-optimal solution to the dual SDP yields a new guess whose distance from is smaller by a constant factor. We exploit the special structure of the corresponding SDPs to show that they are approximately solvable in nearly-linear time. Our approach is quite general, and we believe it can also be applied to obtain nearly-linear time algorithms for other high-dimensional robust learning problems.

1 Introduction

1.1 Background

Consider the following statistical task: Given independent samples from an unknown mean and identity covariance Gaussian distribution on , estimate its mean vector within small -norm. It is straightforward to see that the empirical mean — the average of the samples — has -error at most from with high probability. Moreover, this error upper bound is best possible, within constant factors, among all -sample estimators. That is, in the aforementioned basic setting, there is a sample-optimal mean estimator that runs in linear time.

In this paper, we study the robust (or agnostic) setting when a constant fraction of our samples can be adversarially corrupted. We consider the following model of robust estimation (see, e.g., [DKK+16]) that generalizes other existing models, including Huber’s contamination model [Hub64]:

Definition 1.1.

Given and a family of distributions on , the adversary operates as follows: The algorithm specifies some number of samples , and samples are drawn from some (unknown) . The adversary is allowed to inspect the samples, removes of them, and replaces them with arbitrary points. This set of points is then given to the algorithm. We say that a set of samples is -corrupted if it is generated by the above process.

In the context of robust mean estimation studied in this paper, the goal is to output a hypothesis vector such that is as small as possible. How do we estimate in this regime? A moment’s thought reveals that the empirical mean inherently fails in the robust setting: even a single corrupted sample can arbitrarily compromise its performance. However, one can construct more sophisticated estimators that are provably robust. The information-theoretically optimal error for robustly estimating the mean of is [Tuk75, DG92, CGR15]. That is, when there are enough samples () one can estimate the mean to accuracy . 111Under different assumptions on the distribution of the good data, the optimal error guarantee may be different as well (see Section 1.2). However, the standard robust estimators (e.g., Tukey’s median [Tuk75]) require exponential time in the dimension to compute. On the other hand, a number of natural approaches (e.g., naive outlier removal, coordinate-wise median, geometric median, etc.) can only guarantee error (see, e.g., [DKK+16, LRV16]), even in the infinite sample regime. That is, the performance of these estimators degrades polynomially with the dimension , which is clearly unacceptable in high dimensions.

Recent work [DKK+16, LRV16] gave the first polynomial time robust estimators for a range of high-dimensional statistical tasks, including mean and covariance estimation. Specifically, [DKK+16] obtained the first robust estimators for the mean with dimension-independent error guarantees, i.e., whose error only depends on the fraction of corrupted samples but not on the dimensionality of the data. Since the dissemination of [DKK+16, LRV16], there has been a substantial number of subsequent works obtaining robust learning algorithms for a variety of unsupervised and supervised high-dimensional models. (See Section 1.3 for a summary of related work.)

Although the aforementioned works gave polynomial time robust learning algorithms for several fundamental learning tasks, these algorithms are at least a factor slower than their non-robust counterparts (e.g., the sample average for the case of mean estimation), hence are significantly slower in high dimensions. It is an important goal to design robust learning algorithms with near-optimal sample complexity that are also nearly as efficient as their non-robust counterparts. In particular, we propose the following broad question:

Can we design (nearly-)sample optimal robust learning algorithms — with dimension independent error guarantees — that run in nearly-linear time?

Here by nearly-linear time, we mean that the runtime is proportional to the size of the input, within poly-logarithmic in the input size and factors. In addition to its potential practical implications, we believe that understanding the above question is of fundamental theoretical interest as it can elucidate the effect of the robustness requirement on the computational complexity of high-dimensional statistical learning/estimation.

For example, for the prototypical problem of robustly estimating the mean of a high-dimensional distribution, previous robust algorithms [DKK+16, LRV16, SCV18] have runtime at least for constant . Since the input size is , we would like to obtain algorithms that run in time , where the notation hides logarithmic factors in its argument. As the main contribution of this paper, we obtain such algorithms under different assumptions about the distribution of the good data. Our algorithms have optimal sample complexity, provide the information-theoretically optimal accuracy, and — importantly — run in time .

1.2 Our Results

Our first algorithmic result handles the setting where the good data distribution is sub-gaussian with known covariance. Recall that a distribution on with mean is sub-gaussian if for any unit vector we have that . For this case, we show222To avoid clutter in the relevant expressions, all algorithms in this paper have high constant success probability. By standard techniques, the success probability can be boosted to , for any , at the cost of a increase in the sample complexity.:

Theorem 1.2 (Robust Mean Estimation for Sub-Gaussian Distributions).

Let be a sub-gaussian distribution on with unknown mean and identity covariance. Let and . Given an -corrupted set of samples drawn from , there is an algorithm that runs in time and outputs a hypothesis vector such that with probability at least it holds .

It is well-known (see, e.g., [DKK+17]) that the optimal error guarantee under the assumptions of Theorem 1.2 is , even in the infinite sample regime. Moreover, the sample complexity of the learning problem is known to be even without corruptions. Thus, our algorithm has best possible error guarantee and sample complexity, up to constant factors. Prior work [DKK+16, DKK+17] gave algorithms with the same error and sample complexity guarantees, but with runtime , even for constant . We note that for the very special case that , an error of is information-theoretically possible. However, as shown in [DKS17], any Statistical Query algorithm that runs in time needs to have error . Our algorithm achieves this accuracy guarantee in nearly-linear time. See Section 1.3 for a detailed summary of previous work.

Theorem 1.2 handles the case that the covariance matrix of the good data distribution is known a priori. This is a somewhat limiting assumption. In our second main algorithmic result, we obtain a similarly robust algorithm under the much weaker assumption that the covariance matrix is unknown and bounded from above. Specifically, we show:

Theorem 1.3 (Robust Mean Estimation for Bounded Covariance Distributions).

Let be a distribution on with unknown mean and unknown covariance matrix such that . Let and . Given an -corrupted set of samples drawn from , there is an algorithm that runs in time and outputs a hypothesis vector such that with probability at least it holds .

Similarly, the sample complexity of our algorithm is best possible within a logarithmic factor, even without corruptions; the error guarantee is known to be information-theoretically optimal, up to constants, even in the infinite sample regime. Previous algorithms [DKK+17, SCV18] gave the same sample complexity and error guarantees, but again with significantly higher time complexities in high dimensions. Specifically, the iterative spectral algorithm of [DKK+17] has runtime . See Section 1.3 for more detailed comparisons.

We note that an efficient algorithm for robust mean estimation under bounded covariance assumptions has been recently used as a subroutine [PSBR18, DKK+18b] to obtain robust learners for a wide range of supervised learning problems that can be phrased as stochastic convex programs. This includes linear and logistic regression, generalized linear models, SVMs (learning linear separators under hinge loss), and many others. The algorithm of Theorem 1.3 provides a faster implementation of such a subroutine, hence yields faster robust algorithms for all these problems.

1.3 Related and Prior Work

Learning in the presence of outliers is an important goal in statistics and has been studied in the robust statistics community since the 1960s [Hub64]. After several decades of work, a number of sample-efficient and robust estimators have been discovered (see [HR09, HRRS86] for book-length introductions). For example, the Tukey median [Tuk75] is a sample-efficient robust mean estimator for various symmetric distributions [DG92, CGR15]. However, it is NP-hard to compute in general [JP78, AK95] and the many heuristics for computing it degrade in the quality of their approximation as the dimension scales [CEM+93, Cha04, MS10].

Until recently, all known computationally efficient high-dimensional estimators could only tolerate a negligible fraction of outliers, even for the simplest statistical task of mean estimation. Recent work in the theoretical computer science community [DKK+16, LRV16] gave the first efficient robust estimators for basic high-dimensional unsupervised tasks, including mean and covariance estimation. Since the dissemination of [DKK+16, LRV16], there has been a flurry of research activity on robust learning algorithms in both supervised and unsupervised settings [BDLS17, CSV17, DKK+17, DKS17, DKK+18a, SCV18, DKS18b, DKS18a, HL18, KSS18, PSBR18, DKK+18b, KKM18, DKS19, LSLC18, CDKS18].

For the specific task of robust mean estimation, [DKK+16] designs two related algorithmic techniques with similar sample complexities and error guarantees: a convex programming method and an iterative spectral outlier removal method (filtering). The former method inherently relies on the ellipsoid algorithm (leading to polynomial, yet impractical, runtimes), while the latter only requires repeated applications of power iteration to compute the highest eigenvalue-eigenvector of a covariance-like matrix. The total number of power iteration calls can be as large as , for constant , leading to runtimes of the form . We note that the filter-based robust mean estimation algorithm, as presented in [DKK+16], applies to the sub-gaussian case (as in Theorem 1.2). A slight variant of the method [DKK+17] applies under second moment assumptions (as in Theorem 1.3).

The work [LRV16] gives a recursive dimension-halving technique with near-optimal accuracy, up to a logarithmic factor in the dimension. The aforementioned method requires computing the SVD of a second moment matrix times. Consequently, each iteration incurs runtime . Similarly, the robust mean estimation algorithm under bounded second moments in [SCV18] requires computing the SVD of a matrix multiple times, leading to runtime.

1.4 Our Approach and Techniques

In this section, we provide a detailed outline of our algorithmic approach in tandem with a brief comparison to the most technically relevant prior work. To robustly estimate the unknown mean , we proceed as follows: Starting with an initial guess , in a sequence of iterations we either certify that the current guess is close to the true mean or refine our current guess with a new one that is provably closer to .

Let be the uncorrupted unknown distribution and be the covariance of the good samples. Then we know that the second order moment is equal to when , and is equal to in general. Therefore, the second order moment is minimized when . We use this property to distinguish whether our guess is close to . Of course, the input contains both good samples and bad (corrupted) samples, and the bad samples can change the first two moments significantly. To get around this problem, we try to reweight the samples: let denote the following set

Our approach will try to minimize the weighted second order moment for all , with the intended solution being assigning weight to all the good samples. This can be formalized as an SDP:

| (1) |

This SDP is similar to the convex program used in [DKK+16] but has some important conceptual differences that allow us to get a faster algorithm. The convex program in [DKK+16] is essentially this SDP with . However, of course one cannot solve it directly as we do not know . To overcome this difficulty, [DKK+16] designs a separation oracle, which roughly corresponds to finding a direction of large variance. The whole convex programming algorithm in [DKK+16] then relies on the ellipsoid algorithm and is therefore slow in high dimensions.

In contrast, we fix a guess for the true mean in the SDP. Even though this may not be correct, we will establish a win-win phenomenon: either is a good guess of in which case we get a good set of weights, or is far from and we can efficiently find a new guess that is closer to by a constant factor.

More precisely, we will show that for any guess that is sufficiently close to the actual mean , the optimal value of the SDP is small. In this case, the weights computed by the SDP can be used to produce an accurate estimate of the mean: (see Lemma 3.2). Note that in this case the estimate will be more accurate than the current guess . On the other hand, when the guess is far from , the optimal value of the SDP is large, and the optimal dual solution gives a certificate on why the second order moment cannot be small no matter how we re-weight the samples using . Intuitively, the reason that the second moment matrix cannot have small spectral norm is because of the extra component in the expected second moment matrix. That is, the dual solution gives us information about (Lemma 3.3).

So far, we have sketched our approach of reducing the algorithmic problem to solving a small number of SDPs. To get a fast algorithm, we need to solve the primal and dual SDPs in nearly-linear time. We achieve this by reducing them to covering/packing SDPs and using the solvers in [ALO16, PTZ16]. We note that these solvers rely on the matrix multiplicative weights update method (mirror descent), though we will not use this fact in our analysis. The main technical challenge here is that the approximate solutions to the reduced SDPs may violate some of the original constraints (specifically, the resulting may not be in ). We show that our main arguments are robust enough to handle these mild violations.

A perhaps surprising byproduct of our results is that a natural family of SDPs leads to asymptotically faster algorithms for robust mean estimation than the previous fastest spectral algorithm [DKK+16] for the most interesting parameter regime (corresponding to large dimension so that ). We view this as an interesting conceptual implication of our results: in our setting, principled SDP formulations can lead to faster runtimes compared to spectral algorithms, by exploiting the additional structure of these SDPs. This phenomenon illustrates the value of obtaining a deeper understanding of such convex formulations.

1.5 Structure of This Paper

In Section 3, we describe our algorithmic approach for robust mean estimation and use it to obtain our algorithm for sub-gaussian distributions (thus establishing Theorem 1.2). In Section 4, we show that the corresponding SDPs can be solved in nearly-linear time. In Section 5, we adapt our approach from Section 3 to obtain our algorithm for robust mean estimation under bounded covariance assumptions (thus establishing Theorem 1.3). For the clarity of the presentation, some proofs have been deferred to an appendix.

2 Preliminaries

For , we use to denote the set . We use for the -th standard basis vector, and for the identity matrix. For a vector , we use and to denote the and norms of respectively. We use to denote the inner product of two vectors and : .

For a matrix , we use to denote the spectral norm of , and to denote the maximum eigenvalue of . We use to denote the trace of a square matrix , and or for the entry-wise inner product of and : . A symmetric matrix is said to be positive semidefinite (PSD) if for all vectors , . For two symmetric matrices and , we write when is positive semidefinite.

Throughout this paper, we use to denote the ground-truth distribution. We use for the dimension of , for the number of samples, and for the fraction of corrupted samples. Let be the original set of uncorrupted samples drawn from . After the adversary corrupts an -fraction of , we use to denote the remaining set of good samples, and to denote the set of bad samples added by the adversary. Note that is the input given to the algorithm, and we have , , and .

We use to denote the (unknown) true mean of , and to be our current guess for . We write for the -th sample. Both , , and the ’s are column vectors. For a vector , we define and , and we use to denote the empirical mean weighted by .

We call a vector a uniform distribution over a set if for all and otherwise. Let denote the convex hull of all uniform distributions over subsets of size . Formally,

3 Robust Mean Estimation for Known Covariance Sub-Gaussian Distributions

In this section, we will describe our algorithmic technique and give an algorithm establishing Theorem 1.2.

As we described in Section 1.4, our algorithm is going to make a guess for the actual mean , and try to certify its correctness by an SDP. In Section 3.1, we give the SDP formulation and describe the entire algorithm. In Section 3.2, we show that the optimal value of the primal/dual SDPs are closely related to the distance . When the current guess is close to , we show (Section 3.3) that the solution to the primal SDP is going to give an accurate estimate of . On the other hand, when the current guess is far, in Section 3.4 we analyze the dual solution and show how to find a new guess that is closer to . Finally, we combine these techniques and prove Theorem 1.2 in Section 3.5.

3.1 SDP Formulation and Algorithm Description

As we mentioned in Section 1.4, we will use an SDP to try to certify that our current guess is close to the true mean . To achieve that, we assign weights to the samples while making sure that . More precisely, the primal SDP with parameter and is defined below:

| (2) |

Intuitively, this SDP tries to re-weight the samples to minimize the second moment matrix . The intended solution to this SDP is to assign weight on each of the good samples. This solution will have a small objective value whenever is close to .

When is far from , we need to consider the dual of (2). We will first derive the dual of (2). Note that the primal SDP is equivalent to the following:

Strong duality holds in our setting because the primal SDP admits a strictly feasible solution. The dual SDP can now be written as follows:

Observe that once we fix a dual solution , it is easy to minimize the objective function over : the minimum value is attained by assigning weight to the smallest inner products. Therefore, the dual SDP can be equivalently written as follows:

| (3) |

The dual SDP (3) certifies that there are no good weights that can make the spectral norm small. The intended solution for the dual is , where is the direction between and . Note that when , the value is exactly the squared norm of the projection in the direction . Intuitively, if we project the samples onto the direction of , the mean of the good samples is going to be at distance , so even after removing the farthest -fraction of the projected samples one cannot make the remaining values of small. Of course, in general, the dual solution can be of rank higher than , but we will show that any near-optimal dual solution must be close to rank later in Section 3.4.

The SDPs are parameterized by and , which is our current guess of the true mean . We will solve both SDPs multiple times for different values of , and we will update iteratively based on the solutions to previous SDPs. Eventually, we will obtain some that is close enough to , so that the primal SDP is going to provide a good set of weights , and we can output the weighted empirical mean .

To avoid dealing with the randomness of the good samples, we require the following deterministic conditions on the original set of good samples (which hold with probability ) drawn from the sub-gaussian distribution. For all , we require the following conditions to hold for and for some universal constant :

| (4) | |||

| (5) |

Intuitively, Equations (4) show that removing any -fraction of good samples will not distort the mean and the covariance by too much. Equation (5) says that the good samples are not too far from the true mean.

We note that the above deterministic conditions are identical to the ones used in the convex programming technique of [DKK+16] to robustly learn the mean of . We note that the proof of these concentration inequalities does not require the Gaussian assumption, and it directly applies to sub-Gaussian distributions with identity covariance. It follows from the analysis in [DKK+16] that after samples, these conditions hold with probability at least on the set of good samples.

Throughout the rest of this section, we will assume that the above conditions are satisfied where we set the parameter to be a sufficiently small universal constant; selecting suffices for all our arguments.

We are now ready to present our algorithm (Algorithm 1) to robustly estimate the mean of known covariance sub-gaussian distributions.

Notation. In this section, we will use to denote universal constants that are independent of , , and . We will give a detailed description on how to set these constants in Appendix A.

3.2 Optimal Value of the SDPs

In this subsection, we will give upper and lower bounds on the optimal value of the SDPs (2) and (3). Recall that our high-level idea is to use the dual SDP to improve our guess , until it is close enough to the true mean , and then solve the primal SDP to get a good set of weights. However, we cannot write an if statement based on because we do not know .

Lemma 3.1 allows us to estimate from the optimal value of the SDPs. We will bound the optimal value of the SDPs from both sides using feasible primal and dual solutions. Let denote the optimal value of the SDPs (2), (3) with parameters and . The following lemma shows that when is small and is far away from , then both the optimal values and are close to .

Lemma 3.1 (Optimal Value of the SDPs).

Proof.

We first prove the argument for .

One feasible primal solution is to set for all (and for all ). Therefore,

Notice that can be viewed as a weight vector on and we have . This allows us to use Condition (4) in the second to last step.

One feasible dual solution is where . The dual objective value is the mean of the smallest -fraction of , which is at least

This is because , the smallest entries must include , where is the smallest entries in . Let for all and otherwise. Note that and , so can be viewed as a weight vector on with . Therefore we have

Now we consider . Intuitively, because both SDPs can throw away the bad samples first, and whether we allow them to throw away another -fraction of good samples should not affect the moments too much. It is easy to see that , because the feasible region with parameter is strictly larger () for the primal SDP.

It remains to show that the same lower bound holds for . For the dual SDP with parameter , the objective is the mean of the smallest -fraction of the entries, so we pick to be the smallest entries in and for all instead. Note that Condition (4) holds for all , and the rest of the proof is identical.

To obtain the simpler upper and lower bounds when , we note that the error term , so by increasing we can get . ∎

3.3 When Primal SDP Has Good Solutions

In this section, we show that a good primal solution for any guess will give an accurate weighted empirical mean. Lemma 3.2 proves the contrapositive statement: if the weighted empirical mean , with respect to weight-vector , is far from the true mean, then no matter what our current guess is, cannot be a good solution to the primal SDP. More specifically, we show that the objective value of is at least . Roughly speaking, we get a contribution of from the good samples and a contribution of from the bad samples.

We briefly explain why the bad samples contribute . The empirical mean of the good samples is off by at most by Condition (4). Now if is far away from , the bad samples must shift the mean by more than . Intuitively, if an -fraction of the samples distort the mean by , on average each of these sample contributes an error of , which introduces a total error of in the second moment matrix.

We use to denote (asymptotically) the distance between and at the end of our algorithm. This threshold appears naturally because if , then Lemma 3.1 tells us that . This error subsumes the potential error we could get due to the bad samples shifting the mean by more than , so we must guess some that is from to detect the bad samples. Note that given some at distance to , an optimal solution to the primal SDP will give a much better estimate that is close to .

Lemma 3.2 (Good Primal Solution Correct Mean).

Fix . Let , and . Let be a set of -corrupted samples drawn from a sub-gaussian distribution with identity covariance, where . For all , if where , then for all ,

Proof.

Fix any . If , then because is feasible and by Lemma 3.1,

Therefore, for the rest of this proof, we can assume .

We project the samples along the direction of . Consider the unit vector . To bound from below the maximum eigenvalue, it is sufficient to show that

We first bound from below the contribution of the bad samples by . By triangle inequality,

The last line follows from our choice of , and the good samples satisfy Condition (4). By Cauchy-Schwarz, Since , we have .

We continue to lower bound the contribution of the good samples to the quadratic form by . This is because the true covariance matrix is . By Condition (4),

Putting the good and bad samples together, we have as needed.

The constants in the proof are given in Appendix A. ∎

Lemma 3.2 guarantees that any good solution to the primal SDP gives a good set of weights. In other words, whenever we have a solution to the primal SDP whose objective value is at most , we are done because the weighted empirical mean must be close to the true mean.

3.4 When Primal SDP Has No Good Solutions

We now deal with the other possibility: the primal SDP has no good solution. We will show that, in this case, we can move closer to by solving the dual SDP (3), decreasing by a constant factor.

Lemma 3.1 states that . Intuitively, if the dual SDP throws away all the bad samples, then we know that . If this quantity also concentrates around its expectation, then

Because , we can remove from both sides and get . This condition implies that the top eigenvector of aligns approximately with , which provides a good direction for us to move .

The following lemma formalizes this intuition. Specifically, Lemma 3.3 shows that despite the error from solving the SDP approximately and the errors in the concentration inequalities, we can still use the top eigenvector of to move closer to .

Lemma 3.3 (Good Dual Solution Better ).

Fix and . Let . Assume we have a solution to the dual SDP (3) with parameters and , and the objective value of is at least . Then, we can efficiently find a vector , such that .

Proof.

Because is a feasible solution to the dual SDP (3) with parameters and , we know that . When , Lemma 3.1 implies that and . Since the objective value is the average of the smallest entries of , and one way to choose entries is to focus on the good samples,

We know and . Without loss of generality, we can assume is symmetric. Using Condition (4), we can prove that :

We will continue to show that the top eigenvector of aligns with . Let denote the eigenvalues of , and let denote the corresponding eigenvectors. The conditions on implies that . We decompose and write it as where . Using these decompositions, we can rewrite .

First observe that , because . Moreover, because , we know that . Thus, we have a unit vector with , so the angle between and is at most .

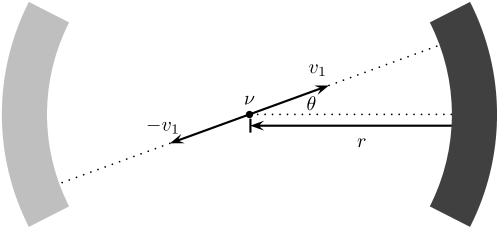

Finally, if we know the exact value of , we can update to . This corresponds to moving to a point that is on a circle of radius centered at (see Figure 1). The distance between and is maximized when is the largest, and this distance is at most . However, in reality, we do not know , and we can only estimate it from the value of . Because we are solving the SDPs to precision , by Lemma 3.1, we can estimate such that . By triangle inequality, the point is at most away from .

One technical issue is that the top eigenvector of can be , so we have two possible directions that are opposite of each other. Let be the point closer to , and be the point farther from . We can distinguish and by solving the SDP (2) with parameters and respectively, and the point with smaller optimal value is . This is because moves at least in the reverse direction, so the distance between and is at least . By Lemma 3.1, , and . Again because , this gap is large enough for separating them if we approximate both and to a factor of .

The constants in the proof are given in Appendix A. ∎

3.5 Proof of Theorem 1.2

We are now ready to prove Theorem 1.2. This is mostly done by applying Lemmas 3.2 and 3.3 in appropriate scenarios. Because of the geometric improvement in Lemma 3.3, we will apply it at most a logarithmic number of times, and then the algorithm can terminate in the case of Lemma 3.2.

Proof of Theorem 1.2 (Correctness and Runtime of Algorithm 1).

Let . When , Condition (4) holds for the good samples with probability at least , which is required in the proofs of Lemmas 3.1, 3.2, and 3.3.

We will use the empirical coordinate-wise median as our initial guess . It is folklore that with high probability, the coordinate-wise median is within of the true mean . In Algorithm 1, whenever we update by Lemma 3.3, we move it closer to . Therefore, throughout the algorithm, the condition always holds, which is required by Proposition 4.1.

The correctness of Algorithm (1) follows immediately from Lemmas 3.2, 3.3, and Proposition 4.1. In each iteration, the algorithm either finds a good solution to the primal SDP (2) and terminates, in which case Lemma 3.2 guarantees that the weighted empirical mean is close to ; or the algorithm finds a good solution to the dual SDP (3), and it will use the top eigenvector of to move the current guess closer to by a constant factor, as in Lemma 3.3. The failing probability is at most by a union bound over three bad events: (i) the good samples do not satisfy Condition (4), (ii) the coordinate-wise median is too far away from , and (iii) the SDP solver is not able to produce an approximate solution at some point.

We now analyze the running time of Algorithm 1. The coordinate-wise median can be computed in time . Whenever the primal SDP (2) has a good solution, the algorithm terminates. The initial choice of satisfies that , and Lemma 3.1 implies that we have a good primal solution if . Because every time we move as in Lemma 3.3, the distance between and decreases by a constant factor, we can move at most times. For each guess , we invoke Proposition 4.1 to either obtain a good primal or a good dual solution. We repeat every use of Proposition 4.1 times, so that the failure probability is at most by a union bound over the iterations. We will use the power method to compute the top eigenvector of , which takes time (see Remark 3.4). Thus, every loop of Algorithm 1 takes time . Therefore, the overall running time is

Remark 3.4.

Recall that the number of iterations of the power method is if we want to compute a -approximate largest eigenvector. Due to the slack in the geometry analysis of Lemma 3.3, we can set to a constant (say ). In addition, the matrix is given implicitly by the positive SDP solver (e.g., [PTZ16]) as the sum of matrix exponentials , where is the number of iterations of the positive SDP solver and for some . To evaluate in the power method, we multiply with each separately, where we use a degree matrix polynomial of to approximate . It takes time to compute , and therefore it takes time to evaluate .

4 Solving Primal/Dual SDPs in Nearly-Linear Time

By combining Lemmas 3.2 and 3.3 from Section 3, we know that we can make progress by either finding any solution to the primal SDP (2) with objective value at most , or by finding an approximately optimal solution to the dual SDP (3) whose objective value is at least . This section is dedicated to proving Proposition 4.1, which shows that this can be done in time .

Proposition 4.1.

Previously, nearly-linear time SDP solvers were developed for packing/covering SDPs [ALO16, PTZ16]. At a high level, we first relate SDPs (2), (3) with a pair of packing/covering SDPs (6), (7), where we switch the objective function with some constraint and introduce an additional parameter . Next, we show that to prove Proposition 4.1, it is sufficient to solve SDPs (6), (7) approximately for the correct value of , and moreover, we can run binary search to find a suitable . Finally, in Section 4.1, we show that our packing/covering SDPs (6), (7) can be solved in time . Note that these running times (specifically, the dependence on ) can be improved if better packing/covering SDP solvers are discovered. For example, [ALO16] mentioned the possibility of achieving a bound of by combining their approach and the techniques from [WMMR15].

| (6) |

| (7) |

where each is a PSD matrix given by333Recall that is the -th sample, and is the -th standard basis vector.

We will first show that the solutions of (6) and (7) are closely related to solutions of our original SDPs (2) and (3). Formally, the following lemma shows that if we (approximately) solve the packing/covering SDPs (6), (7) for some value of and the resulting objective values are close to , then we can translate these solutions back to obtain solutions for SDPs (2) (3) with objective value roughly .

Lemma 4.2.

Fix , and . If we have a solution of SDP (6) with parameters such that , then we can construct a solution of SDP (2) with parameters whose objective value is at most . If we have a solution of SDP (7) with parameters such that , then we can construct a solution of SDP (3) with parameters whose objective value is at least .

Proof.

We first construct a solution to SDP (2) with parameters given . Let . Since , we know that is feasible for SDP (2). SDP (6) guarantees that , so the objective value of SDP (2) at satisfies .

Next, we will construct a solution for the original dual SDP (3) with parameters given . We will work with the following SDP that is equivalent to the dual SDP (3):

Given a dual solution , it is easy to find the optimal values of variables: should be at the -th quantile for and . Under these choices, we recover the objective value of SDP (3), which is the mean of the smallest entries of .

Let , , and . Note that is well-defined, because we always have , otherwise the objective value is at least . Note that is a feasible solution to SDP (3): by the definition of , the constraint translates to , which is exactly . The objective value of is . ∎

We will use binary search to find a suitable , solve the packing/covering SDPs approximately, and then translate the solutions back using Lemma 4.2. The translated solutions will satisfy the conditions of Proposition 4.1. To make sure a suitable exists, we use the following lemma which shows the optimal value of SDPs (6), (7) is continuous and monotone in .

Lemma 4.3.

Proof.

To prove is continuous and non-increasing in , it is sufficient to show that for any and . Let , be optimal solutions that achieve and respectively. Because , is feasible for SDP (6) with parameter , and therefore . Similarly, is feasible for SDP (6) with parameter , because , and thus .

To prove , we focus on the original primal SDP (2) and the packing SDP (6). We first prove . Consider the optimal solution of SDP (2) with parameters . We can verify that is feasible for SDP (6) with parameters : The constraint on the bottom-right block of SDP (6) states that for all , and the constraint on the top-left block is equivalent to . Now assume if . Let be the optimal solution to SDP (6) with . This leads to a contradiction, because is feasible for SDP (2), but its objective value is . ∎

Proof of Proposition 4.1.

Fix and . We first prove that it is sufficient to find some , such that we can compute both

This holds for the following reason: Let and . Then we must have that either or . Assuming and leads to the following contradiction:

Moreover, because is the value of a solution to SDP (2) with parameters , we know that , as needed.

We will define a target interval , such that solving SDPs (6), (7) for any parameters ( will allow us to compute a pair of solutions and such that:

Then, by Lemma 4.2, we can convert these solutions to solutions of SDP (2) and (3) with values and .

We can first solve SDP (6) with , and check if the solution satisfies . If so, we use Lemma 4.2 to convert back to a solution of SDP (2) whose objective value is and we are done. For the rest of the proof, we assume .

Fix any and . Note that they are well-defined because is continuous, , and . For any , by monotonicity, we must have . Therefore, if we can solve the packing/covering SDPs (6), (7) approximately up to a multiplicative factor of , we can find a primal solution with , as well as a dual solution with .

It remains to show that we can find a suitable and solve the SDPs (6) (7) in time . We can find using binary search: if we will decrease , and if we will increase .

We first show that the binary search takes steps. Observe that by monotonicity, . When , Lemma 3.1 implies that and hence . If , then by the same argument as in the proof of Lemma 4.3, we must have , a contradiction. Therefore, the interval has length at least . In summary, we start with an interval of length less than , and the target interval has length at least , so binary search needs at most steps.

Finally, we bound from above the running time of the algorithm in this proposition. In each step of the binary search, we solve packing/covering SDPs (6), (7) for some . We solve these SDPs to precision as required in this proof, which takes time , by Corollary 4.5 from Section 4.1. We repeat every use of Corollary 4.5 times, so that the failure probability is at most when we take a union bound over all iterations. Eventually, when we have a suitable , we can convert the solution back to solutions for SDPs (2) (3) using Lemma 4.2. Therefore, the total running time is

4.1 Positive SDP Solvers

In this subsection, we show how to solve packing/covering SDPs (6), (7) in time . It is known that positive (i.e., packing/covering) SDPs can be solved in nearly-linear time and poly-logarithmic number of iterations [JY11, ALO16, PTZ16]. Because SDPs (6), (7) are packing/covering SDPs, we can apply the positive SDP solvers in [PTZ16] directly (Corollary 4.5).

Lemma 4.4 (Positive SDP Solver, [PTZ16]).

Let be PSD matrices given in factorized form . Consider the following pair of packing and covering SDPs:

We can compute, with probability at least , a feasible solution to the packing SDP with , and together a feasible solution to the covering SDP with in time , where is the total number of non-zero entries in the ’s.

An application of the above lemma yields the following corollary:

Corollary 4.5.

Proof.

The input matrices in the SDPs can be factorized as , where

The total number of non-zeros in all ’s is , so by Lemma 4.4, we can solve SDPs (6), (7) in time with probability . Note that the dual solution should be maintained implicitly to avoid writing down an matrix: the top-left block of the dual solution is , and the diagonals of the bottom-right block is . ∎

5 Robust Mean Estimation under Second Moment Assumptions

In this section, we use the algorithmic ideas from Section 3 to establish Theorem 1.3. The algorithm in this case is similar to the one for the sub-gaussian case with some important differences, due to the different concentration properties in the two settings.

Note that it suffices to prove Theorem 1.3 under the assumption that , i.e., the covariance satisfies . This is without loss of generality: Given a distribution with , we can first divide every sample by , run the algorithm to learn the mean, and multiply the output by .

We will require a set of conditions to hold for the good samples (similar to Conditions (4) and (5) for sub-gaussian distributions in Section 1.3). We would like the set of good samples to have bounded variance in all directions. However, because we did not make any assumption on the higher moments, it may be possible for a few good samples to affect the empirical covariance too much. Fortunately, such samples have small probability and they do not contribute much to the mean, so we can remove them in the preprocessing step (see Remark 5.1).

Recall that , and is the set . We require the following condition to hold: for all ,

| (8) | ||||

where and for some universal constants . It follows from Lemma A.18 of [DKK+17] that these conditions will be satisfied with high constant probability after samples.

The high-level approach is the same as in learning the mean of sub-gaussian distributions: we maintain as our current guess for the unknown mean , and try to move closer to by solving the dual SDP (3); eventually will be close enough, and the primal SDP (2) can provide good weights so that we can output the weighted empirical mean .

The algorithm will be almost identical to Algorithm 1. The only difference is in the “if” statement, where we need a different threshold to decide if the current primal SDP solution is good (or equivalently, whether our guess of is close enough to ).

We are now ready to present our algorithm (Algorithm 2) to robustly estimate the mean of bounded covariance distributions. Algorithm 2 is almost identical to Algorithm 1. The differences are highlighted in bold font. In the if statement, we need a different threshold to decide whether the current primal SDP solution is good (or equivalently, whether our guess of is close enough to ). We use Proposition 5.5 to solve the SDPs. In addition, we need to replace Lemmas 3.2 and 3.3 with Lemmas 5.3 and 5.4, but this merely changes our analysis and has no impact on the algorithm.

Remark 5.1.

We wish to throw away samples that are too far from . However, we do not know , so we run the following preprocessing step. We start with an -corrupted set of samples drawn from (the true distribution) and partition them into two sets of samples, and . We first compute the coordinate-wise median of . Notice that with high probability. We will use to throw away samples that are too far from .

Let be a ball of radius around . Let denote the original set of uncorrupted samples corresponds to . By the bounded-covariance assumption, we know that with high probability, -fraction of the samples in are in . Thus, if we change all samples in to , the resulting set is an -corrupted set of samples drawn from , and all samples in are not too far from . Therefore we can use as the input to Algorithm 2. In the rest of this section, we abuse notation and use to denote the fraction of corrupted samples in .

Notation. In this section, we use to denote universal constants. They can be chosen in a way that is similar to how we set constants for Section 3 in Appendix A.

5.1 Optimal Values of the SDPs

The following lemma is similar to Lemma 3.1. Specifically, Lemma 5.2 shows that when , is approximately . The difference is that (i) in Section 3, is roughly , because we know the true covariance matrix is , but in this section we only know the second moment matrix is bounded; and (ii) we need in both settings, but in this section (rather than as in Section 3) because the values of from the concentration bounds is different.

Lemma 5.2.

Proof.

We take the same feasible primal/dual solutions as in the proof of Lemma 3.1. We get different upper/lower bounds because we use Conditions (8) in this section.

Consider a feasible primal solution with for all and otherwise.

One feasible dual solution is where . Let denote the good samples with smallest . Let for all and otherwise.

The same upper/lower bounds hold for as well. ∎

5.2 When Primal SDP Has Good Solutions

We prove that if the weighted empirical mean is far away from the true mean, then the value of SDP (2) must be large.

The next lemma is similar to Lemma 3.2. The same intuition still holds: if -fraction of the samples distort the mean by , then they must introduce error to the second moment matrix. Note that because the true covariance matrix is no longer , we cannot say anything about the contribution of the good samples.

Lemma 5.3.

Fix . Let , , and . For all , if , then for all , .

Proof.

By Lemma 5.2, we know that if , we have . Therefore, we can assume that .

Let denote the optimal primal solution. For , we have

By the Cauchy-Schwarz inequality and the fact that , we get that . We conclude the proof by observing that

5.3 When Primal SDP Has No Good Solutions

We show that when the primal SDP has no good solutions, we can solve the dual (approximately) and the dual will allow us to move closer to by a constant factor. The next lemma is similar to Lemma 3.3. The first part of the argument changes slightly because we are using Condition (8), while the second part (the geometric argument) is identical to that of Lemma 3.3.

Lemma 5.4.

Fix and . Assume is a solution to dual SDP (3) with parameters , and the objective value of is at least . Then, we can efficiently find a vector such that .

Proof.

By Lemma 5.2, we know that implies that and thus . The dual objective is the mean of the smallest -fraction of the entries . Because one way to choose -fraction is to focus on the good samples,

We know that , . Without loss of generality, we can assume is symmetric. By Condition (8), we can prove as follows.

Therefore, we have a matrix whose inner product with is approximately maximized, this implies that the top eigenvector of aligns with . We omit the rest of the proof because the geometric analysis is identical to that of Lemma 3.3. ∎

5.4 Proof of Theorem 1.3

In this section we prove Theorem 1.3 (Correctness and Runtime of Algorithm 2). By combining Lemmas 5.3 and 5.4, we can make progress by either finding a solution to the primal SDP (2) with objective value at most , or finding an approximately optimal solution to the dual SDP (3) whose objective value is at least . This next proposition shows that this can be done in time .

Proposition 5.5.

We omit the proof of Proposition 5.5 because its proof is almost identical to the proof of Proposition 4.1. The only difference is that the ratio between the objective values of the desired primal/dual solutions is now , instead of as in Proposition 4.1. The problem of computing a desired pair of solutions becomes easier since the gap is larger.

Theorem 1.3 follows directly from Lemmas 5.3, 5.4, and Proposition 5.5. The running time analysis is identical to that of Theorem 1.2, we can move our guess at most times, and for each guess we invoke Proposition 5.5 to obtain a good primal or dual solution. The overall running time is .

Remark 5.6.

We note that in Algorithm 2, we are interested in whether the optimal value of SDPs (2) and (3) is at least or at most . Moreover, when we improve our guess using Lemma 5.4, the dual solution needs to be -approximately optimal. Therefore, we only need to solve SDPs (2) and (3) to precision for some constant . However, we do not know how to solve these SDPs directly in time, and when we reduce them to packing/covering SDPs, the constraint on becomes the objective function in SDP (6), and we must solve SDP (6) more precisely to precision (see, e.g., Lemma 4.2). This is the only reason that we need to pay in the running time of Algorithm 2.

6 Conclusions and Future Directions

In this paper, we studied the problem of robust high-dimensional mean estimation for structured distribution families in the presence of a constant fraction of corruptions. As our main technical contribution, we gave the first algorithms with dimension-independent error guarantees for this problem that run in nearly-linear time. We hope that this work will serve as the starting point for the design of faster algorithms for high-dimensional robust estimation.

A number of natural directions suggest themselves: Do our techniques generalize to robust covariance estimation? We believe so, but we have not explored this direction in the current work. Can we obtain nearly-linear time robust algorithms for other inference tasks under sparsity assumptions [BDLS17] (e.g., for robust sparse mean estimation or robust sparse PCA)? Can we speed-up the convex programs obtained via the SoS hierarchy in this setting [HL18, KSS18]?

The running time of our algorithms is , i.e., it is nearly-linear when the fraction of corruptions is constant. Can we avoid the extraneous dependence in the runtime? We believe progress in this direction is attainable. Note that solving a single covering SDP to multiplicative accuracy incurs a slowdown. Is it possible to reframe the underlying optimization problem so that a constant factor multiplicative accuracy suffices? Alternatively, is it possible to speed-up the iterative filtering technique of [DKK+16]? Exploring alternate certificates of robustness may be a promising avenue towards these goals.

Acknowledgments

We thank Alistair Stewart for useful discussions.

References

- [AK95] E. Amaldi and V. Kann. The complexity and approximability of finding maximum feasible subsystems of linear relations. Theoretical Computer Science, 147:181–210, 1995.

- [ALO16] Z. Allen-Zhu, Y. Lee, and L. Orecchia. Using optimization to obtain a width-independent, parallel, simpler, and faster positive SDP solver. In Proc. 27th Annual Symposium on Discrete Algorithms (SODA), pages 1824–1831, 2016.

- [BDLS17] S. Balakrishnan, S. S. Du, J. Li, and A. Singh. Computationally efficient robust sparse estimation in high dimensions. In Proc. 30th Annual Conference on Learning Theory (COLT), pages 169–212, 2017.

- [CDKS18] Y. Cheng, I. Diakonikolas, D. M. Kane, and A. Stewart. Robust learning of fixed-structure Bayesian networks. In Proc. 33rd Annual Conference on Neural Information Processing Systems (NIPS), 2018.

- [CEM+93] K. L. Clarkson, D. Eppstein, G. L. Miller, C. Sturtivant, and S.-H. Teng. Approximating center points with iterated Radon points. In Proc. 9th Annual Symposium on Computational Geometry (SoCG), pages 91–98, New York, NY, USA, 1993. ACM.

- [CGR15] M. Chen, C. Gao, and Z. Ren. Robust covariance and scatter matrix estimation under Huber’s contamination model. CoRR, abs/1506.00691, 2015.

- [Cha04] T. M. Chan. An optimal randomized algorithm for maximum Tukey depth. In Proc. 15th Annual Symposium on Discrete Algorithms (SODA), pages 430–436, 2004.

- [CSV17] M. Charikar, J. Steinhardt, and G. Valiant. Learning from untrusted data. In Proc. 49th Annual ACM Symposium on Theory of Computing (STOC), pages 47–60, 2017.

- [DG92] D. L. Donoho and M. Gasko. Breakdown properties of location estimates based on halfspace depth and projected outlyingness. Ann. Statist., 20(4):1803–1827, 12 1992.

- [DKK+16] I. Diakonikolas, G. Kamath, D. M. Kane, J. Li, A. Moitra, and A. Stewart. Robust estimators in high dimensions without the computational intractability. In Proc. 57th IEEE Symposium on Foundations of Computer Science (FOCS), pages 655–664, 2016.

- [DKK+17] I. Diakonikolas, G. Kamath, D. M. Kane, J. Li, A. Moitra, and A. Stewart. Being robust (in high dimensions) can be practical. In Proc. 34th International Conference on Machine Learning (ICML), pages 999–1008, 2017. Full version available at https://arxiv.org/abs/1703.00893.

- [DKK+18a] I. Diakonikolas, G. Kamath, D. M. Kane, J. Li, A. Moitra, and A. Stewart. Robustly learning a Gaussian: Getting optimal error, efficiently. In Proc. 29th Annual Symposium on Discrete Algorithms (SODA), pages 2683–2702, 2018.

- [DKK+18b] I. Diakonikolas, G. Kamath, D. M Kane, J. Li, J. Steinhardt, and A. Stewart. Sever: A robust meta-algorithm for stochastic optimization. arXiv preprint arXiv:1803.02815, 2018.

- [DKS17] I. Diakonikolas, D. M. Kane, and A. Stewart. Statistical query lower bounds for robust estimation of high-dimensional Gaussians and Gaussian mixtures. In Proc. 58th IEEE Symposium on Foundations of Computer Science (FOCS), pages 73–84, 2017.

- [DKS18a] I. Diakonikolas, D. M. Kane, and A. Stewart. Learning geometric concepts with nasty noise. In Proc. 50th Annual ACM Symposium on Theory of Computing (STOC), pages 1061–1073, 2018.

- [DKS18b] I. Diakonikolas, D. M. Kane, and A. Stewart. List-decodable robust mean estimation and learning mixtures of spherical Gaussians. In Proc. 50th Annual ACM Symposium on Theory of Computing (STOC), pages 1047–1060, 2018.

- [DKS19] I. Diakonikolas, W. Kong, and A. Stewart. Efficient algorithms and lower bounds for robust linear regression. In Proc. 30th Annual Symposium on Discrete Algorithms (SODA), 2019.

- [HL18] S. B. Hopkins and J. Li. Mixture models, robustness, and sum of squares proofs. In Proc. 50th Annual ACM Symposium on Theory of Computing (STOC), pages 1021–1034, 2018.

- [HR09] P. J. Huber and E. M. Ronchetti. Robust statistics. Wiley New York, 2009.

- [HRRS86] F. R. Hampel, E. M. Ronchetti, P. J. Rousseeuw, and W. A. Stahel. Robust statistics. The approach based on influence functions. Wiley New York, 1986.

- [Hub64] P. J. Huber. Robust estimation of a location parameter. Ann. Math. Statist., 35(1):73–101, 03 1964.

- [JP78] D. S. Johnson and F. P. Preparata. The densest hemisphere problem. Theoretical Computer Science, 6:93–107, 1978.

- [JY11] R. Jain and P. Yao. A parallel approximation algorithm for positive semidefinite programming. In Proc. 52nd IEEE Symposium on Foundations of Computer Science (FOCS), pages 463–471, 2011.

- [KKM18] A. Klivans, P. Kothari, and R. Meka. Efficient algorithms for outlier-robust regression. In Proc. 31st Annual Conference on Learning Theory (COLT), pages 1420–1430, 2018.

- [KSS18] P. K. Kothari, J. Steinhardt, and D. Steurer. Robust moment estimation and improved clustering via sum of squares. In Proc. 50th Annual ACM Symposium on Theory of Computing (STOC), pages 1035–1046, 2018.

- [LRV16] K. A. Lai, A. B. Rao, and S. Vempala. Agnostic estimation of mean and covariance. In Proc. 57th IEEE Symposium on Foundations of Computer Science (FOCS), 2016.

- [LSLC18] L. Liu, Y. Shen, T. Li, and C. Caramanis. High dimensional robust sparse regression. CoRR, abs/1805.11643, 2018.

- [MS10] G. L. Miller and D. Sheehy. Approximate centerpoints with proofs. Comput. Geom., 43(8):647–654, 2010.

- [PSBR18] A. Prasad, A. S. Suggala, S. Balakrishnan, and P. Ravikumar. Robust estimation via robust gradient estimation. arXiv preprint arXiv:1802.06485, 2018.

- [PTZ16] R. Peng, K. Tangwongsan, and P. Zhang. Faster and simpler width-independent parallel algorithms for positive semidefinite programming. arXiv preprint arXiv:1201.5135v3, 2016.

- [SCV18] J. Steinhardt, M. Charikar, and G. Valiant. Resilience: A criterion for learning in the presence of arbitrary outliers. In Proc. 9th Innovations in Theoretical Computer Science Conference (ITCS), pages 45:1–45:21, 2018.

- [Tuk75] J. W. Tukey. Mathematics and picturing of data. In Proceedings of ICM, volume 6, pages 523–531, 1975.

- [WMMR15] D. Wang, M. W. Mahoney, N. Mohan, and S. Rao. Faster parallel solver for positive linear programs via dynamically-bucketed selective coordinate descent. arXiv preprint arXiv:1511.06468, 2015.

Appendix A Setting Constants in Section 3

In this section, we describe how to set universal constants in Section 3. The constants are set in the following order: , , , , , , and . In this order, every only depends on the constants set before it, and there are only lower bounds on the value of , so we can set to a sufficiently large constant. Note that is the last constant we choose, and our guarantee at the end of the day is to output some hypothesis vector that is close to the true mean : .

Recall that in Section 3, , , , and .

The constant appears in the concentration bounds for the good samples (Condition (4)), and it is related to the constants in Chernoff bounds and Hanson-Wright inequality. We can set to be any constant that Condition (4) holds with the right sample complexity.

The constant is a threshold on . When , we can show that is roughly . We set to satisfy as required by Lemma 3.1.

The constant shows up in the branching statement of Algorithm 1. If we use the primal SDP solution, otherwise we use the dual SDP solution. We set to satisfy in the proof of Lemma 3.3, and in the proof of Proposition 4.1.

If we use the dual solution, we know that . If we use the primal solution, we have . We choose where and as needed in the proof of Lemma 3.2.

In the proof of Lemma 3.2, the constants and appear when we argue that the bad samples contribute at least to the second-moment, and the good samples contribute at least . We choose such that , and such that . Finally, because the good samples shift the mean by at most , if the empirical mean is off by more than then most of the error are from the bad samples. We choose so that .