Arbitrage Opportunities in CDS Term Structure: Theory and Implications for OTC Derivatives \authorRaymond Brummelhuis\thanksDept. of Mathematics & Computer Science, Univ. of Reims, France, raymondus.brummelhuis@univ-reims.fr \andZhongmin Luo\thanksDept. of Economics, Mathematics & Statistics, Birkbeck, Univ. of London, UK, zhongmin.luo@btinternet.com.

Abstract

Absence-of-Arbitrage (AoA) is the basic assumption underpinning derivatives pricing theory. As part of the OTC derivatives market, the CDS market not only provides a vehicle for participants to hedge and speculate on the default risks of corporate and sovereign entities, it also reveals important market-implied default-risk information concerning the counterparties with which financial institutions trade, and for which these financial institutions have to calculate various valuation adjustments (collectively referred to as XVA) as part of their pricing and risk management of OTC derivatives, to account for counterparty default risks. In this study, we derive No-arbitrage conditions for CDS term structures, first in a positive interest rate environment and then in an arbitrary one. Using an extensive CDS dataset which covers the 2007-09 financial crisis, we present a catalogue of 2,416 pairs of anomalous CDS contracts which violate the above conditions. Finally, we show in an example that such anomalies in the CDS term structure can lead to persistent arbitrage profits and to nonsensical default probabilities. The paper is a first systematic study on CDS-term-structure arbitrage providing model-free AoA conditions supported by ample empirical evidence.

Keywords: Arbitrage; Asset pricing; OTC derivatives; CVA; XVA; valuation adjustment; counterparty credit risk.

1 Introduction

Derivative pricing theory has as its basic assumption that the financial markets are arbitrage-free, in the sense that there should not exist an opportunity to make a risk-free profit without initial setup costs. With an appropriate mathematical definition (a non-trivial matter, especially in a continuous-time framework: see for example Delbaen and Schachermayer (2006, [16]), Absence-of-Arbitrage can be shown to be equivalent to the existence of an equivalent martingale measure with respect to which prices can be evaluated as expectations of discounted pay-offs: see for example Bjork [5] (2005).

The Over-The-Counter or OTC derivatives represent a market with a notional of US$532 trillion (BIS Statistics [2], 2017), including derivatives on foreign exchange, interest rates, commodities, credit, equities and other derivatives. As part of OTC derivatives market, the Credit Default Swap (or CDS) not only allows participants to speculate on and hedge credit risks, it also reveals market-implied default-risk information about financial institutions’ counterparties. The latter is critical for the pricing and risk-management of OTC derivatives (especially for non-centrally cleared ones), in order to properly account for counterparty credit risk in the form of Credit Valuation Adjustment or CVA and other valuation adjustments collectively referred to as XVA: see for example Brigo, Morini and Pallavicini [6] (2013). One of the main lessons learned from the 2007-09 financial crisis is that the market failed to properly account for counterparty default risks in the pricing and risk management of OTC derivatives. A lot of progresses have been made in this area since the crisis111See for example Brigo, Francischello and Pallavicini for non-linear valuation adjustment pricing framework (2015, [9]), Crepey et al (2013, [14]) for a BSDE-based (Backward stochastic differential equation) approach and Burgard and Kjaer (2013,[13]) for a replicating approach for FVA; Green, Kenyon and Dennis (2014, [17]) and Green and Kenyon (2015, [18]) among others extended the replicating approach to include capital and margin requirements in forms of KVA (Capital Valuation Adjustment) and MVA (Margin Valuation Adjustment) respectively.. In practice, the post-crisis pricing and risk management of OTC derivatives in banks consist of two parts, risk-neutral valuation of the derivative by the Front Office assuming there is no counterparty-default- risk, and the addition of an array of valuation adjustments conducted by the XVA Desk, also computed by risk-neutral valuation in risk-neutral world. Valuation adjustments have become standard practice in pricing and risk management of OTC derivatives for most large banks.

Literature often highlights that a CVA can be seen as a Contingent CDS or CCDS (cf. Brigo, Morini and Pallavicini [6], 2013), which pays the Loss-Given-Default on the residual net present value of a given portfolio. A CCDS is a type of credit derivatives whose notional and maturity are contingent on the time-of-default of an underlying reference entity. To price the CVA or CCDS, the default risk of the reference entity has to be calibrated to liquid CDS rates in a presumably arbitrage-free market. However, this element of the CVA pricing has not received much attention; essentially, the literature typically assumes that the counterparties of financial institutions either have liquidly quoted CDSs contracts on their names, or that sound proxies are available and that the CDS market is arbitrage-free. However, as regards the former assumption, as highlighted in Brummelhuis and Luo (2018a) [10], the vast majority of counterparties of financial institutions are not liquidly quoted in the CDS market and CDS proxy rates have to be constructed. In that reference, a CDS-proxy construction method via Machine Learning techniques has been proposed and shown to be more sound and to produce more accurate results than existing proxy methods: see Brummelhuis and Luo (2018b) [11], for a benchmarking exercise. Regarding the latter, as shown below, the CDS market is not as arbitrage-free as assumed in derivatives pricing theory; in fact, a significant amount of CDS-term-structure arbitrage opportunities exist in the CDS market. Alternatively, interested readers can find a shorter version of the paper for ML-based CDS Proxy Construction in Brummelhuis and Luo (2017 [12]).

Using simple arguments we show that, for CDS contracts of varying maturity on a given name, the CDS-spread times the maturity has to be an increasing function of the maturity. This can be shown without making any modeling assumptions if the risk-free interest rates are positive. When risk-free rates can be negative we derive a version of this theorem in which we multiply the CDS-spreads not by the maturity, but by what we will call the standardized risk-free annuity, which is the present value of an annuity paying a standardized interest rate of 1 over the life-time of the CDS contract (at the same payment dates as the CDS). In the case of positive interest rates this strengthens the first condition above, but its derivation assumes the existence of an equivalent martingale measure or risk-neutral pricing measure222For finite period markets the existence of such a measure is equivalent to absence of arbitrage, but for general continuous time markets in which prices are semi-martingales the latter has to be strengthened to for example the NFLVR-condition of Delbaen and Schachermayer (1994) [15]; in this paper we will generally disregard such subtleties. and the conditional independence of default-times of the other market variables. These assumptions also underlie current standard practice in banks for deriving market-implied (or risk-neutral) default probabilities from CDS quotes by the so-called Bootstrapping approach (see for example O’Kane (2008), [21]) as well as the evaluation of CVAs. We then found that these absence-of-arbitrage conditions can be violated in CDS markets: see subsection 1.1 and section 4 below.

Despite the uniquely important role played by the CDS market, there are only a limited number of studies on CDS-related arbitrage: see Kapadia and Pu (2012, [20]) for an example regarding arbitrage between CDS and equity markets and Bai and Collin-Dufresne (2012, [1]) for an example on arbitrage between CDS and bond markets. A recent study by Jarrow et al (2018, [19]) focused on statistical arbitrages in the CDS term structure by identifying mis-pricing of CDSs based on the gaps between theoretical CDS prices and observed ones; their results however are model-dependent, contrary to ours.

There are potential implications of CDS-term-structure arbitrage for the pricing and risk management of both credit derivatives and general OTC derivatives, because of the requirement to compute the valuation adjustments. Given the importance of the No-arbitrage assumption in deriving default probabilities from observed CDS curves in a presumably efficient CDS market, it is important to understand to what extent this market is arbitrage-free. Do we see potential arbitrage opportunities and are these being taken advantage of by arbitrageurs? As we will see, the answers to this are, respectively, a ”yes” and a ”no”. These questions are of fundamental importance for the pricing and risk management of credit derivatives and XVA.

In the remainder of this introductory section we first present an overview of anomalous CDS trades which violate the simplest of our No-arbitrage conditions and which motivated our study. We then more formally list the research gaps we identified and the contributions we believe this paper makes to the existing literature.

1.1 Anomalous CDS term structures

Let and be the mid-point CDS spreads of two co-initial standard single-name CDS contracts starting at with maturities but otherwise being identical333It means identical vintage, underlying bond, seniority type, currency and notional, etc. in ISDA master agreement.. According to Theorem 1 in section 2, Absence-of-Arbitrage (AoA) in the CDS market implies that:

| (1) |

We will call the pair of CDS trades for which (1) is violated an Arbitrage Trade or more briefly an Anomaly. Note that in that case, necessarily , so the CDS curve is inverted. Inverted yield curves are well-studied by researchers but inverted CDS curves have not attracted much attention from researchers. O’Kane (2008, [21]) remarked that model-independent arbitrage may exist in the CDS market and that negative implied default probabilities can occur for inverted CDS curves. He stated a condition similar to (1) but in a form and with a derivation which suggests it is only holds approximatively, while it is in fact exact. Brigo and Mercurio [8] (2006) also commented on the possibility of negative hazard rates as a result of inverted CDS curves. However, no systematic study has been conducted to assess the significance of this an issue and its implications for OTC derivatives.

In the case of an anomaly violating (1) as described above, an arbitrageur would simultaneously sell the protection against the default of an entity (”Short the CDS”) for a rate over the period of and buy the default protection against the same entity (”Long the CDS”) for a rate of over the period . We refer to this as a paired arbitrage trade, denoted informally by

We now turn to identify potential arbitrage opportunities by checking a list of paired trades against condition (1) with the focus on single-name CDS contracts traded between January of 2007 and June of 2010, which includes the official beginning and end of the 2007-09 crisis 444See National Bureau of Economic Research: http://www.nber.org/cycles.html for a definition of US economic cycles. For this study, we have sourced CDS data from Bloomberg™and Thomson Reuters.

Our data sample is comprehensive in that it contains over 3 million CDS curves, each with 8 CDS contracts of different maturities (i.e., 6-month, 1-year, 2-year, 3-year, 4-year, 5-year, 7-year and 10-year) traded over 868 consecutive trading dates555We avoid data manipulations such as term interpolations to ensure that our data truly reflect the CDS market.. From these CDS trade data, we then identify a list of paired CDS trades that violate condition (1) with focus on the following four paired maturities: , , , , where maturities are measured in years. We therefore note that our analysis in terms of paired maturities is not exhaustive.

Table 1 presents a summary of the number of anomalies (indicated below in brackets) based on the following five attributes: (i) across three major regions, i.e., Asia (42), Europe (295) and North America (2,079); (ii) across sector groups, i.e., Banking (187) and Non-banking (2,229); (iii) across three major currencies, i.e., USD (1,836) and EUR (579) and GBP(1); (iv) across rating class groups, i.e., Investment-grade (1,863), Non-investment grade or NIG (180) and Not Rated (373); (v) across seniority types for the debt obligation underlying a CDS trade, i.e., Senior (2,385), Senior Secured (12) and Subordinated (19). We note that

-

•

As regards regions, the North American region has higher percentage (86%) of anomalies than others. We believe this is mainly due to two reasons: in our CDS data sample, 64% of CDS trades have their underlying entities operating in this region; furthermore, the sample period of our CDS data includes the on-going financial crisis that affected the North American region more than the others regions, which may have contributed to the observed higher proportion of anomalies for the region.

-

•

Regarding sector groups, the 2,229 anomalies in the Non-banking sector corresponds to 92.3% of the total number of anomalies.

-

•

As for rating groups, 1,863 or 77.1% anomalies are associated with Investment-grade debt, leaving the remaining non-negligible number of anomalies associated with either Non-investment-grade or Not-rated debt. For reasons which are further discussed in section 4, non-negligible numbers of anomalies are associated with either AAA-rated (36) or AA-rated (222) names.

-

•

With regard to seniority, almost all anomalies are associated with either senior or senior secured debt, suggesting debt seniority type (junior versus senior) may not be a determining factor explaining the existence of anomalies in our sample.

![[Uncaptioned image]](/html/1811.08038/assets/Arb.png)

To sum up, we have presented a cross-sectional overview of CDS-term-structure arbitrage opportunities identified in this study; in section 4, we present further evidences of such anomalies across time and discuss the implications.

1.2 Research Gaps and Contributions

Before we move to the next section, we present a summary of the research gaps which motivated our study and list the contributions we believe this study makes to literature.

Research gaps

We identified the following research gaps in existing literature:

-

1.

The existing literature valuation adjustment literature assumes that the CDS market, which is the basis for the calibration of counterparty default probabilities, is arbitrage-free. Given the importance of valuation adjustment calculation for OTC derivatives, it is important to investigate whether the CDS market is truly arbitrage-free; if not, it is important to understand how significant the arbitrage opportunities are, how persistent such opportunities are, why would-be arbitrageurs are not taking advantage of them and what the implications are for OTC derivatives pricing and risk management.

-

2.

Past CDS-arbitrage related literature focused on either CDS-bond arbitrage or CDS-equity arbitrage. No systematic study has been conducted to identify and explain CDS-term-structure arbitrage except for a recent paper by Jarrow et al (2018, [19]), where, however, the authors focused on statistical arbitrage using a model-dependent approach.

-

3.

Although O’Kane [21] (2008) and Brigo and Mercurio [8] (2006) commented on the potential occurrence of negative hazard rates in the calibration of default probabilities to CDS curves, no systematic study of arbitrage opportunities in the CDS term structure and of its implications for the pricing and risk management of OTC derivatives has been conducted to date. For example, there does not seem to exist a basically model-free mathematical criterion for a CDS curve to be arbitrage free.

Contributions

We summarize the main contributions of our paper:

-

1.

The paper represents the first systematic study of CDS-term-structure arbitrage on the basis of a simple model-independent criterion for No-arbitrage, supported by empirical evidence and numerical examples based on real data.

-

2.

The No-arbitrage conditions we derive are basically model-independent, assuming at most the existence of an equivalent martingale measure, and sometimes not even that.

-

3.

It shows that violating these conditions can lead to either negative or greater-than-1 conditional default probabilities, which has implications for the pricing and risk management of both credit derivatives and OTC derivatives in general, through the computation of value adjustments such as CVA and DVA.

-

4.

It argues that an explanation of these apparent arbitrage opportunities can be found in the presence of implicit risks and costs which were systematically neglected in the practice of OTC-derivatives pricing prior to the crisis of 2008-9 and which have since become the focus of research efforts of academics, and practitioners through the inclusion of various valuation adjustments, and that taking these into account in the calculation of CDS spreads should reduce arbitrage opportunities in the CDS market.

The rest of the paper is organized as follows: in section 2, we derive the No-arbitrage condition (1) for a CDS term structure with zero modelling assumptions, under the assumption that risk-free rates are non-negative. We do this first (by way of example) for a simple three period model, and then for the continuous time case with both continuous and discrete protection payments.

In section 3, we use the existence of an Equivalent martingale Measure to derive a No-arbitrage condition for a general interest rate environment, with potentially negative short rates, which generalizes (1) if interest rates are positive. In section 4 we present further empirical evidence for CDS-term-structure anomalies and the existence of arbitrage profits. We present numerical examples of the implications of such anomalies for conditional default probabilities. Finally, section 5 concludes.

2 No-arbitrage conditions on CDS Term Structure

We consider a co-initial family of CDS contracts providing protection against the default of a reference entity between times and for arbitrary The default protection seller pays the buyer the Loss-Given-Default should the default occur within in exchange for either a continuously or discretely paid spread of , which is fixed at the inception of the contract and paid by the buyer up till time-of-default or up till the contract’s maturity , whichever is smaller. Here is the time at which the spread is agreed upon between the two parties of the CDS. We are interested in potential static arbitrage opportunities presented by the CDS term structure or CDS curve at any fixed time , which, without loss of generality, we can take to be (corresponding to ”today” or ”now”). Dynamic No-arbitrage conditions for the stochastic evolution of these curves as function of are outside of the scope of the present paper.

2.1 No-arbitrage condition for discretely paid CDS rates: a simple example

We first look at a simple discrete time model, with times and To further simplify, we assume that interest rates are 0 (this will be relaxed in the next section). Suppose that the defaultable bond underlying the CDS contract is a 0-coupon bond with maturity and nominal value 1, and that the reference entity has a strictly positive risk-neutral probability of default before maturity. We assume of course that the entity has not yet defaulted at the trade date of the contract: Consider two CDS contracts, and , both starting at time (the Effective Date of the CDS) with providing protection against default at for a spread of , and the second contract, , providing protection against default at times and for a spread of The spreads are agreed upon at time 0, and therefore known. Let be the, possibly random, recovery-upon-default at the time-of-default, which we assume to be strictly positive.

Suppose that , corresponding to an inverted CDS curve with short-term protection being more expensive than long-term one, and that we short the first CDS, in the sense that we sell protection against default at time for a fee of payable666We follow the convention that protection payments for a given period are done at the end of the period. at , and go long the second one, so that we are buying default protection against a fee of payable at and , assuming no default has yet occurred at the payment times. Our initial investment at time 0 (initial net cashflow) is 0, since the contracts have not started yet. If , both contracts are cancelled on their Effective Date. If , we receive at time 2. If default happens at time 2, the payments-upon-default of the two CDS contracts cancel out, while if we have to pay at If , we receive from the protection seller of the second contract. These are all the possibilities for . Assuming we carry along all received payments in a savings account, our net accumulated cash-flow at time 3 then equals

Hence we have an arbitrage opportunity if

| (2) |

assuming that (if not, then there will always be an arbitrage if ). Note that, in fact, the net value of the position is non-negative at all intermediary times.

Remark 1.

If the CDS spread curve is not inverted, , then by shorting the CDS with the higher spread and going long the other CDS, the net amount we will have received at time 3 is : the situation is different from the previous case of inverted spreads, since now occurs with a minus sign.

It is instructive to examine the above example from the viewpoint of risk-neutral pricing. Let be an equivalent martingale measure and suppose that the conditional risk-neutral probabilities of default over each period are constant:

while Furthermore, assume that the loss-given-defaults at are constant; if the reference entity for the CDS is a zero-coupon bond of face value 1, then We will see that if (2) holds, then either has to be negative or strictly bigger than 1. The fair value at time 0 of the first spread is determined by

since and, similarly,

The equation for the fair value of the second spread is

or , so that

Observe that if , then , and condition (2) would imply that , or , and our risk-neutral pricing model for pricing the CDS would break down.

More generally, letting , we find that

and the condition that forces to be either strictly smaller than 0 or bigger than 1. (If , then the second factor of the product on the right has to be strictly negative, which forces , while if , has to be negative because of the first factor; note that since and are.)

Another way of deriving that Absence of Arbitrage implies that is by observing that the risk-neutral expectation at time 0 of the pay-off of the difference of the two CDS contracts (”short , long ”) is

Since this has to be 0, and since the last term is positive, it follows that

or

| (3) |

which certainly implies that , since Note that (3) is sharper than but that the latter makes no reference to survival probabilities. Inequality (3) would be useful when we would have access to survival probabilities from another source than the CDSs themselves, e.g. from defaultable bond yields.

2.2 No-arbitrage conditions for continuously paid CDS rates

We now put ourselves in a continuous-time framework, and consider a family of co-initial forward CDS contracts providing default-protection over a future time periods , with fixed and arbitrary. We let be the time of default. The party which is long the CDS (the buyer of the default protection) will pay a protection fee between and up till default of the reference entity, in which case he will receive the Loss-given-default (LGD). We will consider both the case of a protection fee which is paid out continuously and one which is paid discretely, at payment dates

In the first case the protection buyer pays a continuous fee at a rate of up till time-of-default, and in the second case he pays at time for , with if , while he only pays the spread over if default occurs between (excluded) and (included). Here the CDS spread is determined at time 0 so that if it is in fact a forward spread.

Let be the loss-given-default or LGD process, with the LGD if default happens at In some of our results below is allowed to be stochastic, in which case we will if necessary assume it is adapted to the relevant filtrations generated by background processes such as the interest rate process. We assume that, for all , is non-negative, and strictly positive with a non-zero probability: , where the expectation can be taken with respect to the objective probability measure, or an equivalent risk-neutral probability, if one exists. We will sometimes limit ourselves to LGDs which are known in advance, though possibly time-dependent, in which case we will write instead of Finally, we let be the risk-free short-rate process.

Our first result generalizes the absence-of-arbitrage condition of the previous section to the continuous-time setting, under condition of non-negative short-rates.

Theorem 1.

Suppose that the risk-free short rate a.s. and that with positive (objective) probability. If there is no arbitrage in the CDS market, and if the protection fee is paid out continuously, then is a strictly increasing function of :

| (4) |

The same inequality holds with discretely paid protection fees, provided the protection-payment dates of the two CDS contracts between and coincide.

Proof. Recall that an arbitrage opportunity over the time-horizon is a process representing a dynamic self-financing portfolio strategy which is bounded from below and has initial cost , while at , a.s. and with strictly positive probability. Suppose now that (4) is not satisfied for some :

| (5) |

where we have written and , to simplify notations. Then, necessarily, We set up a portfolio strategy at time 0 by shorting the CDS for and going long the one for , and investing any cash earned into a savings account (as usual interpreted as borrowing if the amount is negative). This strategy costs 0 to set up. We verify that its value at is non-negative with positive expectation.

(i) Continuous protection payments. If default happens before or at , both contracts are cancelled, and we receive nothing. If default happens before or at , the default payments of the two CDS contracts will cancel out, and the value of our position at will be

where

is the savings account. If default occurs between (excluded) and (included), we receive

assuming (5), where we used that the risk-free rate is non-negative for the third line, so that if and if Finally, if , we receive the next to last line minus the LGD-term, which again is a non-negative amount. Since default will occur in with a positive probability, our gain at is non-negative and strictly positive with a positive probability, and since the value of our position is clearly bounded from below at intermediary times (it is in fact non-negative at all times by essentially the same arguments), we have an arbitrage opportunity. Note that our strategy is in fact a static one.

(ii) Discrete protection payments. Let be the payment dates for the CDS contract over , which is augmented by payment dates for the CDS over If default has not yet happened at , then the protection fee for the sub-period is payed at If is the CDS-spread, his protection fee equals to if default has not yet occurred before , or if default occurred after but before or at This can be summarized by the formula

where With this notation, the value of our strategy at is

This value is clearly positive if , since , while if , it is bounded from below by

where we used that if and otherwise. We therefore have an arbitrage if inequality (4) is violated.

Remark 2.

The theorem remains valid if, in the discrete case, protection payments are made at the time of default instead of at the end of the protection period in which default falls: this simply amounts to replacing by in the proof above, which can be bounded from above or below as before.

Also, we can slightly weaken our assumption on the payment dates of the two CDS contracts, by supposing that the first contract has a set of payment dates which contain the payment dates of the second contract with spread for that period, while is a payment date for the second contract.

Indeed, suppose that and that If no default occurs between and , then the value at of our net protection payment for the period is

while if the time of default falls within this period, a similar analysis shows that this net value is bounded from below by

Arguing as before, we find that we have an arbitrage opportunity if (4) does not hold.

3 Absence-of-Arbitrage conditions between CDS-rates and non-defaultable bond prices

The proof of Theorem 1 above is completely elementary. We will now give a second proof which uses the fundamental theorem of asset pricing, and which will also allow us to generalize this theorem to the case where the risk-free rate can become negative. We will do so under a stronger assumption than Absence-of-Arbitrage, namely the existence of an equivalent martingale measure (or risk-neutral pricing measure) with respect to which the time-of-default and the risk-free short-rate process are independent. In other words, we assume a reduced-form credit risk model. An equivalent martingale measure exists assuming a suitably strengthened form of Absence-of-Arbitrage, such as Delbaen and Schachermayer’s NFLVR condition (1994, [15]). We will moreover assume, for a start that the protection is paid out continuously, at a rate of , and make some remarks on the case of discrete protection payments at the end of this section.

Denoting the risk-neutral survival probability by777In a dynamic setting the spread as determined at would be written as and the correct survival probabilities to use would be the conditional one,

| (6) |

the fair CDS spread at time 0 can these assumptions be expressed as

| (7) |

where is the price at time 0 of a non-defaultable 0-coupon bond maturing at

Remark 3.

If is deterministic, the numerator equals

| (8) |

This formula will still hold, with if the LGD process is also independent of , For actual LGDs, such as those turning up in CVA calculations, the LGD is related to the present value, at time-of-default, of future discounted cash-flows, and would therefore in general depend on the short-rate process. If the CDS-contract sets the LGD is as a fixed fraction of a given nominal, it is clearly constant.

To obtain a variant of Theorem 1 which holds if risk-free rates can be negative, it now suffices to replace by what we will call the standardized (continuous-time) risk-free annuity over , defined as888An annuity would pay a constant interest of over a period ; if , its present value at is given by (9).

| (9) |

Theorem 2.

Assume an equivalent martingale measure exists for the CDS market with respect to which and are independent. Then is an increasing function of

Proof. Writing and for and , and also introduce

which is what we might call a defaultable standardized annuity. Then clearly

is increasing in , since is, so it suffices to show that is increasing. But

since is decreasing, and therefore

Remark 4.

Theorem 2 implies Theorem 1 (modulo the stronger independence assumptions of the former), since

is an increasing function of if the short-rate is non-negative a.s., since is then decreasing in : this can be shown similarly by verifying that the derivative of the logarithm is non-negative. Note that in this case, the conclusion of Theorem 2 is stronger than the one of Theorem 1 (see also the graphical interpretation of these Absence-of-Arbitrage relations below). An advantage however of (4) is that it is formulated purely in terms of the CDS spreads, without reference to the risk-free yield curve.

3.1 A No-Arbitrage relation between CDS and IRS rates

We can reformulate Theorem 2 as a no-arbitrage relation in terms (continuously paid) Interest Rate Swaps (IRS) rates. Recall that the fair (forward) rate for a continuously exchanged fixed-for-floating IRS over is given by

| (10) |

with , the -forward rate at time 0, where we used (10).

Theorem 2 then implies that is an increasing function of Equivalently, if we introduce the -forward price , then we have the

Corollary 1.

One can go one step further, and express in terms of the IRS-forward rates: see Appendix A. This however involves a double integration of IRS-rates with respect to their maturity variables, and the corollary suffices in practice, since we can observe forward bond-prices along with forward IRS rates.

3.2 Graphical interpretation of the No-Arbitrage relations

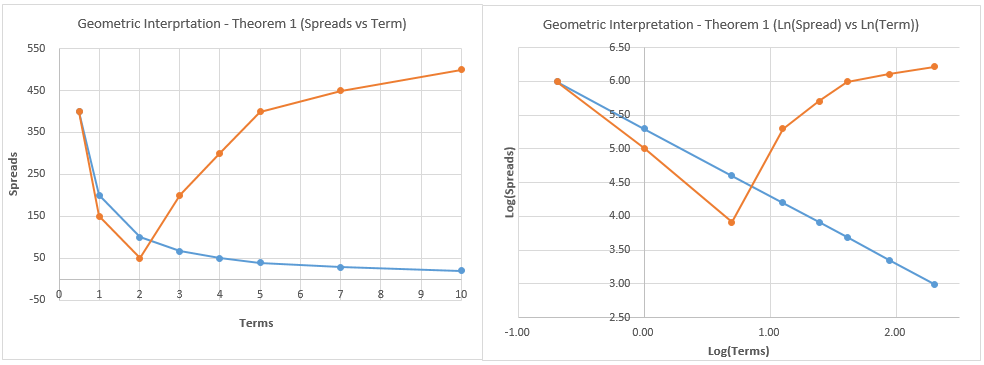

The No-arbitrage condition of Theorem 1 has a simple graphical interpretation: suppose we have a collection of observed rates and that we plot the points against in the -plane. Take a point and draw the hyperbola which passes through this point (so that ). Then all points for which should lie above this hyperbola, if not, there is an opportunity for arbitrage.

In Figure 1, a CDS curve highlighted in orange color is plotted against a hyperbola going through the where and basis points. Clearly, together with , any points located below the hyperbola can form a paired trade to construct arbitrage opportunity as in the proof of Theorem 1, which makes it easy to detect such arbitrage opportunities at a glance.

Alternatively, one can do a log-log plot: against , in which case the points for which should lie above the straight line with slope -1 which passes through The right panel of Figure 1 illustrates the graphical interpretation for Theorem 1 in log-log scale.

A similar construction applies for Theorem 2: it suffices to plot against respectively against

3.3 Discrete protection payments

In practice, the protection leg of a CDS is paid discretely instead of continuously. If we consider families of co-initial CDS-contracts with maturities and protection payment dates coming from a discrete set of tenor-dates , then the protection buyer of a CDS contract whose maturity is pays at dates for : if default hasn’t occurred yet, and if One can repeat the analysis to arrive at the following result:

let

be the discrete-time standardized annuity, and let be the fair CDS spread. Then

Theorem 3.

If an equivalent martingale measure exists and if is independent of the risk-free interest rate process, then is an increasing function of

Proof. The fair spread now equals

where

and it again suffices to verify that is increasing in Now an easy computation shows that , where

It follows that is decreasing in , since

and therefore

Now

and each term in the sum in the numerator is positive since for

One checks by a similar computation that if interest rates are non-negative, and therefore is decreasing in , then divided by the numerator is increasing in , so that we find as in section 2 that is increasing.

4 Further Empirical Evidence

Economists often cite inverted yield curves as signals for a pending economic crisis. However, inversions for CDS-curves does seem not to have been systematically investigated in the literature. In this section we present some further evidence for CDS anomalies summarized across the sample period of our CDS data. We consider the implications of such anomalies for conditional default probabilities.

4.1 CDS-term-structure anomalies across time

In section 1.1, we presented a cross-sectional overview of the CDS-term-structure arbitrages (or anomalies) which fail the No-arbitrage condition of Theorem 1.

We now take a further look at these anomalies across the same sample period using the same CDS data set, where we consider contracts with , that is, starting on the day they are quoted. It is convenient to introduce the Maturity Adjusted Spread Ratio or MAR, defined as

so that Theorem 1 there is arbitrage for the pair of traded if Equivalently, there is arbitrage if the slope is bigger than or equal to the maturity ratio The MAR is a metric for the strength of such an arbitrage opportunity.

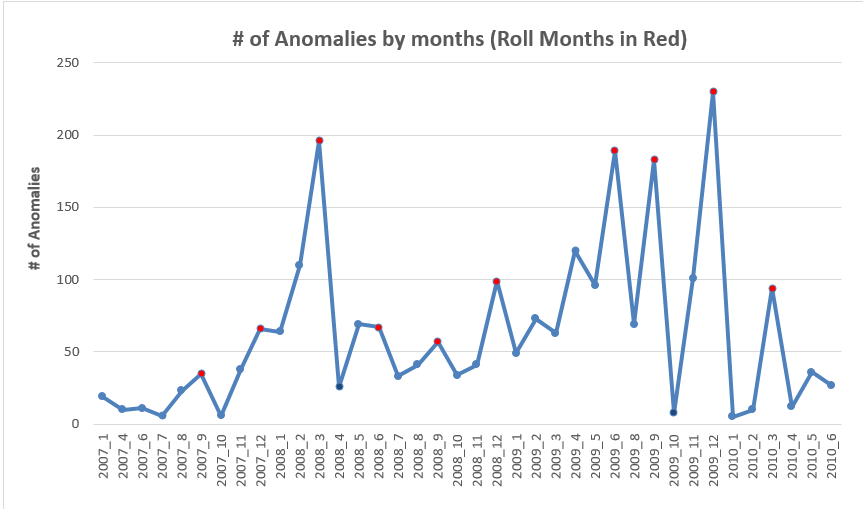

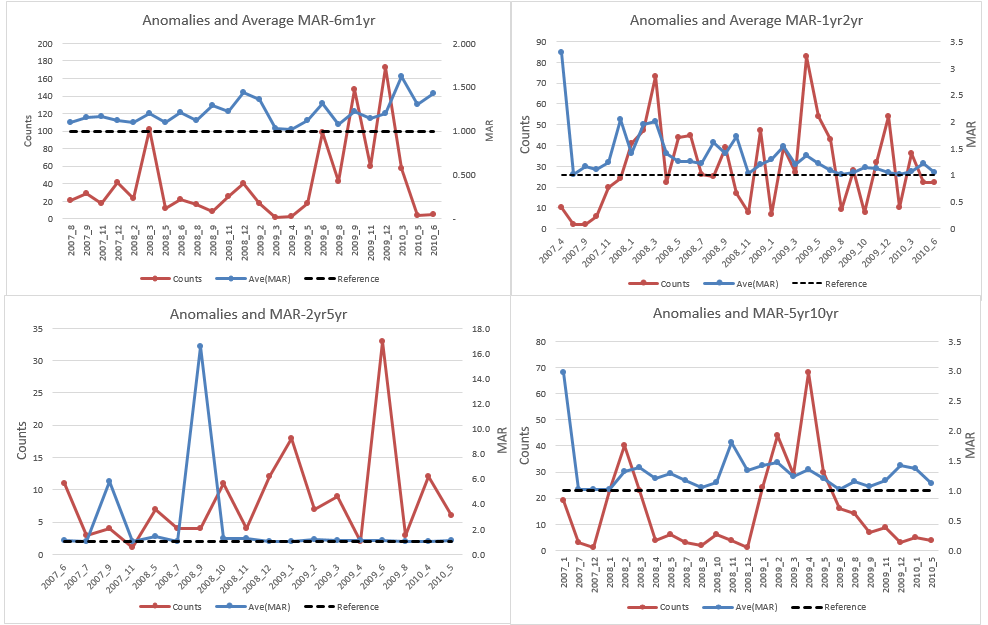

Figure 2 graphs the total number of anomalies per month or Anomaly Counts in our dataset. Figure 3 graphs these in red for each of the four maturity pairs we examined, together with the MARs in blue to indicate the strength for arbitrage opportunities based on each maturity pair.

On the basis of these two figures and on Figure 4 and Table 2, we can make the following observations:

-

1.

We can distinguish three different phases in the anomalies count of Figure 2 which correspond with three phases of the credit crunch: (i) a build-up phase, from July/August-2007 (when BNP Paribas terminated investors’ withdrawal from three of the hedge funds it administered, often considered as the start of the crisis) to March-2008 (when US investment bank Bear Stern collapsed), coinciding with the initial phase of the financial crisis; (ii) a liquidity dry-up phase, from April-2008 to May-2009, during which the number of anomalies decreased while the market was hit by the liquidity crunch; (iii) a post-crisis liquidity recovery and market uncertainty phase, from June-2009 (the official ending of the crisis) onwards during which, as funding and market liquidity recovered, the number of anomalies increased as the market searched for directions amongst ongoing uncertainty, in part related to regulatory reforms hanging over the financial markets. According to Battalio and Schultz (2011, [3]), regulatory confusion and uncertainty created significant bid-ask spreads in the equity option market, and the CDS market was not immune from this either.

Figure 2: The number of Anomalies across time

-

2.

Figure 2 shows that 8 out of the 12 peak-months (highlighted in Red) coincide with the ”Roll Months”, which are the months containing so-called Roll Dates999Our CDS contracts are of 1999/2003 ISDA formats; Roll Dates refer to the 20th of March, June, September and December when less liquid off-the-run CDS contracts expire and more liquid on-the-run ones are traded.. During the Roll Months, the increased number of anomalies can at least partly be attributed to an increased number of expiring and lack of liquid CDS contracts before the Roll Dates.

Figure 3: Anomaly Counts and Arbitrage Opportunity Strengths for Four Strategies

-

3.

Across the four different arbitrage strategies of Figure 3, the ’6m-1yr’ maturity pair had the highest number of arbitrages, 987, closely followed by 975 for the ’1yr-2yr’ pair. For the ’2yr-5yr’ pair we found 151 arbitrage opportunities and for the ’5yr-10yr’ pair, 388. In our data set, CDS-curve arbitrage opportunities occurred most frequently at the short-end of the curve and less frequently for the longer maturity contracts, and the least for 5-year term contracts which are the most liquidly traded. These observations are consistent with an economic principle: when a name gets stressed, its CDS curve often gets inverted at the short-end (such as the 6-month maturity) of the curve and tends to go back to be normally upward-sloping after that. This is because investors tend to believe that if a stressed name survives in the short-term, it will bounce back over longer terms.

-

4.

Figure 3 also depicts the MARs in contrast with the reference line ( indicated by a dark dotted line); as explained above, the greater the (monthly average) MAR number exceeds the reference line, the stronger or the more arbitrage-able the arbitrage opportunity can be. Also, MARs tend to be less volatile than the anomaly counts, except for some outliers. For example, the spike of 16.53 in the MARs shown in Table 2 for the ’2yr-5yr’ couple is caused by Freddie Mac (a US home insurance company) because its 2-year CDS spread went up to 1538 basis points after Lehman Brother’s bankruptcy while its other spreads stayed normal during the month of Sept-2008, as the market expected Freddie Mac to survive after the short-run stress. (The market turned out to be correct: Freddie Mac survived after receiving a governmental bailout.)

-

5.

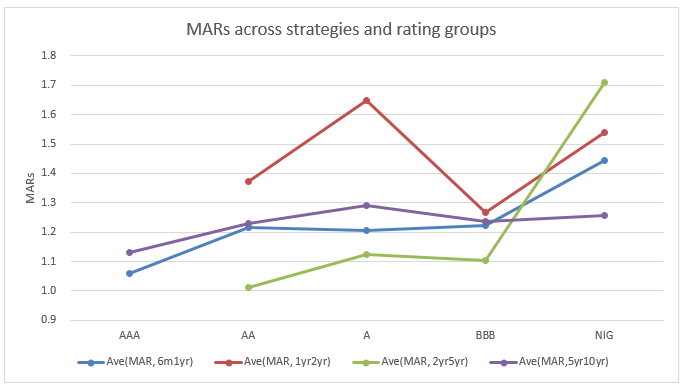

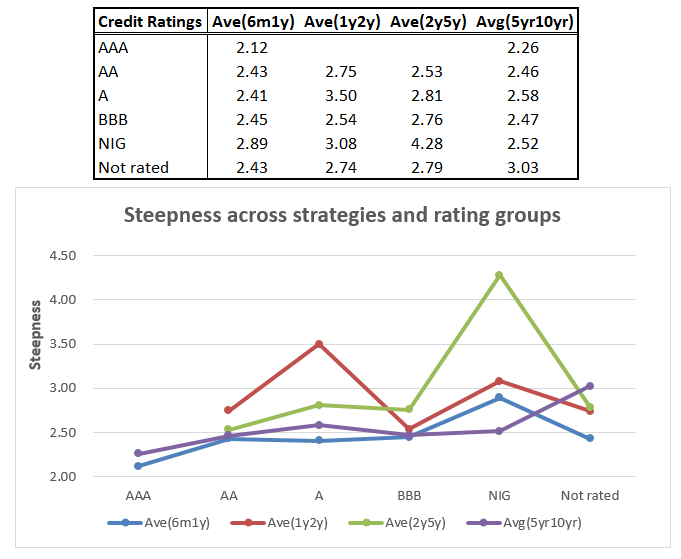

In Table 2, we present the average MAR of the anomalies for the four maturity pairs split out by rating class. We excluded one anomalous trade related to Freddie Mac as an outlier from the ’1yr-2yr’ and ’2yr-5yr’ pairs because it was rated AAA even as it received the US government’s bailout. Figure 4 and Table 2 show that the MAR tends to increase when we go from higher credit-quality ratings groups (AAA) to lower ones ( BBB or Non-investment-Grade rated group (or NIG, ratings lower than), with the exception of the A-rated group for all four strategies. This may be related to an observation of Biswas, Nikolova and Stahel (2015, [4]), who found that CDS contracts on lower rated entities commanded a higher liquidity premium. Such liquidity premia would disincentivise would-be arbitrageurs to take advance of these arbitrage opportunities since it would make it costly to close out the arbitrage strategy prematurely should they wish to do so, explaining why such opportunities are tolerated by the market.

Table 2: Arbitrageability/MARs across strategies and rating groups: numerical results ![[Uncaptioned image]](/html/1811.08038/assets/tblAvgSteepnessAcrossStrategyandRating.png)

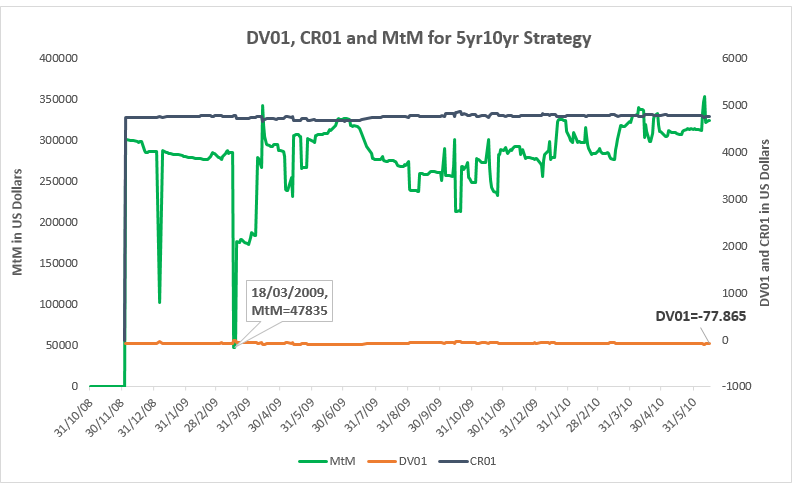

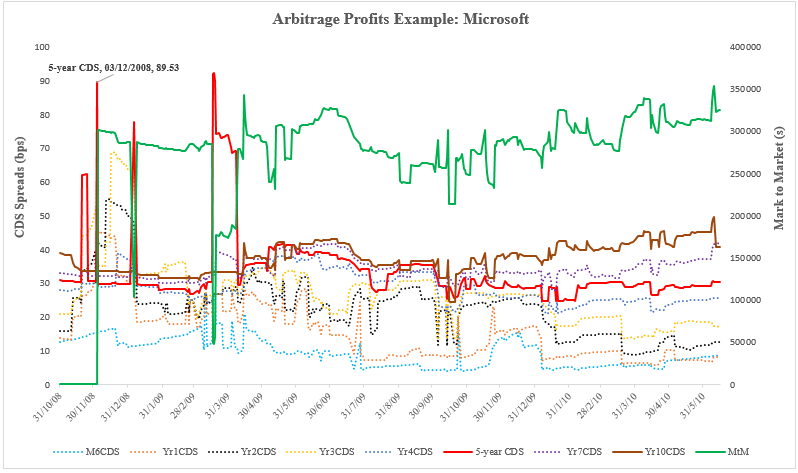

4.2 Numerical example of arbitrage profits across time: Microsoft 5yr-10yr strategy

If two CDS contracts of different maturities, e.g., the 5-year and 10-year, are quoted on the market with spreads which violate the No-arbitrage condition of Theorem (1), we can construct an arbitrage strategy by selling the 5-year default protection and at the same time buying the 10-year default protection. Observing the market quotes for Microsoft on 03/12/2008, we form such a strategy and calculate the Mark-to-Market value for two CDS contracts with notional amounts of 10 Million dollar each. Figure 5 presents the computed Mark-to-Market values (graphed in Green from the right -axis) from ISDA’s standard CDS model101010based on a reduced form model for standard CDS as the one we use in Section 3; see for example O’Kane, 2008, http://www.cdsmodel.com/cdsmodel/ of the resulting strategy using CDS market data from 03/12/2008 to 30/06/2010. We assume zero interest for the observation period, given that interest rates were extremely low then. Besides, as shown in Appendix B, interest rate levels only have a limited impact on CDS valuation.

At the inception of the strategy, the 5-year mid-CDS rate on 03/12/2008 is 89.53 basis points while the 10-year one is 33.55 basis points, The Mark-to-Market value is zero on 03/12/2008, but raises to a strictly positive value immediately afterwards, and consistently stays positive throughout the observation period.

Besides the Mark-to-Market value of our arbitrage strategy, Figure 5 also plots CDS rates (right -axis) for protection on Microsoft for eight different maturities, for each date between 31/10/2008 to 30/06/2010. The CDS rates for the 5-year and 10-year maturities are represented by solid lines in red and brown and the other terms by dotted lines. Other spikes, where the 5-year CDS rate (in red) overshoots the 10-year rate (brown) can be observed later in the period. The 5-year rate is more volatile than the 10-year one, which is probably related to its greater liquidity. In particular, this indicates that arbitrage opportunities like these are not one-offish, instead, they can be recurrent.

4.3 Implications of Arbitrage: Nonsensical Default Probabilities

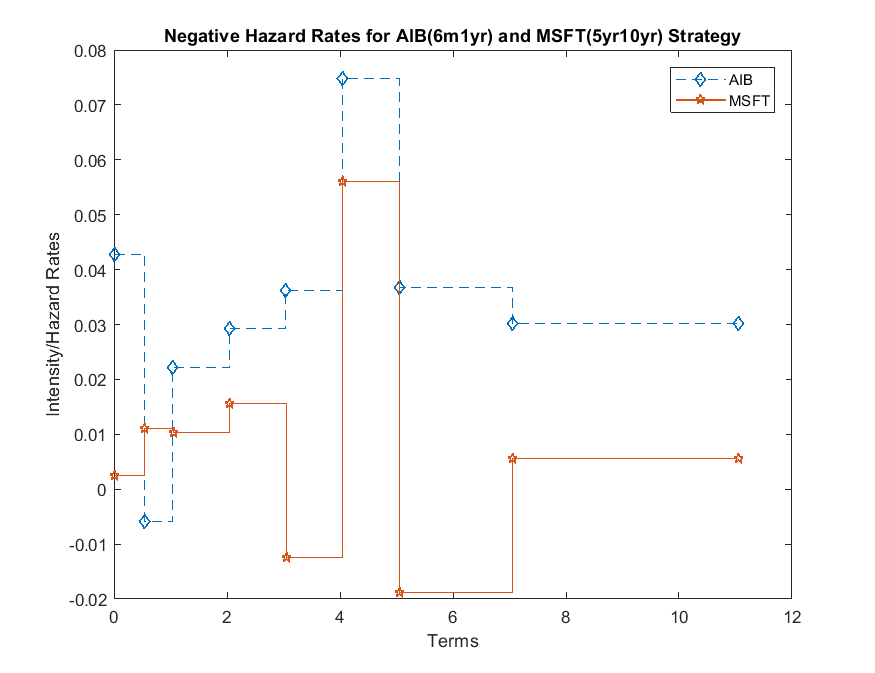

As we already noted in section 2, Remark 1, violation of the No-arbitrage condition of theorem 1 can lead to nonsensical conditional default probabilities as computed in a standard reduced-form model. Observing that the CDS term structures for AIB on 04/12/2008 and Microsoft on 03/12/2008 respectively do violate this the No-arbitrage condition look at the implications for each entity’s the conditional default probabilities, using a standard reduced-form model: the ISDA standard CDS model. This model bootstraps piecewise constant conditional default probabilities or hazard rates from a given CDS curve. Table 3 shows that the bootstrapped hazard rates for 4-year and 7-year terms for Microsoft are negative; also, the bootstrapped 1-year hazard rate for AIB is negative (highlighted in red colors). In both cases, this violates the elementary definition of a probability. Figure 7 depicts the same numerical results in a graph.

![[Uncaptioned image]](/html/1811.08038/assets/AIBMSFTNegativeHazardRatesNumbers.png)

4.4 CDS Term Structure and Credit Valuation Adjustment

We discuss the relation between CDS term structure arbitrage opportunities and CVA. In one direction, the risk-neutral hazard rates and default probabilities which are used for the computation of the CVA of a given OTC derivative contract are backed out from observed CDS curves. If these curves present arbitrages in the sense of our theorems 1-3, these hazard rates can become negative, which will result in an over-valuation of the CVA. Since CVAs are not traded, there are not likely to be other consequences.

In the other direction, CVA costs can provide an explanation for why these arbitrage oportunities are not exploited. Indeed, the would-be arbitrageur faces two kinds of counterparty credit risks: that of the protection buyer of the smaller maturity CDS contract not paying all of his protection fees between and and that of the protection seller not paying the loss-given-default, in particular for default occuring before , when this payment should compensate the loss-given-default payment the arbitrageur himself should make. In other words, the CVA of the arbitrage strategy will make its initial value negative instead of 0. Unaccounted counterparty credit risks to be borne by a would-be arbitrageur can thus help to explain the existence of the significant and persistent amount of CDS-term-structure arbitrage in our study. We note in this respect that Brigo and Capponi (2014, [7]) show in an example that the impact of CVA on the Mark-to-Market value of a 5-year single-name CDS payer contract can vary up to 60 basis points, depending on the default correlation between the two parties.

In addition, other types of valuation adjustments can also explain the arbitrage opportunities observed in our study in form of implicit costs and risks. For example, the counterparty credit risk run by the arbitrageur may be alleviated through the posting of collateral (e.g. in a context of centrally cleared contracts) but the arbitrageur himself would then have to post collateral also, which then corresponds to a non-zero initial investment. Furthermore, liquidity risks might prevent the arbitrageur to prematurely close-out his position. Biswas (2015, [4]) studied the liquidity risk component in a real-world setting, as measured by the bid-ask spread for CDS contracts, based on mainly post-crisis CDS market data. They found that the liquidity risk premiums for CDS contracts are between 12 and 14 basis points depending on whether the contracts are between a dealer and another dealer or between dealer and a buy-side investor. they also found that an entity with lower credit rating has to pay higher liquidity premiums. Since we use data from the time period leading to and during the financial crisis, we expect the liquidity premiums for our mainly dealer and buy-side investors (or end-users) trades to be higher than these numbers.

5 Conclusions & Research Directions

We derived criteria for absence of arbitrage in CDS term structures, under various assumptions (discrete or continuous protection payments, interest rate environments which are positive or not) with no or only minimal modelling assumptions. These criteria provide simple checks for arbitrage opportunities in the CDS market. Based on these criteria and using a comprehensive data set, we found that a significant amount of CDS-term-structure arbitrage opportunities existed in the CDS market prior and during the financial crises.

Violation of the no-arbitrage conditions implies nonsensical conditional default probabilities which will impact on the calculation of CVA and DVA. The existence of such arbitrage opportunities is likely to be connected with hidden risks (counterparty credit risk, liquidity risk) and costs (collateral) which prevents them to be exploited, and which prior to the 2007-09 crises were not systematically taken into account in the pricing of OTC derivatives.

The progress being made in the theory and practice of the valuation adjustment should contribute to the gradual disappearance of these arbitrage opportunities, as should the increase in efficiency and transparency due to the standardisation of OTC derivative contracts and the use of modern information technology. Furthermore, central clearing should contribute to greater liquidity. The existence of arbitrage opportunities should therefore not discourage the financial community from continuing to use the CDS market for the calibration of counterparty default risks.

As possible directions for future research we mention the expansion of our study to maturity pairs other than the four we considered here, and other data sets. We also believe that our analysis can be extended to cover sovereign CDS while accounting for the exchange rate between the protection and premium legs in context of the so-called Quanto CDS; no study has been done on the term-structure arbitrage of such contracts. On a theoretical level, it would be interesting to characterise arbitrage-free CDS term structures: we mention here that one can construct examples of CDS curves which satisfy the criteria of theorems 1 and 2, but which nevertheless cannot be a CDS curve in an arbitrage-free model. This is work in progress.

References

- [1] Bai J. and Collin-Dufresne P., November 2013, ”The CDS-Bond Basis”, AFA 2013 San Diego Meetings Paper, Georgetown Univ., Dept. of Finance and Ecole Polytechnique Fédérale de Lausanne

- [2] Banks for Int’l Settlements, July 2017, Statistical release: OTC derivatives statistics at end June 2017.

- [3] Battalio, R. and Schultz P., 2011, ”Regulatory Uncertainty and Market Liquidity: The 2008 Short Sale Ban’s Impact on Equity Option Markets”, Journal of Finance, Vol66

- [4] Biswas G., Nikolova S. and Stahel C., 2015, ”The Transaction Costs of Trading Corporate Credit”, SSRN.

- [5] Bjork, T., 2004, Arbitrage Theory in Continuous Time, Oxford Univ. Press.

- [6] Brigo, D., Morini M. and Pallavicini A., 2013, Counterparty Credit Risk, Collateral and Funding: With Pricing Cases for All Asset Classes, John Wiley and Sons Ltd.

- [7] Brigo, D., Capponi A., Pallavicini A., 2014, ”Arbitrage-free Bilateral Counterparty risk valuation under collateralization and application to credit default swaps”, Mathematical Finance, Vol:24.

- [8] Brigo, D., and Mercurio F., Interest Rate Models Theory and Practice, with Smile, Inflation and Credit, 2nd Edition, Springer-Verlag, Page 775.

- [9] Brigo, D., Francischello, M., and Pallavicini, A., November 2015, ”Invariance, existence and uniqueness of solutions of nonlinear valuation PDEs and FBSDEs inclusive of credit risk, collateral and funding costs”, https://arxiv.org/abs/1506.00686.

- [10] Brummelhuis, R. and Z. Luo. 2018a. ”CDS Proxy Construction via Machine Learning Techniques: Methodology and Results”. forthcoming, Journal of Financial Data Science.

- [11] Brummelhuis, R. and Z. Luo. 2018b. ”CDS Proxy Construction via Machine Learning Techniques: Parametrization, Correlation and Benchmarking”. forthcoming, Journal of Financial Data Science.

- [12] Brummelhuis, R. and Z. Luo. 2017. ”CDS Rate Construction Methods by Machine Learning Techniques”. SSRN Journals. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2967184.

- [13] Burgard, C. and Kjaer, M., 2011, ”Partial differential equation representations of derivatives with bilateral counterparty risk and funding costs”. The Journal of Credit Risk 7(3), 75–93.

- [14] Crepey, S., Gerboud, R., Grbac, Z., and Ngor, N., 2013, ”Counterparty risk and funding: The four wings of TVA”. Int’l Journal of Theoretical & Applied Finance 16, 1350006.

- [15] Delbaen, F. and Schaechermayer, W., 1994, ”A General Version of the Fundamental Theorem on Asset Pricing”. Mathematishe Annalen 300, 463-520

- [16] Delbaen, F. and W. Schachermayer, 2006, The Mathematics of Arbitrage. Springer Finance, xvi+371 p., ISBN 3-540-21992-7 (2006).

- [17] Green, A., Kenyon C. and Dennis C., 2014, ”KVA: Capital Valuation Adjustment”, Risk, 27.12.

- [18] Green, A. and C. Kenyon. 2015. ”MVA: Initial Margin Valuation Adjustment by Replication and Regression”. Risk 28(5).

- [19] Jarrow R., Li H, Ye X. and Hu M., 2018, ”Exploring Mispricing in the Term Structure of CDS Spreads”, forthcoming, Review of Finance, rfy014, https://doi.org/10.1093/rof/rfy014

- [20] Kapadia N. and Pu X., 2012, ”Limited arbitrage between equity and credit markets”, Journal of Financial Economics 105 (2012) 542564

- [21] O’Kane, D., 2008, Modelling single-name and multi-name Credit Derivatives, John Wiley & Sons Ltd.

Appendix A Forward bond-prices and IRS rates

Proposition 1.

For let

| (12) |

Then

| (13) |

In particular, the forward IRS curve uniquely determines the forward bond prices.

Corollary 2.

If there is no arbitrage in the combined CDS - IRS market then (assuming the existence of an equivalent martingale measure)

| (14) |

is an increasing function on

Proofs. The corollary follows by inserting (13) into (11). The proof of (13) we set up and solve an ODE for the forward bond prices. We fix , and write for and for On dividing both sides of the fundamental relation (10) by , we can rewrite this as

where (which is nothing else but the forward price of ). Differentiation with respect to gives , where we used the fundamental relation again, or

This as a linear non-homogeneous ODE for for with initial condition , whose solution is given by (13).

We make some further observations:

-

1.

In a dynamic setting relations such as the ones established here hold between and/or and and put restrictions on a joint dynamic CDS-IRS model which simultaneously tries to mode the swap and CDS rates.

-

2.

If interest rates (instantaneous rates or forward rates in an HJM model) are non-negative, then forward prices are decreasing in , and consequently has to be increasing in : this puts a restriction on possible IRS forward curves at a given time 0. Similar conditions can be derived for CDS forward curves.

-

3.

In an HJM model, forward prices can be expressed in terms of instantaneous forward rates as

One can ask for a relationship between the ’s and the forward swap rates Recall that

where Differentiating this relation once more, and then using it to eliminate the -term form the resulting expression, we find a first-order Ricatti equation for the forward rate , ,

(15) with and and initial condition The solution of this Ricatti equation is of course implicitly already contained in (13), since the instantaneous forward rate is minus the logarithmic derivative of the forward: for However, in practice, one might also solve this ODE numerically.

Appendix B Risk Sensitivities for 5yr-10yr Microsoft Arbitrage Strategy

Following O’Kane (2008), we measure the Interest Rate Risk Sensitivity by so-called DV01, which measures the Mark-to-Market value denoted by changes with regard to 1 basis point parallel shift for interest rate level or . Similarly, we measure Credit spread risk sensitivity by CR01 as the Mark-to-Market value changes with regard to 1 basis point parallel shift for CDS curve; i.e. . We note that: (1) Figure 8 displays the DV01, CR01 together with MtM results for the 5yr10yr Arbitrage strategy of Microsoft described above. (2) The DV01 for this strategy is between -103 and -11 dollars throughout the data period in our sample; whereas, the CR01 for this strategy is between 4,761 and 4,870 dollars for the sample period. Clearly, CR01 or credit risk instead of DV01 or interest rate risk is the main driver for the MtM for this strategy. (3) We note that, the above observation can be generalized to all single-name CDS; i.e., interest rate sensitivity for single-name CDSs is much smaller than credit spread risk with regard to their respective rates.