Cryptoasset Factor Models

Zura Kakushadze§†111 Zura Kakushadze, Ph.D., is the President and CEO of Quantigic® Solutions LLC, and a Full Professor at Free University of Tbilisi. Email: zura@quantigic.com

§ Quantigic® Solutions LLC

1127 High Ridge Road #135, Stamford, CT 06905 222 DISCLAIMER: This address is used by the corresponding author for no purpose other than to indicate his professional affiliation as is customary in publications. In particular, the contents of this paper are not intended as an investment, legal, tax or any other such advice, and in no way represent views of Quantigic® Solutions LLC, the website www.quantigic.com or any of their other affiliates.

† Free University of Tbilisi, Business School & School of Physics

240, David Agmashenebeli Alley, Tbilisi, 0159, Georgia

(September 6, 2018)

We propose factor models for the cross-section of daily cryptoasset returns and provide source code for data downloads, computing risk factors and backtesting them out-of-sample. In “cryptoassets” we include all cryptocurrencies and a host of various other digital assets (coins and tokens) for which exchange market data is available. Based on our empirical analysis, we identify the leading factor that appears to strongly contribute into daily cryptoasset returns. Our results suggest that cross-sectional statistical arbitrage trading may be possible for cryptoassets subject to efficient executions and shorting.

1 Introduction

Crytoassets333 By “cryptoassets” here we mean digital cryptography-based assets such as cryptocurrencies (e.g., Bitcoin), as well as the plethora of various other digital “coins” and “tokens” (minable as well as non-minable) that have arisen in the recent years. For our specific purposes here, all digital assets that have data on https://coinmarketcap.com a priori are included in “cryptoassets”. have a sizable (albeit highly volatile) total market capitalization measuring in hundreds of billions of dollars. Superfluously, there is also a sizable number of these cryptoassets, edging toward 2,000 as of this writing. The question we ask – and, at least to a some degree, answer – in this note is this: Are there common (risk) factors underlying the cross-section of cryptoasset returns?

There are no evident “fundamentals” for cryptoassets based on which one could attempt to build “fundamental” long-horizon factors for cryptoassets akin to value, growth, etc., for stocks.444 For some literature on long-horizon factors for equities, see, e.g., [Amihud, 2002], [Ang et al, 2006], [Anson, 2013], [Asness, 1995], [Asness et al, 2001], [Asness, Porter and Stevens, 2000], [Banz, 1981], [Basu, 1977], [Carhart, 1997], [Fama and French, 1992], [Fama and French, 1993], [Fama and French, 1996], [Haugen, 1995], [Jegadeesh and Titman, 1993], [Lakonishok, Shleifer and Vishny, 1994], [Liew and Vassalou, 2000], [Pástor and Stambaugh, 2003], [Scholes and Williams, 1977]. However, even for stocks, on short horizons (e.g., overnight returns) in some sense things become simpler as the longer-horizon “fundamentals” (again, such as value and growth) are no longer relevant [Kakushadze and Liew, 2015]. This underlies the construction of the 4-factor model of [Kakushadze, 2015] for equity returns on short-horizons. It is therefore natural to extend the ideas set forth in [Kakushadze, 2015] to cryptoassets, to wit, to daily open-to-close returns.

And this is precisely what this note does. We consider 4(+) factors, to wit, cap (or size, based on market cap), mom (momentum), hlv (based on average intraday volatility), and vol (or liquidity, based on average daily dollar volume). By running out-of-sample Fama-MacBeth regressions [Fama and MacBeth, 1973] and computing annualized t-statistic from the time series of the corresponding regression coefficients, we conclude that vol is not a good predictor (with a possible exception of the previous day’s volume). One possible explanation is that cryptoassets on average trade much less in comparison to their market caps (low “turnover”), so vol does not actually meaningfully measure liquidity. The other three factors cap, mom and hlv do add value, with mom leading by a large margin. In fact, momentum from the day before the previous day is also predictive. The sign of the mom regression coefficient is negative, which indicates a mean-reversion effect in cryptoasset daily returns.555 To our knowledge, our analysis here is the first of its kind. For some cryptoasset investment and trading related literature, see, e.g., [Alessandretti et al, 2018], [Amjad and Shah, 2017], [Baek and Elbeck, 2014], [Bariviera et al, 2017], [Bouoiyour et al, 2016], [Bouri et al, 2017], [Brandvold et al, 2015], [Brière, Oosterlinck and Szafarz, 2015], [Cheah and Fry, 2015], [Cheung, Roca and Su, 2015], [Ciaian, Rajcaniova and Kancs, 2015], [Colianni, Rosales and Signorotti, 2015], [Donier and Bouchaud, 2015], [Dyhrberg, 2015], [Eisl, Gasser and Weinmayer, 2015], [Gajardo, Kristjanpoller and Minutolo, 2018], [Garcia and Schweitzer, 2015], [Georgoula et al, 2015], [Harvey, 2016], [Jiang and Liang, 2017], [Kim et al, 2016], [Kristoufek, 2015], [Lee, Guo and Wang, 2018], [Li et al, 2018], [Liew, Li and Budavári, 2018], [Nakano, Takahashi and Takahashi, 2018], [Ortisi, 2016], [Shah and Zhang, 2014], [Van Alstyne, 2014], [Wang and Vergne, 2017].

The remainder of this note is organized as follows. In Section 2 we describe the data, define our factors, and discuss the results of our regressions. Section 3 briefly concludes with some comments. Appendix A gives R source code for data downloads and running factor regressions.666 The source code given in Appendix A hereof is not written to be “fancy” or optimized for speed or in any other way. Its sole purpose is to illustrate the algorithms described in the main text in a simple-to-understand fashion. Some important legalese is relegated to Appendix B. Tables and figures summarize our results.

2 Factors

2.1 Setup and Data

Unlike stocks, barring any special circumstances such as unexpected halts in trading, cryptoassets trade continuously, 24/7. So, while there are notions of “open” and “close” for cryptoassets, their meanings are different from those for stocks. For our purposes here, again, barring any special circumstances, “open” on any given day means the price right after midnight (UTC time), while “close” on any given day means the price right before midnight (UTC time). In this regard, absent trading halts, the open on a given day is very close to the close of the previous day. The high and low prices then have the usual meaning within the 24 hour window between the open and the close. And the volume is the dollar volume traded in said 24 hour interval. All the prices are also measured in dollars, as is the market cap. We use index to label different cryptoassets cross-sectionally, and index to denote the dates, with corresponding to the most recent date in the time series. So: (or, equivalently, ) is the close price for the cryptoasset labeled by on the day labeled by ; is the open price; is the high price; is the low price; is the dollar volume; is the market cap. All our data was freely downloaded from https://coinmarketcap.com (see below).

Next, we define our daily returns as open-to-close intraday returns:

| (1) |

The use of the log-return (or “continuously compounded” return) is intentional here. For small values it is approximately the same as the standard (“single-period”) return defined as

| (2) |

However, cryptoassets can be very volatile, on average, much more so than stocks, and log-returns “smooth out” the outliers somewhat, so below we use .

Unlike with stocks, there are no “dividends” to worry about for cryptoassets, to wit, in terms of adjusting prices for dividends. However, an issuer can split its cryptoasset. Thus, Xaurum had a forward split 8000-to-1 on August 23, 2016, so its price decreased accordingly. Unfortunately, https://coinmarketcap.com does not adjust historical prices for splits, and there does not appear to be a simple source to look up historical splits data. Fortunately, for the purposes of analyzing our factor models here, such splits are immaterial as all our factors are defined such that they are unaffected by splits. Note that market cap and dollar volume are unaffected, only prices are. However, in our factor definitions for any given day we only use ratios of intraday prices, which therefore are also unaffected. In this paper, the only place where splits become important is when we plot price weighted indexes, and we account for the aforesaid Xaurum split there (see below).

2.2 Factor Model

The factor model is of the form

| (3) |

Here is the number of risk factors, are the factor returns, are the residuals, and are the factor loadings. We include the intercept in , so for a given date , the matrix contains a column equal the unit -vector, which we will take to be the first column in . Below, instead of using the index , we will denote each column by , where {name} stands for the name by which we refer to the corresponding factor: “int” for the intercept, “cap” for size, “mom” for momentum, “hlv” for intraday high and low based volatility, and “vol” for volume. These are direct analogs of the short-horizon factors for stocks defined in [Kakushadze, 2015]. We also consider another binary factor (dummy variable), which we refer to as “mnbl”, based on whether the cryptoasset is minable.

To determine whether a given factor adds value, as in [Fama and MacBeth, 1973], we use annualized t-statistic for each factor, which can be computed using the daily returns as follows:

| (4) | |||

| (5) | |||

| (6) |

Here is the beginning of the period for which the t-statistic is computed, and is the length of said period. Throughout, all time quantities are measured in days. Also, the annualization factor777Note that t-statistic is a horizon-dependent quantity; it scales as the square root of the horizon. is (as opposed to for stocks) as cryptoassets trade 24/7. The meaning of is that it is the annualized Sharpe ratio [Sharpe, 1994] based on the time series of the corresponding factor returns (without subtracting any “benchmark” return from the mean return ). So, in the “zeroth approximation”, above 3 would indicate that the corresponding factor is a relevant predictor, and below 2 would indicate that it is a poor predictor.

2.2.1 Intercept

The intercept plays the role of the “market beta”:

| (7) |

Neutrality w.r.t. is dollar neutrality, which is approximate market neutrality.

2.2.2 Cap (Size)

Size is the natural logarithm of the market cap888 In [Kakushadze, 2015] for stock returns the log of the price was used instead as the market cap is the price times the shares outstanding, and the latter change negligibly on short horizons. The same generally holds for cryptoassets, so we could use the price instead of the market cap. However, considering the split adjustment issues mentioned above, it is simpler to use market cap.

| (8) |

So, on date we use the previous day’s market cap, which is 100% out-of-sample.

2.2.3 Momentum

There are various ways to define the momentum factor loading. For our purposes here, we will define it as the previous day’s open-to-close return:

| (9) |

Again, this definition is 100% out-of-sample. Below we will also analyze momenta (which we refer to as mom1, mom2, …) defined using the days prior to the previous day:

| (10) | |||

| (11) | |||

| (12) |

2.2.4 Intraday Volatility

There are various ways to define the intraday volatility factor. Below we will use the following simple definition:999 For alternative definitions, see [Kakushadze, 2015].

| (13) | |||

| (14) |

Averaging over the previous days (which is done 100% out-of-sample) is necessary to smooth out the noise. Since here we are dealing with a variance-like quantity (as opposed to a correlation-like quantity), looking back days does not introduce out-of-sample instabilities associated with correlations and time series based betas. Below we use the values . Also, note that (13) is the logarithmic intraday volatility. This is because, as is generally the case with volatility, the intraday volatility itself (without taking the log) has a skewed, long-tailed distribution for higher-end values, and, among other things, as a factor it would adversely interfere with the intercept and also result in unnaturally skewed regression residuals .

2.2.5 Volume

For stocks, the average daily dollar volume is a measure of liquidity. For cryptoassets the situation is murkier (see below). Nonetheless, following [Kakushadze, 2015] we define the volume factor loading as follows:

| (15) | |||

| (16) |

Recall that is the daily dollar volume, so is the average daily dollar volume over the days immediately preceding the day labeled by (so it is 100% out-of-sample). Below we use the values . For we have the previous day’s dollar volume. The reason for including it will become clear below.

2.2.6 “Is-Minable” Dummy

Some cryptoassets are minable and some are not. Therefore, it is natural to consider a binary factor loading defined as follows (notwithstanding that a priori it is not clear why it would have an impact on daily returns):

| (17) |

This factor loading is independent of the time index and only depends on .

2.3 Estimation Period and Universe

We downloaded101010 R source code for data downloads and running factor regressions is given in Appendix A. the data from https://coinmarketcap.com for all cryptoassets as of August 19, 2018 (so the most recent date in the data is August 18, 2018), whose number was 1,855. Out of those, 1,851 had downloadable data, albeit for many various fields were populated with “?”, which we converted into NAs. Despite a seemingly large number of cryptoassets, the useful data going back any reasonable number of days only exists for a fraction of them. In order to be able to run our regressions (see below), we only kept cryptoassets with non-NA price (open, close, high, low), volume and market cap data, with an additional filter that no null volume was allowed either (to avoid contamination by stale prices). There were only 362 cryptoassets with such properties starting August 18, 2018 (inclusive) and going back days (i.e., 1 year “padded” with additional 21 days to be able to compute 20-day moving averages out-of-sample), 129 cryptoassets when the filters were applied to days (i.e., 2 years “padded” with additional 21 days), and only 66 cryptoassets when the filters were applied to days (i.e., 3 years “padded” with additional 21 days).111111 Actually, 2 cryptoassets had apparently “artifact” stale prices in the second and third year (looking back), so they had to be excluded from the corresponding regressions (see below). So, the cross-section is pretty “thin”, nowhere near as rich as for stocks. However, we must work with what we have.

2.4 Regressions and Results

So, we run regressions of the daily returns over the loadings (computed as above) for various periods and their subperiods described above and in Tables 1 through 18. Tables 1 through 10 include int (intercept), cap (size), mom (momentum), hlv (intraday volatility) and vol (volume), for various values of and . From these tables it appears that the average daily dollar volume for is a poor predictor. For (i.e., the previous day’s dollar volume) the results are at best mixed and certainly not ground-shaking. While it is possible that the previous day’s volume adds value, it might do so more efficiently as an additional filter (when, e.g., defining a trading signal) as opposed to a stand-alone factor. Tables 11 and 12, which exclude vol and include only int, cap, mom and hlv, appear to support this conclusion. Further, hlv appears to be rather stable w.r.t. the choice of . The mom factor leads by a large margin in all periods (see Tables 11 and 12). The cap and hlv factors appear to work well except in the first year (meaning, going back in time from August 18, 2018, so this is the most recent 1-year period) for the smaller universes based on 129 and 66 cryptoassets (see above). However, these factors work much better for the same period for the larger universe based on 362 cryptoassets (see above), which subsumes the aforesaid smaller universes. Therefore, the most likely explanation would appear to be that this is due to the smallness of the cross-sectional samples for these smaller universes. Further, the hlv factor appears to be the weakest among cap, mom and hlv. However, removing hlv worsens the results (see Table 13), as does removing the intercept (see Table 14).121212 The intercept has variable t-statistic across various periods and universes, including changing its sign. However, this is not surprising as the intercept plays the role of the “market beta”, which is expected to be highly variable on general grounds, as it is for stocks as well as other assets.

Considering how strong the mom factor is, it is natural to also look at momenta from days prior to the previous day, i.e., mom1, mom2, …(defined above). Tables 15 and 16 suggest that mom1 indeed appears to be a good predictor. Going beyond mom1 (see Table 17, which also includes mom2, mom3 and mom4) unsurprisingly gives mixed results as any effect from momentum is expected to decay with time. Note that the regression coefficients for the momenta are negative, which suggests a substantial mean-reversion effect in the aforesaid cryptoasset returns. Including the dummy variable mnbl defined above does not appear to add value (see Table 18).

2.5 “Sanity Check”

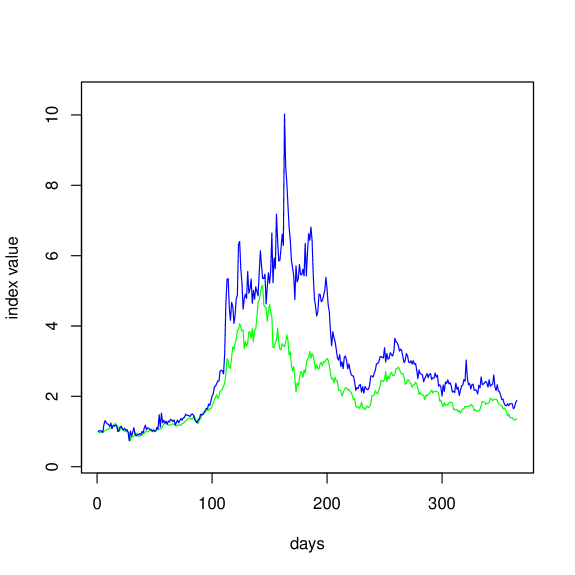

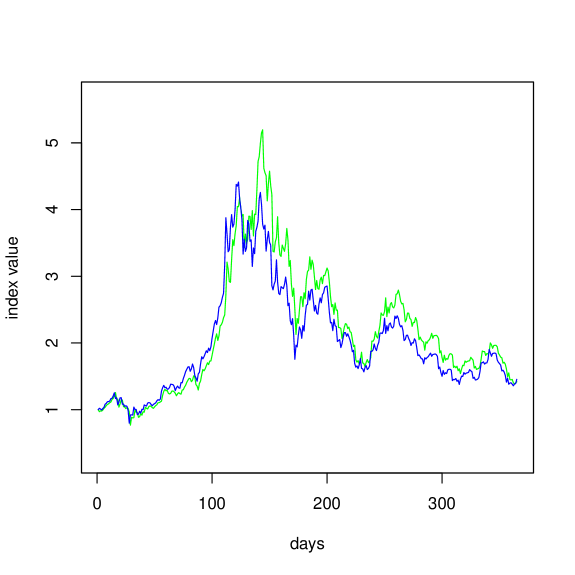

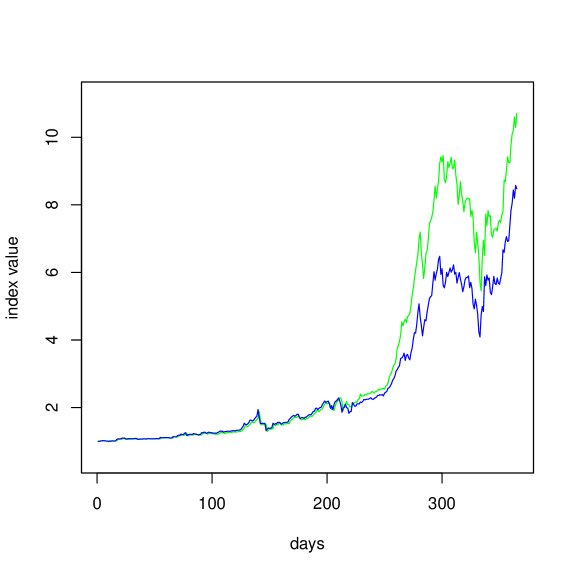

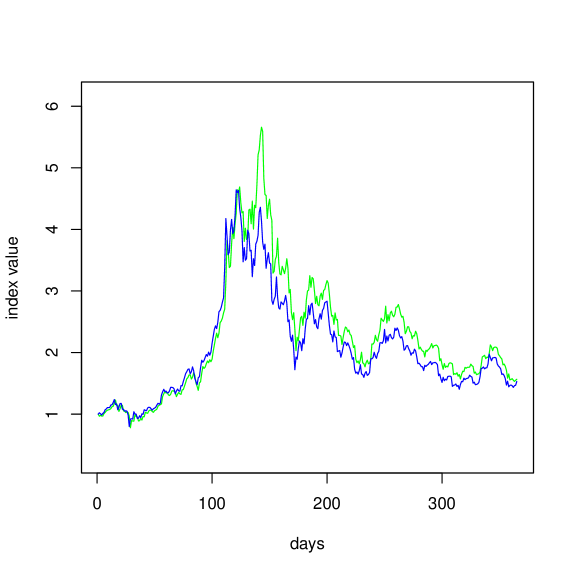

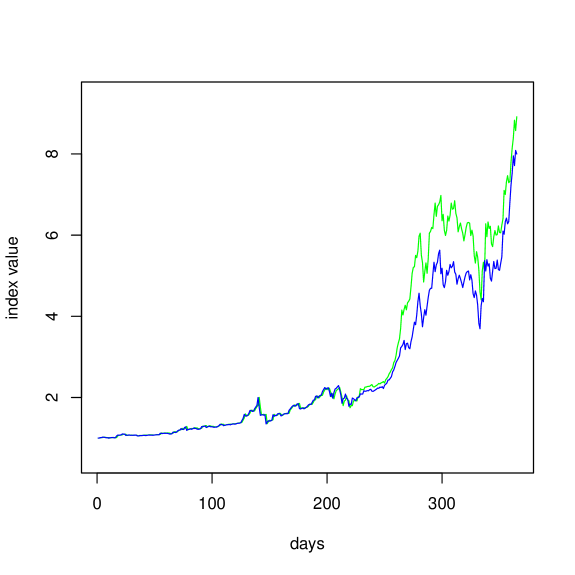

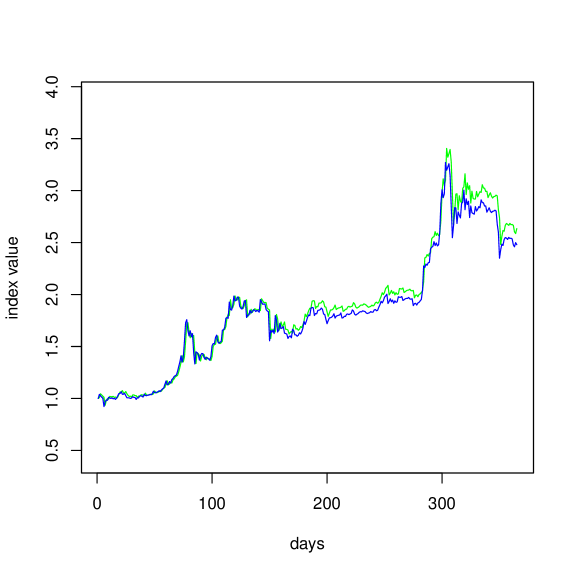

Considering the “flukes” in the performance of cap and hlv during the most recent 1-year period for smaller universes (see above), it makes sense to get at least a superficial visual confirmation that nothing utterly “odd” happened with those universes during that period. A simple thing to do here is to look at the performance of “market indexes” built based on the aforesaid 362, 129 and 66 cryptoasset universes. Thus, we can construct the following indexes (among myriad others):

| (18) | |||

| (19) |

Here is a market cap weighted index for the universe of cryptoassets, and the normalization coefficient is fixed such that equals 1 for the value of corresponding to the earliest date in the time period for which is constructed. The price weighted index is constructed similarly, except that the prices are obtained from the closing prices by adjusting for splits. In our case we only had to adjust for the Xaurum split mentioned above. The results are plotted in Figures 1 through 6. There appears to be nothing “peculiar” about these market indexes for the most recent 1-year period and the aforesaid smaller universes, except for the spike in the price weighted index in Figure 1. However, this spike is due to a single cryptoasset called 42-coin, which is highly priced with a small market cap. Incidently, this is a good example of why price weighted indexes can be misleading.

3 Concluding Remarks

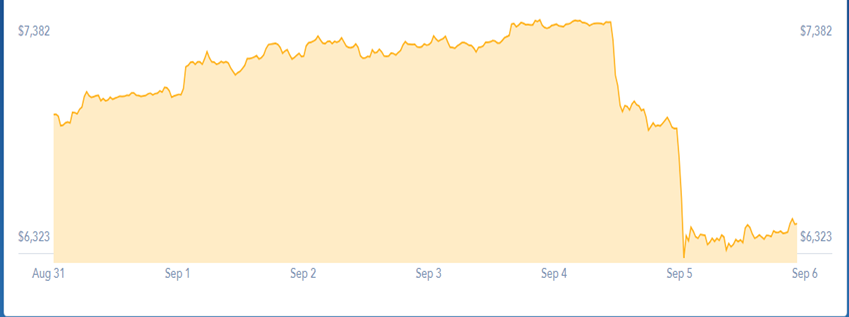

Despite the superfluous ubiquity of cryptoassets, the amount of cross-sectionally available data is still limited as for most cryptoassets it simply does not go far back enough. Cryptoassets come and go, many coins and tokens disappear a short while after issuance, and many are perceived as being scams to raise a quick buck and run with the unsuspecting or uninformed investors’ money. This is still a very young field despite Bitcoin having being around for over 9 years, so the kind of analyses performed in [Kakushadze, 2015] on 2,000, 3,000 and even 4,000 stock tickers going back 5 years is simply impossible for cryptoassets at this nascent stage in their development. It might take another 5-10 years to collect that kind of data, depending on their survival rate – and assuming the whole field does not disappear due to regulatory or some other (less foreseeable) issues.131313 Thus, as this note was being finalized, the cryptoasset market had yet another crash on September 5, 2018 on the news that Goldman Sachs reportedly is putting on hold its plans for a cryptocurrency trading desk [Campbell and Chaparro, 2018]. Also see Figure 7. Only time will tell.

Nonetheless, it is pleasant to observe that the 3 short-horizon factors discussed in [Kakushadze, 2015] for stocks, to wit, cap (size), mom (momentum) and hlv (intraday volatility) work well for cryptoassets as well. The fact that vol (volume) does not seem to add value for cryptoassets (at least beyond the previous day’s volume) is not necessarily surprising as volume is not directional. In fact, on its own it is not a good predictor for stocks either and only works when combined with the other factors. One possible explanation for why vol does not add value for cryptoassets is that it is less evident how well vol describes actual liquidity in cryptoasset markets considering a very different (from stocks) fee structure and executions. Thus, one way to quantify and see the difference between cryptoassets and stocks (as it relates to volume) is to compare their respective cross-sections of ratios of, say, the 20-day average daily dollar volume to the market cap, which is a measure of average daily “turnover”. For the 362 cryptoasset universe (see above) as of August 18, 2018, the cross-sectional summary of this ratio is as follows: Min = , 1st Quartile = , Median = , Mean = , 3rd Quartile = , Max = . For stocks, for the universe of the 500 highest market cap stocks as of (a randomly chosen date) August 31, 2010, that summary reads: Min = , 1st Quartile = , Median = , Mean = , 3rd Quartile = , Max = . The bottom line is that on relative basis (i.e., based on the average daily “turnover”) cryptoassets do not trade anywhere near as much as stocks, so it is not that surprising that the volume is not a good predictor for cryptoassets.

The fact that momentum dominates as a factor for cryptoasset returns means that on short horizons the market is strongly mean-reverting (cross-sectionally). This in turn implies that if one could short a large cross-section of cryptoassets and trade them on short horizons cost-effectively, one might be able to trade a cross-sectional dollar-neutral mean-reversion statistical arbitrage strategy with cryptoassets, along the lines of similar strategies for stocks – perhaps one day soon.

Appendix A R Source Code: Downloads and Regressions

In this appendix we give R (R Project for Statistical Computing, https://www.r-project.org/) source code for downloading cryptoasset data and running factor regressions discussed in the main text. The code is straightforward and self-explanatory. The first function is crypto.data(), which downloads the names, symbols, market caps and various other data for all cryptoassets available at any given time from https://coinmarketcap.com and outputs said data in the file crypto.cap.txt. Among other things, in the column labeled URL, this file contains strings that are used on https://coinmarketcap.com for historical data downloads, which are not the same as symbols (or names). In fact, oddly, there can be cases where two different cryptoassets have the same symbol, so symbols are not unique differentiators. The function crypto.data() internally calls three auxiliary functions shared.get.webpage(), shared.parse.html() and shared.write.table(). These auxiliary functions are given in [Kakushadze and Yu, 2017] (which is freely downloadable) with the names sec.get.webpage(), sec.parse.html(), sec.write.table().

The second function crypto.hist.prc(date) (which also uses the aforesaid 3 auxiliary functions) downloads data for all cryptoassets in the file crypto.cap.txt. There can be a few names for which the data is bad, which are skipped and the corresponding fields from the 11th column (labeled URL) of the file crypto.cap.txt are written in the file crypto.bad.txt. The historical data for the rest of the names is written into tab-delimited text files (one file per name) in the directory CryptoHistData. The sole input date (which is in the format yyyymmdd) of the function crypto.hist.prc(date) corresponds to the date as of which to download the data. This can be modified, e.g., to include the specific lookback date through which to do download the historical data. As-is, this function downloads all available (on https://coinmarketcap.com) historical data starting with date and going back in time (so the lookbacks are name-dependent).

The third function crypto.prc.files() aggregates the data stored in the individual files in the directory CryptoHistData by data type (close, open, high, low, volume, market cap). It reads the file crypto.bad.txt to skip the names therein and generates tab-delimited text files with rows and columns, where is the number of all names excepting those in crypto.bad.txt, and is the number of days for which there is data for the first name in crypto.cap.txt, which is the oldest cryptoasset Bitcoin (as the names in crypto.cap.txt are ranked by market cap, and Bitcoin has the largest one). These files are cr.prc.txt (close price), cr.open.txt (open price), cr.high.txt (high price), cr.low.txt (low price), cr.vol.txt (dollar volume), and cr.cap.txt (market cap). The function also generates two single-column text files cr.name.txt (names of the cryptoassets in the same order as all the other files), and cr.mnbl.txt (1 if the name is minable, otherwise 0). All missing data (including all fields with “?”) is populated with NAs.

The fourth and last function crypto.prc() reads the aforesaid aggregated data files, constructs factor loadings internally referred to as av (average daily dollar volume), size (market cap), mom (momentum) and its delayed variations mom1 through mom4, hlv (intraday volatility), as well as mnbl (the “is-minable” dummy), and runs regressions, which include int (intercept) and are used for computing the annualized t-statistic based on the time series of regression coefficients. The inputs of crypto.prc() are days (the length of the selection period used in fixing the cryptoasset universe by applying the aforesaid non-NA data and non-zero volume filters, which period is further “padded” – see below), back (the length of the skip period, i.e., how many days to skip in the selection period before the lookback period), lookback (the length of the lookback period over which the regression is run), d.r (the extra “padding” added to the selection period plus one day, so the moving averages can be computed out-of-sample; we take d.r = 20), d.v (the same as defined in Section 2), and d.i (the same as defined in Section 2). Thus, for instance, in Table 9 we have days = 3 * 365 (so with d.r = 20 the “padded” selection period contains days), back = 365, and lookback = 365. Therefore, the regressions are run over 365 days by skipping the most recent 365 days, starting with the 366th day in the time series and going back in time (i.e., over the 2nd year in the 3-year time series, looking back). The function crypto.prc() also constructs and plots market cap and price weighted indexes based on the universes and periods over which the regressions are run.

crypto.data <- function ()

{

require(XML)

require(httr)

url <- "https://coinmarketcap.com/all/views/all/"

z <- x <- shared.get.webpage(url)

x <- shared.parse.html(x, keyword = "table")

u <- c(x[22:28])

for(i in 1:length(u))

{

u1 <- grep(u[i], x)

x <- x[-u1]

}

u1 <- grep("[*]", x)

x1 <- x[-u1]

hdr <- c("Rank", "Name", "Symbol", "MktCap", "Price",

"Supply", "Volume", "Ch1h", "Ch24h", "Ch7d",

"URL", "Minable")

x1 <- x1[-(1:10)]

x1 <- matrix(x1, length(x1)/11, 11, byrow = T)

x1 <- x1[, -2]

x1 <- gsub(",", "", x1)

x1 <- gsub("\\$", "", x1)

x1 <- gsub("%", "", x1)

x1 <- cbind(x1, rep("", nrow(x1)), rep("Y", nrow(x1)))

y <- grep("currency-symbol visible-xs", z)

z1 <- z[y]

y <- grep("link-secondary", z1)

z1 <- z1[y]

y <- grep("href", z1)

z1 <- z1[y]

y <- grep("currencies", z1)

z1 <- z1[y]

if(length(z1) != nrow(x1))

stop("ERROR")

x <- x[-(1:10)]

for(i in 1:length(z1))

{

u <- unlist(strsplit(z1[i], "/"))[3]

x1[i, 11] <- u

u1 <- grep("[*]", x[1:11])

if(length(u1) > 0)

{

x1[i, 12] <- "N"

x <- x[-(1:12)]

}

else

x <- x[-(1:11)]

}

x1 <- rbind(hdr, x1)

shared.write.table(x1, "crypto.cap.txt", T)

}

crypto.hist.prc <- function (date)

{

require(XML)

require(httr)

x <- read.delim("crypto.cap.txt", header = T)

x <- as.matrix(x)

univ <- x[, 11]

for(i in 1:length(univ))

{

url <- paste("https://coinmarketcap.com/currencies/",

univ[i],

"/historical-data/?start=20000101&end=", date, sep = "")

x <- shared.get.webpage(url)

x <- shared.parse.html(x, keyword = "table")

n <- length(x)/7

if(n < 1 | trunc(n) != n)

{

write(univ[i], "crypto.bad.txt", append = T)

next

}

x <- matrix(x, length(x)/7, 7, byrow = T)

x[1, ] <- c("Date", "Open", "High", "Low",

"Close", "Volume", "MktCap")

file <- paste("CryptoHistData/", univ[i], ".txt", sep = "")

shared.write.table(x, file, T)

}

}

crypto.prc.files <- function ()

{

match.univ <- function (univ1, univ2)

{

good <- match(univ1, univ2, nomatch = 0)

univ <- univ2[good]

return(univ)

}

read.file <- function(file, header = T)

{

x <- read.delim(file, header = header)

x <- as.matrix(x)

x <- gsub(",", "", x)

return(x)

}

x <- read.file("crypto.cap.txt")

univ <- x[, 11]

mnbl <- x[, 12]

name <- x[, 2]

bad <- readLines("crypto.bad.txt")

take <- is.na(match(univ, bad))

mnbl <- mnbl[take]

name <- name[take]

mnbl[mnbl == "Y"] <- 1

mnbl[mnbl == "N"] <- 0

univ <- univ[take]

shared.write.table(mnbl, file = "cr.mnbl.txt", T)

shared.write.table(name, file = "cr.name.txt", T)

n <- length(univ)

for(i in 1:n)

{

x <- read.file(paste("CryptoHistData/", univ[i],

".txt", sep = ""))

if(i == 1)

{

dates <- x[, "Date"]

d <- length(dates)

prc <- matrix(NA, n, d)

cap <- matrix(NA, n, d)

high <- matrix(NA, n, d)

low <- matrix(NA, n, d)

vol <- matrix(NA, n, d)

open <- matrix(NA, n, d)

dimnames(prc)[[2]] <- dates

dimnames(cap)[[2]] <- dates

dimnames(high)[[2]] <- dates

dimnames(low)[[2]] <- dates

dimnames(vol)[[2]] <- dates

dimnames(open)[[2]] <- dates

prc[1, ] <- x[1:d, "Close"]

cap[1, ] <- x[1:d, "MktCap"]

high[1, ] <- x[1:d, "High"]

low[1, ] <- x[1:d, "Low"]

vol[1, ] <- x[1:d, "Volume"]

open[1, ] <- x[1:d, "Open"]

}

else

{

dates1 <- x[, "Date"]

dates1 <- match.univ(dates, dates1)

prc[i, dates1] <- x[1:length(dates1), "Close"]

cap[i, dates1] <- x[1:length(dates1), "MktCap"]

high[i, dates1] <- x[1:length(dates1), "High"]

low[i, dates1] <- x[1:length(dates1), "Low"]

vol[i, dates1] <- x[1:length(dates1), "Volume"]

open[i, dates1] <- x[1:length(dates1), "Open"]

}

}

mode(prc) <- "numeric"

mode(cap) <- "numeric"

mode(high) <- "numeric"

mode(low) <- "numeric"

mode(vol) <- "numeric"

mode(open) <- "numeric"

shared.write.table(prc, file = "cr.prc.txt", T)

shared.write.table(cap, file = "cr.cap.txt", T)

shared.write.table(high, file = "cr.high.txt", T)

shared.write.table(low, file = "cr.low.txt", T)

shared.write.table(vol, file = "cr.vol.txt", T)

shared.write.table(open, file = "cr.open.txt", T)

}

crypto.prc <- function (days = 365, back = 0,

lookback = days, d.r = 20, d.v = 20, d.i = 20)

{

calc.ix <- function(z, days)

{

ix <- colSums(z[, 1:days])

ix <- ix[days:1]

ix <- ix / ix[1]

return(ix)

}

read.prc <- function(file, header = F, make.numeric = T)

{

x <- read.delim(file, header = header)

x <- as.matrix(x)

if(make.numeric)

mode(x) <- "numeric"

return(x)

}

calc.mv.avg <- function(x, days, d.r)

{

if(d.r == 1)

return(x[, 1:days])

y <- matrix(0, nrow(x), days)

for(i in 1:days)

y[, i] <- rowMeans(x[, i:(i + d.r - 1)], na.rm = T)

return(y)

}

prc <- read.prc("cr.prc.txt")

cap <- read.prc("cr.cap.txt")

high <- read.prc("cr.high.txt")

low <- read.prc("cr.low.txt")

vol <- read.prc("cr.vol.txt")

open <- read.prc("cr.open.txt")

mnbl <- read.prc("cr.mnbl.txt")

name <- read.prc("cr.name.txt", make.numeric = F)

d <- days + d.r + 1

prc <- prc[, 1:d]

cap <- cap[, 1:d]

high <- high[, 1:d]

low <- low[, 1:d]

vol <- vol[, 1:d]

open <- open[, 1:d]

take <- rowSums(is.na(prc)) == 0 & rowSums(is.na(cap)) == 0 &

rowSums(is.na(high)) == 0 & rowSums(is.na(low)) == 0 &

rowSums(is.na(vol)) == 0 & rowSums(is.na(open)) == 0 &

rowSums(vol == 0) == 0

ret <- log(prc[take, -d] / prc[take, -1])

prc <- prc[take, -1]

cap <- cap[take, -1]

high <- high[take, -1]

low <- low[take, -1]

vol <- vol[take, -1]

open <- open[take, -1]

mnbl <- mnbl[take, 1]

name <- name[take, 1]

if(back > 0)

{

ret <- ret[, (back + 1):ncol(ret)]

prc <- prc[, (back + 1):ncol(prc)]

cap <- cap[, (back + 1):ncol(cap)]

high <- high[, (back + 1):ncol(high)]

low <- low[, (back + 1):ncol(low)]

vol <- vol[, (back + 1):ncol(vol)]

open <- open[, (back + 1):ncol(open)]

}

days <- lookback

av <- log(calc.mv.avg(vol, days, d.v))

hlv <- (high - low)^2 / prc^2

hlv <- 0.5 * log(calc.mv.avg(hlv, days, d.i))

take <- rowSums(!is.finite(hlv)) == 0

av <- av[take, ]

hlv <- hlv[take, ]

mom <- log(prc / open)[take, 1:days]

mom1 <- log(prc / open)[take, 1:days + 1]

mom2 <- log(prc / open)[take, 1:days + 2]

mom3 <- log(prc / open)[take, 1:days + 3]

mom4 <- log(prc / open)[take, 1:days + 4]

size <- log(cap)[take, 1:days]

ret <- ret[take, 1:days]

mnbl <- mnbl[take]

name <- name[take]

for(i in 1:days)

{

flm <- cbind(size[, i], mom[, i], hlv[, i], av[, i])

if(i == 1)

fac <- matrix(NA, ncol(flm) + 1, days)

reg <- lm(ret[, i] flm)

fac[, i] <- coefficients(reg)

}

t.stat <- sqrt(365) * rowMeans(fac) / apply(fac, 1, sd)

t.stat <- round(t.stat, 2)

prc <- prc[take, ]

cap <- cap[take, ]

y <- prc[name == "Xaurum", ]

prc[name == "Xaurum", y > 1] <-

prc[name == "Xaurum", y > 1] / 8000

ix.cap <- calc.ix(cap, days)

ix.prc <- calc.ix(prc, days)

plot(1:length(ix.cap), ix.cap, type = "l",

col = "green", xlab = "days", ylab = "index value",

ylim = c(min(c(ix.cap, ix.prc)) - .5,

max(c(ix.cap, ix.prc)) + .5))

lines(1:length(ix.prc), ix.prc, col = "blue")

return(t.stat)

}

Appendix B DISCLAIMERS

Wherever the context so requires, the masculine gender includes the feminine and/or neuter, and the singular form includes the plural and vice versa. The author of this paper (“Author”) and his affiliates including without limitation Quantigic® Solutions LLC (“Author’s Affiliates” or “his Affiliates”) make no implied or express warranties or any other representations whatsoever, including without limitation implied warranties of merchantability and fitness for a particular purpose, in connection with or with regard to the content of this paper including without limitation any code or algorithms contained herein (“Content”).

The reader may use the Content solely at his/her/its own risk and the reader shall have no claims whatsoever against the Author or his Affiliates and the Author and his Affiliates shall have no liability whatsoever to the reader or any third party whatsoever for any loss, expense, opportunity cost, damages or any other adverse effects whatsoever relating to or arising from the use of the Content by the reader including without any limitation whatsoever: any direct, indirect, incidental, special, consequential or any other damages incurred by the reader, however caused and under any theory of liability; any loss of profit (whether incurred directly or indirectly), any loss of goodwill or reputation, any loss of data suffered, cost of procurement of substitute goods or services, or any other tangible or intangible loss; any reliance placed by the reader on the completeness, accuracy or existence of the Content or any other effect of using the Content; and any and all other adversities or negative effects the reader might encounter in using the Content irrespective of whether the Author or his Affiliates is or are or should have been aware of such adversities or negative effects.

The R code included in Appendix A hereof is part of the copyrighted R code of Quantigic® Solutions LLC and is provided herein with the express permission of Quantigic® Solutions LLC. The copyright owner retains all rights, title and interest in and to its copyrighted source code included in Appendix A hereof and any and all copyrights therefor.

References

- [1]

- Alessandretti et al, 2018 Alessandretti, L., ElBahrawy, A., Aiello, L.M. and Baronchelli, A. (2018) Machine Learning the Cryptocurrency Market. Working Paper. Available online: https://arxiv.org/pdf/1805.08550.pdf.

- Amihud, 2002 Amihud, Y. (2002) Illiquidity and stock returns: cross-section and time-series effects. Journal of Financial Markets 5(1): 31-56.

- Amjad and Shah, 2017 Amjad, M.J. and Shah, D. (2017) Trading Bitcoin and Online Time Series Prediction. Working Paper. Available online: http://proceedings.mlr.press/v55/amjad16.pdf.

- Ang et al, 2006 Ang, A., Hodrick, R., Xing, Y. and Zhang, X. (2006) The Cross-Section of Volatility and Expected Returns. Journal of Finance 61(1): 259-299.

- Anson, 2013 Anson, M. (2013) Performance Measurement in Private Equity: The Impact of FAS 157 on the Lagged Beta Effect. Journal of Private Equity 17(1): 29-44.

- Asness, 1995 Asness, C.S. (1995) The Power of Past Stock Returns to Explain Future Stock Returns. Working Paper (unpublished). New York, NY: Goldman Sachs Asset Management.

- Asness et al, 2001 Asness, C., Krail, R.J. and Liew, J.M. (2001) Do Hedge Funds Hedge? Journal of Portfolio Management 28(1): 6-19.

- Asness, Porter and Stevens, 2000 Asness, C.S., Porter, R.B. and Stevens, R.L. (2000) Predicting Stock Returns Using Industry-Relative Firm Characteristics. Working Paper. Available online: https://ssrn.com/abstract=213872.

- Baek and Elbeck, 2014 Baek, C. and Elbeck, M. (2014) Bitcoins as an Investment or Speculative Vehicle? A First Look. Applied Economics Letters 22(1): 30-34.

- Banz, 1981 Banz, R. (1981) The relationship between return and market value of common stocks. Journal of Financial Economics 9(1): 3-18.

- Bariviera et al, 2017 Bariviera, A.F., Basgall, M.J., Hasperué, W. and Naiouf, M. (2017) Some stylized facts of the Bitcoin market. Physica A: Statistical Mechanics and its Applications 484: 82-90.

- Basu, 1977 Basu, S. (1977) The investment performance of common stocks in relation to their price to earnings ratios: A test of the efficient market hypothesis. Journal of Finance 32(3): 663-682.

- Bouoiyour et al, 2016 Bouoiyour, J., Selmi, R., Tiwari, A.K. and Olayeni, O.R. (2016) What drives Bitcoin price? Economics Bulletin 36(2): 843-850.

- Bouri et al, 2017 Bouri, E., Molnár, P., Azzi, G., Roubaud, D. and Hagfors, L.I. (2017) On the hedge and safe haven properties of Bitcoin: Is it really more than a diversifier? Finance Research Letters 20: 192-198.

- Brandvold et al, 2015 Brandvold, M., Molnár, P., Vagstad, K. and Valstad, O.C.A. (2015) Price discovery on Bitcoin exchanges. Journal of International Financial Markets, Institutions and Money 36: 18-35.

- Brière, Oosterlinck and Szafarz, 2015 Brière, M., Oosterlinck, K. and Szafarz, A. (2015) Virtual currency, tangible return: Portfolio diversification with bitcoin. Journal of Asset Management 16(6): 365-373.

- Campbell and Chaparro, 2018 Campbell, D. and Chaparro, F. (2018) Goldman Sachs is ditching near-term plans to open a bitcoin trading desk, instead focusing on a key business for driving Wall Street investment in crypto. Business Insider (September 5, 2018). Available online: https://www.businessinsider.com/goldman-sachs-retreats-from-launching-crypto-trading-desk-2018-9.

- Carhart, 1997 Carhart, M.M. (1997) Persistence in mutual fund performance. Journal of Finance 52(1): 57-82.

- Cheah and Fry, 2015 Cheah, E.T. and Fry, J. (2015) Speculative Bubbles in Bitcoin markets? An Empirical Investigation into the Fundamental Value of Bitcoin. Economics Letters 130: 32-36.

- Cheung, Roca and Su, 2015 Cheung, A., Roca, E. and Su, J.-J. (2015) Crypto-currency Bubbles: an Application of the Phillips-Shi-Yu (2013) Methodology on Mt. Gox Bitcoin Prices. Applied Economics 47(23): 2348-2358.

- Ciaian, Rajcaniova and Kancs, 2015 Ciaian, P., Rajcaniova, M. and Kancs, D. (2015) The economics of BitCoin price formation. Applied Economics 48(19): 1799-1815.

- Colianni, Rosales and Signorotti, 2015 Colianni, S., Rosales, S. and Signorotti, M. (2015) Algorithmic Trading of Cryptocurrency Based on Twitter Sentiment Analysis. Working Paper. Available online: http://cs229.stanford.edu/proj2015/029_report.pdf.

- Donier and Bouchaud, 2015 Donier, J. and Bouchaud, J.-P. (2015) Why Do Markets Crash? Bitcoin Data Offers Unprecedented Insights. PLoS ONE 10(10): e0139356.

- Dyhrberg, 2015 Dyhrberg, A.H. (2015) Bitcoin, gold and the dollar – a GARCH volatility analysis. Finance Research Letters 16: 85-92.

- Eisl, Gasser and Weinmayer, 2015 Eisl, A., Gasser, S. and Weinmayer, K. (2015) Caveat Emptor: Does Bitcoin Improve Portfolio Diversification? Working Paper. Available online: https://ssrn.com/abstract=2408997.

- Gajardo, Kristjanpoller and Minutolo, 2018 Gajardo, G., Kristjanpoller, W.D. and Minutolo, M. (2018) Does Bitcoin exhibit the same asymmetric multifractal cross-correlations with crude oil, gold and DJIA as the Euro, Great British Pound and Yen? Chaos, Solitons & Fractals 109: 195-205.

- Garcia and Schweitzer, 2015 Garcia, D. and Schweitzer, F. (2015) Social signals and algorithmic trading of Bitcoin. Royal Society Open Science 2(9): 150288.

- Georgoula et al, 2015 Georgoula, I., Pournarakis, D., Bilanakos, C., Sotiropoulos, D. and Giaglis, G.M. (2015) Using Time-Series and Sentiment Analysis to Detect the Determinants of Bitcoin Prices. Working Paper. Available online: https://ssrn.com/abstract=2607167.

- Fama and French, 1992 Fama, E.F. and French, K.R. (1992) The Cross-Section of Expected Stock Returns. Journal of Finance 47(2): 427-465.

- Fama and French, 1993 Fama, E.F. and French, K.R. (1993) Common Risk Factors in the Returns on Stocks and Bonds. Journal of Financial Economics 33(1): 3-56.

- Fama and French, 1996 Fama, E.F. and French, K.R. (1996) Multifactor Explanations of Asset Pricing Anomalies. Journal of Finance 51(1): 55-84.

- Fama and MacBeth, 1973 Fama, E.F. and MacBeth, J.D. (1973) Risk, Return and Equilibrium: Empirical Tests. Journal of Political Economy 81(3): 607-636.

- Harvey, 2016 Harvey, C.R. (2016) Cryptofinance. Working Paper. Available online: https://ssrn.com/abstract=2438299.

- Haugen, 1995 Haugen, R.A. (1995) The New Finance: The Case Against Efficient Markets. Upper Saddle River, NJ: Prentice Hall.

- Jegadeesh and Titman, 1993 Jegadeesh, N. and Titman, S. (1993) Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. Journal of Finance 48(1): 65-91.

- Jiang and Liang, 2017 Jiang, Z. and Liang, J. (2017) Cryptocurrency Portfolio Management with Deep Reinforcement Learning. Working Paper. Available online: https://arxiv.org/pdf/1612.01277.pdf.

- Kakushadze, 2015 Kakushadze, Z. (2015) 4-Factor Model for Overnight Returns. Wilmott Magazine 2015(79): 56-62. Available online: https://ssrn.com/abstract=2511874.

- Kakushadze and Liew, 2015 Kakushadze, Z. and Liew, J.K-S. (2015) Custom v. Standardized Risk Models. Risks 3(2): 112-138. Available online: https://ssrn.com/abstract=2493379.

- Kakushadze and Yu, 2017 Kakushadze, Z. and Yu, W. Open Source Fundamental Industry Classification. Data 2(2): 20. Available online: https://ssrn.com/abstract=2954300.

- Kim et al, 2016 Kim, Y.B., Kim, J.G., Kim, W., Im, J.H., Kim, T.H., Kang, S.J. and Kim, C.H. (2016) Predicting Fluctuations in Cryptocurrency Transactions Based on User Comments and Replies. PLoS ONE 11(8): e0161197.

- Kristoufek, 2015 Kristoufek, L. (2015) What Are the Main Drivers of the Bitcoin Price? Evidence from Wavelet Coherence Analysis. PLoS ONE 10(4): e0123923.

- Lakonishok, Shleifer and Vishny, 1994 Lakonishok, J., Shleifer, A. and Vishny, R.W. (1994) Contrarian investment, extrapolation, and risk. Journal of Finance 49(5): 1541-1578.

- Lee, Guo and Wang, 2018 Lee, D.K.C., Guo, L. and Wang, Y. (2018) Cryptocurrency: A New Investment Opportunity? Journal of Alternative Investments 20(3): 16-40.

- Li et al, 2018 Li, T.R., Chamrajnagar, A.S., Fong, X.R., Rizik, N.R. and Fu, F. (2018) Sentiment-Based Prediction of Alternative Cryptocurrency Price Fluctuations Using Gradient Boosting Tree Model. Working Paper. Available online: https://arxiv.org/pdf/1805.00558.pdf.

- Liew, Li and Budavári, 2018 Liew, J.K.-S., Li, R.Z. and Budavári, T. (2018) Crypto-Currency Investing Examined. Working Paper. Available online: https://ssrn.com/abstract=3157926.

- Liew and Vassalou, 2000 Liew, J. and Vassalou, M. (2000) Can Book-to-Market, Size and Momentum be Risk Factors that Predict Economic Growth? Journal of Financial Economics 57(2): 221-245.

- Nakano, Takahashi and Takahashi, 2018 Nakano, M., Takahashi, A. and Takahashi, S. (2018) Bitcoin Technical Trading With Artificial Neural Network. Working Paper. Available online: https://ssrn.com/abstract=3128726.

- Ortisi, 2016 Ortisi, M. (2016) Bitcoin Market Volatility Analysis Using Grand Canonical Minority Game. Ledger 1: 111-118.

- Pástor and Stambaugh, 2003 Pástor, L’. and Stambaugh, R.F. (2003) Liquidity Risk and Expected Stock Returns. Journal of Political Economy 111(3): 642-685.

- Scholes and Williams, 1977 Scholes, M. and Williams, J. (1977) Estimating Betas from Nonsynchronous Data. Journal of Financial Economics 5(3): 309-327.

- Shah and Zhang, 2014 Shah, D. and Zhang, K. (2014) Bayesian regression and Bitcoin. Working Paper. Available online: https://arxiv.org/pdf/1410.1231.pdf.

- Sharpe, 1994 Sharpe, W.F. (1994) The Sharpe Ratio. Journal of Portfolio Management 21(1): 49-58.

- Van Alstyne, 2014 Van Alstyne, M. (2014) Why Bitcoin has value. Communications of the ACM 57(5): 30-32.

- Wang and Vergne, 2017 Wang, S. and Vergne, J.-P. (2017) Buzz factor or innovation potential: What explains cryptocurrencies returns? PLoS ONE 12(1): e0169556.

| t-stat:int | t-stat:cap | t-stat:mom | t-stat:hlv | t-stat:vol | ||

| 20 | 20 | 2.66 | -3.68 | -34.2 | -2.48 | 1.22 |

| 20 | 15 | 2.59 | -3.73 | -34.17 | -2.71 | 1.15 |

| 20 | 10 | 2.54 | -3.67 | -34.18 | -2.58 | 1.1 |

| 20 | 5 | 2.51 | -3.71 | -34.19 | -2.46 | 1.16 |

| 15 | 20 | 2.59 | -3.54 | -34.19 | -2.47 | 1.06 |

| 15 | 15 | 2.56 | -3.61 | -34.16 | -2.71 | 1.08 |

| 15 | 10 | 2.52 | -3.55 | -34.17 | -2.58 | 1.03 |

| 15 | 5 | 2.47 | -3.58 | -34.18 | -2.46 | 1.08 |

| 10 | 20 | 2.53 | -3.38 | -34.17 | -2.43 | 0.84 |

| 10 | 15 | 2.51 | -3.46 | -34.15 | -2.67 | 0.89 |

| 10 | 10 | 2.52 | -3.42 | -34.18 | -2.56 | 0.94 |

| 10 | 5 | 2.49 | -3.48 | -34.19 | -2.46 | 1 |

| 5 | 20 | 2.36 | -3.07 | -34.14 | -2.4 | 0.48 |

| 5 | 15 | 2.34 | -3.15 | -34.12 | -2.62 | 0.53 |

| 5 | 10 | 2.36 | -3.13 | -34.15 | -2.51 | 0.61 |

| 5 | 5 | 2.42 | -3.21 | -34.19 | -2.42 | 0.85 |

| 3 | 20 | 2.23 | -2.87 | -34.06 | -2.42 | 0.27 |

| 3 | 15 | 2.21 | -2.95 | -34.04 | -2.64 | 0.31 |

| 3 | 10 | 2.22 | -2.92 | -34.08 | -2.53 | 0.38 |

| 3 | 5 | 2.27 | -3 | -34.12 | -2.43 | 0.63 |

| 1 | 20 | 3.47 | -5.1 | -33.98 | -2.27 | 2.6 |

| 1 | 15 | 3.44 | -5.17 | -33.96 | -2.52 | 2.6 |

| 1 | 10 | 3.43 | -5.11 | -34 | -2.46 | 2.63 |

| 1 | 5 | 3.5 | -5.24 | -34.06 | -2.44 | 2.87 |

| t-stat:int | t-stat:cap | t-stat:mom | t-stat:hlv | t-stat:vol | ||

| 20 | 20 | 1.83 | -1.45 | -16.87 | -2.72 | -0.06 |

| 20 | 15 | 1.81 | -1.45 | -16.84 | -2.7 | -0.07 |

| 20 | 10 | 1.69 | -1.48 | -16.79 | -3.23 | -0.14 |

| 20 | 5 | 1.54 | -1.37 | -16.75 | -3.16 | -0.26 |

| 15 | 20 | 1.84 | -1.45 | -16.89 | -2.71 | -0.1 |

| 15 | 15 | 1.86 | -1.49 | -16.85 | -2.67 | -0.01 |

| 15 | 10 | 1.74 | -1.53 | -16.81 | -3.19 | -0.07 |

| 15 | 5 | 1.58 | -1.44 | -16.76 | -3.15 | -0.19 |

| 10 | 20 | 1.8 | -1.39 | -16.89 | -2.69 | -0.2 |

| 10 | 15 | 1.83 | -1.44 | -16.85 | -2.63 | -0.09 |

| 10 | 10 | 1.78 | -1.55 | -16.8 | -3.11 | 0.03 |

| 10 | 5 | 1.65 | -1.49 | -16.76 | -3.09 | -0.08 |

| 5 | 20 | 1.68 | -1.29 | -16.85 | -2.69 | -0.38 |

| 5 | 15 | 1.72 | -1.36 | -16.82 | -2.63 | -0.25 |

| 5 | 10 | 1.68 | -1.48 | -16.77 | -3.08 | -0.11 |

| 5 | 5 | 1.71 | -1.61 | -16.72 | -3.04 | 0.12 |

| 3 | 20 | 1.49 | -1 | -16.77 | -2.63 | -0.64 |

| 3 | 15 | 1.53 | -1.06 | -16.73 | -2.54 | -0.54 |

| 3 | 10 | 1.48 | -1.16 | -16.69 | -2.98 | -0.42 |

| 3 | 5 | 1.51 | -1.29 | -16.66 | -2.93 | -0.19 |

| 1 | 20 | 2.29 | -2.26 | -16.72 | -2.8 | 0.75 |

| 1 | 15 | 2.31 | -2.28 | -16.69 | -2.73 | 0.84 |

| 1 | 10 | 2.26 | -2.37 | -16.66 | -3.18 | 0.94 |

| 1 | 5 | 2.3 | -2.55 | -16.63 | -3.2 | 1.16 |

| t-stat:int | t-stat:cap | t-stat:mom | t-stat:hlv | t-stat:vol | ||

| 20 | 20 | -0.39 | 0.18 | -17.17 | -1.01 | -0.67 |

| 20 | 15 | -0.36 | 0.19 | -17.04 | -0.96 | -0.69 |

| 20 | 10 | -0.35 | 0.01 | -17 | -1.55 | -0.66 |

| 20 | 5 | -0.35 | 0.04 | -16.99 | -1.6 | -0.71 |

| 15 | 20 | -0.42 | 0.21 | -17.16 | -0.99 | -0.71 |

| 15 | 15 | -0.37 | 0.2 | -17.06 | -0.89 | -0.69 |

| 15 | 10 | -0.34 | 0.01 | -17.01 | -1.49 | -0.64 |

| 15 | 5 | -0.35 | 0.03 | -17 | -1.56 | -0.68 |

| 10 | 20 | -0.58 | 0.48 | -17.15 | -0.98 | -1.03 |

| 10 | 15 | -0.53 | 0.48 | -17.05 | -0.87 | -1 |

| 10 | 10 | -0.47 | 0.22 | -17.05 | -1.41 | -0.87 |

| 10 | 5 | -0.47 | 0.24 | -17.03 | -1.51 | -0.91 |

| 5 | 20 | -0.82 | 0.79 | -17.08 | -1 | -1.38 |

| 5 | 15 | -0.76 | 0.76 | -16.98 | -0.9 | -1.33 |

| 5 | 10 | -0.71 | 0.5 | -16.99 | -1.43 | -1.18 |

| 5 | 5 | -0.67 | 0.47 | -17.07 | -1.39 | -1.09 |

| 3 | 20 | -1.04 | 1.15 | -16.98 | -1.02 | -1.79 |

| 3 | 15 | -0.99 | 1.13 | -16.88 | -0.91 | -1.74 |

| 3 | 10 | -0.95 | 0.89 | -16.89 | -1.42 | -1.6 |

| 3 | 5 | -0.9 | 0.85 | -16.98 | -1.34 | -1.49 |

| 1 | 20 | -0.28 | 0.09 | -16.69 | -1.12 | -0.69 |

| 1 | 15 | -0.21 | 0.05 | -16.59 | -1.03 | -0.64 |

| 1 | 10 | -0.18 | -0.17 | -16.6 | -1.57 | -0.53 |

| 1 | 5 | -0.13 | -0.24 | -16.67 | -1.57 | -0.43 |

| t-stat:int | t-stat:cap | t-stat:mom | t-stat:hlv | t-stat:vol | ||

| 20 | 20 | 4.39 | -2.43 | -15.37 | -2.84 | 0.37 |

| 20 | 15 | 4.3 | -2.43 | -15.43 | -2.86 | 0.38 |

| 20 | 10 | 4.22 | -2.36 | -15.4 | -2.96 | 0.19 |

| 20 | 5 | 4.04 | -2.28 | -15.33 | -2.9 | 0.09 |

| 15 | 20 | 4.43 | -2.42 | -15.38 | -2.83 | 0.28 |

| 15 | 15 | 4.34 | -2.44 | -15.44 | -2.83 | 0.41 |

| 15 | 10 | 4.28 | -2.38 | -15.41 | -2.92 | 0.23 |

| 15 | 5 | 4.12 | -2.33 | -15.34 | -2.89 | 0.12 |

| 10 | 20 | 4.54 | -2.58 | -15.38 | -2.87 | 0.4 |

| 10 | 15 | 4.44 | -2.61 | -15.44 | -2.88 | 0.54 |

| 10 | 10 | 4.36 | -2.53 | -15.41 | -2.88 | 0.53 |

| 10 | 5 | 4.27 | -2.52 | -15.34 | -2.86 | 0.45 |

| 5 | 20 | 4.62 | -2.81 | -15.39 | -2.95 | 0.49 |

| 5 | 15 | 4.54 | -2.83 | -15.46 | -2.94 | 0.64 |

| 5 | 10 | 4.48 | -2.77 | -15.42 | -2.93 | 0.65 |

| 5 | 5 | 4.5 | -2.86 | -15.34 | -2.89 | 0.88 |

| 3 | 20 | 4.43 | -2.64 | -15.33 | -2.97 | 0.38 |

| 3 | 15 | 4.35 | -2.65 | -15.4 | -2.93 | 0.51 |

| 3 | 10 | 4.3 | -2.59 | -15.36 | -2.9 | 0.51 |

| 3 | 5 | 4.32 | -2.68 | -15.29 | -2.87 | 0.73 |

| 1 | 20 | 5.38 | -4 | -15.36 | -3.03 | 2.07 |

| 1 | 15 | 5.26 | -3.94 | -15.44 | -2.97 | 2.15 |

| 1 | 10 | 5.22 | -3.91 | -15.41 | -2.98 | 2.16 |

| 1 | 5 | 5.31 | -4.11 | -15.36 | -3.02 | 2.39 |

| t-stat:int | t-stat:cap | t-stat:mom | t-stat:hlv | t-stat:vol | ||

| 20 | 20 | 1.38 | -1.02 | -12.64 | -1.87 | -0.15 |

| 20 | 15 | 1.36 | -1.07 | -12.64 | -1.96 | -0.15 |

| 20 | 10 | 1.32 | -1.05 | -12.62 | -2.17 | -0.21 |

| 20 | 5 | 1.26 | -1.12 | -12.58 | -2.31 | -0.24 |

| 15 | 20 | 1.44 | -1.12 | -12.68 | -1.89 | -0.08 |

| 15 | 15 | 1.46 | -1.2 | -12.67 | -1.94 | -0.01 |

| 15 | 10 | 1.43 | -1.2 | -12.66 | -2.15 | -0.05 |

| 15 | 5 | 1.38 | -1.3 | -12.62 | -2.3 | -0.06 |

| 10 | 20 | 1.33 | -0.92 | -12.67 | -1.83 | -0.28 |

| 10 | 15 | 1.35 | -1 | -12.65 | -1.86 | -0.21 |

| 10 | 10 | 1.37 | -1.03 | -12.63 | -2.04 | -0.18 |

| 10 | 5 | 1.34 | -1.19 | -12.59 | -2.26 | -0.16 |

| 5 | 20 | 1.19 | -0.75 | -12.75 | -1.82 | -0.44 |

| 5 | 15 | 1.21 | -0.82 | -12.72 | -1.83 | -0.37 |

| 5 | 10 | 1.23 | -0.87 | -12.68 | -2 | -0.33 |

| 5 | 5 | 1.31 | -1.11 | -12.61 | -2.12 | -0.14 |

| 3 | 20 | 1.09 | -0.56 | -12.74 | -1.73 | -0.6 |

| 3 | 15 | 1.1 | -0.61 | -12.7 | -1.71 | -0.55 |

| 3 | 10 | 1.12 | -0.65 | -12.67 | -1.87 | -0.51 |

| 3 | 5 | 1.2 | -0.89 | -12.6 | -1.99 | -0.32 |

| 1 | 20 | 1.78 | -1.72 | -12.63 | -1.94 | 0.57 |

| 1 | 15 | 1.79 | -1.8 | -12.62 | -1.92 | 0.64 |

| 1 | 10 | 1.8 | -1.83 | -12.6 | -2.11 | 0.69 |

| 1 | 5 | 1.86 | -2.04 | -12.55 | -2.22 | 0.84 |

| t-stat:int | t-stat:cap | t-stat:mom | t-stat:hlv | t-stat:vol | ||

| 20 | 20 | 0.61 | -0.38 | -11.89 | -2.2 | -0.65 |

| 20 | 15 | 0.59 | -0.43 | -11.86 | -2.29 | -0.64 |

| 20 | 10 | 0.53 | -0.39 | -11.81 | -2.63 | -0.72 |

| 20 | 5 | 0.44 | -0.4 | -11.71 | -2.7 | -0.8 |

| 15 | 20 | 0.67 | -0.47 | -11.95 | -2.22 | -0.57 |

| 15 | 15 | 0.7 | -0.57 | -11.89 | -2.24 | -0.49 |

| 15 | 10 | 0.64 | -0.55 | -11.86 | -2.58 | -0.55 |

| 15 | 5 | 0.55 | -0.58 | -11.76 | -2.67 | -0.62 |

| 10 | 20 | 0.59 | -0.31 | -11.92 | -2.17 | -0.75 |

| 10 | 15 | 0.63 | -0.4 | -11.86 | -2.16 | -0.67 |

| 10 | 10 | 0.62 | -0.44 | -11.81 | -2.44 | -0.62 |

| 10 | 5 | 0.53 | -0.51 | -11.71 | -2.61 | -0.68 |

| 5 | 20 | 0.48 | -0.17 | -11.95 | -2.17 | -0.87 |

| 5 | 15 | 0.51 | -0.25 | -11.88 | -2.14 | -0.79 |

| 5 | 10 | 0.51 | -0.31 | -11.81 | -2.42 | -0.73 |

| 5 | 5 | 0.55 | -0.5 | -11.69 | -2.43 | -0.57 |

| 3 | 20 | 0.32 | 0.11 | -11.92 | -2.08 | -1.15 |

| 3 | 15 | 0.35 | 0.07 | -11.84 | -2 | -1.1 |

| 3 | 10 | 0.35 | 0.02 | -11.78 | -2.27 | -1.05 |

| 3 | 5 | 0.39 | -0.16 | -11.66 | -2.27 | -0.89 |

| 1 | 20 | 0.88 | -0.86 | -11.7 | -2.31 | -0.17 |

| 1 | 15 | 0.92 | -0.95 | -11.64 | -2.25 | -0.08 |

| 1 | 10 | 0.91 | -0.99 | -11.59 | -2.53 | -0.04 |

| 1 | 5 | 0.93 | -1.13 | -11.48 | -2.5 | 0.09 |

| t-stat:int | t-stat:cap | t-stat:mom | t-stat:hlv | t-stat:vol | ||

| 20 | 20 | 3.16 | -2.06 | -12.97 | -1.7 | 0.57 |

| 20 | 15 | 3.14 | -2.08 | -13 | -1.69 | 0.58 |

| 20 | 10 | 3.09 | -2.03 | -12.94 | -1.73 | 0.49 |

| 20 | 5 | 3.09 | -2.24 | -12.94 | -1.98 | 0.53 |

| 15 | 20 | 3.27 | -2.23 | -13.03 | -1.76 | 0.7 |

| 15 | 15 | 3.26 | -2.26 | -13.05 | -1.74 | 0.75 |

| 15 | 10 | 3.22 | -2.22 | -13 | -1.76 | 0.68 |

| 15 | 5 | 3.23 | -2.46 | -13 | -2.02 | 0.73 |

| 10 | 20 | 3.13 | -2.06 | -13.06 | -1.72 | 0.53 |

| 10 | 15 | 3.13 | -2.08 | -13.06 | -1.69 | 0.57 |

| 10 | 10 | 3.11 | -2.04 | -13 | -1.68 | 0.54 |

| 10 | 5 | 3.19 | -2.34 | -13 | -1.99 | 0.64 |

| 5 | 20 | 2.92 | -1.87 | -13.18 | -1.69 | 0.38 |

| 5 | 15 | 2.92 | -1.9 | -13.19 | -1.64 | 0.42 |

| 5 | 10 | 2.9 | -1.85 | -13.12 | -1.59 | 0.39 |

| 5 | 5 | 3.06 | -2.18 | -13.06 | -1.89 | 0.62 |

| 3 | 20 | 2.87 | -1.82 | -13.22 | -1.61 | 0.36 |

| 3 | 15 | 2.86 | -1.84 | -13.23 | -1.56 | 0.4 |

| 3 | 10 | 2.84 | -1.78 | -13.15 | -1.49 | 0.37 |

| 3 | 5 | 2.98 | -2.09 | -13.1 | -1.81 | 0.59 |

| 1 | 20 | 3.88 | -3.3 | -13.26 | -1.8 | 1.85 |

| 1 | 15 | 3.88 | -3.33 | -13.28 | -1.73 | 1.91 |

| 1 | 10 | 3.85 | -3.28 | -13.22 | -1.73 | 1.9 |

| 1 | 5 | 3.97 | -3.57 | -13.18 | -2.03 | 2.08 |

| t-stat:int | t-stat:cap | t-stat:mom | t-stat:hlv | t-stat:vol | ||

| 20 | 20 | -1.34 | 1.45 | -10.55 | -0.29 | -1.74 |

| 20 | 15 | -1.29 | 1.44 | -10.53 | -0.33 | -1.77 |

| 20 | 10 | -1.24 | 1.4 | -10.59 | -0.64 | -1.81 |

| 20 | 5 | -1.19 | 1.37 | -10.69 | -0.73 | -1.75 |

| 15 | 20 | -1.4 | 1.53 | -10.52 | -0.29 | -1.82 |

| 15 | 15 | -1.32 | 1.45 | -10.53 | -0.27 | -1.76 |

| 15 | 10 | -1.26 | 1.39 | -10.59 | -0.57 | -1.78 |

| 15 | 5 | -1.2 | 1.35 | -10.68 | -0.68 | -1.71 |

| 10 | 20 | -1.53 | 1.73 | -10.48 | -0.3 | -2.05 |

| 10 | 15 | -1.44 | 1.63 | -10.5 | -0.27 | -1.98 |

| 10 | 10 | -1.4 | 1.56 | -10.58 | -0.51 | -1.98 |

| 10 | 5 | -1.35 | 1.55 | -10.67 | -0.64 | -1.94 |

| 5 | 20 | -1.65 | 1.85 | -10.46 | -0.37 | -2.2 |

| 5 | 15 | -1.54 | 1.73 | -10.48 | -0.33 | -2.11 |

| 5 | 10 | -1.49 | 1.63 | -10.57 | -0.59 | -2.07 |

| 5 | 5 | -1.49 | 1.62 | -10.71 | -0.53 | -1.99 |

| 3 | 20 | -1.84 | 2.16 | -10.4 | -0.41 | -2.55 |

| 3 | 15 | -1.74 | 2.06 | -10.41 | -0.36 | -2.47 |

| 3 | 10 | -1.68 | 1.93 | -10.5 | -0.63 | -2.42 |

| 3 | 5 | -1.65 | 1.88 | -10.65 | -0.53 | -2.27 |

| 1 | 20 | -1.4 | 1.6 | -10.09 | -0.43 | -1.9 |

| 1 | 15 | -1.28 | 1.47 | -10.12 | -0.4 | -1.81 |

| 1 | 10 | -1.21 | 1.33 | -10.2 | -0.69 | -1.75 |

| 1 | 5 | -1.14 | 1.25 | -10.34 | -0.61 | -1.59 |

| t-stat:int | t-stat:cap | t-stat:mom | t-stat:hlv | t-stat:vol | ||

| 20 | 20 | 2.95 | -1.71 | -11.81 | -2.25 | 0.25 |

| 20 | 15 | 2.94 | -1.72 | -11.79 | -2.15 | 0.27 |

| 20 | 10 | 2.82 | -1.62 | -11.65 | -2.29 | 0.14 |

| 20 | 5 | 2.8 | -1.83 | -11.57 | -2.5 | 0.15 |

| 15 | 20 | 3.1 | -1.92 | -11.91 | -2.34 | 0.42 |

| 15 | 15 | 3.1 | -1.94 | -11.87 | -2.2 | 0.48 |

| 15 | 10 | 2.99 | -1.86 | -11.74 | -2.32 | 0.36 |

| 15 | 5 | 2.97 | -2.07 | -11.67 | -2.52 | 0.37 |

| 10 | 20 | 3.01 | -1.8 | -11.93 | -2.32 | 0.31 |

| 10 | 15 | 3.01 | -1.8 | -11.88 | -2.16 | 0.35 |

| 10 | 10 | 2.95 | -1.75 | -11.74 | -2.2 | 0.31 |

| 10 | 5 | 2.98 | -2.02 | -11.65 | -2.48 | 0.34 |

| 5 | 20 | 2.83 | -1.67 | -12.03 | -2.3 | 0.25 |

| 5 | 15 | 2.83 | -1.68 | -11.98 | -2.12 | 0.29 |

| 5 | 10 | 2.75 | -1.6 | -11.83 | -2.11 | 0.23 |

| 5 | 5 | 2.87 | -1.9 | -11.67 | -2.33 | 0.44 |

| 3 | 20 | 2.74 | -1.55 | -12.06 | -2.24 | 0.13 |

| 3 | 15 | 2.74 | -1.56 | -12.01 | -2.05 | 0.18 |

| 3 | 10 | 2.65 | -1.45 | -11.86 | -2 | 0.09 |

| 3 | 5 | 2.74 | -1.72 | -11.7 | -2.22 | 0.29 |

| 1 | 20 | 3.69 | -2.9 | -12.02 | -2.46 | 1.48 |

| 1 | 15 | 3.71 | -2.93 | -11.98 | -2.25 | 1.56 |

| 1 | 10 | 3.62 | -2.87 | -11.82 | -2.27 | 1.51 |

| 1 | 5 | 3.69 | -3.1 | -11.68 | -2.41 | 1.66 |

| t-stat:int | t-stat:cap | t-stat:mom | t-stat:hlv | t-stat:vol | ||

| 20 | 20 | 3.53 | -2.62 | -14.15 | -1.04 | 1.02 |

| 20 | 15 | 3.48 | -2.64 | -14.23 | -1.13 | 1 |

| 20 | 10 | 3.53 | -2.64 | -14.26 | -1.05 | 0.98 |

| 20 | 5 | 3.54 | -2.82 | -14.35 | -1.33 | 1.03 |

| 15 | 20 | 3.56 | -2.73 | -14.17 | -1.06 | 1.1 |

| 15 | 15 | 3.55 | -2.76 | -14.25 | -1.18 | 1.13 |

| 15 | 10 | 3.61 | -2.77 | -14.28 | -1.08 | 1.12 |

| 15 | 5 | 3.65 | -2.98 | -14.37 | -1.39 | 1.2 |

| 10 | 20 | 3.38 | -2.5 | -14.2 | -0.99 | 0.86 |

| 10 | 15 | 3.36 | -2.53 | -14.27 | -1.12 | 0.89 |

| 10 | 10 | 3.41 | -2.49 | -14.28 | -1.05 | 0.87 |

| 10 | 5 | 3.52 | -2.8 | -14.38 | -1.38 | 1.05 |

| 5 | 20 | 3.13 | -2.26 | -14.35 | -0.94 | 0.58 |

| 5 | 15 | 3.11 | -2.29 | -14.43 | -1.06 | 0.61 |

| 5 | 10 | 3.18 | -2.28 | -14.44 | -0.97 | 0.63 |

| 5 | 5 | 3.39 | -2.63 | -14.49 | -1.35 | 0.88 |

| 3 | 20 | 3.11 | -2.27 | -14.4 | -0.86 | 0.68 |

| 3 | 15 | 3.08 | -2.29 | -14.47 | -0.97 | 0.7 |

| 3 | 10 | 3.14 | -2.3 | -14.48 | -0.88 | 0.76 |

| 3 | 5 | 3.35 | -2.64 | -14.53 | -1.3 | 1 |

| 1 | 20 | 4.24 | -4.05 | -14.53 | -1 | 2.42 |

| 1 | 15 | 4.19 | -4.05 | -14.61 | -1.11 | 2.44 |

| 1 | 10 | 4.24 | -3.98 | -14.66 | -1.08 | 2.5 |

| 1 | 5 | 4.43 | -4.35 | -14.76 | -1.55 | 2.75 |

| period | t-stat:int | t-stat:cap | t-stat:mom | t-stat:hlv | |

|---|---|---|---|---|---|

| Table 1 | 20 | 2.07 | -4.22 | -34.11 | -2.54 |

| Table 1 | 15 | 2 | -4.31 | -34.08 | -2.79 |

| Table 1 | 10 | 1.97 | -4.21 | -34.09 | -2.69 |

| Table 1 | 5 | 1.88 | -4.04 | -34.09 | -2.56 |

| Table 2 | 20 | 2.42 | -3.87 | -16.76 | -2.95 |

| Table 2 | 15 | 2.4 | -3.81 | -16.72 | -2.94 |

| Table 2 | 10 | 2.24 | -3.87 | -16.68 | -3.38 |

| Table 2 | 5 | 2.09 | -3.82 | -16.63 | -3.27 |

| Table 3 | 20 | -0.09 | -0.98 | -16.89 | -1.1 |

| Table 3 | 15 | -0.05 | -1.02 | -16.76 | -1.06 |

| Table 3 | 10 | -0.08 | -1.38 | -16.74 | -1.66 |

| Table 3 | 5 | -0.06 | -1.42 | -16.76 | -1.68 |

| Table 4 | 20 | 5.68 | -5.77 | -15.34 | -3.22 |

| Table 4 | 15 | 5.6 | -5.66 | -15.41 | -3.22 |

| Table 4 | 10 | 5.38 | -5.6 | -15.37 | -3.24 |

| Table 4 | 5 | 5.05 | -5.44 | -15.3 | -3.1 |

| period | t-stat:int | t-stat:cap | t-stat:mom | t-stat:hlv | |

|---|---|---|---|---|---|

| Table 5 | 20 | 1.9 | -3.3 | -12.57 | -2.38 |

| Table 5 | 15 | 1.86 | -3.35 | -12.57 | -2.42 |

| Table 5 | 10 | 1.86 | -3.37 | -12.5 | -2.56 |

| Table 5 | 5 | 1.75 | -3.55 | -12.44 | -2.63 |

| Table 6 | 20 | 1.27 | -3.05 | -11.81 | -2.81 |

| Table 6 | 15 | 1.24 | -3.09 | -11.76 | -2.84 |

| Table 6 | 10 | 1.21 | -3.11 | -11.64 | -3.08 |

| Table 6 | 5 | 1.08 | -3.22 | -11.52 | -3.03 |

| Table 7 | 20 | 3.71 | -4.03 | -13.02 | -2.06 |

| Table 7 | 15 | 3.68 | -4.06 | -13.04 | -2.01 |

| Table 7 | 10 | 3.62 | -4.06 | -12.95 | -2.04 |

| Table 7 | 5 | 3.5 | -4.28 | -12.93 | -2.17 |

| Table 8 | 20 | -0.28 | -0.31 | -10.32 | -0.42 |

| Table 8 | 15 | -0.19 | -0.48 | -10.32 | -0.47 |

| Table 8 | 10 | -0.11 | -0.75 | -10.37 | -0.75 |

| Table 8 | 5 | -0.13 | -0.82 | -10.44 | -0.83 |

| Table 9 | 20 | 3.72 | -4.24 | -11.92 | -2.67 |

| Table 9 | 15 | 3.7 | -4.21 | -11.88 | -2.54 |

| Table 9 | 10 | 3.55 | -4.22 | -11.67 | -2.67 |

| Table 9 | 5 | 3.39 | -4.34 | -11.57 | -2.62 |

| Table 10 | 20 | 3.82 | -3.81 | -14.12 | -1.32 |

| Table 10 | 15 | 3.77 | -3.89 | -14.2 | -1.37 |

| Table 10 | 10 | 3.82 | -3.89 | -14.24 | -1.29 |

| Table 10 | 5 | 3.8 | -4.22 | -14.32 | -1.62 |

| period | t-stat:int | t-stat:cap | t-stat:mom |

|---|---|---|---|

| Table 1 | 1.81 | -3.01 | -33.63 |

| Table 2 | 2.2 | -2.14 | -16.5 |

| Table 3 | 0.13 | -0.48 | -16.16 |

| Table 4 | 4.77 | -3.95 | -15.11 |

| Table 5 | 2 | -1.98 | -12.22 |

| Table 6 | 1.45 | -1.31 | -11.44 |

| Table 7 | 3.34 | -2.92 | -12.67 |

| Table 8 | 0.24 | -0.54 | -9.8 |

| Table 9 | 3.28 | -2.5 | -11.56 |

| Table 10 | 3.47 | -3.44 | -13.78 |

| period | t-stat:cap | t-stat:mom | t-stat:hlv |

| Table 1 | -2.28 | -33.23 | -2.23 |

| Table 2 | -1.75 | -16.33 | -3.24 |

| Table 3 | -1.36 | -16.47 | -1.7 |

| Table 4 | -0.93 | -15.03 | -2.94 |

| Table 5 | -1.34 | -12.24 | -2.58 |

| Table 6 | -1.67 | -11.29 | -3 |

| Table 7 | -0.81 | -12.75 | -2.3 |

| Table 8 | -0.35 | -10.08 | -0.51 |

| Table 9 | -0.96 | -11.38 | -2.89 |

| Table 10 | -0.66 | -14.15 | -1.56 |

| period | t-stat:int | t-stat:cap | t-stat:mom | t-stat:mom1 | t-stat:hlv | |

|---|---|---|---|---|---|---|

| Table 1 | 20 | 1.69 | -3.79 | -35.89 | -15.24 | -2.32 |

| Table 1 | 15 | 1.63 | -3.85 | -35.85 | -15.2 | -2.54 |

| Table 1 | 10 | 1.62 | -3.73 | -35.86 | -15.19 | -2.37 |

| Table 1 | 5 | 1.53 | -3.48 | -35.84 | -15.13 | -2.06 |

| Table 2 | 20 | 2.21 | -3.25 | -18.05 | -8.04 | -2.47 |

| Table 2 | 15 | 2.2 | -3.18 | -18 | -8.02 | -2.43 |

| Table 2 | 10 | 2.03 | -3.21 | -17.96 | -7.98 | -2.83 |

| Table 2 | 5 | 1.89 | -3.08 | -17.9 | -7.79 | -2.52 |

| Table 3 | 20 | -0.64 | -0.32 | -19.77 | -9.46 | -1.04 |

| Table 3 | 15 | -0.61 | -0.28 | -19.63 | -9.41 | -0.94 |

| Table 3 | 10 | -0.66 | -0.64 | -19.62 | -9.43 | -1.58 |

| Table 3 | 5 | -0.67 | -0.54 | -19.63 | -9.26 | -1.46 |

| Table 4 | 20 | 5.49 | -4.88 | -16.54 | -7.93 | -2.33 |

| Table 4 | 15 | 5.43 | -4.83 | -16.59 | -7.91 | -2.34 |

| Table 4 | 10 | 5.2 | -4.74 | -16.54 | -7.87 | -2.31 |

| Table 4 | 5 | 4.86 | -4.53 | -16.45 | -7.69 | -2.02 |

| period | t-stat:int | t-stat:cap | t-stat:mom | t-stat:mom1 | t-stat:hlv | |

|---|---|---|---|---|---|---|

| Table 5 | 20 | 1.86 | -3.27 | -13.4 | -5.47 | -2.37 |

| Table 5 | 15 | 1.83 | -3.32 | -13.38 | -5.45 | -2.41 |

| Table 5 | 10 | 1.78 | -3.28 | -13.28 | -5.38 | -2.54 |

| Table 5 | 5 | 1.61 | -3.39 | -13.23 | -5.2 | -2.56 |

| Table 6 | 20 | 1.2 | -2.92 | -12.44 | -4.97 | -2.73 |

| Table 6 | 15 | 1.17 | -2.95 | -12.39 | -4.95 | -2.75 |

| Table 6 | 10 | 1.1 | -2.98 | -12.25 | -4.87 | -3.03 |

| Table 6 | 5 | 0.89 | -2.96 | -12.15 | -4.65 | -2.94 |

| Table 7 | 20 | 3.73 | -4.09 | -14.01 | -5.95 | -2.13 |

| Table 7 | 15 | 3.7 | -4.11 | -14.03 | -5.94 | -2.11 |

| Table 7 | 10 | 3.57 | -4.04 | -13.91 | -5.89 | -2.14 |

| Table 7 | 5 | 3.38 | -4.19 | -13.88 | -5.76 | -2.25 |

| Table 8 | 20 | -0.6 | 0.11 | -11.67 | -6.06 | -0.44 |

| Table 8 | 15 | -0.49 | 0.01 | -11.63 | -6.03 | -0.42 |

| Table 8 | 10 | -0.4 | -0.25 | -11.68 | -5.96 | -0.71 |

| Table 8 | 5 | -0.49 | -0.18 | -11.84 | -6.02 | -0.78 |

| Table 9 | 20 | 3.71 | -4.19 | -12.68 | -5.43 | -2.69 |

| Table 9 | 15 | 3.68 | -4.15 | -12.67 | -5.42 | -2.57 |

| Table 9 | 10 | 3.46 | -4.17 | -12.46 | -5.36 | -2.81 |

| Table 9 | 5 | 3.14 | -4.14 | -12.37 | -5.2 | -2.77 |

| Table 10 | 20 | 3.91 | -3.99 | -15.39 | -6.59 | -1.46 |

| Table 10 | 15 | 3.86 | -4.08 | -15.43 | -6.57 | -1.55 |

| Table 10 | 10 | 3.87 | -3.91 | -15.4 | -6.55 | -1.3 |

| Table 10 | 5 | 3.87 | -4.27 | -15.45 | -6.42 | -1.6 |

| period | int | cap | mom | mom1 | mom2 | mom3 | mom4 | hlv |

| Table 1 | 0.95 | -2.43 | -37.16 | -18.9 | -10.61 | -4.45 | -3.97 | -1.06 |

| Table 2 | 1.47 | -2.55 | -18.26 | -8.54 | -4.63 | -0.54 | -0.65 | -2.29 |

| Table 3 | -0.84 | -0.09 | -21.06 | -10.45 | -5.63 | -2.03 | -0.82 | -1.08 |

| Table 4 | 4.41 | -3.61 | -16.51 | -8.14 | -3.76 | -0.9 | -1.51 | -1.56 |

| Table 5 | 1.23 | -2.83 | -13.36 | -5.59 | -2.58 | -0.8 | -0.72 | -2.38 |

| Table 6 | 0.44 | -2.56 | -12.11 | -4.96 | -1.86 | -0.56 | -0.37 | -2.93 |

| Table 7 | 3.11 | -3.28 | -13.99 | -6.18 | -2.92 | -1.41 | -1.79 | -1.49 |

| Table 8 | -0.66 | -0.92 | -13.17 | -6.68 | -2.15 | -1.62 | 0.66 | -1.76 |

| Table 9 | 2.83 | -3.2 | -12.12 | -5.53 | -1.89 | -1.59 | -2.07 | -1.97 |

| Table 10 | 3.61 | -3.37 | -15.99 | -6.99 | -4.05 | -1.24 | -1.48 | -0.83 |

| period | t-stat:int | t-stat:cap | t-stat:mom | t-stat:hlv | t-stat:mnbl |

| Table 1 | 1.88 | -4.09 | -34.19 | -2.53 | 0.01 |

| Table 2 | 2.25 | -4.04 | -16.67 | -3.32 | -0.88 |

| Table 3 | -0.13 | -1.41 | -16.74 | -1.67 | 0.23 |

| Table 4 | 5.17 | -5.8 | -15.37 | -3.22 | -1.5 |

| Table 5 | 2.04 | -3.68 | -12.43 | -2.61 | -1.18 |

| Table 6 | 1.27 | -3.28 | -11.53 | -2.97 | -0.74 |

| Table 7 | 3.74 | -4.39 | -12.93 | -2.21 | -1.37 |

| Table 8 | -0.06 | -0.79 | -10.4 | -0.76 | -0.22 |

| Table 9 | 3.41 | -4.34 | -11.63 | -2.62 | -0.77 |

| Table 10 | 4.38 | -4.46 | -14.26 | -1.72 | -2.01 |