MS-BDA-18-02864.R2

Ma, Simchi-Levi, and Zhao

Dynamic Pricing (and Assortment) under a Static Calendar

Dynamic Pricing (and Assortment) under a Static Calendar

Will Ma \AFFGraduate School of Business, Columbia University, New York NY 10027, \EMAILwm2428@gsb.columbia.edu \AUTHORDavid Simchi-Levi \AFFInstitute for Data, Systems, and Society, Department of Civil and Environmental Engineering, and Operations Research Center, Massachusetts Institute of Technology, Cambridge, MA 02139, \EMAILdslevi@mit.edu \AUTHORJinglong Zhao \AFFInstitute for Data, Systems, and Society, Massachusetts Institute of Technology, Cambridge, MA 02139, \EMAILjinglong@mit.edu

This work is motivated by our collaboration with a large consumer packaged goods (CPG) company. We have found that while the company appreciates the advantages of dynamic pricing, they deem it operationally much easier to plan out a static price calendar in advance.

We investigate the efficacy of static control policies for revenue management problems whose optimal solution is inherently dynamic. In these problems, a firm has limited inventory to sell over a finite time horizon, over which heterogeneous customers stochastically arrive. We consider both pricing and assortment controls, and derive simple static policies in the form of a price calendar or a planned sequence of assortments, respectively. In the assortment planning problem, we also differentiate between the static vs. dynamic substitution models of customer demand. We show that our policies are within 1-1/e (approximately 0.63) of the optimum under stationary (IID) demand, and 1/2 of the optimum under non-stationary demand, with both guarantees approaching 1 if the starting inventories are large.

We adapt the technique of prophet inequalities from optimal stopping theory to pricing and assortment problems, and our results are relative to the linear programming relaxation. Under the special case of IID single-item pricing, our results improve the understanding of irregular and discrete demand curves, by showing that a static calendar can be -approximate if the prices are sorted high-to-low.

Finally, we demonstrate on both data from the CPG company and synthetic data from the literature that our simple price and assortment calendars are effective.

1 Introduction

We consider the following general revenue management problem. A firm has finite inventory of multiple items to sell over a finite time horizon. The starting inventory is unreplenishable and exogenously given, having been determined by supply chain constraints or a higher-level managerial decision. The firm can control its sales through sequential decisions in the form of accepting/rejecting customer requests, pricing, or adjusting the assortment of items offered. Its objective is to maximize the cumulative revenue earned before the time horizon or inventory runs out.

We consider the setting in which customer demand is distributionally-known and independent over the time horizon; this can be estimated from, e.g., the historical sales data of our partner consumer packaged goods (CPG) company. The literature has also considered other settings, where an unknown IID demand distribution (Besbes and Zeevi 2009, 2012, Agrawal et al. 2017) or an evolving demand process correlated across time (Araman and Caldentey 2009, Ciocan and Farias 2012, Ahn et al. 2019) must be dynamically learned, or where demand is adversarial (Ball and Queyranne 2009, Eren and Maglaras 2010). In our setting, the firm’s decision at one point in time has no impact on its estimate of the demand at another point in time, which is supported by our data (see Section 1.4 and Section 4.1 for further discussion). Instead, the time periods are linked by the inventory constraints, and the firm must trade off between revenue-centric decisions that maximize expected revenue irrespective of inventory consumption and inventory-centric decisions that maximize the yield from the remaining inventory.

Revenue-centric decisions tend to be myopic and maximize the sales volumes of the most popular items, while inventory-centric decisions tend to be conservative and charge higher prices or prioritize selling highly stocked items. Intuitively, the optimal control policy would make revenue-centric decisions when the overall remaining inventory is plentiful for the remaining time horizon, and inventory-centric decisions when the overall remaining inventory is scarce relative to the remaining time horizon.

However, not all companies have the infrastructure to query the state of the inventory in real-time or adjust their decisions instantaneously. In fact, in the case of our partner CPG company, prices must be negotiated with the brick-and-mortar retailers that sell their products. As a result, a price calendar for the year is planned in advance. On the one hand, this allows the CPG company’s management to estimate its promotional budget, make production plans, and coordinate logistics; on the other hand, this allows the retailer to make advertisements, estimate marketing budgets, and lay out shelf space and price labels accordingly.

Motivated by this problem, we analyze the performance of static policies, which must plan out all of the firm’s decisions (in this case, the price for each week) at the start of the time horizon (in this case, one year), in revenue management problems that are intrinsically dynamic, where the optimal control would adapt based on the inventory that remains for the time horizon. If an item’s inventory runs out before the end of the time horizon, then its shelf/catalog price is still marked according to the calendar, but no sales of that item can be realized, since its shelf at the brick-and-mortar retailer would be empty. We show that our static policies are effective on data provided by the CPG company. They are also structurally very simple and have performance guarantees comparable to their dynamic counterparts.

1.1 Models Considered

We consider the time horizon to consist of a discrete number of time periods. This does not lose generality, since a continuous time horizon can be modeled by the limiting case in which the time periods are arbitrarily granular. Similarly, we model each item as having discrete “price points” at which it could be sold. This allows us to both approximate a continuous price range and capture situations where fixed price points have been predetermined by market standards. As is common for many retailers, our CPG company typically chooses prices that end in $.99 (e.g. $15.99, $16.99, $17.99, $19.99). Due to menu costs (Mankiw 1985, Stamatopoulos et al. 2017), such a price ladder is rarely changed.

We will separately consider the following two demand models because the design of effective policies differs significantly between them.

-

1.

Stationary (Section 2.3): the demand distribution for a specific decision, e.g. the purchase probability associated with price , is identical for all time periods .

- 2.

We will also consider two types of decisions made by the firm.

-

1.

Pricing (for a Single Item): There is a single item with a discrete starting inventory. We are given, for each time period and each feasible price , the probability of earning a sale if price is offered during period . The goal is to plan the price to offer during each period , with no sales occurring if inventory has stocked out.

-

2.

Assortment (and Pricing): There are multiple items each with a discrete starting inventory. We are given, for each time period and each assortment of items that could be offered (as well as corresponding prices), the probability of selling each item in during period . The goal is to plan out the assortment of items (and prices) to offer during each period , with no sales occurring if the customer chooses an item that has stocked out.

If the assortment problem includes pricing, then it captures the pricing problem with a single item.

Our results also generalize to the fractional-demand setting, where the demand distribution given for each period and price is over the continuous interval [0,1] (after normalizing), and the sales in the period equal the minimum of the realized demand and remaining inventory. The generalization to -demand gives us considerable modeling power. The dynamic pricing literature (e.g. see Gallego and Van Ryzin (1994), Talluri and Van Ryzin (2006), den Boer (2015), Bitran and Caldentey (2003), Elmaghraby and Keskinocak (2003)) has focused on the case of Bernoulli demand because the firm can control the price with arbitrary granularity and hence ensure that at most one sale occurs during any “time period”. However, in the case of our CPG company, they can only control prices at the week level, during which the demand distribution can range anywhere from a few hundred to a few thousand units. We will apply the generalization to [0,1]-demand on the data provided by the CPG company in Section 4.1.

1.2 Differences between Our Static Policies and Existing Policies

In this paper, we use the term “static” to describe a policy that prescribes a deterministic pricing and/or assortment decision for each period at the very start of the time horizon. Therefore, the decisions of the static policy must be independent of the sales that end up being realized. Should an item that the calendar planned to offer be out of stock, we distinguish between two models for how customers behave.

-

1.

Static Substitution: customers still see the same marked prices (and assortments), but if a customer would have chosen an out-of-stock item, then no sales are realized.

-

2.

Dynamic Substitution: customers only see the calendar-planned items with remaining inventory at the time. They never choose an out-of-stock item, and may or may not substitute to another in-stock item.

This distinction is irrelevant for the dynamic policies previously studied in the literature, since they can be changed on-the-fly to never offer an out-of-stock item.

Our static policies are based on deterministic linear programs (see Section 2.1.1 for details), which can be formulated for a given problem instance (items, inventory, prices, and demand distributions) in advance, and hence be used to derive static policies. At a high level, the LPs use deterministic values to approximate the random execution of a policy, and we can use its optimal solution as a “guide” in designing actual policies.

Such an LP was first used for the single-item pricing problem under stationary demand in Gallego and Van Ryzin (1994), who show that the LP will suggest a single price to offer, and hence a static policy. A recent paper by Chen et al. (2018) also proposes a similar single-price policy in the face of strategic customers, that achieves the same guarantee. However, this single-price policy requires the critical assumption that the demand, as a function over a continuous price range, is regular111 The regularity assumptions (Assumptions 7.1, 7.2 and 7.3 in Talluri and Van Ryzin (2006)) require the demand function (as a function of price) to be strictly decreasing and continuously differentiable and require the revenue function (as a function of demand) to be concave. However, in practice, demand functions are usually not regular. See Figure 5.2 from Talluri and Van Ryzin (2006). . In the general setting with irregular demand or a demand function over discrete price points, the LP will suggest two prices, in which case Gallego and Van Ryzin (1994) develop a policy that adaptively switches between them.

By contrast, we show that it is always better to switch from the higher suggested price to the lower suggested price, and furthermore, we show that a static switching point can be computed in advance based on the LP. The original dynamic pricing policy of Gallego and Van Ryzin (1994) allows the two prices to be offered in either order, but we show that if the policy must be static, then only the high-to-low ordering of prices is effective.

Moving to non-stationary demand, we can no longer directly follow the LP solution. In fact, we may want to modify certain decisions suggested by the LP to ensure that sufficient inventory is “reserved” for higher-revenue time periods (see Example 2.6 in Section 2.4.1). To accomplish this, we introduce a bid price for each item , which can be interpreted as the opportunity cost of a unit of item ’s inventory. Policies based on bid prices are common in revenue management, and bid prices which vary with the time can be derived using the approximate dynamic programming techniques in Adelman (2007), Rusmevichientong et al. (2020). By contrast, our bid prices are time-invariant and reflect the aggregate value of item over the non-stationary time horizon. This may be easier for managers to interpret, and also shows managers that an aggregate forecast of demand over the time horizon is sufficient for determining effective bid prices, if we translate those bid prices into a policy appropriately.

Our static policy is to take the LP solution, remove from the suggested assortments all instances where an item is offered at a price less than , and then follow a de-randomized version of the modified solution. We essentially treat as an acceptance threshold. Our policy is similar to those of Wang et al. (2015), Gallego et al. (2016), in that it imitates the LP solution and independently determines for each item when to discard it from the assortment. However, our discarding rule is static and based on our fixed time-invariant bid prices , whereas their discarding rule is dynamic and based on the realized inventory levels.

1.3 Performance Guarantees and Analytical Techniques

Lower bounds on the performance of static and dynamic policies. Our new results are bolded. \updown Dynamic Policies Static Policies \updownStationary Demand \updownSingle-item Pricing/Assignment [Gallego and Van Ryzin (1994)] [Theorem 2.2] \updownAssortment (and Pricing) [Liu and Van Ryzin (2008); Theorem 2.2] \updownNon-stationary Demand \updownSingle-item Pricing/Assignment [Wang et al. (2015)] [Rusmevichientong et al. (2020); \updownAssortment (and Pricing) [Gallego et al. (2016)] Theorem 2.7] \updownNon-stationary Demand \updownSingle-item Pricing/Assignment [Wang et al. (2015)] [Hajiaghayi et al. (2007); Theorem 2.9] \updownAssortment (and Pricing) [Gallego et al. (2016)] [Theorem 2.9] Note: refers to the amount of starting inventory (or the smallest starting inventory, if there are multiple items).

We establish performance guarantees for our static policies which, in many cases, improve existing guarantees even for dynamic policies. All of our guarantees are ratios relative to the optimal LP objective value, which is an upper bound on the performance of any static or dynamic policy. Generally, these LPs are useful because they portray a relaxation of the optimal policy, and hence an optimal LP solution can be used as a “guide” in designing a policy for the corresponding problem. In this paper, we will focus on converting the LP solution into a static policy.

Our results are outlined in Table 1.3. The baseline performance ratio is for stationary demand and for non-stationary demand. That is, our static policies always earn at least 50% of the optimum in expectation, with the ratio improving to if the given demand distributions are stationary. Both of these ratios are tight. The ratios also increase to 100% as , the starting inventory level when demand has been normalized to lie in [0,1] (or in the assortment setting, the minimum starting inventory among the items), increases to .

In the stationary-demand pricing problem, Gallego and Van Ryzin (1994) derived both the lower bound of and an asymptotic-optimality result. However, their policy is in general dynamic, unless the demand function is regular over a continuous interval – the concavity assumption allows for a single price in the LP. By contrast, we show that the same results can be obtained using our high-to-low static policy, regardless of demand regularity. Additionally, in our analysis, we derive the tightest possible bound for every value of and (the number of time periods), which allows us to establish asymptotic optimality in only (instead of scaling both and ).

In the stationary-demand assortment problem, we analyze the policies originally proposed by Liu and Van Ryzin (2008) and obtain the same bounds as above that are tight in both and . To our knowledge, this type of result, which includes the baseline lower bound of when starting inventory is 1, has been previously unknown222 The results in Golrezaei et al. (2014) imply performance guarantees for our problem, but their ratios are smaller than ours, since they are designed to hold under the more general setting of adversarial demand. Under this demand model, they only obtain a -guarantee under the additional assumptions that each item has a single price, and that starting inventories are asymptotically large. for the assortment problem. Asymptotic optimality was previously derived by Liu and Van Ryzin (2008) when both and .

Moving to non-stationary demand, the lower bound of 1/2 which improves to 1 as has been previously established using dynamic policies, in the assignment problem of Wang et al. (2015) and the more general assortment problem of Gallego et al. (2016). We establish the same bounds using static policies, with an extremely simple analysis based on prophet inequalities from optimal stopping theory. However, our convergence rate of is worse than the rate of achievable with their dynamic policies.

We should mention that the lower bound of 1/2 for static policies under non-stationary demand was also recently established by Rusmevichientong et al. (2020). Their bound and analysis differ from ours in that theirs are relative to the optimal dynamic policy instead of the deterministic LP relaxation. One benefit of using the LP is that it directly extends to the fractional-demand setting, since the LP does not change when demand can take any value in [0,1], which is our application of interest with the CPG company. By contrast, their framework is designed for a very general setting where resources can be reused after a random amount of time. We numerically compare the performance of their policy in Section 4.2.

1.4 Application on Data from CPG Company

We use aggregated weekly sales data from a CPG company to validate our model, and test the performance of our proposed policies. We use random forest to build prediction models that suggest demand distributions (normalized to lie in [0,1], possibly fractional numbers) under different prices. Then we take these distributions as inputs, and numerically compare the performance of our policies to some basic benchmarks.

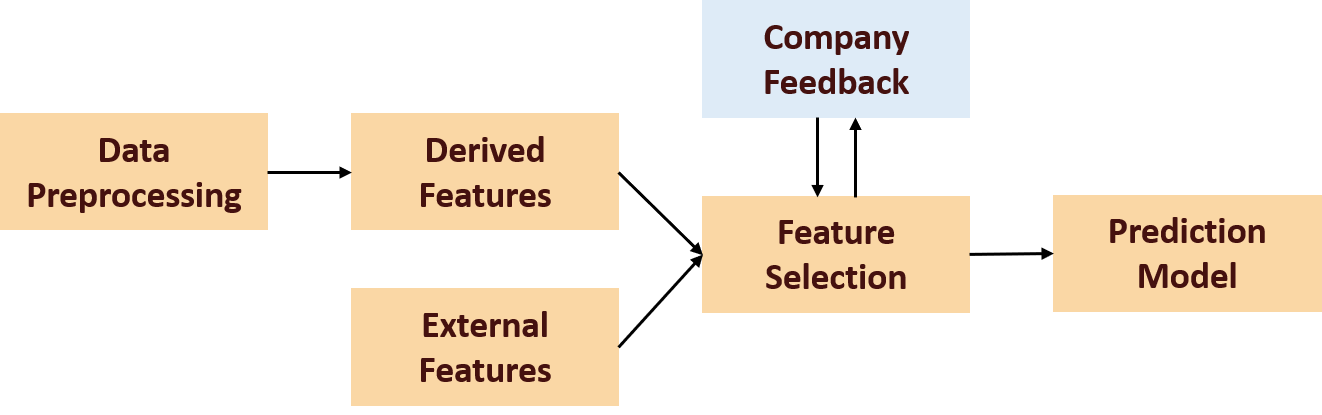

Working together with the CPG company, we used the work flow depicted in Figure 1 to build our demand model. The average out-of-sample percent error in its sales predictions is 19.41%. It is worth highlighting the features selected by the random forest: the tagged price, external competitor prices, and some external features such as seasonality. However, neither internal competitor prices (the prices of other SKUs of the CPG company) nor historical prices were selected. This observation validates our model in the following two aspects: internal competitor prices not being selected suggests that we can separately optimize the price calendar for each item; historical prices not being selected suggests that demand can be modeled as independent over time. The latter aspect is also validated by a stream of empirical literature on the “pantry effect” (Ailawadi and Neslin 1998, Bell et al. 1999), which observes for various consumable goods that if customers attempt to stockpile it when the price is low, then they will untimately consume it more quickly; hence, the low price did not necessarily cannibalize future demand.

Optimizing the price calendar based on our demand model, we find that for scenarios where the starting inventory is of moderate size compared to the total expected demand (i.e., for SKUs that were initially neither overstocked nor understocked), our static policies outperform basic LP-based static policies by 5% under stationarity and 1% under non-stationarity. Furthermore, our static policies lose at most 1% under stationarity and 4% under non-stationarity, compared to the optimal dynamic policies.

Both our theoretical guarantees and computational experiments suggest that static calendars perform nearly as well as their dynamic counterparts. Managers will not lose much from planning a sequence of prices / assortments in advance.

1.5 Related Work

Our 1/2 guarantee for the general assortment and pricing problem under non-stationary demand (and small inventory) is motivated by prophet inequalities, which provide an elegant method for bounding the performance of online vs. offline algorithms (see Samuel-Cahn et al. (1984), Kleinberg and Weinberg (2012)). The basic idea is to compute a threshold price for each item, based on the offline solution, such that either we are satisfied if an item sells out at its threshold price; or, if it does not, we are still satisfied from having had the opportunity to offer that item to every customer. Using prophet inequalities, there are very general results for maximizing welfare in online combinatorial auction settings (Feldman et al. 2014, Dütting et al. 2017).

However, to the best of our knowledge, it is important for these techniques that the objective is welfare, where the decision maker earns a reward equal to the sum of revenue and customer surplus generated. When the objective is revenue alone, elegant connections have been made for the single-parameter domain (Chawla et al. 2010, Correa et al. 2019), which hold under multiple settings including different arrival orderings. Our work is the first to make the connection to revenue maximization for assortment optimization under substitutable choice models, which is essentially a multi-parameter domain. The result is a simple and elegant 1/2 guarantee for assortment and pricing relative to the well-studied linear programming based upper bound, which holds without any assumptions on inventories being large or customers having identical willingness-to-pay distribution. The fact that our thresholds and guarantee are relative to the upper bound is also novel. The aforementioned literature has focused on comparing against the expected value of a “prophet” who knows the realized valuations in advance (a weaker benchmark than the LP).

We also compare our model in which demand is stochastic and distributionally known, to the models in which demand is completely unknown, or adversarial. One of the benefits of the adversarial model is that it does not rely on correct “forecasts” of demand over time. However, the drawback is that the resulting algorithm does not make use of forecasted demand information. Starting with the online booking problem of Ball and Queyranne (2009) in which the decision concerns whether to accept or reject each customer, single-item pricing (Eren and Maglaras 2010, Ma et al. 2018a), assortment optimization (Golrezaei et al. 2014), and joint assortment and pricing (Ma and Simchi-Levi 2017) have all been studied under the adversarial demand model.

The guarantees relative to the optimum are worse than ours, because we have more demand information—in fact, in all of the settings except Golrezaei et al. (2014), the papers resort to instance-dependent competitive ratios because a universal non-zero guarantee is impossible when inventories can be depleted at multiple potential prices. These papers have also tested the empirical performance of their algorithms on datasets and found that using a hybrid strategy (as proposed by Mahdian et al. (2007)) which employs the algorithms from both the adversarial and stochastic demand models performs best. This suggests that our algorithmic improvements in the stochastic demand model are valuable even if the given demand distributions are not 100% correct.

1.6 Outline

In Section 2.1 we define our basic problems and state the assumptions. In Section 2.2 we discuss some generalizations and their required assumptions. In Sections 2.3 – 2.5, we introduce randomized policies in stationary demand, non-stationary demand, and non-stationary demand with large inventory, respectively. Then, in Sections 3.1 and 3.2, we introduce general sampling-based de-randomization methods, and structural de-randomization methods, respectively. These de-randomization methods yield deterministic calendars that (i) have the same theoretical guarantees, (ii) significantly improve computational performance, and (iii) are much easier for companies to accept. Finally, in Sections 4.1 and 4.2, we conduct numerical experiments using real data provided by the CPG company, and synthetic data from the literature. We also introduce how we estimate the demands from the data in Section 4.1.

2 Problem Definitions and Performance Guarantees via Randomized Static Policies

2.1 Problem Definitions

Let and denote the positive and non-negative integers, respectively. For any positive integer , let .

A firm has items to sell over a finite time horizon of time periods. Each item is endowed with units of starting inventory, which is unreplenishable. We assume that , which does not lose generality since at most one unit of any item can be sold during any time period. Let denote .

The firm can offer each item at one of prices, , which are positive real numbers. We will refer to each item-price combination as a product, in which case the general assortment and pricing problem can be described as offering a set of products to each customer.

We let be any downward-closed333A family of subsets is downward-closed if for any and , we also have . family, which can be used to capture both physical constraints such as shelf-size limitations and business constraints whereby certain items cannot be offered at certain prices (or the same item cannot be simultaneously offered at multiple prices in the form of different products). We allow for a constraint on the sets of products that can be feasibly offered, imposing that they must lie in some family of subsets of . We will refer to elements in as assortments.

A static policy is a calendar that must be fixed at the start, prescribing the assortments to offer over the time horizon. In this section, we allow this calendar to be determined in a random fashion at the start. After this calendar has been fixed, sequentially over time , customer arrives and chooses to purchase at most one product from assortment . For the situation in which some of the products in the planned assortment have had their items stock out before time , we distinguish between two models for how customers choose:

-

1.

Customer always sees all of the products in , and if her first choice from has stocked out, no sales are realized (static substitution);

-

2.

Customer only sees the products in that are still in stock444Since is downward-closed, it is guaranteed that this selection of products seen by the customer is still feasible. Furthermore, , the empty set is always allowable., and chooses her favorite product from this selection (dynamic substitution).

We note that dynamic policies, as traditionally studied in the literature, do not need to distinguish between static vs. dynamic substitution, since they can decide the assortments on-the-fly to never offer an out-of-stock item (Rusmevichientong et al. 2020). By contrast, for static policies, both models can be justified. Static substitution occurs in parking systems, where customers are often shown “phantom” parking spots, only to drive there and discover that the spot is occupied (Owen and Simchi-Levi 2017). On the other hand, dynamic substitution occurs if customers switch to a different product when they see that the shelf for their favorite product is empty (Anupindi et al. 1998, Mahajan and Van Ryzin 2001, Honhon et al. 2010, Goyal et al. 2016). One factor that possibly reduces the prevalence of dynamic substitution is brand loyalty, under which customers commit to a favorite brand at the supermarket and make no purchase if that brand has stocked out (Jacoby and Kyner 1973, Amine 1998, Roehm et al. 2002). For product categories where brand loyalty is less common, dynamic substitution is more common.

In either case, for all , , and , we let be the probability of customer choosing product when she sees assortment . Note that for all and , where denotes the probability of customer purchasing nothing when she sees assortment . If , then . If the choice probabilities are equal across , for all assortments and , then we say that demand is stationary. If so, we omit the subscript and refer to the choice probabilities as .

2.1.1 Choice-based deterministic linear programs.

Any (static or dynamic) policy for the assortment problem can be captured by the following LP: let represent the probability of offering assortment at time .

| (1) | |||||

| (2) | |||||

| (3) | |||||

| (4) | |||||

Constraints (2) ensure that total units sold will not exceed the initial inventory, in expectation; constraints (3) ensure that only one price can be chosen in each time period. Note that we can assume equality in constraint (3) because (being downward-closed) always contains the empty assortment ; hence, we can increase until equality is achieved.

When demand is stationary, we let represent the probability of offering assortment at any given time period. Constraints (3) are then equivalent to the single constraint (7).

| (5) | |||||

| (6) | |||||

| (7) | |||||

| (8) | |||||

We derive performance guarantees for our policies, which are based on the deterministic LPs, relative to the optimal objective values of those LPs. This also provides a performance guarantee relative to the revenue of any dynamic policy, which is upper-bounded by the LP objective value—this is a well-known type of result in revenue management.

Lemma 2.1 (Gallego and Van Ryzin (1994), Gallego et al. (2004))

The expected revenue of any (static or dynamic) policy for the assortment problem is upper-bounded by the optimal objective value of CDLP-N from (1) when demand is non-stationary, and CDLP-S from (5) when demand is stationary. Analogously, the expected revenue of any policy for the single-item pricing problem is upper-bounded by the optimal objective value of DLP-S from (14) in Section 3.2.

Hereinafter, we will always use the LP objective value as our optimum and denote it using , where the distinction between the LPs will be clear from the context.

The following mild assumption is required for some of our results. It originated from Golrezaei et al. (2014) and has been nearly omnipresent in the subsequent literature on inventory-constrained assortment optimization (Gallego et al. 2016, Chen et al. 2016, Ma and Simchi-Levi 2017, Rusmevichientong et al. 2020, Ma et al. 2018b, Cheung et al. 2018). {assumption} For all , , , and , we have . This assumption states that the probability of selling a product can only be improved if it is offered as part of a smaller assortment instead of a larger assortment . The condition on the choice probabilities is often called substitutability. It is implied by any random-utility choice model (e.g., the multinomial logit choice model used in our computational study in Section 4.2), which treats the products as substitutes.

2.2 Generalized Model with Multi-Consumption and Fractional Consumption

Before stating our results, we describe a generalized version of the model from Section 2.1 that allows for multiple products, as well as fractional amounts of a product, to be consumed in the same time period. This generalization is natural if we interpret each as a larger-scale epoch (e.g., one week in the case of our CPG company) instead of the choice made by a single customer.

2.2.1 Multiple purchases.

We first consider the generalization where a customer can choose multiple products (but still demands exactly 1 unit of each product chosen). This requires the following modifications to the model from Section 2.1.

We are now given the joint distribution for the set of products demanded, when any assortment is seen by any customer . We assume that the set demanded never contains two different products corresponding to the same item , so that even when there is only one unit of in stock, there is no ambiguity about whether or is purchased.

Note that this assumption can be enforced by restricting to not contain any assortment that simultaneously offers different products corresponding to the same . Such a restriction is natural if the only difference between products and is in price ( vs. ), in which case it is nonsensical to mark item at multiple prices.

The demand is said to be stationary if the distribution of the set of products demanded is identical across for all assortments . The definitions of Assumption 2.1.1 and the CDLPs remain unchanged if now represents the marginal probability of product being demanded when assortment is seen by customer .

2.2.2 Fractional demand consumption.

The further generalization where demand can be fractional (for multiple products) requires the following further modifications to the model.

We are now given the joint distribution for the quantity of each product demanded, when any assortment is seen by any . We assume that this is a joint distribution over , where we have normalized the sales of any item within a time period to lie in (and scaled its prices accordingly). We now allow the starting inventories to be any real numbers that are at least 1. We can assume a lower bound of 1 because any item with can have its demand scaled up by so that the maximum possible sales during a time period is 1.

When demand can be fractional, we assume that the joint distribution of demand only depends on the assortment shown, not the exact quantity of each product available. As a result, we assume static substitution when demand can be fractional. Under static substitution, for each , , and , let be the CDF function for the quantity of product being demanded, should assortment be offered during time . is given and known. As before, demand is said to be stationary if the joint demand distribution is identical across time. In this case, . The definitions of Assumption 2.1.1 and the CDLPs remain unchanged if now represents the expected quantity of product demanded when assortment is shown at time .

We state one final assumption that is required for our result under stationary demand, only when demand can be fractional. This assumption is again very mild, in that it automatically holds for {0,1}-demand, which is the case studied in all of the existing literature. We have to add it as a technical assumption in the setting of [0,1] demands. Whereas we do not make any assumptions (e.g. concavity) on the demand distributions themselves, this assumption concerns the relationships between the different CDF’s for the different prices. {assumption} Let denote the marginal CDF for the quantity of product demanded when assortment is shown at time . For all items , feasible assortments , and prices with , assume that for all ,

The intuitive explanation of Assumption 2.2.2 is that for any amount of remaining inventory for item , the fraction of un-truncated demand sold is greater at the higher price . Assumption 2.2.2 can be seen as a weaker version of a stochastic dominance assumption on the hazard rates of the distributions . We provide examples and detailed discussions in Section 7 in the appendix.

2.3 Stationary Demand

2.3.1 Statement of results.

Our assortment policy probabilistically follows the LP solution, without specifically re-ordering the decisions portrayed in the LP.

This policy that probabilistically imitates the LP was originally studied by Gallego et al. (2004), Liu and Van Ryzin (2008), where it was shown to be empirically effective and asymptotically optimal. We now derive the first provable guarantees for it in the non-asymptotic setting, as well as a tight characterization of how the guarantee depends on both and .

Theorem 2.2

Under the static substitution model (with Assumption 2.2.2 needed if demand is fractional), for the assortment (and pricing) problem under stationary demand, if there are time periods and , then Algorithm 1 earns expected revenue of at least

| (9) |

where denotes a Binomial random variable consisting of trials of probability .

If we let denote the term from expression (9), then

| (10) |

which states that , and increases from to 1 as (regardless of ).

In Section 2.3.2 we sketch our proof technique for Theorem 2.2, and in Section 2.3.3 we show that our approximation guarantee of is tight for every value of and . But first, we demonstrate why Theorem 2.2 does not hold generally under the dynamic substitution model, and identify a special case when it does hold.

Proposition 2.3

The counterexample for Proposition 2.3 is detailed in Appendix 12. Nonetheless, the counterexample requires both multiple prices (i.e., item 1 that can be sold at multiple prices) and multiple items (i.e., a second item that “shields” the first item from being sold at the lower price) to exist. Theorem 2.2 holds in both of the canonical cases of:

-

1.

Single item, multiple prices (because with a single item, dynamic and static substitution are equivalent);

-

2.

Multiple items, single price per item (this is the pure assortment problem without pricing, as stated next in Proposition 2.4).

Proposition 2.4

2.3.2 Two-step proof sketch of Theorem 2.2.

The proof can be divided into two steps, which we will illustrate using the following example. Consider a problem instance with a single item, time periods and starting inventory . Suppose we have two prices. The higher price earns a sale with probability ; the lower price earns a sale with probability , i.e. deterministically. The optimal LP solution from (5) – (8) suggests to offer a higher price for 1.5 time periods, and a lower price for 1.5 time periods.

Let denote the expected revenue of a randomized policy that offers and each with probability one half in each period. Suppose, for the purpose of analysis, that there existed a virtual price with CDF . Note that . We then establish the following sequence of two inequalities:

| (11) | ||||

| (12) |

Inequality (11) relates the LP optimum to the expected revenue of a virtual calendar that always offers . We interpret the LHS as the expectation of some Binomial random variable truncated by initial inventory and the RHS as the expectation of an identical-mean, smaller-variance random variable that is also truncated by initial inventory. Although this virtual calendar cannot actually be offered (because the price never exists), it can bridge our analysis.

Inequality (12) is true under Assumption 2.2.2. If the demand is never truncated by the amount of remaining inventory, then offering the virtual price is equivalent to randomly choosing prices and each with probability one-half. However, if there is truncation, then Assumption 2.2.2 guarantees that the revenue from randomly choosing between the real prices and cannot be less.

2.3.3 Tightness of results.

We now show that the ratio produced in expression (9), which is dependent on and , is tight. The proof of Proposition 2.5 can be found in Section 11 in the appendix.

Proposition 2.5

For any positive integers and , there exists an instance of the stationary-demand single-item pricing problem with time periods and starting inventory, for which the expected revenue of any policy is upper-bounded by expression (9).

2.4 Non-stationary Demand with Small Inventory

In this section, we present our results for non-stationary demand with small inventory. Our results for non-stationary demand in the asymptotic regime will be discussed in Section 2.5.

2.4.1 Statement of results.

In contrast to stationary demand, under the more general setting of non-stationary demand, following the LP solution may be undesirable, because it may be beneficial to “reserve” inventory for the highest-revenue time periods. The following Example 2.6 demonstrates this idea.

Example 2.6

Let there be periods and unit of initial inventory. Let be some small positive number. Let there be two prices: . Let random demands be Bernoulli random variables. During day , the purchase probability of offering the higher price is ; and the purchase probability of offering the lower price is . During day , the purchase probability of offering both prices is .

| Prices | Period 1 | Period 2 |

|---|---|---|

DLP-N suggests that we offer in the first period, then in the second period. The objective value of DLP-N is . By simply using the DLP-N solution as a calendar, the expected revenue is . We can pick to be arbitrarily small and thus directly using LP can be arbitrarily bad. \Halmos

Nonetheless, we can still use the LP as a guide for our reservation policies.

| (13) |

Our assortment policy under non-stationary demand uses each cost as an acceptance threshold. We remove from the planned assortments all products of item being offered at prices below their thresholds. It is probable that the final is an empty set , even if is not empty, because we discard all the products from .

2.4.2 Proof sketch of Theorem 2.7.

By finding the assortment suggested by expression (13), each unit of item sold earns at least one-half of the per-inventory revenue of the corresponding , which is its contribution to the LP objective. Thus, if inventory runs out during the horizon, then we have earned in total at least one-half of the LP upper bound. If inventory never runs out, then the algorithm extracts the full “opportunity” from each time period which also results in at least one-half of the LP upper bound. In other words, setting one-half of the per-inventory revenue as an acceptance threshold is neither too high nor too low, and results in a “win-win” situation. This argument is based on the classical prophet inequalities from Krengel and Sucheston (1977), Samuel-Cahn et al. (1984), where we have modified their argument for optimal stopping to the pricing and assortment settings.

We outline two key steps here, and defer the details of our proof to Section 13 in the appendix.

-

1.

To evaluate Algorithm 2, we take out revenue earned from each period for each product . Since after the discarding rule, the prices should be no less than the threshold, i.e. . Thus, this difference should always be non-negative. That is,

where is an indicator if assortment was selected in period , before the discarding rule from Algorithm 2 was applied; the infimum between , the (random) remaining inventory of item at the end of period , and , the (random) quantity of product demanded, is the actual inventory of item sold in period .

-

2.

We relate the first triple summation term to CDLP-N, the deterministic linear program.

Then after canceling and re-arranging terms we prove the desired result.

2.4.3 Tightness of results.

We now show that the ratio in Theorem 2.7 is tight. It suffices to find an instance in the single-item pricing problem to show that the general result of assortments (and pricing) problem is tight. The proof of Proposition 2.8 can be found in Section 14 in the appendix.

Proposition 2.8

There exists an instance of the non-stationary demand single-item pricing problem for which the expected revenue of any policy is upper-bounded by .

2.5 Non-stationary Demand with Large Inventory

We present alternative policies for non-stationary demand that conduct “reservation” to a lesser degree than in Algorithm 2. Our policies have better performance if starting inventory is large, where the law of large numbers reduces the necessity of reservation, even under non-stationary demand.

We propose a different asymptotic regime from the literature Gallego and Van Ryzin (1997), Talluri and Van Ryzin (1998), Cooper (2002), to name a few. This is because traditional scaling requires and to scale up linearly, and under non-stationarity it is unclear how to scale the system. Instead of letting all and to scale up linearly, we allow for arbitrary dependence among and . This asymptotic regime is more of theoretical interests, and is sometimes used in the theoretical CS literature. Note that in practice, the number of initial inventory of different items may be significantly different, which might require some non-trivial normalization to fit into the standard asymptotic regime.

2.5.1 Statement of results.

In Algorithm 3, can be interpreted as the “reservation” probability, which decreases to zero as initial inventory increases. We reserve inventory by offering the empty set, which is always available. Note that Theorem 2.9 requires no assumption in the static substitution model.

Theorem 2.9

Under either the static substitution model or under Assumption 2.1.1 (substitutability), for the assortment (and pricing) policy where demand may be non-stationary, if , then Algorithm 3 earns revenue that is at least in expectation. In particular, Algorithm 3 is asymptotically optimal as the starting inventories approach infinity.

2.5.2 Proof sketch of Theorem 2.9.

Algorithm 3 scales the LP solution by a factor of , where is a small “reservation” probability. is selected to balance two factors. First, it is small enough such that if we never stock out, then earning is an asymptotically optimal ratio. On the other hand, is large enough such that we stock out with probability at most . This intuition is motivated by a tutorial of Anupam Gupta (Gupta 2009), where they introduced the original work of Hajiaghayi et al. (2007). We improve the bounds in the original paper, so that our bound only depends on , but not on . We also generalize to assortment and pricing problems with fractional-demand consumptions.

We outline two key steps here and defer the details of our proof to Section 15 in the appendix. The intuition is as follows: conditioning on the event that “inventory never runs out”, the expected revenue is at least fraction of the LP objective. Then, we show that this event happens with high probability.

-

1.

Lower bound the expected revenue by a multiplicative factor of the LP objective, i.e. , where is as defined in Algorithm 3.

-

2.

Using concentration of inequality, lower bound the probability that inventory never runs out, i.e. .

3 De-randomization Methods

In this section we introduce de-randomization methods, which yield deterministic calendars that (i) have the same theoretical guarantees, (ii) significantly improve computational performance (See Section 4.2), and (iii) are much easier to accept in practice.

Specifically, we first introduce a general de-randomization method in Section 3.1 that applies to any randomized static policy for joint assortment and pricing that we proposed in Section 2. Then we introduce two specialized de-randomization methods for Algorithms 1 and 2 when there is only a single item. These methods take advantage of the structural properties in the single-item pricing problem. The de-randomization methods are summarized in Table 3.

A summary of de-randomization methods \updown Single-item Pricing Multi-item Joint Assortment and Pricing \updownStationary Demand Theorem 3.5 (or 3.3) Theorem 3.3 \updownNon-Stationary Demand Theorem 3.11 (or 3.3) Theorem 3.3 \updownNon-Stationary Demand with Large Inventory Theorem 3.3 Theorem 3.3

3.1 General De-randomization Methods

In this section, we introduce a general simulation-based de-randomization method that achieves the same guarantee as any policy suggested by Algorithms 1–3 does. We consider the general assortment (and pricing) problem under non-stationary demand, which captures single-item pricing and stationary demand as special cases.

Any policy as suggested by Algorithms 1–3 that independently chooses the assortment in each time period, implies a distribution over static calendars, which can be characterized by the following vector:

where is the probability that we offer in period . Note there might exist such that because our policies could possibly suggest offering nothing in some periods. We will use the following example to illustrate our de-randomization procedure.

Example 3.1

Consider a three-period problem with three options . Note that is always available. Suppose that our randomized policy (possibly from Algorithm 2) is characterized by

This policy implies a distribution over static calendars such that it takes with prob. , with prob. , with prob. , and with prob. (because the assortments for and are drawn independently). The idea of our de-randomization method is to select one of them that garners the same expected revenue as the distribution of calendars does. \Halmos

In general, this distribution over static calendars has a finite but exponentially large support; computing the expected revenue of each calendar using brute force is impossible. Instead, our method identifies the best assortment to offer iteratively over , using simulation. Our method requires a simulator , whose source of randomness (e.g. the random seed) is characterized by . In each single run of the simulator, it randomly generates (i) a calendar of assortments , based on the probabilities suggested by , and (ii) a sequence of demands based on the choice models and the assortments on the calendar. Finally, the simulator calculates revenue based on the simulated assortments and demands. The simulator generates revenue from a bounded interval where is given.

If we query this simulator times, then we obtain an estimator of the expected revenue of policy . We can select to be a large number such that is close to via a concentration inequality. We specify our de-randomization method in Algorithm 4.

Example 3.2

(Example 3.1 Continued.) Let denote a randomized policy that offers and each with probability one half in the first period, offers and each with half-probability in the second period, and finally offers in the third period. Algorithm 4 first finds the better one between and . If the latter is better, in the second iteration it finds the better one between and . \Halmos

This idea of iterative de-randomization, when the support of the randomized solution is exponentially sized, has commonly appeared in the computer science literature (Motwani and Raghavan 1995). However, the need for a simulator to evaluate the assortments at each iteration and the analysis of how many samples are needed to lose at most in the final de-randomized solution are new to our paper, to the best of our knowledge.

We prove the following result, the proof of which is deferred to Section 16 in the appendix.

3.2 Single-Item Stationary Demand

We now introduce a specific de-randomization method for Algorithm 1 (the algorithm for stationary demand) in the special case of single-item pricing. While the generic de-randomization method from Section 3.1 will also suffice, the one presented here contains additional structural insights about the de-randomized calendar. Note that with a single item, dynamic and static substitution are equivalent.

We establish a structural property in Section 3.2.1 which shows that sorting the static calendar in order of high-to-low prices is dominating. We show that sorting in the opposite order (low-to-high) earns strictly less expected revenue, in Example 3.9 in Section 3.2.2. We also show that using only one price (without regularity assumptions) earns strictly less expected revenue, in Proposition 3.10 in Section 3.2.2.

In the single-item pricing problem, we have , and we will omit index . To be able to handle [0,1]-demand (instead of just {0,1}-demand), we require the following assumption. {assumption} For any , either , or , for all .

When demand is stationary, we have the following LP. For simplicity, we omit the infinite price, and we put an inequality instead of an equality in (16).

| (14) | |||||

| (15) | |||||

| (16) | |||||

| (17) | |||||

The LP for pricing under stationary demand has the following structure.

Lemma 3.4 (Gallego and Van Ryzin (1994))

Based on the above LP and the optimal structure from Lemma 3.4, we devise the following policy.

Our policy offers the prices in a high-to-low order, with a static switching point. Intuitively, the high-to-low ordering is desirable, because should we stock out early from higher-than-expected demand realizations, we would rather lose low-priced sales at the end.

Theorem 3.5

We prove Theorem 3.5 in the next section.

3.2.1 Structural property: monotonicity.

We begin by quickly establishing a structural property, Lemma 3.6, as a warm-up to the proof of Lemma 3.7, which is the key to the de-randomization in the single-item stationary demand setting. Let denote the price index for time in a calendar, and denote the optimal price index in a revenue-maximizing calendar. We use to describe the calendar, a vector of price indices. The structural property states the following:

Lemma 3.6

In any calendar , if two consecutive price indices are such that , then indices and can be exchanged in the calendar without decreasing its expected revenue.

The proof of Lemma 3.6 is deferred to Section 17 in the appendix. From this Lemma, we know that there exists an optimal static calendar, the prices of which are non-increasing over time.

Now we strengthen the monotonicity property in Lemma 3.6. Consider a problem instance with time periods and starting inventory . Suppose we have two prices. The higher price of earns a sale with probability ; the lower price of earns a sale with probability , i.e. deterministically. The optimal LP solution (according to Lemma 3.4) suggests offering a higher price index for 1.5 time periods, and a lower price index for 1.5 time periods.

We let denote the expected revenue of a randomized policy that offers in the first period, offers and each with probability one half in the second period, and offers in the third period. We define analogously.

The structural property states that if there is a positive probability that one policy offers a lower price before a higher price, then this policy can be improved. For example,

| (18) |

There is a positive probability that the policy does so, since there is already a 1/4 chance that it offers in period 1 and in period 2. However, the randomized policy could only lead to the calendars or ; in either case it always offers higher prices before lower prices. The conclusion of inequality (18) is that the first policy can be changed to the second policy without reducing revenue; note that the total expected number of periods that both and are offered is still the same (1.5 periods each).

We now formalize inequality (18). Let be the fractional part of a real number .

Lemma 3.7

Consider the following two policies:

-

1.

A policy that offers in each period the same probabilistic mixture of two prices, i.e. a probability of offering the higher price and a probability of offering the lower price;

-

2.

A policy that starts by deterministically offering the higher price for periods, then in the next period offers the higher price with probability and the lower price with probability , and finally switches to offering the lower price in the last periods.

The expected revenue of the second policy is no less than the expected revenue of the first policy.

3.2.2 Switching from high to low is necessary.

We show that switching from a higher price to a lower price is necessary, in the sense that if we switch from a lower price to a higher price, we may fail to achieve the bound by expression (9).

Example 3.9

Let there be periods and unit of initial inventory. Let there be two prices: . The corresponding purchase probabilities are . The LP suggests that we offer both and for exactly one period. The LP objective is

We calculate the bound in expression (9): it suggests a guarantee.

If we offer in period and then in period , this earns an expected revenue of , which is of the LP upper bound.

If we offer in period and then in period , this earns an expected revenue of , which is of the LP upper bound. \Halmos

This example demonstrates that switching from a lower price to a higher price is worse than the bound by expression (9), and it is even worse than the ratio. On the other hand, switching from a higher price to a lower price performs much better.

We also show that two prices are needed to obtain our results in Theorem 2.2. This is because we do not assume regularity assumptions. We state Proposition 3.10 here and defer its proof to Section 18 in the appendix.

Proposition 3.10

There exists an instance of the stationary-demand single-item pricing problem for which the expected revenue of any single price policy is strictly smaller than expression (9).

3.3 Single-Item Non-Stationary Demand

Analogous to Section 3.2, we now introduce a specific de-randomization method for Algorithm 2 (the algorithm for non-stationary demand) in the special case of single-item pricing.

When demand is non-stationary, we have the following LP. Let be the probability that we offer price in time .

| (19) |

In (19), can be interpreted as the per-inventory revenue of the LP. Algorithm 6 guarantees to sell inventory for at least half of this value, since at each time , it maximizes the expected profit with a bid price (opportunity cost) of . The intuition is that when there is only one item, we can treat the threshold as a bid price and maximize with respect to it to obtain a deterministic calendar. This de-randomization is because we use maximization instead of a discarding rule.

Theorem 3.11

For the single-item pricing problem where demand may be non-stationary, Algorithm 6 earns expected revenue at least .

4 Computational Study

4.1 Computational Study: Using Real Data from A CPG Company

We first describe the business model. Then in Section 4.1.1, we explain how we develop the prediction model from data. We discuss the details of feature selection in Section 4.1.2 and justify the motivation of our dynamic pricing model. In Section 4.1.3, we explain how we adapt the prediction model such that its output is consistent with managerial intuition and statistically effective. Finally, in Section 4.1.4, we explain the numerical performance under our proposed policies.

At the end of each year, the CPG company requires a price calendar to be planned for the next year. This calendar contains 52 weekly prices for each SKU. The CPG company then brings this calendar to its channels (e.g. supermarkets) to negotiate the price-to-customers (PTC). We assume that they are the same, since the CPG company has full bargaining power. After the calendar is delivered to channels, the channels decide their yearly advertising strategy, produce flyers, and make price tags. These are the reasons (e.g., long lead time on flyers) why we need to plan a calendar in advance. Customers will not see the prices until the channels release their prices, so there is no anticipatory behavior.

4.1.1 The random forest model.

In this section we explain in detail how we develop the prediction model from the data. We will follow the workflow shown in Figure 1 from Section 1.4.

We begin with weekly sales data in the past 3 years. After cleaning the missing data, we select SKUs that generated 90% of the revenue in the past three years and eliminate the rest. We also eliminate SKUs that were newly introduced in the most recent year. Some SKUs are already grouped together by the company. They are similar brands sold at similar pack sizes. The company requires that all SKUs in the same group be sold at the same price. There are 52 distinct groups in total. We build group-specific prediction models with the same combination of features, i.e., all SKUs use the feature “tagged price”, but it refers to a different tagged price for each SKU.

We derive a list of features from the data that will be used to predict demand at each time step. These features include the price that this group is tagged at, its internal competitor prices, its external competitor prices, and its history prices. The internal competitor prices are the prices of the brands owned by the same company. The external competitor prices are the prices of its true competitors, owned by its rival companies. The features of history prices are take from the past week to the past 3 weeks, as 3 different features.

The external features include industry seasonal trend (after applying moving average), total number of stores in the district, festivals and sports events. The first two features are provided by the company, and the rest are obtained by scripting from the Internet. We create dummy variables for festivals and sports events to characterize categorical data.

Different combinations of features, and the resulting out-of-sample error rates. Tagged price ✓ ✓ ✓ ✓ ✓ Seasonal industry trend (after moving average) ✓ ✓ ✓ ✓ ✓ ✓ Total number of stores in the district ✓ ✓ ✓ ✓ ✓ Festivals and sports events ✓ ✓ ✓ ✓ External competitor prices ✓ ✓ ✓ ✓ ✓ Internal competitor prices (within brand) ✓ ✓ ✓ History prices ✓ ✓ Error rate (average over time periods and different SKUs) 32.21 21.07 21.09 19.47 19.41 19.80

We tested a few algorithms and finally choose to use random forest (Liaw et al. (2002), Ferreira et al. (2015)) as the prediction model. In Section 4.1.3 we will discuss an important challenge associated with random forest prediction and how it is addressed. We aggregate all the features together, then simultaneously perform feature selection and parameter tuning, by using a 5-fold cross-validation. Finally, the average prediction error is reported as 19.41%. This demonstrates a very good prediction model, compared with the number in Ferreira et al. (2015).

4.1.2 Feature selection.

In this section we explain how we select features. We validated our model based on the selected features, because this provides indications of the existence (or non-existence) of different sources of cannibalization effects. For example, if we identified a temporal cannibalization effect, which states that a promotion given today will take away future sales, then our model should address it. Fortunately, there are no such complications, as supported by the data.

In cross-validation, we evaluated each feature combination based on its median absolute percentage error (MdAPE) on the validation set. During this procedure, we engaged in rounds of discussions with the company to ensure that the features selected are interpretable. There are some sub-optimal combinations that the company believed would make more practical sense, and we followed their advice.

These features were both approved by the CPG company’s management as consistent with their expedience and also resulted in the lowest out-of-sample prediction errors — see Table 4.1.1 for the reported error rates. Each column depicts a combination of features, and the corresponding numbers are prediction errors under this feature combination. The first column serves as a benchmark. We omit some trivial duplicates of the same feature, but note that some rows represent many features, e.g., festivals and sports events.

The features that were ultimately selected include: the tagged price, external competitor prices555We do not know the true competitor prices, but we can use ARIMA (Hyndman et al. 2007, 2020), a time series model, to predict competitor prices; by substituting true competitor prices with predicted competitor prices we find the prediction accuracy evaluated on the testing set remains almost unchanged. Thus, we use predicted competitor prices instead of true competitor prices., and some external features. Note that this list includes neither internal competitor prices (from other SKUs of the CPG company) nor historical prices. We validate our model with the following two observations, which suggest that our model captures the real retail dynamics:

Cross-product cannibalization is not significant. A probable reason is that we have already grouped similar brands sold at similar pack sizes. This suggests that we can employ single-item calendar pricing without considering the joint optimization of simultaneously deciding all SKUs’ calendars.

Inter-temporal cannibalization is also not significant. This suggests that demands are not correlated across time, in alignment with our theoretical model. A good explanation of this observation is due to the “pantry effect” (Ailawadi and Neslin 1998, Bell et al. 1999). Even if customers stockpile a product during promotions, this accelerates their consumption rate. Thus, they ultimately purchase as much of the product in subsequent time periods as they otherwise would have, especially for products such as carbonated beverages and ice cream. Therefore, we model demands as independent across time.

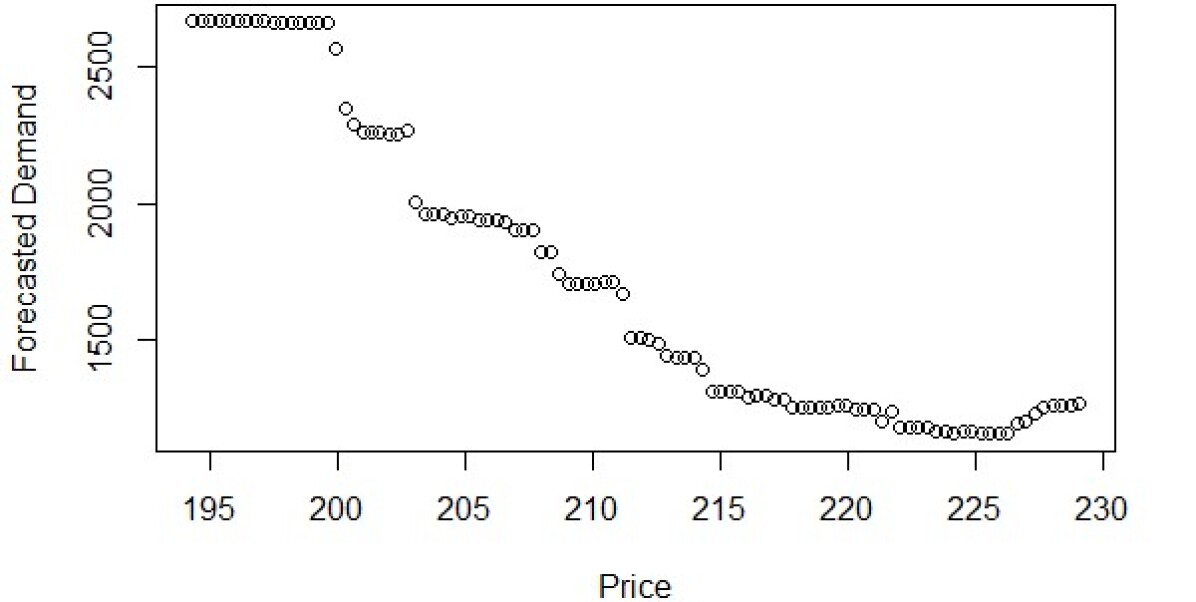

4.1.3 Monotone demand curve.

If we focus on the price-demand relationship, we observe that the direct output of random forest yields a non-monotone prediction. In Figure 2, the black dots show the predicted price-demand curve for one SKU in one week. There are occasions when the predicted demand has positive price elasticity, e.g. when price is between and . Since we are selling consumer packaged goods, there is no conspicuous leisure (Veblen 2017), and price elasticity should be negative. A non-decreasing demand curve is not acceptable to the CPG company from a managerial perspective. Theoretically, a non-decreasing demand curve might also (but not necessarily) violate Assumption 3.2.

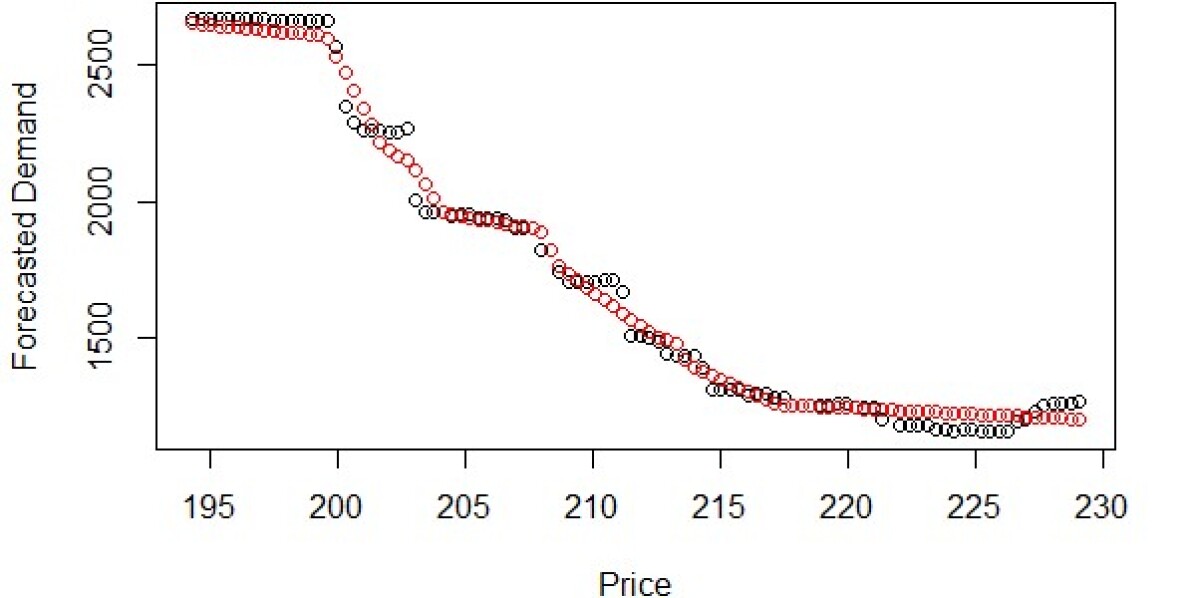

To solve this problem, we introduce curve fitting. First uniformly draw samples from the demand curve. Then fit a piecewise linear function, written as

parameterized by , where is the number of breakpoints, and are indicator functions equal to one if , zero if . We arbitrarily selected to be . Finally, we minimize the mean squared error over these sample points, with shape constraints enforcing a monotonic decreasing function.

We solve the above program using heuristics. The curve-fitting output is depicted in Figure 2 as the red dots. The accuracy is slightly improved from 19.41% to 18.66%. We do not view this improvement as tremendous, but we have built a model that is in greater agreement with managerial suggestions. Finally, a monotone demand curve666To be precise, we derive several scenarios for a specific SKU at a specific price to obtain a discrete distribution, and this suggests a monotone demand curve under each scenario. satisfies Assumption 3.2, as addressed in Section 3.2.

4.1.4 Computational performance of policies.

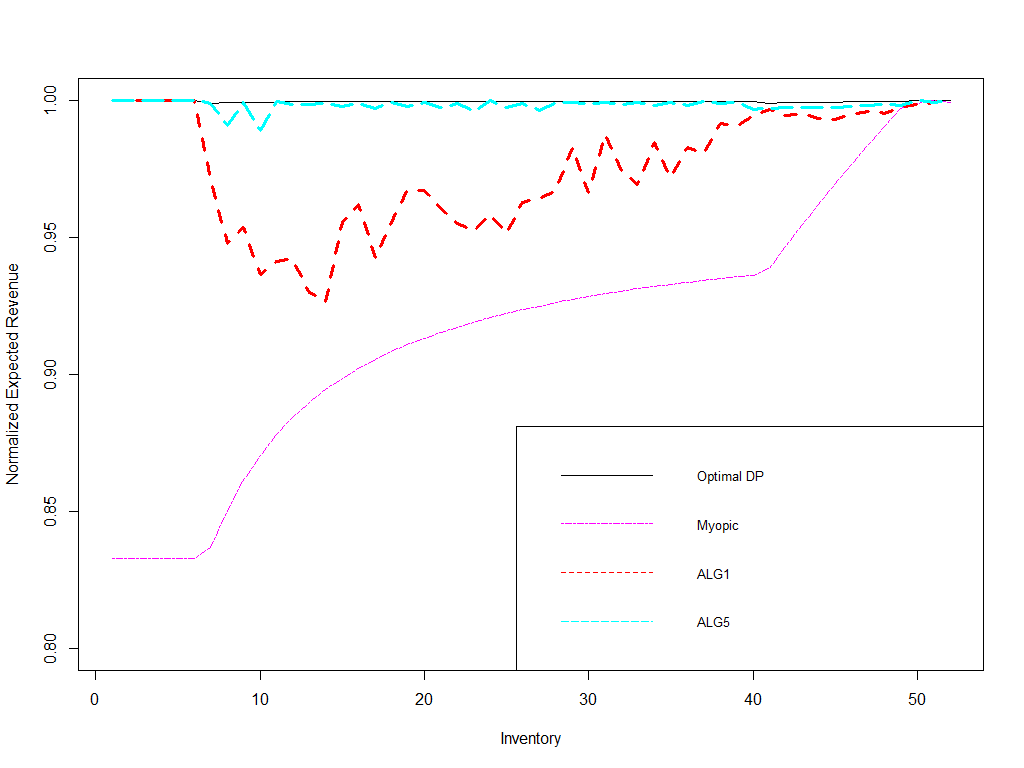

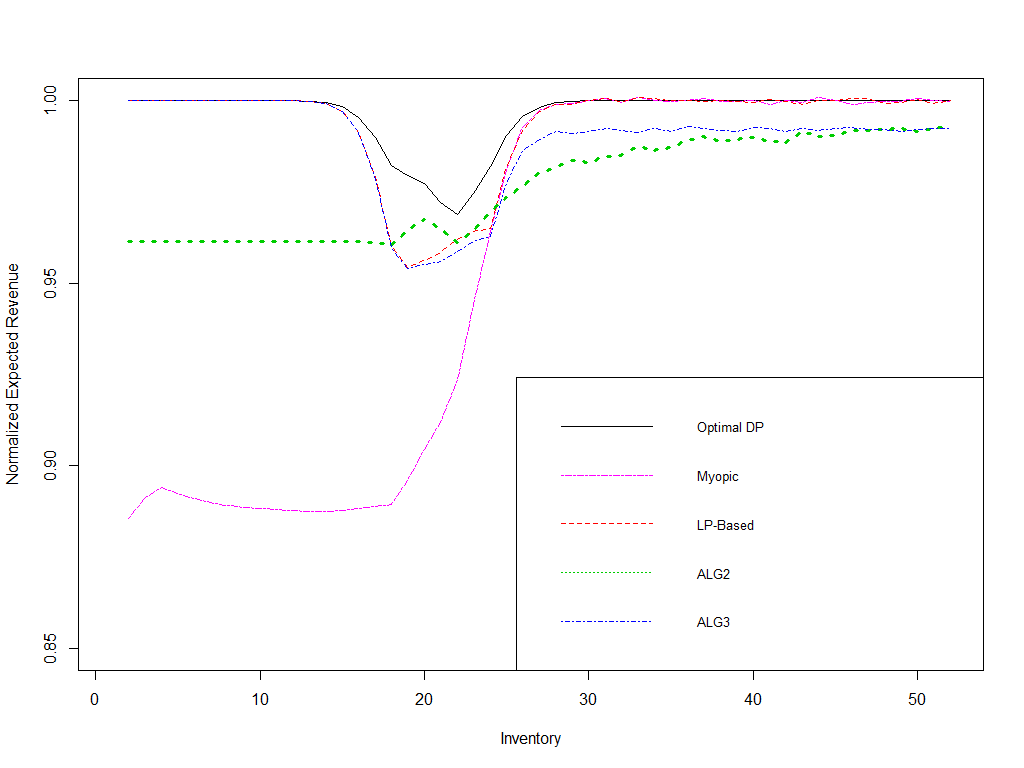

In this section, we take distributions obtained from the above sections as inputs and compare the performance of our policies to selected benchmarks. We fix the feasible price set for each SKU to be the prices from its historical data. The planning horizon is one year, weeks. We normalize demands to take values by dividing the predicted demands by the highest predicted demand. We consider different scenarios in which the starting inventory ranges from unit to units and analyze both stationary and non-stationary demand models.

We compute the expected revenue from our proposed policies (ALG1 from Algorithm 1 under stationarity, ALG2 from Algorithm 2 under non-stationarity, ALG3 from Algorithm 3 under non-stationarity, and ALG5 from Algorithm 5 the deterministic policy under stationarity), the LP upper bound, the Optimal DP for the policy solving the optimal dynamic program, the Myopic policy as one benchmark, and an LP-Based randomized policy as another benchmark. The results are shown in Figures 3 and 4, where we have divided all numbers by the corresponding LP upper bound, meaning that the performance ratio is always between and , with higher ratios indicating better performance.

For scenarios in which the starting inventory is of moderate size compared to the total expected demand (i.e. for SKUs that were initially neither overstocked nor understocked), our static policies outperform basic LP-based policies by 5% under stationarity and 1% under non-stationarity. Furthermore, our static policies lose at most 1% under stationarity and 4% under non-stationarity, compared to the optimal dynamic policies.

Note that in practice, it is rare for the initial inventory level to be very small or very large, since it would have been pre-optimized777Pre-optimized by some higher level managers, Talluri and Van Ryzin (2006). to sell out exactly. When inventory is of moderate size, our policies outperform the existing benchmarks under both stationary and non-stationary demand settings.

In fact, if we consider the prediction model, the expected demand is approximately on each day under different prices, which corresponds to the dip when inventory is around . If we divide them by the time horizon of weeks, we see that the expected units sold per week roughly meets the expected (normalized) demand of . This is the region where the pricing problem is non-trivial in theory, and most common in practice. When the inventory level is such that the problem falls into degenerate cases, all the curves are close to the LP upper bound. This moderate inventory size corresponds to the moderate load scaling factor of , which is the ratio between initial inventory and mean demand in the admission control problems originated from Zhang and Cooper (2005).

4.2 Computational Study: Using Synthetic Data from Literature

In this section, we study the joint assortment and pricing problem, using synthetic data that are commonly adopted in the choice-based deterministic linear program literature, such as Zhang and Cooper (2005), Liu and Van Ryzin (2008), Gallego et al. (2016).

We closely follow their numerical setup. Let there be three items, each of which can be consumed fractionally. The items have initial inventory proportional to . We will later normalize initial inventory by a load scaling factor . Each item has two prices to be offered, high and low. We fix the low prices and let the high price to change from . We also denote these prices as and .

We specify a choice model to be adopted in our computational study. It is an adaption from a mixture of MNL models (see, e.g., Li et al. (2018), McFadden and Train (2000)). However, we interpret the choice probabilities as purchasing market shares, which are between [0,1]. The choice model can be explicitly written as follows

where we adopt the fashion that . The randomness in this model comes from the coefficients in the front of each single MNL model. We let and be Bernoulli random variables. The mean values and are given for any .

In our computational study, we distinguish between a stationary setting and a non-stationary setting. In both settings, . In the stationary setting, . In the non-stationary setting, . We also specify the attractiveness vectors as . We test four different no-purchase vectors to be .

In Tables 4.2–4.2, LP UB stands for the corresponding DLP upper bounds; Myopic stands for the myopic policy that offers the assortment that gives the highest expected revenue, regardless of inventory; LP-Sol stands for the CDLP benchmark, which first solves the LP, then directly uses the optimal solution to implement a (randomized) policy; ALG2 and ALG3 stand for the policy suggested by Algorithm 2 and Algorithm 3, respectively; RST17 stands for the static policy suggested by Rusmevichientong et al. (2020), by considering the extension in their Section 5.2; and DeRLP, DeR2, and DeR3 stand for our de-randomization method from Algorithm 4 applied to the LP-Sol, ALG2, and ALG3, respectively. All of the percentages are relative to the LP upper bound.

Computational performance in the stationary setting LP UB Myopic LP-Sol RST17 DeRLP LP-UB Myopic LP-Sol RST17 DeRLP (0,0) (1,5) 0.6 4300.0 67.76% 74.51% 81.79% 82.19% 3800.0 71.15% 80.15% 86.62% 85.50% 0.8 5200.0 71.28% 80.27% 83.55% 83.90% 4266.7 75.93% 87.41% 88.23% 90.11% 1 6050.0 71.95% 82.77% 81.27% 83.22% 4566.7 78.22% 92.74% 89.74% 92.53% 1.2 6100.0 79.70% 90.54% 89.17% 90.88% 4586.7 83.13% 95.04% 93.77% 95.87% 1.4 6150.0 84.42% 93.46% 92.13% 94.45% 4606.7 86.61% 95.26% 95.85% 97.63% (5,10) (10,20) 0.6 3200.0 91.67% 87.92% 89.54% 91.23% 2468.9 94.46% 92.80% 91.05% 90.81% 0.8 3466.7 94.28% 94.20% 90.97% 93.32% 2533.3 97.47% 97.33% 94.78% 97.33% 1 3500.0 97.37% 97.46% 95.29% 97.47% 2533.3 99.29% 99.35% 98.23% 99.35% 1.2 3500.0 99.14% 99.13% 98.00% 99.09% 2533.3 99.76% 99.81% 99.41% 99.87% 1.4 3500.0 99.86% 99.81% 99.28% 99.89% 2533.3 100.06% 99.92% 99.94% 99.96%

In the stationary setting, we observe from Table 4.2 that Myopic performs the best when inventory is too much, which is not surprising. LP-Sol and RST17 have similar performance. The de-randomization method from Algorithm 4 uniformly improves () on the randomized policy in most scenarios. It also has better performance than RST17 in most scenarios.

Computational performance in the non-stationary setting when the price difference is small LP UB Myopic LP-Sol ALG2 ALG3 RST17 DeRLP DeR2 DeR3 (0,0) 0.6 3936.0 53.76% 81.42% 81.37% 79.29% 84.13% 83.47% 83.40% 83.51% 0.8 4981.3 54.43% 84.65% 84.61% 82.34% 86.26% 86.80% 86.82% 85.39% 1 6026.7 54.50% 86.39% 86.41% 84.23% 84.16% 87.34% 87.59% 87.31% 1.2 6304.0 60.83% 87.17% 87.22% 84.94% 90.08% 89.72% 89.67% 89.60% 1.4 6581.3 66.59% 87.33% 87.38% 85.37% 90.58% 89.43% 89.37% 89.42% (1,5) 0.6 3696.0 65.96% 84.81% 84.75% 82.85% 87.85% 86.03% 85.93% 85.93% 0.8 4396.3 62.98% 91.80% 91.84% 88.75% 87.00% 91.67% 92.28% 92.23% 1 4535.0 66.91% 95.15% 95.16% 91.14% 92.00% 95.95% 96.02% 96.10% 1.2 4673.7 70.39% 94.91% 94.93% 91.38% 94.69% 96.12% 96.11% 96.11% 1.4 4765.1 74.26% 97.00% 96.87% 92.86% 95.20% 97.13% 97.21% 97.22% (5,10) 0.6 2862.7 84.17% 94.29% 94.16% 90.32% 85.83% 95.22% 95.19% 95.13% 0.8 3250.2 90.20% 94.56% 94.47% 90.77% 91.11% 95.50% 95.54% 95.45% 1 3633.9 90.88% 95.24% 95.17% 91.67% 93.20% 95.17% 95.14% 95.16% 1.2 3696.0 95.20% 97.20% 97.09% 92.92% 97.16% 97.50% 97.56% 97.55% 1.4 3730.3 97.96% 97.97% 97.92% 93.55% 98.16% 97.97% 97.85% 97.87% (10,20) 0.6 2364.1 92.34% 91.70% 91.80% 88.57% 92.83% 93.37% 93.37% 93.43% 0.8 2755.7 93.34% 94.63% 94.67% 91.17% 93.46% 95.07% 95.11% 95.08% 1 2878.3 96.58% 96.82% 96.83% 92.70% 96.52% 96.74% 96.65% 96.79% 1.2 2910.8 98.94% 98.97% 99.00% 94.40% 99.05% 98.98% 99.07% 98.99% 1.4 2910.8 99.92% 99.87% 99.87% 94.95% 99.88% 99.87% 99.90% 99.89%

Computational performance in the non-stationary setting when the price difference is large LP UB Myopic LP-Sol ALG2 ALG3 RST17 DeRLP DeR2 DeR3 (0,0) 0.6 48034.0 11.54% 70.38% 92.04% 69.82% 87.43% 84.06% 90.88% 90.49% 0.8 50745.3 13.99% 71.22% 91.36% 71.16% 87.03% 86.35% 91.99% 89.14% 1 53456.7 16.15% 71.47% 89.96% 72.49% 85.30% 74.28% 89.91% 88.36% 1.2 54176.0 18.91% 69.99% 87.80% 71.65% 92.07% 82.56% 87.56% 88.78% 1.4 54895.3 22.73% 69.25% 84.80% 71.21% 92.41% 74.46% 84.25% 91.03% (1,5) 0.6 36064.0 70.34% 67.26% 85.89% 68.89% 87.00% 71.36% 85.82% 87.97% 0.8 37835.7 70.06% 84.14% 83.66% 82.85% 84.41% 87.79% 83.59% 92.26% 1 38195.4 71.51% 87.89% 84.81% 85.54% 85.50% 91.34% 84.36% 93.34% 1.2 38555.0 72.62% 88.64% 86.90% 86.62% 86.30% 94.42% 86.22% 93.61% 1.4 38831.1 73.61% 88.88% 87.01% 87.21% 87.44% 91.94% 87.12% 94.16% (5,10) 0.6 28569.7 76.22% 88.32% 88.41% 85.89% 89.11% 90.74% 89.03% 93.34% 0.8 29574.9 87.57% 88.32% 88.39% 86.34% 88.44% 94.87% 88.65% 96.43% 1 30580.1 96.76% 88.94% 87.70% 87.03% 87.55% 95.67% 87.58% 95.06% 1.2 30758.5 98.52% 99.06% 89.08% 94.47% 89.45% 98.79% 89.46% 92.86% 1.4 30855.2 98.95% 99.30% 99.26% 94.26% 90.88% 99.25% 99.41% 97.83% (10,20) 0.6 21379.9 83.74% 88.02% 86.44% 85.86% 87.89% 94.24% 86.18% 91.16% 0.8 22275.8 97.58% 92.11% 86.74% 90.23% 87.44% 93.75% 87.05% 95.77% 1 22594.0 98.92% 98.81% 91.26% 94.00% 89.01% 99.02% 91.38% 95.73% 1.2 22676.2 99.80% 99.61% 99.56% 95.03% 90.80% 99.71% 99.77% 95.90% 1.4 22676.2 99.96% 100.02% 99.87% 95.20% 92.55% 100.00% 99.79% 100.13%

Moving to non-stationary setting, we observe from Table 4.2 that when the price difference (between and ) is small, our ALG2 is identical to CDLP and performs well (). This is because in many cases, our virtual cost is not large enough to discard any products from the assortment. ALG2 is among the best algorithms in many of the simulation scenarios RST17 also performs well () and is the best algorithm in some of the simulation scenarios The de-randomization method from Algorithm 4 also uniformly improves on the corresponding randomized policy in almost all the scenarios and has better performance than RST17.

In Table 4.2, when the price difference is large, our algorithm performs uniformly well (), while CDLP does not (). Note that when is large and are large, this corresponds to scenarios when inventory is too much. Myopic performs the best when inventory is too high, which is not surprising. For the rest of the scenarios, ALG2 and RST17 have the best performance, and sometimes one has better performance than the other. While it is difficult to say which algorithm performs the best, we remark that RST17 requires more information than ALG2, because RST17 needs to know the exact order in which customers arrive to solve the DP, while ALG2 only needs to know the universe of customers to solve the LP. Again, the de-randomization method from Algorithm 4 uniformly improves on the corresponding randomized policy in almost all the scenarios and has better performance than RST17.

5 Conclusions

We proposed and analyzed a calendar pricing problem that a consumer packaged goods company favors given its operational convenience. We considered both single-item pricing and assortment (and pricing) controls. We showed that our policies are within 1-1/e (approximately 0.63) of the optimum under stationary demand and 1/2 of the optimum under non-stationary demand, with both guarantees approaching 1 if the starting inventory is large. Our techniques to analyze the best-possible performance guarantees are of theoretical interest per se. Finally, we fitted the real problem faced by the CPG company into the fractional demand setting of our model and demonstrated using data provided by the CPG company that our simple price calendars are effective. We also tested our simple policies and literature benchmarks on synthetic data, using the same numerical setup as in the literature.