Bertsimas and Cory-Wright

A Scalable Algorithm For Sparse Portfolio Selection

A Scalable Algorithm for Sparse Portfolio Selection

Dimitris Bertsimas

\AFFSloan School of Management, Massachusetts Institute of Technology, Cambridge, MA, USA.

ORCID: ---

\EMAILdbertsim@mit.edu \AUTHORRyan Cory-Wright

\AFFOperations Research Center, Massachusetts Institute of Technology, Cambridge, MA, USA,

ORCID: ---

\EMAILryancw@mit.edu

The sparse portfolio selection problem is one of the most famous and frequently-studied problems in the optimization and financial economics literatures. In a universe of risky assets, the goal is to construct a portfolio with maximal expected return and minimum variance, subject to an upper bound on the number of positions, linear inequalities and minimum investment constraints. Existing certifiably optimal approaches to this problem have not been shown to converge within a practical amount of time at real-world problem sizes with more than securities. In this paper, we propose a more scalable approach. By imposing a ridge regularization term, we reformulate the problem as a convex binary optimization problem, which is solvable via an efficient outer-approximation procedure. We propose various techniques for improving the performance of the procedure, including a heuristic which supplies high-quality warm-starts, and a second heuristic for generating additional cuts which strengthens the root relaxation. We also study the problem’s continuous relaxation, establish that it is second-order-cone representable, and supply a sufficient condition for its tightness. In numerical experiments, we establish that a conjunction of the imposition of ridge regularization and the use of the outer-approximation procedure gives rise to dramatic speedups for sparse portfolio selection problems.

Sparse Portfolio Selection, Binary Convex Optimization, Outer Approximation. \HISTORYThis paper was first submitted in November . A revision was submitted in March . \SUBJECTCLASSnameprogramming: integer; non-linear: quadratic; finance: portfolio

Design and Analysis of Algorithms-Discrete

1 Introduction

Since the Nobel-prize winning work of Markowitz (1952), the problem of selecting an optimal portfolio of securities has received an enormous amount of attention from practitioners and academics alike. In a universe containing distinct securities with expected marginal returns and a variance-covariance matrix of the returns , the scalarized Markowitz model selects a portfolio which provides the highest expected return for a given amount of variance, by solving:

| (1) |

where is a parameter that controls the trade-off between the portfolios risk and return, and denotes the vector of all ones.

To improve its realism, many authors have proposed augmenting Problem (1) with minimum investment, maximum investment, and cardinality constraints among others (see, e.g., Jacob 1974, Perold 1984, Chang et al. 2000). Unfortunately, these constraints are disparate and sometimes imply each other, which makes defining a canonical portfolio selection model challenging. We refer to Mencarelli and D’Ambrosio (2019) for a survey of real-life portfolio selection constraints.

Bienstock (1996) (see also Bertsimas et al. 1999) defined a realistic portfolio selection model by augmenting Problem (1) with two sets of inequalities. The first set is a generic system of linear inequalites which, through an appropriate choice of data , ensures that various real-world constraints such as allocating an appropriate amount of capital to each market sector hold. The second inequality limits the number of non-zero positions held to , by requiring that the portfolio is -sparse, i.e., . The sparsity constraint is important because (a) managers incur monitoring costs for each non-zero position, and (b) investors believe that portfolio managers who do not control the number of positions held perform index-tracking while charging active management fees (see Bertsimas et al. 1999, for an implementation of portfolio selection with sparsity constraints at a real-world asset management company); see also (Bertsimas and Weismantel 2005, Chap. 11.1) for further discussion on the motivation for setting . Imposing the real-world constraints yields the following portfolio selection model:

| (2) |

Note that Problem (2) is NP-hard—even in the absence of linear inequalities (Gao and Li 2013).

By introducing binary variables which model whether takes non-zero values by requiring that if , we rewrite the above problem as a convex mixed-integer quadratic problem:

| (3) |

In the past years, a number of authors have proposed approaches for solving Problem (2) to certifiable optimality. However, no method has been shown to scale to real-world problem sizes111By “real-world”, we refer to problem instances where the portfolio manager optimizes over an index at least as large as the SP . To our knowledge, the Wilshire index, which contains around frequently traded securities, is the largest index by number of securities. As portfolio optimization problems generally involve optimizing over securities within an index, we have written here as an upper bound, although one could conceivably also optimize over securities from the union of multiple stock indices. where and . This lack of scalability presents a challenge for practitioners and academics alike, because a scalable algorithm for Problem (2) has numerous financial applications, while algorithms which do not scale to this problem size are less practically useful.

1.1 Problem Formulation and Main Contributions

In this paper, we provide two main contributions. Our first contribution is augmenting Problem (2) with a ridge regularization term, namely —where is fixed—to yield:

| (4) |

This problem is more practically tractable222We remark that while Problem (4) is more practically tractable than Problem (2), both problems are NP-hard. Indeed, while the NP-hardness of (4) has not been explicitly written down, it follows directly from (Gao and Li 2013, Section E.C.1), because the covariance matrix used in their proof of NP-hardness is positive definite and can therefore be split into a positive semidefinite matrix plus a diagonal regularization matrix as described in Section 3.2. than Problem (2), for two reasons. First, as we formally establish in Section 4.2, the duality gap between Problem (4) and its second-order cone relaxation decreases as we decrease and becomes at some finite . Second, as we numerically establish in Section 5, the algorithms developed here converge more rapidly when is smaller.

In addition to being more practically tractable, Problem (4) is a computationally useful surrogate for Problem (2). Indeed, as we formally establish in Section 3.4, any optimal solution to Problem (4) is a -optimal solution to Problem (2). Moreover, one can find a solution to Problem (2) which is—often substantially—better than this, by (a) solving Problem (4) and (b) solving a simple quadratic optimization problem over the set of securities with the same support as Problem (4)’s solution and an unregularized objective. Indeed, since there are finitely many -sparse binary support vectors, this strategy recovers an optimal solution to (2) for any sufficiently large .

Our second main contribution is a scalable outer-approximation algorithm for Problem (4). By utilizing Problem (4)’s regularization term, we question the modeling paradigm of writing the logical constraint “ if ” as in Problem (4), by substituting the equivalent but non-convex term for and invoking strong duality and that to obtain a convex mixed-integer quadratic reformulation of the problem. This allows us to propose a new outer-approximation algorithm in the spirit of the methods of Duran and Grossmann (1986), Fletcher and Leyffer (1994) but applied to a perspective reformulation (Frangioni and Gentile 2006, Günlük and Linderoth 2012) of the problem which solves large-scale sparse portfolio selection problems with up to securities to certifiable optimality in s or s of seconds.

1.1.1 Connection Between Regularization and Robustness:

While we have introduced ridge regularization as a device which improves the problems tractability while only marginally affecting the optimal objective value, one can actually interpret the regularizer as a robustification technique which improves the overall quality of the selected portfolio. Indeed, Ledoit and Wolf (2004) (see also Carrasco and Noumon 2011) have demonstrated that, in mean-variance portfolio selection problems, the largest eigenvalues of the sample covariance matrix are systematically biased upwards and the smallest eigenvalues of are systematically biased downwards. As a result, imposing a ridge regularization term (with a properly cross-validated ) leads to portfolios which perform better out-of-sample. In a similar vein, DeMiguel et al. (2009) has shown that the strategy of allocating an identical amount of capital to each security outperforms other popular investment strategies. Since a ridge regularization term encourages investing a more equal amount in each security, DeMiguel et al. (2009)’s work suggests that a ridge regularization term is beneficial.

1.2 The Scalability of State-of-the-Art Approaches

We now review the scalability of existing state-of-the-art approaches, as stated by their authors, in order to justify our claim that no existing method has been shown to scale to problem sizes where and . In this direction, Table 1 depicts the largest problem solved by each approach, as reported by its authors, and Table 2 depicts the constraints imposed.

We remark that, as indicated in Table 2, each of the existing approaches was benchmarked on a different data set using a different solver and a different processor, which makes Table 1 an imperfect comparison with our method. Nonetheless, Table 1 appears to be about as accurate a comparison as we can reasonably hope to achieve within the scope of this work. Indeed, a more accurate comparison would require re-implementing these methods from scratch and benchmarking them using the same machine/solver, which, as we are not aware of publicly available source code for any of these methods other than Vielma et al. (2017)333Note that the techniques in Vielma (2017)’s approach were incorporated within CPLEX as of version (Vielma 2017). Accordingly, the numerical comparison against CPLEX ’s MISOCP solver in Section 5 can be viewed as a comparison against Vielma et al. (2017)’s approach., would require a separate review paper.

| Reference | Solution method | Largest instance solved | |

|---|---|---|---|

| (no. securities) | |||

| Vielma et al. (2008) | Nonlinear Branch-and-Bound | ||

| Bonami and Lejeune (2009) | Nonlinear Branch-and-Bound | n/a | |

| Frangioni and Gentile (2009) | Branch-and-Cut+SDO | n/a | |

| Gao and Li (2013) | Nonlinear Branch-and-Bound | ||

| Cui et al. (2013) | Nonlinear Branch-and-Bound | ||

| Zheng et al. (2014) | Branch-and-Cut+SDO | ||

| Frangioni et al. (2016) | Branch-and-Cut+SDO | ||

| Vielma et al. (2017) | Branch-and-Bound | ||

| Frangioni et al. (2017) | Branch-and-Cut+SDO |

| Reference | Solver | C | MR | SC | SOC | LS | Data Source | |

|---|---|---|---|---|---|---|---|---|

| Vielma et al. (2008) |

CPLEX

|

✓ | ✗ | ✗ | ✓ | ✗ | instances generated | |

| using SP daily returns | ||||||||

| Bonami and Lejeune (2009) |

CPLEX ,

|

✗ | ✗ | ✓ | ✓ | ✓ | instances generated | |

Bonmin |

using SP daily returns | |||||||

| Frangioni and Gentile (2009) |

CPLEX

|

✗ | ✓ | ✓ | ✗ | ✗ | Frangioni and Gentile (2006) | |

| Cui et al. (2013) |

CPLEX

|

✓ | ✓ | ✓ | ✗ | ✗ | self-generated instances | |

| Gao and Li (2013) |

CPLEX ,

|

✓ | ✓ | ✗ | ✗ | ✗ | instances generated | |

MOSEK |

using SP daily returns | |||||||

| Zheng et al. (2014) |

CPLEX

|

✓ | ✓ | ✓ | ✗ | ✗ | Frangioni and Gentile (2006) | |

| OR-library (Beasley 1990) | ||||||||

| Frangioni et al. (2016) |

CPLEX

|

✓ | ✓ | ✓ | ✗ | ✗ | Frangioni and Gentile (2006) | |

| Vielma et al. (2017) |

CPLEX ,

|

✓ | ✗ | ✗ | ✓ | ✗ | instances generated by | |

Gurobi

|

Vielma et al. (2008) | |||||||

| Frangioni et al. (2017) |

CPLEX

|

✓ | ✓ | ✓ | ✗ | ✗ | Frangioni and Gentile (2006) | |

| This paper |

CPLEX

|

✓ | ✓ | ✓ | ✗ | ✗ | Frangioni and Gentile (2006) | |

MOSEK |

OR-library Beasley (1990) |

1.3 Background and Literature Review

Our work touches on three different strands of the mixed-integer non-linear optimization literature, each of which propose certifiably optimal methods for solving Problem (2): (a) branch-and-bound methods which solve a sequence of relaxations, (b) decomposition methods which separate the discrete and continuous variables in Problem (2), and (c) perspective reformulation methods which obtain tight relaxations by linking the discrete and the continuous in a non-linear manner.

Branch-and-bound algorithms:

A variety of branch-and-bound algorithms have been proposed for solving Mixed-Integer Nonlinear Optimization problems (MINLOs) to certifiable optimality, since the work of Glover (1975), who proposed linearizing logical constraints “ if ” by rewriting them as for some . This approach is known as the big- method.

The first branch-and-bound algorithm for solving Problem (2) to certifiable optimality was proposed by Bienstock (1996). This algorithm does not make use of binary variables. Instead, it reformulates the sparsity constraint implicitly, by recursively branching on subsets of the universe of buyable securities and obtaining relaxations by imposing constraints of the form , where is an upper bound on . Similar branch-and-bound schemes (which make use of binary variables) are studied in Bertsimas and Shioda (2009), Bonami and Lejeune (2009), who solve instances of Problem (2) with up to (resp. ) securities to certifiable optimality. Unfortunately, these methods do not scale well, because reformulating a sparsity constraint via the big-M method often yields weak relaxations in practice444Indeed, if all securities are i.i.d. then investing in randomly selected securities constitutes an optimal solution to Problem (2), but, as proven in Bienstock (2010), branch-and-bound must expand nodes to improve upon a naive sparsity-constraint free bound by , and expand all nodes to certify optimality.

Motivated by the need to obtain tighter relaxations, more sophisticated branch-and-bound schemes have since been proposed, which obtain higher-quality bounds by lifting the problem to a higher-dimensional space. The first lifted approach was proposed by Vielma et al. (2008), who successfully solved instances of Problem (2) with up to securities to certifiable optimality, by taking efficient polyhedral relaxations of second order cone constraints. This approach has since been improved by Gao and Li (2013), Cui et al. (2013), who derive non-linear branch-and-bound schemes which use even tighter second order cone and semi-definite relaxations to solve problems with up to securities to certifiable optimality.

Decomposition algorithms:

A well-known method for solving MINLOs such as Problem (2) is called outer approximation (OA), which was first proposed by Duran and Grossmann (1986) (building on the work of Kelley (1960), Benders (1962), Geoffrion (1972)), who prove its finite termination. OA separates a difficult MINLO into a finite sequence of master mixed-integer linear problems and non-linear subproblems (NLOs). This is often a good strategy, because linear integer and continuous conic solvers are usually much more powerful than MINLO solvers.

Unfortunately, OA has not yet been successfully applied to Problem (2), because it requires informative subgradient inequalities from each subproblem to attain a fast rate of convergence. Among others, Borchers and Mitchell (1997), Fletcher and Leyffer (1998) have compared OA to branch-and-bound, and found that branch-and-bound outperforms OA for Problem (2).

In the present paper, by invoking strong duality, we derive a new subgradient inequality, redesign OA using this inequality, and solve Problem (4) to certifiable optimality via OA. The numerical success of our decomposition scheme can be explained by two ingredients: (a) the strength of the subgradient inequality, and (b) the tightness of our non-linear reformulation of a sparsity constraint, as further investigated in a more general setting in Bertsimas et al. (2019).

Perspective reformulation algorithms:

An important aspect of solving Problem (2) is understanding its objective’s convex envelope, since approaches which exploit the envelope perform better than approaches which use looser approximations of the objective (Klotz and Newman 2013). An important step in this direction was taken by Frangioni and Gentile (2006), who built on the work of Ceria and Soares (1999) to derive Problem (2)’s convex envelope under an assumption that is diagonal, and reformulated the envelope as a semi-infinite piecewise linear function. By splitting a generic covariance matrix into a diagonal matrix plus a positive semidefinite matrix, they subsequently derived a class of perspective cuts which provide bound gaps of for instances of Problem (2) with up to securities. This approach was subsequently refined by Frangioni and Gentile (2007), Frangioni and Gentile (2009), who solved auxiliary semidefinite problems to extract larger diagonal matrices, and thereby solve instances of Problem (2) with up to securities.

The perspective reformulation approach has also been extended by other authors. An important work in the area is Aktürk et al. (2009), who, building on the work of Ben-Tal and Nemirovski (2001, pp. 88, item 5), prove that if is positive definite, i.e., , then after extracting a diagonal matrix such that , Problem (2) is equivalent to the following mixed-integer second order cone optimization problem (MISOCO):

| (5) | ||||

| s.t. |

In light of the above MISOCO, a natural question to ask is what is the best matrix to use? This question was partially555Note that weaker continuous relaxations may in fact perform better after branching, as discussed by Dong (2016). answered by Zheng et al. (2014), who demonstrated that the matrix which yields the tightest continuous relaxation is computable via semidefinite optimization, and invoked this observation to solve problems with up to securities to optimality (see also Dong et al. 2015, who derive a similar perspective reformulation of sparse regression problems). We refer the reader to Günlük and Linderoth (2012) for a survey of perspective reformulation approaches.

Connection to our approach:

An unchallenged assumption in all perspective reformulation approaches is that Problem (2) must not be modified. Under this assumption, perspective reformulation approaches separate into a diagonal matrix plus a positive semidefinite matrix , such that is as diagonally dominant as possible. Recently, this approach was challenged by Bertsimas and Van Parys (2020). Following a standard statistical learning theory paradigm, they imposed a ridge regularizer and set equal to , where denotes an identity matrix of appropriate dimension. Subsequently, they derived a cutting-plane method which exploits the regularizer to solve large-scale sparse regression problems to certifiable optimality. In the present paper, we join Bertsimas and Van Parys (2020) in imposing a ridge regularizer, and derive a cutting-plane method which solves convex MIQOs with constraints. We also unify their approach with the perspective reformulation approach, in two steps. First, we note that Bertsimas and Van Parys (2020)’s algorithm can be improved by setting equal to plus a perspective reformulation’s diagonal matrix, and this is particularly effective when is diagonally dominant (see Section 3.2, 5.2). Second, we observe that the cutting-plane approach also helps solve the unregularized problem, indeed, as mentioned previously it successfully supplies a -optimal solution to Problem (2).

1.4 Structure

The rest of this paper is laid out as follows:

- •

-

•

In Section 3, we propose an efficient numerical strategy for solving Problem (4). By observing that Problem (4)’s inner dual problem supplies subgradients with respect to the positions held, we design an outer-approximation procedure which solves Problem (4) to provable optimality. We also discuss practical aspects of the procedure, including a computationally efficient subproblem strategy and a prepossessing technique for decreasing the bound gap at the root node. In addition, we study the problems sensitivity to , and establish theoretically that the support of an optimal portfolio (although not the amount allocated to each security) is stable under small changes in .

-

•

In Section 4, we propose techniques for obtaining certifiably near-optimal solutions quickly. First, we introduce a heuristic which supplies high-quality warm-starts. Second, we observe that Problem (4)’s continuous relaxation supplies a near-exact second-order cone representable lower bound, and exploit this observation by deriving a sufficient condition for the bound to be exact.

-

•

In Section 5, we apply the cutting-plane method to the problems described in Chang et al. (2000), Frangioni and Gentile (2006), and three larger scale data sets: the SP , Russell , and Wilshire . We also explore Problem (4)’s sensitivity to its hyperparameters, and establish empirically that optimal support indices tend to be stable for reasonable hyperparameter choices.

Notation:

We let nonbold face characters denote scalars, lowercase bold faced characters such as denote vectors, uppercase bold faced characters such as denote matrices, and calligraphic uppercase characters such as denote sets. We let denote a vector of all ’s, denote a vector of all ’s, and denote the identity matrix, with dimension implied by the context. If is a -dimensional vector then denotes the diagonal matrix whose diagonal entries are given by . We let denote the set of running indices , denote the elementwise, or Hadamard, product between two vectors and , and denote the -dimensional non-negative orthant. We let denote the relative interior of a convex set , i.e., the set of points in the interior of the affine hull of (see Boyd and Vandenberghe 2004, Section 2.1.3). Finally, we let denote the set of -sparse binary vectors, i.e,

2 Equivalence Between Portfolio Selection and Constrained Regression

We now lay the groundwork for our outer-approximation procedure, by rewriting Problem (4) as a constrained sparse regression problem. To achieve this, we take a Cholesky decomposition of and complete the square. This is justified, because is positive semidefinite and rank-, meaning there exists an . Therefore, by scaling and letting:

| (6) | ||||

| (7) |

be the projections of the return vector onto the span and nullspace of respectively, completing the square yields the following equivalent problem, where we add the constant without loss of generality:

| (8) |

That is, sparse portfolio selection and sparse regression with constraints are equivalent.

We remark that while this connection has not been explicitly noted in the literature, Cholesky decompositions of covariance matrices have successfully been applied in perspective reformulation approaches (see Frangioni and Gentile 2006, pp 233), and more recently for robust portfolio selection problems with transaction costs (see Olivares-Nadal and DeMiguel 2018).

3 A Cutting-Plane Method

In this section, we present an efficient outer-approximation method for solving Problem (4), via its reformulation (8). The key step in deriving this method is enforcing the logical constraint if in a tractable fashion. We achieve this by replacing with , and rewriting (4) as:

| (9) |

where

| s.t. | (10) |

is a diagonal matrix such that , and we do not associate a term with in order to enforce the logical constraint if . Observe that the subproblem generated by attains its minimum by setting whenever , which verifies that we have successfully enforced the logical constraint.

Remark 3.1

The formulation proposed in (9)-(10) is reminiscent of a classical complementarity formulation of a cardinality constraint (see, e.g., Burdakov et al. 2016), where the logical constraint is enforced directly by imposing . Perhaps the main point of difference between (9) and a complementarity formulation is that this paper effectively replaces the logical constraint with a penalty term in the objective and uses the strongly convex regularizer to implicitly enforce the logical constraints, while the complementarity formulation explicitly imposes the logical constraints, which does not, by itself, give rise to new algorithms for solving (4).

Problem (9)’s formulation might appear to be intractable, because it appears to define as a function which is non-convex in . However, is actually convex in . Indeed, in Theorem 3.2, which can be found in Section 3.1, we invoke duality to demonstrate that can be rewritten as the supremum of functions which are linear in , thus proving that is actually convex in .

As is convex in , a natural strategy for solving (9) is to iteratively minimize and refine a piecewise linear underestimator of . This strategy is called outer-approximation (OA), and was originally proposed by Duran and Grossmann (1986). OA works as follows: by assuming that at each iteration we have access to and a set of subgradients at the points , we construct the following underestimator:

By iteratively minimizing over to obtain , and evaluating and its subgradient at , we obtain a non-decreasing sequence of underestimators

which converge to the optimal value of within a finite number of iterations, since is a finite set and OA never visits a point twice. Additionally, we can avoid solving a different mixed-integer linear optimization problem (MILO) at each OA iteration by integrating the entire algorithm within a single branch-and-bound tree, as first proposed by Padberg and Rinaldi (1991), Quesada and Grossmann (1992), using dynamic cut generation, which could be implemented using a cut pool and lazy constraint callbacks; see Fischetti et al. (2016b) for an implementation of this approach for facility location problems. Indeed, lazy constraint callbacks are now standard components of modern MILO solvers such as Gurobi, CPLEX and GLPK which allow users to easily implement single-tree OA schemes—we make use of these callbacks when we develop our single-tree OA scheme in Section 3.2.

As we mentioned in Section 1.3, OA is a widely known procedure. However, it has not yet been successfully applied to sparse portfolio selections problems, largely because of a lack of efficient separation oracles which provide both zeroth and first order information concerning the value of at the point . Therefore, we now outline such a procedure which addresses Problem (4).

3.1 Efficient Subgradient Evaluations

We now rewrite Problem (9) as a saddle-point problem, in the following theorem:

Theorem 3.2

Suppose that Problem (9) is feasible. Then, it is equivalent to the following problem:

| (11) | ||||

| s.t. |

Remark 3.3

Remark 3.4

Proof 3.5

Proof of Theorem 3.2 We prove this result by invoking strong duality. First, observe that, for each fixed , Problem (10)’s dual maximization problem (11) is feasible, because can be increased without bound. Moreover, each inner primal minimization problem is a convex quadratic with linear constraints, and thus satisfies the Abadie constraint qualification whenever it is feasible (Abadie 1967). Therefore, for each fixed , either the inner optimization problem (with respect to ) is infeasible or strong duality holds.

Let us now introduce an auxiliary vector of variables such that . This allows us to rewrite Problem (9) as the following problem, where each set of constraints is associated with a vector of dual variables in square brackets

| (13) | ||||

| s.t. | ||||

where .

This problem has the following Lagrangian:

For a fixed , minimizing this Lagrangian is equivalent to solving the following KKT conditions:

Substituting the above expressions for , into then defines the Lagrangian dual, where we eliminate (by replacing it with a non-negativity constraint) and introduce such that for brevity. The Lagrangian dual reveals that for any such that Problem (10) is feasible:

| s.t. |

Moreover, at binary points , and therefore the above problem is equivalent to solving:

| s.t. |

Minimizing over then yields the result, where we ignore choices of which yield infeasible primal subproblems without loss of generality, as their dual problems are feasible and therefore unbounded by weak duality, and a choice of such that is certainly suboptimal. \Halmos

Theorem 3.2 supplies objective function evaluations and subgradients after solving a single convex quadratic optimization problem. We formalize this observation in the following corollary:

Corollary 3.6

Let be an optimal choice of for a particular subset of securities . Then, a valid subgradient has components given by the following expression for each :

| (14) |

In latter sections of this paper, we design aspects of our numerical strategy by assuming that is Lipschitz continuous in . It turns out that this assumption is valid whenever we can bound666Such a bound always exists, because has a finite number of elements. However, it will, in general, depend upon the problem data. for each , as we now establish in the following corollary (proof due to the well-known subgradient inequality (see Boyd and Vandenberghe 2004), deferred to Appendix 6):

Corollary 3.7

Let be an optimal choice of for a given subset of securities . Then:

| (15) |

3.2 A Cutting-Plane Method-Continued

Corollary 3.6 shows that evaluating yields a first-order underestimator of , namely

| (16) |

at no additional cost. Consequently, a numerically efficient strategy for minimizing is the previously discussed OA method. We formalize this procedure in Algorithm 1. Note that we add the OA cuts via dynamic cut generation to maintain a single tree of partial solutions throughout the process, and avoid the cost otherwise incurred in rebuilding the tree whenever a cut is added.

As noted by Duran and Grossmann (1986, Theorem 3) and Fletcher and Leyffer (1994, Theorem 2), Algorithm 1 terminates with an optimal solution to Problem (4) in a finite number of iterations, because is convex in , is a finite set and Algorithm 1 never selects a binary vector twice. Interestingly, while OA methods which leverage strong duality typically require a constraint qualification assumption to guarantee correctness, the proof of Theorem 3.2 reveals that this is not necessary to ensure the correctness of Algorithm 1. Rather, since each subproblem generated by is a convex quadratic with linear constraints, the Abadie constraint qualification (Abadie 1967) holds automatically, and thus Algorithm 1 converges within iterations in the worst case, and typically far fewer iterations in practice.

As Algorithm 1’s rate of convergence depends heavily upon its implementation, we now discuss some practical aspects of the method:

-

•

A computationally efficient subproblem strategy: For computational efficiency purposes, we would like to solve subproblems which only involve active indices, i.e., indices where , since . At a first glance, this does not appear to be possible, because we must supply an optimal choice of for all indices in order to obtain valid subgradients. Fortunately, we can in fact supply a full OA cut after solving a subproblem in the active indices, by exploiting the structure of the saddle-point reformulation. Specifically, we optimize over the indices where and set for the remaining ’s. This procedure yields an optimal choice of for each index , because it is a feasible choice and the remaining ’s have a weight of in the objective function.

Observe that this procedure yields the strongest possible cut which can be generated at a given for this set of dual variables, because (a) the procedure yields the minimum feasible absolute magnitude of whenever , and (b) there is a unique optimal choice of for the remaining indices, since Problem (11) is strongly concave in when . In fact, if is feasible for some security such that , then we cannot improve upon the current iterate by setting , as our lower approximation gives

where the last inequality holds because .

-

•

Cut generation at the root node: Another important aspect of decomposition methods is supplying as much information777 For completeness, we should note that while supplying this information often substantially accelerates decomposition schemes, it can sometimes do more harm than good, particularly if the cuts applied are nearly parallel to one another. In the context of sparse portfolio selection, our numerical experiments in Section 5 demonstrate the efficacy of supplying information at the root node for all but the simplest sparse porfolio selection problems. as possible to the solver before commencing branching, as advocated by Fischetti et al. (2016b, Section 4.2). One effective way to achieve this is to relax the integrality constraint to in Problem (11), run a cutting-plane method on this continuous relaxation and apply the resulting cuts at the root node before solving the binary problem. Traditionally, this relaxation is solved using Kelley (1960)’s cutting-plane method. However, as Kelley (1960)’s method often converges slowly in practice, we instead solve the relaxation using an

in-outbundle method (Ben-Ameur and Neto 2007, Fischetti et al. 2016b). We supply pseudocode for our implementation of thein-outmethod in Appendix 8.In order to further accelerate OA, a variant of the root node processing technique which is often effective is to also run the

in-outmethod at some additional nodes in the tree, as proposed in (Fischetti et al. 2016b, Section 4.3). This can be implemented using the cut separation method derived in the previous section (and implemented via auser cut callback), by using the current LO solution as a stabilization point for thein-outmethod.To avoid generating too many cuts at continuous points, we impose a limit of cuts at the root node, cuts at all other nodes, and do not run the

in-outmethod at more than nodes. One point of difference in our implementation of thein-outmethod (compared to Ben-Ameur and Neto 2007, Fischetti et al. 2016b) is that we use the true optimal solution to Problem (11)’s continuous relaxation as a stabilization point at the root node (as opposed to the methods current estimate of the optimal solution)– this speeds up convergence of thein-outmethod greatly, and comes at the low price of solving an SOCO to elicit the stabilization point (we obtain the point by solving Problem (27); see Section 4.2). Note that this approach may appear somewhat counter-intuitive, as it involves using the optimal solution to the relaxation to “solve” the relaxation. However, it is actually not, because we are interested in generating a small number of cuts which efficiently describe the surface of the relaxation near its optimal solution, rather than solving the relaxation.Restarting mechanisms, as explored by Fischetti et al. (2016a), may also be useful for further improving the root node relaxation, although we do not consider them in this work.

-

•

Feasibility cuts: The constraints may render some vectors infeasible. In this case, we add the following feasibility cut which bans from appearing in future iterations of OA:

(17) An alternative approach is to derive constraints on which ensure that OA never selects an infeasible . For instance, if the only constraint on is a minimum return constraint then imposing ensures that only feasible ’s are selected. Whenever eliciting these constraints is possible, we recommend imposing them, to avoid infeasible subproblems entirely.

-

•

Extracting Diagonal Dominance: In problems where is diagonally dominant in the sense of Barker and Carlson (1975), i.e., , the performance of Algorithm 1 can often be substantially improved by boosting the regularizer, i.e., selecting a diagonal matrix such that , replacing with , and using a different regularizer for each index , to obtain a more general problem of which (4) is a special case; note that the algorithms developed here remain valid when we have a different regularizer for each index . In general, selecting such a involves solving a semidefinite optimization problem (SDO) (Frangioni and Gentile 2007, Zheng et al. 2014), which is fast when is in the hundreds, but requires a prohibitive amount of memory when is in the thousands. In the latter case, we recommend taking a second-order cone inner approximation of the semidefinite cone and improving the approximation via column generation. Indeed, this approach has recently been shown to provide high-quality solutions to large-scale SDOs which cannot be solved by interior-point methods, due to excessive memory requirements (see Ahmadi et al. 2017, Bertsimas and Cory-Wright 2020).

-

•

Copy of variables: In problems with multiple complicating constraints, many feasibility cuts may be generated, which can hinder convergence greatly. If this occurs, we recommend introducing a copy of in Problem (9), and imposing the following constraints:

(18) while keeping Problem (10) the same. This approach performs well on the highly constrained problems studied in Section 5.2.

3.3 Modeling Minimum Investment Constraints

A frequently-studied extension to Problem (2) is to impose minimum investment constraints, which control transaction fees by requiring that . We now extend our saddle-point reformulation to cope with them.

By letting be a binary indicator variable which denotes whether we hold a non-zero position in the th asset, we model these constraints via Moreover, we incorporate the upper bounds within our algorithmic framework by “disappearing” the constraints into the general linear constraint set .

Moreover, by letting be the dual multiplier associated with the th minimum investment constraint, and repeating the steps of our saddle-point reformulation, we retain efficient objective function and subgradient evaluations in the presence of these constraints. Specifically, including the constraints is equivalent to adding the term to Problem (4)’s Lagrangian, which implies the saddle-point problem becomes:

| (19) | ||||

| s.t. |

Moreover, the subgradient with respect to each index becomes

| (20) |

Finally, if then we can certainly set without loss of optimality. Therefore, we recommend solving a subproblem in the variables for which and subsequently setting for the remaining variables, in the manner discussed in the previous subsection. Indeed, setting for each index where , as discussed in the previous subsection, supplies the minimum absolute value of .

3.4 Sensitivity Analysis

In this section, we study Problem (9)’s dependence on the regularization parameter . This is an important issue in practice, because, as suggested in the introduction, if we are interested in solving Problem (2), we can solve the regularized problem to obtain a support vector , and subsequently resolve the unregularized problem with the support fixed to . Therefore, we are interested in the suboptimality (w.r.t. (2)) of an optimal solution to Problem (4).

We remark that the results in this section rely on basic sensitivity analysis proof techniques which can be found in several optimization textbooks (e.g., Bertsimas and Tsitsiklis 1997, Rockafellar and Wets 2009). Nonetheless, we have included them, due to the central importance of regularization in this work, and because these results are not widely known.

Our first result demonstrates that the optimal support for a larger value of can serve as a high-quality warm-start for a problem with less regularization.

Proposition 3.8

Proof 3.9

Proof of Proposition 3.8 We have that:

where the first inequality holds because decreasing the amount of regularization can only lower the optimal objective value, the second inequality holds because , an optimal choice of with support indices , is a feasible solution with regularization parameter , specifically and the last inequality holds because all solutions lie on the unit simplex. \Halmos

Observe that, by setting , Proposition 3.8 supplies a formal proof of Section ’s claim that is a -optimal solution for .

Our next result justifies our claim in the introduction that for a sufficiently large we recover the same optimal support from Problem (4) as the unregularized Problem (2):

Proposition 3.10

Proof 3.11

Proof of Proposition 3.10 Let us observe that, for each , is concave in as the pointwise minimum of functions which are linear in , and moreover is also a concave function in . By this concavity, it is a standard result from sensitivity analysis (see, e.g., Bertsimas and Tsitsiklis 1997, Chapter 5.6) that the set of all ’s for which a particular is optimal must form a (possibly open) interval. The result then follows directly from the finiteness of . \Halmos

Our final result in this section shows that the optimal support of the portfolio remains unchanged for sufficiently small ’s (proof omitted, follows in the same fashion as Proposition 3.10):

3.5 Relationship with Perspective Cut Approach

In this section, we relate Algorithm 1 to the perspective cut approach introduced by Frangioni and Gentile (2006). It turns out that taking the dual of the inner maximization problem in Problem (11) yields a perspective reformulation, and decomposing this reformulation in a way which retains the continuous and discrete variables in the master problem and outer-approximates the objective is precisely the perspective cut approach, as discussed in a more general setting by Bertsimas et al. (2019, Section 3.4). In this regard, our approach supplies a new and insightful derivation of the perspective cut scheme. In addition, our approach can easily be implemented within a modern mixed-integer optimization solver such as CPLEX or Gurobi, while existing implementations of the perspective cut approach often require tailored branch-and-bound schemes (see Frangioni and Gentile 2006, Section 3.1).

4 Improving the Performance of the Cutting-Plane Method

In portfolio rebalancing applications, practitioners often require a high-quality solution to Problem (4) within a fixed time budget. Unfortunately, Algorithm 1 is ill-suited to this task: while it always identifies a certifiably optimal solution, it does not always do so within a time budget. In this section, we propose alternative techniques which sacrifice some optimality for speed, and discuss how they can be applied to improve the performance of Algorithm 1. In Section 4.1 we propose a warm-start heuristic which supplies a high-quality solution to Problem (4) a priori, and in Section 4.2 we derive a second order cone representable lower bound which is often very tight in practice. Taken together, these techniques supply a certifiably near optimal solution very quickly, which can often be further improved by running Algorithm 1 for a short amount of time.

4.1 Improving the Upper Bound: A Warm-Start Heuristic

In branch-and-cut methods, a frequently observed source of inefficiency is that solvers explore highly suboptimal regions of the search space in considerable depth. To discourage this behavior, optimizers frequently supply a high-quality feasible solution (i.e., a warm-start), which is installed as an incumbent by the solver. Warm-starts are beneficial for two reasons. First, they improve Algorithm 1’s upper bound. Second, they allow Algorithm 1 to prune vectors of partial solutions which are provably worse than the warm-start, which in turn improves Algorithm 1’s bound quality, by reducing the set of feasible binaries which can be selected at each subsequent iteration. Indeed, by pruning suboptimal solutions, warm-starts encourage branch-and-cut methods to focus on regions of the search space which contain near-optimal solutions.

We now describe a heuristic which supplies high-quality solutions for Problem (4), inspired by a heuristic due to Bertsimas et al. (2016, Algorithm 1). The heuristic works under the assumption that is -Lipschitz continuous in , with Lipschitz continuous gradient such that

Note that this assumption is justified whenever the optimal dual variables are bounded; see Corollary 3.7. Under this assumption, the heuristic approximately minimizes by iteratively minimizing a quadratic approximation of at , namely .

This idea is algorithmized as follows: given a sparsity pattern and an optimal sparse portfolio for this given sparsity pattern , the method iteratively solves the following problem, which ranks the differences between each security’s contribution to the portfolio, , and the associated entry of the subgradient of at :

| (24) |

Given , can be obtained by setting for of the indices where is largest (cf. Bertsimas et al. 2016, Proposition 3). We formalize this warm-start procedure in Algorithm 2. Note that Algorithm 2 is a discrete first-order heuristic in the sense of Nesterov (2013, 2018), since as discussed in (Bertsimas et al. 2016, Section 3) it iteratively minimizes a first order approximation of by solving for a stationary point in the first-order approximation.

| s.t. |

Some remarks on Algorithm 2 are now in order:

-

•

In our numerical experiments, we run Algorithm 2 from five different randomly generated -sparse binary vectors, to increase the probability that it identifies a high-quality solution.

-

•

Averaging the dual multipliers across iterations, as suggested in the pseudocode, improves the method’s performance; note that the contribution of each to is , where is the total number of iterations completed by Algorithm 2 and we initially set in order that is defined when we perform the averaging step at the first iteration; note that when we have so the initialization is unimportant.

-

•

Each is the optimal solution of a convex quadratic optimization problem which can be reformulated as a (rotated) second-order cone program. Therefore, each can be obtained via a standard second-order cone solver such as

CPLEX,GurobiorMosek. -

•

The Lipschitz constant is motivated as an upper bound on an entry in a subgradient of , . However, Algorithm 2 is ultimately a heuristic method. Therefore, we recommend picking by cross-validating to minimize the objective obtained by Algorithm 2. In practice, setting was sufficient to reliably obtain high-quality solutions in Section 5, because Algorithm 3 (see Section 4.3) invokes a judicious combination of outer-approximation cuts and this warm-start to convert this warm-start into an optimal solution within seconds. Therefore, we set throughout Section 5, although it may be appropriate to cross-validate if running the method on new data.

4.2 Improving the Lower Bound: A Second Order Cone Relaxation

In financial applications, we sometimes require a certifiably near-optimal solution quickly but do not have time to certify optimality. Therefore, we now derive near-exact lower bounds which can be computed in polynomial time. Immediately, we see that we obtain a valid lower bound by relaxing the constraint to in Problem (4). By invoking strong duality, we now demonstrate that this lower bound can be obtained by solving a single second order cone problem.

Theorem 4.1

Suppose that Problem (4) is feasible. Then, the following three optimization problems attain the same optimal value:

| (25) | ||||

| s.t. |

| (26) | ||||

| s.t. |

| (27) | ||||

| s.t. |

Remark 4.2

Proof 4.3

Proof of Theorem 4.1

Problem (25) is strictly feasible, since the interior of is non-empty and can be increased without bound. Therefore, the Sion-Kakutani minimax theorem (Ben-Tal and Nemirovski 2001, Appendix D.4.) holds, and we can exchange the minimum and maximum operators in Problem (25), to yield:

| (28) | ||||

| s.t. |

Next, fixing and applying strong duality between the inner primal problem

and its dual problem

proves that strong duality holds between Problems (25)-(26).

Next, we observe that Problems (26)-(27) are dual, as can be seen by applying the relation

to rewrite Problem (26) as an SOCO in standard form, and applying SOCO duality (see, e.g., Boyd and Vandenberghe 2004, Exercise 5.43). Moreover, since Problem (26) is strictly feasible (as , are unbounded from above) strong duality must hold between these problems. \Halmos

Having derived Problem (4)’s bidual, namely Problem (27), it follows from a direct application of convex analysis that the duality gap between Problem (4) and (27), , decreases as we decrease and becomes at some finite . Note however that this will, in general, depend upon the problem data (see Hiriart-Urruty and Lemaréchal 2013, Theorem XII.5.2.2). This observation justifies our claim in the introduction that decreasing makes Problem (4) easier.

We now derive conditions under which Problem (26) provides an optimal solution to Problem (4) a priori (proof deferred to Appendix 6).

Corollary 4.4

A sufficient condition for support recovery

Let there exist some and set of dual multipliers which solve Problem (26), such that these two quantities collectively satisfy the following conditions:

| (29) |

We now apply Theorem 4.1 to prove that if is a diagonal matrix, is a multiple of the vector of all ’s and the matrix is empty then Problem (4) is solvable in closed-form. Let us first observe that under these conditions Problem (4) is equivalent to

We now have the following result:

Corollary 4.5

Let . Then, strong duality holds between the problem

| (30) |

and its second-order cone relaxation:

| (31) | ||||

| s.t. |

Moreover, an optimal solution to Problem (30) is for , for .

Proof 4.6

Proof of Corollary 4.5 By Theorem 4.1, a valid lower bound to Problem (30) is given by the SOCO:

| (32) | ||||

| s.t. |

Let us assume that (otherwise the objective value cannot exceed , which is certainly suboptimal). Then, we can let the constraint be binding without loss of optimality for each index , i.e., set for some . This allows us to simplify this problem to:

| (33) | ||||

| s.t. |

The KKT conditions for max- norms (see, e.g., Zakeri et al. 2014, Lemma 1) then reveal that an optimal choice of is given by the th largest value of , i.e., and an optimal choice of is given by , i.e.,

Substituting these terms into the objective function gives an objective of

which implies that an optimal choice of is . Next, substituting the expression into the objective function gives an objective value of , which implies that a lower bound on Problem (30)’s objective is .

Finally, we construct a primal solution via , and the primal-dual KKT condition . This is feasible, by inspection. Moreover, it has an objective value of

and therefore is optimal.

4.3 An Improved Cutting-Plane Method

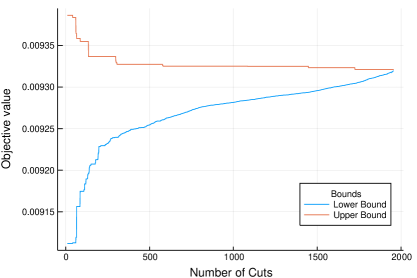

We close this section by combining Algorithm 1 with the improvements discussed in this section, to obtain an efficient numerical approach to Problem (4), which we present in Algorithm 3. Note that we use the larger of and the second-order cone lower bound in our termination criterion, as the second-order cone gap is sometimes less than .

Figure 1 depicts the algorithm’s convergence on the problem port2 with a cardinality value and a minimum return constraint, as described in Section 5.1. Note that we did not use the second-order cone lower bound when generating this plot; the second-order cone lower bound is in this instance, and Algorithm 3 requires cuts to improve upon this bound.

5 Computational Experiments on Real-World Data

In this section, we evaluate our outer-approximation method, implemented in Julia using the JuMP.jl package version and solved using CPLEX version for the master problems, and Mosek version for the continuous quadratic subproblems. We compare the method against big- and MISOCO formulations of Problem (4), solved in CPLEX. To bridge the gap between theory and practice, we have made our code freely available on Github at github.com/ryancorywright/SparsePortfolioSelection.jl.

All experiments were performed on a MacBook Pro with a GHz i Intel®CPU and GB DDR Memory. For simplicity, we ran all methods on one thread, using default CPLEX parameters.

In all experiments which do not involve minimum investment constraints, we solve the following optimization problem, which places a multiplier on the return term but—since the multiplier can be absorbed into the return vector —is mathematically equivalent to Problem (4):

| (34) |

Note that we only consider cases where or , depending on whether we are penalizing low expected return portfolios in the objective or constraining the portfolios expected return.

In the presence of minimum investment constraints, we augment Problem (34) with the constraints , which can be straightforwardly managed by the algorithms derived in this paper in the manner discussed in Section 5.2.

We aim to answer the following questions:

-

1.

How does Algorithm 3 compare to existing commercial codes such as

CPLEX? -

2.

How do constraints affect Algorithm 3’s scalability?

-

3.

How does Algorithm 3 scale as a function of the number of securities in the buyable universe?

-

4.

How sensitive are optimal solutions to Problem (4) to the hyperparameters ?

5.1 A Comparison Between Algorithm 3 and Existing Commercial Codes

We now present a direct comparison of Algorithm 3 with CPLEX version , where CPLEX uses both big-M and MISOCO formulations of Problem (4). Note that the MISOCO formulation which we pass directly to CPLEX is (cf. Ben-Tal and Nemirovski 2001, Aktürk et al. 2009):

| (35) |

We remark that CPLEX’s MISOCO routine can be interpreted as an aggregation of the techniques reviewed in the introduction, since CPLEX mines the optimization literature for techniques which improve its performance. For instance, as discussed by Vielma (2017), CPLEX’s MISOCO routine currently includes the conic disaggregation technique of Vielma et al. (2017). Indeed, this aggregation has been so successful that Bienstock (2010) showed that, in , CPLEX outperformed several of the methods reviewed in the introduction.

We compare the three approaches in two distinct situations. First, when no constraints are applied and the system is empty, and second when a minimum return constraint is applied, i.e., . In the former case we set , while in the latter case we set and as suggested by Cesarone et al. (2009), Zheng et al. (2014) we set in the following manner: Let

| where | ||||||

| where |

and set .

Table 3 (resp. Table 4) depicts the time required for all approaches to determine an optimal allocation of funds without (resp. with) the minimum return constraint. The problem data is taken from the mean-variance portfolio optimization problems described by Chang et al. (2000) and included in the OR-library test set by Beasley (1990). Note that we turned off the second-order cone lower bound for these tests, and ensured feasibility in the master problem by imposing when running Algorithm 3 on the instances with a minimum return constraint (see Section 3.2). Furthermore, as Algorithm 3 is slow to converge for some instances with a return constraint, in Table 4 we ran the method after applying cuts at the root node, generated using the in-out method (see Appendix 8, for the relevant pseudocode).

| Problem | Algorithm 3 | CPLEX Big-M | CPLEX MISOCO | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Time | Nodes | Cuts | Time | Nodes | Time | Nodes | |||

| port | 0.03 | ||||||||

| 0.01 | |||||||||

| 0.01 | |||||||||

| port | 0.01 | ||||||||

| 0.01 | |||||||||

| 0.01 | |||||||||

| port | 0.01 | ||||||||

| 0.01 | |||||||||

| 0.02 | |||||||||

| port | 0.03 | ||||||||

| 0.02 | |||||||||

| 0.03 | |||||||||

| port | 0.15 | ||||||||

| 0.02 | |||||||||

| 0.03 | |||||||||

| Problem | Algorithm 3 | Algorithm 3+in-out | CPLEX Big-M | CPLEX MISOCO | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Time | Nodes | Cuts | Time | Nodes | Cuts | Time | Nodes | Time | Nodes | |||

| port | 0.22 | |||||||||||

| 0.20 | ||||||||||||

| 0.05 | ||||||||||||

| port | 31.47 | |||||||||||

| 82.44 | ||||||||||||

| 10.52 | ||||||||||||

| port | 151.1 | |||||||||||

| 531.3 | ||||||||||||

| 21.32 | ||||||||||||

| port | 2,475 | |||||||||||

| 148.9 | ||||||||||||

| port | 0.40 | |||||||||||

| 0.03 | ||||||||||||

| 0.08 | ||||||||||||

Table 4 indicates that the port instance cannot be solved to certifiable optimality by any approach within an hour when , in the presence of a minimum return constraint. Nonetheless, both Algorithm 3 and CPLEX’s MISOCO method obtain solutions which are certifiably within of optimality very quickly. Indeed, Table 5 depicts the bound gaps of all approaches at s on these problems; Algorithm 3 never has a bound gap larger than .

| Problem | Algorithm 3 | Algorithm 3+in-out | CPLEX Big-M | CPLEX MISOCO | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Gap () | Nodes | Cuts | Gap () | Nodes | Cuts | Gap () | Nodes | Gap () | Nodes | |||

| port | 0 | 0 | 0 | |||||||||

| 0 | ||||||||||||

| 0 | 0 | 0 | ||||||||||

| port | 0.08 | |||||||||||

| 0.19 | ||||||||||||

| 0 | 0 | 0 | ||||||||||

| port | 0.18 | |||||||||||

| 0.29 | 0.29 | |||||||||||

| 0.05 | ||||||||||||

The experimental results illustrate that our approach is several orders of magnitude more efficient than the big- approach on all problems considered, and performs comparably with the MISOCO approach. Moreover, our approach’s edge over CPLEX increases with the problem size.

Our main findings from this set of experiments are as follows:

-

1.

For problems with unit simplex constraints, big- approaches do not scale to real-world problem sizes in the presence of ridge regularization, because they cannot exploit the ridge regularizer and therefore obtain low-quality lower bounds, even after expanding a large number of nodes. This poor performance is due to the ridge regularizer; the big- approach typically exhibits better performance than this in numerical studies done without a regularizer.

-

2.

MISOCO approaches perform competitively, and are often a computationally reasonable approach for small to medium sized instances of Problem (4), as they are easy to implement and typically have bound gaps of in instances where they fail to converge within the time budget.

-

3.

Varying the cardinality of the optimal portfolio does not affect solve times substantially without a minimum return constraint, although it has a nonlinear effect with this constraint.

For the rest of the paper, we do not consider big- formulations of Problem (4), as they do not scale to larger problems with or more securities in the universe of buyable assets.

5.2 Benchmarking Algorithm 3 in the Presence of Minimum Investment Constraints

In this section, we explore Algorithm 3’s scalability in the presence of minimum investment constraints, by solving the problems generated by Frangioni and Gentile (2006) and subsequently solved by Frangioni and Gentile (2007), Frangioni and Gentile (2009), Zheng et al. (2014) among others888This problem data is available at www.di.unipi.it/optimize/Data/MV.html. These problems have minimum investment, maximum investment, and minimum return constraints, which render many entries in infeasible. Therefore, to avoid generating an excessive number of feasibility cuts, we use the copy of variables technique suggested in Section 3.2.

Additionally, as the covariance matrices in these problems are highly diagonally dominant (with much larger on-diagonal entries than off-diagonal entries), the method does not converge quickly if we do not extract any diagonal dominance. Indeed, Appendix 7.1 shows that the method often fails to converge within s for the problems studied in this section when we do not extract a diagonally dominant term. Therefore, we first preprocess the covariance matrices to extract more diagonal dominance, as discussed in Section 3.2. Note that we need not actually solve any SDOs to preprocess the data, as high quality diagonal matrices for this problem data have been made publicly available by Frangioni et al. (2017) at http://www.di.unipi.it/optimize/Data/MV/diagonals.tgz (specifically, we use the entries in the “s” folder of this repository). After reading in their diagonal matrix , we replace with and use the regularizer for each index , where (we do this for all approaches benchmarked here, including CPLEX’s MISOCO routine).

We now compare the times for Algorithm 3 and CPLEX’s MISOCO routines to solve the diagonally dominant instances in the dataset generated by Frangioni and Gentile (2006), along with a variant of Algorithm 3 where we use the in-out method at the root node, and another variant where we apply the in-out method at both the root node and additional nodes. In all cases, we take , which ensures that , since on this dataset is around orders of magnitude smaller than and thus the net contribution of the regularization term to the objective is negligible. Table 6 depicts the average time taken by each approach, and demonstrates that Algorithm 3 substantially outperforms CPLEX, particularly for problems without an explicit cardinality constraint, but with an implicit cardinality constraint of for due to the minimum investment constraints where is uniformly drawn from (Frangioni and Gentile 2007). We provide the full instance-wise results in Appendix 7.1, and also consider the possibility of supplying the cuts from the in-out method to CPLEX before running the MISOCP method therein.

| Problem | Algorithm 3 | Algorithm 3 in-out | Algorithm 3 in-out 50 | CPLEX MISOCO | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Time | Nodes | Cuts | Time | Nodes | Cuts | Time | Nodes | Cuts | Time | Nodes | ||

| 200+ | 6 | 1.55 | 1,298 | 236.3 | 1.77 | 1,262 | 209.4 | 7.4 | 910.4 | 118 | 87.74 (0) | 95.3 |

| 200+ | 8 | 1.95 | 1,968 | 260.3 | 2.30 | 1,626 | 217 | 7.97 | 949.1 | 97.3 | 73.42 (0) | 79.8 |

| 200+ | 10 | 7.74 | 7,606 | 509.7 | 4.33 | 3,686 | 298.9 | 10.35 | 2,066 | 175.5 | 161.9 (0) | 184 |

| 200+ | 12 | 25.57 | 28,830 | 203.8 | 2.06 | 1,764 | 71.6 | 9.04 | 1,000 | 33.9 | 353.1 (4) | 398.1 |

| 200+ | 200 | 18.71 | 23,190 | 208.4 | 2.79 | 2,288 | 92 | 10 | 1,394 | 56.1 | 599.3 (9) | 735.1 |

| 300+ | 6 | 16.83 | 9,141 | 974.2 | 23.59 | 8,025 | 864.1 | 29.92 | 5,738 | 565.9 | 434.5 (3) | 157.6 |

| 300+ | 8 | 44.68 | 21,050 | 1,577 | 64.46 | 19,682 | 1457.8 | 61.0 | 14,236 | 1,036 | 489.5 (5) | 174.0 |

| 300+ | 10 | 88.57 | 44,160 | 1,901 | 78.05 | 33,253 | 1438.4 | 110.2 | 24,487 | 971.5 | 472.0 (5) | 171.9 |

| 300+ | 12 | 16.16 | 13,880 | 262.7 | 4.65 | 3,181 | 127.4 | 15.94 | 1475 | 66.7 | 401.5 (4) | 158.2 |

| 300+ | 300 | 21.36 | 18,140 | 262.1 | 9.24 | 6,288 | 191.9 | 24.33 | 5,971 | 168.4 | 600.0 (10) | 219.2 |

| 400+ | 6 | 54.47 | 13,330 | 1,717 | 66.52 | 12,160 | 1,619 | 85.51 | 11,070 | 1,402 | 531.7 (8) | 84.0 |

| 400+ | 8 | 173.8 | 35,390 | 2,828 | 160.9 | 32,930 | 2,709 | 163.3 | 28,020 | 2,363 | 534.0 (8) | 80.8 |

| 400+ | 10 | 158.0 | 55,490 | 1,669 | 104.5 | 32,314 | 1369.7 | 81.48 | 22,130 | 824.9 | 517.9 (8) | 74.8 |

| 400+ | 12 | 3.97 | 4,324 | 116.6 | 1.9 | 1,214 | 48.6 | 15.67 | 627.4 | 29.8 | 478.0 (4) | 75.3 |

| 400+ | 400 | 8.68 | 7,540 | 120.5 | 5.19 | 3,539 | 88.8 | 21.31 | 3,210 | 79.4 | 600.0 (10) | 74.2 |

Our main findings from this experiment are as follows:

-

•

Algorithm 3 outperforms

CPLEXin the presence of minimum investment constraints. Interestingly, the log output indicates thatCPLEX’s custom heuristics typically obtain incumbent solutions which are better than those obtained by Algorithm 2 and supplied to Algorithm 3 as a warm-start. This suggests that Algorithm 3’s superior numerical performance arises because it can develop high-quality (i.e., better than the SOCO bound) lower bounds more quickly. This shouldn’t be too surprising, since beating a continuous relaxation bound involves branching (or cutting), which is cheaper to perform on a pure binary formulation than a MISOCO formulation. -

•

Running the

in-outmethod at the root node improves solve times when , but does more harm than good when , because in the latter case Algorithm 3 already performs well. -

•

Running the

in-outmethod at non-root nodes does more harm than good for easy problems, but improves solve times for larger problems ( with ), as reported in Appendix 7.1. -

•

With a cardinality constraint, Algorithm 3’s solve times are comparable to those reported by Zheng et al. (2014), Frangioni et al. (2016) (note however that this comparison is imperfect since all three approaches were run on different machines; the source code for the other two approaches is unavailable and hence we cannot obtain truly comparable data). This can be explained by the fact that all three methods solve these problems in s of seconds, and thus these problems can be viewed as “easy”. Without an explicit cardinality constraint (but with minimum investment constraints which impose an implicit cardinality constraint of Frangioni and Gentile (2007)), our solve times are two orders of magnitude faster than those reported by Zheng et al. (2014)’s (an average of s for ), and an order of magnitude faster than those by Frangioni et al. (2016) (an average of s for ).

-

•

As shown in Appendix 7.1, applying the diagonal dominance preprocessing technique proposed by Frangioni and Gentile (2007) yields faster solve times than applying the technique proposed by Zheng et al. (2014), even though the latter technique yields tighter continuous relaxations (Zheng et al. 2014). This might occur because Frangioni and Gentile (2007)’s technique prompts our approach to make better branching decisions and/or Zheng et al. (2014)’s approach is only guaranteed to yield tighter continuous relaxations before (i.e., not after) branching.

-

•

As shown in Appendix 7.1, passing the cuts generated by the

in-outmethod toCPLEXdoes more harm than good. This can be explained by the fact that the SOCP relaxation, which is very affordable to compute, is at least as strong as the lower approximation generated by thein-outmethod (indeed, thein-outmethod can be interpreted as a linearization of the SOCP relaxation about a “cleverly” sampled set of points), while providing the in-out method’s lower approximation toCPLEXincreases the amount of work whichCPLEXneeds to perform at each node in the branch-and-bound tree.

5.3 Exploring the Scalability of Algorithm 3

In this section, we explore Algorithm 3’s scalability with respect to the number of securities in the buyable universe, by measuring the time required to solve several large-scale sparse portfolio selection problems to provable optimality: the SP , the Russell , and the Wilshire . In all three cases, the problem data is taken from daily closing prices from January to December , which are obtained from Yahoo! Finance via the R package quantmod (see Ryan and Ulrich (2018)), and rescaled to correspond to a holding period of one month. We apply Singular Value Decomposition to obtain low-rank estimates of the correlation matrix, and rescale the low-rank correlation matrix by each asset’s variance to obtain a low-rank covariance matrix . We also omit days with a greater than change in closing prices when computing the mean and covariance for the Russell and Wilshire , since these changes occur on low-volume trading and typically reverse the next day.

Tables 7–9 depict the times required for Algorithm 3 and CPLEX MISOCO to solve the problem to provable optimality for different choices of , , and Rank. In particular, they depict the time taken to solve (a) an unconstrained problem where and (b) a constrained problem where containing a minimum return constraint computed in the same fashion as in Section 5.1.

| Rank | Algorithm 3 | CPLEX MISOCO | Algorithm 3 | CPLEX MISOCO | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Time | Nodes | Cuts | Time | Nodes | Time | Nodes | Cuts | Time | Nodes | |||

| Rank | Algorithm 3 | CPLEX MISOCO | Algorithm 3 | CPLEX MISOCO | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Time | Nodes | Cuts | Time | Nodes | Time | Nodes | Cuts | Time | Nodes | |||

| Rank | Algorithm 3 | CPLEX MISOCO | Algorithm 3 | CPLEX MISOCO | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Time | Nodes | Cuts | Time | Nodes | Time | Nodes | Cuts | Time | Nodes | |||

Our main finding from this set of experiments is that Algorithm 3 is substantially faster than CPLEX’s MISOCO routine, particularly as the rank of increases. The relative numerical success of Algorithm 3 in this section, compared to the previous section, can be explained by the differences in the problems solved: (a) in this section, we optimize over a sparse unit simplex, while in the previous section we optimized over minimum-return and minimum-investment constraints, (b) in this section, we use data taken directly from stock markets, while in the previous section we used less realistic synthetic data, which evidently made the problem harder.

5.4 Exploring Sensitivity to Hyperparameters

Our next set of experiments explores Problem (4)’s stability to changes in its hyperparameter .

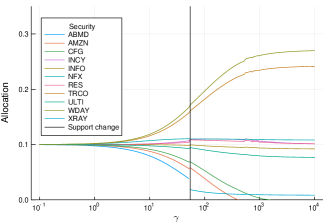

We first explore optimizing over a rank– approximation of the Russell with a one month holding period, a sparsity budget and a weight .

Figure 2 depicts the relationship between and for this set of hyperparameters, and indicates that is stable with respect to small changes in . Moreover, the optimal support indices when is small (to the left of the vertical line) are near-optimal when is large , while the optimal support indicies when is large (to the right of the vertical line) are optimal for Problem (2), which echoes our sensitivity analysis findings and particularly Proposition 3.10. This suggests that a good strategy for cross-validating could be to solve Problem (4) to certifiable optimality for one value of , find the best value of conditional on using these support indices, and finally resolve Problem (4) with the optimal .

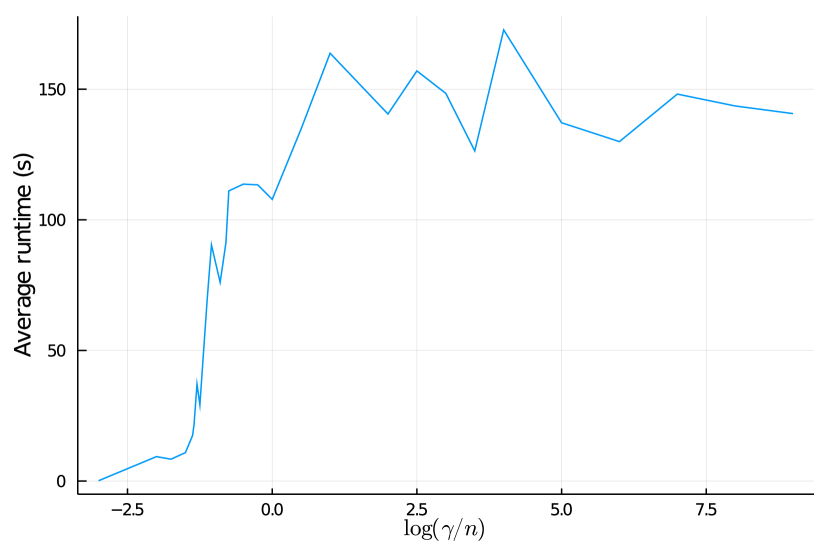

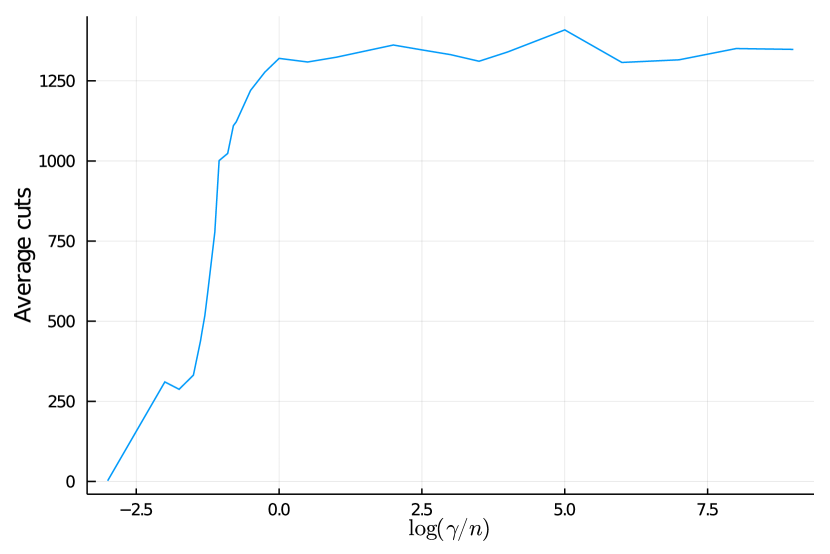

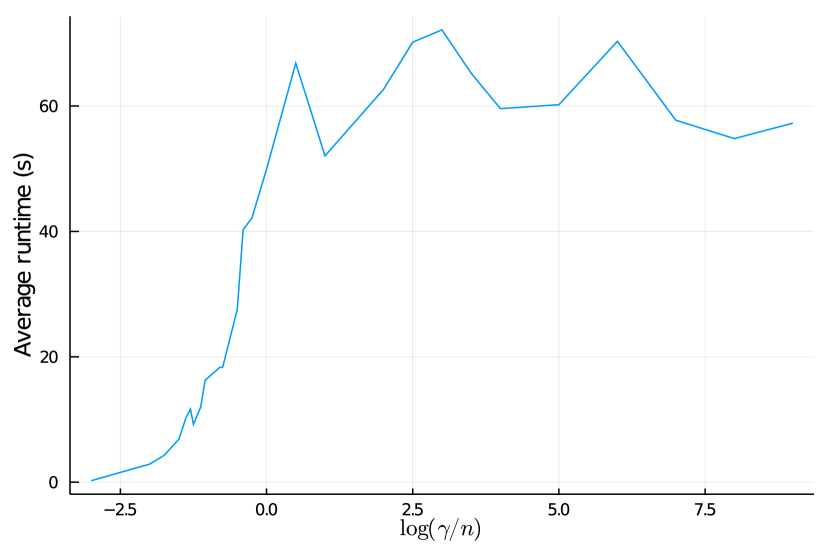

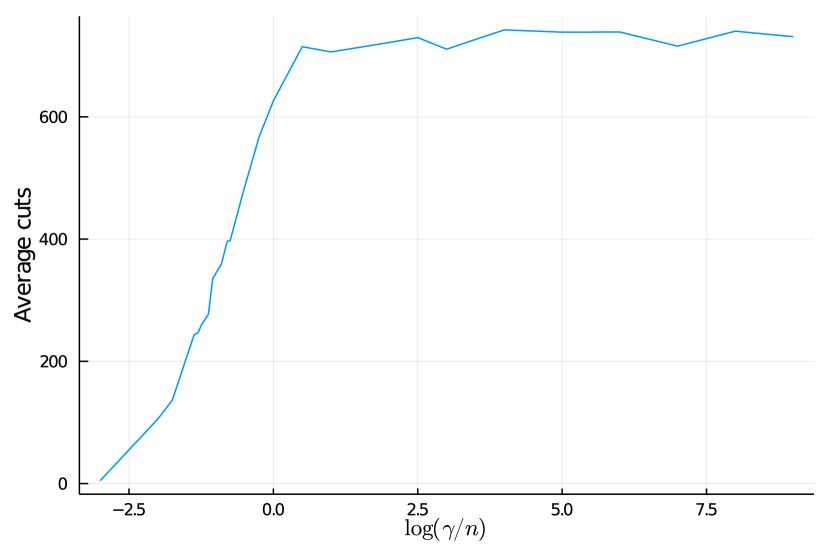

Our final experiment studies the impact of the regularizer on both solve times and the number of cuts generated, in order to justify our assertion in the introduction that increasing the amount of regularization in the problem makes the problem easier. In this direction, we solve the ten and instances with minimum investment and minimum return constraints studied in Section 5.2 for different values of (with the copy of variables technique and in-out method on). We report the average runtime and number of cuts generated by Algorithm 3 across the instances for each in Figures 3 () and 4 ().

Observe that the average runtime is essentially non-decreasing in , and for both and there exists a finite at which all instances can be solved using a single cut. This empirically verifies Section 3.4’s sensitivity analysis findings.

5.5 Summary of Findings From Numerical Experiments

We are now in a position to answer the four questions introduced at the start of this section. Our findings are as follows:

-

1.

In the absence of complicating constraints, Algorithm 3 is substantially more efficient than commercial MIQO solvers such as

CPLEX. This efficiency improvement can be explained by (a) our ability to generate stronger and more informative lower bounds via dual subproblems, and (b) our dual representation of the problems’ subgradients. Indeed, the method did not require more than one second to solve any of the constraint-free problems considered here, although this phenomenon can be partially attributed to the problem data used. Moreover, the solve times are comparable to those reported by other recent methods such as Zheng et al. (2014), Frangioni et al. (2016, 2017); note that this comparison is imperfect since the cited approaches were run on different machines and their source code is unavailable, which precludes a truly fair comparison. -

2.

Although imposing complicating constraints, such as minimum investment constraints, slows Algorithm 3, the method performs competitively in the presence of these constraints. Moreover, running the

in-outcutting-plane method at the root node substantially reduces the initial bound gap, and allows the method to supply a certifiably near-optimal (if not optimal) solution in seconds. This suggests that running thein-outmethod at the root node should be considered as a viable and more scalable alternative to existing root node techniques, particularly in the presence of complicating constraints such as minimum investment constraints, or if the cardinality budget is at least (although it can do more harm than good for easier problems). -

3.

Algorithm 3 scales to solve real-world problem instances which comprise selecting assets from universes with thousands of securities, such as the Russell and the Wilshire , while existing commercial solvers such as

CPLEXeither solve these problems much more slowly or do not successfully solve them, because they cannot attain sufficiently strong lower bounds quickly. -

4.

Solutions to Problem (4) are stable with respect to the hyperparameter .

Acknowledgments

We are grateful to the anonymous referees of this and previous versions of the paper for insightful comments which improved the quality of the manuscript, Brad Sturt for editorial comments on a previous version of the paper, and Jean Pauphilet for providing a Julia implementation of the in-out method.

References

- Abadie (1967) Abadie J (1967) On the Kuhn-Tucker theorem. Nonlinear programming (North-Holland Publishing Co., Amsterdam).

- Ahmadi et al. (2017) Ahmadi AA, Dash S, Hall G (2017) Optimization over structured subsets of positive semidefinite matrices via column generation. Disc. Optim. 24:129–151.

- Aktürk et al. (2009) Aktürk MS, Atamtürk A, Gürel S (2009) A strong conic quadratic reformulation for machine-job assignment with controllable processing times. Oper. Res. Letters 37(3):187–191.

- Barker and Carlson (1975) Barker G, Carlson D (1975) Cones of diagonally dominant matrices. Pacific Journal of Mathematics 57(1):15–32.

- Beasley (1990) Beasley JE (1990) OR-library: distributing test problems by electronic mail. J. Oper. Res. Soc. 41(11):1069–1072.

- Ben-Ameur and Neto (2007) Ben-Ameur W, Neto J (2007) Acceleration of cutting-plane and column generation algorithms: Applications to network design. Networks 49(1):3–17.

- Ben-Tal and Nemirovski (2001) Ben-Tal A, Nemirovski A (2001) Lectures on modern convex optimization: Analysis, algorithms, and engineering applications, volume 2 (SIAM Philadelphia, PA).

- Benders (1962) Benders JF (1962) Partitioning procedures for solving mixed-variables programming problems. Numerische mathematik 4(1):238–252.

- Bertsimas and Cory-Wright (2020) Bertsimas D, Cory-Wright R (2020) On polyhedral and second-order cone decompositions of semidefinite optimization problems. Oper. Res. Letters 48(1):78–85.

- Bertsimas et al. (2019) Bertsimas D, Cory-Wright R, Pauphilet J (2019) A unified approach to mixed-integer optimization problems with logical constraints. arXiv:1907.02109 .

- Bertsimas et al. (1999) Bertsimas D, Darnell C, Soucy R (1999) Portfolio construction through mixed-integer programming at Grantham, Mayo, van Otterloo and company. Interfaces 29(1):49–66.

- Bertsimas et al. (2016) Bertsimas D, King A, Mazumder R (2016) Best subset selection via a modern optimization lens. Ann. Statist. 44(2):813–852.

- Bertsimas and Shioda (2009) Bertsimas D, Shioda R (2009) Algorithm for cardinality-constrained quadratic optimization. Comput. Optim. Appl. 43(1):1–22.

- Bertsimas and Tsitsiklis (1997) Bertsimas D, Tsitsiklis JN (1997) Introduction to linear optimization, volume 6 (Athena Scientific Belmont, MA).

- Bertsimas and Van Parys (2020) Bertsimas D, Van Parys B (2020) Sparse high-dimensional regression: Exact scalable algorithms and phase transitions. Ann. Stat. 48(1):300–323.

- Bertsimas and Weismantel (2005) Bertsimas D, Weismantel R (2005) Optimization over integers, volume 13 (Dynamic Ideas Belmont).

- Bienstock (1996) Bienstock D (1996) Computational study of a family of mixed-integer quadratic programming problems. Math. Prog. 74(2):121–140.

- Bienstock (2010) Bienstock D (2010) Eigenvalue techniques for proving bounds for convex objective, nonconvex programs. IPCO 29.

- Bonami and Lejeune (2009) Bonami P, Lejeune MA (2009) An exact solution approach for portfolio optimization problems under stochastic and integer constraints. Oper. Res. 57(3):650–670.

- Borchers and Mitchell (1997) Borchers B, Mitchell JE (1997) A computational comparison of branch and bound and outer approximation algorithms for 0–1 mixed integer nonlinear programs. Comp. & Oper. Res. 24(8):699–701.

- Boyd and Vandenberghe (2004) Boyd S, Vandenberghe L (2004) Convex Optimization (Cambridge University Press, Cambridge, UK).

- Burdakov et al. (2016) Burdakov OP, Kanzow C, Schwartz A (2016) Mathematical programs with cardinality constraints: reformulation by complementarity-type conditions and a regularization method. SIAM J. Opt. 26(1):397–425.

- Carrasco and Noumon (2011) Carrasco M, Noumon N (2011) Optimal portfolio selection using regularization. Technical report, University of Montreal.