Sparse Logistic Regression Learns All Discrete Pairwise Graphical Models

Abstract

We characterize the effectiveness of a classical algorithm for recovering the Markov graph of a general discrete pairwise graphical model from i.i.d. samples. The algorithm is (appropriately regularized) maximum conditional log-likelihood, which involves solving a convex program for each node; for Ising models this is -constrained logistic regression, while for more general alphabets an group-norm constraint needs to be used. We show that this algorithm can recover any arbitrary discrete pairwise graphical model, and also characterize its sample complexity as a function of model width, alphabet size, edge parameter accuracy, and the number of variables. We show that along every one of these axes, it matches or improves on all existing results and algorithms for this problem. Our analysis applies a sharp generalization error bound for logistic regression when the weight vector has an constraint (or constraint) and the sample vector has an constraint (or constraint). We also show that the proposed convex programs can be efficiently solved in running time (where is the number of variables) under the same statistical guarantees. We provide experimental results to support our analysis.

1 Introduction

Undirected graphical models provide a framework for modeling high dimensional distributions with dependent variables and have many applications including in computer vision (Choi et al.,, 2010), bio-informatics (Marbach et al.,, 2012), and sociology (Eagle et al.,, 2009). In this paper we characterize the effectiveness of a natural, and already popular, algorithm for the structure learning problem. Structure learning is the task of finding the dependency graph of a Markov random field (MRF) given i.i.d. samples; typically one is also interested in finding estimates for the edge weights as well. We consider the structure learning problem in general (non-binary) discrete pairwise graphical models. These are MRFs where the variables take values in a discrete alphabet, but all interactions are pairwise. This includes the Ising model as a special case (which corresponds to a binary alphabet).

The natural and popular algorithm we consider is (appropriately regularized) maximum conditional log-likelihood for finding the neighborhood set of any given node. For the Ising model, this becomes -constrained logistic regression; more generally for non-binary graphical models the regularizer becomes an norm. We show that this algorithm can recover all discrete pairwise graphical models, and characterize its sample complexity as a function of the parameters of interest: model width, alphabet size, edge parameter accuracy, and the number of variables. We match or improve dependence on each of these parameters, over all existing results for the general alphabet case when no additional assumptions are made on the model (see Table 2). For the specific case of Ising models, some recent work has better dependence on some parameters (see Table 2 in Appendix A).

We now describe the related work, and then outline our contributions.

Related Work

In a classic paper, Ravikumar et al., (2010) considered the structure learning problem for Ising models. They showed that -regularized logistic regression provably recovers the correct dependency graph with a very small number of samples by solving a convex program for each variable. This algorithm was later generalized to multi-class logistic regression with group-sparse regularization, which can learn MRFs with higher-order interactions and non-binary variables (Jalali et al.,, 2011). A well-known limitation of (Ravikumar et al.,, 2010; Jalali et al.,, 2011) is that their theoretical guarantees only work for a restricted class of models. Specifically, they require that the underlying learned model satisfies technical incoherence assumptions, that are difficult to validate or check.

| Paper | Assumptions | Sample complexity () |

| Greedy algorithm (Hamilton et al.,, 2017) | 1. Alphabet size | |

| 2. Model width | ||

| 3. Degree | ||

| 4. Minimum edge weight | ||

| 5. Probability of success | ||

| Sparsitron (Klivans and Meka,, 2017) | 1. Alphabet size | |

| 2. Model width | ||

| 3. Minimum edge weight | ||

| 4. Probability of success | ||

| -constrained logistic regression [this paper] | 1. Alphabet size | |

| 2. Model width | ||

| 3. Minimum edge weight | ||

| 4. Probability of success |

A large amount of recent work has since proposed various algorithms to obtain provable learning results for general graphical models without requiring the incoherence assumptions. We now describe the (most related part of the extensive) related work, followed by our results and comparisons (see Table 2). For a discrete pairwise graphical model, let be the number of variables and be the alphabet size; define the model width as the maximum neighborhood weight (see Definition 1 and 2 for the precise definition). For structure learning algorithms, a popular approach is to focus on the sub-problem of finding the neighborhood of a single node. Once this is correctly learned, the overall graph structure is a simple union bound. Indeed all the papers we now discuss are of this type. As shown in Table 2, Hamilton et al., (2017) proposed a greedy algorithm to learn pairwise (and higher-order) MRFs with general alphabet. Their algorithm generalizes the approach of Bresler, (2015) for learning Ising models. The sample complexity in (Hamilton et al.,, 2017) grows logarithmically in , but doubly exponentially in the width . Note that an information-theoretic lower bound for learning Ising models (Santhanam and Wainwright,, 2012) only has a single-exponential dependence on . Klivans and Meka, (2017) provided a different algorithmic and theoretical approach by setting this up as an online learning problem and leveraging results from the Hedge algorithm therein. Their algorithm Sparsitron achieves single-exponential dependence on the width .

Our Contributions

-

•

Our main result: We show that the -constrained333It may be possible to prove a similar result for the regularized version of the optimization problem using techniques from (Negahban et al.,, 2012). One needs to prove that the objective function satisfies restricted strong convexity (RSC) when the samples are from a graphical model distribution (Vuffray et al.,, 2016; Lokhov et al.,, 2018). It is interesting to see if the proof presented in this paper is related to the RSC condition. logistic regression can be used to estimate the edge weights of a discrete pairwise graphical model from i.i.d. samples (see Theorem 15). For the special case of Ising models (see Theorem 6), this reduces to an -constrained logistic regression. We make no incoherence assumption on the graphical models. As shown in Table 2, our sample complexity scales as , which improves the previous best result with dependency444This improvement essentially comes from the fact that we are using an norm constraint instead of an norm constraint for learning general (i.e., non-binary) pairwise graphical models (see our remark after Theorem 15). The Sparsitron algorithm proposed by Klivans and Meka, (2017) learns a -constrained generalized linear model. This -constraint gives rise to a dependency for learning non-binary pairwise graphical models.. The analysis applies a sharp generalization error bound for logistic regression when the weight vector has an constraint (or constraint) and the sample vector has an constraint (or constraint) (see Lemma 20 and Lemma 30 in Appendix B). Our key insight is that a generalization bound can be used to control the squared distance between the predicted and true logistic functions (see Lemma 1 and Lemma 2 in Section 3.2), which then implies an norm bound between the weight vectors (see Lemma 5 and Lemma 7).

-

•

We show that the proposed algorithms can run in time without affecting the statistical guarantees (see Section 2.3). Note that is an efficient runtime for graph recovery over nodes. Previous algorithms in (Hamilton et al.,, 2017; Klivans and Meka,, 2017) also require runtime for structure learning of pairwise graphical models.

-

•

We construct examples that violate the incoherence condition proposed in (Ravikumar et al.,, 2010) (see Figure 1). We then run -constrained logistic regression and show that it can recover the graph structure as long as given enough samples. This verifies our analysis and shows that our conditions for graph recovery are weaker than those in (Ravikumar et al.,, 2010).

- •

Notation. We use to denote the set . For a vector , we use or to denote its -th coordinate. The norm of a vector is defined as . We use to denote the vector after deleting the -th coordinate. For a matrix , we use or to denote its -th entry. We use and to the denote the -th row vector and the -th column vector. The norm of a matrix is defined as . We define throughout the paper (note that this definition is different from the induced matrix norm). We use to represent the sigmoid function. We use to represent the dot product between two vectors or two matrices .

2 Main results

We start with the special case of binary variables (i.e., Ising models), and then move to the general case with non-binary variables.

2.1 Learning Ising models

We first give a definition of an Ising model distribution.

Definition 1.

Let be a symmetric weight matrix with for . Let be a mean-field vector. The -variable Ising model is a distribution on that satisfies

| (1) |

The dependency graph of is an undirected graph , with vertices and edges . The width of is defined as

| (2) |

Let be the minimum edge weight in absolute value, i.e., .

One property of an Ising model distribution is that the conditional distribution of any variable given the rest variables follows a logistic function. Let be the sigmoid function.

Fact 1.

Let and . For any , the conditional probability of the -th variable given the states of all other variables is

| (3) |

where , and . Moreover, satisfies , where is the model width defined in Definition 1.

Following Fact 1, the natural approach to estimating the edge weights is to solve a logistic regression problem for each variable. For ease of notation, let us focus on the -th variable (the algorithm directly applies to the rest variables). Given i.i.d. samples , where from an Ising model , we first transform the samples into , where and . By Fact 1, we know that where satisfies . Suppose that , we are then interested in recovering by solving the following -constrained logistic regression problem

| (4) |

where is the loss function

| (5) |

Eq. (5) is essentially the negative log-likelihood of observing given at the current .

Let be a minimizer of (4). It is worth noting that in the high-dimensional regime (), may not be unique. In this case, we will show that any one of them would work. After solving the convex problem in (4), the edge weight is estimated as .

The pseudocode of the above algorithm is given in Algorithm 1. Solving the -constrained logistic regression problem will give us an estimator of the true edge weight. We then form the graph by keeping the edge that has estimated weight larger than (in absolute value).

Theorem 1.

Let be an unknown -variable Ising model distribution with dependency graph . Suppose that the has width . Given and , if the number of i.i.d. samples satisfies , then with probability at least , Algorithm 1 produces that satisfies

| (6) |

2.2 Learning pairwise graphical models over general alphabet

Definition 2.

Let be the alphabet size. Let be a set of weight matrices satisfying . Without loss of generality, we assume that every row (and column) vector of has zero mean. Let be a set of external field vectors. Then the -variable pairwise graphical model is a distribution over where

| (7) |

The dependency graph of is an undirected graph , with vertices and edges . The width of is defined as

| (8) |

We define .

Remark. The assumption that has centered rows and columns (i.e., and for any ) is without loss of generality (see Fact 8.2 in (Klivans and Meka,, 2017)). If the -th row of is not centered, i.e., , we can define and , and notice that . Because the sets of matrices with centered rows and columns (i.e., and ) are two linear subspaces, alternatively projecting onto the two sets will converge to the intersection of the two subspaces (Von Neumann,, 1949). As a result, the condition of centered rows and columns is necessary for recovering the underlying weight matrices, since otherwise different parameters can give the same distribution. Note that in the case of , Definition 2 is the same as Definition 1 for Ising models. To see their connection, simply define as follows: , .

For a pairwise graphical model distribution , the conditional distribution of any variable (when restricted to a pair of values) given all the other variables follows a logistic function, as shown in Fact 2. This is analogous to Fact 1 for the Ising model distribution.

Fact 2.

Let and . For any , any , and any ,

| (9) |

Given i.i.d. samples , where for , the goal is to estimate matrices for all . For ease of notation and without loss of generality, let us consider the -th variable. Now the goal is to estimate matrices for all .

To use Fact 2, fix a pair of values , let be the set of samples satisfying . We next transform the samples in to as follows: , if , and if . Here is a function that maps a value to the standard basis vector , where has a single 1 at the -th entry. For each sample in the set , Fact 2 implies that , where satisfies

| (10) |

Suppose that the width of satisfies , then defined in (10) satisfies , where . We can now form an -constrained logistic regression over the samples in :

| (11) |

Let be a minimizer of (11). Without loss of generality, we can assume that the first rows of are centered, i.e., for . Otherwise, we can always define a new matrix by centering the first rows of :

| (12) | ||||

Since each row of the matrix in (11) is a standard basis vector (i.e., all zeros except a single one), , which implies that is also a minimizer of (11).

The key step in our proof is to show that given enough samples, the obtained matrix is close to defined in (10). Specifically, we will prove that

| (13) |

Recall that our goal is to estimate the original matrices for all . Summing (13) over (suppose ) and using the fact that gives

| (14) |

In other words, is a good estimate of .

Suppose that , once we obtain the estimates , the last step is to form a graph by keeping the edge that satisfies . The pseudocode of the above algorithm is given in Algorithm 2.

Theorem 2.

Let be an -variable pairwise graphical model distribution with width . Given and , if the number of i.i.d. samples satisfies , then with probability at least , Algorithm 2 produces that satisfies

| (15) |

Corollary 2.

Remark ( versus constraint). The matrix defined in (10) satisfies . This implies that and . Instead of solving the -constrained logistic regression defined in (11), we could solve an -constrained logistic regression with . However, this will lead to a sample complexity that scales as , which is worse than the sample complexity achieved by the -constrained logistic regression. The reason why we use the constraint instead of the tighter constraint in the algorithm is because our proof relies on a sharp generalization bound for -constrained logistic regression (see Lemma 30 in the appendix). It is unclear whether a similar generalization bound exists for the constraint.

Remark (lower bound on the alphabet size). A simple lower bound is . To see why, consider a graph with two nodes (i.e., ). Let be a -by- weight matrix between the two nodes, defined as follows: , , and otherwise. This definition satisfies the condition that every row and column is centered (Definition 2). Besides, we have and , which means that the two quantities do not scale in . To distinguish from the zero matrix, we need to observe samples in the set . This requires samples because any specific sample (where and ) has a probability of approximately to show up.

2.3 Learning pairwise graphical models in time

Our results so far assume that the -constrained logistic regression (in Algorithm 1) and the -constrained logistic regression (in Algorithm 2) can be solved exactly. This would require complexity if an interior-point based method is used (Koh et al.,, 2007). The goal of this section is to reduce the runtime to via first-order optimization method. Note that is an efficient time complexity for graph recovery over nodes. Previous structural learning algorithms of Ising models require either complexity (e.g., (Bresler,, 2015; Klivans and Meka,, 2017)) or a worse complexity (e.g., (Ravikumar et al.,, 2010; Vuffray et al.,, 2016) require runtime). We would like to remark that our goal here is not to give the fastest first-order optimization algorithm (see our remark after Theorem 4). Instead, our contribution is to provably show that it is possible to run Algorithm 1 and Algorithm 2 in time without affecting the original statistical guarantees.

To better exploit the problem structure555Specifically, for the -constrained logisitic regression defined in (4), since the input sample satisifies , the loss function is -Lipschitz w.r.t. . Similarly, for the -constrained logisitic regression defined in (11), the loss function is -Lipschitz w.r.t. because the input sample satisfies ., we use the mirror descent algorithm666Other approaches include the standard projected gradient descent and the coordinate descent. Their convergence rates depend on either the smoothness or the Lipschitz constant (w.r.t. ) of the objective function (Bubeck,, 2015). This would lead to a total runtime of for our problem setting. Another option would be the composite gradient descent method, the analysis of which relies on the restricted strong convexity of the objective function (Agarwal et al.,, 2010). For other variants of mirror descent algorithms, see the remark after Theorem 4. with a properly chosen distance generating function (aka the mirror map). Following the standard mirror descent setup, we use negative entropy as the mirror map for -constrained logistic regression and a scaled group norm for -constrained logistic regression (see Section 5.3.3.2 and Section 5.3.3.3 in (Ben-Tal and Nemirovski,, 2013) for more details). The pseudocode is given in Appendix H. The main advantage of mirror descent algorithm is that its convergence rate scales logarithmically in the dimension (see Lemma 57 in Appendix I). Specifically, let be the output after mirror descent iterations, then satisfies

| (16) |

where is the empirical logistic loss, and is the actual minimizer of . Since each mirror descent update requires time, where is the number of samples and scales as , and we have to solve regression problems (one for each variable in ), the total runtime scales as , which is our desired runtime.

There is still one problem left, that is, we have to show that (where is the minimizer of the true loss ) in order to conclude that Theorem 6 and 15 still hold when using mirror descent algorithms. Since is not strongly convex, (16) alone does not necessarily imply that is small. Our key insight is that in the proof of Theorem 6 and 15, the definition of (as a minimizer of ) is only used to show that (see inequality (b) of (28) in Appendix B). It is then possible to replace this step with (16) in the original proof, and prove that Theorem 6 and 15 still hold as long as is small enough (see (60) in Appendix I).

Our key results in this section are Theorem 3 and Theorem 4, which show that Algorithm 1 and Algorithm 2 can run in time without affecting the original statistical guarantees.

Theorem 3.

In the setup of Theorem 6, suppose that the -constrained logistic regression in Algorithm 1 is optimized by the mirror descent method (Algorithm 3) given in Appendix H. Given and , if the number of mirror descent iterations satisfies , and the number of samples satisfies , then (6) still holds with probability at least . The total time complexity of Algorithm 1 is .

Theorem 4.

In the setup of Theorem 15, suppose that the -constrained logistic regression in Algorithm 2 is optimized by the mirror descent method (Algorithm 4) given in Appendix H. Given and , if the number of mirror descent iterations satisfies , and the number of samples satisfies , then (15) still holds with probability at least . The total time complexity of Algorithm 2 is .

Remark. It is possible to improve the time complexity given in Theorem 3 and 4 (especially the dependence on and ), by using stochastic or accelerated versions of mirror descent algorithms (instead of the batch version given in Appendix H). In fact, the Sparsitron algorithm proposed by Klivans and Meka, (2017) can be seen as an online mirror descent algorithm for optimizing the -constrained logistic regression (see Algorithm 3 in Appendix H). Furthermore, Algorithm 1 and 2 can be parallelized as every node has an independent regression problem.

3 Analysis

3.1 Proof outline

We give a proof outline for Theorem 6. The proof of Theorem 15 follows a similar outline. Let be a distribution over , where satisfies . Let and be the expected and empirical logistic loss. Suppose . Let s.t. . Our goal is to prove that is small when the samples are constructed from an Ising model distribution. Our proof can be summarized in three steps:

- 1.

- 2.

- 3.

For the general setting with non-binary alphabet (i.e., Theorem 15), the proof is similar to that of Theorem 6. The main difference is that we need to use a sharp generalization bound when and (see Lemma 30 in Appendix B). This would give us Lemma 2 (instead of Lemma 1 for the Ising models). The last step is to use Lemma 7 to bound the infinity norm between the two weight matrices.

3.2 Supporting lemmas

Lemma 1 and Lemma 2 are the key results in our proof. They essentially say that given enough samples, solving the corresponding constrained logistic regression problem will provide a prediction close to the true in terms of their expected squared distance.

Lemma 1.

Let be a distribution on where for , . We assume that for a known . Given i.i.d. samples , let be any minimizer of the following -constrained logistic regression problem:

| (17) |

Given and , if the number of samples satisfies , then with probability at least over the samples, .

Lemma 2.

Let be a distribution on , where . Furthermore, satisfies , where . We assume that for a known . Given i.i.d. samples from , let be any minimizer of the following -constrained logistic regression problem:

| (18) |

Given and , if the number of samples satisfies , then with probability at least over the samples, .

The proofs of Lemma 1 and Lemma 2 are given in Appendix B. Note that in the setup of both lemmas, we form a pair of dual norms for and , e.g., and in Lemma 2, and and in Lemma 1. This duality allows us to use a sharp generalization bound with a sample complexity that scales logarithmic in the dimension (see Lemma 20 and Lemma 30 in Appendix B).

Definition 3 defines a -unbiased distribution. This notion of -unbiasedness is proposed by Klivans and Meka, (2017).

Definition 3.

Let be the alphabet set, e.g., for Ising model and for an alphabet of size . A distribution on is -unbiased if for , any , and any assignment to , .

For a -unbiased distribution, any of its marginal distribution is also -unbiased (see Lemma 3).

Lemma 3.

Let be a -unbiased distribution on , where is the alphabet set. For , any , the distribution of is also -unbiased.

Lemma 4 describes the -unbiased property of graphical models. This property has been used in the previous papers (e.g., (Klivans and Meka,, 2017; Bresler,, 2015)).

Lemma 4.

Let be a pairwise graphical model distribution with alphabet size and width . Then is -unbiased with . Specifically, an Ising model distribution is -unbiased.

In Lemma 1 and Lemma 2, we give a sample complexity bound for achieving a small error between and . The following two lemmas show that if the sample distribution is -unbiased, then a small error implies a small distance between and .

Lemma 5.

Let be a -unbiased distribution on . Suppose that for two vectors and , , where . Then .

Lemma 6.

Let be a -unbiased distribution on . For , let be the one-hot encoded . Let be two matrices satisfying and , for . Suppose that for some and , we have , where . Then777For a matrix , we define . Note that this is different from the induced matrix norm. .

3.3 Proof sketches

We provide proof sketches for Theorem 6 and Theorem 15 using the supporting lemmas. The detailed proof can be found in Appendix F and G.

Proof sketch of Theorem 6. Without loss of generality, let us consider the -th variable. Let , and . By Fact 1 and Lemma 1, if , then with probability at least . By Lemma 4 and Lemma 3, is -unbiased with . We can then apply Lemma 5 to show that if , then with probability at least . Theorem 6 then follows by a union bound over all variables.

Proof sketch of Theorem 15. Let us again consider the -th variable since the proof is the same for all other variables. As described before, the key step is to show that (13) holds. Now fix a pair of , let be the number of samples such that the -th variable is either or . By Fact 2 and Lemma 2, if , then with probability at least , the matrix satisfies , where is defined in (10). By Lemma 7 and Lemma 4, if , then with probability at least , . Since is -unbiased with , in order to have samples for a given pair, we need the total number of samples to satisfy . Theorem 15 then follows by setting and taking a union bound over all pairs and all variables.

4 Experiments

In both simulations below, we assume that the external field is zero. Sampling is done via exactly computing the distribution.

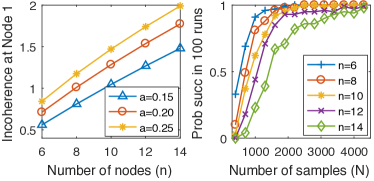

Learning Ising models. In Figure 1 we construct a diamond-shape graph and show that the incoherence value at Node 1 becomes bigger than 1 (and hence violates the incoherence condition in (Ravikumar et al.,, 2010)) when we increase the graph size and edge weight . We then run 100 times of Algorithm 1 and plot the fraction of runs that exactly recovers the underlying graph structure. In each run we generate a different set of samples. The result shown in Figure 1 is consistent with our analysis and also indicates that our conditions for graph recovery are weaker than those in (Ravikumar et al.,, 2010).

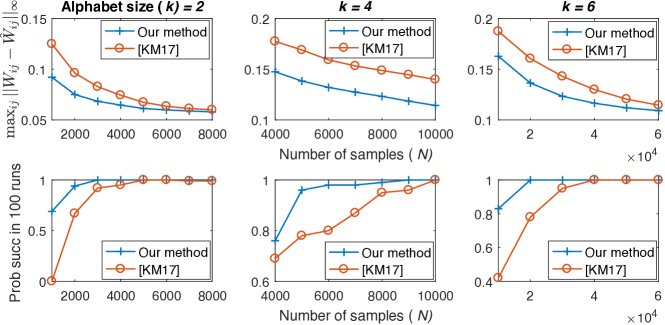

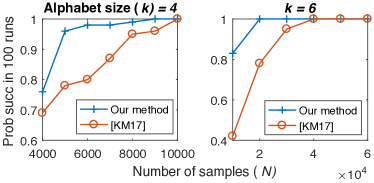

Learning general pairwise graphical models. We compare our algorithm (Algorithm 2) with the Sparsitron algorithm in (Klivans and Meka,, 2017) on a two-dimensional 3-by-3 grid (shown in Figure 2). We experiment two alphabet sizes: . For each value of , we simulate both algorithms 100 runs, and in each run we generate random matrices with entries . As shown in the Figure 2, our algorithm requires fewer samples for successfully recovering the graphs. More details about this experiment can be found in Appendix J.

5 Conclusion

We have shown that the -constrained logistic regression can recover the Markov graph of any discrete pairwise graphical model from i.i.d. samples. For the Ising model, it reduces to the -constrained logistic regression. This algorithm has better sample complexity than the previous state-of-the-art result ( versus ), and can run in time. One interesting direction for future work is to see if the dependency in the sample complexity can be improved. Another interesting direction is to consider MRFs with higher-order interactions.

References

- Agarwal et al., (2010) Agarwal, A., Negahban, S., and Wainwright, M. J. (2010). Fast global convergence rates of gradient methods for high-dimensional statistical recovery. In Advances in Neural Information Processing Systems, pages 37–45.

- Aurell and Ekeberg, (2012) Aurell, E. and Ekeberg, M. (2012). Inverse ising inference using all the data. Physical review letters, 108(9):090201.

- Banerjee et al., (2008) Banerjee, O., Ghaoui, L. E., and d’Aspremont, A. (2008). Model selection through sparse maximum likelihood estimation for multivariate gaussian or binary data. Journal of Machine learning research, 9(Mar):485–516.

- Bartlett and Mendelson, (2002) Bartlett, P. L. and Mendelson, S. (2002). Rademacher and gaussian complexities: Risk bounds and structural results. Journal of Machine Learning Research, 3(Nov):463–482.

- Ben-Tal and Nemirovski, (2013) Ben-Tal, A. and Nemirovski, A. (Fall 2013). Lectures on modern convex optimization. https://www2.isye.gatech.edu/~nemirovs/Lect_ModConvOpt.pdf.

- Bento and Montanari, (2009) Bento, J. and Montanari, A. (2009). Which graphical models are difficult to learn? In Advances in Neural Information Processing Systems, pages 1303–1311.

- Bresler, (2015) Bresler, G. (2015). Efficiently learning ising models on arbitrary graphs. In Proceedings of the forty-seventh annual ACM symposium on Theory of computing (STOC), pages 771–782. ACM.

- Bubeck, (2015) Bubeck, S. (2015). Convex optimization: Algorithms and complexity. Foundations and Trends® in Machine Learning, 8(3-4):231–357.

- Choi et al., (2010) Choi, M. J., Lim, J. J., Torralba, A., and Willsky, A. S. (2010). Exploiting hierarchical context on a large database of object categories. In Computer vision and pattern recognition (CVPR), 2010 IEEE conference on, pages 129–136. IEEE.

- Eagle et al., (2009) Eagle, N., Pentland, A. S., and Lazer, D. (2009). Inferring friendship network structure by using mobile phone data. Proceedings of the national academy of sciences, 106(36):15274–15278.

- Hamilton et al., (2017) Hamilton, L., Koehler, F., and Moitra, A. (2017). Information theoretic properties of markov random fields, and their algorithmic applications. In Advances in Neural Information Processing Systems, pages 2463–2472.

- Jalali et al., (2011) Jalali, A., Ravikumar, P., Vasuki, V., and Sanghavi, S. (2011). On learning discrete graphical models using group-sparse regularization. In Proceedings of the Fourteenth International Conference on Artificial Intelligence and Statistics, pages 378–387.

- Kakade et al., (2012) Kakade, S. M., Shalev-Shwartz, S., and Tewari, A. (2012). Regularization techniques for learning with matrices. Journal of Machine Learning Research, 13(Jun):1865–1890.

- Kakade et al., (2009) Kakade, S. M., Sridharan, K., and Tewari, A. (2009). On the complexity of linear prediction: Risk bounds, margin bounds, and regularization. In Advances in neural information processing systems, pages 793–800.

- Klivans and Meka, (2017) Klivans, A. R. and Meka, R. (2017). Learning graphical models using multiplicative weights. In Proceedings of the 58th Annual IEEE Symposium on Foundations of Computer Science (FOCS), pages 343–354. IEEE.

- Koh et al., (2007) Koh, K., Kim, S.-J., and Boyd, S. (2007). An interior-point method for large-scale -regularized logistic regression. Journal of Machine learning research, 8(Jul):1519–1555.

- Lee et al., (2007) Lee, S.-I., Ganapathi, V., and Koller, D. (2007). Efficient structure learning of markov networks using -regularization. In Advances in neural Information processing systems, pages 817–824.

- Lokhov et al., (2018) Lokhov, A. Y., Vuffray, M., Misra, S., and Chertkov, M. (2018). Optimal structure and parameter learning of ising models. Science advances, 4(3):e1700791.

- Marbach et al., (2012) Marbach, D., Costello, J. C., Küffner, R., Vega, N. M., Prill, R. J., Camacho, D. M., Allison, K. R., Consortium, T. D., Kellis, M., Collins, J. J., and Stolovitzky, G. (2012). Wisdom of crowds for robust gene network inference. Nature methods, 9(8):796.

- Negahban et al., (2012) Negahban, S. N., Ravikumar, P., Wainwright, M. J., and Yu, B. (2012). A unified framework for high-dimensional analysis of -estimators with decomposable regularizers. Statistical Science, 27(4):538–557.

- Ravikumar et al., (2010) Ravikumar, P., Wainwright, M. J., and Lafferty, J. D. (2010). High-dimensional ising model selection using -regularized logistic regression. The Annals of Statistics, 38(3):1287–1319.

- Rigollet and Hütter, (2017) Rigollet, P. and Hütter, J.-C. (Spring 2017). Lectures notes on high dimensional statistics. http://www-math.mit.edu/~rigollet/PDFs/RigNotes17.pdf.

- Santhanam and Wainwright, (2012) Santhanam, N. P. and Wainwright, M. J. (2012). Information-theoretic limits of selecting binary graphical models in high dimensions. IEEE Transactions on Information Theory, 58(7):4117–4134.

- Shalev-Shwartz and Ben-David, (2014) Shalev-Shwartz, S. and Ben-David, S. (2014). Understanding machine learning: From theory to algorithms. Cambridge university press.

- Von Neumann, (1949) Von Neumann, J. (1949). On rings of operators. reduction theory. Annals of Mathematics, pages 401–485.

- Vuffray et al., (2016) Vuffray, M., Misra, S., Lokhov, A., and Chertkov, M. (2016). Interaction screening: Efficient and sample-optimal learning of ising models. In Advances in Neural Information Processing Systems, pages 2595–2603.

- Yang et al., (2012) Yang, E., Allen, G., Liu, Z., and Ravikumar, P. K. (2012). Graphical models via generalized linear models. In Advances in Neural Information Processing Systems, pages 1358–1366.

- Yuan and Lin, (2007) Yuan, M. and Lin, Y. (2007). Model selection and estimation in the gaussian graphical model. Biometrika, 94(1):19–35.

Appendix A Related work on learning Ising models

For the special case of learning Ising models (i.e., binary variables), we compare the sample complexity among different graph recovery algorithms in Table 2.

| Paper | Assumptions | Sample complexity () |

| Information-theoretic lower bound (Santhanam and Wainwright,, 2012) | 1. Model width , and | , |

| 2. Degree | , | |

| 3. Minimum edge weight | ||

| 4. External field | ||

| -regularized logistic regression (Ravikumar et al.,, 2010) | is the Fisher information matrix, | |

| is set of neighbors of a given variable. | ||

| 1. Dependency: such that | ||

| eigenvalues of | ||

| 2. Incoherence: such that | ||

| 3. Regularization parameter: | ||

| 4. Minimum edge weight | ||

| 5. External field | ||

| 6. Probability of success | ||

| Greedy algorithm (Bresler,, 2015) | 1. Model width | |

| 2. Degree | ||

| 3. Minimum edge weight | ||

| 4. Probability of success | ||

| Interaction Screening (Vuffray et al.,, 2016) | 1. Model width | |

| 2. Degree | ||

| 3. Minimum edge weight | ||

| 4. Regularization parameter | ||

| 5. Probability of success | ||

| -regularized logistic regression (Lokhov et al.,, 2018) | 1. Model width | |

| 2. Degree | ||

| 3. Minimum edge weight | ||

| 4. Regularization parameter | ||

| 5. Probability of success | ||

| -constrained logistic regression (Rigollet and Hütter,, 2017) | 1. Model width | |

| 2. Minimum edge weight | ||

| 3. Probability of success | ||

| Sparsitron (Klivans and Meka,, 2017) | 1. Model width | |

| 2. Minimum edge weight | ||

| 3. Probability of success | ||

| -constrained logistic regression [this paper] | 1. Model width | |

| 2. Minimum edge weight | ||

| 3. Probability of success |

Note that the algorithms in (Ravikumar et al.,, 2010; Bresler,, 2015; Vuffray et al.,, 2016; Lokhov et al.,, 2018) are designed for learning Ising models instead of general pairwise graphical models. Hence, they are not presented in Table 2.

As mentioned in the Introduction, Ravikumar et al., (2010) consider -regularized logistic regression for learning Ising models in the high-dimensional setting. They require incoherence assumptions that ensure, via conditions on sub-matrices of the Fisher information matrix, that sparse predictors of each node are hard to confuse with a false set. Their analysis obtains significantly better sample complexity compared to what is possible when these extra assumptions are not imposed (see (Bento and Montanari,, 2009)). Others have also considered -regularization (e.g., (Lee et al.,, 2007; Yuan and Lin,, 2007; Banerjee et al.,, 2008; Jalali et al.,, 2011; Yang et al.,, 2012; Aurell and Ekeberg,, 2012)) for structure learning of Markov random fields but they all require certain assumptions about the graphical model and hence their methods do not work for general graphical models. The analysis of (Ravikumar et al.,, 2010) is of essentially the same convex program as this work (except that we have an additional thresholding procedure). The main difference is that they obtain a better sample guarantee but require significantly more restrictive assumptions.

In the general setting with no restrictions on the model, Santhanam and Wainwright, (2012) provide an information-theoretic lower bound on the number of samples needed for graph recovery. This lower bound depends logarithmically on , and exponentially on the width , and (somewhat inversely) on the minimum edge weight . We will find these general broad trends, but with important differences, in the other algorithms as well.

Bresler, (2015) provides a greedy algorithm and shows that it can learn with sample complexity that grows logarithmically in , but doubly exponentially in the width and also exponentially in . It is thus suboptimal with respect to its dependence on and .

Vuffray et al., (2016) propose a new convex program (i.e. different from logistic regression), and for this they are able to show a single-exponential dependence on . There is also low-order polynomial dependence on and . Note that given and , the degree is bounded by (the equality is achieved when every edge has the same weight and there is no external field). Therefore, their sample complexity can scale as worse as . Later, the same authors (Lokhov et al.,, 2018) prove a similar result for the -regularized logistic regression using essentially the same proof technique as (Vuffray et al.,, 2016).

Rigollet and Hütter, (2017) analyze the -constrained logistic regression for learning Ising models. Their sample complexity888Lemma 5.21 in (Rigollet and Hütter,, 2017) has a typo: The upper bound should depend on . Accordingly, Theorem 5.23 should depend on rather than . has a better dependence on ( vs ) than (Lokhov et al.,, 2018). However, naïvely extending their analysis to the -constrained logistic regression will give a sample complexity exponential in the alphabet size999This is because the Hessian of the population loss has a lower bound that depends on for and ..

In this paper, we analyze the -constrained logistic regression for learning discrete pairwise graphical models with general alphabet. Our proof uses a sharp generalization bound for constrained logistic regression, which is different from (Lokhov et al.,, 2018; Rigollet and Hütter,, 2017). For Ising models (shown in Table 2), our sample complexity matches that of (Klivans and Meka,, 2017). For non-binary pairwise graphical models (shown in Table 2), our sample complexity improves the state-of-the-art result.

Appendix B Proof of Lemma 1 and Lemma 2

The proof of Lemma 1 relies on the following lemmas. The first lemma is a generalization error bound for any Lipschitz loss of linear functions with bounded and .

Lemma 7.

(see, e.g., Corollary 4 of (Kakade et al.,, 2009) and Theorem 26.15 of (Shalev-Shwartz and Ben-David,, 2014)) Let be a distribution on , where , and . Let be a loss function with Lipschitz constant . Define the expected loss and the empirical loss as

| (19) |

where are i.i.d. samples from distribution . Define . Then with probability at least over the samples, we have that for all ,

| (20) |

Lemma 8.

(Pinsker’s inequality) Let denote the KL-divergence between two Bernoulli distributions , with . Then

| (21) |

Lemma 9.

Let be a distribution on . For , , where is the sigmoid function. Let be the expected logistic loss:

| (22) |

Then for any , we have

| (23) |

where denotes the KL-divergence between two Bernoulli distributions , with .

Proof.

Simply plugging in the definition of the expected logistic loss gives

where (a) follows from the fact that

∎

We are now ready to prove Lemma 1 (which is restated below):

Lemma.

Let be a distribution on where for , . We assume that for a known . Given i.i.d. samples , let be any minimizer of the following -constrained logistic regression problem:

| (24) |

Given and , suppose that , then with probability at least over the samples, we have that .

Proof.

We first apply Lemma 20 to the setup of Lemma 1. The loss function defined above has Lipschitz constant . The input sample satisfies . Let . According to Lemma 20, with probability at least over the draw of the training set, we have that for all ,

| (25) |

where and are the expected loss and empirical loss.

Let for a global constant , then (25) implies that with probability at least ,

| (26) |

We next prove a concentration result for . Here is the true regression vector and is assumed to be fixed. First notice that is bounded because . Besides, the has Lipschitz 1, so . Hoeffding’s inequality gives that . Let for a global constant , then with probability at least over the samples,

| (27) |

The proof of Lemma 2 is identical to the proof of Lemma 1, except that it relies on the following generalization error bound for Lipschitz loss functions with bounded -norm.

Lemma 10.

Let be a distribution on , where , and . Let be a loss function with Lipschitz constant . Define the expected loss and the empirical loss as

| (29) |

where are i.i.d. samples from distribution . Define . Then with probability at least over the draw of samples, we have that for all ,

| (30) |

Lemma 30 can be readily derived from the existing results. First, notice that the dual norm of is . Using Corollary 14 in (Kakade et al.,, 2012), Theorem 1 in (Kakade et al.,, 2009), and the fact that for , we conclude that the Rademacher complexity of the function class is at most . We can then obtain the standard Rademacher-based generalization bound (see, e.g., (Bartlett and Mendelson,, 2002) and Theorem 26.5 in (Shalev-Shwartz and Ben-David,, 2014)) for bounded Lipschitz loss functions.

Appendix C Proof of Lemma 3

Lemma 3 is restated below.

Lemma.

Let be a -unbiased distribution on , where is the alphabet set. For , any , the distribution of is also -unbiased.

Proof.

For any , any , and any , we have

| (31) |

where (a) follows from the fact that and is a -unbiased distribution. Since (31) holds for any , any , and any , by definition, the distribution of is -unbiased. ∎

Appendix D Proof of Lemma 4

The lemma is restated below, followed by its proof.

Lemma.

Let be a pairwise graphical model distribution with alphabet size and width . Then is -unbiased with . Specifically, an Ising model distribution is -unbiased.

Proof.

Let , and assume that . For any , any , and any , we have

| (32) |

where (a) follows from the definition of model width. The lemma then follows (Ising model corresponds to the special case of ). ∎

Appendix E Proof of Lemma 5 and Lemma 7

The proof relies on the following basic property of the sigmoid function (see Claim 4.2 of (Klivans and Meka,, 2017)):

| (33) |

We first prove Lemma 5 (which is restated below).

Lemma.

Let be a -unbiased distribution on . Suppose that for two vectors and , , where . Then .

Proof.

For any , any , let be the -th variable and be the variables. Let (respectively ) be the vector obtained from by setting (respectively ). Then we have

| (34) |

Here (a) follows from the fact that is a -unbiased distribution, which implies that and . Inequality (b) is obtained by substituting (33). Inequality (c) uses the following fact

| (35) |

To see why (35) holds, note that if both , then (35) is true since . Otherwise, (35) is true because the left-hand side is at least 1 while the right-hand side is at most 1. The last equality (d) follows from that is independent of .

We now prove Lemma 7 (which is restated below).

Lemma.

Let be a -unbiased distribution on . For , let be the one-hot encoded . Let be two matrices satisfying and for . Suppose that for some and , we have , where . Then .

Proof.

Fix an and . Let (respectively ) be the vector obtained from by setting (respectively ). Let be the one-hot encoding of . Then we have

| (36) |

Here (a) follows from that is a -unbiased distribution and (33). Inequality (b) follows from (35). Because , (36) implies that

| (37) | ||||

| (38) |

Since (37) and (38) hold for any , we can sum over and use the fact that and to get

Therefore, we have , for any and . ∎

Appendix F Proof of Theorem 6

We first restate Theorem 6 and then give the proof.

Theorem.

Let be an unknown -variable Ising model distribution with dependency graph . Suppose that the has width . Given and , if the number of i.i.d. samples satisfies , then with probability at least , Algorithm 1 produces that satisfies

| (39) |

Proof.

For ease of notation, we consider the -th variable. The goal is to prove that Algorithm 1 is able to recover the -th row of the true weight matrix . Specifically, we will show that if the number samples satisfies , then with probability as least ,

| (40) |

We then use a union bound to conclude that with probability as least , .

Let , , and . By Fact 1, , where . Further, . Let be the solution of the -constrained logistic regression problem defined in (4).

By Lemma 1, if the number of samples satisfies , then with probability at least , we have

| (41) |

By Lemma 4, is -unbiased (Definition 3) with . By Lemma 5, if for some constant , then (41) implies that

| (42) |

Note that and . Let for some constant and , (42) then implies that

| (43) |

The number of samples needed is .

We have proved that (40) holds with probability at least . Using a union bound over all variables gives that with probability as least , . ∎

Appendix G Proof of Theorem 15

The following lemma will be used in the proof.

Lemma 11.

Let , where is a -unbiased distribution on . Given , conditioned on , is also -unbiased.

Proof.

For any , , and , we have

| (44) |

where (a) follows from the fact that for , (b) follows from the fact that is -unbiased. ∎

Now we are ready to prove Theorem 15, which is restated below.

Theorem.

Let be an -variable pairwise graphical model distribution with width and alphabet size . Given and , if the number of i.i.d. samples satisfies , then with probability at least , Algorithm 2 produces that satisfies

| (45) |

Proof.

To ease notation, let us consider the -th variable (i.e., set inside the first “for” loop of Algorithm 2). The proof directly applies to other variables. We will prove the following result: if the number of samples , then with probability at least , the matrices produced by Algorithm 2 satisfies

| (46) |

Suppose that (46) holds, summing over and using the fact that gives

| (47) |

Theorem 15 then follows by taking a union bound over the variables.

The only thing left is to prove (46). Now fix a pair of , let be the number of samples such that the -th variable is either or . By Lemma 2 and Fact 2, if , then with probability at least , the minimizer of the constrained logistic regression satisfies

| (48) |

Recall that is the one-hot encoding of the vector , where and . Besides, satisfies

| (49) |

Let be formed by centering the first rows of . Since each row of is a standard basis vector (i.e., all 0’s except a single 1), . Hence, (48) implies

| (50) |

By Lemma 4, we know that is -unbiased with . By Lemma 11, conditioned on , is also -unbiased. Hence, the condition of Lemma 7 holds. Applying Lemma 7 to (50), we get that if , the following holds with probability at least :

| (51) |

So far we have proved that (46) holds for a fixed pair. This requires that . Recall that is the number of samples that the -th variable takes or . We next derive the number of total samples needed in order to have samples for a given pair. Since is -unbiased with , for , we have , and hence . By the Chernoff bound, if the total number of samples satisfies , then with probability at least , we have samples for a given pair.

To ensure that (51) holds for all pairs with probability at least , we can set and and take a union bound over all pairs. The total number of samples required is .

Appendix H Mirror descent algorithms for constrained logistic regression

Algorithm 3 gives a mirror descent algorithm for the following -constrained logistic regression:

| (52) |

We use the doubling trick to expand the dimension and re-scale the samples (Step 2 in Algorithm 3). Now the original problem becomes a logistic regression problem over a probability simplex: .

| (53) |

where . In Step 4-11 of Algorithm 3, we follow the standard simplex setup for mirror descent algorithm (see Section 5.3.3.2 of (Ben-Tal and Nemirovski,, 2013)). Specifically, the negative entropy is used as the distance generating function (aka the mirror map). The projection step (Step 9) can be done by a simple normalization operation. After that, we transform the solution back to the original space (Step 12).

Algorithm 4 gives a mirror descent algorithm for the -constrained logistic regression:

| (54) |

For simplicity, we assume that 101010For , we need to switch to a different mirror map, see Section 5.3.3.3 of (Ben-Tal and Nemirovski,, 2013) for more details.. We then follow Section 5.3.3.3 of (Ben-Tal and Nemirovski,, 2013) to use the following function as the mirror map :

| (55) |

The update step (Step 8) can be computed efficiently in time, see the discussion in Section 5.3.3.3 of (Ben-Tal and Nemirovski,, 2013) for more details.

Appendix I Proof of Theorem 3 and Theorem 4

Lemma 12.

Lemma 57 follows from the standard convergence result for mirror descent algorithm (see, e.g., Theorem 4.2 of (Bubeck,, 2015)), and the fact that the gradient in Step 6 of Algorithm 3 satisfies (reps. the gradient in Step 6 of Algorithm 4 satisfies ). This implies that the objective function after rescaling the samples is -Lipschitz w.r.t. (reps. -Lipschitz w.r.t. ).

We are now ready to prove Theorem 3, which is restated below.

Theorem.

In the setup of Theorem 6, suppose that the -constrained logistic regression in Algorithm 1 is optimized by the mirror descent method (Algorithm 3) given in Appendix H. Given and , if the number of mirror descent iterations satisfies , and the number of i.i.d. samples satisfies , then (6) still holds with probability at least . The total run-time of Algorithm 1 is .

Proof.

We first note that in the proof of Theorem 6, we only use in order to apply the result from Lemma 1. In the proof of Lemma 1 (given in Appendix B), there is only one place where we use the definition of : the inequality (b) in (28). As a result, if we can show that (28) still holds after replacing by , i.e.,

| (58) |

By Lemma 57, if the number of iterations satisfies , then

| (59) |

As a result, we have

| (60) |

where (a) follows from (26), (b) follows from (59), (c) follows from the fact that is the minimizer of , and (d) follows from (27). The number of mirror descent iterations needed for (58) to hold is . In the proof of Theorem 6, we need to set (see the proof following (42)), so the number of mirror descent iterations needed is .

The proof of Theorem 4 is identical to that of Theorem 3 and is omitted here. The key step is to show that (58) holds after replacing by . This can be done by using the convergence result in Lemma 57 and applying the same logic in (60). The runtime of Algorithm 2 can be analyzed in the same way as above. The -constrained logistic regression dominates the total runtime. It requires time for each pair and each variable in , where is the subset of samples that a given variable takes either or . Since , the total runtime is .

Appendix J More experimental results

We compare our algorithm (Algorithm 2) with the Sparsitron algorithm in (Klivans and Meka,, 2017) on a two-dimensional 3-by-3 grid (shown in Figure 2). We experiment three alphabet sizes: . For each value of , we simulate both algorithms 100 runs, and in each run we generate the matrices with entries . To ensure that each row (as well as each column) of is centered (i.e., zero mean), we will randomly choose between two options: as an example of , or . The external field is zero. Sampling is done via exactly computing the distribution. The Sparsitron algorithm requires two sets of samples: 1) to learn a set of candidate weights; 2) to select the best candidate. We use samples for the second part. We plot the estimation error and the fraction of successful runs (i.e., runs that exactly recover the graph) in Figure 3. Compared to the Sparsitron algorithm, our algorithm requires fewer samples for successfully recovery.