Nuclear Norm Regularized Estimation of Panel Regression Models111We are grateful for comments and suggestions from the participants of the 2016 IAAE Conference, 2017 UCLA-USC Conference, 2017 Cambridge INET Panel Conference, 2018 International Conference of Econometrics in Chengdu, 2018 EMES, 2018 AMES, and seminars at Boston University, Columbia University, Northwestern University, Oxford University, University of Bath, University of Chicago, UC Riverside, University of Iowa, University of Surrey, Yale University, University Carlos III in Madrid, and CEMFI. We also thank Riccardo D’Adamo and Sarah Moon for improving the presentation. Weidner acknowledges support from the Economic and Social Research Council through the ESRC Centre for Microdata Methods and Practice grant RES-589-28-0001 and from the European Research Council grants ERC-2014-CoG-646917-ROMIA and ERC-2018-CoG-819086-PANEDA.

Abstract

In this paper we investigate panel regression models with interactive fixed effects. We propose two new estimation methods that are based on minimizing convex objective functions. The first method minimizes the sum of squared residuals with a nuclear (trace) norm regularization. The second method minimizes the nuclear norm of the residuals. We establish the consistency of the two resulting estimators.

Those estimators have a very important computational advantage compared to the existing least squares (LS) estimator, in that they are defined as minimizers of a convex objective function.

In addition, the nuclear norm penalization helps to resolve a potential identification problem for interactive fixed effect models, in particular when the regressors are low-rank and the number of the factors is unknown.

We also show how to construct estimators that are asymptotically equivalent to the least squares (LS) estimator in Bai (2009) and Moon and Weidner (2017) by using our nuclear norm regularized or minimized estimators as initial values for a finite number of LS minimizing iteration steps. This iteration avoids any non-convex minimization, while the original LS estimation problem is generally non-convex, and can have multiple local minima.

Keywords: Interactive Fixed Effects, Factor Models, Nuclear Norm Regularization, Convex Optimization, Iterative Estimation

1 Introduction

In this paper we consider a linear panel regression model of the form

| (1) |

where and label the cross-sectional units and the time periods, respectively, is an observed dependent variable, are observed regressors, are unknown regression coefficients, and are unobserved factors and factor loadings, is an unobserved idiosyncratic error term, denotes the number of factors, and denotes the number of regressors. The factors and loadings are also called interactive fixed effects. They parsimoniously represent heterogeneity in both dimensions of the panel, and they contain the conventional additive error components as a special case. We assume that , and for our asymptotic results we will consider and as fixed, as . We can rewrite this model in matrix notation as

| (2) |

where and , and , , and are matrices, while and are and matrices, respectively. The parameters and are treated as non-random throughout the whole paper, that is, all stochastic statements are implicitly conditional on their realization. Without loss of generality we assume .

One widely used estimation technique for interactive fixed effect panel regressions is the least squares (LS) method,666 The LS estimator in this context is also sometimes called concentrated least squares estimator, and was originally proposed by Kiefer (1980). which treats and as parameters to estimate (fixed effects).777Other estimation methods of panel regressions with interactive fixed effects include the quasi-difference approach (e.g., Holtz-Eakin, Newey, and Rosen 1988), generalized method of moments estimation (e.g. Ahn, Lee, and Schmidt 2001, 2013), the common correlated random effect method (e.g., Pesaran 2006), the decision theoretic approach (e.g., Chamberlain and Moreira 2009), and Lasso type shrinkage methods on fixed effects (e.g., Cheng, Liao, and Schorfheide 2016, Lu and Su 2016, Su, Shi, and Phillips 2016). Let the Frobenius norm of an matrix be . Then, the LS estimator for reads

| (3) |

where is the number of factors chosen in the estimation. A matrix can be written as , for some and , if and only if . The profiled least square objective function can therefore equivalently be expressed as

| (4) |

It is known that under appropriate regularity conditions (including exogeneity of with respect to ), for , and as at the same rate, the LS estimator is -consistent and asymptotically normal, with a bias in the limiting distribution that can be corrected for (e.g., Bai 2009, Moon and Weidner 2015, 2017).

The LS estimation approach is convenient, because it does not restrict the relationship between the unobserved heterogeneity () and the observed explanatory variables (). However, the calculation of requires solving a non-convex optimization problem. While is a convex function of and , the profiled objective function is in general not convex in , and can have multiple local minima, as will be discussed in Section 2.1 in more detail. The reason for the non-convexity is that the constraint is non-convex. This non-convexity can become a serious computational obstacle, for example, when the number of regressors is too large to allow for a simple grid-search over (for a given , the optimization over is a principal components problem that can generally be solved quickly in the linear regression case). For generalizations to non-linear panel regression models (e.g., Chen 2014, Chen, Fernández-Val, and Weidner 2021), the optimization of the non-convex objective function with respect to the high-dimensional factors and loadings becomes even more challenging.

In this paper, we make several important contributions to the literature of panel regression with interactive fixed effects:

Our first contribution is to overcome the non-convexity issue of the least squares estimation problem above by considering a panel regression with nuclear norm regularization, which provides a convex relaxation of the rank constraint in (4). To be more specific, let be the vector of singular values of .888 The non-zero singular values of are the square roots of non-zero eigenvalues of . Singular values are non-negative by definition. The rank of a matrix is equal to the number of non-zero singular values, that is, , where equals the number of non-zero elements of the vector (sometimes calles the “-norm” of ). The nuclear norm of is defined by , that is, the nuclear norm of the matrix is simply the -norm of the vector .999 The nuclear norm is the convex envelope of over the set of matrices with spectral norm at most one, see e.g. Recht, Fazel, and Parrilo (2010). The nuclear norm is also sometimes called trace norm, Schatten 1-norm, or Ky Fan n-norm. Our index notation for the nuclear norm , Frobenius norm , and spectral norm is motivated by the unifying formula . A convex relaxation of (4) can then be obtained by replacing the non-convex constraint by the convex constraint , for some constant . This gives

| (5) |

where in the second line we replace the constraint on the nuclear norm by a nuclear-norm penalty term.101010The normalizations with and in (5) are somewhat arbitrary, but turn out to be convenient for our purposes. Choosing a particular penalization parameter is equivalent to choosing a particular value for , and we find it more convenient to parameterize the convex relaxation of by instead of .

For a given the nuclear-norm regularized estimator reads

We also define for fixed and .111111 Here, the limit is for fixed and , and has nothing to do with our large , asymptotic considerations. We will show in Section 2.2 that , that is, can alternatively be obtained by minimizing the nuclear norm of . The nuclear norm minimizing estimator is novel to the literature as far as we know.

The second contribution of the paper is to derive asymptotic properties of and . We establish asymptotic results for and when both panel dimensions become large. Under appropriate regularity conditions we show -consistency of these estimators. We also show how to use and as initial values for a finite iteration procedure (avoiding a non-convex optimization) that gives improved estimates that are asymptotically equivalent to the LS estimator.

The third contribution of the paper is to solve a potential identification problem for interactive fixed effect models by employing the nuclear norm penalization. Notice that without restrictions on the parameter matrix in (2), we cannot separate and uniquely, because for any other parameter we can write

implying that and are observationally equivalent. If any non-trivial linear combination of the regressors is a high-rank matrix, then the assumption that is sufficient to identify , because will be large for any other value of . However, if some of the regressors have low rank (as, for example, in Gobillon and Magnac 2016, where is a panel of treatment variables) and the true number of factors is unknown, then there is an identification problem, and some regularization device is needed to resolve this. In Section 2 we show that, under appropriate assumptions on the covariates, the nuclear norm penalization indeed provides such a regularization device to uniquely identify .

Nuclear norm penalized estimation has been widely studied in the machine learning and statistical learning literature. There, the parameter of interest is usually the matrix that we call in our model. In particular, there are many papers that use this penalization method in matrix completion (e.g., Recht, Fazel, and Parrilo 2010 and Hastie, Tibshirani, and Wainwright 2015 for recent surveys), and for reduced rank regression estimation (e.g., Rohde and Tsybakov 2011). More recently, nuclear norm penalization has also been used in the econometrics literature: Bai and Ng (2017, 2019) use it to improve estimation in a pure factor model. Athey, Bayati, Doudchenko, Imbens, and Khosravi (2021) apply nuclear norm penalization to treatment effect estimation with unbalanced panel data due to missing observations together with a regularization on the high dimensional regression coefficients – their primary interest is to predict the left-hand side variable using the regularization. Chernozhukov, Hansen, Liao, and Zhu (2018) consider panel regression models with heterogeneous coefficients, while in this paper we focus on panel regression with homogenous coefficients. To the best of our knowledge, our results here on the estimates of the common regression coefficients are new in this literature, and the nuclear norm minimizing estimator has also not been proposed previously.

Since the 2018 working paper version of the current paper, there has been a lot of closely related work using similar penalization methods in the context of panel data, factor models, and network structures: Alidaee, Auerbach, and Leung (2020) and Ma, Su, and Zhang (2022) focus on network structures, utilizing penalized regression and latent community detection methods, respectively, to recover and analyze network structures. In the context of panel data models, Chernozhukov, Hansen, Liao, and Zhu (2018) employ low-rank estimations to analyze heterogeneous effects across both individuals and time. Belloni, Chen, Madrid Padilla, and Wang (2023), Wang, Su, and Zhang (2022), and Feng (2023) extend this approach to quantile regressions, significantly extending our own discussion of this in Section 6. Miao, Li, and Su (2020) and Miao, Phillips, and Su (2023) explore panel threshold models and high-dimensional VARs with common factors. Chen (2022) integrates these concepts into a unified framework for high-dimensional conditional factor models, demonstrating the flexibility and wide-ranging applicability of nuclear norm penalization. Beyhum and Gautier (2022) extend the factor models to include nonstrong factors. Fernández-Val, Freeman, and Weidner (2021) employ the nuclear norm penalization to estimate low-rank approximation of nonseparable panel models. Beyhum and Gautier (2019) introduce an approach where low-rank interactive effects are treated as an approximate model, with the rank of the best approximation being unknown and allowed to grow with the sample size. Chetverikov and Manresa (2022) and Mugnier (2022) consider grouped fixed effects models, using (nuclear norm) penalization methods in their initial estimation of regression slopes. Armstrong, Weidner, and Zeleneev (2022) also utilize the convexity of the nuclear norm to robustify estimation of the regression slopes in interactive fixed effects panel regressions. In summary, these studies demonstrate the versatility of the nuclear norm penalization and related convexification methods in handling panel data, and more complex network structures.

The paper is organized as follows. Section 2 discusses theoretical motivations for employing nuclear norm regularization instead conventional rank restrictions. In Section 3 we derive consistency results on and . Section 4 shows how to use these two estimates as a preliminary step to construct an estimator through iterations that achieves asymptotic equivalence to the fixed effect estimator. Section 5 investigates finite sample properties via simulations. We then briefly discuss extensions to non-linear panel models with interactive fixed effects in Section 6, and Section 7 concludes the paper. All technical derivations and proofs are presented in the appendix or supplementary appendix.

2 Motivation of Nuclear Norm Regularization

In this section we provide further motivation and explanation of the nuclear norm regularized estimation method. This estimation approach comes with the computational advantage of having a convex objective function, and it also provides a solution to the identification problem of interactive fixed effect models with low-rank regressors.

2.1 Convex Relaxation

We have already introduced the profile LS objective function and its convex relaxation in the introduction. Here, we explain those objective functions further. Firstly, we want to briefly explain why is indeed convex. We have introduced the nuclear norm as , but it is not obvious from this definition that is convex in , because the singular values themselves are generally not convex functions of , except for . A useful alternative definition of the nuclear norm is

| (6) |

that is, the nuclear norm is dual to the spectral norm . From this it is easy to see that is indeed a matrix norm, and thus convex in .121212 Let and be matrices of the same size. Then, by (6) there exists a matrix of the same size with such that , which is the triangle inequality for the nuclear norm. Together with absolute homogeneity of this implies convexity. Therefore, the nuclear norm regularized objective function

as a function of is convex. Profiling with respect to preserves convexity, that is, is also convex.

By contrast, the least squares objective function is generally non-convex in the parameters , and . However, the non-convexity of the LS minimization over and is actually not a serious problem in computing the profile objective function , as long as the regression model is linear and one of the dimensions or is not too large.131313The optimal and are simply given by the leading principal components of . Calculating them requires finding the eigenvalues and eigenvectors of either the matrix or the matrix , which takes at most a few seconds on modern computers, as long as , or so. The non-zero eigenvalues of and are identical, and are equal to the square of the non-zero singular values of . Recall that is the largest singular value of the matrix , for . One can show (see Moon and Weidner 2017) that the profile least squares objective function is

| (7) |

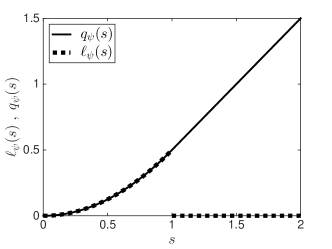

where the largest singular values are omitted in the sum - because they are absorbed by the principal component estimates and . The remaining problem in calculating is the generally non-convex minimization of over .141414 In our discussion here we focus on the calculation of via minimization of the profile objective function . More generally, can be obtained by any method that minimizes over , , , see e.g. Bai (2009) or the supplementary appendix in Moon and Weidner (2015). For any such method the non-convexity of the objective function is a potential problem, because the algorithm may converge to a local minimum, or potentially even to a critical point that is not a local minimum. To illustrate the potential difficulty caused by this non-convexity, in Figure 1 we plot for the simple example described in Appendix A.1. In this example is non-convex and has two local minima, one of which (the global one) is close to the true parameter . The figure also shows that is convex and only has a single local minimum.

For any define the functions and by

| (12) |

For an matrix let and . We can then rewrite (7) as

| (13) |

where satisfies

| (14) |

Here, the normalization with is natural, because under standard assumptions the largest singular value of is of order , as and grow. The formulation (13) is interesting for us, because the following lemma shows that we have a very similar representation for .

Lemma 1.

For any and any we have

The proof is given in the appendix. Figure 2 shows the functions and for real valued arguments and . For values the functions are identical, but at the function has a non-continuous jump, implying that is non-convex, while continues linearly for , thus remaining convex.

Comparing and we see that the parameter that counts the number of factors is replaced by the parameter that characterizes the magnitude at which the singular values of are considered to be factors, and for a given the relationship between and is given by (14). Large corresponds to small , and vice versa. Furthermore, has singular values151515See Lemma S.1 in the supplementary appendix for details.

that is, the nuclear norm penalization shrinks the singular values of towards zero by a fixed amount.

Fixing as opposed to fixing already changes the functional form of the profile objective function, because according to (14) their relationship depends on . In addition, the objective function is convexified by replacing the function that is applied to the singular values of with the function , as defined in (12). The function provides a convex continuation of for .

Using the closed-form expression for in Lemma 1, and noticing that it is convex in , one can compute the minimizer of using various optimizing algorithms for a convex function (see chapter 5 of Hastie, Tibshirani, and Wainwright 2015). If the dimension of is small, then one may even use a simple grid search method to find . We will discuss a data dependent choice of the penalty parameter in Section 5.

2.2 Unique Matrix Separation

When estimating the interactive fixed effect model (1), in practice both and are unknown. Showing that and can be consistently estimated jointly is a difficult problem in general.161616The problem of joint identification of and is often avoided in the literature. Some papers (e.g. Bai 2009, Li, Qian, and Su 2016, Moon and Weidner 2017) assume that the number of factors is known when showing consistency for an estimator of . Alternatively, Lu and Su (2016) allow for unknown , but assume consistency of their estimator for . Within the interactive fixed effects estimation framework this joint inference problem has only been successfully addressed when both of the following assumptions are satisfied:171717 Some existing estimation methods avoid specifying when estimating , but always at the cost of some additional assumptions on the data generating process. For example, the common correlated effects estimator of Pesaran (2006) avoids choosing , but requires assumptions on how the factors enter into the observed regressors , and requires all regressors of interest to be high-rank.

-

(C1)

There is a known upper bound such that .

-

(C2)

All the regressors are “high-rank regressors”, that is, is large for all .

Under those assumptions (and other regularity conditions) the consistency proofs of Bai (2009) and Moon and Weidner (2015) are applicable to the LS estimator for that uses factors in the estimation, and one can also show the convergence rate result , as . To obtain a consistent estimator for one can then apply inference methods from pure factor models without regressors (e.g. Bai and Ng 2002, Onatski 2010, Ahn and Horenstein 2013) to the matrix .

The condition (C2) above is particularly strong, because “low-rank regressors” are quite common in practice. If we can write , then we have , and the condition (C2) is violated. For example, Gobillon and Magnac (2016) estimate an interactive fixed effects model in a panel treatment effect setting, where the main regressor of interest indeed can be multiplicatively decomposed in this way, with being the treatment indicator of unit , and being the time indicator of treatment. Those interactive fixed effects models for panel treatment effect applications have grown very popular recently.181818Other recent applications in the same vein as Gobillon and Magnac (2016) are Chan and Kwok (2016), Powell (2022), Gobillon and Wolff (2020), Adams (2017), Piracha, Tani, and Tchuente (2017), Li (2018), to list just a few. This literature is also related to the synthetic control method (Abadie and Gardeazabal 2003, Abadie, Diamond, and Hainmueller 2010, Abadie, Diamond, and Hainmueller 2015; see also Hsiao, Ching, and Wan 2012). However, when is unknown, then the presence of such low-rank regressors creates an identification problem, as illustrated by the following example.

Example 1.

Consider a single () low-rank regressor , with vectors and . Let , , and . Then, model (1) with parameters , , , is observationally equivalent to the same model with parameters , , , , because we have . Thus, is observationally equivalent to any other value if the true number of factors is unknown.

The example shows that regression coefficients of low-rank regressors are not identified if is unknown, because could simply be absorbed into the factor structure , which is also a low-rank matrix. Therefore, without some additional assumption or regularization device, the two low-rank matrices and cannot be uniquely disentangled, which is what we mean by “unique matrix separation” in the title of this section.

Nuclear Norm Minimizing Estimation

In the following we explain how the nuclear norm minimization approach overcomes the restrictions (C1), that is, how to estimate regression coefficients when is unknown. We already introduced in Section 1. Using Lemma 1 we can now characterize differently. It is easy to see that , for , and therefore , for . Lemma 1 thus implies that . Another way to see this is as follows. According to (14), the limit corresponds to choosing very large, i.e., . In this case, , and the profile objective function is From this we deduce

Notice that for we trivially have , but the rescaled objective function nevertheless has a non-trivial limit as . Since rescaling the objective function by a constant does not change the minimizer we thus find that

| (15) |

that is, the small limit of the nuclear norm regularized estimator is the nuclear norm minimizing estimator . The objective function is convex in .

We cannot expect the LS estimator to have good properties (in particular consistency) if we choose the number of factors equal to, or close to, its maximum possible value . It is therefore somewhat surprising that has a well-defined limit as , and that we are able to show consistency of the limiting estimator under appropriate regularity conditions in the following sections, because the resulting estimator for is certainly not consistent for in that limit.191919 The limit (for fixed , ) of the optimal in (5) is , which as and grow converges to for consistent , that is, the estimator for that corresponds to is not consistent for .

The main significance of is that it provides an estimator for that does not require any choice of “bandwidth parameter”, because neither nor needs to be specified. It thus provides a method to estimate consistently without requiring knowledge of an upper bound on as in the condition (C1) above. In a second step we can then estimate consistently by applying, for example, the Bai and Ng (2002) method for pure factor models without regressors to the matrix .

Notice that the pooled OLS estimator minimizes , the -norm of the singular values of the residual matrix, , while the nuclear norm minimizing estimator minimizes the -norm, of the residual matrix. The relationship between these two estimators is therefore analogous to that of the OLS estimator and the LAD (least absolute deviation) estimator for cross-sectional samples. is robust with respect to the unobserved factors, which are “outliers” in the singular value spectrum, while the pooled OLS estimator is not robust towards the presence of those unobserved factors (because they may be correlated with the regressors).

Nuclear Norm Penalization Approach for Matrix Separation

Next, we explain how the nuclear norm regularization approach helps to overcome the restrictions (C2) above, that is, how to estimate regression coefficients for low-rank regressors when is unknown. The goal is to provide conditions on the regressors under which the nuclear norm penalization approach indeed solves the matrix separation problem for low-rank regressors and interactive fixed effects.

We first want to answer this in a simplified setting, where the objective function is replaced by the expected objective function, that is, we consider

| (16) |

Here, the expectation is conditional on all the regressors , and also implicitly on all the parameters and , because those are treated as non-random.202020 can be viewed as a population version of for an appropriately defined population distribution of conditional on . But independent of this interpretation, is a convenient tool for discussing the necessary non-collinearity condition on the regressors without requiring asymptotic analysis.

For a matrix , let and be the projectors onto and orthogonal to the column span of , where is the identity matrix of appropriate dimensions, and refers to the Moore-Penrose generalized inverse. Remember also our notation for . For vectors we write for the Euclidian norm.

Proposition 1.

Suppose that , , and are fixed. Let , and , for all . For all assume that

| (17) |

Then, , as .

The proof is given in the appendix. The proposition considers fixed , , with only .212121 Display (S.10) in the appendix provides a bound on for finite , but the limit is what matters most to us, because that limit allows to identify . The statement of the proposition implies that . Thus, the proposition provides conditions under which the nuclear norm regularization approach identifies the true parameter . The proposition does not restrict the rank of the regressors, so the result is applicable to both low-rank and high-rank regressors. The assumption requires strict exogeneity of all regressors, but we will allow for pre-determined regressors in consistency results of Section 3.2 below.

The beauty of Proposition 1 is that it provides a very easy to interpret non-collinearity condition on the regressors . It requires that for any linear combination of the regressors the part , which cannot be explained by neither nor , is larger in terms of nuclear norm than the part , which can be explained by both and . For a single () regressor with , as in Example 1, the condition simply becomes . Here, and are the residual sum of squares and the explained sum of squares, respectively, of a regression of on the and analogously for and . In Example 1 we obviously have and , that is, the parameters , , , are ruled out by the condition on the regressors in Proposition 1.

Related to the regularity condition (17) of Proposition 1, it is possible to show (see Bai 2009, Moon and Weidner 2017) that the weaker condition for any linear combination is sufficient for local identification of in a sufficiently small neighbourhood around . However, that weaker condition is not sufficient for global identification of , as illustrated by the examples in the supplementary appendix S.3 of Moon and Weidner (2017). The stronger condition (17) in Proposition 1 guarantees global identification of when using the nuclear norm penalization approach as a regularization device.

Providing such global identification conditions for models with low-rank regressors and unknown is a new contribution to the interactive fixed effects literature.222222 If the model would not have any idiosyncratic errors (i.e. ), then , and a natural solution to this identification problem would be to choose as the solution to the rank minimization problem where at the true parameters we have , that is, we are minimizing the number of factors required to describe the data. However, once idiosyncratic errors are present, then this rank minimization does not work, because is of large rank for all . Our approach here is similar to the “Identification via a Strict Convex Penalty” proposed in Chen and Pouzo (2012).

3 Consistency of and

Proposition 1 above provides an identification result for for fixed and , based on the expected objective function. We now turn to the actual estimates and and investigate their properties as .

All our consistency results for are for asymptotic sequences where , as , but we do not usually make the dependence of on the sample size explicit. In addition, we assume that the number of the regressors and the true number of factors are both fixed. However, we do not restrict whether the factors are strong or weak, nor do we restrict the magnitude of in any matrix norm.

3.1 Consistency Results for Low-Rank Regressors

Here, we consider a special case where the regressors are of low rank. This section is short, because the results here are relatively straightforward extensions of Section 2.2. The more general case that allows both high-rank and low-rank regressors will be discussed in the following subsection.

Theorem 1.

Consider with , and assume that

-

(i)

There exists a constant such that

(18) for all sample sizes .

-

(ii)

, and .

Then we have

Various examples of DGP’s for that satisfy the assumption can be found in the supplementary appendix S.2 of Moon and Weidner (2017). Loosely speaking, that condition is satisfied as along as the entries have zero mean, some appropriately bounded moments, and are not too strongly correlated across and over . The condition requires all regressors to be low-rank. The interpretation of condition (18) is the same as for condition (17) in Proposition 1, and Theorem 1 is indeed a sample version of that proposition, except that low-rank regressors are required here.

The theorem shows that both and , for , converge to at a rate of at least . The proof of the theorem is provided in the appendix, and is a relatively easy generalization of the proof of Proposition 1. This is because the assumption that all the regressors are low-rank allows to easily decouple the contribution of the high-rank matrix and the low-rank matrix to the penalized objective function . However, dealing with the contribution of the idiosyncratic errors becomes more complicated once high-rank regressors are present, as will be explained in the following.

3.2 Consistency Results for General Regressors

The previous subsection considered the case where all regressor matrices are low-rank. We now study situation where all or some of the regressor matrices are high-rank.

3.2.1 Consistency of and

Applying Lemma 1 and the model for we have

The proof strategy for Theorem 1 requires that both and are low-rank, which allows to (approximately) separate off in this expression for . But if one of the regressors is a high-rank matrix that proof strategy turns out not to work anymore, because the singular value spectrum of the sum of two high-rank matrices and does not decompose (or approximately decompose) into a contribution from and from , but instead all singular values depend on both of those high-rank matrices in a complicated non-linear way.

We therefore now follow a different strategy, where instead of studying the objective function after profiling out , we now explicitly study the properties of the estimator for . Let

For the results in this subsection we are going to first show consistency of , and afterwards use that to obtain consistency of . This is a very different logic than in the preceding section, where consistency of is usually not achieved, because we do not impose any lower bound on . In order to achieve consistency of one requires not be too small. The approach here is much more similar to the machine learning literature (e.g., Negahban, Ravikumar, Wainwright, and Yu 2012), where the matrix that we call is usually the object of interest, and correspondingly a lower bound on the penalization parameter is required. We also follow that literature here by imposing a so-called “restricted strong convexity” condition below, which is critical to show consistency of and consequently of in the following.

It is convenient to introduce some additional notation: Let be the vector that vectorizes the columns of . Denote as the inverse operator of , so for we have . We use small letters to denote vectorized variables and parameters. Let and . Define . Using this, we express the model (2) as , where all the summands are -vectors, and the least-squares objective function reads .

Assumption 1 (Restricted Strong Convexity).

Let

We assume that

there exists , independent from and , such that for any

with

we have

,

for all , .

The intuitive interpretation of Assumption 1 is very similar to condition (17) in Proposition 1: The cone contains matrices that are close to , in the sense that the part of that cannot be explained by and is small compared to the remaining part of , in terms of nuclear norm. The assumption then imposes that all those matrices in the cone are sufficiently different from the regressors, in the sense that cannot be perfectly explained by .

Specifically, the condition assumes that the quadratic term, , of the profile likelihood function, , is bounded below by a strictly convex function, , if belongs in the cone . Notice that without any restriction on the parameter , we cannot find a strictly positive constant such that . Assumption 1 imposes that if we restrict the parameter set to be the cone , then we can find a strictly convex lower bound of the quadratic term of the profile likelihood. Assumption 1 corresponds to the restricted strong convexity condition in Negahban, Ravikumar, Wainwright, and Yu (2012), and it plays the same role as the restricted eigenvalue condition in recent LASSO literature (e.g., see Candes and Tao (2007) and Bickel, Ritov, and Tsybakov (2009)).

Notice that for we have and , and therefor , implying that Assumption 1 is trivially satisfied for any .

Assumption 1 requires that for a lower bound of is given by the strictly convex function . To have some intuition, suppose that the regressor is scalar and assume that without loss of generality because the projection operator is invariant to the scale change. Also assume that . Then,

In this case, if the limit of the distance between the regressor and the restricted parameter set is positive, Assumption 1 is satisfied if , the distance of the normalized regressor and convex cone , is positive. An obvious necessary condition for this is that the normalized regressor does not belong in the cone , that is,

For example, if has an approximate factor structure

with , then we can use random matrix theory results to show that Assumption 1 is satisfied.

Lemma 2 (Convergence Rate of ).

The lemma shows that once we impose restricted strong convexity and a lower bound on , then we can indeed bound the difference between and . This lemma is obviously key to obtain a consistency result for . Notice furthermore that

that is, once we have a consistency result for (or equivalently ), then we can also show consistency of . Using that derivation strategy we obtain the following theorem, which provides a consistency result for both and .

Theorem 2.

The additional regularity conditions imposed in Theorem 2 are weak and quite general. As mentioned before, various examples of that satisfy (i) can be found in the supplementary appendix S.2 of Moon and Weidner (2017); these include weakly dependent errors, and nonidentical but independent sequences of errors. Condition (ii) is satisfied if the regressors are exogenous with respect to the error, , and are weakly correlated over and across so that is bounded asymptotically. Condition (iii) is the standard non-collinearity condition for the regressors. Condition (iv) restricts the choice of the regularization parameter , which has to converge to zero (as discussed before for identification and consistency of ), but not too quickly (if is too small, then picks up all the noise and cannot be consistent). The conditions (i) and (iv) are sufficient regularity conditions for (19). To see this in more detail, since with , we have

Then, choosing makes satisfy with probability approaching one, and the rate condition in (iv) guarantees this.

Theorem 2 requires to grow faster than . By choosing appropriately we can therefore obtain a convergence rate of that is just below , which is essentially the same convergence rate that we found in Section 3.1 for the case of only low-rank regressors.

For the special case we have , and if then satisfies (19), one can show that

| (20) |

with probability approaching one (wpa1), see the appendix for a proof of this. In this case, the regularized estimator of becomes the pooled OLS estimator, wpa1.

3.2.2 Consistency of

Here, we establish consistency of the nuclear norm minimization estimator for high-rank regressors. For simplicity we only discuss the case of a single regressor () in the main text, and we simply write for the regressor matrix in this subsection. The general case of multiple regressors () is discussed in Appendix B.6.

Remember that is the minimizer of the objective function . Asymptotically separating the contribution of the low-rank matrix to the singular values of the sum is possible under a strong factor assumption.232323 In Moon and Weidner (2015, 2017) we use the perturbation theory of linear operator to do exactly that. However, characterizing the singular values of the sum of two high-rank matrices requires results from random matrix theory that are usually only shown under relatively strong assumptions on the distribution of the matrix entries. We therefore first provide a theorem under high-level assumptions, and afterwards discuss how to verify those assumptions using results from random matrix theory. We write SVD for “singular value decomposition” in the following.

Theorem 3.

Suppose that , and assume that as , with , we have

-

(i)

, and .

-

(ii)

There exists a finite positive constant such that , wpa1.

-

(iii)

Let be the SVD of .242424That is, and is an matrix of singular vectors, is a diagonal matrix, and is an matrix of singular vectors. We assume

-

(iv)

There exists a constant such that , wpa1.

-

(v)

Let be the SVD of the matrix . We assume that there exists such that , wpa1.

We then have .

The theorem considers the case , because the two panel dimensions are not treated symmetrically in the assumptions and proof of this theorem. Alternatively, we could consider , but then we also need to swap and , and replace by and by in all the assumptions (the case is ruled out here for technical reasons). For both and the statement of theorem can be written as , that is, we have the same convergence rate result here for as in Theorem 1 above.

Condition (i) in the theorem is quite weak, we already discussed the rate restriction on above, and we have as long as is finite. Condition (ii) almost follows from , because we have , and the assumption is only slightly stronger than this in assuming a fixed upper bound with probability approaching one, which can also be verified for many error distributions. Condition (iii) is a high level condition and will be satisfied if

| (21) |

for some finite constant , where and are the columns of and , respectively. An example of DGP’s of and that satisfies condition (21) is given by Assumption LL (i) and (ii) in Moon and Weidner (2015). Condition (iv) rules out “low-rank regressors”, for which we typically have , but is satisfied generically for “high-rank regressors”, for which has singular values of order , so that is of order . Condition (v) requires that the singular vectors of are sufficiently different from the singular vectors . If and are independent, then we expect that assumption to hold quite generally.

4 Post Nuclear Norm Regularized Estimation

In Section 3 we have shown that and are consistent for at a -rate, which is a slower convergence rate than the -rate at which the LS estimator converges to under appropriate regularity conditions. Our Monte Carlo results in Section 5 confirm this relatively slow rate of convergence of and , that is, those rates are not an artifact of our proof strategy, but are a genuine property of those estimators. In this section we investigate how to establish an estimator that is asymptotically equivalent to the LS estimator, and yet avoids minimizing any non-convex objective function. Our suggestion is to use either or as a preliminary estimator and iterate estimating and a finite number of times.

The conditions that are usually needed to show that the global minimizer of the objective function is consistent for (i.e. Assumption A in Bai (2009), or Assumption 4 in Moon and Weidner (2017)) are not required here, because we have already shown consistency of or under different conditions (our discussion in Section 2.2 highlights those differences). It is therefore convenient to introduce a local version of the LS estimator in (3) as

| (22) |

where is a sequence of positive numbers such that and . Those rate conditions guarantee that is an interior point of , wpa1, under the assumptions of Theorem 4 below. If the global minimizer is consistent, then we expect wpa1, but is consistent by definition even if is not. Our goal in the following is to obtain an estimator that is asymptotically equivalent to .

For simplicity, we first discuss the case where the number of factors is known. For unknown we recommend using a consistent estimator of instead, and we discuss estimation of in Section 5 below. Starting from our initial nuclear norm regularized or minimized estimators we consider the following iteration procedure to obtain improved estimates of :

-

Step 1:

For set (or ), the preliminary consistent estimate for .

-

Step 2:

Estimate the factor loadings and the factors of the step residuals by the principle component method:

-

Step 3:

Update the -stage estimate by

(23) -

Step 4:

Iterate step 2 and 3 a finite number of times.

The following theorem shows that if the initial estimator is consistent, then gets close to as the number of iteration increases. This result is very similar to the quadratic convergence result of a Newton-Raphson algorithm for minimizing a smooth objective function, and the above iteration step is indeed very similar to performing a Newton-Raphson step to minimize .

Theorem 4.

Assume that and grow to infinity at the same rate, and that

-

(i)

, and .

-

(ii)

, and for all .

-

(iii)

.

-

(iv)

.

Then, if the sequence in (22) satisfies and we have

Assume furthermore that

-

(iv)

, for a sequence such that .

For we then have

Here, assumption (i) is a strong factor condition, and is often used in the literature on interactive fixed effects. The conditions in assumption (ii) of the theorem have been discussed in previous sections and are quite weak (remember that ). Assumption (iii) guarantees that is locally convex around – that condition can equivalently be written as for any , which connects more closely to our discussion in Section 2.2. This is a non-collinearity condition on the regressors after profiling out both and . Only the true values and appear in that non-collinearity condition, and it is therefore much weaker than the corresponding assumptions required for consistency of in Bai (2009) and Moon and Weidner (2017). Our results from the previous sections show that for both and , under appropriate assumptions, where is typically either or slightly slower than this, if is chosen appropriately.

The following corollary is an immediate consequence of Theorem 4.

Corollary 1.

Let the assumptions of Theorem 4 hold, and assume that . For we then have

The first statement of the corollary shows that if the initial estimators and satisfy typical convergence rates results derived in the previous sections, then the iterated estimator is asymptotically equivalent to after iterations or more. Remember that if is consistent, then we have wpa1, but by showing asymptotic equivalence with here we avoid imposing conditions that require consistency of .

From the results in Bai (2009) and Moon and Weidner (2017) we also know that is asymptotically normally distributed, but potentially with a bias in the limiting distribution. According to the corollary the same is therefore true for for . Asymptotic bias corrections could then also be applied to , , to eliminate the bias in the limiting distribution and allow for inference on . See Bai (2009) and Moon and Weidner (2017) for details.

5 Implementation and Monte Carlo Simulations

To implement the nuclear norm regularized estimator we need to choose the regularization parameter , and for the post estimator we need to determine the number of factors . In this section we suggest a data dependent choice of as well as an estimate of . We assume that an upper bound is known.

Data Dependent Choice of .

We suggest the following procedure to choose .

-

Step 1:

Calculate the nuclear norm minimizing estimator , and the corresponding residuals

-

Step 2:

Choose , calculate principal components of ,

and use those to eliminate all the factors in . The new residuals are

-

Step 3:

Choose

This choice of is motivated by the condition (19) in Lemma 2, which guarantees that is sufficiently large to obtain estimates that are close to . Notice also that the nuclear norm minimizing estimator in step 1 does not require any regularization parameter to be specified.

Estimation of

The post nuclear norm regularized estimator introduced above assumes that the number of factors is known. In practice needs to be estimated, for example, by applying a consistent estimation method for the number of the factors in a pure factor model to the residuals , see e.g. Bai and Ng (2002), Onatski (2010) and Ahn and Horenstein (2013).

For our Monte Carlo simulations below we use an alternative estimation method that thresholds the singular values of using the estimate introduced above. Namely, we estimate by

The motivation behind this estimator is that those singular values of that are significantly larger than should correspond to factors, while singular values close to and smaller should originate from idiosyncratic noise. The choice of the factor 2 in the formula for is somewhat arbitrary, any alternative factor larger than one would also be plausible here.

Monte Carlo Results

We generate data from the following linear panel model regression model with two regressors (including the intercept) and two factors:

| (24) |

where ; ; ; all mutually independent. Table 1 reports the bias and standard deviation for the various estimators for different combinations of and .

![[Uncaptioned image]](/html/1810.10987/assets/x3.png)

As shown in Table 1, the nuclear norm regularized estimator and the nuclear norm minimization estimator have biases due to the regularization which vanish slowly as the sample size increases. This confirms that those estimators are indeed not consistent, but only have a convergence rate to . The table also shows that the post nuclear norm regularized estimation () quickly reduces the bias, and essentially agrees with the LS estimator (which is a consistent estimator in this MC design) after two iterations, as the theory predicts. The columns ATL(1) - ALT(5) in that table contain the results for an alternative bias corrected estimator that is presented in the appendix. It turns out that the alternative bias correction method is less effective in reducing the bias, and we therefore do not discuss it in the main text. Our recommendation in practice for inference on is the iteration procedure for explained in the previous section.

6 Extension to Single Index Models

We now consider the following generalization of the penalized LS estimator,

where is a known convex function of the single index , which also depends on the observed variables . The single index has the same structure as the conditional mean of the linear model (2), and for and we obtain the penalized LS estimator that was studied in previous sections. The nuclear norm penalty term is unchanged.

Let be the expected objective function, conditional on ,252525Remember that we consider as non-random, that is, all expectations are implicitly conditional on as well. Also, we condition on all the observed here, implying that we only consider strictly exogenous regressors in this section, but in principle the results could be extended to dynamic models. and denote derivatives of and with respect to by , , , etc. Let be the index evaluated at the true parameters. Let denote the domain of . We make the following assumptions on the objective function.

Assumption 2.

Let be such that , for some . Assume:

-

(i)

is independently distributed across and over , conditional on .

-

(ii)

The objective function is convex in , and once continuously differentiable in almost everywhere in . For any function the first derivative exists almost surely, and satisfies .

-

(iii)

is four times continuously differentiable in , with derivatives bounded uniformly over , . There exists such that .

-

(iv)

, for all .

Here, the last assumption crucially connects the distribution of conditional on with the chosen objective function . For the LS case we have , and Assumption 2 then becomes the familiar mean independence condition . This condition excludes a predetermined regressor. Some further examples for data generating processes and corresponding objective functions are

-

(a)

Maximum likelihood: Let conditional on have probability mass or density function , set and , and assume that is strictly convex in and three times continuously differentiable. A concrete example is a binary choice probit model, where , and is the cdf of .

-

(b)

Weighted Least Squares: Let outcomes be generated from the linear model (2) with , and let , and . Here, the are observed weights for each observation. A special case is , where is an indicator of a missing outcome .

-

(c)

Quantile Regression: Let outcomes be generated from the linear model (2), but instead of the mean restriction for we impose the quantile restriction , and we let , and , where is the quantile regression objective function, and is a chosen quantile of interest. See also Belloni, Chen, Madrid Padilla, and Wang (2023), Wang, Su, and Zhang (2022), and Feng (2023) for this case.

Some additional regularity conditions are needed to guarantee that those examples satisfy Assumption 2. For many models (e.g. quantile regressions and binary choice likelihood) we have . Then, the lower bound on in Assumption 2(iii) will require us to impose that is a bounded set, which can be guaranteed by assuming that and are uniformly bounded. Apart from that it is straightforward to verify Assumption 2 under standard regularity conditions for the respective model. Notice also that Assumption 2(ii) is formulated with the quantile regression case in mind, where is not well-defined at , but that is a probability zero event for continuously distributed .

In the following theorem we show that for with and the regressors have a generalized factor structure. We present the special case where there exists a single regressor (i.e., ) and the regressor is strictly exogenous for technical simplicity.

Theorem 5.

Let Assumption 2 be satisfied. Let , , and . Let . Assume that

-

(i)

.

-

(ii)

The regressor can be decomposed as such that , and .

-

(iii)

satisfies .

Then we have .

Condition (i) of the theorem is a restriction on the growth rate of the nuclear norm of , which was not required for the results in Section 3, where we assumed only that is fixed. However, this condition (i) imposes only an upper bound on the growth of ; it allows that contains both strong factors and weak factors.262626For a discussion of weak factors we refer to Onatski (2012).

Condition (ii) is satisfied if the regressor has a generalized factor structure,

where and , and we have with .

The proof of Theorem 5 is presented in the appendix, where we also discuss how the result could in principle be extended to regressors, which requires some additional technical restrictions. Notice also that the convergence rate of in Theorem 5 is different from the convergence rate obtained in Section 3, but this is likely an artifact of our proof strategy for Theorem 5. Finally, the analog of the nuclear-norm minimizing estimator to non-linear models is given by (limit for fixed ), but we do not provide results for that limiting estimator here. The goal of this section was not to fully discuss the non-linear case, but to highlight the potential of the nuclear norm penalization approach beyond the linear model that is main focus of this paper.

7 Conclusions

In this paper we analyze two new estimation methods for interactive fixed effect panel regressions that are based on convex objective functions: (i) nuclear norm penalized estimation, and (ii) nuclear norm minimizing estimation. The resulting estimators can also be applied in situations where the LS estimator may not be consistent, in particular when low-rank regressors are present and the true number of factors is unknown. We provide consistency and convergence rate results for the new estimators of the regression coefficients, and we show how to use them as a preliminary estimator to achieve asymptotic equivalence to the local version of the LS estimator. We have focused on the linear model with homogenous coefficients, which is a natural starting point to understand the usefulness of nuclear norm penalization approach for panel regression models, but there are several ongoing extensions, including developing a unified method to deal with non-linear models, heterogeneous coefficients, treatment effect estimation, nonparametric sieve estimation, and high-dimensional regressors, see Section 6 above, and also Athey, Bayati, Doudchenko, Imbens, and Khosravi (2021) and Chernozhukov, Hansen, Liao, and Zhu (2018).

References

- (1)

- Abadie, Diamond, and Hainmueller (2010) Abadie, A., A. Diamond, and J. Hainmueller (2010): “Synthetic control methods for comparative case studies: Estimating the effect of California’s tobacco control program,” Journal of the American statistical Association, 105(490), 493–505.

- Abadie, Diamond, and Hainmueller (2015) (2015): “Comparative politics and the synthetic control method,” American Journal of Political Science, 59(2), 495–510.

- Abadie and Gardeazabal (2003) Abadie, A., and J. Gardeazabal (2003): “The economic costs of conflict: A case study of the Basque Country,” American economic review, 93(1), 113–132.

- Adams (2017) Adams, C. (2017): “Identification of Treatment Effects from Synthetic Controls,” Available at SSRN 2904172.

- Ahn and Horenstein (2013) Ahn, S. C., and A. R. Horenstein (2013): “Eigenvalue ratio test for the number of factors,” Econometrica, 81(3), 1203–1227.

- Ahn, Lee, and Schmidt (2001) Ahn, S. C., Y. H. Lee, and P. Schmidt (2001): “GMM estimation of linear panel data models with time-varying individual effects,” Journal of Econometrics, 101(2), 219–255.

- Ahn, Lee, and Schmidt (2013) Ahn, S. C., Y. H. Lee, and P. Schmidt (2013): “Panel data models with multiple time-varying individual effects,” Journal of Econometrics, 174(1), 1–14.

- Alidaee, Auerbach, and Leung (2020) Alidaee, H., E. Auerbach, and M. P. Leung (2020): “Recovering network structure from aggregated relational data using penalized regression,” arXiv preprint arXiv:2001.06052.

- Armstrong, Weidner, and Zeleneev (2022) Armstrong, T. B., M. Weidner, and A. Zeleneev (2022): “Robust Estimation and Inference in Panels with Interactive Fixed Effects,” arXiv preprint arXiv:2210.06639.

- Athey, Bayati, Doudchenko, Imbens, and Khosravi (2021) Athey, S., M. Bayati, N. Doudchenko, G. Imbens, and K. Khosravi (2021): “Matrix completion methods for causal panel data models,” Journal of the American Statistical Association, 116(536), 1716–1730.

- Bai (2009) Bai, J. (2009): “Panel data models with interactive fixed effects,” Econometrica, 77(4), 1229–1279.

- Bai and Ng (2002) Bai, J., and S. Ng (2002): “Determining the Number of Factors in Approximate Factor Models,” Econometrica, 70(1), 191–221.

- Bai and Ng (2017) (2017): “Principal Components and Regularized Estimation of Factor Models,” arXiv preprint arXiv:1708.08137.

- Bai and Ng (2019) (2019): “Rank regularized estimation of approximate factor models,” Journal of Econometrics, 212(1), 78–96.

- Belloni, Chen, Madrid Padilla, and Wang (2023) Belloni, A., M. Chen, O. H. Madrid Padilla, and Z. Wang (2023): “High-dimensional latent panel quantile regression with an application to asset pricing,” The Annals of Statistics, 51(1), 96–121.

- Beyhum and Gautier (2019) Beyhum, J., and E. Gautier (2019): “Square-root nuclear norm penalized estimator for panel data models with approximately low-rank unobserved heterogeneity,” arXiv preprint arXiv:1904.09192.

- Beyhum and Gautier (2022) (2022): “Factor and Factor Loading Augmented Estimators for Panel Regression With Possibly Nonstrong Factors,” Journal of Business & Economic Statistics, pp. 1–12.

- Bickel, Ritov, and Tsybakov (2009) Bickel, P. J., Y. Ritov, and A. B. Tsybakov (2009): “Simultaneous analysis of Lasso and Dantzig selector,” The Annals of Statistics, pp. 1705–1732.

- Candes and Tao (2007) Candes, E., and T. Tao (2007): “The Dantzig selector: Statistical estimation when p is much larger than n,” The Annals of Statistics, pp. 2313–2351.

- Chamberlain and Moreira (2009) Chamberlain, G., and M. J. Moreira (2009): “Decision theory applied to a linear panel data model,” Econometrica, 77(1), 107–133.

- Chan and Kwok (2016) Chan, M., and S. Kwok (2016): “Policy evaluation with interactive fixed effects,” Preprint. Available at https://ideas.repec.org/p/syd/wpaper/2016-11.html.

- Chen (2014) Chen, M. (2014): “Estimation of nonlinear panel models with multiple unobserved effects,” Warwick Economics Research Paper Series No. 1120.

- Chen, Fernández-Val, and Weidner (2021) Chen, M., I. Fernández-Val, and M. Weidner (2021): “Nonlinear factor models for network and panel data,” Journal of Econometrics, 220(2), 296–324.

- Chen (2022) Chen, Q. (2022): “A Unified Framework for Estimation of High-dimensional Conditional Factor Models,” arXiv preprint arXiv:2209.00391.

- Chen and Pouzo (2012) Chen, X., and D. Pouzo (2012): “Estimation of nonparametric conditional moment models with possibly nonsmooth generalized residuals,” Econometrica, 80(1), 277–321.

- Cheng, Liao, and Schorfheide (2016) Cheng, X., Z. Liao, and F. Schorfheide (2016): “Shrinkage estimation of high-dimensional factor models with structural instabilities,” The Review of Economic Studies, 83(4), 1511–1543.

- Chernozhukov, Hansen, Liao, and Zhu (2018) Chernozhukov, V., C. Hansen, Y. Liao, and Y. Zhu (2018): “Inference For Heterogeneous Effects Using Low-Rank Estimations,” arXiv preprint arXiv:1812.08089.

- Chetverikov and Manresa (2022) Chetverikov, D., and E. Manresa (2022): “Spectral and post-spectral estimators for grouped panel data models,” arXiv preprint arXiv:2212.13324.

- Feng (2023) Feng, J. (2023): “Nuclear Norm Regularized Quantile Regression with Interactive Fixed Effects,” Econometric Theory, p. 1–31.

- Fernández-Val, Freeman, and Weidner (2021) Fernández-Val, I., H. Freeman, and M. Weidner (2021): “Low-rank approximations of nonseparable panel models,” The Econometrics Journal, 24(2), C40–C77.

- Franguridi and Moon (2022) Franguridi, G., and H. R. Moon (2022): “A uniform bound on the operator norm of sub-Gaussian random matrices and its applications,” Econometric Theory, 38(6), 1073–1091.

- Gobillon and Magnac (2016) Gobillon, L., and T. Magnac (2016): “Regional policy evaluation: Interactive fixed effects and synthetic controls,” Review of Economics and Statistics, 98(3), 535–551.

- Gobillon and Wolff (2020) Gobillon, L., and F.-C. Wolff (2020): “The local effects of an innovation: Evidence from the French fish market,” Ecological Economics, 171, 106594.

- Hastie, Tibshirani, and Wainwright (2015) Hastie, T., R. Tibshirani, and M. Wainwright (2015): Statistical learning with sparsity: the lasso and generalizations. CRC press.

- Holtz-Eakin, Newey, and Rosen (1988) Holtz-Eakin, D., W. Newey, and H. S. Rosen (1988): “Estimating Vector Autoregressions with Panel Data,” Econometrica, 56(6), 1371–95.

- Hsiao, Ching, and Wan (2012) Hsiao, C., H. S. Ching, and S. K. Wan (2012): “A panel data approach for program evaluation: measuring the benefits of political and economic integration of Hong kong with mainland China,” Journal of Applied Econometrics, 27(5), 705–740.

- Kiefer (1980) Kiefer, N. (1980): “A time series-cross section model with fixed effects with an intertemporal factor structure,” Unpublished manuscript, Department of Economics, Cornell University.

- Li, Qian, and Su (2016) Li, D., J. Qian, and L. Su (2016): “Panel data models with interactive fixed effects and multiple structural breaks,” Journal of the American Statistical Association, 111(516), 1804–1819.

- Li (2018) Li, K. (2018): “Inference for factor model based average treatment effects,” Available at SSRN 3112775.

- Lu and Su (2016) Lu, X., and L. Su (2016): “Shrinkage estimation of dynamic panel data models with interactive fixed effects,” Journal of Econometrics, 190(1), 148–175.

- Ma, Su, and Zhang (2022) Ma, S., L. Su, and Y. Zhang (2022): “Detecting latent communities in network formation models,” The Journal of Machine Learning Research, 23(1), 13971–14031.

- Miao, Li, and Su (2020) Miao, K., K. Li, and L. Su (2020): “Panel threshold models with interactive fixed effects,” Journal of Econometrics, 219(1), 137–170.

- Miao, Phillips, and Su (2023) Miao, K., P. C. Phillips, and L. Su (2023): “High-dimensional VARs with common factors,” Journal of Econometrics, 233(1), 155–183.

- Moon and Weidner (2015) Moon, H. R., and M. Weidner (2015): “Linear Regression for Panel With Unknown Number of Factors as Interactive Fixed Effects,” Econometrica, 83(4), 1543–1579.

- Moon and Weidner (2017) (2017): “Dynamic linear panel regression models with interactive fixed effects,” Econometric Theory, 33(1), 158–195.

- Mugnier (2022) Mugnier, M. (2022): “Make the Difference! Computationally Trivial Estimators for Grouped Fixed Effects Models,” arXiv preprint arXiv:2203.08879.

- Negahban, Ravikumar, Wainwright, and Yu (2012) Negahban, S., P. Ravikumar, M. J. Wainwright, and B. Yu (2012): “A unified framework for high-dimensional analysis of M-estimators with decomposable regularizers,” Statisical Science, 27(4), 538–557.

- Onatski (2010) Onatski, A. (2010): “Determining the number of factors from empirical distribution of eigenvalues,” The Review of Economics and Statistics, 92(4), 1004–1016.

- Onatski (2012) (2012): “Asymptotics of the principal components estimator of large factor models with weakly influential factors,” Journal of Econometrics, 168(2), 244–258.

- Pesaran (2006) Pesaran, M. H. (2006): “Estimation and Inference in Large Heterogeneous Panels with a Multifactor Error Structure,” Econometrica, 74(4), 967–1012.

- Piracha, Tani, and Tchuente (2017) Piracha, M., M. Tani, and G. Tchuente (2017): “Immigration Policy and Remittance Behaviour,” IZA Discussion Paper.

- Powell (2022) Powell, D. (2022): “Synthetic Control Estimation Beyond Comparative Case Studies: Does the Minimum Wage Reduce Employment?,” Journal of Business & Economic Statistics, 40(3), 1302–1314.

- Recht, Fazel, and Parrilo (2010) Recht, B., M. Fazel, and P. A. Parrilo (2010): “Guaranteed minimum-rank solutions of linear matrix equations via nuclear norm minimization,” SIAM review, 52(3), 471–501.

- Rohde and Tsybakov (2011) Rohde, A., and A. B. Tsybakov (2011): “Estimation of high-dimensional low-rank matrices,” The Annals of Statistics, 39(2), 887–930.

- Su, Shi, and Phillips (2016) Su, L., Z. Shi, and P. C. Phillips (2016): “Identifying latent structures in panel data,” Econometrica, 84(6), 2215–2264.

- Wang, Su, and Zhang (2022) Wang, Y., L. Su, and Y. Zhang (2022): “Low-rank panel quantile regression: Estimation and inference,” arXiv preprint arXiv:2210.11062.

Appendix A Appendix

A.1 An Example of a Non-convex LS Profile Objective Function

As an example for a non-convex LS profile objective function we consider the following linear model with one regressor and two factors:

where

and , , , and , , , , are all independent of each other. For , we generate the panel data for , and plot the LS objective function (3) in Figure 1, which is discussed in the main text.

A.2 Alternative Bias Correction

In this section, we discuss an alternative bias reduction method used in the Monte Carlo simulations in Section 5. The alternative method reduces the bias of the score function of the regularized least squares objective function . We introduce the procedure in a heuristic way without presenting a rigorous proof. We have implemented this alternative method in our Monte Carlo simulations, and while it indeed improves the nuclear-norm penalized estimates (see Table 1), it does not perform better than the iteration method described in Section 4.

Recall that , where . Define

We can write

Let , and

Suppose that we choose such that

| (A.1) |

Then, in view of (12) and (14), we write the profile objective function of the regularized least squares as

| (A.2) |

This shows that the term is the main source of the regularization bias. We suggest to approximate as follows,

| (A.3) |

where , with

From (A.2) and (A.3) we expect that should be a good approximation to . This heuristic suggests that we may reduce the bias of the nuclear norm regularized estimation by modifying the objective function.

For this, suppose that is a data dependent choice of that satisfies the condition (A.1). Let be a consistent estimator of . Let be an preliminary estimator. For example, or .

For , define

and

We modify the nuclear norm regularized objective function as

and update the estimator as

Appendix B Supplementary Appendix

B.1 Proofs for Section 2.1

For matrix , let the singular value decomposition of be given by , where , with .

Lemma S.1.

For any we have

where the minimization is over all matrices of the same size as and .

Proof of Lemma S.1.

The dependence of the various quantities on is not made explicit in this proof. Let . A possible value for is , where and , and therefore we have

The nuclear norm satisfies . A possible value for is , where and , which indeed satisfies , and therefore we have

where in the second step we found and plugged in the minimizing . By combining the above upper and lower bound on we obtain , which is the first statement of the lemma. Since is unique, we deduce that is the minimizing value, which is the second statement in the lemma. ∎

B.2 Proofs for Section 2.2

The function that appears in Lemma S.1 was defined in (12). We now define a similar function by for , and for , that is, we have

| (S.3) |

and for matrices we define . Using Lemma S.1 and the definition of the nuclear norm we can write

| (S.6) |

As already discussed in the main text, it is natural to rescale the profiled nuclear norm penalized objective function by , because it then has a non-trivial limit as . Using instead of therefore helps to clarify the scaling with in various expressions. The following lemma summarizes some properties of the function , which are useful for the subsequent proofs.

Lemma S.2.

Let and be matrices, be an matrix, and be a matrix. We then have

-

(i)

.

-

(ii)

, and .

-

(iii)

.

Proof of Lemma S.2.

# Part (i): From the definition of in (S.3) one finds for all . We thus obtain

# Part (ii): For this is just the triangle inequality for the nuclear norm. For we use (S.6) to write

where in the second step we reparameterized in the minimization problem, in the third step we used the triangle inequality for the nuclear norm, and in the final step we employed again (S.6). We have thus shown the first statement of this part. The second statement is obtained from the first statement by replacing and .

# Part (iii): We first show the result for . Let and be the singular value decompositions of those matrices. We then have and . Furthermore, we have . By choosing we obtain

| (S.7) |

which is the statement of part (iii) of the lemma for . For we find

where in the first step we used (S.6); in the second step we used (S.7) with replaced by ; in the third step we decomposed into four parts; in the fourth step we used that the minimization over implies that and at the optimum, because the components and of appear nowhere else in the objective function, so that choosing and is optimal; the fifth step is obvious (it is actually an equality, which is less obvious, but not required for our argument); in the sixth step we replaced and by an unrestricted in the minimization problems, which can only make the minimizing values smaller (again, this is actually an equality, but is sufficient to show here); and the final step again employs (S.6). We have thus shown the desired result. ∎

Before presenting the next lemma it is useful to introduce some further notation. For let . Let be an matrix such that the column span of equals the column span of the matrix . Analogously, let be an matrix such that the column span of equals the column span of the matrix .

Lemma S.3.

Proof of Lemma S.3.

We have

Here, we first plugged in the model for , then used part (iii) of Lemma S.2 with and , and in the final step used part (ii) of Lemma S.2. In the same way we obtain

where in the last step we also used part (i) of Lemma S.2. Furthermore, we find

where we used part (ii) of Lemma S.2 and the triangle inequality for the nuclear norm. Combining the inequalities in the last three displays gives

The derivation so far was valid for all . For the left hand side of the last display simply is . For we have, by (S.6),

so that we have shown the statement of the lemma. ∎

Lemma S.4.

Let model (2) hold, and let , and , for all . Then we have, for all ,

Proof of Lemma S.4.

Using the model and the assumptions on in the proposition we find

where the expectation is also implicitly conditional on , because is treated as non-random throughout the whole paper. Because is just a constant that does not depend on the parameters and , we can thus rewrite the definition of in (16) as

We can obtain from the profiled objective function that was defined in (5) by simply setting in the model (2). The bound on in Lemma S.3 is therefore applicable to if we just set in that lemma. We thus have, for all ,

We have , because minimizes , and combining this with the result in the last display gives the statement of the lemma. ∎

Proof of Proposition 1.

Let

Using the absolute homogeneity of the nuclear norm this definition implies that for any we have

| (S.8) |

Since the ball is a compact set and is a continuous function, there exists a value where the minimum is attained, that is, . By the assumption on the regressors in Proposition 1 we thus have .

Next, applying part (i) of Lemma S.2 we obtain

| (S.9) |

and also using Lemma S.4 we thus find that

From this and (S.8) with we obtain for any that272727 The bound (S.10) is sufficient for our purposes since we ultimately consider the limit here, but for a fixed value of (and ) this bound is potentially very crude if high-rank regressors are present. From Lemma S.4 one could then obtain a sharper bound on by not using part (i) of Lemma S.2 to simplify .

| (S.10) |

and therefore , as . ∎

B.3 Proofs for Section 3.1

Lemma S.5.

Let and . Assume that

satisfies . Then we have, for all ,

and

Proof of Lemma S.5.

By definition we have . Combining this with Lemma S.3 and equation (S.9), and writing , we obtain

The definition of in the theorem together with the absolute homogeneity of the nuclear norm implies

We have

because we have , and therefore , and also , and therefore .

We also have

and similarly

Combining the above inequalities gives the finite sample bound in the theorem,

and the same bound holds for if we set , because all bounds above, including Lemma S.3 are applicable for as well. Finally, the asymptotic statements in the theorem are immediate corollaries of the finite sample bounds. ∎

B.4 Proofs for Section 3.2.1

Lemma S.6.

Suppose that and are two matrices with ranks of and are and , respectively.

-

(i)

.

-

(ii)

.

-

(iii)

.

-

(iv)

If and , then .

-

(v)

If (or equivalently ), then .

Recall that the rank of is , which is fixed. Throughout the rest of the appendix, we use the following singular value decomposition of ,

| (S.11) |

where with , with , is the diagonal matrix of singular values of .

Suppose that is normalized as . Then, we have

Some further notation:

Let

These are the profile objective functions of and , respectively, which concentrate out parameter the . We also use the notation and .

Proof of Lemma 2.

# Step 1: Use (19) to show

By definition, we have

where . Let and . Then

Here the first inequality holds since , the second inequality holds by the Hölder inequality, the third inequality holds by (19), and the last inequality holds by the triangle inequality. We furthermore have

Therefore,

Thus, we have

Proof of Theorem 2..

Part (ii). Let Then, by definition we have

Under the assumption of the theorem we have and . Also, by Part (a) we have

Combining these, we can deduce the required result for Part (b). ∎

Proof of (20).

Since is positive semi-definite, by the Hölder inequality, and , we have

The required result follows since . ∎

B.5 Sufficient Conditions for Restricted Strong Convexity

In this section we discuss Assumption 1 in more detail. Define the distance between a matrix and the cone by

The following lemma provides an alternative formulation for our restricted strong convexity assumption.

Lemma S.7.

Let there exists a positive constant such that for any with , the regressors satisfy

Then Assumption 1 holds.

Proof of Lemma S.7.

Recall the definition where . Firstly, if , then the required result holds for any constant . Secondly, if , then the required result holds for because . Thus, in the following we only need to consider the case and . Also let .

Define , and . Then, for any and , we have

| (S.12) |

where the inequality holds because since and is a cone. Notice that

where and . This implies

with . Therefore, we have

Then, the required result of the lemma follows by the assumptions in the lemma. ∎

Lemma S.8.

Consider . Let be the singular values of the matrix . Assume that there exists a sequence such that

-

(i)

-

(ii)

wpa1.

-

(iii)

.

Then Assumption 1 is satisfied with .

This lemma could be generalized to . We would then need to impose the conditions for in the lemma for all linear combinations , in an appropriate uniform sense over all with .

Proof of Lemma S.8.

For given matrix , and matrix , and matrix , we want to find a lower bound on

By definition, we have

Also, (e.g., see Lemma 3.4 of Recht, Fazel, and Parrilo (2010)), and therefore . Using this we find

Here, we have weakened the constraint (allowing more values for ), and the minimizing value therefore weakly decreases. It is easy to see that for we have

because the optimal here equals rescaled by a non-negative number. We therefore have

Let

be the singular value decomposition of with singular values and normalized singular vectors and . The optimal in the last optimization problem has the form

for some (see Lemma S.1). Here, occurs if the constraint is not binding, that is, if . We therefore have

Here, the optimal equals , and we thus have

Let . For any there exists such that . We can therefore write

Shifting we can rewrite this as

where

Notice that is nonnegative and weakly decreasing and is weakly increasing. Then, for any integer valued sequence between 1 and such that ,

The assumptions of the lemma thus guarantee that . The definition of together with Lemma S.7 thus guarantees that Assumption 1 is satisfied with . ∎

Remarks

-

(a)