OPRE-2018-10-607.R1

Ma, Simchi-Levi, and Teo

Single-leg RM with Limited Demand Information

On Policies for Single-leg Revenue Management with Limited Demand Information

Will Ma \AFFGraduate School of Business, Columbia University, New York, NY 10027, \EMAILwm2428@gsb.columbia.edu \AUTHORDavid Simchi-Levi \AFFInstitute for Data, Systems, and Society, Department of Civil and Environmental Engineering, and Operations Research Center, Massachusetts Institute of Technology, Cambridge, MA 02139, \EMAILdslevi@mit.edu \AUTHORChung-Piaw Teo \AFFNUS Business School, National University of Singapore, Singapore, \EMAILbizteocp@nus.edu.sg \ABSTRACT

In this paper we study the single-item revenue management problem, with no information given about the demand trajectory over time. When the item is sold through accepting/rejecting different fare classes, Ball and Queyranne (2009) have established the tight competitive ratio for this problem using booking limit policies, which raise the acceptance threshold as the remaining inventory dwindles. However, when the item is sold through dynamic pricing instead, there is the additional challenge that offering a low price may entice high-paying customers to substitute down. We show that despite this challenge, the same competitive ratio can still be achieved using a randomized dynamic pricing policy. Our policy incorporates the price-skimming technique from Eren and Maglaras (2010), but importantly we show how the randomized price distribution should be stochastically-increased as the remaining inventory dwindles. A key technical ingredient in our policy is a new “valuation tracking” subroutine, which tracks the possible values for the optimum, and follows the most “inventory-conservative” control which maintains the desired competitive ratio. Finally, we demonstrate the empirical effectiveness of our policy in simulations, where its average-case performance surpasses all naive modifications of the existing policies.

online algorithms, competitive ratio, revenue management, dynamic pricing

1 Introduction

In the single-leg revenue management problem, a firm is selling multiple products that share a single capacity over a finite time horizon. The prices of the products and the unreplenishable starting capacity are all exogenously determined. The firm’s objective is to maximize its total revenue earned, by dynamically controlling the availability of different products over time. The tradeoff lies between “myopic” controls which maximize revenue at an immediate point in time, and “conservative” controls which preserve capacity for the remaining time horizon.

This problem was originally motivated by airlines. Indeed, for a single flight leg, it has a limited seat capacity, and the products correspond to different “fare classes” (e.g. economy, basic economy) dictating prices at which seats could be sold. The flight’s seat capacity and fare classes have been determined long in advance, through factors such as business strategy and competitor price points. Finally, the time horizon is finite, ending upon the flight’s departure.

We study this problem in the setting where very limited information is given or can be learned about demand. This setting was introduced by Ball and Queyranne (2009), Lan et al. (2008), who derive heuristic controls based on only knowledge of the fare class prices. These papers consider booking limit policies, which can be described as follows. Initially, all of the fare classes are made available to customers. Once the fraction of total seats sold surpasses a critical threshold, the lowest fare becomes unavailable. Progressively higher fares are made unavailable until the flight either becomes full or takes off.

An important assumption made in these papers is that the demands for the different fare classes are independent. That is, although the lower fares are made available until their booking thresholds are reached, there is no risk of cannibalization in sales, where a customer who would have accepted a higher fare substitutes down into buying a lower fare. A classical justification for this is that the fare classes are designed to segment customers and achieve price discrimination—i.e., the drawbacks of basic economy are supposed to dissuade price-insensitive travelers from buying down.

However, fare classes rarely achieve perfect price discrimination, and in the age of e-commerce, increasingly many airlines are introducing overlapping fare families despite the cannibalization (Fiig et al. 2012). Furthermore, most items (unlike seats on an airplane) are sold using a single price and not packaged into fare classes at all. Motivated by these two facts, our goal is to derive advanced pricing controls for the single-leg revenue management problem under limited demand information, which do not require the assumption of no cannibalization.

1.1 Dynamic Pricing Model

In this paper, we focus on the dynamic pricing problem of a single retail item being marked at a single price, with no fare classes at all. To connect back to airlines, we can interpret this as offering an assortment with all fare classes greater than or equal to the posted price. In the conclusion of the paper, we explain why this immediately implies the same results for the airline model with fare classes and substitution, as long as substitution follow a random-utility choice model.

We let denote the set of prices which the firm could feasibly offer at any point in time, corresponding to the set of fare classes discussed earlier. We usually assume to be discrete for ease of exposition and computation. In Section 5.1, we allow for to be any continuous price interval, and derive comparable theoretical results to those when the interval is approximated using discrete prices. Discreteness of is further justified in industries with established price points to charge for items, e.g. prices ending in 99 cents.

The dynamic pricing problem proceeds as follows. The item starts with units of discrete inventory. Sequentially-arriving customers each have a valuation , denoting the maximum price in that the customer is willing to pay. We colloquially refer to customer as arriving in “time ”; however, we emphasize that does not correspond to an actual unit of time and that the total number of customers is unknown. An online algorithm sequentially charges a price for each customer , and if , then revenue is earned and one unit of inventory is depleted.

In settings where no information is given about demand, an online algorithm is evaluated by comparing its total revenue earned on different sequences of valuations to that of a clairvoyant optimum. For any such sequence , the offline optimum is defined as the maximum revenue that could have been earned from deterministically knowing all the valuations in advance, equal to the sum of the largest values in . For , if an online algorithm can guarantee that its revenue is at least on every sequence , then it is said to be -competitive. If is best-possible in that any (potentially randomized) online algorithm cannot uniformly guarantee better than revenue over all sequences , then is called the competitive ratio.

We now describe the nature of and what is known about it before the online algorithm has to decide price . We consider the following variants.

-

1.

Public vs. Personalized Pricing: In public pricing, must be decided before knowing anything about valuation . The motivation for this is an e-commerce platform that posts a public price without knowing which customer will arrive next. After customer arrives and makes a purchase decision based on price , (the distribution of) can be estimated based on her characteristics such as IP address (and this distribution can be posterior-updated based on her purchase decision). The platform can then update its price for the next customer.

By contrast, in personalized pricing, (the distribution of) is given before having to decide . The motivation for this is an e-commerce platform that uses a customer’s characteristics upon login to charge them a personalized price. Like before, customer then makes a purchase decision based on price . However, in personalized pricing the online algorithm has more information (namely, about ) before having to make each decision .

-

2.

Deterministic vs. Stochastic Valuations: To illustrate our basic technique, and to relate to the model of Ball and Queyranne (2009), we first assume that each valuation can be deterministically estimated based on the characteristics of customer . We then extend to the setting where only a distribution for can be estimated each time. We would like to point out in the public pricing setting, clickstream data (the user’s navigation path after they saw the price) can also be incorporated to generate these distributional estimates, which can greatly improve the accuracy as found by Montgomery et al. (2004).

We emphasize that under all combinations of variants, when deciding price , (the distributions of) valuations and the purchase decisions of customers are known, and any information about valuations or the length is unknown.

1.2 Outline of Theoretical Results

Before stating our new results for the variants above, we first observe that—if personalized pricing is permitted on deterministic valuations, then our dynamic pricing model is equivalent to the multi-fare-class model of Ball and Queyranne (2009). Indeed, if the platform can always charge the maximum-willingness-to-pay of any customer it sells to, then it has achieved the same price discrimination assumed by fare classes. Ball and Queyranne (2009) show in their model that the competitive ratio depends on only the price set and not the starting inventory . Letting denote this optimal competitive ratio, the booking limit policies of Ball and Queyranne (2009) imply -competitive pricing policies in our model under the personalized, deterministic variant.

In light of this, our main theoretical contribution is the following results in progressively more difficult/general variants.

-

1.

In Section 3, we derive -competitive public pricing policies for deterministic valuations. We motivate our main algorithmic idea in Section 3.1, illustrate it through geometrically “stacking” the valuations in Sections 3.2, and formalize it in Section 3.3. We consider variations which satisfy intuitive properties that will become useful later, in Sections 3.4–3.5.

-

2.

In Section 4, we extend our earlier ideas for deterministic valuations into -competitive public pricing policies for stochastic valuations. A unique challenge arises in Section 4.2, where we use sampling to convert a -competitive algorithm with exponential runtime into a -competitive algorithm with polynomial runtime.

All of these policies are best-possible. Indeed, since Ball and Queyranne (2009) show that a personalized pricing policy on deterministic valuations cannot be better than -competitive, any online policy in our more difficult/general variants cannot be better then -competitive.

Our policies use the price-skimming technique of Eren and Maglaras (2010), who analyze how the price of an item should be distributed (e.g. across stores, across time) when the price set is known but demand is completely unknown. Their model corresponds to ours when the inventory constraint is irrelevant (i.e. when ), in which case they show that the competitive ratio is also . By contrast, our work shows how the price-skimming distribution should change over time based on remaining inventory. In fact, our policies satisfy the following structural property:

“At any time step, the price distribution which maximizes the competitive ratio is strictly stochastically-decreasing in the amount of remaining inventory.”

This is analogous to a classical structural property when the demand sequence is distributionally-known in advance and dynamic programming can be used (Gallego and Van Ryzin 1994, Zhao and Zheng 2000):

“At any time step, the price which maximizes the expected revenue is strictly decreasing in the amount of remaining inventory.”

This structural property turns out to be crucial for good empirical performance. In fact, in Section 5.2 we extend the results in Eren and Maglaras (2010) to derive a -competitive public pricing policy which does not require any information about the valuations; however, such a policy is inventory-oblivious and performs poorly in computational experiments.

1.3 Computational Experiments

In Section 6, we conduct simulations in the personalized online revenue management setting popularized by Golrezaei et al. (2014), where the stochastic valuation distribution of each customer is revealed before a personalized price is offered, but nothing is known about future customers. For a fixed price set and starting inventory, we randomly generate 10000 sequences with different lengths and valuation distributions, that capture the full range of instances from “myopic” controls (which always maximize the immediate revenue) being optimal to “conservative” controls (which always offer the maximum price) being optimal. We compare the average-case performance of our policy to those of Ball and Queyranne (2009), Eren and Maglaras (2010), as well as combinations and modifications of them designed to exploit personalized information, and the baseline “myopic” and “conservative” controls. We repeat this experiment for different price ranges, price granularities (discrete vs. continuous prices), and staring inventory levels. We draw the following conclusions:

-

1.

Policies that make use of information about both the valuation distributions and the remaining inventory perform significantly better than those that do not, with awareness of remaining inventory being particularly important;

-

2.

Among the two policies that do so, (the personalized form of) our policy accounts for inventory more precisely than (the personalized form of) the booking limit policy of Ball and Queyranne (2009), allowing it to achieve not only -competitiveness in theory, but improved average-case performance in practice.

We should note that although we only tested policies designed for worst-case performance on an unknown demand sequence, it is certainly plausible for a policy without such a worst-case guarantee to have good average-case performance. However, we know of no such candidates, and have tried to exhaustively test all variants of known algorithms which operate under our framework (where it is not possible to forecast/learn future demand), and have found our Valuation Tracking procedure to perform best. Developing alternative policies in this setting, not based on worst-case analysis, would be an interesting direction for future work.

2 Literature Review

Single-leg revenue management is a cornerstone problem in revenue management and pricing, as outlined in Talluri and Van Ryzin (2006). Many different approaches for modeling demand have been considered over the years, as surveyed in Araman and Caldentey (2011), den Boer (2015). When nothing is known or can be learned about demand, one often resorts to competitive ratio analysis (Borodin and El-Yaniv 2005), and this has been done for the single-item revenue management problem, where the decision is accept-reject, in Ball and Queyranne (2009). Our work extends their booking limit idea to pricing (cf. Maglaras and Meissner 2006), by integrating it with the price-skimming idea from Eren and Maglaras (2010) and its interpretation as a randomized price (Bergemann and Schlag 2008), in what we call a “Valuation Tracking” procedure.

We now compare our algorithmic ideas and results with other streams of literature.

Valuation tracking vs. prophet inequalities.

The algorithmic idea of “tracking” what a clairvoyant would do and imitating it dates back to the “prophet inequalities” of Krengel and Sucheston (1977). Prophet inequalities have seen a recent surge in the computer science literature (Kleinberg and Weinberg 2012, Dütting et al. 2016, 2017, Correa et al. 2017, 2018), and like our paper, they also establish ratio guarantees relative to a clairvoyant optimum in pricing problems.

However, the crucial difference is that in the prophet inequalities literature, it is assumed that the universe of possible demand functions is given at the start (or can be sampled from, like in Azar et al. (2014)). Even if the buyers can arrive in an “adversarial” order (chosen adaptively by the “almighty” adversary from Kleinberg and Weinberg (2012)), it is guaranteed that each demand function given at the start will appear exactly once. By contrast, our valuation tracking technique operates with only knowledge of the universe of prices; it is not promised that there exists a customer who is willing to pay the highest price. Our guarantees are also different in that they are parametrized by the given universe of prices , while the classical prophet inequality result is a uniform -guarantee. Although our guarantee of is usually smaller than , it holds under less information about demand.

Valuation tracking vs. water-filling/water-level algorithms.

After each customer, our valuation tracking procedure geometrically “stacks” her valuation above the ’th largest valuation seen thus far, in effect “balancing” the heights assigned to the units of inventory (see Section 3.2, Figure 1). This idea is similar to many algorithms which use “water-filling” to balance the levels of different buckets. For example, in the Adwords problem, the buckets correspond to different advertisers’ budgets, and the algorithm prioritizes assigning ads to buckets which are the lowest percent to being full (Kalyanasundaram and Pruhs 2000, Mehta et al. 2007, Devanur et al. 2013). In e-commerce, a similar algorithm for personalized recommendation is used to make different items’ inventories sell out at roughly the same time (Golrezaei et al. 2014, Chen et al. 2016, Ma and Simchi-Levi 2017, Cheung et al. 2018). Online water-filling algorithms have also been used for allocation in Gaussian channels (Thekumparampil et al. 2014).

Although the idea is similar, our valuation tracking procedure balances the valuations assigned to the different units of a single item, while the above water-filling algorithms balance the allocation rates of different items. The constant competitive ratio guarantees in the above papers generally do not apply to our setting, because they don’t consider the pricing decision for an item—the only exception is Ma and Simchi-Levi (2017). However, our valuation tracking is a much more specialized procedure for a single item, and our competitive ratio guarantee is strictly greater than their corresponding guarantee, for any price set . Our valuation tracking procedure also leads to public pricing algorithms, whereas they always assume the ability to personalize.

Valuation tracking vs. dynamic learning and pricing.

Dynamic pricing (with inventory constraints) has been extensively studied in the setting where demand is initially unknown and must be learned over time. The learning problem with stationary demand was initiated by Besbes and Zeevi (2009), and has been subsequently studied by Babaioff et al. (2011), Badanidiyuru et al. (2012, 2013), Babaioff et al. (2015), den Boer and Zwart (2015), to list a few references. Inventory-constrained dynamic learning and pricing has also been studied in various Bayesian (Araman and Caldentey 2009, Chen and Wu 2016) and minimax (Lim and Shanthikumar 2007, Zhang et al. 2016) settings.

Although these papers all consider posted-pricing decisions under limited inventory (called “budgets” in some cases), their main algorithmic challenge is in when to explore new prices to learn unknown demand rates, vs. when to exploit prices already known to generate a high revenue rate. By contrast, for our valuation tracking algorithm, the adversarial demand cannot be learned, and the main algorithmic challenge in how to “hedge” against the different possibilities for the valuation that will arrive next. The theoretical guarantees are also different—in learning and pricing, the focus is usually on how the “regret” (the difference from the optimum) scales with the number of IID customers ; while in competitive analysis, the focus is on ratio guarantees which hold without any assumptions on the number of customers or their valuations being IID.

3 Algorithms for Public Pricing and Deterministic Valuations

In this section we consider the variant of the model introduced in Section 1.1 with deterministic valuations and public pricing. We assume a discrete set of prices but all of our results carry over to having a continuous range of prices taking the form , as we discuss in Section 5.1.

For any positive integer , let denote the set . We assume that consists of discrete prices, i.e. , sorted . We define to be 0, and then the valuation at any time lies in , with representing the lack of a customer during time . Similarly, we define to be , and then the price at any time lies in , with representing the firm shutting off demand during time , which is the only option if its inventory is out of stock. Let be the indicator variable for making a sale during time , i.e. it is 1 if , and 0 otherwise.

Let denote the number of time steps. None of the algorithms in this paper assume any knowledge of ; note that can always be made arbitrarily large by inserting customers with valuation 0. We will hereafter treat as the unknown total number of customers, and interchangeably use the phrases “customer ” or “time ” to refer to valuation (even if it is 0).

In the public pricing variant, an online algorithm must choose each based on only the history of past prices and valuations, . This history also determines the values of . The online algorithm does not know , and has no information about the current valuation or the future valuations , when choosing . By contrast, the offline optimum knows the entire sequence before having to choose any prices. Given any valuation sequence , we use the and variables to refer to the execution of an online algorithm on the valuation sequence. Since the online algorithm may be randomized, we treat and as random variables. Let denote the total revenue earned by the online algorithm, equal to . Then is its expected revenue. Meanwhile, let denote the offline optimum for sequence , equal to the largest valuations from . Formally, an online algorithm is said to be -competitive if

| (1) |

For an initial setup given by and , the maximum possible value of in (1) is called the competitive ratio. We will omit the arguments in and when the context is clear.

As explained in Section 1.1, since our problem captures the problems of both Ball and Queyranne (2009) and Eren and Maglaras (2010), an upper bound for the value of in (1) is given by , as defined below.

Definition 3.1

For any , , and , define:

-

•

for all (recall that );

-

•

;

-

•

.

The interpretation of in Ball and Queyranne (2009) is the fraction of initial inventory “set aside” for prices and higher. The interpretation of in Eren and Maglaras (2010) is the fraction of time that price should be charged. Both of these papers establish that the competitiveness guarantee in (1) cannot be greater than , via Yao’s minimax principle (Yao 1977). In this paper, we derive -competitive algorithms for our dynamic pricing problem, which shows that the competitive ratio in fact equals .

3.1 New Techniques, and why Existing Techniques Fail

We explain the need for our main technical ingredient—a new “valuation tracking” procedure which incorporates both booking limits and price-skimming—by explaining why naive attempts to derive a -competitive algorithm fail under our dynamic pricing model.

We consider the following example, where the price set is , and we will refer to customers with these valuations as being of type-L (Low), type-M (Medium), and type-H (High), respectively. The competitive ratio for this price set derived by Ball and Queyranne (2009) and Eren and Maglaras (2010) is . We describe below their policies for this example.

-

•

Booking Limits (Ball and Queyranne 2009): Initially charge $1; increase the price to $2 after 1/2 of the starting inventory has been sold; further increase the price to $4 after 3/4 of the starting inventory has been sold. (This is the variant of booking limits with “theft nesting”.)

-

•

Price-skimming (Eren and Maglaras 2010): Charge $1 for 1/2 of the time steps; charge $2 for 1/4 of the time steps; charge $4 for 1/4 of the time steps.

These policies have the benefit that they never need any information about the valuations. However, we now see why these policies fail to be -competitive, under our dynamic pricing model.

Attempt 1: Direct implementation of booking limits.

It is easy to see that this would not be 1/2-competitive—suppose just one type-H customer arrived at the start. The algorithm would be charging the low price of $1, while the offline optimum would be the customer’s valuation of $4.

Any direct implementation of price-skimming would suffer similarly, since there could be a single type-H customer who arrives during a time when the price is set to $1.

Attempt 2: Price-skimming as a randomized price.

It appears that the problem with Attempt 1 can be solved using the “random price” interpretation of price-skimming—instead of deterministically partitioning the time horizon according to ratios and offering prices 1,2,4 respectively, one could at each time step choose the prices randomly with respective probabilities . Then, if a single type-H customer arrives, the expected revenue would be

which is 1/2 of the customer’s valuation of $4. It can be checked that 1/2 of the customer’s valuation is also earned when it is $1 or $2; this is by construction of the price-skimming distribution.

However, having a fixed price-skimming distribution is no longer effective under inventory constraints. Indeed, if a long sequence of type-L customers arrive, then this would deplete the inventory with high probability, and type-H customers who arrive last-minute would not be served, and the ratio of optimum earned would again be 1/4.

Attempt 3: Naive incorporation of booking limits into price-skimming.

It appears that the problem with Attempt 2 can be solved by respecting the booking limits, i.e. forbidding price-skimming from randomly choosing the price of $1 after 1/2 of the starting inventory has been sold. However, this still fails to be 1/2-competitive, as shown by the following example. Suppose the starting inventory is , and that 2 type-H customers arrive followed by a type-L customer, with no customers arriving after that. The optimum would be $9. However, the algorithm’s revenue would only equal $4: it would earn $2 in expectation from each of the type-H customers, depleting 2 units of inventory, and then earn $0 from the type-L customer due to the booking limit.

Our procedure: Valuation tracking.

The problem with Attempt 3 leads to the following observation—the optimum is guaranteed to increase from the first 4 customers (since there are 4 units of inventory), so in order to be 1/2-competitive, the algorithm must maintain the initial price-skimming distribution for the first 4 customers. After that, the algorithm can respect booking limits as long as customers rejected in this way would not increase the optimum, and in fact should do so, to avoid the problem in Attempt 2 of stocking out. This motivates our procedure below.

-

•

Valuation Tracking: At each time , let denote the smallest value (possibly 0) in the 4 largest valuations to have arrived before time . Then, randomly choose the price so that if the unknown valuation at time satisfies , then the algorithm earns in expectation

(2)

In (2), is the gain in the offline optimum should the valuation of customer be , and 1/2 is the desired competitive ratio. The constraint that the algorithm’s revenue exactly equals (2) forces the algorithm to use the most inventory-conservative control which maintains 1/2-competitiveness, thereby hedging against a stockout. The price distribution used at each time depends on the inventory state, and in fact, the calculation for the algorithm’s expected revenue must account for the probability of stocking out before time . The surprising fact is that it is possible to choose price distributions (for each inventory state) which collectively guarantee expected revenue of (2).

Remark about personalization.

In this paper we also consider the setting where a customer’s valuation is distributionally-given before her price is decided. It is possible to modify the above examples to show that the attempts similarly fail in this setting—see E-supplement 8.

3.2 Illustration of Valuation Tracking Procedure

As explained above, the goal of Valuation Tracking is to earn a constant -fraction of the gain in from each customer arriving. This requires tracking the current value of , i.e. the sum of the largest valuations to have arrived before the current time step. We now illustrate how this is done and why it is possible to be -competitive.

We consider the same example with and . We consider a starting inventory of , and suppose that 5 customers, with valuations , have already arrived. The current value of is then the sum of these 5 valuations, .

The procedure considers the possibilities for the increase in from the next customer, which we denote as (recall that a pricing decision must be made before knowing the valuation of the next customer). Since the smallest valuation currently counted toward is 1, if the valuation of the next customer if 4, then ; if it is 2, then . If the next customer has valuation not exceeding 1, then . The procedure wants to guarantee that its expected revenue on the next customer is at least , for all of these possible valuations. To accomplish this, it has to consider the probability that it has stocked out at this point; on those sample paths its revenue is 0.

Our procedure cleanly accounts for the probability of stocking out using the following approach. Each customer is assigned to a specific unit of inventory upon arrival. Each inventory unit maintains a variable , which is the maximum valuation of a customer previously assigned to it. The next customer is always assigned to an unit with the smallest value of , regardless of whether that unit has already been sold. In this way, the assignment procedure is deterministic, and allows us to maintain an invariant: the probability a unit has been sold is dependent on only the (deterministic) value of .

For each customer, the procedure makes an offer to her only if unit has not been sold, at a random price exceeding . The higher is, the more likely it is that unit has been sold, and the lower the expected revenue from that customer. However, if is high, then the potential increase in from that customer is also lower; if the valuation of the customer does not exceed , then both the procedure’s revenue and are 0. By properly choosing the distributions for the random prices, our procedure is able to maintain the invariant on the probability of each unit being sold, while earning in expectation from each customer.

Returning to the example, given that the first 5 customers had valuations , the values of for are shown in the LHS of Fig. 1. The next customer, “customer #6”, is assigned to inventory unit 2. After her valuation is revealed to be 2, the updated configuration is shown on the RHS of Fig. 1, regardless of whether she was offered a price.

Customer #6 would have been turned away if unit 2 was sold before her arrival, even if other units were available. When , the probability that a unit has been sold equals if is , respectively. These probabilities correspond to the values of from Definition 3.1. Since was 1 before customer #6 arrived, she is made an offer with probability , at a random price exceeding 1. The price is 2 with probability proportional to , and 4 with probability proportional to (again using the values of ), hence each price would be offered with probability . The customer’s valuation is 2, so she will only buy the item if offered price 2, which occurs with total probability . Note that:

-

1.

Customer #6 increases the probability of unit 2 being sold from to , which is consistent with her increasing from 1 to 2;

-

2.

Customer #6 increases the value of , equal to , by 1 (from 12 to 13);

-

3.

Customer #6 brings in expected revenue .

Therefore, during time step 6, our procedure has earned expected revenue . We will show that it achieves this for a general , and all time steps , regardless of the valuation of customer .

3.3 Valuation Tracking Procedure and Analysis

We now formalize our valuation tracking procedure, in Algorithm 1.

In line 1, the procedure offers exactly one of the prices , with the offering probabilities summing to unity. Note that it cannot branch to line 1 if . This can be seen in the following way. If , then must have been assigned to some past customer with . At time , either inventory unit was already sold, or customer was offered a price at most , which she would have accepted. In either case, must be .

The analysis of Algorithm 1 is conceptually simple. Let be the index in such that at the end of time , and be the index such that . We show that the following claims are maintained:

-

1.

At the end of each time step , the probability that any inventory unit has been sold is ;

-

2.

During a time step , if the valuation of the customer exceeds the level of the inventory unit she is assigned to, i.e. , then:

-

(a)

The expected revenue earned by Algorithm 1 is ;

-

(b)

The increase in the offline optimum is .

-

(a)

If during a time step , then both the revenue of Algorithm 1 and the gain in are 0.

These claims establish the following theorem, whose full proof is deferred to E-supplement 9.

Theorem 3.2

Algorithm 1 is -competitive.

3.4 Modified Algorithm based on Valuation Tracking Procedure

In this section we present a modified version of Algorithm 1 which is useful for the subsequent developments under the stochastic-valuation model in Section 4.

First we show how to modify Algorithm 1 so that its decision at each time depends on only the remaining inventory, instead of the entire history of purchase decisions .

Definition 3.3

For all , let denote the random variable for the amount of remaining inventory at the end of time , which is equal to .

Our modified algorithm makes an offer to customer according to the probability that unit hasn’t been sold, conditioned on the realized value of . In this way, its decisions depend on only the inventory state, instead of the exact decisions of past customers.

Definition 3.4 (Algorithm 1’)

Define the following algorithm for choosing the price at each time , based on the past valuations and the amount of remaining inventory .

Algorithm 1’ chooses the distribution for by “averaging” over all runs of Algorithm 1 which have the same value of . We first remark that this can be done in polynomial time, despite there being exponentially many sample paths for Algorithm 1. We prove the following in E-supplement 10.

We now introduce some notation to disambiguate between random variables depicting the runs of different algorithms.

Definition 3.6

For an algorithm , let , , and be the random variables for the price at time , purchase decision at time , and inventory remaining at the end of time , respectively. Let be the random variable for the total revenue earned by algorithm . We will omit the superscripts when the context is clear.

We show that Algorithms 1 and 1’ are virtually the same in that they have identical distributions for the remaining inventory at each time step, as well as the random price at each time step conditioned on any value of remaining inventory. This also establishes that Algorithm 1’ is feasible, in that it does not try to make a sale with zero remaining inventory.

Lemma 3.7

For all , such that , and , .

Also, for all and , .

Lemma 3.7, proven in E-supplement 10, is a consequence of the design of Algorithm 1’. For all , the random price is identically distributed as , conditional on any value for the amount of remaining inventory at the end of time . Hence if and are identically distributed, then so are and . This allows us to inductively establish that the two algorithms have the same aggregate behavior after combining all sample paths, even though their behavior may differ given a specific history of purchase decisions. This also makes it easy to see that the expected revenues of the two algorithms are the same. Lemma 3.7 directly implies the following theorem.

Theorem 3.8

Algorithm 1’ is -competitive.

3.5 Further Modified Algorithm and Structural Properties

In this section we present a further-modified version of Algorithm 1’ which satisfies two structural properties: (i) it never offers price to a customer if it has remaining inventory, offering the maximum price instead; (ii) the distribution of prices offered to a customer is strictly stochastically-decreasing (see Corollary 3.12) in the amount of remaining inventory. Property (ii) is the stochastic analogue of the classical structural result from Gallego and Van Ryzin (1994, Thm. 1) and its generalization to non-homogeneous demand in Zhao and Zheng (2000, Thm. 3): at any time step, if the firm has more inventory, then the optimal offering price is strictly lower.

Definition 3.9 (Algorithm 1”)

We prove the following general lemma, which is intuitively easy to see, in E-supplement 10.

Lemma 3.10

Let be any pricing algorithm. Let be the modified algorithm which: whenever would offer price to a customer while there is remaining inventory, offers price instead. Then on any valuation sequence , .

Lemma 3.10 shows that Algorithm 1” is -competitive. Now, we would like to further show that the probability of Algorithm 1’ rejecting, or correspondingly the probability of Algorithm 1” offering the maximum price, is smaller when conditioned on larger values of remaining inventory.

Theorem 3.11

Suppose that the unconditional probability of Algorithm 1’ rejecting customer , , lies in (0,1). Then for any with and ,

This structural property is intuitive, and we defer its proof to E-supplement 10. Theorem 3.11 allows us to conclude with the following corollary about strict stochastic dominance.

Corollary 3.12

For any , suppose with , and let denote the CDF’s of the price offered by Algorithm 1” at time conditional on the remaining inventory being , respectively. Then for all , and moreover, the dominance is strict in that for some price .

This intuitive property of raising prices as inventory dwindles contributes to the strong empirical performance of our algorithm, as we will explain in Section 6.

4 Algorithms for Public Pricing and Stochastic Valuations

In this section we extend the results from Section 3 to allow for stochastic valuations. The model with stochastic valuations differs from the model with deterministic valuations studied in the previous section in the following ways.

-

•

The valuation of each arriving customer is now randomly drawn from some distribution. The valuations of different customers are independent, but not necessarily identically distributed.

-

•

An online public pricing algorithm is given the valuation distribution of each customer after the price for that customer has been chosen.

-

•

The algorithm also sees the purchase decision of the customer at the price offered, and hence can posterior-update this valuation distribution for the customer if it wishes.

Definition 4.1

We use the following notation, defined for all :

-

•

: the valuation of customer , a random variable taking values in ;

-

•

: the probability vector for the distribution of , with and .

With stochastic valuations, we say that an online algorithm is -competitive if

| (3) |

In (3), the numerator is the revenue earned in expectation over both the randomness in the valuations and any randomness in the algorithm, while the denominator is the clairvoyant optimum defined as the expected sum of the largest valuations. We note that this optimum is an upper bound on the revenue of the optimal dynamic program knowing distributions in advance, and hence any value of which satisfies (3) implies the same guarantee relative to the optimal DP. Moreover, since the guarantee in (3) cannot be greater than even when are deterministic (in which case the DP value equals ), our -competitive algorithms are still optimal if one were to use the DP value in the denominator of definition (3) instead. By using the relaxation , our denominator is much easier to analyze.

We should point out that with stochastic valuations, another commonly-studied relaxation which could have been used in the denominator of (3) is the deterministic linear program (DLP) with distributions . By the same argument about being deterministic, the competitive ratio relative to the DLP also cannot be greater than . However, we provide in E-supplement 11 examples of where the competitive ratio relative to the DLP is strictly smaller than . Therefore, we choose our relaxation because it automatically provides the tight competitive ratio relative to the DP. Nonetheless, we believe that pinpointing the different value of competitive ratio relative to the DLP is an interesting theoretical problem.

4.1 Optimally-Competitive Algorithm with Exponential Runtime

Having defined our clairvoyant optimum, we now derive -competitive algorithms in the stochastic-valuation model. We do so by using our valuation tracking procedure as a subroutine, in a similar way to the development in Section 3.4, which may be helpful to reference.

Conceptually, our algorithm is a generalization of Algorithm 1’ to stochastic valuations. However, since the assignment procedure in Algorithm 1 is no longer deterministic, we describe the algorithm the following way. At a time step , having seem distributions and knowing remaining inventory :

-

1.

Consider a run of Algorithm 1 to the end of time , where are randomly drawn according to . For all , compute , where the probability is over both the random valuations, and the random prices chosen by the algorithm. (If has measure 0, then choose price .)

-

2.

For each , choose price with probability .

We will call this algorithm and use random variables (coming from Definition 3.6) to refer to its execution. It will be seen that is a feasible policy when we establish that and are identically distributed at every time step .

We allow to use Exponential running time, which is required for computing the conditional probabilities . To see why, note that the geometric stacking configuration from Algorithm 1 is no longer fixed once the valuations are stochastic. Therefore, our polynomial-time computation trick (Lemma 3.5) for Algorithm 1’ (the special case of under deterministic valuations) can no longer be used. Instead, we compute by brute force, enumerating all histories of prices offered and valuations realized which would lead to . Each such history implies a stacking configuration based on , from which the random price distribution of Algorithm 1 can be computed. Taking a weighted average over these histories tells us the probability with which would equal each price .

For now, we ignore computational considerations and show that the exponential-time algorithm is -competitive as an online algorithm; in Section 4.2 we show how we can sample from the conditional distribution of given , to achieve polynomial runtime while only losing in the competitiveness. The following lemma is analogous to Lemma 3.7 and proved in E-supplement 12.

Lemma 4.2

For all , such that , and ,

| (4) |

Also, for all and ,

| (5) |

Lemma 4.2 establishes that is a feasible policy, i.e. it does not try to make a sale with no inventory remaining. Having established this, it remains to prove that is optimally competitive. Theorem 4.3 is proved in E-supplement 12.

Theorem 4.3

. By Theorem 3.2, for all realizations . Therefore, is -competitive.

We should point out that although does not inherit the polynomial-time property from Algorithm 1’, it does inherit the structural property of the price at any time being stochastically-decreasing in the amount of remaining inventory. This is immediate from Theorem 3.11, which holds conditioned on any realization of .

Also, note the following. and are only guaranteed to be identically distributed when averaged over all the sample paths up to time such that the total remaining inventory is . They may not be identically distributed when conditioned on a specific purchase sequence such that , or a specific valuation sequence . Nonetheless, our method works in general. For example, if valuations were correlated, then we would condition on both and . One benefit of conditioning on only in the independent case is to limit the state space, which is necessary for our polynomial-time sampling algorithm in Section 4.2.

4.2 Emulating the Exponential-runtime Algorithm using Sampling

In this section we show how to “emulate” , using sampling, to achieve a polynomial runtime. First we provide a high-level overview of the challenges and the techniques used to overcome them.

First, suppose we are at the start of time , with inventory remaining. If we randomly sample a run of Algorithm 1 (drawing valuations randomly) such that , and copy price for time , then we would match the probabilities prescribed . This motivates the following algorithm: sample runs of Algorithm 1 to the end of until hitting one where , and then choose the price for time according to lines 1–1 of Algorithm 1. Such an algorithm is equivalent to , and thus would be -competitive.

However, on sample paths where is small, the sampling could take arbitrarily long. We limit the number of sampling tries so that the algorithm deterministically finishes in polynomial time, and show that the total measure of sample paths which fail at any point is . Unfortunately, there could be correlation between the sampling failing, and having high revenue on a sample path. Nonetheless, we can couple the sample paths of the sampling algorithm to those of the exponential-time algorithm, mark the first point of failure on each sample path, and bound the difference in revenue after that point.

The details of the sampling algorithm, which we will call , are specified in Algorithm 2. Note that in line 2 of the algorithm, is a positive integer to be chosen later. The decision of what to do when the sampling fails, i.e. defaults to line 2, is inconsequential, since in our analysis we do not expect any revenue from a sample path after the first point of failure.

To analyze the revenue of Algorithm 2, we consider a hypothetical algorithm which behaves identically to Algorithm 2, except even when it defaults to line 2, it is able to behave as if the sampling succeeded and makes the same decisions as lines 2–2. Such an algorithm is equivalent to , and hereafter we will refer to it as . The results of the sample runs do not affect the outcome of the algorithm, but help with bookkeeping.

Definition 4.4

Let be the indicator random variable for the sampling in Algorithm 2 failing at time , defined for all . Let deterministically. Analogously, let be the indicator random variable for the sampling in “failing” at time , .

For convenience, here we will use different random variables to denote the valuations in the runs of and : and , respectively. We will also use the notation from Definition 3.6.

Definition 4.5

Define the history up to time to consist of realizations up to and including the sampling at time . Formally, for all , let , where:

-

•

is a binary variable in indicating whether the sampling failed at time , for all ;

-

•

is a price in , for all ;

-

•

is a valuation in , for all .

Furthermore, define the following vectors of random variables for all :

-

•

;

-

•

.

Now, we would like to partition the sample paths by the history up to the first point of failure, and prove that the two algorithms behave identically up to this point.

Definition 4.6

Let denote the histories up to time such that the first failure in the sampling occurs at time . Formally, for all , is the set of such that and . ( and are arbitrary, and thus .)

Lemma 4.7

For a run of Algorithm 2, is a set of mutually exclusive and collectively exhaustive events. Analogously, for a run of , is a set of mutually exclusive and collectively exhaustive events.

Furthermore, , for all and .

Lemma 4.7 is straight-forward, so we defer its proof to E-supplement 12. Having proved it, we can write:

| (6) | |||||

| (7) |

Since we also know that , our goal is to compare the expected revenues of the two algorithms conditional on each history .

When , i.e. the sampling never fails, it is easy to see that the two revenues are equal. Indeed, for any :

| (8) | |||||

Lemma 4.8

Recall that is the expected value of the offline optimum with drawn independently according to . For and ,

| (9) |

Substituting (8), for , and (9), for , into (6) and (7), we conclude that

| (10) |

By Definition 4.6, the expression in parentheses is the total probability of the sampling failing at any point, before choosing the final price . We bound the term for each separately. As increases, the number of samples increases, so the probability of failure decreases:

Lemma 4.9

For all ,

It now follows easily that the sampling algorithm is within of being optimally competitive.

Theorem 4.10

5 Extensions

All proofs from this section are deferred to E-supplement 13.

5.1 A Continuum of Prices

In this section we show how to modify Algorithm 1 for the setting where valuations lie in . We let and rescale the price interval to be . The competitive ratio obtained will be , recovering the competitive ratio from Ball and Queyranne (2009).

Consider Algorithm 3. Now keeps track of the highest valuation assigned to inventory unit thus far, starting at 0. It is easy to see that the distributions specified in lines 3 and 3 are proper.

To analyze the competitiveness of Algorithm 3, we prove lemmas analogous to Lemmas 9.2–9.4. We use the same notation as in Definition 9.1, except instead of and , we use to denote the value of at the end of time , taking a value in .

Lemma 5.1

At the end of each time step , the probability that any inventory unit has been sold is 0 if , and if . Formally, for all ,

| (11) |

Lemma 5.2

Suppose in a time step . Then the expected revenue earned by the algorithm during time step is .

5.2 No Information on Valuations

In this section we discuss whether it is possible for an online algorithm to be -competitive without any information (before or after, deterministic or distributional) on the valuations.

First we show that this is impossible for any online algorithm which price-skims independently, i.e. realizes its random price at each time step using an independent source of random bits.

Proposition 5.3

Suppose that either: (i) and valuations can be 0 (as usual); or (ii) and valuations cannot be 0. (Recall that is the number of prices.) Then for any online algorithm where each chosen independently based on the sales history , there exists a sequence such that

However, we show that it is possible to be -competitive if the online algorithm can price-skim in a “coordinated” fashion, with the same probabilities as in Eren and Maglaras (2010).

Proposition 5.4

Consider the following random-fixed-price policy:

-

1.

Initially, choose a random price which is equal to each with probability ;

-

2.

Offer price as long as there is remaining inventory.

This policy is -competitive.

It is known that correlated randomness is very powerful in the design of online algorithms (see, e.g., Karp et al. (1990), who derive an extremely elegant solution to the online matching problem using correlated randomness). Indeed, we can use our policy from Proposition 5.4 under our previous models with more information on the valuations and still have a -competitive algorithm. However, this is impractical for several reasons. First, the fact that a single random price is fixed makes the algorithm have large variance in its performance. Second, the random-fixed-price policy does not show how the price should evolve as inventory is depleted; namely, it does not satisfy the intuitive structural property in dynamic pricing that the price is greater if the remaining inventory is less as we showed in Section 3.5. In Section 6, we will test the performance of the random-fixed-price policy, and see that in fact it performs worse than booking limits (which does not have a theoretical guarantee).

5.3 Personalized Revenue Management Model

In this section we consider the personalized online revenue management setup introduced by Golrezaei et al. (2014), where:

-

•

the stochastic decision of each customer can be modeled accurately upon her arrival to the e-commerce platform (by using her characteristics);

-

•

however, the overall intensity and characteristics of customers to arrive over time is difficult to model (and treated as unknown/arbitrary).

This corresponds to the stochastic-valuation model in Section 4, with the change that during each time step , the distribution of each is first given, and then the algorithm can offer a personalized price. The public pricing algorithms from Section 4 can still be applied, and will be -competitive. Furthermore, it is not possible to be better than -competitive even with this personalized information, as discussed in Section 1.1.

Nonetheless, in this section we specify how our online algorithms can exploit personalized information to strictly improve their decisions, while remaining -competitive. Take any -competitive algorithm for the stochastic-valuation model (e.g. the algorithm from Section 4.1). For each time step and inventory level such that , consider the distribution for the price chosen by algorithm conditioned on (this depends on the previously-observed valuation distributions ). Since now we also know the distribution of valuation , we can compute the probability of algorithm making a sale during time ,

| (12) |

as well as its expected revenue,

| (13) |

We can interpret (13) as the reward given to the algorithm during time in exchange for the probability (12) of consuming inventory. The price distribution used by the algorithm to obtain such an exchange was chosen without knowing the distribution of . However, since now we do know the distribution of , we can potentially make a decision which achieves more expected reward under the same consumption probability. Specifically, we solve the following LP:

| (14) | |||||

| (15) | |||||

| (16) | |||||

| (17) | |||||

represents the probability that we should offer price at time , conditioned on the remaining inventory being . We know that setting each is a feasible solution, and hence the optimal objective value of the optimization problem is at least (13). Let denote an optimal solution to the optimization problem, for all and .

Proposition 5.5

Consider the online algorithm which, at each time step , sets the price randomly according to probabilities , where is the remaining inventory at the start of time . Then for any sequence of valuation distributions , the total expected revenue of this algorithm is at least .

Proposition 5.5 is established in the same way as Theorems 3.8 and 4.3—for , we can inductively ensure from constraint (15) that the distribution for the inventory level time is identical for both algorithms. Since the modified algorithm has the same distribution for inventory state at each time and earns at least as much revenue as in expectation on every possible state, its total revenue can only be greater. In fact, as we will see in Section 6, the modification with personalization often earns much greater revenue, since through solving the LP formed by (14)–(17), it often finds a higher-revenue way to maintain the same inventory consumption probability.

Finally, we remark that if is a continuum (following the extension from Section 5.1), then the LP (14)–(17) would have infinitely many variables, but because it has only two constraints, an optimal solution would need support size at most two. In fact, most parametric forms commonly used to describe a demand function over , including linear, log-linear, and logit, are regular, in which case an optimal solution has support of size one and the LP can be tractably solved (cf. Talluri and Van Ryzin 2006, Sec. 7.3).

6 Computational Experiments

In this section we test the performance of our algorithm in simulations, following the personalized online revenue management setup (with stochastic valuations) discussed in Section 5.3.

6.1 Experimental Setup and Algorithms Compared

The only information given initially is the starting inventory and the price set , where we let . Based on and , we generate different arrival sequences of varying lengths . The valuation distribution for any particular customer is log-linear (exponential). That is, there is a price sensitivity parameter such that the probability of her valuation exceeding any price satisfies

| (18) |

This then induces a discrete distribution over the maximum-willingness-to-pay values of by setting for all ; note that these probabilities indeed sum to 1, by equation (18).

We choose this family of distributions due to the convenience of equation (18) and the property that the immediate revenue is decreasing in whenever (cf. Talluri and Van Ryzin 2006, Sec. 7.3). This property is important for creating a non-trivial tradeoff between offering lower prices which maximize immediate revenue, vs. offering higher prices which maximize revenue per inventory. We do not believe our results to be sensitive to the exact family of demand used as long as this property is satisfied.

For each arrival sequence we generate, we draw the parameters independently from the same distribution, i.e. fluctuations in price sensitivity are stationary over time. Therefore, arrival sequences are mainly distinguished by their total number of customers , where under small it is optimal to offer lower prices, while under large it is optimal to offer higher prices. Of course, is initially unknown, and online algorithms must immediately decide a personalized price for each customer upon seeing her valuation distribution (equivalently, price sensitivity ).

We now describe the algorithms and benchmarks we test. First we describe algorithms which are oblivious to both valuation distributions and remaining inventory.

- •

-

•

IPS (Independent Price-Skimming): same as PS, but independently reset the random price for each customer. This policy is described in Section 3.1 (see “Attempt 2”).

-

•

Conservative: always charge the maximum price of .

Now we describe algorithms which are valuation-oblivious but react to remaining inventory.

- •

-

•

BL-PS (Booking Limits with Price-Skimming): same as BL, but instead of deterministically charging the base price, use PS to randomly choose a price above the base price. This policy is described in Section 3.1 (see “Attempt 3”).

Now we modify the previous algorithms to offer personalized prices based on knowledge of valuation distributions. Whenever the previous algorithm would have offered a base price, the modified algorithm looks for an opportunity to offer a higher price which also has a higher immediate revenue, for each customer (as discussed earlier, this could only be possible if the base price satisfies ). In this way, we get the personalized modifications PS-P, IPS-P, BL-P of the earlier price-skimming, independent price-skimming, and booking limits methods for setting base prices, respectively. BL-P reacts to remaining inventory but PS-P and IPS-P are inventory-oblivious. Another similar inventory-oblivious algorithm we will test is the Myopic algorithm, which greedily offers to each customer the price among all prices which maximizes immediate revenue , essentially doing personalization with a fixed base price of 1.

Finally, we test our Valuation Tracking procedure with stochastic valuations and personalization, as described in Section 5.3. To be precise, we consider our public pricing algorithm for stochastic valuations, sample 1000 times (see Section 4.2) to estimate the price it would offer (replacing -prices with as in Section 3.5), and then look for an opportunity to offer a personalized price, repeating this process at each time step. Our algorithm is similar to BL-P in that it is both valuation-aware and inventory-aware, but reacts to inventory in a different way.

For reference, we will also compare with the optimal DP (dynamic programming) benchmark which knows the entire arrival sequence in advance (but still does not know the realizations of the valuations like does), for a total of 11 algorithms tested.

6.2 Parameter Values and Results

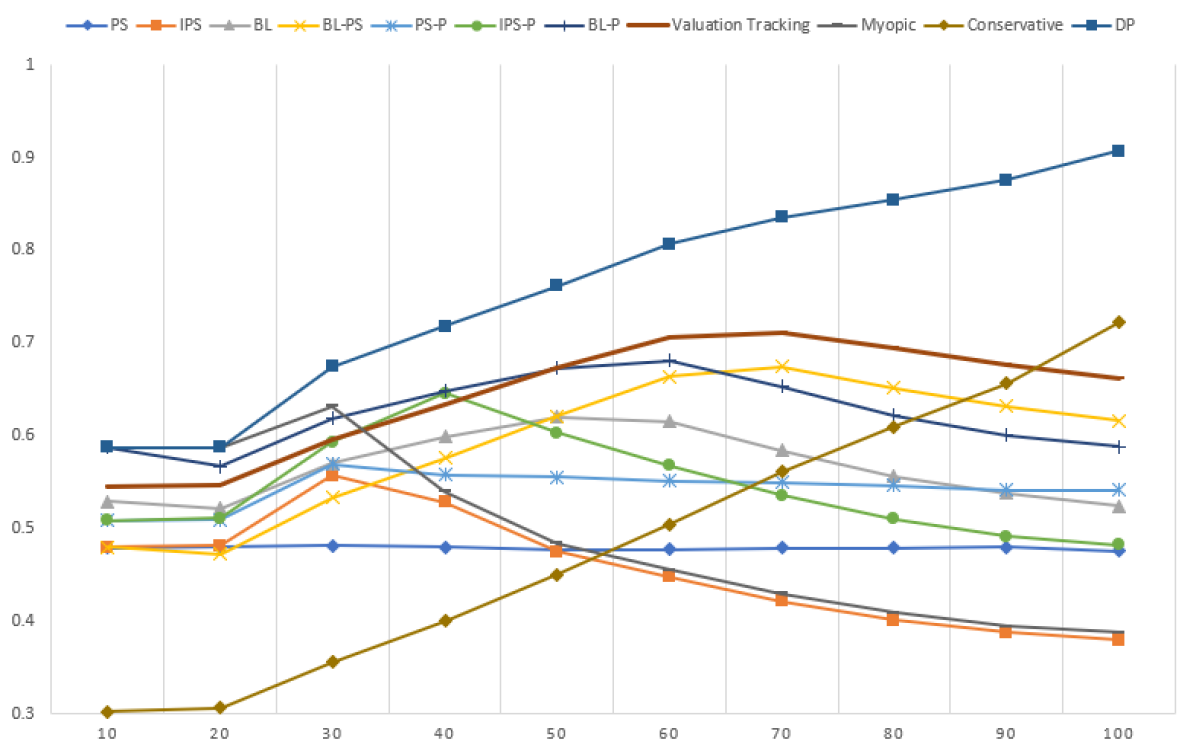

We fix the price set to be for now, and vary its granularity and range later in Section 6.3. We consider two scenarios for starting inventory: small () and large (). Under both values of , we generate arrival sequences for 10 different lengths: . We independently generate 1000 sequences for each value of , resulting in a total of 10000 arrival sequence instances for each inventory scenario.

Recall from Section 6.1 that valuation distributions are log-linear. We independently draw the price sensitivity parameter of each customer uniformly from the range [1/3,4/3], which ensures that even under the smallest value of , the maximum price of 4 does not also maximize the immediate revenue function (since the immediate revenue decreases over prices ). Meanwhile, the upper bound of was calibrated so that at the maximum length of , the Conservative algorithm can expect to sell most of the units of inventory at the maximum price (and hence is best-performing at the largest values of , as will be evidenced).

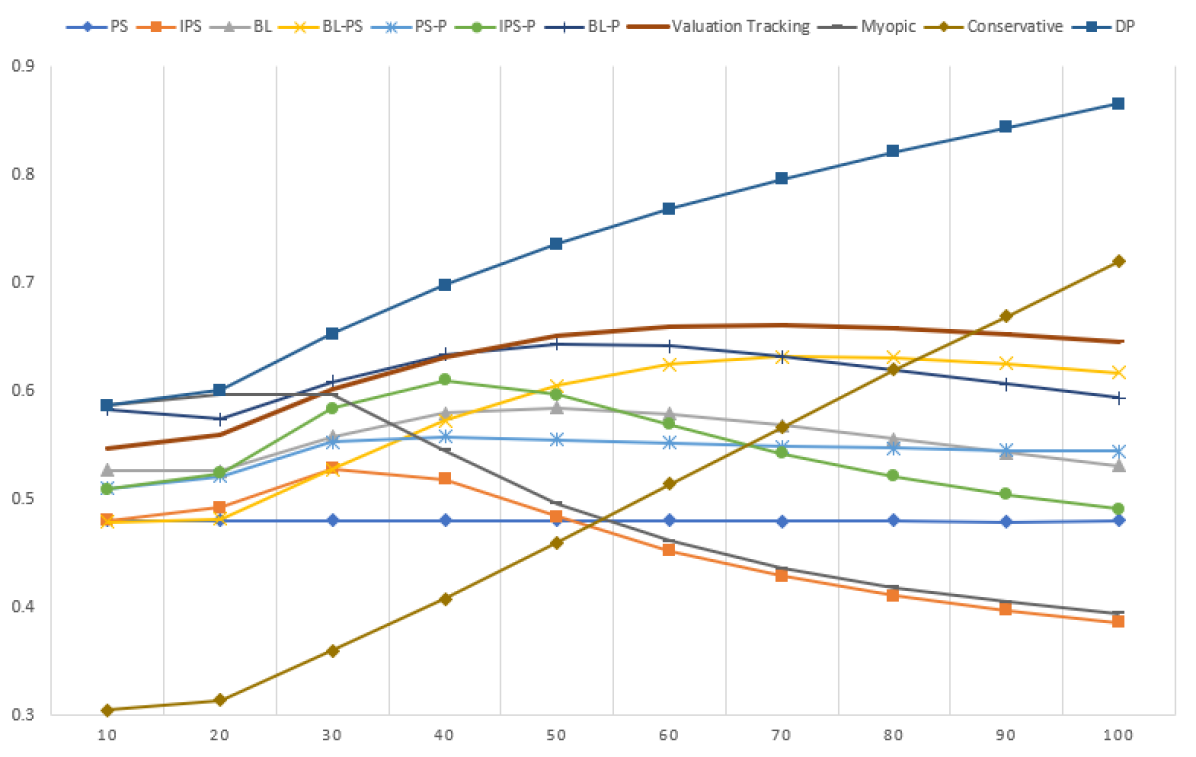

For each instance, and each of the 11 algorithms from Section 6.1 as well as , we run 1000 simulations to empirically estimate the revenue earned (with the exception of DP, for which we can exactly calculate the expected revenue). We divide the revenue earned by , to get a performance ratio for each algorithm on each instance. We display the average performance of each algorithm over the 10000 instances, for both inventory scenarios and , in Table 6.2.

Average performance of each algorithm and benchmark over the instances, under both scenarios of starting inventory . The algorithms are sorted by whether they are valuation-aware and/or inventory-aware. The performance of our algorithm is bolded. \updown Valuation-oblivious Valuation-aware Benchmarks \updown Inventory-obl. Inventory-aware Inventory-obl. Inventory-aware \updown PS IPS BL BL-PS PS-P IPS-P BL-P Val. Tracking Myopic Conservative DP \up 48.0% 45.8% 55.5% 57.9% 54.3% 54.5% 61.3% 62.6% 49.3% 49.3% 73.7% \down 47.9% 45.6% 56.6% 59.2% 54.3% 54.5% 62.4% 64.5% 49.1% 48.7% 76.1%

We observe that there is noticeable separation in performance between the four categories of algorithms (valuation-oblivious vs. -aware, inventory-oblivious vs. -aware). Among the algorithms aware of neither valuations nor inventory, PS attains exactly the theoretically guarantee of , while IPS performs worse. Among the algorithms aware of both, Valuation Tracking outperforms BL-P. All in all, awareness of inventory appears to be more important than awareness of valuations, especially at the larger starting inventory of , and the three best algorithms—Valuation Tracking, BL-P, and BL-PS (which performs well relative to its category)—all raise their prices as the remaining inventory dwindles. The intuition for why this yields good average-case performance over all the instances is that:

-

•

When turns out to be small, the algorithms would have set low prices and maximized sales;

-

•

When turns out to be large, the algorithms would have raised their prices to get more out of their inventories.

We now delve into why Valuation Tracking is better for reacting to inventory than booking limits. We dis-aggregate the results from Table 6.2 and plot the performances of each algorithm as a function of , averaging over the 1000 instances with that length. We plot the results in Figures 2–3.

We observe the following trends in both Figure 2 (for ) and Figure 3 (for ).

-

•

At the smallest and largest values of , the Myopic and Conservative algorithms, which maximize revenue-per-customer and revenue-per-inventory respectively, are best-performing (aside from the future-knowing DP algorithm). This further corroborates the legitimacy of our range of tested—not only are the aggregate performances of the Myopic and Conservative benchmarks comparable in Table 6.2, we have covered the full spectrum of lengths from Myopic being best to Conservative being best.

-

•

The improvement of Valuation Tracking over BL-P can be attributed to noticeably better performance at large , at the expense of slightly worse performance at small .

The second bullet suggests that our algorithm is more conservative with inventory than booking limits. To understand why, we have to look at the definitions of the algorithms. Both algorithms essentially set aside the same fractions of inventory, given by from Definition 3.1, “to be sold at each price”. However, booking limits are based on sales, and offers low prices (assuming low prices maximize revenue-per-customer) at the start until a fixed amount (specifically, units) of inventory is sold. By contrast, our algorithm is based on the possible realizations of the valuation, and starts considering higher prices from the start based on the exact valuation distribution.

We also emphasize that Valuation Tracking cannot be matched by simply taking BL-P and making it more inventory-conservative by combining it with a more conservative algorithm. Indeed, as evidenced in Figures 2–3, the performance curve of Valuation Tracking lies well above any convex combination formed by the other curves. We believe that Valuation Tracking is fundamentally the more precise way to react to inventory under the stochastic nature of our pricing problem, while booking limits were invented for the revenue management problem where the decision is to deterministically accept/reject.

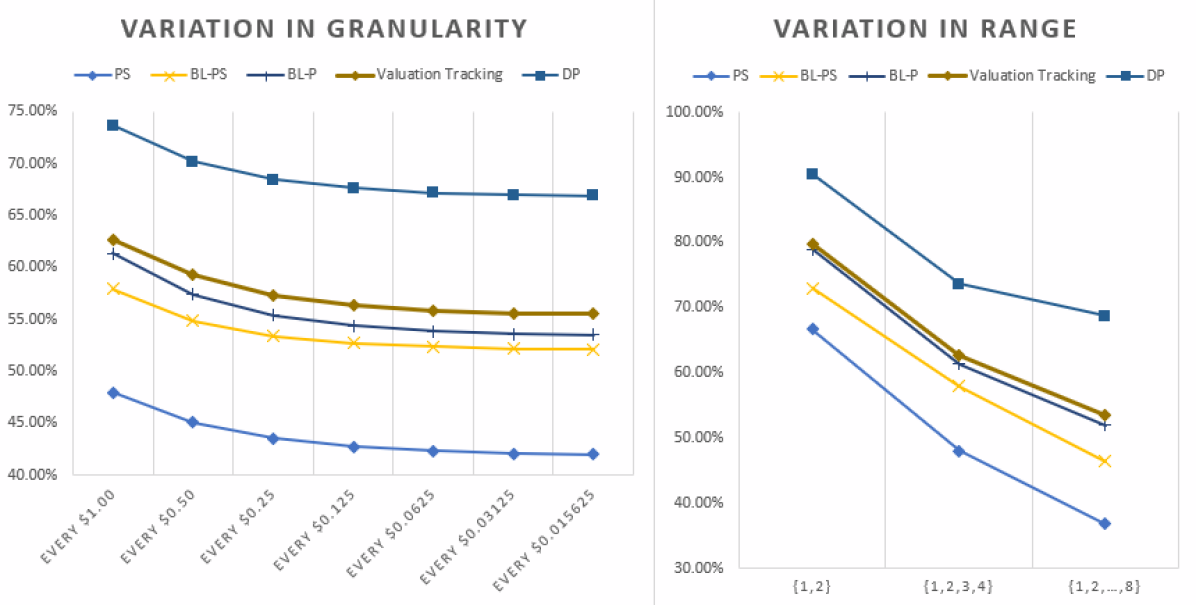

6.3 Varying the Price Set

We verify the robustness of our results from Section 6.2 by varying the price set to be different from . We consider two ways to vary :

-

•

Increase the granularity of by allowing feasible prices to come in increments of 0.5 (i.e. ), 0.25, 0.125, etc., all the way down to increments of 0.015625.

-

•

Consider a maximum price of 2 or 8 instead, while maintaining granularity at the integer level (i.e. or ).

We repeat the experiments from Section 6.2 for the small-inventory scenario of , and plot the average performances of the algorithms over the instances in Figure 4. For brevity, we only display the performances of PS (which always equals the competitive ratio guarantee of ), the three best algorithms from Section 6.2 (BL-PS, BL-P, and Valuation Tracking), and DP.

The relative performances of the algorithms in Figure 4 does not differ from those originally observed in Table 6.2. In fact, a higher granularity of prices increases the advantage of our Valuation Tracking algorithm over BL-P, since with more possible pricing decisions there is more room for improvement. Similarly, a larger range of prices makes valuation-awareness more important, and hence we see the drop in the performance of BL-PS when .

7 Conclusion

In this paper we have studied the fundamental single-item dynamic pricing problem with no knowledge of future valuations, and derived the best-possible competitive ratio. Our policies unify the inventory-dependent booking policies in Ball and Queyranne (2009) with the random price-skimming policies in Eren and Maglaras (2010). An important feature of our policies is that they show at each time step how the price distribution should depend on inventory when the future is unknown, complementing classical results which show how the optimal price should depend on inventory when the future is known. Our policies were derived using a new “valuation tracking” technique, which geometrically tracks the optimum and hedges against the arrival sequence immediately ending in the most inventory-conservative fashion.

Finally, we explain why our analysis of single-leg revenue management for dynamic pricing, where each customer has a valuation and chooses the lowest fare not exceeding it, captures substitution under any form of random-utility choice model. Suppose instead that the firm could offer an assortment of fare classes, and that each customer has a ranked list (in order of decreasing utility) of fare classes she is willing to purchase, and chooses the highest-ranked fare class that is offered to her. We can define to be the maximum fare in the list that customer is willing to purchase, and then the offline optimum would still be the sum of the largest values from . Meanwhile, we can modify the online algorithm so that whenever it would have offered price , it now shows all fares greater than or equal to . This algorithm would still make a sale whenever , except now it has the opportunity to earn revenue greater than , if customer does not choose the lowest offered fare. As a result, our -competitive algorithms under the pricing model imply corresponding -competitive algorithms under the assortment model.

Nevertheless, we would like to end on two open questions related to the assortment generalization. First, our argument above assumes random-utility choice models; however in practice certain fare classes could be designed as “decoys” for other fare classes. It is not known whether this effect can be accommodated by our dynamic pricing algorithm. Second, our algorithms imply an “assortment-skimming” distribution over revenue-ordered assortments, but this assumes there is no limit on the number of fare classes offered. We believe that assortment skimming under cardinality constraints is an interesting problem.

Acknowledgments

The authors would like to thank He Wang for insightful discussions.

References

- Araman and Caldentey (2009) Araman VF, Caldentey R (2009) Dynamic pricing for nonperishable products with demand learning. Operations research 57(5):1169–1188.

- Araman and Caldentey (2011) Araman VF, Caldentey R (2011) Revenue management with incomplete demand information. Wiley Encyclopedia of Operations Research and Management Science .

- Azar et al. (2014) Azar PD, Kleinberg R, Weinberg SM (2014) Prophet inequalities with limited information. Proceedings of the twenty-fifth annual ACM-SIAM symposium on Discrete algorithms, 1358–1377 (Society for Industrial and Applied Mathematics).

- Babaioff et al. (2011) Babaioff M, Blumrosen L, Dughmi S, Singer Y (2011) Posting prices with unknown distributions. In ICS (Citeseer).

- Babaioff et al. (2015) Babaioff M, Dughmi S, Kleinberg R, Slivkins A (2015) Dynamic pricing with limited supply. ACM Transactions on Economics and Computation (TEAC) 3(1):4.

- Badanidiyuru et al. (2012) Badanidiyuru A, Kleinberg R, Singer Y (2012) Learning on a budget: posted price mechanisms for online procurement. Proceedings of the 13th ACM Conference on Electronic Commerce, 128–145 (ACM).

- Badanidiyuru et al. (2013) Badanidiyuru A, Kleinberg R, Slivkins A (2013) Bandits with knapsacks. 2013 IEEE 54th Annual Symposium on Foundations of Computer Science, 207–216 (IEEE).

- Ball and Queyranne (2009) Ball MO, Queyranne M (2009) Toward robust revenue management: Competitive analysis of online booking. Operations Research 57(4):950–963.

- Bergemann and Schlag (2008) Bergemann D, Schlag KH (2008) Pricing without priors. Journal of the European Economic Association 6(2-3):560–569.

- Besbes and Zeevi (2009) Besbes O, Zeevi A (2009) Dynamic pricing without knowing the demand function: Risk bounds and near-optimal algorithms. Operations Research 57(6):1407–1420.

- Borodin and El-Yaniv (2005) Borodin A, El-Yaniv R (2005) Online computation and competitive analysis (cambridge university press).

- Chen and Wu (2016) Chen L, Wu C (2016) Bayesian dynamic pricing with unknown customer willingness-to-pay and limited inventory. Working Paper .

- Chen et al. (2016) Chen X, Ma W, Simchi-Levi D, Xin L (2016) Dynamic recommendation at checkout under inventory constraint. manuscript on SSRN .

- Cheung et al. (2018) Cheung WC, Ma W, Simchi-Levi D, Wang X (2018) Inventory balancing with online learning. arXiv preprint arXiv:1810.05640 .

- Correa et al. (2017) Correa J, Foncea P, Hoeksma R, Oosterwijk T, Vredeveld T (2017) Posted price mechanisms for a random stream of customers. Proceedings of the 2017 ACM Conference on Economics and Computation, 169–186 (ACM).

- Correa et al. (2018) Correa J, Foncea P, Pizarro D, Verdugo V (2018) From pricing to prophets, and back! Operations Research Letters .

- den Boer (2015) den Boer AV (2015) Dynamic pricing and learning: historical origins, current research, and new directions. Surveys in operations research and management science 20(1):1–18.

- den Boer and Zwart (2015) den Boer AV, Zwart B (2015) Dynamic pricing and learning with finite inventories. Operations research 63(4):965–978.

- Devanur et al. (2013) Devanur NR, Jain K, Kleinberg RD (2013) Randomized primal-dual analysis of ranking for online bipartite matching. Proceedings of the Twenty-Fourth Annual ACM-SIAM Symposium on Discrete Algorithms, 101–107 (SIAM).

- Dütting et al. (2017) Dütting P, Feldman M, Kesselheim T, Lucier B (2017) Prophet inequalities made easy: Stochastic optimization by pricing non-stochastic inputs. 2017 IEEE 58th Annual Symposium on Foundations of Computer Science (FOCS), 540–551 (IEEE).

- Dütting et al. (2016) Dütting P, Fischer FA, Klimm M (2016) Revenue gaps for discriminatory and anonymous sequential posted pricing. CoRR, abs/1607.07105 .

- Eren and Maglaras (2010) Eren SS, Maglaras C (2010) Monopoly pricing with limited demand information. Journal of revenue and pricing management 9(1-2):23–48.

- Fiig et al. (2012) Fiig T, Isler K, Hopperstad C, Olsen SS (2012) Forecasting and optimization of fare families. Journal of Revenue and Pricing Management 11(3):322–342.

- Gallego and Van Ryzin (1994) Gallego G, Van Ryzin G (1994) Optimal dynamic pricing of inventories with stochastic demand over finite horizons. Management science 40(8):999–1020.

- Golrezaei et al. (2014) Golrezaei N, Nazerzadeh H, Rusmevichientong P (2014) Real-time optimization of personalized assortments. Management Science 60(6):1532–1551.

- Kalyanasundaram and Pruhs (2000) Kalyanasundaram B, Pruhs KR (2000) An optimal deterministic algorithm for online b-matching. Theoretical Computer Science 233(1):319–325.

- Karp et al. (1990) Karp RM, Vazirani UV, Vazirani VV (1990) An optimal algorithm for on-line bipartite matching. Proceedings of the twenty-second annual ACM symposium on Theory of computing, 352–358 (ACM).

- Kleinberg and Weinberg (2012) Kleinberg R, Weinberg SM (2012) Matroid prophet inequalities. Proceedings of the forty-fourth annual ACM symposium on Theory of computing, 123–136 (ACM).

- Krengel and Sucheston (1977) Krengel U, Sucheston L (1977) Semiamarts and finite values. Bulletin of the American Mathematical Society 83(4):745–747.

- Lan et al. (2008) Lan Y, Gao H, Ball MO, Karaesmen I (2008) Revenue management with limited demand information. Management Science 54(9):1594–1609.

- Lim and Shanthikumar (2007) Lim AE, Shanthikumar JG (2007) Relative entropy, exponential utility, and robust dynamic pricing. Operations Research 55(2):198–214.

- Ma and Simchi-Levi (2017) Ma W, Simchi-Levi D (2017) Online resource allocation under arbitrary arrivals: Optimal algorithms and tight competitive ratios. manuscript on SSRN .

- Maglaras and Meissner (2006) Maglaras C, Meissner J (2006) Dynamic pricing strategies for multiproduct revenue management problems. Manufacturing & Service Operations Management 8(2):136–148.

- Mehta et al. (2007) Mehta A, Saberi A, Vazirani U, Vazirani V (2007) Adwords and generalized online matching. Journal of the ACM (JACM) 54(5):22.

- Montgomery et al. (2004) Montgomery AL, Li S, Srinivasan K, Liechty JC (2004) Modeling online browsing and path analysis using clickstream data. Marketing science 23(4):579–595.

- Talluri and Van Ryzin (2006) Talluri KT, Van Ryzin GJ (2006) The theory and practice of revenue management, volume 68 (Springer Science & Business Media).

- Thekumparampil et al. (2014) Thekumparampil KK, Thangaraj A, Vaze R (2014) Sub-modularity of waterfilling with applications to online basestation allocation. arXiv preprint arXiv:1402.4892 .

- Yao (1977) Yao ACC (1977) Probabilistic computations: Toward a unified measure of complexity. Foundations of Computer Science, 1977., 18th Annual Symposium on, 222–227 (IEEE).

- Zhang et al. (2016) Zhang H, Shi C, Qin C, Hua C (2016) Stochastic regret minimization for revenue management problems with nonstationary demands. Naval Research Logistics (NRL) 63(6):433–448.

- Zhao and Zheng (2000) Zhao W, Zheng YS (2000) Optimal dynamic pricing for perishable assets with nonhomogeneous demand. Management science 46(3):375–388.

E-Companion

8 Why Attempts using Existing Techniques Fail even with Personalization