How Not To Do Mean-Variance Analysis

Abstract

We use the 2014 market history of two high-returning biotechnology exchange-traded funds to illustrate how ex post mean-variance analysis should not be done. Unfortunately, the way it should not be done is the way it generally is done—to our knowledge.

![[Uncaptioned image]](/html/1810.10726/assets/Plato.jpg)

ἀγεωμὲτρητος

μηδεὶς

εἰςίτω

Let no one ignorant of geometry enter here

1 Preface

Ex post mean-variance analysis is a financial application of descriptive statistics. But descriptive statistics, where the sum of square deviations from the mean plays a fundamental role, has a strong geometric flavor. In this paper we emphasize the geometry of mean-variance analysis.

Geometry starts with points.

The primary points in our geometric exposition are two biotechnology

exchange-traded funds,

FBT – First Trust NYSE Arca Biotechnology Indx Fund

and

XBI – SPDR S&P Biotech ETF.

The graphs of the 2013-12-31-normalized adjusted closing prices,

and ,

of the two funds are shown in Figure 2.1, as well as the

graph of an unattended long portfolio, UIP, in the two funds.

UIP’s normalized adjusted closing price vector,

| (1.1) |

is necessarily a convex combination of and .

Normalized adjusted closing prices are the horses that drive our mean-variance cart. When the adjusted closing price vectors , and are replaced by their daily return vectors , and , you move into a higher dimensional space with all geometry left behind.

The pictures that follow tell the whole story. Thanks to the TikZ vector-graphics language these pictures are precise, numerical images—not just schematic drawings.

2 Normalized adjusted closing prices – a geometric example

Figure 2.1 shows the 2014 history of an unattended

investment portfolio, UIP, in two high-returning exchange

traded funds, FBT and XBI. The 2013-12-31

closing composition

of UIP was

| (2.1) |

but these closing proportions never reoccured in 2014. Indeed UIP closed with more than 25% in XBI (green higher than blue) for most of the first quarter, whereas XBI was less than 25% of UIP (blue higher than green) for much of the remaining three quarters. However Figure 2.1 does shows the geometry of the 3:1 proportions. On every vertical line, the brown UIP point is exactly 3/4 of the way from the green XBI point to the blue FBT point.

There were exactly 253 market days from 2013-12-31 to 2014-12-31 inclusive. Each of the four adjusted closing price graphs in Figure 2.1 represents the changing value of $100 invested at 2013-12-31 closing prices in the corresponding fund or portfolio over the next 252 market days. Each graph corresponds to a point , and the three points, of (2.1), are on the line segment

| (2.2) |

in —with corresponding to . (Appendix A describes how normalized adjusted closing prices can be computed.)

Portfolio UIP represents a completely passive, unattended investment. Think of an investor as having money in FBT and XBI at the close of 2013. Suppose that FBT represents exactly 75% of his total investment at that time and XBI 25%. UIP then simply tracks each $100 of his investment through 2014. The investor does absolutely nothing, and all dividends from the two funds are automatically reinvested.

However the continually reallocated portfolio CRP, mostly

hidden by UIP, is an entirely different matter. Here the

investor decides, a priori, that 75% FBT and 25% XBI are the right

proportions for his investment. Accordingly, before each market day of

2014, he reinvests his money so as to start the day with exactly these

proportions in the two funds.

Algorithm 2.1 computes the growth of $100 under this scenario.

Note.

The % signs above begin a comment.

It is difficult to make out the red CRP graph from the brown UIP graph in Figure 2.1. These graphs are very close, and the UIP graph is drawn over the CRP graph, hiding it from view for the most part. It is only toward the end of 2014 that one can really make out the differences.

Figure 2.2 is a blow-up of December 2014. The differences in the graphs are now quite visible. Here we see that the red CRP graph is slightly higher than the brown UIP graph throughout December—and clearly higher on December 31. It follows that CRP returned more than UIP over 2014.

Note that the 2014-12-31 value of must be

by (1.1) and the terminal values of FBT and XBI shown on Figure 2.2. It follows that UIP had a total return of 46.90% over 2014. In fact CRP returned 47.32% over 2014, more than UIP and just slightly less than FBT.

Here are the adjusted closing prices of the four funds over the month of December 2014.

| date | FBT | XBI | UIP | CRP |

|---|---|---|---|---|

| 2014-12-01 | 145.736 | 135.477 | 143.171 | 143.490 |

| 2014-12-02 | 147.918 | 139.052 | 145.702 | 146.048 |

| 2014-12-03 | 148.034 | 139.184 | 145.821 | 146.169 |

| 2014-12-04 | 147.123 | 138.121 | 144.873 | 145.215 |

| 2014-12-05 | 148.150 | 140.580 | 146.258 | 146.622 |

| 2014-12-08 | 151.214 | 141.417 | 148.765 | 149.114 |

| 2014-12-09 | 151.807 | 145.504 | 150.231 | 150.630 |

| 2014-12-10 | 148.699 | 142.379 | 147.119 | 147.508 |

| 2014-12-11 | 148.786 | 142.720 | 147.269 | 147.661 |

| 2014-12-12 | 146.878 | 142.480 | 145.778 | 146.179 |

| 2014-12-15 | 142.657 | 136.400 | 141.093 | 141.469 |

| 2014-12-16 | 140.807 | 135.609 | 139.507 | 139.888 |

| 2014-12-17 | 145.851 | 142.076 | 144.907 | 145.314 |

| 2014-12-18 | 150.737 | 146.628 | 149.710 | 150.129 |

| 2014-12-19 | 152.212 | 147.990 | 151.156 | 151.579 |

| 2014-12-22 | 150.463 | 146.886 | 149.569 | 149.990 |

| 2014-12-23 | 143.842 | 139.313 | 142.710 | 143.107 |

| 2014-12-24 | 145.968 | 141.988 | 144.973 | 145.380 |

| 2014-12-26 | 149.554 | 145.261 | 148.481 | 148.897 |

| 2014-12-29 | 150.017 | 145.790 | 148.960 | 149.378 |

| 2014-12-30 | 148.151 | 144.258 | 147.178 | 147.592 |

| 2014-12-31 | 147.544 | 144.973 | 146.901 | 147.321 |

The geometric equation (2.1) holds on every line of

Table 2.1, but the proportions of FBT and

XBI in UIP,

| (2.3) |

are different on every line. The 2013-12-31, 3:1 proportions come closest to being realized on the 2014-12-31 line of Table 2.1, where UIP closes at 75.33% FBT : 24.67% XBI.

As for daily returns,

| (2.4) |

the 2014 return vector equation,

| (2.5) |

is valid in due to continual reallocation. This

insures that the corresponding mean returns satisfy

| (2.6) |

as required by “The Standard Mean-Variance Portfolio Selection Model” of [2, pp. 3-4].

The ancillary folder that accompanies this article includes three

files, FXUZ7.csv,

matlab/FXUC2014.mat, and

matlab/FXZC2014.mat, that contain the normalized adjusted closing

prices used for this article.

3 How not to do mean-variance analysis

The Financial Toolbox

with the MATLAB programming language is perhaps the most popular

resource for doing mean-variance analysis. We have computed our

mean-variance tables using MATLAB scripts

in the matlab subdirectory of the ancillary

folder that accompanies this article.

Our MATLAB script hn2mv1a.m illustrates the problem with

mean-variance analysis as it is usually practiced. The script

begins with the line

load FXUC2014.mat; % A dates fundsA legendA

which loads the matrix of adjusted closing prices,

displayed in Figure 2.1. This matrix has rank 3 rather than

4, since is a linear combination of

and

(1.1).

Next we remove from and append the

columns

so that

becomes a matrix of rank 2. Geometrically, describes 5

points on a line in , and since the

line does not pass through the origin.

The hn2mv1a.m script continues with the lines

⬇

%% get asset moments from adjusted closing prices

ptf = Portfolio;

ptf = estimateAssetMoments(ptf, A, ’dataformat’, ’prices’);

[mn, cv] = getAssetMoments(ptf);

Here mn and cv are the and

mean daily return and covariance of

daily return matrices corresponding to the daily return

matrix

derived from via (2.4). The annualized results are

shown in Table 3.1.

| FBT | XBI | UIP | UIP2 | UIP3 | |

| 0.4245 | 0.4324 | 0.4235 | 0.4244 | 0.4274 | |

| 0.2656 | 0.3491 | 0.2777 | 0.2963 | 0.3203 | |

| covariance | |||||

| FBT | 0.0705 | 0.0804 | 0.0729 | 0.0753 | 0.0778 |

| XBI | 0.0804 | 0.1219 | 0.0905 | 0.1008 | 0.1112 |

| UIP | 0.0729 | 0.0905 | 0.0771 | 0.0815 | 0.0859 |

| UIP2 | 0.0753 | 0.1008 | 0.0815 | 0.0878 | 0.0942 |

| UIP3 | 0.0778 | 0.1112 | 0.0859 | 0.0942 | 0.1026 |

One problem with Table 3.1 is immediately obvious. How can the mean returns of the long portfolios UIP and UIP2 be less than the mean return of either component fund? A dimensional problem is less obvious but just as troubling. We start with an adjusted closing price history, , which corresponds to five points on a line segment (a one simplex) in ; but, to do mean-variance analysis on , we must jump to the four simplex in generated by the five linearly independent columns of the daily return matrix (). It simply doesn’t make sense to us!

This is the -picture of what is happening. The pink region is the image of the 4-simplex in generated by the five columns of . (The coordinates in the picture are percentages.)

Figure 3.1 is a graphic representation of Table 3.1. The red, continually reallocated region represents all obtainable :

all such that

| (3.1) | |||

| with the and from Table 3.1, and | |||

| (3.2) | |||

The following five portfolios are equally -spaced on the efficient frontier. They were computed with the line

P = estimateFrontier(ptf, 5);

in the MATLAB script hn2mv1a.m.

Every portfolio in the continually reallocated region, other than the generating funds FBT, XBI, UIP, UIP2, and UIP3, must be reallocated at the close each market day of 2014 in order to retain its original 2013-12-31 closing proportions.

On the other hand, the unattended path in Figure 3.1

shows the actual mean returns and standard deviations of return of

all unattended portfolios in FBT and XBI as computed

directly from their adjusted closing price vectors (2.2)

via MATLAB Example 1 (script hn2mv2.m) below.

We should note that the MATLAB lines

of hn2mv1a.m,

eCRP = 252 * mean(rCRP); % eCRP = 0.4265

sigCRP = sqrt(252) * std(rCRP, 1); % sigCRP = 0.2783

produced the coordinates for the two CRP points of Figure

3.1. The rCRP in this code

corresponds to the vector of

(2.5) or the from

via (2.4). They are the same.

4 The mean periodic return problem

Figure 4.1 on the next page and the

hn2domv3.m script below it illustrate a serious problem with

mean periodic returns. This is a simple, artifical example, where a fund

gains 50% in the first quarter of the year, loses 67% in the second

quarter, gains 200% in the third quarter, and loses 17% in the forth

quarter.

An investor in the fund realizes that his fund has returned 25% over the year, but the trip has been terribly rocky; he decides to bail out.

Not so fast, his investment adviser tells him. Just add up the quarterly

returns:

You have avergaed averaged over 40% per quarter. The fund may seem a

bit risky, but, in view of its history, you should expect to

average 40% per quarter next year as well. It’s clear from the numbers.

Figure 4.1 tells the whole story. Mean periodic returns tend to accentuate the positive. Mean periodic discounts do just do just the opposite.

Definition 1 (Effective return and discount).

Let and be the the adjusted closing prices of a security

on two different market days with occuring before . Then

the effective return of the security over that period of time

is defined as

and the effective discount as

The equation

always holds, and and always

have the same sign, positive, negative, or zero.

The means of periodic changes in year-to-date return and periodic

changes in date-to-end-of-year discount are the appropriate measures of

effective performance of a security over a year. In the the example of

Figure 4.1, the annualized mean of the changes

in year-to date return is

and the annualized mean of changes in date-to-end-of-year discount is

These annualized means do satisfy Definition 1,

.

Note.

The and above correspond to the e_0 and e_1 in the MATLAB code underneath Figure 4.1. Likewise and correspond to e_r and e_d.

On the other hand, the MATLAB code shows that the mean return, , and the mean discount, , have opposite signs, and . These computations show that mean returns and mean discounts are essentially incompatible with the theory of interest. The mean return problem has been noted, for example, in [3, pp. 104-105].

SEC Rule 156 below might apply to the situation illustrated by

Figure 4.1 and the

hn2mv3.m script which follows it.

Rule 156: Investment Company Sales Literature

Under the federal securities laws, including section 17(a) of the

Securities Act of 1933 (15 U.S.C. 77q(a)) and section 10(b) of the

Securities Exchange Act of 1934 (15 U.S.C. 78j(b)) and Rule 10b-5

thereunder (17 CFR Part 240), it is unlawful for any person,

directly or indirectly, by the use of any means or instrumentality

of interstate commerce or of the mails, to use sales literature

which is materially misleading in connection with the offer or sale

of securities issued by an investment company. Under these

provisions, sales literature is materially misleading if it:

1. Contains an untrue statement of a material fact or

2. omits to state a material fact necessary in order to make a

statement made, in the light of the circumstances of its use,

not misleading.

Rule 156 raises an interesting question. Is the use of mean-variance

analysis, as it appears to be practiced today, “materially misleading”

when an investment company tells a client to “expect” a 160% return

over the next year based on a 25% total return over the past year? This

sort of reasoning reminds us of Mark Twain’s analysis of the expected

shortening of the lower Mississippi due to the rounding of its bends

over time

(Appendix B).

More realistically, consider the example of FBT. In Table 3.1 we have seen that the annualized mean daily return of FBT over 2014 was . An investor with a marginal knowledge of the theory of interest might ask his advisor what the corresponding annualized mean daily discount was. If the advisor were perplexed by this question, the investor could explain that to get the annualized mean discount you simply replace the daily return equation (2.4) by the daily discount equation

| (4.1) |

and sum the results. The advisor might then be mildly concerned by the

annualized average discount, , if he were

told that returns and discounts over the same period of time are

supposed to satisfy the equation

,

according to the theory of interest, but, in fact, .

5 How to do it – the linear model

Our MATLAB script hn2mv1L.m is a linear variant of the

hn2mv1a.m script

of Section 3. We again remove

from and append the unattended portfolio vectors

and to the

result. Then we add the unattended, long-short portfolio

ZNS, with normalized adjusted closing price vector

| (5.1) |

to , so that becomes the matrix

of rank 2. Finally, we put back into ,

| (5.2) |

and, since is independent of the other six columns of , the rank of increases to 3.

When the lines

⬇

%% get asset moments from adjusted closing prices

ptf = Portfolio;

ptf = estimateAssetMoments(ptf, A, ’dataformat’, ’prices’);

[mn, cv] = getAssetMoments(ptf);

of hn2mv1a.m are replaced with the lines

⬇

%% get daily changes in year to date return

R_0 = diff(A / 100); % divide by 100 so that A(1, :) == 1

%% get (annualized) asset moments

E_0 = sum(R_0) % total return

Sig_0 = sqrt(252) * std(R_0, 1); % standard deviation of return

V_0 = 252 * cov(R_0, 1); % covariance of return

in hn2mv1L.m, we arrive at the mean-variance results

The covariance matrix has rank three, but the upper-left block has rank only two, since the four unattended portfolios UIP through ZNS are affine combinations of the two funds FBT and XBI. Moreover, the corresponding portion of the total return matrix mirrors these affine combinations (in contrast to the confusing order of the five mean return values in the of Table 3.1).

Figure 5.1 shows the obtainable corresponding to Table 5.1. This nonlinear triangle is the -image of the triangle in with vertices , and .

Note.

We mentioned the theory of interest in the last section and the relationship between discount and return. To continue this discusion let be adjusted closing prices of a given security over successive investment periods. Then the total return, , and the total discount, , of the security over this time interval are given by

Thus and conform to the return-discount requirement of the theory of interest,

but a corresponding summand pair only conforms by accident.

5.1 The linear model – part 2

The covariance matrix of Table 5.1 is the Gram matrix, , of the risk vector matrix

| (5.3) |

or

Z_0 = R_0 - ones(252, 1) * (E_0 / 252)

in MATLAB code.

The columns of represent pure risk in that the sum of each

column is zero (= zero total return).

Table 5.1 and Figure 5.1 are summaries of the 2014 adjusted closing price histories of FBT, XBI, UIP, UIP2, UIP3, ZNS, and CRP. and are the complete histories split into their return and risk parts.

For example, let and be the total return and

risk vector of any one of the seven funds in Table

5.1. Then Algorithm 5.1 will compute

the the normalized 2014 adjusted closing price history of

this fund (starting from $100 at the close of 2013-12-31).

Algorithm 5.1: To compute the adjusted closing price vector

from and

Our MATLAB code that illustrates this linear model section is organized into four scripts.

hn2mv1L.m – compute the seven fund mean-variance

table for the linear model

hn2mv1L1.m – construct (and save) the orthogonal

system (UEZ2014.mat)

hn2mv1L2.m – generate an adjusted closing price

history from the orthogonal system

hn2mv1L3.m – construct the seven fund

table corresponding to the orthogonal

system

We have already described the first script, hn2mv1L.m.

The second script, hn2mv1L1.m, takes the risk matrix

(5.3) apart orthogonally,

| (5.4) |

where is defined by

| (5.5) | ||||||

and the resulting is

| (5.6) |

The orthonormal matrix and the FBT, XBI,

ZSN, CRP columns (1, 2, 6, 7) of (Table 5.1)

and (5.6) are saved as U, E_0, and

Z_0 in the MATLAB file UEZ2014.mat. MATLAB Example

2 verifies the contents this file.

Table 5.2 below contains all of the information in Table 5.1 in a more compact, geometric form. The computation reproduces the of Table 5.1

The and rows of Table 5.2 are exactly the same as those of Table 5.1, but the of Table 5.2 replaces the of Table 5.1 and, in each column, .

Figure 5.2 shows the -plane in the risk hyperplane . It exactly reflects the data in Table 5.2. Of course is not in -plane as evidenced by its nonzero -coordinate and the fact that its projection onto the -plane is linearly incompatible with its total 2014 return, .

The illustrative unattended portfolio

(at 2013-12-31 closing prices) in Figure 5.1 and 5.2 had total 2014 return with and .

6 History: adjusted closing prices revisted

Let us close this article with a revised version of Figure 2.1. The revision, Figure 6.1, shows the same adjusted-closing-price history of the exchange traded funds FBT and XBI and the continually reallocated portfolio CRP, but now the unattended long-short portfolio, ZNS, has replaced UIP. Of the four funds and portfolios, ZNS (purple) had the highest 2014 return with the least volatility.

These normalized adjusted closing prices were generated from

UEZ2014.mat by the MATLAB script hn2mv1L3.m. They are

recorded, to 5-decimal places (along with the prices of UIP,

UIP2, and UIP3), in the comma-separated-value file

FXUZC7.csv.

Now the MATLAB script hn2mv1b.m, with the of 5.2 in

the

ptf = estimateAssetMoments(ptf, A, ’dataformat’, ’prices’);

code produces

with the corresponding TikZ image

Here the continually-reallocated black-dotted portfolio points are exactly 1/2 and 3/4 of the -way from FBT to XBI on the red, continually-reallocated, FBT-to-XBI path.

7 Conclusion

The growth in value of an unattended investment portfolio P over a given interval of time can be completely described by a normalized adjusted closing price equation

| (7.1) |

where the are the proportions of the securities in the portfolio P at the close of the day of normalization. The corresponding mean periodic return equation,

| (7.2) |

does not follow when and periodic return vectors are defined by

| (7.3) |

Appendix A An adjusted closing price primer

The adjusted closing prices of a security are artificial “closing prices” that are adjusted to incorporate all dividends and splits. The day-to-day growth of a security or an unattended investment portfolio of securities is completely described by its adjusted closing prices. If the adjusted closing price of the security/portfolio is on market day 0 and on a later market day 1, then its total return from day 0 to day 1 is . Two adjusted closing price vectors for a given security that cover the same time interval must be positive scalar multiples of each other. Thus the returns, , of the security from one market day to another do not depend on any particular adjusted closing price representation.

Table A.1 shows how one can compute adjusted

closing prices for the exchange traded fund XBI over the period

2013-12-31 through 2014-12-31. The required input data are all closing

prices for the fund over this period as well as the dividends it made

during the period with their ex-dividend dates. On each line the adjusted closing

price is computed by

The adjusted closing shares in the table increase on each

ex-dividend day and are constant in between. If the closing price on the

market day prior to an ex-dividend day is and the dividend on the

ex-dividend day is , then the adjusted closing shares on the

ex-dividend day must be increased by a factor of in

order that an investor who has his dividends reinvested maintains the

value of his investment.

The adjusted closing prices in Table A.1 are “normalized” at 100.000 on 2013-12-31. To compute the adjusted closing prices for the 243 missing days just fill in the missing closing prices and multiply them by the corresponding adjusted closing shares. Also note that these closing prices and distributions have not been adjusted for the 3:1 split in 2015.

| adjusted | adjusted | |||

| market | distri- | closing | closing | closing |

| day | bution | price | shares | price |

| 2013-12-31 | 130.20 | 0.768049 | 100.000 | |

| 0.768049 | ||||

| 2014-03-20 | 160.17 | 0.768049 | 123.018 | |

| 2014-03-21 | 0.333023 | 153.15 | 0.769649 | 117.872 |

| 0.769649 | ||||

| 2014-06-19 | 153.32 | 0.769649 | 118.003 | |

| 2014-06-20 | 0.616142 | 153.42 | 0.772754 | 118.556 |

| 0.772754 | ||||

| 2014-09-18 | 159.94 | 0.772754 | 123.594 | |

| 2014-09-19 | 0.562774 | 158.27 | 0.775483 | 122.736 |

| 0.775483 | ||||

| 2014-12-18 | 189.08 | 0.775483 | 146.628 | |

| 2014-12-19 | 0.490997 | 190.34 | 0.777502 | 147.990 |

| 0.777502 | ||||

| 2014-12-31 | 186.46 | 0.777502 | 144.973 |

A.1 Yahoo!Finance

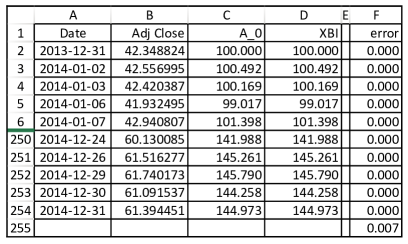

Yahoo!Finance is a good source for adjusted closing prices of an individual security, like our XBI. Simply download the daily, historical prices over the time interval desired as a CSV (comma-separated-value) file and open the file in a spreadsheet program (e.g., Excel).

This spreadsheet will have seven labeled columns:

Date,Open,High,Low,Close,Adj Close,Volume.

Delete all but the “Date” and the “Adj Close” columns. We will

assume these are now columns A and B, respectively, as in the

spreadsheet image (Figure

A.1) below.

The Yahoo adjusted closing prices are not normalized at any particular date. Yahoo simply sets the adjusted closing price of a security at the close of the latest market day equal to its closing price on that day, Then previous adjusted closing prices must be rescaled if the day is an ex-distribution or an ex-split day.

To normalize your Yahoo adjusted prices at say 100 on a particular date (i.e., 2013-12-31 in Figure A.1) start a new normalized adjusted closing price column on your spreadsheet, say column C, by putting

| = B[date row]*100/B$[date row] (with [date row] = the row number) | (A.1) |

in the cell of that date. The number 100 should appear in this cell (i.e., in cell C2). Now you need only fill up and/or down from this cell to get all normalized adjusted closing prices in column C. (We only filled down in in Figure A.1.)

The normalized adjusted closing prices in column C of Figure

A.1 were generated from the prices in column B as described

above. These prices were then rounded to 3 decimal places. The numbers

in the D column come from our anc/FXUZ7.cvs file. They were

generated by the process used to generate Table

A.1 from the closing prices and distributions of

XBI. Out of the 253 market days considered, the C

(A_0) price was 0.001 greater than the D (XBI) price

on 7 days. Otherwise the two columns of adjusted closing prices were

exactly the same. (These 7 “errors” occurred in the 243 rows that have

been collapsed in Figure A.1.)

Appendix B Life on the Mississippi

In the space of one hundred and seventy-six years the Lower Mississippi has shortened itself two hundred and forty-two miles. That is an average of a trifle over one mile and a third per year. Therefore, any calm person, who is not blind or idiotic, can see that in the Old Oolitic Silurian Period, just a million years ago next November, the Lower Mississippi River was upwards of one million three hundred thousand miles long, and stuck out over the Gulf of Mexico like a fishing-rod. And by the same token any person can see that seven hundred and forty-two years from now the Lower Mississippi will be only a mile and three-quarters long, and Cairo and New Orleans will have joined their streets together, and be plodding comfortably along under a single mayor and a mutual board of aldermen. There is something fascinating about science. One gets such wholesale returns of conjecture out of such a trifling investment of fact.

– Mark Twain

References

- [1] Stephen G. Kellison “The Theory of Interest, 3rd Edition” McGraw-Hill, 2009

- [2] Harry M. Markowitz “Mean-Variance Analysis in Portfolio Choice and Capital Markets” Blackwell, 1987

- [3] David F. Swensen “Pioneering Portfolio Management” FREE PRESS, 2009