The Second-Price Knapsack Problem: Near-Optimal Real Time Bidding in Internet Advertisement

Abstract

In many online advertisement (ad) exchanges, ad slots are each sold via a separate second-price auction. This paper considers the bidder’s problem of maximizing the value of ads they purchase in these auctions, subject to budget constraints. This ’second-price knapsack’ problem presents challenges when devising a bidding strategy because of the uncertain resource consumption: bidders win if they bid the highest amount, but pay the second-highest bid, unknown a priori. This is in contrast to the traditional online knapsack problem, where posted prices are revealed when ads arrive, and for which there exists a rich literature of primal and dual algorithms.

The main results of this paper establish general methods for adapting these primal and dual online knapsack selection algorithms to the second-price knapsack problem, where the prices are revealed only after bidding. In particular, a methodology is provided for converting deterministic and randomized knapsack selection algorithms into second-price knapsack bidding strategies, that purchase ads through an equivalent set of criteria and thereby achieve the same competitive guarantees. This shows a connection between the traditional knapsack selection algorithm and second-price auction bidding algorithms, that has not previously been leveraged.

Empirical analysis on real ad exchange data verifies the usefulness of this method, and gives examples where it can outperform state-of-the-art techniques.

1 Introduction

Online advertising is one of the fastest growing sectors in the Information Technology (IT) industry. Total digital ad spending in the U.S. increased by 16% year-over-year in 2016 to $83 billion, and the global digital advertising market is projected to reach a total of $330 billion by 2020.111Digital advertising spending worldwide from 2015 to 2020 (in billion U.S. dollars) https://www.statista.com/statistics/237974/online-advertising-spending-worldwide/ The increasing volume of web traffic led to the birth of ad exchanges, resulting in a larger market where advertisers have a stronger chance of locating a preferential ad-context and publishers generate more revenue by being matched with these advertisers.

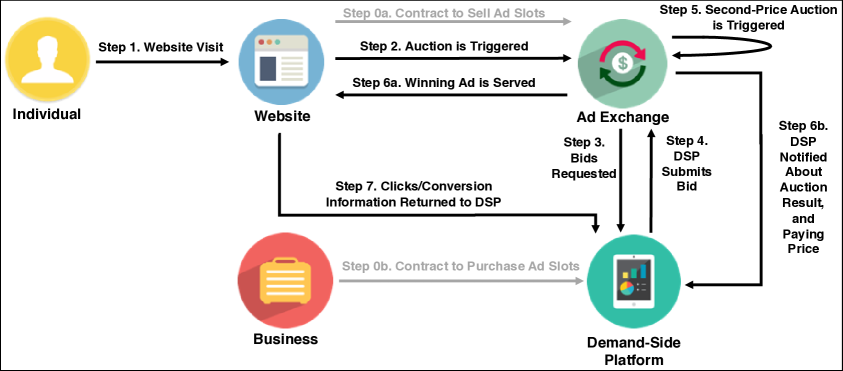

These ad exchanges use a variety of auction mechanisms. One popular auction framework is real-time bidding (RTB). Under the RTB framework, an auction for each ad slot is triggered when a user visits a web-page, with the auction containing contextual parameters; the ad exchange then solicits bid requests from several Demand Side Platforms (DSPs), who each can return a bid for an advertiser it represents; finally the winning ad reaches the publisher. The paying price in RTB is set according to a second-price auction mechanism, i.e. the winner is the bidder with the highest bid, provided that it is above the floor price set by the exchange, and the winner pays a maximum of the floor price and the second highest bid. Given that the auction must be completed before the web-page loads, this imposes latency requirements for the DSP. Notably the bid price calculated and submitted by a DSP must be done within about 10 milliseconds, requiring simple bidding strategies. Furthermore, DSPs may receive a large number of bid requests from exchanges per second, while billions of people explore the web around the globe. Hence, a DSP’s job can be quite intensive, and there is a limit to the complexity/number of updates that can be made to the bidding strategy in an online setting. We represent the process of online advertising, bidding and ad allocation in Figure 1.

This paper considers the budget constrained bidding problem from the perspective of a bidder (DSP) who represents a single advertiser, a common scenario for large companies. The bidder wants to maximize the total value of ads (indexed by ) they purchase, where the value of each ad is known to the bidder using contextual parameters (user and ad slot information), subject to a budget constraint . The bidder must create a bidding policy where they bid based on the information available to them at the time of the auction: the value of the ad , the results of the previous auctions, and their remaining budget. Unlike a traditional knapsack problem, there are two significant difficulties when finding an optimal bidding policy. First, the bidder does not know whether they will win an auction based on the amount that they bid, since the paying price is not determined before completion of the auction. Second, even if they win the auction, they do not know beforehand the amount that they pay: they only know that it will be less than the amount they bid. We generalize this framework to a second-price knapsack problem with uncertain budget consumption in (2.1). We refer to this problem as the second-price knapsack problem.

1.1 Our Contribution

The main thesis of this paper is that myriad primal and dual algorithms for the traditional online knapsack problem, where participants choose whether to select items with known prices as they arrive, can be adapted to the budget-constrained second-price knapsack problem, where participants must bid on items with unknown prices. In particular, we provide a methodology for converting deterministic (dual) and randomized (primal) online knapsack selection algorithms into second-price knapsack bidding strategies offering the same competitive guarantees. This establishes a strong connection that has not been mentioned in the literature, and yields competitive algorithms for advertising companies (among others) that are readily implementable.

The paper starts by building an intuition for why this connection might be expected. To do so, we study the retrospective offline setting, in which the set of ads and paying prices are known. Considering this as a selection problem rather than a bidding problem, it reduces to a traditional knapsack problem. From the offline greedy knapsack algorithm, a threshold policy on the value-to-price ratio is optimal for the linear relaxation of this selection problem which is a known result. That is, we select all ads where , and some fraction where , where is an optimal solution to the dual problem. In our specific context, where , the greedy approach yields a near-optimal solution to the integer selection problem as well. The question is whether this can be turned into an implementable bidding strategy in the second-price knapsack setting, where the information is not available at the time of bidding. Because of the structure of the second-price auction mechanism, we can recover exactly this near-optimal selection with a linear form of bidding only based on the value of the ad.

We then consider the online second-price knapsack problem with budget constraints and known time horizon. We show that under common assumptions (stable arrivals of bid requests, and stable reserve prices and competitors’ bidding strategies) we recover the random-permutation assumption that many online-knapsack algorithms rely on. We then establish our main contribution: using the structure of a second-price auction, we show how one can adapt very general classes of primal and dual online knapsack selection algorithms, and apply them to this second-price knapsack problem with uncertain budget consumption. Concretely, we provide a methodology for converting deterministic and randomized selection algorithms into bidding strategies for the second-price knapsack problem. These adaptations will, in effect, select ads according to the same mechanisms, and therefore achieve the same competitive ratios.

We provide examples of these second-price knapsack algorithms, which give us a competitive ratio of , where is small in practice and sublinear with respect to the number of ads that arrive. This yields a theoretical result on an important variation of the standard online knapsack problem which arises in the context of Internet advertisement.

Finally we use the iPinYou dataset to give numerical support to our work, and contrast with current state-of-the-art adaptive pacing algorithms. iPinYou is currently the largest DSP in China. The dataset contains logs of features, bids, assignments, feedback for all impressions over a season. We process the contextual information for every impression, score the market price and customer feedback (click). From reviewing the data, the different features clearly affect the value of an impression which also changed based on the advertiser. We fit a model for each advertiser to estimate the value of an ad based on the contextual features. We evaluate the performance of our example bidding strategy in the online setting and compare it to both adaptive pacing, and the offline optimum value for different advertisers and budgets. We find that for bidders with the budget to purchase only of the ads they are interested in, the example algorithm that is provided performs near-optimally and can outperform adaptive pacing, which is a popular approach both in the literature and in practice, by an average of 25.9%. These results demonstrate the practical implications of the work.

While this paper focuses on the second-price knapsack mechanism, the theorems also apply to all deterministic, single slot, dominant strategy incentive compatible (DSIC) mechanisms222For any deterministic DSIC auction, and given the actions of the other participants, there exists a price for which the bidder wins whenever they bid above , and if so they pay price . It can easily be seen that the main results hold, with identical proofs.. This encompasses many of the mechanisms that are used in practice for the online ad industry (with some notable exceptions being randomized mechanisms and variations of first-price auctions). The paper’s results have a significant practical impact for online advertisers, by recognizing connections between online selection algorithms for the traditional knapsack problem and bidding algorithms for the second-price knapsack problem, that have not traditionally been leveraged.

1.2 Related Work

Knapsack problems and the design and analysis of online algorithms have been widely studied in operations research, while the specific RTB context has been studied more within the computer science community. We do not review the broader ad allocation and planning problems which can be combined to our work on bidding strategies.

Our bidding policies are based on a theoretical analysis of the knapsack problem, and its variant the packing problem. In fact, we cast the optimal bidding policy as the solution to a knapsack problem with budget uncertainty, as stated in (2.1). We refer the interested reader to Kellerer et al. (2004) for a thorough review of knapsack problems. As for the online knapsack problem, Marchetti-Spaccamela and Vercellis (1995) prove that the competitive ratio can be pushed away from near-optimality to in the adversarial knapsack problem, even for randomized algorithms. Lueker (1998) designs a value-to-bid threshold function which depends on the ratio budget spent over leftover time to design a binary decision function. They then provide a scheme for approximating the optimal thresholding function from observed realizations. The fractional knapsack problem has been studied in Noga and Sarbua (2005). In our work we use packing duality theory, through which we are able to derive the desired optimality guarantees.

In order to avoid the adversarial setup of the online problem, recent literature considered variations of the stochastic setting. Kleywegt and Papastavrou (1998) analyze the stochastic case where items are drawn from an i.i.d. distribution. Under this framework, extensive research has been done for the bandits with knapsacks problem. Further under the random permutation model, Devanur and Hayes (2009) prove a competitive ratio for their algorithm, which is based on a linear program (LP). Their approach solves offline the LP associated to a sample of the items, which is large enough to recover the distribution and thus provide concentration inequalities. These then provide guarantees on the dual variables from the sub-sampled LP to the true LP. Integer optimization tools then bridge the gap to recover the true solution. Feldman et al. (2010), Agrawal et al. (2014) use similar ideas, but using a dynamic algorithm solving multiple LPs in online fashion. This approach yields tighter bounds given the sharper estimate of the dual parameters from the data. In their work, they focus on providing a competitive ratio analysis for when the input size is large.

On the other hand, Buchbinder et al. (2009) provide a wide variety of algorithms for more general online optimization problems. They approach these by using Primal-Dual algorithms which yield arbitrarily good competitive ratios while violating dual constraints by some factor. These compare to thresholding functions by setting dual prices for budget consumptions. Babaioff et al. (2008) analyze the special case of the secretary problem where weights are in . Buchbinder and Naor (2005, 2006) give an algorithm with a multiplicative competitive ratio of for the online knapsack problem based on a general online primal-dual framework where are respectively constraining upper and lower bounds on the individual value of ads, the resulting competitive ratio scales with the bounds. These algorithms were applied to second-price auctions by (Chakrabarty et al. 2007, Zhou and Naroditskiy 2008), although the analysis focuses on worst-case guarantees in the adversarial setting, as opposed to our work which studies expected value guarantees in the random permutation setting. Important work on the knapsack problem has also been done in the setting where values are unknown. Badanidyuru et al. (2018) study this setting, and develop primal-dual algorithms with sublinear regret.

We now relate the knapsack problems to the RTB literature. The design of a bidding strategy requires an algorithm to cast real-time decisions for the bidder based on contextual information. Recent contributions have been made to the bidding strategies by formulating the problem as an online knapsack problem. Notably in the advertisement community, Chakrabarty et al. (2007) design the problem by assuming bounds on items’ values, which are small compared to the total budget, under adversarial arrivals. Similarly to Lueker (1998), they design an online algorithm based on a threshold function guiding their bidding strategy. Their algorithms depend on some input parameters which directly influences its performance. We extend their work by proving near-optimality of a threshold based algorithm under some large-scale assumptions. The idea of using a threshold function was first introduced by Williamson (1992), however they design an asymptotically optimal strategy only when the arrival distribution is known.

Much of the RTB literature makes very stylized and stringent assumptions to provide tractability. These may be assumptions on the distribution of the arrivals or assuming that the probability of winning an auction is a direct function of the amount bid. Keyword auctions have been studied while others deal with more empirical and data driven questions (see Edelman and Ostrovsky 2007, Zhou and Lukose 2007, Chen et al. 2011, Lee et al. 2012, 2013, Zhang et al. 2014, Yuan et al. 2013, Ren et al. 2018). There is also relevant work in the stochastic setting, by Jiang et al. (2014), which uses mean-field approximation to model competitors’ behaviors and creates an algorithm that converges to an optimal solution in expectation.

The most similar work to our own is recent work on adaptive pacing for the online second-price knapsack problem under budget constraints, when the valuation distributions for different bidders are unknown and independent Balseiro and Gur (2017). Their algorithm tries to learn the dual parameter in order to keep the expenditure path stable over time, which is an approach we leverage as well. The adaptive pacing algorithm is shown to offer asymptotic optimality for both the stable and arbitrary settings, and converges to an equilibrium in dynamic strategies. Existence of an asymptotically optimal constant competitive ratio, versus the offline oracle, is also shown. Unlike our results in Section 2.3, though, a competitive ratio is not explicitly given the finite setting.

2 Model and Analysis

We take the bidder position of a DSP representing an advertiser. When we are presented with an auction for a new ad slot, we must decide whether to bid on the ad or not, and if so, how much to bid. We consider the set of all non-anticipatory bidding policies , which satisfy our budget constraint, where for any and ad we bid some amount . We win the auction when is the highest bid (and above the floor/reserve price defined for the auction, although this can be considered as another bidder without loss of generality), and pay the maximum of the other bids. We label this paying price , and note that we win the auction whenever and always pay when we win. Upon winning the auction, we collect value , known prior to the auction. The objective is to design a bidding strategy that maximizes the total collected value under budget constraint .

Our main difficulty in designing a bidding strategy for the online setting is that we do not know the paying price a priori. We first consider the offline traditional knapsack problem in which is known. We then show there exists a simple near-optimal bidding policy for the online second-price auction setting where is unknown which is a linear function only of the value of the ads and some bid parameter .

For the online problem, we then provide our main results in Theorems 1 and 2, which establish a methodology for adapting a variety of selection algorithms from the traditional online knapsack problem to bidding algorithms in the second price knapsack problem. Using these theorems, we reconsider the specific problem of training the bid parameter for our second-price knapsack strategy, in an online setting. To illustrate this, we show how work by Agrawal et al. (2014) for an online one-shot-learning algorithm with a competitive ratio of , can be applied to the online second-price knapsack problem where the paying prices are unknown, achieving the same competitive ratio. This is summarized in Example 1.

2.1 Model Framework

We consider the model with respect to a bidding policy satisfying the budget constraint, where we bid for ad . Although the paying price is unknown, we win if , and pay amount . This allows us to cast the second-price knapsack problem with budget uncertainty, hence labeled (2.1), for the online setting as:

In the offline setting where the paying price is known at the time of bidding, the problem reduces to a traditional knapsack problem. Items arrive with known value and paying price . If we want to select this item we just bid some amount at least as large as and pay . If we do not want to select the item we just bid . We rewrite the problem by replacing our policy with equivalent selection variables and have:

| (K) |

2.2 Near Optimality of the Linear Bid

In this section we build an intuition for why the connection between the second-price knapsack problem and the traditional knapsack problem might be expected. This is done through an analysis of the offline problem.

We make use of two assumptions, that are observed to be reasonable based on an empirical review of the iPinYou data (see Section 3).

Assumption 1 (Value-to-Price Uniqueness).

The ratios are unique for our selection of ads .

Assumption 2 (Low-Individual-Impact).

For each ad, and .

From these assumptions, the first result for the second-price knapsack problem follows: there exists an implementable bidding policy that recovers a near optimal selection of ads for the offline setting, where the bid amount is only a function of the same information that is available when ads arrive online. In particular, this near-optimal bid amount is not a function of the price that must be paid in order to win the auction!

Proposition 1.

Consider the optimization problem (2.1): for any set of ads with values , we seek a bidding policy to maximize total value of ads purchased subject to our budget . Then there exists some constant such that the linear bidding policy which bids an amount

yields a feasible set of purchased ads with a total value within of the optimal value.

This is very similar to a recent result by Conitzer et al. (2019). However our work, which was done independently, has a couple distinctions which are valuable to this paper. First, the Conitzer et al. (2019) result proves optimality of the linear bid by assuming that the bidder can arbitrarily choose to purchase any subset of the ads where the amount we bid equals the highest competitor bid, and requires some a priori knowledge about how many ads this will apply to. In contrast, we directly show near-optimality without this a priori knowledge. The second difference is that their proof is a direct argument, while ours uses the dual problem to prove near-optimality. Because the dual interpretation is used in Sections 2.3 and 3, this version of the proof gives some additional insight as it relates to the main results in Section 2.3.

An overview of the proof is as follows, let us again consider the traditional knapsack problem in (K). The linear programming relaxation (K-LP) can then be written as:

| (K-LP) |

The dual problem to (K-LP) is:

| (K-Dual) | |||

where ads are such that . Dual prices allow us to solve (K-LP) exactly: we select an item if and only if is above a certain threshold parameter (see Fisher 1981, Kellerer et al. 2004, Bertsekas 1995). We then demonstrate that the optimality gap between (K-LP) and (K) is bounded by a small amount because . Finally, we turn offline selection into an implementable online bidding policy for the second-price knapsack problem (that is not a function of ).

2.3 Adapting Online Knapsack Algorithms

In this section we present our main results (Theorems 1 and 2): methods for adapting online knapsack selection algorithms on finite time horizon , where we select ads based on some function of at time where the paying price is known, to the second-price online knapsack setting, where we must make a bid without knowledge of a priori.

In essence, these methods provide a generalization of selection policies, ill-defined when the paying price is unknown, to implementable bidding policies, which are now suited for the second-price problem.

We present two such methods. The first is a method for deterministic selection policies, and applies widely to dual online knapsack algorithms, and the second is a method for randomized selection policies, and applies widely to primal online knapsack algorithms. We give examples for each method, including a one-shot learning algorithm, that creates an online, near-optimal bidding policy under the random permutation setting.

We say that a deterministic algorithm has competitive ratio for the online problem if:

where denotes the performance obtained by the offline optimum on a random instance , is the performance of the online algorithm, and the expectation is taken over the randomness in online instances.

Because the online knapsack algorithms of interest to us rely on the random permutation assumption, we explore what this requires in the second-price knapsack problem. We assume a stable setting, where our competitors have consistent bidding strategies, the auction platform keeps consistent reserve prices, and ad opportunities arrive in a random order. From these assumptions we recover the random permutation assumption on an expanded set of ads, including some synthetic zero-value ads. This property states that for a set of future ads, they are equally likely to arrive in any order. These assumptions directly imply the following lemma.

Assumption 3.

Conditioned on ads arriving over some period of time, all permutations of the arrival order are equally likely.

Assumption 4.

Competitors have consistent bidding strategies and the auction platform keeps consistent reserve pricing methods over time. That is, given ad with specific contextual parameters (giving us value ), the competitors bid the same amount for the ad, and the auction platform sets the same reserve price for us, regardless of when it arrives. As a result, paying price is the same for us if we win the ad, regardless of which week the ad arrives in.

Lemma 1 (Random Permutation).

Proof.

From assumption 3, any arrival of ads, as measured by their values , are equally likely. From assumption 4, the paying prices remain the same for all ads, regardless of the order they arrive in. As a result any arrival of ads, as measured by both and are equally likely, which is the random permutation property. ∎

The random permutation assumption is technical, only necessary to recover the same theoretical guarantees as online knapsack algorithms which use a variation of the assumption. In practical settings where the assumption can be violated, our methodology can still be applied.

We continue to our main results: methods for taking a wide class of online knapsack algorithms, where we select the ad at time based on some function of and , and turning them into online bidding strategies for the second-price knapsack problem, where we need to submit a bid without prior knowledge of the price .

For the remainder of the section, we let denote the remaining budget at time , and denote the history available to the bidder at time (including the values of previous ads, the maximum of our competitors’ bids, the reserve price, and the auction outcome).

2.3.1 Deterministic Algorithms

The first method summarized in Theorem 1 holds for deterministic online knapsack selection algorithms, and follows a similar reasoning to Lemma 4 from the appendix. To the best of our knowledge, this Theorem can be applied to all dual-based online knapsack algorithms.

Theorem 1.

Consider an online knapsack algorithm, where at time step we select an ad if , for some continuous function which is monotonically increasing with respect to and satisfies and .

In the second price setting, we can recover exactly this set of ads without a priori knowledge of , and therefore achieve the same competitive ratio, by bidding:

Further if implements a budget feasible selection algorithm then our bidding policy is also budget feasible.

Proof.

We prove that this algorithm recovers all ads where

, and no ads where . If , then because is monotonically increasing with respect to , we have that , so we win the auction by bidding . Similarly if , then because is monotonically increasing with respect to , we have that , so we do not win the auction by bidding .

Because is not dependent on the a priori unknown price , this is an implementable bidding strategy in the online second price knapsack problem. Further given feasibility of the selection policy, then we have , so our bids verify which guarantees feasibility of our bidding policy. ∎

We now give an example of how Theorem 1 can be applied. We consider existing work on a one-shot learning for the online knapsack by Agrawal et al. (2014). Using this, we give a bidding policy for the online second price knapsack problem, that has a competitive ratio of under the random permutation setting. While there are improved results upon which Theorem 1 could be applied (e.g., Agrawal and Devanur 2015), we think the given example is a very intuitive approach, shares similarities to Proposition 1, gives a good introduction to the process of adapting deterministic online knapsack algorithms, and offers a low latency making it practical for DSPs to implement.

Example 1 (Agrawal et al. (2014)).

Let denote total budget and let be an upper bound on the paying price for any ad. Select a training ratio , s.t. satisfies:

| (1) |

For the first fraction of ads, we record the highest bid for each ad, after the auction is completed. This is what we would have had to bid (and pay) in order to win the ad. Determine the optimal dual price solution to (OLA-LP) given below:

| (OLA-LP) |

We then apply Theorem 1, and turn the selection policy of Agrawal et al. (2014) into a bidding policy for the remaining fraction of ads. For these remaining ads, we bid for ads , where is our remaining budget. The bidding policy is feasible by definition in the second-price setting. From Theorem 1, we recover the same set of ads as would the algorithm from Agrawal et al. (2014) in the traditional knapsack setting, therefore recovering the same competitive ratio of . Given the offline optimum remains unchanged under both settings, our adaptation to the problem where the paying prices are unknown enjoys the same competitive ratio of relative to the optimal bidding policy. The methodology in Theorem 1 allowed to adapt the existing selection policy when paying prices are known to our bidding policy under the unknown second price.

Contextually, since our budget is very large relative to ad prices, this process could be applied for a very small , and would give a very strong competitive bound. For clarity we now present Example 1 in Algorithm 1 as pseudo-code.

2.3.2 Randomized Algorithms

The second method, summarized in Theorem 2, holds for randomized online knapsack selection algorithms. This Theorem can be applied to a variety of primal online knapsack algorithms, to adapt them into randomized bidding policies for the second-price knapsack problem.

Theorem 2.

Consider an online knapsack algorithm, where at time step we select an ad with probability , for some (right-)continuous function which is decreasing with respect to , and satisfies and . By defining , we create a CDF with domain .

In the second price setting, we can purchase ads with the same probability as , without a priori knowledge of , and therefore achieve the same competitive ratio, by bidding:

Further if implements a budget feasible selection algorithm with probability 1, then our bidding policy is also budget feasible.

Proof.

We first show that is well defined. Because is decreasing in , and satisfies and , we have that is increasing, with domain , with and . Therefore defines a (right-)continuous CDF for some distribution.

Next, we show that randomly drawing , and then bidding , will recover ad with probability . In the second price setting, we recover ad if and only if we bid . This happens when , which occurs with probability . From the definition of , we have , so we recover the ad with the initial desired probability.

Because is not dependent on the a priori unknown price , this is an implementable randomized bidding strategy in the online second price knapsack problem. Further given feasibility of the randomized selection policy, then we have a.s. Thus our bids verify a.s., which guarantees feasibility of our randomized bidding policy. ∎

Next, we give an example of how Theorem 2 can be applied, to create a bidding strategy for the second-price knapsack problem with a strong competitive ratio in the stable setting.

Example 2 (Kesselheim et al. (2014)).

Let denote total budget and let be an upper bound on the paying price for any ad. Similarly, given a scaling factor and a set of observed ads , we denote the set of feasible solutions to the linear relaxation of (K) where the budget is scaled by and only ads from can be selected. Formally this is the set .

For every ad arrival , we solve a fractional scaled ad selection for the knapsack problem, where in particular the scaling factor is . We then interpret the fractional selection as a randomized selection policy, which can be readily implemented as a bidding policy in the second price setting using Theorem 2. In particular at ad arrival , we let the function of optimal solutions to the scaled problem

| (PLA-LP) |

with paying price and we define the CDF accordingly. Then we sample , and bid where is the leftover budget.

Consider a modified version of our strategy. We first bid regardless of our leftover budget, but only carry out the selection if the paying price is smaller than our leftover budget. That is we bid . This modified bidding policy realizes the same probabilistic selection policy from the randomized rounding procedure in Kesselheim et al. (2014). Therefore Lemma 2 and subsequently Theorem 3 from Kesselheim et al. (2014) hold for our proposed bidding policy.

Finally our policy achieves the competitive ratio of . Equivalently , for , the randomized algorithm achieves an expected competitive ratio of relative to the optimal bidding policy over the entire set of ads .

Again in our context this process could be applied for small , and would give a very strong competitive ratio. For clarity we now present Example 2 in Algorithm 2 as pseudo-code.

We conclude this section by pointing that our theorems generalize to deterministic auctions, where for every auction, there exists a value , such that the bidder wins the auction if they bid at least and pay exactly . The proofs can be directly adapted using this simple property.

3 Empirical Results

In this section we use the iPinYou dataset to give numerical support to our work. Assigning as the expected click-through rate per advertiser for that impression, we measure the efficiency of Algorithm 1 and show we are able to recover near-optimal ad bundles in an online setting. These results are robust to changes in budget, and are consistent for all advertisers, which highlights the effectiveness of our methods. We also compare our results against adaptive pacing.

3.1 iPinYou Dataset

Until recently, academics were limited in studying the application of RTB strategies since bidding data is generally kept secretive. Fortunately in 2013, iPinYou Information Technologies Co., Ltd (iPinYou), the largest DSP in China, began a competition for RTB algorithms and released three seasons of data for a small number of advertisers. Each season corresponds to one week of data, with the entire release totaling 35GB. To the best of our knowledge, this is the first publicly available RTB dataset.

Data Format

For the competition, iPinYou released information for different types of exchange activity: bids, impressions, clicks, and conversions. Combined, these datasets capture most of the relevant data from an auction: 1) The contextual ad features which are sent along with bid requests (ad slot parameters, viewer demographics), 2) The winning bid amount and the paying price (which we refer to as the market price), and 3) The user feedback, i.e. clicks and conversions on the won impression. The dataset variables and advertisers also vary by season, so we chose to focus our numerical testing on season three of the data, which included advertiser and user IDs.

| Feature | Description |

|---|---|

| iPinYou ID | A unique identifier for every bid in an auction. |

| Timestamp | Date of the auction. |

| Log type | Outcome of the ad - whether the user clicked or purchased. |

| Bidding price | The amount bid by the advertiser. |

| Paying price | The amount paid by the winner of the auction. |

| Advertiser ID | Information concerning the advertiser. |

| Col # | Feature |

|---|---|

| 1 | Bid ID |

| 2 | Timestamp |

| 3 | Log type |

| 4 | iPinYou ID |

| 5 | User-Agent |

| 6 | IP |

| 7 | Region |

| 8 | City |

| 9 | Ad Exchange |

|---|---|

| 10 | Domain |

| 11 | URL |

| 12 | Anonymous URL ID |

| 13 | Ad slot Id |

| 14 | Ad slot width |

| 15 | Ad slot height |

| 16 | Ad slot visibility |

| 17 | Ad slot format |

|---|---|

| 18 | Ad slot floor price |

| 19 | Creative ID |

| 20 | Bidding price |

| 21 | Paying price |

| 22 | Key page URL |

| 23 | Advertiser ID |

| 24 | User Tags |

Data Summary Statistics

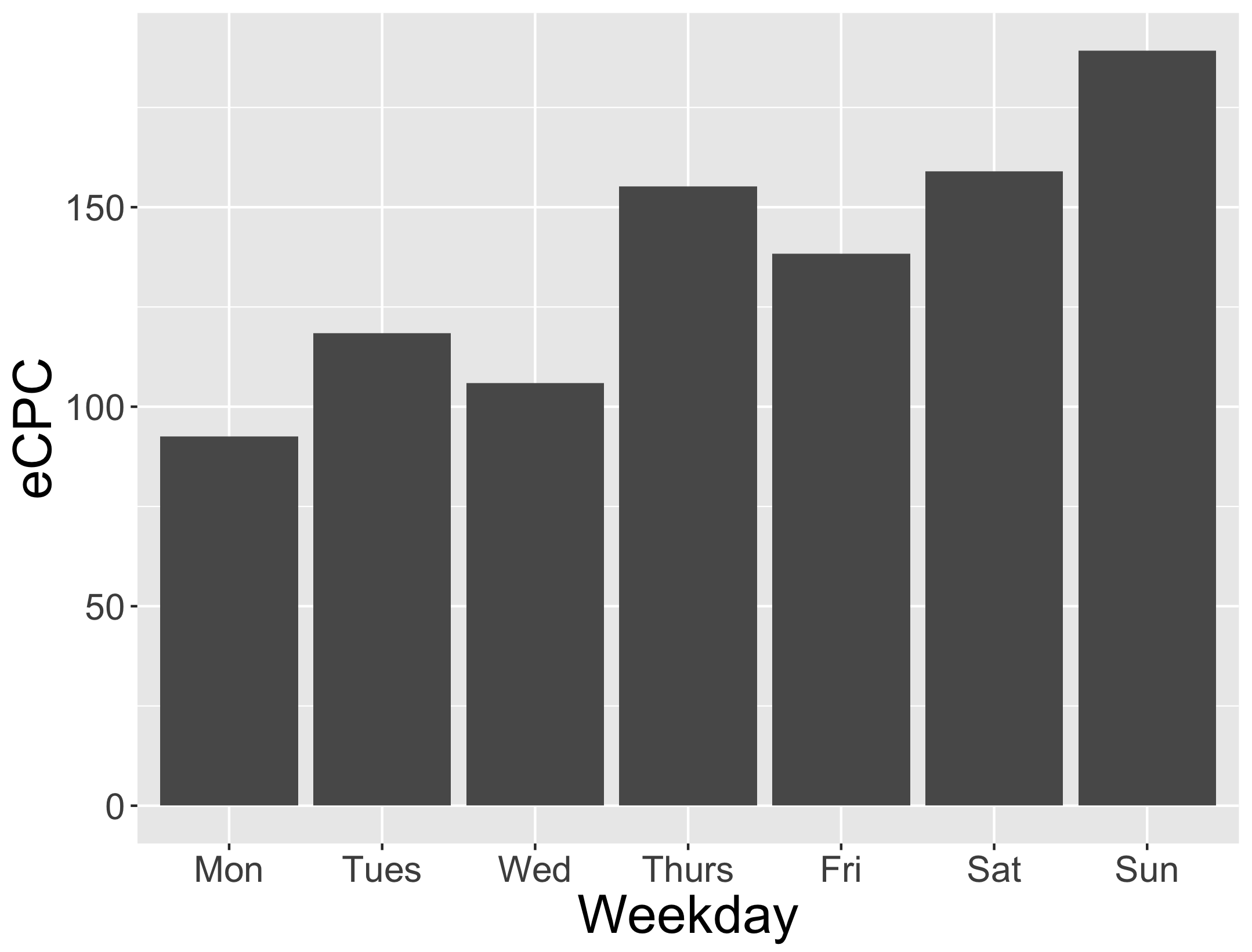

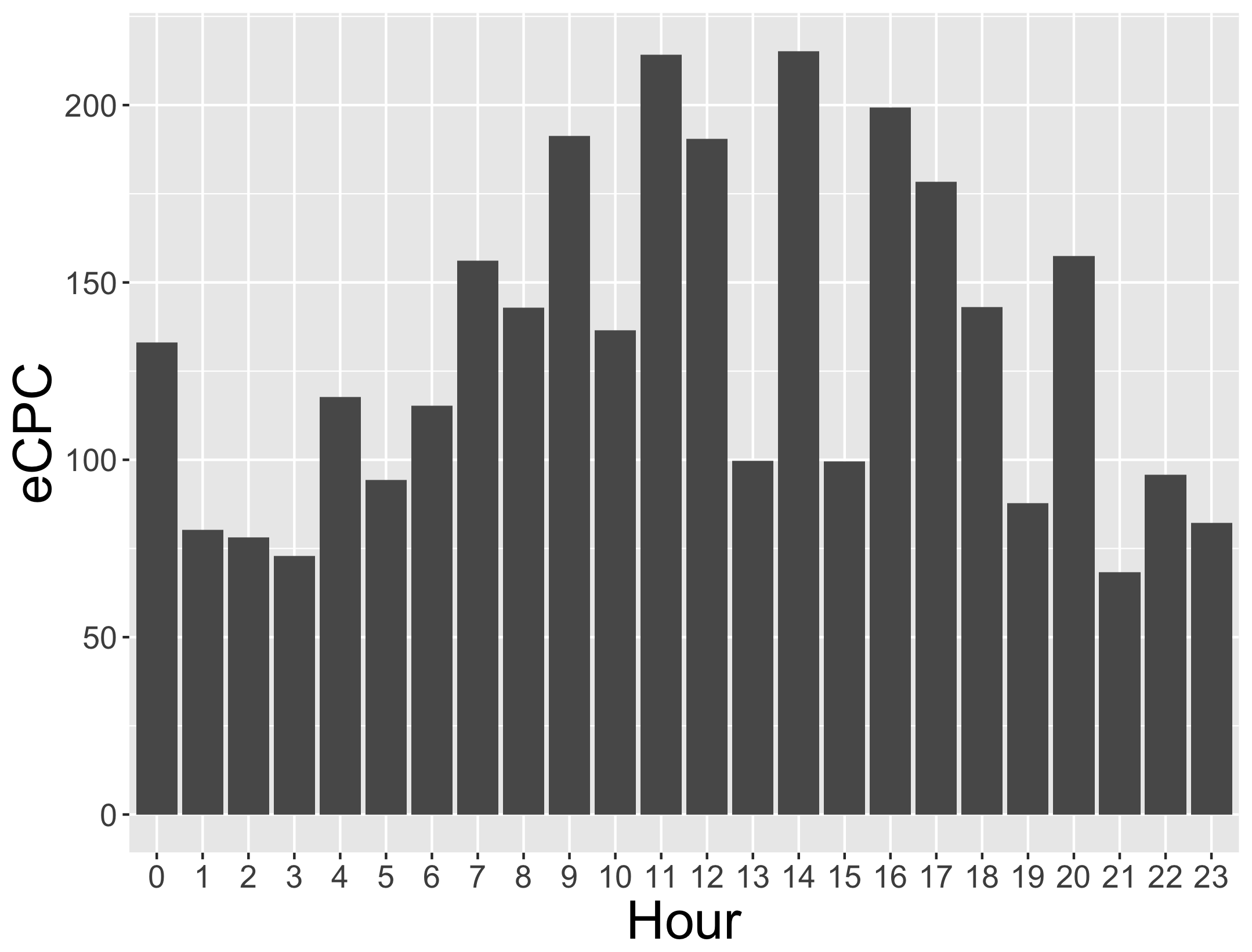

Season three contains information about five advertisers in different fields: Chinese vertical e-commerce, software, international e-commerce, oil and tires. All advertisers have click-through rate CTR on their won auctions inferior to 0.1%. Although the cost for achieving an impression is similar across advertisers (80 RMB per thousand impressions), the expected cost per click differs by advertiser. Further the conversion rate CVR varies also. From a review of the data it was clear the extent to which features affected the CTR, with the influence of a given feature varying for each advertiser. This motivated modeling a different predicted click-through rate (pCTR) estimator for each advertiser, to account different customer feedback trends depending on the day and time. From the logs, we also review the variations of cost-per-click (CPC) compared to individual features. We plot relevant CPC variations against different features in Figure 2.

This brief review of the iPinYou dataset suggests there exist opportunities for more efficient bidding strategies among each advertiser. In addition we also report the basic statistics from the third season of data (June 6-12) in Table 3.

| Advertiser ID | Impressions | Clicks | Tot. Bid | Tot. Cost | CTR | eCPC |

|---|---|---|---|---|---|---|

| 11458 | 3,083,055 | 2,452 | 924,916,500 | 212,400,191 | 0.080% | 86.62 |

| 3358 | 1,742,104 | 1,350 | 405,466,041 | 160,943,087 | 0.077% | 119.22 |

| 3386 | 2,847,802 | 2,068 | 854,340,600 | 219,066,895 | 0.073% | 105.93 |

| 3427 | 2,593,765 | 1,922 | 612,619,071 | 210,239,915 | 0.074% | 109.39 |

| 3476 | 1,970,360 | 1,027 | 488,187,425 | 156,088,484 | 0.052% | 151.98 |

3.2 Data Pre-Processing

Starting with the iPinYou data shown in Table 1, processing was performed to get the data in a usable format. We first deleted the small number of ad impressions for which there was missing data and duplicated to remove a small number of redundant rows. We extracted the weekday and hour feature from timestamps. From user agent text, we extracted operating systems. We also split the column of the tag list of user interests into a large number of binary variables, representing user interests in all the specific categories. We also removed unique features or nearly unique such as Bid ID, Log Type, iPinYou ID, URL, Anonymous URL ID and Key Page URL that we could not train our predictors on.

3.3 Experimental Setup

Success in our empirical work is measured with respect to some known values for each ad. In practice, advertisers value success based on their click-through-rate (CTR) and conversion rate. Each advertiser values the balance between clicks and conversions differently, which is captured in the general literature as the Key Performance Indicator (KPI), defined as a linear combination:

where the factor is advertiser specific. However as seen in Table 3, the small number of conversions presented an issue and we made the decision to set for our testing, meaning .

To evaluate the threshold strategy, we therefore assign ad values as follows: we create a estimator for each advertiser, and set the value of each ad equal to the estimate for the ad. To calculate for each ad we split most categorical features into multiple columns of {0,1}, such as the long-term interests and the demographic fields. A single ad is represented by vector of over 50 features. We then relied on logistic regressions from R’s GLM package to predict the probability of a click. While this gave us a good estimator and was sufficient for our purposes, in practice the prediction is an essential piece of any bidding strategy and advertisers would be well-served by devoting considerable resources to creating the best prediction model possible. In contrast, our priority is just evaluating the effectiveness of our algorithms given an assumed set of values for ads chosen reasonably.

A common difficulty in the experimental setup for RTB research comes from the fact that we only possess detailed ad information for auctions that the advertiser won. Thus in our testing phase, we cannot let an advertiser buy an advert they did not win. We approached this the same manner as previous researchers, and we design a bidding system where each advertiser is only shown auctions they won from the data, but we allow each advertiser a budget only a fraction of the amount they actually spent (otherwise with full budget, the optimal strategy would always be to win every ad they previously won at the same price, which is made possible through bidding your remaining budget at every step because of the second-price auction mechanism). We chose to evaluate several fractional budget amounts, and we set the budget for each advertiser as , , , and of the original total they actually spent.

Let us specifically review the testing process for a fixed advertiser under a budget limit. At each time step:

-

1.

We draw an ad randomly from our test set (that the current advertiser won from our data) and we pass it as a bid request.

-

2.

The bidding strategy computes a bid amount for this contextual request, which does not exceed the remaining budget.

-

3.

If the bid is higher than the paying price, then the advertiser wins the auction. The paying price is subtracted from the remaining budget and the value is added to the objective.

3.4 Results

In this section we present results of testing. To create our testing data, we randomly select one million records per advertiser, for each of the five advertisers in the third season of the iPinYou data. We set our values for each advertiser, using a logistic regression for on the entire testing data set. A summary of the testing data, including the total predictions are given in Table 4.

| Advertiser ID | Impressions | Clicks | Tot. Bid | Tot. Cost | CTR | eCPC |

|---|---|---|---|---|---|---|

| 1458 | 1,000,000 | 800 | 300,000,000 | 68,884,867 | 0.080% | 86.11 |

| 3358 | 1,000,000 | 798 | 232,746,786 | 92,410,850 | 0.080% | 115.80 |

| 3386 | 1,000,000 | 732 | 300,000,000 | 76,918,986 | 0.073% | 105.08 |

| 3427 | 1,000,000 | 742 | 236,188,992 | 81,096,832 | 0.074% | 109.29 |

| 3476 | 1,000,000 | 515 | 247,763,552 | 79,181,869 | 0.052% | 153.75 |

The next step was benchmarking the optimal bundle that could be achieved for a given budget in the test dataset, in the offline setting. We created benchmarks for each of the five advertisers, and each choice of budget (, , , and ).

After benchmarking we tested the online version of Algorithm 1 which follows from the methodology in Theorem 1. To do this we determined the optimal threshold for each budget choice on the . During this training period we bid our value, and deplete the entire training budget. We then took the remaining data, and applied the dual threshold bidding with that same constant in the online setting. We recorded the total value and actual clicks for the selection of ads. This is done for ten random permutations of the data333Because the data includes a very large number of ad auctions, and the value of each ad is small relative to the total, the results are extremely robust to random permutations. The standard deviation of results in the tables is less than 0.1%.. The test results are summarized in Table 5.

| Advertiser ID | pCTR | % of Opt. Bundle pCTR | Actual Clicks | % of Opt. Bundle Clicks |

| 1458 | 756 | 98.3% | 754 | 98.3% |

| 3358 | 741 | 97.5% | 728 | 98.1% |

| 3386 | 587 | 95.5% | 490 | 94% |

| 3427 | 686 | 97.5% | 620 | 96.1% |

| 3476 | 482 | 97.6% | 426 | 97% |

| Total | 3,253 | 97.3% | 3,018 | 96.9% |

| Advertiser ID | pCTR | % of Opt. Bundle pCTR | Actual Clicks | % of Opt. Bundle Clicks |

| 1458 | 712 | 98.5% | 702 | 98% |

| 3358 | 675 | 97.3% | 630 | 97.7% |

| 3386 | 456 | 94.9% | 339 | 93.6% |

| 3427 | 626 | 97.7% | 575 | 97% |

| 3476 | 426 | 97.5% | 382 | 97.4% |

| Total | 2,894 | 97.3% | 2,628 | 97% |

| Advertiser ID | pCTR | % of Opt. Bundle pCTR | Actual Clicks | % of Opt. Bundle Clicks |

| 1458 | 669 | 98.4% | 653 | 98.3% |

| 3358 | 618 | 97.6% | 578 | 97.8% |

| 3386 | 355 | 95.7% | 236 | 94.8% |

| 3427 | 572 | 97.9% | 528 | 97.6% |

| 3476 | 362 | 97.6% | 335 | 98.8% |

| Total | 2,576 | 97.6% | 2,330 | 97.7% |

| Advertiser ID | pCTR | % of Opt. Bundle pCTR | Actual Clicks | % of Opt. Bundle Clicks |

| 1458 | 638 | 98.8% | 619 | 98.0% |

| 3358 | 574 | 98.1% | 534 | 98.2% |

| 3386 | 272 | 95.6% | 184 | 95.3% |

| 3427 | 523 | 97.1% | 496 | 96.3% |

| 3476 | 299 | 97.3% | 287 | 96.6% |

| Total | 2,306 | 97.7% | 2,120 | 97.2% |

We also compared our algorithm’s performance to that of adaptive pacing, over the randomly permuted data. We apply adaptive pacing in accordance with the algorithm used to show its theoretical properties (Balseiro and Gur 2017). We begin by bidding our value while learning to be more selective over time, and use the recommended step size (that is, and ). We chose this parameterization in order to provide a fair benchmark that does not make use of prior information, for either method 444In fact, with perfect prior information (e.g., the offline setting), it can be seen that the optimal initialization of adaptive pacing is just and (i.e. no adaptiveness), which recovers the optimal bundle of ads from Proposition 1, and actually does not feature any ’pacing’ as the bid multiplier is constant. Therefore considering the best implementation of adaptive pacing in hindsight, for all possible values of and , is not a fair comparison.. For each strategy, we record the percentage of the optimal bundle’s pCTR that was recovered, as well as the performance ratio (defined as the value of Algorithm 1 to that of adaptive pacing). The results are recorded in Table 6.

| Advertiser ID | Algorithm 1 | Adaptive Pacing | Performance Ratio |

|---|---|---|---|

| 1458 | 98.3% | 99.5% | 98.8% |

| 3358 | 97.5% | 99.4% | 98.1% |

| 3386 | 95.5% | 99% | 96.5% |

| 3427 | 97.5% | 99.4% | 98.2% |

| 3476 | 97.6% | 99.6% | 98% |

| Total | 97.3% | 99.4% | 98% |

| Advertiser ID | Algorithm 1 | Adaptive Pacing | Performance Ratio |

|---|---|---|---|

| 1458 | 98.5% | 97.8% | 100.7% |

| 3358 | 97.3% | 98.3% | 99% |

| 3386 | 94.9% | 96.5% | 98.4% |

| 3427 | 97.7% | 98% | 99.7% |

| 3476 | 97.5% | 98.1% | 99.3% |

| Total | 97.3% | 97.8% | 99.5% |

| Advertiser ID | Algorithm 1 | Adaptive Pacing | Performance Ratio |

|---|---|---|---|

| 1458 | 98.4% | 93.3% | 105.5% |

| 3358 | 97.6% | 95% | 102.7% |

| 3386 | 95.7% | 88.9% | 107.6% |

| 3427 | 97.9% | 93.9% | 104.2% |

| 3476 | 97.6% | 92.4% | 105.6% |

| Total | 97.6% | 93.1% | 104.8% |

| Advertiser ID | Algorithm 1 | Adaptive Pacing | Performance Ratio |

|---|---|---|---|

| 1458 | 98.7% | 78% | 126.6% |

| 3358 | 98% | 83.7% | 117.1% |

| 3386 | 95.5% | 66.1% | 144.4% |

| 3427 | 97% | 78.5% | 123.6% |

| 3476 | 97.2% | 73.3% | 132.7% |

| Total | 97.6% | 77.5% | 125.9% |

The results are interesting. For advertisers with a large budget fraction of (enough to afford half the ads they are interested in), we see that adaptive pacing performs almost perfectly, which in fact validates our parameter tuning for their algorithm. In contrast, though, we see that the performance of adaptive pacing degrades significantly as advertisers become more selective. At budget of , which represents a common level of selectivity among bidders in reality, adaptive pacing incurs significant performance degradation. This makes sense intuitively for selective bidders, as adaptive pacing’s dual parameter search takes longer to converge to the optimum, and then oscillates more significantly around the optimum because of the step direction imbalance. At this budget fraction of , the algorithm buys roughly that fraction of impressions, so about ad arrivals are not purchased and lead the algorithm to become slightly less selective, while are purchased and lead the algorithm to become significantly more selective. In contrast when the budget fraction is , this search is much more balanced and has less variance. In comparison, Algorithm 1 does not have these downsides, and outperforms adaptive pacing by on average when the budget fraction is . Thus Algorithm 1 could have a significant practical impact for bidders in practice, where they typically only have a budget large enough to purchase a small fraction of the ad impressions they might be interested in.

One may argue that this is not a fair comparison, as the empirical setting provided in this paper does not capture adaptive pacing’s ability to react to fundamental marketplace changes. However, in practice it is not clear that this ability is always a net positive. In particular, it is shown in Figure 2 that there are strong seasonal effects throughout the week, where obtaining clicks is cheaper on certain days or during certain times of the day. Because adaptive pacing will smooth the expenditure path over time, this would lead to over/underspending on certain days of the week and also certain hours of the day, when compared to the offline optimum (see Section 2.2). While it has been shown that adaptive pacing can recover a constant competitive ratio in this setting, the competitive ratio is unknown, and the losses could potentially be significant (Balseiro and Gur 2017). In contrast, the algorithm from Example 1 can be trained to avoid these problems.

4 Conclusions

In this paper we studied strategies for real-time bidding on Internet advertising exchanges, under the second-price auction format. In particular, we showed a strong connection between selection algorithms for the online knapsack problem with known prices and bidding algorithms for the second-price knapsack problem with unknown prices. This connection has not been leveraged before, and our results yield competitive and readily implementable algorithms for advertising companies.

To establish these results, we first built an intuition for the connection, by analyzing the offline problem and showing near-optimality of a linear bidding strategy, because of the second-price auction format: in fact the ads recovered are exactly the ones with a value-to-price ratio above some threshold. We then established two specific methods for taking primal and dual online knapsack algorithms, which select ads based on their value and posted price, and turning them into bidding strategies for the second-price knapsack problem, where we do not have a priori knowledge of the other bids (and therefore prices). We give two examples of online knapsack algorithms, adapted to the second-price knapsack setting. In particular, we showed how with an online one-shot learning algorithm, we could use a linear form of bidding to recover a bundle of ads with competitive ratio , where could be small given the context.

Evaluating the adapted algorithm from Example 1 on the iPinYou dataset, we showed that we can recover something close to the optimal bundle of ads as expected, giving empirical support to the findings. In particular, for bidders that are more selective, and only have the budget to purchase of the ads they are interested in, we show that our methods can significantly outperform adaptive pacing, raising the total value of ads purchased by an average of 25.9%.

While this is not a perfect comparison, as the empirical setting provided in this paper does not capture adaptive pacing’s ability to react to fundamental marketplace changes, it was argued in Section 3 that this is not always a positive. In particular, there are predictable variations in the value of ads throughout the week, where getting clicks is cheaper during certain days of the week and certain hours of the day. However, adaptive pacing will balance its expenditure rate across all these fluctuations, causing it to either underspend or overspend at certain times. In contrast, the algorithm from Example 1 can be trained to avoid this pitfall.

Therefore the trade-offs in practice, between the work in this paper and adaptive pacing, can be summarized as follows: adaptive pacing requires very little management, but will have some undetermined losses due to predictable seasonal variations, while the online algorithms from Section 2.3 can avoid these problems, but must be regularly monitored (and potentially retrained) due to fundamental changes in the marketplace such as changes in competitor behavior. This suggests there might be some instances in practice, where advertisers would prefer the algorithms provided in this paper.

This also suggests there is further room for the development of new algorithms, that combine the best aspects from each of these: being robust to predictable seasonal variations in the attractiveness of ads (over the course of the week), while still being able to adapt to long-term underlying changes in the marketplace.

Acknowledgement

The authors would like to thank Haihao Lu. The paper evolved from a Spring 2017 course project at MIT involving him and the authors, that used the iPinYou dataset to evaluate bidding strategies from a literature review of existing work. Haihao also provided thoughtful feedback on the final version of the paper.

References

- Agrawal and Devanur (2015) Shipra Agrawal and Nikhil R Devanur. Fast algorithms for online stochastic convex programming. In Proceedings of the Twenty-Sixth Annual ACM-SIAM Symposium on Discrete Algorithms, pages 1405–1424. Society for Industrial and Applied Mathematics, 2015.

- Agrawal et al. (2014) Shipra Agrawal, Zizhuo Wang, and Yinyu Ye. A dynamic near-optimal algorithm for online linear programming. Operations Research, 62(4):876–890, 2014.

- Babaioff et al. (2008) Moshe Babaioff, Nicole Immorlica, David Kempe, and Robert Kleinberg. Online auctions and generalized secretary problems. ACM SIGecom Exchanges, 7(2):7, 2008.

- Badanidyuru et al. (2018) Ashwinkumar Badanidyuru, Robert Kleinberg, and Aleksanders Slivkins. Bandits with knapsacks. Journal of the ACM, 65, 2018.

- Balseiro and Gur (2017) Santiago Balseiro and Yonatan Gur. Learning in repeated auctions with budgets: Regret minimization and equilibrium. 2017.

- Bertsekas (1995) Dimitri P Bertsekas. Dynamic programming and optimal control. Athena scientific Belmont, MA, 1995.

- Buchbinder and Naor (2005) Niv Buchbinder and Joseph Naor. Online primal-dual algorithms for covering and packing problems. In ESA, volume 3669, pages 689–701. Springer, 2005.

- Buchbinder and Naor (2006) Niv Buchbinder and Joseph Naor. Improved bounds for online routing and packing via a primal-dual approach. In Foundations of Computer Science, 2006. FOCS’06. 47th Annual IEEE Symposium on, pages 293–304. IEEE, 2006.

- Buchbinder et al. (2009) Niv Buchbinder, Joseph Seffi Naor, et al. The design of competitive online algorithms via a primal–dual approach. Foundations and Trends® in Theoretical Computer Science, 3(2–3):93–263, 2009.

- Chakrabarty et al. (2007) Deeparnab Chakrabarty, Yunhong Zhou, and Rajan Lukose. Budget constrained bidding in keyword auctions and online knapsack problems. In Workshop on Sponsored Search Auctions. WWW, 2007.

- Chen et al. (2011) Ye Chen, Pavel Berkhin, Bo Anderson, and Nikhil R Devanur. Real-time bidding algorithms for performance-based display ad allocation. In Proceedings of the 17th ACM SIGKDD international conference on Knowledge discovery and data mining, pages 1307–1315. ACM, 2011.

- Conitzer et al. (2019) Vincent Conitzer, Christian Kroer, Eric Sodomka, and Nicolas Stier-Moses. Multiplicative pacing equilibria in auction markets. Working Paper, 2019.

- Devanur and Hayes (2009) Nikhil R Devanur and Thomas P Hayes. The adwords problem: online keyword matching with budgeted bidders under random permutations. In Proceedings of the 10th ACM conference on Electronic commerce, pages 71–78. ACM, 2009.

- Edelman and Ostrovsky (2007) Benjamin Edelman and Michael Ostrovsky. Strategic bidder behavior in sponsored search auctions. Decision support systems, 43(1):192–198, 2007.

- Feldman et al. (2010) Jon Feldman, Monika Henzinger, Nitish Korula, Vahab Mirrokni, and Cliff Stein. Online stochastic packing applied to display ad allocation. Algorithms–ESA 2010, pages 182–194, 2010.

- Fisher (1981) Marshall L Fisher. The lagrangian relaxation method for solving integer programming problems. Management science, 27(1):1–18, 1981.

- Jiang et al. (2014) Chong Jiang, Carolyn L. Beck, and R. Srikant. Bidding with limited statistical knowledge in online auctions. ACM SIGMETRICS Performance Evaluation Review, 41, 2014.

- Kellerer et al. (2004) Hans Kellerer, Ulrich Pferschy, and David Pisinger. Introduction to np-completeness of knapsack problems. In Knapsack problems, pages 483–493. Springer, 2004.

- Kesselheim et al. (2014) Thomas Kesselheim, Andreas Tönnis, Klaus Radke, and Berthold Vöcking. Primal beats dual on online packing lps in the random-order model. In Proceedings of the forty-sixth annual ACM symposium on Theory of computing, pages 303–312. STOC, 2014.

- Kleywegt and Papastavrou (1998) Anton J Kleywegt and Jason D Papastavrou. The dynamic and stochastic knapsack problem. Operations Research, 46(1):17–35, 1998.

- Lee et al. (2012) Kuang-chih Lee, Burkay Birant Orten, Ali Dasdan, and Wentong Li. Estimating conversion rate in display advertising from past performance data, August 13 2012. US Patent App. 13/584,545.

- Lee et al. (2013) Kuang-Chih Lee, Ali Jalali, and Ali Dasdan. Real time bid optimization with smooth budget delivery in online advertising. In Proceedings of the Seventh International Workshop on Data Mining for Online Advertising, page 1. ACM, 2013.

- Lueker (1998) George S Lueker. Average-case analysis of off-line and on-line knapsack problems. Journal of Algorithms, 29(2):277–305, 1998.

- Marchetti-Spaccamela and Vercellis (1995) Alberto Marchetti-Spaccamela and Carlo Vercellis. Stochastic on-line knapsack problems. Mathematical Programming, 68(1-3):73–104, 1995.

- Noga and Sarbua (2005) John Noga and Veerawan Sarbua. An online partially fractional knapsack problem. In Parallel Architectures, Algorithms and Networks, 2005. ISPAN 2005. Proceedings. 8th International Symposium on, pages 5–pp. IEEE, 2005.

- Ren et al. (2018) Kan Ren, Weinan Zhang, Ke Chang, Yifei Rong, Yong Yu, and Jun Wang. Bidding machine: Learning to bid for directly optimizing profits in display advertising. IEEE Transactions on Knowledge and Data Engineering, 30(4):645–659, 2018.

- Williamson (1992) Elizabeth Louise Williamson. Airline network seat inventory control: Methodologies and revenue impacts. PhD thesis, Massachusetts Institute of Technology, 1992.

- Yuan et al. (2013) Shuai Yuan, Jun Wang, and Xiaoxue Zhao. Real-time bidding for online advertising: measurement and analysis. In Proceedings of the Seventh International Workshop on Data Mining for Online Advertising, page 3. ACM, 2013.

- Zhang et al. (2014) Weinan Zhang, Shuai Yuan, Jun Wang, and Xuehua Shen. Real-time bidding benchmarking with ipinyou dataset. arXiv preprint arXiv:1407.7073, 2014.

- Zhou and Lukose (2007) Yunhong Zhou and Rajan Lukose. Vindictive bidding in keyword auctions. In Proceedings of the ninth international conference on Electronic commerce, pages 141–146. ACM, 2007.

- Zhou and Naroditskiy (2008) Yunhong Zhou and Victor Naroditskiy. Algorithm for stochastic multiple-choice knapsack problem and application to keywords bidding. In Proceedings of the 17th international conference on World Wide Web, pages 1175–1176. ACM, 2008.

Appendix A Proof of Proposition 1

In this section we provide a proof of Proposition 1. First we introduce some necessary Lemmas, and provide the proof of the Proposition at the end of the section.

Consider (K-LP). As we are trying to minimize a convex piecewise linear function, the optimal value is interpretable as the value-to-price ratio threshold , above which we will select an ad. We provide the following known optimality lemma, similar to Fisher [1981].

Lemma 2.

Consider the offline knapsack problem (K) and its linear programming relaxation (K-LP). Let denote the value and the paying price of advertisement . There exists some constant such that we can recover an optimal solution to formulation (K-LP) using a fractional selection policy such that

and for the ads with .

Proof.

The proof relies on complementary slackness. Let denote the optimal solution to the (K-LP), and let and the optimal solution to its dual formulation (K-Dual) (these exist by clearly evident strong duality). The following complementary slackness condition entails the described selection policy:

-

1.

If . Since , it follows that from the feasibility conditions for (4). From the second complementary slackness condition we have so we fully purchase the ad.

-

2.

If . From the structure of (4) we see that we minimize each choice of subject to and . If then it follows that we have and . From the first complementary slackness condition it follows that i.e. we do not purchase the ad.

-

3.

Otherwise , we purchase some fraction, spending down the remaining budget.

∎

To prove near-optimality of selecting all ads strictly above this value-to-price threshold, we use Assumption 1.

Let us consider the formulations (K) and (K-LP), let us denote the offline dual threshold as and the optimal solution to (K-LP) as . From Lemma 2, for the ads where we have , and for the ads where we have . Finally by the uniqueness assumption, we have a single ad indexed by with and , . Define the functions and as the optimal objective values for (K-LP) and (K) with budget B. We derive the following lemma which guarantees the near-optimality of our strategy:

Lemma 3.

Proof.

We notice that when our budget is rather than for (K-LP), then the optimal solution from Lemma 2 is an integer solution, and thus also optimal for the corresponding integer program. We find a similar result for a budget of as well. Combining these results we have:

| (3) |

Then, since feasibility of a solution stays ensured when provided with a larger budget, we get the inequalities:

| (4) |

We then simplify this inequality to the Lemma’s result. ∎

When we combine this with Assumption 2, which states that the value of each ad is small relative to the total value of the optimal bundle (which holds for the context of RTB), we are near-optimal.

So far these results, conditioned on us knowing the paying-price of an ad, are known results for the offline knapsack algorithm. Notably, our selection criteria involves knowledge of the paying price , which we can not use in a bidding strategy for the second-price knapsack problem (as will not be known a priori). The following lemma bridges that gap. This lemma is a known result, that has been used in several other papers [e.g., Zhou and Naroditskiy, 2008].

Lemma 4 (Scaled linear bid).

For any set of ads with values and paying prices , and for any constant , let be the linear bidding strategy in the online setting which bids for every impression the amount

Then exactly recovers the ads where under the second-price auction mechanism.

Proof.

Let us consider the linear form of bidding with parameter , where we bid the amount for ad . The auction is won if and only if the paying price is lower than the bid, i.e. .

Therefore because of the second price auction format we find that a linear form of bidding wins the exact set of ads as the dual threshold strategy, and pays the same price.

∎

These Lemmas provide the pieces for the formal proof of Proposition 1.

Proof.

Proof of Proposition 1

Consider the (K) and (K-LP) formulations from section 2.2 and the subsequent notations. With lemma 3, we know that the total value we can obtain from is bounded by the value of the linear relaxation with corrected budget and value, i.e. by .

Using lemma 4, we could recover the same set of ads as in the linear relaxation by using a scaled linear bid with parameter for the online problem (2.1). Therefore by using this strategy, we are within of the optimal bidding strategy with budget , i.e. the value . This concludes the proof..bib

∎