Term structure modeling for multiple curves

with stochastic discontinuities

Abstract.

We develop a general term structure framework taking stochastic discontinuities explicitly into account. Stochastic discontinuities are a key feature in interest rate markets, as for example the jumps of the term structures in correspondence to monetary policy meetings of the ECB show. We provide a general analysis of multiple curve markets under minimal assumptions in an extended HJM framework and provide a fundamental theorem of asset pricing based on NAFLVR. The approach with stochastic discontinuities permits to embed market models directly, unifying seemingly different modeling philosophies. We also develop a tractable class of models, based on affine semimartingales, going beyond the requirement of stochastic continuity.

Key words and phrases:

HJM model, semimartingale, affine process, NAFLVR, large financial market, multiple yield curves, stochastic discontinuities, forward rate agreement, market models, Libor rate2010 Mathematics Subject Classification:

60G44, 60G48, 60G57, 91B70, 91G20, 91G30.JEL classification: C02, C60, E43, G12.

1. Introduction

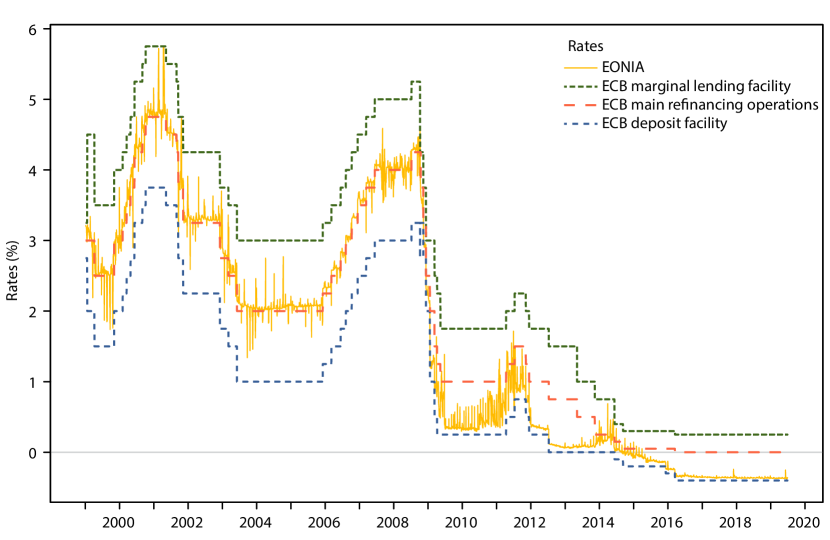

This work aims at providing a general analysis of interest rate markets in the post-crisis environment. These markets exhibit two key characteristics. The first one is the presence of stochastic discontinuities, meaning jumps occurring at predetermined dates. Indeed, a view on historical data of European reference interest rates (see Figure 1) shows surprisingly regular jumps: many of the jumps occur in correspondence of monetary policy meetings of the European Central Bank (ECB), and the latter take place at pre-scheduled dates. This important feature, present in interest rate markets even before the crisis, has been surprisingly neglected by existing stochastic models.

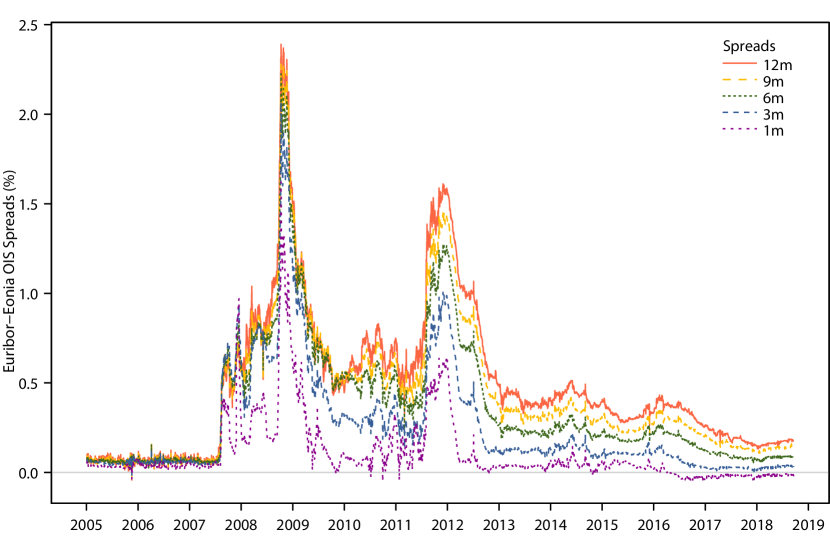

The second key characteristic is the co-existence of different yield curves associated to different tenors. This phenomenon originated with the 2007 – 2009 financial crisis, when the spreads between different yield curves reached their peak beyond 200 basis points. Since then the spreads have remained on a non-negligible level, as shown in Figure 2. This was accompanied by a rapid development of interest rate models, treating multiple yield curves at different levels of generality and following different modeling paradigms. The most important curves to be considered in the current economic environment are the overnight indexed swap (OIS) rates and the interbank offered rates (abbreviated as Ibor, such as Libor rates from the London interbank market) of various tenors. In the European market these are respectively the Eonia-based OIS rates and the Euribor rates.

It is our aim to propose a general treatment of markets with multiple yield curves in the light of stochastic discontinuities, meanwhile unifying the existing multiple curve modeling approaches. The building blocks of this study are OIS zero-coupon bonds and forward rate agreements (FRAs), which constitute the basic traded assets of a multiple curve financial market. While OIS bonds are bonds bootstrapped from quoted OIS rates, a FRA is an over-the-counter derivative consisting of an exchange of a payment based on a floating rate against a payment based on a fixed rate. FRAs can be regarded as the fundamental components of all interest rate derivatives written on Ibor rates.

The main contributions of the present paper can be outlined as follows:

-

•

A general forward rate setup for the term structure of FRAs and OIS bond prices inspired by the seminal Heath-Jarrow-Morton (HJM) approach of Heath et al. (1992), suitably extended to allow for stochastic discontinuities. We derive a set of necessary and sufficient conditions characterizing risk-neutral measures with respect to a general numéraire process (Theorem 3.7). This framework unifies and generalizes the existing approaches in the literature.

-

•

We study market models in general and, on the basis of minimal assumptions, derive necessary and sufficient drift conditions in the presence of stochastic discontinuities (Theorem 4.1). This approach covers modeling under forward measures as a special case. Moreover, the generality of our forward rate formulation with stochastic discontinuities enables us to directly embed market models.

-

•

We propose a new class of model specifications, based on affine semimartingales as recently introduced in Keller-Ressel et al. (2018), going beyond the classical requirement of stochastic continuity. We illustrate the potential for practical applications by means of some simple examples.

-

•

Finally, we provide a general description of a multiple curve financial market under minimal assumptions and a characterization of absence of arbitrage. We prove the equivalence between the notion of no asymptotic free lunch with vanishing risk (NAFLVR) and the existence of an equivalent separating measure (Theorem 6.3). To this effect, we rely on the theory of large financial markets and we extend to multiple curves and to an infinite time horizon the main result of Cuchiero, Klein and Teichmann (2016). To the best of our knowledge, this represents the first rigorous formulation of an FTAP in the context of multiple curve financial markets.

1.1. The modeling framework

We briefly illustrate the ingredients of our modeling framework, referring to the sections in the sequel for full details. First, forward rate agreements (FRAs) are quoted in terms of forward rates. More precisely, the forward Ibor rate at time with tenor and settlement date is given as the unique value of the fixed rate which assigns the FRA value zero at inception . This leads to the fundamental representation of FRA prices

| (1.1) |

where is the price at time of an OIS zero-coupon bond with maturity and is a fixed rate. Formula (1.1) implicitly defines the yield curves for different tenors , thus explaining the terminology multiple yield curves. In the following, we will simply call the associated markets multiple curve financial markets (compare with Definition 2.2 below).

The forward rate formulation makes some additional assumptions on the yield curves. More specifically, it postulates that the right-hand side of (1.1) admits the representation

| (1.2) |

Here, denotes the OIS forward rate, so that , while is the -tenor forward rate and is a multiplicative spread. We extend the usual HJM formulation by considering a measure containing atoms which by no-arbitrage will be precisely related to the set of stochastic discontinuities in the dynamics of forward rates and multiplicative spreads.

Representations (1.1) and (1.2) constitute two seemingly different starting points for multiple curve modeling: market models and HJM models, respectively. In the following, we shall derive no-arbitrage drift restrictions for both classes. Moreover, we will show that the two classes can be analyzed in a unified setting (see Appendix B).

1.2. Stochastic discontinuities in interest rate markets

One of the main novelties of our approach consists in the presence of stochastic discontinuities, representing events occurring at announced dates but with a possibly unanticipated informational content. The importance of jumps at predetermined times is widely acknowledged in the financial literature, see for example Merton (1974), Piazzesi (2001, 2005, 2010), Kim and Wright (2014), Duffie and Lando (2001) (see also the introductory section of Keller-Ressel et al. (2018)). However, to the best of our knowledge, stochastic discontinuities have never been taken explicitly into account in stochastic models for the term structure of interest rates. This feature is extremely relevant in financial markets. For instance, the Governing Council (GC) of the European Central Bank (ECB) holds its monetary policy meetings on a regular basis at predetermined dates, which are publicly known for about two years ahead. At such dates the GC takes its monetary policy decisions and determines whether the main ECB interest rates will change. In turn, these key interest rates are principal determinants of the Eonia rate, as illustrated by Figure 1.

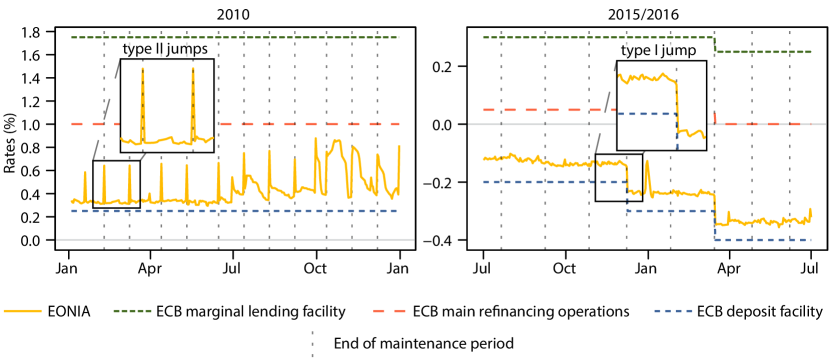

A closer inspection of Figure 1 reveals the presence of two different types of stochastic discontinuities in the Eonia rate. On the one hand, there are structural jumps in correspondence to monetary policy decisions. This type of discontinuity is evidenced by a step-like jump of the Eonia rate in correspondence to a new level of the ECB lending rate (see Figure 3, right panel). On the other hand, there are spiky jumps which are unrelated to the monetary policy and occur at the end of the maintenance periods of banks’ deposits. Indeed, in the Eurosystem banks are required to hold deposits on accounts with their national central bank over fixed maintenance periods. Banks who fail to keep sufficient reserves during the period need to borrow in the interbank market before the close of the maintenance period, thereby generating a temporary liquidity pressure in interbank lending which leads to a jump in the Eonia rate (see e.g. Beirne (2012) and Hernandis and Torró (2013)). This second type of stochastic discontinuity is evidenced by the spikes in the left panel of Figure 3. More formally, we distinguish these two kinds of stochastic discontinuities as follows: jumps of type I are step-like jumps to a new level and jumps of type II are upward/downward jumps followed by a fast continuous decay/ascent to the pre-jump level.

Our framework allows for the possibility of both type I and type II stochastic discontinuities. In addition, by relaxing the classical assumption that the term structure of bond prices is absolutely continuous (see equation (1.2)), we also allow for discontinuities in time-to-maturity at predetermined dates. In a credit risky setting, term structures with stochastic discontinuities have been recently studied in Gehmlich and Schmidt (2018) and Fontana and Schmidt (2018). Finally, besides stochastic discontinuities as described above, we also allow for totally inaccessible jumps, representing events occurring as a surprise to the market and generated by a general random measure with absolutely continuous compensator. Such jumps have been already considered in several multiple curve models (see e.g. Crépey et al. (2012) and Cuchiero, Fontana and Gnoatto (2016)).

1.3. Overview of the literature

The literature on multiple curve models has witnessed a tremendous growth over the last years. Therefore, we only give an overview of the contributions that are the most related to the present paper, referring to the volume of Bianchetti and Morini (2013) and the monographs by Henrard (2014) and Grbac and Runggaldier (2015) for further references and a guide to post-crisis interest rate markets. Multiplicative spreads for modeling multiple curves have been first considered in Henrard (2007). Adopting a short rate approach, an insightful empirical analysis has been conducted by Filipović and Trolle (2013), showing that spreads can be decomposed into credit and liquidity components. The extended HJM approach developed in Section 3 generalizes the framework of Cuchiero, Fontana and Gnoatto (2016), who consider Itô semimartingales as driving processes and, therefore, do not allow for stochastic discontinuities (see Remark 3.12 for a detailed comparison). HJM models taking into account multiple curves have been proposed in Crépey et al. (2015) with Lévy processes as drivers and in Moreni and Pallavicini (2014) in a Gaussian framework. In the market model setup, the extension to multiple curves was pioneered by Mercurio (2010) and further developed in Mercurio and Xie (2012). More recently, Grbac et al. (2015) have developed an affine market model in a forward rate setting, further generalized by Cuchiero et al. (2019). All these models, both HJM and market models, can be easily embedded in the general framework proposed in this paper.

1.4. Outline of the paper

In Section 2, we introduce the basic assets in a multiple curve financial market. The general multi-curve framework inspired by the HJM philosophy, extended to allow for stochastic discontinuities, is developed and fully characterized in Section 3. In Section 4, we introduce and analyze general market models with multiple curves. In Section 5, we propose a flexible class of models based on affine semimartingales, in a setup which allows for stochastic discontinuities. In Section 6, we prove a version of the fundamental theorem of asset pricing for multiple curve financial markets, by relying on the theory of large financial markets. Finally, the two appendices contain some technical results and a result on the embedding of market models into the extended HJM framework.

2. A general analysis of multiple curve financial markets

In this section, we provide a general description of a multiple curve market under minimal assumptions. We assume that the interbank offered rates (Ibor) are quoted for a finite set of tenors , with . Typically, about seven tenors, ranging from 1 day to 12 months, are available in the market. For a tenor , the Ibor rate for the time interval fixed at time is denoted by . For , we denote by the price at date of an OIS zero-coupon bond with maturity .

Definition 2.1.

A forward rate agreement (FRA) with tenor , settlement date , strike and unitary notional amount, is a contract in which a payment based on the Ibor rate is exchanged against a payment based on the fixed rate at maturity . The price of a FRA contract at date is denoted by and the payoff at maturity is given by

| (2.1) |

The two addends in (2.1) are typically referred to as floating leg and fixed leg, respectively. We define the multiple curve financial market as follows.

Definition 2.2.

The multiple curve financial market is the financial market containing the following two sets of traded assets:

-

(i)

OIS zero-coupon bonds, for all maturities ;

-

(ii)

FRAs, for all tenors , all settlement dates and all strikes .

The assets included in Definition 2.2 represent the quantities that we assume to be tradable in the financial market. We emphasize that, in the post-crisis environment, FRA contracts have to be considered on top of OIS bonds as they cannot be perfectly replicated by the latter, due to the risks implicit in interbank transactions.

We work under the standing assumption that FRA prices are determined by a linear valuation functional. This assumption is standard in interest rate modeling and is also coherent with the fact that we consider clean prices, i.e., prices which do not model explicitly counterparty and liquidity risk (the counterparty and liquidity risk of the interbank market as a whole is of course present in Ibor rates, recall Figure 2). Clean prices are fundamental quantities in interest rate derivative valuation and they also form the basis for the computation of XVA adjustments, see Section 1.2.3 in Grbac and Runggaldier (2015) and Brigo et al. (2018).

Recalling (2.1), the value of the fixed leg of a FRA at time is given by . Hence, we obtain that is an affine function of .

Definition 2.3.

The forward Ibor rate at for tenor and maturity is the unique value satisfying .

Due to the affine property of FRA prices combined with the above definition, the fundamental representation

follows immediately for , while for we have of course

Starting from this expression, under no additional assumptions, we can decompose the value of the floating leg of the FRA into a multiplicative spread and a tenor-dependent discount factor. Indeed, setting , we can write

| (2.2) |

where represents a multiplicative spread and a discount factor satisfying , for all and . More precisely, it holds that

where denotes the simply compounded OIS rate at date for the period . The discount factor is therefore given by

We shall sometimes refer to as -tenor bonds. These bonds essentially span the term structure, while accounts for the counterparty and liquidity risks in the interbank market, which do not vanish as .

Remark 2.4.

In the classical pre-crisis single curve setup, the FRA price is given by the textbook formula

The single curve setting can be recovered from our approach by setting and , for all and . This also highlights that, in a single curve setup, FRA prices are fully determined by OIS bond prices.

Remark 2.5.

Representation (2.2) allows for a natural interpretation via a foreign exchange analogy, following some ideas going back to Bianchetti (2010). Indeed, Ibor rates can be thought of as simply compounded rates in a foreign economy, with the currency risk playing the role of the counterparty and liquidity risks of interbank transactions. In this perspective, represents the price at date (in units of the foreign currency) of a foreign zero-coupon bond with maturity , while represents the spot exchange rate between the foreign and the domestic currencies. The quantity appearing in (2.2) corresponds to the value at date (in units of the domestic currency) of a payment of one unit of the foreign currency at maturity . In view of Remark 2.4, the pre-crisis scenario assumes the absence of currency risk, in which case . Related foreign exchange interpretations of multiplicative spreads have been discussed in Cuchiero, Fontana and Gnoatto (2016), Macrina and Mahomed (2018) and Nguyen and Seifried (2015).

With the additional assumption that OIS and -tenor bond prices are of HJM form, we obtain our second fundamental representation (1.2). In the following, we will show that such a representation allows for a precise characterization of arbitrage-free multiple curve markets and leads to interesting specifications by means of affine semimartingales.

3. An extended HJM approach to term structure modeling

In this section, we present a general framework for modeling the term structures of OIS bonds and FRA contracts, inspired by the seminal work by Heath et al. (1992). We work in an infinite time horizon (models with a finite time horizon can be treated by stopping the relevant processes at ). As mentioned in the introduction, a key feature of the proposed framework is that we allow for the presence of stochastic discontinuities, occurring in correspondence of a countable set of predetermined dates , with , for every , and .

We assume that the stochastic basis supports a -dimensional Brownian motion together with an integer-valued random measure on , with compensator , where is a kernel from into , with denoting the predictable sigma-field on and a Polish space with its Borel sigma-field. We refer to Jacod and Shiryaev (2003) for all unexplained notions related to stochastic calculus.

As a first ingredient, we assume the existence of a general numéraire process , given by a strictly positive semimartingale admitting the representation

| (3.1) |

where is an -valued progressively measurable process so that a.s. for all and is a -measurable function satisfying a.s. for all . Note that, in view of (Jacod and Shiryaev, 2003, Theorem II.1.33), the last condition is necessary and sufficient for the well-posedness of the stochastic integral . The process is assumed to be a finite variation process of the form

| (3.2) |

where is an adapted process satisfying a.s. for all and is an -measurable random variable taking values in , for each . Note that this specification of explicitly allows for jumps at times , the stochastic discontinuity points of . The assumption that ensures that the summation in (3.2) involves only a finite number of terms, for every .

Remark 3.1.

Requiring minimal assumptions on enables us to unify different modeling approaches. Usually, it is postulated that , with representing the OIS short rate. In the setting considered here, can also be generated by a sequence of OIS bonds rolled over at dates , compare (Klein et al., 2016, Definition 5) for a precise notion. This allows to avoid the unnecessary assumption of existence of a bank account. In market models, the usual choice for is the OIS-bond with the longest available maturity, see Remark 4.2. Moreover, it is also possible to choose as the physical probability measure and as the growth-optimal portfolio. By this, we cover the benchmark approach to term structure modeling (see Bruti-Liberati et al. (2010) and Platen and Heath (2006)). While these examples refer to situations where the numéraire is tradable, we do not necessarily assume that represents the price process of a traded asset or portfolio (with the exception of Section 6). This generality yields additional flexibility, since may also represent a state-price density or pricing kernel in the spirit of Constantinides (1992), embedding a choice of the discounting asset and a probability change into a single process (compare also with Remark 3.11). As explained below, the focus of Sections 3–5 will be on deriving necessary and sufficient conditions for the local martingale property of -denominated prices under .

The reference probability measure is said to be a risk-neutral measure for the multiple curve financial market with respect to if the -denominated price process of every asset included in Definition 2.2 is a -local martingale. One of our main goals consists in deriving necessary and sufficient conditions for to be a risk-neutral measure. In Section 6, under the additional assumption that the numéraire is tradable, we will prove a fundamental theorem characterizing absence of arbitrage in the sense of NAFLVR, for which the existence of a risk-neutral measure is a sufficient condition (see Remark 6.4).

In view of representation (2.2), modeling a multiple curve financial market requires the specification of multiplicative spreads and -tenor bond prices, for . The multiplicative spread process is assumed to be a strictly positive semimartingale, for each . Similarly as in (3.1), we assume that admits the representation

| (3.3) |

for every , where , and satisfy the same requirements of the processes , and , respectively, appearing in (3.1). In line with (3.2), we furthermore assume that

| (3.4) |

where is an adapted process satisfying a.s., for all and , and is an -measurable random variable taking values in , for each and .

We let , for all . We assume that, for every and , the -tenor bond price process is of the form

| (3.5) |

where

| (3.6) |

Note that , for all . We adopt the convention , for all and . For every and , we assume that the forward rate process satisfies

| (3.7) |

for all , where is a pure jump adapted process of the form

with for all . Moreover, for all , and , we also assume that .

Remark 3.2.

-

(1)

The above framework allows for a general modeling of type I and type II stochastic discontinuities (see Section 1.2), as we illustrate by means of explicit examples in Section 5. Moreover, the dependence on in equations (3.3)–(3) allows the discontinuities to have a different impact on different yield curves. This is consistent with the typical market behavior, which shows a dampening of the discontinuities over longer tenors.

-

(2)

The discontinuity dates play two distinct but equally important roles. On the one hand, they represent stochastic discontinuities in the dynamics of all relevant processes. On the other hand, they represent discontinuity points in maturity of bond prices (see equation (3.5)). As shown in Theorem 3.7 below, absence of arbitrage will imply a precise relation between these two aspects.

Assumption 3.3.

The following conditions hold a.s. for every :

-

(i)

the initial forward curve is -measurable, real-valued and satisfies , for all ;

-

(ii)

the drift process is a real-valued, progressively measurable process, in the sense that the restriction

is -measurable, for every . Moreover, it satisfies for all that , and

-

(iii)

the volatility process is an -valued progressively measurable process, in the sense that the restriction

is -measurable, for every . Moreover, it satisfies for all that , and

-

(iv)

the jump function is a -measurable real-valued function satisfying for all and . Moreover, it satisfies

Assumption 3.3 implies that the integrals appearing in the forward rate equation (3) are well-defined for -a.e. . Moreover, the integrability requirements appearing in conditions (ii)–(iv) of Assumption 3.3 ensure that we can apply ordinary and stochastic Fubini theorems, in the versions of Veraar (2012) for the Brownian motion and Proposition A.2 in Björk et al. (1997) for the compensated random measure. The mild measurability requirement in conditions (ii)–(iii) holds if and are -measurable, for every , with denoting the progressive sigma-algebra on , see (Veraar, 2012, Remark 2.1).

Remark 3.4.

There is no loss of generality in taking a single measure instead of different measures for each tenor . Indeed, dependence on the tenor can be embedded in our framework by suitably specifying each forward rate in (3) and using a common measure .

For all , and , we set

As a first result, the following lemma (whose proof is postponed to Appendix A) gives a semimartingale representation of the process .

Lemma 3.5.

Suppose that Assumption 3.3 holds. Then, for every and , the process is a semimartingale and admits the representation

| (3.8) |

The -tenor bond price process admits an equivalent representation as a stochastic exponential, which will be used in the following. The following corollary is a direct consequence of Lemma 3.5 and (Jacod and Shiryaev, 2003, Theorem II.8.10), using the fact that a.s., for all .

Corollary 3.6.

Suppose that Assumption 3.3 holds. Then, for every and , the process admits the representation

We are now in a position to state the central result of this section, which provides necessary and sufficient conditions for the reference probability measure to be a risk-neutral measure with respect to the numéraire . We recall that a random variable on is said to be sigma-integrable with respect to a sigma-field if there exists a sequence of measurable sets increasing to such that for every , see Definition 1.15 in He et al. (1992). A random variable is sigma-finite with respect to if and only if the generalized conditional expectation is a.s. finite. For convenience of notation, let , , and for all , and , so that . Let

Theorem 3.7.

Suppose that Assumption 3.3 holds. Then is a risk-neutral measure with respect to if and only if, for every ,

| (3.9) |

a.s. for every and, for every and , the random variable

| (3.10) |

is sigma-integrable with respect to , and the following four conditions hold a.s.:

-

(i)

for a.e. , it holds that

-

(ii)

for every and for a.e. , it holds that

-

(iii)

for every , it holds that

-

(iv)

for every and , it holds that

Remark 3.8.

By considering separately the cases and , we can obtain a more explicit version of condition (i) of Theorem 3.7, which is equivalent to the validity of the two conditions, for every and a.e. ,

| (3.11) | ||||

| (3.12) |

The conditions of Theorem 3.7 together with Remark 3.8 admit the following interpretation. First, for condition (i) requires that the drift rate of the numéraire process equals the short end of the instantaneous yield on OIS bonds, plus two additional terms accounting for the volatility of itself.111Note that, at the present level of generality, the rate does not represent a riskless rate of return. For , condition (i) requires that, at the short end, the instantaneous yield on the floating leg of a FRA equals the instantaneous yield plus a risk premium determined by the covariation between the numéraire process and the multiplicative spread process .

Second, condition (ii) is a generalization of the well-known HJM drift condition. In particular, if and the process does not have local martingale components, then condition (ii) reduces to the drift restriction established in Proposition 5.3 of Björk et al. (1997) for single-curve jump-diffusion models.

Finally, conditions (iii) and (iv) are new and specific to our setting with stochastic discontinuities. Together, they correspond to excluding the possibility that, at some predetermined date , prices of -denominated assets exhibit jumps whose size can be predicted on the basis of the information contained in . Indeed, such a possibility would violate absence of arbitrage (compare with Fontana et al. (2019)).

Proof.

of Theorem 3.7 Recall that , . By definition, is a risk-neutral measure with respect to if and only if the processes and are -local martingales, for every , and . In view of (2.2) and using the notational convention introduced above, this holds if and only if the process is a -local martingale, for every and . An application of Corollary A.1 together with Corollary 3.6 and equations (3.1)–(3.4) yields

| (3.13) |

where is an adapted process given by

is a pure jump finite variation process given by

and is a pure jump finite variation process given by

where in the last equality we made use of (3) together with the definition of the process . The process appearing in (3) is the local martingale

Note that the set is evanescent for every and , as a consequence of the fact that a.s. for all .

Suppose that is a -local martingale, for every and . In this case, (3) implies that the finite variation process is also a -local martingale. By means of (Jacod and Shiryaev, 2003, Lemma I.3.11), this implies that the pure jump finite variation process is of locally integrable variation. Since the two processes and do not have common jumps, it holds that

As a consequence of this fact, both processes and are of locally integrable variation. Noting that

Theorem 5.29 of He et al. (1992) implies that the random variable is sigma-integrable with respect to , for every . This is equivalent to the sigma-integrability of

| (3.14) |

with respect to . Since is -measurable, the sigma-integrability of (3.14) with respect to can be equivalently stated as the sigma-integrability of (3.10) with respect to . Moreover, the fact that is of locally integrable variation is equivalent to the a.s. finiteness of the integral

thus proving the integrability conditions (3.9), (3.10). Having established that the two processes and are of locally integrable variation, we can take their compensators (dual predictable projections), see (Jacod and Shiryaev, 2003, Theorem I.3.18). This leads to

| (3.15) |

where

| (3.16) |

is a local martingale, is an adapted process given by

and, in view of (He et al., 1992, Theorem 5.29), is a pure jump finite variation predictable process with

for all . If is a -local martingale, then by equation (3.15) the process must be null (up to an evanescent set), being a predictable local martingale of finite variation, see (Jacod and Shiryaev, 2003, Corollary I.3.16). In particular, analyzing separately its absolutely continuous and discontinuous parts, this holds if and only if outside of a set of -measure zero and a.s. for every . Let us first consider the absolutely continuous part

The integral appearing in the last line is a.s. finite for a.e. as a consequence of (3.9). Taking leads to the requirement

for a.e. , which gives condition (i) in the statement of the theorem. In turn, inserting this last condition into the equation directly leads to condition (ii). Considering then the pure jump part, the condition a.s., for all , leads to

| (3.17) |

a.s. for all . Condition (iii) in the statement of the theorem is obtained by taking , while condition (iv) follows by inserting condition (iii) into (3.17).

Conversely, if the integrability conditions (3.9), (3.10) are satisfied then the finite variation processes and appearing in (3) are of locally integrable variation. One can therefore take their compensators and obtain representation (3.15). It is then easy to verify that, if the four conditions (i)–(iv) hold, then the processes and appearing in (3.15) are null, up to an evanescent set. This proves the local martingale property of , for every and . ∎

Remark 3.9.

The foreign exchange analogy introduced in Remark 2.5 carries over to the conditions established in Theorem 3.7. In particular, in the special case where , for all , it can be easily verified that conditions (i)–(ii) reduce exactly to the HJM conditions established in Koval (2005) in the context of multi-currency HJM semimartingale models.

3.1. The OIS bank account as numéraire

In HJM models, the numéraire is usually chosen as the OIS bank account , with denoting the OIS short rate. In this context, an application of Theorem 3.7 enables us to characterize all equivalent local martingale measures (ELMMs, see Section 6) with respect to the OIS bank account numéraire. To this effect, let be a probability measure on equivalent to and denote by its density process, i.e., , for all . We denote the expectation with respect to by and assume that

| (3.18) |

for an -valued progressively measurable process satisfying the integrability condition a.s. for all , a -measurable function satisfying the integrability condition a.s. for all , and a family of random variables taking values in such that is -measurable and , for all . Denote

Corollary 3.10.

Suppose that Assumption 3.3 holds. Let be a probability measure on equivalent to , with density process given in (3.18). Assume furthermore that a.s. for all . Then, is an ELMM with respect to the numéraire if and only if, for every ,

| (3.19) |

a.s. for every and, for every and , the random variable

is sigma-integrable under with respect to , and the following conditions hold a.s.:

-

(i)

for a.e. , it holds that

-

(ii)

for every and for a.e. , it holds that

-

(iii)

for every , it holds that

-

(iv)

for every and , it holds that

Proof.

By means of Bayes’ formula, is an ELMM if and only if is a local martingale under , for every and . The result therefore follows by applying Theorem 3.7 with respect to . By applying Lemma A.1, we obtain that

Note that a.s., as a consequence of the assumption that a.s. together with the elementary inequality , for . The process is of the form (3.1), (3.2) with

, and . Since

a.s., for all , it can be easily checked that condition (3.19) is equivalent to (3.9). The corollary then follows from Theorem 3.7 noting that, for any -measurable random variable which is sigma-integrable under with respect to , it holds that

where we have used the fact that , for every . ∎

Remark 3.11.

Remark 3.12.

The HJM framework of Cuchiero, Fontana and Gnoatto (2016) can be recovered as a special case with no stochastic discontinuities, setting in (3.6), taking the OIS bank account as numéraire and a jump measure generated by a given Itô semimartingale. Cuchiero, Fontana and Gnoatto (2016) show that most of the existing multiple curve models are covered by their framework, which a fortiori implies that they can be easily embedded in our framework.

4. General market models

In this section, we consider market models and develop a general arbitrage-free framework for modeling Ibor rates. As shown in Appendix B, market models can be embedded into the extended HJM framework considered in Section 3, in the spirit of Brace et al. (1997). This is possible due to the fact that the measure in the term structure equation (3.5) may contain atoms. However, it turns out to be simpler to directly study market models as follows.

In the spirit of market models, and differently from Definition 2.2, in this section we assume that only finitely many assets are traded. For each , let be the set of settlement dates of traded FRA contracts associated to tenor , with and , for . We consider an equidistant tenor structure, i.e. , for all and . Let us also define , corresponding to the set of all traded FRAs. The starting point of our approach is representation (1.1),

| (4.1) |

for , , and . The financial market contains OIS zero-coupon bonds for all maturities 222Note that we need to consider an extended set of maturities for OIS bonds since the payoff of a FRA contract with settlement date and tenor takes place at date . as well as FRA contracts for all , and .

Let be a filtered probability space supporting a -dimensional Brownian motion and a random measure , as described in Section 3. We assume that, for every tenor and maturity , the forward Ibor rate satisfies

| (4.2) |

In the above equation, is a real-valued adapted process satisfying a.s., is a progressively measurable -valued process satisfying the integrability condition a.s., is a family of random variables such that is -measurable, for each , and is a -measurable function that satisfies

The dates represent the stochastic discontinuities occurring in the market. We assume that OIS bond prices are of the form (3.5) for , for all , with the associated forward rates being as in (3).

The main goal of this section consists in deriving necessary and sufficient conditions for a reference probability measure to be a risk-neutral measure with respect to a general numéraire of the form (3.1) for the financial market where FRA contracts and OIS zero-coupon bonds are traded, and FRA prices are modeled via (4.1) and (4.2) for the discrete set of settlement dates. We recall that

Theorem 4.1.

Suppose that Assumption 3.3 holds for and for all maturities . Then is a risk-neutral measure with respect to if and only if all the conditions of Theorem 3.7 are satisfied for and for all , and, for every ,

| (4.3) |

a.s. for all , and, for each and , the random variable

| (4.4) |

is sigma-integrable with respect to , and the following two conditions hold a.s.:

-

(i)

for all and a.e. , it holds that

-

(ii)

for all and , it holds that

Condition (i) of Theorem 4.1 is a drift restriction for the Ibor rate process. In the context of a continuum of traded maturities, as in Theorem 3.7, this condition can be separated into a condition on the short end and an HJM-type drift restriction (see conditions (i) and (ii) in Theorem 3.7). Condition (ii), similarly to conditions (iii), (iv) of Theorem 3.7, corresponds to requiring that, for each , the size of the jumps occurring at date in FRA prices cannot be predicted on the basis of the information contained in .

Proof.

In view of representation (4.1), is a risk-neutral measure with respect to if and only if is a -local martingale, for every , and is a -local martingale, for every and . Considering first the OIS bonds, Theorem 3.7 implies that is a -local martingale, for every , if and only if conditions (3.9), (3.10) as well as conditions (i)–(iv) of Theorem 3.7 are satisfied for and for all . Under these conditions, equation (3.15) for gives that

| (4.5) |

for every , where the local martingale is given by

as follows from equation (3.16), with

By relying on (4.2) and (4.5), we can compute

| (4.6) |

where is a local martingale given by

is an adapted real-valued process given by

is a pure jump finite variation process given by

and is a pure jump finite variation process given by

If is a local martingale, for every and , then (4.6) implies that the processes and are of locally integrable variation. Similarly as in the proof of Theorem 3.7, this implies the validity of conditions (4.3) and (4.4), due to Theorem 5.29 in He et al. (1992). Let us denote by the compensator of , for , and . We have that

The local martingale property of together with equation (4.6) implies that the predictable finite variation process

| (4.7) |

is null (up to an evanescent set), for every and . Considering separately the absolutely continuous and discontinuous parts, this implies the validity of conditions (i), (ii) in the statement of the theorem.

Conversely, by Theorem 3.7, if conditions (3.9), (3.10) as well as conditions (i)–(iv) of Theorem 3.7 are satisfied for and for all , then is a -local martingale, for all . Furthermore, if conditions (4.3), (4.4) are satisfied and conditions (i), (ii) of the theorem hold, then the process given in (4.7) is null. In turn, by equation (4.6), this implies that is a -local martingale, for every and , thus proving that is a risk-neutral measure with respect to . ∎

Remark 4.2.

In market models, the numéraire is usually chosen as the OIS zero-coupon bond with the longest available maturity (terminal bond). In addition, the reference probability measure is the associated -forward measure, see Section 12.4 in Musiela and Rutkowski (1997). Exploiting the generality of the process , this setting can be easily accommodated within our framework. Indeed, if a.s., Corollary 3.6 shows that holds as long as the processes appearing in (3.1) and (3.2) are specified as

Under this specification, a direct application of Theorem 4.1 yields necessary and sufficient conditions for to be a risk-neutral measure with respect to the terminal OIS bond as numéraire.

4.1. Martingale modeling

Typically, market models start directly from the assumption that each Ibor rate is a martingale under the -forward measure associated to the numéraire . In our context, this assumption is generalized into a local martingale requirement under the -forward measure, whenever the latter is well-defined. More specifically, suppose that is a true martingale and define the -forward measure by . As a consequence of Girsanov’s theorem (see (Jacod and Shiryaev, 2003, Theorem III.3.24)) and equation (4.5), the forward Ibor rate satisfies under the measure

| (4.8) |

for some adapted real-valued process , where the process is a -Brownian motion defined by and the compensator of the random measure under is given by

In this context, Theorem 4.1 leads to the following proposition, which provides a characterization of the local martingale property of forward Ibor rates under forward measures.

Proposition 4.3.

Suppose that Assumption 3.3 holds for and for all . Assume furthermore that is a true -martingale, for every . Then the following are equivalent:

-

(i)

is a risk-neutral measure;

-

(ii)

is a local martingale under , for every and ;

-

(iii)

for every and , it holds that

outside a subset of of -measure zero, and, for every and , the random variable satisfies

Proof.

Under these assumptions, is a risk-neutral measure if and only if is a local martingale under , for every and . The equivalence then follows from the conditional version of Bayes’ rule (see (Jacod and Shiryaev, 2003, Proposition III.3.8)), while the equivalence is a direct consequence of equation (4.8) together with (He et al., 1992, Theorem 5.29). ∎

5. Affine specifications

One of the most successful classes of processes in term-structure modeling is the class of affine processes. This class combines a great flexibility in capturing the important features of interest rate markets with a remarkable analytical tractability, see e.g. Duffie and Kan (1996), Duffie et al. (2003), as well as Filipović (2009) for a textbook account. In the literature, affine processes are by definition stochastically continuous and, therefore, do not allow for jumps at predetermined dates. In view of our modeling objectives, we need a suitable generalization of the notion of affine process. To this effect, Keller-Ressel et al. (2018) have recently introduced affine semimartingales by dropping the requirement of stochastic continuity. Related results on affine processes with stochastic discontinuities in credit risk may be found in Gehmlich and Schmidt (2018). In the present section, we aim at showing how the class of affine semimartingales leads to flexible and tractable multiple curve models with stochastic discontinuities.

We consider a countable set of discontinuity dates, with , for every , and . We assume that the filtered probability space supports a -dimensional special semimartingale which is further assumed to be an affine semimartingale in the sense of Keller-Ressel et al. (2018) and to admit the canonical decomposition

where is a finite variation predictable process, is a continuous local martingale with quadratic variation and is the compensated jump measure of . Let be the continuous part of and the continuous part of the random measure , in the sense of (Jacod and Shiryaev, 2003, § II.1.23). In view of (Keller-Ressel et al., 2018, Theorem 3.2), under weak additional assumptions it holds that

| (5.1) | ||||

In (5.1), we have that and , for , and , for . is a Borel measure on for all , such that for all , . Finally, we assume that vanishes a.s. outside the set of stochastic discontinuities .

We use the affine semimartingale as the driving process of a multiple curve model, as presented in Section 3. In particular, we focus here on modeling the -tenor bond prices and the multiplicative spreads in such a way that the resulting model is affine in the sense of the following definition, which extends the approach of (Keller-Ressel et al., 2018, Section 5.3).

Definition 5.1.

The multiple curve model is said to be affine if

| (5.2) | |||||

| (5.3) |

for all , where and are predictable processes such that, for every and ,

and, for all and ,

with denoting the set of -valued predictable processes which are integrable with respect to in the semimartingale sense, and similarly for . The measure is specified as in equation (3.6).

For all and , let us also define

We furthermore assume that a.s., for all , which ensures that is a special semimartingale (see (Jacod and Shiryaev, 2003, Proposition II.8.26)). To complete the specification of the model, we suppose that takes the form

| (5.4) |

where is an adapted real-valued process satisfying a.s., for all , and is a -dimensional -measurable random vector, for all .

We aim at characterizing when is a risk-neutral measure for an affine multiple curve model. By Remark 3.8, we see that a necessary condition is that

| (5.5) |

Under the present assumptions and in the spirit of Theorem 3.7, the following proposition provides sufficient conditions for to be a risk-neutral measure for the affine multiple curve model introduced above. For convenience of notation we let for all and , so that .

Proposition 5.2.

Consider an affine multiple curve model as in Definition 5.1 and satisfying (5.5). Assume furthermore that

| (5.6) |

for every and . Then is a risk-neutral measure with respect to given as in (5.4) if the following three conditions hold a.s. for every :

-

(i)

for a.e. , it holds that

-

(ii)

for every , a.e. and for every , it holds that

(5.7) -

(iii)

for every and , it holds that

Proof.

For all , the present integrability assumptions ensure that and are special semimartingales. Hence, (Jacod and Shiryaev, 2003, Theorem II.8.10) implies that admits a stochastic exponential representation of the form (3.3), (3.4), with

and , for all , where we define the set . Due to (5.4), condition (i) of Theorem 3.7 reduces to , for a.e. and (see also equation (3.12) in Remark 3.8), from which condition (i) directly follows. The integrability conditions appearing in Definition 5.1 enable us to apply the stochastic Fubini theorem in the version of Theorem IV.65 of Protter (2004) and, moreover, ensure that is a special semimartingale, for every and . This permits to obtain a representation of as in Lemma 3.5, namely

In view of the affine structure (5.1) and comparing with (3.5), it holds that

and , for all , and . In the present setting condition (ii) of Theorem 3.7 takes the form

| (5.8) |

Clearly, condition (ii) of the proposition is sufficient for (5) to hold, for every and a.e. . In the present setting, conditions (iii), (iv) of Theorem 3.7 can be together rewritten as follows, for every , and ,

from which condition (iii) of the proposition follows by making use of (5.1). Finally, in the present setting the integrability condition (3.9) appearing in Theorem 3.7 reduces to condition (5.6). In view of Theorem 3.7, we can conclude that is a risk-neutral with respect to . ∎

Remark 5.3.

Condition (ii) is only sufficient for the necessary condition (5). Only if the coordinates of are linearly independent, then this condition is also necessary.

The following examples illustrate the conditions of Proposition 5.2.

Example 5.4 (A single-curve Vasiček specification).

As first example we study a classical single-curve (i.e., ) model without jumps, driven by a one-dimensional Gaussian Ornstein-Uhlenbeck process. Let be the solution of

where is a Brownian motion and are positive constants. As driving process in (5.2) we choose the three-dimensional affine process

The coefficients in the affine semimartingale representation (5.1) are time-homogeneous, i.e. and , given by

and . The drift condition (ii) implies

We are free to specify and choose

This in turn implies that

It can be easily verified that this corresponds to the Vasiček model, see Section 10.3.2.1 in Filipović (2009). Note that this also implies . Choosing leads to the numéraire . Hence, all conditions in Proposition 5.2 are satisfied and the model is free of arbitrage. An extension to the multi-curve setting is presented in Example 5.6.

Example 5.5 (A single-curve Vasiček specification with discontinuity).

As next step, we extend the previous example by introducing a discontinuity at time . Our goal is to provide a simple, illustrative example with jump size depending on the driving process and we therefore remain in the single-curve framework.

We assume that there is a multiplicative jump in the numéraire at time depending on , where and is an independent normally distributed random variable with variance . As driving process in (5.2) we consider the five-dimensional affine process

where . The size of the jump in is specified by

which can be achieved by . The coefficients in the affine semimartingale representation (5.1) , are as in Example 5.4, with zeros in the additional rows and columns. In addition we have and . Moreover,

Finally, we choose for

, , and . for and for can be derived from as in the previous example by means of the drift condition (ii). Condition (iii) is the interesting condition for this example. This condition is equivalent to

| (5.9) |

which can be satisfied by choosing . Equation (5.9), together with the specification of for ensures that . Choosing we obtain that the model is free of arbitrage and the term structure is fully specified: indeed, we recover for and the bond pricing formula from the previous example

while, for ,

The coefficients and are the well-known solutions of the Riccati equations, such that

see Section 10.3.2.1 and Corollary 10.2 in Filipović (2009) for details and explicit formulae. The example presented here extends Example 6.15 of Keller-Ressel et al. (2018) to a fully specified term-structure model.

Example 5.6 (A simple multi-curve Vasiček specification).

We extend Example 5.4 to the multi-curve setting and consider . For simplicity, we choose as driving diffusive part a two-dimensional Gaussian Ornstein-Uhlenbeck process:

where is a two-dimensional Brownian motion with correlation . The driving process in (5.2) is specified as

The coefficients and , are time-homogeneous and obtained similarly as in Example 5.4 from (5.1). Note that

The coefficients are chosen as in Example 5.4, while . We note that and set . Moreover, we choose and

Now, choose , so that and can be calculated from by means of the drift condition (ii). At this stage, the model is fully specified. It is not difficult to verify that we are in the affine framework computed in detail in Section 4.2 of Brigo and Mercurio (2001), where explicit expressions for bond prices may be found. Moreover, we obtain and condition (ii) (and (iii), trivially) from Proposition 5.2 is satisfied. Condition (i) also holds: in this regard, note that

Since all conditions of Proposition 5.2 are now satisfied, we can conclude that the model is free of arbitrage.

Example 5.7 (A multi-curve Vasiček specification with discontinuities).

We extend the previous example by allowing for discontinuities, which can be of type I as well as of type II (see Section 1.2) and can have a different impact on the OIS and on the Ibor curves. As in Example 5.6, we consider a two-dimensional Gaussian Ornstein-Uhlenbeck process:

The driving process in (5.2) is enlarged as follows:

where the process is defined as

for some . A large value of corresponds to a high speed of mean-reversion in and generates a spiky behavior, corresponding to discontinuities of type II (recall Figure 3). On the contrary, a small value of generates long-lasting jumps, which are in line with discontinuities of type I. For simplicity, the random variables are i.i.d. standard normal, independent of and . The set of stochastic discontinuities is described by the time points and the measure is defined as in (3.6). The coefficients and are time-homogeneous and

,

and for . Moreover,

so that

and for all and .

We assume that jumps in and in the spread occur at the stochastic discontinuities and are specified by

which can be achieved by choosing

From this specification, it follows that the spread is given by

In line with Remark 3.2, the parameters and control the different impact of the stochastic discontinuities on the numéraire (and, hence, on the OIS curve) and on the spread (and, hence, on the Ibor curve). The functions , for and , are chosen as

and . For we choose

and . With this specification, it can be checked that condition (ii) of Proposition 5.2 is satisfied. Furthermore, it can be verified that

Therefore, condition (i) of Proposition 5.2 is satisfied by setting . By choosing and and calculating

we can see that condition (iii)

is satisfied for all and . We can conclude that the term structure is fully specified and, by Proposition 5.2, the model is free of arbitrage.

6. An FTAP for multiple curve financial markets

In this section, we characterize absence of arbitrage in a multiple curve financial market. At the present level of generality, this represents the first rigorous analysis of absence of arbitrage in post-crisis fixed-income markets.

As introduced in Definition 2.2, a multiple curve financial market is a large financial market containing uncountably many securities. An economically convincing notion of no-arbitrage for large financial markets has been introduced in Cuchiero, Klein and Teichmann (2016) under the name of no asymptotic free lunch with vanishing risk (NAFLVR), generalizing the classic requirement of NFLVR for finite-dimensional markets (see Delbaen and Schachermayer (1994) and Cuchiero and Teichmann (2014)). In this section, we extend the main result of Cuchiero, Klein and Teichmann (2016) to an infinite time horizon and apply it to a general multiple curve financial market.

Let be a filtered probability space satisfying the usual conditions of right-continuity and -completeness, with . Let us recall that a process is said to be a semimartingale up to infinity if there exists a process satisfying , for all , and such that is a semimartingale with respect to the filtration defined by

see Definition 2.1 in Cherny and Shiryaev (2005). We denote by the space of real-valued semimartingales up to infinity equipped with the Emery topology, see Stricker (1981). For a set , we denote by its closure with respect to the Emery topology.

We denote by the parameter space characterizing the traded assets included in Definition 2.2. We furthermore assume the existence of a tradable numéraire with strictly positive adapted price process . For notational convenience, we represent OIS zero-coupon bonds by setting , for all and . We also set for all , and .

For , we denote by the family of all subsets containing elements. For each , we define the collection of -discounted prices by

For each , , we assume that is a semimartingale on and we denote by the set of all -valued, predictable processes which are integrable up to infinity with respect to , in the sense of Definition 4.1 in Cherny and Shiryaev (2005). We assume that trading occurs in a self-financing way and we say that a process is a -admissible trading strategy if and a.s. for all . The set of wealth processes generated by -admissible trading strategies with respect to is defined as

The set of wealth processes generated by trading in at most arbitrary assets is given by . By allowing to trade in arbitrary finitely many assets and letting the number of assets increase to infinity, we arrive at generalized portfolio wealth processes. The corresponding set of -admissible wealth processes is given by , so that all admissible generalized portfolio wealth processes in the multiple curve financial market are finally given by

Remark 6.1.

The set can be equivalently described as the set of all admissible generalized portfolio wealth processes which can be constructed in the financial market consisting of the following two subsets of assets:

-

(i)

OIS zero-coupon bonds, for all maturities ,

-

(ii)

FRAs, for all tenors , all settlement dates and strike ,

for some fixed arbitrary strike . This follows from our standing assumption of linear valuation of FRAs together with the associativity of the stochastic integral.

Since each element is a semimartingale up to infinity, the limit exists pathwise and is finite. We can therefore define and , the convex cone of bounded claims super-replicable with zero initial capital.

Definition 6.2.

We say that the multiple curve financial market satisfies no asymptotic free lunch with vanishing risk (NAFLVR) if

where denotes the norm closure in of the set .

The following result provides a general formulation of the fundamental theorem of asset pricing for multiple curve financial markets.

Theorem 6.3.

The multiple curve financial market satisfies NAFLVR if and only if there exists an equivalent separating measure , i.e., a probability measure on such that for all .

Proof.

We divide the proof into several steps, with the goal of reducing our general multiple curve financial market to the setting considered in Cuchiero, Klein and Teichmann (2016).

1) In view of Remark 6.1, it suffices to consider FRA contracts with fixed strike , for all tenors and settlement dates . Consequently, the parameter space can be reduced to , which can be further transformed into a subset of via .

2) Without loss of generality, we can assume that is a semimartingale up to infinity, for every and . Indeed, let and . Similarly as in the proof of (Cherny and Shiryaev, 2005, Theorem 5.5), for each , there exists a deterministic function such that and . Setting , the associativity of the stochastic integral together with (Cherny and Shiryaev, 2005, Theorem 4.2) allows to prove that

Henceforth, we shall assume that , for all and .

3) For and , let and . The functions and are two inverse isomorphisms between and and can be extended to and . For , , let us define the process by , for all . Since , the process is a semimartingale on . Let . We define the process by , for all , and . As in the proof of (Cherny and Shiryaev, 2005, Theorem 4.2), it holds that . Moreover, it can be shown that

| (6.1) |

for all . Conversely, if , the process defined by , for , belongs to and it holds that

for all . Furthermore, holds if .

4) In view of step 3), we can consider an equivalent financial market indexed over in the filtration . To this effect, for each , , let us define

and the sets

and , where the closure in the definition of is taken in the semimartingale topology on the filtration . Let be a sequence converging to in the topology of (on the filtration ). By definition, for each , there exists a set such that for some -admissible strategy . In view of (6.1), it holds that

for all . Since the topology of is stable with respect to changes of time (see Proposition 1.3 in Stricker (1981)), the sequence converges in the semimartingale topology (on the filtration ) to . This implies that . An analogous argument allows to show the converse inclusion, thus proving that In view of Definition 6.2, this implies that NAFLVR holds for the original financial market if and only if it holds for the equivalent financial market indexed over on the filtration .

5) It remains to show that, for every , , the set satisfies the requirements of (Cuchiero, Klein and Teichmann, 2016, Definition 2.1). First, is convex and, by definition, each element starts at and is uniformly bounded from below by . Second, let and two bounded -predictable processes such that . By definition, there exist processes and such that , for . If , then

so that the required concatenation property holds. Moreover, if . The theorem finally follows from (Cuchiero, Klein and Teichmann, 2016, Theorem 3.2). ∎

Remark 6.4.

An equivalent local martingale measure (ELMM) is a probability measure on such that is a -local martingale, for all , and . Under additional conditions (namely of locally bounded discounted price processes, see (Cuchiero, Klein and Teichmann, 2016, Section 3.3)), it can be shown that NAFLVR is equivalent to the existence of an ELMM. In general, one cannot replace in Theorem 6.3 a separating measure with an ELMM, as shown by an explicit counterexample in Cuchiero, Klein and Teichmann (2016). However, as a consequence of Fatou’s lemma, the existence of an ELMM always represents a sufficient condition for NAFLVR. Assuming that the numéraire is tradable, an ELMM corresponds to a risk-neutral measure (see Section 3), which has been precisely characterized in the previous sections of the paper.

Remark 6.5.

Absence of arbitrage in large financial markets has also been studied by Kabanov and Kramkov (1998) in the sense of no asymptotic arbitrage of the first kind (NAA1), which is a weaker requirement than NAFLVR, see (Cuchiero, Klein and Teichmann, 2016, Section 4). Differently from Kabanov and Kramkov (1998), we work on a fixed filtered probability space and not on a sequence of probability spaces. On the other hand, we allow for uncountably many traded assets (see Definition 2.2).

7. Conclusions

The aim of this paper has been to introduce stochastic discontinuities into term structure modeling in a multi-curve setup. Stochastic discontinuities are a key feature in interest rate markets and we introduced two types for the classification of these jumps. To this end, we provided a general analysis of post-crisis multiple curve markets under minimal assumptions.

Three key results have been developed in our work: first, we provide a characterization of absence of arbitrage in an extended HJM setting. Second, we provide a similar characterization for market models. Both results rely on a fundamental theorem of asset pricing for multiple curve financial markets. Third, we provide a flexible class of multi-curve models based on affine semimartingales, a setup allowing for stochastic discontinuities.

While the focus of our analysis is a fundamental treatment of pricing in multiple curve markets, it is worth emphasizing that this framework has a large potential for many other applications such as risk management, requiring further studies. In particular for the latter, a proper modeling of the market price of risk and taking macro-economic variables into account are equally important.

Appendix A Technical results

The following technical result on ratios and products of stochastic exponentials easily follows from Yor’s formula, see (Jacod and Shiryaev, 2003, § II.8.19).

Corollary A.1.

For any semimartingales , and with , it holds that

Proof.

of Lemma 3.5 Due to Assumption 3.3 it can be verified by means of Minkowski’s integral inequality and Hölder’s inequality that the stochastic integrals appearing in (3.5) are well-defined, for every and . Let , for all . For , equation (3) implies that

Due to Assumption 3.3, we can apply ordinary and stochastic Fubini theorems, in the versions of Theorem 2.2 in Veraar (2012) for the stochastic integral with respect to and in the version of Proposition A.2 in Björk et al. (1997) for the stochastic integral with respect to the compensated random measure . We therefore obtain

| (A.1) |

In (A), the finiteness of follows by Assumption 3.3 together with an analogous application of ordinary and stochastic Fubini theorems.

To complete the proof, it remains to establish (3.5) for . To this effect, it suffices to show that for all , where , and similarly for . By (Jacod and Shiryaev, 2003, Proposition II.1.17), implies that, for every , . Therefore, it holds that only if , for some . For , equations (A) and (3) together imply that

where the last equality follows from the convention . By induction over , the same reasoning yields that

for all . Finally, the semimartingale property of -tenor bond prices follows from (A). ∎

Appendix B Embedding of market models into the HJM framework

The general market model considered in Section 4, as specified by equation (4.2), can be embedded into the extended HJM framework of Section 3. For simplicity of presentation, let us consider a market model for a single tenor (i.e., ) and suppose that the forward Ibor rate is given by (4.2), for all , with for all . Always for simplicity, let us assume that there is a fixed number of discontinuity dates, coinciding with the set of dates , with . We say that can be embedded into an extended HJM model if there exists a sigma-finite measure on , a spread process and a family of forward rates such that

| (B.1) |

where is given by (3.5), for all . In other words, in view of equation (2.2), the HJM model generates the same forward Ibor rates as the original market model, for every date .

We remark that, since a market model involves OIS bonds only for maturities , there is no loss of generality in taking the measure in (3.5) as a purely atomic measure of the form

| (B.2) |

More specifically, if OIS bonds for maturities are defined through (3.5) via a generic measure of the form (3.6), then there always exists a measure as in (B.2) generating the same bond prices, up to a suitable specification of the forward rate process.

The following proposition explicitly shows how a general market model can be embedded into an HJM model. For , we define

so that is the smallest such that .

Proposition B.1.

Suppose that all the conditions of Theorem 4.1 are satisfied, with respect to the measure given in (B.2), and assume furthermore that a.s. for all and . Then, under the above assumptions, the market model can be embedded into an HJM model by choosing

- (i)

- (ii)

Moreover, the resulting HJM model satisfies all the conditions of Theorem 3.7.

Proof.

Since the proof involves rather lengthy computations, we shall only provide a sketch. For , by means of Theorem 4.1 and the assumption a.s. for all , the process is a strictly positive -local martingale, so that a.s. for all and . Let us define the process by . An application of Corollary A.1, together with equation (3.3) and Corollary 3.6, yields a stochastic exponential representation and a semimartingale decomposition of the process .

For the spread process given in (3.3), we start by imposing and . We then proceed to determine the processes describing the forward rates satisfying (3). In view of (B.1), for each , we determine the process by matching the Brownian part of with the Brownian part of , while the jump function is obtained in a similar way by matching the totally inaccessible jumps of with the totally inaccessible jumps of . The drift process is then univocally determined by imposing condition (ii) of Theorem 3.7. As a next step, for each , the random variable appearing in (3.3), (3.4) is determined by requiring that

| (B.3) |

Then, for each and , the random variable is determined by requiring that

| (B.4) |

while for . Note that for and . At this stage, the forward rates are completely specified. With this specification, it can be verified that conditions (4.3) and (4.4) respectively imply that conditions (3.9) and (3.10) of Theorem 3.7 are satisfied, using the fact that Assumption 3.3 as well as conditions (3.9), (3.10) are satisfied for and by assumption. Moreover, it can be checked that, if condition (ii) of Theorem 4.1 is satisfied, then the random variables and resulting from (B.3), (B.4) satisfy conditions (iii), (iv) of Theorem 3.7, for every and . It remains to specify the process appearing in (3.4). To this effect, an inspection of Lemma 3.5 and Corollary 3.6 reveals that, since the measure is purely atomic, the terms and do not appear in condition (i) of Theorem 3.7 and in condition (3.11), respectively. Since (3.11) holds by assumption, follows by imposing condition (i) of Theorem 3.7. We have thus obtained that the two processes

are two local martingales starting from the same initial values, with the same continuous local martingale parts and with identical jumps. By means of (Jacod and Shiryaev, 2003, Theorem I.4.18 and Corollary I.4.19), we conclude that (B.1) holds for all . ∎

We want to point out that the specification described in Proposition B.1 is not the unique HJM model which allows embedding a given market model . Indeed, and can be arbitrarily specified as long as they satisfy

together with suitable integrability requirements. An analogous degree of freedom exists concerning the specification of the functions and . Note also that the random variable given in Proposition B.1 can be equivalently expressed as

References

- (1)

- Beirne (2012) Beirne, J. (2012), ‘The EONIA spread before and during the crisis of 2007-2009: The role of liquidity and credit risk’, J. Int. Money Finance 31(3), 534–551.

- Bianchetti (2010) Bianchetti, M. (2010), ‘Two curves, one price’, Risk Magazine (Aug), 74–80.

- Bianchetti and Morini (2013) Bianchetti, M. and Morini, M., eds (2013), Interest Rate Modelling After the Financial Crisis, Risk Books, London.

- Björk et al. (1997) Björk, T., Di Masi, G. B., Kabanov, Y. and Runggaldier, W. (1997), ‘Towards a general theory of bond markets’, Finance Stoch. 1(2), 141–174.

- Brace et al. (1997) Brace, A., Gatarek, D. and Musiela, M. (1997), ‘The market model of interest rate dynamics’, Math. Finance 7, 127–155.

- Brigo et al. (2018) Brigo, D., Buescu, C., Francischello, M., Pallavicini, A. and Rutkowski, M. (2018), Risk-neutral valuation under differential funding costs, defaults and collateralization. Preprint, available at ArXiv 1802.10228.

- Brigo and Mercurio (2001) Brigo, D. and Mercurio, F. (2001), Interest Rate Models - Theory and Practice, Springer Verlag. Berlin Heidelberg New York.

- Bruti-Liberati et al. (2010) Bruti-Liberati, N., Nikitopoulos-Sklibosios, C. and Platen, E. (2010), ‘Real-world jump-diffusion term structure models’, Quant. Finance 10(1), 23–37.

- Cherny and Shiryaev (2005) Cherny, A. and Shiryaev, A. (2005), On stochastic integrals up to infinity and predictable criteria for integrability, in M. Émery, M. Ledoux and M. Yor, eds, ‘Séminaire de Probabilités XXXVIII’, Springer, Berlin - Heidelberg, pp. 165–185.

- Constantinides (1992) Constantinides, G. (1992), ‘A theory of the nominal term structure of interest rates’, Rev. Financial Stud. 5(4), 531–552.

- Crépey et al. (2015) Crépey, S., Grbac, Z., Ngor, N. and Skovmand, D. (2015), ‘A Lévy HJM multiple-curve model with application to CVA computation’, Quant. Finance 15(3), 401–419.

- Crépey et al. (2012) Crépey, S., Grbac, Z. and Nguyen, H. N. (2012), ‘A multiple-curve HJM model of interbank risk’, Math. Financ. Econ. 6(3), 155–190.

- Cuchiero, Fontana and Gnoatto (2016) Cuchiero, C., Fontana, C. and Gnoatto, A. (2016), ‘A general HJM framework for multiple yield curve modeling’, Finance Stoch. 20(2), 267–320.

- Cuchiero et al. (2019) Cuchiero, C., Fontana, C. and Gnoatto, A. (2019), ‘Affine multiple yield curve models’, Math. Finance 29(2), 568–611.

- Cuchiero, Klein and Teichmann (2016) Cuchiero, C., Klein, I. and Teichmann, J. (2016), ‘A new perspective on the fundamental theorem of asset pricing for large financial markets’, Theory Probab. Appl. 60(4), 561–579.

- Cuchiero and Teichmann (2014) Cuchiero, C. and Teichmann, J. (2014), ‘A convergence result for the Emery topology and a variant of the proof of the fundamental theorem of asset pricing’, Finance Stoch. 19(4), 743–761.

- Delbaen and Schachermayer (1994) Delbaen, F. and Schachermayer, W. (1994), ‘A general version of the fundamental theorem of asset pricing’, Math. Ann. 300(3), 463–520.

- Duffie et al. (2003) Duffie, D., Filipović, D. and Schachermayer, W. (2003), ‘Affine processes and applications in finance’, Ann. Appl. Probab. 13(3), 984–1053.

- Duffie and Kan (1996) Duffie, D. and Kan, R. (1996), ‘A yield-factor model of interest rates’, Math. Finance 6(4), 379–406.

- Duffie and Lando (2001) Duffie, D. and Lando, D. (2001), ‘Term structures of credit spreads with incomplete accounting information’, Econometrica 69(3), 633–664.

- Filipović (2009) Filipović, D. (2009), Term Structure Models: A Graduate Course, Springer Verlag. Berlin Heidelberg New York.

- Filipović and Trolle (2013) Filipović, D. and Trolle, A. B. (2013), ‘The term structure of interbank risk’, J. Fin. Econ. 109(3), 707–733.

- Fontana et al. (2019) Fontana, C., Pelger, M. and Platen, E. (2019), ‘On the existence of sure profits via flash strategies’, J. Appl. Probab. 56(2), 384–397.

- Fontana and Schmidt (2018) Fontana, C. and Schmidt, T. (2018), ‘General dynamic term structures under default risk’, Stoch. Proc. Appl. 128(10), 3353–3386.

- Gehmlich and Schmidt (2018) Gehmlich, F. and Schmidt, T. (2018), ‘Dynamic defaultable term structure modelling beyond the intensity paradigm’, Math. Finance 28(1), 211–239.

- Grbac et al. (2015) Grbac, Z., Papapantoleon, A., Schoenmakers, J. and Skovmand, D. (2015), ‘Affine LIBOR models with multiple curves: Theory, examples and calibration’, SIAM J. Financ. Math. 6(1), 984–1025.

- Grbac and Runggaldier (2015) Grbac, Z. and Runggaldier, W. J. (2015), Interest Rate Modeling: Post-Crisis Challenges and Approaches, Springer Verlag. Berlin Heidelberg New York.

- He et al. (1992) He, S.-W., Wang, J.-G. and Yan, J.-A. (1992), Semimartingale Theory and Stochastic Calculus, Science Press - CRC Press, Beijing.

- Heath et al. (1992) Heath, D., Jarrow, R. A. and Morton, A. J. (1992), ‘Bond pricing and the term structure of interest rates’, Econometrica 60(1), 77–105.

- Henrard (2007) Henrard, M. (2007), ‘The irony in the derivatives discounting’, Willmott Magazine (July), 92–98.

- Henrard (2014) Henrard, M. (2014), Interest Rate Modelling in the Multi-curve Framework, Palgrave Macmillan, London.

- Hernandis and Torró (2013) Hernandis, L. and Torró, H. (2013), ‘The information content of Eonia swap rates before and during the financial crisis’, J. Bank. Finance 37(12), 5316–5328.

- Jacod and Shiryaev (2003) Jacod, J. and Shiryaev, A. (2003), Limit Theorems for Stochastic Processes, 2nd edn, Springer Verlag, Berlin.

- Kabanov and Kramkov (1998) Kabanov, Y. and Kramkov, D. (1998), ‘Asymptotic arbitrage in large financial markets’, Finance Stoch. 2(2), 143–172.

- Keller-Ressel et al. (2018) Keller-Ressel, M., Schmidt, T. and Wardenga, R. (2018), ‘Affine processes beyond stochastic continuity’, Ann. Appl. Probab. (forthcoming).

- Kim and Wright (2014) Kim, D. H. and Wright, J. H. (2014), Jumps in bond yields at known times, Technical report, National Bureau of Economic Research.

- Klein et al. (2016) Klein, I., Schmidt, T. and Teichmann, J. (2016), No arbitrage theory for bond markets, in J. Kallsen and A. Papapantoleon, eds, ‘Advanced Modelling in Mathematical Finance’, Springer, Cham, pp. 381–421.

- Koval (2005) Koval, N. (2005), Time-inhomogeneous Lévy processes in Cross-Currency Market Models, PhD thesis, University of Freiburg.

- Macrina and Mahomed (2018) Macrina, A. and Mahomed, O. (2018), ‘Consistent valuation across curves using pricing kernels’, Risks 6(1), 1 – 39.

- Mercurio (2010) Mercurio, F. (2010), ‘Modern LIBOR market models: using different curves for projecting rates and for discounting’, Int. J. Theor. Appl. Fin. 13(1), 113–137.

- Mercurio and Xie (2012) Mercurio, F. and Xie, Z. (2012), ‘The basis goes stochastic’, Risk Magazine (Dec), 78–83.

- Merton (1974) Merton, R. (1974), ‘On the pricing of corporate debt: the risk structure of interest rates’, J. Finance 29(2), 449–470.

- Moreni and Pallavicini (2014) Moreni, N. and Pallavicini, A. (2014), ‘Parsimonious HJM modelling for multiple yield-curve dynamics’, Quant. Finance 14(2), 199–210.

- Musiela and Rutkowski (1997) Musiela, M. and Rutkowski, M. (1997), Martingale Methods in Financial Modelling, Springer, Berlin.

- Nguyen and Seifried (2015) Nguyen, T. A. and Seifried, F. T. (2015), ‘The multi-curve potential model’, Int. J. Theor. Appl. Fin. 18(7), 1550049.

- Piazzesi (2001) Piazzesi, M. (2001), An econometric model of the yield curve with macroeconomic jump effects.

- Piazzesi (2005) Piazzesi, M. (2005), ‘Bond yields and the federal reserve’, J. Pol. Econ. 113(2), 311–344.

- Piazzesi (2010) Piazzesi, M. (2010), Affine term structure models, in Y. Aït-Sahalia and L. P. Hansen, eds, ‘Handbook of Financial Econometrics: Tools and Techniques’, Vol. 1, Elsevier, Amsterdam, pp. 691–766.

- Platen and Heath (2006) Platen, E. and Heath, D. (2006), A Benchmark Approach to Quantitative Finance, Springer Verlag. Berlin Heidelberg New York.

- Protter (2004) Protter, P. (2004), Stochastic Integration and Differential Equations, 2nd edn, Springer Verlag. Berlin Heidelberg New York.