Forecasting financial crashes with quantum computing

Abstract

A key problem in financial mathematics is the forecasting of financial crashes: if we perturb asset prices, will financial institutions fail on a massive scale? This was recently shown to be a computationally intractable (NP-hard) problem. Financial crashes are inherently difficult to predict, even for a regulator which has complete information about the financial system. In this paper we show how this problem can be handled by quantum annealers. More specifically, we map the equilibrium condition of a toy-model financial network to the ground-state problem of a spin-1/2 quantum Hamiltonian with 2-body interactions, i.e., a quadratic unconstrained binary optimization (QUBO) problem. The equilibrium market values of institutions after a sudden shock to the network can then be calculated via adiabatic quantum computation and, more generically, by quantum annealers. Our procedure could be implemented on near-term quantum processors, thus providing a potentially more efficient way to assess financial equilibrium and predict financial crashes.

I Introduction

Imagine a financial network where institutions (banks, companies…) hold a number of assets as well as part of the other institutions in the network. Could a small change in asset value cause a massive drop in the market value of the institutions? Or in other words, could there be a financial crash? At present, we mainly rely on empirical or statistical tools to answer this question Sornette et al. (1996); Estrella and Mishkin (1998); Johansen and Sornette (2000); Sornette (2004); Bussiere and Fratzscher (2006); Frankel and Saravelos (2012). It is not clear that these methods can systematically and reliably predict financial crashes Laloux et al. (1999); Brée et al. (2010), because indicators of a crisis generally fail at predicting the next crisis Grabel (2003). Our failure to prevent these events is directly responsible for economic crises and their devastating consequences.

Mathematically, the problem of forecasting a crash is intractable, even for extremely simple financial networks. It was recently shown in Ref. Hemenway and Khanna (2017) that this problem belongs to the complexity class NP-hard even for extremely simple toy models, meaning that there are no known efficient classical algorithms to solve it111Mathematically speaking, NP (aka Nondeterministic Polynomial) is the class of problems for which a non-deterministic classical verifier can check the validity of the solution in polynomial time. Notice that this does not say anything about the hardness of finding the solution to the problem. NP-Hard is the class of problems for which finding the solution cam be reduced, in polynomial time, to that of finding the solution of any problem in NP. Those NP-Hard problems that are also in NP are called NP-Complete. In practice, NP-Complete and NP-Hard problems are amongst the hardest problems in computer science.. In general, financial crashes cannot be avoided by performing stress-tests or institution evaluations (without a global knowledge of the network due to privacy issues, thus relying on reconstruction methods). Even given complete knowledge of all the assets and cross-holdings in a simple network of 20–30 institutions, it would take more time than the age of the universe – 13.7 billion years! – to compute the effect of a perturbation.

While the situation might seem dire, there are proof-of-principle calculations showing that quantum computing may be able to tackle this type of problems more efficiently, both in theory Kaminsky and Lloyd (2004); Lucas (2014) and in practice Xu et al. (2012); Perdomo-Ortiz et al. (2012); Bian et al. (2013); Babbush et al. (2014). In particular, quantum computing has proved to be a valid alternative at tackling some complex financial problems Orús et al. (2019); Ding et al. (2019); Martin et al. (2019).

In this paper, we show that the problem of predicting financial crashes and, more generically, assessing the equilibrium of a financial network, is amenable to quantum annealers, at least for simple financial toy models. These quantum processors solve problems using the idea of adiabatic quantum computation, which uses nature’s remarkable ability to find the lowest-energy eigenstate – the ground state – of complex Hamiltonians Farhi et al. (2000). We begin by showing that finding the equilibrium condition of a simple toy-model financial network is equivalent to finding the ground-state of a specific spin-1/2 Hamiltonian with 2-body interactions. This is our problem Hamiltonian, which has the form of a quadratic unconstrained binary optimization (QUBO) problem, and which commercially available quantum annealers are well suited to solve Lucas (2014). Once the annealer finds a candidate ground state, we can forecast a potential crash simply by reading out the system’s state, interpreted as a financial equilibrium configuration.

The structure of this paper is as follows. In Sec. II we describe the toy model of financial network. In Sec. III we show how computing the equilibrium configuration of such a financial network is equivalent to finding the ground state of some quantum spin Hamiltonian. In Sec. IV we discuss on the required resources to implement the resulting Hamiltonian, specifically the required number of qubits. In Sec. V we exemplify the model of financial network with a simple numerical experiment for a randomly-generated network, observing a crash. Finally, in Sec. VI we wrap up with our conclusions and remarks.

II Financial network model

We consider here a simple model of financial network proposed originally in Ref. Elliott et al. (2014). In this model there are institutions as well as assets. Institutions could be countries, banks, companies… whereas an asset is any object or project with an intrinsic value. Financial institutions can own shares of the underlying assets. Moreover, there are interdependencies between the institutions modelled by linear dependencies. Such cross-holdings model the fact that some institutions may own shares of other institutions, as well as approximate debt contracts between institutions.

Mathematically, we denote by the price of asset , and by the fraction (percentage) of asset owned by institution . We define as the matrix of ownership. Additionally, let be the matrix of cross-holdings among institutions. The component is the fraction of institution owned by institution . Following the convention in Refs. Elliott et al. (2014) and Hemenway and Khanna (2017), we set , and define as the amount of self-ownership of institution . Matrix is thus a diagonal matrix with entries on the diagonal. The model can then be seen in terms of a complex network of interdependencies. Following Ref. Hemenway and Khanna (2017), we further define the equity value of institution as , i.e., the value of institution due to ownership of assets and cross-holdings. In matrix notation, we can then write , such that . As explained in Ref. Hemenway and Khanna (2017), matrix is guaranteed to be invertible. Additionally, the market value of institution is its equity value rescaled with its self-ownership, i.e., . The market values are then the solution to the linear equation

| (1) |

As explained in Refs.Elliott et al. (2014); Hemenway and Khanna (2017), the model further introduces the notion of failure. This means that if the market value of an institution drops below a certain critical threshold, then the institution suffers an extra discontinuous loss in equity value. This non-linear behavior models the fact that if an institution cannot pay its own operating costs, then it may see a sudden drop in revenues. Moreover, if confidence in the institution is downgraded, then it may also see a sudden drop in its value since it will become difficult to, e.g., attract investors. Mathematically, this is modelled by a step-function such that if the market value of institution drops below a critical threshold , then it incurs a failure and its equity value drops by an additional . Thus, if we define with the Heaviside step-function, then the market values satisfy

| (2) |

While Eq. (refeq1) is linear, Eq. (2) is highly non-linear due to the presence of the failure term . In practice, this non-linearity is what makes it extremely difficult to determine the market values of institutions after a small change in the prices of assets. Specifically, given an equilibrium which satisfies Eq. (2), if the sum of all assets’ prices drop by , then it is NP-hard to determine the maximum number of failures that could happen once the new equilibrium is reached Hemenway and Khanna (2017). This means that predicting a crash of the financial network due to small changes of the individual prices of assets is a computationally-intractable problem. Let us also remark that this simple, minimal model of financial network, does not target the probability of a change of prices happening, but rather what will happen to the network shall this change take place.

III Financial equilibrium as quantum ground state

In the following, we will describe how to find a state which satisfies the financial equilibrium condition on a quantum annealer. We begin by stating the financial equilibrium condition, Eq. (2), as a variational problem. We then express this variational problem in terms of classical binary variables, and promote it to the problem of finding the ground state of a spin-1/2 Hamiltonian with many-qubit interactions. Finally, we reduce the many-qubit interactions to 2-qubit interactions, which are easier to implement experimentally Chancellor et al. (2017). We will also calculate the computational resources necessary to solve this problem.

III.1 Variational Setup

Given set of institutions, holdings and prices, the market values at financial equilibrium satisfy Eq. (2). This equilibrium may not be unique. In general, though, one would have

| (3) |

The above expression is strictly larger than zero away from equilibrium, and equal to zero and therefore minimum at equilibrium. Thus, we have recast the problem of finding the market values in equilibrium as a variational problem: the vector at equilibrium will be the one that minimizes the classical cost function for a given network configuration.

III.2 Bit variables for market values

We now write in terms of classical bit variables. This can be done by approximating the variables in terms of classical bits using the usual binary notation,

| (4) |

with bits . The market value of institution is then codified, up to the desired approximation, by the string of bits . This sets an upper-bound on market value of .

III.3 Polynomial expansion of failure

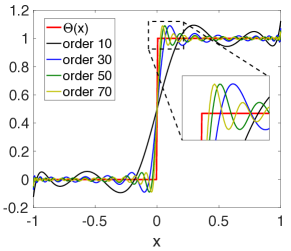

Next, we need a procedure to deal with the failure terms , which are highly non-linear and modelled by the Heaviside unit step function, which is discontinuous. In order to obtain an appropriate Hamiltonian for a quantum annealer, it would be desirable to have a continuous function instead. Moreover, we will need a Hamiltonian that can be efficiently described, even if it has many-qubit interactions. Under these constraints, we have found that the most viable option is to approximate the Heaviside function by a polynomial expansion. Of course, such an expansion is not unique. While it would be possible to find the optimal polynomial of a given degree approximating the function in a given interval and for a given error norm Gajny et al. (2016), standard approximations exist in terms of, e.g., shifted Legendre polynomials Cohen and Tan (2012), which are sufficient to show the validity of our approach. In particular, one can make use of the Fourier-Legendre expansion

| (5) |

in the interval , with the th Legendre Polynomial. As shown in Fig. 1, the truncated series produces a reasonable approximation to the sudden discontinuity of the failure for polynomials of moderate-order. In our case, we can choose , so that we get directly the expansion for in the correct range .

Thus, from now on we will take the approximation

| (6) |

where is some polynomial of degree in and domain . This approximation makes the failure term easier to handle for our purposes, while still being strongly non-linear.

III.4 Promoting to quantum Hamiltonian

At this point we promote function in Eq. (3) to a quantum Hamiltonian, under the approximations described above. Specifically, we have now a classical function , where are the bits for the market value of institution , and where we also used the polynomial approximation of the step function in Eq. (6). Considering Eqs.(3), (4) and (6) together, one can see after some inspection that is also a polynomial in the bit variables . More specifically,

| (7) |

i.e., it is a Boolean polynomial of degree .

We then define the quantum Hamiltonian by promoting the classical bit variables to diagonal qubit operators with eigenvalues , i.e., . In terms of spin-1/2 Pauli operators, these can be written as , with the -Pauli matrix. The quantum Hamiltonian is then

| (8) |

which is nothing but the left hand side of Eq. (3), with the failure term approximated polynomially as in Eq. (6), and written in terms of qubit operators. This Hamiltonian is automatically hermitian. It is also a polynomial of degree in the qubit operators. Each term in involves many-qubit interactions for different sets of qubits, ranging from 0-qubit terms up to -qubit terms at most. The explicit form of the Hamiltonian can be computed whenever necessary on a case-by-case basis. The number of terms in will be analyzed later in detail.

III.5 From many-qubit to 2-qubit

The Hamiltonian in Eq. (8) could already be used as input for a quantum annealer that allowed for multiqubit interactions Chancellor et al. (2017); Leib et al. (2016). However, state-of-the-art quantum processors target, for practical reasons, Hamiltonians with at most 2-qubit interactions. Mathematically, finding the ground state of such Hamiltonians amounts to solving QUBO problems. It would then be desirable to have a Hamiltonian made of at most 2-qubit interactions. Thus, the final step of our derivation is to bring the interactions in the Hamiltonian of Eq. (8) down to 2-qubit terms at most.

To get such a modified Hamiltonian, we use the technique proposed in Ref. Chancellor et al. (2017), which allows to implement effective -qubit interactions using extra ancilla qubits and 2-qubit interactions only. Suppose that we are given a -qubit interaction of the type

| (9) |

where for convenience we now use the notation in terms of the -Pauli matrix and is the interaction prefactor. The trick is to write another Hamiltonian , made of at most 2-qubit interactions, and such that it reproduces the low-energy spectrum of . This is achieved by introducing extra ancilla qubits and the Hamiltonian

| (10) | |||||

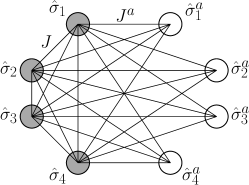

The topology of the interactions is shown in Fig. 2. All the “logical” qubits are all coupled among themselves via 2-body interactions with strength . Each ancilla qubits are coupled to every logical qubits, with 2-body interactions of strength . Moreover, there are magnetic fields and accounting for 1-qubit terms. The idea, as explained in Ref. Chancellor et al. (2017), is to find the values of and such that the low-energy spectrum of reproduces the energy spectrum of . This is achieved by the choice

| (11) |

with any satisfying the conditons and . The low-energy sector of the Hamiltonian in Eq. (10), with couplings as in Eq. (11), reproduces the spectrum of the Hamiltonian in Eq. (9) up to an overall additive energy constant. This is guaranteed for the part of the spectrum satisfying , and allows the annealer to sample over low-energy states effectively reproducing the energy landscape of the many-qubit interactions on logical qubits.

IV Required resources

Let us now consider how many qubits are needed. First, qubits are required to describe each one of the market values , amounting to a total cost in logical qubits of . Second, the cost in ancilla qubits can be estimated from the number of interaction terms composing the Hamiltonian. A spin Hamiltonian constructed from a Boolean polynomial of degree has 0-qubit terms, 1-qubit terms, …, -qubit terms, giving a maximum of

| (12) |

interaction terms. For and , the leading term of Eq. (12) is the binomial coefficient for . Thus, for together with , and using , we have that

| (13) |

Therefore, the number of terms to specify the Hamiltonian is a polynomial in and , whose degree is controlled by . This means that the total number of qubits needed to implement our protocol is

| (14) |

where we used . Since is the degree of the polynomial approximating the step function, we see that this is actually acting as a resource truncation parameter: it controls the scaling exponent of the required resources. Two important remarks about Eq. (14) are also in order. First, it is an asymptotic expression which often heavily overestimates the number of qubits required in practice. Second, it implies that for a moderate value of the failure term can be very strongly non-linear, which is what makes the classical problem NP-hard, while keeping a polynomial scaling of the required quantum resources. In fact, this problem is NP-hard for any , because our derivation shows that it is as hard as finding the ground state of an arbitrary spin-glass Barahona (1982). Consequently, the computational running time will depend on the specifics of the instance and of the quantum annealing process, exactly as for the spin-glass problem.

V A simple numerical experiment

We provide in this section a simple numerical example in order to show a typical crash situation. We have at least two motivations for this. First, we believe that this example shows very clearly several of the concepts discussed earlier, which may be easier to understand with a simple plot rather than with many equations. Second, it provides an idea of a range of parameters where it would be possible to observe the “crash” on a quantum processor222Notice that Ref.Ding et al. (2019) is assessing financial equilibrium, but not the crash itself..

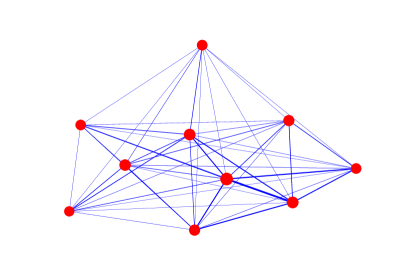

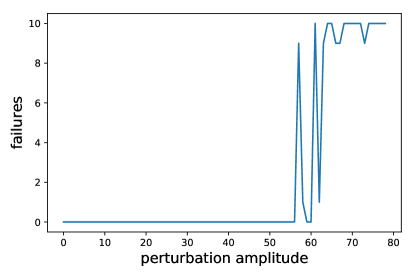

We generated a random financial network with institutions, with a minimum self-ownership of , as well as with assets, with prices ranging from to . We then perturb the network by substracting a random vector from the asset prices. This perturbation has a maximum amplitude . We then look at the number of failures of institutions as a function of the perturbation amplitude.

Following the above procedure we generated an example of random financial network as in Fig. 3. In the figure, dots correspond to the institutions and links and their thickness represent cross-holdings and their amount. For the perturbation that we described, we find that the number of failures depends on the perturbation as in Fig. 4. We clearly see the phase transition from the “normal” to the “crash” phase in the figure: when the perturbation amplitude is , basically all institutions in the financial network fail, i.e., their market values drop to zero. Notice that the region were the crash happens is very small, roughly for the perturbation amplitude between and . Following standard condensed-matter arguments (finite-size scaling), the amplitude of this region is expected to shrink as the number of institutions grows, thus making the transition sharper and therefore making the prediction of the crash after a small perturbation even harder.

VI Conclusions and remarks

Here we have shown how the problem of forecasting financial crashes, which is NP-hard, can be handled by quantum annealers, at least for some simple toy-models of financial network. Specifically, our procedure allows the efficient construction of a QUBO formula by writing Eq. (3) in terms of -Pauli matrices and 2-qubit interactions only, and which can be used in state-of-the-art quantum processors to predict a potential massive failure of financial institutions after a small shock to the system. Our result shows that quantum computers could help, at least in principle, in forecasting such situations, in addition to other known applications in finance Orús et al. (2019). One should however keep in mind that current quantum processors still have limited computational capabilities, specially in comparison with the best state-of-the-art classical algorithms. Nevertheless, and still within these limitations, it is already possible to perform proof-of-principle experiments with such quantum processors, paving the way towards the development of more powerful and less noisy quantum computational devices.

While our results are constructed for a minimal financial network model, more complex networks can be handled similarly. Thus, these results show that near-term quantum processors, such as the D-Wave machine, may become useful in the early prediction of financial crashes. From a broader perspective, our results show how quantum computers can be used to handle problems related to financial equilibrium, and in particular to forecast the financial consequences of different courses of action.

There is plenty of room for further research. For instance, we could explore ways of improving the efficiency and accuracy of our procedure. This is particularly important, since the number of required qubits, as estimated in Sec. IV, grows up quickly with the number of institutions and the precision required for the non-linear term, thus hindering a practical application of our protocol. In spite of this, in a separate publication Ding et al. (2019) we present an experimental implementation of our algorithm on a commercially available quantum annealing processor, where QUBO formulas are the input, and for a limited number of qubits, thus showing that such an implementation is indeed possible, at least as a proof of principle. Notice, though, that more complex financial network models may require of extra resources which were not considered here. Additionally, it would be very interesting to extend this protocol to deal with other financial equilibrium problems.

Acknowledgements.- We acknowledge discussions with the members of the Q4Q commission of the QWA.

References

- Sornette et al. (1996) D. Sornette, A. Johansen, and J.-P. Bouchaud, Journal de Physique I 6, 167 (1996).

- Estrella and Mishkin (1998) A. Estrella and F. S. Mishkin, Review of Economics and Statistics 80, 45 (1998).

- Johansen and Sornette (2000) A. Johansen and D. Sornette, SSRN 212568 (2000), 10.2139/ssrn.212568.

- Sornette (2004) D. Sornette, Princeton Science Library (2004), 10.1063/1.1712506.

- Bussiere and Fratzscher (2006) M. Bussiere and M. Fratzscher, Journal of International Money and Finance 25, 953 (2006).

- Frankel and Saravelos (2012) J. Frankel and G. Saravelos, Journal of International Economics 87, 216 (2012).

- Laloux et al. (1999) L. Laloux, M. Potters, R. Cont, J.-P. Aguilar, and J.-P. Bouchaud, Europhysics Letters (EPL) 45, 1 (1999).

- Brée et al. (2010) D. Brée, D. Challet, and P. P. Peirano, Quantitative Finance, 13 (2010).

- Grabel (2003) I. Grabel, Eastern Economic Journal 29, 243 (2003).

- Hemenway and Khanna (2017) B. Hemenway and S. Khanna, Algorithmic Finance 5, 95–110 (2017).

- Kaminsky and Lloyd (2004) W. M. Kaminsky and S. Lloyd, in Quantum Computing and Quantum Bits in Mesoscopic Systems (Springer US, 2004) pp. 229–236.

- Lucas (2014) A. Lucas, Frontiers in Physics 2 (2014), 10.3389/fphy.2014.00005.

- Xu et al. (2012) N. Xu, J. Zhu, D. Lu, X. Zhou, X. Peng, and J. Du, Physical Review Letters 108 (2012), 10.1103/physrevlett.108.130501.

- Perdomo-Ortiz et al. (2012) A. Perdomo-Ortiz, N. Dickson, M. Drew-Brook, G. Rose, and A. Aspuru-Guzik, Scientific Reports 2 (2012), 10.1038/srep00571.

- Bian et al. (2013) Z. Bian, F. Chudak, W. G. Macready, L. Clark, and F. Gaitan, Physical Review Letters 111 (2013), 10.1103/physrevlett.111.130505.

- Babbush et al. (2014) R. Babbush, A. Perdomo-Ortiz, B. O’Gorman, W. Macready, and A. Aspuru-Guzik, “Construction of energy functions for lattice heteropolymer models: Efficient encodings for constraint satisfaction programming and quantum annealing,” in Advances in Chemical Physics: Volume 155 (John Wiley and Sons, Ltd, 2014) Chap. 5, pp. 201–244.

- Orús et al. (2019) R. Orús, S. Mugel, and E. Lizaso, Reviews in Physics 4, 100028 (2019).

- Ding et al. (2019) Y. Ding, L. Lamata, M. Sanz, J. Martín-Guerrero, E. Lizaso, S. Mugel, X. Chen, R. Orús, and E. Solano, “Towards prediction of financial crashes with a d-wave quantum computer,” (2019), arXiv:1904.05808 .

- Martin et al. (2019) A. Martin, B. Candelas, A. Rodríguez-Rozas, J. D. Martín-Guerrero, X. Chen, L. Lamata, R. Orús, E. Solano, and M. Sanz, “Towards pricing financial derivatives with an ibm quantum computer,” (2019), arXiv:1904.05803 .

- Farhi et al. (2000) E. Farhi, J. Goldstone, S. Gutmann, and M. Sipser, “Quantum computation by adiabatic evolution,” (2000), arXiv:quant-ph/0001106 .

- Elliott et al. (2014) M. Elliott, B. Golub, and M. O. Jackson, American Economic Review 104, 3115 (2014).

- Chancellor et al. (2017) N. Chancellor, S. Zohren, and P. A. Warburton, npj Quantum Information 3 (2017), 10.1038/s41534-017-0022-6.

- Gajny et al. (2016) L. Gajny, O. Gibaru, E. Nyiri, and S.-C. Fang, Numerical Algorithms 75, 827 (2016).

- Cohen and Tan (2012) M. A. Cohen and C. O. Tan, Applied Mathematics Letters 25, 1947 (2012).

- Leib et al. (2016) M. Leib, P. Zoller, and W. Lechner, Quantum Science and Technology 1, 015008 (2016).

- Barahona (1982) F. Barahona, Journal of Physics A: Mathematical and General 15, 3241 (1982).