Rank Dynamics for Functional Data

Abstract

The study of the dynamic behavior of cross-sectional ranks over time for functional data and the ranks of the observed curves at each time point and their temporal evolution can yield valuable insights into the time dynamics of functional data. This approach is of interest in various application areas. For the analysis of the dynamics of ranks, estimation of the cross-sectional ranks of functional data is a first step. Several statistics of interest for ranked functional data are proposed. To quantify the evolution of ranks over time, a model for rank derivatives is introduced, where rank dynamics are decomposed into two components. One component corresponds to population changes and the other to individual changes that both affect the rank trajectories of individuals. The joint asymptotic normality for suitable estimates of these two components is established. The proposed approaches are illustrated with simulations and three longitudinal data sets: Growth curves obtained from the Zürich Longitudinal Growth Study, monthly house price data in the US from 1996 to 2015 and Major League Baseball offensive data for the 2017 season.

Keywords: Decomposition of rank derivatives; Functional data analysis; House price dynamics; Major League Baseball; Zürich Longitudinal Growth Study.

1 Introduction

In many statistical applications, practitioners are interested in relative, as opposed to absolute, behavior of random quantities. For example, in growth studies, one is often interested in growth faltering, stunting and more generally determining whether children are tall, normal or small for their age. Such determinations are based on an assessment of how individuals rank relative to others, where an individual’s rank will change as the individual ages. In sports, many interested parties aim to track the longitudinal changes in the relative rankings of the best players and teams. For example, the compensation a player receives is tied to relative performance. Related studies have been done on regression models for conditional distribution functions and quantiles (Kim,, 2007; Kim and Yang,, 2011; Wu and Tian,, 2013; Tian and Wu,, 2014; Cho et al.,, 2016; Kürüm et al.,, 2018, for example), while our focus here is on modeling the temporal evolution of longitudinal ranks.

In the case of univariate measurements, ranking data is straightforward and well-studied. However, one cannot rank multivariate data because there is no total ordering in . For the same reason, functional data that correspond to infinite-dimensional objects similarly cannot be ordered (for overviews, see, e.g., Ramsay and Silverman,, 1997; Horvath and Kokoszka,, 2012; Wang et al.,, 2016). In related work, the analysis of sports data with functional data analysis techniques has been recently considered by Chen and Fan, (2018), archetypoids of functional trajectories were applied to sports statistics by Vinué and Epifanio, (2017), and Martin-Barragan et al., (2016) studied epigraph and hypograph indices which are the proportions of sample trajectories entirely lying above or below certain curves.

While functional data cannot be ordered, they are time-indexed and a total ordering exists cross-sectionally at each fixed time. This can be utilized to transform functional data into trajectories that consist of ranks, viewed as functions of time. Of interest then is the modeling of the ranks of individuals and their patterns over time. In this paper, we discuss statistical tools to study such rank dynamics. In particular, we introduce a novel decomposition for rank dynamics, where we show that rank derivatives can be naturally decomposed into two components, corresponding to a population and an individual contribution to the rank evolution, respectively. A simple example for the effect of the population on individual ranks occurs when the scores of the population improve overall, but a particular individual stays the same, say a runner maintains a certain level of speed but the population of runners at large is getting faster — then the individual runner’s rank will drop within the population, even though the individual’s performance is not worse than before.

As rank dynamics depend on the interplay between individual and population changes and make reference to the cross-sectional population at each time where functional values are obtained, rank dynamics is quite different from common dynamic models in functional data analysis, where only the time dynamics of individuals viewed by themselves are the focus, with the associated notions of derivatives of observed trajectories and empirical dynamics. These previous approaches could be characterized as dynamics learning from functional data, and include derivative principal components, identification of differential equations, and dynamic regression modeling (Ramsay and Ramsey,, 2002; Wu and Perloff,, 2005; Ramsay et al.,, 2007; Wang et al., 2008b, ; Wang et al., 2008a, ; Hegland et al.,, 2009; Müller and Yao,, 2010; Dai et al.,, 2018).

More specifically, to study rank dynamics one first transforms the observed functional data through a probability transform that is implemented at each time point. We assume that the functional data are densely sampled with negligible noise and that there is a stochastic process with square integrable trajectories which are in the Hilbert space . The process generates the sample of trajectories, which are the observed functional data. If the functional data are measured on a time grid with additive noise, one can implement a pre-smoothing step (Müller et al.,, 2006; Hall and Van Keilegom,, 2007).

Our starting point is the cross-sectional distribution

| (1) |

for each , where the domain is a compact interval. Without loss of generality, we consider . The process of local probability transforms associated with is then

Since the subject-specific random process conveys the information which fraction of individuals has larger and which fraction has lower values at time compared to a selected individual, we refer to as the rank process associated with the functional process .

We note that the range of the rank process is always the interval and multiplying it by the sample size gives the actual ranks. Indeed, the distribution of is uniform on for every , as it corresponds to the local probability transform. In a finite sample situation there are various ways to carry out the probability transform from a sample of data , depending on how one estimates the cumulative distribution function . If one uses the empirical distribution function one obtains the actual ranks, but one can also use smooth versions of empirical distribution functions, which often are advantageous (Falk,, 1984) and yield approximate ranks.

The paper is organized as follows. In Section 2, we introduce a time-dynamic model for ranked functional data to quantify the temporal evolution of rank processes, which is a key contribution of this paper. In Section 3, we discuss several measures for the central tendency and variation of the rank trajectories, and in Section 4 the estimation of these population quantities. Asymptotic distributions and finite-sample performance of the proposed estimates are demonstrated in Sections 5 and 6, respectively. Data illustrations are provided in Section 7, where we demonstrate rank dynamics for three scenarios including Zürich growth curves, house price trajectories and Major League Baseball data.

2 A Time-Dynamic Model for Ranked Functional Data

Increases or decreases in an individual’s rank trajectory depend on both the subject’s functional trajectory and the functional trajectories of all other individuals in the sample, as the subject’s rank at time depends on these two inputs. This decomposition is exemplified by the keeping up with the Joneses paradigm, where subjects’ happiness is assessed through an individual’s relative standing and its changes, compared to their peers, i.e., critically important are the subject’s rank and especially the changes in rank (e.g., Barnett et al.,, 2010; Nguyen,, 2016).

To quantify relative changes in a sample of functional data, it is expedient to utilize derivatives . Recalling that is the cross-sectional distribution of at time and and taking the derivative of with respect to leads to

| (2) |

where

| (3) |

The two terms in (2) provide the decomposition of the rank derivative into two components for each subject. The first component reflects the changes in the distribution of the original process with respect to time. More specifically, indicates how population changes influence the rank of a given subject, where positive (negative) values of for a specific subject mean that the underlying functional trajectories for the other subjects are generally decreasing (increasing) at time , which leads to an increase (decrease) in rank for the selected subject that is entirely due to a change in the characteristics of the general population. On the other hand, the second component represents the subject’s own contribution to the rank dynamics. Since , positive (negative) values of contribute to an increase (decrease) in rank due to individual change. Note that even if a subject’s underlying functional trajectory is increasing, the population change could increase even faster and potentially overpower a subject’s own contribution, leading to a decrease in rank.

To gain a better understanding of the nature of the model in (2), it is helpful to consider the case where is a constant function. In this case, we have that for all , and the change in rank is completely determined by the rest of the population, i.e., the rank only changes when the population changes. Similarly, for a subject that traverses on a constant rank trajectory, it holds that for all , which means that population and subject driven components match each other, for all .

To determine the contributions of population and individual effects, it is then of interest to quantify the overall contributions of and to the rank derivative. For this, we define the rank component contributions

When is large, changes in rank are primarily dictated by changes in the population trajectories. In contrast, if dominates , the changes in rank are due to changes in individual trajectories.

3 Summary Measures for Rank Processes

Suppose we have a sample of trajectories that are subject-specific independently and identically distributed realizations of a smooth underlying process , for . It is then of interest to have measures that quantify longitudinal central tendency and stability of both subject-specific and population ranks that are functionals of the corresponding rank processes with as per (1) and . A beneficial feature of the rank process approach is that like other rank-based methods, the analysis does not depend on the scale of the data and allows for direct comparisons of different data sources and measurement scales through comparing the corresponding rank processes.

Subject-specific integrated rank

A natural way to summarize a subject’s overall rank is to integrate the subject’s rank trajectory over the time domain, i.e., to consider the subject-specific measure

| (4) |

Subject-specific rank volatility

It is also of interest to quantify how variable a subject is in terms of rank, which can be quantified by

| (5) |

Subject-specific rank dynamics

For smooth rank processes, one can define a rank derivative , . If it is non-zero, then the subject’s rank trajectory crosses the trajectories of other subjects, i.e., the rank of the subject will change over time. Pertinent measures include

| (6) |

quantifying how variable the rank of a subject is over the time interval.

Population rank stability

Since for all , we have that under mild assumptions. Although the mean functions are therefore not interesting, the variation of on subdomains is of interest, as it can pinpoint temporal regions where ranks tend to change and the intensity of pairwise crossings of the rank trajectories is high. We define time-dependent rank stability as

| (7) |

Integrating this quantity leads to an overall population rank stability coefficient, for which we choose

| (8) |

Note that if the underlying functional data never cross paths, then for all , and thus the overall rank stability is , while the closer is to 0, the lower is rank stability, i.e., the trajectories of the functional data exhibit more frequent crossings.

4 Estimation

The starting point is to estimate the rank trajectories . Suppose for all subjects, processes are observed on a regular dense grid on the time domain, i.e., there exists a design distribution function such that for and . We assume that the underlying surface is differentiable in both and . To obtain smooth estimates of the rank process, we utilize a kernel function , which is a pdf, and an integrated kernel , which is a cdf. Furthermore, we assume:

-

(A1)

With probability 1, the process has continuously differentiable sample paths and there exists a constant such that .

-

(A2)

The kernel is a symmetric pdf on such that,

The kernel is a cdf such that its derivative exists almost everywhere, is bounded on and is a symmetric pdf such that

-

(A3)

The kernel has a compact support, assumed to be . On , the first and second derivatives and exist and are bounded.

-

(A4)

The design distribution function is four times continuously differentiable on . There exist such that for all .

We provide two strategies for the estimation of based on the sample as follows.

Cross-sectional empirical distributions

The most straightforward approach to obtain a ranked sample from a dense functional sample is to estimate the empirical distribution at each time point . Obtaining cross-sectional empirical distributions in this manner is equivalent to taking cross-sectional ranks and scaling them, i.e.,

| (9) |

The empirical ranking defined in (9) has several benefits. It is very simple to implement, and its interpretation is very clear. However, since we aim to obtain differentiable rank functions that allow us to study the decomposition of rank dynamics into population and individual components, we need smooth estimates of the rank processes.

Smooth rank functions

Smooth estimation of conditional/cross-sectional distribution functions has been well investigated (e.g., Hall et al.,, 1999; Wu and Tian,, 2013; Veraverbeke et al.,, 2014; Belalia et al.,, 2017). Define

and for

where are bandwidths. Here, we utilize a kernel estimate of given by well-established methods described in Roussas, (1969) and Samanta, (1989),

| (10) |

Thus, a smooth estimator for the rank process can be obtained by

| (11) |

We will discuss the selection of bandwidths and in the Supplementary Material.

Using one of the two methods described above, we obtain the estimated rank for level at time , yielding the surface or , and hence estimate the measures , and given in (4)–(6), respectively, by plugging in either of the two estimators of , applying numerical integration. Estimation of the measures , and (6)–(8) requires the estimation of the rank derivatives , while identifying the components of the time-dynamic model as per (2) requires estimation of , , and .

For estimating , one can make use of local polynomial smoothing, or a similar method. To estimate and defined in (3), we take partial derivatives of (10), yielding

| (12) |

where

and for ,

where are bandwidths as in and .

For subject , the estimated components are

| (13) |

where is an estimate of the derivative for example by local polynomial smoothing. From these estimators we obtain the estimated decomposition The component contributions and may be estimated by numerically integrating the estimated components and ,

| (14) |

The measures in (6) can then be estimated by plugging in based on trajectory ; estimators for and in (7) and (8) are obtained using the sample mean of .

5 Theoretical Justifications

We demonstrate the asymptotic normality of , the joint asymptotic normality of , given a curve , and the asymptotic normality of . We denote convergence in distribution by , and define

All proofs and auxiliary results are in the Supplementary Material. Throughout, we use the notations and for the joint cdf and pdf of and , and also the notation , where indicates . We further need to assume:

-

(A5)

The partial derivatives are bounded over and , for .

-

(A6)

The partial derivatives , and are bounded over and .

The following proposition is similar to some results in literature, for example Roussas, (1969); we omit the proof. Theorem 1 is our main result. The proof and auxiliary lemmas are in the Supplementary Material.

Proposition 1.

Theorem 1.

By continuous mapping, the asymptotic normality of follows.

Corollary 1.

These results provide rates of convergence and theoretical justifications for the estimated rank dynamics.

6 Simulation

For the implementation of the dynamic model in Section 2 and the summary measures in Section 3, two important auxiliary parameters and are involved to obtain the kernel estimators for the rank trajectories and the two components, and , of the rank derivatives. In this section, we use simulations to evaluate the finite-sample performance of the bandwidth selection method in the Supplementary Material, and the kernel estimators for and in model (2).

Denote and as the probability density function and cumulative distribution function of the standard Gaussian distribution. Suppose we observe trajectories for subjects on a dense time grid , where , , , , , , , , , and , independently across . Hence, the true values of , and are respectively

To assess the performance of the cross-validation (CV) selected bandwidths , we compared the mean integrated squared errors (MISEs) of and obtained with the CV bandwidths as well as with the optimal choice given by

where is the set of bandwidth pairs considered,

and is the maximum value of considered. The impact of boundary effects is known to distort bandwidth selection and is removed by cutting off and in the integration.

In the simulations, we used , , and considered three different sample sizes , 50 and 200. The kernels and used in Sections 6 and 7 are the pdf and cdf of standard normal distributions truncated on , respectively. Specifically,

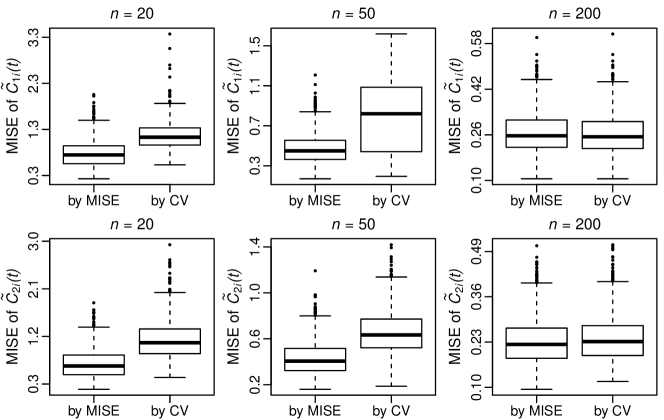

where and are the pdf and cdf of standard normal distributions, respectively. We use these kernels as in practical implementations they yield smooth estimates , , and , while the pdf kernel has a compact support. Boxplots of the MISEs corresponding to the optimal bandwidths chosen by MISE and CV in each of the 1000 Monte Carlo runs for , 50 and 200 are shown in Figure 1. The main message is that CV performs satisfactorily, as it tracks the optimal choice closely, especially for larger sample sizes .

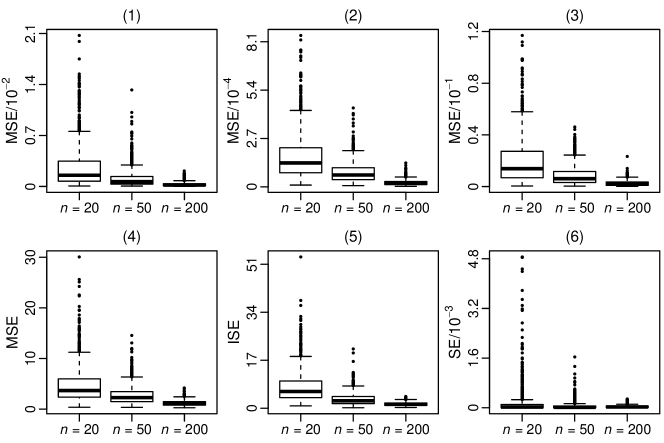

Boxplots of the MSEs, ISE or SE for the estimation of the rank summary measures (4)–(8) based on the kernel estimators and obtained with the optimal bandwidths chosen by CV are shown in Figure 2. Overall the proposed estimators are seen to converge fast to the true values as increases.

7 Applications

We demonstrate our methods with three functional datasets which are very different in nature. The first is the Zürich longitudinal growth data; the second is US median house price data at the county level; the third is based on the 2017 Major League Baseball (MLB) season, where our interest lies in offensive or hitting performances. We find that by transforming the original processes into rank processes we are able to find new and interesting characterizations for the individuals in each dataset.

7.1 Zürich Longitudinal Growth Data

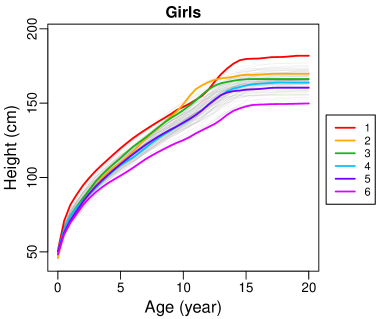

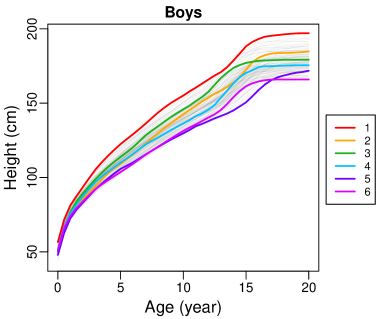

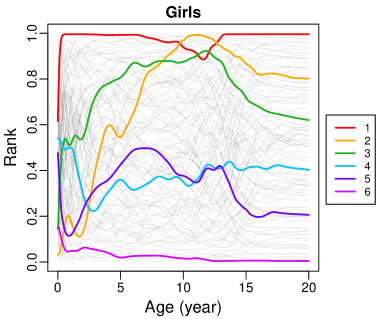

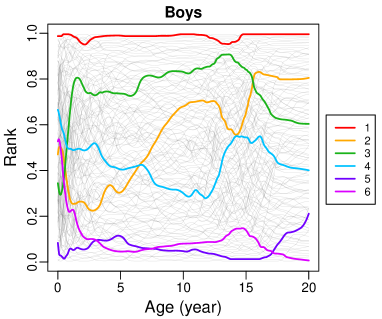

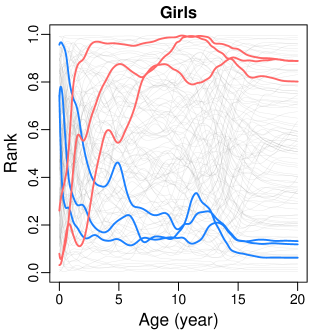

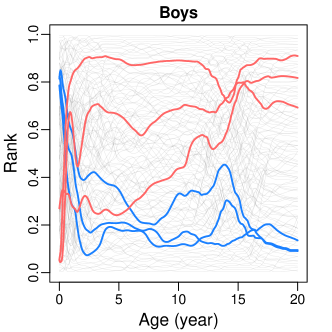

The Zürich longitudinal growth data consist of dense longitudinal height measurements for 112 girls and 120 boys from birth to age 20 and the measurements are known to contain very little noise (Gasser et al.,, 1990). It is helpful to compare the ranking for individuals; we highlight the same six girls and six boys throughout, with their height trajectories shown in Figure 3.

We find that the two ranking methods yield similar results, with the smooth rank functions resembling the empirical ranks. Visually, it is clear that taking a ranked perspective with functional data is appealing. For example, from Figure 4, Girl 1 and Boy 1 are seen to be generally tall throughout, and Girl 2 and Boy 2 are seen to have volatile ranks as they age. Ranks are fairly stable from ages 5 until 10 and 12 for girls and boys, respectively; subsequently, the ranks are more dynamic, with higher volatility.

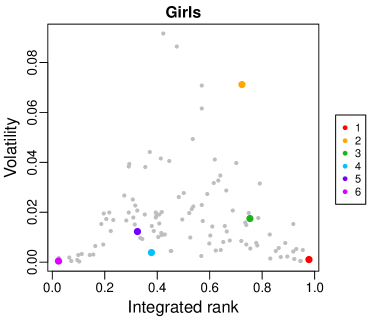

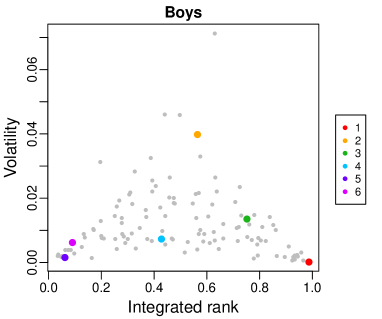

We also obtained the estimates of the rank summary statistics (4)–(8) for the Zürich longitudinal growth data, based on the smooth ranks defined in (11). In Figure 5 we see that Girl 1 and Boy 1 have very high ranks and that the ranks are almost constant throughout. On the other hand, we find that Girl 2 and Boy 2 have overall middle ranks that are quite volatile. The rank volatility plots are bell-shaped, as subjects with integrated ranks near 0 and 1 cannot have high volatility. On the other hand, subjects with moderate integrated ranks have less restricted volatility. We also highlight the subjects with the highest and lowest values of the subject-specific rank increases from start to end as in (6) in Figure 6, where captures the overall ranking trend for a subject, i.e., subjects with large values of have large increases or decreases in ranks from the beginning to the end of the time domain.

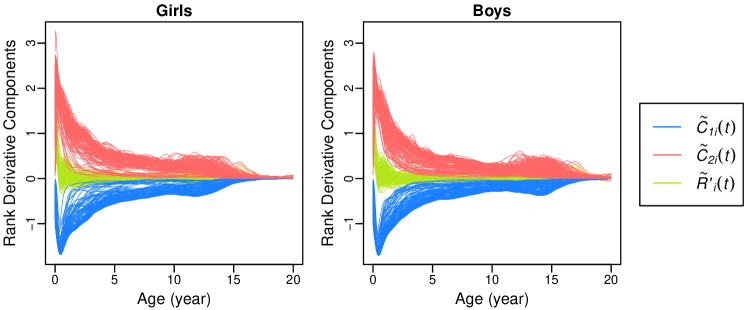

We also applied the rank decomposition (2) to the Zürich growth data. Figure 7 shows the rank derivative decomposition for all subjects in the study. The population trends quantified by the negative terms tend to lower an individual’s rank as the population of children at large is growing, while individuals are also growing as reflected by the positive terms . For the growth data, this decomposition indicates that the population and individual components of the rank derivative are roughly equal in size. Indeed, the estimated contributions from the first component for girls and boys are 0.487 and 0.486, with and 0.514, respectively, for the second component. We conclude that in human growth an individual’s change in rank is the result of a fine balance of individual growth which is counterbalanced by population trends in growth when considering individual rank trajectories. Rank volatility is seen to increase during times of growth spurts, where the population tends to grow relatively fast while individuals may have accelerated or delayed growth, with resulting rank changes.

7.2 House Price Data

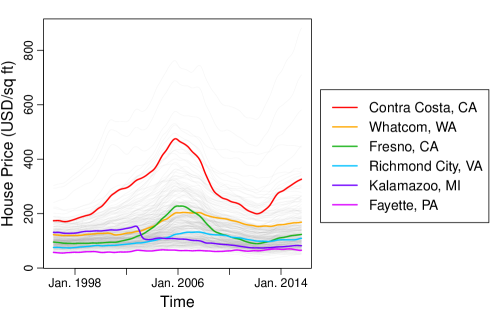

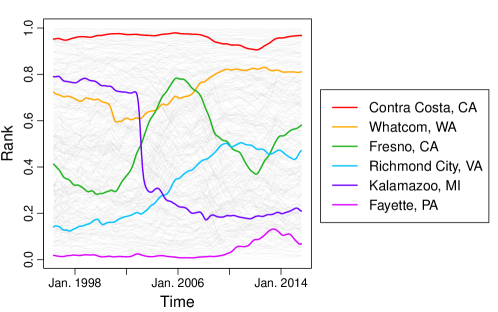

House price data are available from Zillow. We consider here monthly longitudinal median house prices after inflation adjustment for house transactions in 306 counties in the US from May 1996 to August 2015. To compare the ranking for individual markets, we highlight the same six counties throughout, as in Figure 8. Adopting the smooth rank function version defined in (11), in Figure 9 house prices in Contra Costa and Fayette are seen to be generally high and low throughout, respectively, and those in Fresno are seen to have significant rank variation. We find that ranks were fairly stable before 2002 and became more dynamic afterward.

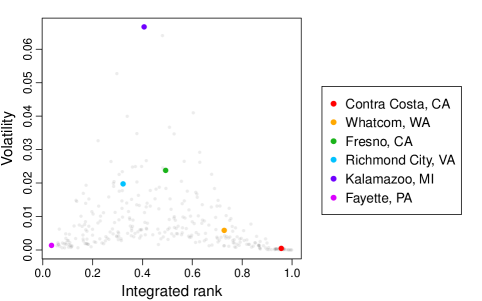

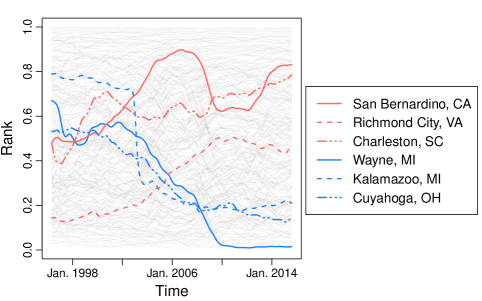

We also estimated the rank summary statistics for the house price data. In Figure 10 we see that Contra Costa county and Fayette county have very high and low ranks respectively and that their ranks were almost constant throughout the time period considered. On the other hand, we find that Kalamazoo has moderate ranks that are very volatile. These findings are in agreement with Figure 9 and the rank volatility plot has a similar shape to that in Figure 5, as expected. Highlighting the counties with the highest and lowest gains in rank as in (6) in Figure 11, we find that the magnitudes of difference in ranks between the beginning and the ending for the house price data are not as large as those for the Zürich growth curves.

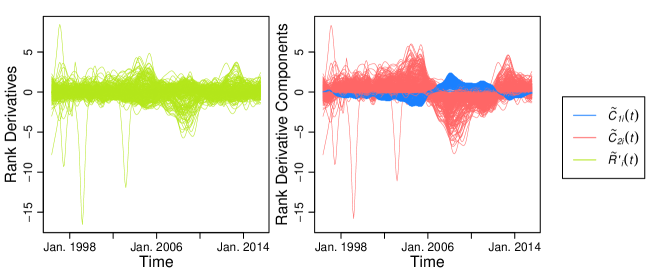

We also applied the dynamic rank decomposition (2) to the house price curves. Figure 12 shows the rank derivative decomposition for all counties in the study. The house price ranks were more volatile a few years before and after the 2008 financial crisis. The population components also reveal that county median house prices were increasing in general before 2006, turned to drop from 2007, and then gradually recovered and increased again since 2012. The individual component is seen to contribute more to the rank derivative than the population component. This is also reflected by the estimated contributions from the two components, and , as per (14). As shown in Figure 8, a general trend cana be discerned from the house price trajectories: Prices initially increased until 2005, decreased from 2005 to 2012, and then increased again. The house price population dynamics points predominantly downwards until 2008, with individual markets exercising strong counterforces; this means a county where price growth was sluggish fell back in rank; the opposite happened between 2008 and 2012 — a county where house prices were stable was gaining against the population and its rank increased.

7.3 Major League Baseball Offensive Data

Another area where relative rank is important is in sports. Major League Baseball (MLB) teams routinely spend over $100 million on player salaries every year. It is therefore of paramount interest to rank players in terms of ability so that teams can invest efficiently in individual players. Although there are many factors which contribute to the overall value of a player, one of the most important is offensive performance, and accordingly we focus on ranking MLB players in terms of offense.

Baseball has recently become a game dominated by statistics (see Baumer and Zimbalist,, 2013; Silver,, 2012, and the movie Moneyball for instance). As such, statisticians and sabermetricians look for simple yet informative measures for assessing player performance. By far, the most widely used statistic to quantify offensive performance is the batting average (BA), which is the number of hits a player has divided by the number of attempts. While the batting average is simple to understand, it has several shortcomings; for example, late in the season, when the number of attempts or at-bats is high, the average will not easily reveal changes in performance.

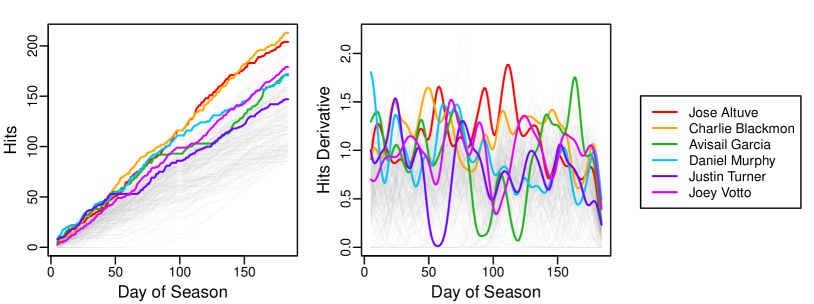

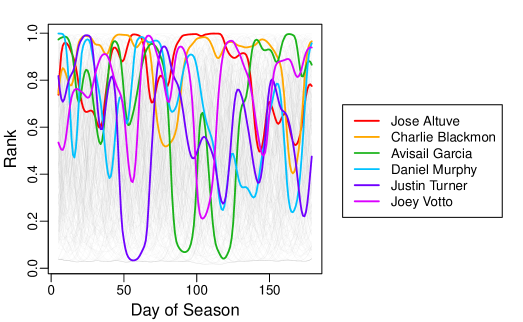

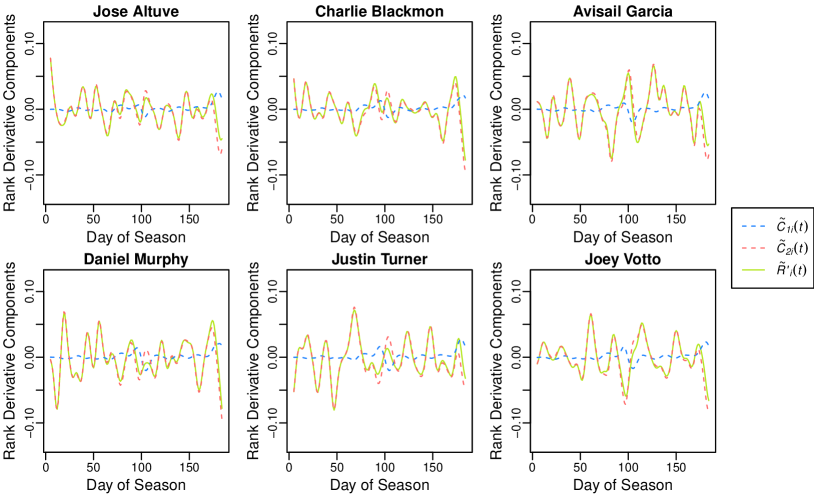

In light of the drawbacks of using batting average as a response, we tracked the number of hits a player accrued for each day in the 2017 MLB season (http://www.baseballmusings.com/), and then took the derivative of this trajectory, which we used as our functional response. This derivative can be viewed as a local batting average, or the change in hits divided by the change in days. It is thus less affected by long-term history because it is an instantaneous measure. This response therefore characterizes the heat of a player, which is the level of their current performance. The original hits trajectories and corresponding hits derivatives trajectories in Figure 13, obtained by local polynomial smoothing, are our starting point for the rank analysis. The objective is to quantify the player’s ranks and changes in ranks in this dataset, aiming to identify top players. We first transform the hit derivative trajectories into rank trajectories using the smooth representation in (11), visualized in Figure 14, where the differences in rank for the six highlighted players are highlighted. For example, this visualization makes it clear that Joey Votto improved drastically throughout the season, moving from a rank near 0.25 at the beginning of the season, to finishing with a rank of nearly 1.

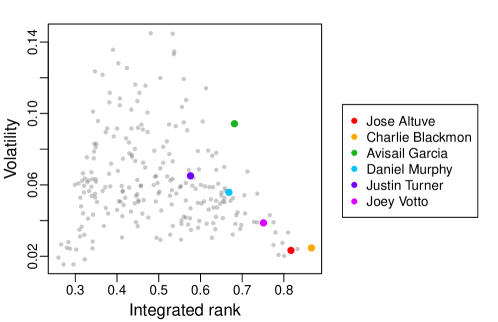

We also applied the rank summary statistics, which prove to be informative. The rank volatility versus integrated rank plot, shown in Figure 15 has direct applications in assessing offensive performance from the 2017 MLB season. Naturally, all six of the highlighted players have relatively high ranks. In addition to average performance, we can see that two of the players, Jose Altuve and Charles Blackmon, had high integrated rank and low volatility, which are two features of the most valuable players. These players are consistently performing at a high level with respect to the rest of the sample. As shown in Figure 15, the player with the highest integrated rank and fairly low volatility is Charlie Blackmon. Taking the viewpoint of a team deciding on which players to acquire, this plot also allows one to select players who have modest average ranks but have low volatility. Players of this type are desirable when looking for consistent backup players, for example. Finally, the player-specific change in ranks as per (6) quantifies whether players are generally improving or deteriorating over the season.

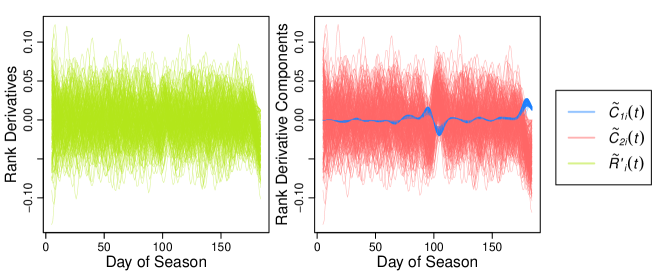

When fitting the rank derivative decomposition model (2) to these baseball data, we find that the subject specific component contributes much more than the population component . This is not surprising as the population of hits derivative curves , does not have a very clear pattern. Thus rank is determined to a large extent by individual effort alone, with estimated contributions for the population component and for the individual component. This is visualized in Figures 16 and 17, where the second component is seen to dominate the first. In addition, an ascent followed by a descent period can be seen in the population component curves around Day 100. This is due to the “All Star Break”, which is a break for all the players except the All Stars. i.e., the best players from each team, who play in an exhibition game. Thus, the hits derivatives decrease toward zero for almost all players during the break and then recover after the games are resumed. Hence the population components first ascend and then descend accordingly. The ascending phase of the population component near the end of the season is due to the same reason, i.e., fewer games are available at that time.

Finally, the overall rank stability coefficient in (8), which is an overall scaled measure of how variable the rank trajectories are, can be used to compare all three functional data set that we have considered, i.e., the Zürich growth data, the housing price data and the baseball player data. The estimates of based on the smooth rank estimation are shown in Table 1. The baseball players’ rank curves have the lowest stability, with the most volatility of ranks and a much higher degree of crossing trajectories. Moreover, the rank trajectories are not much influenced by population trends. In the Zürich growth and house price data, we observe much higher degrees of stability, with the highest level of rank stability and associated lowest rank volatility for the growth data. Especially for the growth data, crossings of rank trajectories are not common. Rank trajectories for the housing data and even more so for the growth data are driven to a large extent by population trends, where population distributions uniformly move to higher levels for the growth data with increasing age, while they have increasing and decreasing phases for the house price data. Notably, for the growth data, the trajectory dynamics are driven in equal parts by population trends and individual growth patterns, while for the housing price data population trends play a slightly smaller role.

| Zürich growth | House price | Baseball | |

| Girls | Boys | ||

| 0.9866 | 0.9883 | 0.4500 | |

8 Discussion

Cross-sectional ranking of functional data is a powerful tool for exploratory functional data analysis. To the best of our knowledge, the proposed perspectives in this paper are new to the field of functional data analysis and allow for quantification of the rank dynamics of a stochastic process. These methods are simple to understand and straightforward to implement. The decomposition of rank dynamics into population and individual components allows to better understand the forces that shape observed rank trajectories, and the summary measures of rank volatility, rank stability and rank gain are useful.

For the estimation of the two components and in (3), we could alternatively use local quadratic regression. This would be asymptotically equivalent to the kernel estimator in (12) under regularity assumptions on the smoothness of weight functions and the shape of kernels (Müller,, 1987). However, the kernel method we employ here has an explicit form which facilitates theoretical derivations, and makes implementation straightforward, while the local quadratic regression involves the inverse of a matrix of dimension at least . This provides strong motivation for the proposed method.

Our estimation methods and theory are geared towards densely observed functional data. One possible approach for the case of sparsely observed functional data is to divide the time domain into bins in a preprocessing step, followed by estimating the cross-sectional distribution at time by using local Fréchet regression (Petersen and Müller,, 2019) based on the preliminary distributions observed at the midpoints of the bins – these are the empirical distributions derived from the observations falling into each bin. The two components can then be obtained, e.g., by taking difference quotients of the cross-sectional distribution estimates. To work out the details and full theoretical justification of such a method will be a future research project.

Acknowledgements

Funding: This work was supported by NSF Grant DMS-1712864.

Appendices

Appendix A Bandwidth Selection for the Kernel Estimator

It is important to provide a data-driven approach for bandwidth selection for the kernel estimator in (10). For a complete discussion on optimal bandwidth selection for nonparametric conditional distribution and quantile functions, see Li et al., (2013). A simple objective function used in this paper is

where is the maximum value considered for , and is the leave-one-out kernel estimator.

Alternative methods for selecting bandwidths include independently choosing the optimal bandwidths in the and directions, and also using cross-validation schemes for bandwidth selection in the nonparametric cross-sectional distribution estimation. To accelerate the cross-validation process, -fold cross validation can be used instead when the sample size is relatively large. One can also perform the cross-validation on a random subset with indices rather than the entire sample. Another method is changing the sampling unit in the cross validation from single pairs to trajectories/subjects, i.e., performing one-curve-left-out cross-validation or assigning subsets of pairs to training or test sets in -fold cross-validation.

Appendix B Details on Theoretical Results

To derive the asymptotic normality for , and , we first need to calculate the means, variances of and (some) covariances between , for . For completeness, we include auxiliary Lemma 1 and 2, which are well-known. Proof can be found in, e.g., Rosenblatt, (1956), Roussas, (1969), Silverman, (1986), Samanta, (1989), Stoker, (1993), Jones, (1994), and Cai and Roussas, (1999).

Lemma 1.

Lemma 2.

Let be a 2-dimensional random vector. Assume that the joint density and cdf of , and , are twice and three times continuously differentiable, respectively. Under assumption (A2), for any , as ,

Define

and for ,

Lemma 3.

Assume (A2)–(A6). Furthermore, assume that the cross-sectional density and cdf at any time are twice and three times continuously differentiable, respectively, and that the joint density and cdf at times and are continuous and twice continuously differentiable, respectively. Arbitrarily fix and . For and , as : For , ,

For , ,

For , ,

Lemma 4.

Proof.

We prove the convergence rate of as the other proofs are analogous. Define

The derivative of is computed as

where all the terms are uniform over and . Hence, with such that and lying between and such that ,

since

∎

Proof of Theorem 1.

With the optimal bandwidths of the order and and by Lemma 4, as ,

Under the assumption , it suffices to show the asymptotic normality of . By the CLT, as ,

Note that and . Denote

By Slutsky’s theorem, as ,

where . By the continuous mapping theorem, as ,

where . Thus as ,

where by Lemma 3,

For a given curve , the two components of the rank derivative and the corresponding estimates are , , and , , respectively. Again by Slutsky’s theorem, the proof is complete. ∎

References

- Barnett et al., (2010) Barnett, R. C., Bhattacharya, J., and Bunzel, H. (2010). Choosing to keep up with the Joneses and income inequality. Economic Theory, 45(3):469–496.

- Baumer and Zimbalist, (2013) Baumer, B. and Zimbalist, A. (2013). The Sabermetric Revolution: Assessing the Growth of Analytics in Baseball. University of Pennsylvania Press.

- Belalia et al., (2017) Belalia, M., Bouezmarni, T., and Leblanc, A. (2017). Smooth conditional distribution estimators using Bernstein polynomials. Computational Statistics & Data Analysis, 111:166–182.

- Cai and Roussas, (1999) Cai, Z. and Roussas, G. G. (1999). Weak convergence for smooth estimator of a distribution function under negative association. Stochastic Analysis and Applications, 17(2):145–168.

- Chen and Fan, (2018) Chen, T. and Fan, Q. (2018). A functional data approach to model score difference process in professional basketball games. Journal of Applied Statistics, 45(1):112–127.

- Cho et al., (2016) Cho, H., Hong, H. G., and Kim, M.-O. (2016). Efficient quantile marginal regression for longitudinal data with dropouts. Biostatistics, 17(3):561–575.

- Dai et al., (2018) Dai, X., Tao, W., and Müller, H.-G. (2018). Derivative principal components for representing the time dynamics of longitudinal and functional data. Statistica Sinica, 28:1583–1609.

- Falk, (1984) Falk, M. (1984). Relative deficiency of kernel type estimators of quantiles. Annals of Statistics, 12(1):261–268.

- Gasser et al., (1990) Gasser, T., Kneip, A., Ziegler, P., Largo, R., and Prader, A. (1990). A method for determining the dynamics and intensity of average growth. Annals of Human Biology, 17(6):459–474.

- Hall and Van Keilegom, (2007) Hall, P. and Van Keilegom, I. (2007). Two-sample tests in functional data analysis starting from discrete data. Statistica Sinica, 17(4):1511–1531.

- Hall et al., (1999) Hall, P., Wolff, R. C. L., and Yao, Q. (1999). Methods for estimating a conditional distribution function. Journal of the American Statistical Association, 94(445):154–163.

- Hegland et al., (2009) Hegland, M., Hooker, G., and Roberts, S. (2009). Finite element thin plate splines in density estimation. ANZIAM Journal, 42:712–734.

- Horvath and Kokoszka, (2012) Horvath, L. and Kokoszka, P. (2012). Inference for Functional Data with Applications. Springer, New York.

- Jones, (1994) Jones, M. (1994). On kernel density derivative estimation. Communications in Statistics - Theory and Methods, 23(8):2133–2139.

- Kim, (2007) Kim, M.-O. (2007). Quantile regression with varying coefficients. Annals of Statistics, 35(1):92–108.

- Kim and Yang, (2011) Kim, M.-O. and Yang, Y. (2011). Semiparametric approach to a random effects quantile regression model. Journal of the American Statistical Association, 106(496):1405–1417.

- Kürüm et al., (2018) Kürüm, E., Hughes, J., Li, R., and Shiffman, S. (2018). Time-varying copula models for longitudinal data. Statistics and Its Interface, 11(2):203–221.

- Li et al., (2013) Li, Q., Lin, J., and Racine, J. S. (2013). Optimal bandwidth selection for nonparametric conditional distribution and quantile functions. Journal of Business & Economic Statistics, 31(1):57–65.

- Martin-Barragan et al., (2016) Martin-Barragan, B., Lillo, R., and Romo, J. (2016). Functional boxplots based on epigraphs and hypographs. Journal of Applied Statistics, 43(6):1088–1103.

- Müller, (1987) Müller, H.-G. (1987). Weighted local regression and kernel methods for nonparametric curve fitting. Journal of the American Statistical Association, 82(397):231–238.

- Müller et al., (2006) Müller, H.-G., Stadtmüller, U., and Yao, F. (2006). Functional variance processes. Journal of the American Statistical Association, 101:1007–1018.

- Müller and Yao, (2010) Müller, H.-G. and Yao, F. (2010). Empirical dynamics for longitudinal data. Annals of Statistics, 38(6):3458–3486.

- Nguyen, (2016) Nguyen, H. V. (2016). Keeping up with the Joneses: Neighbourhood wealth and hypertension. Journal of Happiness Studies, 17(3):1255–1271.

- Petersen and Müller, (2019) Petersen, A. and Müller, H.-G. (2019). Fréchet regression for random objects with Euclidean predictors. The Annals of Statistics, 47(2):691–719.

- Ramsay and Silverman, (1997) Ramsay, J. and Silverman, B. (1997). The Analysis of Functional Data. Springer-Verlag, Berlin.

- Ramsay et al., (2007) Ramsay, J. O., Hooker, G., Campbell, D., and Cao, J. (2007). Parameter estimation for differential equations: A generalized smoothing approach (with discussion). Journal of the Royal Statistical Society: Series B (Statistical Methodology), 69(5):741–796.

- Ramsay and Ramsey, (2002) Ramsay, J. O. and Ramsey, J. B. (2002). Functional data analysis of the dynamics of the monthly index of nondurable goods production. Journal of Econometrics, 107(1-2):327–344.

- Rosenblatt, (1956) Rosenblatt, M. (1956). Remarks on some nonparametric estimates of a density function. Annals of Mathematical Statistics, 27(3):832–837.

- Roussas, (1969) Roussas, G. G. (1969). Nonparametric estimation of the transition distribution function of a Markov process. Annals of Mathematical Statistics, 40(4):1386–1400.

- Samanta, (1989) Samanta, M. (1989). Non-parametric estimation of conditional quantiles. Statistics & Probability Letters, 7(5):407–412.

- Silver, (2012) Silver, N. (2012). The Signal and the Noise: Why Most Predictions Fail – but Some Don’t. Penguin.

- Silverman, (1986) Silverman, B. W. (1986). Density Estimation for Statistics and Data Analysis. Monographs on Statistics and Applied Probability. Chapman and Hall, London.

- Stoker, (1993) Stoker, T. M. (1993). Smoothing bias in density derivative estimation. Journal of the American Statistical Association, 88(423):855–863.

- Tian and Wu, (2014) Tian, X. and Wu, C. O. (2014). Estimation of rank-tracking probabilities using nonparametric mixed-effects models for longitudinal data. Statistics and Its Interface, 7(1):87–99.

- Veraverbeke et al., (2014) Veraverbeke, N., Gijbels, I., and Omelka, M. (2014). Preadjusted non-parametric estimation of a conditional distribution function. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76(2):399–438.

- Vinué and Epifanio, (2017) Vinué, G. and Epifanio, I. (2017). Archetypoid analysis for sports analytics. Data Mining and Knowledge Discovery, 31(6):1643–1677.

- Wang et al., (2016) Wang, J.-L., Chiou, J.-M., and Müller, H.-G. (2016). Functional data analysis. Annual Review of Statistics and Its Application, 3:257–295.

- (38) Wang, S., Jank, W., and Shmueli, G. (2008a). Explaining and forecasting online auction prices and their dynamics using functional data analysis. Journal of Business and Economic Statistics, 26:144–160.

- (39) Wang, S., Jank, W., Shmueli, G., and Smith, P. (2008b). Modeling price dynamics in eBay auctions using principal differential analysis. Journal of the American Statistical Association, 103:1100–1118.

- Wu and Tian, (2013) Wu, C. O. and Tian, X. (2013). Nonparametric estimation of conditional distributions and rank-tracking probabilities with time-varying transformation models in longitudinal studies. Journal of the American Statistical Association, 108(503):971–982.

- Wu and Perloff, (2005) Wu, X. and Perloff, J. M. (2005). China’s income distribution, 1985–2001. Review of Economics and Statistics, 87(4):763–775.