Abstract

The concept of a Lévy subordinator is generalized to a family of non-decreasing stochastic processes, which are parameterized in terms of two Bernstein functions. Whereas the independent increments property is only maintained in the Lévy subordinator special case, the considered family is always strongly infinitely divisible with respect to time (IDT), meaning that a path can be represented in distribution as a finite sum with arbitrarily many summands of independent and identically distributed paths of another process. Besides distributional properties of the process, we present two applications to the design of accurate and efficient simulation algorithms. First, each member of the considered family corresponds uniquely to an exchangeable max-stable sequence of random variables, and we demonstrate how the associated extreme-value copula can be simulated exactly and efficiently from its Pickands dependence measure. Second, we show how one obtains different series and integral representations for infinitely divisible probability laws by varying the parameterizing pair of Bernstein functions, without changing the law of one-dimensional margins of the process. As a particular example, we present an exact simulation algorithm for compound Poisson distributions from the Bondesson class, for which the generalized inverse of the distribution function of the associated Stieltjes measure can be evaluated accurately.

keywords:

strong infinitely divisible w.r.t. time; subordinator; infinitely divisible law; Pickands dependence function; Bondesson class; Bernstein function.sectioning ection]subsection \setkomafontcaptionlabel

Subordinators which are infinitely divisible w.r.t. time: Construction, properties, and simulation of max-stable sequences and infinitely divisible laws

Jan-Frederik Mai111Technische Universität München, Parkring 11, 85478 Garching–Hochbrück, mai@tum.de. and Matthias Scherer222Technische Universität München, Parkring 11, 85478 Garching–Hochbrück, scherer@tum.de.

Version of March 9, 2024

2010 AMS Subject Classification: 60G51; 60G70; 60G09.

1 Introduction

We recall that a Lévy subordinator is a non-decreasing stochastic process on a probability space with independent and stationary increments, whose paths are almost surely right-continuous and start at , see [Bertoin (1999)] for a textbook treatment. Intuitively, Lévy subordinators are the continuous-time analog of discrete-time random walks with non-negative increments. The law of , that is its finite-dimensional distributions, is fully determined by the law of any random variable with , whose Laplace transform is given by

| (1) |

where the so-called Lévy measure satisfies the condition and is a drift constant. The function is a so-called Bernstein function, see [Schilling et al. (2010)] for a textbook treatment, and the number is called the killing rate of , because it corresponds to an exponential rate at which jumps to the absorbing graveyard state , i.e. is “killed.” The so-called Lévy–Khinchin formula (1) establishes a one-to-one correspondence between Bernstein functions and Lévy subordinators, so that (or equivalently the pair ) provides a convenient analytical description of the law of .

The purpose of the present article is to embed the concept of a Lévy subordinator into a larger family of non-decreasing processes that can be parameterized in terms of a pair of two Bernstein functions. On the one hand, the enlarged family of processes still satisfies the concept of being strongly infinite divisible with respect to time, as explained below, which renders it a natural generalization from an algebraic viewpoint. On the other hand, our generalization is inspired by two practical applications: Firstly, the processes can be used to construct and simulate multivariate extreme-value distributions. Second, they provide a reasonable framework to derive series representations for infinitely divisible laws on the positive half-axis, which can be used for simulation.

For a pair of a distribution function of some non-negative random variable with finite, positive mean and a Lévy subordinator without drift, the present article studies distributional properties of the stochastic process

| (2) |

the integral being defined pathwise in the usual Riemann–Stieltjes sense, and . By definition, (using the notations and ), the path is almost surely non-decreasing and right-continuous, and for . We call a pair admissible, whenever is not almost surely equal to the trivial process . Our interest in this semi-parametric family of stochastic processes is fueled both by theoretical and practical aspects. In the following Section 2 we study distributional properties, whereas Sections 3 and 4 give applications of the presented class of processes to the design of simulation algorithms. More precisely, the following list outlines the organization of the remaining article and the contributions made:

-

•

Section 2: It turns out that is strongly infinitely divisible with respect to time (strong IDT)333This property is called time-stable in [Kopp, Molchanov (2018)]., meaning that for arbitrary we have the distributional equality

where , , denote independent copies of . In particular, from the viewpoint of the theory on infinite divisibility, the considered family of stochastic processes is a natural extension of the concept of a Lévy subordinator. Lévy subordinators arise in the special case when corresponds to a Bernoulli distribution with success probability , see Example 2.7. Strong IDT processes have first been introduced in [Mansuy (2005)] and further examples have been studied in [Es-Sebaiy, Ouknine (2008), Hakassou, Ouknine (2012)]. These references give some examples of strong IDT processes with an emphasis on Gaussian processes. A LePage series representation for strong IDT processes without Gaussian component, in particular for non-decreasing strong IDT processes, is derived in [Kopp, Molchanov (2018)] and has been refined in the non-decreasing case by [Mai (2018b)].

We demonstrate how several distributional properties of can be inferred conveniently from the parameterizing pair , thus pave the way to an analytical treatment of via its parameters. In particular, in addition to the defining integral representation we present an integration-by-parts formula and a canonical LePage series representation for in the spirit of [Kopp, Molchanov (2018)]. Section 2.3 studies the natural filtration of the process . While Lévy subordinators have independent increments, we demonstrate how the support of the probability measure controls the ability of to “see into the future.” In particular, for a compound Poisson subordinator and support of bounded, the increment can be decomposed into a sum of one part that is measurable with respect to , and another part that is independent thereof. This peculiar property might be one explanation as to why strong IDT processes are, so far, not very well studied.

-

•

Section 3: Due to [Mai, Scherer (2014), Theorem 5.3], a sequence of -valued random samples drawn from the random distribution function is an exchangeable min-stable exponential sequence, meaning that has an exponential distribution with rate , , and (not all zero). Equivalently, is an exchangeable max-stable sequence. If has unit mean, i.e. if , the associated function is called a stable tail dependence function, defined on the set of non-negative sequences that are eventually zero. The stable tail dependence function uniquely characterizes the law of and, equivalently, the law of . Since min- (resp. max-) stability is closely related to multivariate extreme-value theory, an understanding of the law of is thus tantamount with the understanding of an associated family of multivariate extreme-value copulas. In particular, a simulation algorithm for the random vector is equivalent to one for the associated extreme-value copula.

Section 3 shows how the random vector can be simulated exactly. To this end, we make use of a simulation algorithm from [Dombry et al. (2016)], which requires to simulate from the so-called Pickands dependence measure associated with , a finite measure on the -dimensional unit simplex. In the present situation, we demonstrate how this simulation can be achieved efficiently and accurately.

-

•

Section 4: Fixing , the random variable has an infinitely divisible law on , which is invariant with respect to many changes in the parameterizing pair . This fact can be used to derive different series representations for the same infinitely divisible law from Definition (2), when either is of compound Poisson type or the support of is bounded. In spirit, this methodology is quite similar to seminal ideas in [Bondesson (1982)], who proposes alternative series representations for infinitely divisible laws on . Section 4 demonstrates how the -parameterization of provides a very convenient setting to derive a simulation algorithm for distributions from the so-called Bondesson class, whenever the Stieltjes measure is given in a more convenient form than the Lévy measure. In fact, if is chosen as a compound Poisson subordinator with unit exponential jumps, the definition of defines a bijection between the Bondesson class and distributions having finite mean and left-end point of support equal to zero.

Finally, Section 5 concludes and an appendix contains the technical proofs.

2 Anatomy of the process

2.1 Technical preliminaries

Throughout, we denote by a (possibly killed) Lévy subordinator without drift and with Lévy measure on , i.e. with killing rate . We assume that is non-zero, i.e. is not identically zero. Its associated Bernstein function is denoted by

implicitly using the short-hand notations and in order to enforce .

Remark 2.1 (Why driftless?)

A positive drift of the Lévy subordinator would imply a drift of the process , namely

| (3) |

On the one hand, this is inconvenient, because it requires an additional integrability condition on , so that (3) exists at all. We will later postulate that satisfies , which is a weaker condition. For instance, the distribution function is admissible in the sequel but does not satisfy (3). On the other hand, the assumption of a driftless Lévy subordinator is without loss of generality. To explain this, we will see that falls into the family of non-decreasing strong IDT processes. It follows from a structural result in [Mai (2018b)] that, just like for the subfamily of Lévy subordinators, such processes can be decomposed uniquely into , with a drift and a non-decreasing strong IDT process without drift. This allows us to concentrate our study on the driftless case, because the more general case is simply obtained by adding a drift a posteriori.

For later reference, we introduce the following sets of distribution functions (cdfs)

It is convenient to study the law of in terms of the function

for , arbitrary, and .

Lemma 2.2 (Laplace exponent of )

Let , arbitrary, and . Then

Proof

See the Appendix.

We view as a mapping from the set of sequences, which are eventually zero, to . The substitution shows that is homogeneous of order one, that is

for . In the case and this implies in particular that the random variable is infinitely divisible for each . The mapping specifies the law of uniquely, i.e. its finite-dimensional distributions. This is due to the fact that the law of the random vector is uniquely determined by the values of its multivariate Laplace transform on , which follows from the Stone–Weierstrass Theorem (polynomials are dense in the space of continuous functions on ). Consequently, the mapping , which in turn by Lemma 2.2 is specified by and , is a convenient analytical description for the law of .

Since is right-continuous, so is for each fixed . This implies that is almost surely right-continuous as integral over right-continuous functions. The condition in the definition of implies , which results in a.s.. The condition in the definition of is necessary (but needs not be sufficient) to have for . In order to explain this, we recall [Mai (2018a), Lemma 3], which is required several times later on.

Lemma 2.3 (Bernstein functions associated with )

For the function

| (4) |

is a Bernstein function, and the mapping is a bijection between and the set of Bernstein functions without drift. The Lévy measure associated with is determined in terms of by the equation , , where denotes the generalized inverse of . The inverse mapping from the set of Lévy measures on to is given by

where denotes the generalized inverse of .

Proof

See [Mai (2018a), Lemma 3].

Lemma 2.3 implies in particular that the integral is finite for all if and only if it is finite for a single fixed . Now is equivalent to and from Lemma 2.2 we see that this necessarily requires to be finite for those on which puts mass, hence, in particular .

While the condition in the definition of is necessary to prevent the non-interesting case , we have claimed that this this needs not be sufficient but depends on the specific choice of and . To this end, we introduce the set

of -admissible distribution functions.

Lemma 2.4 (Admissibility)

The following statements are equivalent.

-

(a)

is admissible, i.e. .

-

(b)

, i.e. .

-

(c)

for arbitrary and .

Proof

See the Appendix.

Example 2.5 ( in compound Poisson case)

Let be a (driftless) compound Poisson subordinator with intensity and jump size distribution , where denotes a generic jump size random variable on with Laplace transform . It follows that and

Since , for we obtain by concavity of , which implies for those compound Poisson subordinators whose jump size distribution has finite mean.

As already mentioned, for each the random variable is infinitely divisible. We denote the Bernstein function associated with by

| (5) |

The last equality follows for from Lemma 2.2 in the special case and for general by the facts that (i) the right-hand side of (5) defines a Bernstein function as mixture of Bernstein functions and (ii) a Bernstein function is uniquely determined by its values on , see [Gnedin, Pitman (2008), p. 36].

Lemma 2.6 derives two alternative stochastic representations of the process . The LePage representation in part (b) is a particular special case of a result from [Kopp, Molchanov (2018), Theorem 4.2].

Lemma 2.6 (Alternative stochastic representations)

Let be an admissible pair, i.e. .

-

(a)

Integration-by-parts-formula:

-

(b)

LePage series representation:

Let be an iid sequence drawn from the probability measure . Independently, let be an iid sequence of unit exponential random variables. We then have the following equality in distribution:

Proof

See the Appendix.

Example 2.7 (The special case of a Lévy subordinator)

Suppose that for , with associated Bernstein function

An arbitrary (driftless) Lévy subordinator leads to an admissible pair and obviously we have . So statement (b) in Lemma 2.6 provides an infinite series representation for an arbitrary Lévy subordinator , namely

| (6) |

In the special case when is a standard (unit intensity) Poisson process, this formula boils down to the well-known counting process representation

| (7) |

Representation (6) is a quite natural generalization of (7), and by Lemma 2.6(b) it is general enough to comprise all Lévy subordinators. In particular, it is worth mentioning that the probability law of the is , which can be any probability law on . This means that, conversely, if is an arbitrary probability law on and is an iid sequence drawn from , (6) defines a Lévy subordinator without drift and with associated Lévy measure .

2.2 Distributional properties

Recall that an infinitely divisible distribution on is of compound Poisson type if its associated Bernstein function is bounded, i.e. .

Lemma 2.8 (When does have a compound Poisson distribution?)

Let be admissible. The Bernstein function is bounded if and only if the following two conditions are satisfied:

-

(a)

is bounded, i.e. is a compound Poisson subordinator.

-

(b)

is bounded, i.e. the random variable has bounded support.

Proof

See the Appendix.

Recall that an infinitely divisible law on is said to have killing, if it assigns positive mass to , which is the case if and only if its associated Lévy measure satisfies . In terms of the associated Bernstein function , this means for all positive . In this case, we also say that the Bernstein function has killing.

Lemma 2.9 (When does have a positive killing rate?)

Let be admissible. The Bernstein function has killing if and only if at least one of the following two conditions is satisfied:

-

(a)

has killing, i.e. the left end point of the support of is strictly positive.

-

(b)

has killing, i.e. .

Proof

See the Appendix.

Since we are only interested in a description of the probability law of , it is helpful to briefly ponder on potential redundancies, i.e. to investigate the question: When do two different pairs lead to exactly the same probability law of the associated processes ? To address this issue in a mathematically rigorous manner, we introduce the equivalence relation

The equivalence class of an admissible pair is denoted by , or also by , in the sequel. Determining the equivalence class of a pair is surprisingly involved. It is not difficult, however, to see that for an admissible pair the equivalence class is invariant with respect to . Depending on the admissible pair, there can be even more redundancies, as the following example demonstrates.

Example 2.10 (The curious case Fréchet distribution)

With a parameter and consider the Fréchet distribution and observe that . For arbitrary it is not difficult to compute

Let be a Lévy subordinator without drift and such that , i.e. such that is admissible. It follows that

Consequently, the function , hence the law of , depends on the choice of only via the scalar . In particular, in order to study the probability law of it is sufficient to choose one particular . Choosing , i.e. a standard Poisson process, we know444See, e.g., [Mai (2018a)]. that with a -stable random variable . In contrast to Lévy subordinators, which have independent increments, this stochastic process looks peculiar at first glimpse. The whole path of the process is already known if one just observes for one . This phenomenon is studied in more detail in Section 2.3.

2.3 The natural filtration of

In this paragraph we investigate the amount of information one can obtain by observing the process up to some time . The result is remarkable and different to most classes of stochastic processes commonly used. We begin with an auxiliary result that shows how much information about we can filter out of an observation of .

Lemma 2.11 (Filtering out from )

Let be a (driftless) compound Poison subordinator with positive jump sizes. We define by the information from observing up to time , similarly we define and interpret . Moreover, we assume , where denotes the right-end point of the support of . Then

| (8) |

Proof

See the Appendix.

Intuitively, Lemma 2.11 means that observing up to allows us to anticipate the process up to time . In the sequel, we decompose the increments of into two parts. To this end, we assume and pick the Lévy subordinator arbitrary. We then observe for using Lemma 2.6(a) that

Remark 2.12 (Situation of Lemma 2.11)

In the situation of Lemma 2.11, i.e. when is a (driftless) compound Poisson process, we have . This means that in such a situation, the increments of the process can be split up into a part that can be anticipated from observing the past and a part that is independent of the past. This is quite an astonishing property for a stochastic process and far off the “usual” property of Lévy processes having independent increments.

We can continue to investigate and and find:

The second expression for particularly shows that it is infinitely divisible with associated Bernstein function

| (9) |

Example 2.13 (The case )

This example was first considered in [Bernhart et al. (2015)]. Investing it in the present context (note that ), we find

The function tends to zero as increases to infinity. This is intuitive in the sense that the larger , the more we know about the increment for fixed .

Equation (8) suggests that for with unbounded support, i.e. for all , the whole path of the Lévy subordinator, and, hence , is known already when observing the path of on , for . Indeed, the following two examples confirm this presumption that is later shown with Lemma 2.16.

Example 2.14 (The case and )

Let be a Poisson process with unit intensity, whose jump time sequence we denote by , and the distribution function of the unit exponential law. In particular, has unbounded support. One can show that for all . In words, this means that the whole path of is determined completely by the path on for arbitrarily small . To accomplish this, we show in the Appendix that the function

is holomorphic on . Since holomorphic functions on are determined everywhere, once they are determined on a small real interval, such as for , the claim follows.

Example 2.15 (The case )

Let be a random variable with Laplace transform , , then the associated IDT subordinator is given as , see Example 2.10. This is a peculiar stochastic process, as observing it at some corresponds to knowing it everywhere. We have furthermore seen in Example 2.10 that the choice of Lévy subordinator is arbitrary, provided admissibility. In particular, we are free to choose a compound Poisson process with unit intensity and unit exponentially distributed jumps, i.e. , which is a convenient choice for the following considerations. We truncate via . Clearly, we then have and converges to pointwise. We find for and the Bernstein function of , see (9),

both observations confirming our knowledge about .

Lemma 2.16 (The case of unbounded support of )

Like in Lemma 2.11, we assume that is a compound Poisson subordinator, but now let have unbounded support, i.e. . Then for arbitrary we have

Proof

See the Appendix.

3 Application 1: Simulation of extreme-value copulas

Throughout this section, we fix one admissible pair . The fact that in Lemma 2.2 is homogeneous of order implies by virtue of [Mai, Scherer (2014), Theorem 5.3] that the infinite exchangeable sequence of random variables

with independent unit exponentials, independent of , is min-stable multivariate exponential with survival function given by

| (10) |

which means that has a univariate exponential distribution with rate , not all equal to zero. The exponential rate of each component equals and it is convenient to normalize it to , which then implies that the -variate function defines a so-called stable tail dependence function in dimension . If for the law of does not satisfy , we can always change from to for some such that has this property. This is even unique, i.e. for any given there is a unique such that satisfies . Given this normalization, the function , , defines a so-called extreme-value copula. For background on the latter, the reader is referred to [Joe (1997), Nelsen (2006), Gudendorf, Segers (2009)]. Loosely speaking, extreme-value copulas are the dependence structures behind the limit of appropriately normalized componentwise maxima of independent and identically distributed random vectors, which is of paramount interest in multivariate extreme-value theory. The relationship between strong IDT subordinators and multivariate extreme-value theory has already been investigated in the present authors’ references [Mai, Scherer (2014), Bernhart et al. (2015), Mai (2018a), Mai (2018b)]. On one hand, the probability space (10) can directly be used to simulate the random vector , where . However, due to the infinite series representation of in Lemma 2.6(b) and the fact that the increments of are typically not independent, this is a non-trivial task in general, although feasible in particular cases, an example with a Poisson process and support of bounded is provided in [Mai (2018a), Section 3.1]. However, there is an alternative approach to accomplish the simulation in the general case, as described in the sequel.

It is well-known from [De Haan, Resnick (1977), Ressel (2013)] that the stable tail-dependence function is uniquely associated with a probability measure on the unit simplex subject to the constraint that each component has expected value . To wit, there exists a random vector , uniquely determined in law, taking values in and satisfying for each , such that

which is called the Pickands representation of , named after [Pickands (1981)]. It is important to notice that depends on the dimension . In particular, in our situation where is arbitrary the first components of are not equal in distribution to , not even when re-scaled. In order to simplify notation, however, we omit to highlight this dependence on for the rest of this paragraph.

The simulation algorithm in [Dombry et al. (2016), Algorithm 1], based on a seminal idea by [Schlather (2002)], shows how to simulate a random vector exactly and efficiently, if one has at hand a simulation algorithm for the vector . More precisely, it is shown that

| (11) | ||||

where denote independent copies of , independently of iid unit exponentials, and equals the smallest for which is smaller than the minimal component of . Thus, deriving an efficient and exact simulation algorithm for is essentially the key to deriving an efficient and exact simulation algorithm for the extreme-value copula associated with in dimension . The purpose of the present section is to demonstrate how this is possible. Concluding, one concrete application of the stochastic processes considered in the present article is to enlarge the repertoire of extreme-value copulas for which exact and efficient simulation strategies are available.

3.1 The Pickands representation of

We assume that so that is a proper stable tail dependence function. This condition implies that

so that is a probability measure on . Notice that this probability measure has already been important in Lemma 2.6(b). In the sequel, we show that it also occupies a commanding role when determining the Pickands representation of . Denoting by a generic random variable drawn from this probability law, observe that

The important observation from this computation is that the vector

takes values in and, conditioned on , the measure is a probability measure on . To see this, notice that conditioned on , the measure is a probability measure on , since

Consequently, we have found the unique Pickands dependence measure, as summarized in the following lemma.

Lemma 3.1 (Pickands representation of )

A random sample from Q can be drawn according to the following algorithm.

-

(i)

Draw uniformly distributed on .

-

(ii)

Draw a sample of the random variable .

-

(iii)

Draw independent and identically distributed random variables from the distribution function .

-

(iv)

Draw a random variable from the probability law .

-

(v)

Compute the random vector , defined by

-

(vi)

Return

Remark 3.2 (Expected runtime of the algorithm in Lemma 3.1)

When using the stochastic representation (11) together with Lemma 3.1 to simulate the extreme-value copula , the runtime of the simulation algorithm is random itself. However, [Dombry et al. (2016), Proposition 4] shows that the expected value of in (11) equals , which in the present situation can be computed in closed form by

The last estimate follows from the estimate

where the inequality follows from the argument of the proof of Lemma 2.4. Since the simulation of in Lemma 3.1 itself is apparently of linear order in the dimension , the total expected runtime for the exact simulation of the extreme-value copula according to the representation (11) with the help of Lemma 3.1 has expected order between and and can be computed explicitly in terms of the Bernstein function .

In the sequel, we work out some concrete examples, demonstrating the versatility of Lemma 3.1.

3.2 Examples

Example 3.3 (The Lévy subordinator case)

Consider the distribution function , for , with associated Bernstein function

An arbitrary Lévy subordinator leads to an admissible pair and obviously . Furthermore, is satisfied whenever . It is well-known that equals the survival copula of a so-called Marshall–Olkin distribution, named after [Marshall, Olkin (1967)], see [Mai, Scherer (2009), Mai, Scherer (2011)]. Furthermore, it is observed for that a random variable is Bernoulli-distributed with success probability . In order to simulate from the Pickands measure, additionally required is also a simulation algorithm for with given . With a Bernoulli random variable with success probability , it is observed that

hence . Summarizing, the random vector can be simulated as follows:

-

(i)

Draw the random variable .

-

(ii)

Simulate iid Bernoulli variables with success probability .

-

(iii)

Draw a random variable which is uniformly distributed on .

-

(iv)

Compute the random vector as

-

(v)

Return Q, where , for .

Example 3.4 (The case )

In the special case when is a standard Poisson process, one observes that and Lemma 3.1 boils down to a result in [Mai (2018a), Lemma 4]. It can thus be viewed as a generalization thereof.

Example 3.5 (The case )

The Pickands function is studied in [Bernhart et al. (2015), Theorem 2]. However, no simulation algorithm for has been found in that reference, a gap which we now fill. It is observed that

is the Bernstein function associated with a compound Poisson subordinator with unit exponential jumps and unit intensity. Hence, any leads to an admissible pair by Lemma 4.1 below. In order to ensure , must be normalized such that . Second, for any fixed the distribution function is trivial to simulate from via the inversion method, see [Mai, Scherer (2017), p. 234]. Furthermore, the distribution function of the random variable is given by , which is also easy to simulate from by the inversion method. Consequently, the simulation algorithm in Lemma 3.1 is straightforward to implement, whenever the Lévy subordinator is chosen such that the probability law of , that is

can be simulated from.

Example 3.6 (The case )

The Pickands function is computed in closed form in [Bernhart et al. (2015), Theorem 1]. It is given by

where is the ordered list of . However, no simulation algorithm for has been found in that reference, a gap which we now fill. It is observed that

is the Bernstein function associated with a compound Poisson subordinator with unit intensity and jumps that are uniformly distributed on . Hence, any leads to an admissible pair by Lemma 4.1 below and [Bernhart et al. (2015), Lemma 3] shows that the Bernstein function runs through all possible Bernstein functions when is varied. In order to ensure , must be normalized such that . Second, for any fixed the distribution function is easy to simulate from via the inversion method. Furthermore, the density of the random variable is computed to be

This density is bounded, so rejection-acceptance sampling with the uniform law on can be implemented to achieve an exact simulation scheme of , see [Mai, Scherer (2017), p. 235]. Consequently, the simulation algorithm in Lemma 3.1 is straightforward to implement, whenever the Lévy subordinator is chosen such that the probability law of , that is

can be simulated from.

Figure 1 schematically visualizes those admissible pairs for which either former literature or the present article provides knowledge about the associated extreme-value copula .

4 Application 2: Series representations for infinitely divisible laws

We recall from Equations (4) and (5), using Lemma 2.3, that the law of the random variable is infinitely divisible on with associated Bernstein function

| (12) |

This double integral representation indicates that the roles of and can be switched without changing the one-dimensional marginal distribution of . More precisely,

| (13) |

where for a given Lévy subordinator the function is uniquely determined by the equality , and for a given the Lévy subordinator is uniquely determined by the equality . Recall that the bijection between the set of Lévy measures on and is explicitly stated in Lemma 2.3.

Since admissibility by definition means that the law of is non-trivial, one consequence of this “duality” is that is admissible if and only if is admissible, which implies the following simple admissibility criterion, that could alternatively also be proved directly.

Lemma 4.1 (Simple admissibility criterion)

Let and a Lévy subordinator without drift. If is bounded and satisfies , the pair is admissible, no matter how is chosen.

Proof

See the Appendix.

The integral definition of becomes an infinite series whenever the integrator is a (driftless) compound Poisson process, i.e. if is bounded. Switching the roles of and according to the duality (13), we also obtain a series representation for if is a (driftless) compound Poisson subordinator, i.e. if is bounded. The following example, based on an idea originally due to [Bondesson (1982)], illustrates how this can be useful. We denote by ID the set of all infinitely divisible laws on .

Example 4.2 (Series representations for ID from duality)

Reconsidering Example 3.3, on the left-hand side of (13) let , for , such that and is a Poisson process with unit intensity, whose unit exponential inter-arrival times we denote by and the associated jump times are . Then (13) becomes

where is the survival function of the Lévy measure of , and its generalized inverse. In particular, this series is almost surely finite in case of a compound Poisson distribution, i.e. if is bounded (resp. is finite). This is more or less the representation of an infinitely divisible law in terms of a series representation involving only independent exponentials that [Bondesson (1982)] proposes as a basis for his simulation ansatz (restricted to laws on in the present context). It is of particular use in those cases where the survival function of the Lévy measure has an inverse in closed form. If, in addition, the Lévy measure is finite, i.e. one has a compound Poisson distribution, one obtains an exact simulation algorithm. When simulating this compound Poisson law, the representation is useful particularly if we have no simulation algorithm for the jump size distribution at hand, but we are able to compute the inverse of the Laplace transform of the jump size distribution in closed form.

Remark 4.3 (Alternative series representation for ID)

Example 2.7 shows that Lemma 2.6(b) provides a series representation for ID that is different from that in Example 4.2, namely

where is an iid sequence distributed according to the probability measure , independent of . This representation is always an infinite series, even when has a compound Poisson distribution. However, if a closed form of is unknown but a simulation algorithm for the random variables is known, this series representation might be preferred over the one in Example 4.2.

The series representation in Example 4.2 was based on the choice of a Poisson process as integrator. In the sequel, we choose as integrator a compound Poisson process with unit exponential jumps. In this case, Lemma 4.4 below shows that the law of lies in the so-called Bondesson family BO, see [Bondesson (1981)]. This means that the survival function of the Lévy measure equals the Laplace transform of a measure on , called the Stieltjes measure. From an analytical viewpoint, the Bernstein function , which is said to be complete in this case, can be represented as

with the Stieltjes measure on satisfying . There are examples for laws on BO for which the Stieltjes measure is way more convenient to handle than the associated Lévy measure555See, e.g., Families 3, 5, 27, 28, 29, 33, 35, 45, 46, 63, 64, 88, and 89 in the list of complete Bernstein functions of [Schilling et al. (2010), Chapter 15]., we provide some examples below. For these cases, Lemma 4.4 below provides a series representation in a similar spirit as that for ID in Example 4.2.

We fix as a compound Poisson subordinator with unit exponential jumps and unit intensity, i.e. . Furthermore, we let be arbitrary, and only assume that the left-end point of the support of equals zero, which by Lemma 2.3 is equivalent to postulating , i.e. has no killing. In this situation, the measure

| (14) |

is well-defined for all Borel sets , and we observe that

so is a proper Stieltjes measure. To simplify notation, we denote

and obtain the following result. The series representation in part (c) is a special case of the series representation discussed in [Bondesson (1982), p. 862].

Lemma 4.4 (Series representation in terms of the Stieltjes measure)

Let and a compound Poisson subordinator with unit intensity and unit exponentially distributed jumps, i.e. .

-

(a)

The law of is in with associated Stieltjes measure .

- (b)

-

(c)

We have the following equality in law, with iid unit exponentials:

Proof

See the Appendix.

Like the series representation in Example 4.2 for ID is useful if the Lévy measure is nice, the representation in Lemma 4.4(c) can be used to construct simulation algorithms for infinitely divisible distributions from the Bondesson family, when the Stieltjes measure is nice. In case of a compound Poisson distribution the series is even finite, hence the simulation algorithm is exact. We provide some examples to demonstrate this procedure.

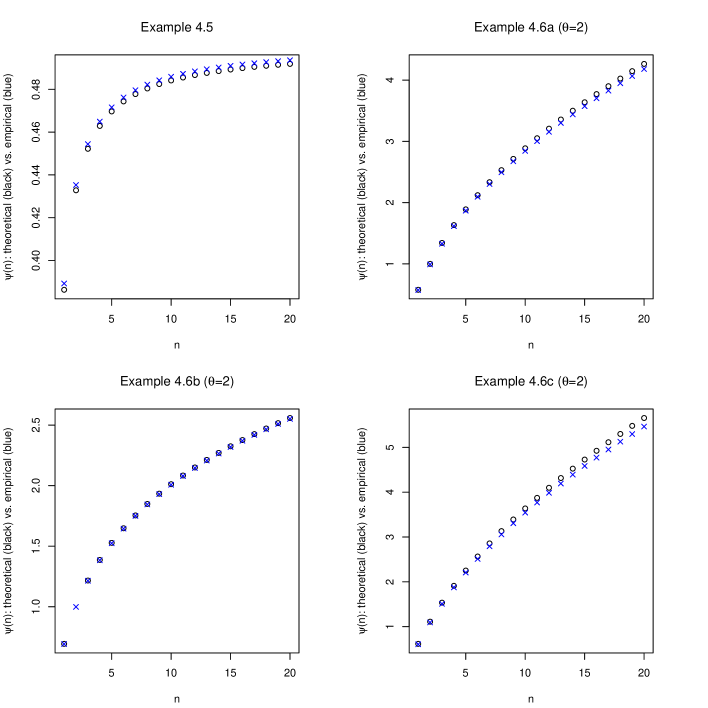

Example 4.5 (Exact simulation of some compound Poisson laws)

Let be some finite measure on , hence it automatically is a Stieltjes measure. We denote by a generic random variable in BO associated with this Stieltjes measure. There exists a distribution function of some non-negative random variable with and a constant such that . The Lévy measure associated with this Stieltjes measure is determined by its survival function, which satisfies , where denotes the Laplace transform of . In this case, we have that

where is the generalized inverse of the distribution function . Consequently, according to Lemma 4.4(c) the compound Poisson distribution with intensity and jump size density has the finite series representation

| (15) |

with iid unit exponentials. It is not difficult to come up with examples for such that is in closed form, but neither is a simulation algorithm for the density at hand, nor is the inverse of in closed form. In such a situation, (15) provides a convenient basis for an exact simulation algorithm. One particular example is given by Family 45 in [Schilling et al. (2010), Chapter 15]: we have and and obtain for , leading to

The associated Bernstein function is given by .

Example 4.6 (A few non-compound Poisson examples)

With a parameter , we consider the complete, unbounded Bernstein functions

which correspond to Families 5, 33, and 64 in [Schilling et al. (2010), Chapter 15]. For each of them, the associated Stieltjes measure has a convenient form, namely

and the associated function from Lemma 4.4 can be computed in closed form, to wit

Figure 2 presents, based on observations, the empirical and theoretical Bernstein function in all of the four cases.

5 Conclusion

We have studied a semi-parametric family of non-decreasing stochastic processes , which comprises (possibly killed) Lévy subordinators without drift as a special case. Whereas a Lévy subordinator is conveniently specified by a Bernstein function , the process is specified by a pair of two Bernstein functions. From a theoretical point of view, we have demonstrated that the parameterization in terms of a distribution function and a Lévy subordinator provides a convenient apparatus to study distributional properties of . In particular, we have established a canonical series representation and have studied the natural filtration of , highlighting that the independent increment property is exclusive to the Lévy subordinator subfamily. From a practical point of view, we have explained how to simulate exactly and accurately the -variate extreme-value copula associated with each process . Furthermore, we have used the derived setting to establish a series representation for infinitely divisible laws from the Bondesson family that is given in terms of its Stieltjes measure only.

Appendix: Proofs

Proof (of Lemma 2.2)

Writing out the Riemann–Stieltjes definition of , introducing for and the notation

we have

Using the bounded convergence theorem in and the stationary and independent increment property of in implies

The order of the two remaining integrations can be switched by Tonelli’s Theorem. When integrating with respect to , it is further possible to change from to , since the at most countably many jump times of play no role in the integration. This finishes the proof.

Proof (of Lemma 2.4)

The equivalence of and is obvious, as well as the fact that implies (a) and (b). The only non-obvious statement is that admissibility implies (c). Denote the biggest argument by . From the probabilistic viewpoint the statement is pretty obvious, since admissibility means that for all . But this implies that

since is non-decreasing, which implies the claim. Alternatively, we can argue fully analytically by computing

where follows from (-)admissibility and the above inequality from the estimate , which holds for any concave function on with and , such as . To see this, for , concavity and imply that

Proof (of Lemma 2.6)

As an auxiliary step, we first show that

| (16) |

To this end, we observe that

| (17) |

which follows from and .

Second, we find for the estimate

| (18) |

Now we use dominated convergence, justified by the admissibility condition and Equation (Proof), to find

| (19) |

The limit inside the integral being zero is obvious for . For we use the following argument: Consider a random variable with , for and fixed . Again we use dominated convergence, justified by and

to find

Finally, the random variable is infinitely divisible and its Bernstein function is found to be . In Equation (19) we have shown that this tends to zero as , for all , which establishes the claimed identity (16).

-

(a)

We use the integration-by-parts formula from [Hewitt, Stromberg (1969), Theorem 21.67, p. 419] and (16) to find

-

(b)

Denoting by the Dirac measure at a point in the plane, we note that is a Poisson random measure on with mean measure by [Resnick (1987), Proposition 3.8]. Consequently, denoting the stochastic process on the right-hand side of the claim in statement (b) by , the Laplace functional formula for Poisson random measure [Resnick (1987), Proposition 3.6] yields

for arbitrary and , establishing the claim.

Proof (of Lemma 2.8)

First of all, may be represented as

| (20) |

which follows from (5) with the help of Tonelli’s Theorem. The sufficiency of the conditions (a) and (b) is clear from this representation, since is bounded and the improper integral is actually a finite integral , where is the right-end point of the support of . Necessity is more difficult to observe. To this end, assume that is unbounded. There is an and a such that for by the condition in the definition of . Consequently,

is obviously unbounded. Hence, we already see that needs to be bounded. In this case, is of compound Poisson type, i.e. there is a Laplace transform of a positive random variable on and a number such that . Consequently, we observe from (20) that

By assumption, we know that is bounded, so we see with the help of Fatou’s Lemma that

But tends to zero as , since it is the Laplace transform of a positive random variable. Consequently, the assumption for arbitrarily large leads to the contradiction . Rather, we must have that for with some finite , which turns the last inequality into

and is not a contradiction.

Proof (of Lemma 2.9)

Sufficiency of the conditions (a) and (b): By Lemma 2.3, has killing if and only if the left-end point of the support of is strictly positive. In this case, for all and one immediately observes from (5) that has killing in this case (since , hence is non-zero by assumption). Also, if has killing, from (20) for all , hence has killing.

Necessity of the conditions (a) and (b): Assume that neither (a) nor (b) holds. Denoting the Lévy measure associated with the Bernstein function by , (5) can be re-written as

where the last equality follows from the assumptions that . Taking the limit as on both sides of this equation, and using the bounded convergence theorem, it follows that , so has no killing.

Proof (of Lemma 2.11)

We denote with jump sizes and Poisson process , whose sequence of jump-times we denote by .

The inclusion ‘’ is immediate from the representation .

The inclusion ‘’ requires us to recover the jump times and jump sizes of the process up to time from observing the process up to time . This can be done inductively.

If , then and we are done. Else, we recover the first jump time by as well as .

If , then and we are done. Else, we recover the second jump time by as well as

This procedure is repeated until .

Proof (that is holomorphic in Example 2.14)

Using [Gilman et al. (2007), Theorem 7.2, p. 124], it is sufficient to prove that the defining series of converges uniformly on all compact subsets of . Each compact subset of is contained within a set of the form for some constants . On this set, we have for arbitrary real that

| (21) |

Furthermore, the law of the iterated logarithm implies that (a.s.)

Consequently, we obtain for almost all the estimate

| (22) |

These estimates, together with the identity for real , imply for large enough that

Since the last expression tends to zero as , uniform convergence of the defining series on all compact subsets of is shown.

Proof (of Lemma 2.16)

We approximate by the sequence of distribution functions , for , and observe that

This, in turn, implies that for . As shown in the considerations preceding the lemma, the random variable equals the sum of a (non-negative) part that is measurable with respect to , and another (non-negative) part which is independent thereof and infinitely divisible. We denote the Bernstein function associated with by and compute, using (9) and (1), that

Consequently, converges to zero in law, and hence converges to zero almost surely, since the limit is a constant. This implies that converges to . Since is measurable with respect to for all , we conclude that is measurable with respect to , yielding the claim.

Proof (of Lemma 4.1)

The conditions on imply that it is the Bernstein function associated with a compound Poisson subordinator whose jump size distribution has finite mean. Example 2.5 shows that . In particular, is admissible, which implies admissibility of by the aforementioned duality.

Proof (of Lemma 4.4)

- (a)

-

(b)

We recall from Lemma 2.3 that is a bijection between and Lévy measures on . Furthermore, it is clear that the mapping is injective. Left to show is only that every Stieltjes measure is attainable, i.e. that is surjective. To this end, it is sufficient to show for an arbitrary Stieltjes measure that the measure

is a Lévy measure on . To this end, we observe that

The claimed expression for can be retrieved directly from Lemma 2.3, while noticing that .

-

(c)

This is a direct consequence of part (b) and the definition of the process .

References

- [Bernhart et al. (2015)] G. Bernhart, J.-F. Mai, M. Scherer, On the construction of low-parametric families of min-stable multivariate exponential distributions in large dimensions, Dependence Modeling 3 (2015) pp. 29–46.

- [Bertoin (1999)] J. Bertoin, Subordinators: Examples and Applications, in École d’Été de Probabilités de Saint-Flour XXVII-1997, Lecture Notes in Mathematics, Springer 1717 (1999) pp. 1–91.

- [Bondesson (1981)] L. Bondesson, Classes of infinitely divisible distributions and densities, Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete 57:1 (1981) pp. 39–71.

- [Bondesson (1982)] L. Bondesson, On simulation from infinitely divisible distributions, Advances in Applied Probability 14 (1982) pp. 855–869.

- [Cuadras, Augé (1981)] C.M. Cuadras, J. Augé, A continuous general multivariate distribution and its properties, Communication in Statistics - Theory and Methods 10 (1981) pp. 339–353.

- [De Haan (1984)] L. De Haan, A spectral representation for max-stable processes, Annals of Probability 12:4 (1984) pp. 1194–1204.

- [De Haan, Resnick (1977)] L. De Haan, S.I. Resnick, Limit theory for multivariate sample extremes, Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete 40 (1977) pp. 317–337.

- [Dombry et al. (2016)] C. Dombry, S. Engelke, M. Oesting, Exact simulation of max-stable processes, Biometrika 103 (2016) pp. 303–317.

- [Es-Sebaiy, Ouknine (2008)] K. Es-Sebaiy, Y. Ouknine, How rich is the class of processes which are infinitely divisible with respect to time, Statistics and Probability Letters 78 (2008) pp. 537–547.

- [Galambos (1975)] J. Galambos, Order statistics of samples from multivariate distributions, Journal of the American Statistical Association 70 (1975) pp. 674–680.

- [Gilman et al. (2007)] J.P. Gilman, I. Kra, R.E. Rodriguez, Complex Analysis: In the Spirit of Lipman Bers, Springer (2007).

- [Gnedin, Pitman (2008)] A. Gnedin, J. Pitman, Moments of convex distribution functions and completely alternating sequences, Probability and Statistics: Essays in Honor of David A. Freedman 2 (2008) pp. 30–41.

- [Gudendorf, Segers (2009)] G. Gudendorf, J. Segers, Extreme-value copulas, In: Copula Theory and its Applications, (P. Jaworski, F. Durante, W.K. Härdle, T. Rychlik, T. Eds.), Springer, New York (2009) pp. 129–145.

- [Gumbel (1960)] E.J. Gumbel, Bivariate exponential distributions, Journal of the American Statistical Association 55 (1960) pp. 698–707.

- [Gumbel (1961)] E.J. Gumbel, Bivariate logistic distributions, Journal of the American Statistical Association 56 (1961) pp. 335–349.

- [Hakassou, Ouknine (2012)] A. Hakassou, Y. Ouknine, A contribution to the study of IDT processes, working paper (2012).

- [Hewitt, Stromberg (1969)] E. Hewitt, K. Stromberg, Real and abstract analysis, Springer-Verlag, Heidelberg (1969).

- [Joe (1997)] H. Joe, Multivariate Models and Dependence Concepts, Chapman & Hall, Boca Raton (1997).

- [Kopp, Molchanov (2018)] C. Kopp, I. Molchanov, Series representations of time-stable stochastic processes, Probability and Mathematical Statistics (2018, in press).

- [Mai (2018a)] J.-F. Mai, Extreme-value copulas associated with expected scaled maxima of independent random variables, Journal of Multivariate Analysis 166 (2018) pp. 50–61.

- [Mai (2018b)] J.-F. Mai, Canonical spectral representation for exchangeable max-stable sequences, working paper (2018).

- [Mai, Scherer (2009)] J.-F. Mai, M. Scherer, Lévy-frailty copulas, Journal of Multivariate Analysis 100 (2009) pp. 1567–1585.

- [Mai, Scherer (2011)] J.-F. Mai, M. Scherer, Reparameterizing Marshall–Olkin copulas with applications to sampling, Journal of Statistical Computation and Simulation 81 (2011) pp. 59–78.

- [Mai, Scherer (2014)] J.-F. Mai, M. Scherer, Characterization of extendible distributions with exponential minima via processes that are infinitely divisible with respect to time, Extremes 17 (2014) pp. 77–95.

- [Mai, Scherer (2017)] J.-F. Mai, M. Scherer, Simulating Copulas, 2nd edition, World Scientific Press (2017).

- [Mansuy (2005)] R. Mansuy, On processes which are infinitely divisible with respect to time, working paper (2005).

- [Marshall, Olkin (1967)] A.W. Marshall, I. Olkin, A multivariate exponential distribution, Journal of the American Statistical Association 62 (1967) pp. 30–44.

- [Nelsen (2006)] R.B. Nelsen, An Introduction to Copulas, 2nd edition, Springer, New York (2006).

- [Pickands (1981)] J. Pickands, Multivariate extreme value distributions, Proceedings of the 43rd Session ISI, Buenos Aires (1981) pp. 859–878.

- [Resnick (1987)] S.I. Resnick, Extreme values, regular variation and point processes, Springer-Verlag (1987).

- [Ressel (2013)] P. Ressel, Homogeneous distributions and a spectral representation of classical mean values and stable tail dependence functions, Journal of Multivariate Analysis 117 (2013) pp. 246–256.

- [Schilling et al. (2010)] R. Schilling, R. Song, Z. Vondracek, Bernstein Functions, De Gruyter (2010).

- [Schlather (2002)] M. Schlather, Models for stationary max-stable random fields, Extremes 5 (2002) pp. 33–44.

- [Segers (2012)] J. Segers, Max-stable models for multivariate extremes, Statistical Journal 10 (2012) pp. 61–82.