Prices, Profits, Proxies, and Production ††thanks: The “ⓡ” symbol indicates that the authors’ names are in certified random order, as described by Ray ⓡ Robson (2018). An earlier version of this paper was circulated as “Prices, Profits, and Production: Identification and Counterfactuals.”

This version: June, 2022)

Abstract

This paper studies nonparametric identification and counterfactual bounds for heterogeneous firms that can be ranked in terms of productivity. Our approach works when quantities and prices are latent, rendering standard approaches inapplicable. Instead, we require observation of profits or other optimizing-values such as costs or revenues, and either prices or price proxies of flexibly chosen variables. We extend classical duality results for price-taking firms to a setup with discrete heterogeneity, endogeneity, and limited variation in possibly latent prices. Finally, we show that convergence results for nonparametric estimators may be directly converted to convergence results for production sets.

JEL classification: C5, D24.

Keywords: Counterfactual bounds, cost minimization, nonseparable heterogeneity, partial identification, profit maximization, production set, revenue maximization, shape restrictions.

Introduction

This paper studies nonparametric identification of production sets and counterfactual bounds for firms, allowing multiple inputs and outputs, in an environment where both quantities and prices can be latent. We assume an analyst has data on the values of an optimization problem, such as profits, costs, or revenues, as well as prices or price proxies.

Identifying heterogeneous production sets is challenging in situations where the observability of some outputs/inputs or prices is problematic. For instance, in the housing market output quantities and output prices cannot be directly observed because houses provide different services that are hard to measure. However, housing values that can serve as price proxies may be observed (Epple et al., 2010). Other industries, such as health and banking, suffer from similar issues with unobservable inputs or outputs.111In the health industry, it is difficult to measure inputs such as drugs since they vary widely in their physical characteristics. However, prices and total costs may be observable (Bilodeau et al., 2000). In the banking industry, outputs such as business loans and consumers loans are difficult to measure because a loan is a financial service that entails many unobservable goods and services. However, the price of a loan is observed as well as profits in some settings (Berger et al., 1993). The latency of quantities makes standard approaches to estimate production functions not directly applicable. In addition, the latency of prices makes classical approaches using duality theory impossible to apply as well. In contrast, we require observability of values and prices or price proxies. While these variables are not always observed, they are available in many existing data sets.222See Epple et al. (2010), Combes et al. (2021), and Albouy and Ehrlich (2018) in the context of housing; Burke et al. (2019) in the context of agriculture; Nerlove (1963) and Fabrizio et al. (2007) in the context of electricity generation; Roberts and Supina (1996), Foster et al. (2008), and Doraszelski and Jaumandreu (2013) in the context of manufacturing.

In order to obtain identification of firm-specific production possibility sets we exploit variation in prices or price proxies across markets and variation of optimization values across firms. Our framework extends classical duality theory by allowing (i) rich forms of complementarity and substitutability between outputs and inputs with discrete heterogeneity across firms, (ii) endogeneity between prices and productivity due to simultaneity and market entry decisions, and (iii) omitted prices of flexibly chosen variables. Classical duality theory focuses on either a nonstochastic or representative agent framework in which all prices are observed. Important contributions include Shephard (1953), Fuss and McFadden (1978), and Diewert (1982) among many others.

We assume that firms can be ranked in terms of productivity that can take finitely many values. This assumption is key to unpack heterogeneity in multiple output/input production sets across firms from data such as prices or price proxies and scalar values of an optimization problem. We formalize this by assuming that a firm with higher productivity has access to all the production possibilities of a less productive firm, and more. Our framework covers Hicks-neutral heterogeneity in productivity as a special case.

Our approach exploits the rich shape constraints in our environment for identification and counterfactual analysis. Leveraging that firms can be ranked according to discrete productivity, we present a new method to identify the structural value function (e.g. profit function). This technique works with bounded measurement error, but allows rich forms of selection into market. We require a weak monotone presence assumption, so that if a firm is present in some market with certain observables, then each more productive firm must be present in some market with the same observables. This handles certain monotone selection rules, e.g. only firms that can make nonnegative profits enter, but is much more general.

We next tackle the important possibility that not all prices are observed. Instead, we use price proxies, which are unknown functions of the missing prices. As one example, we show that aggregate market-level quantities can serve as price proxies. We leverage homogeneity of the value function to recover these unknown functions. This technique is new, and is applicable to other settings with homogeneity of a structural function, and is therefore of independent interest.

Once the structural value function is identified, we turn to recoverability of the production sets. Here we leverage the classic insight that the value function serves as the support function of the production set. This allows us to characterize the most that can be said about heterogeneous production sets, even when price variation is limited. Building on this, we present a general framework for counterfactual questions such as sharp bounds on quantities or profits at a new price. Importantly, these bounds hold for each level of productivity, and thus characterize features of the distribution of firm behavior.

As mentioned previously, relative to classic work on duality we make several contributions by incorporating heterogeneity, endogeneity due to selection, and potential lack of prices.333Outside of the firm problem, duality has been used in the presence of heterogeneity in discrete choice (McFadden, 1981), matching models (Galichon and Salanié, 2015), hedonic models (Chernozhukov et al., 2017), dynamic discrete choice (Chiong et al., 2016), and the additively separable framework of Allen and Rehbeck (2019). Even when prices are observed but contain limited variation, we contribute by providing new results using structural value functions to recover sets and conduct counterfactual analysis. This builds on Farrell (1957) and Afriat (1972), who study efficiency measurement and conditions under which producer datasets are consistent with the hypothesis of optimization. Relatedly, Hanoch and Rothschild (1972) focuses on finite deterministic datasets of individual firms’ profits or costs, and prices. Hanoch and Rothschild (1972) does not study identification of the production set or the profit function, but focuses on providing necessary and sufficient conditions under which an observed production function is consistent with profit maximization or cost minimization.444Cherchye et al. (2016) studies the identification of profits and production sets with a finite deterministic dataset on prices and quantities. Another paper studying limited price variation is Varian (1984), which works with quantities and prices and does not study unobservable heterogeneity.555See also Cherchye et al. (2014) and Cherchye et al. (2018). Cherchye et al. (2018) differs from this paper because they assume observed input quantities in the context of cost minimization. While observation of prices and quantities implies observation of profits, the reverse is not true.

This paper contributes to the recent literature on identification and estimation of multi-output production with unobservable heterogeneity (e.g., Cunha et al., 2010, De Loecker et al., 2016, and Grieco and McDevitt, 2016). We differ since we do not observe quantities and we do not impose separability or parametric restrictions on the shape of production sets. Because we allow production of multiple outputs in flexible ways, use cross-sectional variation, and do not observe quantities, we also differ from an important recent literature studying single output production in dynamic panel settings using quantities data, including Griliches and Mairesse (1995), Olley and Pakes (1996), Levinsohn and Petrin (2003), Ackerberg et al. (2015), and Gandhi et al. (2020).666As noted in Ackerberg et al. (2015), some output and input data often come in the form of sales and expenditures that need to be transformed into quantities. We work directly with total values (e.g. profits, total costs, or revenues).

We also contribute to the literature studying recoverability of sets. We build on the tight relationship between the structural value function and the production possibility sets of firms, by providing an equality relating estimation error of value functions and estimation error of production possibility sets. This result allows one to adapt consistency results for any nonparametric estimators of the value function for the purpose of set estimation. The result is related to a classical result in convex analysis linking the distance of support functions with the distance of the corresponding sets, which has been exploited previously in the literature on partial identification.777See, for instance, Beresteanu and Molinari (2008), Beresteanu et al. (2011), Kaido and Santos (2014), Kaido (2016), and Kaido et al. (2019). We cannot apply the classical result since it would require seeing negative prices.

The rest of this paper proceeds as follows. In Section 1, we present a model of heterogeneous production in which firms are rankable in terms of productivity. Section 2 shows how to identify the structural value function. In Section 3, we extend our methodology to environments where one observes proxies that determine unobservable prices. Our main identification result for production possibility sets is in Section 4. Section 5 provides a general framework to conduct sharp counterfactual analysis in production environments. In Section 6, we show duality between estimation error in value functions and production sets. We conclude in Section 7. All proofs can be found in Appendix A. An estimator of the restricted profit function and an illustrative application are in Appendices B and C. The Online Appendix contains extensions, simulations, and additional results.

1. Setup

This paper studies recoverability of the technology of heterogeneous firms given data on the value function of their maximization problems, as well as data on prices or price proxies that alter the maximization problems.

The technology of heterogeneous firms is described by a correspondence . Each set describes the possible input/output (or “netput”) vectors that are feasible for a firm of type . The variable captures unobservable heterogeneity in productivity. Negative components of correspond to net demands by the firm and positive components correspond to net supply. This formulation allows us to treat single output and multi-output firms in a common framework.888An alternative approach is to use transformation functions. See Grieco and McDevitt (2016) for a recent application. We require the following conditions.

Definition 1.

A correspondence is a production correspondence if, for every ,

-

(i)

is closed and convex;

-

(ii)

satisfies free disposal: if is in , then any such that for all is also in ;

-

(iii)

satisfies the recession cone property: if is a sequence of points in satisfying as , then accumulation points of the set lie in the negative orthant of .

These conditions rule out infinite profits and ensure that the maximization problems we consider have a solution.999See Kreps (2012), p. 199 for more details.

We study the general restricted profit maximization problem

where is a vector of restricted or fixed variables, denotes the variables of choice, and is a vector of prices of . The variable of choice is constrained to belong to the convex set defined as

We refer to as the restricted production correspondence.101010More formally, it is only a multi-valued mapping because it can be empty for certain combinations of and . We note that the results in this paper do not need the full strength of being a production correspondence. Instead, we require that the set be closed and convex, satisfy free disposal, and satisfy the recession cone property.

The behavioral restriction of this model is that given , the firm chooses to maximize restricted profits, taking prices as given. In the special case where is not present, this is the usual profit maximization setup. When consists of inputs, this covers revenue maximization. When consists of outputs, this is cost minimization once we interpret negative as inputs and write

We emphasize that throughout, can be a vector, and so we cover cost minimization with multiple inputs, and revenue maximization with multiple outputs.

Overall, we consider firms that are price-taking in the variables of choice , and study a static problem without uncertainty. We note though that in principle the production set is general enough to describe paths of production possibilities throughout time, as would arise if there is investment.

1.1. Setting and Data

We study identification in settings in which an analyst observes many realizations of certain values of the restricted profit maximization problem as prices vary. In the most general version, we observe noisy measurements of restricted profits, which are the values of the restricted problem. Specifically, we consider the setup

where and are observed,111111We use bold font for random variables and random vectors and regular font for their realizations. is unobserved measurement error, and is unobservable productivity level. For each component of , the analyst either observes the corresponding price, or more generally observes a price proxy that is linked to the unobserved price by the relationship , where consists of some control variables. We provide further examples and discussion of such proxies in Section 3.

As an example of observables for cost minimization of hospitals (Bilodeau et al., 2000), the analyst observes total cost on variable inputs (labor, supplies, food for patients, drugs, and energy), input prices or input-price proxies, fixed outputs (inpatient care and outpatient visits), and the fixed inputs (number of physicians and capital). We emphasize that we do not need to observe the quantities of the flexibly chosen variables.121212As discussed in the introduction, for additional data sets, see Nerlove (1963), Roberts and Supina (1996), Fabrizio et al. (2007), Foster et al. (2008), Epple et al. (2010), Doraszelski and Jaumandreu (2013), Albouy and Ehrlich (2018), Burke et al. (2019), and Combes et al. (2021).

Now we turn to the description of the sources of variation in our setup. Although we do not fully flesh out an equilibrium model incorporating selection, we provide an informal discussion of these forces. First, prices can vary across markets due to variation in endowments or the income or tastes of consumers. Our results apply when an analyst observes a single firm from each market, and has observations from many markets. Our results also apply when an analyst observes multiple firms in each market. We focus on the former case to simplify presentation, so that we can avoid market-level subscripts.

2. Recoverability of Restricted Profit Function

Our ultimate goal is to learn about the production correspondence. We proceed in three steps. In this section, we first identify the restricted profit function (or value function) for heterogeneous firms assuming that the prices are perfectly observed. In Section 3 we show how to apply our analysis to the general case with unobserved prices. In subsequent sections we show how to use information on the restricted profit function to recover features of the production correspondence and describe the most that can be learned concerning counterfactual questions.

Identifying the restricted profit function for heterogeneous firms is challenging. The value function is nonseparable in latent productivity. Both the restricted variables and prices may be endogenous. This leads to simultaneity and selection biases. We consider a setting without panel data or instruments. We present a new technique to identify the restricted profit function that addresses these challenges. The key restrictions of the technique are that (i) heterogeneity is one dimensional and allows us to rank firms, and (ii) there are finitely many types of firms.

2.1. Production Monotonicity

It is well-known that the firm problem admits a representative agent, and in principle this observation can be used to recover a representative agent restricted profit function. Even a representative agent analysis here is nontrivial because of challenging selection/simultaneity issues discussed previously. Here, we wish to recover not only a representative agent restricted profit function, but also recover the heterogeneous structural restricted profit functions. Recovering heterogeneous structural functions allows us to a conduct rich counterfactual analysis concerning how different types of firms are differentially affected by a policy.

To get traction on this problem, we assume firms are rankable in terms of productivity. We think of heterogeneous productivity as an ability to produce more with a given level of inputs (or produce the same output using lower levels of inputs). In other words, the production set of a firm with lower value of productivity is a subset of the production set of a firm with a higher productivity (see Figure 1). Note that if and only if for all . This means that more productive firms have access to a bigger set of production possibilities, and will make more profits or pay lower costs given prices. We formalize this monotonicity by the following ranking assumption on the restricted profit function.

Assumption 1 (Strict Monotonicity).

For every , , , and in the support, if , then .

Strict monotonicity of structural functions has been considered previously in e.g. Matzkin (2003). Assumption 1 is satisfied in many settings. For instance, it is satisfied in a standard single output production function setting with Hicks-neutral productivity. To be more specific, let the single output be and let inputs be and , interpreted as labor and capital. Then the set is described by tuples that satisfy , where is the production function. If for some nonnegative, strictly increasing function , and is a nonnegative strictly convex function, then is strictly increasing in . In this case, satisfies Assumption 1.

More generally, the function for strictly increasing functions , , and fits into our setup.131313Li and Sasaki (2017) study a related setup with random coefficients Cobb-Douglas technology, imposing that the ratio of random coefficients is a monotone function of a single latent scalar random variable. A more general setup would allow a different shock to enter , and (e.g. Doraszelski and Jaumandreu, 2018) and would be outside of our framework. Overall, while Hicks-neutral heterogeneity is a special case of our framework when there is a single output, it is considerably more restrictive than needed for the monotonicity assumption to hold.

The assumption that production sets are nested in is equivalent to the profit function being weakly increasing in . Thus, value functions are the “right” structural function in which to impose monotonicity if we think of higher productivity as leading to more production possibilities. One may draw the intuition that in general other structural functions are monotone in unobservable heterogeneity. This intuition is false without more structure.

Example 1 (Nonmonotonicity of Inputs/Outputs).

Consider the production sets depicted in Figure 2. Each production set is given by , where for all . Here, for all positive and Assumption 1 is satisfied. Given the price vector in Figure 2, the optimal levels of inputs and outputs are nonmonotone in productivity since and . For a numerical example see Online Appendix C.

Failures of monotonicity in the optimal choice of input or output have been discussed as well in Pakes (1996, Section 4). Thus, rather than focus on the structural functions describing optimal input/output choices, this paper focuses instead on the restricted profit function, which is monotone in a scalar unobservable under the assumption that production sets are nested in .

2.2. Discrete Heterogeneity and Monotone Selection

With this setup, we consider a new technique to identify the restricted profit function allowing endogeneity. The reason endogeneity is a central concern in such problems is that constraints may be endogenous. For example, in the cost minimization problem, output () is typically a choice variable for the firm. An additional endogeneity concern is that firms may choose in which markets to operate. This can induce a selection issue, though we emphasize that once a market is chosen, the input/output vector is determined taking market prices as fixed. As discussed in Section 1.1, price variation in our setting arises because firms operate in different markets, which have different endowments or consumer tastes.

The key restriction we impose is that there are finitely many types of firms. We formalize this as follows.

Assumption 2 (Finite Heterogeneity).

, where is finite and unknown to the researcher.

This assumption allows us to identify structural functions without instruments. If instruments are available, continuous heterogeneity can be tackled by existing techniques provided there is no measurement error; see for example Online Appendix B. We emphasize that heterogeneity here is in terms of the production types, but due to measurement error in the data we may see continuous distributions of the restricted values, even when we condition on all other observables. In this modeling decision we are close to structural dynamic discrete choice literature that often assumes unobserved discrete heterogeneity that is smoothed out by some continuous idiosyncratic noise (e.g. extreme value distributed preference shock). See, for instance, Arcidiacono and Miller (2011).141414For applications of discrete unobserved heterogeneity, see Fox and Gandhi (2016) in multinomial choice and Bonhomme and Manresa (2015) with panel data. We are not aware of any identification results that allow for both measurement error and continuous nonseparable structural unobserved heterogeneity in cross-sectional data.

We allow rich selection into markets, but impose a monotonicity restriction relating the types of firms that can be present, conditional on certain observables.

Assumption 3 (Monotone Presence).

for all , , , and in the support such that .

This means that if we see a firm of type active in some market and producing , conditional on , then for any higher productivity , there is some market in which the higher type is active at the same value of conditioning variables. In principle, this other “market” could be the same market in which the firm with productivity is present. The key restriction is that since we also condition on quantities, we need the higher type to also produce the same quantities.

As an example, consider the (unrestricted) profit function. Suppose entry depends on whether a firm obtains nonnegative profits. Specifically,

where there are no restricted variables. Since we assume monotonicity of in , this is a monotone threshold rule, and satisfies Assumption 3.

Assumption 3 is considerably more general than a one-sided selection rule. Importantly, it is only about the support of conditional on some other variables. The reason we require this is that while reasonable selection rules into markets may result in a one-sided threshold rule, here we also need to allow selection into the quantities of the restricted variables . For example, as increases the optimal quantity of the restricted variables may change. Assumption 3 allows this and is satisfied if, for example, there are other unobserved variables that shift the optimal choice of restricted variables (e.g. unobserved prices of the restricted variables).

2.3. Identification

We now turn to identification of the restricted profit function. First, recall that we observe potentially mismeasured restricted profits:

If is independent of , then Assumption 2 implies that the conditional distribution of can be written as a finite mixture of shifted distributions of :

where is the conditional cumulative distribution function (c.d.f.) of conditional on and , and is the c.d.f. of . There are numerous ways to identify the above finite mixture model under different sets of assumptions that may be valid in different environments (see, for instance, Kitamura and Laage, 2018 and references therein). However, most of these results use either repeated measurements (i.e. panels) or use variation in conditioning variables, and require some form of exclusion restrictions (e.g., some conditioning variables affect but do not affect ), or the presence of instruments. We propose a new set of assumptions to identify the above finite mixture in cross-sections, without instruments and exclusion restrictions. Moreover, our approach is constructive and the assumptions are easy to interpret.

Let denote the restricted profit difference between firms with adjacent productivity. We impose the following assumption on the measurement error .

Assumption 4.

-

(i)

is independent of , mean zero, has connected support, and satisfies for some ;

-

(ii)

(Separatedness) There exists in their support such that

We note that multiplicative measurement error can be handled by similar independence and separatedness assumptions.151515The bounded support and separatedness conditions in Assumption 4 can be relaxed using results in Schennach (2016) if one has access to repeated cross-sections.

Assumption 4(i) means that the measurement error is classical. It also imposes a location normalization on the boundedly-supported measurement error.161616For examples of papers studying boundedly-supported measurement errors see Hu and Ridder (2010), D’Haultfœuille and Février (2015), and Hu et al. (2017). The bounded support assumption is empirically relevant in many settings. For instance, revenues and costs cannot be negative, which provides a one-sided bound. Assumption 4(ii) is more substantial. This assumption imposes that the gap between the structural profits of the types adjacent to must be sufficiently small compared with the support of measurement error. This can be restrictive in certain empirical settings but is essential for this method. We argue that boundedness and separatedness are appropriate in our empirical illustration in Appendix C.

Note that Assumption 4(ii) has to be imposed on one triplet only. Thus, in general, the measurement error may completely change the ranking of restricted profits. Moreover, this triplet does not need to be known. A simple sufficient condition for Assumption 4(ii) that uses shape restrictions of the restricted profit function is stated in the following result.

Lemma 1 (Rich Support).

This exploits homogeneity in prices, i.e. for all and . The idea behind Lemma 1 is that although the difference between profits evaluated at a particular price may not be big enough to offset the effect of the measurement error (e.g. ), by exploiting homogeneity we always can find big enough such that

The conditions of Lemma 1 guarantee that an extreme price can be found in the support for every finite . Thus, the support of prices does not have to be unbounded, just sufficiently large relative to the initial difference.

Now we can state our main identification result for the restricted profit function.

Theorem 1.

Here, we may not be able to identify the structural restricted profit function for certain arguments outside of the support. This is particularly relevant for low types; there may be many combinations of prices and quantities such that low types do not produce either because it is infeasible for them or unprofitable.

Importantly, Theorem 1 only imposes a mild restriction on the stochastic dependence between unobservable heterogeneity and observed and . In particular, in cost minimization settings, the output level and input prices can be related to the distribution of productivity in flexible ways. What is key is the monotonicity restriction on selection into markets described in Assumption 3.

The intuition behind Theorem 1 is that without restricting the dependence structure, monotonicity in the restricted profit function implies that firms always can be ranked. The assumption of the discrete heterogeneity allows us to match firms with the same ranking across different markets, and thereby construct the restricted profit function.

Theorem 1 can be used to weaken assumptions usually made in analysis of restricted profit maximizing behavior. For instance, with cost minimization, Bilodeau et al. (2000) focuses on a parametric setup with additively separable heterogeneity and assumes that fixed variables are exogenous. While working with the same observables, our methodology does not require parametric restrictions, and does not assume exogeneity.

Remark 1 (Testability).

Theorem 1 identifies the restricted profit function without using the shape restrictions that characterize such functions. Thus, the assumptions in this paper are testable. Specifically, for each , the identified function must be convex, monotonically decreasing, and homogeneous of degree in the prices of the flexible variables . These implications can be tested with data on the values of the restricted problem , the restricted quantities , and prices .

3. Unobservable Prices and Proxies

In Section 2, we showed how to identify the restricted profit function when the entire vector of prices of flexibly chosen variables, , is observed. In many empirical applications not all prices are observed. This may cause concern about omitted price bias (see Zellner et al., 1966, Klette and Griliches, 1996, Katayama et al., 2003, and Epple et al., 2010). However, the researcher may have access to some observable proxies that are informative about unobservable prices. For example, the rental rate of capital may be linked to market-specific characteristics such as short-term and long-term interest rates. Wages may be linked to the unemployment level or aggregate labor supply. De Loecker et al. (2016) uses output price, market shares, product dummies, firm location, and export status as proxies for unobservable input prices. In the housing market, an analyst may use location as a price proxy for a house as in Combes et al. (2021).171717Hedonic pricing models also exhibit similar structure. However, in that literature it is assumed that both prices and proxies are observed. See, for instance, Ekeland et al. (2004).

This section studies how to identify the function linking prices proxies to unobserved prices through

where is an unknown function and is a component of the vector of prices of the flexibly-chosen variables. We show how to identify using the fact that the restricted profit function is homogeneous of degree , though as discussed in the Introduction, the technique we present is new and applies to any degree of homogeneity.181818Homogeneity has been used for identification in Matzkin (1992), which differs in techniques and setting. We assume that every price has its own excluded proxy , which is a proxy that affects its own price and does not affect any other prices. The vector of common proxies may include common market characteristics such as size of the market or other macroeconomic characteristics. Importantly, since is fully nonparametric, can include categorical variables such as location (e.g. country or state) and time (e.g. month or year) identifiers. The special case in which price is observed corresponds to , where is the price of . To simplify the exposition we drop from the notation, and analysis may be interpreted conditional on . For instance, we write instead of . We denote and .

Note that we assume prices are not a function of or any other unobservables. Importantly, this rules out measurement error in prices. In our setup prices vary across markets, but are constant within a given market. Price-taking behavior implies that prices can be a function of the distribution of in a market, but not the firm-specific productivity .

We first present an informal outline how to identify when one observes unrestricted profits, so that there are no restricted variables and the subscript can be dropped. If the function were known, we could identify directly by previous arguments. What remains is to identify . Recall that the profit function is homogeneous of degree , which from Euler’s homogeneous function theorem yields the system of equations

Replacing prices with price proxies, we obtain

| (1) |

Define . Because is exclusive to , the cross-partial derivatives satisfy for . We thus have

Plugging this in to (1) we obtain

| (2) |

Assume for now that is identified. Thus the only unknowns involve . By varying , holding everything else fixed, Equation 2 can be used to generate a system of equations. We show that when a certain rank condition is satisfied, it is possible to identify the entire function using an appropriate scale/location normalization. We note that if all prices are observed except one, then we may directly apply Equation 2 to learn about .

To formalize this, we impose location/scale conditions and some regularity conditions on .

Assumption 5.

-

(i)

for all , i.e. the price of the -st flexibly chosen variable is observed;

-

(ii)

The value of is known at one point, i.e. there exist known and such that ;

-

(iii)

where each set is an interval with nonempty interior;

-

(iv)

is continuous everywhere and differentiable on the interior of , and the set

has Lebesgue measure zero for every .

Assumptions 5(i)-(ii) allow us to identify the scale and the location, respectively, of the multivariate function . Since we can always relabel both outputs and inputs, Assumption 5(i) is equivalent to assuming that at least one price (not necessary ) is observed.

We now turn to our rank condition. This condition ensures that the system of equations generated from (2) has sufficient variation to recover terms such as .

Definition 2.

We say that satisfies the rank condition at a point if there exists a collection such that

-

(i)

;

-

(ii)

The square matrix

is nonsingular.

We will apply this rank condition to in place of . It is helpful to recall that by Hotelling’s lemma, partial derivatives of take the form

where is the supply for good . Thus, this rank condition applied to may equivalently be interpreted as a rank condition involving the supply function for the goods as well as certain derivatives of . In words, variation in observed prices should induce enough variation in supply of goods with unobserved prices.

The following result provides conditions under which the price-proxy function is identified. We note that while our exposition above covered the case of unrestricted profits, the following result holds for the more general setting of restricted profits. Thus, instead of the function , we will use its restricted version defined via , where is fixed.

Theorem 2.

Suppose Assumption 5 holds. Then is identified over the support of if for some , the following conditions hold:

-

(i)

is identified for each and in the support;

-

(ii)

For every , there exists in the support such that satisfies the rank condition at .

To interpret (i), recall that Theorem 1 provides conditions under which is identified from the conditional distribution of conditional and . To apply those results one just needs to replace by . Here we highlight that given some way to identify a structural function of the form of , we can identify . Thus, if a researcher has another means of identifying the structural function , then this theorem can be applied.

Part (ii) requires sufficiently rich variation in the reduced form profit function for some value of productivity . To further interpret the rank condition, we study it in two parametric examples in Online Appendix D. There we show that the rank condition can be satisfied for the Diewert (1973) profit function, but can fail for every possible parameter value with Cobb-Douglas technology. The reason Cobb-Douglas fails is that its profit function is additively separable when logs are taken.

Remark 2 (Other Degrees of Homogeneity).

It is straightforward to generalize our technique to a homogeneous function of any degree since the main identifying equation (2) can be rewritten as

| (3) |

Here we study the restricted profit function, so , but an analogous equation holds for other homogeneous structural functions. As one example, recall the supply function is homogeneous of degree in prices for a price-taking, profit-maximizing firm.

Remark 3 (Aggregation).

The key shape restriction used for identification in this section is homogeneity of a structural function. Importantly, homogeneity is a shape restriction that is preserved under expectations. Note that while we use homogeneity of degree here, this is true for any degree of homogeneity. See in particular Equation 3, which has structure that is preserved under expectations. For this reason, our results work as well with a representative agent analysis involving mean structural demand. We formalize this in Online Appendix G.

3.1. Value as Proxy

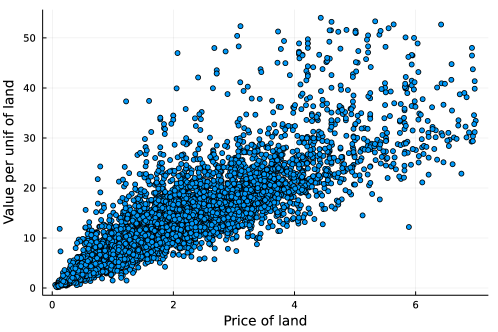

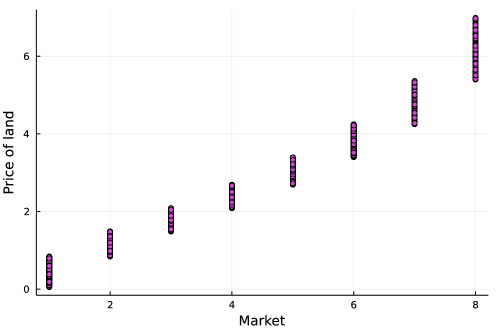

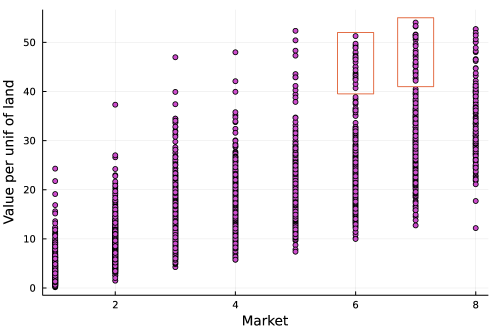

This section shows how to interpret Epple et al. (2010) through the lens of price proxies. Specifically, we show that average house values in a market can be used as a proxy for a missing output price. We use this setup as well in the empirical illustration in Appendix C.

Epple et al. (2010) consider the production of housing in which all goods and services provided by a house are treated as a single output. The analyst observes total revenue of selling a house, and the price of land. Variation in these observables is driven by market variation. Importantly, output and its price are both unobserved. Each source of unobservability is recognized as an important problem for the measurement of housing production. Building on Epple et al. (2010) we show how average values in a market serve as a price proxy for this missing price.

In contrast to Epple et al. (2010), who work with a representative firm, we study identification in the presence of heterogeneity. As in Epple et al. (2010) we assume constant returns to scale in land and materials, so we can write

where is the production function per-acre, and output and materials are in units per acre (land). The production set associated with this production function is . Firms treat land as pre-determined and choose and . We work with the profit function per-acre, written as

where , , and are prices of output, materials, and land, respectively. Since the price of materials is unobserved, Epple et al. (2010) assume that it is the same across markets and equals 1. We will make the same assumption and drop from the notation.

Since land is pre-determined, its price does not affect the optimal choice of output or materials. Thus, the value of housing and the average value of housing in a market with price , denoted , do not depend on price of land . Since is monotone in , the average value is also monotone in . Importantly, is identified when we observe total revenue .

Lemma 2.

Suppose the distribution of firm productivity is the same across markets and the other assumptions of this section hold. If is strictly increasing in , then average value of housing per market is a price proxy, i.e. there exists a function such that

This equation is analogous to Equation in Epple et al. (2010) if we interpret their results as a representative agent analysis.

We note here that by using value as a price proxy for output, if profits were observed and the price of materials () varied, we could directly use the average value and identify using Theorem 2. Here, we do not observe profits and the price of materials is assumed fixed at . We thus impose an addition zero-profit assumption as in Epple et al. (2010). While that paper assumes a single type of firm, which attains zero profits, we assume that profits are zero on average in a given market202020Melitz and Redding (2014) show that free-entry and constant returns of scale imply that ex-ante expected profits are zero, net of entry cost. Here we can assume entry cost is zero. In equilibrium, firms will have zero-profits on average just before firms with negative profits leave the market.:

where and are the realizations of the aggregate output per-acre and the aggregate demand for materials per-acre in a given market. Since and are observed, the equilibrium assumption nonparametrically recovers a revenue function from production minus materials cost (recall that ),

Moreover, since by definition, we also identify material costs

We identify the function since we identify and . In particular, will solve the following differential equation:

| (4) |

Knowing we can identify for different levels of heterogeneity since the observed is equal to . Thus, our approach generalizes Epple et al. (2010) to allow for unobserved heterogeneity in productivity. For a formal generalization of the results in Section 3 to settings with other observables see Online Appendix F.

4. Identification of the Production Correspondence

In Section 2, we showed how to identify the restricted profit function allowing endogenous entry and correlation between fixed quantities and productivity, without requiring instruments. Section 3 extends this result to settings when some prices are not observed but the analyst has price proxies, and provides examples of such proxies.

We now focus on how any of these identification results for the restricted profit function can be used to identify the primitive object of interest: the production correspondence. For the sake of notational simplicity from now on, we focus on the profit function though the results can be adapted to the restricted profit function by conditioning on .

Recall that we start with identification of the profit function only over the support of prices. For notational simplicity, we work with prices and not price proxies.212121More generally we can identify the profit function over the support of , where is the vector of price proxies. The support of prices may consist of all nonnegative numbers, or may be much smaller, i.e. finite. We present a sharp identification result for the production correspondence that covers both cases.

First, we note that is homogeneous of degree in prices. It is also convex in prices, hence continuous. These features lead to consideration of the following richness assumption, which ensures may be recovered uniquely. Let denote the conditional support of conditional on (if and are independent, then does not vary with ).

Assumption 6.

for all , where and are the closure and the interior of , respectively.

The set

consists of all prices where is known because of homogeneity. If that set has “holes,” then we can fill them by taking the closure of the set since is convex, hence continuous.222222Beyond continuity, the manner in which convexity affects the data requirements that ensure point identification is subtle, and depends on the shape of . We provide an illustrative example in Online Appendix E. Assumption 6 means that after we consider the implications of homogeneity and continuity, it is as if we have full variation in prices. Figure 3 is an example of a set satisfying this assumption. Another example is the Cartesian product of all natural numbers, . Thus, Assumption 6 does not impose that the support of contains an open ball.

Theorem 3.

Let be identified by some previous argument over the set for all . Moreover, let be defined via

for all . Then

-

(i)

can generate the data and for each , is a closed, convex set that satisfies free disposal.232323By generate the data we mean that the profit function induced by agrees with the identified profit function for all and .

-

(ii)

A production correspondence can generate the data if and only if

for every and . It follows that for any such , , for each .

-

(iii)

If Assumption 6 holds, then is the only production correspondence that can generate the data.

Parts (i) and (ii) of Theorem 3 are a sharp identification result stating the most that can be said about the production correspondence under our assumptions. These results are related to Varian (1984), Theorem 15.242424The set is related to the “outer” set considered in Varian (1984), Section 7. The set is constructed from price and profit information, however, rather than price and quantity information as in Varian (1984). However, Varian (1984) works only with finite datasets, which are comparable to having a finite support of prices in our setting. In addition, Varian (1984) observes prices and quantities while we observe prices and profits. Recall that observing prices and quantities implies observation of profits. Finally, Varian (1984) does not consider unobservable heterogeneity.

Theorem 3(ii) establishes that is the envelope of all production correspondences that can generate the data (see Figure 4). We note, however, that may not be a production correspondence because it need not satisfy the recession cone property (recall Definition 1(iii)).252525To see this, suppose that a firm of type has 2-dimensional output/input set, prices are a constant vector , and profits at that price are given by . Then the set is . This set induces infinite profits for a price-taking firm whenever . Hence, this set violates the recession cone property, which is necessary for the firm problem to have a maximizer since is closed and nonempty, e.g. Kreps (2012), Proposition 9.7. Note from part (iii), when Assumption 6 holds it follows that is a production correspondence, and thus satisfies the recession cone property.

Theorem 3(iii) is related to classic work on the identification of a deterministic production set from a deterministic profit function.262626See e.g. Kreps (2012), Corollary 9.18 for a textbook result. In this paper, however, we begin with the distribution of profits and prices. Part (iii) shows that with this distribution, it is possible to identify the distribution of features of , such as the distribution of possible profit-maximizing quantities. We emphasize that this is true even if quantities are unobservable. An additional manner in which (iii) differs from textbook analysis is that, in econometric settings, it is not always natural to assume that all prices are observed (). Theorem 3 clarifies the variation in prices sufficient for nonparametric identification of production sets. We note that while Assumption 6 is sufficient for point identification of , it is not necessary as illustrated in Online Appendix E.

Remark 4.

Our identification analysis does not impose any a priori restrictions that certain dimensions of correspond to inputs, i.e. weakly negative numbers. This additional restriction can be imposed by modifying the set constructed in Theorem 3. Specifically, the set constructed in this theorem may be intersected with an appropriate half-space that encodes that certain dimensions (corresponding to inputs) must be nonpositive. We note that an analogous restriction for outputs is not informative because of the assumption of free disposal.

5. Sharp Counterfactual Bounds

Theorem 3 makes use of a shape restriction to characterize the identified set of the production correspondence for profit-maximizing, price-taking firms. This shape restriction may be used for a dual purpose of providing sharp counterfactual bounds. This follows a long tradition in revealed preference. Varian (1982, 1984) has exploited the close connections between empirical content, recoverability of structural functions, and counterfactuals. Recent work in demand analysis building on these connections includes Blundell et al. (2003, 2017), Allen and Rehbeck (2019), and Aguiar and Kashaev (2021). In this section we describe a method to bound objects of interest outside of the support of the data.

Since homogeneity and convexity of the heterogeneous profit function allow us to identify it over , we can associate the conditional support (of prices condition on ) with the set where is identified. That is why, for notational simplicity and in this section only, we assume that is a closed subset of the unit sphere for all , and we consider counterfactual prices with norm normalized to 1.

We first present a result characterizing quantities consistent with profit maximization. Theorem 3(ii) is the basis for the following proposition.

Proposition 1.

Let be a finite subset of the unit sphere . Given and , the set of output/input functions can generate if and only if

The vector is interpreted as a candidate supply vector given price and productivity ; it need not be unique and thus may not be equivalent to the supply function. Recall that as discussed in Remark 4, we do not impose a priori restrictions that certain components of are inputs; this would correspond to imposing additional sign restrictions on the functions described in the proposition.

Proposition 1 essentially states that for each there must exist output/input vectors such that the weak axiom of profit maximization holds (Varian, 1984). We note, however, that the primitive observables of our paper are the distribution of profits and prices.

We can adapt Proposition 1 to answer counterfactual questions by considering a hypothetical tuple of prices and quantities. If Proposition 1 applies with these additional counterfactual values, then they are feasible given the theory. In more detail, we present bounds on counterfactual objects, potentially with additional restrictions. The counterfactual values involve a function of interest. The restrictions involve a function that depends on the counterfactual price and quantity . We encode the restrictions by the combinations such that . For instance, if the counterfactual price is fixed to a given vector and no restrictions are imposed on , then . The upper bound with heterogeneity level is given by

| s.t. | |||

The lower bound is given by

| s.t. | |||

We provide some examples covered by this general setup. Note that these bounds hold for each , and thus one may also bound the distribution of and . We reiterate that these upper and lower bounds apply to prices on the unit sphere, though they may be adapted for prices off the unit sphere as illustrated in the following examples.

Example 2 (Profit bounds for a counterfactual price).

Suppose that we are interested in upper and lower bounds for profits at a given counterfactual price . When prices are on the unit sphere, we may specify and . Then the problem can be simplified to get

where is the envelope of all production possibility sets consistent with the data defined in Theorem 3. The above bounds are sharp in the following sense: if is finite, then it is feasible, i.e. there exists a production set that can generate . If is not finite, then for any finite level there exists a production set that can generate . Analogous statements hold for the lower bounds . Recall that we assume the support of prices is a subset of the unit sphere. This may be imposed in empirical settings by replacing prices with normalized prices . For counterfactual questions involving a price off the unit sphere , one can bound counterfactual profits at price and then multiply the upper and lower bounds by .

Example 3 (Quantity bounds for a counterfactual price).

Suppose that we are interested in the upper and lower bounds for for a given counterfactual price , where is a vector. For example, with we are interested in bounds on the first component of . Then and .

Example 4 (Profit bounds for a counterfactual quantity).

Suppose a regulator is considering imposing a new regulation that the first component of the output/input vector is fixed at . For example, in analysis of health care (Bilodeau et al., 2000) a hospital may be required to treat a certain number of patients. To bound profits we may write the objective function as . The constraint is given by .272727Note that the problem may not have a solution since the set of parameters that satisfy restrictions may be empty. Bounds on profits with this quantity may be useful for a regulator wondering whether a hospital of type would be profitable with the hypothetical regulation. If the upper bound on profits is negative, the answer is definitively no. If the lower bound on profits is positive, the answer is definitively yes.282828This maintains the assumptions of price-taking, profit-maximizing behavior with a technology that is described by a production correspondence. An additional question a regulator might ask is which types of firms could still be profitable. This can be addressed by studying functions and as varies. Note that the constraints are general, and inequality constraints may be incorporated as well by using indicator functions.

When is finite, computing bounds in Examples 2 and 3 is straightforward since they are the values of linear programs. Example 4 is also a linear program if we add the additional constraint that the counterfactual price is fixed, . In general, the computational difficulty of the bounds and depends on the nature of the objective function and the constraint.

6. Estimation of Production Sets and Consistency

The previous identification results describe how to identify the profit or restricted profit function. Appendix B describes one estimator of the restricted profit function, but there are many depending on assumptions concerning exogeneity or whether productivity is discrete or continuous. This section links any estimator of the restricted profit function to an induced estimator of the corresponding production set. As in previous section, for notational convenience we work with the profit function, though the analysis applies to the restricted profit function by conditioning. In the restricted case, we would instead estimate the restricted production correspondence.

We now describe how an estimator of the profit function may be used to construct an estimator of the production possibility set for a firm with productivity level . The main result in this section relates the estimation error of (for ) and that of the constructed set (for ). Consistency and rates of convergence results for thus have analogous statements for .

As setup, we now formalize our notions of distance both for functions and sets. We present our result for a fixed . We assume that is identified over (we assume Assumption 6). Given a fixed and , a natural estimator for is

This set is a plug-in estimator motivated by Theorem 3. A commonly used notion of distance between convex sets is the Hausdorff distance. The Hausdorff distance between two convex sets is given by

Unfortunately, the Hausdorff distance between and can be infinite. For this reason we will consider the Hausdorff distance between certain extensions of these sets. The following example illustrates why the original distance may be infinite.

Example 5.

Suppose that and for some ,

Note that although for every finite , the Hausdorff distance between these sets is infinite for every finite .

Example 5 illustrates a technical concern with the Hausdorff distance that arises because of the unboundedness of production possibility sets. However, in empirical applications one may be interested in production possibility sets in regions that correspond to prices that are bounded away from zero. Thus, instead of working with all possible prices we will work only with certain empirically relevant compact convex subsets of . We consider the Hausdorff distance between extensions such as

where is convex and compact. These sets nest the original sets (e.g. ) because the inequalities hold only for , not for every . Moreover, the parts of the production possibility frontiers of the sets and coincide at points that are tangential to price vectors from (see Figure 5).

We now turn to the main result in this section, which establishes an equality relating the distance between and , and the distance between extensions of and . Our distance for these profit functions is given by

To state the following result, let be a collection of all compact, convex, and nonempty subsets of .

Theorem 4.

Maintain the assumption that is homogeneous of degree 1 and convex.292929Recall that this is equivalent to price-taking, profit-maximizing behavior with technology described by a production correspondence. Suppose, moreover, that for every , is an estimator of that is homogeneous of degree and continuous. If is convex, then

for every .

Theorem 4 is a nontrivial extension of a well-known relation between the Hausdorff distance and the support functions of convex compact sets to convex, closed, and unbounded sets.303030See Kaido and Santos (2014) for a recent application of this result for convex compact sets. Homogeneity of an estimator can be imposed by rescaling the data by dividing by one of the prices. Unfortunately, convexity can be more challenging to impose and so we turn to a related result that covers cases in which is not convex. To formalize our result, we introduce two additional parameters:

Proposition 2.

Maintain the assumption that is homogeneous and convex. Suppose, moreover, that for every , is an estimator of that is homogeneous of degree and continuous. If and , then

with probability approaching , for every . In particular,

7. Conclusion

In this paper we provide an update to classical duality theory in order to identify heterogeneous production sets in the presence of endogeneity, measurement error, omitted prices, and unobservable quantities. Our framework’s main strength is to unpack rich heterogeneity as well as rich substitution/complementarity patterns with market level variation, using values of optimization problems. We achieve this by exploiting all shape constraints imposed by the economic environment we consider. This includes a key restriction that firms can be ranked in terms of productivity, and there are finitely many types of firms. Our identification results are constructive and can be applied in many available data sets.

Acknowledgments

We thank the editor, the associate editor, and three anonymous referees for their comments and suggestions. We are grateful to Paul Grieco, Lance Lochner, Rosa Matzkin, Salvador Navarro, David Rivers, Susanne Schennach, Holger Sieg, and Al Slivinsky for useful comments and encouragement. We also thank the ceminar participants at Duke University, University of Montreal, McMaster University, and attendants of NASMES 2019, Empirical Microeconomics Workshop at University of Calgary, MEG 2019, CESG 2019, NAWMES 2020, vNAPW XI, WARP 2020, and CIREQ Montreal Econometrics Conference.

References

- (1)

- Ackerberg et al. (2015) Ackerberg, Daniel A, Kevin Caves, and Garth Frazer (2015) “Identification properties of recent production function estimators,” Econometrica, 83 (6), 2411–2451.

- Afriat (1972) Afriat, Sidney N (1972) “Efficiency estimation of production functions,” International economic review, 568–598.

- Aguiar and Kashaev (2021) Aguiar, Victor H and Nail Kashaev (2021) “Stochastic revealed preferences with measurement error,” The Review of Economic Studies, 88 (4), 2042–2093.

- Albouy and Ehrlich (2018) Albouy, David and Gabriel Ehrlich (2018) “Housing productivity and the social cost of land-use restrictions,” Journal of Urban Economics.

- Allen and Rehbeck (2019) Allen, Roy and John Rehbeck (2019) “Identification with additively separable heterogeneity,” Econometrica, 87 (3), 1021–1054.

- Arcidiacono and Miller (2011) Arcidiacono, Peter and Robert A Miller (2011) “Conditional choice probability estimation of dynamic discrete choice models with unobserved heterogeneity,” Econometrica, 79 (6), 1823–1867.

- Beresteanu et al. (2011) Beresteanu, Arie, Ilya Molchanov, and Francesca Molinari (2011) “Sharp identification regions in models with convex moment predictions,” Econometrica, 79 (6), 1785–1821.

- Beresteanu and Molinari (2008) Beresteanu, Arie and Francesca Molinari (2008) “Asymptotic properties for a class of partially identified models,” Econometrica, 76 (4), 763–814.

- Berger et al. (1993) Berger, Allen N, Diana Hancock, and David B Humphrey (1993) “Bank efficiency derived from the profit function,” Journal of Banking & Finance, 17 (2-3), 317–347.

- Bilodeau et al. (2000) Bilodeau, Daniel, Pierre-Yves Cremieux, and Pierre Ouellette (2000) “Hospital cost function in a non-market health care system,” Review of Economics and Statistics, 82 (3), 489–498.

- Blundell et al. (2003) Blundell, Richard W, Martin Browning, and Ian A Crawford (2003) “Nonparametric Engel curves and revealed preference,” Econometrica, 71 (1), 205–240.

- Blundell et al. (2017) Blundell, Richard W, Dennis Kristensen, and Rosa Liliana Matzkin (2017) “Individual counterfactuals with multidimensional unobserved heterogeneity,”Technical report, cemmap working paper.

- Bonhomme and Manresa (2015) Bonhomme, Stéphane and Elena Manresa (2015) “Grouped patterns of heterogeneity in panel data,” Econometrica, 83 (3), 1147–1184.

- Brunel (2016) Brunel, Victor-Emmanuel (2016) “Concentration of the empirical level sets of Tukey’s halfspace depth,” Probability Theory and Related Fields, 1–32.

- Burke et al. (2019) Burke, Marshall, Lauren Falcao Bergquist, and Edward Miguel (2019) “Sell low and buy high: arbitrage and local price effects in Kenyan markets,” The Quarterly Journal of Economics, 134 (2), 785–842.

- Cherchye et al. (2014) Cherchye, Laurens, Thomas Demuynck, Bram De Rock, and Kristof De Witte (2014) “Non-parametric Analysis of Multi-output Production with Joint Inputs,” The Economic Journal, 124 (577), 735–775.

- Cherchye et al. (2018) Cherchye, Laurens, Thomas Demuynck, Bram De Rock, and Marijn Verschelde (2018) “Nonparametric identification of unobserved technological heterogeneity in production,” Working Paper Research 335, National Bank of Belgium, https://EconPapers.repec.org/RePEc:nbb:reswpp:201802-335.

- Cherchye et al. (2016) Cherchye, Laurens, Bram De Rock, and Barnabe Walheer (2016) “Multi-output profit efficiency and directional distance functions,” Omega, 61, 100 – 109, https://doi.org/10.1016/j.omega.2015.07.010.

- Chernozhukov et al. (2017) Chernozhukov, Victor, Alfred Galichon, Marc Henry, and Brendan Pass (2017) “Single market nonparametric identification of multi-attribute hedonic equilibrium models,” arXiv preprint arXiv:1709.09570.

- Chiong et al. (2016) Chiong, Khai Xiang, Alfred Galichon, and Matt Shum (2016) “Duality in dynamic discrete-choice models,” Quantitative Economics, 7 (1), 83–115.

- Combes et al. (2021) Combes, Pierre-Philippe, Gilles Duranton, and Laurent Gobillon (2021) “The production function for housing: Evidence from France,” Journal of Political Economy, 129 (10), 2766–2816.

- Cunha et al. (2010) Cunha, Flavio, James J Heckman, and Susanne M Schennach (2010) “Estimating the technology of cognitive and noncognitive skill formation,” Econometrica, 78 (3), 883–931.

- De Loecker et al. (2016) De Loecker, Jan, Pinelopi K Goldberg, Amit K Khandelwal, and Nina Pavcnik (2016) “Prices, markups, and trade reform,” Econometrica, 84 (2), 445–510.

- D’Haultfœuille and Février (2015) D’Haultfœuille, Xavier and Philippe Février (2015) “Identification of mixture models using support variations,” Journal of Econometrics, 189 (1), 70–82.

- Diewert (1982) Diewert, W Erwin (1982) “Duality approaches to microeconomic theory,” Handbook of mathematical economics, 2, 535–599.

- Diewert (1973) Diewert, W.E (1973) “Functional forms for profit and transformation functions,” Journal of Economic Theory, 6 (3), 284 – 316, https://doi.org/10.1016/0022-0531(73)90051-3.

- Doraszelski and Jaumandreu (2013) Doraszelski, Ulrich and Jordi Jaumandreu (2013) “R&D and productivity: Estimating endogenous productivity,” Review of Economic Studies, 80 (4), 1338–1383.

- Doraszelski and Jaumandreu (2018) (2018) “Measuring the bias of technological change,” Journal of Political Economy, 126 (3), 1027–1084.

- Ekeland et al. (2004) Ekeland, Ivar, James J Heckman, and Lars Nesheim (2004) “Identification and estimation of hedonic models,” Journal of political economy, 112 (S1), S60–S109.

- Epple et al. (2010) Epple, Dennis, Brett Gordon, and Holger Sieg (2010) “A new approach to estimating the production function for housing,” American Economic Review, 100 (3), 905–24.

- Fabrizio et al. (2007) Fabrizio, Kira R., Nancy L. Rose, and Catherine D. Wolfram (2007) “Do Markets Reduce Costs? Assessing the Impact of Regulatory Restructuring on US Electric Generation Efficiency,” American Economic Review, 97 (4), 1250–1277, 10.1257/aer.97.4.1250.

- Farrell (1957) Farrell, Michael James (1957) “The measurement of productive efficiency,” Journal of the Royal Statistical Society: Series A (General), 120 (3), 253–281.

- Foster et al. (2008) Foster, Lucia, John Haltiwanger, and Chad Syverson (2008) “Reallocation, firm turnover, and efficiency: selection on productivity or profitability?” American Economic Review, 98 (1), 394–425.

- Fox and Gandhi (2016) Fox, Jeremy T and Amit Gandhi (2016) “Nonparametric identification and estimation of random coefficients in multinomial choice models,” The RAND Journal of Economics, 47 (1), 118–139.

- Fuss and McFadden (1978) Fuss, Melvyn and Daniel McFadden eds. (1978) Production Economics: A Dual Approach to Theory and Applications: Applications of the Theory of Production: Elsevier.

- Galichon and Salanié (2015) Galichon, Alfred and Bernard Salanié (2015) “Cupid’s invisible hand: Social surplus and identification in matching models.”

- Gandhi et al. (2020) Gandhi, Amit, Salvador Navarro, and David A Rivers (2020) “On the identification of gross output production functions,” Journal of Political Economy, 128 (8), 2973–3016.

- Glaeser et al. (2005) Glaeser, Edward L, Joseph Gyourko, and Raven E Saks (2005) “Why have housing prices gone up?” American Economic Review, 95 (2), 329–333.

- Grieco and McDevitt (2016) Grieco, Paul LE and Ryan C McDevitt (2016) “Productivity and quality in health care: Evidence from the dialysis industry,” The Review of Economic Studies, 84 (3), 1071–1105.

- Griliches and Mairesse (1995) Griliches, Zvi and Jacques Mairesse (1995) “Production functions: the search for identification,”Technical report, National Bureau of Economic Research.

- Hanoch and Rothschild (1972) Hanoch, Giora and Michael Rothschild (1972) “Testing the assumptions of production theory: a nonparametric approach,” Journal of Political Economy, 80 (2), 256–275.

- Hu and Ridder (2010) Hu, Yingyao and Geert Ridder (2010) “On deconvolution as a first stage nonparametric estimator,” Econometric Reviews, 29 (4), 365–396.

- Hu et al. (2017) Hu, Yingyao, Susanne M Schennach, and Ji-Liang Shiu (2017) “Injectivity of a class of integral operators with compactly supported kernels,” Journal of Econometrics, 200 (1), 48–58.

- Kaido (2016) Kaido, Hiroaki (2016) “A dual approach to inference for partially identified econometric models,” Journal of econometrics, 192 (1), 269–290.

- Kaido et al. (2019) Kaido, Hiroaki, Francesca Molinari, and Jörg Stoye (2019) “Confidence intervals for projections of partially identified parameters,” Econometrica, 87 (4), 1397–1432.

- Kaido and Santos (2014) Kaido, Hiroaki and Andres Santos (2014) “Asymptotically efficient estimation of models defined by convex moment inequalities,” Econometrica, 82 (1), 387–413.

- Katayama et al. (2003) Katayama, Haijime, Shihua Lu, and James R Tybout (2003) “Why plant-level productivity studies are often misleading, and an alternative approach to interference.”

- Kim et al. (2020) Kim, Youngseok, Peter Carbonetto, Matthew Stephens, and Mihai Anitescu (2020) “A fast algorithm for maximum likelihood estimation of mixture proportions using sequential quadratic programming,” Journal of Computational and Graphical Statistics, 29 (2), 261–273.

- Kitamura and Laage (2018) Kitamura, Yuichi and Louise Laage (2018) “Nonparametric Analysis of Finite Mixtures.”

- Klette and Griliches (1996) Klette, Tor Jakob and Zvi Griliches (1996) “The inconsistency of common scale estimators when output prices are unobserved and endogenous,” Journal of applied econometrics, 11 (4), 343–361.

- Kreps (2012) Kreps, David M (2012) Microeconomic foundations I: choice and competitive markets, 1: Princeton university press.

- Kriegel et al. (2011) Kriegel, Hans-Peter, Peer Kröger, Jörg Sander, and Arthur Zimek (2011) “Density-based clustering,” Wiley Interdisciplinary Reviews: Data Mining and Knowledge Discovery, 1 (3), 231–240.

- Levinsohn and Petrin (2003) Levinsohn, James and Amil Petrin (2003) “Estimating production functions using inputs to control for unobservables,” The Review of Economic Studies, 70 (2), 317–341.

- Li and Sasaki (2017) Li, Tong and Yuya Sasaki (2017) “Constructive Identification of Heterogeneous Elasticities in the Cobb-Douglas Production Function,” arXiv preprint arXiv:1711.10031.

- López and Still (2007) López, Marco and Georg Still (2007) “Semi-infinite programming,” European Journal of Operational Research, 180 (2), 491–518.

- Manole and Khalili (2021) Manole, Tudor and Abbas Khalili (2021) “Estimating the number of components in finite mixture models via the Group-Sort-Fuse procedure,” The Annals of Statistics, 49 (6), 3043–3069.

- Matzkin (1992) Matzkin, Rosa L (1992) “Nonparametric and distribution-free estimation of the binary threshold crossing and the binary choice models,” Econometrica: Journal of the Econometric Society, 239–270.

- Matzkin (2003) (2003) “Nonparametric estimation of nonadditive random functions,” Econometrica, 71 (5), 1339–1375.

- McFadden (1981) McFadden, Daniel (1981) “Econometric models of probabilistic choice,” Structural analysis of discrete data with econometric applications, 198272.

- Melitz and Redding (2014) Melitz, Marc J and Stephen J Redding (2014) “Heterogeneous firms and trade,” in Handbook of international economics, 4, 1–54: Elsevier.

- Nerlove (1963) Nerlove, Marc (1963) “Returns to Scale in Electricity Supply,” Measurement in Economics.

- Olley and Pakes (1996) Olley, G Steven and Ariel Pakes (1996) “The Dynamics of Productivity in the Telecommunications Equipment Industry,” Econometrica, 64 (6), 1263–1297.

- Pakes (1996) Pakes, Ariel (1996) “Dynamic structural models, problems and prospects: mixed continuous discrete controls and market interaction,” in Advances in Econometrics, Sixth World Congress, 2, 171–259, by C. Sims.

- Ray ⓡ Robson (2018) Ray, Debraj ⓡ Arthur Robson (2018) “Certified random: A new order for coauthorship,” American Economic Review, 108 (2), 489–520.

- Roberts and Supina (1996) Roberts, Mark J and Dylan Supina (1996) “Output price, markups, and producer size,” European Economic Review, 40 (3-5), 909–921.

- Rockafellar (1970) Rockafellar, R Tyrrell (1970) Convex Analysis: Princeton University Press.

- Schennach (2016) Schennach, Susanne M (2016) “Recent advances in the measurement error literature,” Annual Review of Economics, 8, 341–377.

- Shephard (1953) Shephard, Ronald William (1953) Cost and production functions: Princeton University Press.

- Varian (1982) Varian, Hal R (1982) “The nonparametric approach to demand analysis,” Econometrica: Journal of the Econometric Society, 945–973.

- Varian (1984) (1984) “The nonparametric approach to production analysis,” Econometrica: Journal of the Econometric Society, 579–597.

- Zellner et al. (1966) Zellner, Arnold, Jan Kmenta, and Jacques Dreze (1966) “Specification and estimation of Cobb-Douglas production function models,” Econometrica: Journal of the Econometric Society, 784–795.

Appendix A Proofs of Main Results

A.1. Proof of Lemma 1

A.2. Proof of Theorem 1

First, note that since the support of is a connected set (Assumption 4(i)) and is discrete, the conditional support of conditional on and is a union of connected sets for all and in their joint support. Hence, we can find the shortest (with respect to Lebesgue measure) isolated connected segment of the support for every and . Next, among those short segments we can find the shortest one. By construction this segment will correspond to from Assumption 4(ii). As a result, under Assumption 4, we can find an interval in the support of conditional on , , and such that

and

for any . Hence, we identify

where we leverage that has mean zero even after conditioning.

Thus, we can also recover the distribution of by subtracting the identified from the known distribution of . Since and have bounded support and are independent conditional on and , we can constructively identify the moment generating function of conditional on and as the ratio of the moment generating functions of conditional on and and . Since the distribution of conditional on and is discrete, its moment generating function is sufficient for its identification. Note that the moment generating function of is well-defined and is never equal to zero since is a bounded random variable.

Assumption 3 implies that whenever a type occurs with positive probability conditional on and , then higher types also occur with positive probability. Assumption 1 then implies that the ranking over restricted profits is equivalent to the ranking over productivity . As a result, if some firm of type does not operate given and , then it has to be a low type. Let be the support of conditional on and . Fix some and . Since the support of is finite, the set will also be finite. As a result, Assumption 1 implies that

That is, the most productive firm will make more profits than any other firm. Note that the firm with productivity , if it is present in the market, will be the second one in terms of restricted profits :

In general, given and , if the firm with productivity operates (), then

Note that we may not be able to identify the structural restricted profit function for arguments in which is too low.

A.3. Proof of Theorems 2

Fix some , and take from the statement of the theorem and from condition (ii). We abuse notation and drop and . By homogeneity of degree 1 of we have that for every

| (A.1) |

Moreover, since (recall that we dropped and from the notation) and for , we have that

| (A.2) |

for every . Combining (A.1) and (A.2) we get that

as long as for every . This latter condition is satisfied for almost every with respect to Lebesgue measure by Assumption 5(iv). From Assumption 5(i), , so we obtain that

| (A.3) |

Let . Note that does not depend on . Since satisfies the rank condition there exists a nonsingular and such that equation (A.3) can be rewritten as

| (A.4) |

where and . Since is of full rank and is identified, and is identified, is identified. Since the choice of was arbitrary and we know the location (Assumption 5(ii)), we identify for every .

A.4. Proof of Theorem 3

It is immediate that is closed, convex, and satisfies free disposal for every . Moreover, for every and . Thus, conclusion (i) follows from the fact that is identified for each and by Theorem 1.

To establish conclusion (ii), recall that under the assumptions of Theorem 1, any given production set can generate the data if and only if for every . The set is constructed as the largest set (not necessary production set) consistent with profit maximization. This set is closed, convex, and satisfies free disposal. Since a production correspondence also must satisfy the recession cone property, we obtain that .

A.5. Proof of Proposition 1

Fix some . To simplify notation we drop from the objects below (e.g. and ). Suppose can generate . Since are profit-maximizing output/input vectors we must have . To prove that for all , assume the contrary. But then is not maximizing profits at since is available. The contradiction proves necessity.

To prove sufficiency consider

where denotes the convex hull of a set , i.e. the smallest convex set containing . The summation is the Minkowski sum. is sometimes referred to as the free-disposal convex hull of . In particular, note that is convex, closed, and satisfies free disposal.

We obtain that for every ,

Because is finite, is bounded. Thus, its convex hull is also bounded. This implies that is finite for every , hence the recession cone property is satisfied for the set .313131We note that Varian (1984) studies a result related to this proposition, taking as primitives a deterministic dataset of prices and quantities. He does not verify the recession cone property.

It is left to show that

for every . The first equality is assumed. Suppose the second equality is not true for some . Then there exists such that . Since it can be represented as a finite convex combination of points from . But since

for all it has to be the case that

The contradiction completes the proof. Since the choice of was arbitrary the result holds for all .

A.6. Proof of Theorem 4 and Proposition 2

The Hausdorff distance between two convex sets is given by

Alternatively, the Hausdorff distance can be defined as