Probabilistic error analysis for some approximation schemes to optimal control problems

Abstract.

We introduce a class of numerical schemes for optimal stochastic control problems based on a novel Markov chain approximation, which uses, in turn, a piecewise constant policy approximation, Euler-Maruyama time stepping, and a Gauß-Hermite approximation of the Gaußian increments. We provide lower error bounds of order arbitrarily close to 1/2 in time and 1/3 in space for Lipschitz viscosity solutions, coupling probabilistic arguments with regularization techniques as introduced by Krylov. The corresponding order of the upper bounds is 1/4 in time and 1/5 in space. For sufficiently regular solutions, the order is 1 in both time and space for both bounds. Finally, we propose techniques for further improving the accuracy of the individual components of the approximation.

Keywords: Optimal stochastic control, Markov chain approximation schemes, error estimates

1. Introduction

Let be a probability space with filtration induced by an -Brownian motion for some . We consider a controlled process governed by

| (1.1) |

where and take values, respectively, in and . We assume that the control vector process belongs to the set of progressively measurable processes with values in . For any , we will denote by the unique strong solution of (1.1), under the assumptions specified later. To simplify the notation, where no ambiguities arise, we will indicate the starting point of the processes involved as a subscript in the expectation, i.e. .

Given and two real valued functions and , namely the running and terminal cost, respectively, for any , , the value function of the optimal control problem we consider is defined by

| (1.2) |

It is well known that this problem is related to the solution of a second order Hamilton-Jacobi-Bellman (HJB) equation for which, in the general case, solutions are considered the viscosity sense (see, for instance, [12]). Furthermore, explicit solutions for this kind of nonlinear equations are rarely available, so that their numerical approximation becomes vital. The seminal work by Barles and Souganidis [5] establishes the basic framework for convergence of numerical schemes to viscosity solutions of HJB equations. The fundamental properties required are: monotonicity, consistency, and stability of the scheme. We recall that, in multiple dimensions, standard finite difference schemes are in general non-monotone. As an alternative to finite difference schemes, semi-Lagrangian (SL) schemes [30, 11, 14] are monotone by construction. The schemes we introduce belong to this family.

In general, the provable order of convergence for second order HJB equations is significantly less than one. By a technique pioneered by Krylov based on “shaking the coefficients” and mollification to construct smooth sub- and/or super-solutions, [25, 27, 2, 3, 4] prove certain fractional convergence orders, mainly using PDE-based techniques which rely on a comparison principle between viscosity sub- and super-solutions and estimates on the consistency error of the numerical scheme.

Here, we study a new family of SL schemes based on a discrete time approximation of the optimal control problem. We use purely probabilistic techniques and a direct comparison of the two optimal control problems to obtain error estimates which are, to our knowledge, the best ones available in the literature under these weak assumptions.

An important step in order to define our scheme is to approximate the set of controls by piecewise constant controls. This introduces an asymmetry between the upper and the lower bound of the error, and it is the lower bound where we get an improvement over known results.

The approach most closely related to ours is arguably [26], especially Section 5 therein, where approximations based on piecewise constant policies and subsequently on discrete-time random walks are studied. The analysis there utilizes a combination of stochastic and analytic techniques, in particular through controlling the approximation error by the truncation error between the generator of the controlled process and its discrete approximation, and Itô’s lemma with the dynamic programming principle to aggregate the local error over time. We will be able to improve the order of the error bounds partly by using recent improved estimates for the piecewise constant policy approximation in [23], but also by avoiding the use of the truncation error, the order of which is limited to 1, and replacing it by a direct estimate of the strong and weak approximation error of the scheme for the stochastic differential equation.

The main contributions of this paper are as follows.

-

•

We propose new discrete approximations of controlled diffusion processes based on piecewise constant controls over intervals of length and Gauß-Hermite points.

-

•

We present a novel analysis technique for the resulting semi-discrete approximations by purely probabilistic arguments and direct use of the dynamic programming principle.

This allows us to derive one-sided, lower error bounds of order for timestep and spatial mesh size , for Lipschitz viscosity solutions (assumptions (H1) to (H3) below). They coincide with the two-sided bounds in [14] for the standard linear-interpolation SL scheme, i.e. , and improve them for . The achieved upper bounds are identical to [14], i.e. of order . For sufficiently smooth solutions, the corresponding error bounds are of order in both and .

The paper is organised as follows. In Section 2 we present the setting and the main assumptions for the optimal control problem and we describe the piecewise constant policy approximation. In Section 3 the Markov-chain approximation scheme is introduced and error bounds are obtained in Section 4. Section 5 discusses the order obtained in the case of smooth solutions and further improvements of the components of the scheme, including higher order time stepping and interpolation, while Section 6 demonstrates the improvement achieved by a higher order scheme numerically. Section 7 concludes.

2. Main assumptions and preliminaries

In what follows, denotes the Euclidean norm in for any and its induced matrix norm. We consider standard assumptions on the optimal control problem:

-

(H1)

is a compact subset of a separable metric space;

-

(H2)

and are continuous functions and there exists such that for any

-

(H3)

and are continuous functions and there exists such that for any

Under these assumptions one can prove the following regularity result on :

Proposition 2.1 ([39, Proposition 3.1, Chapter IV]).

Let (H1)-(H3) be satisfied. There exists such that for any and

(where denotes the Lipschitz constant of and only depends on and in assumption (H2)).

Hereafter we assume . Indeed, if this is not the case it is possible to consider the augmented dynamics with and the modified terminal cost . Denoting by , it is sufficient to observe that to recover the aforementioned case.

A fundamental property satisfied by the value function is the following Dynamic Programming Principle (DPP) (see, for instace [39, Theorem 3.3, Chapter IV]): for any , one has

| (2.1) |

The main ideas of our approach apply to a general class of discrete-time schemes. Let and . We introduce a time mesh for .

The first step in our approximation is to introduce a time discretization of the control set. We consider the set of controls in that are constant in each interval for , i.e.

In what follows, we will identify any element of by the sequence of random variables taking values in (denoted by for simplicity) and will write . We denote by the value function obtained by restricting the supremum in (1.2) to controls in , that is

| (2.2) |

Clearly, since , one has for any ,

| (2.3) |

Under assumptions (H1)-(H3), an upper bound of order for the error related to this approximation was first obtained by Krylov in [26]. Recently, this estimate has been improved to the order in [23], so that one has

| (2.4) |

for some constant . While the estimates in [26] and [23] are obtained for bounded and , it follows by similar but more tedious steps that the results also hold in our framework taking a constant growing polynomially in the space variable, as already remarked in [23].

The DPP for the value function reads

| (2.5) |

In particular, the restriction of the control set to implies that the supremum in (2.5) is taken over the set of control values (compared with (2.1)). The family of schemes we consider are recursively defined by an approximation of (2.5) and lead to the definition of a numerical solution approximating .

3. Markov chain approximation schemes

We present a class of schemes which are based on a Markov chain approximation of the optimal control problem (2.2). This follows the classical philosophy presented in [28], although they take the opposite direction and use finite difference approximations to construct Markov chains, while here we use time stepping schemes and quadrature formulae to define SL schemes. Similar probabilistic interpretations of such schemes have been given in [11, 26, 15] for the time-dependent case and in [30] for the infinite horizon case. What is new here is the construction of schemes with provable higher order error bounds, and the direct use of the dynamic programming principle for the discrete approximation to derive these bounds.

3.1. Euler-Maruyama scheme

We start with an approximation of the process by the Euler-Maruyama scheme. For any given , we consider the following recursive relation:

| (3.1) |

for . The increments are independent, identically distributed random variables such that

| (3.2) |

We will denote by the solution to (3.1) associated with the control and such that . Under assumptions (H1)-(H2), the rate of strong convergence of the scheme (3.1) is , as given, e.g., in [24]. Although the result from there is not directly applicable here as the coefficients are non-Lipschitz in time due to the jumps in the control process, we can follow the same steps as in the proof of [32, Theorem 1.1, Chapter I], using the fact that the controls are constant over individual timesteps. Therefore, one has:

Proposition 3.1.

Let assumptions (H1)-(H2) be satisfied. Then there exists a constant (independent of ) such that for any , one has

For completeness, a sketch of the proof is reported in the appendix.

As a consequence, denoting

for any , thanks to the Lipschitz continuity of , one has

| (3.3) |

Moreover, still satisfies a DPP,

| (3.4) |

3.2. Gauß-Hermite quadrature

Recalling that , we can also write (3.4) as

| (3.5) |

The discrete-time scheme we are going to define is based on the Gauß-Hermite approximation of the right-hand term in (3.5).

Let us start for simplicity with the case .

Let and be the Hermite polynomial of order , i.e.

(see for instance [22, Section 7.8] for this definition and the following results). We denote by the zeros of and by the corresponding weights, given by

Therefore, defining

for any smooth real-valued function (say at least ) we can make use of the following approximation (see [22, p. 395]):

| (3.6) |

Indeed, the quadrature formula in (3.6), is exact when the function is a polynomial of degree lower or equal to .

Now observe first that . Moreover, setting in (3.6) and using that equality holds in this case, one gets . We can therefore define a sequence of i.i.d. random variables such that for any

Using the fact that the quadrature formula integrates linear and quadratic functions exactly with respect to the Gaußian measure for , we have and

| 0 | ||||||||

For any control , in the sequel we will denote by the Markov chain approximation of the process recursively defined by

| (3.7) |

with . Therefore, starting from (3.5) and applying the Gauß-Hermite quadrature formula (3.6), our scheme will be defined by

| (3.8) |

Remark 1.

Iterating, we obtain the following representation formula for :

The rate of weak convergence

In this section, we prove the rate of weak convergence of the random walk defined by (3.7) to the process given by the Euler-Maruyama scheme (3.1).

Proposition 3.2.

Let assumptions (H1)-(H2) be satisfied and let . Then there exists a constant such that for any function one has

for any , , and , and where we denoted for

Proof.

We adapt a standard argument from numerical quadrature. Let us take for simplicity (the case works in the same way) and denote By Taylor expansion, we can write

for some . In the same way we get

for some . At this point we recall that, by construction, the Gauß-Hermite quadrature formula is exact for any polynomial of degree , so for any we have

This implies that

where we have used the fact that for some . Calculating explicitly in the second line and by the fact that depends only on in (H2), the constant can be given as

and only depends on and the constants in assumption (H2). ∎

Multi-dimensional Brownian motion

In the case of , it is classical (see, e.g. [13, Section 5.6]) to define an approximation by a tensor product of the formula (3.6), that is

| (3.9) |

Then, denoting for any the vector and the scalar , one can define an approximation to by

| (3.10) |

This differs from the traditional Markov chain approximation approach taken in [28, Section 5.3], where monotone finite difference schemes (i.e., those leading to positive weights) are used to define the matrix of transition probabilities.

It is easy to observe that the construction in (3.9) leads to an exponential growth of the computational complexity in the dimension , as it requires at each time step and for each node the evaluation of the solution at points. Retracing the proof of Proposition 3.2, one can deduce that in order to guarantee a weak error estimates of order , it is sufficient to find weights and nodes , , for some possibly lower than , which integrate exactly all polynomials of degree lower or equal than . Moreover, the probabilistic interpretation of our scheme also requires that , . Such pairs then have to satisfy

with and defined by

where is a basis for the space of polynomials of degree in and .

The existence of a solution of the form for some follows from Tchakaloff’s Theorem (see [35], and also [6] for a recent simpler proof).

A constructive method for independent Gaußian random variables as in the present case is proposed in [16], while an efficient procedure for the general, dependent case applied to the uniform measure is given in [36]. This gives a substantial reduction for large and moderate in particular. Table 4.1 in [36] gives numerical values for versus for and different , such as: : ; : ; : ; : .

We end by noting that sparse grid quadrature (see, e.g. [20]), which has been shown to overcome the curse of dimensionality for integrals of sufficiently regular functions, is not suitable here because of the negativity of weights which is essential to their construction. On the other hand, applying cubature on Wiener space (see [29]) may be a possible extension.

In what follows, we will use the notation to generalise (3.8) to any .

Lipschitz regularity of approximation

We conclude this section with a regularity result for . This is an important property of our scheme strongly exploited in Proposition 3.4 and Section 4.

Proposition 3.3.

Let (H1)-(H3) be satisfied. There exists such that

for any and (where is the Lipschitz constant of and only depends on and the constant in Assumption (H2)).

Proof.

The result can be proved by backward induction in . For , is Lipschitz with constant given by (H3). Let be Lipschitz continuous with constant (only depending on and in Assumption (H2)) for any . By classical estimates and thanks to the definition of such that and , one can show by a straightforward calculation that

Hence, by the definition of one has

where only depends on in (H2), which gives Iterating, one obtains which concludes the proof. ∎

3.3. The fully discrete scheme

In order to be able to compute the numerical solution practically in reasonable complexity, we need to introduce some sort of recombination, otherwise the total number of nodes of all trajectories grows exponentially in .

Let and consider the space grid . Let denote the standard multilinear interpolation operator with respect to the space variable which satisfies for every Lipschitz function (with Lipschitz constant ):

| (3.11a) | |||

| (3.11b) | |||

| (3.11c) | |||

We define an approximation on this fixed grid, denoted by , by:

| (3.12) |

for and . We will refer to this as the fully discrete scheme.

From the properties of multilinear interpolation, for all there exist , with and such that Then with (3.12),

with and .

Therefore, are interpretable as transition probabilities of a controlled Markov chain with state space . The number of transitions from node is .

Proposition 3.4.

Let assumptions (H1)-(H3) be satisfied. Then, there exists such that

Proof.

Observe that, in absence of further regularity assumptions, this introduces the following “inverse CFL condition” for the convergence of the fully discrete scheme: as

4. Error estimates

In order to obtain error estimates for the scheme described in Section 3, we will adapt the technique of “shaking coefficients” and regularization introduced by Krylov in [25, 27] and studied later by many authors (see for instance [2, 3, 4]) for obtaining the rate of convergence of monotone numerical scheme for second order HJB equations. We do so without passing through the PDE consistency error and work instead with the direct estimates we presented in the previous section.

We refer to Section 5 for a discussion of the regular case.

4.1. Regularization

Let and let be the set of -valued progressively measurable processes bounded by which are constant in each time interval ], that is,

For any pair , let us consider the process defined by the following -perturbation of the dynamics (3.1):

| (4.1) |

for with . We define the following “perturbed” value function:

| (4.2) |

Proposition 4.1.

Let assumptions (H1)-(H3) be satisfied. Then there exists a constant such that for any and

Proof.

The Lipschitz continuity of follows by the standard estimate

Let us fix a control and . For any , By the definition of processes (3.1) and (4.1) one has for any

Using the fact that and , and the Lipschitz continuity of and (assumption (H2)), a straightforward calculation shows that

with a positive constant independent of and . By iteration we finally get

for any and we can conclude that there exists such that

∎

We point out that for the perturbed value function the following DPP holds:

| (4.3) |

The step that follows consists in a regularization of the function . We consider a smooth function supported in the unit ball with , and we define as the sequence of mollifiers Then define, for any ,

| (4.4) |

Proposition 4.2.

Let assumptions (H1)-(H3) be satisfied. Then,

-

(i)

there exists such that

-

(ii)

the function is for and for any there is such that

(4.5) -

(iii)

satisfies the following super-dynamic programming principle

(4.6)

4.2. Improved lower bound

Applying (3.3), Proposition 4.1 and Proposition 4.2, we obtain

| (4.7) |

for some new . Moreover, by Proposition 4.2 ( and ) and Proposition 3.2 we also have

We can then iterate this inequality to get

| (4.8) |

where we have used that for some

Hence, combining (4.8) and (4.7), we can conclude that for any

Balancing the terms with and , i.e. taking , by one has

| (4.9) |

To conclude, the interpolation error has to be added giving an overall error of

Optimising the choice of with respect to we get This effectively leads to order in time and in space, which can be made arbitrarily close to and , respectively, by choosing large enough.

Remark 2 (Comparison with existing results).

By a Taylor expansion it is possible to compute the consistency error of the scheme with respect to the associated HJB equation. Considering, for simplicity, the uncontrolled one-dimensional () case with , using the fact that , and , one gets

which shows that the scheme has order consistency, for all . Applying the results in [14], this would lead to error estimates of order , i.e., with the optimal choice of order in and in . A similar limitation applies to the analysis in [26].

The improvement we get for the lower bound is due to the fact that, splitting the two contributions of the error coming from Euler-Maruyama time stepping and the Gauß-Hermite quadrature formula, we can reduce the second one by increasing , whereas for the first one the lower regularity requirement allows us to get order .

4.3. Upper bound

The first important observation is that the estimates based on the convexity of the supremum operator (Proposition 4.2()) work only in the direction of the lower bound. Due to the regularity of the numerical solution (see Proposition 3.3), we can apply the approach from [2, 25, 27] to reverse the role of numerical and exact solution and exploit the same arguments by regularization of . However, to estimate the error introduced by the piecewise approximation of the controls we rely on (2.4). This restricts the convergence rate to order 1/4 in and in and hence it will not lead to an improvement with respect to the rates in [14] even for large .

5. The regular case and improvements

5.1. The regular case

If the value function can be shown to be sufficiently smooth, the regularization step is not necessary and it is also possible to consider the rate of weak convergence of the Euler-Maruyama scheme, which is one, and under differentiability assumptions on this gives

Thus, we obtain the following lower estimate

| (5.1) |

which is of order 1 as we would expect in the regular case. For sufficiently smooth functions, the interpolation error reduces to . This, together with (5.1), gives estimates for the lower bound of order . It is also shown in [23] that holds if is sufficiently smooth. For this leads to error estimates of order 1. In many cases, this corresponds to the practically observed situation so that choosing is sufficient to observe convergence, with order 1, of the fully discrete scheme.

5.2. Higher order time stepping

In the smooth case it can also be beneficial to consider higher order approximation schemes for the stochastic differential equation (in the non-smooth case, the necessity of heavier regularization neutralizes the improvements from the higher order schemes). For instance, in the case of coefficients independent of time, one could adapt the weak-second order Taylor scheme (see [24])

to the controlled equation (1.1) and obtain an error contribution of order from the time stepping scheme for the semi-discrete approximation. Retracing the steps of the proof of Proposition 3.2, is still sufficient to guarantee order 2 for the Gauß-Hermite approximation, as the higher order terms resulting from are integrated sufficiently accurately. The overall lower bound of the error for the fully discrete scheme would be , which leads to order in and in . However, no improvement of the upper bound is guaranteed due again to the control approximation, which, as explained in [23], can be improved only if is smooth too, which is usually not the case even if is.

5.3. Higher order interpolation

A remaining bottleneck is the accumulated interpolation error , which is dictated by the need for (multi-)linear interpolation to ensure the monotonicity of the scheme. Some recent results (see [34]) indicate that monotonicity of the interpolation step is not needed to ensure convergence of the scheme, as long as the interpolation is “limited” to avoid overshoots. An interesting example is the monotonicity preserving cubic interpolation (see [19], and [14, Section 6] for an application to semi-Lagrangian schemes) which preserves the monotonicity of the input data in intervals where the data are monotone, and is of high order if the data are monotone overall. In special cases where the monotonicity of the value function is known a priori (such as typical utility maximisation problems in finance), this may lead to a practical improvement of the order, as evidenced in our numerical tests, although a theoretical proof of the higher order seems difficult.

6. Numerical tests

In what follows, as application of our method and to test its numerical properties, we consider a problem from mathematical finance which consists in pricing a European option under a Black-Scholes model with unequal lending and borrowing rates. This model, originally proposed in [9] and analysed analytically in [1] as special case of the framework studied therein, has frequently been used as a test case for numerical methods in the literature (see, e.g., [18, 38] for the solution of HJB PDEs by discretisation and penalisation, respectively, [21, 7, 8] for regression-based BSDE methods, and [17] for a deep learning method for the PDE solution).

The relaxation of the assumption of a single funding rate has recently attracted renewed attention in the financial industry in the context of collateralization (see, e.g., [31]).

The market frictions introduce a nonlinearity of the pricing rule with respect to the payoff and an asymmetry between long and short positions in the option. We focus here on the latter. Appendix A.1 in [18] gives a derivation – by a hedging argument – of the following HJB equation for the value of the option at time given a value of the underlying asset of ,

considered with a terminal condition , where is the payoff function of the option at maturity , and are the borrowing and lending rates, respectively, and the volatility. With the change of variable one can pass to the function as solution of

| (6.1) |

We note that this PDE is semi-linear, with a nonlinearity in the first and zero order terms. In the situation of a fixed, globally constant optimiser , the equation has constant coefficients.

The option price can be interpreted as the value function of a control problem as follows,

with the set of progressively measurable processes with values in and .

As the volatility is constant, independent of the control process, this is an ideal test for our method as it singles out the error from the Markov chain approximation and allows us to assess the improvement achieved by a higher order quadrature rule. The optimal feedback control is piecewise constant as a function of both time and space, with a small number of jump points for practically relevant payoffs.

This fits into the previous framework with the minor extension of a controlled discount factor. For the value function of the problem with piecewise constant control processes we have the following DPP:

| (6.2) |

where . Therefore, adapting to the present case the definitions given in Section 3, in particular (3.12), we can define a fully discrete scheme by

with and .

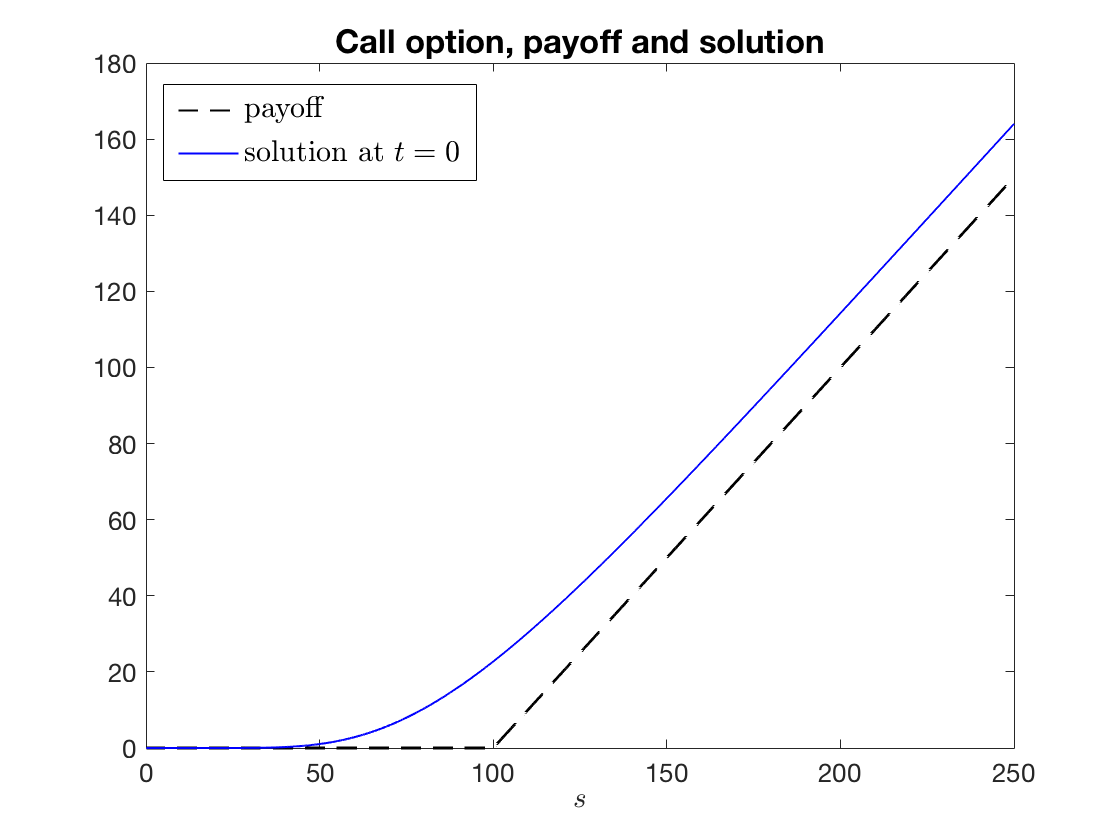

We consider as terminal conditions a a call payoff

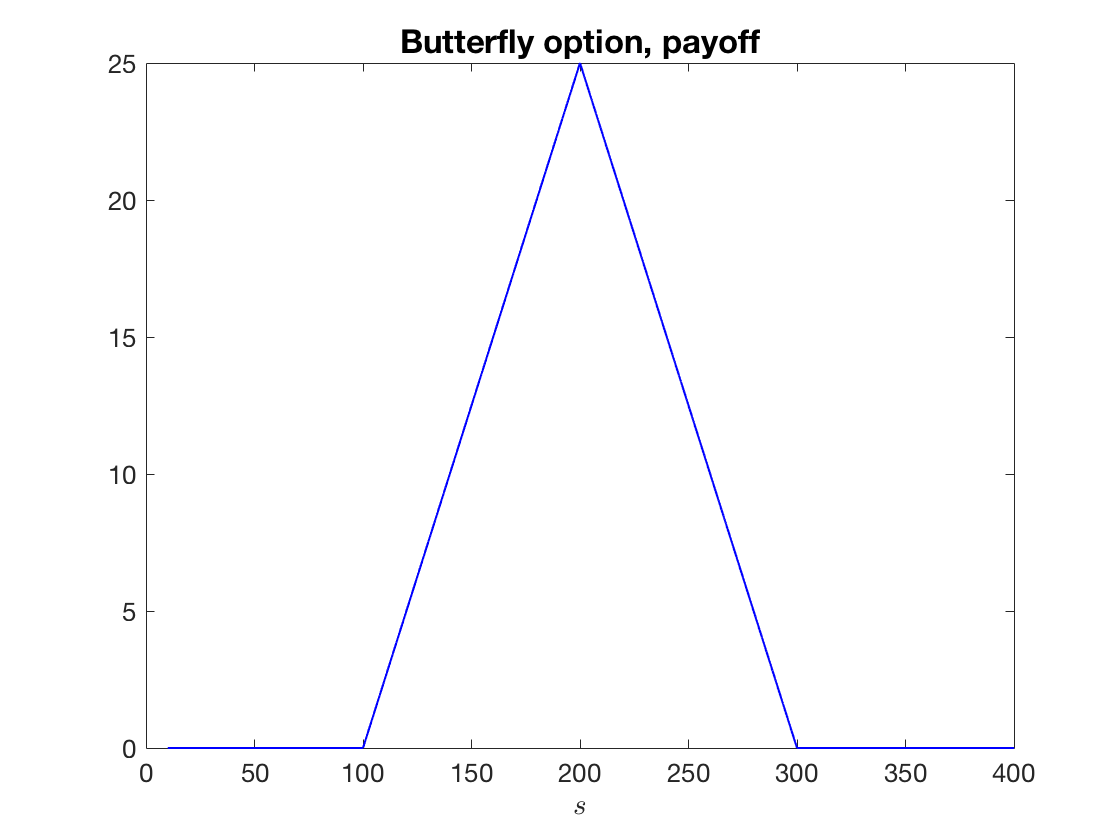

and a so-called butterfly payoff

The parameters used are given in Table 2.

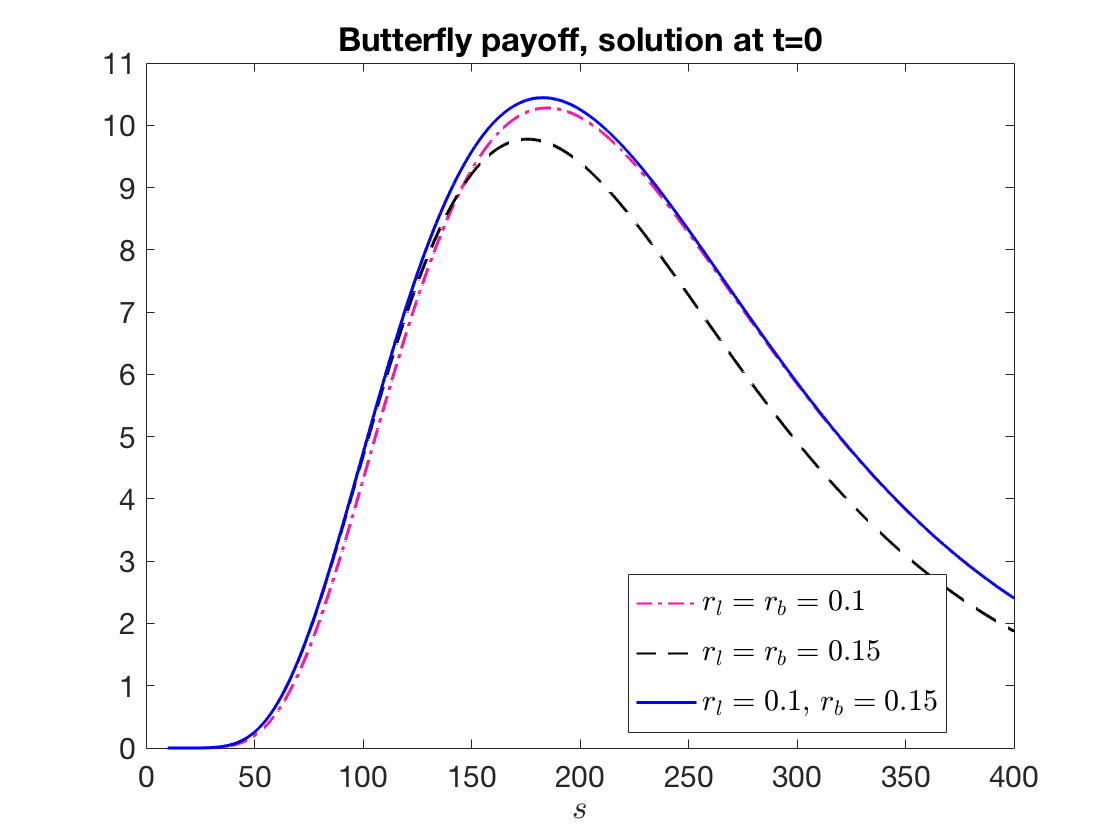

The call payoff and numerical solution for the value function are given in Figure 1, left. The butterfly payoff is shown in Figure 1, right, while the numerical approximation to the value function is shown in Figure 2, left, blue solid curve. In the call case, the optimal control is constant at . For the butterfly, in addition to , as used elsewhere throughout the paper, we also plot the value functions for (dash-dotted magenta curve) and (dashed black curve), which are seen to be strictly smaller. This demonstrates that the constant strategies are sub-optimal.

The focus of our tests is to establish whether a higher order version of the semi-Lagrangian scheme with , in particular the case , leads to better accuracy and higher convergence rate than the standard case . To this end, we compute numerical approximations with an increasing number of timesteps, .

We note that the Euler scheme for fixed control is exact in this setting, and the time discretisation error therefore of order for , provided smooth enough solutions. In order to balance this term and the interpolation error of order , we choose (an ‘inverse CFL condition’) or . In the case of , this makes the spatial error negligible compared to the time stepping error of order .

In Table 3, we list the error evaluated in the maximum norm over a suitable spatial interval and the resulting estimated convergence order, for the call payoff (observe that in this case the problem becomes linear with and an exact solution is available). In this case, as the optimal control is constant, this allows us to verify the achievable order in the simplest case of a linear problem with constant coefficients. Indeed, the order is approximately 1 for and 3 for .

| error | order | CPU (s) | error | order | CPU (s) | |

|---|---|---|---|---|---|---|

| 1 | 2.25E-01 | - | 0.02 | 5.99E-01 | - | 0.04 |

| 2 | 5.97E-02 | 1.91 | 0.03 | 6.94E-02 | 3.11 | 0.08 |

| 3 | 2.64E-02 | 1.18 | 0.13 | 9.80E-03 | 2.82 | 0.47 |

| 4 | 1.20E-02 | 1.13 | 0.92 | 2.63E-03 | 1.90 | 1.54 |

| 5 | 6.06E-03 | 0.99 | 3.85 | 3.48E-04 | 2.92 | 8.10 |

| 6 | 3.28E-03 | 0.88 | 26.00 | 3.00E-05 | 3.54 | 59.58 |

| 7 | 1.75E-03 | 0.91 | 276.01 | 2.91E-06 | 3.36 | 613.85 |

| 8 | 9.02E-04 | 0.95 | 2382.37 | 4.40E-07 | 2.73 | 4834.02 |

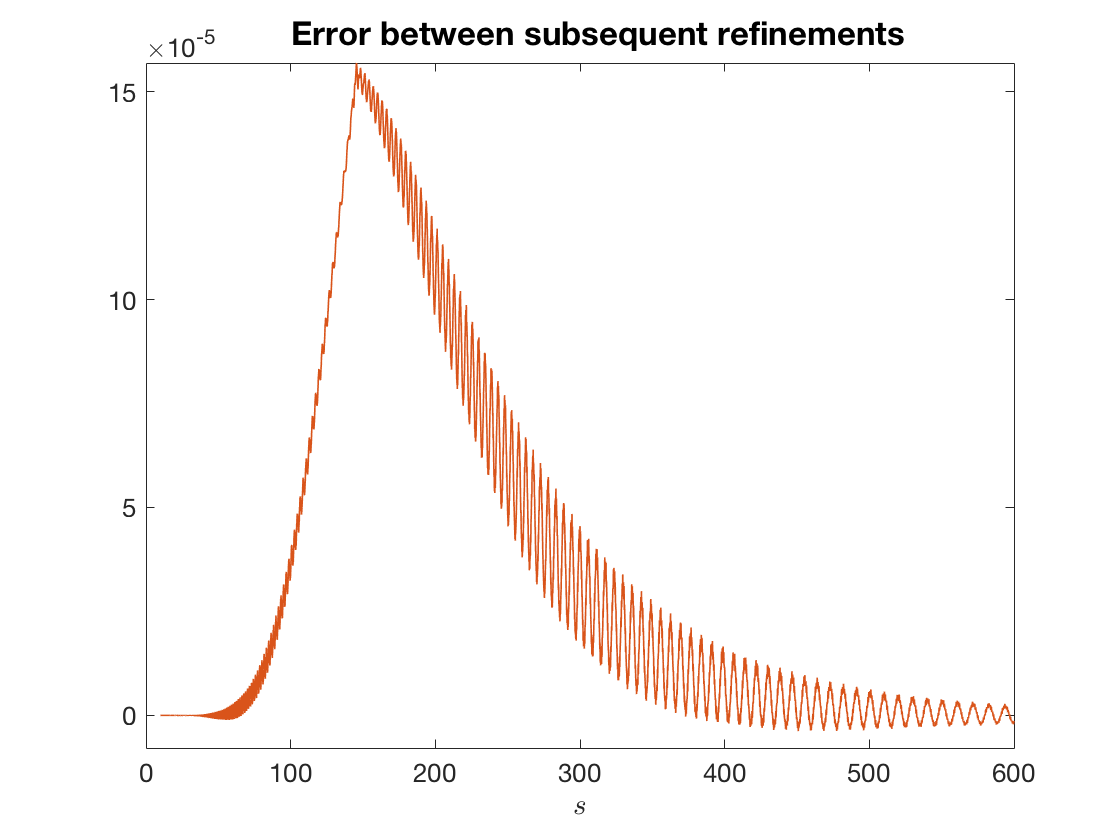

The corresponding results for the butterfly payoff are given in Table 4 (in this case, we do not have an exact solution and the error is considered as the difference between numerical solutions for subsequent mesh refinements). A typical shape of the error as a function of (at ) is shown in Figure 2, right. Here, the optimal control is piecewise constant in space, switching from to at a time-dependent value of , between 150 and 200 in this case. This results in a ‘kink’ in the controlled term in (6.1), and therefore the best regularity we can expect is that is Lipschitz at this point, and smooth everywhere else. We therefore show separately the maximum error in two different intervals, namely , sufficiently far from the non-smooth point, and , containing the non-smooth point.

| CPU(s) | CPU(s) | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| error | order | error | order | error | order | error | order | |||

| 1 | 1.39E 00 | - | 1.81E 00 | - | 0.01 | 1.11E 00 | - | 1.36E 00 | - | 0.01 |

| 2 | 7.65E-02 | 4.18 | 1.81E-01 | 3.33 | 0.01 | 1.69E-01 | 2.72 | 3.74E-01 | 1.86 | 0.02 |

| 3 | 1.65E-02 | 2.21 | 5.13E-02 | 1.82 | 0.02 | 2.40E-02 | 2.81 | 6.39E-02 | 2.55 | 0.05 |

| 4 | 1.02E-02 | 0.70 | 3.75E-02 | 0.45 | 0.10 | 3.63E-03 | 2.73 | 1.53E-02 | 2.06 | 0.28 |

| 5 | 4.65E-03 | 1.13 | 1.44E-02 | 1.38 | 0.80 | 1.35E-03 | 1.42 | 5.39E-03 | 1.51 | 1.10 |

| 6 | 3.04E-03 | 0.61 | 1.13E-02 | 0.35 | 3.98 | 4.03E-04 | 1.75 | 1.44E-03 | 1.91 | 7.12 |

| 7 | 1.89E-03 | 0.68 | 4.99E-03 | 1.18 | 28.54 | 5.48E-05 | 2.88 | 3.51E-04 | 2.03 | 54.76 |

| 8 | 8.46E-04 | 1.16 | 2.32E-03 | 1.10 | 302.29 | 5.77E-06 | 3.25 | 1.57E-04 | 1.16 | 530.14 |

The order of the scheme with is still 1 in both cases. For , the order in the first interval is still around 3, whereas it is reduced to around 2 close to the non-smooth point.

Finally, in Table 5, we report results where we replace the piecewise linear spatial interpolation with the piecewise cubic, and piecewise monotone interpolation defined in [19], as discussed in Section 5.3. Conjecturing an interpolation error of order per timestep, the most efficient refinement is achieved by balancing the time accumulated error with (for ) and we hence choose , or .

| CPU(s) | CPU(s) | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| error | order | error | order | error | order | error | order | |||

| 1 | 1.05E-01 | - | 5.16E-01 | - | 0.01 | 4.39E-02 | - | 2.06E-01 | - | 0.03 |

| 2 | 5.78E-02 | 0.86 | 2.00E-01 | 1.37 | 0.02 | 2.33E-02 | 0.91 | 1.18E-01 | 0.80 | 0.06 |

| 3 | 1.58E-02 | 1.87 | 7.91E-02 | 1.34 | 0.04 | 1.03E-02 | 1.18 | 4.23E-02 | 1.48 | 0.18 |

| 4 | 1.14E-02 | 0.47 | 3.64E-02 | 1.12 | 0.09 | 4.22E-03 | 1.29 | 1.62E-02 | 1.39 | 0.73 |

| 5 | 5.28E-03 | 1.11 | 1.54E-02 | 1.24 | 0.38 | 1.45E-03 | 1.54 | 5.44E-03 | 1.57 | 2.79 |

| 6 | 3.07E-03 | 0.78 | 1.18E-02 | 0.38 | 6.66 | 4.13E-04 | 1.81 | 1.36E-03 | 2.00 | 13.22 |

| 7 | 1.86E-03 | 0.72 | 5.01E-03 | 1.24 | 27.54 | 5.51E-05 | 2.91 | 3.47E-04 | 1.98 | 53.53 |

| 8 | 8.34E-04 | 1.16 | 2.30E-03 | 1.12 | 111.57 | 6.17E-06 | 3.16 | 1.56E-04 | 1.15 | 218.77 |

The results are very similar to those in Table 4, but obtained for a significantly smaller number of spatial nodes. Due to the higher computational cost of the interpolation, though, this only results in savings for the highest refinement levels reported here.

7. Conclusions and perspectives

This paper analyses numerical schemes for HJB equations based on a discrete time approximation of the optimal control problem. Using purely probabilistic arguments and under very general assumptions, in Section 4 we give a bound for the solution generated by such an approximation. The error bound obtained in this way allows us to improve one side of previous results from the literature. In ongoing work [33], we are investigating the use of duality to obtain symmetric bounds.

The theoretically obtained convergence orders, although sharper than previously known results, are still not sharp in applications, where the solution is often at least piecewise more regular than is assumed for the analysis.

The new technique of splitting the total error into contributions from different approximation stages, however, allows us to understand why our higher order version outperforms the standard semi-Lagrangian scheme in numerical tests, despite the fact that the consistency order used in the traditional analysis is identically 1 for all schemes.

Acknowledgements: The first author acknowledges Olivier Bokanowski for a preliminary discussion on the subject.

Appendix A Bounds for the Euler-Maruyama approximation

We consider the Euler-Maruyama approximation given by (3.1) for . This leads to the following expression for for :

Moreover, by the very definition of :

Hereafter, we do not keep track of individual constants and denote by any nonnegative constant depending only on and in assumption (H2) (an explicit computation of the constants involved can be found in [33, Appendix A.1]). Using the Cauchy-Schwartz inequality and Itô isometry, and (H2), one can easily show that

We now estimate the last term on the right-hand side. For any , by the Cauchy-Schwartz and Doob maximal inequalities, one has

for some constant independent of . Then, thanks to the linear growth of the coefficients and due to assumption (H2), one obtains

Recalling that by classical estimates on the process (see for instance [37, Theorem 3.1]) one has

we can put these estimates together to obtain

Then, using the discrete version of Gronwall’s inequality, one can conclude that for any ,

for some constant independent of and . The result of Proposition 3.1 then follows from Hölder’s inequality.

References

- [1] A.L. Amadori. Nonlinear integro-differential evolution problems arising in option pricing: a viscosity solutions approach. Differ. Integral Equ., 16(7):787–811, 2003.

- [2] G. Barles and E.R. Jakobsen. On the convergence rate of approximation schemes for Hamilton-Jacobi-Bellman equations. M2AN Math. Model. Numer. Anal., 36:33–54, 2002.

- [3] G. Barles and E.R. Jakobsen. Error bounds for monotone approximation schemes for Hamilton-Jacobi-Bellman equations. SIAM J. Numer. Anal., 43(2):540–558, 2005.

- [4] G. Barles and E.R. Jakobsen. Error bounds for monotone approximation schemes for parabolic Hamilton-Jacobi-Bellman equations. Math. Comput., 74(260):1861–1893, 2007.

- [5] G. Barles and P.E. Souganidis. Convergence of approximation schemes for fully nonlinear second order equations. Asymptotic Anal., 4:271–283, 1991.

- [6] C. Bayer and J. Teichmann. The proof of Tchakaloff’s theorem. Proc. Am. Math. Soc., 134(10):3035–3040, 2006.

- [7] C. Bender and R. Denk. A forward scheme for backward SDEs. Stoch. Proc. Appl., 117(12):1793–1812, 2007.

- [8] C. Bender, N. Schweizer, and J. Zhuo. A primal–dual algorithm for BSDEs. Math. Financ., 27(3):866–901, 2017.

- [9] Y.Z. Bergman. Option pricing with differential interest rates. Rev. Financ. Stud., 8(2):475–500, 1995.

- [10] W.H. Beyer. CRC Standard Mathematical Tables. CRC Press, 28th edition, 1987.

- [11] F. Camilli and M. Falcone. An approximation scheme for the optimal control of diffusion processes. RAIRO Modél. Math. Anal. Numér., 29(1):97–122, 1995.

- [12] M.G. Crandall, H. Ishii, and P.L. Lions. User’s guide to viscosity solutions of second order partial differential equations. Bull. Amer. Math. Soc., 27(1):1–67, 1992.

- [13] P.J. Davis and P. Rabinowitz. Methods of numerical integration. Dover Publications, second edition, 2007.

- [14] K. Debrabant and E.R. Jakobsen. Semi-Lagrangian schemes for linear and fully non-linear diffusion equations. Math. Comp., 82(283):1433–1462, 2012.

- [15] K. Debrabant and E.R. Jakobsen. Semi-Lagrangian schemes for parabolic equations. In T. Gerstner and P. Kloeden, editors, Recent Developments in Computational Finance: Foundations, Algorithms and Applications, pages 279–297. World Scientific, 2013.

- [16] E.A. DeVuyst and P.V. Preckel. Gaussian cubature: A practitioner’s guide. Math. Comput. Model., 45(7-8):787–794, 2007.

- [17] W. E, J. Han, and A. Jentzen. Deep learning-based numerical methods for high-dimensional parabolic partial differential equations and backward stochastic differential equations. Commun. Math. Stat., 5(4):349–380, 2017.

- [18] P.A. Forsyth and G. Labahn. Numerical methods for controlled Hamilton–Jacobi–Bellman PDEs in finance. J. Comput. Financ., 11(2):1–44, 2007.

- [19] F.N. Fritsch and R.E. Carlson. Monotone piecewise cubic interpolation. SIAM J. Numer. Anal., 17(2):238–246, 1980.

- [20] T. Gerstner and M. Griebel. Numerical integration using sparse grids. Numer. Algorithms, 18:209–232, 1998.

- [21] E. Gobet, J.-P. Lemor, and X. Warin. A regression-based monte carlo method to solve backward stochastic differential equations. Ann. Appl. Probab., 15(3):2172–2202, 2005.

- [22] F.B. Hildebrand. Introduction to Numerical Analysis. New York: McGraw-Hill, 1956.

- [23] E.R. Jakobsen, A. Picarelli, and C. Reisinger. Improved order 1/4 convergence of Krylov’s piecewise constant policy approximation. Electron. Comm. Probab., 24(59):1–10, 2019.

- [24] P.E. Kloeden and E. Platen. Numerical Solution of Stochastic Differential Equations. Berlin, New York, Springer-Verlag, 1992.

- [25] N.V. Krylov. On the rate of convergence of finite-difference approximations for Bellman’s equations. St. Petersburg Math. J., 9:639–650, 1997.

- [26] N.V. Krylov. Approximating value functions for controlled degenerate diffusion processes by using piece-wise constant policies. Electron. J. Probab., 4(2):1–19, 1999.

- [27] N.V. Krylov. On the rate of convergence of finite-difference approximations for Bellman’s equations with variable coefficients. Probab. Theory Relat. Fields, 117:1–16, 2000.

- [28] H.J. Kushner and P. Dupuis. Numerical Methods for Stochastic Control Problems in Continuous Time. Springer Verlag, New York, second edition, 2001.

- [29] T. Lyons and N. Victoir. Cubature on Wiener space. P. Roy. Soc A-Math. Phy., 460(2041):169–198, 2004.

- [30] J.L. Menaldi. Some estimates for finite difference approximations. SIAM J. Control Optim., 27:579–607, 1989.

- [31] F. Mercurio. Bergman, Piterbarg, and beyond: pricing derivatives under collateralization and differential rates. In J.A. Londoño, J. Garrido, and D. Hernández-Hernández, editors, Actuarial Sciences and Quantitative Finance, Springer P. Math. Stat., ICASQF, June 2014, pages 65–95. Springer, 2015.

- [32] G.N. Milstein. Numerical Integration of Stochastic Differential Equations. Kluwer Academic Publishers, MA, 1995.

- [33] A. Picarelli and C. Reisinger. Duality-based a posteriori error estimates for some approximation schemes for optimal investment problems. Computers & Mathematics with Applications, 2019. doi: 10.1016/j.camwa.2019.12.010.

- [34] C. Reisinger and P.A. Forsyth. Piecewise constant policy approximations to Hamilton–Jacobi–Bellman equations. Appl. Numer. Math., 103:27–47, 2016.

- [35] V. Tchakaloff. Formules de cubatures mécaniques à coefficients non négatifs. Bull. Sci. Math., 81(2):123–134, 1957.

- [36] M. Tchernychova. Carathéodory cubature measures. PhD thesis, University of Oxford, 2015.

- [37] N. Touzi. Optimal Stochastic Control, Stochastic Target Problems, and Backward SDE, volume 29 of Fields Institute for Research in Mathematical Sciences,. Springer, New York, 2013.

- [38] J.H. Witte and C. Reisinger. A penalty method for the numerical solution of Hamilton–Jacobi–Bellman (hjb) equations in finance. SIAM J. Numer. Anal., 49(1):213–231, 2011.

- [39] J. Yong and X.Y. Zhou. Stochastic Controls: Hamiltonian Systems and HJB Equations, volume 43 of Applications of Mathematics. Springer-Verlag, New York, 1999.