Sample Complexity of Sinkhorn Divergences

Aude Genevay Lénaic Chizat Francis Bach Marco Cuturi Gabriel Peyré

DMA, ENS Paris INRIA INRIA and DI, ENS Paris Google and CREST ENSAE CNRS and DMA, ENS Paris

Abstract

Optimal transport (OT) and maximum mean discrepancies (MMD) are now routinely used in machine learning to compare probability measures. We focus in this paper on Sinkhorn divergences (SDs), a regularized variant of OT distances which can interpolate, depending on the regularization strength , between OT () and MMD (). Although the tradeoff induced by that regularization is now well understood computationally (OT, SDs and MMD require respectively , and operations given a sample size ), much less is known in terms of their sample complexity, namely the gap between these quantities, when evaluated using finite samples vs. their respective densities. Indeed, while the sample complexity of OT and MMD stand at two extremes, for OT in dimension and for MMD, that for SDs has only been studied empirically. In this paper, we (i) derive a bound on the approximation error made with SDs when approximating OT as a function of the regularizer , (ii) prove that the optimizers of regularized OT are bounded in a Sobolev (RKHS) ball independent of the two measures and (iii) provide the first sample complexity bound for SDs, obtained,by reformulating SDs as a maximization problem in a RKHS. We thus obtain a scaling in (as in MMD), with a constant that depends however on , making the bridge between OT and MMD complete.

1 Introduction

Optimal Transport (OT) has emerged in recent years as a powerful tool to compare probability distributions. Indeed, Wasserstein distances can endow the space of probability measures with a rich Riemannian structure (Ambrosio et al., 2006), one that is able to capture meaningful geometric features between measures even when their supports do not overlap. OT has been, however, long neglected in data sciences for two main reasons, which could be loosely described as computational and statistical: computing OT is costly since it requires solving a network flow problem; and suffers from the curse-of-dimensionality, since, as will be made more explicit later in this paper, the Wasserstein distance computed between two samples converges only very slowly to its population counterpart.

Recent years have witnessed significant advances on the computational aspects of OT. A recent wave of works have exploited entropic regularization, both to compare discrete measures with finite support (Cuturi, 2013) or measures that can be sampled from (Genevay et al., 2016). Among the many learning tasks performed with this regularization, one may cite domain adaptation (Courty et al., 2014), text retrieval (Kusner et al., 2015) or multi-label classification (Frogner et al., 2015). The ability of OT to compare probability distributions with disjoint supports (as opposed to the Kullback-Leibler divergence) has also made it popular as a loss function to learn generative models (Arjovsky et al., 2017; Salimans et al., 2018; Beaumont et al., 2002).

At the other end of the spectrum, the maximum mean discrepancy (MMD) (Gretton et al., 2006) is an integral probability metric (Sriperumbudur et al., 2012) on a reproducing kernel Hilbert space (RKHS) of test functions. The MMD is easy to compute, and has also been used in a very wide variety of applications, including for instance the estimation of generative models (Li et al., 2015; MMD-GAN; Li et al., 2017).

OT and MMD differ, however, on a fundamental aspect: their sample complexity. The definition of sample complexity that we choose here is the convergence rate of a given metric between a measure and its empirical counterpart, as a function of the number of samples. This notion is crucial in machine learning, as bad sample complexity implies overfitting and high gradient variance when using these divergences for parameter estimation. In that context, it is well known that the sample complexity of MMD is independent of the dimension, scaling as (Gretton et al., 2006) where is the number of samples. In contrast, it is well known that standard OT suffers from the curse of dimensionality (Dudley, 1969): Its sample complexity is exponential in the dimension of the ambient space. Although it was recently proved that this result can be refined to consider the implicit dimension of data (Weed and Bach, 2017), the sample complexity of OT appears now to be the major bottleneck for the use of OT in high-dimensional machine learning problems.

A remedy to this problem may lie, again, in regularization. Divergences defined through regularized OT, known as Sinkhorn divergences, seem to be indeed less prone to over-fitting. Indeed, a certain amount of regularization seems to improve performance in simple learning tasks (Cuturi, 2013). Additionally, recent papers (Ramdas et al., 2017; Genevay et al., 2018) have pointed out the fact that Sinkhorn divergences are in fact interpolating between OT (when regularization goes to zero) and MMD (when regularization goes to infinity). However, aside from a recent central limit theorem in the case of measures supported on discrete spaces (Bigot et al., 2017), the convergence of empirical Sinkhorn divergences, and more generally their sample complexity, remains an open question.

Contributions.

This paper provides three main contributions, which all exhibit theoretical properties of Sinkhorn divergences. Our first result is a bound on the speed of convergence of regularized OT to standard OT as a function of the regularization parameter, in the case of continuous measures. The second theorem proves that the optimizers of the regularized optimal transport problem lie in a Sobolev ball which is independent of the measures. This allows us to rewrite the Sinkhorn divergence as an expectation maximization problem in a RKHS ball and thus justify the use of kernel-SGD for regularized OT as advocated in (Genevay et al., 2016). As a consequence of this reformulation, we provide as our third contribution a sample complexity result. We focus on how the sample size and the regularization parameter affect the convergence of the empirical Sinkhorn divergence (i.e., computed from samples of two continuous measures) to the continuous Sinkhorn divergence. We show that the Sinkhorn divergence benefits from the same sample complexity as MMD, scaling in but with a constant that depends on the inverse of the regularization parameter. Thus sample complexity worsens when getting closer to standard OT, and there is therefore a tradeoff between a good approximation of OT (small regularization parameter) and fast convergence in terms of sample size (larger regularization parameter). We conclude this paper with a few numerical experiments to asses the dependence of the sample complexity on and in very simple cases.

Notations.

We consider and two bounded subsets of and we denote by and their respective diameter . The space of positive Radon measures of mass 1 on is denoted and we use upper cases to denote random variables in these spaces. We use the notation to say that is bounded by a polynomial of order in with positive coefficients.

2 Reminders on Sinkhorn Divergences

We consider two probability measures and on . The Kantorovich formulation (1942) of optimal transport between and is defined by

| () |

where the feasible set is composed of probability distributions over the product space with fixed marginals :

where (resp. ) is the marginal distribution of for the first (resp. second) variable, using the projection maps along with the push-forward operator ♯.

The cost function represents the cost to move a unit of mass from to . Through this paper, we will assume this function to be (more specifically, we need it to be ). When is endowed with a distance , choosing where yields the -Wasserstein distance between probability measures.

We introduce regularized optimal transport, which consists in adding an entropic regularization to the optimal transport problem, as proposed in (Cuturi, 2013). Here we use the relative entropy of the transport plan with respect to the product measure following (Genevay et al., 2016):

| () |

where

| (1) |

Choosing the relative entropy as a regularizer allows to express the dual formulation of regularized OT as the maximization of an expectation problem, as shown in (Genevay et al., 2016)

where This reformulation as the maximum of an expectation will prove crucial to obtain sample complexity results. The existence of optimal dual potentials is proved in the appendix. They are unique and a.e. up to an additive constant.

To correct for the fact that , (Genevay et al., 2018) propose Sinkhorn divergences, a natural normalization of that quantity defined as

| (2) |

This normalization ensures that , but also has a noticeable asymptotic behavior as mentioned in (Genevay et al., 2018). Indeed, when one recovers the original (unregularized) OT problem, while choosing yields the maximum mean discrepancy associated to the kernel , where MMD is defined by:

In the context of this paper, we study in detail the sample complexity of , knowing that these results can be extended to .

3 Approximating Optimal Transport with Sinkhorn Divergences

In the present section, we are interested in bounding the error made when approximating with .

Theorem 1.

Let and be probability measures on and subsets of such that and assume that is -Lipschitz w.r.t. and . It holds

| (3) | |||||

| (4) |

Proof.

For a probability measure on , we denote by the associated transport cost and by its relative entropy with respect to the product measure as defined in (1). Choosing a minimizer of , we will build our upper bounds using a family of transport plans with finite entropy that approximate . The simplest approach consists in considering block approximation. In contrast to the work of Carlier et al. (2017), who also considered this technique, our focus here is on quantitative bounds.

Definition 1 (Block approximation).

For a resolution , we consider the block partition of in hypercubes of side defined as

To simplify notations, we introduce , , . The block approximation of of resolution is the measure characterized by

for all , with the convention .

is nonnegative by construction. Observe also that for any Borel set , one has

which proves, using the symmetric result in , that belongs to . As a consequence, for any one has . Recalling also that the relative entropy is nonnegative over the set of probability measures, we have the bound

We can now bound the terms in the right-hand side, and choose a value for that minimizes these bounds.

The bound on relies on the Lipschitz regularity of the cost function. Using the fact that for all , it holds

where is the Lipschitz constant of the cost (separately in and ) and is the diameter of each set .

As for the bound on , using the fact that we get

where we have defined and similarly for . Note that in case is a discrete measure with finite support, is equal to (minus) the discrete entropy of as long as is smaller than the minimum separation between atoms of . However, if is not discrete then blows up to as goes to and we need to control how fast it does so. Considering the block approximation of with constant density on each block and (minus) its differential entropy , it holds . Moreover, using the convexity of , this can be compared with the differential entropy of the uniform probability on a hypercube containing of size . Thus it holds and thus .

Summing up, we have for all

The above bound is convex in , minimized with . This yields

4 Properties of Sinkhorn Potentials

We prove in this section that Sinkhorn potentials are bounded in the Sobolev space regardless of the marginals and . For , is a reproducing kernel Hilbert space (RKHS): This property will be crucial to establish sample complexity results later on, using standard tools from RKHS theory.

Definition 2.

The Sobolev space , for , is the space of functions such that for every multi-index with the mixed partial derivative exists and belongs to . It is endowed with the following inner-product

| (5) |

Theorem 2.

When and are two compact sets of and the cost is , then the Sinkhorn potentials are uniformly bounded in the Sobolev space and their norms satisfy

with constants that only depend on (or for ),, and for . In particular, we get the following asymptotic behavior in : as and as .

To prove this theorem, we first need to state some regularity properties of the Sinkhorn potentials.

Proposition 1.

If and are two compact sets of and the cost is , then

-

•

for all

-

•

is L-Lipschitz, where L is the Lipschitz constant of

-

•

and

and the same results also stand for (inverting and in the first item, and replacing by ).

Proof.

The proofs of all three claims exploit the optimality condition of the dual problem:

| (6) |

Since is a probability measure, is a convex combination of and thus We get the desired bounds by taking the logarithm. The two other points use the following lemmas:

Lemma 1.

The derivatives of the potentials are given by the following recurrence

| (7) |

where

and .

Lemma 2.

The sequence of auxiliary functions verifies . Besides, for all , for all , is bounded by a polynomial in of order .

The detailed proofs of the lemmas can be found in the appendix. We give here a sketch in the case where . Lemma 1 is obtained by a simple recurrence, consisting in differentiating both sides of the dual optimality condition. Differentiating under the integral is justified with the usual domination theorem, bounding the integrand thanks to the Lipschitz assumption on , and this bound is integrable thanks to the marginal constraint. Differentiating once and rearranging terms gives:

| (8) |

where is defined in Lemma 1. One can easily see that and this allows to conclude the recurrence, by differentiating both sides of the equality. From the primal constaint, we have that . Thus thanks to Lemma 1 we immediately get that . For , since we get that and this proves the second point of Proposition 1. For higher values of , we need the result from Lemma 2. This property is also proved by recurrence, but requires a bit more work. To prove the induction step, we need to go from bounds on , for and to bounds on , for and . Hence only new quantities that we need to bound are . This is done by another (backwards) recurrence on which involves some tedious computations, based on Leibniz formula, that are detailed in the appendix. ∎

Combining the bounds of the derivatives of the potentials with the definition of the norm in , is enough to complete the proof of Theorem 2.

Proof.

(Theorem 2) The norm of in is

From Proposition 1 we have that and thus we get that . We just proved the bound in but we actually want to have a bound on . This is immediate thanks to the Sobolev extension theorem (Calderón, 1961) which guarantees that under the assumption that is a bounded Lipschitz domain. ∎

This result, aside from proving useful in the next section to obtain sample complexity results on the Sinkhorn divergence, also proves that kernel-SGD can be used to solve continuous regularized OT. This idea introduced in Genevay et al. (2016) consists in assuming the potentials are in the ball of a certain RKHS, to write them as a linear combination of kernel functions and then perform stochastic gradient descent on these coefficients. Knowing the radius of the ball and the kernel associated with the RKHS (here the Sobolev or Matérn kernel) is crucial to obtain good numerical performance and ensure the convergence of the algorithm.

5 Approximation from Samples

In practice, measures and are only known through a finite number of samples. Thus, what can be actually computed in practice is the Sinkhorn divergence between the empirical measures and , where and are n-samples from and , that is

where are i.i.d random variables distributed according to . On actual samples, these quantities can be computed using Sinkhorn’s algorithm (Cuturi, 2013).

Our goal is to quantify the error that is made by approximating by their empirical counterparts , that is bounding the following quantity:

| (9) |

where are the optimal Sinkhorn potentials associated with and are their empirical counterparts.

Theorem 3.

Consider the Sinkhorn divergence between two measures and on and two bounded subsets of , with a , -Lipschitz cost . One has

where and constants only depend on ,,, and for . In particular, we get the following asymptotic behavior in :

An interesting feature from this theorem is the fact when is large enough, the convergence rate does not depend on anymore. This means that at some point, increasing will not substantially improve convergence. However, for small values of the dependence is critical.

We prove this result in the rest of this section. The main idea is to exploit standard results from PAC-learning in RKHS. Our theorem is an application of the following result from Bartlett and Mendelson (2002) ( combining Theorem 12,4) and Lemma 22 in their paper):

Proposition 2.

(Bartlett-Mendelson ’02) Consider a probability distribution, a B-lipschitz loss and a given class of functions. Then

where is the Rademacher complexity of class defined by where are iid Rademacher random variables. Besides, when is a ball of radius in a RKHS with kernel the Rademacher complexity is bounded by

Our problem falls in this framework thanks to the following lemma:

Lemma 3.

Let , then there exists such that:

Proof.

Inserting and using the triangle inequality in (9) gives

From Theorem 2, we know that the all the dual potentials are bounded in by a constant which doesn’t depend on the measures. Thus the second term is bounded by .

The first quantity needs to be broken down further. Notice that it is non-negative since is the maximizer of so we can leave out the absolute value. We have:

| (10) | ||||

| (11) | ||||

| (12) |

Both (10) and (12) can be bounded by while (11) is non-positive since is the maximizer of . ∎

To apply Proposition 2 to Sinkhorn divergences we need to prove that (a) the optimal potentials are in a RKHS and (b) our loss function is Lipschitz in the potentials.

The first point has already been proved in the previous section. The RKHS we are considering is with . It remains to prove that is Lipschitz in on a certain subspace that contains the optimal potentials.

Lemma 4.

Let . We have:

-

(i)

the pairs of optimal potentials such that belong to ,

-

(ii)

is B-Lipschitz in on with .

Proof.

Let us prove that we can restrict ourselves to a subspace on which is Lipschitz in .

To ensure that is Lipschitz, we simply need to ensure that the quantity inside the exponential is upperbounded at optimality and then restrict the function to all that satisfy that bound.

Recall the bounds on the optimal potentials from Proposition 1. We have that ,

Since we assumed to be a bounded set, denoting by the diameter of the space we get that at optimality

Let us denote , we have that ,

We now have all the required elements to prove our sample complexity result on the Sinkhorn loss, by applying Proposition 2.

Proof.

(Theorem 3) Since is Lipschitz and we are optimizing over which is a RKHS, we can apply Proposition 2 to bound the in Lemma 3. We get:

where (Lemma 4), (Theorem 2). We can further bound by where is the kernel associated to (usually called Matern or Sobolev kernel) and thus which doesn’t depend on or . Combining all these bounds, we get the convergence rate in with different asymptotic behaviors in when it is large or small. ∎

Using similar arguments, we can also derive a concentration result:

Corollary 1.

With probability at least ,

where are defined in the proof above, and with .

Proof.

We apply the bounded differences (Mc Diarmid) inequality to . From Lemma 4 we get that , , and thus, changing one of the variables in changes the value of the function by at most . Thus the bounded differences inequality gives

Choosing yields that with probability at least

and from Theorem 3 we already have

∎

6 Experiments

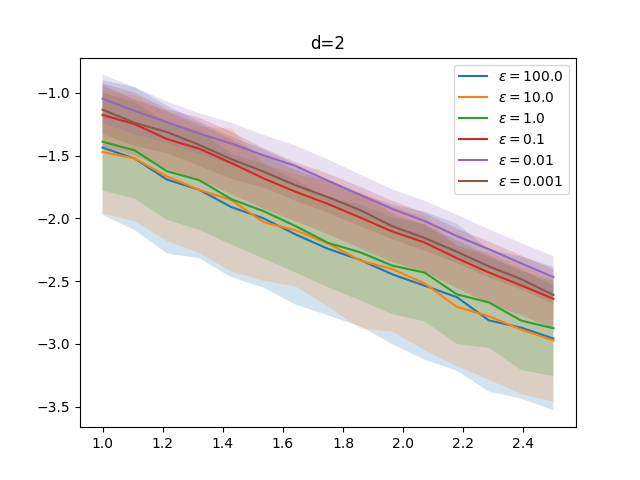

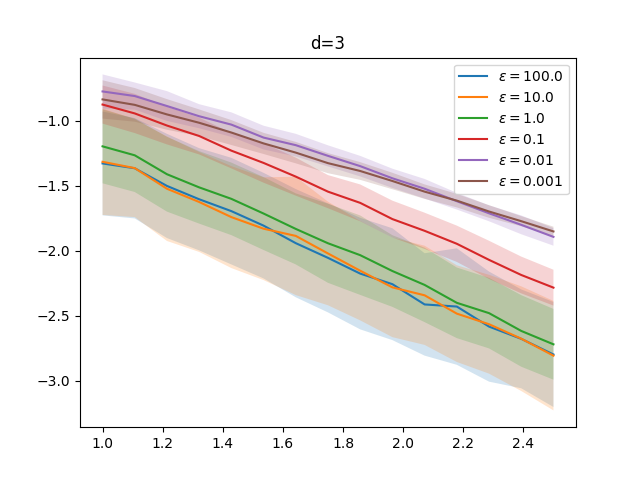

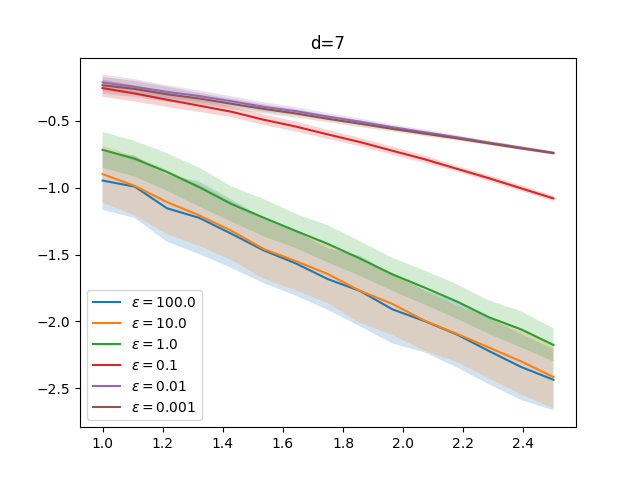

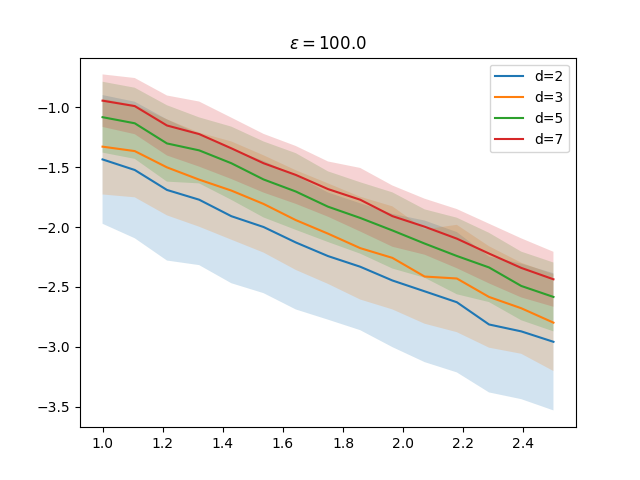

We conclude with some numerical experiments on the sample complexity of Sinkhorn Divergences. Since there are no explicit formulas for in general, we consider where , and and are two independent -samples from . Note that we use in this section the normalized Sinkhorn Divergence as defined in (2), since we know that and thus as .

Each of the experiments is run times, and we plot the average of as a function of in log-log space, with shaded standard deviation bars.

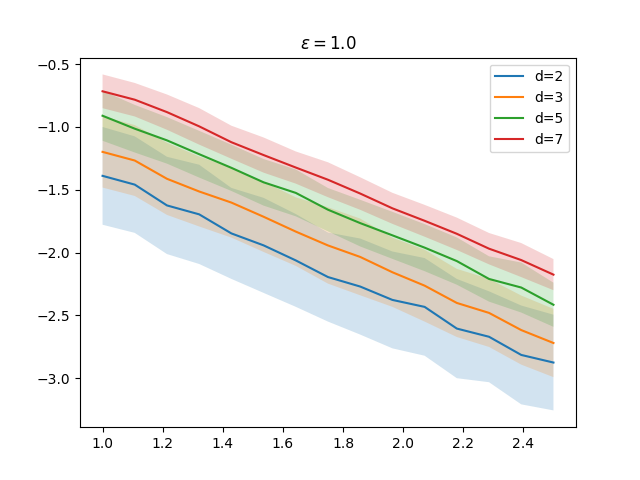

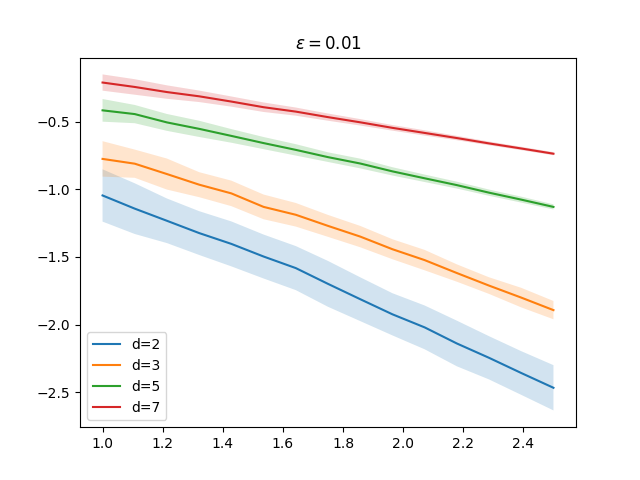

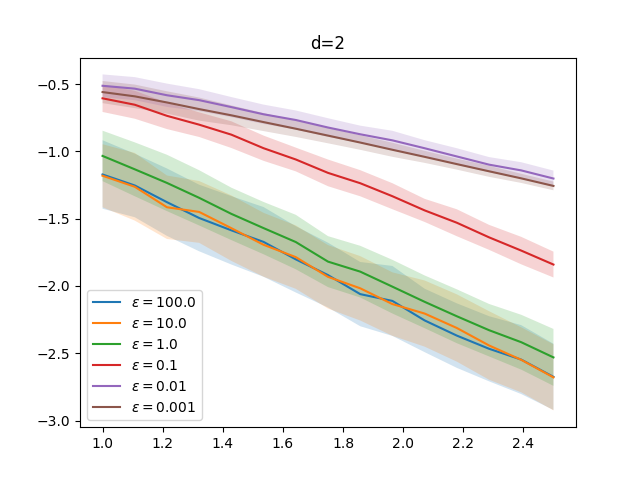

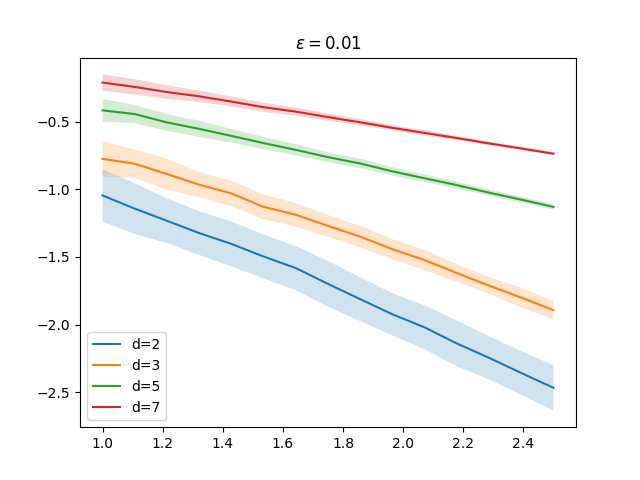

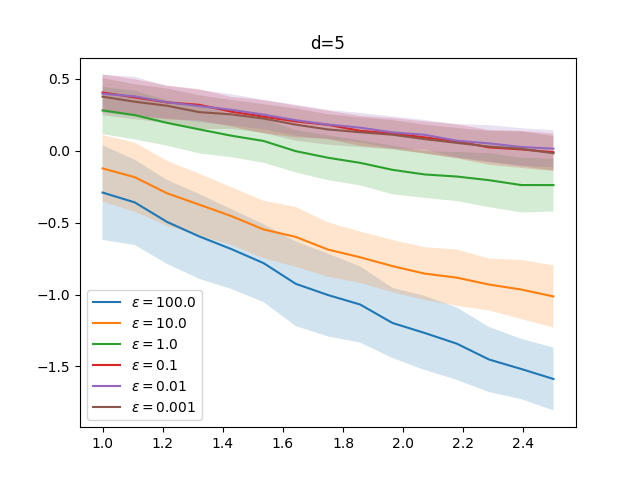

First, we consider the uniform distribution over a hypercube with the standard quadratic cost , which falls within our framework, as we are dealing with a cost on a bounded domain. Figure 1 shows the influence of the dimension on the convergence, while Figure 2 shows the influence of the regularization on the convergence for a given dimension. The influence of on the convergence rate increases with the dimension: the curves are almost parallel for all values of in dimension 2 but they get further apart as dimension increases. As expected from our bound, there is a cutoff which happens here at . All values of have similar convergence rates, and the dependence on becomes clear for smaller values. The same cutoff appears when looking at the influence of the dimension on the convergence rate for a fixed . The curves are parallel for all dimensions for but they have very different slopes for smaller .

We relax next some of the assumptions needed in our theorem to see how the Sinkhorn divergence behaves empirically. First we relax the regularity assumption on the cost, using . As seen on the two left images in figure 3 the behavior is very similar to the quadratic cost but with a more pronounced influence of , even for small dimensions. The fact that the convergence rate gets slower as gets smaller is already very clear in dimension 2, which wasn’t the case for the quadratic cost. The influence of the dimension for a given value of is not any different however.

We also relax the bounded domain assumption, considering a standard normal distribution over with a quadratic cost. While the influence of on the convergence rate is still obvious, the influence of the dimension is less clear. There is also a higher variance, which can be expected as the concentration bound from Corollary 1 depends on the diameter of the domain.

For all curves, we observe that and impact variance, with much smaller variance for small values of and high dimensions. From the concentration bound, the dependency on coming from the uniform bound on is of the form , suggesting higher variance for small values of . This could indicate that our uniform bound on is not tight, and we should consider other methods to get tighter bounds in further work.

7 Conclusion

We have presented two convergence theorems for SDs: a bound on the approximation error of OT and a sample complexity bound for empirical Sinkhorn divergences. The convergence rate is similar to MMD, but with a constant that depends on the inverse of the regularization parameter, which nicely complements the interpolation property of SDs pointed out in recent papers. Furthermore, the reformulation of SDs as the maximization of an expectation in a RKHS ball also opens the door to a better use of kernel-SGD for the computation of SDs.

Our numerical experiments suggest some open problems. It seems that the convergence rate still holds for unbounded domains and non-smooth cost functions. Besides, getting tighter bounds in our theorem might allow us to derive a sharp estimate on the optimal to approximate OT for a given , by combining our two convergence theorems together.

References

- Ambrosio et al. (2006) L. Ambrosio, N. Gigli, and G. Savaré. Gradient flows in metric spaces and in the space of probability measures. Springer, 2006.

- Arjovsky et al. (2017) M. Arjovsky, S. Chintala, and L. Bottou. Wasserstein gan. arXiv preprint arXiv:1701.07875, 2017.

- Bartlett and Mendelson (2002) P. L. Bartlett and S. Mendelson. Rademacher and gaussian complexities: Risk bounds and structural results. Journal of Machine Learning Research, 3(Nov):463–482, 2002.

- Beaumont et al. (2002) M. A. Beaumont, W. Zhang, and D. J. Balding. Approximate bayesian computation in population genetics. Genetics, 162(4):2025–2035, 2002.

- Bigot et al. (2017) J. Bigot, E. Cazelles, and N. Papadakis. Central limit theorems for sinkhorn divergence between probability distributions on finite spaces and statistical applications. arXiv preprint arXiv:1711.08947, 2017.

- Calderón (1961) A. Calderón. Lebesgue spaces of differentiable functions. In Proc. Sympos. Pure Math, volume 4, pages 33–49, 1961.

- Carlier et al. (2017) G. Carlier, V. Duval, G. Peyré, and B. Schmitzer. Convergence of entropic schemes for optimal transport and gradient flows. SIAM Journal on Mathematical Analysis, 49(2):1385–1418, 2017.

- Chen et al. (2016) Y. Chen, T. Georgiou, and M. Pavon. Entropic and displacement interpolation: a computational approach using the hilbert metric. SIAM Journal on Applied Mathematics, 76(6):2375–2396, 2016.

- Courty et al. (2014) N. Courty, R. Flamary, and D. Tuia. Domain adaptation with regularized optimal transport. In Joint European Conference on Machine Learning and Knowledge Discovery in Databases, pages 274–289. Springer, 2014.

- Cuturi (2013) M. Cuturi. Sinkhorn distances: Lightspeed computation of optimal transport. In Adv. in Neural Information Processing Systems, pages 2292–2300, 2013.

- Dudley (1969) R. Dudley. The speed of mean glivenko-cantelli convergence. The Annals of Mathematical Statistics, 40(1):40–50, 1969.

- Frogner et al. (2015) C. Frogner, C. Zhang, H. Mobahi, M. Araya, and T. Poggio. Learning with a Wasserstein loss. In Adv. in Neural Information Processing Systems, pages 2044–2052, 2015.

- Genevay et al. (2016) A. Genevay, M. Cuturi, G. Peyré, and F. Bach. Stochastic optimization for large-scale optimal transport. In D. D. Lee, U. V. Luxburg, I. Guyon, and R. Garnett, editors, Proc. NIPS’16, pages 3432–3440. Curran Associates, Inc., 2016.

- Genevay et al. (2018) A. Genevay, G. Peyre, and M. Cuturi. Learning generative models with sinkhorn divergences. In International Conference on Artificial Intelligence and Statistics, pages 1608–1617, 2018.

- Gretton et al. (2006) A. Gretton, K. Borgwardt, M. Rasch, B. Schölkopf, and A. Smola. A kernel method for the two-sample-problem. In Adv. in Neural Information Processing Systems, pages 513–520, 2006.

- Kantorovich (1942) L. Kantorovich. On the transfer of masses (in Russian). Doklady Akademii Nauk, 37(2):227–229, 1942.

- Kusner et al. (2015) M. Kusner, Y. Sun, N. Kolkin, and K. Q. Weinberger. From word embeddings to document distances. In Proc. of the 32nd Intern. Conf. on Machine Learning, pages 957–966, 2015.

- Li et al. (2017) C.-L. Li, W.-C. Chang, Y. Cheng, Y. Yang, and B. Póczos. MMD GAN: Towards deeper understanding of moment matching network. arXiv preprint arXiv:1705.08584, 2017.

- Li et al. (2015) Y. Li, K. Swersky, and R. Zemel. Generative moment matching networks. In International Conference on Machine Learning, pages 1718–1727, 2015.

- Ramdas et al. (2017) A. Ramdas, N. G. Trillos, and M. Cuturi. On wasserstein two-sample testing and related families of nonparametric tests. Entropy, 19(2):47, 2017.

- Salimans et al. (2018) T. Salimans, H. Zhang, A. Radford, and D. Metaxas. Improving GANs using optimal transport. In International Conference on Learning Representations, 2018.

- Sriperumbudur et al. (2012) B. Sriperumbudur, K. Fukumizu, A. Gretton, B. Schoelkopf, and G. Lanckriet. On the empirical estimation of integral probability metrics. Electronic Journal of Statistics, 6:1550–1599, 2012.

- Weed and Bach (2017) J. Weed and F. Bach. Sharp asymptotic and finite-sample rates of convergence of empirical measures in wasserstein distance. arXiv preprint arXiv:1707.00087, 2017.

Appendix

Proof.

(Lemma 1) For better clarity, we carry out the computations in dimension 1 but all the arguments are valid in higher dimension and we will clarify delicate points throughout the proof.

Differentiating both sides of the optimality condition (6) and rearranging yields

| (13) |

Notice that . Thus by immediate recurrence (differentiating both sides of the equality again) we get that

| (14) |

where and

To extend this first lemma to the -dimensional case, we need to consider the sequence of indexes which corresponds to the axis along which we successively differentiate. Using the same reasoning as above, it is straightforward to check that

where and

∎

Proof.

(Lemma 2)

The proof is made by recurrence on the following property :

: For all , for all , is bounded by a polynomial in of order .

Let us initialize the recurrence with

| (15) | |||||

| (16) |

Recall that . Let , we get that which is of the required form.

Now assume that is true for some . This means we have bounds on , for and . To prove the property at rank we want bounds on , for and . The only new quantity that we need to bound are . Let us start by bounding which corresponds to and we will do a backward recurrence on . By applying Leibniz formula for the successive derivatives of a product of functions, we get

| (17) | |||||

| (18) | |||||

| (19) | |||||

| (20) |

Thanks to we have that so the highest order term in in the above inequality is . Thus we get which is of the expected order

Now assume are bounded with the appropriate polynomials for . Let us bound

| (21) | |||||

| (22) |

The first term is bounded with a polynomial of order by recurrence assumption. Regarding the terms in the sum, they also have all been bounded and

So

To extend the result in , the recurrence is made on the the following property

| (23) |

where is a multi-index since we are dealing with multi-variate functions, and is defined at the end of the previous proof. The computations can be carried out in the same way as above, using the multivariate version of Leibniz formula in (18) since we are now dealing with multi-indexes. ∎