Robust Statistical learning with Lipschitz and convex loss functions

Abstract

We obtain estimation and excess risk bounds for Empirical Risk Minimizers (ERM) and minmax Median-Of-Means (MOM) estimators based on loss functions that are both Lipschitz and convex. Results for the ERM are derived under weak assumptions on the outputs and subgaussian assumptions on the design as in [2]. The difference with [2] is that the global Bernstein condition of this paper is relaxed here into a local assumption. We also obtain estimation and excess risk bounds for minmax MOM estimators under similar assumptions on the output and only moment assumptions on the design. Moreover, the dataset may also contains outliers in both inputs and outputs variables without deteriorating the performance of the minmax MOM estimators.

Unlike alternatives based on MOM’s principle [24, 29], the analysis of minmax MOM estimators is not based on the small ball assumption (SBA) of [22]. In particular, the basic example of non parametric statistics where the learning class is the linear span of localized bases, that does not satisfy SBA [39] can now be handled. Finally, minmax MOM estimators are analysed in a setting where the local Bernstein condition is also dropped out. It is shown to achieve excess risk bounds with exponentially large probability under minimal assumptions insuring only the existence of all objects.

1 Introduction

In this paper, we study learning problems where the loss function is simultaneously Lipschitz and convex. This situation happens in classical examples such as quantile, Huber and regression or logistic and hinge classification [42]. As the Lipschitz property allows to make only weak assumptions on the outputs, these losses have been quite popular in robust statistics [17]. Empirical risk minimizers (ERM) based on Lipschitz losses such as the Huber loss have received recently an important attention [45, 15, 2].

Based on a dataset of points in , a class of functions and a risk function defined on , the statistician want to estimate an oracle or to predict an output at least as good as . The risk function is often defined as the expectation of a loss function with respect to the unknown distribution of a random variable : . Hereafter, the risk is assumed to have this form for a loss function such that, for any , , for some function , where the set is a convex set containing all possible values of . The loss function is said Lipschitz and convex when the following assumption holds.

Assumption 1.

There exists such that, for any , is -Lipschitz and convex.

Many classical loss functions satisfy Assumption 1 and we recall some of them below.

-

•

The logistic loss defined, for any and , by satisfies Assumption 1 with .

-

•

The hinge loss defined, for any and , by satisfies Assumption 1 with .

- •

-

•

The quantile loss is defined, for any , , by where, for any , . It satisfies Assumption 1 with . For , the quantile loss is the loss.

All along the paper, the following assumption is also granted.

Assumption 2.

The class is convex.

When and the data are independent and identically distributed (i.i.d.), for any , the empirical risk is a natural estimator of . The empirical risk minimizers (ERM) [43] obtained by minimizing are expected to be close to the oracle . This procedure and its regularized versions have been extensively studied in learning theory [20]. When the loss is both convex and Lipschitz, results have been obtained in practice [4, 12] and theory [42]. Risk bounds with exponential deviation inequalities for the ERM can be obtained under weak assumptions on the outputs , but stronger assumptions on the design . Moreover, fast rates of convergence [41] can only be obtained under margin type assumptions such as the Bernstein condition [8, 42].

The Lipschitz assumption and global Bernstein conditions (that hold over the entire as in [2]) imply boundedness in -norm of the class , see the discussion preceding Assumption 4 for details. This boundedness is not satisfied in linear regression with unbounded design so the results of [2] don’t apply to this basic example such as linear regression with a Gaussian design. To bypass this restriction, the global condition is relaxed into a “local” one as in [15, 42], see Assumption 4 below.

The main constraint in our results on ERM is the assumption on the design. This constraint can be relaxed by considering alternative estimators based on the “median-of-means” (MOM) principle of [37, 9, 18, 1] and the minmax procedure of [3, 5]. The resulting minmax MOM estimators have been introduced in [24] for least-squares regression as an alternative to other MOM based procedures [29, 30, 31, 23]. In the case of convex and Lipschitz loss functions, these estimators satisfy the following properties 1) as the ERM, they are efficient under weak assumptions on the noise 2) they achieve optimal rates of convergence under weak stochastic assumptions on the design and 3) the rates are not downgraded by the presence of some outliers in the dataset.

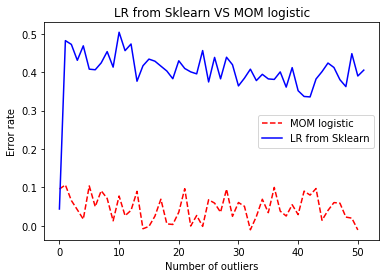

These improvements of MOM estimators upon ERM are not surprising. For univariate mean estimation, rate optimal sub-Gaussian deviation bounds can be shown under minimal moment assumptions for MOM estimators [14] while the empirical mean needs each data to have sub-Gaussian tails to achieve such bounds [13]. In least-squares regression, MOM-based estimators [29, 30, 31, 23, 24] inherit these properties, whereas the ERM has downgraded statistical properties under moment assumptions (see Proposition 1.5 in [25]). Furthermore, MOM procedures are resistant to outliers: results hold in the “” framework of [23, 24], where inliers or informative data (indexed by ) only satisfy weak moments assumptions and the dataset may contain outliers (indexed by ) on which no assumption is made, see Section 3. This robustness, that almost comes for free from a technical point of view is another important advantage of MOM estimators compared to ERM in practice. Figure 1 444All figures can be reproduced from the code available at https://github.com/lecueguillaume/MOMpower illustrates this fact, showing that statistical performance of the standard logistic regression are strongly affected by a single corrupted observation, while the minmax MOM estimator maintains good statistical performance even with of corrupted data.

Compared to [29, 24], considering convex-Lipschitz losses instead of the square loss allows to simplify simultaneously some assumptions and the presentation of the results for MOM estimators: -assumptions on the noise in [29, 24] can be removed and complexity parameters driving risk of ERM and MOM estimators only involve a single stochastic linear process, see Eq. (3) and (6) below. Also, contrary to the analysis in least-squares regression, the small ball assumption [22, 33] is not required here. Recall that this assumption states that there are absolute constants and such that, for all , . It is interesting as it involves only moments of order and of the functions in . However, it does not hold with absolute constants in classical frameworks such as histograms, see [39, 16] and Section 5.

Finally, minmax MOM estimators are studied in a framework where the Bernstein condition is dropped out. In this setting, they are shown to achieve an oracle inequality with exponentially large probability (see Section 4). The results are slightly weaker in this relaxed setting: the excess risk is bounded but not the risk and the rates of convergence are “slow” in in general. Fast rates of convergence in can still be recovered from this general result if a local Bernstein type condition is satisfied though, see Section 4 for details. This last result shows that minmax MOM estimators can be safely used with Lipschitz and convex losses, assuming only that inliers data are independent with enough finite moments to give sense to the results.

To approximate minmax MOM estimators, an algorithm inspired from [24, 26] is also proposed. Asymptotic convergence of this algorithm has been proved in [26] under strong assumptions, but, to the best of our knowledge, convergence rates have not been established. Nevertheless, the simulation study presented in Section 7 shows that it has good robustness performances.

The paper is organized as follows. Optimal results for the ERM are presented in Section 2. Minmax MOM estimators are introduced and analysed in Section 3 under a local Bernstein condition and in Section 4 without the Bernstein condition. A discussion of the main assumptions is provided in Section 5. Section 6 presents the theoretical limits of the ERM compared to the minmax MOM estimators. Finally, Section 7 provides a simulation study where a natural algorithm associated to the minmax MOM estimator for logistic loss is presented. The proofs of the main theorems are gathered in Sections A, B and C.

Notations

Let be measurable spaces and let denote a convex set . Let be a class of measurable functions and let be a random variable with distribution . Let denote the marginal distribution of . For any probability measure on , and any function , let . Let denote a loss function measuring the error made when predicting by . It is always assumed that there exists a function such that, for any , . Let for in denote the risk and let denote the excess loss. If and Assumption 1 holds, an equivalent risk can be defined even if . Actually, for any , so one can define . W.l.o.g. the set of risk minimizers is assumed to be reduced to a singleton . is called the oracle as provides the prediction of with minimal risk among functions in . For any and , let , for any , let and . For any set for which it makes sense, , . For any real numbers , we write when there exists a positive constant such that , when and , we write .

2 ERM in the sub-Gaussian framework

This section studies the ERM, improving some results from [2]. In particular, the global Bernstein condition in [2] is relaxed into a local hypothesis following [42]. All along this section, data are independent and identically distributed with common distribution . The ERM is defined for by

| (1) |

The results for the ERM are shown under a sub-Gaussian assumption on the class with respect to the distribution of . This result is the benchmark for the following minmax MOM estimators.

Definition 1.

Let . is called -sub-Gaussian (with respect to ) when for all and all

Assumption 3.

The class is -sub-Gaussian with respect to , where .

Under this sub-Gaussian assumption, statistical complexity can be measured via Gaussian mean-widths.

Definition 2.

Let . Let be the canonical centered Gaussian process indexed by (in particular, the covariance structure of is given by for all ). The Gaussian mean-width of is .

The complexity parameter driving the performance of is presented in the following definition.

Definition 3.

Let . In [8], the class is called -Bernstein if, for all , . Under Assumption 1, is -Bernstein if the following stronger assumption is satisfied

| (2) |

This stronger version was used, for example in [2] to study ERM. However, under Assumption 1, Eq (2) implies that

Therefore, for any . The class is bounded in -norm, which is restrictive as this assumption is not verified by the class of linear functions for example. To bypass this issue, the following condition is introduced.

Assumption 4.

There exists a constant such that, for all satisfying , we have .

In Assumption 4, Bernstein condition is granted in a -sphere centered in only. Outside of this sphere, there is no restriction on the excess loss. From the previous remark, it is clear that we necessarily have (as long as there exists some such that ). This relaxed assumption is satisfied for many Lipschitz-convex loss functions under moment assumptions and weak assumptions on the noise as it will be checked in Section 5. The following theorem is the main result of this section.

Theorem 1.

Theorem 1 is proved in Section A.1. It shows deviation bounds both in norm and for the excess risk, which are both minimax optimal as proved in [2]. As in [2], a similar result can be derived if the sub-Gaussian Assumption 3 is replaced by a boundedness in assumption. An extension of Theorem 1 can be shown, where Assumption 4 is replaced by the following hypothesis: there exists such that for all in a -shpere centered in , . The case is the most classical and its analysis contains all the ingredients for the study of the general case with any parameter . More general Bernstein conditions can also be considered as in [42, Chapter 7]. These extensions are left to the interested reader.

Notice that none of the assumptions 1, 2, 3 and 4 involve the output directly. All assumptions on are done through the oracle . Yet, as will become transparent in the applications in Section 5, some assumptions on the distributions of are required to check the assumptions of Theorem 1. These assumptions are not very restrictive though and Lipschitz losses have been quite popular in robust statistics for this reason.

3 Minmax MOM estimators

This section presents and studies minmax MOM estimators, comparing them to ERM. We relax the sub-Gaussian assumption on the class and the i.i.d assumption on the data .

3.1 The estimators

The framework of this section is a relaxed version of the i.i.d. setup considered in Section 2. Following [23, 24], there exists a partition of in two subsets unknown to the statistician. No assumption is granted on the set of “outliers” . “Inliers”, , are only assumed to satisfy the following assumption. For all , has distribution , has distribution and for any and any function for which it makes sense .

Assumption 5.

are independent and, for any , and .

Assumption 5 holds in the i.i.d case but it covers other situations where informative data may have different distributions.

Typically, when is the class of linear functions on , and are vectors with independent coordinates , then Assumption 5 is met if the coordinates have the same first and second moments for all .

Recall the definition of MOM estimators of univariate means.

Let denote a partition of into blocks of equal size (if is not a multiple of , just remove some data).

For any function and , let .

MOM estimator is the median of these empirical means:

The estimator achieves rate optimal sub-Gaussian deviation bounds, assuming only that , see for example [14]. The number is a tuning parameter. The larger , the more outliers are allowed. When , is the empirical mean, when , the empirical median.

Following [24], remark that the oracle is also solution of the following minmax problem:

Minmax MOM estimators are obtained by plugging MOM estimators of the unknown expectations in this formula:

| (5) |

The minmax MOM construction can be applied systematically as an alternative to ERM. For instance, it yields a robust version of logistic classifiers. The minmax MOM estimator with is the ERM.

The linearity of the empirical process is important to use localisation technics and derive “fast rates” of convergence for ERM [21], improving “slow rates” derived with the approach of [44], see [41] for details on “fast and slow rates”. The idea of the minmax reformulation comes from [3], where this strategy allows to overcome the lack of linearity of some alternative robust mean estimators. [23] introduced minmax MOM estimators to least-squares regression.

3.2 Theoretical results

3.2.1 Setting

The assumptions required for the study of estimator (5) are essentially those of Section 2 except for Assumption 3 which is relaxed into Assumption 5. Instead of Gaussian mean width, the complexity parameter is expressed as a fixed point of local Rademacher complexities [7, 10, 6]. Let denote i.i.d. Rademacher random variables (uniformly distributed on ), independent from . Let

| (6) |

The outputs do not appear in the complexity parameter. This is an interesting feature of Lipschitz losses. It is necessary to adapt the Bernstein assumption to this framework.

Assumption 6.

There exists a constant such that for all if then where

| (7) |

Assumptions 6 and 4 have a similar flavor as both require the Bernstein condition in a -sphere centered in with radius given by the rate of convergence of the associated estimator (see Theorems 1 and 2). For the sphere is a -sphere centered in of radius which can be of order (see Section 3.2.3). As a consequence, Assumption 6 holds in examples where the small ball assumption does not (see discussion after Assumption 9).

3.2.2 Main results

We are now in position to state the main result regarding the statistical properties of estimator (5) under a local Bernstein condition.

Theorem 2.

Suppose that , which is possible as long as . The deviation bound is then of order and the probability estimate . Therefore, minmax MOM estimators achieve the same statistical bound with the same deviation as the ERM as long as and are of the same order. Using generic chaining [40], this comparison is true under Assumption 3. It can also be shown under weaker moment assumption, see [35] or the example of Section 3.2.3.

When , the bounds are rate optimal as shown in [2]. This is why these bounds are called rate optimal sub-Gaussian deviation bounds. While these hold for ERM in the i.i.d. setup with sub-Gaussian design in the absence of outliers (see Theorem 1), they hold for minmax MOM estimators in a setup where inliers may not be i.i.d., nor have sub-Gaussian design and up to outliers may have contaminated the dataset.

This section is concluded by presenting an estimator achieving (5) simultaneously for all . For all and , define and let

| (10) |

Now, building on the Lepskii’s method, define a data-driven number of blocks

| (11) |

and let be such that

| (12) |

Theorem 3.

Theorem 3 states that achieves the results of Theorem 2 simultaneously for all . This extension is useful as the number of outliers is typically unknown in practice. However, contrary to , the estimator requires the knowledge of and . These parameters allow to build confidence regions for , which is necessary to apply Lepski’s method. Similar limitations appear in least-squares regression [24] and even in the basic problem of univariate mean estimation. In this simpler problem, it can be shown that one can build sub-Gaussian estimators depending on the confidence level (through ) under only a second moment assumption. On the other hand, to build estimators achieving the same risk bounds simultaneously for all , more informations on the distribution of the data are required, see [14, Theorem 3.2]. In particular, the knowledge of the variance, which allows to build confidence intervals for the unknown univariate mean, is sufficient. The necessity of extra-information to obtain adaptivity with respect to is therefore not surprising here.

3.2.3 Some basic examples

The following example illustrates the optimality of the rates provided in Theorem 2 even under a simple -moment assumption.

Lemma 1 ([19]).

In the framework with , we have , where is the covariance matrix of .

The proof of Lemma 1 is recalled in Section B for the sake of completeness. Lemma 1 grants only the existence of a second moment for even though the rate obtained is the same as the one we would get under a sub-Gaussian assumption given that . Moreover, Section 5 shows that Assumptions 4 and 6 are satisfied when and is a vector with i.i.d. entries having only a few finite moments. Theorem 2 applies therefore in this setting and the Minmax MOM estimator (5) achieves the optimal fast rate of convergence . This shows that when the model is the entire space , the results for the ERM from Theorem 1 obtained under a sub-Gaussian assumption is the same as the one for the minmax MOM from Theorem 2 under only weak moment assumption.

However, Lemma 1 does not describe a typical situation. Having of the same order as under only a second moment assumption is mainly happening on large models such as the entire space . For smaller size models such as the -ball (the unit ball of the -norm), the picture is different: should be bigger than unless has enough moment. To make this statement simple let us consider the case . In that case, we have . Let us now describe under various moment assumptions on to see when compares with .

Let be a random vector. It follows from Equation (3.1) in [36] that

where and is a non-increasing rearrangement of the absolute values of the coordinates of . Assume that are i.i.d. distributed like such that and . Assume that has moments, for and let be such that . Then, using Jensen’s inequality, we obtain

It follows that

Hence,

Assume that , with . Then,

In particular,

Let us now show that these estimates are sharp by considering where is a Rademacher variable, is a Bernouilli variable (independent of ) with mean and . We have and because when . Let be i.i.d. copies of . We have

As a consequence, for all ,

and so . As a consequence, under only a moment assumption one cannot have better than .

As a consequence, can be much larger than when has less than moments, for instance, can be of the order of when has only moments. This picture is different from the one given by Lemma 1 where we were able to get equivalence between and only under a second moment assumption.

4 Relaxing the Bernstein condition

This section shows that minmax MOM estimators satisfy sharp oracle inequalities with exponentially large deviation under minimal stochastic assumptions insuring the existence of all objects. These results are slightly weaker than those of the previous section: the risk is not controlled and only slow rates of convergence hold in this relaxed setting. However, the bounds are sufficiently precise to imply fast rates of convergence for the excess risk as in Theorems 2 if a slightly stronger Bernstein condition holds.

Given that data may not have the same distribution as , the following relaxed version of Assumption 5 is introduced.

Assumption 7.

are independent and for all , has distribution , has distribution . For any , and for all .

When Assumption 6 does not necessary hold, the localization argument has to be modified. Instead of the -norm, the excess risk is used to define neighborhoods around . The associated complexity is then defined for all and by

| (13) |

where

There are two important differences between on one side and in Definition 2 or in (6) on the other side. The first one is the extra variance term . Under the Bernstein condition, this term is negligible in front of the “expectation term” see [8]. In the general setting considered here, the variance term is handled in the complexity parameter. The second important consequence is that is a fixed point of the complexity of localized around with respect to the excess risk rather than with respect to the -norm. An important consequence is that this quantity is harder to compute in practical examples. As a consequence, the results of this section are more of theoretical importance.

Theorem 4.

Recall that Assumptions 1 and 2 are only meaning that the loss function is convex and Lipschitz and that the class is convex. Assumption 7 says that inliers are independent and define the same excess risk as over . In particular, Theorem 4 holds, as Theorem 2, without assumptions on the outliers and with weak assumptions on the outputs of the inliers (we remrak that excess loss function is well-defined under no assumption on – even if – because ). Moreover, the excess risk bound holds with exponentially large probability without assuming sub-Gaussian design, a small ball hypothesis or a Bernstein condition. This generality can be achieved by combining MOM estimators with convex-Lipschitz loss functions.

The following result discuss relationships between Theorems 2 and 4. Introduce the following modification of the Bernstein condition.

Assumption 8.

Let . There exists a constant such that for all if then where, for defined in (6),

Assumption 8 is slightly stronger than Assumption 4 since the -metric to define the sphere is replaced by the excess risk metric. If Assumption 8 holds then Theorem 5 implies the same statistical bounds for (5) as Theorem 2 up to constants, as shown by the following result.

Theorem 5.

Proof.

First, for all where . Moreover, and are non-increasing, therefore by Assumption 8 and the definition of , ,

Hence, .

5 Bernstein’s assumption

This section shows that the local Bernstein condition holds for various loss functions and design . In Assumption 4 and 6, the comparizon between and is only required on a -sphere. In this section, we prove that the local Bernstein assumption can be verified over the entire -ball and not only on the sphere under mild moment conditions. The class is assumed to satisfy a “ -norm equivalence assumption”, for .

Assumption 9.

Let . There exists such that for all ,

Assumption 9 is a “” norm equivalence assumption over . A “” norm equivalence assumption over has been used for the study of MOM estimators (see [29]). Examples of distributions satisfying Assumption 9 can be found in [33, 34].

There are situations where the constant depends on the dimension of the model. In that case, the results in [29, 24] provide sub-optimal statistical upper bounds. For instance, if is uniformly distributed on and where is the indicator of then for all , so . This dependence with respect to the dimension is inevitable. For instance, in [29, 24], a norm equivalence is required. In this case, which ultimately yields sub-optimal rates in this example. On the other hand, as will become clear in this section, the rates given in Theorem 2 or Theorem 3 are not deteriorated in this example. This improvement is possible since the Bernstein condition is only required in a neighborhood of .

5.1 Quantile loss

Assumption 10.

Let be the constant defined in Assumption 9. There exist and such that, for all and for all in such that , we have , where is the conditional density function of given .

Theorem 6.

Consider the example from Section 3.2.3, assume that and let . If , Assumption 10 holds for and an associated as long as and, for all and for all in such that , . As , the first condition reduces to . In this situation, the rates given in Theorems 2 and 3 are still . This gives a partial answer, in our setting, to the issue raised in [39] regarding results based on the small ball method.

5.2 Huber Loss

Consider the Huber loss function defined, for all , and , by where if and otherwise. Introduce the following assumption.

Assumption 11.

Let be the constant defined in Assumption 9. There exist and such that for all and all in such that , , where is the conditional cumulative function of given .

Under this assumption and a “” assumption, the local Bernstein condition is proved to be satisfied in the following result whose proof is postponed to Section C.2.

5.3 Logistic classification

In this section we consider the logistic loss function.

Assumption 12.

The following result is proved in Section C.3.

The proof is postponed to Section C.3. As for the Huber Loss and the Hinge Loss, the rates of convergence are not deteriorated when may depend on the dimension as long as is smaller than some absolute constant.

5.4 Hinge loss

In this section, we show that the local Bernstein condition holds for various design for the Hinge loss function. We obtain the result under the assumption that the oracle is actually the Bayes rules which is the function minimizing the risk over all measurable functions from to . Recall that, under this assumption, where . In that case, the Bernstein condition (see [8]) coincides with the margin assumption (see [41, 32]).

Assumption 13.

Let be the constant defined in Assumption 9. There exist and such that for all , for all ,

Theorem 9.

The proof is postponed to Section C.4.

6 Comparison between ERM and minmax MOM

In this section, we show that robustness properties with respect to heavy-tailed data and to outliers of the minmax MOM estimator in Theorem 2 cannot be achieved by the ERM. We prove two lower bounds on the statistical risk of ERM. First, we show that ERM is not robust to contamination in the design and second that ERM cannot achieve the optimal rate with a sub-Gaussian deviation under only moment assumptions.

We first show the absence of robustness of ERM w.r.t. contamination by even a single input variable. We consider the absolute loss function of linear functionals . Let denote i.i.d. Gaussian vectors, and suppose that there exists such that . Assume that a vector was added to (and that this is the only corrupted data). Hence, we are given the dataset . Consider the ERM constructed on this dataset i.e where . In this context, the following lower bound holds.

Proposition 1.

There exist absolute constants and such that the following holds. If the contamination vector satisfies , with , then with probability at least , .

When , from Theorem 2 with , minmax MOM estimators yields, with probability at least , on the same dataset as the one used by ERM in Proposition 1. If then the ERM is suboptimal compared with the minmax MOM estimator.

Proof. To show that is outside , it is enough to show that is smaller than the smallest value of over . It follows from Gaussian concentration that, with probability at least ,

| (14) |

Let us now bound from bellow the empirical loss function uniformly over all in . First,

| (15) |

Then, it follows from Borell-TIS inequality (see Theorem 7.1 in [27] or pages 56-57 in [28]) that with probability at least . Therefore, , where

On , we have for all that . Therefore, using (15) and for a large enough constant ,

| (16) |

It follows from Proposition 1 that ERM is not consistant when there is even a single outlier among the . By comparison, the minmax MOM has optimal performance even when the dataset has been corrupted by up to outliers when . This shows a first advantage of the minmax MOM approach.

Now, we prove a second advantage of the minmax MOM over the ERM by considering heavy-tailed design. We also consider the absolute -loss function as in the previous example and suppose that data are generated from a linear model in dimension : where and are independent mean zero random variables and (we choose so that we have access to a canonical definition of median which simplifies the proof). Our aim is to show that if the design has only a second moment then the ERM cannot achieve the optimal rate with a sub-Gaussian deviation that is as does the minmax MOM for all .

Proposition 2.

Let and . There exist and two symmetric and independent random variables such that , and, for any and , we have . Let be i.i.d. copies of such that for some . Let . Then, with probability at least ,

Proof. Let and let be uniformly distributed over . Let denote a Rademacher variable, let be a Bernoulli variable with parameter and . We assume that and are independent and let . Let and let be a dataset of i.i.d. copies of , where .

Since the median of is , for all with equality iff . As a consequence, for all and the only minimizer of is . In other words, is the oracle. For all ,

Since and , we have , that is, the -norm is equivalent to the absolute value.

Observe that is solution of the minimization problem

Here, defining , is a random variable such that

Notice that, almost surely, all are different. In particular, is the absolute value of the empirical median . Therefore, when the median of does not belong to . This holds when or . Introduce the following sets

Define also the following events

By Hoeffding’s inequality (see Chapter 2 in [11]), as is a family of i.i.d. random variables distributed like , with probability at least ,

Since , are independent, centered random variables taking values in . By Hoeffding’s inequality, with probability at least ,

Using a union bound, we have when . Since the ’s and the ’s are independent, on the event , we have

The last inequality holds since . Moreover,

When , this implies

Therefore, on the event , and so

We want to show that on the event , for some well-chosen constant . We have if and only if

In particular, if

| (17) |

then the median of takes value in , resp. in . Since, for all and for all , in these cases, . Since , the proof is finished if (17) is proved.

Let us now prove that (17) holds on the event . On this event, only one equals to . Therefore only one equals to and all the others equal . Moreover, for all . Therefore, if denotes the only index such that , then either or . If , on ,

Moreover, all the equal when . Therefore, . Overall, which is equivalent to . Likewise, if then . Therefore, on the event (17) holds.

Proposition 2 shows that the distance between the ERM and is larger than with probability at least . This probability is larger than for large values of , which shows that the ERM does not have sub-Gaussian deviations. Let us now show that, using the same data and a number of blocks (or using the adaptive estimator (12)), the minmax MOM estimators achieve the rate with probability at least . This will show a second advantage of minmax MOM estimators compared with ERM for heavy-tailed designs.

To apply Theorem 2 (or Theorem 3 for the adaptive estimator), we show that the local Bernstein condition is satisfied for the example of Proposition 2 and compute the complexity parameter . We have

As a consequence, satisfies (6). We now prove Assumption 6 in this particular example. Let be such that so that, for is defined in (7) with and defined later,

Let be such that . We have to show that for some well chosen and . It follows from (39) that where and is the cdf of given . Therefore, if we denote by the cdf of , we have

Let us choose such that (which holds for instance when ). In that case, and so for all . We therefore have

Moreover, since , we have

Assume that , so . Then, we have

For , this yields , which concludes the proof of the Berntein’s assumption.

7 Simulation study

This section provides a short simulation study that illustrates our theoretical findings for the minmax MOM estimators. Let us consider the following setup: , where are independent and identically distributed, with , and

where . Let be i.i.d with the same distribution as . We the study the minmax MOM estimator defined as:

| (18) |

Following [24], a gradient ascent-descent step is performed on the empirical incremental risk constructed on the block of data realizing the median of the empirical incremental risk. Initial points and are taken at random. In logistic regression, the step sizes and are usually chosen equal to , where is the matrix with row vectors equal to and denotes the operator norm. In a corrupted environment, this choice might lead to disastrous performance. This is why and are computed at each iteration using only data in the median block: let denote the median block at the current step, then one chooses where is the matrix with rows given by for . In practice, is chosen by robust cross-validation choice as in [24].

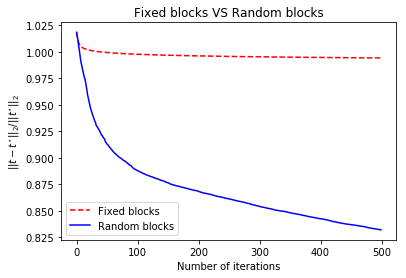

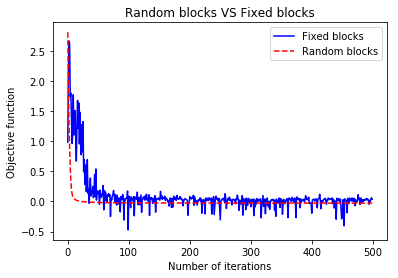

In a first approach and according to our theoretical results, the blocks are chosen at the beginning of the algorithm. As illustrated in Figure 2, this first strategy has some limitations. To understand the problem, for all , let denote the following set

If the minimum of lies in , the algorithm typically converges to this minimum if one iteration enters . As a consequence, when the minmax MOM estimator (18) lies in another cell, the algorithm does not converge to this estimator.

To bypass this issue, the partition is changed at every ascent/descent steps of the algorithm, it is chosen uniformly at random among all equipartition of the dataset. This alternative algorithm is described in Algorithm 1. In practice, changing the partition seems to widely accelerate the convergence (see Figure 2).

Simulation results are gathered in Figure 2. In these simulations, there is no outlier, and with i.i.d with the same distribution as . Minmax MOM estimators (18) are compared with the Logistic Regression algorithm from the scikit-learn library of [38].

The upper pictures compare performance of MOM ascent/descent algorithms with fixed and changing blocks. These pictures give an example where the fixed block algorithm is stuck into local minima and another one where it does not converge. In both cases, the changing blocks version converges to .

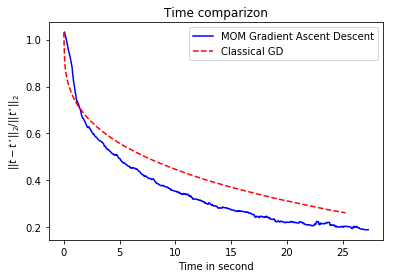

Running times of logistic regression (LR) and its MOM version (MOM LR) are compared in the lower picture of Figure 2 in a dataset free from outliers. LR and MOM LR are coded with the same algorithm in this example, meaning that MOM gradient descent-ascent and simple gradient descent are performed with the same descent algorithm. As illustrated in Figure 2, running each step of the gradient descent on one block only and not on the whole dataset accelerates the running time. The larger the dataset, the bigger the benefit is expected.

The resistance to outliers of logistic regression and its minmax MOM alternative are depicted in Figure 1 in the introduction. We added an increasing number of outliers to the dataset. Outliers in this simulation are such that and , with as above. Figure 1 shows that logistic classification is mislead by a single outlier while MOM version maintains reasonable performance with up to 50 outliers (i.e % of the database is corrupted).

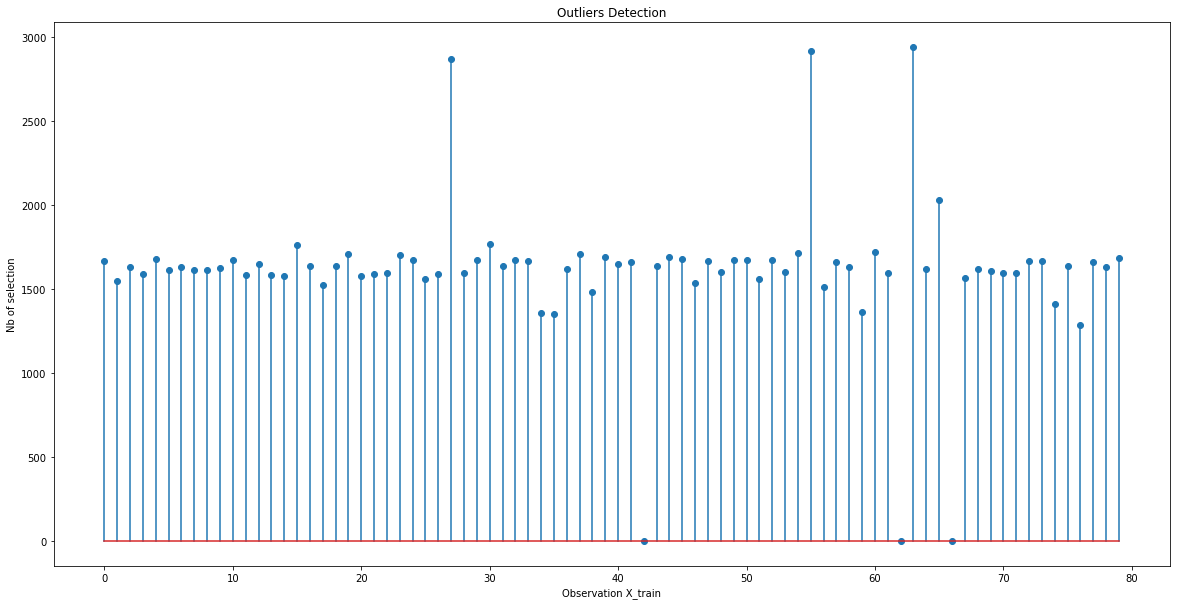

A byproduct of Algorithm 1 is an outlier detection algorithm. Each data receives a score equal to the number of times it is selected in a median block in the random choice of block version of the algorithm. The first iterations may be misleading: before convergence, the empirical loss at the current point may not reveal the centrality of the data because the current point may be far from . Simulations are run with , and iterations and therefore only the score obtained by each data in the last iterations are displayed. outliers with and have been introduced at number , and . Figure 3 shows that these are not selected once.

8 Conclusion

The paper introduces a new homogenity argument for learning problems with convex and Lipschitz losses. This argument allows to obtain estimation rates and oracle inequalities for ERM and minmax MOM estimators improving existing results. The ERM requires sub-Gaussian hypotheses on the class with respect to the distribution of the design and a local Bernstein condition (see Theorem 1), both assumptions can be removed for minmax MOM estimators (see Theorem 5). The local Bernstein conditions provided in this article can be verified in several learning problems. In particular, it allows to derive optimal risk bounds in examples where analyses based on the small ball hypothesis fail. Minmax MOM estimators applied to convex and Lipschitz losses are efficient under weak assumptions on the outputs , under minimal assumptions on the class with respect to the distribution of the design and the results are robust to the presence of few outliers in the dataset. A modification of these estimators can be implemented efficiently and confirm all these conclusions.

Appendix A Proof of Theorems 1, 2, 3 and 4

A.1 Proof of Theorem 1

The proof is splitted in two parts. First, we identify an event where the statistical behavior of the regularized estimator can be controlled. Then, we prove that this event holds with probability at least (3). Introduce and define the following event:

where is a parameter appearing in the definition of in Definition 3.

Proposition 3.

On the event , one has

Proof.

By construction, satisfies . Therefore, it is sufficient to show that, on , if , then . Let be such that . By convexity of , there exists and such that

| (19) |

For all , let be defined for all by

| (20) |

The functions are such that , they are convex because is, in particular for all and and so that the following holds:

| (21) |

Until the end of the proof, the event is assumed to hold. Since , . Moreover, by Assumption 4, , thus

| (22) |

From Eq. (A.1) and (22), since . Therefore, . This proves the -bound.

Now, as , . Since ,

This show the excess risk bound.

Proposition 3 shows that has the risk bounds given in Theorem 1 on the event . To show that holds with probability (3), recall the following results from [2].

Lemma 2.

A.2 Proof of Theorem 2

The proof is splitted in two parts. First, we identify an event where the statistical properties of from Theorem 2 can be established. Next, we prove that this event holds with probability (8). Let and be positive numbers to be chosen later. Define

where the exact form of and are given in Equation (33). Set the event to be such that

| (25) |

A.2.1 Deterministic argument

The goal of this section is to show that, on the event , and .

Lemma 3.

If there exists such that

| (26) |

then .

Proof.

Assume that (26) holds, then

| (27) |

Moreover, if for all , then

| (28) |

By definition of and (28), . Moreover, by (27), any satisfies . Therefore .

Proof.

Let be such that . By convexity of , there exists and such that . For all , let be defined for all by

| (29) |

The functions are convex because is and such that , so for all and . As , for any block ,

| (30) |

As , on , there are strictly more than blocks where . Moreover, from Assumption 6, . Therefore, on strictly more than blocks ,

| (31) |

From Eq. (A.2.1) and (31), there are strictly more than blocks where . Therefore, on , as ,

In addition, on the event , for all , there are strictly more than blocks where . Therefore

Lemma 5.

Grant Assumption 6 and assume that . On the event , .

A.2.2 Stochastic argument

This section shows that holds with probability at least (8).

Proposition 4.

Proof.

Let and set so, for all , . Let , . Let

Let denote the set of indices of blocks which have not been corrupted by outliers, and let . Basic algebraic manipulations show that

By Assumptions 1 and 5, using that ,

Therefore,

| (32) |

Using Mc Diarmid’s inequality [11, Theorem 6.2], for all , with probability larger than ,

Let denote independent Rademacher variables independent of the . By Giné-Zinn symmetrization argument,

As is 1-Lipschitz with , using the contraction lemma [28, Chapter 4],

Let be a family of independent Rademacher variables independent of and . It follows from the Giné-Zinn symmetrization argument that

By the Lipschitz property of the loss, the contraction principle applies and

To bound from above the right-hand side in the last inequality, consider two cases 1) or 2) . In the first case, by definition of the complexity parameter in (6),

In the second case,

Let be such that ; by convexity of , there exists such that and with . Therefore,

and so

By definition of , it follows that

Therefore, as , with probability larger than , for all such that ,

| (33) |

A.2.3 End of the proof of Theorem 2

A.3 Proof of Theorem 3

Let and consider the event defined in (25). It follows from the proof of Lemmas 3 and 4 that on . Setting , on , for all , so . By definition of , it follows that and by definition of , which means that . It is proved in Lemmas 3 and 4 that on , if satisfies then . Therefore, . On , since , . Hence, on , the conclusions of Theorem 3 hold. Finally, by Proposition 4,

A.4 Proof of Theorem 4

The proof of Theorem 4 follows the same path as the one of Theorem 2. We only sketch the different arguments needed because of the localization by the excess loss and the lack of Bernstein condition.

Define the event in the same way as in (25) where is replaced by and the localization is replaced by the “excess loss localization”:

| (34) |

where . Our first goal is to show that on the event , . We will then handle .

Lemma 6.

Proof.

Let and be in and . We have because is convex and for all and , using the convexity of , we have

and so . Given that we also have . Therefore, and is convex.

For all , so that is continuous onto in and therefore its level sets, such as , are relatively closed to in .

Finally, let be such that . Define . Note that for so that . Since is relatively closed to in , we have and in particular otherwise, by convexity of , we would have . Moreover, by maximality of , is such that and the results follows for .

Proof.

Let be such that . It follows from Lemma 6 that there exists and such that and . According to (A.2.1), we have for every , . Since , on the event , there are strictly more than blocks such that and so . As a consequence, we have

| (35) |

Moreover, on the event , for all , there are strictly more than blocks such that . Therefore,

| (36) |

We conclude from (35) and (36) that and that every such that satisfies . But, by definition of , we have

Therefore, we necessarily have .

Now, we prove that is an exponentially large event using similar argument as in Proposition 4.

Proposition 5.

Sketch of proof. The proof of Proposition 5 follows the same line as the one of Proposition 4. Let us precise the main differences. We set and for all , where is the same quantity as in the proof of Proposition 5. Let us consider the contraction introduced in Proposition 5. By definition of and , we have

Using Mc Diarmid’s inequality, the Giné-Zinn symmetrization argument and the contraction lemma twice and the Lipschitz property of the loss function, such as in the proof of Proposition 4, we obtain with probability larger than , for all ,

| (37) |

Now, it remains to use the definition of to bound the expected supremum in the right-hand side of (37) to get

| (38) |

Appendix B Proof of Lemma 1

Proof.

We have

Let denote the covariance matrix of and consider its SVD, where is an orthogonal matrix and is a diagonal matrix with non-negative entries. For all , we have . Then

Moreover, for any such that ,

By orthonormality, and , then, for any such that ,

Finally, we obtain

and therefore the fixed point is such that

Appendix C Proofs of the results of Section 5

We begin this Section with a simple Lemma coming from the convexity of .

Lemma 8.

For any ,

where we recall that .

Proof.

Let . By convexity of , and because minimizes the risk over .

C.1 Proof of Theorem 6

Let . Let be such that . For all denote by the conditional c.d.f. of given . We have

By Fubini’s theorem,

Therefore,

where . It follows that

| (39) |

Since for all , is twice differentiable, from a second order Taylor expansion we get

where for all , is some point in . For the first order term, we have

For all , we have which is integrable with respect to . Thus, by the dominated convergence theorem, it is possible to interchange integral and limit and therefore using Lemma 8, we obtian

Given that for all , for all it follows that

C.2 Proof of Theorem 7

Let . Let be such that . We have

where . Let denote the c.d.f. of given . Since for all , is twice differentiable in its second argument (see Lemma 2.1 in [15]), a second Taylor expansion yields

where for all , is some point in . By Lemma 8, with the same reasoning as the one in Section C.1, we get

Moreover, for all ,

Now, let . It follows from Assumption 10 that . Since , by Markov’s inequality, . By Holder and Markov’s inequalities,

By Assumption 9, it follows that , which concludes the proof.

C.3 Proof of Theorem 8

C.4 Proof of Theorem 9

Let such that . Let be in such that . For all in let us denote . It is easy to verify that the Bayes estimator (which is equal to the oracle) is defined as . Consider the set . Since , by Markov’s inequality . Let be in . If (i.e ) and we obtain

where we used the fact that on , . Using the same analysis for the other cases we get that

Therefore,

| (41) |

By Holder and Markov’s inequalities,

References

- [1] Noga Alon, Yossi Matias, and Mario Szegedy. The space complexity of approximating the frequency moments. J. Comput. System Sci., 58(1, part 2):137–147, 1999. Twenty-eighth Annual ACM Symposium on the Theory of Computing (Philadelphia, PA, 1996).

- [2] P. Alquier, V. Cottet, and G. Lecué. Estimation bounds and sharp oracle inequalities of regularized procedures with lipschitz loss functions. arXiv preprint arXiv:1702.01402, 2017.

- [3] Jean-Yves Audibert and Olivier Catoni. Robust linear least squares regression. Ann. Statist., 39(5):2766–2794, 2011.

- [4] Francis Bach, Rodolphe Jenatton, Julien Mairal, Guillaume Obozinski, et al. Convex optimization with sparsity-inducing norms. Optimization for Machine Learning, 5:19–53, 2011.

- [5] Y. Baraud, L. Birgé, and M. Sart. A new method for estimation and model selection: -estimation. Invent. Math., 207(2):425–517, 2017.

- [6] Peter L. Bartlett, Olivier Bousquet, and Shahar Mendelson. Local Rademacher complexities. Ann. Statist., 33(4):1497–1537, 2005.

- [7] Peter L Bartlett, Olivier Bousquet, Shahar Mendelson, et al. Local rademacher complexities. The Annals of Statistics, 33(4):1497–1537, 2005.

- [8] Peter L. Bartlett and Shahar Mendelson. Empirical minimization. Probab. Theory Related Fields, 135(3):311–334, 2006.

- [9] Lucien Birgé. Stabilité et instabilité du risque minimax pour des variables indépendantes équidistribuées. Ann. Inst. H. Poincaré Probab. Statist., 20(3):201–223, 1984.

- [10] Stéphane Boucheron, Olivier Bousquet, and Gábor Lugosi. Theory of classification: a survey of some recent advances. ESAIM Probab. Stat., 9:323–375, 2005.

- [11] Stéphane Boucheron, Gábor Lugosi, and Pascal Massart. Concentration inequalities. Oxford University Press, Oxford, 2013. A nonasymptotic theory of independence, With a foreword by Michel Ledoux.

- [12] Sébastien Bubeck. Convex optimization: Algorithms and complexity. Foundations and Trends® in Machine Learning, 8(3-4):231–357, 2015.

- [13] Olivier Catoni. Challenging the empirical mean and empirical variance: a deviation study. Ann. Inst. Henri Poincaré Probab. Stat., 48(4):1148–1185, 2012.

- [14] Luc Devroye, Matthieu Lerasle, Gabor Lugosi, Roberto I Oliveira, et al. Sub-gaussian mean estimators. The Annals of Statistics, 44(6):2695–2725, 2016.

- [15] Andreas Elsener and Sara van de Geer. Robust low-rank matrix estimation. arXiv preprint arXiv:1603.09071, 2016.

- [16] Qiyang Han and Jon A. Wellner. Convergence rates of least squares regression estimators with heavy-tailed errors. 2017.

- [17] Peter J Huber and E. Ronchetti. Robust statistics. In International Encyclopedia of Statistical Science, pages 1248–1251. Springer, 2011.

- [18] Mark R. Jerrum, Leslie G. Valiant, and Vijay V. Vazirani. Random generation of combinatorial structures from a uniform distribution. Theoret. Comput. Sci., 43(2-3):169–188, 1986.

- [19] Vladimir Koltchinskii. Local Rademacher complexities and oracle inequalities in risk minimization. Ann. Statist., 34(6):2593–2656, 2006.

- [20] Vladimir Koltchinskii. Empirical and rademacher processes. In Oracle Inequalities in Empirical Risk Minimization and Sparse Recovery Problems, pages 17–32. Springer, 2011.

- [21] Vladimir Koltchinskii. Oracle inequalities in empirical risk minimization and sparse recovery problems, volume 2033 of Lecture Notes in Mathematics. Springer, Heidelberg, 2011. Lectures from the 38th Probability Summer School held in Saint-Flour, 2008, École d’Été de Probabilités de Saint-Flour. [Saint-Flour Probability Summer School].

- [22] Vladimir Koltchinskii and Shahar Mendelson. Bounding the smallest singular value of a random matrix without concentration. Int. Math. Res. Not. IMRN, (23):12991–13008, 2015.

- [23] G. Lecué and M. Lerasle. Learning from mom’s principles: Le cam’s approach. To appear in Stochastic processes and their applications, 2017.

- [24] G. Lecué and M. Lerasle. Robust machine learning by median-of-means: theory and practice. To appear in the Annals of Statistics, 2017.

- [25] Guillaume Lecué and Shahar Mendelson. Performance of empirical risk minimization in linear aggregation. Bernoulli, 22(3):1520–1534, 2016.

- [26] G. Lecué, M. Lerasle, and T. Mathieu. Robust classification via mom minimization. arXiv:1808.03106, 2018.

- [27] Michel Ledoux. The concentration of measure phenomenon, volume 89 of Mathematical Surveys and Monographs. American Mathematical Society, Providence, RI, 2001.

- [28] Michel Ledoux and Michel Talagrand. Probability in Banach Spaces: isoperimetry and processes. Springer Science & Business Media, 2013.

- [29] Gabor Lugosi and Shahar Mendelson. Risk minimization by median-of-means tournaments. To appear in JEMS, 2016.

- [30] Gabor Lugosi and Shahar Mendelson. Regularization, sparse recovery, and median-of-means tournaments. Preprint available on arXiv:1701.04112, 2017.

- [31] Gabor Lugosi and Shahar Mendelson. Sub-gaussian estimators of the mean of a random vector. To appear in Ann. Statist. arXiv:1702.00482, 2017.

- [32] Enno Mammen and Alexandre B. Tsybakov. Smooth discrimination analysis. Ann. Statist., 27(6):1808–1829, 1999.

- [33] Shahar Mendelson. Learning without concentration. In Conference on Learning Theory, pages 25–39, 2014.

- [34] Shahar Mendelson. Learning without concentration. J. ACM, 62(3):Art. 21, 25, 2015.

- [35] Shahar Mendelson. On multiplier processes under weak moment assumptions. In Geometric aspects of functional analysis, volume 2169 of Lecture Notes in Math., pages 301–318. Springer, Cham, 2017.

- [36] Shahar Mendelson, Alain Pajor, and Nicole Tomczak-Jaegermann. Reconstruction and subgaussian operators in asymptotic geometric analysis. Geom. Funct. Anal., 17(4):1248–1282, 2007.

- [37] A. S. Nemirovsky and D. B. Yudin. Problem complexity and method efficiency in optimization. A Wiley-Interscience Publication. John Wiley & Sons, Inc., New York, 1983. Translated from the Russian and with a preface by E. R. Dawson, Wiley-Interscience Series in Discrete Mathematics.

- [38] F. Pedregosa, G. Varoquaux, A. Gramfort, V. Michel, B. Thirion, O. Grisel, M. Blondel, P. Prettenhofer, R. Weiss, V. Dubourg, J. Vanderplas, A. Passos, D. Cournapeau, M. Brucher, M. Perrot, and E. Duchesnay. Scikit-learn: Machine learning in Python. Journal of Machine Learning Research, 12:2825–2830, 2011.

- [39] Adrien Saumard. On optimality of empirical risk minimization in linear aggregation. Bernoulli, 24(3):2176–2203, 2018.

- [40] Michel Talagrand. Upper and lower bounds for stochastic processes, volume 60 of Ergebnisse der Mathematik und ihrer Grenzgebiete. 3. Folge. A Series of Modern Surveys in Mathematics [Results in Mathematics and Related Areas. 3rd Series. A Series of Modern Surveys in Mathematics]. Springer, Heidelberg, 2014. Modern methods and classical problems.

- [41] Alexandre B. Tsybakov. Optimal aggregation of classifiers in statistical learning. Ann. Statist., 32(1):135–166, 2004.

- [42] Sara van de Geer. Estimation and testing under sparsity, volume 2159 of Lecture Notes in Mathematics. Springer, [Cham], 2016. Lecture notes from the 45th Probability Summer School held in Saint-Four, 2015, École d’Été de Probabilités de Saint-Flour. [Saint-Flour Probability Summer School].

- [43] Vladimir Vapnik. The Nature of Statistical Learning Theory. Springer-Verlag New York, Inc., New York, NY, USA, 1995.

- [44] Vladimir Vapnik. Statistical learning theory, volume 1. Wiley New York, 1998.

- [45] W.-X. Zhou, K. Bose, J. Fan, and H. Liu. A new perspective on robust m-estimation: Finite sample theory and applications to dependence-adjusted multiple testing. 2018.