- IC

- Improvement Condition

- RLS

- Regularized Least Squares

- TL

- Transfer Learning

- HTL

- Hypothesis Transfer Learning

- ERM

- Empirical Risk Minimization

- TEAM

- Target Empirical Accuracy Maximization

- RKHS

- Reproducing kernel Hilbert space

- DA

- Domain Adaptation

- LOO

- Leave-One-Out

- HP

- High Probability

- RSS

- Regularized Subset Selection

- FR

- Forward Regression

- PSD

- Positive Semi-Definite

- SGD

- Stochastic Gradient Descent

- OGD

- Online Gradient Descent

- EWA

- Exponentially Weighted Average

- EMD

- Effective Metric Dimension

- PDE

- Partial Differential Equation

- SDE

- Stochastic Differential Equation

- FD

- Frequent Directions

- OFU

- Optimism in the Face of Uncertainty

- TS

- Thompson Sampling

Efficient Linear Bandits through Matrix Sketching

Abstract

We prove that two popular linear contextual bandit algorithms, OFUL and Thompson Sampling, can be made efficient using Frequent Directions, a deterministic online sketching technique. More precisely, we show that a sketch of size allows a update time for both algorithms, as opposed to required by their non-sketched versions in general (where is the dimension of context vectors). This computational speedup is accompanied by regret bounds of order for OFUL and of order for Thompson Sampling, where is bounded by the sum of the tail eigenvalues not covered by the sketch. In particular, when the selected contexts span a subspace of dimension at most , our algorithms have a regret bound matching that of their slower, non-sketched counterparts. Experiments on real-world datasets corroborate our theoretical results.

1 Introduction

The stochastic contextual bandit is a sequential decision-making problem where an agent interacts with an unknown environment in a series of rounds. In each round, the environment reveals a set of feature vectors (called contexts, or actions) to the agent. The agent chooses an action from the revealed set and observes the stochastic reward associated with that action (bandit feedback). The strategy used by the agent for choosing actions based on past observations is called a policy. The goal of the agent is to learn a policy minimizing the regret, defined as the difference between the total reward of the optimal policy (i.e., the policy choosing the action with highest expected reward at each round) and the total reward of the agent’s policy.

Contextual bandits are a popular modelling tool in many interactive machine learning tasks. A typical area of application is personalized recommendation, where a recommender system selects a product for a given user from a set of available products (each described by a feature vector) and receives a feedback (purchase or non-purchase) for the selected product.

We focus on the stochastic linear bandit model (Auer, 2002; Dani et al., 2008), where the set of actions (or decision set) is a finite111 Note that our regret bounds do not actually depend on the cardinality of the sets . set , and the reward for choosing action is given by where is a fixed and unknown vector of real coefficients and is a zero-mean random variable. The regret in this setting is defined by

| (1) |

where is the optimal action at round . Bounds on the regret typically apply to any individual sequence of decision sets and depend on quantities arising from the interplay between , the sequence of decision sets, and the randomness of the rewards. Note that is a random variable because the actions selected by the policy are functions of the past observed rewards. For this reason, our regret bounds only hold with probability at least , where is a confidence parameter. By choosing , we can instead bound the expected regret by paying only a extra factor in the bound.

We consider two of the most popular algorithms for stochastic linear bandits: OFUL (Abbasi-Yadkori et al., 2011) and linear Thompson Sampling (Agrawal and Goyal, 2013) (linear TS for short). While exhibiting good theoretical and empirical performances, both algorithms require time to update their model after each round. In this work we investigate whether it is possible to significantly reduce this update time while ensuring that the regret remains nicely bounded.

The quadratic dependence on is due to the computation of the inverse correlation matrix of past actions (a cubic dependence is avoided because each new inverse is a rank-one perturbation of the previous inverse). The occurrence of this matrix is caused by the linear nature of rewards: to compute their decisions, both algorithms essentially solve a regularized least squares problem at every round. In order to improve the running time, we sketch the correlation matrix using a specific technique —Frequent Directions, (Ghashami et al., 2016)— that works well in a sequential learning setting. While matrix sketching is a well-known approach (Woodruff, 2014), to the best of our knowledge this is the first work that applies sketching to linear contextual bandits while providing rigorous performance guarantees.

With a sketch size of , a rank-one update of the correlation matrix takes only time , which is linear in for a constant sketch size. However, this speed-up comes at a price, as sketching reduces the matrix rank causing a loss of information which —in turn— affects the least squares estimates used by the algorithms. Our main technical contribution shows that when OFUL and linear TS are run with a sketched correlation matrix, their regret blows up by a factor which is controlled by the spectral decay of the correlation matrix of selected actions. More precisely, we show that the sketched variant of OFUL, called SOFUL, achieves a regret bounded by

| (2) |

where is the sketch size and is upper bounded by the spectral tail (sum of the last eigenvalues) of the correlation matrix for all rounds. In the special case when the selected actions span a number of dimensions equal or smaller than the sketch size, then implying a regret of order . Thus, we have a regret bound matching that of the slower, non-sketched counterpart.222The regret bound of OFUL in (Abbasi-Yadkori et al., 2011, Theorem 3) is stated as , however, it can be improved for low-rank problems by using the “log-det” formulation of the confidence ellipsoid. When the correlation matrix has rank larger than the sketch size, the regret of SOFUL remains small to the extent the spectral tail of the matrix grows slowly with . In the worst case of a spectrum with heavy tails, SOFUL may incur linear regret. In this respect, sketching is only justified when the computational cost of running OFUL cannot be afforded. Similarly, we prove that the efficient sketched formulation of linear TS enjoys a regret bound of order

| (3) |

Once again, for our bound is of order , which matches the regret bound for linear TS. When the rank of the correlation matrix is larger than the sketch size, the bound for linear TS behaves similarly to the bound for SOFUL.

Finally, we show a problem-dependent regret bound for SOFUL. This bound, which exhibits a logarithmic dependence on , depends on the smallest gap between the expected reward of the best and the second best action across the rounds,

| (4) |

When this bound is of order which matches the corresponding bound for OFUL. Experiments on six real-world datasets support our theoretical results.

Additional related work.

For an introduction to contextual bandits, we refer the reader to the recent monograph of Lattimore and Szepesvári (2018). The idea of applying sketching techniques to linear contextual bandits was also investigated by Yu et al. (2017), where they used random projections to preliminarly draw a random -dimensional subspace which is then used in every round of play. However, the per-step computation time of their algorithm is cubic in rather than quadratic like ours. Morover, random projection introduces an additive error in the instantaneous regret which becomes of order for any value of the confidence parameter bounded away from . A different notion of compression in contextual bandits is explored by Jun et al. (2017), where they use hashing algorithms to obtain a computation time sublinear in the number of actions. An application of sketching (including Frequent Directions) to speed up 2nd order algorithms for online learning is studied by Luo et al. (2016), in a RKHS setting by Calandriello et al. (2017), and in stochastic optimization by Gonen et al. (2016).

2 Notation and preliminaries

Let be the Euclidean ball of center and radius and let . Given a positive definite matrix , we define the inner product and the induced norm , for any . Throughout the paper, we write to denote . The contextual bandit protocol is described in Algorithm 1.

We introduce some standard assumptions for the linear contexual bandit setting. At any round the decision set is finite and such that for all and for all . The noise sequence is conditionally -subgaussian for some fixed constant . Formally, for all and all , . Note that this implies and . Finally, we assume that a known upper bound on is available.

Both OFUL and Linear TS operate by computing a confidence ellipsoid to which belongs with high probability. Let be the matrix of all actions selected up to round by an arbitrary policy for linear contextual bandits. For , define the regularized correlation matrix of actions and the regularized least squares (RLS) estimate as

| (5) |

The following theorem (Abbasi-Yadkori et al., 2011, Theorem 2) bounds in probability the distance, in terms of the norm , between the optimal parameter and the RLS estimate .

Theorem 1 (Confidence Ellipsoid).

Let be the RLS estimate constructed by an arbitrary policy for linear contextual bandits after rounds of play. For any , the optimal parameter belongs to the set with probability at least , where

| (6) |

OFUL.

The actions selected by OFUL are solutions to the following constrained optimization problem

Note that maximizes the expected reward estimate plus a term that provides an upper confidence bound for the RLS estimate in the direction of .

Linear TS.

The linear Thompson Sampling algorithm of Agrawal and Goyal (2013) is Bayesian in nature: the selected actions and the observed rewards are used to update a Gaussian prior over the parameter space. Each action is selected by maximixing over , where is a random vector drawn from the posterior. As shown by Abeille and Lazaric (2017), linear TS can be equivalently defined as a randomized algorithm based on the RLS estimate (see Algorithm 3).

The random vectors are drawn i.i.d. from a suitable multivariate distribution that need not be related to the posterior. In order to prove regret bounds, it is sufficient that the law of satisfies certain properties.

Definition 1 (TS-sampling distribution).

A multivariate distribution on , absolutely continuous w.r.t. the Lebesgue measure, is TS-sampling if it satisfies the following two properties:

-

•

(Anti-concentration) There exists such that for any with , .

-

•

(Concentration) There exist such that for all ,

Similarly to OFUL, linear TS uses the notion of confidence ellipsoid. However, due to the properties of the sampling distribution , the ellipsoid used by linear TS is larger by a factor of order than the ellipsoid used by OFUL. This causes an extra factor of in the regret bound, which is not known to be necessary.

Note that both OFUL and linear TS need to maintain (or ), which requires time to update. In the next section, we show how this update time can be improved by sketching the regularized correlation matrix .

3 Sketching the correlation matrix

The idea of sketching is to maintain an approximation of , denoted by , where is a small constant called the sketch size. If we choose such that approximates well, we could use in place of . In the following we use the notation to denote the sketched regularized correlation matrix. The RLS estimate based upon it is denoted by

| (7) |

A trivial replacement of with does not yield an efficient algorithm. On the other hand, using the Woodbury identity we may write

where . Here matrix-vector multiplications involving require time , while matrix-matrix multiplications involving require time . So, as long as and can be efficiently maintained, we obtain an algorithm for linear stochastic bandits where can be updated in time . Next, we focus on a concrete sketching algorithm that ensures efficient updates of and .

Frequent Directions.

Frequent Directions (FD) (Ghashami et al., 2016) is a deterministic sketching algorithm that maintains a matrix whose last row is invariably . On each round, we insert into the last row of , perform an eigendecomposition , and then set , where is the smallest eigenvalue of . Observe that the rows of form an orthogonal basis, and therefore is a diagonal matrix which can be updated and stored efficiently. Now, the only step in question is an eigendecomposition, which can also be done in time —see (Ghashami et al., 2016, Section 3.2). Hence, the total update time per round is . The updates of matrices and are summarized in Algorithm 4.

It is not hard to see that FD sketching sequentially identifies the top- eigenvectors of the matrix . Thus, whenever we use a sketched estimate, we lose a part of the spectrum tail. This loss is captured by the following notion of spectral error,

| (8) |

where are the eigenvalues of the correlation matrix . Note that . For matrices with low rank or light-tailed spectra we expect this spectral error to be small. In the following, we use to denote the quantity which occurs often in our bounds involving sketching. Note that and as the spectral error vanishes.

Since the matrix is used to compute both the RLS estimate and the norm , the sketching of clearly affects the confidence ellipsoid. The next theorem quantifies how much the confidence ellipsoid must be blown up in order to compensate for the sketching error. Let be the smallest eigenvalue of the FD-sketched correlation matrix and let . The following proposition due to Ghashami et al. (2016) (see the proof of Thm. 3.1, bound on ) relates to defined in (8).

Proposition 1.

For any , any , and any sketch size , it holds that .

A key lemma in the analysis of regret is the following sketched version of (Abbasi-Yadkori et al., 2011, Lemma 11), which bounds the sum of the ridge leverage scores. Although sketching introduces the spectral error , it also improves the dependence on the dimension from to whenever is sufficiently small.

Lemma 1 (Sketched leverage scores).

| (9) |

We can now state the main result of this section.

Theorem 2 (Sketched confidence ellipsoid).

Let be the RLS estimate constructed by an arbitrary policy for linear contextual bandits after rounds of play. For any , the optimal parameter belongs to the set with probability at least , where

| (10) | ||||

| (11) |

Note that (11) is larger than its non-sketched counterpart (6) due to the factors . However, when the spectral error vanishes, becomes of order , which improves upon (6) since we replace the dependence on the ambient space dimension with the dependence on the sketch size . In the following, we use the abbreviation .

4 Sketched OFUL

Equipped with the sketched confidence ellipsoid and the sketched RLS estimate, we can now introduce SOFUL (Algorithm 5), the sketched version of OFUL.

SOFUL enjoys the following regret bound, characterized in terms of the spectral error.

Theorem 3.

The regret of SOFUL with FD-sketching of size w.h.p. satisfies

Similarly to Abbasi-Yadkori et al. (2011), we also prove a distribution dependent regret bound for SOFUL. This bound is polylogarithmic in time and depends on the smallest difference between the rewards of the best and the second best action in the decision sets,

Theorem 4.

The regret of SOFUL with FD-sketching of size w.h.p. satisfies

Proofs of the regret bounds appear in the supplementary material (Section 6.3).

5 Sketched linear TS

In this section we introduce a variant of linear TS (Algorithm 3) based on FD-sketching. Similarly to SOFUL, sketched linear TS (see Algorithm 6) uses the FD-sketched approximation of the correlation matrix in order to select the action .

Note that, in this case, we need both and to compute . Using the generalized Woodbury identity (Corollary 1 in Section 6.2 for proofs), we can write

where

Note that can still be computed in time because is a diagonal matrix.

The confidence ellipsoid stated in Theorem 2 applies to any contextual bandit policy, and so also to the constructed by sketched linear TS. However, as shown by Abeille and Lazaric (2017), the analysis needs a confidence ellipsoid larger by a factor equal to the bound on appearing in the concentration property of the TS-sampling distribution. More precisely, the TS-confidence ellipsoid is defined by

where

| (12) |

The quantity is defined in (10) and are the concentration constants of the TS-sampling distribution (Definition 1). We are now ready to prove a bound on the regret of linear TS with FD-sketching.

Theorem 5.

The regret of FD-sketched linear TS, run with sketch size w.h.p. satisfies

6 Proofs

We start with the proof of a simple lemma that is used in the definition of OFUL (see Algorithm 2).

Lemma 2.

For any positive definite matrix , for any and , the solution of

| s.t. |

has value .

Proof.

Let so that . Then the optimization problem can be equivalently rewritten as

| s.t. |

Then the solution is clearly , which achieves the claimed value. ∎

Our regret analyses follow (Abbasi-Yadkori et al., 2011; Abeille and Lazaric, 2017) and related works. However, due to the sketching of the correlation matrix, some key components of the proofs now depend on the spectral error (8). In Section 6.2, we present tools specific to the analysis of linear bandits with FD-sketching. These tools are used to bound the instantaneous regret in terms of the norm and the ridge leverage scores . Armed with these results, we then prove our regret bounds in Sections 6.3 and 6.4.

Next, we recall some standard tools from the analysis of linear bandits. All results in Section 6.1 are by Abbasi-Yadkori et al. (2011).

6.1 Tools from the analysis of linear contextual bandits

Recall that with .

Lemma 3 (Determinant-trace inequality).

Lemma 4 (Ridge leverage scores).

| (13) |

For , we also have that

| (14) |

Theorem 6 (Self-normalized bound for vector-valued martingales).

Let

where is a conditionally -subgaussian real-valued stochastic process and is any -valued stochastic process such that is measurable with respect to the -algebra generated by . Then, for any , with probability at least , for all , where

| (15) |

Theorem 6 is key to showing that lies within the confidence ellipsoid centered at the estimate at time step , this irrespective of the process that selected the used to build .

6.2 Linear algebra and sketching tools

We start by introducting a basic relationship between the correlation matrix of actions and its FD-sketched estimate with sketch size . Recall that is the smallest eigenvalue of for and . Recall also that .

Proposition 2.

Let be the matrix computed by FD-sketching at time step (where ). Then

where is a matrix of eigenvectors of . Moreover,

Proof.

By construction, where . Thus,

Summing both sides of the above over we get

which implies the desired result. ∎

In the following lemma, we show a sketch-specific version of the determinant-trace inequality (Lemma 3). When the spectral error is small, the right-hand side of the inequality depends on the sketch size rather than the ambient dimension .

Lemma 5.

Proof.

Let be the eigenvalues of . We start by looking at the ratio of determinants. Throughout the proof, unless stated explicitly, denote . Using Proposition 2 we can write

| (16) |

since because has rank at most . We now use the AM-GM inequality, stating that

Using the AM-GM inequality, the product in (16) can be bounded as

| (17) |

where the last inequality holds because

| (by Proposition 2) | ||||

| (by definition of ) | ||||

The next lemma is similar to (Abbasi-Yadkori et al., 2011, Lemma 11). However, now the statement depends on the sketched matrix instead of . Although we pay in terms of the spectral error , we also improve the dependence on the dimension from to whenever is sufficiently small.

Lemma 6 (Sketched leverage scores).

| (18) |

Proof.

Throughout the proof, unless stated explicitly, we drop the subscripts containing . Therefore, , , , and . Consider a following decomposition:

| (by Proposition 2) | ||||

| (since is Positive Semi-Definite (PSD)) | ||||

Furthermore, this implies that

| (multiply both sides by ) | ||||

Finally, combining the above with Lemma 4, equation (14), and using the fact that , we obtain

| (by Lemma 5) | ||||

where the last inequality follows from Proposition 1. ∎

Now we prove Theorem 2, characterizing the confidence ellipsoid generated by the sketched estimate.

Theorem 2

(Sketched confidence ellipsoid – restated). For any , the optimal parameter belongs to the set

with probability at least , where

Proof.

Denote . Throughout the proof we frequently use Proposition 2, implying . For brevity, in the following we drop subscripts containing in matrices. Let , and by definition of the sketched estimate we have that

| (19) | ||||

| (20) |

Then, by (20), for any we have that

| (21) | ||||

| (by Cauchy-Schwartz) |

We now choose and proceed by bounding terms in the above. By the choice of , we have that , and

where we used the fact that by definition of , .

Finally, by Theorem 6, for any , with probability at least ,

The left-hand side of (21) can now upper bounded as

| (22) |

Now we handle the ratios of norms in the right-hand side of (22). First, by Proposition 2,

since and, using the same reasoning,

Substituting these into (22) gives

Now we provide a deterministic bound on . Using Lemma 5 we have

This proves the first statement (10). Finally, (11) follows by Proposition 1, that is . ∎

We close this section by computing a closed form for , the square root of the inverse of the sketched correlation matrix. This is used by sketched linear TS for selecting actions. We make use of the following result —see. e.g., (Higham, 2008, Theorem 1.35).

Theorem 7 (Generalized Woodbury matrix identity).

Let and , with , and assume that is nonsingular. Let be defined on the spectrum of , and if let be defined at . Then .

This is used to prove the following.

Corollary 1.

For , let

Then

6.3 Proof of the regret bound for SOFUL (Theorem 3)

We start with a preliminary lemma.

Lemma 7.

For any , the instantaneous regret of SOFUL satisfies

Proof.

Now we are ready to prove the regret bound.

Proof of Theorem 3..

Proof of Theorem 4.

Recall that

Similarly to the proof of Theorem 3, we use Lemma 7 to bound the instantaneous regret. However, we first use the gap assumption to bound the regret in terms of the sum of squared instantaneous regrets,

| (24) | ||||

| (25) | ||||

| (26) |

where (25) holds because . Inequality (24) holds because

| (by Cauchy-Schwartz) |

and because of Lemma 7.

6.4 Proof of the regret bound for Sketched Linear TS (Theorem 5)

Here is used to denote the FD-sketched RLS estimate of linear TS (Algorithm 6). As in (Abeille and Lazaric, 2017), we split the regret as follows

| (27) |

where

is an “optimistic” reward function. Most of the proof is concerned with bounding the first term in (27). The second term is instead obtained in way similar to the analysis of OFUL. Fix any , let , and introduce events

and . Observe that, by definition,

| (28) |

We also use the following lower bound on the probability of .

Lemma 8.

.

Proof.

We study the regret when occurs,

| (using (28)) | ||||

| (29) |

where we introduced the notation

First we focus on , and get that

| (because implies ) | ||||

| (using (28)) |

Consider the following set of “optimistic” coefficients such that and, moreover, belongs to the sketched TS confidence ellipsoid,

Then, for

| (30) |

We now use (Abeille and Lazaric, 2017, Proposition 3 and Lemma 2) (restated below here for convenience) to argue about the convexity of and relate its gradient to the chosen action.

Proposition 3.

For any finite set of actions such that , is convex on . Moreover, it is continuous with continuous first derivatives (except for a zero-measure set w.r.t. the Lebesgue measure).

Lemma 9.

For any , we have

(except for a zero-measure w.r.t. the Lebesgue measure).

Relying on the two results above, we can proceed as follows. Introduce . Then by Proposition 3, is convex for since . Then, by letting , for any we have

| (by Cauchy-Schwartz) | ||||

where the last inequality holds for all and by the triangle inequality. Substituting this into (30), and taking expectation with respect to yields

| (31) |

where we use to denote the -algebra generated by the random variables . Now we further upper bound while bounding the probability of event occurring in (31). This is done in the following lemma, whose proof (omitted here) is identical to the proof of (Abeille and Lazaric, 2017, Lemma 3), where ellipsoids are replaced by their sketched counterparts.

Lemma 10.

Assume that is a TS-sampling distribution with anti-concentration parameter . Then, for we have that

We now proceed with the main argument of the proof. Using ,

| (by Lemma 10.) |

The above combined with (31) implies that

| (32) |

Finally, summing (32) over time we get

Note that we can already bound using (12). However, we cannot bound the expectation right away, so we rewrite the above as follows

| (33) |

where we introduce the martingale

Next, we use the Azuma-Hoeffding inequality to upper-bound .

Theorem 8 (Azuma-Hoeffding inequality).

If a supermartingale corresponding to a filtration satisfies for some constant for , then for any ,

Now verify that for any ,

Thus, by the Azuma-Hoeffding inequality, with probability at least we have

| (34) |

Now we focus our attention on the remaining term:

| (35) |

where the last step is due to Lemma 6.

7 Experiments

In this section we present experiments on six publicly available classification datasets.

Setup.

The idea of our experimental setup is similar to the one described by Cesa-Bianchi et al. (2013). Namely, we convert a -class classification problem into a contextual bandit problem as follows: given a dataset of labeled instances , we partition it into subsets according to the class labels. Then we create sequences by drawing a random permutation of each subset. At each step the decision set is obtained by picking the -th instance from each one of these sequences. Finally, rewards are determined by choosing a class and then consistently assigning reward to all instances labeled with and reward to all remaining instances.

Datasets.

We perform experiments on six publicly available datasets for multiclass classification from the openml repository (Vanschoren et al., 2013) —dataset IDs 1461, 23, 32, 182, 22, and 44, see the table below here for details.

| Dataset | Examples | Features | Classes |

|---|---|---|---|

| Bank | 45k | 17 | 2 |

| SatImage | 6k | 37 | 6 |

| Spam | 4k | 58 | 2 |

| Pendigits | 11k | 17 | 10 |

| MFeat | 2k | 48 | 10 |

| CMC | 1.4k | 10 | 3 |

Baselines.

The hyperparameters (confidence ellipsoid radius) and (RLS regularization parameter) are selected on a validation set of size via grid search on for OFUL, and for linear TS.

Results

We observe that on three datasets, Figure 2, sketched algorithms indeed do not suffer a substantial drop in performance when compared to the non-sketched ones, even when the sketch size amounts to of the context space dimension. This demonstrates that sketching successfully captures relevant subspace information relatively to the goal of maximizing reward.

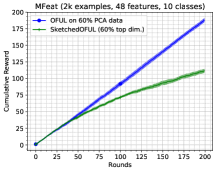

Because the FD-sketching procedure considered in this paper is essentially performing online PCA, it is natural to ask how our sketched algorithms would compare to their non-sketched version run on the best -dimensional subspace (computed by running PCA on the entire dataset). In Figure 3, we compare SOFUL and sketched linear TS to their non-sketched versions. In particular, we keep , and of the top principal components, and notice that, like in Figure 2, there are cases with little or no loss in performance.

References

- Abbasi-Yadkori et al. (2011) Y. Abbasi-Yadkori, D. Pál, and C. Szepesvári. Improved algorithms for linear stochastic bandits. In Advances in Neural Information Processing Systems, pages 2312–2320, 2011.

- Abeille and Lazaric (2017) M. Abeille and A. Lazaric. Linear Thompson sampling revisited. Electronic Journal of Statistics, 11(2):5165–5197, 2017.

- Agrawal and Goyal (2013) S. Agrawal and N. Goyal. Thompson sampling for contextual bandits with linear payoffs. In International Conference on Machine Learing (ICML), pages 127–135, 2013.

- Auer (2002) P. Auer. Using confidence bounds for exploitation-exploration trade-offs. Journal of Machine Learning Research, 3(Nov):397–422, 2002.

- Calandriello et al. (2017) D. Calandriello, A. Lazaric, and M. Valko. Efficient second-order online kernel learning with adaptive embedding. In Conference on Neural Information Processing Systems (NIPS), pages 6140–6150, 2017.

- Cesa-Bianchi et al. (2013) N. Cesa-Bianchi, C. Gentile, and G. Zappella. A gang of bandits. In Conference on Neural Information Processing Systems (NIPS), pages 737–745, 2013.

- Dani et al. (2008) V. Dani, T. P. Hayes, and S. M. Kakade. Stochastic linear optimization under bandit feedback. In Conference on Computational Learning Theory (COLT), pages 355–366, 2008.

- Ghashami et al. (2016) M. Ghashami, E. Liberty, J. M. Phillips, and D. P. Woodruff. Frequent directions: Simple and deterministic matrix sketching. SIAM Journal on Computing, 45(5):1762–1792, 2016.

- Gonen et al. (2016) A. Gonen, F. Orabona, and S. Shalev-Shwartz. Solving ridge regression using sketched preconditioned SVRG. In International Conference on Machine Learing (ICML), pages 1397–1405, 2016.

- Higham (2008) N. J. Higham. Functions of matrices: theory and computation, volume 104. Siam, 2008.

- Jun et al. (2017) K.-S. Jun, A. Bhargava, R. Nowak, and R. Willett. Scalable generalized linear bandits: Online computation and hashing. In Conference on Neural Information Processing Systems (NIPS), pages 99–109, 2017.

- Lattimore and Szepesvári (2018) T. Lattimore and C. Szepesvári. Bandit Algorithms. Cambridge University Press, 2018.

- Luo et al. (2016) H. Luo, A. Agarwal, N. Cesa-Bianchi, and J. Langford. Efficient second order online learning by sketching. In Conference on Neural Information Processing Systems (NIPS), pages 902–910, 2016.

- Vanschoren et al. (2013) J. Vanschoren, J. N. van Rijn, B. Bischl, and L. Torgo. OpenML: Networked Science in Machine Learning. SIGKDD Explorations, 15(2):49–60, 2013.

- Woodruff (2014) D. Woodruff. Sketching as a tool for numerical linear algebra. Foundations and Trends in Theoretical Computer Science, 10(1–2):1–157, 2014.

- Yu et al. (2017) X. Yu, M. R. Lyu, and I. King. Cbrap: Contextual bandits with random projection. In Conference on Artificial Intelligence (AAAI), pages 2859–2866, 2017.