Exact Solutions for Optimal Investment Strategies and

Indifference Prices under Non-Differentiable Preferences

Abstract

We propose an algorithm to calculate the exact solution for utility optimization problems on finite state spaces under a class of non-differentiable preferences. We prove that optimal strategies must lie on a discrete grid in the plane, and this allows us to reduce the dimension of the problem and define a very efficient method to obtain those strategies. We also show how fast approximations for the value function can be obtained with an a priori specified error bound and we use these to replicate results for investment problems with a known closed-form solution. These results show the efficiency of our approach, which can then be used to obtain numerical solutions for problems for which no explicit formulas are known.

1 Introduction

One of the classical problems in mathematical finance concerns the optimal investment in risky assets by an investor who is risk averse. Explicit solutions for the trade-off between risk and return that characterize such problems were derived in the seminal work of Merton [9]. His work showed that a certain combination of risk preferences and assumptions on the dynamics of asset prices leads to a stochastic control problem in continuous time which can be solved explicitly. In the most well-known example it is assumed that the risky asset prices are Geometric Brownian Motions and that risk tolerance is linear in wealth. In that case the optimal investment strategy turns out to be linear in wealth as well and an explicit formula can be derived for the proportion of wealth that is invested in the risky asset if the investor behaves optimally.

This result has been extended in many directions. Under the linear risk tolerance structure, better known as Constant Relative Risk Aversion (CRRA), more complicated asset dynamics can be treated. One may still obtain relatively simple characterizations of optimal investment strategies when some of the parameters describing the dynamics of the risky asset vary over time in a deterministic way, for example. The resulting strategies are again linear in wealth but the coefficients will then vary over time. Kraft [7] has shown that this also holds when risky asset prices are generated by the stochastic volatility model introduced by Heston [6], which is generally considered to give a more realistic description of equity prices.

Another direction for generalizations also uses Geometric Brownian Motion process to describe asset prices, an assumption that is also known as Black-Scholes dynamics due to its use in the famous paper on option pricing [2], but chooses different preferences. The class of utility functions known as Symmetrically Adjusted Hyperbolic Absolute Risk Aversion (SAHARA) also generates closed-form solutions. The optimal investment strategies are not linear and not even monotone in this case, since risk aversion is always positive but not always increasing when wealth levels become lower. Such preferences can therefore be used to describe the phenomenon where investors ”gamble for resurrection”, meaning that they may take more risky positions once their wealth levels become really low.

For most utility functions and equity dynamics, no closed form solution can be derived for the optimal investment problem in continuous time. One therefore has to resort to numerical methods to generate suitable approximations to the optimal strategies. This makes calculations much more time consuming, which is in particular problematic when the optimal strategies are used as input for further calculations.

This is for example the case when one wants to determine what is known as the indifference price for an asset or contingent claim which cannot be perfectly replicated using other assets in the market. Replication (in continuous time) means that a continuously updated portfolio can be defined which generates exactly the same payoff as a certain contingent claim. If this is the case, absence of arbitrage dictates that the price of the contingent claim is the same as the costs of setting up the initial portfolio which replicates it. But claims which cannot be replicated, i.e. claims which render the market incomplete cannot be priced using such methods.

An alternative definition for the selling price of such a claim states that the seller of the claim (who thus receives the price of the claim) should be indifferent, in terms of his or her expected utility, between selling the claim and receiving its price in compensation, or not selling the claim. Analogously, the buying price for such a claim should be chosen in such a way that paying this price at the initial time and receiving the payoffs of the claim afterwards, lead to exactly the same expected utility over the lifetime of the claim as not paying its price and not receiving its cashflows. This shows that these indifference pricing methods always lead to two different optimal investment problems that must be solved. Once involves optimal investment when the claim payoffs and initial buying or selling transactions are taken into consideration, while the other one involves optimal investment when there are no claims involved. Requiring the solutions to those two problems to be the same then implicitly defines what the price of a claim, i.e. the indifference price should be.

In practice, there are not that many indifferent pricing problems that can be solved explicitly. One therefore often has to rely on numerical approximations which are based dynamics in discrete time. In this paper we will show that exact solutions can be found for optimal investment and indifference pricing problems in discrete time if risk preferences are characterized by a class of utility functions which are piecewise linear. We require asset prices to be Markovian on a finite state space, and we take the binomial model of Cox, Ross and Rubinstein [4] as canonical example. We show that our class of utility functions is defined has certain properties which are inherited if they are propagated backwards in time under the dynamic programming equations which characterize optimal policies. As a result, we can prove that efficient algorithms exist which generate the exact solution for those policies and the associated value functions or indifference prices.

Our technique is based on a grid constructed in the plane, where is the total wealth and is the wealth invested in risky assets. Such a grid consists of two sets of parallel lines with different slopes and we prove that the optimal strategy must always lie on this grid. This property allows us to define a method, which to the best of our knowledge has not been proposed before, to determine the optimal strategy in a very efficient way. When more risk factors are involved, such as a stochastic volatility component, we can still reduce the analysis of such more complicated problems to the design of a suitable grid on which optimal strategies must lie, and this testifies to the flexibility of the method we propose.

We also show that very efficient algorithms can be defined which generate approximations to the exact optimal investment policies and value functions if one is willing to allow small errors. These errors can be guaranteed to stay smaller than an a priori specified error tolerance. The use of functions that are piecewise linear and thus characterized by their singular points to determine exact and approximate solutions has been used before in the context of option pricing, see [5].

To illustrate the working of the algorithm, we define discretized versions of the equity models mentioned above and approximate the corresponding risk preferences using members of our specific class of utility functions. This allows us to reproduce the optimal strategies derived for these very special cases with a very high accuracy. However, we believe that our method is particularly useful in cases where no closed-form strategies for the continuous-time version of the investment problem are known, or when one wants to study the optimal behaviour of investors with non-differentiable preferences in a discrete time setting.

The structure of the paper is as follows. In the following section we define the asset price dynamics and non-differentiable preferences that together characterize our optimal investment problem. In Section 3 we prove the main results of the paper and Section 4 then applies our algorithm in a number of illustrative cases. We draw conclusions and discuss possible extensions of our method in the last Section.

2 The Optimization Problem

In this section we specify our model and introduce our main assumptions, which concern the behaviour of risky assets and the risk preferences of the investor. Asset price dynamics are considered on a finite horizon in discrete time and must be Markovian. Asset prices are restricted to lie on a lattice in which every price has two possible successor price values one time step later111This binomial assumption could be extended to, for example, a trinomial specification but since every trinomial step can be described by two recombining binomial steps we restrict ourselves to the binomial case.. Investors’ preferences must correspond to a utility function which is a member of a particular set of functions, which we call class .

2.1 Optimal Investment in Risky Assets

We define for a given maturity and tree size a binomial tree

with the number of possible asset values at timestep , , and functions and which describe possible transitions of the risky asset in terms of rates of return, and which should satisfy

for all and . We take and define the riskfree return and require that for all . The probability that a transition from to will take place is denoted by and the transition to thus has probability . The mean rate of return for the riskfree rate is defined by

and the riskneutral probabilities for this economy are the ones which satisfy

so

The functions , , , and need to be specified in our setup, and then and follow from the previous equations. The well know standard binomial tree model introduced by Cox, Ross and Rubinstein [4] corresponds to choosing

in this specification.

In this economy we will aim to maximize expected utility over a a set of allowed investment strategies which must be in the set of all processes which are a function of times on the tree and a given vector state process (with ) which may contain, besides the current stock price and current wealth , other information known at time which is collected in the vector . This vector may be empty or contain additional observable information; we will treat, for example, the case of stochastic volatility or an untradeable process in later sections. The functions map to and have the interpretation of the value of the wealth that is invested in the risky asset .

For a given utility function on the real line (i.e. a function which is increasing and concave) we define the optimization problem

| (1) |

subject to

| (2) |

where is the Markov chain we defined above on our tree , and with given.

2.2 Non-differentiable Preferences

We will always assume that the utility function of our investment problem (1) is in a class of functions on the real line ( defined below.

Defintion 1

The class consists of functions such that

1. is piecewise linear with a finite number of points where it is not differentiable,

2. is concave, and

3. there exists an such that is constant for .

It immediately follows that any is continuous on its entire domain and that both its right-hand side derivative and lefthand-side derivative exist. Since the derivative equals zero for large enough values and can only decrease, functions in are increasing. By concavity, the right-hand side derivative must always be equal or smaller than the left-hand side derivative and we call the finite set of unique, (increasingly) ordered points where these two derivatives are unequal, i.e. where , the set of singular values, denoted by , see [5]. A function is uniquely characterized by its singular values, the values in its singular values and its left-hand side derivative at the smallest singular value, .

Lemma 1

Assume and let for .

-

(i)

For we have that are in and so is with the first singular value of .

-

(ii)

Assume that and and define . The set is a non-empty compact interval in (which may consist of a single point).

Proof. The first statement of (i) is immediate. The function is concave if is, and adding makes the function constant for large enough. For (ii) we first notice that goes to for and for and is continuous on which implies that it attains a maximal value on . The set is bounded and closed. Since is concave this set must be an interval.

3 Main Results

The combination of the asset price properties and risk preferences defined above will now allow us to prove a number of results which lead to an explicit characterization of the optimal investment policies.

3.1 Dynamic Programming

The Dynamic Programming Principle (See for example [1]) gives a backward recursion for the value function for our optimization problem in the state at a time on the tree. For the problems we consider in this paper, we will be able to represent the value function

using a function of wealth which is in for every value of the rest of the state vector. In this section, for example, we use a state and we will write for its value in such states. We use the notation for the smallest value which makes the strategy defined by optimal.

This implies, by (2) and the the Dynamic Programming Principle, that

with

| (3) | |||||

The functions and are defined for every . We must have that for every which means that the value function is of class in all nodes at the final time . We will show in this section that this property is inherited by the value function in all earlier states at all earlier times. We do this by assuming that for any given , both and are in this class, and by proving that the same holds for . To lighten notation we will from now on suppress the dependency on for the functions and and the time dependence of when no confusion can arise. The expression for then becomes, for example,

| (4) | |||||

To prove that the properties of value functions in class are preserved when applying the dynamic programming equations, we denote by , and , the singular values of and , respectively. We also set , . We see from (4) that it will be useful to characterize the points where equals a singular value for or where equals a singular value for . We will call this subset of the grid . We thus define on the sets

and the grid for

| (5) | |||||

| (6) |

To give unique coordinates to every point of the grid we also define:

In the next lemmas, we take to be any point in .

Lemma 2

For every , is concave, and for every , is concave. For both these functions the derivative strictly decreases at an intersection with the grid, i.e. when .

Proof. In both cases the functions are sum of compositions of a concave piecewise linear function and a linear function. Such a composition returns a concave piecewise linear function. An intersection with the grid means that is in for certain or in for certain (or both). This means that the derivative of or strictly decreases by the definition of singular value, while the other derivative must either stay constant or decrease as well.

In the next lemma we show that if is a point which maximizes for a certain and does not lie on the grid, then the function is constant in in the closure of the parallelogram to which belongs. Moreover, for this no other optimal points exist outside .

Lemma 3

If then for all and all .

Proof. The function is linear on , since it is the sum of two compositions of linear functions with (fixed) linear functions as long as we stay in . If is an internal maximum of the function for the fixed value of , the function must be constant for all such that . Since the derivative of strictly decreases when and using part (ii) of Lemma 1 shows that there can be no optimal points outside .

Lemma 4

The optimal trajectory is a subset of and contains .

Proof. By Lemma 3, if an optimal point is not on but in a parallelogram , then all points of which have the same value of are optimal and no points outside are optimal for that . Since is defined as the minimum of all optimal points for a given , we must have that .

The parallelogram contains wealth values beyond the last intersection point on the grid , so the function is constant on . This implies, by Lemma 2, that every point in is optimal. For values of beyond the last intersection point we may thus conclude that that .

Lemma 5

For all , the functions and are continuous on their domain .

Proof. Let . By Lemma 3, must222We use the notation for the function here to lighten notation. be on the grid . Suppose that there exists an such that for all , is constant and . Since is linear in on , the function must also be constant for all values and such that , and it must attain smaller values than this constant for points outside . By the definition of as the minimum of all possible optimal points for a fixed , we conclude that all points on the two lower sides of are optimal points . This proves the continuity of at the point .

Assume now that is the unique maximum of . Let be a sequence converging to and set . We know that the optimal points must be on the grid and that the grid is formed by a finite number of lines which are not vertical. Therefore the sequence must be bounded. Passing to a subsequence if necessary we can assume that converges to a value , so converges to . To prove continuity of in , we must show that .

Since is continuous, there must exist for any given a such that for . Assume for ; for such we have, by the optimality of , that . Taking the limit and using that is continuous since its a composition of continuous functions, we conclude that but by definition of the function we also have that . This implies . Since the optimal point corresponding to is unique we get and this proves the continuity of at .

The continuity of then implies the continuity of .

Lemma 6

For all , the function is concave on its domain .

Proof. The function moves continuously on the grid by Lemmas 3 and 5 and is linear between two intersections of grid lines. We therefore only need to establish concavity at points where is on such an intersection, since in all other points, is the sum of two compositions of concave functions with (fixed) linear functions and therefore concave.

Let be a value which corresponds to a point of intersection: for some and . In order to establish the concavity of in , we compute the left-hand side and right-hand side derivatives of at this point.

If is larger than but close enough to we must have that or which means that equals or respectively, by (5) and (6). From (4) we know that

and we notice that the first term on the right-hand side is constant for while the second term is constant for . Thus allows us to conclude that in , the right-hand side derivative equals either in the first case or in the second case. Since we chose the optimal strategy, it should equal the maximum of the two:

| (7) |

To find the left-hand side derivative, we consider values of that are smaller than but close enough to . Again, we must have that equals or and by again calculating the value of for these two possibilities and now choosing the smallest of the two, we find:

| (8) |

We must now show that by comparing the right-hand sides of (7) and (8) to finish the proof.

This can be established by the optimality condition for our choice of . Since this choice was determined by maximizing the piecewise linear function we must have that and at least one of the inequalities must be strict. Since

we have

with at least one of the two inequalities strict. But we also have that

by concavity of and . Using these four inequalities to compare the right-hand sides of (7) and (8), we establish that holds and this finishes the proof.

Theorem 1

We have .

Proof. We check the properties of Definition 1 for : piecewise linearity and differentiability outside a finite set follow from the fact that for all , the fact that is linear for points in where is not in the subset of of intersection points , and the fact that the set of intersections is finite. That is concave was shown in Lemma 5. The fact that eventually becomes constant follows from Lemma 4, since it is shown there that for large enough . This is because is constant on , since it is a linear combination of the functions and which are evaluated in points beyond their last singular value, where they are constant.

From the proofs of the Theorem and the Lemmas preceding it, we can now easily derive an algorithm to determine the value functions and optimal investment strategy in every state on the tree.

Corollary 1

Assume that and have singular values and respectively, and let

Then , the singular values of in reverse order, its values in these points, the optimal strategies and the left-hand side derivatives satisfy, for ,

| (9) |

with , , , and . The sequence of singular values in reverse order stops when either or for certain .

Proof. We know that the points must take the form since they must be on the grid by Lemma 4 and the derivative of should not be continuous in the points so they must be on the intersections of the grid. We also have by Lemma 4 that the line is in so the intersection point on the grid with the highest wealth value must be , by the continuity of . This gives the first singular values in reverse order, so and and . Direct calculation shows that intersection points on the grid are given by

so we are done when we prove that . But this follows from (8).

3.2 Reducing the Number of Singular Values

The technique for obtaining the value function in every point of the tree gives exact results but it is computationally expensive since at every time step the number of singular values doubles in every node. However, by using a method introduced in [1], we can reduce the number of points involved in the calculations. This generates an approximation for the value function that can be calculated faster, while keeping the approximation errors within explicit bounds that we can specify a priori.

The idea is to remove some singular values at every step in order to simplify the computation of the value function, while controlling the error generated by such an elimination procedure. We fix a given maximal level of the error and we modify every value functions immediately after it has been calculated, and hence before it is used in calculations for the subsequent time step, by deleting singular values. We do this in such a way that the new value functions differ at most from on their whole domain.

More precisely, to construct an approximation for the function that has singular values , , and corresponding values , we delete singular values in the following way. We set for and starting from , we try to find the largest singular value for which the distance in the interval , between the straight line connecting with and the graph of the function is less than : this means that we define the set

and set if this set is empty and if it is not empty.

Notice that the distance between and the straight line through and increases as increases, by virtue of the concavity of . After we have determined , we delete all the points and we repeat the procedure for the next value of . We continue until the penultimate singular value is reached. We do not modify the function before the first and after the last singular value.

Using this procedure we obtain a new value function which is again in the class but with a reduced number of singular values and which differs from less than on its whole domain. Since we have that, for every :

implies that the new value function in will be

Using a simular argument we find that and hence we have that for all .

The optimal strategy for wealth that is obtained after replacing and by and , respectively, can be different from the case where no substitutions have been made, but the value that it generates differs or less from the original value .

3.3 Extending the number of Risk Factors

We now consider the case where there is another risk factor, , which is not tradeable, but which may influence the terminal value of a contingent claim which is deducted from the final wealth.

We therefore now define a multi-nomial tree with nodes that are characterized by with still representing the stock value for a stock that can be traded, and a factor which cannot be traded but may be correlated to or drive the dynamics of (while still leading to two different return values at every step) such as the stochastic volatility in a Heston Model.

We now have

| (10) |

The dynamics for the risky asset remain as defined earlier, but the values of may have a different structure.

At every time step the nodes that can be reached from are , , and , with probabilities , , and respectively333As before we suppress some notation; for example, is short for and an abbreviation of etcetera. Notice that is itself shorthand notation for the probability that both and attain the ”upper” values of their two possibilities in the next time step.. We assume that is a riskfactor that cannot be traded, so we still only allow investment in stock and cash.

In this section, our state is and we will write and for the smallest value which makes the strategy defined by

optimal.

This implies that

with

| (11) |

We define and and write

for functions

These two functions are in and they have singular values and which can be found by combining the singular values of and and by combining those of and respectively. The corresponding values and can easily be determined by summing the corresponding values of the constituting functions. We are then back in the situation of Theorem 1 since we can then write

for functions and which are both in . This means that we can use the algorithm described in Corollary 1 to calculate the value function in each point of the tree.

This construction shows that we can treat the case where the stock dynamics depends on an untradeable factor. We now show how this can be exploited to treat an optimal portfolio problem which involves the stochastic volatility model for equity prices that was proposed by Heston [6]. In that model, the squared volatility process and log stock price process are assumed to satisfy the stochastic differential equations

| (12) | |||||

| (13) |

for given , where are correlated standard Brownian Motion processes with correlation coefficient , and , , , and are strictly positive constants.

We now define the stochastic processes , at times as the discrete counterpart to the continuous time process :

| (14) | |||||

where the variables are i.i.d. distributed in , with444Notice that we have taken the positive part of the variance process to ensure positivity of this process. This choice corresponds to the full truncation scheme of Lord et al. in [8].

This generates a tree which is not recombining, and we therefore modify it as follows. Let and define , and analogously. We take and for certain which describe how fine the mesh is that we will take, and then define the set of tree nodes in (10) using and .

A node on the tree, which represents the state of our dynamic process, must have the form for some , and . From this state, transitions are possible to four possible new states of the form for where

This will in general not give a new state of the form for certain and , because the tree is not recombining. But in [11] it is shown that weak convergence of the process on the tree to its counterpart in continuous time will still be guaranteed if we use, in each of these four points, linear interpolation based on the four points on the grid with the smallest distance to the intended location. We follow this approach here as well and therefore determine and such that

for and use the linear combination

| (15) |

with linear interpolation weights

The weights can be interpreted as new probabilities , since the four different transitions from the current state are each divided over four future states each, to create sixteen transitions in total. On our tree, we implement this by simply taking a linear combination of four value functions in class , since this results in a function which is again in class , and this function can be determined very efficiently using the associated set of singular values. Figure 2 illustrates the construction: four transitions to points which may not be on the grid are replaced by sixteen transitions which are on the grid and since the weights are positive and sum to one, these can be interpreted as a new set of probabilities on the tree.

We now write (11), using (15), as

where

The two functions and are in and they have singular values which can be found by combining the singular values of the functions

of which they are a linear combination. We are then back in the situation of Theorem 1 and the algorithm in Corollary 1 can be applied.

4 Numerical Examples

We now apply our method to a set of different investment and indifference pricing problems in both complete and incomplete markets.

4.1 Optimal Portfolio Choice

In our first numerical example we calculate the optimal strategy and optimal value function for an investor in a Black-Scholes economy with bonds, which earn a constant rate of return per unit of time, and stocks with a constant mean rate of return and volatility . We consider an investment horizon of (year) and use the standard binomial tree with time steps , so , and are all constant over time. We take , and , unless otherwise specified.

4.1.1 Constant Relative Risk Aversion Case

We first consider the utility function

| (16) |

with constant relative risk aversion (CRRA), for .

If we take small time steps, the value function in our discrete time setup around the initial wealth value and initial stock value , i.e. , should be close to to the continuous time limit value function derived by Merton [9]. That value function, and the corresponding optimal investment strategy, are

We represent the utility function for terminal wealth using an approximating function which is in class , by defining equidistant singular points on the interval . We used initial singular points, time steps.

Results are shown in Figure 3. The red lines correspond to the optimal strategy in the continuous time limit, as derived by Merton, and the blue lines show the results of our algorithm. We note that the value functions are very close, even though the optimal strategies show a rather different behaviour.

4.1.2 Constant Absolute Risk Aversion Case

In a similar way, we analyze exponential preferences, which correspond to constant absolute, instead of relative, risk aversion. This means that and

We keep the other parameters the same as in the previous subsection.

Results for this case are shown in Figure 4.

4.2 Indifference Pricing in a Complete Market

We can use either the CARA or the CRRA utility function to check the price of vanilla derivatives in the complete market that is generated by our stock price tree and the riskfree asset. As mentioned in the introduction, the utility indifference price at time zero of a European option with payoff at a date is the solution to the equation where and are value functions with and respectively. This means that we assign the same value today to an amount of wealth without a derivative as to a position where we know that we have to pay the payoff at the maturity date , but get compensated for this by receiving the price to add to our current wealth .

In a complete market such as the Cox-Ross-Rubinstein (CRR) model we consider here, we can create a separate portfolio with stocks and bonds which perfectly replicates the payoff and which has an initial price that equals the CRR value of the option. This means that must equal this value, since there is a perfect separation between stock and bonds investments that we use to pay off the option and stocks an bonds that we use to create a portfolio which optimizes the utility function of the rest of the wealth . Showing that the utility indifference price equals the CRR price thus requires that our algorithm generates the nonlinear optimal investment in stocks that will now be needed, which is known as . The value of can be calculated from as

which, in our complete market, should be the same for all values of . The corresponding initial , i.e. the number of stocks that we will invest in to replicate the payoff of a single option, can be found by

and should also not depend on .

As an example, we take put options with maturity and strike prices between and , while the current stock price equals . The results in Figure 5 for the Exponential Utility Indifference Prices and Deltas show excellent agreement with the corresponding CRR values. We found equally good agreement for other utility functions.

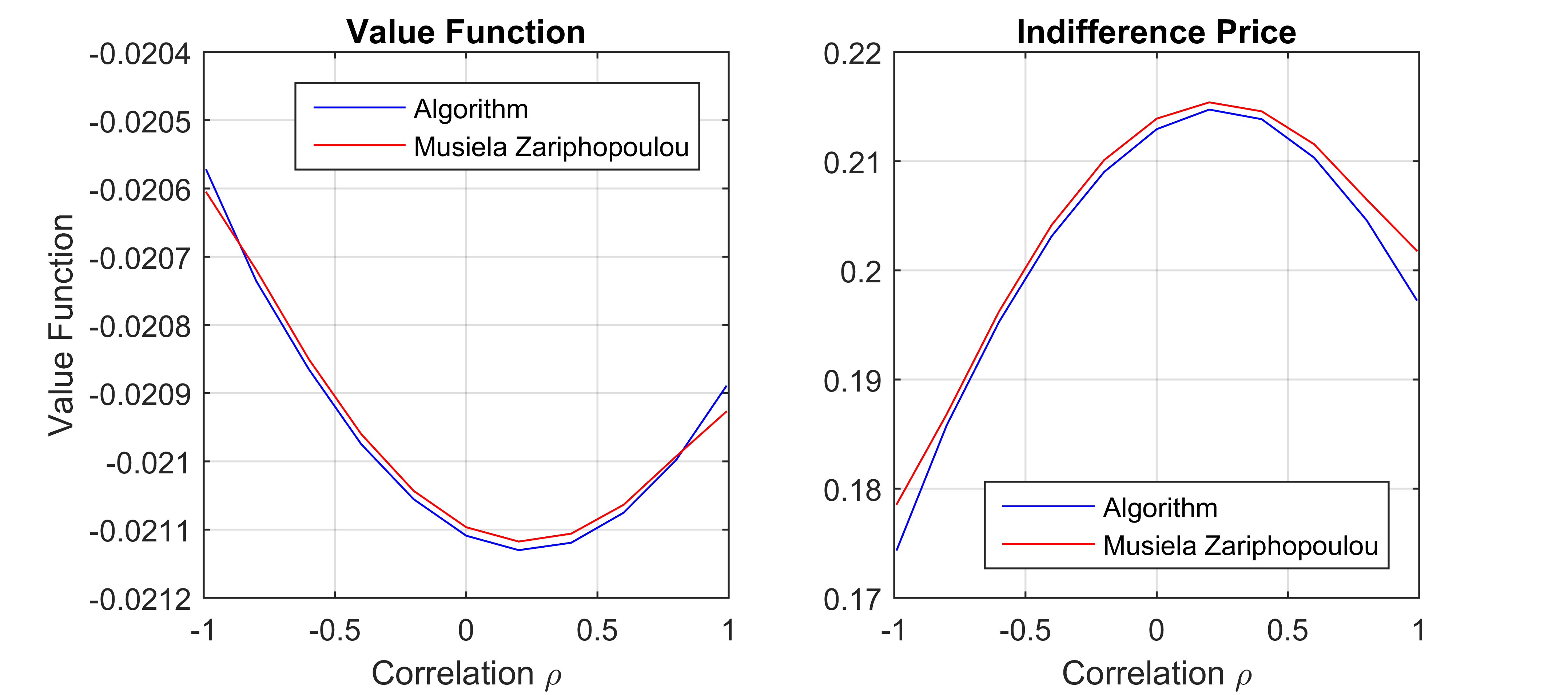

4.3 Indifference Pricing in an Incomplete Market

We now turn to an example where the market is incomplete. Since this means that no perfect riskless replication is possible, there is no universal price for derivatives: the utility indifference price that any agent would agree to pay for a certain future payoff will now depend on his or her risk preferences.

We use the economy introduced by Zariphopoulou and Musiela model in [10], with a tradeable stock and another price process which is correlated but untradeable:

with . They derive an explicit expression for the utility indifference price at time zero for a payoff at a future time under constant absolute risk aversion preferences and zero interest rate. This price equals

| (17) |

In our discrete time version of this model, we used the same parameters for the economy as before, but zero interest rates, and determine the price of a times a put option with strike . We find for singular points and timesteps the results in figure 6, which are compared to the theoretical value which is found using Monte Carlo simulations based on (17).

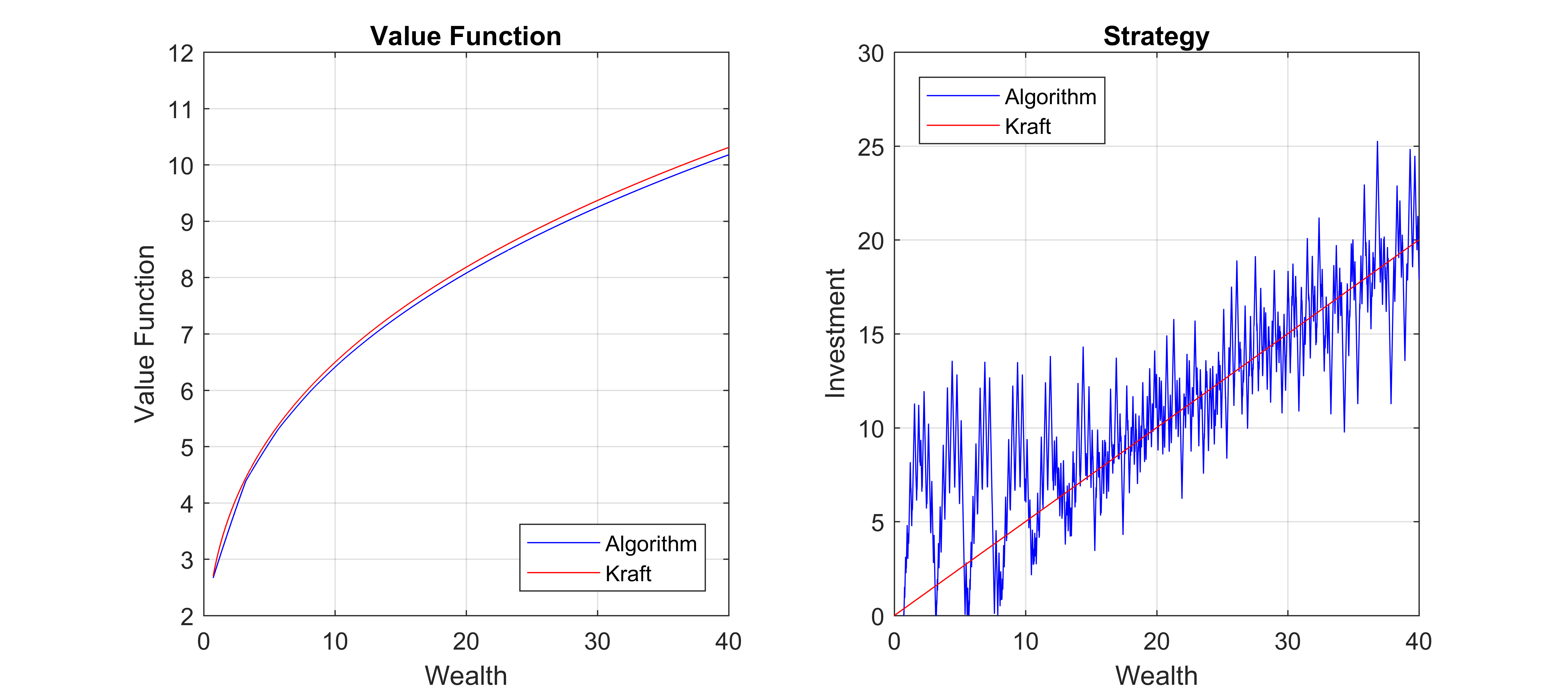

4.4 Optimal Investment under Stochastic Volatility

In a paper by Kraft [7] explicit forms are given for the optimal investment strategy in Heston’s stochastic volatility model. When in (13) for a given the optimal investment strategy for power utility (16) equals

with

For the parameter values , , maturity , correlation , volatility of volatility , mean reversion and level we find the figures below for the optimal strategy at different points in time.

We used risk aversion parameter and market price of volatility risk parameter . The graphs in Figure 7 were calculated with time steps, gridpoints in the (log) stock price direction and in the (squared) volatility direction. We used singular points to start with. We show the results halfway the time to maturity i.e. for in the middle of the grid. Other points for gave equally good results.

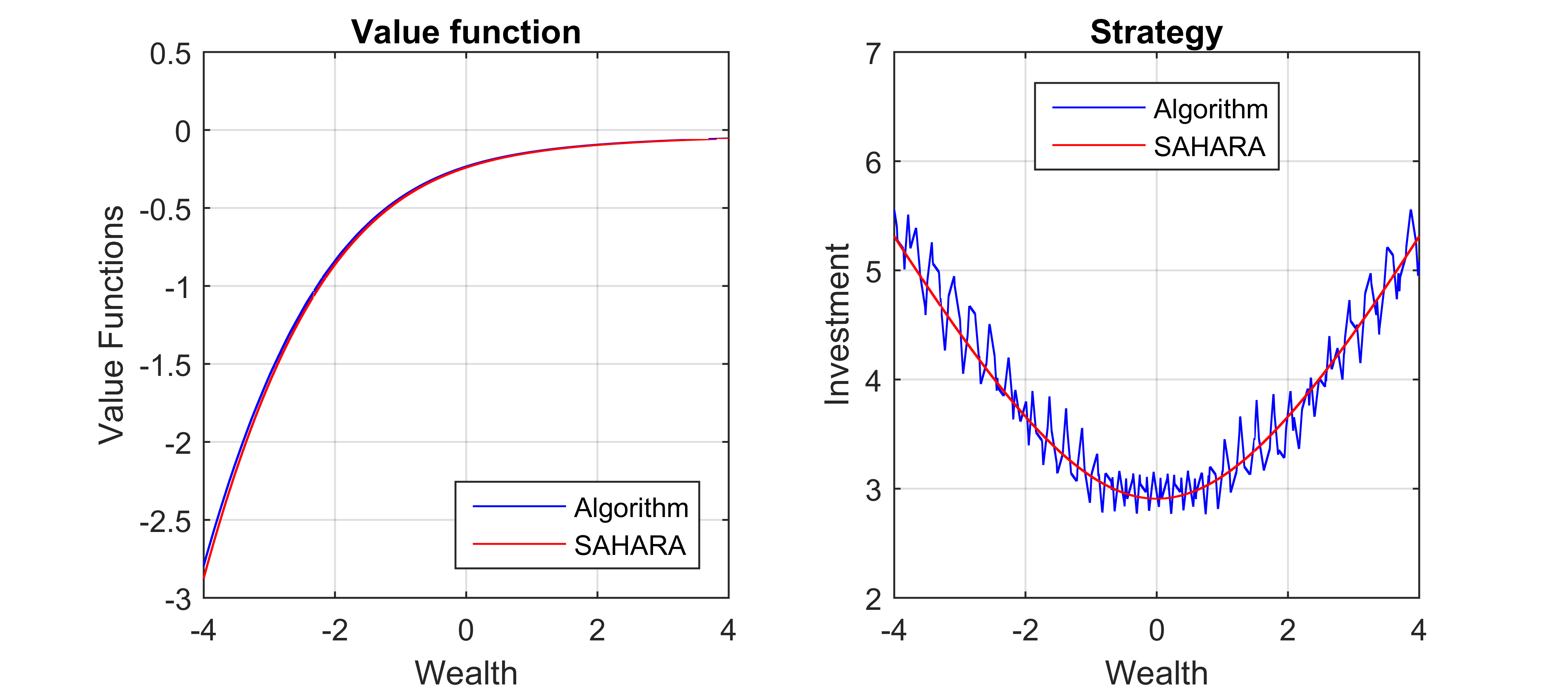

4.5 An Example of Nonlinear Optimal Policies

In the examples that we have treated so far, closed-form solutions were available for the optimal investment policies. These always took the shape of a linear function of current wealth. We now show that our algorithm can also accurately represent a more complicated strategy, which is optimal for the class of Symmetrically Adjusted Hyperbolic Absolute Risk Aversion preferences (SAHARA). Such preferences are characterized by the utility function

where is a risk aversion parameter unequal to one555Another member of this family of utility functions can be found by taking the limit but we will not consider that case here. and a scaling parameter. Under the Black-Scholes dynamics introduced earlier, the optimal strategy turns out to be [3]

The corresponding value function satisfies so it has the same functional form as the terminal value but with a different, time-dependent scaling parameter.

Figure 8 shows the result of a calculation with 75 singular points and 20 time steps for and . The Black-Scholes economy parameters were left unchanged from earlier cases. We find again excellent agreement, both for the value function and the optimal strategy, even though the latter is not linear for this specification.

5 Conclusions and Further Research

We have shown how discrete time optimal investment and indifference pricing problems for asset prices on trees can be solved exactly if one assumed that the utility function which describes the investor’s preferences is assumed to be piecewise linear. We used this to reproduce accurate approximations for some well-known examples of such problems for which closed-form solutions have been derived in the literature. However, we believe that our approach will be particularly useful if it can be utilized for cases where the solution is unknown. This is for example the case when preferences are not know in parametric form, but have to be approximated based on empirical evidence which is based on a limited number of experiments. When the detailed behaviour of the utility function is not known but its general shape is know, our method can be used to calculate optimal investment strategies based on a crude piecewise linear approximation.

We also note that it is very easy in our framework to incorporate state-dependent payments which lead to a change of wealth, since such a payment can simply be represented by a horizontal shift of the value function.

There is a number of extensions of this work that may be interesting. In this paper we restrict ourselves to the case where multiple risk factors may influence our single risky asset, but we do not treat the case where investment in more than one risky asset is possible. Introducing this possibility will introduce more sets of parallel lines when defining the grid that must contain the optimal investment strategy, which clearly complicates the analysis and the design of efficient algorithms. We hope to address this issue in subsequent work.

References

- [1] Dimitri P. Bertsekas and Steven E. Shreve. Stochastic Optimal Control: The Discrete-Time Case. Athena Scientific, 2007.

- [2] F. Black and M. Scholes. The pricing of options and corporate liabilities. J. of Political Economy, 81:637–654, 1973.

- [3] A. Chen, A.A.J. Pelsser, and M.H. Vellekoop. Modeling non-monotone risk aversion using SAHARA utility functions. Journal of Economic Theory, 146(5):2075 – 2092, 2011.

- [4] J.C. Cox, S.A. Ross, and M. Rubinstein. Option pricing: a simplified approach. Journal of Financial Economics, 7:229–263, 1979.

- [5] M. Gaudenzi, M.A Lepellere, and A . Zanette. The singular points method for pricing American path-dependent options. Journal of Computational Finance, 14:1460–1559, 2010.

- [6] S. Heston. A closed-form solution for options with stochastic volatility with applications to bond and currency options. Review of Financial Studies, 6:327–343, 1993.

- [7] H. Kraft. Optimal portfolios and Heston’s stochastic volatility model: an explicit solution for power utility. Quantitative Finance, 5:303–313, 2005.

- [8] R. Lord, R. Koekkoek, and D. Van Dijk. A comparison of biased simulation schemes for stochastic volatility models. Quantitative Finance, 10(2):177–194, 2010.

- [9] R.C. Merton. Lifetime portfolio selection under uncertainty: the continuous-time case. Rev. Econom. statist., 51(3):247–257, 1969.

- [10] M. Musiela and T. Zariphopoulou. An example of indifference prices under exponential preferences. Finance and Stochastics, 8(2):229–239, 2004.

- [11] M.H. Vellekoop and J.W. Nieuwenhuis. A tree-based method to price American options in the Heston model. Journal of Computational Finance, 13(1):1–21, 2009.