Statistical dependence: Beyond Pearson’s 111This work has been partly supported by the Finance Market Fund, grant number 261570

Abstract

Pearson’s is the most used measure of statistical dependence. It gives a complete characterization of dependence in the Gaussian case, and it also works well in some non-Gaussian situations. It is well known, however, that it has a number of shortcomings; in particular for heavy tailed distributions and in nonlinear situations, where it may produce misleading, and even disastrous results. In recent years a number of alternatives have been proposed. In this paper, we will survey these developments, especially results obtained in the last couple of decades. Among measures discussed are the copula, distribution-based measures, the distance covariance, the HSIC measure popular in machine learning, and finally the local Gaussian correlation, which is a local version of Pearson’s . Throughout we put the emphasis on conceptual developments and a comparison of these. We point out relevant references to technical details as well as comparative empirical and simulated experiments. There is a broad selection of references under each topic treated.

1 Introduction

Pearson’s , the product moment correlation, was not invented by Pearson, but rather by Francis Galton. Galton, a cousin of Charles Darwin, needed a measure of association in his hereditary studies, Galton (1888; 1890). This was formulated in a scatter diagram and regression context, and he chose (for regression) as the symbol for his measure of association. Pearson (1896) gave a more precise mathematical development and used as a symbol for the population value and for its estimated value. The product moment correlation is now universally referred to as Pearson’s . Galton died in 1911, and Karl Pearson became his biographer, resulting in a massive 4-volume biography, Pearson (1922; 1930). All of this and much more is detailed in Stigler (1989) and Stanton (2001). Some other relevant historical references are Fisher (1915; 1921), von Neumann (1941; 1942) and the survey paper by King (1987).

Write the covariance between two random variables and having finite second moments as . The Pearson’s , or the product moment correlation, is defined by

with being the standard deviation of and similarly for . The correlation takes values between and including and . For a given set of pairs of observations of and , an estimate of is given by

| (1) |

with , and similarly for . Consistency and asymptotic normality can be proved using an appropriate law of large numbers and a central limit theorem, respectively.

The correlation coefficient has been, and probably still is, the most used measure for statistical association. There are several reasons for this.

-

(i)

It is easy to compute (estimate), and it is generally accepted as the measure of dependence, not only in statistics, but in most applications of statistics to the natural and social sciences.

-

(ii)

Linear models are much used, and in a linear regression model of on , say, is proportional to the slope of the regression line. More precisely; if where is a sequence of zero-mean iid error terms whose second moment exists, then

This also means that and its estimate appears naturally in a linear least squares analysis

-

(iii)

In a bivariate Gaussian density

the dependence between and is completely characterized by . In particular, two jointly Gaussian variables are independent if and only if they are uncorrelated (See e.g. Billingsley (2008, 384–85) for a formal proof of this statement). For a considerable number of data sets, the Gaussian distribution works at least as a fairly good approximation. Moreover, joint asymptotic normality often appears as a consequence of the central limit theorem for many statistics, and the joint asymptotic behavior of such statistics are therefore generally well defined by the correlation coefficient.

-

(iv)

The product moment correlation is easily generalized to the multivariate case. For stochastic variables , their joint dependencies can simply (but not always accurately) be characterized by their covariance matrix , with being the covariance between and . Similarly the correlation matrix is defined by , with being the correlation between and . Again, for a column vector , the joint normality density is defined by

where is the determinant of the covariance matrix (whose inverse is assumed to exist), and . Then the complete dependence structure of the Gaussian vector is given by the pairwise covariances , or equivalently the pairwise correlations . This is remarkable: the entire dependence structure is determined by pairwise dependencies. We will make good use of this fact later when we get to the local Gaussian dependence measure in Section 6.

-

(v)

It is easy to extend the correlation concept to time series. For a time series , the autocovariance and autocorrelation function, respectively, are defined, assuming stationarity and existence of second moments, by and for arbitrary integers and . For a Gaussian time series, the dependence structure is completely determined by . For linear (say ARMA) type series the analysis as a rule is based on the autocovariance function, even though the entire joint probability structure cannot be captured by this in the non-Gaussian case. Even for nonlinear time series and nonlinear regression models the autocovariance function has often been made to play a major role. In the frequency domain all of the traditional spectral analysis is based again on the autocovariance function. Similar considerations have been made in spatial models such as in linear Kriging models, see Stein (1999).

In spite of these assets, there are several serious weaknesses of Pearson’s . These will be briefly reviewed in Section 2. In the remaining sections of this paper a number of alternative dependence measures going beyond the Pearson will be described. The emphasis will be on concepts, conceptual developments and comparisons of these. We do provide some illustrative plots of key properties, but when it comes to technical details, empirical and simulated experiments with numerical comparisons, we point out relevant references instead.

2 Weaknesses of Pearson’s

We have subsumed, somewhat arbitrarily, the problems of Pearson’s under three issues:

2.1 The non-Gaussianity issue

A natural question to ask is whether the close connection between Gaussianity and correlation/covariance properties can be extended to larger classes of distributions. The answer to this question is a conditional yes. The multivariate Gaussian distribution is a member of the vastly larger class of elliptical distributions. That class of distributions is defined both for discrete and continuous variables, but we limit ourselves to the continuous case. An elliptical distribution can be defined in terms of a parametric representation of the characteristic function or the density function. For our purposes it is simplest to phrase this in terms of a density function.

Consider a stochastic vector and a non-negative Lebesgue measurable function on such that

Further, let and let be a positive definite matrix, then an elliptical density function parameterized by , and is given by

| (2) |

where is a normalizing factor given by

The parameters and can be interpreted as location and scale parameters, respectively, but they cannot in general be identified with the mean and covariance matrix . In fact the parameters and in equation (2) may remain meaningful even if the mean and the covariance matrix do not exist. If they do exist, can be identified with the mean, and is proportional to the covariance matrix, the proportionality factor in general depending on . A redefinition of may then make this proportionality factor equal to 1, cf. Gómez, Gómez-Villegas, and Mari’in (2003) and Landsman and Valdez (2003).

A number of additional properties of elliptical distributions, among other things pertaining to linear transformations, marginal distributions and conditional distributions are surveyed in Gómez, Gómez-Villegas, and Mari’in (2003) and Landsman and Valdez (2003). Many of these properties are analogous to those of the multivariate normal distribution, which is an elliptical distribution defined by .

Unfortunately, the equivalence between uncorrelatedness and independence is generally not true for elliptical distributions. Consider for instance the multivariate -distribution with degrees of freedom

| (3) |

Unlike the multinormal distribution where the exponential form of the distribution forces the distribution to factor if is a diagonal matrix (uncorrelatedness), this is not true for the distribution defined in equation (3) if is diagonal. In other words, if two components of a bivariate distribution are uncorrelated, they are not necessarily independent. This pinpoints a serious deficiency of the Pearson’s in measuring dependence in distributions, and indeed in general elliptical (and of course non-elliptical) distributions.

2.2 The robustness issue

As is the case for regression, it is well known that the product moment estimator is sensitive to outliers. Even just one single outlier may be very damaging. There are therefore several robustified versions of , primarily based on ranks. The idea of rank correlation goes back at least to Spearman (1904), and it is most easily explained through its sample version. Given scalar observations , we denote by the rank of among . (There are various rules for treating ties). The estimated Spearman rank correlation function given pairwise observations of two random variables and is given by

If and have continuous cumulative distribution functions and , and joint distribution function , then the population value of the Spearman’s is given by

| (4) |

and hence it is a linear transformation of the correlation between the two uniform variables and . The rank correlation is thought to be especially effective in picking up linear trends in the data, but it suffers in a very similar way as the Pearson’s to certain nonlinearities of the data which are treated in the next subsection. Spearman’s may be modified to a rank autocorrelation measure for time series in the obvious way, see Knoke (1977), Bartels (1982), Hallin and Mélard (1988), and Ferguson, Genest, and Hallin (2000).

Another way of using the ranks is the Kendall’s rank correlation coefficient given by Kendall (1938). Again, consider the situation of pairs of the random variables and . Two pairs of observations and , are said to be concordant if the ranks for both elements agree; that is, if both and or if both and . Similarly, they are said to be discordant if and or if and . If one has equality, they are neither concordant nor discordant, even though there are various rules for treating ties in this case as well. The estimated Kendall is then given by

The population value can be shown to be

| (5) |

Both and are expressible in terms of the copula (see Section 3) associated with . It is then perhaps not surprising that both and are bivariate measures of monotone dependence. This means that (i) they are invariant with respect to strictly increasing (decreasing) transformations of both variables, and (ii) they are equal to (or ) if one of the variables is an increasing (or decreasing) transformation of the other one. Property (i) does not hold for Pearson’s , and is not directly expressible in terms of the copula of either. The invariance property (i) is also shared by the van der Waerden (1952) correlation based on normal scores. Some will argue that this invariance property make them more desirable as dependence measures in case and are non-Gaussian.

The asymptotic normality of the Spearman’s and Kendall’s was established early. Some of the theory is reviewed in Kendall (1970). It can be viewed as special cases of much more general results obtained by Hallin, Ingenbleek, and Puri (1985) and Ferguson, Genest, and Hallin (2000). For some details in the time series case we refer to Tjøstheim (1996). A more recent account from the copula point of view is given by Genest and Rémillard (2004). They show in Section 3 of their paper that serialized and non-serialized versions of Spearman’s and other linear rank statistics share the same limiting distribution.

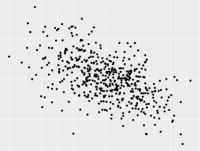

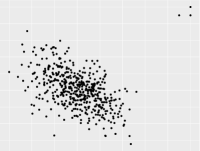

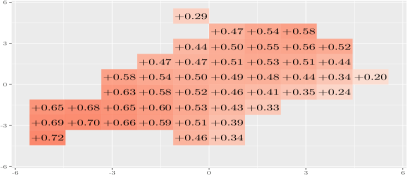

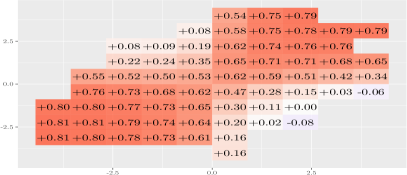

We will illustrate the robustness issue using a simple example. In Figure 1a we see 500 observations that have been simulated from the bivariate Gaussian distribution having correlation . The sample value for Pearson’s is . If we add just three outliers to the data, however, as shown in Figure 1b, the sample correlation changes to . The sample versions of Spearman’s for the simulated data in Figures 1a and 1b are on the other hand very similar: and , and the corresponding values for the estimated Kendall’s are and .

2.3 The nonlinearity issue

This is probably the most serious issue with Pearson’s , and it is an issue also for the rank based correlations of Spearman and Kendall. All of these (and similar measures), are designed to detect rather specific types of statistical dependencies, namely those for which large values of tend to be associated with large values of , and small values of with small values of (positive dependence), or the opposite case of negative dependence in which large values of one variable tend to be associated with small values of the other variable. It is easy to find examples where this is not the case, but where nevertheless there is strong dependence. A standard introductory text book example is the case where

| (6) |

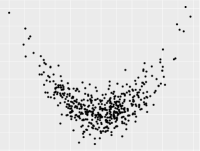

Here, is uniquely determined once is given; i.e., basically the strongest form of dependence one can have. If , however, it is trivial to show that , and moreover that and will also fail spectacularly. A version of this situation is illustrated in Figure 1c, where we have generated 500 observations of the standard normally distributed independent variables and , and calculated as . Still, . The sample values for Pearson’s , Spearman’s and Kendall’s are , and respectively, and none of them are significantly different from zero.

Essentially the same problem will occur if and , where and are independent of each other and independent of . It is trivial to show that if , whereas and are clearly dependent. This example typifies the kind of dependence one has in ARCH/GARCH time series models: If is a time series of zero-mean iid variables and if the time series is independent of , and and are given by the recursive relationship

| (7) |

where the stochastic process is the so-called volatility process, then the resulting model is a GARCH(1,1) model. Further, , and and are non-negative constants satisfying . This model can be extended in many ways and the ARCH/GARCH models are extremely important in finance. A recent book is Francq and Zakoian (2011). The work on these kind of models was initiated by Engle (1982), and he was awarded the Nobel prize for his work. The point as far as Pearson’s is concerned, is that and are uncorrelated for , but they are in fact strongly dependent through the volatility process , which can be taken to measure financial risk. This is probably the best known and most important model class where the dependence structure of the process is not at all revealed by the autocorreletion function. The variables are uncorrelated, but contain a dependence structure that is very important from an economic point of view.

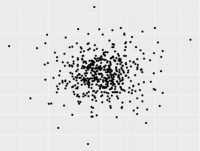

In Figure 1d we see some simulated data from a GARCH(1,1)-model with iid , , and , with on the horizontal axis, and on the vertical axis. In this particular case, , despite the strong serial dependence that is seen to exist directly from equation (7).

The nonlinearity issue will be analysed very extensively and quite systematically in the following sections, but there have also been various more ad hoc solutions to this problem. We will just mention briefly two of them here. Slightly more details are given in the survey paper Tjøstheim (1996), and much more details in the literature cited there.

-

(a)

Higher moments: An «obvious» ad hoc solution in the nonlinear GARCH case is to compute the product moment correlation on squares instead of themselves. It is easily seen that the squares are autocorrelated. This is the idea behind the McLeod and Li (1983) test. It requires the existence of 4th moments, though, which will not always be fulfilled for models of financial time series that typically have heavy tails, see e.g. Teräsvirta et al. (2010, Ch. 8).

-

(b)

Frequency based tests: These are also based on higher product moments, but in this instance one takes the Fourier transform of these to obtain the so-called bi-spectrum and tri-spectrum, on which in turn independence tests can be based (Subba Rao and Gabr 1980; Hinich 1982).

In the following sections we will look at ways of detecting nonlinear and non-Gaussian structures by going beyond Pearson’s .

3 Beyond Pearson’s : The copula

For two variables one may ask, why not just take the joint density function or the cumulative distribution function as a descriptor of the joint dependence? The answer is quite obvious. If a parametric density model is considered, it is usually quite difficult to give an interpretation of the parameters in terms of the strength of the dependence. An exception is the multivariate normal distribution of course, but even for elliptical distributions the «correlation» parameter is not, as we have seen, necessarily a good measure of dependence. If one looks at nonparametric estimates for multivariate density functions, to a certain degree one may get an informal indication of strength of dependence in certain regions from a display of the density, but the problems increase quickly with dimension due both to difficulties of producing a graphical display and to the lack of precision of the estimates due to the curse of dimensionality.

Another problem in analyzing a joint density function is that it may be difficult to disentangle effects due to the shape of marginal distributions and effects due to dependence among the variables involved. This last problem is resolved by the copula construction. Sklar’s (1959) theorem states that a multivariate cumulative distribution function with marginals , can be decomposed as

| (8) |

where is a distribution function over the unit cube . Klaassen and Wellner (1997) point out that Hoeffding (1940) had the basic idea of summarizing the dependence properties of a multivariate distribution by its associated copula, but he chose to define the corresponding function on the interval instead of on the interval . In the continuous case, is a function of uniform variables , using the well-known fact that for a continuous random variable , is uniform on [0,1]. Further, in the continuous case is uniquely determined by Sklar’s (1959) theorem.

The theorem continues to hold for discrete variables under certain weak regularity conditions securing uniqueness. We refer to Nelsen (1999) and Joe (2014) for extensive treatments of the copula. Joe (2014), in particular, contains a large section on copulas in the discrete case. See also Genest and Nešlehová (2007). For simplicity and in keeping with the assumptions in the rest of this paper we will mostly limit ourselves to the continuous case.

The decomposition (8) very effectively disentangle the distributional properties of a multivariate distribution into a dependence part measured by the copula C and a marginal part described by the univariate marginals. Note that is invariant with respect to one-to-one transformations of the marginal variables . In this respect it is analogous to the invariance of the Kendall and Spearman rank based correlation coefficients.

A representation in terms of uniform variables can be said to be in accord with a statistical principle that complicated models should preferably be represented in terms of the most simple variables possible, in this case uniform random variables. A possible disadvantage of the multivariate uniform distribution is that tail behavior of distributions may be difficult to discern on the uniform scale, as it may result in singular type behavior in the corners of the uniform distribution with accumulations of points there in a scatter diagram on or . It is therefore sometimes an advantage to change the scale to a standard normal scale, where the uniform scores are replaced by standard normal scores with being the cumulative distribution of the standard normal distribution. This leads to a more clear representation of tail properties. This scale is sometimes used in copula theory (see e.g. Joe (2014)), and we have used it systematically in our work on local Gaussian approximation described in Section 6.

The decomposition in (8) is very useful in that it leads to

large classes of models that can be specified by defining the marginals

and the copula function separately. It has great flexibility in that

very different models can be chosen for the marginal distribution, and

there is a large catalog of possible parametric models available for the

copula function ; it can also be estimated nonparametrically. The

simplest one is the Gaussian copula. It is constructed from a

multivariate Gaussian distribution with correlation

matrix . It is defined by

| (9) |

such that are standard normal variables for . It should be carefully noted that if one uses (9) in model building, one is still allowed to put in a marginal cumulative distribution functions of one’s own choice, resulting in a joint distribution that is not Gaussian. A multivariate Gaussian distribution with correlation matrix is obtained if the marginals are univariate Gaussians. If the marginals are not Gaussians the correlation matrix in the distribution obtained by (8) will not in general be . Klaassen and Wellner (1997) present an interesting optimality property of the normal scores rank correlation coefficient, the van der Waerden correlation, as an estimate of .

A similar construction taking as its departure the multivariate -distribution can be used to obtain a -copula.

A general family of copulas is the family of Archimedean copulas. It is useful because it can be defined in an arbitrary dimension with only one parameter belonging to some parameter space . A copula is called Archimedean if it has the representation

| (10) |

where is a continuous, strictly decreasing and convex function such that . Moreover, is a parameter within some parameter space . The function is called the generator function and is the pseudo inverse of . We refer to Joe (2014) and Nelsen (1999) for more details and added regularity conditions. In practice, copulas have been mostly used in the bivariate situation, in which case there are many special cases of the Archimedian copula (10), such as the Clayton, Gumbel and Frank copulas. In particular the Clayton copula has been important in economics and finance. It is defined by

| (11) |

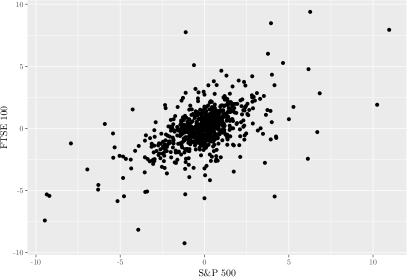

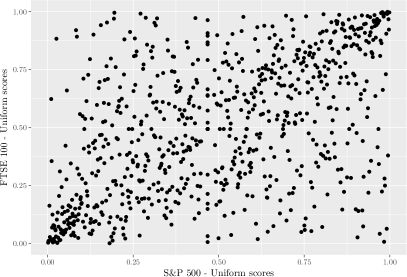

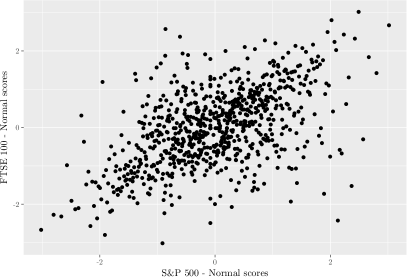

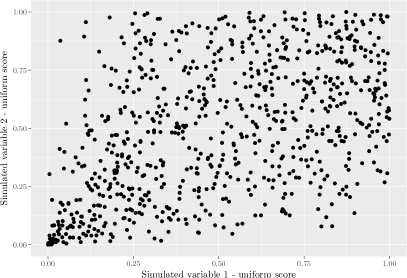

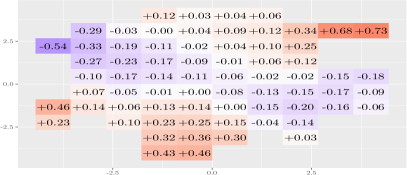

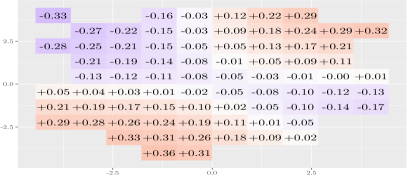

We will throughout this paper illustrate several points using a bivariate data set on some financial returns. We use daily international equity price index data for the United States (i.e. the S&P 500) and the United Kingdom (i.e. the FTSE 100). The data are obtained from Datastream (2018), and the returns are defined as

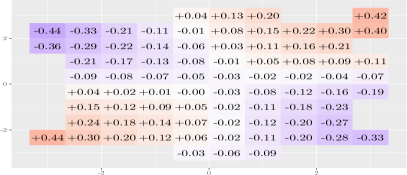

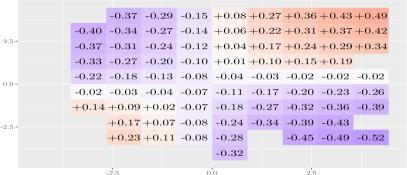

where is the price index at time . The observation span covers the period from January 1st 2007 through December 31st 2009, in total 784 observations. In Figure 2, four scatterplots are presented.

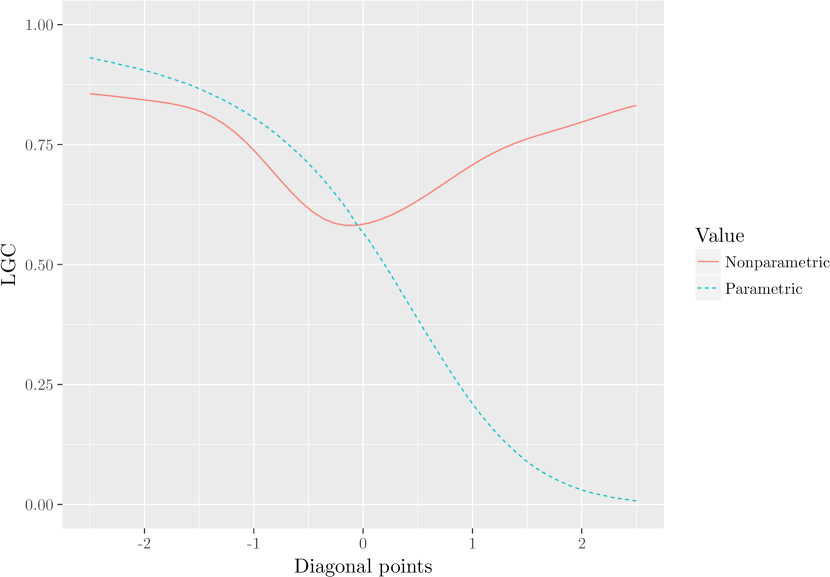

Figure 2a displays a scatterplot of the observed log-returns, with S&P 500 on the horizontal axis, and the FTSE 100 on the vertical axis. Figure 2b displays the uniform scores of the same data, and we see indications of a singular behavior of the copula density in the lower left and upper right corners of the unit square. In Figure 2c the observations have been transformed to normal scores, which more clearly reveals the tail properties of the underlying distribution. Finally, Figure 2d shows the scatter plot of 784 simulated pairs of variables, on uniform scale, from a Clayton copula fitted to the return data. This plot partially resembles Figure 2b, in particular in the lower left corner. However, there are some differences in the upper right corner. We will look into this discrepancy in Section 6.

In Figure 2a, and perhaps more clearly in Figure 2c, we see that there seems to be stronger dependence between the variables when the market is going either up or down, which is very sensible from an economic point of view, but it is not easy to give an interpretation of the parameter of the Clayton copula in terms of such type of dependence. In fact, in this particular case, . The difficulty of giving a clear and concrete interpretation of copula parameters in terms of measuring strength of dependence can be stated as a potential issue of the copula representation. In this respect it is very different from the Pearson’s . We will return to this point in much detail in Section 6, where we define a local correlation.

Another issue of the original copula approach has been the lack of good practical models as the dimension increases, as it would for example in a portfolio problem in finance. This has recently been sought solved by the so-called pair copula construction. To simplify, in a trivariate density , by conditioning this can be written , and a bivariate copula construction, e.g. a Clayton copula, can be applied to the conditional density with fixed. This conditioning can be extended to higher dimensions under a few simplifying assumptions, resulting in a so-called vine copula, of which there are several types. The procedure is well described by Aas et al. (2009), and has found a number of applications. The Clayton canonical vine copula, for instance, allows for the occurrence of very strongly correlated downside events and has been successfully applied in portfolio choice and risk management operations. The model is able to reduce the effects of extreme downside correlations and produces improved statistical and economical performance compared to elliptical type copulas such as the Gaussian copula (9) and the -copula, see Low et al. (2013).

Other models developed for risk management applications are so-called panic copulas to analyze the effect of panic regimes in the portfolio profit and loss distribution, see e.g Meucci (2011). A panic reaction is taken to mean that a number of investors react in the same way, such that the statistical dependence becomes very strong between financial returns from various financial objects, in this way rendering the risk spreading of the portfolio illusory. We will return to this situation in Section 6 where among other things we can show that in a panic situation the local correlation increases and approaches one as a function of a copula parameter. The copula has also been used directly for independence testing; see e.g. Genest and Rémillard (2004) and Mangold (2017).

Most of the copula theory and also most of the applications are to variables that are assumed to be iid, but there is also a growing literature on stochastic processes such as Markov chains. The existence of both auto dependence and cross dependence in a multivariate stochastic process is quite challenging. Some of the mathematical difficulties in the Markov chain case is clearly displayed in the paper Darsow, Nguyen, and Olsen (1992). They used the ordinary copula, but it is not obvious how the theory of Markov processes can be helped by the concept of a copula. That work was limited to first order Markov chain. The pair copula has also been introduced in a Markov theory framework, and then in higher-order Markov processes, by Ibragimov (2009). Again, so far, the impact on Markov theory has not been overwhelming. This may partly be due to complicated technical conditions.

Two other papers using copulas (and pair copulas) in serial dependence are Beare (2010) and Smith et al. (2010). When it comes to parametric time series analysis, especially for multivariate time series, it has been easier to implement the copula concept as developed for iid variables. This is well documented in the survey paper by Patton (2012). The reason is that the auto dependence can first be filtered out by a marginal fit to each component series, and the copula could then be applied to the residuals which may be assumed to be iid or at least can be replaced by an iid vector process asymptotically. More precisely in the framework of Patton and others,

| (12) |

where in the bivariate case primarily considered by Patton,

Here can be taken as the -algebra generated by for . and is a stochastic vector variable, e.g. higher lags of measurable with respect to . The estimation can be done in two steps, cf. also Chen and Fan (2006). First the parameters of the marginal processes are estimated. Then a copula modeling stage is applied to the estimated residuals

In this context both parametric and nonparametric (resulting in a semiparametric model) models have been considered for the residual distribution . In the parametric case, time dependence can be allowed for , whereas in the nonparametric case there is no dependence of permitted in . Much more details and references are provided in Patton (2012). The modeling in (12) is restricted to the bivariate case. Modeling of both cross and auto dependence, including use of vine copulas, in a multivariate time series or Markov process is given in Smith (2015). Time dependent risk is treated using a dynamic copula model by Oh and Patton (2018).

4 Beyond Pearson’s : Global dependence functionals and tests of independence

Studies of statistical dependence may be said to center mainly around two problems: (i) definition and estimation of measures of dependence and (ii) tests of independence. Of course these two themes are closely related. Measures of association such as the Pearson’s can also be used in tests of independence, or more precisely: tests of uncorrelatedness. On the other hand, test functionals for tests of independence can also in many, but not all, cases be used as a measures of dependence. A disadvantage with measures derived from tests is that they are virtually always based on a distance function and therefore non-negative. This means that they cannot distinguish between negative and positive dependence, whatever this may mean in the general nonlinear case. We will return to this later in the paper.

Most of the test functionals are based on the definition of independence in terms of cumulative distribution functions or in terms of density functions. Consider stochastic variables . These variables are independent if and only if their joint cumulative distribution function is the product of the marginal distribution functions: , and the same is true for all subsets of variables of . If the variables are continuous, this identity can be phrased in terms of the corresponding density functions instead. A typical test functional is then designed to measure the distance between the estimated joint distributions/densities and the product of the estimated marginals. This is not so easily done for parametric densities, since the dependence on parameters in the test functional may be very complex, and tests of independence may be more sensibly stated in terms of the parameters themselves, as is certainly the case for the Gaussian distribution. Therefore one would usually estimate the involved distributions nonparametrically, which, for joint distributions, may be problematic for moderate and large ’s due to the curse of dimensionality. We will treat these problems in some detail in Sections 4.2-4.5.

Before starting on the description of the various dependence measures, let us remark that Rényi (1959) proposed that a measure of dependence between two stochastic variables and , , should ideally have the following 7 properties:

-

(i)

is defined for any neither of which is constant with probability 1.

-

(ii)

.

-

(iii)

.

-

(iv)

if and only if and are independent.

-

(v)

if either or , where and are measurable functions.

-

(vi)

If the Borel-measurable functions and map the real axis in a one-to-one way to itself, then .

-

(vii)

If the joint distribution of and is normal, then , where is Pearson’s .

The product moment correlation satisfies only (i), (ii) and (vii).

One can argue that the rules i) - vii) do not take into account the difference between positive and negative dependence; it only looks at the strength of the measured dependence. If this wider point of view were to be taken into account, (iii) could be changed into (iii’) : , (v) into (v’): or if there is a deterministic relationship between and . Finally, (vii) should be changed into (vii’) requiring . Moreover, some will argue that property (vi) may be too strong to require. It means that the strength of dependence is essentially independent of the marginals as for the copula case.

We will discuss these properties as we proceed in the paper. Before we begin surveying the test functionals as announced above, we start with the maximal correlation which, it will be seen, is intertwined with at least one of the test functionals to be presented in the sequel.

4.1 Maximal correlation

The maximal correlation is based on the Pearson . It is constructed to avoid the problem demonstrated in Section 2.3 that Pearson’s can easily be zero even if there is strong dependence.

It seems that the maximal correlation was first introduced by Gebelein (1941). He introduced it as

where is the Pearson’s . Here the supremum is taken over all Borel-measurable functions with finite and positive variance for and . The measure gets rid of the nonlinearity issue of . It is not difficult to check that if and only if and are independent. On the other hand cannot distinguish between negative and positive dependence, and it is in general difficult to compute.

The maximal correlation cannot be evaluated explicitly except in special cases, not the least because there does not always exist functions and such that . If this equality holds for some and , it is said that the maximal correlation between and is attained. Rényi (1959) gave a characterization of attainability.

Czáki and Fischer (1963) studied mathematical properties of the maximal correlation and computed it for a number of examples. Abrahams and Thomas (1980) considered maximal correlation in the context of stochastic processes. A multivariate version of maximal correlation was proposed in Koyak (1987). In a rather influential paper, at least at the time, Breiman and Friedman (1985) presented the ACE (alternating conditional expectation) algorithm for estimating the optimal functions and in the definition of the maximal correlation. They applied it both to correlation and regression. Some curious aspects of the ACE algorithm is highlighted in Hastie and Tibshirani (1990, 84–86).

Two more recent publications are Huang (2010), where the maximal correlation is used to test for conditional independence, and Yenigün, Székely, and Rizzo (2011), where it is used to test for independence in contingency tables. The latter paper introduces a new example where can be explicitly computed. See also Yenigün and Rizzo (2014).

4.2 Measures and tests based on the distribution function

We start with, and in fact put the main emphasis on, the bivariate case. Let and be stochastic variables with cumulative distribution functions and . The problem of measuring the dependence between and can then be formulated as a problem of measuring the distance between the joint cumulative distribution function of and the distribution function formed by taking the product of the marginals. Let be a candidate for such a distance functional. It will be assumed that is a metric, and it is natural to require, Skaug and Tjøstheim (1996), that

| (13) |

Clearly, such a measure is capable only of measuring the strength of dependence, not its direction. Corresponding to requirement (vi) in Rényi’s scheme listed in the beginning of this section, one may want to require invariance under transformations, or more precisely

| (14) |

where , and . Here and are increasing functions, and are the marginals and bivariate distribution functions of the random variables and , respectively.

For distance functionals not satisfying equation (14), one can at least obtain scale and location invariance by standardizing such that and , assuming that the second moment exists. In practice, empirical averages and variances must be employed, but asymptotically the difference between using empirical and theoretical quantities is a second order effect. In Skaug and Tjøstheim (1996) and Tjøstheim (1996) such a standardization has been employed for all functionals.

Pearson’s can be expressed as a functional on , and although not generally as a distance functional depending on and . For instance, with and standardized, the Pearson correlation squared can be expressed,

Clearly does not satisfy either of the conditions (13) or (14). Similarly, the square of the population values of the Spearman rank correlation and Kendall’s are obtained by squaring in the formulas (4) and (5). For these measures the requirement (13) is not fulfilled, whereas the invariance property does hold.

A natural estimate of a distance functional is obtained by setting

where may be taken to be the empirical distribution functions given by

and

or a normalized version with replaced by for given observations . Similarly, for a stationary time series at lag ,

Conventional distance measures between two distribution functions and are the Kolmogorov-Smirnov distance

and the Cramér-von Mises type distance of a distribution from a distribution

Here satisfies (13) and (14), whereas satisfies (13) but not (14).

Most of the work pertaining to measuring dependence and testing of independence has been done in terms of the Cramér-von Mises distance. This work started already by Hoeffding (1948) who looked at iid pairs , and studied finite sample distributions in some special cases. With considerable justification it has been named the Hoeffding-functional by some. This work was continued by Blum, Kiefer, and Rosenblatt (1961) who provided an asymptotic theory, still for the iid case. It was extended to the time series case with a resulting test of serial independence in Skaug and Tjøstheim (1993a). A recent paper using a copula framework is Kojadinovic and Holmes (2009). We will briefly review the time series case because it illustrates some of the problems, and because some of the same essential ideas as for the Hoeffding-functional have been used in more recent work on the distance covariance, which we treat in Section 4.3. Since does not depend on for a stationary time series, we simply write in the following.

In the time series case the Cramér-von Mises distance at lag is given by

where and are the joint and marginal distributions of and , respectively. Replacing theoretical distributions by empirical ones leads to the estimate

| (15) |

Assuming to be ergodic, we have that almost surely as .

To construct a test of serial independence we need the distribution of under the assumption of the null hypothesis of being iid. Let . Then it is possible to represent as

where is a von Mises U-statistic in the technical sense of Denker and Keller (1983) with a degenerate symmetric kernel function. Using asymptotic theory, Carlstein (1988), Denker and Keller (1983) and Skaug (1993), of this statistic or the related U-statistic one has (Skaug and Tjøstheim 1993a, Theorem 2) the convergence in distribution

| (16) |

where is an independent identically distributed sequence of variables, and where the are the eigenvalues of the eigenvalue problem

with

If the distribution of each is continuous, then is distribution free, i.e., its distribution does not depend on . Then all calculations can be carried out with being the uniform distribution, in which case and , and the distribution of the right hand side of (16) can be tabulated by truncating it for a large value of the summation index. Similar distribution results will be seen to hold for test functionals in Sections 4.3 and 4.4.

A test of the null hypothesis of independence, or rather pairwise independence at lag , can now be constructed. It is then reasonable to reject if large values of is observed. Thus a test of level is:

where is the upper -point in the null distribution of . Since the exact distribution of is unknown, we can use the asymptotic approximation furnished by retaining a finite number of terms in (16). For and small this works well. However, as increases, in general (Skaug and Tjøstheim 1993a) the level is severely overestimated. The results of Skaug and Tjøstheim (1993a) have since been very considerably extended and improved by Hong (1998).

Under the hypothesis of being iid the bootstrap is a natural tool to use for constructing the null distribution and critical values. For moderate and large ’s the bootstrapping yields a substantially better approximation to the level.

Under the alternative hypothesis that and are dependent, the test statistic will in general be asymptotically normal with a different rate from that of (16), but the power function will be complicated; see e.g. Hong (2000).

To extend the scope to testing of serial dependence among , or alternatively between a set of several random variables for which there are iid observations of the set, one might use a functional

| (17) |

The asymptotic theory under the null hypothesis of independence for such a test has been examined by Delgado (1996) using empirical process theory, but due to the curse of dimensionality, problems in practice might be expected for moderately large ’s. As an alternative Skaug and Tjøstheim (1993a) used a “Box-Pierce-Ljung” analogy, testing for pairwise independence in all of the pairs using the statistic

| (18) |

The asymptotic theory of such a test is given in Skaug (1993). Hong (1998) noted that

| (19) |

has better size properties for large .

There have been several contributions to the limit theory of statistics such as (15) and (17) using empirical process theory. Delgado did that based on developments in Blum, Kiefer, and Rosenblatt (1961), but the limiting Gaussian process is complicated with a complex covariance matrix which makes it difficult to tabulate critical values. Ghoudi, Kulperger, and Rémillard (2001) based their work on the so-called Möbius transformation promoted by Deheuvels (1981a; 1981b) in his papers on independence testing. This transformation takes explicitly into account the joint distribution function of all subsets of mentioned in the second paragraph of Section 3. To explain the Möbius transformation, let , be random variables. For let denote the marginal cumulative distribution function of and let be the corresponding joint cumulative distribution function. Consider a subset , and for any , define

where is the number of elements in a set , , where by convention , and where is the vector whose th component is defined by if , and otherwise. Then one can state the following criterion of independence: are independent if and only if for any . This is shown in e.g. Ghoudi, Kulperger, and Rémillard (2001). In that paper it is also shown how this transformation leads to a Gaussian empirical process limit with a relatively simple covariance function, making it easier to tabulate critical values. The authors manage to do this both for the Cramér-von Mises statistic and the Kolmogorov-Smirnov statistic, and they consider three cases: iid vector samples, time series samples and residuals in time series models. See also Beran, Bilodeau, and Lafaye de Micheaux (2007).

Genest and Rémillard (2004) use the Möbius transformation in testing of independence in a copula framework, and Ghoudi and Rémillard (2018) use it to obtain tests for independence of residuals in a parametric model

where the iid innovations have mean 0 and variance 1.

As an alternative to testing uncorrelatedness in time series using the Pearson at accumulated lags as in the Box-Ljung-Pierce statistic, one could test for a constant spectral density. Quite general specification tests in terms of the spectral density has been considered by Anderson (1993), who looked at tests of constant by using both the Cramér-von Mises and the Kolmogorov-Smirnov criteria. Hong (2000) introduced a spectral counterpart for the independence tests based on the marginal distribution function for a time series and the lag distribution function introduced earlier in this section. This was achieved by replacing the ordinary autocorrelation function by the dependence measure

and then taking Fourier transforms, which leads to

| (20) |

where . It is shown in Hong (2000) how this can be used to construct a test of independence that has power in cases where the tests based on the ordinary spectrum has not. However, as explained in a note in that paper, weak power can be expected for this test against ARCH/GARCH type dependence.

Instead of stating independence in terms of cumulative distribution functions this can alternatively be expressed in terms of the characteristic function. Székely, Rizzo, and Bakirov (2007) and Székely and Rizzo (2009), as will be seen in Section 4.3, make systematic use of this in their introduction of the distance covariance test. Two random variables and are independent if and only if the characteristic functions satisfy

where

This was exploited by Csörgö (1985) and Pinkse (1998) to construct tests for independence based on the characteristic function in the iid and time series case, respectively. Further work on testing of conditional independence was done by Su and White (2007). See also Fan et al. (2017). Hong (1999) put this into a much more general context by replacing in (20) by

By taking Fourier transform of this quantity one obtains

| (21) |

Hong (1999) called (21) the generalized spectral density function. Here can be estimated by

where is a kernel weight function, is a bandwidth or lag order, and

with

Under the null hypothesis of serial independence becomes a constant function of frequency :

with , where . In order to test for independence one can compare and using e.g. an -functional. More work related to this has been done by Hong and Lee (2003) and Escanciano and Velasco (2006).

4.3 Distance covariance

We have seen that there are at least two ways of constructing functionals that are consistent against all forms of dependence, namely those based on the empirical distribution function initiated by Hoeffding (1948) and briefly reviewed above, and those based on the characteristic function represented by Csörgö (1985) in the iid case and Pinkse (1998) in the serial dependence case, and continued in Hong (1999; 2000) in a time series spectrum approach. Se also Fan et al. (2017). Both Pinkse and Hong use a kernel type weight function in their functionals. Thus, Pinkse uses a weight function in the functional

where for a pair of two random variables

Let . Pinkse in his simulation experiments chose the weight functions and .

The authors of two remarkable papers, Székely, Rizzo, and Bakirov (2007) and Székely and Rizzo (2009), take up the characteristic function test statistic again in the non-time series case. But what distinguishes these from earlier papers is an especially judicious choice of weight function reducing the empirical characteristic function functional to empirical moments of differences between the variables, or distances in the vector case, this leading to covariance of distances. Some of these ideas go back to what the authors term an “energy statistic”; see Székely (2002), Székely and Rizzo (2013) and also Székely and Rizzo (2012). It has been extended to time series and multiple dependencies by Davis et al. (2018), Fokianos and Pitsillou (2017), Zhou (2012), and Dueck et al. (2014), Dueck, Edelman, and Richards (2015) and Yao, Zhang, and Shao (2018). In the locally stationary time series case there is even a theory, see Jentsch et al. (2018). The distance covariance, dcov, seems to work well in a number of situations, and it has been used as a yardstick by several authors writing on dependence and tests of independence. In particular it has been used as a measure of comparison in the work on local Gaussian correlation to be detailed in Section 6. There are also points of contacts, as will be seen in Section 4.4, with the HSIC measure of dependence popular in the machine learning community.

The central ideas and derivations are more or less all present in Székely, Rizzo, and Bakirov (2007). The framework is that of pairs of iid vector variables in and , respectively, and the task is to construct a test functional for independence between and . Let , and be the characteristic functions involved, where is the inner product in and , respectively. The starting point is again the weighted characteristic functional

| (22) |

where is a weight function to be chosen, Note that it is easy to choose so that if and only if and are independent. Similarly, one defines

| (23) |

and . The distance correlation, dcor, is next defined by, assuming ,

These quantities can be estimated by the empirical counterparts given observations of the vector pair with

| (24) |

where, for a set of observations the empirical characteristic functions are given by

and

It turns out that it is easier to handle the weight function in the framework of the empirical characteristic functions. It will be seen below that

| (25) |

is a good choice. Here is the Euclidean norm in and similarly for . Moreover, the normalizing constants are given by , . For it to make sense to introduce the weight function on the empirical characteristic function one must show that the empirical functionals converges to the theoretical functionals for this weight function. This is not trivial because of the singularity at for given by (25). A detailed argument is given in the proof of Theorem 2 in Székely, Rizzo, and Bakirov (2007).

The advantage of introducing the weight function for the empirical characteristic functions is that one can compute the squares in (24) and then interchange summation and integration. The resulting integrals can be computed using trigonometric identities, in particular the odd symmetry of products of cosines and sines which makes corresponding integrals disappear. The details are given in the proof of Theorem 1 in Székely, Rizzo, and Bakirov (2007) and in Lemma 1 of the Appendix of Szekely and Rizzo (2005) who in turn refer to Prudnikov, Brychkov, and Marichev (1986) for the fundamental lemma

for with

| (26) |

and where the weight function considered above corresponds to and or in (25). The general -case corresponds to a weight function

With the simplification all of this implies that as defined in (24), can be computed as

where

| (27) |

which explains the appellation distance covariance. In fact, it is possible to further simplify this by introducing

for . Similarly, one can define and and

and

and similarly for . From this one can easily compute . The computations are available in an R-package: Rizzo and Szekely (2018).

As is the case of the empirical joint distribution functional it can be expected that the curse of dimensionality will influence the result for large and moderate values of and . Obviously, in the time series case, it is possible to base oneself on pairwise distances as in (18) or (19), which has been done in Yao, Zhang, and Shao (2018).

Letting , it is not difficult to prove that an alternative expression for is given by (assuming and )

| (28) |

where , are iid. This expression will be useful later in Section 4.4 in a comparison with the HSIC statistic. Properly scaled has a limiting behavior under independence somewhat similar to that of (16) in Section 4.2. Namely, under the condition of existence of first moment, , converges in distribution to a quadratic form

where are independent standard normal variables, are non-negative constants that depend on the distribution of . One can also obtain an empirical process limit theorem, Theorem 5 of Székely, Rizzo, and Bakirov (2007). In the R-package, as for the case of the empirical distribution function, it has been found advantageous to rely on re-sampling via permutations. This is quite fast since the algebraic formulas (27) are especially amenable to permutations. Both Székely, Rizzo, and Bakirov (2007) and Székely and Rizzo (2009) in their experiments only treat the case of in (26).

Turning to the properties (i) - (vii) of Rényi (1959) listed in the beginning of this section, it is clear that (i) - (iv) are satisfied by . Moreover, according to Székely, Rizzo, and Bakirov (2007), if , then there exists a vector , a non-zero real number and an orthogonal matrix such that , which is not quite the same as Rényi’s requirement (v). Also, the general invariance in his property (vi) does not seem to hold. The final criterion (vii) of Rényi is that the dependent measure should reduce to the absolute value of Pearson’s in the bivariate normal case. This is not quite the case for the dcov, but it comes close, as is seen from Theorem 6 of Székely and Rizzo (2009). In fact, if is bivariate normal with and and with correlation , then and

4.4 The HSIC measure of dependence

Recall the definition and formula for the maximal correlation. This, as stated in Section 4.1 gives rise to a statistic , where if and only if and are independent. But it is difficult to compute since it requires the supremum of the correlation taken over Borel-measurable and . In the framework of reproducing kernel Hilbert spaces (RKHS) it is possible to pose this problem, or an analogous one, much more generally, and one can compute an analogue of quite easily. This is the so-called HSIC (Hilbert-Schmidt Independence Criterion).

Reproducing kernel Hilbert spaces are very important tools in mathematics as well as in statistics. A general reference to applications in statistics is Berlinet and Thomas-Agnan (2004). In the last decade or so there has also been a number of uses of RKHS in dependence modeling. These have often been published in the machine learning literature. See e.g Gretton, Herbrich, et al. (2005), Gretton and Györfi (2010), Gretton and Györfi (2012) and Sejdinovic et al. (2013).

We have found the quite early paper by Gretton, Bousquet, et al. (2005) useful both for a glimpse of the general theory and for the HSIC criterion in particular.

A reproducing kernel Hilbert space is a separable Hilbert space of functions on a set , such that the evaluation functional is a continuous linear functional on for every . Then, from the Riesz representation theorem, Muscat (2014), chapter 10, there exists an element such that , where is the inner product in . Applying this to and another point we have . The function from to is the kernel of the RKHS . It is symmetric and positive definite because of the symmetry and positive definiteness of the inner product in . We use the notation for the kernel.

The next step is to introduce another set with a corresponding RKHS and to introduce a probability structure and probability measures , and on , and , respectively. With these probability measures and function spaces and one can introduce correlation of functions of stochastic variables on , and . This is an analogy of the functions used in the definition of the maximal correlation. In RKHS setting the covariance (or cross covariance) is an operator on the function space . Note also that this has a clear analogy in functional statistics, see e.g. Ferraty and Vieu (2006).

It is time to introduce the Hilbert-Schmidt operator: A linear operator is called a Hilbert-Schmidt operator if its Hilbert-Schmidt (HS) norm

where and are orthonormal bases of and , respectively. The HS-norm generalizes the Froebenius norm for a matrix . Finally, we need to define the tensor product in this context: If and , then the tensor product operator is defined by

Moreover, by using the definition of the HS norm it is not difficult to show that

We can now introduce an expectation and a covariance on these function spaces. Again, the analogy with corresponding quantities in functional statistics will be clear. We assume that and are furnished with probability measures , and with and being -algebras of sets on and . The expectations and are defined by, and are stochastic variables in and , respectively,

and

where and are well-defined as elements in and because of the Riesz representation theorem. The norm is obtained by

where as before and are independent but have the same distribution , and where is defined in the same way. With given , we can now define the cross covariance operator as

Now, take to be identified with defined above as a result of the Riesz representation theorem, and defined in exactly the same way. The Hilbert-Schmidt Information Criterion (HSIC) is then defined as the squared HS norm of the associated cross-covariance operator

Let and be kernel functions on and . Then (Gretton, Bousquet, et al. 2005, Lemma 1), the HSIC criterion can be written in terms of these kernels as

| (29) |

Existence is guaranteed if the kernels are bounded. The similarity in structure to (28) for the distance covariance should be noted (partly due to the identity but going deeper as will be seen below when HSIC is compared to dcov). Note that the kernel functions depend on the way the spaces and and their inner products are defined. In fact it follows from a famous result by Moore-Aronszajn, see Aronszajn (1950), that if is a symmetric, positive definite kernel on a set , then there is a unique Hilbert space of functions on for which is a reproducing kernel. Hence as will be seen next, in practice when applying the HSIC criterion, the user has to choose a kernel.

With some restrictions the HSIC measure is a proper measure of dependence in the sense of the Rényi (1959) criterion (iv): From Theorem 4 of Gretton, Bousquet, et al. (2005) one has that if the kernels and are universal (universal kernel is a mild continuity requirement on the kernel) on compact domains and , then if and only if and are independent. The compactness assumption results from the application of an equality for bounded random variables taken from Hoeffding (1963), that is being used actively in the proof.

A big asset of the HSIC measure it that its empirical version is easily computable. In fact if we have independent observations and independent observations , then

| (30) |

where tr is the trace operator and the matrices are defined by

where is the Kronecker delta. It is shown in Gretton, Bousquet, et al. (2005) that this estimator converges towards . The convergence rate is . There is also a limit theorem for the asymptotic distribution, which under the null hypothesis of independence and scaled with converges in distribution to the random variable , where the are independent standard normal variables, and and are eigenvalues of integral operators associated with centralized kernels derived from and and integrating using the probability measures and , respectively. Again, this should be compared to the limiting variable for the statistic in the Cramér- von Mises functional (16). Critical values can be obtained for , but as a rule one seems to rely more on resampling as is the case for most independence test functionals.

It is seen from (30) that computation of the empirical HSIC criterion requires the evaluation of and . Then appropriate kernels have to be chosen. Two commonly used kernels are the Gaussian kernel given by

and the Laplace kernel

Pfister and Peters (2017) describe a recent R-package involving HSIC. Gretton, Bousquet, et al. (2005) use these kernels in comparing the HSIC test with several other tests, including the dcov test in, among other cases, an independent component setting. Both of these tests do well, and one of these tests does not decisively out-compete the other one. This is perhaps not so unexpected because there is a strong relationship between these two tests. This is demonstrated by Sejdinovic et al. (2013). They look at both the dcov test and the HSIC test in a generalized setting of semimetric spaces, i.e with kernels and distances defined on such spaces and . For a given distance function they introduce a distance-induced kernel, and under certain regularity conditions they establish a relationship between these two quantities. There is a related paper by Lyons (2013) which obtains similar results but not in an explicit RKHS context, in fact in a general dcov context.

Let and be distance measures on the semi-metric spaces and , respectively. Then a generalized dcov distance functional can be defined as, compare again to (28),

This distance covariance in metric spaces characterizes independence, that is, if and only if and are independent, and if the metrics and satisfy an additional property, termed strong negative type. See Sejdinovic et al. (2013) for more details. An asset of the RKHS formulation is that it is very general. As was seen from the introduction of HSIC above, the sets and can have a metric space structure, and probability measures , and can still be introduced, and the definition of HSIC given in the beginning of this section and the accompanying decomposition (29) still make sense in this generalized framework. It can then be shown that, Theorem 24 in Sejdinovic et al. (2013), one has the following equivalence: Let and be any two kernels on and that generate and , respectively, and let , then . Among the regularity conditions required for this result is the assumption of “negative type”, which is satisfied in standard Euclidean spaces.

However, it is not possible to find a direct RKHS representation of the characteristic function representation (23) of .

Lately there have been other extensions of both the dcov and HSIC to conditional dependence, partial distance and to time series. A few references are Szekely and Rizzo (2014), Chwialkowski and Gretton (2014), Zhang et al. (2012) and Pfister et al. (2018). A recent tutorial on RKHS is Gretton (2017).

4.5 Density based tests of independence

Intuitively, one might think that knowing that the density exists should lead to increased power of the independence tests due to more information. This is true, at least for some examples (see e.g. Teräsvirta, Tjøstheim, and Granger (2010), Chapter 7.7). As in the preceding sections one can construct distance functionals between the joint density under dependence and the product density under independence. A number of authors have considered such an approach; both in the iid and time series case, see e.g. Rosenblatt (1975), Robinson (1991), Skaug and Tjøstheim (1993b; 1996), Granger, Maasoumi, and Racine (2004), Hong and White (2005), Su and White (2007) and Berrett and Samworth (2017). For two random variables and having joint density and marginals and the degree of dependence can be measured by , where is now the distance measure between two bivariate density functions. The variables are normalized with and . It is natural to consider the Rényi (1959) requirements again, in particular the requirements (iv) and (vi).

All of the distance functionals considered will be of type

| (31) |

where is a real-valued function such that the integral exists. If is of the form , we have

| (32) |

which by the change of variable formula for integrals is seen to have the Rényi property (vi). Moreover, if and if and only if , then Rényi property (iv) is fulfilled. Several well-known distance measures for density functions are of this type. For instance, letting we obtain the Hellinger distance

between and . The Hellinger distance is a metric and hence satisfies the Rényi property (iv).

Chung et al. (1989) defined the so-called directed divergence of degree , which is also related to the Rényi divergence, Rényi (1961),

| (33) |

It is seen that the Hellinger distance is a special case . Clearly, the measure satisfies (vi), and for , using Hölder’s inequality,

with equality if and only if . Hence, satisfies (iv) for .

The familiar Kullback-Leibler information (entropy) distance is obtained as a limiting case as ,

| (34) |

Since this distance is of type (32), it satisfies (vi), and it can also be shown to satisfy (iv). Going outside the range , for in (33), the test-of-fit distance in Bickel and Rosenblatt (1973) emerges. See also Granger and Lin (1994). A very recent paper linking with other recent approaches to independence testing is Berrett and Samworth (2017).

All of the above measures are trivially extended to two arbitrary multivariate densities. However, estimating such densities in high or moderate dimensions may be difficult due to the curse of dimensionality. A functional built up from pairwise dependencies can be considered instead such as in (18) and (19).

For a given functional depending on two densities and , may be estimated by . There are several ways of estimating the densities, e.g. the kernel density estimator,

for given observations . Here , where is the bandwidth (generally a matrix), is the kernel function, and is the dimension of . The kernel function is usually taken to be a product of one-dimensional kernels; i.e., , where each generally is non-negative and satisfies

Once estimators for , and in the integral expression (31) for have been obtained, the integral can be computed by numerical integration or by empirical averages using the ergodic theorem (or law of large numbers in the iid case). Consequently for a given lag in the time series case,

Here is the joint density of , and is a weight function, e.g., for some chosen constant .

Under regularity conditions (see e.g. Skaug and Tjøstheim (1996)}, consistency and asymptotic normality can be obtained for the estimated test functionals. It should be noted that the leading term in an asymptotic expansion of the standard deviation of for the estimated Kullback-Leibler functional and the estimated Hellinger functional is of order . This is of course the same as for the standard deviation of a parametric estimate in a parametric estimation problem. In that situation the next term of the Edgeworth expansion is of order , and for moderately large values of the first order term will dominate. However, for the functionals considered above, due to the presence of an -dependent bandwidth, the next terms in the Edgeworth expansion are much closer, being of order and , and since typically or , must be very large indeed to have the first term dominate in the asymptotic expansion. As a consequence, first order asymptotics in terms of the normal approximation cannot be expected to work well unless is exceedingly large. Hence, basing a test of independence directly on the asymptotic theory may be hazardous as the real test size will typically deviate substantially from the nominal size. In this sense the situation is quite different from the empirical functionals treated in the previous sections, where there is no bandwidth parameter involved.

All of this suggests the use of the bootstrap or permutations as an alternative for constructing the null distribution. One may anticipate that it picks up higher-order terms of the Edgeworth expansion (Hall 1992, Chapters 3 and 4), although no rigorous analysis to confirm this has been carried out for the functionals discussed here.

The fact that the permutation test yields an exact size, and that resampling tests generally perform much better, underscores a major point. In tests involving a bandwidth it is absolutely essential to use resampling in practice. The asymptotic theory is far too inaccurate except possibly in cases where the sample size is extremely large. In the empirical functional case treated in Sections 4.2 and 4.3, the asymptotic theory is incomparably more accurate, but even in this case the experience so far seems to be that resampling generally does slightly better.

It is quite difficult to undertake local asymptotic power analyses for the functionals based on estimated density functions. For reasons mentioned above, asymptotic studies could be expected to be unreliable unless is very large. It has therefore been found more useful to carry out comparative simulation studies against a wide choice of alternatives using a modest sample size, see e.g. Skaug and Tjøstheim (1993; 1996) and Hong and White (2005). These references also contain applications to real data.

4.6 Test functionals generated by local dependence relationships

If one has bivariate normal data with standard normal marginals and one gets observations scattered in a close to circular region around zero, and most test functionals will easily recognize this as a situation of independence. However, as pointed out by Heller, Heller, and Gorfine (2013), if data are generated along a circle, e.g. for some stochastic noise variable , then and are dependent, but the dcov, and undoubtedly other test functionals, among which -based tests, fail. They give some other examples as well of similar failures for test functionals to detect symmetric geometric patterns. Heller, Heller, and Gorfine (2013) point a way out of this difficulty, namely by looking at dependence locally (along the circle) and then aggregate the dependence by integrating or by other means over the local regions. There are of course several ways of measuring local dependence and we will approach this problem more fundamentally in Section 5.

Before coming to the paper by Heller, Heller, and Gorfine (2013) and papers using similar approaches, partly for historic reasons, we look briefly at the correlation integral and the so-called BDS test named after its originators Brock, Dechert and Scheinkman. This test has a local flavor at its basis, but the philosophy is a bit different from the other tests presented in the current subsection. The BDS test attracted much attention among econometricians in the 1990s, and it has since been improved.

The starting point is the correlation integral introduced in Grassberger and Procaccia (1983) as a means of measuring fractal dimension of deterministic data. It measures serial dependence patterns in the sense that it keeps track of the frequency with which temporal patterns are repeated in a data sequence. Let be a sequence of numbers and let

Then the correlation integral for embedding dimension is given by

Here, for , , where is the indicator function and is a cut off threshold which could be a multiple of the standard deviation in the case of a stationary process. The parameter may also be considered to be a tuning parameter. Let

If is an absolutely regular (Bradley, 1986, p.169) stationary process the above limit exists and is given by

where is the joint cumulative distribution function of . Since

it is easily seen that if consists of iid random variables, then

This theory is the starting point for the BDS test. Under the hypothesis of independence, and excluding the case of uniformly distributed random variables, Broock et al. (1996) have established asymptotic normality of under an appropriate scaling factor . As mentioned, the test has found considerable use among econometricians, but it suffers from some limitations, the arbitrariness of the choice of , the probability of rejecting independence does not always approach 1 as , and finally, and probably most critically, the convergence to the asymptotic normal distribution may be very slow, making bootstrapping a possible alternative. These problems were pointed out by Genest, Ghoudi, and Rémillard (2007) who proposed a rank based extension, where these difficulties are to a large degree eliminated. Because the limiting distribution of the rank-based test statistics is margin-free, their finite-sample p-values can be easily calculated by simulations.

Next, returning to the test of Heller, Heller, and Gorfine (2013), note that if and (in and , say) are continuous and are dependent, then there exists a point in the sample space of , and radii and around and , respectively, such that the joint distribution of is different from the product of the marginals in the neighborhood defined by and . The next step is the introduction of a distance functions in the sample spaces of and , and following Heller, Heller, and Gorfine (2013) we do not distinguish between these distance functions in our notation. Consider the indicator functions and . For a sample one gets pairs of values of zeros and ones from the indicator functions that can be set up in a contingency table structure. Evidence against independence may then be quantified by Pearson’s chi-square test statistic or the likelihood ratio test for contingency tables.

The data is used to guide in the choice of , and . For every sample point , that point is in its turn chosen to be and for every sample point , , it is chosen in turn to define and (thus defining the locality of the test). The remaining observations are then inserted in the indicator functions. For every pair based on this one can construct a classic test statistic for a Pearson chi-square test for a contingency table. To test for independence these quantities are aggregated in a test statistic . Critical values are obtained by resampling. The test, taking local properties into account, works very well for the circle example and several other examples, both similar to the circle example and not. See also Heller et al. (2016).

The next paper in this category, Reshef et al. (2011), is published in Science. The idea behind their MIC (Maximal Information Coefficient) statistic consists in computing the mutual information as defined in (34) locally over a grid in the data set and then take as statistic the maximum value of these local information measures as obtained by maximizing over a suitable choice of grid. The authors compare with several other classifiers on simulated and real data with apparently good results. Some limitations of the method are identified in a later article by Reshef et al. (2013). Another follow-up article is Chen et al. (2016). See also Kinney and Atwal (2014), Reshef et al. (2014) and Murrell, Murrell, and Murrell (2014). There are, however, publications where the results are more mixed. See Simon and Tibshirani (2014) and Gorfine, Heller, and Heller (2012). In particular these two papers give several examples where the MIC is clearly inferior to dcov.

The two final papers in this category are Wang et al. (2015) and Wang et al. (2017). In both papers the authors defines the locality by means of a neighborhood of and then consider suitable -values. Consequently, as remarked by Wang et al. (2015) their test may be best suited to nonlinear regression alternatives of the form . Wang et al. (2015) denote by , observations of the stochastic variables and in the construction of their CANOVA test statistic. They define the within neighborhood sum of squares statistic as

where is an integer constant which is supposed to be chosen by the user. Then defines the -neighborhood structure. The assumption of CANOVA is that dependence should imply that “similar/neighbor -values lead to similar -values”. Thus when and are dependent, small values of are expected. Critical values of is determined by permutations. The test for 4 values of (2, 4, 8, 12) is compared to a number of other tests among them Pearson’s , the Kendall and Spearman correlation coefficients, dcov, MIC, and the Hoeffding-test based on the empirical distribution function. The CANOVA tests does not do particularly well for linear models and it fails for the circle data with weak noise, but its performance on the tested nonlinear examples is very good.

The paper by Wang et al. (2017) follows much of the same pattern and ideas. The -values are first used to construct bagging neighborhoods. And then they get an out-of-bag estimator of , based on the bagging neighborhood structure. The square error is calculated to measure how well is predicted by . Critical values are again obtained by permutations in the resulting statistic. In a comparison with other methods five out of eight examples consist of various sinusoidal function with added noise, where the new test does very well.

5 Beyond Pearson’s : Local dependence

The test functionals treated in Section 4 deal with the the second aspect of modelling dependence stated in the beginning of that section, namely that of testing of independence. These functionals all do so by the computation of one non-negative number, which is derived from local properties in Section 4.6. This number properly scaled may possibly be said to deal with the the first aspect stated, namely that of measuring the strength of dependence. But, as such, it can be faulted in several ways. Unlike the Pearson , these functionals do not distinguish between positive and negative dependence, and it is not local, thus not allowing for stronger dependence in multivariate tails as is felt intuitively is the case for data in finance for example.

In Section 6 the main story will be the treatment of local Gaussian correlation which in a sense returns to the Pearson but a local version of which satisfies many of Rényi (1959)’s requirements. But first, in the present section, we go back to some other attempts to define local dependence, starting with a remarkable paper by Lehmann (1966), who manages to define positive and negative dependence in a quite general nonlinear situation.

5.1 Quadrant dependence

Lehmann’s theory is based on the concept of quadrant dependence. Consider two random variables and with cumulative distribution . Then the pair or its distribution function is said to be positively quadrant dependent if

| (35) |

Similarly, or is said to be negatively quadrant dependent if (35) holds with the central inequality sign reversed.

The connection between quadrant dependence and Pearson’s is secured through a lemma of Hoeffding (1940). The lemma is a general result and resembles the result by Székely (2002) in his treatment of the so-called Cramér functional, a forerunner of the Cramér - von Mises functional. If denotes the joint and and the marginals, then assuming that the necessary moments exist,