Optimal Weighted Low-rank Matrix Recovery with Subspace Prior Information

Abstract

Matrix sensing is the problem of reconstructing a low-rank matrix from a few linear measurements. In many applications such as collaborative filtering, the famous Netflix prize problem, and seismic data interpolation, there exists some prior information about the column and row spaces of the ground-truth low-rank matrix. In this paper, we exploit this prior information by proposing a weighted optimization problem where its objective function promotes both rank and prior subspace information. Using the recent results in conic integral geometry, we obtain the unique optimal weights that minimize the required number of measurements. As simulation results confirm, the proposed convex program with optimal weights requires substantially fewer measurements than the regular nuclear norm minimization.

Index Terms:

Conic integral geometry, Matrix sensing, Subspace prior information, .I Introduction

Low rank matrix recovery (also known as matrix sensing) has appeared in numerous applications in recent years. For example, Netflix prize problem[1, 2], collaborative filtering[3], seismic data interpolation[4, 5], system identification [6], and sensor network localization[7]. Mathematically, our goal is to recover a low-rank matrix with rank from a few linear measurements of the form , where is a linear operator. An idealistic approach is the following optimization problem:

| (1) |

However, this problem is NP-hard and computationally intractable. A common alternative is to relax the objective function into the closest convex function. In fact, since rank is the number of nonzero elements of the singular value vector, its convex relaxation amounts to norm of this vector known as the nuclear norm of the matrix. Then, one may solve the following convex problem:

| (2) |

where computes the sum of singular values. A special case of matrix sensing known as matrix completion is to complete from a few observed entries:

| (3) |

where is the sampling operator that extracts the observed entries of . Let us denote the column and row spaces of by and , respectively. By solving (I) or (I), with high probability, one can successfully recover by observing entries111For the sake of simplicity, we investigate only square matrices in this work. The extension to non-square matrices is straightforward.[8]. The main challenge in recovering in the problems (I) and (I) is to identify column and row spaces of . If they are known, one can recover from at most linear measurements of the form where and are orthonormal bases of and , respectively222In this paper, we occasionally use instead of to avoid complexity.. In this work, we consider the matrix sensing problem when prior information about the row and column spaces of is available. To be precise, consider two -dimensional subspaces and withe known principle angles333See Section II-A for definition. with the column and row subspaces of , i.e. and , respectively. Intuitively, if and it seems that one can recover using less measurements compared to the prior-less case. Interestingly, this case happens in many applications of interest. For example, in recommender systems, similar users share similar attributes and knowing how a particular user rates a particular item, provides some prior subspace information about the row and column spaces of the ground-truth matrix.

I-A Motivations and Conjectures

The problem (I) is connected with a large body of literature known as compressed sensing (CS) pioneered by the works in [9] and [10]. In the same way that minimization seeks for the sparsest solution in vectors, aims at recovering the minimum rank solution under a suitable incoherent sensing operator. Naturally, there exists a parallel between CS and matrix sensing. In fact, minimization is a special case of the nuclear norm minimization in which is diagonal. A general question is whether the parallels between compressed sensing and matrix sensing always hold? Let us consider a relevant example. It is known that prior information about the support (non-zero locations) of a vector can be incorporated into minimization by assigning larger weights to the off-support locations than support locations444In fact, inaccurate locations are penalized more.[11], leading to a reduction in the required number of measurements. Now, let us go back to the matrix world. Consider a matrix that lives in a union of row and column subspaces denoted by . Suppose that we are given a subspace that is slightly mis-aligned with . Can we hope for a reduction in the required number of measurements by penalizing the orthogonal complement of ? Are the parallels still strong?

I-B Notation

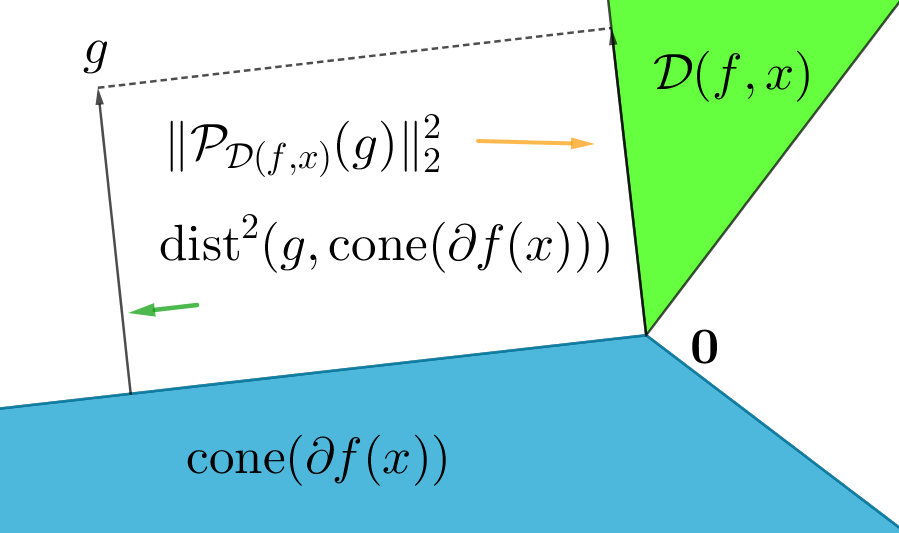

Throughout the paper, scalars are denoted by lowercase letters, vectors by lowercase boldface letters, and matrices by uppercase boldface letters. The th element of a vector is shown either by or . denotes the pseudo-inverse operator. is the identity matrix of size . The complement of an event is shown by . The nullspace of linear operators is denoted by . For a matrix , the operator norm is defined as . The unit ball and unit sphere are shown by and , respectively. Also, we have which refers to the -ball of matrices according to the Frobenius norm. Consider a matrix with reduced SVD form . Define and . We denote the matrix by the notation . Also define the support of by the linear subspace

| (4) |

where and are unique orthogonal projections onto and , respectively. and are the projection of matrix onto the linear subspace and , respectively, and are defined as

We represent the projection onto a cone with a same notation; namely,

| (5) |

The polar of a cone is defined as . for a vector means that . Also, by , we mean . is a diagonal matrix in which the main diagonal is determined by the elements of . For a function , stands for the adjoint of the function . denotes the singular values of sorted non-increasingly. , and denote , and , respectively. denotes the Frobenius inner product of two matrices and .

I-C Contributions

In this work, we propose a new approach for exploiting the prior subspace information leading to a considerable reduction in the required number of measurements. Consider a rank matrix with column and row subspaces and . Assume that we are given two subspaces and , each with dimension , that have known angles from and . Let and 555Throughout, we will occasionally exclude the symbol when referring to angle degree for the sake of simplicity. represent the principle angles that and form with and , respectively. We implicitly take these prior subspace information into account by proposing the following optimization problem.

| (6) |

where,

| (7) |

The weights and reflect the uncertainty in the prior column space information. The same argument holds for and in the prior row space information. In this work, we obtain the unique weights that minimize the required number of measurements. These weights are optimal since they minimize the number of measurements that needs for exact recovery of . To find optimal weights, we exploit the concept of statistical dimension in conic integral geometry. The statistical dimension specifies the boundary of success and failure of . To be precise, we obtain upper and lower bounds with asymptotically vanishing distances for the statistical dimension of a certain convex cone and thereby calculate a threshold for the minimum required number of measurements. Then, we solve the optimization problem

| (8) |

to reach the optimal weight vector . To better highlight our contributions, we summarize the novelties below.

-

1.

Proposing a new optimization model for matrix sensing: We propose a new convex optimization problem in (I-C) that promotes both rank and subspace information. A benefit of this model is that by suitably tuning the weights, it consistently outperforms even when the accuracy of subspace prior information is unreliable. When , the prior information is reliable and less penalty is assigned to than . The same argument applies to . If the subspace prior information is at the boundary of reliability (i.e. ), then by setting , reduces to .

-

2.

Obtaining an upper-bound for the required sample complexity of : We obtain a closed-form relation for the sufficient number of measurements that needs for successful recovery (denoted by ). This bound depends on the weights and the principal angles . By setting , the bound simplifies to the required sample complexity of .

-

3.

Obtaining an error estimate bound for : We prove that the sufficient number of measurements (i.e. ) is also necessary for successful recovery. To be more precise, we show that differs from the minimum required number of measurements up to an asymptotically vanishing term.

-

4.

Proposing a new strategy for finding optimal weights: In the proposed model (I-C), we obtain the weights that minimize the required sample complexity for exact recovery. If one takes the sample complexity as the optimality criterion, then, these weights are optimal. Also, we show that, they are unique up to a positive scaling. We further propose a simple algorithm (called Optweights) that efficiently computes the unique optimal weights.

-

5.

Obtaining closed-form expressions for and : We find that the spaces and sign of (i.e. and , respectively) are rotated versions of spaces. More precisely,

for any arbitrary , where and are some orthonormal bases of , which explicitly depend on the weights and the principal angles , .

-

6.

Obtaining the limiting behavior of spectral functions: For any non-increasingly ordered vector and Gaussian ensemble with , we obtain a closed-form relation for the limiting behavior of

I-D Intuition

The optimal weights in depend on the orientation of the subspace with respect to . Before we provide our analytical results, we intuitively describe the behavior of the weights in special cases of the relative orientation.

-

•

When the principle angles between and with dimensions and , respectively, are all small (close to ), provides a good estimate of and we expect to be small (penalization weight for ). In contrast, is a poor estimation of which should be significantly penalized (large ). Further, if , it is expected that the required number of measurements for approaches the optimal value .

-

•

When the principle angles are all large (close to ), provides a fair estimate of ; therefore is expected to be large, while shall be small. Again, we predict a reduced number of required measurements for .

-

•

When are all around , and are the same in terms of similarity to . This means that the available data does not add any useful information for the recovery. Alternatively, all the weights become equal and the weighted problem simplifies to the standard problem . Hence, we expect the same number of measurements.

-

•

When the angles are evenly distributed around (for instance, ), we expect a similar case as if all the angles were . This is partly because of the fact that both and will have the same set of principal angles with , and partly because we penalize all the subspace with a single weight. In other words, the directions in are on average unrelated to , while some specific directions might be close to .

Similar statements also hold for row space prior information and .

I-E Applications

The application of subspace prior information in matrix sensing is very broad (seismic data interpolation [5], FDD666Frequency division duplexing. massive MIMO777Multiple input multiple output. [12], Dynamic sensor network localization[7], collaborative filtering [3], Netflix problem [1] and subspace tracking); we list some of them below.

-

•

The Netflix problem[1]. Let us consider a large pool of movies which are seen or could potentially be seen by a pool of users. The Netflix matrix is formed by the rating of the users to the movies; the rows correspond to the movies and the columns to the users. The element in the th row and th column represents the score that user gives to the movie . However, many of such scores are unavailable, as not all users have seen all the films. The challenge is to estimate the unavailable scores based on the known values. It is well-studied that the Netflix matrix can be fairly approximated to be low-rank; therefore, matrix completion techniques based on relaxing the rank constraint are popular for solving the problem. In some cases, nevertheless, we might have prior information about the Netflix matrix that could improve the performance of the completion task. For instance, we might know in advance that the scores of a certain user is not much affected by the music of the movie, while the special effects significantly influences his/her scores. Another case of prior information happens in film festivals where the movies are first evaluated by professionals and critics before ordinary users. In both cases, the prior information can be translated into the angles between the columns of the Netflix matrix and some known subspaces (e.g., the subspace generated by the average score of the professionals).

-

•

Subspace tracking. In many setups such as in radars, it is important to estimate the subspace of the signal (e.g., to denoise the signal). Nevertheless, due to the dynamics of the system, this subspace is constantly evolving. In subspace tracking one aims at updating the estimate for the subspace based on the previous estimates and some measurements related to the recent state of the subspace. In other words, the partial similarity of the current signal subspace to its previous states is used as a key to reduce the number of required measurements.

-

•

Dynamic sensor network localization[7]. Consider a moving network of low-power sensors scattered in an area (e.g., in the sea). The goal is to locate various objects in this area based on the observed distances to some neighboring sensors. For this purpose, the relative position of the sensors should be determined first. However, each sensor can measure its distance to only nearby sensors. It is well-known that the matrix formed by the pairwise squared distances of the sensors is low-rank; however, only some of the elements of this matrix are measurable and the matrix is also dynamically changing. Again at each time instance, the similarity of the distance matrix to its previous versions can be employed to enhance the quality of its estimation.

-

•

Time-varying channel estimation in FDD massive MIMO communication[12]. Let us imagine a multi-user wireless communication system in which the users with single-antenna transmitters are communicating with a multi-antenna base-station. The users are generally moving which makes the communication channels time-varying. It is known that due to the correlated nature of the user channels, the matrix constructed by the channel impulse responses (channel matrix) is low-rank [12]. Besides, the physical movement of the users compared to the communication rate is rather slow; hence, the channel matrix at each time instance can be fairly estimated using the previous time instance. Indeed, the associated channel Doppler frequency provides a maximum level of dissimilarity between the channels at consecutive time instances (could be interpreted as upper-bounds on the angles between the subspaces). By exploiting this property, one can reduce the transmission overhead reserved for channel estimation (pilots), which in turn increases the spectral efficiency.

I-F Roadmap

The paper is organized as follows. A more clear definition of principal angles between subspaces besides a few concepts from convex geometry are reviewed in Section II. Section III is dedicated to obtaining bounds for the required number of measurements in and . Section IV is about our strategy of finding optimal weights. In Section V, we present some numerical experiments which validate our theory. We shall describe related works in Section VI. Section VII is devoted to important lemmas that frequently used in our analysis. Lastly, the paper is concluded in Section VIII.

II Preliminaries

II-A Principal angles between subspaces

Consider two subspaces and of an Euclidean vector space with . There exist non-increasingly sorted angles called the principal angles, the least one is obtained by:

| (9) |

The th one () is given by:

| (10) |

are called principal vectors. Moreover, each subspace is spanned by a set of linearly independent vectors. In fact, there exist orthonormal bases and for subspaces and , respectively. Also,

| (11) |

where

| (12) |

In the following, basic concepts of convex geometry are reviewed.

II-B Descent Cones

The descent cone at a point consists of the set of directions that do not increase and is given by:

| (13) |

The descent cone reveals the local behavior of near and is a convex set for convex functions. There is also a relationship between decent cone and subdifferential [13, Chapter 23] given by:

| (14) |

II-C Statistical Dimension

Definition 1.

Statistical Dimension[14]: Let be a convex closed cone. Statistical dimension of is defined as:

| (15) |

where, is an i.i.d. standard normal vector and is the projection of onto the set defined as: .

Statistical dimension extends the concept of linear subspaces to convex cones. Intuitively, it measures the size of a cone. Furthermore,

| (16) |

determines the precise number of measurements corresponding to the transition from failure to success in .

II-D Optimality Condition

In the following, we characterize when succeeds in the noise-free case.

Proposition 1.

[15, Proposition 2.1] Optimality condition: Let be a proper convex function. The vector is the unique optimal point of if and only if .

The next theorem determines the number of measurements needed for successful recovery of for any proper convex function .

Theorem 1.

[14, Theorem 2]: Let be a proper convex function and a fixed sparse vector. Suppose that independent Gaussian linear measurements of are observed via the affine constraint . Then, for a given tolerance if

we have

Besides, if

then,

Also in [14], the following error bound for the statistical dimension is provided:

Theorem 2.

[14, Theorem 4.3] For any :

| (17) |

III The measurement Threshold for successful recovery

Fix a probability of failure . Denote the normalized number of measurements that and need for exact recovery of a matrix by

respectively. In [14, Proposition 4.7], an upper-bound for is provided. To facilitate the calculations, we obtain an upper-bound for in harmony with our strategy of finding optimal weights in this work. The proposed upper-bound asymptotically equals the upper-bound in [14, Proposition 4.7].

Proposition 2.

Consider a matrix with rank . Suppose that with limiting ratios and with . Then,

for

| (18) |

with

| (19) |

where

| (20) |

and

| (21) |

Proof. See Appendix A-D.

Remark 1.

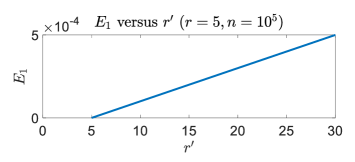

(Prior work) In [14, Equation 4.8] an upper-bound is derived for . Here, we compare our bound i.e. with theirs. Denote the difference between and the upper-bound in [14, Equation 4.8] by . From Figure 3, we observe that the error is negligible when is not far from which is practically common. Moreover, since the upper-bound [14, Equation 4.8] describes well (the error is at most ), regarding Figure 3, one can infer that also approximates suitably up to an asymptotically vanishing error term.

In what follows, we obtain an upper-bound for . This bound helps us to find the optimal weights later. The strategy of providing this bound is, to some extent, similar to the strategy used in Proposition 2. However, the derivation is more elaborate; in fact, this bound, unlike , depends on the principal angles i.e. and the weight vector making it more involved.

Proposition 3.

Consider a rank matrix with column and row subspaces and , respectively. Also, assume that we are given the subspaces and with dimension that have known principal angles and with and , respectively. Then,

| (22) |

for

| (23) |

with

| (24) |

where

| (25) |

| (26) |

| (27) |

Proof. See Appendix A-E.

Remark 2.

(Special case of Proposition 3) Interestingly, coincides with when we set . In other words, this implies the fact that the required number of measurements of in the special case of is the same as the number of measurements that needs for successful recovery.

From Remarks 1 and 2, it is obvious that is the same as . Thus, one could simply think of the following question:

-

•

Is a good description of ?

In the following Lemma, we provide a positive answer to this question. In fact, we demonstrate that the proposed upper-bound in Proposition 3 is asymptotically tight.

Lemma 1.

The number of measurements that with parameters and , needs for exact recovery of satisfies the following error bound:

| (28) |

where

Proof. See Appendix A-F

It is worth mentioning that the error term is independent of , constant and vanishes asymptotically.

IV How to find optimal weights

In this section, we propose the strategy of finding the unique optimal weights. First, we present a general Lemma about the function . Actually, this Lemma states that this function (ignoring the infimum on in the definition of statistical dimension) is strictly convex with respect to . This Lemma helps us later in proving the uniqueness of optimal weights.

Lemma 2.

Assume does not contain the origin. Also, denote a random matrix with i.i.d. standard normal entries. Consider the function

| (29) |

The function is strictly convex and continuous at . Further, it attains its minimum in the set .

Proof. See Appendix A-G.

Now, we introduce our strategy of finding the unique optimal weights. Consider the error bound in Lemma 1. By taking infimum from both sides, it holds that

| (30) |

is surrounded by the same upper and lower-bounds up to an asymptotically vanishing constant term. We minimize this expression so as to reach the optimal weights via

| (31) |

The reason to name these weights, optimal, lies in the fact that they asymptotically (as ) minimize the required number of measurements in . Note that in the second equality of (IV), we converted two variables and into a single vector variable . This is since in of (3) always appears along with the scalar (namely in the form of ). Therefore, by finding (last term in (IV)), we can reach the optimal weights up to a positive scaling factor. As a matter of fact, by the aid of Lemma 2, is unique and lies in the set . Hence, is unique up to a positive scaling factor. Note that this scaling factor is not the case since it is effectless on . To obtain in (IV), we propose a simple algorithm in Algorithm 1 called Optweights. In Optweights, we solve the convex optimization problem

| (32) |

to reach the triple .

Qualitatively speaking, Algorithm 1 is based on alternating minimization (AM) approach. AM method is used to solve multivariate unconstrained optimization problems. The idea is based on optimizing each coordinate, individually. The advantages of our proposed algorithm are

-

•

Each iteration is cheap.

-

•

Unlike the gradient-based algorithms, it needs no step-size tuning.

-

•

It is simple to implement.

In essence, Optweights (Algorithm 1) converts the multivariate optimization problem into some with scalar variables. For solving scalar optimization problems in Optweights (i.e. Step 10 in Algorithm 1), we use Golden Section Search (GSS) method (Algorithm 2) which tries to narrow the range of values ( and in Algorithm 2) inside which the minimum is known to exist.

V Numerical experiments

In this section, we present the result of some computer experiments designed to evaluate the effect of optimal weighting strategy in matrix sensing given some prior subspace information. Note that the optimal weights are obtained using Algorithm 1. First, we construct a matrix

| (33) |

with . Then, we construct two subspaces and with dimension , that have known principal angles and with column and row subspaces of the ground-truth matrix i.e. and , respectively. Note that, the bases and are chosen such that

Next, we compute the optimal weights by Algorithm 1. We compare with for different and . Our assessment criterion is the probability of success over Monte Carlo trials. A trial is declared successful if

| (34) |

where is the solution of optimization problems provided by CVX MATLAB package [16]. Below, we investigate different cases of principal angles.

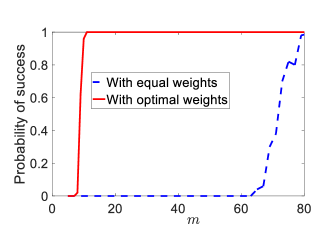

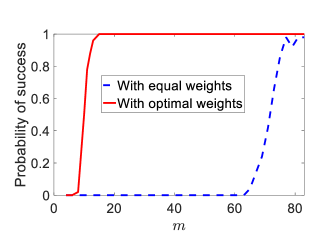

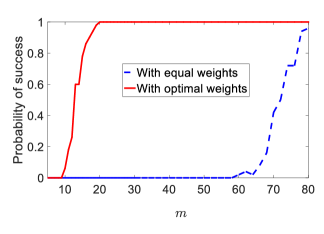

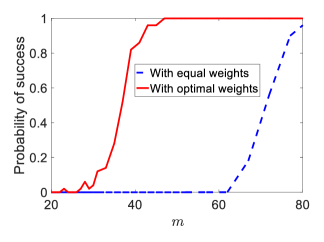

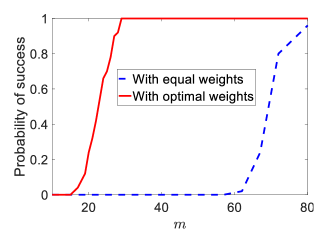

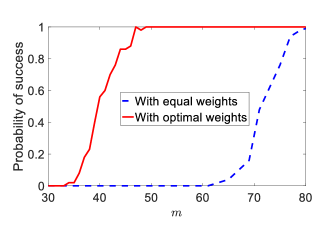

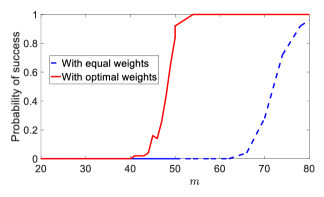

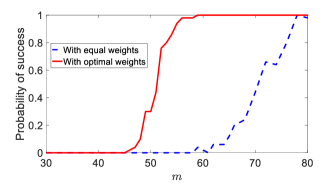

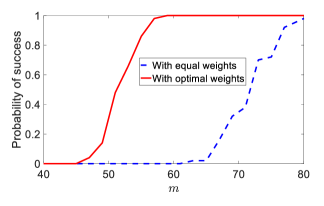

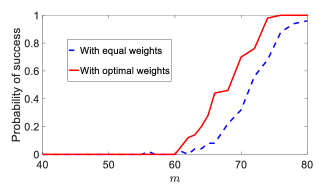

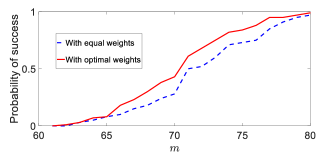

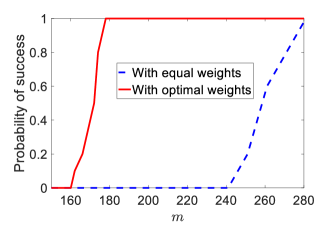

In Figure 4, we tested some cases of excellent prior subspace information in which and are slightly diverged from and . Also, we set the deviation level of column and row subspaces roughly the same. From Figures 4–4, it is observed that the required sample complexity of reaches the optimal number of measurements i.e. . Besides, its sample complexity is far from that in . In Figure 5, and , are close to and , respectively. Figures 5–5 show that even when and are very far from and , respectively, the reduction of sample complexity is possible. It is worth mentioning that one can also hope to reach the optimal number of measurements when there exists a subspace with dimension that is very close to . This case can be observed in Figure 5.

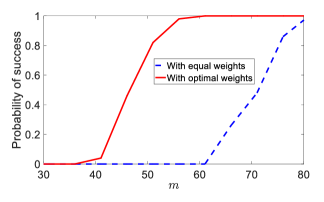

In Figure 6, we test a scenario where the principal angles are not so small but less than . One can see from Figures 6–6 that as much as the principal angles get less, more reduction is achievable in the required sample complexity.

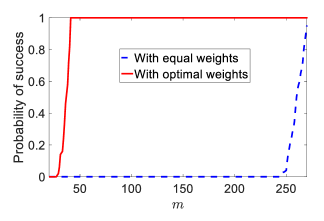

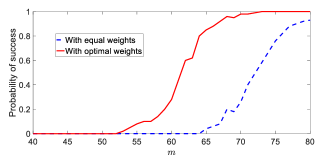

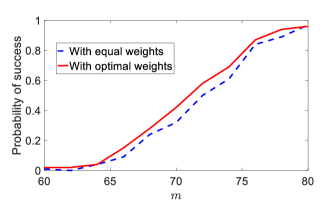

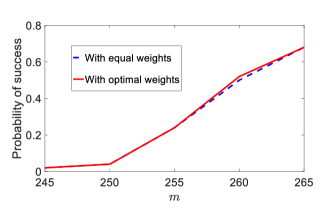

In Figure 7, optimal weighting strategy is investigated when there exists weak prior subspace information about the column and row space of . By weak prior, we mean a case that and are almost as close to and as they are to and . In these cases, (see Figures 7–7) the sample complexity of our algorithm approaches the one in .

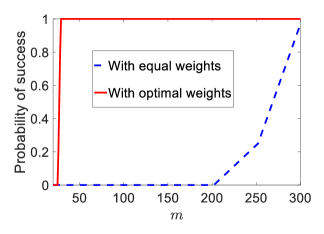

In the last experiment shown in Figure 8, we consider the case where accuracies of and are different. From Figures 8–8, it is observed that a huge sample complexity reduction is feasible when either prior column or row subspace information is close to the respective subspaces of the ground-truth matrix.

![[Uncaptioned image]](/html/1809.10356/assets/x19.png)

![[Uncaptioned image]](/html/1809.10356/assets/x20.png)

![[Uncaptioned image]](/html/1809.10356/assets/x22.png)

VI Related works and Key differences

In [3], a non-uniform sampling distribution is considered for a Netflix data set and is shown that a properly weighted trace norm of the form

| (35) |

works well where and are the probability of observing row and column of the matrix.

In [17], a non-uniform sampling scheme is considered in which the authors propose a generalized nuclear norm which penalizes the directions in the vector space of non-uniformly; namely, allocates larger weights to certain directions than others.

In [5], the authors heuristically propose the following optimization problem to exploit prior subspace information:

| (36) |

where and with dimension are the estimates of column and row subspaces of the rank ground-truth matrix , , and is an upper-bound for . However, they did not answer how to explicitly find and .

In [18], the authors investigated the same objective function as in [5]. They showed that the isometry constant for can be more conservative and thus the required bound for robust recovery can be lowered provided that the prior subspace information is good (). Only in case of , they suggest to choose so as to maximize the RIP bound. There are some key differences between our work and [18] which are listed below:

-

•

They assume that the subspace estimate and the ground-truth subspace are of the same dimension . This assumption fails to occur in practical scenarios in some certain settings for example in Netflix problem where a higher dimensional subspace estimate is available to the practitioner (see Subsection I-E for more explanations). In our work, we consider a generalized case where high dimensional row and column subspaces are angled from the row and column subspaces of interest.

-

•

The meaning of optimal in that work differs from ours in that their weights maximize the RIP constants while ours minimize the required sample complexity.

-

•

[18] considers only the effect of the largest principal angle on the performance bounds while in fact all principal angles directly affect the performance bounds.

-

•

The measurement bound in [18] depends on while our bound is independent of the sampling operator.

-

•

There is a wide range of principal angles () for which no improvement is predicted in [18], inevitably reaching the performance bound of . The only exception that our algorithm reaches the performance bound of is the case . For instance, is considered to be a weak prior subspace information in [18], while it is excellent in our work, leading to a huge sample complexity reduction. Also, when , unlike ours, their bound is not optimal in the sense of sample complexity. Overall, our proposed method acts much better in terms of the required sample complexity.

VII Useful Lemmas

VII-A Constructing a basis for

In this section, we find a special basis for that simplifies the sample complexity analysis in . The following lemma precisely states this.

Lemma 3.

Consider a rank matrix with column and row subspaces and , respectively. Also, assume that we are given the subspaces and , each with dimension , that have known principal angles and with and , respectively. Then, there exist bases , , , and

such that

| (38) | |||

| (39) |

where

and is defined as

| (41) |

Lemma (3) allows us to find which is later helpful. Below, we state a lemma that includes this, along with a crucial decomposition of for an arbitrary matrix .

Lemma 4.

Consider a matrix with column and row spaces and , respectively. Then, in (I-C) with the convention for an arbitrary matrix is decomposed as:

| (42) |

where, and are defined in Lemma 3. Also,

| (47) | |||

| (52) | |||

| (53) | |||

| (54) | |||

| (55) |

where

| (56) | |||

| (57) | |||

| (58) | |||

| (59) |

and , , and are orthonormal bases. Also, and are upper-triangular matrices.

Lemma 5.

Let be the reduced SVD form of . Then, the unsorted SVD of is obtained as

| (60) |

Corollary 1.

Let and . Then, and for an arbitrary matrix are obtained by

| (61) | |||

| (62) |

Proof. See Appendix A-H

VII-B Spectral Analysis of Large Random Matrices

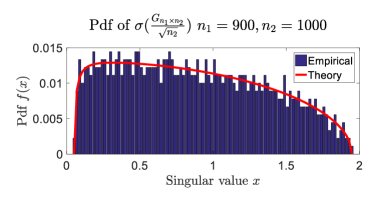

In this part, we aim at specifying the behavior of singular values of large i.i.d. random Gaussian matrices e.g. . First, we state a well-known fact that specifies the limiting behavior of eigenvalues of random matrices to the Marčenko Pastur law [19] ([20, Theorem 3.6]). Here, we approximate the distribution of singular values of a random i.i.d. standard normal matrix by a version of Marčenko–Pastur Law [19]. The proof uses a change of variable to match the argument for singular values which does not much differ from [20, Theorem 3.6] and thus we omitted the uninteresting details of this change.

Fact 1.

Let () be a matrix with i.i.d. standard normal distribution, , and be defined as in (20). Then, the probability density function (pdf) of is given by:

| (63) |

One can see from Figure 9 that the empirical density estimate of singular values of a random matrix with Gaussian ensemble (shown with bars) harmonizes with the obtained bound in Fact 1 (shown with dashed line).

In the following lemma, we obtain the limiting behavior of for a non-increasingly ordered vector .

Lemma 6.

Consider a random matrix whose elements are drawn from i.i.d. standard normal distribution. Let be the non-increasingly ordered elements of . Suppose and . Then, we have:

| (64) |

where and are defined in (20).

Proof. See Appendix A-I.

Remark 3.

(On the tightness of in (6)) In the proof of Proposition 3, we face examples of (6) for which (usually is chosen to be small while is large) and is chosen as

| (65) |

where is a scaling factor (usually less than one) and is a random matrix 888The matrix in the proofs of Proposition 3 is deterministic and not random. However, the final result shall not be much different. distributed as . We test some examples of this flavor in Table I and the upper-bound is numerically observed to be tight for the mentioned cases. Noteworthy, if s are all equal, the inequality in (6) turns into equality.

VIII Conclusion

In this work, we presented a new approach for exploiting subspace prior information in matrix sensing. We assumed that two given subspaces form some known angles with the column and row spaces of the ground-truth matrix. We exploited these angles by introducing a new weighted optimization problem and obtained the unique optimal weights that minimize the required number of measurements. The outcome of our work is to use considerably less measurements compared with the regular nuclear norm minimization.

References

- [1] A. SIGKDD, “Netflix,” in Proceedings of kdd cup and workshop, 2007.

- [2] N. Srebro, “Learning with matrix factorizations phd thesis,” 2004.

- [3] N. Srebro and R. R. Salakhutdinov, “Collaborative filtering in a non-uniform world: Learning with the weighted trace norm,” in Advances in Neural Information Processing Systems, pp. 2056–2064, 2010.

- [4] V. Oropeza and M. Sacchi, “Simultaneous seismic data denoising and reconstruction via multichannel singular spectrum analysis,” Geophysics, vol. 76, no. 3, pp. V25–V32, 2011.

- [5] A. Aravkin, R. Kumar, H. Mansour, B. Recht, and F. J. Herrmann, “Fast methods for denoising matrix completion formulations, with applications to robust seismic data interpolation,” SIAM Journal on Scientific Computing, vol. 36, no. 5, pp. S237–S266, 2014.

- [6] M. Fazel, H. Hindi, and S. P. Boyd, “Log-det heuristic for matrix rank minimization with applications to hankel and euclidean distance matrices,” in American Control Conference, 2003. Proceedings of the 2003, vol. 3, pp. 2156–2162, IEEE, 2003.

- [7] A. M.-C. So and Y. Ye, “Theory of semidefinite programming for sensor network localization,” Mathematical Programming, vol. 109, no. 2-3, pp. 367–384, 2007.

- [8] Y. Chen, S. Bhojanapalli, S. Sanghavi, and R. Ward, “Completing any low-rank matrix, provably,” The Journal of Machine Learning Research, vol. 16, no. 1, pp. 2999–3034, 2015.

- [9] E. J. Candes and T. Tao, “Decoding by linear programming,” IEEE transactions on information theory, vol. 51, no. 12, pp. 4203–4215, 2005.

- [10] D. L. Donoho, “For most large underdetermined systems of linear equations the minimal -norm solution is also the sparsest solution,” Communications on pure and applied mathematics, vol. 59, no. 6, pp. 797–829, 2006.

- [11] E. J. Candes, M. B. Wakin, and S. P. Boyd, “Enhancing sparsity by reweighted minimization,” Journal of Fourier analysis and applications, vol. 14, no. 5-6, pp. 877–905, 2008.

- [12] W. Shen, L. Dai, B. Shim, S. Mumtaz, and Z. Wang, “Joint csit acquisition based on low-rank matrix completion for fdd massive mimo systems,” IEEE Communications Letters, vol. 19, no. 12, pp. 2178–2181, 2015.

- [13] R. T. Rockafellar, Convex analysis. Princeton university press, 2015.

- [14] D. Amelunxen, M. Lotz, M. B. McCoy, and J. A. Tropp, “Living on the edge: Phase transitions in convex programs with random data,” Information and Inference: A Journal of the IMA, vol. 3, no. 3, pp. 224–294, 2014.

- [15] V. Chandrasekaran, B. Recht, P. A. Parrilo, and A. S. Willsky, “The convex geometry of linear inverse problems,” Foundations of Computational mathematics, vol. 12, no. 6, pp. 805–849, 2012.

- [16] M. Grant and S. Boyd, “CVX: Matlab software for disciplined convex programming, version 2.1,” Mar. 2014.

- [17] R. Angst, C. Zach, and M. Pollefeys, “The generalized trace-norm and its application to structure-from-motion problems,” in Computer Vision (ICCV), 2011 IEEE International Conference on, pp. 2502–2509, IEEE, 2011.

- [18] A. Eftekhari, D. Yang, and M. B. Wakin, “Weighted matrix completion and recovery with prior subspace information,” IEEE Transactions on Information Theory, 2018.

- [19] V. A. Marčenko and L. A. Pastur, “Distribution of eigenvalues for some sets of random matrices,” Mathematics of the USSR-Sbornik, vol. 1, no. 4, p. 457, 1967.

- [20] Z. Bai and J. W. Silverstein, Spectral analysis of large dimensional random matrices, vol. 20. Springer, 2010.

- [21] R. A. Horn and C. R. Johnson, “Matrix analysis,” 2013.

- [22] R. A. Horn and C. R. Johnson, Matrix analysis. Cambridge university press, 1990.

- [23] D. P. Bertsekas, “Convex optimization theory athena scientific, 2009,” 2014.

- [24] S. Qiao and X. Wang, “Computing the singular values of 2-by-2 complex matrices,” McMaster University, 2002.

- [25] S. Foucart and H. Rauhut, A mathematical introduction to compressive sensing, vol. 1. Birkhäuser Basel, 2013.

Appendix A Proof of Main Result and Lemmas

A-A Proof of Lemma 3

Proof.

Assume and be some orthonormal bases for and , respectively. Also, since and are uniquely characterized by their respective projection matrices i.e. and , without loss of generality, assume that

where , and are orthonormal bases forming the subspaces , , , and , respectively. (otherwise one could redefine , and by taking SVD of and , since rotation in and does not affect and ).

The column space of any matrix in can be decomposed into the spaces , , and , where for the last three, we construct an orthonormal basis as follows:

| (66) |

such that

forms an orthonormal basis for the column span of any matrix in . Similar to the above statements, there exist orthonormal bases

| (67) |

such that

forms an orthonormal basis for the row space of any arbitrary matrix in . Lastly, it is easy to verify that the matrices and can be represented in the bases and as follows:

∎

A-B Proof of Lemma 4

Proof.

Define

The expression in (I-C) can be reformulated as

| (68) |

We start our derivation by (38) and (39) to find , which are the essential components of . By (38) and (39), it is simply holds that

| (69) |

Also, we have:

| (70) |

It also follows that

| (71) |

We next simplify (A-B) by applying a QR decomposition to the matrix in the bracket. Namely,

| (76) | |||

| (81) | |||

| (82) |

where is an orthonormal basis and is an upper-triangular matrix. We rewrite (A-B) as

| (83) |

where the last equality is since . With a similar approach on the row space of , one may write

| (84) |

where

| (85) |

is an orthonormal basis of and

| (86) |

is an triangular matrix. Lastly, for an arbitrary (the relation (68)) may be written as (42). ∎

A-C Proof of Lemma 5

Proof.

Since

| (87) |

it follows that

| (88) |

As is a diagonal matrix, one may deduce from (42) that

| (89) |

provides an unsorted SVD form for . ∎

A-D Proof of Proposition 2

Proof.

Before proving the result, we define some notations which are required in our analysis.

| (90) | |||

are defined in the same way as . We begin the proof by bounding the statistical dimension as follows:

| (91) |

where follows from the fact that the infimum of an affine function is concave and Jensen’s inequality. Next, we proceed by showing that

| (92) |

where in , we decomposed the term in the Frobenius norm into and and used the relation

| (93) |

By using the definitions in Lemma 3, it is straightforward to check that

for an arbitrary matrix . Hence,

| (94) |

where in , we also used the rotational invariance of spectral norm. By rewriting and simplifying the above expression, we reach

| (95) |

where in , as and have orthonormal columns, the entries of are i.i.d. standard Gaussian which, without loss of generality, we denote by again. For simplicity, we replaced by . We also used the rotational invariance of Frobenius and spectral norms. By further simplifying, we reach

| (96) |

In , we only used the fact that the entries of , and have i.i.d. standard normal distribution. Borrowing the notations of (90), one may write

| (97) |

In , we decomposed the space into the spaces for . Also, we used the relation

| (98) |

where the first inequality is due to the triangle inequality of spectral norm. The second is due to the definition of in (2). In fact,

| (99) |

We further use Hoffman-Wielandt Theorem [21, Corollary 7.3.5] to reach

| (100) |

The minimizations in the above expression have closed form relations. Indeed, its is not hard to check that

| (101) |

for arbitrary scalar and positive . We incorporate this fact into (A-D) to get

| (102) |

Lastly, by invoking Lemma 6 and Remark 3, we obtain

| (103) |

∎

A-E Proof of Proposition 3

Proof.

Before proving the result, we define some notations:

| (104) |

We begin with the definition of which is used in :

| (105) |

where in , we used the chain rule lemma of subdifferential [13, Theorem 23.9]. By using the facts that is a self-adjoint function i.e. and also the decomposition in (42), we rewrite the above expression as

| (106) |

The set is defined as

| (107) |

By incorporating (A-E) into (A-E), we have that

| (108) |

We proceed by writing

| (109) |

where is since are orthonormal bases and Frobenius norm has rotational invariance property. Also, we used the fact that has the same distribution as . So, for simplicity, we replace instead of . By using (61) and (62) in Lemma 5 and replacing by , (A-E) can be further simplified:

| (110) |

In the last expression of (A-E), we decompose the matrices inside the Frobenius norm into the disjoint sets as follows:

| (111) | |||

| (112) |

where and are defined as

| (113) | |||

| (114) |

in this part999The definitions of and in (113) and (114) slightly differ from those in (56) and (57) as the weights are accompanied with .. Moreover, it is straightforward to check that (111) and (112) can be more simplified and rewritten as:

| (115) | ||||

where

Incorporate (115) into (A-E) to reach

| (116) |

Since the entries of and are i.i.d. standard normal variables, we have . Combining (A-E) with the fact (A-D), we reach101010Notice that using the fact (A-D) leads to an asymptotically equal expression due to the explanations in Remark 1 and Figure 3.:

We solve the minimizations in (A-E), one by one: First for the minimization in the second line of (A-E), we have that

| (118) |

where in the above equations, the first equality is due to Hoffman–Wielandt Theorem [22, Corollary 7.3.5]. The equality in (A-E) is because of the relations

| (119) |

[22, Lemma 3.3.8], and the fact that is an increasing convex function on . In (A-E), we benefited from [22, Theorem 3.3.14 a] and [22, Problem 3]. In the third line of (A-E), we use

| (120) |

where the first equality comes from Hoffman–Wielandt Theorem [22, Corollary 7.3.5]. The second is the result of [22, Lemma 3.3.8], convexity besides monotonicity of in the interval and

| (121) |

which follows from [22, Theorem 3.3.14 a]. Other minimizations in (A-E) can be solved using similar strategies. After simplifying , in (A-E) and employing (A-E), (A-E), we may rewrite (A-E) as

A-F Proof of Lemma 1

Proof.

First, define . To control the error term, we benefit from

| (125) |

For any , there exists such that:

| (126) |

In (A-F), follows from a chain rule lemma in subdifferential [23, Chapter 4] namely and Lemma 3. In , the rotational invariance of Frobenius norm is used. In , we used the relation for any conforming matrices . is the result of and rotational invariance of spectral norm. follows from (A-E) and that for any . In , since the singular values of the matrix

| (127) |

which is a submatrix of in 3, are [24, Equation 6], it holds that the singular values of are

| (128) |

Also, the same result holds for the singular values of . Namely,

| (129) |

Hence, . Lastly, is the result of the inequality . Moreover, for the denominator of (125), it holds that

| (130) |

where

| (131) |

In , we used the definition of nuclear norm. In , is obtained from 61. Also, we used the fact that . In , we used 42 and the facts and . is the consequence of the fact that

| (132) |

and only contributes to the Frobenius inner product. follows from Cauchy Schwartz inequality and the rotational invariance of Frobenius norm. By considering (14), (42), the fact that

| (133) |

and (61), does not depend on the singular values of , i.e. . So, a matrix

| (134) |

can be chosen to have equality in . Lastly, follows from the definitions (56) and (57) and some simplifications.

A-G Proof of Lemma 2

Proof.

Continuity in bounded points. For continuity, it must be shown that sufficiently small changes in result in arbitrary small changes in . Let . By definition of , it holds that

| (137) |

Since

| (138) |

(due to A-F)) and

| (139) |

(see (A-F)), we have

| (140) |

As a consequence, we obtain

| (141) |

Since is bounded, continuity holds.

Convexity. Let and . Then,

Since otherwise, we have:

By taking the infimum over , we reach a contradiction. Below, we proceed to prove the convexity of :

| (142) |

Since this holds for any , is a convex function. As the square of a non-negative convex function is convex, is a convex function. Finally, the function is the average of convex functions, hence is convex. In (A-G), the equality comes from the definition of “dist”. uses the argument

| (143) |

In fact, the left and right hand sides of (A-G) have the same value on . To more clarify this fact, when , both the right and left hand sides of (A-G), take the same value

| (144) |

To verify (A-G), it remains to prove

| (145) |

To prove the above equality, we argue by contradiction. Suppose that the above “”turns to “”for all . By setting , we reach a contradiction.

Strict convexity. We prove strict convexity by contradiction. If were not strictly convex, there would be vectors such that

| (146) |

For each in (146), the left-hand side is smaller than or equal to the right-hand side. Therefore, in (146), and are almost surely equal (except at a measure zero set) with respect to Gaussian measure. Moreover, it holds that

| (147) |

where the inequality above, follows from (A-G). stems from the strict convexity of . is due to the definition of . From (A-G), it can be deduced that the set is a convex set. Since the distance to a convex set, e.g. (i.e. ) is a 1-Lipschitz function, namely

| (148) |

and continuous with respect to , is continuous with respect to . Thus, there exists an open ball around that we may write the following relation for some

| (149) |

Since is a measure zero set, the above statement contradicts (146). Hence, we have strict convexity. Continuity besides convexity of implies that is convex on the whole domain .

Attainment of the minimum. Suppose that . Then, we may write:

| (150) |

where in A-G, the inequality comes from triangle inequality of Frobenius norm. The equality is the result of the decomposition provided in Lemma 4 and the rotational invariance of Frobenius norm. Lastly, is obtained by combining the facts

for any non-singular and conforming matrices ,

and (128), (129). By squaring (A-G), we reach

| (151) |

Using the relation ([25, Proposition 8. 1]) and Marcov’s inequality, we obtain

| (152) |

Then, it holds that

| (153) |

where in (A-G), stems from total probability theorem. is since is positive. follows from (151) and (152). Lastly, is because provides a lower-bound for the expression in the brackets inside the expectation.

In (A-G), is because the infimum of an affine function is concave and Jensen’s inequality. In , we set . is because of Hoffman–Wielandt Theorem [21, Corollary 7.3.5]. IV follows from (101). is the result of Lemma 6. is since

| (156) |

comes from is a decreasing function and for sufficiently small is less than . So, this completes the proof. ∎

A-H Proof of Corollary 1

A-I Proof of Lemma 6

Proof.

Define a random vector where its elements s are randomly chosen without replacement from the set . Since s and s are all positive and non-increasingly ordered, it is straightforward to check that

| (158) |

Due to the Fact 1 and the conditional expectation, we may write:

| (159) |

| (160) |

where we used the fact that in the first equality. Now, we use the relation

| (161) |

which comes from the fact that the distribution of singular values of a Gaussian matrix tends to the Marčenko–Pastur law [20, Theorem 3.6] with probability one. By substituting (A-I) into (A-I), we shall have that

| (162) |

which concludes the result.

∎