Inferring Microclimate Zones from Energy Consumption Data

Abstract

Climate zones are an established part of urban energy management. California is divided into 16 climate zones, for example, and each zone imposes different energy-related building standards — so for example different zones have different roofing standards. Although developed long ago, these zones continue to shape urban policy. New climate zone definitions are now emerging in urban settings. Both the County of Los Angeles and the US Department of Energy have recently adopted refined zones — for restructuring electricity rates, and for scoring home energy efficiency. Defining new zones is difficult, however, because climates depend on variables that are difficult to map [1].

In this paper we show that Los Angeles climate zones can be inferred from energy use data. We have studied residential electricity consumption (EC) patterns in Los Angeles data. This data permits identification of geographical zones whose EC patterns are characteristically different from surrounding regions. These regions have topographic boundaries in Los Angeles consistent with microclimates.

Specifically, our key finding is that EC-microclimate zones — regions in which block groups have similar Electricity Consumption patterns over time — resemble environmental microclimate zones. Because they conform to microclimates, but are based directly on EC data, these zones can be useful in urban energy management.

We also show how microclimates and household electricity consumption in Los Angeles are strongly linked to socioeconomic variables like income and population density. These links permit data-driven development of microclimate zones that support zone-specific modeling and improved energy policy.

Index Terms:

Data science • electricity consumption • energy use • economics • econometric models • climate zones • microclimates.I Introduction

Urban energy management is an important problem facing all cities. In this paper, we describe some results of analyses on residential electricity consumption (EC), using monthly consumer data from regional energy utilities, including the Los Angeles Department of Water and Electricity (LADWP), SoCal Edison, SoCal Gas, and others. Specifically, we focus here on analysis of block group totals, giving a summary of EC in small Census-defined neighborhoods.

This increasing availability of data makes it possible to go beyond traditional accounting, and to perform more comprehensive analysis of patterns and processes in energy systems. The Los Angeles electricity consumption data offers examples of the importance of resource flows [2] and of climate [3] in urban design, showing how better understanding of both can prove useful in policy. In particular, we show that it gives insight into connections between EC and microclimates [4].

I-A Climate Zones and Energy Policy

Energy use depends on climate. As a result, in areas like California with diverse climates, climate zones have important roles in energy management. For example, the California Energy Commission has divided the state into 16 Energy Climate Zones [5, 6], such as for coastal Los Angeles (#6), Long Beach/El Toro (#8), and inland Los Angeles/Pasadena (#9). Different energy-related building standards are imposed in each zone, such as for HVAC or roofing.

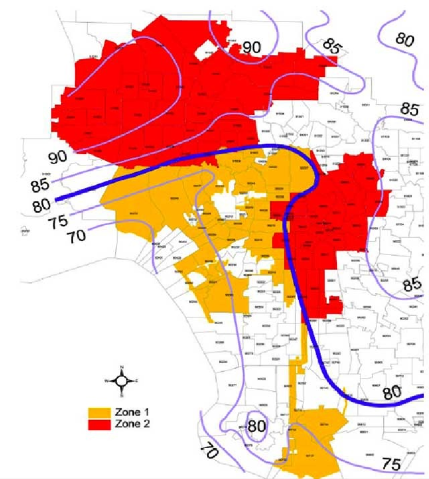

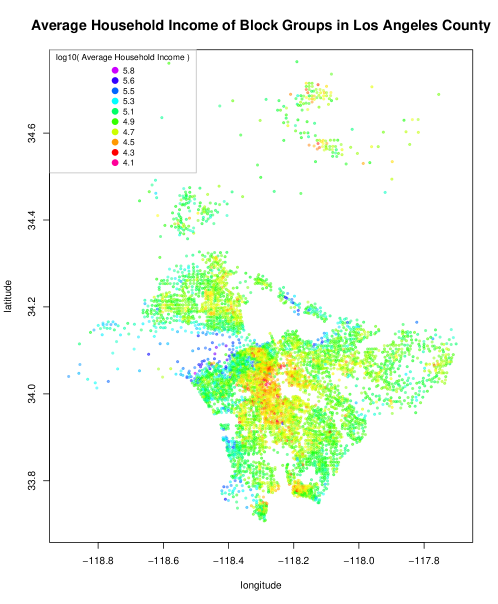

Climate zones also have been used in defining rates, which are vital controls on electricity consumption. LADWP, in its rate restructuring about ten years ago [7], defined two microclimate zones based on historical temperature averages. These zones are shown in Figure 1; Zone 1 (to the west) has higher electricity rates.

Although these zones were defined with energy use in mind, they will need to evolve to remain in step with rapid growth in these areas. Finer zone granularity in Los Angeles could aid in improving energy management.

Faced with increasing complexity of consumer demand and energy supply options, the California Energy Commission and state-wide electricity providers evolved the California IEPR (Integrated Energy Policy Report) over the past decade (e.g., [8, 9, 10, 11, 12, 13]). It has been ‘a biennial integrated energy policy report that assesses major energy trends and issues facing the state’s electricity, natural gas, and transportation fuel sectors and provides policy recommendations to conserve resources; protect the environment; ensure reliable, secure, and diverse energy supplies; enhance the state’s economy; and protect public health and safety’. In IEPR workshops pressing electricity issues are reviewed, with significant impact on urban policy and action plans. Many topics focus on climate.

Recently the state of California embarked on an ambitious plan to improve efficiency: Assembly Bill 758 [14] requires the California Energy Commission, California Public Utilities Commission, and other stakeholders to develop a comprehensive program to increase energy efficiency in existing buildings. An action plan was passed in August 2015 [15] to double energy efficiency savings in retail gas and electricity use by 2030. The December 2016 update [16] reports on complex econometric forecasting models, and strategies that can contribute to this requirement. Progress is being tracked dynamically [17]. New kinds of energy policy are now needed.

Very recently, this ambitious plan became more ambitious. In May 2018, California required solar energy in all new residential construction starting in 2020 [18, 19]. The 2020 energy code also will require greater insulation, window, and appliance efficiencies. In August 2018, California also approved a bill requiring California to generate 100% of its energy from carbon-free sources by 2045 [20]. Furthermore it passed a mandate to generate at least 60% of its energy from renewable resources by 2030. These plans require rapid innovations in energy management.

I-B The Key Idea: Data-driven Microclimate Zones

In [21] we showed that residential electricity consumption data can be sufficient to infer climate. Briefly: home electricity consumption data includes a history of climate.

As a result, we were able to identify microclimates — regional climate patterns — from residential Electricity Consumption (EC) data for Los Angeles. Although these ‘EC-microclimate zones’ were obtained with clustering, they resemble environmental microclimate zones.

Furthermore, a data-driven approach permits the incorporation of quantitative models into policy. In our data, EC-microclimates are strongly linked with economic variables, highlighting connections between climate, economics, and energy use. Existing models can be sharpened for microclimates, and support data-driven energy policy.

I-C Overall Findings

Climate zones have well-established roles in energy policy [5], and Los Angeles is interesting in its diversity of microclimates. We were interested in determining how microclimates are related to residential Electricity Consumption (EC).

Some central findings for our data were as follows:

-

•

EC data can be used to identify zones with similar EC patterns.

-

•

These zones appear strongly related to climate, so we call them EC-microclimate zones.

-

•

These EC-microclimate zones can be validated as corresponding to climate.

-

•

EC-microclimate zones are also strongly linked to income, suggesting that they could be useful in energy-related models and policy.

-

•

more accurate large-scale models for EC can be developed by developing different models for each EC-microclimate zone.

Findings for household electricity consumption (HEC):

-

•

HEC patterns are highly region-specific geographically, in ways related to climate.

-

•

in each EC-microclimate zone, follows a GPRF (Gaussian Process Random Field).

-

•

is highly correlated with socioeconomic variables like income.

-

•

Energy demand () forecasts can be improved by building separate models in each microclimate zone.

The most important finding was that clustering of time series of residential electricity consumption (EC) identified geographic regions of similar patterns that appear related to climate. These EC-microclimate zones, inferred from EC data, have many potential applications in energy managment.

II Electricity Consumption Data Analysis

We analyzed data from the California Center for Sustainable Communities (CCSC) containing 2006-2011 monthly electricity consumption histories for Los Angeles County. An earlier analysis of electricity consumption per capita in California [23] showed both the promise and difficulty of accurate modeling, and the importance of model choice in obtaining forecasts. To gain an understanding of electricity consumption, we analyzed data from about 5000 block groups (census-related street-level geographic regions).

In this paper, for insight into residential electricity consumption patterns, we consider aggregative results for residential block groups in Los Angeles County. Electricity consumption in a block group depends on the number of consumers (‘households’), and the ratio measures household electricity consumption. Our analysis here is based on monthly consumption and household count values in individual block groups. The data ranges can vary by orders of magnitude. We study logarithmically-scaled consumption, which turns out to be approximately normally distributed:

Here ; all logarithms are to base 10 in this paper.

II-A Overview of the Data

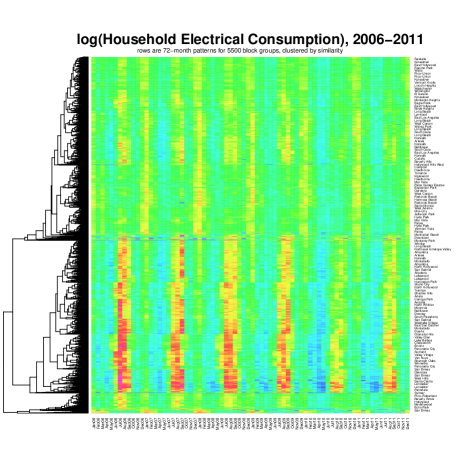

A panoramic display of block group data is in Figure 2. Each row in this figure shows the history of one Census block group in Los Angeles County, showing its variation in consumption over the 72 months 2006-2011. The rows have been hierarchically clustered by similarity (of their consumption pattern); hierarchical structure is displayed in the dendrogram on the left. The neighborhood name for about every 50th block group is shown, suggesting that the clusters correspond both to geographical regions and to climate in Los Angeles.

With the dataset of Figure 2 in mind, in this paper we define an electricity consumption pattern as a sequence of 72 monthly values (over the six years). The patterns show clear annual cycles, with strong seasonal influences on consumption. However, the Summer consumption pattern visible in the lower half of the heatmap appears almost absent in the top half, where the highest consumption appears to be in Winter. The upper half of the table shows very different consumption patterns than the lower half. (The upper half is coastal, while the lower half is inland.)

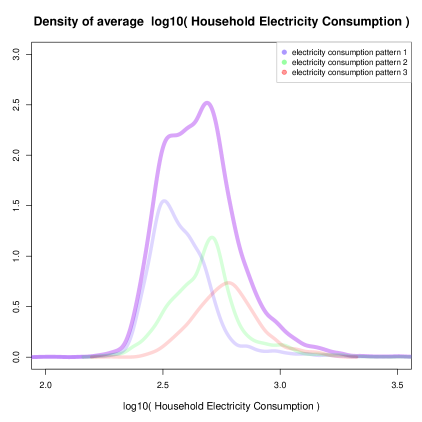

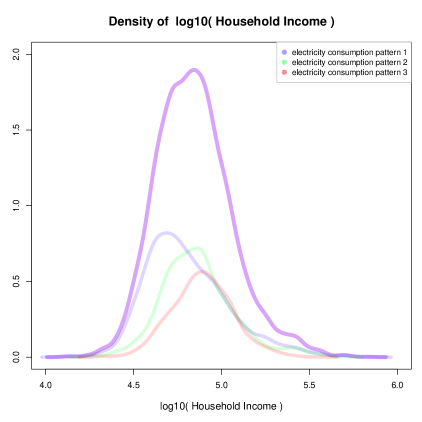

The distribution of Household Electricity Consumption values appears approximately lognormal — i.e., the distribution of is approximately normal. The log-transformed distribution actually has slight positive skew, and is sometimes modeled as a mixture of normal distributions [24].

Figure 6 shows the distribution of over all block groups. The histogram is not quite normal, but resembles a weighted sum (mixture) of normal distributions.

Household Electricity Consumption (HEC) in these zones turns out to be strongly correlated with a number of variables, including income, topography, and property values. HEC patterns in each zone differ seasonally, and are influenced by economic trends over time. Our analysis of patterns suggests the importance of income and economic variables, as well as climate, in the similarity and variability of annual electricity consumption patterns.

II-B log(HEC) as a Gaussian Process Random Field

The HEC data can be modeled as a Log-Gaussian Process over a 2D geographic space. More precisely, when is viewed as a random variable depending on its (longitude,latitude)-coordinates, we claim it can be modeled as a Gaussian Process Random Field.

A Gaussian Process is often defined as a collection of random variables, any finite number of which have joint Gaussian distributions defined by a mean function and covariance function [25]. This is often viewed as describing a distribution over functions, where ‘a finite number of variables’ corresponds to ‘the function values at a finite number of input points’. Specifically, when , are two points of the input space (on which and are defined as functions), functions are said to follow this distribution when

Generally, random processes involve index values like that are one-dimensional (such as ‘time’). When values are -dimensional with , the Gaussian Process is called a Gaussian Process Random Field.

A common form of covariance function on pairs of random variables is the squared exponential

(In Gaussian Process regression, it is common to use instead

where are parameters that are fit by the regression [26, §6.4.2].)

Another way of presenting this is to say that the values are from a continuous input space, and for each , the Gaussian process is a normally distributed random variable. Furthermore, given values , the random variables have a -dimensional normal distribution with mean and covariance matrix with entries .

For our HEC data, we let denote a 2D (longitude, latitude)-position in degrees, and and be two such positions. Then the geographical distance between them is their major-arc distance (when converted to radians), i.e., spatial distance, in miles. Thus is approximately proportional to .

Also, at each such 2D position , we have a random variable . For the block group located at , our dataset contains 72 samples of this random variable, a time series of monthly values over 2006-2011. Treating the samples as vectors, can be estimated as the vectors’ covariance.

We validate these properties below after defining EC-microclimate zones more formally.

III Seasonal Electricity Consumption Patterns and Microclimate Zones

III-A Clustering of EC Patterns

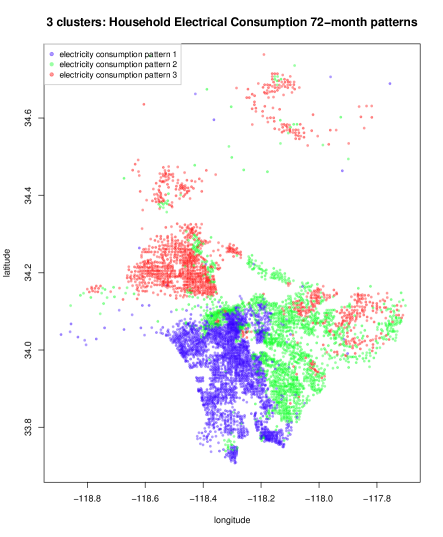

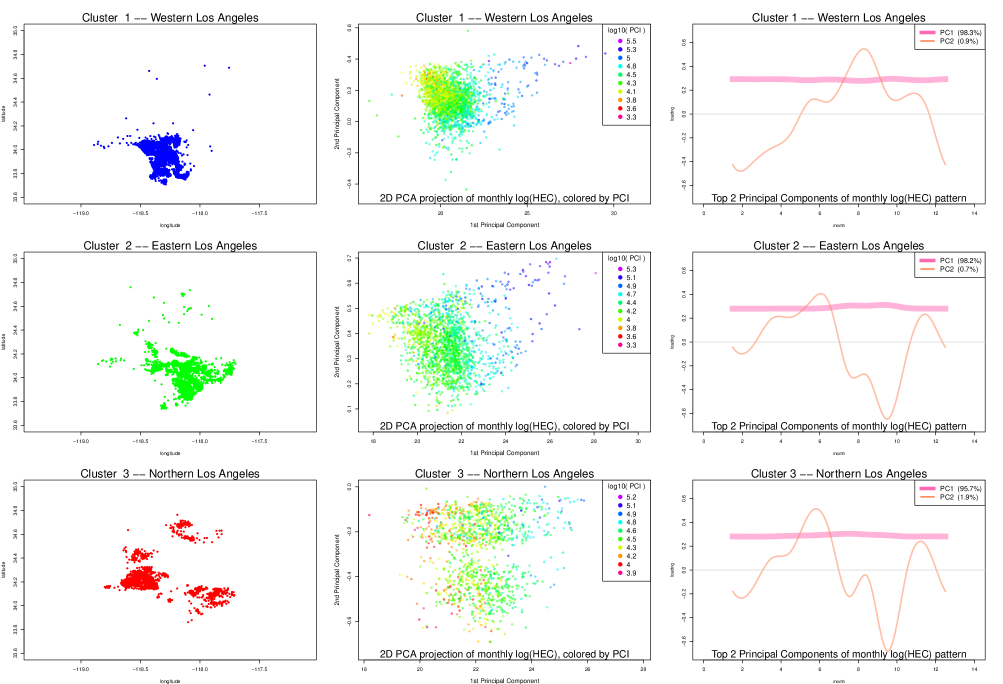

Figure 3 shows three average electricity consumption patterns obtained by clustering, motivated by Figure 2. The EC patterns of each block group (a sequence of length 72 values, for each month over the six years 2006-2011, normalized to total to 1) were clustered using the -means algorithm into = 3 clusters. To visualize the result, a single point was then plotted at the central (latitude,longitude) location of the block group, and colored according to its cluster. The map shows a connection between electricity consumption and geography, suggesting association between EC and climate.

The electricity consumption patterns of each block group were first computed as a sequence of 72 values of , for each month over the six years 2006-2011, that were also normalized to total to 1. These sequences were clustered using the -means algorithm (in R, with standard settings and 25 random restarts) into clusters.

The log-transformation is natural (and matters) for HEC patterns. As mentioned earlier, the distribution of is approximately normal, and the distribution of HEC is highly skewed. Second, numeric measures like HEC are often multiplicative in nature, the product of many independent factors, and so their log is a sum of independent factors (and ultimately: normal). Economic variables that range over multiple orders of magnitude also have this property [27].

The normalization of HEC patterns to total to 1 also matters, as it makes their shape significant, not their scale. If HEC patterns reflect climate variation, and we cluster them by Euclidean distance (as in -means clustering), then the absolute scale of the patterns (scale of consumption) can be factored out; normalization removes this scale. Later on Principal Component Analysis also reveals that patterns in a climate zone differ primarily by scale multipliers. So both log-transformation and scale normalization improve results of clustering.

Other distance measures could have been used in clustering. Correlation of HEC patterns is a natural alternative, for example, and time-series measures of similarity also. Euclidean distance may not be the best measure, but we show later with PCA that annual energy use patterns in each cluster actually have limited variation. Normalizing the total to 1 factors out the scale of the patterns, which turns out to be their primary feature. Normalized patterns can then be compared with Euclidean distance.

III-B EC-Microclimates

A Microclimate is often defined by a restricted range of environmental variables, including temperature, wind, relative humidity, and vegetation [4]. Cities (such as Los Angeles) with diverse patterns of variables support diverse microclimates.

The regions defined by clusters visible in Figure 3 are contiguous geographic regions, although they are defined only by EC patterns. Furthermore, they behave like climate zones, reflecting environmental characteristics that impact electricity consumption over the year. The three regions in the figure — western Los Angeles, the San Gabriel valley, and the San Fernando valley — all have distinct microclimates.

For this reason we refer to them as EC-Microclimate Zones.

It is well-known that microclimates affect energy use [28], but we have not found any discussion of the reverse, i.e., that EC is sufficient to identify microclimate.

This is the central finding of our work: EC-microclimate zones — regions in which block groups have similar Electricity Consumption patterns over time — resemble environmental microclimate zones. HEC data includes a history of climate.

IV Validity of EC-Microclimate Zones as Microclimate Zones

Environmental microclimates appear to cause predictable seasonal EC patterns, and different microclimates have patterns that differ in characteristic ways. Analogously, we can show that EC-microclimates resemble environmental microclimates in several ways: (1) both environmental- and EC-microclimates exhibit random field structure; (2) both conform to topography; (3) the clusters of EC patterns in EC-microclimates exhibit limited variance. In these perspectives, EC-microclimates behave like actual microclimates.

IV-A Microclimates and EC-Microclimates as Random Fields

It has been observed before that microclimate variables (wind speed, local temperature, wind pressure, and total solar irradiation) can be modeled as a Gaussian Process Random Field, and this has been exploited in modeling electricity consumption [1].

In this paper we do the reverse: show that electricity consumption in each zone apparently can be modeled as a random field ( approximates a Gaussian Process). The result is novel, yet consistent with [1]. Both microclimates and EC-microclimates can be modeled by similar random fields. In each zone, is a summary of microclimate variables. So given two distinct microclimates, we expect the patterns of corresponding EC-microclimate zones to be distinct. Figure 4 shows that this does hold for our data.

IV-B Topography, Basins, Valleys, and Microclimates

The EC-microclimate zones in Figure 3 that are bounded by hillsides are essentially basins, each with a distinct climate. Figure 5 shows corresponding Los Angeles topography.

The red region to the northwest is an inland area (the San Fernando Valley), while the blue regions to the southwest are coastal areas (western Los Angeles). These two regions have different climates. The adjacent green region (eastern Los Angeles and the San Gabriel Valley) is surrounded by hills, with a warm climate. In this perspective, clustering the EC patterns has managed to identify regions separated by topography, because their characteristic patterns are distinct.

Generally, EC-microclimate zones we have produced conform to basin-like regions in Los Angeles. In [29] and [30], we show that increasing the value of identifies a more refined set of regions, again with topographical features separating them. Below, we show that limited variance of EC patterns in each zone offers an explanation for this structure.

IV-C Properties of k-Means Solutions

We have used -means clustering to obtain microclimate zones for small values of (up to 10). The -means algorithm performs greedy minimization of the total within-cluster sum of squares [31] for clusters, where the () are clusters with mean , containing points (vectors of 72 values, normalized so that they sum to 1). A natural question is whether this clustering algorithm has some justification.

First, the stability of the clusters obtained is a central question. The number of random restarts used with -means is important here: if the clustering ultimately returned is the best clustering obtained from these restarts, then higher numbers of restarts give more stable results. In other words, the clusters returned by -means are identical more often with more restarts.

Figure 8 shows that, for our data with 100 random restarts, clusters for were stable. More specifically, as nstarts (the number of restarts) increases, the number of points (block groups) with more than one

Beyond this, some data points can lie near the boundary of two clusters, and the randomness in -means can assign them to one or the other. With 100 restarts, there are few such points with clusters. Even higher numbers of restarts can reduce the number, but because -means is greedy, in different runs might yield clusters that differ on a few points. It is important to realize that the randomness in -means could yield clusters that vary in this way.

| nstart | = | 10 | nstart | = | 25 | nstart | = | 50 | nstart | = | 100 | nstart | = | 250 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2 | 0 / 5474 | = | 0.0 % | 0 / 5474 | = | 0.0 % | 0 / 5474 | = | 0.0 % | 0 / 5474 | = | 0.0 % | 0 / 5474 | = | 0.0 % |

| 3 | 0 / 5474 | = | 0.0 % | 0 / 5474 | = | 0.0 % | 0 / 5474 | = | 0.0 % | 0 / 5474 | = | 0.0 % | 0 / 5474 | = | 0.0 % |

| 4 | 0 / 5474 | = | 0.0 % | 0 / 5474 | = | 0.0 % | 0 / 5474 | = | 0.0 % | 0 / 5474 | = | 0.0 % | 0 / 5474 | = | 0.0 % |

| 5 | 5 / 5474 | = | 0.1 % | 5 / 5474 | = | 0.1 % | 0 / 5474 | = | 0.0 % | 0 / 5474 | = | 0.0 % | 0 / 5474 | = | 0.0 % |

| 6 | 2970 / 5474 | = | 54.3 % | 29 / 5474 | = | 0.5 % | 35 / 5474 | = | 0.6 % | 35 / 5474 | = | 0.6 % | 13 / 5474 | = | 0.2 % |

| 7 | 238 / 5474 | = | 4.3 % | 258 / 5474 | = | 4.7 % | 126 / 5474 | = | 2.3 % | 2 / 5474 | = | 0.0 % | 2 / 5474 | = | 0.0 % |

| 8 | 4242 / 5474 | = | 77.5 % | 3 / 5474 | = | 0.1 % | 3 / 5474 | = | 0.1 % | 0 / 5474 | = | 0.0 % | 0 / 5474 | = | 0.0 % |

| 9 | 1826 / 5474 | = | 33.4 % | 288 / 5474 | = | 5.3 % | 282 / 5474 | = | 5.2 % | 35 / 5474 | = | 0.6 % | 52 / 5474 | = | 0.9 % |

| 10 | 3509 / 5474 | = | 64.1 % | 1632 / 5474 | = | 29.8 % | 42 / 5474 | = | 0.8 % | 287 / 5474 | = | 5.2 % | 11 / 5474 | = | 0.2 % |

| 11 | 3644 / 5474 | = | 66.6 % | 15 / 5474 | = | 0.3 % | 9 / 5474 | = | 0.2 % | 5 / 5474 | = | 0.1 % | 0 / 5474 | = | 0.0 % |

| 12 | 5409 / 5474 | = | 98.8 % | 1835 / 5474 | = | 33.5 % | 1844 / 5474 | = | 33.7 % | 1261 / 5474 | = | 23.0 % | 37 / 5474 | = | 0.7 % |

Optimizing the objective function obtains spherical clusters around the centroids (the mean patterns). Basins and valleys do often have rough spherical shape, and -means appears to do well when zones correspond to basins — a situation in which they are justifiable as defining microclimates. In [29] we explore optimization of ; in this paper we only study results for .

Instead of using a clustering algorithm, we could use a method for extracting mixture models [31], and obtain probability distributions over models rather than separate clusters. We have elected to use clustering because boundaries (and policy) of municipalities are hard, preventing mixtures. All zones in this paper are regions having a single model, not a mixture.

In each of these three perspectives — random fields, topography, and results of clustering — EC-Microclimates behave like microclimates.

V Electricity Consumption Patterns

and Per Capita Income

Electricity consumption is often linked to economics. For example, in [32, p.65] electricity consumption in the United States is linked to GNP. Furthermore it is known that individuals with the greatest income have the greatest consumption [33], while lifeline consumers have much lower use [34].

In this section we develop simple econometric models relating HEC to income — like crude HEC forecasting models. Our results above show seasonal consumption is linked to microclimate. Income distributions often resemble a mixture of lognormal distributions [24]. Figure 6 shows that this holds for the distribution of as well as the distribution of .

V-A Linking Household Income and Electricity Consumption

The map of Household Income in Figure 5 shows that higher-income block groups are located in the western Los Angeles basin, particularly in hillside and coastal areas, while lower-income block groups are mainly in flat inland areas. The microclimates of these locations differ.

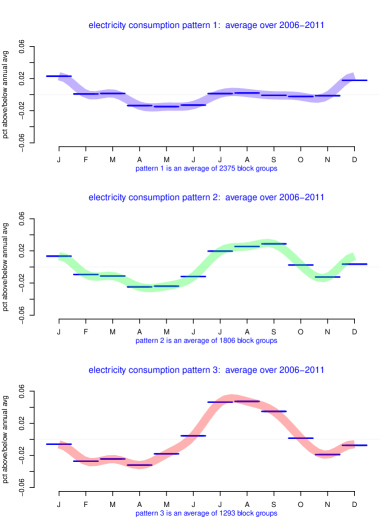

The association between microclimate and income helps explain why higher-income consumers have different electricity consumption profiles. Figure 4 suggests that higher-income block groups have higher consumption in Winter, while lower-income block groups have higher consumption in Summer. The 3 microclimates have different seasonal demand.

| (overall) | ||||

| (cluster 1) | ||||

| (cluster 2) | ||||

| (cluster 3) |

V-B Variation of Electricity Consumption and Income

To understand the magnitude of seasonal variations of HEC for the block groups, we can use Principal Components Analysis (PCA) [26]. Figure 9 shows the result of PCA on sequences of 12 monthly averages of over the six years. Points are colored by Per Capita Income (PCI) of the regions.

One interesting aspect of the resulting components is that they give a straightforward model of annual electricity consumption that explains 99+% of the variance in annual electricity consumption with three components, and the first alone explains 95.7%.

The plots at right in Figure 9 show the first 2 principal components presented as consumption patterns over the twelve months. The first component is an ‘augmentation’ above the baseline that is almost evenly-spread across all 12 months; the other components depend on the zone. The first component explains almost all of the variance. Essentially, all patterns in a microclimate differ almost entirely by a small additive amount — given by the coefficient of the first principal component. Since the first component is nearly constant, the difference is nearly an additive constant.

In Figure 9, the plots in the middle show the block groups projected on the first 2 principal components. There is a clear color gradient from blue to red in both dimensions; block groups with higher PCI generally have higher coefficients in all components. Thus: regional variation in electricity consumption is strongly linked to income. Because PCI is a correlate (proxy) of property values, this also shows that higher property values are associated with greater variation in HEC.

How can one principal component explain so much of the variance? Notice that the principal component information tells us a great deal about each zone. Any given 12-month pattern in Zone satisfies , where is the first principal component, and . But since the first principal component is nearly constant, , and . In other words, every vector in zone is essentially plus an additive constant ‘shift’ determined by .

Because adding a constant determined by to is equivalent to multiplying HEC by a scaling factor, higher-income block groups differ from others in the zone only in having a higher scale.

V-C Electricity Consumption in each Microclimate Zone

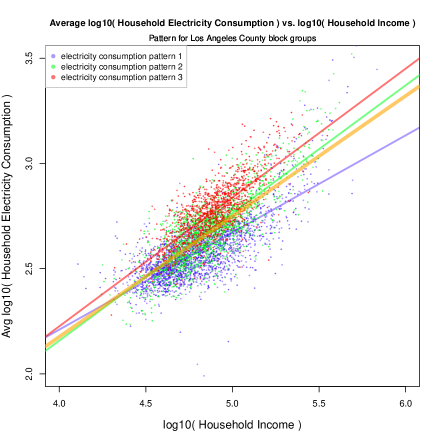

In our data, division into microclimate zones (i.e., conditioning on EC-microclimate) yields more accurate models of electricity consumption. Figure 9 shows the same result when the data is subdivided into the three clusters identified earlier (western, eastern, and northern Los Angeles). As one would expect, this division permits even more accurate results from PCA. Again, however, a single principal component explains almost all variance in each cluster/region.

Figure 10 shows the joint distribution between and . The distribution appears almost gaussian, with strong correlation. Subdividing the block groups over the three clusters gets three smaller gaussian-like distributions, with stronger correlation. Electricity consumption patterns differ visibly in each EC-microclimate zone.

V-D Predicting Electricity Consumption

Distributions of values often appear gaussian, particularly within EC-microclimate zones. Earlier we discussed the Gaussian Process structure of the data; in fact the structure depends on the zone.

Figure 2 shows how the values of differ by zone; each row is a time series of 72 samples for a given block group. At least 3 different kinds of patterns are visible, and were detected as EC-microclimate zones by clustering. Thus the random field discussed earlier is better represented by 3 different GPRFs, one for each zone.

Gaussian Process Regression [25] is a method for learning a Gaussian Process from a given set of data points. For a training set defining a function , it derives a covariance matrix that can be used to make predictions for the function value at any new input point :

where , and (i.e., is the level of noise in the values [25, 26]).

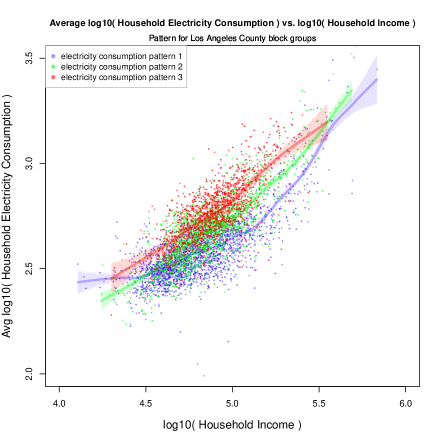

Figure 11 shows the result of Clustered Gaussian Process Regression, performing Gaussian Process regression for points in each cluster (EC-microclimate zone). Again, clustering the data improves accuracy significantly. These results give a better fit to the data than the linear regression models in Figure 10; they also show that household electricity consumption increases nonlinearly for households of extremely high income. The highest-income block groups appear price-insensitive.

Gaussian Process Prediction, or Kriging, is the use of Gaussian Process Regression to obtain predicted values [35]. The regression can yield predictions for any input . Their accuracy depends on noise in the data, but Gaussian Process regression also produces standard error bounds, providing a quantitative estimate of accuracy. In Figure 11, each regression line includes -standard-error ‘band’; these bands are tallest for extreme values of Household Income (PHI), high or low. The plot shows the variance is heteroskedastic, and is greatest at high income: EC of the wealthiest neighborhoods is most difficult to predict accurately.

Kriging is an important method of geostatistics, used often to make predictions based on spatio-temporal data [25]. It might have potential in prediction of energy demand.

VI Modeling Electricity Consumption with Clustered Regression and Mixture Regression

A 2014 prediction model for household EC developed by the state of California is shown in Figure 12 — the first econometric model in [27]. This statewide model can be compared with the models we consider below. Notice that this model is an aggregate model over 1980-2013, where the models below are over the 6-year period 2006-2011. Notice also that the model uses natural log transformations on income variables, where we have used the base-10 log. Assuming its variable PPH = Persons Per Household is the ratio of income Per Household to income Per Person, Thus this model is of the same kind as the models presented in this paper, emphasizing per household modeling because the EC data provides that. We could get more accurate results with separate models for each microclimate zone.

The clustering phases in microclimate zone derivation and in clustered regression can be the same. Micro-models are models defined on a specific zone. In this way we can integrate micro-models with microclimates.

| natural log of EC per household | |||

| by planning area, 1980-2013 | |||

| + | 7.1881 | overall constant | |

| + | 0.3935 | Persons per Household | |

| + | 0.1419 | Per capita income (2013$) | |

| 0.0042 | UnEmpRate | Unemployment Rate | |

| 0.0870 | ResElecRate | Residential Electricity Rate (2013 /kWh) | |

| + | 0.0323 | log(CoolDays) | Number of Cooling Degree Days (70o) |

| + | 0.0181 | log(HeatDays) | Number of Heating Degree Days (60o) |

| 0.5784 | LADWP | Los Angeles Dept of Water & Power | |

| ⋮ |

The Residential Sector Electricity Econometric Model (for California Energy Demand Updated Forecast, 2014) is the first model in [27, p.A-1]: All coefficients are statistically significant (their estimated error is outside 3 standard deviations). Some variables have been omitted. The model is described as: “All variables in logged form except time and unemployment rate”. In other words, the model uses natural log transformations on variables.

This is a statewide model for California. The ‘LADWP’ variable is one of five utility ‘planning area’ dummy variables, indicating differences for the Los Angeles region covered by LADWP. It is like the zone conditionals in our models, except that it only adds a constant offset.

VI-A Clustered Regression models of Electricity Consumption

Figure 9 suggests that division by cluster permits to be well-described at the block group level with a linear statistical model involving Per Capita Income. In the format of a general linear model [36] conditioned on EC-microclimate zones :

In other words, we obtain a model for each microclimate zone ; all logs are to base 10. This is precisely what is shown in Figure 10. The regression model for the entire dataset (all three zones) with , can be split into the three models shown in Figure 10 with higher values. In [29] we develop methods to split optimally.

Modeling in this way has been referred to as Clustered Regression — defining a set of independent regression models on subsets of the input that are defined by clusters [37, 38]. Strategies for computing these models range from simple -means clustering followed by construction of regression models, to ‘-regression’ models that extend -means clustering to an iterative regression algorithm.

It is pointed out in [37] that clustered regression models are inequivalent to standard regression trees or ensemble methods, and can outperform them significantly. The 3 seasonal patterns (defined earlier in Figure 3 and Figure 9) show how the cyclic seasonal pattern is modeled more accurately with a different regression model in each of the 3 clusters. The values suggest this also, but visual confirmation is in Figure 10: the heavier line is a model for the whole dataset, and the three other lines are models for the clusters. The overall joint distribution of and appears gaussian, but divides clearly into distinct distributions by cluster.

VI-B Clustered vs. Mixture Models

Figure 6 showed earlier that the distributions both of and of are approximately gaussian, with approximately gaussian contributions from each EC-microclimate zone. As a result they are sometimes modeled as mixtures — weighted sums of several gaussian distributions.

As noted in [31, Ch.11], it is possible to shift the ‘clustered’ (‘zoned’) approach in this paper to one based on mixtures:

-

•

the EM algorithm is the standard parameter estimation method for gaussian mixtures.

-

•

the -means algorithm is a special case of the EM algorithm for gaussian mixtures (‘hard EM’) that uses an ‘argmax’ distance measure instead of probabilistic combination.

-

•

clustered regression is a special case of what is called a mixture of experts, in which linear regression models are combined with gating functions assigning weights to parts of the input space. The resulting mixture of regression models is called a mixture regression [31, Section 11.2.4].

In other words, the microclimate methods for clusters can generalize directly to mixtures. Although we have just presented the model formula as defining a set of separate models on zones , mixture regression yields a single model in which every block group has a weighted contribution to each zone.

A benefit of mixtures is that they can extend clustered models to larger scale. In this perspective, microclimates are latent variables, and the -means algorithm is a vector quantization method for finding the best single value for these variables. Instead, however, more general EM algorithms can obtain mixtures of regression experts with hidden variables [31, Section 11.4.3–4]. These algorithms could even be applied naturally at the consumer level, on the full EC dataset.

In principle we could also generalize zones to mixtures: each block group could have weighted participation in multiple zones. This might give another way to move from analysis of block group aggregates to large-scale consumer-level analysis.

However, as mentioned earlier, urban policy is based on community boundaries, not mixtures. Urban boundaries are hard. For example, ‘Piecewise Gaussian Processes’ are used for urban data analysis in [39]. These partition the block groups into zones like our zoned Gaussian Process models.

VII Conclusions

In this paper we have studied annual patterns of residential electricity use in Los Angeles. Specifically, we studied patterns as a sequence of 72 monthly values (over the six years 2006-2011) of household electricity consumption (HEC) in about 5000 block groups, and obtained interesting findings about the central importance of Household Income (PHI) on HEC, as summarized in Section I-C.

We found that temporal HEC patterns contain significant information about climate. Clustering normalized values yields clusters that correspond both to climate and to geographic regions. We therefore have called these regions EC-microclimate zones.

We showed also that EC-microclimate zones behave like environmental microclimate zones in three perspectives: random fields, topography, and results of -means clustering. Both kinds of zones follow a Gaussian Process Random Field (GPRF) — a 2D random process in which pairs of points follow Gaussian distributions, but with covariance constrained by their geographic distance. Microclimate variables (wind speed, local temperature, wind pressure, and total solar irradiation) have been modeled as Gaussian Process Random Fields in the past [1]. However, we are unaware of other work showing that follows a GPRF.

Generally, EC-microclimate zones we have produced conform to regions bounded by hillsides — essentially basins, each with a distinct climate. Furthermore, both kinds of zones also exhibit a hierarchical structure, in which microclimates subdivide (into ‘submicroclimates’). Los Angeles topography and climate appears important in these subdivisions. We have used -means here because it is a common choice and it obtains spherical clusters that appear to fit well with basin structures. The PCA results earlier showed why normalizing an EC-pattern to total to 1 would be successful, since patterns in a cluster have limited variation — so use of normalization and Euclidean clustering is justifiable. However alternative clustering methods merit investigation.

The rest of this paper has shown how clustering can be a foundation for building complex models. Clustered Regression is the natural extension of ordinary linear regression to cope with different zones. Clustered Gaussian Process Regression involves the same extension. Although the data can be roughly approximated by a single Gaussian distribution, dividing the data first by clustering into more homogeneous zones permits better approximations and more accurate models. This was shown in Figures 6 and 10.

We discussed at the start of this paper how prediction models are currently of great interest in energy management. Gaussian Process Regression models also include prediction methods that come with error bounds. Kriging — basically a very flexible form of interpolation — is used heavily in geostatistics. It can be used as a prediction method for EC, as shown in Figure 11. In [29] we explore issues in modeling.

There are many other directions for further work. For example, other measures of electricity consumption similarity and variation are possible, and other methods can be used to analyze consumption patterns. It appears that the idea of a ‘EC-microclimate zone’ can be useful in developing better energy policy. In [30] we show that these zones permit useful forms of ‘micropolicy’ (microclimate-specific policy).

One interesting way to check the effectiveness of these zones would be to consider other urban resources — like water. The link between HEC and Income is consistent with published results about water consumption in Los Angeles: affluent neighborhoods consume three times more water than others, and water use depends heavily on Per Capita Income [22]. The three regions in Figure 3 resemble the three geographical clusters based on water use in [22]. Considering resources like water would be a natural extension of this work.

References

- [1] Y. Sun, Y. Heo, H. Xie, M. Tan, J. Wu, and G. Augenbroe, “Uncertainty Quantification of Microclimate Variables in Building Energy Simulation,” Journal of Building Performance Simulation, vol. 7, no. 1, pp. 17–32, 2014.

- [2] S. Pincetl, P. Bunje, and T. Holmes, “An expanded urban metabolism method: Toward a systems approach for assessing urban energy processes and causes,” Landscape and Urban Planning, vol. 107, no. 3, pp. 193–202, 2012.

- [3] E. Erell, “The application of urban climate research in the design of cities,” Advances in Building Energy Research, vol. 2, no. 1, pp. 95–121, 2008.

- [4] UK Meteorological Office, “Microclimates,” National Meteorological Library and Archive, Tech. Rep. Fact sheet No. 14, 2011.

- [5] California Energy Commission, “California Climate Zone Descriptions,” CEC, Tech. Rep. P400-95-041, 2015.

- [6] Pacific Energy Center, “California Climate Zones and Bioclimatic Design,” CEC, Tech. Rep., 2008.

- [7] L.A. DWP, “LADWP Board of Commissioners approves Electric Rate Plan that promotes Energy Conservation,” Los Angeles Department of Water & Power, Tech. Rep., 2008.

- [8] California Energy Commission, “2013 California Integrated Energy Policy Report,” CEC, Tech. Rep. CEC-100-2013-001-CMF, 2013.

- [9] ——, “2014 California Integrated Energy Policy Report,” CEC, Tech. Rep. CEC-100-2014-001-CMF, 2014.

- [10] ——, “2015 California Integrated Energy Policy Report,” CEC, Tech. Rep. CEC-100-2015-001-CMF, 2015.

- [11] ——, “2016 California Integrated Energy Policy Report,” CEC, Tech. Rep. CEC-100-2016-001-CMF, 2016.

- [12] ——, “2017 California Integrated Energy Policy Report,” CEC, Tech. Rep. CEC-100-2017-001-CMF, 2017.

- [13] ——, “2018 California Integrated Energy Policy Report,” CEC, Tech. Rep. CEC-100-2018-001-CMF, 2018.

- [14] ——, “Assembly Bill 758: Comprehensive Energy Efficiency Program for Existing Buildings,” CEC, Tech. Rep., 2017.

- [15] ——, “Assembly Bill 758: Existing Buildings Energy Efficiency Action Plan — Final,” CEC, Tech. Rep. tn=206015, 2015.

- [16] ——, “Assembly Bill 758: 2016 Existing Buildings Energy Efficiency Action Plan Update — Final,” CEC, Tech. Rep. tn=214801, 2016.

- [17] ——, “California Energy Efficiency — Tracking Progress,” CEC, Tech. Rep. online report, 2018.

- [18] N. A. of Housing Builders, “The Nation Watches as California Mandates Solar Power (for 2020),” NAHBNow, May 2018.

- [19] CEC, “Energy Commission Adopts Standards Requiring Solar Systems for New Homes, First in Nation,” CEC News Release, May 2018.

- [20] Ivan Penn, “California Lawmakers Set Goal for Carbon-Free Energy by 2045,” The New York Times, 28 August 2018.

- [21] T. Vu and D. Parker, “Extracting Urban Microclimates from Electricity Bills,” Proc. 31st AAAI Conf. on Artificial Intelligence (AAAI’17), 2017.

- [22] C. Mini, T. Hogue, and S. Pincetl, “Residential Water Consumption in Los Angeles: What are the Drivers and are Conservation Measures Working?” UCLA Inst. of the Environment & Sustainability, Tech. Rep., 2014.

- [23] A. Kandel, M. Sheridan, and P. McAuliffe, “Comparison of Per Capita Electricity Consumption in the United States and California,” California Energy Commission, Staff Paper, 2008.

- [24] A. B. Atkinson and F. Bourguignon, Handbook of Income Distribution. Elsevier, 2014.

- [25] C. Rasmussen and C. Williams, Gaussian Processes for Machine Learning. MIT Press, 2006.

- [26] C. Bishop, Pattern Recognition and Machine Learning. Springer, 2006.

- [27] California Energy Commission, “California Energy Demand — Updated Forecast, 2015-2025,” CEC, Tech. Rep. CEC-200-2014-009, 2014.

- [28] P. Moonena, T. Defraeyec, V. Dorerb, B. Blockend, and J. Carmelieta, “Urban Physics: Effect of the micro-climate on comfort, health and energy demand,” Frontiers of Architectural Research, vol. 1, no. 3, pp. 197–228, 2012.

- [29] D. Parker and T. Vu, “Mining with Micro-Models – and its application in Urban Energy Management,” Submitted, 2018.

- [30] ——, “Developing Data-Driven ‘Micropolicy’: (Microclimate-specific Policy) for Urban Resource Management,” Submitted, 2018.

- [31] K. Murphy, Machine Learning: a Probabilistic Perspective. MIT Press, 2012.

- [32] A. Pabla, Electric Power Distribution. Tata McGraw-Hill, 2004.

- [33] S. Pachauri, An Energy Analysis of Household Consumption. Springer Science & Bus. Media, 2007.

- [34] J. Murdock, “LA Electricity Use — Finding the Right Price,” Urban & Regional Planning, UCLA, Master’s Project, 2013.

- [35] C. Williams, “Prediction with Gaussian Processes: From Linear Regression to Linear Prediction and Beyond,” in Learning and Inference in Graphical Models. Kluwer, 1998.

- [36] R. Chambers and T. Hastie, Statistical Models in S. Wadsworth & Brooks/Cole, 1992.

- [37] L. Torgo and J. da Costa, “Clustered Partial Linear Regression,” Machine Learning, vol. 50, pp. 303–319, 2003.

- [38] ——, “Clustered Multiple Regression,” in Data Analysis, Classification, and Related Methods, H. Kiers, J.-P. Rasson, P. Groenen, and M. Schader, Eds. Springer-Verlag, 2000, pp. 217–222.

- [39] H.-M. Kim, B. Mallick, and C. Holmes, “Analyzing Nonstationary Spatial Data using Piecewise Gaussian Processes,” J. American Statistical Association, vol. 100, no. 470, pp. 653–668, 2005.

![[Uncaptioned image]](/html/1809.10019/assets/x12.png) |

Thuy Vu Thuy Vu is currently a graduate student in the Computer Science Department, University of California, Los Angeles. His current research focuses on scalable learning methods for data-intensive applications in natural language processing and data mining. He received the B.S. in Computer Science from University of Science, Vietnam in 2005, and was a researcher at the Institute for Infocomm Research, Singapore from 2006-2011. |

![[Uncaptioned image]](/html/1809.10019/assets/x13.png) |

D. Stott Parker D. Stott Parker has been on the faculty of the UCLA Computer Science Department since 1979. He received an A.B. in Mathematics from Princeton in 1974. and a Ph.D. in Computer Science from the University of Illinois in 1978. His interests center around data mining in general, and scientific data management in particular. His research spans database management, knowledge base management, biomedical databases, neuroimaging, and literature mining. |