Contextual Bandits with Cross-Learning

Contextual Bandits with Cross-Learning

Santiago Balseiro \AFFColumbia Business School, Columbia University, New York, NY, srb2155@columbia.edu \AUTHORNegin Golrezaei \AFFSloan School of Management, Massachusetts Institute of Technology, Cambridge, MA, golrezae@mit.edu \AUTHORMohammad Mahdian, Vahab Mirrokni, and Jon Schneider \AFFGoogle Research, New York, NY, mahdian, mirrokni, jschnei@google.com

In the classical contextual bandits problem, in each round , a learner observes some context , chooses some action to perform, and receives some reward . We consider the variant of this problem where in addition to receiving the reward , the learner also learns the values of for some other contexts in set ; i.e., the rewards that would have been achieved by performing that action under different contexts . This variant arises in several strategic settings, such as learning how to bid in non-truthful repeated auctions, which has gained a lot of attention lately as many platforms have switched to running first-price auctions. We call this problem the contextual bandits problem with cross-learning. The best algorithms for the classical contextual bandits problem achieve regret against all stationary policies, where is the number of contexts, the number of actions, and the number of rounds. We design and analyze new algorithms for the contextual bandits problem with cross-learning and show that their regret has better dependence on the number of contexts. Under complete cross-learning where the rewards for all contexts are learned when choosing an action, i.e., set contains all contexts, we show that our algorithms achieve regret , removing the dependence on . For any other cases, i.e., under partial cross-learning where for some context-action pair of , the regret bounds depend on how the sets impact the degree to which cross-learning between contexts is possible. We simulate our algorithms on real auction data from an ad exchange running first-price auctions and show that they outperform traditional contextual bandit algorithms.

contextual bandits, cross learning, bidding, first-price auctions111Part of this work has appeared in Balseiro et al. (2019).

1 Introduction

In the contextual bandits problem, a learner repeatedly observes some context and, depending on the context, the learner takes some action and receives some reward. The learner’s goal is to maximize their total reward over some number of rounds. The contextual bandits problem is a fundamental problem in online learning: it is a simplified (yet analyzable) variant of reinforcement learning and it captures a large class of repeated decision problems. In addition, the algorithms developed for the contextual bandits problem have been successfully applied in domains like ad placement, news recommendation, and clinical trials (Kale et al. 2010, Li et al. 2010, Villar et al. 2015).

Ideally, one would like an algorithm for the contextual bandits problem which performs approximately as well as the best stationary strategy (i.e., the best fixed mapping from contexts to actions). This can be accomplished by running a separate instance of some low-regret algorithm for the non-contextual bandits problem (e.g., EXP3 proposed in Auer et al. 2002) for every context. This algorithm achieves regret , where is the number of contexts, the number of actions, and the number of rounds. This bound can be shown to be tight (Bubeck and Cesa-Bianchi 2012). Since the number of contexts can be very large, these algorithms can be impractical to use, and modern current research on the contextual bandits problem instead aims to achieve low regret with respect to some smaller set of policies (Auer et al. 2002, Langford and Zhang 2008, Beygelzimer et al. 2011).

Some settings, however, possess additional structure between the rewards and contexts that allow one to achieve less than regret while still competing with the best stationary strategy. In this paper, we look at a specific type of structure we call cross-learning between contexts that is particularly common in strategic settings with private information in which agents can compute counterfactual rewards under different contexts. In variants of the contextual bandits problem with this structure, playing an action in some context at round not only reveals the reward of playing this action in this context (which the learner receives), but also reveals to the learner the rewards for some other context in some set , which depends on the action played. The set can include every context, a case which we refer to as complete cross-learning, or only a subset of contexts, which we refer to as partial cross-learning. Partial cross learning setting can be used to model conservative learners that only use local information obtained from contexts that are “close” to each other in some sense. Such a conservative learner might be concerned about inaccuracies in their cross-learning model due to a significant differences in the contexts.

Contextual bandits with cross learning appear in many settings including (i) bidding in non-truthful auctions, (ii) multi-armed bandits with exogenous costs, (iii) dynamic pricing with variable cost, (iv) sleeping bandits, and (v) repeated Bayesian games with private types. While our model and results are general, the main application of interest in this paper is the problem of bidding in non-truthful auctions (such as first-price auctions), which we describe in detail below. We refer the reader to Section 5 for more details about the other applications.

1.1 Bidding in Non-truthful Auctions

The problem of bidding in non-truthful auctions has gained a lot of attention recently as online advertising platforms have recently switched from running second-price to first-price auctions. Many online publishers have adopted header bidding, in which publishers offer ad impressions to multiple ad exchanges simultaneously using a first-price auction, rather than offering ad impressions sequentially to different exchanges, which would typically auction impressions using second-price auctions, in a waterfall fashion. Additionally, some major ad exchanges have adopted first-price auctions to sell all their inventory (Cox 2019). In a first-price auction, the highest bidder is the winner and pays their bid (as opposed to second-price auctions where the winner pays the second highest-bid). First-price auctions are non-truthful mechanisms as bidders have incentives to shade bids so that they enjoy a positive utility when they win (Vickrey 1961). As opposed to second-price auctions in which bidding is simple, determining bids in first-price auctions is challenging as bidders need to take into account the competitive landscape, which is typically unknown.

More formally, in the problem of bidding in repeated non-truthful auctions, at every round, the bidder receives a (private) value for the current item, and based on this, must submit a bid for the item. The auctioneer then collects the bids from all participants, and decides whether to allocate the item to our bidder, and if so, how much to charge the bidder. The bidding problem in first-price auctions can be seen as a contextual bandits problem for the bidder where the context is the bidder’s value for the item, the action is their bid, and their reward is their net utility from the auction: zero if they do not win, and their value for the item minus their payment if they do win. Note that this problem also allows for cross-learning between contexts – the net utility that would have been received if they had value instead of value is just , which can be computed from the outcome of the auction assuming the value and highest competing bid (that influences ) are independent of each other; that is is the set of all possible contexts.

This independence assumption, however, may not hold in practice, as we also observe in our empirical studies in Section 6. When the bidder’s value (context) is correlated with the highest competing bid, with the same action/bid, the chance of winning (i.e., ) under two values that are far from each other may not be the same. For instance, when there is a positive correlation between values and highest competing bids, as the value increases, the highest competing bid may increase as well, reducing the chance of winning. To handle this, such learners can only allow for cross-learning between close values. That is, can be chosen to be the set of contexts that are close enough to .

1.2 Main Contributions

We introduce and study contextual bandit problems with cross-learning between contexts. In this problem, for every action , there is a directed graph over the set of contexts , where an edge in indicates that playing action in context , reveals the reward of action in context . We refer to these graphs as cross-learning (CL) graphs, where these graphs are known to the learner. (Set , defined before, is the set of vertices of out-neighbors of node/context in CL graph .) We study to what extent cross-learning between contexts can improve regret bounds. In many settings, the number of possible contexts can be huge: exponential in the number of actions or uncountably infinite. This makes the naive -regret algorithm undesirable in these settings. We show that the extent with which cross-learning can improve the regret bounds depend on how “well-connected” the CL graphs are. For instance, when CL graphs are complete graphs, i.e., under complete cross-learning between contexts, we show that it is possible to design algorithms which completely remove the dependence on the number of contexts in their regret bound. For any other general CL graphs, i.e., under partial cross-learning, in addition to the CL graphs themselves, the improvement in obtained regret depends on how contexts and rewards are generated.

We consider both settings where the contexts are generated stochastically (from some distribution that may or may not be known to the learner) and settings where the contexts are chosen adversarially. Similarly, we also consider settings where the rewards are generated stochastically and settings where they are chosen adversarially. By considering stochastic rewards, we can capture environments under which the obtained reward (given a context) is stationary and predictable. Whereas by considering adversarial rewards, we can capture environments with non-stationary and hard-to-predict rewards. Similarly, stochastic (respectively adversarial) contexts model environments with stationary and predictable (respectively unpredictable) side information. Our results, which are also summarized in Table 1, include:

-

•

Stochastic rewards, stochastic or adversarial contexts: We design an algorithm called UCB1.CL with regret of , where is the average size of the minimum clique cover of the CL graphs; the minimum clique cover of a directed graph is defined in Definition 2.1. Observe that for complete CL graphs, , and hence UCB1.CL obtains regret under complete cross-learning, removing the dependence of the regret bound on the number of contexts . On the other hand, when CL graphs contain only self-loops, i.e., under no cross-learning, , which leads to a regret of , as expected.

-

•

Adversarial rewards, stochastic contexts with known distribution: We design an algorithm called EXP3.CL with regret of , where is the average size of the maximum acyclic subgraph of the CL graphs; see Definition 2.3. We again note that for complete CL graphs, we have , which implies that EXP3.CL obtains regret of under complete cross-learning.

-

•

Adversarial rewards, stochastic contexts with unknown distribution: We design an algorithm called EXP3.CL-U with regret .222For this result to hold we need an assumption that CL graph for any . Here, “U” stands for Unknown distribution.

-

•

Lower bound for adversarial rewards, adversarial contexts: We show that when both rewards and contexts are controlled by an adversary, even under complete cross-learning, any algorithm must obtain a regret of at least .

| Stoc. Rewards | Adv. Rewards & | Adv. Rewards & | ||||

| Stoc. Contexts | ||||||

| Stoc. | Adv. | Known | Unknown | Adv. Contexts | ||

| Contexts | Contexts | Context Dist. | Context Dist. | |||

| Complete CL | Upper Bound | |||||

| Lower Bound | ||||||

| Partial CL | Upper Bound | |||||

| Lower Bound | ||||||

All of these algorithms are easy to implement, in the sense that they can be obtained via simple modifications from existing multi-armed bandit algorithms like EXP3 (Auer et al. (2002)) and UCB1 (Robbins 1952, Lai and Robbins 1985a), and efficient, in the sense that all algorithms run in time at most per round (and for many of the applications mentioned above, this can be further improved to time per round). Our main technical contribution is our analysis of UCB1.CL, which requires arguing that UCB1 can effectively use the information from cross-learning despite it being drawn from a distribution that differs from the desired exploration distribution. We accomplish this by constructing a linear program whose value upper bounds (one of the terms in) the regret of UCB1.CL, and bounding the value of this linear program.

Our EXP3.CL and EXP3.CL-U algorithms that are designed for the adversarial rewards and stochastic contexts setting are modifications of the EXP3 algorithm. These algorithms maintain a weight for each action in each context, and update the weights via multiplicative updates by an exponential of an estimator of the reward, taking advantage of cross-learning between contexts via their update rules and estimators. The main difference between EXP3.CL and EXP3.CL-U is how their reward estimators are constructed. In EXP3.CL, which is designed for the case of known context distribution , the estimator is unbiased, and crucially uses the knowledge of to obtain minimal variance. In EXP3.CL-U, which is designed for the case of unknown context distribution , the estimator is only unbiased under the complete cross-learning setting. The estimator, however, is consistently biased for the partial cross-learning setting, easing the analysis. See Section 3.2.2 for more details.

To shed lights on how tight regret bounds of our algorithms are, we further present regret lower bound for the aforementioned settings; see Table 1. We show that when both rewards and contexts are generated stochastically, any algorithm must obtain a regret of at least , where , which is defined in Definition 2.5, can be seen as variant of the maximum acyclic subgraph number . In all of regret lower bounds, we assume that CL graphs do not depend on actions; that is, for any . We further show a regret lower bound of when rewards are generated stochastically and contexts are generated adversarially. This regret lower bound also leads to the same regret lower bound for the case of adversarial rewards and stochastic contexts.

By comparing our regret lower bounds with the regret of our algorithms, we observe that regret of our algorithms are indeed tight for many CL graphs in various settings. Consider settings where either (i) rewards are generated stochastically and contexts are either stochastic or adversarial, or (ii) rewards are adversarial and contexts are stochastic (with known context distribution). Then, for these settings, our regret upper bounds are tight for CL graphs that are the union of disjoint cliques. In fact, our regret upper bounds are tight for an even larger family of graphs, including line graphs, and any undirected graph that is perfect. Perfect graphs include all bipartite graphs, forests, interval graphs, and comparability graphs of posets (see, e.g., West et al. 1996).

Our regret upper bound for the settings with adversarial rewards and stochastic contexts (with unknown context distribution), i.e., regret of EXP3.CL-U algorithm, does not match its associated regret lower bound. In Appendix 11, we present another candidate algorithm for this setting, which can be viewed as a variant of EXP3.CL algorithm that uses an empirical estimate of context distribution in place of the true context distribution, which is not available. While this variant performs very well in our empirical studies in Section 6, because of several technical challenges explained in Appendix 11, we are not able to show the regret of this algorithm matches the regret lower bound. We leave analyzing the regret of this variant as a future research direction.

We also apply our results to some of the applications listed above. In each case, our algorithms obtain optimal regret bounds with asymptotically less regret than a naive application of contextual bandits algorithms. In particular, for the problem of learning to bid in a first-price auction, standard contextual bandit algorithms get regret . Our algorithms achieve regret . This is optimal even when there is only a single context (value). Note that in this problem, the set of contexts (values) and actions (bids) are infinite. Thus, one needs to discretize the set of contexts and actions, and such discretizations increases regret. Since our algorithms have regret bounds that are independent of , discretizing the context space arbitrarily finely does not deteriorate performance (indeed, as we show in Section 5, we can often implement our algorithms for infinite context spaces). We discuss the results for the other applications in Section 5.

Finally, we test the performance of these algorithms on real auction data from a first-price ad exchange. In order for cross-learning to be effective in first-price auctions, the bidder should be able to determine the counterfactual utility for different values. That is, after observing the outcome of the auction, the bidder should predict how would their utility change if their value was different. As stated earlier, this is possible when the bidder’s values are independent of other players’ bid. In practice, however, one would expect certain degree of correlation between these quantities and, thus, the independence assumption might not hold. Even though our algorithms under the assumption of complete cross-learning do not explicitly account for correlation, numerical results show that our algorithms are somewhat robust to errors in the cross-learning hypothesis and outperform traditional bandit algorithms.

1.3 Related Work

For a general overview of research on the multi-armed bandit problem, we recommend the reader to the survey by Bubeck and Cesa-Bianchi (2012). Our algorithms build off of pre-existing algorithms in the bandits literature, such as EXP3 (Auer et al. 2002) and UCB1 (Robbins 1952, Lai and Robbins 1985a). Contextual bandits were first introduced under that name in Langford and Zhang (2008), although similar ideas were present in previous works (e.g., the EXP4 algorithm was proposed in Auer et al. 2002).

One line of research related to ours studies bandit problems under other structural assumptions on the problem instances which allow for improved regret bounds. Slivkins (2011) study a setting where contexts and actions belong to a joint metric space, and context/action pairs that are close to each other give similar rewards, thus allowing for some amount of “cross-learning.” See also Hazan and Megiddo (2007) and Lu et al. (2009) for works that consider local smoothness over a continuum of contexts that lie in a known metric space. Some other structural assumptions widely studied in the contextual bandit literature include contextual Gaussian process bandits (Krause and Ong 2011), linear bandits (Li et al. 2010), and contextual bandits with covariates (Rigollet and Zeevi 2010, Perchet et al. 2013, Qian and Yang 2016, Guan and Jiang 2018). These structural assumptions allow for some amount of cross-learning between contexts; however, they do not capture the general cross-learning setting we study in this paper, nor do they fit into our setting as we require the learner to be able to obtain sample rewards from other contexts.333See also Van Parys and Golrezaei (2020) for the work that leverages convex structural information and Kakade et al. (2009), Niazadeh et al. (2021) for work that exploits combinatorial structures.

Several works (Mannor and Shamir 2011, Alon et al. 2015) study a partial-feedback variant of the (non-contextual) multi-armed bandit problem where performing some action provides some information on the rewards of performing other actions (thus interpolating between the bandits and experts settings). Our setting can be thought of as a contextual version of this variant, and our results in the partial cross-learning setting share similarities with these results (indeed, three of the four graph invariants we consider – , , and the independence number of graph , denoted by – appear prominently in the bounds of Mannor and Shamir 2011, Alon et al. 2015, albeit applied to different graphs). However, since the learner cannot choose the context each round, these two settings are qualitatively different. As far as we are aware, the specific problem of contextual bandits with cross-learning between contexts has not appeared in the literature before.

Recently there has been a surge of interest in applying methods from online learning and bandits to auction design. The majority of the work in this area has been from the perspective of the auctioneer (Morgenstern and Roughgarden 2016, Mohri and Medina 2016, Cai and Daskalakis 2017, Dudík et al. 2017, Kanoria and Nazerzadeh 2017, Golrezaei et al. 2019, 2021b) in which the goal is to learn how to design an auction over time based on bidder behavior. In fact, many papers have looked at this problem in a simple posted price auction; see, for example Araman and Caldentey (2009), Farias and Van Roy (2010), Cheung et al. (2017), den Boer and Zwart (2013), and Besbes and Zeevi (2009). Some recent work, which is at the intersection of learning and auction design, studies this problem from the perspective of a buyer learning how to bid (Weed et al. 2016, Feng et al. 2018, Braverman et al. 2018). (See Golrezaei et al. (2021a) for a recent work that considers both perspectives of a buyer and a seller.) In particular, Weed et al. (2016) studies the problem of learning to bid in a second-price auction over time, but where the bidder’s value remains constant (so there is no context). More generally, ideas from online learning (in particular, the concept of no-regret learning) have been applied to the study of general Bayesian games, where one can characterize the set of equilibria attainable when all players are running low-regret learning algorithms; see, for example, (Hartline et al. 2015, Golrezaei et al. 2020).

2 Model and Preliminaries

We start with providing a short overview of non-contextual multi-armed bandits. We then present contextual multi-armed bandits problems, which will be our focus.

2.1 Non-Contextual Multi-Armed Bandits

In the classic (non-contextual) multi-armed bandit problem, a learner chooses one of arms per round over the course of rounds. On round , the learner receives some reward for pulling arm (where the rewards may be chosen adversarially and may depend on ). The learner’s goal is to maximize their total reward.

Let denote the arm pulled by the decision maker’s algorithm at round . The algorithm maps the history set of pulled arms and their realized rewards during the first rounds, any (realized) randomness in the first rounds, and the total number of rounds to an arm , where this mapping can be deterministic or random. Throughput this work, we assume that all the algorithms know the total number of rounds . This assumption, which is common in the literature, can be relaxed via the doubling trick (see, e.g., Auer et al. 2002, Bubeck and Cesa-Bianchi 2012, Lattimore and Szepesvári 2020). This trick, which can be applied in a black-box fashion, can efficiently deal with an unknown number of rounds by repeatedly running an algorithm with horizons of increasing length.

2.2 Contextual Multi-Armed Bandits

In our model, we consider a contextual multi-armed bandits problem. In the contextual bandits problem, in each round , the learner is additionally provided with a context , and the learner now receives reward if they pull arm on round while having context . The contexts are either chosen adversarially at the beginning of the game or drawn independently each round from some distribution . Similarly, the rewards are either chosen adversarially or each independently drawn from some distribution . We assume as is standard that is always bounded in .

Again, let denote the arm pulled by the decision maker’s algorithm at round under context . Here, at around , the algorithm maps the history set of contexts, the pulled arms and their realized rewards during the first rounds, as well as, the current context , any (realized) randomness in the first rounds, and the total number of rounds to an arm , where this mapping can be deterministic or random.

In the contextual bandits setting, we define the regret of an algorithm in terms of regret against the best stationary benchmark , mapping a context to an action . That is, the regret is defined as , where is the arm pulled by on round . The definition of best stationary policy depends slightly on how contexts and rewards are generated. In all of these definitions, as is common in the bandit literature (e.g., the seminal work of Lai and Robbins 1985b), we assume that the best stationary policy is unique. Nonetheless, all of our gap-independent results continue to hold even when the best stationary policy is non-unique.

-

•

Benchmark under stochastic rewards. When rewards are stochastic, i.e., is drawn independently444As is the case with standard stochastic bandits, our proofs work even when the rewards are correlated across actions and contexts, as long as they are independent across rounds. from with mean , we define to be the stationary policy that maximizes the expectation of performance over rewards , which leads to the optimal policy . That is, under the best stationary policy, for every context , an arm with the highest average reward is pulled. We highlight that unlike our algorithms, the benchmark has full knowledge of the reward distributions of all the arms under any contexts and given this knowledge, under context , it chooses arm with the highest average reward .

-

•

Benchmark under adversarial rewards and stochastic contexts. When rewards are adversarial but contexts are stochastic, we define to be the stationary policy that maximizes the expectation of performance over contexts , where the last equation follows because contexts are identically distributed across all the rounds. This is achieved by the policy since the benchmark is separable over contexts.

-

•

Benchmark under adversarial rewards and contexts. When both rewards and contexts are adversarial, we define to be the stationary policy which maximizes . Precisely, . In this case, it suffices for the adversary to only specify in each round , i.e., the rewards for context , as the other rewards are never realized.

Our choices of benchmarks are unified in the following way: in all of the above cases, is the best stationary policy in expectation for someone who knows all the decisions of the adversary and details of the system ahead of time, but not the randomness in the instantiations of contexts/rewards from distributions. This matches commonly studied notions of regret in the contextual bandits literature.

We now comment on our benchmark when rewards are adversarial and contexts are stochastic. In this case, there are two different natural ways to define “the best stationary policy.” The first maximizes the empirical cumulative rewards or, equivalently, the rewards the specific contexts we observed in the run of our algorithm: The second way that we consider in this work simply maximizes the reward of this strategy in expectation over all time Under , at the beginning of the game, the adversary knows all the rewards, but not when each context will occur, and hence, is the best stationary strategy in expectation, where the expectation is taken with respect to contexts. (Recall that is maximized under the best stationary strategy .) Under , on the other hand, at the beginning of the game, the adversary knows all the rewards and contexts in each round, and hence is the best stationary strategy in hindsight.

In this paper, when rewards are adversarial and contexts are stochastic, all bounds we show are with respect to the best stationary strategy in expectation, i.e., This is because the best stationary strategy in hindsight is too strong when contexts are stochastically drawn from a known distribution. With the latter strategy as a benchmark, no algorithm can be shown to achieve sub-linear regret when the number of contexts is large enough (see Theorem 8.1 in Appendix 8). That being said, when rewards and contexts are chosen adversarially, policy is no longer well motivated as contexts are not generated stochastically. Hence, when rewards and contexts are chosen adversarially, the stationary policy we consider is the best policy in hindsight (i.e., )

We conclude by noting that there is a simple way to construct an algorithm with sublinear regret of for the contextual bandits problem from a sublinear-regret algorithm for the classic bandits problem: simply maintain a separate instance of for every different context . In the contextual bandits literature, this is sometimes referred to as the -EXP3 algorithm when is EXP3 (Bubeck and Cesa-Bianchi 2012). The -EXP3 algorithm has regret of order . We define the -UCB1 algorithm similarly, which also obtains regret when rewards are generated stochastically. Our goal in this work is to develop algorithms with better dependence on the number of contexts by exploiting the possibility of cross learning between them. See the formal definition of cross learning between contexts in the next section.

2.3 Contextual Multi-Armed Bandits with Cross-Learning between Contexts

We consider a variant of the contextual bandits problem we call (partial) contextual bandits with cross-learning. In this variant, whenever the learner pulls arm in round while having context and receives reward , they also learn the value of for some subset of contexts (e.g., contexts similar to ). More precisely, for every action , we specify a directed graph over the set of contexts . An edge in indicates that playing action in context , reveals the reward of action in context . We assume that all self-loops are present in all graphs (i.e., playing action in context , reveals the reward of action in context ). We refer to these graphs as cross-learning (CL) graphs, and we assume that the CL graphs are known to the learner.

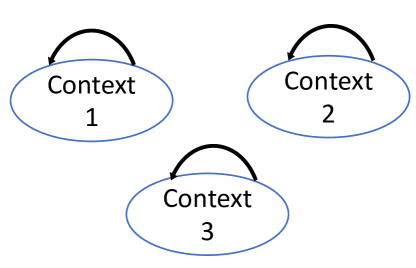

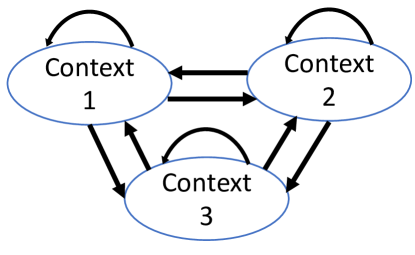

Throughout the paper, we pay a special attention to two particular cases of contextual bandits with cross learning: (i) contextual bandits with no cross-learning and (ii) contextual bandits with complete cross-learning. In the former, the graphs for every only contain self-loops. In the latter, the graphs are fully connected, that is, there is an edge between every pair of contexts. When we are not in either of these two special cases, we refer to the setting as contextual bandits with partial cross-learning. Figure 1 depicts three examples of CL graphs: (i) a CL graph with three contexts () and no cross-learning between contexts (see Figure 1(a)), (ii) a CL graph with three contexts () and complete cross-learning between contexts (see Figure 1(b)), and (iii) a CL graph with partial cross-learning (see Figure 1(c)). In Figure 1(c), contexts are ordered and cross learning happens when , i.e., between consecutive contexts.

In most of the applications we consider in this work (see Section 5), one can consider complete cross-learning between contexts. For example, in the problem of bidding in non-truthful auctions, if a bidder wins an auction with a certain bid, it is generally possible to evaluate the counterfactual outcome “how much utility would have been obtained if the valuation was different but the bid was the same.” Such counterfactual outcomes can be estimated if, for the same bid, a change in the bidder’s value would not affect the bids of competitors. In many applications, however, such counterfactual outcomes cannot be estimated for all contexts but, instead, for contexts that are “close” to each other in some sense. In the bidding example, it is reasonable to assume that small changes in the bidder’s valuation should not drastically impact the competitive landscape. Therefore, partial cross-learning can be used to model conservative learners that only use local information obtained from cross-learning. Such a conservative learner might be concerned about inaccuracies in their cross-learning model due to a significant differences in the contexts.

We highlight that in defining our regret bounds for the contextual bandit setting with cross-learning between contexts, we use our stationary benchmarks defined in Section 2.2. We finish this section by presenting graph invariants. These invariants appear in our analysis of our algorithms, as well as, our regret bounds.

2.3.1 Graph Invariants

Throughout the remainder of this section, we will assume that all graphs are directed and contain all self-loops. Given a vertex in , let denote the set of in-neighbors, i.e., the set of vertices such that there exists an edge , and let denote the set of vertices of out-neighbors, i.e., the set of vertices such that there exists an edge . Because all our graphs contain self-loops, and .

We define the following quantities of graph : (i) clique covering number, denoted by , (ii) independence number, denoted by , and (iii) maximum acyclic subgraph number, denoted by . These quantities will appear in our regret bounds. We further define another metric, denoted by , which can be thought of as an “ variant” of (see Lemma 2.4). This function will appear in our lower bounds, provided in Section 4. Finally, at the end of this section, we present a lemma comparing these quantities. To wit, we show that for any graph , we have .

Definition 2.1 (Clique Covering Number)

A subclique of a graph is a subset of vertices such that for any two vertices , there exists an edge . A clique cover of a graph is a partition of its set of vertices into subcliques (we say is the size of the clique cover). The clique covering number is the minimum size of a clique cover of .

For CL graphs associated with complete cross-learning (see Figure 1(b)), . For CL graphs associated with no cross-learning (see Figure 1(a)), . For the CL graph in Figure 1, is .

Definition 2.2 (Independence Number)

An independent set in a graph is a subset of vertices such that for any two distinct vertices , the edge does not exist in . The independence number is the maximum size of an independent set of .

Again, it is easy to see that for the CL graphs in Figures 1(a), 1(b), and 1(c), is , , and , respectively.

Definition 2.3 (Maximum Acyclic Subgraph Number)

An acyclic subgraph of a graph is a set of vertices that can be ordered such that for any , there is no edge . The maximum acyclic subgraph number is the size of the largest acyclic subgraph of .

We note that for the CL graphs in in Figures 1(a), 1(b) and 1(c), is again , , and , respectively. The following lemma sheds light on the maximum acyclic subgraph number .

Lemma 2.4

For all directed graphs with self-loops,

Next, we define another graph quantity and compare all the quantities that we have defined so far.

Definition 2.5

The value of a graph (with vertex set ) is given by

Comparing the definition of with in Lemma 2.4 confirms that can be seen as variant of the maximum acyclic subgraph number . For the CL graphs in Figures 1(a), 1(b) and 1(c), is again , , and , respectively. The result for the CL graph in Figure 1(c) can be obtained by choosing for all in an independent set of in Definition 2.5; alternatively, it follows from the fact that ; see the following lemma.

Lemma 2.6 (Comparing Graph Quantities)

For all graphs ,

Furthermore, when is the union of disjoint cliques, equality holds for all inequalities and all invariants equal .

Lemma 2.6 shows that for any graph , its independence number is smaller than its variant of the maximum acyclic number, i.e., , and the latter is smaller than or equal to the maximum acyclic number of the graph, i.e., . Finally, is smaller than or equal to the clique covering number of the graph . These inequalities will help us compare our regret bounds under the cross learning; see Section 4. In Lemma 2.6, we further show that if graph is the union of disjoint cliques, then .

3 Algorithms for Cross-Learning Between Contexts

In this section, we present three algorithms for the contextual bandits problem with cross-learning. The first algorithm called UCB1.CL is designed for settings with stochastic rewards and adversarial contexts (Section 3.1). The two other algorithms called EXP3.CL and EXP3.CL-U are designed for settings with adversarial rewards and stochastic contexts. While EXP3.CL (Section 3.2.1) has full knowledge of the context distribution, EXP3.CL-U (Section 3.2.2) does not have this knowledge. (“U” in EXP3.CL-U stands for “Unknown” context distribution.) Then, in Section 3.3, we show that even with complete cross-learning, it is impossible to achieve regret better than when both rewards and contexts are controlled by an adversary (in particular, when both rewards and contexts are adversarial, cross-learning may not be beneficial at all).

3.1 UCB1.CL Algorithm for Stochastic Rewards

In this section, we present a low-regret algorithm, called UCB1.CL, for the contextual bandits problem with cross-learning in the stochastic reward setting: i.e., every reward is drawn independently from an unknown distribution supported on . Importantly, this algorithm works even when the contexts are chosen adversarially, unlike our algorithms for the adversarial reward setting. We call this algorithm UCB1.CL (Algorithm 1). For simplicity, we will begin by describing UCB1.CL and the intuition behind it in the complete cross-learning setting (when all the graphs are the complete directed graph). We will then describe how to modify it for the case of partial cross-learning.

3.1.1 UCB1.CL Algorithm for Complete Cross-learning

The UCB1.CL algorithm is a generalization of -UCB1; both algorithms maintain a mean and upper confidence bound for each action in each context, and always choose the action with the highest upper confidence bound. The difference being that UCB1.CL uses cross-learning to update the means and confidence bounds for every context. Namely, when arm is pulled in a round under context , we update the means and confidence bounds for arm in every other context . (Recall that we under complete cross-learning, the CL graphs are complete directed graphs.)

While there are similarities between -UCB1 and UCB1.CL, the analysis of UCB1.CL requires new ideas to deal with the fact that the observations of rewards may be drawn from a very different distribution than the desired exploration distribution. Very roughly, the analysis is structured as follows. Since rewards are stochastic, in every context , there is a “best arm” that the optimal policy always plays. Every other arm is some amount worse in expectation than the best arm. Here, and is the average reward of arm under context . After observing this arm times, one can be confident that this arm is not the best arm. We can decompose the regret into the regret incurred “before” and “after” the algorithm is confident that an arm is not optimal in a specific context. The regret after the algorithm is confident, which we call “post-regret,” can be bounded using standard techniques from the bandit literature. Our main contribution is the bound of the regret that UCB1.CL incurs before it gets confident. We refer to this regret as “pre-regret.”

Consider a complete cross-learning setting and fix an arm and let be the number of times the algorithm pulls arm in context before pulling arm a total of times across all contexts. Because once arm is pulled times, we are confident about the optimality of pulling that arm in context , we only need to control the number pulls before . Therefore, the pre-regret of arm is roughly .

We control the pre-regret by setting up a linear program in the variables with the objective of . Because counts all pulls of arm before , we have that . This inequality, while valid, does not lead to a tight regret bound. To obtain a tighter inequality, we first sort the contexts in terms of the samples needed to learn whether an arm is optimal, i.e., in increasing order of . Because a different context is realized in every round, we can consider the inequality , which counts the subset of first pulls of arm . This set of inequalities give us our desired bound for pre-regret. Under partial cross-learning, we have similar set of inequalities. These inequalities, however, are slightly modified to incorporate the CL graph under partial cross-learning.

3.1.2 UCB1.CL Algorithm for Partial Cross-learning

In the case of partial cross-learning, we can run almost the same algorithm as described above, with the slight change that instead of updating our statistics for arm in every context, we only update these statistics for the contexts which we learn about – i.e., exactly the contexts in (recall that an edge in indicates that playing action in context , reveals the reward of action in context ). Much of the same intuition applies to the analysis as well, with the change that now the solution of the linear program we obtain will depend on properties of the graphs (specifically, their clique numbers; see Theorem 3.1).

3.1.3 Regret of UCB1.CL Algorithm

Let be the average clique cover size of all graphs . Recall that is the clique covering number of graph and is defined in Definition 2.1. In Theorem 3.1, we show that algorithm UCB1.CL incurs at most regret. Observe that when we have complete cross-learning, the CL graph , , is a complete graph with . Thus, Theorem 3.1 gives the regret of for the case of complete cross-learning. Observe that the dependency on the number of contexts is completely removed in the regret bound. For the case of no cross-learning, the CL graph , , only contains self-loops with . Then, with no cross-learning, Theorem 3.1 gives the regret of , as expected.

Theorem 3.1 (Regret of UCB1.CL)

Let (where ). Then, UCB1.CL (Algorithm 1) has an expected gap-dependent regret of and an expected gap-independent regret of for the contextual bandits problem with cross-learning in the setting with stochastic rewards and adversarial contexts, where , and , which is the clique covering number of the CL graph , is defined in Definition 2.1.

To develop some intuition for Theorem 3.1, consider the case when is the union of disjoint cliques. In this case, all metrics (including ) presented in Lemma 2.6 of Section 2.3.1 take value . Because each component is disjoint and fully connected, it is possible to cross learn for all contexts within each clique, but contexts from different cliques provide no information on each other. Hence, the learning problem perfectly decouples across cliques and leads to a regret of . The clique covering number measures the number of cliques needed to cover the graph and thus captures to what extent we can cross learn on graphs that do not perfectly decompose into disjoint cliques.

3.1.4 Proof of Theorem 3.1

Proof 3.2

Proof of Theorem 3.1 We begin by defining the following notation. Let be the mean of distribution . Let , and let . Let be the gap between the expected reward of playing arm in context and of playing the optimal arm in context . Let be the number of times arm has been pulled in context up to round . Note that the regret of our algorithm is then equal to

Fix a value to be chosen later. Note that the sum of all terms in the above expression with is at most . We can therefore write

For convenience of notation, from now on, without loss of generality, we assume that all , and suppress the condition in the indicator variables.

Now, define . This quantity represents the number of times one must pull arm to observe that arm is not the best arm in context (we will show this later). Define (as in Algorithm 1)

Note that , which can be written as , is equal to the number of times up to round we observe the reward of arm in context . We now define

| (1) | ||||

| (2) |

These two quantities represent the regret incurred before and after (respectively) the algorithm “realizes” an arm is not optimal in a specific context. We refer to and as pre- and post-regret, respectively. With these quantities, almost surely, we have

| (3) |

In the following two lemmas, we will bound the expected values of and . In particular, the following lemma that bounds is our main technical contribution in this proof.

Lemma 3.3 (Bounding the Pre-regret)

Let be the quantity defined in (1). Then,

Proof 3.4

Proof of Lemma 3.3 Fix an action , and let be a minimal clique covering of the graph . Let equal the value of such that . For each , define

The quantity can be thought of the number of times we play arm in a context belonging to clique . Note that since is a clique, this is also (a lower bound on) the number of times we observe the reward of all the arms in clique .

Note that for all , (since is a clique, all contexts in have an edge leading to ). It follows that . (Under complete cross-learning, .) Now, define as

The quantity can be thought of as the number of times action is played during context before the th time we have observed the payoff of action in this context (and the other contexts of ). Note that since , it is true that

and therefore

Fix an , and order the contexts in given by so that (and thus ). From the ordering of the , we have the following system of inequalities:

| (4) |

To see why the above inequalities hold, for simplicity, focus on the second inequality (the same argument can be applied for other inequalities). First note that by the fact that , we have

(Recall that .) This implies that

The right hand side of the above inequality is in turn at most , since each time or and , increases by 1. This proves the second inequality in (4); the other inequalities follow similarly.

Now, we wish to bound . To do this, multiply the th inequality in Equation (4) by (for the last inequality, just multiply it through by ), and sum all of these inequalities to obtain

where the second equation follows because , and the third equation holds because for any . Therefore, summing over all , we have that

Finally, summing over all actions , we have that

We next proceed to bound the expected value of . This follows from the standard analysis of UCB1. A proof is provided in the appendix.

Lemma 3.5 (Bounding the Post-regret)

Let be the quantity defined in (2). Then,

Substituting the results of Lemmas 3.3 and 3.5 into (3) with , we obtain

| (5) |

where the inequality holds because by definition, . This proves our gap-dependent regret bound. For the gap-independent bound, observe that . Then, one can still apply the the results of Lemmas 3.3 and 3.5 to bound and . By doing so, we obtain

Substituting in , it is straightforward to verify that , as desired.

3.2 Algorithms for Adversarial Rewards and Stochastic Contexts

Here, we consider contextual bandits problem with cross learning when the rewards are adversarially chosen but contexts are stochastically drawn from some distribution . We consider two settings: in the first setting, the learner knows the distribution over contexts and in the second setting, the context distribution is unknown.

3.2.1 EXP3.CL Algorithm for Known Context Distribution

In this section, we present an algorithm called EXP3.CL (Algorithm 2). Similar to -EXP3, discussed in the introduction, EXP3.CL maintains a weight for each action in each context, and updates the weights via multiplicative updates by an exponential of an unbiased estimator of the reward. There are two main differences between -EXP3 and EXP3.CL. First, while -EXP3 only updates the weight of the chosen action for the current context (i.e., ), EXP3.CL uses the information from cross-learning to update the weight of the chosen action for more contexts. Precisely, suppose that EXP3.CL plays arm in round under context . Then, EXP3.CL updates the weight of any context in . (For the case of complete cross-learning, the weight of all contexts are updated.)

Second, to take advantage of the information from cross-learning, EXP3.CL modifies -EXP3 by changing the unbiased estimator in the update rule. For -EXP3, is an unbiased estimator (over the algorithm’s randomness) of the reward the adversary chooses from pulling arm in context , where is the probability the algorithm chooses action in round if the context is . However, to minimize regret, EXP3.CL chooses an unbiased estimator with minimal variance (as the expected variance of this estimator shows up in the final regret bound). The new estimator in question is

| (6) |

It is easy to see that this is an unbiased estimator of the reward of arm under context (see the proof of Theorem 3.6). Observe that in the denominator of the estimator, we only consider contexts . This is because we only learn the reward of arm under context when this arm is played under context . Note that by definition, .

Let be the average size of the maximum acyclic subgraph over all graphs . We will show that EXP3.CL obtains at most regret. Then, with complete cross-learning, Theorem 3.6 provides regret of , completing removing the dependency on the number of contexts . This is because under complete cross-learning, CL graphs are complete graphs and their maximum acyclic subgraph number is one. In addition, as expected, with no cross-learning, Theorem 3.6 provides regret of .

Theorem 3.6 (Regret of EXP3.CL)

At a high level, the fact that EXP3.CL obtains a good regret bound follows from the quality of the estimator used in this algorithm. Once we have this estimator, we follow the standard analysis of multiplicative weights/EXP3 algorithms. More specifically, we use the sum of the weights as a proxy for the regret bound of the EXP3.CL. Roughly speaking, the higher the sum of the weights , the better EXP3.CL has performed till time (see how the weights are updated in this algorithm). In light of this, in the proof, for any context , we lower/upper bound the expected value of as a function of mean and variance of the estimator in EXP3.CL, as well as, the expected reward earned by EXP3.CL. Comparing the lower bound with the upper bound gives us the desired regret bound.

3.2.2 EXP3.CL-U Algorithm for Unknown Context Distribution

In Section 3.2.1, we presented an algorithm called EXP3.CL with regret of for the setting with adversarial rewards and stochastic contexts. This algorithm uses the knowledge of the context distribution to come up with an unbiased estimator with low variance. In this section, we relax the assumption of knowing distribution , and we present an algorithm for the contextual bandits problem with cross-learning in the setting when rewards are adversarial and contexts are stochastic, but when the learner does not know the distribution over contexts. We call this algorithm EXP3.CL-U (see Algorithm 3). In this algorithm, we additionally assume all the CL graphs , are the same and equal to a single graph (we will see that this assumption is critical to constructing a consistently biased estimator for the rewards; see our discussion about the expectation of our estimator, i.e., later in this section). Since we assume that for any , in the algorithm, we simply write and in place of and ).

EXP3.CL-U is similar to EXP3.CL, in that all the algorithms maintain a weight for each action in each context, and update the weights via multiplicative updates by an exponential of an estimator of the reward. The main difference between EXP3.CL-U and EXP3.CL is their estimators. The estimator in EXP3.CL, given in Equation (6), uses the knowledge of distribution while the estimator in EXP3.CL, which is defined below, cannot use such knowledge:

| (7) |

We highlight that unlike the estimator in EXP3.CL, is not an unbiased estimator of for partial cross learning. (This estimator is only unbiased under complete cross-learning.) Indeed, we have that:

However, note that we can write in the form , where is a function which only depends on a context (and in this case is given by ). That is, our estimator is consistently biased across all actions for a fixed context . It turns out this property is enough to adapt the previous analysis of Theorem 3.6.

Given this estimator, the question is why does EXP3.CL-U have regret of order (see Theorem 3.7) when the dependence on in EXP3.CL is only of order ? The answer lies in understanding how the variance of the unbiased estimator used affects the regret bound of the algorithm. In the standard analysis of EXP3 (and EXP3.CL and -EXP3), one of the quantities in the regret bound is the total expected variance of the estimator of rewards. In -EXP3, this quantity takes the form

However, in EXP3.CL-U (where the desired exploration distribution can differ from the exploration distribution due to cross-learning), this quantity becomes

Optimizing (through selecting the parameter ) leads to a regret bound. In the case of complete cross-learning, and we have a regret bound.

Theorem 3.7 (Regret of EXP3.CL-U)

Consider the contextual bandits problem with adversarial rewards, and stochastic contexts, where all the CL graphs are equal to and the context distribution is unknown. Let be the maximum acyclic subgraph number of (defined in Definition 2.3). Then EXP3.CL-U (Algorithm 3) incurs at most regret in this setting.

Observe that the regret bound of both EXP3.CL-U and EXP3.CL algorithm scales with the maximum acyclic subgraph number of (i.e., defined in Definition 2.3), where for complete cross-learning settings and when there is no cross-learning between contexts. However, as stated earlier, while the regret of EXP3.CL scales with , the regret of EXP3.CL-U scales with . An interesting open problem is determining whether it is possible to achieve regret in the adversarial reward regime without knowing the distribution over contexts.

We have explored this open problem by considering an extension of EXP3.CL algorithm. For this discussion, we focus on the complete cross-learning setting. The main feature of EXP3.CL is its low-variance unbiased estimator , where the denominator is . However, this unbiased estimator and, in particular, its denominator require knowledge of the distribution over contexts. Our idea is to replace this unbiased estimator with a similar estimator , where is some sufficiently close approximation to that does not require knowledge of the distribution over contexts. One natural choice is to replace the true probability of context with the current empirical probability to get While our empirical evaluation in Section 6 provides some convincing evidence that the proposed approach works well, we were not able to theoretically prove that the described algorithm obtains regret on the order of . In Appendix 11, we discuss the main technical challenges we encountered for analyzing this algorithm. Nonetheless, we conjecture that this proposed algorithm incurs at most regret.

3.3 Adversarial Rewards and Adversarial Contexts

A natural question is whether we can design an algorithm whose regret is lower than that of -EXP3 when both the rewards and contexts are chosen adversarially (but where we still can cross-learn between different contexts). A positive answer to this question would subsume the results of the previous sections. Unfortunately, we next show that even under complete cross-learning, any learning algorithm for the contextual bandits problem with cross-learning must necessarily incur regret (which is achieved by -EXP3).

We will need the following regret lower-bound for the (non-contextual) multi-armed bandits problem from Auer et al. (2002).

Lemma 3.8 (Auer et al. 2002)

There exists a distribution over instances of the multi-armed bandit problem where any algorithm must incur an expected regret of at least .

For concreteness, we describe one instance of a reward distribution over instances (parametrized by and ), denoted by , that satisfies Lemma 3.8. This distribution is the uniform distribution over instances under which rewards of each arm are drawn from independent Bernoulli distributions. In the th instance, the rewards of arm are drawn from (i.e., a Bernoulli distribution with mean ), and the rewards of all other arms are drawn from (i.e., in th instance, arm is the optimal arm and this arm outperforms all other arms by at least ).

With this lemma, we can construct the following lower-bound for the contextual bandits problem with (complete) cross-learning by connecting independent copies of these hard instances in sequence with one another so that cross-learning between instances is not possible.

Theorem 3.9 (Regret Lower Bound for Adversarial Rewards and Adversarial Contexts)

There exists a distribution over instances of the contextual bandit problem with complete cross-learning where any algorithm must incur a regret of at least .

Proof 3.10

Proof of Theorem 3.9

Divide the rounds into epochs of rounds each. Label the contexts , and adversarially assign contexts so that the context during the th epoch is always .

Next, assign rewards so that if is in the th epoch and . In other words, during the th epoch in which the context is , the rewards of all other contexts are zero. On the other hand, for in the th epoch, set rewards according to a hard instance for the multi-armed bandit problem sampled from the distribution satisfying Lemma 3.8. Call this random instance , and let be the (random) optimal action to play in , i.e., the action with rewards drawn from . Figure 2 provides a pictorial representation of the worst-case instance.

| contexts | 0 | 0 | |||

|---|---|---|---|---|---|

| 0 | 0 | ||||

| 0 | 0 | ||||

| time | |||||

Note that in this construction, cross-learning between contexts offers zero additional information, since all cross-learned rewards will be deterministically (and thus can be simulated by a learner without access to cross-learning). It suffices to show that any contextual bandits algorithm in the classic setting (i.e., without cross-learning) must incur regret at least on this distribution over instances.

Consider the (optimal) stationary strategy that plays (i.e., the optimal action under instance ) whenever the context is . Fix an arbitrary contextual bandit algorithm and consider its performance on the th epoch. We argue that receives at least more reward in expectation than algorithm on this epoch because the length of the epochs is . To see this, note that if this were not the case, by examining the restriction of to the rounds in this epoch, we can construct an algorithm for the regular multi-armed bandit problem that would violate Lemma 3.8.

It follows that over all epochs our strategy receives at least more reward in expectation than algorithm . Thus, any algorithm must have regret at least when compared to the optimal stationary strategy.\Halmos

4 Regret Lower Bounds under Cross-Learning

In this section, we prove some lower bounds on regret for contextual bandits with cross-learning that complement the results of the previous two sections. In our lower bounds, we will consider a restricted set of instances where the graph of each arm is equal to the same graph . We present two lower bounds. The first lower bound, presented in Theorem 4.1, is for a setting with stochastic rewards and stochastic contexts. We show that in this setting, any algorithm must incur expected regret of , where is defined in Definition 2.5. The second lower bound, presented in Theorem 4.2, is for a setting with stochastic rewards and adversarial contexts. We show that in this setting, any algorithm must incur expected regret of , where is the maximum acyclic subgraph number of graph and is defined in Definition 2.3. Recall that by Lemma 2.6, for all graphs , , and by Theorem 3.1, when , , the expected regret of UCB1.CL under stochastic rewards and stochastic/adversarial contexts is .

We note that per Lemma 2.6, if graph is the union of disjoint cliques, then . Note that for complete cross-learning setting (i.e., fully connected CL graph), and for no cross-learning setting (i.e., CL graphs with only self loops), is equal to the number of contexts . This shows that our regret bounds are tight for certain graphs that are the union of disjoint cliques. In fact, our regret bounds are tight for an even larger family of graphs: all graphs where . This is true for unions of disjoint cliques, for the line graph in Figure 1(c), and more generally for any undirected graph (i.e., directed graphs with symmetric edges) which is perfect. In graph theory, a perfect (undirected) graph is a graph where for any subgraph of , the size of the largest clique of is equal to the chromatic number of (the minimum number of colors needed to color the vertices of so that no two adjacent vertices share the same color). It follows as a simple corollary of the perfect graph theorem (Lovász 1972b, a) that any perfect graph satisfies . Perfect graphs include all bipartite graphs, forests, interval graphs, and comparability graphs of posets (see, e.g., West et al. 1996).

4.1 Regret Lower Bound with Stochastic Rewards and Contexts

The following theorem is the main result of this section.

Theorem 4.1 (Lower Bound with Stochastic Rewards and Contexts)

Any learning algorithm solving the contextual bandits problem with cross-learning (for a fixed CL graph ) and stochastic rewards and stochastic contexts must incur expected regret of , where is defined in Definition 2.5.

Note also Theorem 4.1 holds as a lower bound in the adversarial rewards and stochastic contexts setting. Although the regret benchmarks differ slightly between the adversarial rewards and stochastic rewards setting, they differ by at most , which is subsumed by the regret bound in Theorem 4.1. See Appendix 8.1 for more details.

Roughly, the proof of Theorem 4.1 proceeds as follows. For each context, we choose a “hard” distribution of rewards such that any algorithm that has only seen samples of rewards must incur expected regret in their next round. Now, if we fix a distribution over contexts, then after rounds, we expect to have seen approximately total samples of rewards from context , where . Over all rounds, our regret is therefore at least Taking the supremum over , we find that the total expected regret is at least ; see the definition of in Definition 2.5.

4.2 Regret Lower Bound with Stochastic Rewards and Adversarial Contexts

We now present our second lower bound for the setting with stochastic rewards and adversarial contexts. When we allow the contexts to be adversarially chosen, we can improve the lower bound to .

Theorem 4.2 (Lower Bound with Stochastic Rewards and Adversarial Contexts)

Any learning algorithm solving the contextual bandits problem with cross-learning (for a fixed CL graph ) with stochastic rewards and adversarial contexts must incur regret , where is the maximum acyclic subgraph number of graph and is defined in Definition 2.3.

Note that when the graphs are undirected, (since in that case, the definition of acyclic subgraph and independent set coincide), and therefore (by Lemma 2.6). It follows that when all are undirected and equal, the lower bound of Theorem 4.2 matches the upper bound of Theorem 3.6 in the setting where contexts are stochastic. Likewise, as stated earlier, when is the disjoint union of cliques, all of our graph invariants coincide, and our lower bounds are tight. In other settings and for other feedback structures an instance-dependent gap between the best upper bound and best lower bound persists; reducing this gap is an interesting open problem.

5 Discussion on Applications of Cross-Learning and Implementation of Proposed Algorithms

In this section, we discuss how to apply our results on cross-learning to the problem of how to bid in a first-price auction. We show that our algorithms yield a non-trivial improvement over naively applying -EXP3 or -UCB. We further discuss how to efficiently implement our algorithms when the number of contexts is infinite. Before presenting our results for first-price auctions, we provide other applications that enjoy cross-learning between contexts and thus fit our framework.

5.1 Applications with Cross-learning: Beyond Bidding in First-price Auctions

The following applications can be modeled as contextual bandit problems with cross-learning between contexts. Here, we present an overview of these applications and we defer the details of how to apply our algorithms to these applications to Appendix 12.

-

1.

Multi-armed bandits with exogenous costs: Consider a multi-armed bandit problem where at the beginning of each round , a cost for playing arm at this round is publicly announced. That is, choosing arm this round results in a net reward of . This captures settings where, for example, a buyer must choose every round to buy one of substitutable goods – they are aware of the price of each good (which might change from round to round) but must learn over time the utility each type of good brings them.

This is a contextual bandits problem where the context in round is the costs () at this time. Cross-learning between contexts is present in this setting: given the net utility of playing action with a given up-front cost , one can infer the net utility of playing with any other up-front cost . For the problem of multi-armed bandits with exogenous costs, standard contextual bandit algorithms get regret . Our algorithms get regret , which is tight. See Appendix 12 for more details.

-

2.

Dynamic pricing with variable cost: Consider a dynamic pricing problem where a firm offers a service (or sells a product) to a stream of customers who arrive sequentially over time. Consumers have private and independent willingness-to-pay and the cost of serving a customer is exogenously given and customer dependent. After observing the cost, the firm decides on what price to offer to the consumer who decides whether to accept the service at the offered price. The optimal price for each consumer is contingent in the cost; for example, when demand is relatively inelastic consumers that are more costly to serve should be quoted higher prices. This extends dynamic pricing problems to cases where the firm has exogenous costs (see, e.g., den Boer 2015 for an overview of dynamic pricing problems).

This is a special case of the multi-armed bandits with exogenous costs problem defined earlier, and hence an instance of contextual bandits with cross-learning.

-

3.

Sleeping bandits: Consider the following variant of “sleeping bandits,” where there are arms and in each round some subset of these arms are awake. The learner can play any arm and observe its reward, but only receives this reward if they play an awake arm. This problem was originally proposed in Kleinberg et al. (2010), where one of the motivating applications is ecommerce settings where not all sellers or items (and hence “arms”) might be available every round.

This is a contextual bandits problem where the context is the set of awake arms. Again, cross-learning between contexts is present in this setting: given the observation of the reward of arm , one can infer the received reward for any context by just checking whether . For our variant of sleeping bandits, standard contextual bandit algorithms get regret . Our algorithms get regret , which is tight. By applying our algorithms, we can achieve regret in the original sleeping bandits setting studied in Kleinberg et al. (2010), which recovers their results and is similarly tight.

-

4.

Repeated Bayesian games with private types: Consider a player participating in a repeated Bayesian game. Each round the player learns their (private and independent) type for the current game, performs some action, and receives some utility (which depends on their type, their action, and the other players’ actions). Again, this can be viewed as a contextual bandit problem where a player’s types are contexts, actions are actions, and utilities are rewards, and once again this problem allows for cross-learning between contexts (as long as the player can compute their utility based on their type and all players’ actions).

5.2 Bidding in first-price auctions

In the problem of learning to bid in a first-price auction, every round (for a total of rounds) an item is put up for auction. This item has value to our bidder. Based on , our bidder submits a bid . Simultaneously, other bidders submit bids for this item; we let be the highest bid of the other bidders in the auction. If , the buyer receives the item and pays , obtaining an utility of ; otherwise, the buyer does not receive the item and pays nothing, obtaining a utility of zero. More formally, the net utility is . The buyer only learns whether or not they receive the item and how much they pay – notably, they do not learn (i.e., this is a non-transparent first price auction). The bidder’s goal is to maximize their total utility (total value of items received minus total payment) over the course of rounds.

As stated in the introduction, this problem can be seen as a contextual bandits problem for the bidder where the context is the bidder’s value for the item, the action is their bid, and their reward is their net utility from the auction: 0 if they do not win, and their value for the item minus their payment if they do win. This problem, indeed, allows for cross-learning between contexts: The net utility that would have been received if they had value instead of value is just , which can be computed from the outcome of the auction assuming the value and highest competing bid (that influences ) are independent of each other.

Here, we assume that the value and the highest competing bid are independently drawn each round from distributions and , respectively, where both distributions are unknown to the bidder. The independence assumption is motivated by the fact that, in online advertising markets, most advertisers base bids on cookies, which are bits of information stored on users’ browsers. Because cookies are private, cookie-based bids are typically weakly correlated. In Section 6, we conduct some experiments using data from a major advertising platform and observe that our cross-learning algorithms that assume complete cross-learning between values perform well even when values are not perfectly independent of the other bids. Nonetheless, conservative learners might be still concerned about such correlation. Under such correlation, with the same action/bid, the chance of winning (i.e., ) under two values that are far from each other may not be the same. For instance, when there is a positive correlation between values and highest competing bids, as the value increases, the highest competing bid may increase as well, reducing the chance of winning. To handle this, such learners can only allow for cross-learning between close values. We remark that, from the theoretical perspective, when the correlation between values and bids is arbitrary, cross-learning is impossible and the decision maker cannot do better than running a different learning algorithm for each context. A promising research direction is to incorporate correlation by introducing a statistical or behavioral model to capture the dependency between bids and values.

Naively applying -UCB to our problem by discretizing the value space and bid space into and pieces respectively results in a regret bound of (here the last two terms come from discretization error). Optimizing and , we find that when , we can achieve regret in this way. On the other hand, by taking advantage of (complete) cross-learning between contexts and applying UCB1.CL, after discretizing the bid space into pieces, results in a regret bound of . By optimizing this, we get an algorithm which achieves regret. It follows from a reduction to known results about dynamic pricing that any algorithm must incur regret when learning to bid (even when the value is fixed) – see Appendix 9 for details.555The regret lower bound of is driven by our binary feedback structure. Under the binary feedback structure, which is commonly assumed in the literature, a bidder can only learn whether they win or lose in an auction. The follow-up paper Han et al. (2020) shows that a regret bound of is attainable when the highest bid is revealed at the end of each auction to all the bidders who lost the auction.

Interestingly, in the case of bidding in first-price auctions, the decision maker can also potentially cross-learn across different actions/bids. For example, if the decision maker wins when submitting a bid , then they simultaneously learn that any higher bid would also win the auction. Conversely, if the decision maker does not win, then they learn that lower bids also would necessarily lose in the auction. While our algorithm does not explicitly take into account cross-learning across actions, the previous lower bound shows that, in the worst case, cross-learning across actions does not lead to any additional benefit (in terms of lower regret) if we are already cross-learning across contexts. We emphasize that our algorithms apply when the auctioneer runs other non-truthful auctions.

5.3 Implementation of Proposed Algorithms

We conclude with a brief note on implementation efficiency of our algorithms. Even though, under complete cross-learning, the regret bounds we prove in Section 3 do not scale with , note that the computational complexity of all three of our algorithms from Section 3 (UCB1.CL, EXP3.CL, and EXP3.CL-U) scales with the number of contexts : both algorithms have time complexity per round and space complexity . In many of the above settings, the number of contexts can be very large. For example, when the space of contexts is the interval , the number of contexts is infinite. However, these settings often also have additional structure which let us run these same algorithms with improved complexity.

Most generally, for all the settings we consider, the observed reward is always affine with respect to a function mapping a context into for some small dimension . The function is computable by the learner. That is, for each and , it is possible to write , where and ; moreover, the coefficients and are directly revealed to the learner each round. It in turn follows that the averages stored by UCB1.CL are simply linear functions of . Since there is one such function for each arm , this requires a total of space (i.e., we simply store the running averages and and then determine the average reward using the formula ). Similarly, the coefficients can be updated each round in time simply by updating the average for . For example, for the update is given by

Likewise, the weights stored by EXP3.CL, for example, are always of the form , and again it suffices to just maintain a linear function of (with the caveat that to compute the estimators, we must be able to efficiently take expectations over our known distribution on contexts).

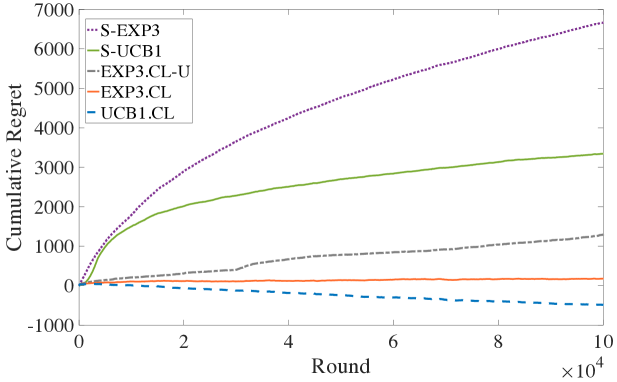

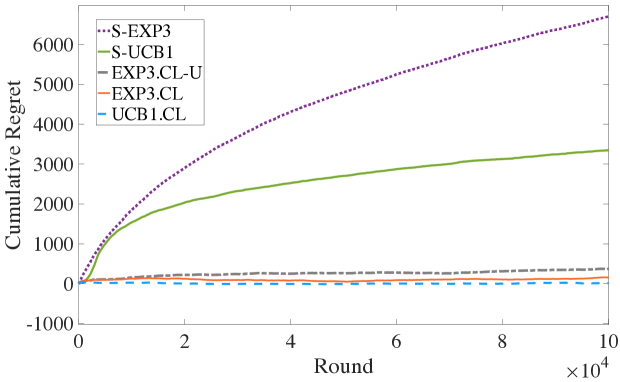

6 Empirical Evaluation

In this section, we empirically evaluate the performance of our contextual bandit algorithms on the problem of learning how to bid in a first-price auction.

Recall that our cross-learning algorithms rely on cross-learning between contexts being possible: if the outcome of the auction remains the same, the bidder can compute their net utility they would receive given any value they could have for the item. This is true if the bidder’s value for the item is independent of the other bidders’ values for the item. Of course, this assumption (while common in much research in auction theory) does not necessarily hold in practice. We can nonetheless run our contextual bandit algorithms (with complete cross-learning) as if this were the case, and compare them to existing contextual bandit algorithms which do not make this assumption.

Our basic experimental setup is as follows. We take existing first-price auction data from a large ad exchange that runs first-price auctions on a significant fraction of traffic, remove one participant (whose true values we have access to), substitute in one of our bandit algorithms for this participant, and replay the auction. This experiment answers the question “how well would this (now removed) participant do if they instead ran this bandit algorithm?”

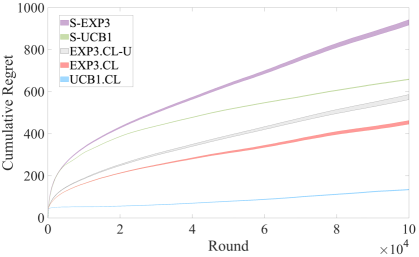

We collected anonymized data from 10 million consecutive auctions from this ad exchange, which were then divided into 100 groups of auctions. To remove outliers, bids and values above the 90% quantile were removed, and remaining bids/values were normalized to fit in the interval.666Our numerical results in Appendix 13 show that the performance of our algorithms is robust to outliers and, thus, not sensitive to how outliers are handled. We then replayed each group of auctions, comparing the performance of our algorithms with cross-learning (UCB1.CL, EXP3.CL, and EXP3.CL-U) and the performance of classic contextual bandits algorithms that take no advantage of cross-learning (-EXP3, and -UCB1). To run EXP3.CL, we do not assume that we know the distribution over contexts. Instead, we replace the estimator in EXP3.CL with its empirical version, presented at the end of Section 3.2.2. More specifically, we consider the following estimator where does not require knowledge of the distribution over contexts. Here, is the empirical estimate (sample mean) of the true probability of context .

All algorithms considered here require a discretized set of actions. Thus, allowable bids are discretized to multiples of . Parameters for each of these algorithms (including level of discretization of contexts for -EXP3 and -UCB1) were optimized via cross-validation on a separate data set of auctions from the same ad exchange.