Exact adaptive confidence intervals for small areas

Abstract

In the analysis of survey data it is of interest to estimate and quantify uncertainty about means or totals for each of several non-overlapping subpopulations, or areas. When the sample size for a given area is small, standard confidence intervals based on data only from that area can be unacceptably wide. In order to reduce interval width, practitioners often utilize multilevel models in order to borrow information across areas, resulting in intervals centered around shrinkage estimators. However, such intervals only have the nominal coverage rate on average across areas under the assumed model for across-area heterogeneity. The coverage rate for a given area depends on the actual value of the area mean, and can be nearly zero for areas with means that are far from the across-group average. As such, the use of uncertainty intervals centered around shrinkage estimators are inappropriate when area-specific coverage rates are desired. In this article, we propose an alternative confidence interval procedure for area means and totals under normally distributed sampling errors. This procedure not only has constant frequentist coverage for all values of the target quantity, but also uses auxiliary information to borrow information across areas. Because of this, the corresponding intervals have shorter expected lengths than standard confidence intervals centered on the unbiased direct estimator. Importantly, the coverage of the procedure does not depend on the assumed model for across-area heterogeneity. Rather, improvements to the model for across-area heterogeneity result in reduced expected interval width.

Keywords: empirical Bayes, Fay-Herriot model, frequentist coverage, hierarchical model, prediction interval, shrinkage.

1 Introduction

Studies that gather data from non-overlapping areas (subpopulations) are common in a variety of disciplines, including ecology Brewer \BBA Nolan (\APACyear2007), education Wall (\APACyear2004), epidemiology Ghosh \BOthers. (\APACyear1999), and public policy Maples (\APACyear2017). As policy interventions have become more targeted, the demand for precise estimates of population characteristics of these areas has increased. To estimate target quantities, sample surveys may use “direct” estimators, which are only based on the area-specific sample data. Direct estimators typically utilize survey weights, with corresponding inferences made based on the sampling design Rao \BBA Molina (\APACyear2015). When the direct estimates are area-specific sample averages (possibly weighted), the central limit theorem justifies the area-specific sampling model , where is a design-unbiased and consistent direct estimate of , the th area mean, and is the variance of the direct estimate under the sampling design. If additionally the survey data are sampled independently across areas, the joint sampling model for the area-specific direct estimates is

| (1) |

where , , and a diagonal matrix with elements .

For a specific area , when is assumed known, the classical “direct” confidence interval for is

| (2) |

where is the th quantile of the standard normal distribution. This direct confidence interval has the important property of area-specific coverage under the sampling model (1), since

| (3) |

for all and .

However, it is sometimes the case that there are areas with small sample sizes under the survey design, resulting in unacceptably wide direct confidence intervals Pfeffermann (\APACyear2013). When additional precision is needed, model-based estimators are used to borrow information from other areas and utilize area-level auxiliary covariates. A statistical model for across-area heterogeneity is referred to as a linking model in the small area estimation literature. For example, the popular Fay-Herriot model Fay \BBA Herriot (\APACyear1979) posits that , independently across areas, where is a vector of observed area-specific covariates. If appropriate values of were known, then Bayes’ rule could be used to obtain the conditional distribution of given . From this distribution, one could compute a Bayesian credible interval

| (4) |

where and are the conditional mean and variance of given , respectively.

In practice, appropriate values for the linking model parameters are unknown. A Bayesian approach is to place a prior distribution on , from which the joint posterior distribution of may be obtained You \BBA Chapman (\APACyear2006). A more common approach is an empirical Bayes strategy, whereby “plug-in” estimates of are obtained from the marginal likelihood of , which is itself obtained by integrating the density of the sampling model (1) for over the values of with respect to the linking model. Given such an estimate of , the empirical Bayes confidence interval is given by

| (5) |

where and are the conditional mean and variance of , given and using as the parameters in the linking model. Adjustments are often made to due to the uncertainty in estimating .

The Bayesian credible interval procedure has the property of population-level coverage, in the sense that the coverage level is on average with respect to the linking model. Specifically,

| (6) |

where is the probability density of under the linking model. The empirical Bayes confidence interval procedure has this property asymptotically in the number of groups, as long as is a consistent estimator of . However, neither nor have area-specific coverage, as defined in (3). This is because they are centered around a biased estimator of . To illustrate this lack of area-specific coverage, consider the Fay-Herriot linking model

| (7) |

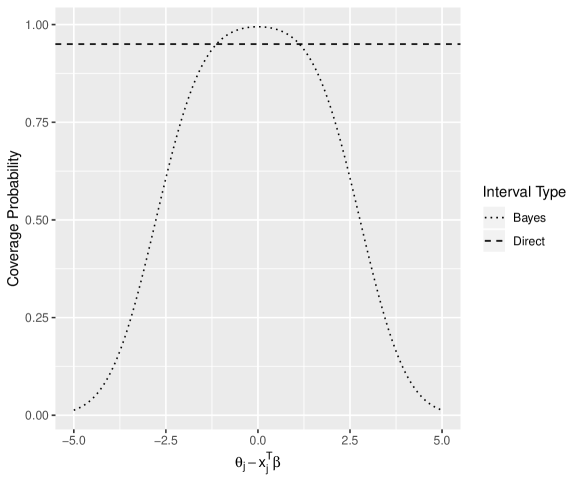

where is a vector of covariates for area . Standard conditional probability calculations (provided in the appendix) give that the area-specific coverage of is a function of and can be expressed as , where is the standard normal cumulative distribution function. In general, the coverage probability for a given area will be higher than the nominal level when is close to and lower when is far away from , a relationship that is visualized in Figure 1. This difference is amplified when the linking model variance is small relative to the sampling variance .

In many applications, policy decisions and interventions are frequently targeted at outlying groups or areas. In these cases, it is important that uncertainty intervals have area-specific coverage, so that the study has sufficient power to detect extreme values of the target quantity, regardless of what it may be. If area-specific coverage is desired, neither the nor interval procedures can be recommended, as their coverage levels will vary as a function of the target quantity . However, intervals generated by the direct interval procedure may also be unsatisfactory, since they may be too wide to be useful when area sample sizes are small, as they do not make use of information across areas. In this article we propose a confidence interval procedure for small area analysis that maintains exact area-specific coverage, while also allowing for information sharing across areas, thereby offering improved precision over direct interval procedures. Like direct confidence intervals, these intervals have exact area-specific coverage under the sampling model (1), regardless of whether or not a particular linking model is accurate. Importantly, unlike the Bayes and empirical Bayes procedures, our procedure is appropriate for area-level inference in that it maintains area-specific coverage rates. However, like the Bayes and empirical Bayes intervals, our proposed intervals will be shorter than the direct intervals on average with respect to the linking model.

Our proposed interval procedure extends that of \citeAyuhoff16, who developed an adaptive procedure with area-specific coverage using an exchangeable linking model. In this article we extend this idea to the types of linking models often used for small area analysis, including models that allow for area-specific features and spatial or temporal correlation between area means. In Section 2, we briefly review the interval procedure first developed by \citeApratt63, and extended by \citeAyuhoff16 to include the case of unknown sampling variances. We also demonstrate how to apply these ideas to the analysis of small areas, using the spatial Fay-Herriot linking model as a running example. Section 3 describes a simulation study designed to compare interval procedures under a variety of linking models. In Section 4 we apply our methodology to estimate household radon levels in 196 U.S. counties. A discussion follows in Section 5.

2 Methods

2.1 The FAB interval procedure

We first consider constructing a confidence interval procedure for a specific group , based on the sampling model (1), where for now we assume to be known. Let be any function mapping to the unit interval , possibly depending on data from other areas, that is, . Then, assuming the sampling model, it is easily verified that

| (8) |

is a valid frequentist confidence region, satisfying the area-specific coverage property (3). The standard direct interval corresponds to .

Now suppose that, based on and a linking model, we believe is likely to be near some value . We encode this belief with a normal probability distribution . For example, and might be the conditional expectation and variance of , given and the linking model. Given such information, we may prefer an area-specific interval procedure that, relative to the direct interval, is more precise (has shorter expected width) for values of near , at the expense of having longer expected width for values of deemed unlikely by the linking model. We may then wish to use the area-specific interval procedure that minimizes the expected width, relative to the linking model.

The minimizer of this expected width among all frequentist intervals can be obtained using results of \citeApratt63, who considered frequentist interval construction for a single mean parameter with a normal prior distribution. The frequentist interval that has minimum width, on average with respect to a distribution for , can be shown to be given by (8) with

| (9) | ||||

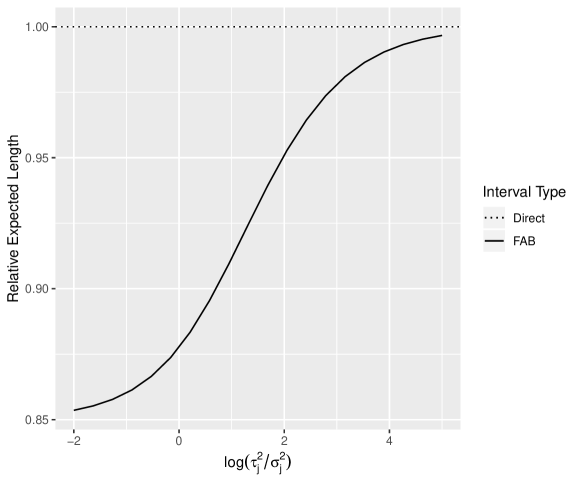

Following \citeAyuhoff16, we refer to confidence intervals constructed in this way as FAB intervals because, thinking of the conditional distribution of given as a prior distribution, they are “frequentist, assisted by Bayes”. Importantly, even if is located in a region of low probability under the linking model, a FAB interval will still maintain area-specific coverage for . As such, the FAB interval procedure is coverage-robust to misspecification of the linking model. In terms of precision, if the linking model reasonably describes the across-area heterogeneity in means, then the FAB procedure will represent an improvement over the direct procedure, on average across areas (Figure 2). In contrast, the Bayes and empirical Bayes interval procedures do not maintain constant area-level coverage rates even if the linking model perfectly describes the across-area distribution of (unless all area-specific means are the same).

2.2 FAB intervals for the spatial Fay-Herriot model

The spatial Fay-Herriot model is frequently employed by researchers and statistical agencies due to the abundance of cross-sectional survey data that come from non-overlapping geographic areas such as counties, neighborhoods, school districts, and electoral precincts. Area-level direct estimates from this type of data typically exhibit high spatial autocorrelation, in which areas closer together tend to have similar values for their target quantities, even after accounting for the auxiliary covariates.

The spatial Fay-Herriot model includes the sampling model (1) which we assume to be correct, and a spatial linking model for across-unit heterogeneity of the ’s, which we do not assume is correct. The linking model can be written as

| (10) |

where parameterizes the dispersion and spatial relationship of the random effects. The conditional autoregressive (CAR) model and the simultaneous autoregressive (SAR) model are two of the main approaches for structured covariance modeling of spatially autocorrelated areal data Banerjee \BOthers. (\APACyear2014). Following Singh \BOthers. (\APACyear2005) and Pratesi \BBA Salvati (\APACyear2008), we consider the SAR model

| (11) |

where is a neighborhood proximity matrix, a spatial relationship parameter, and a mean-zero random vector with independent normal entries, each with variance . A binary contiguity neighborhood matrix is often chosen for , in which if areas and are neighbors and zero otherwise. Regardless of the choice of , it is typically first row-standardized to make the row elements sum to one. When the proximity matrix is standardized in this way, is non-singular when , and can be treated as a spatial autocorrelation parameter.

Combining the above equations, the linking model for becomes

| (12) |

Our proposed confidence interval for a small area mean is obtained by first using data from the other groups, along with the linking model (12) to obtain a mean and variance that describe the likely values of , and then using these values to construct the FAB interval given by (8) and (9). Recall that the resulting confidence interval has exact coverage for , regardless of the value of or the accuracy of the linking model, as long as the sampling model is correct and the values of and are chosen independently of the value of .

A fully Bayesian approach to obtaining values of and would be to take them to be the conditional mean and variance of given , under a suitable prior distribution for the parameters of the linking model, and computed using a Markov chain Monte Carlo approximation algorithm. However, this can be prohibitively computationally costly, as a separate approximation would need to be run for each area. As a more feasible alternative, we suggest an empirical Bayes approach in which are first estimated from the marginal distribution of , which are then used to obtain empirical Bayes estimates of the ’s. The resulting conditional mean and variance of , using “plug-in” values of and , are given by

| (13) | ||||

where

In sum, the steps to obtain a FAB interval are

-

1.

Estimate linking model parameters using data from all counties other than . Details of maximum likelihood estimation for the spatial Fay-Herriot are provided in the Appendix.

-

2.

Obtain a normal prior distributions for both using plug-in estimates from the fitted linking model. In the case of the spatial Fay-Herriot model, the prior mean and prior variance are given by (13).

-

3.

Obtain the optimal -function for county given prior information about , as described in Section 2.1.

-

4.

Construct the FAB -interval .

2.3 Unknown within-area variances

The procedure detailed above assumes that the sampling variance is known (or known with a high degree of accuracy). However, in practice the variance of the direct estimate of each area is rarely known, and only consistent estimates are available. Under the assumption that the response is normally distributed within area ,

| (14) |

where is the effective number of degrees of freedom for area implied by the sampling design Cochran (\APACyear1977). \citeAyuhoff16 extended Pratt’s original -interval to the case of an unknown sampling variance as follows: If the sample statistics and are independent, where and , then for any nondecreasing function ,

| (15) |

where is the th quantile of the distribution with degrees of freedom, is a valid confidence interval with area-specific coverage. The function can be selected on the basis of prior information about not only the target quantity , but also the sampling variance . If this prior information can be summarized by a normal distribution for and an inverse-gamma distribution for , it is possible to obtain the function that minimizes the prior expected length of the interval (15) via numerical methods described in \citeAyuhoff16. To obtain this prior information, we recommend specifying a linking model for both and , possibly allowing for the presence of auxiliary covariates in the model for . As before, parameters of the linking model can be estimated and moment-matching used to obtain a normal distribution for and an inverse-gamma distribution for , which represent the indirect information about with which a FAB -interval may be constructed. We provide an empirical example of the FAB -interval procedure in Section 4.

3 Simulation study

To compare the properties of FAB intervals and direct intervals, we constructed a simulation study in which area means may exhibit spatial autocorrelation and/or association with an explanatory variable. We aimed to quantify the reduction in expected interval width obtained via the FAB interval procedure relative to the direct interval procedure. Throughout the study, we assumed the sampling model with known for all areas , yielding the direct confidence interval .

Forty-nine areas were located on a lattice. For each of 5000 datasets, we simulated area means under the following procedure:

-

1)

Draw

-

2)

Set

-

3)

Draw

-

4)

Draw ,

This data generating procedure was repeated eight times, one for each setting of , and . In each repetition, the neighborhood matrix was assumed to be a row standardized binary contiguity matrix (a binary contiguity matrix is defined such that the th entry equals 1 if areas and border each other, and otherwise).

3.1 Intervals with Area-Specific Coverage

For each area in a dataset, we constructed five types of 95% confidence intervals that have area-specific coverage. These consist of the direct interval and four different FAB intervals based on maximum likelihood estimation of linking models ranging in complexity. The linking models considered were

-

1)

The exchangeable model: independently across groups .

-

2)

The covariate model: independently across groups .

-

3)

The spatial model: .

-

4)

The full model: .

Under each data generating process, average interval lengths over all simulations for these five confidence interval procedures were calculated. Average lengths relative to the direct interval are given in Table 1 for each of the four FAB procedures. For the simulations in which the data were generated with strong spatial autocorrelation , the spatial FAB intervals outperformed their non-spatial counterparts in terms of average interval width. Similarly, the non-spatial FAB intervals are slightly narrower than their spatial counterparts when the data is generated without spatial autocorrelation due to the increased uncertainty that comes with estimating . For lower values of the random effect variance , the FAB intervals are significantly narrower due to the increased precision of the available indirect information. When a covariate is a strong predictor of the area mean, FAB intervals estimated under a linking model with a covariate were narrower than those without a covariate. Most importantly, no matter the linking model, FAB intervals were narrower on average than intervals based on direct estimates alone. The percentage decrease in interval length ranged from 0.4% to 13.2%.

| Linking Model | ||||||||

|---|---|---|---|---|---|---|---|---|

| Exchangeable | 0.868 | 0.901 | 0.995 | 0.996 | 0.938 | 0.976 | 0.996 | 0.996 |

| Covariate | 0.869 | 0.901 | 0.869 | 0.901 | 0.939 | 0.977 | 0.939 | 0.976 |

| Spatial | 0.868 | 0.877 | 0.996 | 0.996 | 0.939 | 0.939 | 0.996 | 0.996 |

| Full | 0.869 | 0.878 | 0.869 | 0.878 | 0.940 | 0.940 | 0.940 | 0.940 |

It is important to note that a given FAB interval is not guaranteed to be narrower than the corresponding direct interval. Rather, FAB intervals will be narrower on average than direct intervals. Table 2 details the percentage of areas with shorter FAB intervals than direct intervals by simulation.

| Linking Model | ||||||||

|---|---|---|---|---|---|---|---|---|

| Exchangeable | 96.7% | 91.9% | 81.3% | 81.5% | 86.8% | 83.6% | 81.7% | 81.9% |

| Covariate | 96.5% | 91.4% | 96.5% | 91.5% | 86.1% | 82.7% | 86.0% | 82.6% |

| Spatial | 96.6% | 95.5% | 79.2% | 79.4% | 85.9% | 88.4% | 79.6% | 80.2% |

| Full | 96.4% | 95.2% | 96.4% | 95.2% | 85.1% | 87.5% | 85.0% | 87.5% |

3.2 Comparison to Empirical Bayes

In addition to the direct interval and four FAB intervals, we also calculated empirical Bayes (EB) intervals based on the four linking models detailed above. Because empirical Bayes intervals are not constrained to have area-specific coverage, they are able to be narrower than FAB intervals, particularly when each area-level mean is well-predicted by the linking model (e.g., is small). However, as shown in Table 3, empirical Bayes and FAB intervals have increasingly similar average widths as increases.

| Type | Linking Model | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| EB | Exchangeable | 2.387 | 3.182 | 3.903 | 3.903 | 3.601 | 3.816 | 3.903 | 3.905 |

| EB | Covariate | 2.445 | 3.203 | 2.447 | 3.195 | 3.609 | 3.818 | 3.608 | 3.818 |

| EB | Spatial | 2.511 | 2.682 | 3.904 | 3.904 | 3.621 | 3.597 | 3.904 | 3.905 |

| EB | Full | 2.576 | 2.726 | 2.580 | 2.719 | 3.633 | 3.609 | 3.632 | 3.610 |

| FAB | Exchangeable | 3.402 | 3.530 | 3.902 | 3.902 | 3.679 | 3.826 | 3.903 | 3.905 |

| FAB | Covariate | 3.405 | 3.533 | 3.405 | 3.531 | 3.682 | 3.828 | 3.682 | 3.828 |

| FAB | Spatial | 3.403 | 3.440 | 3.903 | 3.903 | 3.682 | 3.681 | 3.904 | 3.905 |

| FAB | Full | 3.405 | 3.443 | 3.406 | 3.442 | 3.686 | 3.685 | 3.686 | 3.685 |

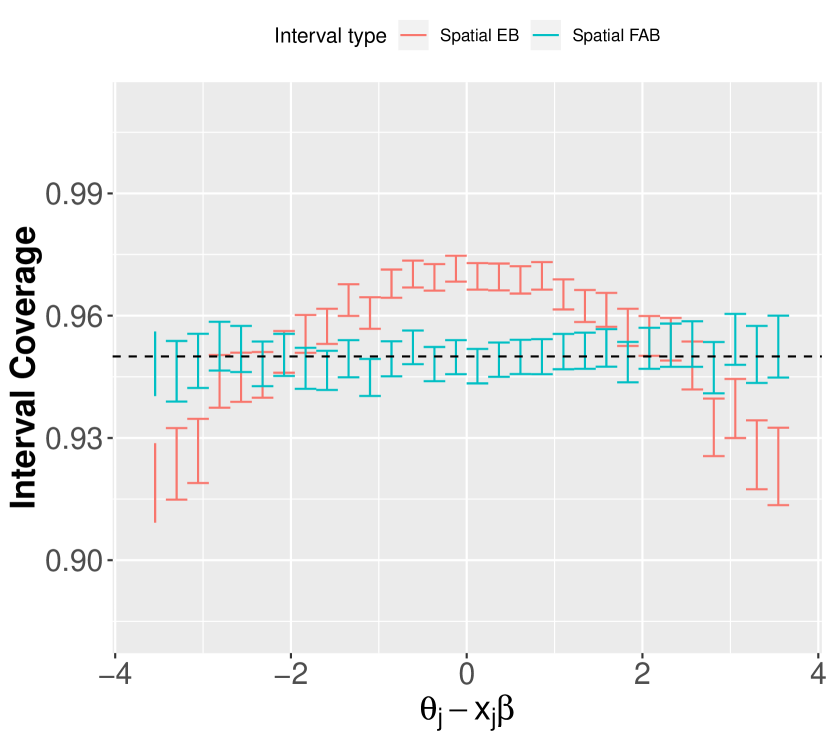

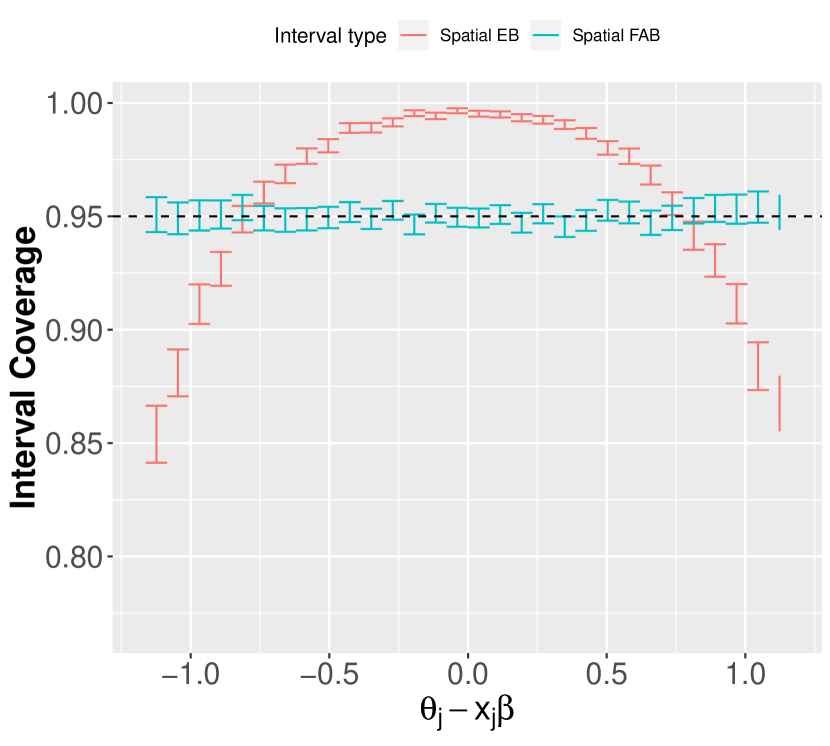

However, Table 3 does not tell the full story. Although the empirical Bayes confidence intervals approximately achieve coverage on average across areas, the actual coverage rate depends on the value of unknown target quantity . For values of that are close to their predicted means under the linking model, the EB interval has greater than coverage. For values much farther away, it has much less (Figure 3), since each EB interval is centered around a biased estimate of the target quantity. In fact, with the exception of two points, the frequentist coverage of the EB interval is unequal to for all values of . Unlike the EB interval, the FAB interval shares the property of constant coverage with the direct interval.

4 Empirical example: Household radon levels

Between 1987 and 1988, the U.S. Environmental Protection Agency collected household-level data on radon concentration as part of its State Residential Radon Survey (SRRS). The data consist of a stratified random sample of 12,777 homes, each located in one of 472 counties in nine different states. We examine a subset of the SRRS data, concentrating on four of the nine states in the study: Minnesota, Wisconsin, Michigan, and Indiana. These states are geographically close and demographically similar to one another, so patterns of radon concentration may be similar across this region. Within these four states, there are 3,767 household measurements, located in 209 distinct counties. One of the primary goals of the study was to “provide the best estimate and uncertainty quantification of a county’s true geometric mean of radon screening measurements” Price \BOthers. (\APACyear1996).

price1996 analyzed the subset of the SRRS data from the state of Minnesota, developing a linear mixed model to construct 95% Bayesian credible intervals for county-specific geometric mean radon levels. However, these intervals do not have 95% coverage at the county level. In particular, as outlined in Section 1, they will suffer from undercoverage for counties with exceptionally high or low true means. Such systematic undercoverage can be dangerous, because counties with extremely high radon levels present significant public health risks to their communities and need to be detected to necessitate appropriate policy action. As such, we should use interval procedures that maintain known, constant county-specific coverage rates.

Of the 209 counties in the data, 124 of them have fewer than ten sampled households, and 72 have fewer than five sampled households. For these counties, direct confidence intervals will be extremely wide, which can limit their usefulness in practice. However, the average precision of these intervals can be improved by using FAB intervals to borrow information across counties. In this section, we compare direct intervals to several FAB interval procedures corresponding to different linking models for the county-specific means.

Following \citeAprice1996, we make a small empirical adjustment to the radon concentration values to mitigate the impact of very low concentration measurements that arise as a byproduct of measurement error. In addition, we also follow the authors in assuming that adjusted radon concentrations within counties follow a roughly log-normal distribution, which appears warranted by exploratory data analysis. Letting be the log adjusted radon concentration measurement for household in county , we assume the within-county sampling model , where is the unknown true geometric mean radon concentration for county and is the unknown variance of log radon measurements in county . Under the assumption of random sampling within counties, the county sample mean is distributed as , where is the variance of the sample mean. We define , where is the sample standard deviation of log-radon measurements within county . is an unbiased and consistent estimate of .

We illustrate the use of FAB intervals for this small area analysis by considering several linking models for across-county heterogeneity, of which the most general is the spatial Fay-Herriot model. This model uses county-level surficial radium content (ppm), measured by the National Uranium Resource Evaluation (NURE), as an area-level predictor in a linear model. Under this model, are jointly normally distributed, with , where is the measured surficial radium content for area . is defined as in (12), where the proximity matrix represents the row-standardized squared exponential distance between county centroids (measured via longitude and latitude), since no counties in Minnesota and Wisconsin are first-order neighbors of counties in Michigan or Indiana. Explicitly,

| (16) |

where represents the distance between the centroids of county and county . The diagonal elements of are equal to zero.

We also consider three simplifications of this model, corresponding to assumptions that either the regression coefficient and/or the spatial autocorrelation . Let the matrix be an matrix consisting of a column of ones and the column vector and let . Specifically, the four linking models examined are

-

1.

full model: ;

-

2.

spatial model: ;

-

3.

covariate model: ;

-

4.

exchangeable model: .

Unlike in the simulation study, here we treat the county-level variance parameters as unknown, resulting in -intervals instead of -intervals. We model the sampling variance parameters as i.i.d. and estimate the hyperparameters and via marginal maximum likelihood. Details of this procedure are provided in the appendix. Given estimates and based on data from other areas, we obtain prior information that is used to construct the FAB -interval. For computational convenience, we obtain prior information for separately, using plug-in estimates when estimating . This procedure is analogous to that detailed in Section 2 and the appendix.

Because the county-level variances are unknown, we are able to construct confidence intervals with constant coverage for the 196 of the 209 counties with a sample size of at least two. For each of these counties, we construct FAB intervals for a specific county under the four linking models specified above via the following process:

-

1.

Estimate linking model parameters using data from all counties other than .

-

2.

Obtain prior distributions for both and using plug-in estimates from the fitted linking model. This yields a normal distribution for and an inverse-gamma distribution for .

-

3.

Obtain the optimal -function for county given prior information about and (obtained using data not from ), as described in Section 2.3.

-

4.

Construct the FAB -interval .

where the quantiles correspond to a those from a -distribution with degrees of freedom.

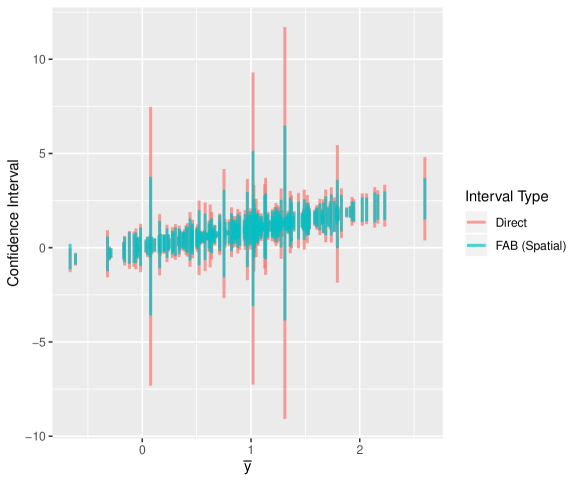

As visualized in Figure 4 and depicted numerically in Table 4, FAB intervals under each of the four linking models are significantly narrower than the direct interval, representing a 23-26% improvement in average interval width. Incorporating a spatial linking model significantly reduces interval width, and including covariate information does not appear to have much of an impact on average interval width. Although a specific FAB interval is not guaranteed to be narrower than the corresponding direct interval, the vast majority of the FAB intervals represented improvements. The proportion of counties with narrower FAB intervals varied from 89 to 96 percent of the counties, depending on the quality of the chosen linking model.

| Type | Linking Model | Mean Width | Relative Width | % Intervals Improved |

|---|---|---|---|---|

| Direct | - | 1.701 | 1.000 | - |

| FAB | Exchangeable | 1.312 | 0.771 | 89.8% |

| FAB | Covariate | 1.312 | 0.771 | 88.8% |

| FAB | Spatial | 1.257 | 0.739 | 96.4% |

| FAB | Full | 1.256 | 0.739 | 95.5% |

In general, EB confidence intervals for county-specific radon levels are narrower than those constructed via the FAB procedure, although this is not always the case. Under the full linking model, the empirical Bayes interval is narrower than the corresponding FAB interval for 128 out of the 196 counties. The differences are most pronounced in the counties for which the combination of small sample size and high sampling variance is present. Regardless, EB intervals lack county-specific coverage, which limits their use in making county-specific inferences.

5 Discussion

In the field of small area analysis, researchers typically use confidence interval procedures that either have constant coverage across areas but do not share information, or utilize shared information but lack constant coverage. Although the empirical Bayes procedures commonly used in the literature have coverage on average across groups, the actual coverage rate may differ substantially for some values of , calling into question the resulting area-specific inferences. The FAB procedures developed by \citeAyuhoff16 and outlined in this article have constant coverage for each area regardless of what the true area-level means are, and are valid for all linear mixed models with normal sampling variances. This class of models is very flexible, enabling researchers accommodate auxiliary covariates, as well as spatial and temporal autocorrelation.

Importantly, although the empirical Bayes confidence interval procedure is guaranteed to have asymptotic marginal coverage on average if and only if the linking model is true, the FAB procedure will always have constant coverage, regardless of the chosen linking model. This is not to say that the linking model is unimportant; a properly specified linking model can substantially reduce expected FAB interval width, as evidenced by the simulation study and empirical example.

FAB intervals are somewhat more computationally demanding to calculate than direct confidence intervals or empirical Bayes intervals since model estimations must occur to obtain confidence intervals for areas. This can be burdensome under complex linking models, such as the spatial Fay-Herriot model, when the number of areas is large. Since FAB intervals will always have constant coverage, regardless of whether the linking model or the estimation procedure is correct, computational shortcuts can be taken to significantly reduce the burden, if necessary. For example, when the number of areas is large, one possibility is to separate the areas into heterogeneous clusters and construct prior distributions for areas belonging to a given cluster based the direct estimates from other clusters. This means that only models must be estimated, instead of , resulting in computational gains. When the number of areas is prohibitively large, we recommend simply estimating the hyperparameters of the linking model once and then using those estimates to calculate all FAB intervals. Although this will violate the condition of independence necessary to guarantee area-specific coverage, the influence of a single area on model estimates is likely to be small in such a context, so the FAB intervals will have very close to coverage for all areas.

One area of future work is to extend the FAB procedure to generalized linear mixed models by constructing FAB intervals for target quantities when responses are discrete or categorical. This has significant applications in the small area estimation literature for applications such as disease mapping, where researchers are often interested in inferring area-level relative risks.

The FAB procedure for constructing confidence intervals with area-specific coverage can be implemented using a variety of software packages for estimating small area estimation models, such as sae Molina \BBA Marhuenda (\APACyear2015) or lme4 Bates \BOthers. (\APACyear2015). The only additional computational functionality needed is the Bayes optimal -function, which we have implemented in R and made available in the fabCI R package on CRAN. Replication code for the paper is provided at https://github.com/burrisk/fabci.

Appendix A Credible interval coverage rates for the Fay Herriot model

Under the sampling model and prior , the posterior distribution

.

Accordingly, the symmetric credible interval can be expressed as

For a given value of , the coverage probability is

where is the standard normal cumulative distribution function.

Appendix B ML estimation of spatial Fay-Herriot hyperparameters

To estimate the hyperparameters based on data from a subset of areas , where , we recommend using either ML or REML procedures based on the data from all areas in . We provide the details for ML estimation below, although REML estimation is straightforward, using transformed data , where is a matrix that is orthogonal to . For more details about REML estimation for the spatial Fay-Herriot model, see \citeApratesisalvati08. Both ML and REML estimation of the spatial Fay-Herriot model are implemented in the sae R package and we also provide an implementation in the replication code.

Defining the marginal variance , where , the log-likelihood function is given by

The MLE of is of a familiar form, with

The partial derivatives with respect to and are given by , where

where . We can then use these to calculate the Fisher information matrix, which is the matrix of expected second derivatives of .

where . From this, we can solve for the maximum likelihood estimates of and by Fisher’s scoring.

where is the matrix of first partial derivatives with respect to and . Since and are constrained to lie in the intervals and , we reduce the step size if the proposed Fisher scoring step violates one or more constraints. The algorithm iterates until convergence.

To obtain estimates of the subset of area means , we find their conditional means given , , and under the sampling and linking model. These can be expressed as

Appendix C ML Estimation of sampling variance hyperparameters

Suppose that the sampling model for the unbiased direct estimates of the area-specific sampling variances is

where is an unbiased and consistent estimate of the sampling variance , based on a sample of observations. We model the variances of log-radon levels hierarchically, under the assumption that

For each area , we are interested in estimating and via maximum likelihood, based on data from a subset of areas , where . Then the log-likelihood is

where , is the cardinality of and is the Gamma function.

The partial derivatives of the log-likelihood with respect to and are

where is the digamma function, the derivative of the log-gamma function. In Section 4, we use the L-BFGS optimization algorithm with the box constraint to find and , the maximum likelihood estimates of and . Due to the low dimensionality of the problem, second order information can be utilized to speed up convergence, and the second order partial derivatives are

where is the trigamma function. An optimization algorithm that uses first-order information about and is implemented in the replication code.

References

- Banerjee \BOthers. (\APACyear2014) \APACinsertmetastargelfandspatialbook{APACrefauthors}Banerjee, S., Carlin, B.\BCBL \BBA Gelfand, A. \APACrefYear2014. \APACrefbtitleHierarchical Modeling and Analysis for Spatial Data Hierarchical modeling and analysis for spatial data. \APACaddressPublisherCRC Press. \PrintBackRefs\CurrentBib

- Bates \BOthers. (\APACyear2015) \APACinsertmetastarlme4package{APACrefauthors}Bates, D., Mächler, M., Bolker, B.\BCBL \BBA Walker, S. \APACrefYearMonthDay2015. \BBOQ\APACrefatitleFitting Linear Mixed-Effects Models Using lme4 Fitting linear mixed-effects models using lme4.\BBCQ \APACjournalVolNumPagesJournal of Statistical Software6711–48. {APACrefDOI} \doi10.18637/jss.v067.i01 \PrintBackRefs\CurrentBib

- Brewer \BBA Nolan (\APACyear2007) \APACinsertmetastarbrewer07{APACrefauthors}Brewer, M\BPBIJ.\BCBT \BBA Nolan, A\BPBIJ. \APACrefYearMonthDay2007. \BBOQ\APACrefatitleVariable smoothing in Bayesian intrinsic autoregressions Variable smoothing in Bayesian intrinsic autoregressions.\BBCQ \APACjournalVolNumPagesEnvironmetrics188841–857. \PrintBackRefs\CurrentBib

- Cochran (\APACyear1977) \APACinsertmetastarCochran77{APACrefauthors}Cochran, W\BPBIG. \APACrefYear1977. \APACrefbtitleSampling Techniques, 3rd Edition. Sampling techniques, 3rd edition. \APACaddressPublisherJohn Wiley and Sons, Inc,. \PrintBackRefs\CurrentBib

- Fay \BBA Herriot (\APACyear1979) \APACinsertmetastarfayherriot{APACrefauthors}Fay, R.\BCBT \BBA Herriot, R. \APACrefYearMonthDay1979. \BBOQ\APACrefatitleEstimates of income for small places: An application of James-Stein procedures to census data Estimates of income for small places: An application of James-Stein procedures to census data.\BBCQ \APACjournalVolNumPagesJ. Amer. Statist. Assoc.74269-277. \PrintBackRefs\CurrentBib

- Ghosh \BOthers. (\APACyear1999) \APACinsertmetastarghosh99{APACrefauthors}Ghosh, M., Natarajan, K., Walter, L.\BCBL \BBA Kim, D. \APACrefYearMonthDay1999. \BBOQ\APACrefatitleHierarchical Bayes GLMs for the analysis of spatial data: An application to disease mapping Hierarchical Bayes GLMs for the analysis of spatial data: An application to disease mapping.\BBCQ \APACjournalVolNumPagesJournal of Statistical Planning and Inference75305-318. \PrintBackRefs\CurrentBib

- Maples (\APACyear2017) \APACinsertmetastarmaples17{APACrefauthors}Maples, J\BPBIJ. \APACrefYearMonthDay2017. \BBOQ\APACrefatitleImproving small area estimates of disability: combining the American Community Survey with the Survey of Income and Program Participation Improving small area estimates of disability: combining the American Community Survey with the Survey of Income and Program Participation.\BBCQ \APACjournalVolNumPagesJournal of the Royal Statistical Society: Series A (Statistics in Society)18041211-1227. \PrintBackRefs\CurrentBib

- Molina \BBA Marhuenda (\APACyear2015) \APACinsertmetastarsaepackage{APACrefauthors}Molina, I.\BCBT \BBA Marhuenda, Y. \APACrefYearMonthDay2015jun. \BBOQ\APACrefatitlesae: An R Package for Small Area Estimation sae: An R package for small area estimation.\BBCQ \APACjournalVolNumPagesThe R Journal7181–98. {APACrefURL} \urlhttps://journal.r-project.org/archive/2015/RJ-2015-007/RJ-2015-007.pdf \PrintBackRefs\CurrentBib

- Pfeffermann (\APACyear2013) \APACinsertmetastarpfeffermann{APACrefauthors}Pfeffermann, D. \APACrefYearMonthDay2013. \BBOQ\APACrefatitleNew important developments in small area estimation New important developments in small area estimation.\BBCQ \APACjournalVolNumPagesStatistical Science28140-68. \PrintBackRefs\CurrentBib

- Pratesi \BBA Salvati (\APACyear2008) \APACinsertmetastarpratesisalvati08{APACrefauthors}Pratesi, M.\BCBT \BBA Salvati, N. \APACrefYearMonthDay2008. \BBOQ\APACrefatitleSmall area estimation: the EBLUP estimator based on spatially correlated random area effects Small area estimation: the EBLUP estimator based on spatially correlated random area effects.\BBCQ \APACjournalVolNumPagesStatistical Methods and Applications171113–141. \PrintBackRefs\CurrentBib

- Pratt (\APACyear1963) \APACinsertmetastarpratt63{APACrefauthors}Pratt, J\BPBIW. \APACrefYearMonthDay1963. \BBOQ\APACrefatitleShorter Confidence Intervals for the Mean of a Normal Distribution with Known Variance Shorter confidence intervals for the mean of a normal distribution with known variance.\BBCQ \APACjournalVolNumPagesAnn. Math. Statist.342574–586. \PrintBackRefs\CurrentBib

- Price \BOthers. (\APACyear1996) \APACinsertmetastarprice1996{APACrefauthors}Price, P., Nero, A.\BCBL \BBA Gelman, A. \APACrefYearMonthDay1996. \BBOQ\APACrefatitleBayesian prediction of mean indoor radon concentrations for Minnesota counties Bayesian prediction of mean indoor radon concentrations for Minnesota counties.\BBCQ \APACjournalVolNumPagesHealth Physics716922-936. \PrintBackRefs\CurrentBib

- Rao \BBA Molina (\APACyear2015) \APACinsertmetastarrao15{APACrefauthors}Rao, J\BPBIN\BPBIK.\BCBT \BBA Molina, I. \APACrefYear2015. \APACrefbtitleSmall Area Estimation Small area estimation. \APACaddressPublisherJohn Wiley and Sons, Inc. \PrintBackRefs\CurrentBib

- Singh \BOthers. (\APACyear2005) \APACinsertmetastarsingh05{APACrefauthors}Singh, B., Shukla, G.\BCBL \BBA Kundu, D. \APACrefYearMonthDay2005. \BBOQ\APACrefatitleSpatio-temporal models in small-area estimation Spatio-temporal models in small-area estimation.\BBCQ \APACjournalVolNumPagesSurvey Methodology312183–195. \PrintBackRefs\CurrentBib

- Wall (\APACyear2004) \APACinsertmetastarwall04{APACrefauthors}Wall, M\BPBIM. \APACrefYearMonthDay2004. \BBOQ\APACrefatitleA close look at the spatial structure implied by the CAR and SAR models A close look at the spatial structure implied by the CAR and SAR models.\BBCQ \APACjournalVolNumPagesJournal of Statistical Planning and Inference1212311 - 324. \PrintBackRefs\CurrentBib

- You \BBA Chapman (\APACyear2006) \APACinsertmetastaryouchapman06{APACrefauthors}You, Y.\BCBT \BBA Chapman, B. \APACrefYearMonthDay2006. \BBOQ\APACrefatitleSmall area estimation using area level models and estimated sampling variances Small area estimation using area level models and estimated sampling variances.\BBCQ \APACjournalVolNumPagesSurvey Methodology3297-103. \PrintBackRefs\CurrentBib

- Yu \BBA Hoff (\APACyear2016) \APACinsertmetastaryuhoff16{APACrefauthors}Yu, C.\BCBT \BBA Hoff, P\BPBID. \APACrefYearMonthDay2016. \BBOQ\APACrefatitleAdaptive multigroup confidence intervals with constant coverage Adaptive multigroup confidence intervals with constant coverage.\BBCQ \APACjournalVolNumPagesBiometrika1052319-335. \PrintBackRefs\CurrentBib