Exact Solutions for a GBM-type Stochastic Volatility Model having

a Stationary Distribution

Alan L. Lewis111Newport Beach, California, USA; email: alewis@financepress.com

Abstract

We find various exact solutions for a new stochastic volatility (SV) model: the

transition probability density, European-style option values, and (when it

exists) the martingale defect. This may represent the first example of

an SV model combining exact solutions, GBM-type volatility noise,

and a stationary volatility density.

1 Introduction

We develop the following stochastic volatility (SV) model for the real-world (P-measure) evolution of a financial asset , such as a broad-based stock index:

(4)

Here are correlated Brownian motions with correlation . Also

are constant parameters of the model, meant to be estimated from financial time series. We generally assume throughout that (,

although we sometimes admit or even .

We also develop

a risk-neutral (Q-measure) version of the model, which is used for option valuation.

In that one, becomes a cost-of-carry: , where is an interest rate and is a dividend yield. In addition,

, and

, (a possibly different parameter) while the other parameters

remain identical to their P-measure values.

An attractive feature of the model is that the stochastic volatility is driven by a geometric Brownian motion (GBM)-type noise. GBM volatility seems to be favored by time series analysis over the “square-root” variance noise of popular affine-type diffusion models, such as

the Heston ’93 model.222See, for example [2] and [10]. Extended with the drifts shown, I call it the ‘Extended GBM’ model, or XGBM for short.

As we show, the model admits an exact solution for the transition density, vanilla option values,

and some other quantities of interest. In these solutions, we find two qualitatively

different regimes:

•

Case 1: ,

•

Case 2: .

In Case 1, the driving volatility process is mean-reverting and has a stationary density.

In Case 2, with probability 1, as grows large , similar to the

SABR model. Indeed, the lognormal SABR model is a special case of (4)

when the drifts are absent.

However, a weakness of the SABR model is its lack of

a stationary density for the volatility. Thus (under Case 1), we have here what may represent the first example of an SV model combining: GBM-type volatility noise, a stationary volatility density, and exact solutions.

Numerically, we find option values (and

thus implied volatilities) continuous vs. , including at the

borderlines case: .

In brief, the problem is solvable because it is reducible to the evolution problem for a 1D

diffusion operator admitting a spectral expansions in terms of confluent hypergeometric functions and . The other special function that will appear frequently is

the Gauss hypergeometric function. The etc are Pochhammer symbols. All these functions are

built-in in Mathematica, where everything is implemented.

Structurally, the model is similar to the one-factor short-term

interest rate model, ,

originally due to Merton and which I fully solved in [4] (reprinted in [6]).

The solvability of Merton’s model suggests, but does not prove, that associated 2D

SV models such as (4) are also solvable. Another suggestion that my XGBM SV model

might be solvable is the discussion found in [3] (Sec. 9.5).

As it turns out, moving from the interest rate model to the associated stochastic volatility model is

tricky. One reason is the “reduced” PDE coefficients become complex-valued,

which complicates the associated spectral expansion. Another reason is that

the “fundamental transform” needed for option valuation (using the language of [5]) requires a regularization for Case 2. All that is explained below; key formulas are boxed.

We seek the bivariate transition probability density defined by . The initial condition is , using the Dirac delta. All parameters are real; assume . Using subscripts for derivatives, the corresponding Kolmogorov backward PDE problem is

(11)

The system (8) is a MAP (Markov Additive Process), where is the additive component and is the Markov component. This is also seen in the -independence in the coefficients of (11). The MAP property implies

which in turn implies the existence of a Fourier representation:

(12)

for a characteristic function to be determined below.

In the Heston ’93 model (also a MAP), is found in terms of Bessel functions. Here the situation is not quite so simple: we’ll find that itself requires an integration using confluent hypergeometric functions and . The additional integration means that numerical evaluations of the

exact formulas will take an order of magnitude more computer time than Heston. Pure numerics, such as a PDE approach, will be similar in the two models.

2.1 Reduction to an auxiliary problem for

Because of the MAP property it suffices to solve (11) with . Let , suppressing the display of the dependence. Applying to both sides of (11) and using parts integrations (the boundary terms vanish) yields:

(15)

Letting , where yields

(18)

The superscripts on and distinguish them from similar

expressions introduced later where the sign of is flipped from the convention here.

The mnemonic is that indicates that occurs as , so the sign is minus.

That is, . The

sign on refers to the risk-neutral case where ; i.e.,

.

As we see, starting from real , and regardless of the

superscripts, the reduced problems have real

, while . If the Fourier inversion is

performed along the real -axis, and of course is real, we also have

and . In terms of , (12) reads:

(19)

We call the (auxiliary model) Green function, although we may also refer to its Laplace

transform as a Green function.

2.2 Spectral expansion for (overview)

Suppressing the -dependence, has a Laplace transform with respect to ,

call it , where is the transform variable. When we

invert the transform via a Bromwich contour in the complex -plane, we’ll

discover various singularities which are associated to the spectrum.

See Fig. 1 for a typical case.

The simplest situation has real parameters, .

Then, we’ll find that has

1.

A branch cut singularity at .

2.

A set of poles (or sometimes an empty set) at . These poles are

are a finite set of non-positive reals, lying in .

The net result of the Laplace inversion is a spectral expansion of the form:

(20)

The specifics are given in Sec. 2.3 and developed in detail in Appendix A..

The poles generate the discrete spectrum and the discrete sum term in (20).

Here denotes a “pole condition”, which is a criterion on the parameters for the

discrete contribution to appear at all. This term may be absent.

The branch cut singularity marks the right edge of the

-plane interval , which is the continuous spectrum, leading to the integral term in (20). This term is always present.

As we saw in Sec. 2.1, for XGBM we need ,

but , complex functions of the Fourier parameter .

In that case, the general form (20) still holds, but the structure of the spectrum is altered.

A continuous spectrum remains along . However, the poles generally leave the

real -axis, as illustrated in Fig. 1.

The figure illustrates two poles, shown as the ‘crossed-circles’.

Indeed, since (complex) varies continuously under a Fourier inversion, we have pole trajectories . Examples are shown in Fig. 2 for a case with (initially) three poles. The illustrated trajectories start in the real interval as in the real parameter case, then

leave the real -axis, and finally return to touch the branch cut – at which point they leave the

discrete spectrum. In turn, this leads to other complications which

are seen in Fig. 3 and discussed later. Overall, the complex parameter case

is, well, complex!

2.3 Spectral expansion for (result)

As shown, the transition density we seek is found in terms of a Green function for an auxiliary 1D PDE with (two) complex coefficients. Simplifying the notation,

the reduced problem (18) reads:

(23)

As before, real , while with .

Solving (23) is the key to the XGBM model. From that solution, all the other results in this article follow. I find:

Theorem 1(auxiliary Green function).

Let denote the greatest integer in ,

is the Pochhammer symbol, and the further notations

Assume real , while with

. Then, the spectral representation solution to PDE problem 23 is given by

(24)

where

and

Proof: In outline, we construct the solution by Laplace transform of (23) with respect to . This leads to an ODE reducible to Kummer’s differential equation, with Laplace transform parameter

. The ODE solution

is constructed; we perform the Laplace inversion by a Bromwich contour, which yields a first solution for . Finally the spectral representation (24), which is a second solution

for , is found by applying the Residue Theorem to the Bromwich inversion. Details are found in Appendix A.

2.4 Summary for the transition density

To summarize at this point, the transition density for the P-model XGBM system (8) is given by

This is the stationary density for the (standardized) stand-alone volatility process; i.e., when . When , then (24) still holds without a stationary limit. In that case, the particle mass eventually accumulates arbitrarily close to .

For general , (26) holds with

(27)

2.5.2 The norm-preserving case: .

Suppose in (23) are real and . With no killing, the Green function should be norm-preserving on : .

Let’s check that for the sub-case .

With and , then . Then, using the stationary

density from (26), Theorem 1 reads:

(28)

where

and

now with

We are also using the convention that if .

Recall we suppose , so the stationary density exists. Since , the

remaining terms must have a zero -integral. Indeed this is true because,

which follows from taking the parameters and in the integral (52) below, and

Here (ii) follows from the relation

(29)

which we found from Mathematica, where is arbitrary real,

and then specializing to . ∎

Remarks for the sub-case: . Norm preservation for this

sub-case is best shown with the fundamental transform developed later in Sec. 5.

With that, the property amounts to showing that . But, referring to

(58), it is easy to see that and then

is immediate from (56)-(57).

2.5.3 The SABR model limit: no drifts

Drop the drifts

in (4) and you have the (lognormal) SABR model. Then (24)

yields previously

known SABR results. Details are found in Appendix B.

3 Risk-neutral evolution

Given a P-measure diffusion, to avoid arbitrage opportunities, options must be valued under an equivalent Q-measure diffusion. The usual short-hand trick to finding it are Girsanov substitutions: and

in (4). Here are Q-Brownian motions and are, respectively, market prices of equity and volatility risk.

We assume a world with a constant “cost-of-carry” , where

is a short-term interest rate, and is a constant dividend yield thrown off by the asset.

Then, given our

parametrization in (4), the absence of arbitrage requires

In principle, any functional choice that preserves the inaccessibility of

all the spatial boundaries will bring closure to the model and satisfy the “no-arbitrage” principle: P-Q equivalence

as measures. In practice, one wants to preserve ‘closed formness’. Indeed, a convention in financial modelling (although not required by the general theory) is to

arrange both the P and Q evolutions to have similar parameterizations. This allows a successful

solution method for one to work for the other. In this spirit, our

simple choice here takes a constant. With that,

(33)

where , and now (4) and (33) together complete the model.

To simplify the notations, let us agree that all the evolutions and Brownian motions in this section are ‘under Q’. Then we have, equivalently, the Q-model:

(37)

3.1 The issue of martingality

The XGBM model nests the lognormal SABR model as a special case: see

(105) in Appendix B. Recall that, under the lognormal SABR

model, the stock price process can suffer ‘loss of martingality’ due to the

correlation parameter . Specifically, is: (i) a true

martingale when , and (ii) a strictly local martingale when

. Since every local martingale that is bounded from below is a

supermartingale: (when .

Indeed, when ,

I calculate explicitly in [6] the martingale defect. For the full XGBM

model, correspondingly: when is the discounted stock price process

a true martingale? Equivalently, fixing a forward settlement date , when is the forward price process a true martingale? Suppressing , the evolution for that is:

(41)

A prescription for answering this question is given in [5],[6]

for the general stochastic volatility evolution

.

To determine if this process is martingale-preserving (for the forward),

introduce the auxiliary volatility process :

Then, the forward suffers a loss of martingality if and only if the auxiliary process can

‘explode’; i.e., reach in finite time with strictly positive probability. From

(41), for the case under consideration,

Then, by applying the Feller explosion criteria (details in [5]), one

can establish that can explode if and only if ; i.e.,

.

Even better, when , one can find the martingale defect by,

equivalently, finding the absorption-at-zero probability for the inverse process

. From Itô,

(42)

With the first time the -process hits zero, is defined by

Then, the martingale defect is given by

, with an explicit formula found

in Appendix C.

In summary, the XGBM model, parametrized at (33)

suffers a loss of martingality for the forward only when is found in the interval

.

For (broad-based) equity applications, the condition is typically harmless:

one will usually estimate both (negative option ‘skews’) and (volatility

has a stationary density). But for other applications (possibly with

positive option skews or negative ’s), it is an issue to keep in mind.

4 Option valuation – Case 1:

Let denote the XGBM transition density under the Q-evolution. From (25),

with , , and taking dummy , we have

(43)

(44)

Here is again given at (24). Let denote

the time-0 value of a Euro-style option with time- bounded payoff function .

Then, since is the time-0 discounted expected value of the payoff under the

-evolution, we have generally

(45)

While (45) offers a quasi-analytic solution, it has an embarrassing number of

integrations: 4(!), counting the integration for itself. We’ll eliminate two.

Proceeding formally, suppose it’s legitimate to do the

integral in (45) first. Then, if the following integral

exists, define a fundamental transform

(46)

where is an analyticity strip for in the complex -plane.

Note that we are now generalizing (45) by moving the -integration off

the real -axis.

For options, our preferred strip for Fourier inversions is: . It can be shown that

our preferred strip is contained within for XGBM because the model is

(i)norm-preserving and (ii) martingale-preserving

(under the mild restriction .333To

show that (i) and (ii) lead to analyticity in the preferred strip, see Th. 4.7

in [6].

We will show below that the question mark in front of (46) can

be removed for Case 1.

Next, in a familiar argument, define the (generalized) payoff transform

(47)

with located in some other analyticity strip . We can always

find a nice payoff such that these two horizontal strips intersect: .

Finally, by the arguments in my article “A Simple Option Formula for General Jump-diffusion and other Exponential Lévy Processes” (reprinted in [6]), (45) becomes

(48)

In other words, is a point in the -plane marking the intersection of a horizontal integration contour in with the imaginary -axis. Again, we can arrange things

so that we are working in the preferred strip: . Reported numerics are found from versions of (48).

For example, with , with strike price , and

, all reported put option values are computed from:

(49)

Removing the question mark in (46). Recall that the SABR model is a special

case of the XGBM model, with the transition density given at (110) in Appendix B.

It turn out that, for the SABR model, the integral in (46) does not exist.

This problem was discussed in [6] (Sec. 8.13, pg. 407), but we will recap briefly

here. For SABR, the existence of (46) amounts to integrating (110) from

Appendix B with respect to

, at fixed . Extracting the few terms in (110)

with dependence yields the integral

which does not exist because the integrand is not integrable

as .444, as , where depend upon but not .

Now, for the SABR limit, there is no discrete spectral contribution to

in (24). The lesson from SABR is that, in the general XGBM case, problems may lie with

integrating the continuous spectrum term. Indeed, extracting all the dependencies

from the continuous spectrum term in (24), the corresponding XGBM integral is

Now, first consider the integrand as . As ,

, where are bounded constants independent of .

Since ,

much like the SABR case with Bessel functions discussed in footnote 4. The

exponential in harmless at small , so we see the crux of the

matter is the term , which is integrable

iff555Integrability is clear when . The

borderline case is not as immediate, but (52) below

shows that (*) also exists when as long as .

(50)

When the integrability condition holds, so does (46).

Recall we have seen this condition before at (26) in the P-model: there

needed for the existence of a stationary limit of the stand-alone volatility process. In

most financial applications (with calibrated parameters), the integrability condition will be satisfied.

Thus, to borrow a characterization from physics, Case 1 is the “physical case”. Case 2 is the

“unphysical case” (including SABR). Case 2 is, of course, still mathematically well-defined.

What about ? Since

this term will have positive real part in the preferred -plane strip. As the

remaining integrand terms in (*) have power law behavior as , the

net effect is exponential decay in at large , so all is well in that limit.

To summarize at this point, we have the following situation.

In the risk-neutral model, when the integrability condition (50) holds,

option values are given by (48), with given by (46). If the integrability condition does not hold

(Case 2), option values are still given by (48),

but is not

given by (46). Instead, that integral needs to be regularized:

see Sec. 5 for details. In this section, we now continue, assuming

(50) holds.

Option valuation – continued.

To perform the integration in (*), use a formula from

Slater ([9], (3.2.51)-(3.2.52)):

(51)

Here is

the Gauss hypergeometric function. Note that the two conditions on above

can overlap, allowing both integral relations to

be true at the same time.

Applying (51) to our problem (*) above yields:

(52)

(53)

Note denotes the

complex conjugate of (since is real). The integration

conditions and from Slater reduce to: .

(Recall in fact is OK for Case 1 as long as ).

The -value restrictions can be checked along any putative

-plane integration contour; I have found the formulas suffice for all

the test examples of Sec. 7.

The discrete term integration.

From (24) and (46), the discrete term in the spectral expansion requires

where and is given at (52).

The integral (**) can be performed using another formula from Slater, (3.2.16):

(54)

Note that, since is an integer for our application, is a terminating polynomial of . Thus,

Remarks. Note that the last Slater integral (54) requires

, which translates to . It can be seen that this condition is

automatically satisfied here as follows. First, is equivalent to

. But, if contributes to the discrete spectrum, then

(see Appendix A or the sum cutoff

in (55). When this last inequality is

satisfied, the l.h.s. will be positive. And certainly if with

positive but otherwise arbitrary, then .

4.1 Frequently used notations under risk-neutrality

Here we collect in one place notation we have introduced and will

frequently refer to subsequently.

Note that here and throughout, we frequently suppress -dependencies to ease notations,

as we have done with .

4.2 Summary: fundamental transform for Case 1

Putting it all together, for , we have the spectral representation:

(55)

with other notations in Sec. 4.1. Again, some -dependencies are suppressed.

5 Option valuation – Case 2:

To handle this case, we’ll adapt the method I used for the SABR model in [6].

Consider , a putative time-independent solution to the PDE

in the top line of (23). Suppose

as and decays at large . Note an initial condition plays no role in this time-independent

problem. (With and ,

we write this solution as ). With that putative solution, the

fundamental transform can be constructed as

(56)

Here a regularized fundamental transform is defined by

(57)

Let’s review why this works. First, both terms on the r.h.s. of (56)

manifestly satisfy the PDE associated to the fundamental transform – the top line of (23) again. Second, as , because satisfies a Dirac mass initial

condition, we have . Thus, , which is the correct initial condition for the fundamental transform. Third, the integral in (57)

exists because as , so the problematic integrand in (*)

is tamed by this new behavior. Finally, correctly decays at large because both terms on the r.h.s. of (56) do.

Using the notations in Sec. 4.1 and the confluent hypergeometric , I find

(58)

which has the advertised -behaviors.

Now recall

(59)

Since has a Taylor expansion about , this implicitly defines coefficients such that

I find (again using the Gauss hypergeometric function ) that

Note that, since , the first sum of is and the second sum is

; since , the net effect is , as promised.

The term-by-term integrals that are now needed in (57) can be done

by the previously given formulas from Slater. The net result is that the previously introduced (for Case 1) generalizes to where

In addition, we need to introduce the new function where

These functions use the new notations:

From these, form

(60)

and obtain finally, for Case 2,

(61)

Don’t forget that – both here and in (55).

Equation (61) is the Case 2 replacement for (55); option values

are computed from this new using the previous (48) and (49).

6 Small and large time asymptotics

By ‘time’, we refer to the time-to-option-expiration .

6.1 Small

For small , option prices at strike tend to their parity

values, and the implied volatility smile, , tends

to a non-trivial limit.

Indeed, it is well-known that the limiting asymptotic smile in general SV models

does not depend upon the diffusion drifts; it is solely determined

by the variance-covariance system. In our case, that system is (105), which is the (lognormal) SABR model.

The asymptotic smile formula for that one is well-known. The version I like is666I am copying in (62) from eq. (12.33) in [6] (Ch. 12). It is easily shown to be equivalent

to other SABR model sources. For example, to show it is equivalent to (8.32) in [8], identify my with in Paulot and apply some

routine algebra.

(62)

6.2 Large

The large option behavior is determined from the large behavior

of the fundamental transform .

Case 1: . In this case, following the method in [5] (Ch. 6),

one looks for the behavior (as grows large) in the spectral expansion (55). When there is a discrete

component in that expansion, then is the principal eigenvalue.

When there is only a continuous spectrum, but still real , a better nomenclature

for (borrowing from physics) might be be ‘mass gap’. In any event, we define by

Tentatively, assume the parameters are such that there is indeed a discrete spectrum,

and identify from the leading term of that. Using the notation

associated to (55), one has

Then, the prescription in the cited reference is to look for a saddle point

in the complex -plane along the purely imaginary axis (so is real).

The saddle point is a solution to , where the prime indicates

the -derivative. Having found that, the asymptotic

option implied volatility is given by the very simple relation

(63)

With , it’s easy to find

(64)

Notice that we work in the “martingale-preserving” regime (recall Sec. 3.1),

where . Since we assume throughout that ,

in that regime and , which is the preferred (and

guaranteed) analyticity strip for . Thus, we have found that when is such that a

discrete spectrum exists, then

where is given by (64). But, what is the criterion for

a discrete spectrum to exist? From (55), and since is real,

a discrete spectrum exists when

Now, since we are discussing Case 1, which has , the remaining

sub-case to be addressed here is . Since there

is no discrete spectrum, only the continuous spectrum

term contributes. One reads off from (55) that

with some whose specific form doesn’t matter for our purpose.

Let’s introduce the notation , which

marks the critical value of such that a discrete spectrum emerges.

To summarize, we’ve found under Case 1 (and the martingale-preserving regime) that

the principal eigenvalue/mass gap is:

(67)

Smoothness. Notice that Thus

which shows that of (67)

is continuous at . By differentiating, it is

easy to see that is

also continuous at . In other

words is smooth, in the sense

of being continuously differentiable, throughout the Case 1 regime:

.

Examples.

With and , then ,

, and . Or,

with and , then

, and . This is how the

entries in Table 1 were found.

Case 2.

For simplicity, suppose no cost-of-carry parameters, so

. As gets large under Case 2 the fundamental transform does not decay,

but instead has a non-trivial, but relatively simply limit:

. From (49):

(68)

Here the contour is defined by , and .

Note that is not a new function in our development; indeed, , where the r.h.s. was found previously at (58). Hence,

(69)

and recall Sec. 4.1 for other notations.777The

case most easily follows by seeking a

stationary solution to the top line of (23)

with . One easily find . Alternatively,

it can be checked by proving .

Numerical examples using (68-69) are found in the entry in Table 2. A similar discussion for the SABR model

is found in [6] (Sec. 8.12.1).

7 Numerical examples for option prices

Formulas are implemented in Mathematica; prices use (49).

All required special functions are built in.

We have a double integration. Additional complications that must be handled are now discussed.

Implementation notes: Case 1.

For the ‘physical’ Case 1 (), we have a double integration using confluent

hypergeometric functions with complex arguments. Results are not immediate.

For example, with my choices for cutoffs and Precision parameters, option prices are found in 0.5-2 minutes on my desktop

machine.

The main complication in this case is that, prior to the Fourier integration over , one must identify

the transition points (if any: see Appendix A) where the discrete and continuous parts of are discontinuous.

In Mathematica, I wrote a module GetAllTransitionPts[..], which returns a list of

such points. As I integrate in the -plane over the line for ,

the list only includes transition points in that (finite) interval. Now, in Mathematica, when

integrating using NIntegrate[..] and typical defaults, the integration is adaptive and you

don’t know in advance what points will be sampled. In the function returning the integrand,

I first determine if each sample point

is near any transition point , nearness meaning , where

is small. If not near, I just return

the ‘normal’ integrand. If near, I return the linearly interpolated -value, using the endpoint

values at and . This keeps continuous, while

avoiding troublesome evaluations of the discontinuous components too close to their

transition points.

Implementation notes: Case 2.

For the unphysical Case II (), the good news is that there are no discontinuity points. The bad news is that the integrand

requires the infinite sum at (60). I truncate that sum, and

make some use of Mathematica’s Parallelize. This case

is really computationally tedious: results can take a half-hour or more.

Examples.

As a first example, see Tables 1 and 2

for Cases 1 and 2 respectively. Table 3 shows

additional at-the-money implied volatilities at larger , the easiest regime for spectral

solutions. There

is good convergence to the exact analytic results at ,

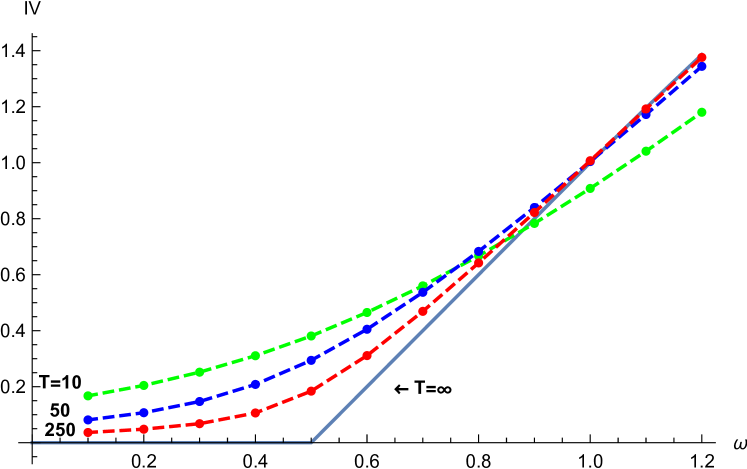

found in Sec. 6.2. Table 3 results are plotted Fig. 4.

Various results were spot-checked for consistency with Monte Carlos. As a stronger check, Table 4 shows some

comparisons and good agreement with option values from a PDE solver.888The PDE solver was developed by Y. Papadopoulos, who

provisionally extended the method in [7] to the XGBM model (private communication).

Option

Implied

Option

Implied

Option

Implied

T

Price

Vol(%)

Price

Vol(%)

Price

Vol(%)

0.25

4.126

20.69

4.033

20.23

4.543

22.79

2

11.57

20.57

10.78

19.17

18.15

32.46

20

30.97

17.82

28.68

16.44

61.26

38.65

100

61.94

17.54

58.03

16.14

95.06

39.30

500

94.98

17.51

92.81

16.10

99.999

39.42

100

17.51

100

16.09

100

39.46

Table 1: At-the-money option values for Case 1: .

Other risk-neutral model parameters: , , ,

, . Under the stationary density, for respectively. The Implied Vol entries are found from the square-root of (63).

Option

Implied

Option

Implied

Option

Implied

T

Price

Vol(%)

Price

Vol(%)

Price

Vol(%)

0.25

3.705

18.58

3.809

19.11

3.962

19.87

2

7.287

12.93

8.268

14.68

10.35

18.39

20

9.577

5.38

13.56

7.64

15.49

8.74

100

9.756

2.45

18.50

4.68

15.554

3.92

500

9.758

1.10

25.82

2.95

15.554

1.75

9.758

0

100

0

15.554

0

Table 2: At-the-money option values for Case 2: .

Other risk-neutral model parameters: , , , , .

The middle column is technically a Case 1 edge case, but it was computed two ways

with the same result: (i) using Case 1 code with and (ii) using

Case 2 code with . For (ii), the sums in (60)

were truncated at terms. The price entries are computed from (68).

Implied Volatility (decimal)

Case 2

Case 1

T

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

0.1672

0.2044

0.2518

0.3105

0.381

0.465

0.560

0.667

0.783

0.908

1.041

1.180

0.0813

0.1070

0.1470

0.2080

0.294

0.405

0.537

0.683

0.840

1.004

1.172

1.344

0.0364

0.0481

0.0678

0.1061

0.184

0.311

0.469

0.642

0.822

1.007

1.192

1.376

0

0

0

0

0

0.2

0.4

0.6

0.8

1.0

1.196

1.386

Table 3: Large behavior of the Implied Volatility.

Other risk-neutral model parameters: , ,

, , , . The entries

are computed from the exact relations in Sec. 6.2. The

data are plotted in Fig. 4.

Implied Volatility at Various Strikes

Case A

Case B

Strike

PDE

Exact

PDE

Exact

3400

0.6384

0.6384

3600

0.5854

0.5854

0.2813

0.2812

3800

0.5322

0.5322

0.2765

0.2765

4000

0.4787

0.4787

0.2719

0.2719

4200

0.4252

0.4252

0.2675

0.2676

4400

0.3742

0.3742

0.2634

0.2635

4600

0.3344

0.3344

0.2594

0.2595

4800

0.3196

0.3196

0.2557

0.2558

5000

0.3263

0.3263

0.2522

0.2524

5200

0.3420

0.3420

0.2490

0.2492

5400

0.3604

0.3604

0.2462

0.2463

5600

0.3792

0.3792

0.2437

0.2437

Table 4: Numerical check: PDE vs. (quasi) exact solutions. Table entries show

the implied volatility (decimal) for two cases. For Case A: . For Case B: .

Common parameters: , , ,

, , , . As ,

this is a Case 1 comparison. Parameters and PDE values come from an XGBM model calibration against a (July 5, 2002) DAX index option chain using software developed by Y. Papadopoulos (footnote 8). Exact values are implied vols using prices computed from (49).

8 Other applications: -model parameter estimation

Maximum likelihood estimation (MLE) is the preferred approach – feasible using the transition density at (25) with a volatility proxy for the ’s.

Key are dimensionless ratios such as

and ,

where .

If the data observations are such that these ratios

are not particularly small, then a fast and efficient (say C/C++) implementation

is likely needed. However, when the ,

as may be the case with daily or weekly observations, then small-time asymptotics

for the transition density should be effective and the exact formulas can simply serve

as checks. Results along these lines will be reported in another publication.

References

[1]

Milton Abramowitz and Irene A. Stegun.

Handbook of Mathematical Functions.

Dover, 1972.

[2]

P. Christoffersen, K. Jabobs, and K. Mimouni.

Volatility dynamics for the S&P500: Evidence from realized

volatility, data returns, and option prices.

Review of Financial Studies, 23(8):3141–3189, 2010.

[3]

Pierre Henry-Labordere.

Analysis, Geometry, and Modeling in Finance: Advanced Methods in

Option Pricing.

Chapman & Hall/CRC, 2009.

[4]

Alan L. Lewis.

Applications of eigenfunction expansions in continuous-time finance.

Math. Finance, 8:349–383, 1998.

reprinted in Lewis (2016).

[5]

Alan L. Lewis.

Option Valuation under Stochastic Volatility: with Mathematica

Code.

Finance Press, Newport Beach, California, 2000.

[6]

Alan L. Lewis.

Option Valuation under Stochastic Volatility II: With

Mathematica Code.

Finance Press, Newport Beach, California, 2016.

[7]

Y. A. Papadopoulos and A. L. Lewis.

A first option calibration of the GARCH diffusion model by a PDE

method.

arXiv:1801.06141 [q-fin.CP], 2018.

[8]

Louis Paulot.

Asymptotic Implied Volatility at the Second Order With Application

to the SABR Model.

Revised version published at arxiv.org, Oct 11 2010.

arXiv:0906.0658v2 [q-fin.PR], also available in P.K. Friz et al.

(editors), ‘Large Deviations and Asymptotic Methods In Finance’, Springer

2015.

[9]

L.J. Slater.

Confluent Hypergeometric Functions.

Cambridge University Press, 1960.

[10]

M. Tegner and R. Poulsen.

Volatility is log-normal – but not for the reason you think.

risks, 6(2), 2018.

9 Appendix A – Proof of Theorem 1

The goal is to solve problem (23) for . With , the Laplace transform

exists and solves

(70)

The associated homogeneous ODE

(71)

is converted

to Kummer’s differential equation in two steps. First, suppressing the dependence on ,

let , choosing

(72)

This yields the ODE

Second, let , where , choosing

(73)

With that,

solves Kummer’s differential equation

Note that in the case of real coefficients with , we have

both and , regardless of the sign of . To

construct , we need solutions to Kummer’s equation that are relatively small

as and respectively. Suitable choices here are the confluent hypergeometric

functions and . We denote the associated solutions to (71)

as and . Using the above notations,

(74)

In terms of those, the solution to (70) has the well-known form:

(75)

where is the Wronskian of . With that, a first solution

for the Green function is given by the Bromwich Laplace inversion

(76)

where is a vertical line in the complex -plane to the right of any singularities.

As is a probability transition density, bounded on ,

then is regular for all . Thus, any vertical contour to the right of suffices

for : see Fig. 1.

First solution (Auxiliary Green function by Bromwich inversion):

(80)

9.1 Spectral solution, Case 2

Case 2 is simpler in some respects, so a good place to begin.

We construct the spectral solution from (80) via the Residue Theorem, extending the

Bromwich contour to the closed path shown in Fig. 1. The precise nature

of that path is explained below.

As one sees from

(80), is dependent upon the parameters and . Both

have a (square-root) branch point singularity at ,

using ‘c’ for ‘cut’.

Regardless of the value of (real) , this branch point is always present in the

left half -plane on the negative axis. We construct a branch cut along the negative axis, extending from to . Then, we integrate infinitesimally above and below the cut, along

the contours and (Fig. 1).

Now may also have pole singularities inside the closed contour.

Note the branch-cut is outside. However, it will be shown below that there

are no such poles when , our Case 2. It can also be shown

that the contribution from the integrations along the curved quarter-circles of

Fig. 1 vanish as these contour segments extend to .

Hence, in that case, is regular everywhere inside the closed contour of the figure:

we have for Case 2, by the Residue Theorem,

(81)

Now change integration variables from to by letting

along and respectfully.

Then, as ,

abbreviating . Importantly, while generally

depends upon the Fourier parameter , it is independent of the Laplace parameter .

Similarly, as ,

Notice that, since , we have

for every fixed ,

(82)

Suppressing dependencies on , recall that

Using the representation (59) and abbreviating , along :

Similarly, along :

Comparing, in light of (82), we have the key relation

(84)

In other words, is the same function of dummy integration variable above and below the cut.999Another thing to notice is that, when the parameters are real,

then is also real along the cut. This follows because, under those assumptions,

we have and , where the asterisk denotes

complex conjugation. However, generally in our application. To

elaborate, that’s because we have and,

in general (with non-zero correlation) is not real along any Fourier inversion contour in the complex -plane, although itself is real. In turn, this causes to not be real, which causes

. To see the implications of that, take the case where .

Then, we have

where the last equality follows from (86). Using this last equality and (9.1), now (85) reads

(87)

The relation (87) gives the continuous spectrum contribution to .

The computation has been done assuming , but the reader can repeat it for

and find (87) again. Also, remember that we treat two cases: Case 1, where and Case 2, where .

We will establish below that, for Case 2, the continuous spectrum contribution is the sole

contribution. Accepting that, we can summarize at this point with

Spectral solution, Case 2 ():

(88)

Remarks.

(i) The subscript ‘c’ in (88) refers to the ‘continuous’

spectrum, which is the entire spectrum under Case 2. Later, we use ‘d’ for the ‘discrete’ spectrum

contribution.

(ii) Recall that the speed density associated to a diffusion is

proportional to the stationary density, given for our problem at (26).

If you remove

from (88), what remains is invariant under ,

a well-known general property of diffusions.

9.2 Spectral solution, Case 1

Referring to Fig. 1, let denote the entire (counter-clockwise)

closed contour and the open interior bounded by .

In addition to the identified branch cut singularity at , may have

simple pole singularities at various . In that case, applying the Residue

Theorem generalizes (81) to:

(89)

Here

denotes the simple pole residue of at and is already given at

(88). The next step is locating these putative poles.

Looking at (80), there are potentially poles lurking in

and . However, while has a simple pole at , where is a positive integer

(see [1]) the function actually appears in the regularized form , which

is everywhere regular. This leads us to seek possible poles in , which has simple

poles should , where , here a generally terminating sequence. These

poles correspond to the vanishing of the

Wronskian in (77). More specifically, we have the

(90)

As we shall see, assuming (Case 1) and dependent upon the other parameters, there may exist zero or a finite number of such .

9.2.1 Sub-case: real parameters

It is helpful to begin with

the sub-case where all the parameters ) are real, with ,

and of any sign. In that case, from (80),

where . Notice that is real, non-negative, and

independent of .

To find , we must have both real and non-positive. For to be real,

we must have real and lying on the real -axis with . Since ,

at , we have . For , we have .

Hence, is both real and negative only when . For emphasis:

•

under

real parameters, the only possible poles the discrete spectra lie on the negative real -axis in-between the

branch cut at and the origin.

The reader should picture a graph of as increases from to . Suppose

, so that . Suppose is sufficiently large so that

. Finally, note that, for ,

Thus, is monotone increasing over and, under the assumptions, crosses the

-axis exactly once within the interval. That crossing point is the location of the pole

where .

Under these same assumptions, is there a pole – i.e., a value

of where ? For this to be true, would have to be even larger, now

sufficiently large so that . If this last relation holds,

then by the same argument, there is a unique point such that .

It may be helpful to think of the relation as simply

a version of our previous relation (for ) except we have .

Moreover, by picturing how the graph of shifts vertically as , one sees

that, when the putative exists, then so does and .

The case of general for any positive integer should be clear. To have ,

must be sufficiently large so that .

When that last relation holds, there is a unique point such that .

Moreover, when the putative exists, then so do all the for .

In addition, these real poles are ordered in the permissible interval such that

(91)

What is the condition for at least one pole? As we have seen, for to exist, we must

have ; i.e.,

(92)

As promised, (92) shows there is no discrete

spectrum for Case 2 ) – at least for the real parameter sub-case.

What is , the largest value of in (91)? It is the largest integer such that . Let denote the

largest integer contained in under the assumption that . Then we have found that

(93)

Finally, provided (92) holds and , what

is ? The relation is easily solved for to yield

(94)

Summarizing at this point we have now developed (89) to

(95)

where is found in (94) and is found in (93).

It remains to calculate the required residues at these poles.

9.2.2 Residues

From (80), since , we have .

Since , we have . Recalling

that is regular everywhere, we have

where denotes either or . Also, from the representation (59),

since the pole in suppresses the second factor of . Here denotes

when and vice-versa.

Recall that, as ,

Thus, as

Putting it all together we have, as ,

where we have written using the Pochhammer symbol.

Factoring out the stationary density, we have found that

Summarizing, with real parameters, we have fleshed out (89) to read

(96)

where

and using the other notations above. The expression (96) completes

the proof of Theorem 1 for the case of real parameters.

9.2.3 General case: complex parameters

As we saw in Sec. 2.1, complex parameters arise

under the reduction of the bivariate XGBM model to (23).

For example, recall what happens when trying to calculate option values under the

risk-neutral (Q) model. Then, one has

the mapping of equation (44).

That is, where is in the preferred Fourier

inversion strip () and

(97)

With these changes, in (80) still

‘works’. Since remains real under these complexifications, the

spectral solution components remains the same:

the location of both the branch point at and the associated branch

cut is unchanged.101010More carefully, by ‘the same’, I mean

the formula for continues to be (88),

already derived allowing complex values for .

What does change is that the formerly non-negative parameter should now

be considered complex; it remains -independent. Now at fixed :

With complex , let’s write again the pole criteria (90), which reads

(98)

For any complex number , then has a branch point singularity

at the origin. With the branch cut conventionally placed along the

negative -axis, then in the cut plane with .

Thus , which shows for all .

This applies to our situation (98) with the identification . In other words, since in the cut -plane, we

can take the real part of both sides of (98) to find that

(99)

For a non-empty discrete spectrum, we need a solution to (98) for . That

requires to be satisfied. The poles themselves

are still given by the same formula (94), now

(100)

The same formulas as before still hold for the residues. Thus, we have the

generalization, with complex parameters:

(101)

where

Comparing (101) to the previous (96), the formulas are

very close – the only change is in the pole condition and sum limit.

Complications induced by the Fourier inversion. When using the above formulas for the bivariate model, as we

have discussed, the parameter depends upon the

Fourier parameter . For each fixed , when ,

the number of discrete eigenvalues is

given from the above by .

Thus, when integrating along a contour in the complex -plane to implement

(49), you will often find changing by unit steps

along the integration contour.

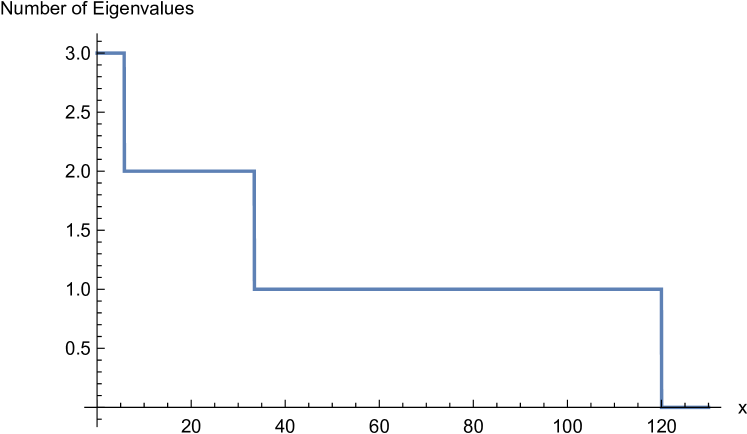

An example should make this clear. Take the risk-neutral XGBM option model with , ,

, and . To find option values, we perform a Fourier inversion by integrating along

for . Fig. 5 plots the

number of eigenvalues (number of elements in the discrete spectrum) as varies

along this contour. As you can see, at the beginning of the contour (),

there are 3 eigenvalues in the spectrum, but they each subsequently drop out as increases,

at transition points . Thus, at large , indeed for

all , the discrete spectrum is empty.

What is going on that causes the drop-outs?

If you look at trajectory plots

of in the complex -plane (as varies), you will find that the

drop-outs occur precisely where the touch the branch cut (Fig. 2).

Note that the branch-cut itself is not in the region . Thus, the qualification in (98) is important and is enforced by the behavior we have just described.

Eigenvalues reaching the branch cut is a new feature of the complex parameter case. With real

parameters, can approach the cut – but only from the real axis. So, if it

reached the cut, it would reach it at the branch point end-point only, where the formulas tend to be

smoother.

A complication associated with this behavior is that the two components of the

spectral expansions above (discrete and continuous) can show discontinuities

at these transition points – even though their sum is smooth.

While itself will be smooth as passes

through a transition value, there may

be off-setting discontinuities in the (continuous and discrete) components and or associated functions. Examples of associated functions to are the marginals

in which the terminal volatility is integrated out. See

Fig. 3 for examples of how the branch

cut touches of Fig. 2 manifest themselves in discontinuities

of and , while remains continuous in . This behavior needs to be carefully handled in

any coding implementation: we discussed our particular method in Sec. 7.

10 Appendix B – The SABR model limit

If one drops the drifts from (4), the system becomes

(105)

which is the lognormal SABR model. Equivalently, (8) becomes

(109)

Now, (25) holds with ,

, and . Tracing the implications in Theorem 1, there are considerable simplifications. Using the notations there, since

, there is no discrete spectrum contribution. In the continuous spectra integrand, the key simplification

is the relation (see [1]):

where is a modified Bessel function. One can also show from [1] that

Eqn (110) agrees with a representation for the SABR transition density previously found in [6] (Ch. 8, eqn (8.81)). Note that in (110) I have flipped the sign of dummy integration variable relative to (25) to make the comparison with [6].

11 Appendix C – The martingale defect

The XGBM model under the risk-neutral (Q-measure) evolution

is given at (33). Using from there, define ,

and . We also need , ,

, and .

Then, one can show that the martingale defect under that model is given by

(111)

Here is an absorption probability, given by:

(112)

(113)

(114)

(115)

Proof: Follows easily from the absorption probability found in Sec 13.2.9 of

Ch. 13 of [6].

Remarks. As discussed in [5], an alternative route to

the martingale defect is the relation .

Showing the equivalence of this last relation to (111) is

a good exercise for the interested reader when . A direct check for general

has eluded us.

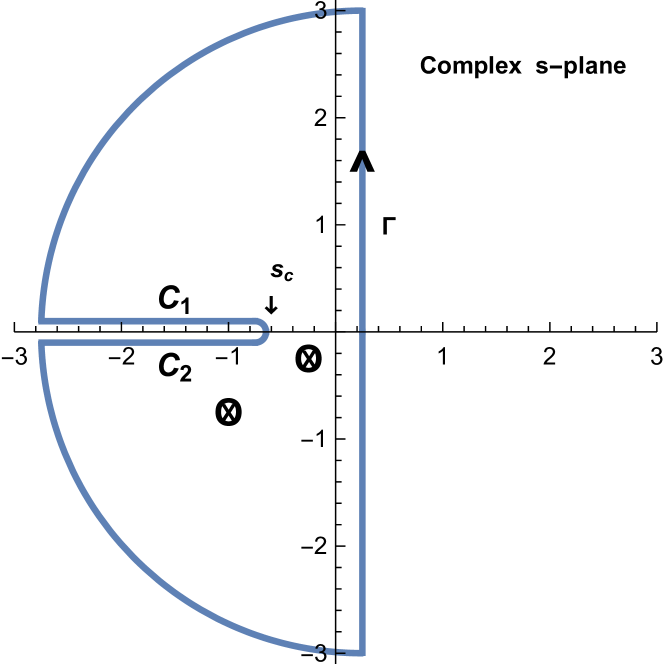

Figure 1: Green function inversion contour in the complex -plane

Notes. The vertical contour is the Bromwich (Laplace) inversion contour in the complex -plane for the auxiliary Green function . The Residue Theorem converts the integral along into an integral along the branch-cut (which extends along the line plus contributions from poles (shown as crossed-circles). The figure is schematic: there generally may be zero or more poles. The branch-cut endpoint is at , where . The poles move in the -plane as the separate Fourier inversion parameter moves in the complex -plane. However, as changes (while other parameters are fixed), the branch-cut endpoint remains fixed.

Figure 2: Eigenvalue Trajectories in the Complex -plane vs.

Notes. Parameters: , , , and . Fourier integration is along the contour , where at most 3 eigenvalues , contribute. Top chart shows the . Bottom chart shows parametric plots of as increases along the contour. Middle chart shows detail to make the trajectory clearer. The trajectories touch the branch cut and the corresponding eigenvalues disappear from the solution at for respectively.

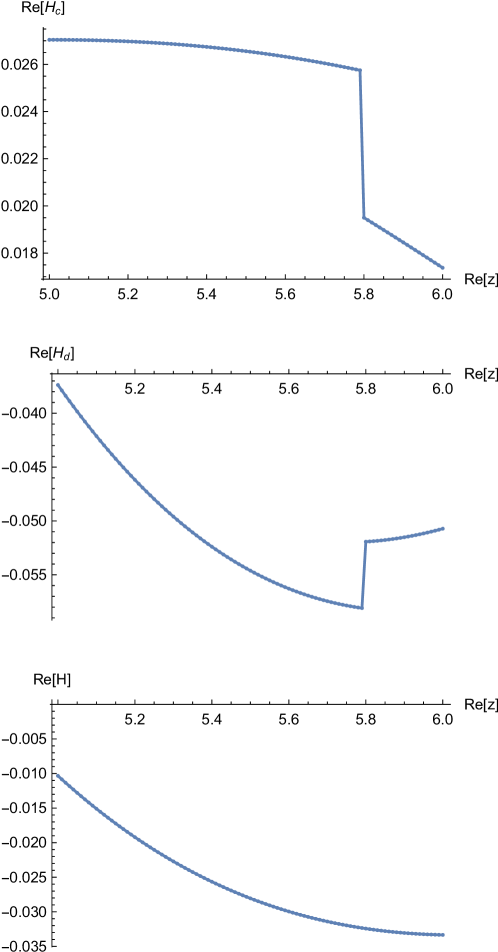

Figure 3: Continuous, Discrete, and Full Fundamental Transform:

vs.

Notes. Model parameters as in Fig.2. The trajectory for the eigenvalue along the Fourier integration contour touches the branch cut at . At that point the fundamental transform is regular (smooth), while the continuous and discrete components, and respectively, have offsetting jumps. This behavior occurs whenever a discrete eigenvalue touches the -plane branch cut as it leaves the solution.

Figure 4: Large T behavior of the Implied VolatilityFigure 5: Discrete Spectrum Size along a Fourier Integration Contour