Hierarchical algorithm for TMVN expectationsJ. Huang, F. Fang, G. Turkiyyah, J. Cao, M.G. Genton, and D.E. Keyes

Hierarchical algorithm for computing the expectations of truncated multi-variate normal distributions in dimensions††thanks: Submitted to the editors .

Abstract

In this paper, we study the -dimensional integral representing the expectation of a function where is the truncated multi-variate normal (TMVN) distribution with zero mean, is the vector of integration variables for the -dimensional random vector , is the inverse of the covariance matrix , and and are constant vectors. We present a new hierarchical algorithm which can evaluate using asymptotically optimal operations when has “low-rank” blocks with “low-dimensional” features and is “low-rank”. We demonstrate the divide-and-conquer idea when is a symmetric positive definite tridiagonal matrix, and present the necessary building blocks and rigorous potential theory based algorithm analysis when is given by the exponential covariance model. Numerical results are presented to demonstrate the algorithm accuracy and efficiency for these two cases. We also briefly discuss how the algorithm can be generalized to a wider class of covariance models and its limitations.

keywords:

Exponential Covariance Model, Fourier Transform, Hierarchical Algorithm, Low-dimensional Structure, Low-rank Structure, Truncated Multi-variate Normal Distribution.03D20, 34B27, 62H10, 65C60, 65D30, 65T40

1 Introduction

In this paper, we study the efficient computation of the expectation of function given by

| (1) | |||||

where the -dimensional random vector follows the truncated multivariate normal distribution (TMVN), is the -dimensional multivariate Gaussian probability density function with zero mean and covariance matrix , is the inverse of the symmetric positive definite (SPD) covariance matrix , is the integration variable, and the integration limits are and which form a hyper-rectangle in . The efficient computation of is very important for many applications, including those in spatial and temporal statistics and in the study of other high dimensional random data sets where the Gaussian distribution is commonly used, see [3, 4, 5, 6, 10, 13, 16, 17, 43] and references therein. Note that is a constant. When has low-rank properties, can be evaluated efficiently using existing low-rank linear algebra techniques [23, 27, 29, 31]. we ignore this term to simplify our discussions in this paper.

Due to the “curse of dimensionality”, direct evaluation of the -dimensional integral using standard quadrature rules is computationally demanding (and impossible for many settings using today’s supercomputers), and most existing schemes either scale poorly when the dimension increases or rely on the Monte Carlo methods for very high dimensional cases [8, 12, 18, 19, 20, 22, 35, 30, 37, 38, 40, 41]. A good review of existing techniques can be found in [19]. The purpose of this paper is to show that when there exist special structures in and (or equivalently in ), fast direct evaluation of the -dimensional integral becomes possible. In particular, when the function is “low-rank” and the matrix has hierarchical low-rank blocks with “low-dimensional” singular vectors in their singular value decompositions, asymptotically optimal hierarchical algorithms can be developed, by compressing these compact features and efficiently processing them “locally” on a hierarchical tree structure. We leave the mathematical rigorous definitions of the “low-rank” and “low-dimensional” concepts to later discussions, but only mention that such “compact” structures exist in many important applications. For example, when the high dimensional data can be properly clustered, e.g., by using their spatial or temporal locations and relative distance or pseudo-distance, the matrix blocks describing the “interactions” between different clusters are often low-rank as revealed by the principal component analysis (PCA).

This paper presents the algorithm analysis and implementation details for two representative matrices: (a) when is a tridiagonal SPD matrix; and (b) when has the same form as the covariance matrix in the exponential covariance model in one dimensional setting. In case (b) when is the exponential covariance matrix, the original covariance matrix is approximately a tridiagonal system. In the numerical algorithm for both cases, a downward pass is first performed on a hierarchical tree structure, by introducing a -variable to divide the parent problem (involving a function with no more than “effective” variables) into two child problems, each involving a function with no more than “effective” variables. The relation coefficients between the parent’s effective variables, new -variable, and children’s effective variables are computed and stored for each tree node. At the leaf level, the one dimensional integral which only involves one variable is evaluated either analytically or numerically, and then approximated numerically by a global Fourier series representation. An upward pass is then performed, to recursively forming the approximating Fourier series of the parent’s -effective variable function using those from its two children. The function value in Eq. (1) is simply given by the constant function (with two “null variables”) at the root level of the tree structure. The presented hierarchical algorithms share many similar features as many existing fast hierarchical algorithms in scientific computing, including the classical fast Fourier transform (FFT) [11], multigrid method (MG) [9, 28], fast multipole method (FMM) [25, 26], and the fast direct solvers (FDS) and hierarchical matrix (-matrix) algorithms [23, 31, 27, 29].

This paper is organized as follows. In Sec. 2, we introduce the mathematical definitions of the “low-rank” and “low-dimensional” concepts. In Sec. 3, we present the details of a hierarchical algorithm for computing when is a tridiagonal matrix. In Sec. 4, we show how the algorithm can be generalized to the case when has the same form as the exponential covariance matrix in one dimensional setting, and present the rigorous analysis using potential theory from ordinary and partial differential equation analysis, as the exponential covariance model in one dimension is closely related with the Green’s function and integral equation solutions of the boundary value ordinary differential equation . Numerical results are presented to demonstrate the accuracy, stability, and complexity of the new hierarchical algorithm for both cases. In Sec. 5, we discuss how the algorithm can be generalized to more complicated cases as well as its limitations. In particular, our current algorithm implementation relies heavily on existing numerical tools and software packages for accurately processing multi-variable functions (e.g., high dimensional non-uniform FFT or sparse grid techniques). Many of these tools are unfortunately still unavailable even when the number of independent variables is approximately . Finally in Sec. 6, we summarize our results.

2 Low-rank and Low-dimensional Properties

Our algorithm can be applied to a function with the following structure,

| (2) |

where is assumed to be a small constant independent of , and each function is a single variable function, not necessarily a continuous function. As the separation of variables

can be considered as the non-orthogonalized function version of the singular value matrix decomposition

we refer to a function with a representation in Eq. (2) as a low-rank (rank-) function. Plugging Eq. (2) into Eq. (1), the original problem of evaluating now becomes the evaluations of integrals, each has the form

| (3) |

We focus on in the following discussions, and simply denote as .

For the inverse of the covariance matrix , we assume it belongs to a class of hierarchical matrices (-matrices) [27, 29] with low-rank off-diagonal blocks. A sample Hierarchical matrix after (left) and (right) divisions is demonstrated in Fig. 1, where the blue square block represents the self-correlation within each cluster of random variables , and the green block shows the correlation between two different clusters. We define a cluster in the original domain as a set of indices of the column vectors, and a cluster in the target space as a set of indices of the row vectors. The correlation between the cluster of the original domain and cluster of the target space is described by the matrix block formed by only extracting the -entries from the -columns. We consider -matrices with low-rank off-diagonal blocks, by assuming that the ranks of all the off-diagonal blocks are bounded by a constant , which is independent of the block matrix size. We use to represents the dimension of a subspace or the rank of a matrix in this paper, and the rank of the off-diagonal blocks can be different from the rank in Eq. (2). In numerical linear algebra, “low-rank off-diagonal block” means that the off-diagonal block of size has the following singular value decomposition

where and are of size and respectively contain the orthonormal vectors in the target space and original domain, and is a size diagonal matrix with ordered and non-negative diagonal entries. As the random variables are clustered hierarchically, we index the block matrices differently from those commonly used in matrix theory to emphasize this hierarchical structure in the -matrix, where represents the level of the matrix block, and is its index in that particular level. The original matrix is defined as the level matrix. After the division, the matrix blocks are indexed , , , and . The diagonal matrix blocks will be further divided and the off-diagonal matrices become leaf nodes to form an adaptive quad-tree structure. In the left of Fig. 1, the matrix denotes the second matrix block at level , representing the correlations between the second cluster in the original domain and first cluster in the target space. For the covariance matrix, as the target space and original domain are the one and the same, the indices of the random variables (and integration variables ) will be used to cluster the indices of both the target space and original domain, to form a uniform binary tree structure. In the following, we focus on the integration variables , which are referred to as the -variables.

Next, we consider the “low-dimensional” concept, by studying a function with -variables , , , of the form

When the dimension of the vector space is much less than , , we say is a “low-dimensional” function. Assuming the basis for the vector space is given by , the function can be considered as an “effective” variable function, where the new -variables are combinations of the -variables and satisfy the relation

The low-rank and low-dimensional structures exist in many practical systems. The well studied low-rank concept measures the rank of a matrix block and is closely related with the principal component analysis in statistics and singular value decomposition (SVD) in numerical linear algebra. When the data can be clustered, the covariance matrix block describing the relations between two different clusters is often low-rank, and both the storage of such a matrix block and related operations can be reduced significantly using today’s low-rank linear algebra techniques. The low-dimensional property in this paper considers the special structures in the singular vectors of the SVD decomposition of the low-rank off-diagonal blocks. Consider two clusters of the -variables and the space formed by extracting all the corresponding sub-vectors describing the relations of these two clusters from the singular vectors in the SVD decompositions of all the off-diagonal matrices. When the covariance matrix is defined by a covariance function using the spatial or temporal locations (or pseudo-locations) and of the corresponding random variables and , the covariance function is often “smooth” and only contains “low-frequency” information when , it can be well approximated by a few terms of truncated Taylor expansion (or other basis functions) when a separation of variables is performed on the covariance function determined by the two location variables and . In this case, all the singular vectors are the discretized versions of the polynomial basis functions at locations corresponding to the cluster index sets. The dimension of the space formed by these singular vectors is therefore determined by the highest degree of the polynomial basis functions. When the vectors are extracted from these singular vectors, the function will be low-dimensional and the number of effective variables is also determined by the highest degree of the polynomial basis functions. The special structures in the singular vectors were also used in [31, 32, 33]. The low-rank and low-dimensional concepts will be further studied in the next two sections.

3 Case I: Tridiagonal System

We demonstrate the basic ideas of the hierarchical algorithm by studying a simple tridiagonal system

| (4) |

We assume and first consider a constant function to simplify the notations and discussions. The algorithm for more general low-rank in Eq. (3) only requires a slight change in the code for the leaf nodes, which will become clear after we present the algorithm details for the simplified integration problem

| (5) | |||||

where . The tridiagonal matrix is a very special -matrix, where each off-diagonal matrix block only contains one non-zero number either at the lower-left or upper-right corner of the matrix block and is rank . The singular vectors are either or . For any given cluster of indices, the number of effective variables in is therefore no more than 2, and the only non-zero numbers are located either at the first or the last entry in the singular vectors , , , .

3.1 Divide and Conquer on a Hierarchical Tree

Note that the -variables and are coupled in the integrand only through one term . If this “weak coupling” term had not been there, then we would have two completely decoupled “child problems”, and the integral could be evaluated as

If the same assumptions could be made to each “child problem”, then the high-dimensional integral would become the product of one-dimensional integrals.

A convenient tool to decouple the -variables in order to have two child problems is to use the Fourier transform formula for the Gaussian distribution as

| (6) |

where and . Note that the variables and are decoupled on the right hand side. Completing the square in Eq. (5) and applying the formula in Eq. (6) to the resulting term (in red) in the integral, we get

where and are both single -variable functions given by

Note that the -variables in the original problem (associated with a root node at level of a binary tree structure) are divided into two subsets of the same size, each set is associated with a “child node” and a single -variable function , or .

By introducing two new -variables and for the functions and , respectively, the same technique can be applied to decouple the -variables and in and the -variables and in , to derive

where

Repeating this procedure recursively on the hierarchical tree structure derived by recursively dividing the parent’s -variable set into two child subsets of the same size, a hierarchical -function will be defined for each tree node, where is the index of the tree node defined in the same way as that of the -variable sets. One can show that for a parent node with index , its -function (with at most two -variables and ) can be computed from the two child functions and (each with at most two -variables) by integrating the -variable used to decouple the parent problem using Eq. (6) as

| (7) |

At the finest level when the -variable set only contains one -variable , the two -variable function is given by

where for the interior nodes and for the two boundary nodes at the leaf level. For each boundary node in the tree structure, its associated -function only involves one -variable as the other becomes a null variable. In Fig. 2, we show the detailed decoupling procedure and the functions when , where the first index of indicates the level at which the new -variable is introduced, and the second index is its index at this level, ordered from bottom (left boundary of -variables) to top (right boundary) in the figure.

Remark: Each parent’s -function has no more than two -variables, and it can be computed using the two children’s -functions, each with no more than two -variables, as shown in Eq. (7). Note that the decoupling process is performed on a hierarchical binary tree structure, by introducing one new -variable and dividing parent’s -variable set into two children’s subsets of the same size. As the depth of the tree is so a total of -variables will be introduced for each tree branch from the root to leaf level. However, as the singular vectors are either or . For a tree node containing a particular set of -variable indices from to , there are at most two non-zero vectors in the vector set , with the non-zero entry located either at the first or the last entry in one of the two non-zero singular vectors of size . The number of effective variables in is therefore no more than 2, and

Therefore all the -functions in the hierarchical tree structure have no more than two effective variables and are “low-dimensional” functions.

3.2 Algorithm Details

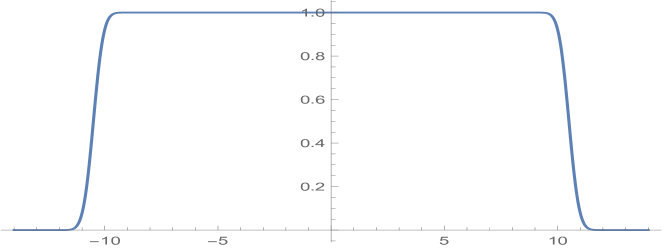

Notice that in Eq. (7), because of the rapid decay of the weight function , one only needs to accurately approximate the function in the region . In our algorithm implementation, we define a filter function

where we set so that the function is approximately when (), and smoothly decays to at () , as shown in Fig. 3.

At a leaf node, the integral is computed analytically either using

for a boundary node, or

for an interior node and then evaluated at a set of uniformly distributed sample points in for the two -variables. The function values are then filtered by the pointwise multiplication with the filter function for each variable. The Fourier series of the leaf node function, when needed, can be derived by a FFT using the filtered function values. In the formula, we use the Faddeeva function [2, 1, 15, 34] defined as for a complex number , to avoid the possible overflow/underflow when computing small times large values. An upward pass is then performed to recursively compute the parent’s filtered function values at the Fourier interpolation points using its children’s filtered function values at different , , and interpolation points through 5 steps: (i) multiplying two children’s values at each sample point; (ii) point-wise multiplication with the filter function; (iii) applying the fast Fourier transform (FFT) to the variable in the region to get the Fourier coefficients from the filtered function values at each interpolation point; (iv) the parent’s -function value at each and interpolation point is derived by applying the formula

to integrate the Fourier series expansion of variable from (iii) analytically; and (v) the function values will be further filtered. If needed, a FFT can be performed to derive the parent’s Fourier series expansion coefficients. Note that the Fourier series in the region can be extended to the whole space as such extension will only introduce an error within machine precision when evaluating the integral in Eq. (7). At the root node, its -function returns the value we are searching for.

The algorithm for efficiently evaluating Eq. (5) can be summarized as the following two passes. In the downward pass, the parent problem is decoupled by applying the Fourier transform to the coupling term, to obtain two child problems. At the finest level, a function with two -variables is created for each leaf node followed by an upward pass to obtains each parent’s function values at the Fourier interpolation points from those of its two children’s functions. At the root level, the constant function (with null -variables) gives the result of the integral in Eq. (5). The recursively implemented Matlab code for the upward pass is presented in Algorithm .

3.3 Preliminary Numerical Results

We present some preliminary results to demonstrate the accuracy and efficiency of the numerical algorithm for the tridiagonal system in Eq. (5). In the numerical experiments, we set all to , , , and all other to . We first study the accuracy of the algorithm. For , we compute a reference solution using Mathematica with and , the result is . For , Mathematica returns the result with an estimated error , even though and are requested. For , direct computation using Mathematica simply becomes impossible. In Table 2, we show the Matlab results for different dimensions and numbers of terms in the Fourier series expansion. For all cases, our results converge when increases. For , our result matches Mathematica result to machine precision as soon as enough Fourier terms are used. For , our converged results agree with Mathematica result in the first digits, and we strongly believe our results are more accurate. The numerical tests are performed on a laptop computer with Intel i7-3520M CPU @2.90GHz, with RAM. For and , approximately function values at the Fourier interpolation points have to be stored in the memory (), which exceeds the installed RAM size, hence no result is reported.

| 4 | 8 | 16 | |

| =16 | 2.326607912389402 | 6.736597967982384 | 56.44481808043047 |

| =32 | 2.289334215119377 | 6.624246691958165 | 55.44625398858155 |

| =64 | 2.289334215088778 | 6.624246691490006 | 55.44625397830180 |

| =128 | 2.289334215088779 | 6.624246691490009 | 55.44625397830178 |

| =256 | 2.289334215088778 | 6.624246691490005 | 55.44625397830176 |

| =512 | 2.289334215088778 | 6.624246691490003 | 55.44625397830172 |

| 32 | 64 | 1024 | |

| =16 | 3962.697712673563 | 19531008.87334120 | 1.182324449792241e+118 |

| =32 | 3884.575992952042 | 19067179.07844248 | 1.019931849681238e+118 |

| =64 | 3884.575991340509 | 19067179.06178229 | 1.019931834748418e+118 |

| =128 | 3884.575991340506 | 19067179.06178229 | 1.019931834748411e+118 |

| =256 | 3884.575991340500 | 19067179.06178224 | 1.019931834748369e+118 |

| =512 | 3884.575991340498 | 19067179.06178220 | N/A |

We demonstrate the efficiency of our algorithm by presenting the Matlab simulation time for different dimensions. In the experiment, we present the CPU times for different and values, and the unit is in seconds. Clearly, the CPU time grows approximately linearly as the dimension increases. As a 3-variable {, , and } function has to be processed in the current implementation when finding the parent’s values at the Fourier interpolation points, the CPU time grows approximately by a factor of as doubles. For and , approximately memory is required, which exceeds the maximum available RAM size, hence no result is reported.

| 4 | 8 | 16 | 32 | 64 | |

| CPU time | 0.02 | 0.04 | 0.15 | 0.34 | 0.80 |

| CPU time | 0.06 | 0.27 | 0.96 | 2.26 | 4.60 |

| CPU time | 0.12 | 2.15 | 6.81 | 16.5 | 39.1 |

| CPU time | 0.24 | 12.5 | 49.1 | 130 | 315 |

| 128 | 256 | 512 | 1024 | 2048 | |

| CPU time | 1.95 | 3.75 | 8.29 | 16.6 | 40.1 |

| CPU time | 10.2 | 23.5 | 49.2 | 103 | 214 |

| CPU time | 88.5 | 228 | 445 | 970 | 1942 |

| CPU time | 718 | 1769 | 3476 | 8310 | N/A |

4 Case II: Exponential Matrix

In the second case, we consider a matrix defined by the exponential covariance function

To simplify the discussions, we consider a simple 1D setting from spatial or temporal statistics and assume that the rate of decay and each random number is observed at a location . We assume the -locations , are ordered from smallest to largest and the matrix entries are ordered accordingly. We demonstrate how to evaluate the -dimensional integral

| (8) |

for the given constant vectors and using operations. Results for different values can be derived by rescaling the -locations and -variables. The presented algorithm can be easily generalized to when is a low-rank function.

Similar to the tridiagonal matrix case, we generate a binary tree by recursively dividing the parent’s -location set (or equivalently the -variable set) into two child subsets, each containing exactly half of its parent’s points. The hierarchical binary tree is then reflected as a hierarchical matrix as demonstrated in Fig. 1. Unlike the (uniform) binary tree generated for the -location set, the corresponding structure in the matrix sub-division process can be considered as an adaptive quad-tree, where only the diagonal blocks of the matrix are subdivided. Once an off-diagonal block is generated, it becomes a leaf node and no further division is required. Because of the hierarchical structure of the matrix and the low-rank properties of the off-diagonal blocks (which will be discussed next), the exponential matrix is a special -matrix.

4.1 Divide and Conquer on a Hierarchical Tree

Unlike the tridiagonal system, each off-diagonal matrix in this case is a dense matrix. For this exponential matrix, all the off-diagonal matrices are rank-1 matrices, which can be seen from the separation of variables

In matrix language, the off-diagonal block can be written as

| (9) |

for and . The singular value decomposition of can be easily derived using Eq. (9) as

where the left and right singular vectors and are of size and respectively the normalized vectors of the discretized functions and .

When the -variables are divided into subsets and , the root matrix can be subdivided accordingly into blocks

where the first index of is the current level of the block matrix and the second index is its order in this level. Same indexing rules are used for the -locations and -variables. Completing the square, the quadratic form in the integrand can be reformulated as

where the first two green terms are the child problems to be processed recursively at finer levels in the divide-and-conquer strategy, is a constant to be determined, and the last red term shows how the two child problems are coupled. Similar to the tridiagonal case, by introducing a single -variable and applying the Fourier transform formula in Eq. (6) to the coupling term (in red), we get

where and are the single -variable functions for the two child nodes given by

| (10) |

Note that the -variables are completely decoupled in the two child problems, and the coupling is now through the -variable.

In order to have a divide-and-conquer algorithm on the hierarchical tree structure, the two child problems should have the following properties:

-

•

By properly choosing the parameter , the new matrices and should be symmetric positive definite; and

-

•

The off-diagonal blocks of these new matrices should be low-rank.

We found that the choice of is not unique, and there exist a range of values for the child problems to have these properties. The choice of is addressed next.

4.2 Potential Theory based Analysis

In this section, we apply the potential theory from the analysis of ordinary and partial differential equations and show how the divide-and-conquer strategy can be successfully performed on the hierarchical tree structure. Purely numerical linear algebra based approaches for more general cases will be briefly addressed later.

4.2.1 Green’s Functions

We present the results for to simplify the notations and assume . We start from the observation that

is the domain Green’s function of the ordinary differential equation (ODE) two-point boundary value problem

| (11) |

where , and . The proof is simply a straightforward validation that satisfies both the ODE and boundary conditions.

In the following discussions, we consider the continuous version of the original matrix problem, where the matrix is the discretized Green’s function , the two off-diagonal submatrices and are the discretized and , respectively. Some simple algebra manipulations show that the submatrices and can be considered as the discretized and , and the coefficients and for the linear terms of the -variables and in Eq. (10) are the discretized and , respectively.

Remark: The observation also allows easy proof of the positive definiteness of the matrix , which is the discretized Green’s function . In order to show that for any vector , the quadratic form satisfies , we consider its continuous version defined as

where and is the continuous version of the (discretized) vector . As , applying the integration by parts, we have

As , therefore , and applying the boundary conditions of the ODE, we have . We refer to the two-variable function as a positive definite function. The positive definiteness of the matrix can be proved in a similar way using the discretized integration by parts.

A particular choice of can be determined by considering the corresponding child ODE problems as follows. We first study the root problem and define its two children as the left child and right child, and the locations of the left child and of the right child satisfy the condition as the -locations of the -variables in the two child problems are separated and ordered. We pick a location between the two clusters of -locations. Note that the choice of is not unique. We have the following results for the root node.

Theorem 4.1.

If we choose , then

-

•

for the left child, the new function is the Green’s function of the ODE problem

The function is positive definite.

-

•

For the right child, the new function is the Green’s function of the ODE problem

The function is positive definite.

-

•

The two child ODE problem solutions and can be derived by subtracting a single layer potential defined at from the parent’s solution of Eq. (11), so that solutions and satisfy the zero interface condition at . The other boundary condition for each child ODE problem is the same as its parent’s boundary condition.

These results can be easily validated by plugging in the functions to the ODE problems. The positive definiteness of the child Green’s function can be proved using the same integration by part technique as we did for the parent’s Green’s function.

For a general parent node on the tree structure, we have the following generalized results.

Theorem 4.2.

Consider a parent node with the corresponding function defined on the interval , and is a point separating the two children’s -locations. Then there exists a number which depends on , such that

-

•

for the left child, the new function is the Green’s function of the ODE problem

The function is positive definite.

-

•

For the right child, the new function is the Green’s function of the ODE problem

The function is positive definite.

-

•

The two child ODE problem solutions and can be derived by subtracting a single layer potential defined at from the parent’s solution of Eq. (11), so that solutions and satisfy the zero interface condition at . The other boundary condition for each child ODE problem is the same as its parent’s boundary condition.

The detailed formulas for the number and Green’s functions are presented in the Appendix. The proof of the theorem is simply validations of the formulas.

4.2.2 Parent-children Relations

In the matrix form, for a general parent node at level in the hierarchical tree structure with left child and right child , its -function

| (12) |

can be decomposed into two child problems as

where

| (13) |

In the formulas, is the vector containing all the -variables introduced at coarser levels to subdivide ’s parents’ -functions. , , and are respectively the vectors containing the -variables of the parent , child , and child . {,}, {,}, and {,} are respectively the lower and upper integration bounds of , , and . , , and are respectively the discretized Green’s functions of the parent , child , and child , which satisfy

, , and are respectively the -location vectors of the parent and child and , and and are the discrete function values of and in the Green’s functions evaluated at different -locations. is a scalar term representing the linear combinations of the terms, and by separating the -variables, it can be written as

After introducing the new -variable to divide the parent’s problem to two subproblems of child and child , each with half of the parent ’s -variables, we have , , and

| (14) |

For the root node, is the given matrix and is an empty set. At a leaf node, we have

where is a column vector of the same size as (the size equals to the number of levels in the hierarchical tree structure). Analytical formula is available for using

| (15) |

4.2.3 Dimension Reduction and Effective Variables

Note that for a node at level , its -function will contain as many as -variables introduced at parent levels. Therefore for a -dimensional problem, the number of -variables for a leaf node can be as many as . However, inspecting the term for the function , if one introduces a new single variable , then is effectively a single variable function of . We therefore study the effective variables and their properties in this section.

From Eq. (14), we see that when a new -variable is introduced to divide the parent problem into two child problems, the additional terms added to the linear terms of the -variables in the exponent are for child and for child , where and are the discrete function values of and in the Green’s functions evaluated at different -locations. For all the Green’s functions, and are always a combination of the basis functions and . This can be seen either from the ODE problems or from the Green’s functions in the Appendix. Therefore, switching the basis to and , the term can always be written as

| (16) |

where and are the vectors derived by evaluating the functions and at the -locations. Clearly, after this change of variables from -variables to {, }, each -function is effectively a function with no more than variables. We define and as the effective -variables.

Our numerical experiments show that at finer levels of the hierarchical tree structure when the interval size of the tree node becomes smaller, the two basis functions and are closer to linear dependent which will cause numerical stability issues. For better stability properties, orthogonal or near orthogonal basis functions are used. A sample basis is when the -locations of the -variables are in the interval . When is the center of the interval, the two functions are orthogonal to each other when measured using the standard norm with a constant weight function. For a parent node with effective -variables and basis functions , where the vector represents the discretized at the -locations, in the divide-and-conquer strategy, the effective -variables should satisfy the relations

| (17) |

where , , are respectively the continuous basis for the parent, child 1, and child 2, and are the effective -variables of child and child for the discrete basis vectors and , respectively. In the Appendix, we present the detailed formulas demonstrating the relations between parent ’s and children’s effective -variables for the basis choice {, }.

In the tridiagonal case discussed in Section 3, we only need to study the -functions when their -variables satisfy , as outside the interval the integrand value is controlled by the factor and hence can be neglected. Similar results can be obtained for the exponential case, when a proper set of basis is chosen. Assuming all the -locations are approximately uniformly distributed in the interval , we have the following theorem for the effective -variables and .

Theorem 4.3.

Assume the matrix is defined by the exponential covariance function, the -locations are uniformly distributed in the interval , and all the -variables satisfy . When the basis functions are chosen as for each tree node, then there exists a constant independent of , such that the corresponding effective -variables and (combinations of the -variables) satisfy the conditions and .

The proof of this theorem is simply the leading order analysis of the parent-children effective -variable relations, and the fact that , , , and , where is the number of levels in the tree structure. We skip the proof details. Interested readers can request a copy of our Mathematica file for further details. We point out that when the basis functions are chosen as , the effective -variables become unbounded.

Remark: In the numerical implementation, instead of using the upper bound for a tree node , the ranges and of the effective -variables and are computed using the parent-children effective -variable relations in Eq. (17) and stored in the memory. Similar to the tridiagonal case, a filter function is applied to the -functions so that the filtered function smoothly decays to zero in the region or , see Fig. 3. Then the Fourier series of the filtered -function is constructed in the region , and finally the constructed Fourier series is expanded to the whole space when deriving parent’s -function values. In the algorithm implementation, when the uniform FFT [14] can no longer be applied, we use the open source NUFFT package developed in [24, 36] to accelerate the computation of the Fourier series.

4.3 Pseudo-algorithm

Similar to the tridiagonal case, the algorithm can be summarized as the following two passes: In the downward pass, the parent problem is decoupled by applying the Fourier transform to the coupling term, to obtain two child problems. Six coefficients are derived so that the effective -variables of the current node satisfy

| (18) |

where and are the parent’s effective -variables. Also, the ranges and of the effective -variables and are computed. A total of numbers are stored for each node. Note that both the storage and number of operations are constant for each tree node. The pseudo-algorithm is presented in Algorithm , where the details of computing the numbers for each node is presented in the Appendix.

At the finest level, a function with one effective variable is constructed analytically using Eq. (15). A numerically equivalent two-variable Fourier series expansion is then constructed by evaluating the analytical solution at the interpolation points, applying the filter function, and then applying FFT to derive the Fourier series expansion which is considered valid in the whole space. An upward pass is then performed, to obtains each parent’s Fourier coefficients from those of its two children’s functions. For each parent node, we first replace the child’s effective -variables with , and using Eq. (18) and the numbers from the downward pass, then evaluate each child’s global Fourier series at the uniform interpolation points of , and (determined by the ranges and from the downward pass, we set the range of to ). In this step, we have to use the NUFFT as the numbers for different tree nodes are different so the uniform FFT is not applicable. Multiplying the two children’s function values and the filter function values at each interpolation point, we then apply the FFT to the variable and derive the Fourier series of at each and interpolation point. The integral

is then evaluated analytically at each and interpolation point. Finally, another 2D FFT is performed to derive the coefficients of . At the root level, the constant function (with no -variables) gives the result of the integral. In the implementation, as we use unified formulas for both the boundary nodes and interior nodes, the two functions and become unnecessary, see Appendix for details. Except for the detailed implementations in the functions , , and , the recursively implemented Matlab algorithm for the upward pass is identical in structure as the presented Algorithm for the tri-diagonal case, we therefore skip the pseudo-code.

The algorithm complexity can be computed as follows. In both the upward pass and downward pass, constant numbers of operations and storage are required for each tree node, the overall algorithm complexity and memory requirement are therefore both asymptotically optimal for the -dimensional integration problem.

4.4 Preliminary Numerical Results

We present some preliminary results to demonstrate the accuracy and efficiency of the numerical algorithm for the exponential case. The -location points are randomly chosen in and sorted. A uniform tree is then generated by recursively subdividing the -locations and corresponding -variables, and the same settings of and are used as in the tridiagonal case. We first study the accuracy of the algorithm. For , we compute a reference solution using Mathematica, with an estimated error . For , Mathematica returns the result with an estimated error . For , direct computation using Mathematica becomes impossible. In Table 5, we show the Matlab results for different dimensions when Fourier series terms are used in the approximation. The error tolerance for the NUFFT solver is set to . For all cases, our results converge when increases. For both and , our converged results match those from Mathematica within the estimated error from Mathematica.

In the current implementation, as the exponential case involves operations on a 3-variables function for each child when forming the parent’s Fourier series expansion, while both the storage and operations for the tridiagonal case can be compressed so one only works on 2-variable functions (variables for child and for child ), the exponential solver therefore requires more operations and memory than the tridiagonal case. We tested our code on a desktop with 16GB memory and Intel Xeon CPU E3-1225 v6 @3.30GHz. For and , More than memory is already required, hence no result for is reported.

| 4 | 8 | 16 | |

| =16 | 9.646301617204299 | 118.8260790816760 | 21594.43676761628 |

| =32 | 9.631244805483258 | 116.7475848966488 | 17592.18271523017 |

| =64 | 9.631287915305332 | 116.7505122381643 | 17591.75082916860 |

| =128 | 9.631287915311097 | 116.7505122544810 | 17591.75095515863 |

| =256 | 9.631287915311061 | 116.7505122544801 | 17591.75095515877 |

| 32 | 64 | 128 | |

| =16 | 1131582930.741270 | 4.332761307147880e+18 | 7.074841023044070e+37 |

| =32 | 550963842.9679267 | 1.046292247268069e+18 | 9.380354831605098e+36 |

| =64 | 540456718.9698794 | 8.163524406713720e+17 | 3.432262767034514e+36 |

| =128 | 540456737.4129881 | 8.163182314210313e+17 | 3.394537652388589e+36 |

| =256 | 540456737.4129064 | 8.163182314206217e+17 | 3.394537652164628e+36 |

Remark: We explain the large errors when (and ) for large values. When the dimension of the problem increases, its condition number also increases exponentially. For each leaf node, if we assume the numerical solution has a relative error in each leaf node function , in the worst case, the relative error for the dimensional integral can be approximated by as the leaf node functions will be “multiplied” together in the upward pass to get the final integral value. Clearly, the condition number of the analytical problem grows exponentially as increases. In our current implementation, we set the error tolerance of the NUFFT solver to relative error. Therefore, a very rough estimate for the error when , assuming is large enough so the leaf node function is resolved to machine precision, is given by , i.e., at most digits are correct if the worst case happens. Our numerical results show that for the same value, all the converged results match at least in the first significant digits in Table 5.

We demonstrate the efficiency of our algorithm by presenting the Matlab simulation time for different and values, and the unit for the CPU time is in seconds. The current Matlab code has not been fully vectorized or parallelized, and significant performance improvement in the prefactor of the algorithm is expected from a future optimized code. However, the numerical results in Table 6 using our existing code sufficiently and clearly show the asymptotic algorithm complexity: the CPU time grows approximately linearly as the dimension increases, and it increases by a factor of approximately as doubles.

| 4 | 8 | 16 | 32 | 64 | |

| CPU time | 1.03 | 2.96 | 6.67 | 14.1 | 29.2 |

| CPU time | 8.06 | 23.4 | 53.8 | 115 | 238 |

| CPU time | 65.2 | 191 | 445 | 949 | 1965 |

| 128 | 256 | 512 | 1024 | 2048 | |

| CPU time | 59.4 | 119 | 244 | 471 | 951 |

| CPU time | 491 | 988 | 1924 | 3889 | 7766 |

| CPU time | 4049 | 8029 | 16068 | 32465 | 65073 |

5 Generalizations and Limitations

In both the tridiagonal and exponential cases, we present the algorithms for the case . For a general with low-rank properties, i.e.,

as is a small number, we can evaluate the expectation of each term and then add up the results. As the -variables are already separated in the representation, the downward decoupling process can be performed the same as that in the tridiagonal or exponential case. At the finest level, the leaf node’s function becomes

Note that analytical formula is in general not available for , a numerical scheme has to be developed to compute the Fourier coefficients of . This is clearly numerically feasible as the integral is one-dimensional and is effectively a single variable function.

Next we consider more general matrices. We restrict our attention to the symmetric positive definite -matrices, and discuss the required low-rank and low dimensional properties in order for our method to become asymptotically optimal . A minimal requirement from the algorithm is that the off-diagonal matrices should be low rank. Consider a parent’s matrix with such low rank off-diagonals and the corresponding -variables,

where the first index is the current level of the block matrices and point sets, and we assume is low rank, . Then we can rewrite the quadratic term in the exponent of the integrand as

where the first two green terms are the child problems to be processed recursively at finer levels after we use a number of -variables to decouple the and variables using Eq. (6). Clearly, the number of effective variables cannot be smaller than in this case. There are several difficulties in this divide-and-conquer strategy. First, the constant matrix should be chosen so that the resulting children’s matrices are also symmetric positive definite. As the choice of is not unique, its computation is currently done numerically using numerical linear algebra tools, and we are still searching for additional conditions so that we can have uniqueness in and better numerical stabilities in the algorithm. Second, consider a covariance matrix of a general data set, compared with the original off-diagonal matrix blocks in and , the numerical rank of the off-diagonal blocks of the new child matrices and , may increase. In the worst case, the new rank can be as high as the old rank plus . When this happens, the number of -variables required will increase rapidly when decoupling the finer level problems, and the number of effective variables also increases dramatically. Fortunately, for many problems of interest today, the singular vectors and also have special structures. For example, when the off-diagonal covariance function can be well-approximated by a low degree polynomial expansion using the separation of variables, then the singular vectors are just the discretized versions of these polynomials, therefore the rank of all the old and new off-diagonal matrix blocks cannot be higher than the number of the polynomial basis functions, and the number of effective variables is also bounded by this number. In numerical linear algebra language, this means that all the left (or right) singular vectors of the off-diagonal blocks belong to the same low-dimensional subspace, so that the singular vectors of the new child matrices and can be represented by the same set of basis vectors in the subspace. For problems with this property, our algorithm can be generalized, by numerically finding the relations between the effective variables in the downward pass, and finding the parent’s function coefficients using its children’s in the upward pass. The numerical complexity of the resulting algorithm remains asymptotically optimal .

However, our algorithm also suffers from several severe limitations due to the lack of effective tools for high dimensional problems. The main limitation is the large prefactor in the complexity, as the prefactor grows exponentially when the rank of the off-diagonal blocks (and hence the number of effective variables) increases. We presented the results when the number of effective variables are no more than in this paper. When this number increases to , it may still be possible to introduce the sparse grid ideas [7, 21, 39, 42] when integrating the multi-variable -functions. When this number is more than , as far as we know, no current techniques can analytically handle problems of this size. Also, notice that for the current numerical implementation of the exponential case, fast algorithms such as FFT and NUFFT have to be introduced or the computation will become very expensive. However, as far as we know, existing NUFFT tools are only available in , , and dimensions. Finally, as the condition number of the problem increases exponentially as increases, it is important to have very accurate representations of the -functions for the hierarchical tree nodes so reasonable accurate results are possible in higher dimensions. We are currently studying possible strategies to overcome these hurdles, by studying smaller matrix blocks so the rank can be lower, and more promisingly, by coupling the Monte Carlo approach with our divide-and-conquer strategy [17]. Results along these directions will be reported in the future.

6 Conclusions

The main contribution of this paper is an asympotically optimal algorithm for evaluating the expectation of a function

where is the truncated multi-variate normal distribution with zero mean for the -dimensional random vector , when the off-diagonal blocks of are “low-rank” with “low-dimensional” features and is “low-rank”. In the algorithm, a downward pass is performed to obtain the relations between the parent’s and children’s effective variables, followed by an upward pass to construct the -functions for each node on the hierarchical tree structure. The function at the tree root returns the desired expectation. Numerical results are presented to demonstrate the accuracy and efficiency of the algorithm. The generalizations and limitations of the new algorithm are also discussed, with possible strategies so the algorithm can be applied to a wider class of problems.

Acknowledgement

J. Huang was supported by the NSF grant DMS1821093, and the work was finished while he was visiting professors at the King Abdullah University of Science and Technology, National Center for Theoretical Sciences (NCTS) in Taiwan, Mathematical Center for Interdisciplinary Research of Soochow University, and Institute for Mathematical Sciences of the National University of Singapore.

Appendix

We first present the detailed formulas for the Green’s function of a parent node and the functions and of ’s left child and right child . These functions are defined as

We assume parent’s -locations satisfy . We choose to separate the parent’s locations, and the child intervals are therefore and , respectively.

Case 1: is the root node (, ): The functions are

Case 2: is a left boundary node(): The functions are

Case 3: is a right boundary node(): The functions are

Case 4: is an interior node: The functions are

Next, we present the relations of the parent ’s two -variables and with the left child ’s two -variables {, } and right child ’s two -variables {, }. We use to represent the new -variable introduced to divide the parent problem into two sub-problems of child and child . We use a unified set of basis functions for each node on the hierarchical tree structure. For the parent node, the basis functions are . The basis functions for the left and right children are and , respectively, where and are either the interface points when further subdividing the two child problems, or the mid-point of the child intervals when they become leaf nodes.

Case 1: is the root node (, ): Parent has no effective -variables.

Case 2: is a left boundary node():

Case 3: is a right boundary node():

Case 4: is an interior node:

Mathematica files for computing these formulas are available.

References

- [1] Sanjar M Abrarov and Brendan M Quine. Efficient algorithmic implementation of the voigt/complex error function based on exponential series approximation. Applied Mathematics and Computation, 218(5):1894–1902, 2011.

- [2] Sanjar M Abrarov and Brendan M Quine. On the fourier expansion method for highly accurate computation of the voigt/complex error function in a rapid algorithm. arXiv preprint arXiv:1205.1768, 2012.

- [3] Reinaldo B Arellano-Valle and Adelchi Azzalini. On the unification of families of skew-normal distributions. Scandinavian Journal of Statistics, 33(3):561–574, 2006.

- [4] Reinaldo B Arellano-Valle, Márcia D Branco, and Marc G Genton. A unified view on skewed distributions arising from selections. Canadian Journal of Statistics, 34(4):581–601, 2006.

- [5] Reinaldo B Arellano-Valle and Marc G Genton. On the exact distribution of the maximum of absolutely continuous dependent random variables. Statistics & Probability Letters, 78(1):27–35, 2008.

- [6] Adelchi Azzalini and Antonella Capitanio. The skew-normal and related families, volume 3. Cambridge University Press, 2014.

- [7] Volker Barthelmann, Erich Novak, and Klaus Ritter. High dimensional polynomial interpolation on sparse grids. Advances in Computational Mathematics, 12(4):273–288, 2000.

- [8] Zdravko I Botev. The normal law under linear restrictions: simulation and estimation via minimax tilting. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 79(1):125–148, 2017.

- [9] Achi Brandt. Multi-level adaptive solutions to boundary-value problems. Mathematics of computation, 31(138):333–390, 1977.

- [10] Stefano Castruccio, Raphaël Huser, and Marc G Genton. High-order composite likelihood inference for max-stable distributions and processes. Journal of Computational and Graphical Statistics, 25(4):1212–1229, 2016.

- [11] James W Cooley and John W Tukey. An algorithm for the machine calculation of complex fourier series. Mathematics of computation, 19(90):297–301, 1965.

- [12] Peter Craig. A new reconstruction of multivariate normal orthant probabilities. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 70(1):227–243, 2008.

- [13] Clément Dombry, Marc G Genton, Raphaël Huser, and Mathieu Ribatet. Full likelihood inference for max-stable data. arXiv preprint arXiv:1703.08665, 2017.

- [14] Matteo Frigo and Steven G Johnson. Fftw: An adaptive software architecture for the fft. In Acoustics, Speech and Signal Processing, 1998. Proceedings of the 1998 IEEE International Conference on, volume 3, pages 1381–1384. IEEE, 1998.

- [15] Walter Gautschi. Efficient computation of the complex error function. SIAM Journal on Numerical Analysis, 7(1):187–198, 1970.

- [16] Marc G Genton. Skew-elliptical distributions and their applications: a journey beyond normality. CRC Press, 2004.

- [17] Marc G Genton, David E Keyes, and George Turkiyyah. Hierarchical decompositions for the computation of high-dimensional multivariate normal probabilities. Journal of Computational and Graphical Statistics, 27(2):268–277, 2018.

- [18] Alan Genz. Numerical computation of multivariate normal probabilities. Journal of computational and graphical statistics, 1(2):141–149, 1992.

- [19] Alan Genz and Frank Bretz. Computation of multivariate normal and t probabilities, volume 195. Springer Science & Business Media, 2009.

- [20] Alan Genz, Frank Bretz, Tetsuhisa Miwa, Xuefei Mi, F Leisch, F Scheipl, B Bornkamp, M Maechler, and T Hothorn. Multivariate normal and t distributions. http://cran. r-project. org/web/packages/mvtnorm/mvtnorm. pdf, 2014.

- [21] Thomas Gerstner and Michael Griebel. Numerical integration using sparse grids. Numerical algorithms, 18(3):209–232, 1998.

- [22] John Geweke. Efficient simulation from the multivariate normal and student-t distributions subject to linear constraints and the evaluation of constraint probabilities, 1991.

- [23] Leslie Greengard, Denis Gueyffier, Per-Gunnar Martinsson, and Vladimir Rokhlin. Fast direct solvers for integral equations in complex three-dimensional domains. Acta Numerica, 18:243–275, 2009.

- [24] Leslie Greengard and June-Yub Lee. Accelerating the nonuniform fast fourier transform. SIAM review, 46(3):443–454, 2004.

- [25] Leslie Greengard and Vladimir Rokhlin. A fast algorithm for particle simulations. Journal of computational physics, 73(2):325–348, 1987.

- [26] Leslie Greengard and Vladimir Rokhlin. A new version of the fast multipole method for the laplace equation in three dimensions. Acta numerica, 6:229–269, 1997.

- [27] Wolfgang Hackbusch. A sparse matrix arithmetic based on -matrices. part i: Introduction to -matrices. Computing, 62(2):89–108, 1999.

- [28] Wolfgang Hackbusch. Multi-grid methods and applications, volume 4. Springer Science & Business Media, 2013.

- [29] Wolfgang Hackbusch and Boris N Khoromskij. A sparse -matrix arithmetic. Computing, 64(1):21–47, 2000.

- [30] Vassilis Hajivassiliou, Daniel McFadden, and Paul Ruud. Simulation of multivariate normal rectangle probabilities and their derivatives theoretical and computational results. Journal of econometrics, 72(1-2):85–134, 1996.

- [31] Kenneth L Ho and Leslie Greengard. A fast direct solver for structured linear systems by recursive skeletonization. SIAM Journal on Scientific Computing, 34(5):A2507–A2532, 2012.

- [32] Kenneth L Ho and Lexing Ying. Hierarchical interpolative factorization for elliptic operators: differential equations. Communications on Pure and Applied Mathematics, 69(8):1415–1451, 2016.

- [33] Kenneth L Ho and Lexing Ying. Hierarchical interpolative factorization for elliptic operators: integral equations. Communications on Pure and Applied Mathematics, 69(7):1314–1353, 2016.

- [34] Till Moritz Karbach, Gerhard Raven, and Manuel Schiller. Decay time integrals in neutral meson mixing and their efficient evaluation. arXiv preprint arXiv:1407.0748, 2014.

- [35] Michael P Keane. 20 simulation estimation for panel data models with limited dependent variables. 1993.

- [36] June-Yub Lee and Leslie Greengard. The type 3 nonuniform fft and its applications. Journal of Computational Physics, 206(1):1–5, 2005.

- [37] Christian Meyer. Recursive numerical evaluation of the cumulative bivariate normal distribution. arXiv preprint arXiv:1004.3616, 2010.

- [38] Tetsuhisa Miwa, AJ Hayter, and Satoshi Kuriki. The evaluation of general non-centred orthant probabilities. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 65(1):223–234, 2003.

- [39] Fabio Nobile, Raúl Tempone, and Clayton G Webster. A sparse grid stochastic collocation method for partial differential equations with random input data. SIAM Journal on Numerical Analysis, 46(5):2309–2345, 2008.

- [40] Ioannis Phinikettos and Axel Gandy. Fast computation of high-dimensional multivariate normal probabilities. Computational Statistics & Data Analysis, 55(4):1521–1529, 2011.

- [41] James Ridgway. Computation of gaussian orthant probabilities in high dimension. Statistics and computing, 26(4):899–916, 2016.

- [42] Jie Shen and Haijun Yu. Efficient spectral sparse grid methods and applications to high-dimensional elliptic problems. SIAM Journal on Scientific Computing, 32(6):3228–3250, 2010.

- [43] Alec Stephenson and Jonathan Tawn. Exploiting occurrence times in likelihood inference for componentwise maxima. Biometrika, 92(1):213–227, 2005.