Insider Trading with Penalties

Abstract

We consider a one-period Kyle (1985) framework where the insider can be subject to a penalty if she trades. We establish existence and uniqueness of equilibrium for virtually any penalty function when noise is uniform. In equilibrium, the demand of the insider and the price functions are in general non-linear and remain analytically tractable because the expected price function is linear.

We use this result to investigate the trade off between price efficiency and “fairness”: we consider a regulator that wants to minimise post-trade standard deviation for a given level of uninformed traders’ losses. The minimisation is over the function space of penalties; for each possible penalty, our existence and uniqueness theorem allows to define unambiguously the post-trade standard deviation and the uninformed traders’ losses that prevail in equilibrium.

Optimal penalties are characterized in closed-form. They must increase quickly with the magnitude of the insider’s order for small orders and become flat for large orders: in cases where the fundamental realizes at very high or very low values, the insider finds it optimal to trade despite the high penalty. Although such trades –if they occur– are costly for liquidity traders, they signal extreme events and therefore incorporate a lot of information into prices.

We generalize this result in two directions by imposing a budget constraint on the regulator and considering the cases of either non-pecuniary or pecuniary penalties. In the first case, we establish that optimal penalties are a subset of the previously optimal penalties: the patterns of equilibrium trade volumes and prices is unchanged. In the second case, we also fully characterize the constrained efficient points and penalties and show that new patterns emerge in the demand schedules of the insider trader and the associated price functions.

1 Introduction

This paper derives and uses analytical results about a one-period Kyle (1985) model with non-Gaussian noises and penalties associated with insider trading. The natural benchmark for such a framework is a one-period Kyle model with non-Gaussian noise and without penalties. Characterizing the benchmark equilibrium is useful in order to study the more general case with penalties.

Rochet and Vila (1994) have studied this problem under the assumption that the informed trader is able to observe the noise trader’s demand and can therefore condition its order to this demand. In that context, they show existence and uniqueness of equilibrium regardless of the distributional assumptions on the noises. Unfortunately, their approach does not allow in general to construct explicitly the equilibrium. Furthermore, it does not seem possible to replicate their result in the presence of penalties.555In Rochet and Vila (1994), the proof of existence and uniqueness relies on the fact that equilibrium price functions are optimal price functions in the sense that they minimise the expected insider gains’ functional. This property holds true because they can write the chain of equivalences equilibrium optimal price function, where is the aggregate order. With a penalty , the central link breaks down, because then the first order condition of the insider’s program combined with the price efficiency condition yields . But allowing for penalties on insider trading is crucial for our purpose. Indeed, we want to understand how a regulator can trade off efficiently between information incorporation and protection of liquidity traders, and how he can slide along the efficient choices depending on the weights he attributes to these two conflicting objectives.

Bagnoli, Viswanathan, and Holden (2001) study different models of market making with one or several strategic agents without the assumption of normality and without hypothetizing that strategic agents can observe the noise traders’ demand. A one-period Kyle model with one strategic trader and non-Gaussian noise is a particular instance of their analysis. Their results imply that in that case, when the distribution of the noise equals in law a linear transformation of the fundamental, a linear equilibrium exists. In this equilibrium, the demand of the IT has the same distribution as the demand of the NT, what we call a mimicking property.666We provide a discussion in Appendix C. Bagnoli, Viswanathan, and Holden (2001) only focus on linear equilibria. When adding an arbitrary penalty function to the model, one can no longer expect to have linear equilibria, and there is a priori no method to construct equilibria explicitly in a systematic manner.

We use a setup that remains tractable after the introduction of any penalty function — at the cost of a distributional assumption. We find that uniform noise has the property that even though the IT demand function and the price function are non-linear, the expected price function is linear, whatever the penalty . The equilibrium demand then simply appears as the maximiser of a known objective. We obtain uniqueness of the equilibrium among virtually all strategies for any penalty as a simple corollary of our analysis. By contrast, proving a general uniqueness result for the one-period Kyle model with Gaussian noise without penalty was an extremely involved mathematical problem which was only addressed almost thirty years after the Kyle (1985) seminal paper (Boulatov, Kyle, and Livdan (2013), McLennan, Monteiro, and Tourky (2017)).

2 The Model

As in the one-period version of Kyle (1985), the model features a risk-neutral insider trader (IT), noise traders (NT) and competitive market makers (MM). Agents are trading an asset with fundamental value . The IT perfectly observes and places an order . NT have a stochastic demand independent of . MM observes the total demand and executes orders at a price such that she breaks even on average.

The first difference of our model with Kyle (1985) is that we consider uniform – instead of Gaussian – noises:

The choice of as the support is for clarity and without loss of generality; one could equivalently assume and with and : see Appendix A.1.

The second difference is that a regulator may decide to penalize trades of size by a cost . We interpret as a product : is the exogenous probability that the regulator starts and successfully completes an investigation, while is the cost imposed to the IT conditional on the investigation being successful and the order of the IT being . Success of the investigation means that the regulator correctly identifies the order of the informed trader and gathers sufficient evidence to enforce payment of the corresponding fine. In other cases, the IT can not be constrained to pay any fine. Under these assumptions, the regulator never makes type 1 errors (never convicts a trader that didn’t use insider information) but can make type 2 errors (not convicting a trader that did use insider information).

2.1 The Insider Trader’s Problem

2.1.1 Benchmark Equilibrium without Penalties

In the absence of penalties, the IT solves

| (1) |

taking the price function of the MM as given. The MM breaks even on average:

| (2) |

From the discussion in section 1, defined by

| (3) | |||||

| (4) |

is an equilibrium of the one-period Kyle model without penalty. We refer to it as the (linear) mimicking equilibrium. Indeed, and are equal in distribution. Notice that the image of is . We will prove later that this equilibrium is unique among all equilibria featuring a non-decreasing demand whose image lies in .

With penalties, the optimal demand is no longer mimicking the random demand . One intuitive interpretation is that while mimicking allows the IT to best conceal herself from the market maker, she can’t hide from the regulator (in case investigation is open and succeeds). This leads to a lower demand than in the case without penalties. We now define formally the equilibrium with penalties.

2.1.2 One-Period Kyle Model with Penalties

The IT solves

| (5) |

taking the price function of the MM as given. The MM breaks even on average:

| (6) |

This game involving the IT and the MM is denoted . An equilibrium of is a pair such that solves (5) and satisfies (6).

The interval in the maximisation program (5) is the set of admissible insider’s demand. In order to be able to prove uniqueness, we make the following assumption:

Assumption 1

The bounds of are those that obtain in the linear mimicking equilibrium when there is no penalty function. They are therefore natural: a demand function whose image is not contained in would imply that for some values of the fundamental , the magnitude of the IT order is higher when there is a penalty, compared to the linear equilibrium without penalty.777At present, we do not know whether an equilibrium featuring such a demand function can exist.

To conclude this section, we state two remarks and introduce some notation.

(i) The data of a strategy implies a pricing function via equation (6). That is, if is part of an equilibrium, then the pricing function must be given by . We denote the pricing function associated with a demand schedule by .

(ii) In the IT’s maximisation program (5), the pricing function only intervenes through the expected price function, denoted and defined by

| (7) |

represents the price that the risk-neutral IT will face on average if she places an order . The program (5) can be rewritten in terms of the expected price function only:

| (8) |

2.1.3 Out-of-Equilibrium Pricing

The noise we consider has bounded support. Moreover, the discussion above indicates that the equilibrium demand functions we will consider satisfy . This means that the aggregate order, belongs to a bounded set . The conditional expectation in (6) is not defined for values of , meaning that we must make an assumption on the out-of-equilibrium pricing of the MM:

Assumption 2

For any equilibrium of we consider, with non-decreasing and , we always impose the following out-of-equilibrium pricing (letting ):

This assumption states that when the MM observes a positive aggregate order larger than its maximal possible equilibrium size, she prices the asset as if it had realized at its maximal value, . Similarly, when the aggregate order is negative with a magnitude larger than the maximal possible equilibrium size, the MM prices as if . When constructing equilibria, we do not always recall that Assumption 2 is used to define the out-of-equilibrium pricing. When verifying that is an equilibrium, one must not only check that maximises the IT’s program (5) among all in the candidate support , but also among values of in . For these values of , the aggregate order realizes in the out-of-equiibrium region with positive probability, in which case Assumption 2 defines the price .

Finally, notice that Assumption 2 fully characterizes out-of-equilibrium pricing: indeed, any belongs to the support of , since is and .

2.1.4 A first example

We now present an example of an equilibrium of . More illustrations can be found in section 3.4, where we discuss the intuitions behind some typical behaviours of the equilibrium demand and price functions in the presence of penalties.

Let and

Under this penalty function, the insider trader undergoes an expected sanction of if she trades. This example is particularly important because we will see that such penalty functions are among the optimal regulations.

We will show that is an equilibrium, where

| (9) |

As we will see, the price function is non-linear but the expected price function satisfies . Hence, the IT maximises under the same expected price function as in the linear mimicking equilibrium. Facing an expected price identical to the one without penalties, the IT only trades when its previously optimal strategy — the linear mimicking demand — allows her to recoup the penalty on average. Without penalties, the profit of the IT when she observes a fundamental is . With a constant penalty upon trading equal to , the IT does not trade as long as . When , the IT considers as a sunk cost and optimizes as if there was no penalty, thus selecting . Notice that the demand function is non-linear and exhibits a jump at .

2.1.5 Indistinguishable Equilibria

In the equilibrium of the example above, the IT would earn the same profit upon observation of by selecting or : zero in both cases. In general, when the penalty function exhibits jumps, we should expect the existence of such indifference points. At these points, the IT can achieve a given profit by placing a small order and undergoing a small expected sanction or by placing a larger order, associated with a larger expected penalty. However, as long as the set of such that the maximisation program of the IT (5) admits several solutions has measure zero, these indifference points will almost surely not be reached. The equilibrium will therefore be independent of the choice of the maximiser , in the sense that any ex post model observable is almost surely the same — e.g. demand of the IT , observed price — and any ex ante model quantity — such as the IT expected profit or the expected penalty collected from the IT — is the same. In that case, we wish to consider that any choice of maximiser induces the same equilibrium. We formalize this by introducing an equivalence relation between equilibria that we call indistinguishability.

Assume that and are two solutions of the IT’s maximisation program (5) and agree outside of a countable set. In that case, . This means that if is an equilibrium then so is . This leads us to the following definition.

Definition 1

Let and be two equilibria of . We say that and are indistinguishable if and agree outside of a countable set. Indistinguishability defines an equivalence relation over the set of equilibria of .

2.2 The regulator’s problem

In our model, the regulator is concerned about two quantities:888 In section 5.2, the regulator additionally needs to take care of the expected fine she collects for budget reasons. (i) the post-trade standard deviation of the fundamental, and (ii) the P& L of the uninformed traders:

| (10) |

Quantity (i) matters because one would like to have informative prices: when (i) is small, the residual uncertainty about is also small. Quantity (ii) captures the willingness of the regulator to have liquid markets. In a liquid market, agents who have to trade for non-fundamental reasons do not experience high losses. This corresponds to a situation where is not too negative. The core issue is that improving upon criterion (i) generally causes criterion (ii) to worsen.

Let

| (11) |

be the expectation of the post-trade standard deviation of and

| (12) |

denote the expected P& L of the NT.

The objective of the regulator can now be stated as the characterization of the efficient frontier, with the following definition:

Definition 2

(i) A point is implementable if it is the outcome of an equilibrium of for some admissible penalty .

(ii) An implementable point is dominated by if is implementable and , with at least one strict inequality.

(iii) The set of implementable non-dominated points is called the efficient frontier.

In section 5.2, we will need the following refinement of (ii):

(ii’) An implementable point belonging to some subset of the plane is dominated in by if is implementable, , with at least one strict inequality and .

Points outside the efficient frontier are irrelevant from the regulator’s perspective, as she can improve upon one of his objectives without harming the other one. By contrast, any point belonging to the efficient frontier could be picked by a regulator for a suitable weighting999Not necessarily linear. of the objectives. Our goal is to characterize the efficient frontier and the penalties that implement it.

2.3 Admissible penalty functions

We do not impose any restriction on the penalty function, except that it only depends in a non-decreasing manner on the magnitude of the order of the insider trader, and that there is no sanction when she does not trade.

Definition 3

is a penalty function if it is symmetric and non-decreasing, left-continuous over and satisfies . The set of penalty functions is denoted .

The class is very general and defined by economically relevant requirements. In particular, it would be unnatural and perhaps politically hard to implement to impose a higher sanction on a smaller trade. The left-continuity assumption simply makes sure that the supremum of the possible profits is attainable.

3 Existence and uniqueness of equilibrium for

In this section, we set out to prove the following Theorem:

Theorem 4

For any , the Kyle game with penalty function admits a unique equilibrium .101010Recall that equilibria are identified with their equivalence class, see Definition 1 . In general, and are non-linear.

One consequence of this result is that for each , the regulator’s quantities of interest are defined unambiguously as the outcomes of the unique equilibrium in . In particular, the efficient frontier is defined unambiguously.

3.1 Analysis of the expected price function

3.1.1 Under uniform noises, the expected price function is linear regardless of the IT demand

Lemma 1 contains the key observation at the root of our analysis. Recall that for any odd non-decreasing function , we denote by the pricing function associated with (equation (6)) and given , is the expected price function (equation (7)): is the price that the IT will face on average if she places an order .

Lemma 1

Let be an odd non-decreasing function, and . The expected price function is linear on :

Lemma 1 is crucial because it makes the surprising statement that the expected price function that must prevail in equilibrium is without requiring any knowledge: neither the form of nor guesses about or are needed.

In turn, this implies that the equilibrium demand of the IT, , must be a maximiser of

| (13) |

as the IT maximises its expected profit knowing that . This demand induces some price function . Remark that, again by Lemma 1, the expected price indeed satisfies . This indicates that is an equilibrium of

While this discussion provides the intuition on how we construct the equilibrium of for an arbitrary , several technical issues must be addressed in order to make the argument formal. One must check that any selection of maximiser is non-decreasing and take care of the out-of-equilibrium pricing: notice in particular that Lemma 1 only characterizes over , while we need to compute the IT’s expected profit for all admissible demands . Additional results are also required to establish uniqueness of he equilibrium of . The main step in that direction is to show that admits a unique maximiser except for a countable number of values of (section 3.2).

We now provide the proof of this lemma. Section 3.1.2 clarifies the main intuitions.

Proof of Lemma 1. We use the notation for a density and for a conditional density. Write

That is, for , is uniform over

| (14) | |||||

where

and only disagree when there is such that and is locally constant at , i.e. they agree outside of a countable set. Then, letting ,

Now since

by differentiation it is enough to show that a.e.. Using the expression of found above, we obtain that for :

a.e.. This is because a.e., , and .

Having identified , we know that the insider trader’s problem is to maximise as defined in (13). Because we will use this function throughout the paper, we repeat its definition here:

Definition 5

The insider’s expected profit (under the correct expected price function ) for a demand when the fundamental value is is

| (15) |

Notice that is an “expected” profit because we interpret as an average cost —an investigation may not be started or not succeed— while is an expected price because the realization of is random and the realized price is .

3.1.2 Intuition

In order to isolate the intuition behind Lemma 1, let us consider the case where is continuous and strictly increasing.

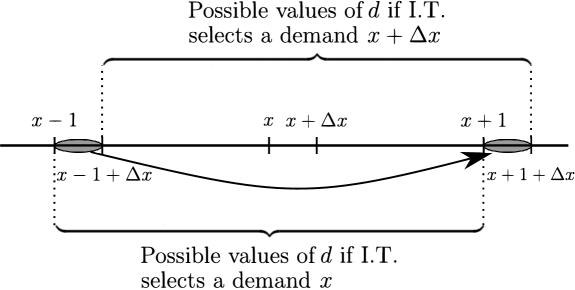

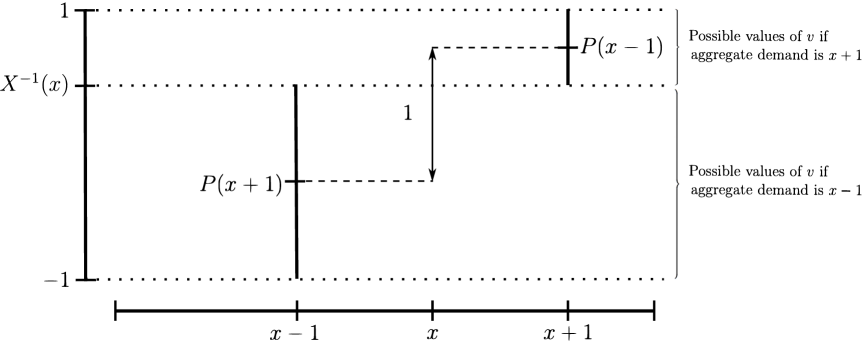

Assume that the market maker observes an aggregate order . Since the demand of the noise traders takes values in , the possible demands of the IT consistent with the observation of are exactly the admissible demands such that . Because admissible demands satisfy and , the information obtained by the market maker when she observes is that . Thus, she knows that . Intuitively, the fact that the aggregate order is positive rules out extreme negative values of and the MM deduces a lower bound on , .

Moreover, due to the uniform noise assumption, all values of above this lower bound are equally likely. Therefore, the price is given by the midpoint of the interval .

In a similar manner, when , the price is given by the midpoint of the interval .

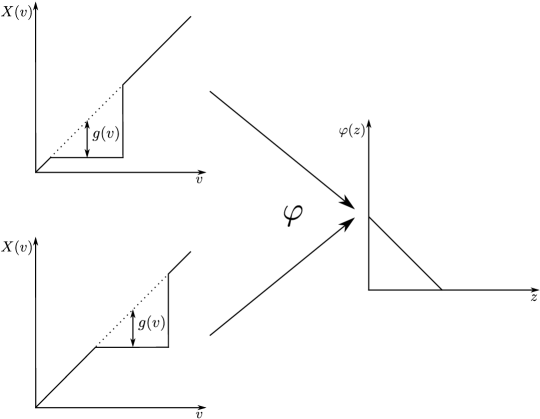

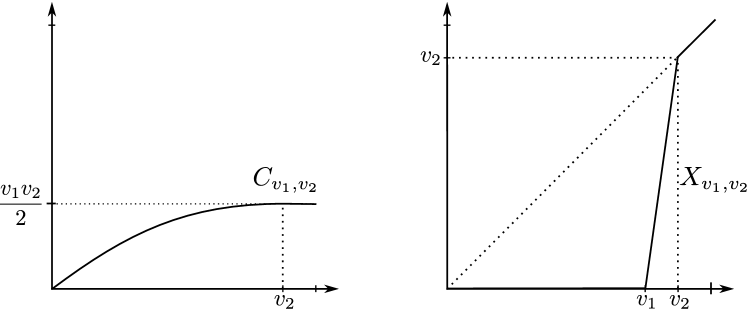

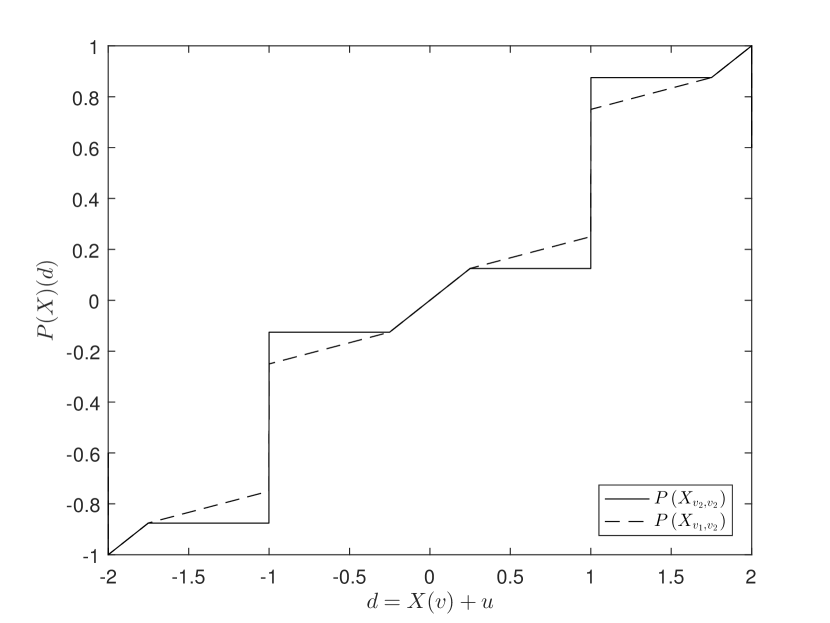

Now, assume that the IT wants to place an order . The IT is only concerned by the expected price impact, , which is a uniform average of the over , the set of possible aggregate demands given an IT demand . If, instead, the IT decides to place an order , the set of possible aggregate demands is : see Figure 1.

Thus, the only contribution to the marginal increase in expected price is due to the fact that the weight that was attributed to the interval is now attributed to the interval . Crucially, this weight is the same due to the uniform noise assumption. Considering a vanishing , one concludes that the marginal impact of increasing demand on expected price is proportional to .

We have seen above that is the midpoint of , and that is the midpoint of . Therefore, the marginal impact on the expected price is proportional to the distance between these two midpoints:

Figure 2 provides an illustration of this result. This shows that the expected price function is linear. Notice that the arguments above rely heavily on the uniform noise assumption: with other noises, one cannot expect in general to have a linear expected price function.

3.2 Candidate optimal demands are unique up to changes on a countable set

In this section, we set out to obtain an unambiguous definition of the strategy that will be our maximiser.

Definition 6

Let , be two intervals of . A correspondence is non-decreasing if for any in , .

Notice that if is a one-to-one mapping, then we recover the usual notion of a non-decreasing function.

Lemma 2

Let be a non-decreasing correspondence. Then for all in except on a countable set, is a singleton.

Proof. The argument is the same as for the proof that a non-decreasing function has at most a countable number of discontinuities.

For a given penalty , let be the correspondence mapping to the set of maximisers of the insider trader’s profit function when she observes a realization of the fundamental:

Recall that is defined in (15).

Lemma 3

For any , , and is a non-decreasing correspondence.

Proof. First, let us show that is never empty. Let , the function has a finite upper bound as . Let and such that . There is an extraction of , still denoted , such that converges to and either (i) is increasing or (ii) is decreasing. By symmetry, we can assume without loss of generality that or and the case holds. Let us first consider case (i). Since is left-continuous and is continuous, converges to : therefore and . Let us now consider case (ii). Since is non decreasing, it has a right limit at denoted by which is greater than . Taking the limit in the definition of , the value of converges to . Using the fact that converges to , we conclude that and .

Now, let us show that is a non-decreasing correspondence. Let in and and . For any :

Using the fact that and , for any ,

By definition, , thus . Since this inequality holds for any and , we get that : the correspondence is non-decreasing.

The combination of Lemmas 2 and 3 ensures that the maximiser of the IT’s expected profit is unique except for a countable number of values of :

Lemma 4

There exists a non-decreasing function such that for all except on a countable set,

All such agree outside of a countable set.

As we identify equilibria in a same equivalence class, as introduced in Definition 1, we do not need to specify which particular we consider: we can unambiguously talk about “a maximiser” of the expected profit. We are now ready to derive the main result of this section.

3.3 Existence and uniqueness of the equilibrium of

We recast the statement of Theorem 4 by indicating what the equilibrium optimal demand is:

Let and be a maximiser of . Then is an equilibrium of . This is the unique equilibrium among the pairs such that is non-decreasing.

Proof of Theorem 4. From Lemma 1, for . Since is a maximiser of , is an optimal response to the expected price function among all . To confirm that is an equilibrium, we need to check what happens if the IT makes a choice outside of the candidate support , knowing that the out-of-equilibrium pricing is defined by Assumption 2. Consider for instance the case , as the case is identical by symmetry. Then

| (16) | |||||

This is because when , and so from (14), is uniform over and .

As maximises , and for , maximises over : is an equilibrium.

We now prove uniqueness. Let be a non-decreasing strategy of the IT. By Lemma 1, the expected price associated with is for . But the computation of outside of is the same as the computation of in (16). Hence, for all . So, if is an equilibrium of such that is non-decreasing, and maximise the same objective over . Since the maximisers agree outside of a countable set, so do and . In turn, we have . Hence, and are the same equilibrium, which establishes uniqueness.

3.4 Examples of equilibria

In this section, we use Theorem 4 in order to understand how the presence of penalties affects the trading strategy of the IT and the pricing function.

Consistent with intuition, penalties reduce the demand of the IT. By how much is reduced depends on the functional form of the cost and the realisation of . This leads in general to a non-linear demand schedule. In the following examples, we will illustrate some important determinants of the IT demand.

The price function can be very flat in some regions and increase sharply in others. In particular, the price impact of a marginal uninformed trade strongly depends on both the realisations of and . By constrast, in the mimicking equilibrium of the model without penalties, this price impact is constant, regardless of the distributional assumptions on the noise.

We consider three examples of penalty: quadratic, linear, and constant over large trades.

3.4.1 Quadratic cost

In this very particular instance, remains linear after the introduction of the penalty. Imposing quadratic costs is akin to increasing the perceived expected price impact. Since this cost is in while the gross gains of trading are in , the IT always trade as soon as , and the magnitude of the trade increases with the absolute value of . Note that the result that is linear can also obtain in a one-period Kyle model with Gaussian noises when one makes one of the following assumptions: (i) there is a quadratic penalty on trading, (ii) the insider is risk-averse instead of risk-neutral, (iii) the insider observes a signal imperfectly correlated with instead of observing directly.

![[Uncaptioned image]](/html/1809.07545/assets/x3.png)

![[Uncaptioned image]](/html/1809.07545/assets/x4.png)

, . Left panel: IT demand . Right panel: price function .

Due to the presence of the penalty, the insider trades less than in the linear mimicking equilibrium, so that ( in this example).

When , any demand of the IT is compatible with the observed aggregate order, so all values remain equally likely, as explained in section 3.1.2. No information is incorporated and the price remains at the initial expected value of the asset: 0. When , one knows that has not realized at a very low value. This provides a lower bound on and the price becomes positive. As increases, so do the lower bound and the price, until . In that case, one knows for sure that the IT has placed an order , which means that , and reaches 1. The situation is symmetrical for values of below .

3.4.2 Linear cost

When the penalty is linear, , the maximisation program of the IT can be rewritten as

If , one sees that a linear cost has the same effect as reducing the value of the fundamental by an amount , and having no cost. Therefore, the strategy of the IT for values is a translation of the linear mimicking strategy over . Similarly, the strategy of the IT for values is a translation of the linear mimicking strategy over . This creates the two increasing linear segments in the left panel of Figure 4. In the flat middle section, is not sufficient to cover the expected penalty and the IT does not trade.

![[Uncaptioned image]](/html/1809.07545/assets/x5.png)

![[Uncaptioned image]](/html/1809.07545/assets/x6.png)

, . Left panel: IT demand . Right panel: price function .

The price function depicted in the right panel of Figure 4 exhibits a flat section in the center surrounded by increasing linear segments. The intuition is exactly the same as in the quadratic penalty case: when the magnitude of is small (), all values of remain (equally) possible and no information is incorporated. As grows, a lower bound on can be deduced and the price increases. The key difference with the quadratic penalty case is that the price function jumps at . Indeed, when , the market maker knows for sure that the insider has placed a positive order. But the IT only does so when . By contrast, if , remains possible, so we can only deduce that . In terms of information incorporation, there is a huge difference between and .

3.4.3 Constant cost on trades of magnitude larger than

Absent penalties, the IT picks . Hence, if she is sanctionned only for trades of magnitude larger than , she will not change her demand as long a : this corresponds to the increasing linear section in the middle of Figure 5. For intermediate values of , the IT prefers to block her demand at the value (or ) in order to avoid the penalty: this corresponds to the flat sections in Figure 5. When becomes large enough (), the penalty is recouped in expectation by using the strategy that prevails in the absence of costs: it appears as a sunk cost and the IT selects again the demand . This corresponds to the increasing linear sections at the left and right of Figure 5.

![[Uncaptioned image]](/html/1809.07545/assets/x7.png)

![[Uncaptioned image]](/html/1809.07545/assets/x8.png)

, , .

Left panel: IT demand . Right panel: price function .

The price function jumps at and . The intuition is as in the linear penalty case. When exceeds , the MM knows that the demand of the IT was larger than which rules out all values of at the left of , the left jump of . Similarly, when exceeds , the MM knows that the demand of the IT was larger than , which rules out all values of at the left of , the right jump of .

A robustness exercise in the case of Gaussian noise is conducted in Appendix B.1 and shows that most of the effects described above qualitatively subsist.

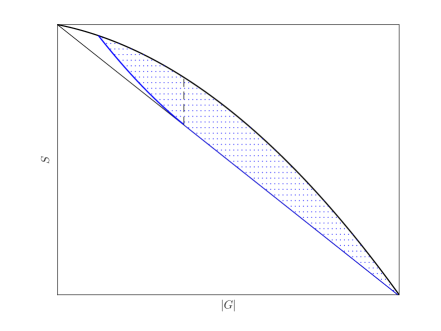

4 Efficient frontier without a budget constraint

We now solve the regulatory problem laid out in section 2.2 by proving the following theorem:

Theorem 7

The equation of the efficient frontier is

The set of regulations that implements the efficient frontier is exactly the class defined as

| (17) | |||||

When , the demand of the insider writes

for the associated with .

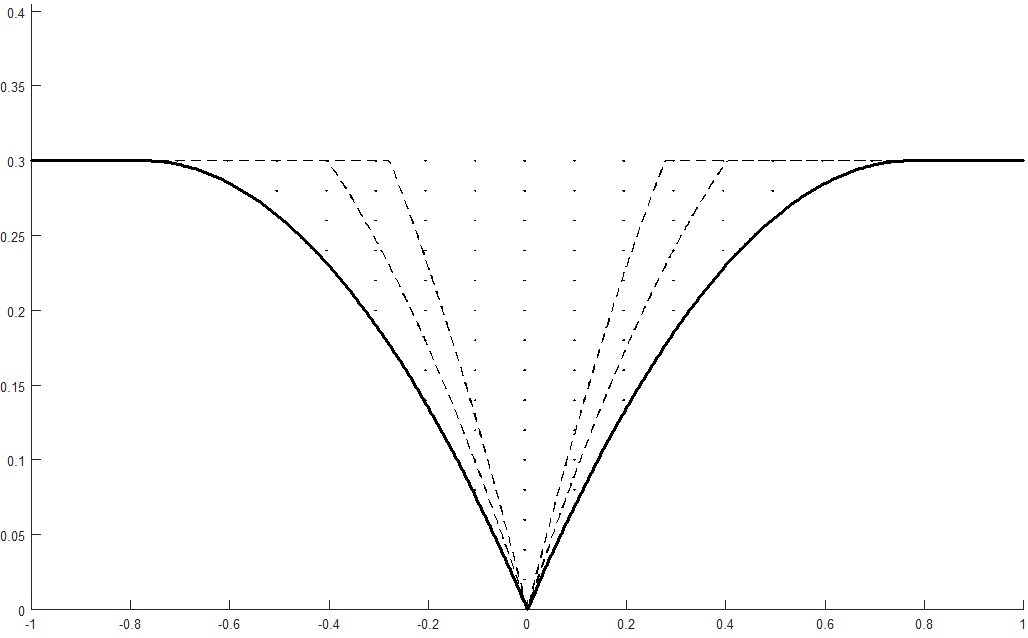

Figure 6 gives a graphical representation of functions in .

If two penalties in are associated with the same , they implement the same demand schedule . Moreover, it is easy to see that any point in the efficient frontier is implemented by for exactly one value of .111111A direct calculation shows that the P& L of the uninformed traders under the demand is . Hence, the value of that implements the point of the efficient frontier is the solution to . Therefore, parametrizes the efficient frontier. Points associated with a small (resp. large) are selected by a regulator who puts more weight on information incorporation (resp. on restricting the uninformed traders’ losses).

Any regulator that puts nonzero weight on both objectives must at least somewhat reduce insider trading, but not totally. As we shall detail later, the optimal solution is to allow some large trades for large realisations of , because they incorporate a lot of information; more precisely, the regulator wants to implement for large values of . The cutoff point in the schedule then appears as the solution to the equation (Recall that is the profit of the IT when there is no penalty). This characterizes the magnitude of above which the penalty appears as a sunk cost to the insider, who then effectively optimizes as if there was no penalty and selects the mimicking demand .

With noise and with and , one can conduct a similar reasoning. By identifying the points where the mimicking strategy exactly compensates for the penalty , we find that the cutoff points become

Moreover, the maximal we need to consider is the smallest one that suppresses net profits even at the extreme realizations ; so is now varying in the interval . Details can be found in Appendix A.1.

The thick line represents the lower bound in the definition of when (then, ) : any penalty in must be above this line. Given that a penalty is symmetrical and non-decreasing over , the graph of a function in must be included in the dotted area. The two dashed lines represent two such functions.

4.1 Preliminary results on the regulator’s objective

Before characterizing the efficient frontier, we need to derive some useful formulas.

The expected net profit of the insider trader in state is

| (18) |

Note that in terms of the profit function , the net profit is .

The overall expected net profit (after fine, if any) is

| (19) |

The expected penalty that the insider undergoes is

The overall expected gross profit (before fine, if any) is

| (20) |

Observe that we can write

| (21) |

This way of seeing the expected losses of the uninformed traders as (an affine transformation of) the distance between and the identity will be useful in section 5.1. We continue by providing some convenient expressions of the quantities defined above.

Lemma 5

In equilibrium, the net profits satisfy

| (22) | |||||

| (23) |

Proof. Consider the parametrized objective function

defined in (15). Notice that (i) is linear in and therefore absolutely continuous, (ii) . (i) and (ii) guarantee that the assumptions of Theorem in Milgrom and Segal (2002) are satisfied. In the present case, this theorem tells us that we can write:

since the insider does not make any profit when the fundamental is . Finally,

Lemma 6 expresses the expected post-trade standard deviation as a function of the demand profile . One consequence of this Lemma is that large orders associated with large values of the fundamental are the ones that contribute the most to incorporating information into prices. Indeed, the values of such that the product is large have the strongest negative impact on , as can be seen from (24). This provides intuition on why is the class of optimal penalties: when , the regulator knows that the IT will trade large quantities should realize at a large value because penalties are flat for large . Although costly for the uninformed traders, these orders are those that contribute the most to reducing uncertainty about , making the regulator unwilling to prevent them.

Lemma 6

The expected post-trade standard deviation satisfies

| (24) |

Proof. By the proof of Lemma 1, is uniform over

Since the standard deviation of a uniform variable over equals , Lemma 6 is an immediate consequence of the following result: if is an odd non-decreasing function from to , then the expected length of the interval equals , which we must now prove.

For , define

What we need to prove is that . By symmetry, , thus, it remains to prove that:

Let us consider fixed. The random variable takes values in : using Fubini theorem,

By definition of , if then . Besides, if , then using the fact that is non decreasing, . Thus:

Let us remark that can hold for two different values of if and only if is discontinuous at or . In particular,

It follows from this discussion that :

where is the Lebesgue measure on . Since is non-decreasing, it has a countable number of discontinuity points. In particular and:

Now,

Going back to the expression of , we obtain

Integrating over :

where in line , we used the fact that is odd. This concludes the proof.

4.2 Characterization of the efficient frontier

4.2.1 Shape of the efficient frontier and efficient demand functions

In this section, we give the shape of the efficient frontier and explain what demand schedules are compatible with it. We call these schedules efficient demand functions.

Lemma 7

Let be a penalty function in . In the equilibrium of ,

with equality if and only if there is such that for and for .

Proof. Due to Lemma 6, what we need to show is that

This is equivalent to

or

| (25) |

which holds because for .

For the equality to hold, it is necessary and sufficient to have or almost everywhere. Since is non-decreasing, it is equivalent to for and for , where

Equation (25) is particularly convenient because it immediately indicates what type of demand function is needed to implement the efficient frontier. Of course, is an endogenous outcome: what remains to be seen is what regulations implement the efficient demand functions.

4.2.2 Implementation of the efficient demand functions

Lemma 8

The efficient demand functions derived in Lemma 7 are implemented exactly by the penalties .

By construction, penalties in are flat for large values of and increase quickly as departs from 0 (see Figure 6). Intuitively, this is what is required to implement the efficient demand functions. Indeed, when realizes at a small value, the marginal impact of increasing demand on the expected penalty is large, and the IT prefers to refrain from trading. For large, however, the penalty schedule being flat on large demands, a large order allows to cover the expected fine, which appears as a sunk cost. The IT then optimizes as in the linear mimicking equilibrium and demands . The proof of the Lemma can be found in Appendix A.

4.2.3 Proof of Theorem 7, illustrations and discussions

The proof of Theorem 7 is complete: Lemma 7 characterizes the efficient frontier and due to Lemma 8, achieving the efficient frontier can only be done by selecting a cost , characterized by a .

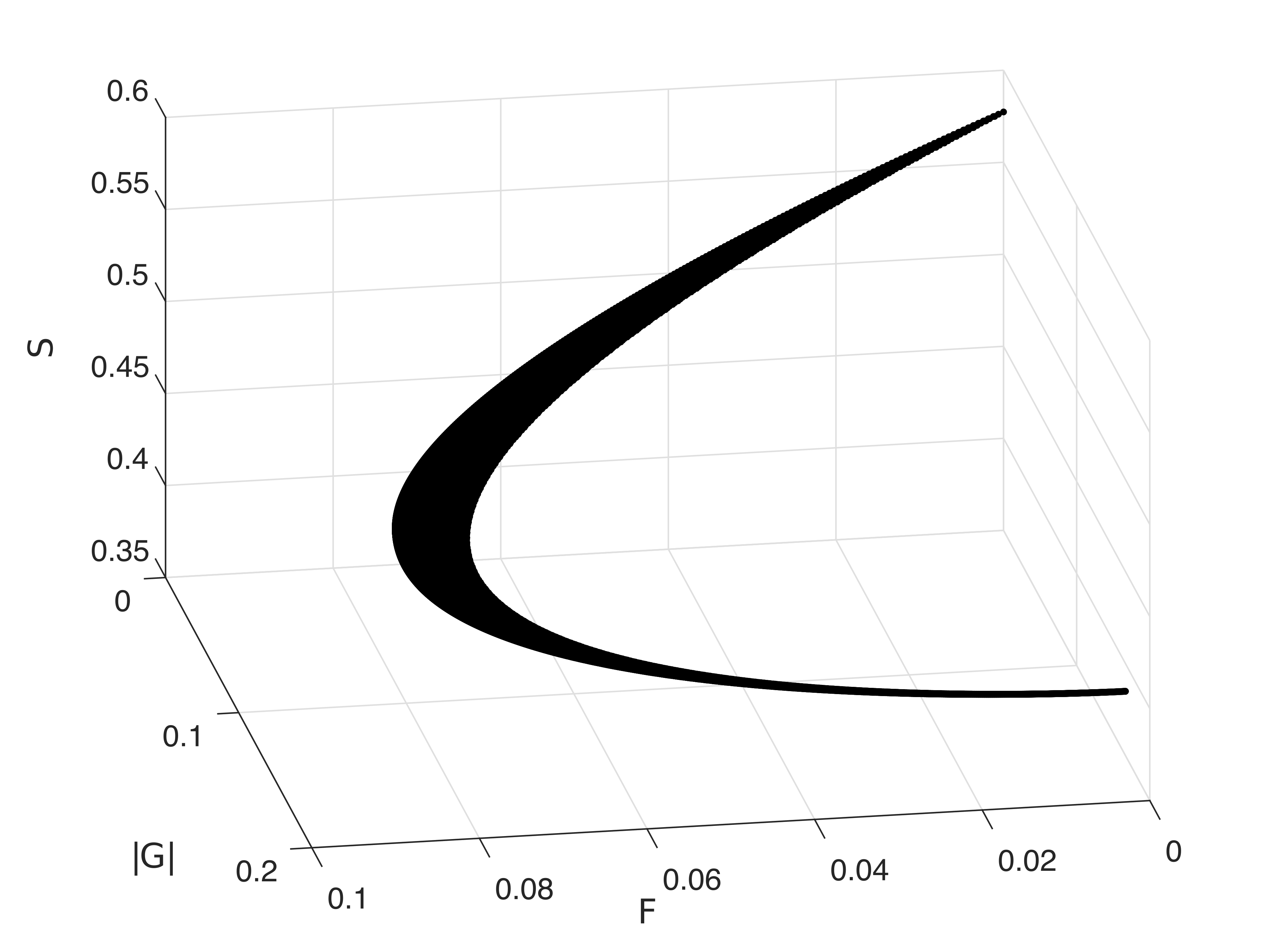

Note that by varying between 0 and , one clearly covers the full efficient frontier. As increases, the losses () of the uninformed traders decrease from to 0, while the expected post-trade standard deviation increases from to .

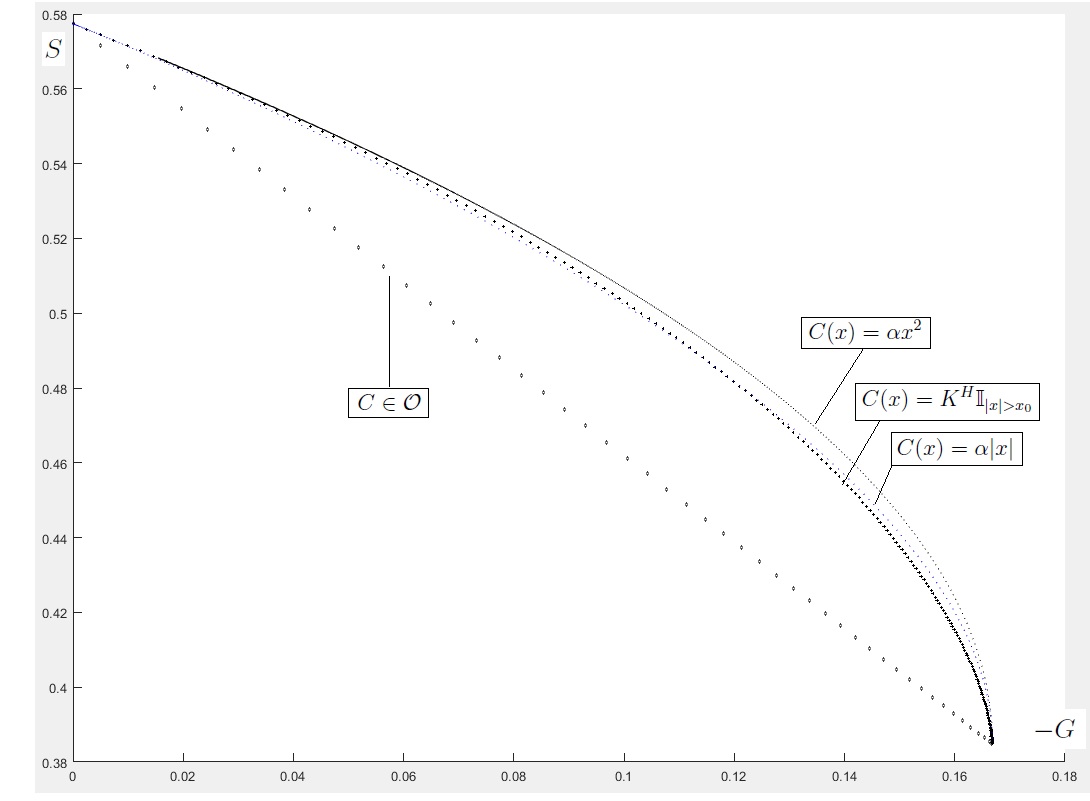

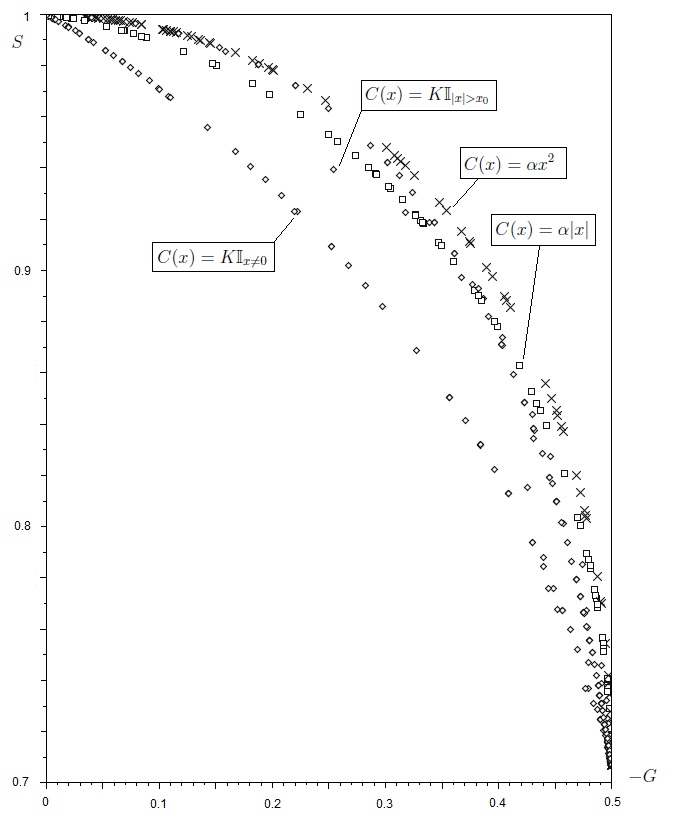

Each point of Figure 7 corresponds to a penalty function ; it represents the outcomes in the unique equilibrium of . The losses of the uninformed traders, , read on the -axis. The expected post-trade standard deviation, , reads on the -axis. For a fixed -coordinate (a fixed ) the preferred option of the regulator is to select a point with the smallest -coordinate (that minimises ).

Consistent with Theorem 7, penalties in achieve the efficient frontier, which is linear as indicated by Lemma 7.

Outcomes corresponding to quadratic and linear penalties (, for varying ) are also reported in Figure 7. As one can see, they perform significantly worse than penalties . This is also the case of penalties with no cost on small trades and big costs on large trades, . Here is a constant large enough so that the insider never chooses to trade more than . The fact that these particular penalty functions perform poorly compared to penalties in is consistent with the intuition given above Lemma 6. Indeed, they imply that for small and for large (the opposite of the demand functions implied by ), so that the reduction of the expected standard deviation, measured by the term (see Lemma 6), is low.

Figure 7 shows that quadratic costs are the most inefficient among the considered costs. In fact, they have the worst performance among all penalty functions:

Proposition 1

Quadratic penalties implement the upper frontier of the locus of outcomes generated by all penalty functions in , i.e. they induce the highest possible expected post-trade standard deviation for a given P & L of the uninformed traders.

Proof. See Appendix A.

5 Efficient frontiers under a budget constraint

So far, by imposing virtually no restriction on the set of admissible penalties, our analysis potentially assumes away a real-world constraint on the regulator: investigation costs. Conducting investigations requires time, financial and human resources. How do the regulator’s efficient policies change in that case?

In section 5.1, we consider the case of non-pecuniary penalties: the regulator cannot balance its budget by collecting fines. This translates into a bound on the investigation probability, which in turn caps the maximal expected penalty that can be imposed an insider trades. In section 5.2, we study pecuniary fines. In that case, the regulator needs to collect at least some fines to balance its budget. This constraint forces the regulator to select “intermediate” levels of penalties: if is too small, not enough fines are collected, but the same holds if is too large, as this induces insider traders to refrain from trading.

5.1 Non-pecuniary penalties

We maintain the assumption that investigation occurs with a constant probability, , leaving the analysis of the case where is a function of an observable (e.g. the aggregate order) for future research. We also suppose that the regulator cannot use fines to relax its budget constraint. This is the case as soon as penalties are non-pecuniary, e.g. an imprisonment sentence.

5.1.1 Setup and Characterization of the efficient frontier

With an investigation cost , since the expected expenses of the regulator are given by , and denoting the alloted budget , we consider the constraint

| (26) |

Note that the insider trader optimizes under an expected penalty schedule , where is the actual sanction conditional on investigation success. Absent a cap on , the regulator could trivially get around its budget constraint by reducing and increasing . We would be back to the case studied in section 4. There are, however, several reasons that justify the existence of a bound on . The first one is simply that the worst possible sanction, say lifetime imprisonment, does not provide utility. Another rationale comes from the fact that the stronger a sanction, the harder it is to implement it, as the legally required amount of evidence increases. For instance, in the Netherlands at the end of the XXth century, a very strong penalization of insider trading was enforced, which actually led to a quasi-impossibility to convict people of insider trading.121212This is documented in SEC (1998). From (26), with a cap on , the insider trader faces an expected penalty

| (27) |

The constraint on , equation (27), means that we now work with a restricted set of admissible penalties:131313 Of course, we could obtain the same constraint by ignoring investigation costs, setting and assuming that the cap on is below 1/2. The idea here is that if investigation was systematic, the bound would likely be non-binding. It only becomes binding because investigation is costly, which reduces the expected penalty that the IT faces. The extent to which it binds depends on the budget-relevant parameters and : see (27).

Definition 8

In the non-pecuniary case, the set of admissible penalties with a budget constraint is

Note that is equivalent to (27) because any penalty in is symmetrical and non-decreasing over . Moreover, the budget constraint is an actual constraint for ; for , .

What happens when one restricts the set of admissible penalties? First, some previously efficient points may no longer be feasible. Second, some points that were not previously efficient may no longer be dominated by any point still implementable under the budget constraint. We recast Definition 2 in this new setting:

Definition 9

In the non-pecuniary case, the efficient frontier under a budget constraint is the set of points implementable by a penalty in that are not dominated by any point implementable by a penalty in .

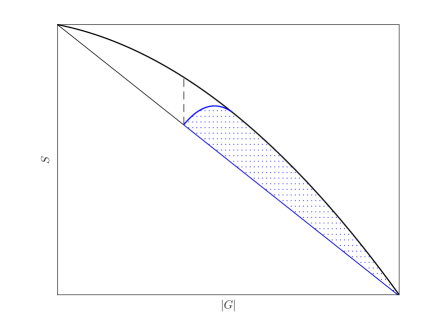

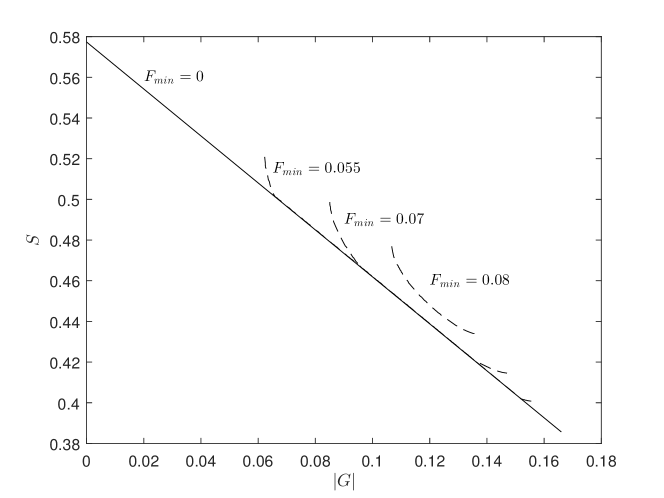

As discussed above, the introduction of a constraint on the set of admissible penalties should in general make new efficient points appear. Consider for instance the situation depicted in panel (a) of Figure 8. The dotted region represents the set of feasible points under the constraint. Points of the previously efficient frontier (oblique straight line) at the right of the dashed line are still feasible and therefore still efficient. Those at the left on the dashed line are not implementable anymore. The lower frontier of the blue area is the new efficient frontier. In particular, new efficient points appear at the left of the dashed line.

By contrast, in panel (b), there are no feasible points at the left of the dashed line: the efficient frontier is truncated.

It is a priori quite unclear in which situation we are. Denote

is the set of efficient penalties derived in section 4.2.2, that are still feasible under the budget constraint. These penalties are still efficient under the budget constraint. Moreover, by direct computation, we obtain that as varies in , describes the interval

where

| (28) |

The truncature of the previously efficient frontier at the right (in the plane) of is part of the efficient frontier under the budget constraint. In light of the discussion above, the key question is to know what happens at the left of . Theorem 11 shows that no penalty in can implement (i.e. we are in the situation of panel (b)).

This immediately implies the characterisation of the constrained efficient frontier:

Theorem 10

The efficient frontier under the constraint is the truncature of the efficient frontier of Theorem 7 and is implemented exactly by penalties in .

Theorem 10 is a consequence of the following:

Theorem 11

Let . Under the constraint , the expected losses of the uninformed traders are at least

This lower bound is attained by the demand schedules for and by the only, where

These demand schedules are implemented by the penalties where .

Theorem 11 shows that one cannot implement with and provides penalty functions that achieve . While the imply the same expected losses of the uninformed traders, they all imply different expected post-trade standard deviations. In particular, all the for are not efficient penalties.

We supplement the proof with several discussions, and therefore present it in a separate section.

5.1.2 Proof of Theorem 11 and intuition

Step 1: transformation of the problem into a constrained problem of distance maximisation.

Recall equation (21):

This means that obtaining the bound of the Theorem is equivalent to showing

| (29) |

subject to the constraint that maximises the net profit .

Let , so that we are looking for an upper bound of . By Lemma 5 and under the constraint , we obtain:

| (30) | |||||

This is because, when , the IT can achieve at least a net profit of . Therefore, the maximum in (29) is less or equal to

subject to the constraints (i) , and (ii) and is non-decreasing. (i) comes from (30), and (ii) is an immediate consequence of the properties of an optimal demand schedule .

Notice how crucial Lemma 5 is, and therefore how effective the result of Milgrom and Segal (2002) is. Once noted that implies a lower bound on the net profit at 1, Lemma 5 allows (i) to incorporate the constraint the is a maximiser in a parsimonious way, (ii) to reduce the two constraints — and must maximise —, into a single condition, , which is particularly convenient, as it is a bound in a maximisation problem.

Absent the fact that must be non-decreasing, which translates into the fact that is non-decreasing, the maximisation of subject to (and ) would be standard: to “spread mass as unenvenly as possible”, one would pick with . This is not feasible, however, because it violates the monotonicity constraint. The are then natural candidate maximisers, as they are constructed in a similar spirit of variance maximisation, but respect the monotonicity constraint.

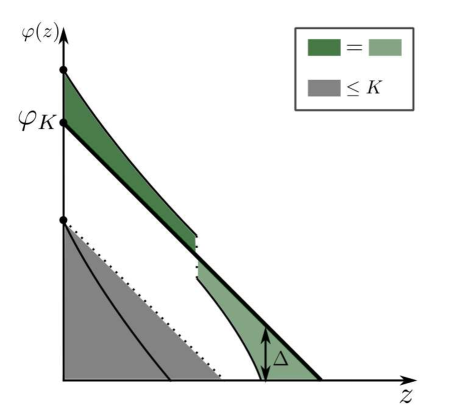

The all have the same norm, but are away from zero over different intervals. This hints at the fact that for a general function , when trying to find a bound on , we will have no way to know where must be small or large, and therefore little grip on . The idea is then to consider the repartition function of , because (i) one can reconstruct the moments of with those of (see Step 3) and (ii) it does not matter where is large, only how often it is large. In fact, all the have the same repartition function, which suggests that this is the correct perspective to adopt.

For any function and , let

Since is non-decreasing, we have

| (31) |

for all . Now, define

is subject to a monotonicity constraint (namely must be non-decreasing), which we need to transform into a constraint for . Clearly, if increases at speed 1, decreases at speed 1. What we show here is that if increases at speed less than 1 then decreases at speed larger than 1.

Since , the set is nonempty, so we can consider

Since we can also define

Because of (31), the function can not jump upwards, hence and . By construction of and , we have:

| (33) |

Since , we have:

| (34) |

We can now obtain (32):

Step 3: expression of the moments of as a function of the moments of .

Recall that

| (35) |

Step 4: translation into a functional maximisation problem with respect to the transform .

Using the previous discussion,

| (36) | |||||

where is the set of measurable functions and Clearly, in (36) the right-hand-side of Line 1 equals the term in Line 2.

Define for . Note that . If , . Otherwise, using the fact that ,

Hence, would be strictly less than .

Define : we proved that . Besides, by construction, . Define

Because , we have for and for . Hence:

(i) Starting from a point (lowest thick dot on the -axis), (solid black curved line) remains below the dotted line and its integral is therefore smaller than the area of the grey region, itself below . (ii) After crossing , must remain below . Here, the crossing occurs through a downwards jump of .

Thus, the supremum in (36) is attained only by the function and equal to

which establishes the bound of the Theorem.

Step 5: The maximum in (29) is attained exclusively by the demand schedules defined in the Theorem.

First, it is easy to see that these demand schedules achieve the maximum in (29). It remains to show that they are the only one to do so. Let be a demand schedule obtained under a penalty , . Let us suppose that it achieves the maximum in (29). Consider, as in step , the function associated with . The function is then a supremum of (36) and by step , . Since

the supremum of is at least . Let us remark that:

Since , the function is continuous: the supremum of and thus of is attained at a point . Since , and for , . Since , we obtain

with equality if and only if outside and over . But there must be equality because . Hence has the above form, and the demand function , given by , is equal to as stated in the Theorem, with .

Step 6: It is easy to see that the demand schedules are implemented by the penalties . This allows to conclude the proof of the Theorem.

One consequence of Theorem 10 is that it is not possible to infer from a regulator’s choice of penalty whether she is constrained or not. In the non-pecuniary case, a regulator subject to a binding budget constraint effectively behaves like an unconstrained regulator that would assign less weight to curtailing the losses of the uninformed traders. In the next section, we study the case of pecuniary penalties and show that, by contrast to the previous result, the introduction of the constraint creates new efficient points. In theory, observing that the regulator has selected one of these points would imply that she is constrained.

5.2 Pecuniary penalties

We now consider pecuniary penalties, collected by the regulator. For simplicity, we maintain the assumption of a constant and assume that a potential cap on does not bind. We suppose that the regulator must have a balanced budget in expectation. The budget constraint (26) transforms into

| (37) |

If , since we assume that a potential cap on is not binding, there is no constraint, and we are back to the case studied in section 4. The interesting case is therefore .

Definition 12

The efficient surface is the locus of points generated by any such that no can weakly (i) increase , (ii) decrease , (iii) increase with at least one among (i), (ii) or (iii) being in fact strictly.

Recall that , and denote respectively the P & L of the uninformed traders, the expected post-trade standard deviation and the expected collected fine. When convenient, we use the notations , or to say that the quantities are implied by the demand schedule .

5.2.1 Characterization of the efficient surface

Let be the set of indices

Theorem 13

A parametric equation of the efficient surface in the space is

and it is achieved exactly by the demand schedules where

These demand functions can be implemented by the penalties where

There is a key difference in proving Theorem 11 and Theorem 13. Here, the most natural candidate optimiser of the weighted objective, i.e. the pointwise minimiser, turns out to be an implementable demand schedule. Since pointwise minimisation is a simple task, the proof of Theorem 13 is fairly straightforward. Such an approach was not possible in proving Theorem 11.

Proof. As a consequence of Lemma 5, in equilibrium the expected fine satisfies

and we are working under a constraint .

By Lemma 6, an upper bound constraint on the expected post-trade standard deviation translates into a constraint

This leads us to consider the following minimisation problem:

for some weights . Gathering terms, we obtain that this program is equivalent to

| (38) |

For , define

Case 1: . is the restriction to of a second-order polynomial with positive leading coefficient. Therefore it reaches its minimum at either 0, , or when the first order condition is satisfied, say at , and achieves the minimum as soon as . Given that

algebra shows that

Let and . We have obtained that with the function given in the Theorem, the equality

holds. Direct calculations show that is implemented by . This means that we have found an implementable demand schedule that maximises the integral in (38) pointwise, which implies that is a minimiser of the program (38), and it is the only one because the pointwise minimisation of the integral in (38) has a unique solution.

Case 2: . is now either linear or with a negative leading coefficient, meaning that its minimum is attained either at 0 or . Algebra shows that (for ) if and only if

| (39) |

and

where, by condition (39), . With we conclude as before that is the unique minimiser of (38). Finally, if (39) is not satisfied, the minimiser of (38) is identically zero, which corresponds to defined in the Theorem.

Finally, it is easy to see that the constructed above describe the set as vary, and is the family of indices specified in the Theorem. So any index in corresponds to an efficient demand function. This shows that is the family of efficient demand functions.

The proof is complete, because the set of maxima we obtain as vary is connected, which implies that we have found all the points of the efficient surface.

5.2.2 Efficient frontiers for various regulator’s budgets

Assume that the regulator has budget , which translates into a constraint

Definition 14

The -efficient frontier is the set of non-dominated points in

We can now construct the -efficient frontiers from the efficient surface (denote the projection on the -plane):

Lemma 9

The -efficient frontier is the set of points of that are not dominated in .

Proof. See Appendix A.

This means that to obtain the -efficient frontier, one must first project the relevant points of , and then select those that are efficient in the plane (note that this second step is necessary, as the projection of a point of the efficient surface will in general not be a point of the efficient frontier). was found by solving an optimization problem, from which the -efficient frontiers are deduced geometrically: we do not need to solve again a minimisation problem.

We are now in a position to provide the -efficient frontiers: see Figure 13.

An important difference emerges with respect to the case of non-pecuniary penalties studied above. Here, the efficient frontiers are not truncatures of the frontier that obtains absent the constraint. Of course, the penalties in that implement are still part of the -efficient frontier, but new constrained efficient points emerge (dotted arcs), which are associated with penalty functions and demand schedules that were not previously optimal. The efficient frontier does not even intersect the unconstrained frontier for very large. To see why, note that the maximal expected fine under a penalty in is

This means that if , no penalty in allows to balance the regulator’s budget. In fact, a penalty that provides the highest expected fine (regardless of and ) is (defined in Theorem 13), and it gives .

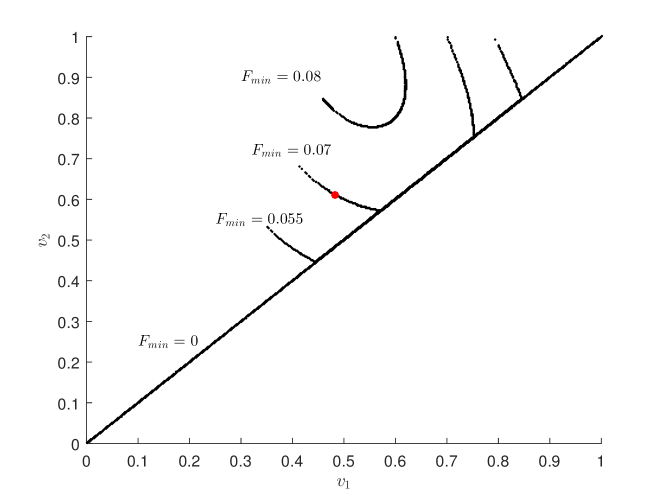

From Lemma 9, we know that points of the -efficient frontier correspond to points in , which means that they are associated with demand schedules of the form defined in Theorem 13. To understand how the budget constraint modifies the nature of the optimal strategies, Figure 14 plots the used on the -efficient frontier for various values of .

As an illustration, the red filled dot, which corresponds to represents the demand schedule (where is defined in Theorem 13) and indicates that this demand schedule implements one point of the efficient frontier when the budget constraint of the regulator is such that .

When , we obtain the line , in which case is implemented by a penalty , consistent with section 4.2.2. We observe that as increases, one needs to widen the gap . The intuition is that the linear section over of the demand schedule best resolves the trade off between large fines and large trade volumes of the insider trader and allows to collect a relatively high amount of fines in expectation. As an example, recall that the demand schedule that implies the highest expected fine (1/12) had .

When the regulator must balance its budget through the collection of pecuniary fines, some previously optimal strategies are no longer feasible as they do not induce the insider trader to pay enough fines in expectation. New constrained efficient points appear, and the class of efficient penalties is modified, as well as the equilibrium demand schedules and price functions.

and .

Figure 15 compares the price functions implied by a demand schedule efficient absent a budget constraint, and a constrained efficient demand schedule . Contrary to , has no flat sections and is everywhere increasing. In particular, in the unconstrained case, the random price is partly discrete: with positive probability, it will be equal to one of the ordinates of the flat sections of . Conversly, in the case of a strong budget constraint, the random price has a continuous density.

References

- (1)

- Bagnoli, Viswanathan, and Holden (2001) Bagnoli, M., S. Viswanathan, and C. Holden (2001): “On the Existence of Linear Equilibria in Models of Market Marking,” Mathematical Finance, 11(1), 1–31.

- Boulatov, Kyle, and Livdan (2013) Boulatov, A., A. Kyle, and D. Livdan (2013): “Uniqueness of Equilibrium in the single period Kyle ’85 model,” Working paper.

- Kyle (1985) Kyle, A. (1985): “Continuous Auctions and Insider Trading,” Econometrica, 53(6), 1315–1335.

- McLennan, Monteiro, and Tourky (2017) McLennan, A., P. Monteiro, and R. Tourky (2017): “On uniqueness of equilibrium in the Kyle model,” Math. Finan. Econ., 11, 161–172.

- Milgrom and Segal (2002) Milgrom, P., and I. Segal (2002): “Envelope Theorems for Arbitrary Choice Sets,” Econometrica, 70(2), 583–601.

- Rochet and Vila (1994) Rochet, J.-C., and J.-L. Vila (1994): “Insider Trading without Normality,” Review of Economic Studies, 61, 131–152.

- SEC (1998) SEC (1998): “Insider Trading: A US Perspective,” Speech by SEC Staff.

Appendix A Additional Proofs

A.1 Normalization of supports to

Assume and with and . We want to map an equilibrium with these noise terms and penalty to an equilibrium with normalized noises. Let for . defines a penalty in .

Let be an equilibrium of under uniform noises distributed over , and admissible demands . Let be the linear application mapping to :

Similar to Lemma 1, the expected price function must be where

For any , the maximisation program of the IT is

This can be rewritten as

Or:

By definition of , the solution of this program is given by . Recalling that the actual demand of the IT is , we obtain

We can also express the price function using . Since is linear, we can write

because and are independent variables.

So the equilibrium with noises and , penalty and admissible demands can be mapped to the equilibrium of with normalized noises and admissible demands . By the same procedure, one can do the reverse mapping.

Absent penalties, and the profit at is given by

This recoups a cost as soon as is outside

and is maximal when , where it equals .

Finally, we note that the model quantities of interest (, and ) are mapped one-to-one and ranked identically regardless of the chosen supports, i.e. the assertions “”,“” or “” do not depend on which supports we consider. Therefore, the choice of as the support of the noises is without loss of generality once we assume uniform distributions and a centered uninformed traders’ demand.

A.2 Proposition 1

Using Lemma 6, we can write

| (40) | |||||

By Cauchy-Schwarz inequality

Plugging this into (40), we obtain

| (42) |

This inequality determines the highest possible given . But there is equality in (42) if and only if there is equality in the Cauchy-Schwarz bound (A.2). This is the case if and only if the two functions in the left-hand side are colinear, i.e. if is proportional to : . Since for , . We conclude by noting that if and is defined by , the quadratic penalty implements .

A.3 Lemma 8

We first need to introduce some definitions:

Let be a function defined over and . We define:

One can define similarly and . Let us recall the first order conditions satisfied by a function at a local maximum.

If is a local maximum of , then:

We will also use the following real analysis result:

Lemma 10

Any continuous function on with a null left derivative is contant.

Let be a penalty function such that the strategy of the IT satisfies that for any , is either or . Since the strategy of the IT is non-decreasing, there exists such that for any and for any .

Besides, the penalty function must be continuous on . Indeed, if , using the fact that ,

thus, since is non-decreasing,

Taking the limit as goes to , we see that is right continuous at . Since by hypothesis it is left continuous on , the penalty function is continuous on .

Let us show that has a null left derivative on . If , we know that is a profit maximiser at : :. Using the first order condition for the lower left derivative recalled above, at , . Since , we obtain . Yet, is increasing, so the lower and upper left derivatives must be positive : . Thus:

This means that the cost function admits a left derivative at any , and the value of this left derivative is zero.

Thus is continuous and has a null left derivative on . Using Lemma 10, we obtain that is constant on . Let us denote by the value of on this interval.

The IT does not trade for . In that case, since we know that , we must have

By continuity of the left-hand term and the fact that the right-hand term is non-decreasing, we obtain

There must be equality for , because otherwise it would not be optimal to select on the right neighborhood of . For the same reason, can not jump at . This implies that , or and therefore must belong to .

Assume conversely that . Then for , the insider trader will make negative expected profits if she trades, so that . For , there are two cases to consider. (i) The IT plays . In that case, the expected penalty appears as a sunk cost and the best choice is , leading to a net profit of . (ii) The IT plays . The net profit is then

where the second line uses the fact that . Since

choice (i) is always preferred. Hence, if , for and for , which concludes the proof.

A.4 Lemma 9

(i) We first show that the -efficient frontier is included in the set of points of

that are not dominated in .

Let be in the -efficient frontier. By definition, there is implemented by such that , and . Only two cases are possible: (a) or (b) is dominated by a point non-dominated in the closure (in ) of all the implementable points, which is exactly . ( is obtained by constructing a sequence where each point dominates the previous one and define as its limit, or as if the procedure stops at .) In case (a), we see that , and since it is in the -efficient frontier, it cannot be dominated in that space. In case (b), since is in the -efficient frontier, we must have and and , so and we conclude as in case (a).

(ii) Let us show the other inclusion. It is enough to prove that if a point is dominated in , it is dominated in .

Let and be associated with this point. Assume is dominated in , say by , associated with . As before, either or is dominated by a point in . In both cases, this means that there exists a point in whose projection dominates . This concludes the proof.

Appendix B Robustness checks: the case of Gaussian noise

B.1 Shape of and under Gaussian noise

Which effects of section 3.4 are peculiar to uniform noises and which effects are robust to other distributional assumptions?

The qualitative behaviour of the demand function does not depend on the distribution of the noise. Consider for instance a cost with . When the magnitude of the optimal demand absent penalties is below , it remains optimal under the penalty . The IT then blocks its demand at in order to avoid the expected penalty , as long as trading does not allow to recoup on average. For sufficiently large ( for some ), the IT switches back to trading. This creates a jump in the demand function at . All these effects are independent of the assumptions on the noise.

The qualitative behaviour of the price function is robust as far as non-linearity is concerned. Flat sections in the demand schedule induce steep sections in the price function . Indeed, when increases slowly as a function of , the information that is likely to have increased a little (obtained through the observation of ) implies that is likely to have increased a lot. Similarly, steep sections of induce flat sections of . Since the introduction of penalties produces steep and flat sections for , it produces flat and steep sections for .

What does not hold in general is the fact that has discontinuities. Those are due to the fact that the uniform distribution has a discontinuous density . In general, one must have discontinuities in the density of the noise to obtain discontinuities in the price function. With a continuous noise density, jumps are replaced with sections where increases fast.

To support these arguments, we report the equilibrium for the model with Gaussian noise () and penalty .141414We are not able to prove formally existence (and even less uniqueness) in the case of Gaussian noise. What we do is run a fixed-point algorithm on equations (5) and (6) and assume that the functions to which it converges indeed correspond to an exact equilibrium. We consider the same penalties as above: quadratic, linear and constant on large trades.

![[Uncaptioned image]](/html/1809.07545/assets/2-X-Gauss-K-2-dim.png)

![[Uncaptioned image]](/html/1809.07545/assets/2-P-Gauss-K-2-dim.png)

, . Left panel: IT demand . Right panel: price function .

![[Uncaptioned image]](/html/1809.07545/assets/1-X-Gauss-K-2-dim.png)

![[Uncaptioned image]](/html/1809.07545/assets/1-P-Gauss-K-2-dim.png)

, . Left panel: IT demand . Right panel: price function .

![[Uncaptioned image]](/html/1809.07545/assets/0-X-Gauss-K-1-xc-05-dim.png)

![[Uncaptioned image]](/html/1809.07545/assets/0-P-Gauss-K-1-xc-05-dim.png)

, , .

Left panel: IT demand . Right panel: price function .

B.2 Figure 7 under Gaussian noise

We repeat the construction of Figure 7 by assuming Gaussian noise: . We obtain Figure 19. The constant costs upon nonzero trades are doing best among the penalty functions considered. This is consistent with the results in the uniform noise case. Other penalties are suboptimal, as before, and the locus of points they generate is very similar in shape.

Appendix C Discussion: Bagnoli, Viswanathan, and Holden (2001)

Consider a static Kyle model where the NT trade with noise and the fundamental has distribution . We provide an informal discussion with two results that complement those of Bagnoli, Viswanathan, and Holden (2001). Result 1 is new. Result 2 provides an alternative proof for a particular case of their work. Recall that the model is said to be with individual orders when the market maker observes the set where is the order of the insider trader, and to be with aggregate orders when she observes instead.

Let , which we do not necessarily assume to be 0. We focus on increasing demand schedules . We have the following

Result 1 (individual orders) A mimicking equilibrium strategy must be affine in .

Since and are indistinguishable, the price function is given by

Therefore, the maximisation program of the IT is

Since in distribution, in distribution and the program reduces to

Since is an equilibrium strategy, the derivative of this expression evaluated at must be zero:

Therefore, must satisfy the ODE

i.e. is affine (in fact linear in ).

We already see that if it is impossible to mimick the noise in an affine manner, we can’t have a mimicking equilibrium. If, however, this is possible, we automatically have an equilibrium:

Result 2 (individual orders and aggregate orders) If there exists increasing and linear in such that in distribution, and is the corresponding pricing function, is an equilibrium.

In the case of individual orders, this result is immediate from the arguments above: indeed is affine so the first order condition, which is satisfied for indeed characterizes a global maximum.

Then, we note that the result extends to the case of aggregate orders. Indeed since and are indistinguishable, by symmetry

so, since is linear, as before, therefore is still an optimal demand.