A TEST FOR DETECTING STRUCTURAL BREAKDOWNS IN MARKETS USING EIGENVALUE DISTRIBUTIONS

Abstract

Correlations among stock returns during volatile markets differ substantially compared to those from quieter markets. During times of financial crisis, it has been observed that ‘traditional’ dependency in global markets breaks down. However, such an upheaval in dependency structure happens over a span of several months, with the breakdown coinciding with a major bankruptcy or sovereign default. Even though risk managers generally agree that identifying these periods of breakdown is important, there are few statistical methods to test for significant breakdowns. The purpose of this paper is to propose a simple test to detect such structural changes in global markets. This test relies on the assumption that asset price follows a Geometric Brownian Motion. We test for a breakdown in correlation structure using eigenvalue decomposition. We derive the asymptotic distribution under the null hypothesis and apply the test to stock returns. We compute the power of our test and compare it with the power of other known tests. Our test is able to accurately identify the times of structural breakdown in real-world stock returns. Overall we argue, despite the parsimony and simplicity in the assumption of Geometric Brownian Motion, our test can perform well to identify the breakdown in dependency of global markets.

JEL classification: C01, C12, C58

Keywords: Correlation matrix, Fluctuation Test, Local Power

1 Introduction

An important problem in statistical modeling of financial time series is to analyze and detect structural changes in the relationship among stock returns. Pearson Correlation is one of the widely used metrics in financial risk management to indicate the relationship among various returns. Long-term risk-averse investors tend to hold portfolios of assets whose returns are not positively correlated for diversification benefits. However, there is compelling empirical evidence that the correlation structure among returns of the assets cannot be assumed to be constant over time, see, e.g. [Forbes and Rigobon, 2002], [Krishnan et al., 2009], [Wied et al., 2012] and [Wied, 2017]. In particular, in periods of financial crisis, correlations among stock returns increase, a phenomenon which is sometimes referred to as diversification meltdown. In this paper, we detect and test for these structural changes by considering the constancy of correlation matrix. [Wied et al., 2012] has shown that testing for changes of correlation can be more powerful than testing for changes in covariance, especially when there is more than one change point. However, one of the drawbacks of these existing tests ([Wied et al., 2012] and [Wied, 2017]) is that pairwise comparison of correlation matrix is not a scalable solution when there are large number of stocks involved in the portfolio. Instead of the vector of successively calculated pairwise correlation coefficients, we consider the largest eigenvalue of sample correlation matrix and derive its limiting distribution, based on the assumption of Geometric Brownian motion (GBM) of stockprice and some proof ideas from [Anderson, 1963]. Our key contributions are as follows: Our proposed test is scalable to portfolios with large number of stocks as ours does not involve any pair-wise comparisons. It is easily explainable to all the stakeholders and fairly straightforward to implement.

Outline

First, we show how the returns are normality using the assumption of GBM for stock prices. Next, we define our test statistic and derive its distribution using results from [Anderson, 1963]. Our test statistic is qualitatively very similar to the one defined in [Wied et al., 2012] and [Wied, 2017] as discussed in section 2.2. Towards the end of this section, we give a simplified expression for the asymptotic distribution of test statistic for the cases of two-stock and three-stock portfolios. In section 3, we demonstrate the performance of our test on known stock indices such as SNP500, DOWJones, etc. In section 4, we derive the power of our test and compare it with those of existing methods. Finally, in section 5, we discuss the merits and demerits of our approach.

2 Test statistic

In this section, we derive the distribution of eigenvalues of sample correlation matrix when the returns are iid multivariate normal by making use of results from [Anderson, 1963]. Further, we define our test statistic and use these results to derive its asymptotic distribution. First, we start off by showing how the returns will be iid normal under the assumption that the stock price follows a Geometric Brownian Motion.

2.1 The Geometric Brownian Motion - preliminaries

The Geometric Brownian Motion is a continuous time stochastic process in which the logarithm of a random variable follows a Wiener’s process with some drift [Sheldon Ross, 2014]. Geometric Brownian motion (GBM) describes the evolution of the stock price over time and is widely used in mathematical finance to calculate the price of options [Brigo et al., 2007]. The GBM is modeled using the following stochastic differential equation:

| (1) |

Here, and denote the drift and volatility of the stock price, respectively. is a standard Brownian motion, also known as Wiener’s Process, that is characterised by independent identically distributed (iid) increments of random variables that follow a Gaussian distribution with zero mean and a standard deviation equal to the square root of the time step. It can be seen that at every time , depends only . In other words, the conditional distribution of the future price given all the price information up to time , depends only on the present price at time but not on the past prices - i.e. a Markov property.

Using Itôs lemma, equation 1 can be rewritten as follows:

| (2) |

where log denotes the standard natural logarithm. Integrating this equation (2) from to , leads to:

| (3) |

Rearranging the equations and substituting the boundary conditions and , the process describing the stock price is obtained as follows:

| (4) |

Equation (4) shows that if asset price follows a GBM, then the logarithmic returns follow a normal distribution.

Note that in equation (3), we can approximate the log returns using Taylor series approximation of

| (5) |

Using the approximation in equation (5), we can see that the returns approximately follow normal distribution using the assumption of GBM for stock prices.

2.2 Asymptotic distribution of eigenvalues and Test Statistic

Asymptotic distribution of the eigenvalues of sample covariance matrix is derived in equations (2.1 - 2.13) of [Anderson, 1963]. The theorem and results are as follows:

Say is a -dimensional vector distributed according to and . From multivariate central limit theorem, is asymptotically normally distributed. Let be the eigenvalues of , where , and be the eigenvalues of , where .

First, we give the results for the simple case where all the characteristic roots of are equal, that is, , say. Define , where is a x diagonal matrix with as diagonal elements, and is the x identity matrix. Clearly, is also a x diagonal matrix with elements say, . Asymptotic distribution of is given by

| (6) |

where,

If the largest eigenvalue, , has a multiplicity of instead of , where , then test statistic is slightly modified as , where is the x sample eigenvalue diagonal matrix and is the x identity matrix. The distribution of is same as the one given above in equation (6) with replaced by . For example, when the maximum eigenmultiplicity is just 1 (the case when all the eigenvalues are unique), our equation (6) simplifies to

| (7) |

2.2.1 Simplification for two-stock portfolio

We can simplify the above distribution in equation (6) for the simple case of two-stock portfolio, i.e. . Let , where are standardized returns. Also, let . The correlation matrix, , at time can be represented as

whose eigenvalues are and and the corresponding eigenvectors are and . Let be its largest eigenvalue.

The sample correlation matrix, , at time is

Also, let be the largest eigenvalue of

The test statistic is defined as follows:

where, are the maximum eigenvalues at times and respectively. Note that our test statistic is qualitatively very similar to the one defined in [Wied et al., 2012] as , where is scalar constant.

From equation (7), we can see that the asymptotic distribution of is

2.2.2 Simplification for three-stock portfolio

In this subsection, we derive an expression for the asymptotic distribution of the test statistic for a three-stock portfolio, i.e. . Let , where are standardized returns. Also, let . The correlation matrix, , at time can be represented as

The characteristic equation for the above matrix is

| (8) |

Solving for in equation (8), gives the eigenvalues of the correlation matrix .

Let , then equation (8) becomes

| (9) |

where, ,

Further, let , and .

From AM-GM inequality, we can see that . If , [Weisstein, 2018]’s equations (57-73) give the real roots to equation (9) as

where

Similarly, we can find the roots corresponding to the correlation matrix, , at time . Let and be the smallest roots corresponding to and respectively. As this is the case of multiplicity being 1, from equation (7), we can see that the asymptotic distribution of is

3 Testing on stock returns

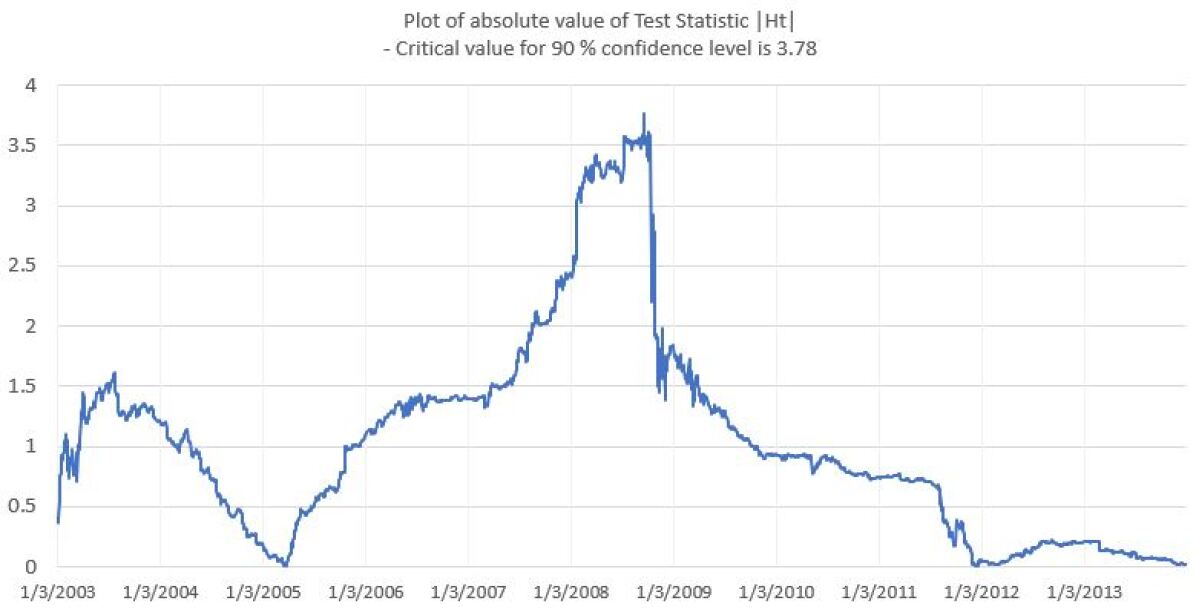

First, we demonstrate our test on the same stocks (SNP500 and DAX indices) considered in [Wied et al., 2012]; the highest value of the test statistic is 3.79; as seen from Figure 1, this coincides with the collapse of Lehman Brothers around 18 September, 2008, and is slightly greater than the critical value for 90% confidence level.

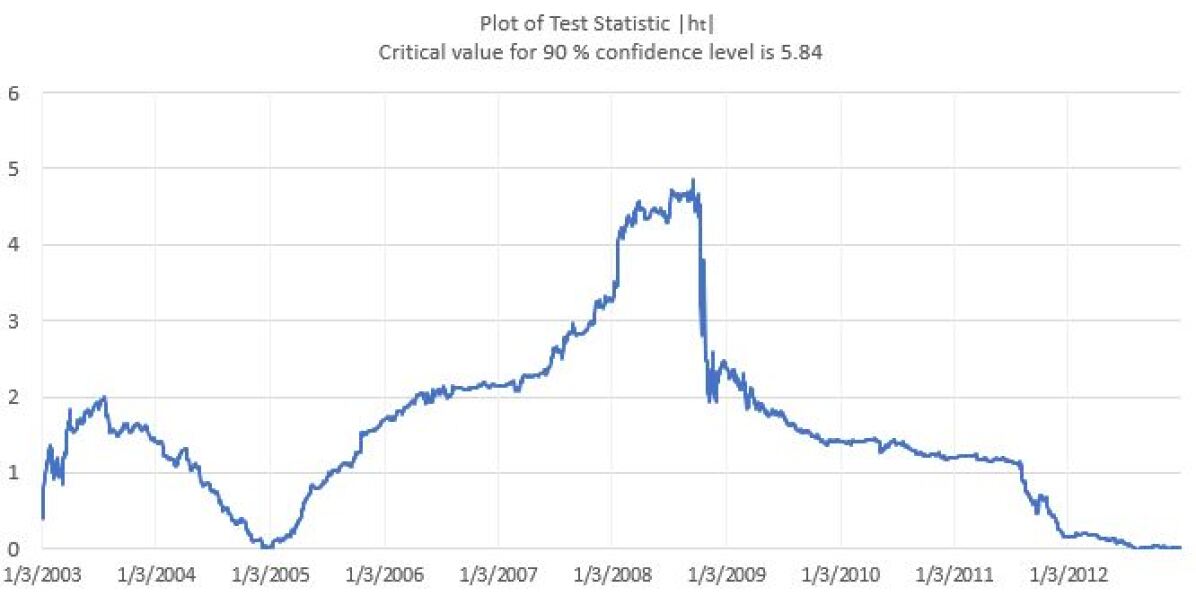

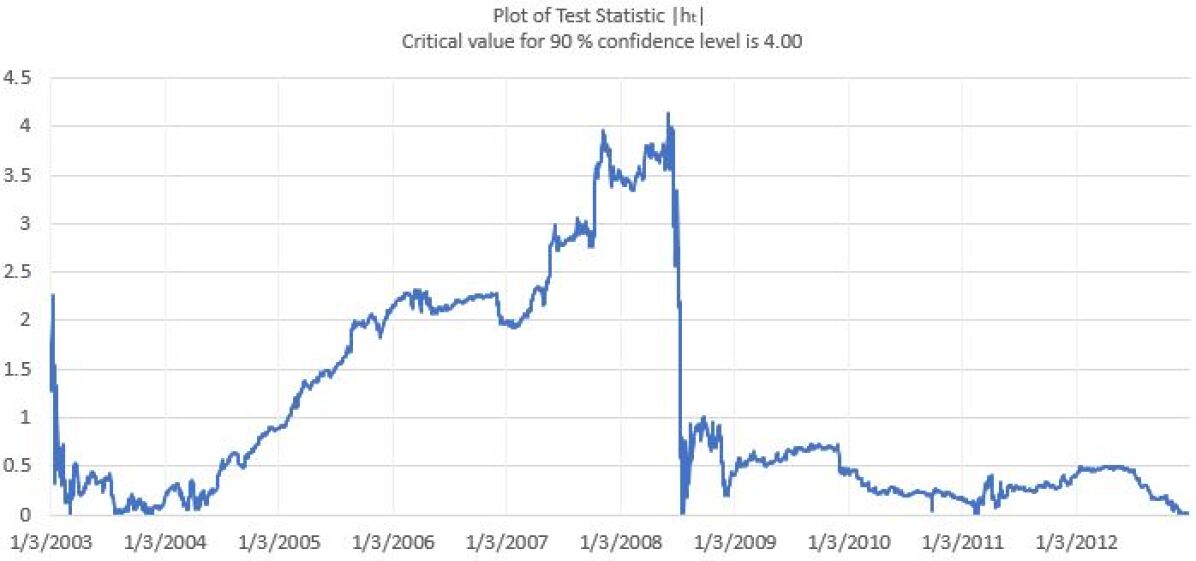

Next, we demonstrate our test on a three-stock portfolio for two cases. In case (i), we have two American Indices (SNP 500 and DOWJones) and a German Index (DAX). In case (ii), we have indices from US, Germany and Japan (SNP, DAX and Nikkei respectively). As expected, it can be seen from Figure 2, the correlation structure has been disturbed more in case(ii), where all the indices are from different countries, as against case(i) where 2 indices are from the same country (US).

4 Local power

First, we derive the distribution of the test statistic for the alternative hypothesis under consideration for cases (1-4) mentioned below, where the correlation changes once at time . For case(5), the correlation changes twice, once at time and once at .

-

1.

, and ,

-

2.

, and ,

-

3.

, and ,

-

4.

, and ,

-

5.

, and , and

First we derive the expressions for cases (1-4) where correlation changes only once. Let be the time until which the correlation remains and from time to the correlation remains .

So, the correlation matrices for duration and can be written as

Therefore, the correlation matrix at time can be written as

where

From equation (6), we can get the distribution of and, hence, the distribution of .

When the correlation changes only once at , the form of our test statistic at is

Substituting the distributions of and , we have,

Where, is standard normal distribution

E.g. For case (1) and , we have , and

We can derive a similar expression for the case (5) where the correlation changes at two times, and , in the total duration () under consideration.

The test statistic at is

Substituting the distributions of , , and, , we have the distribution of as

We checked the power of our test for cases (1-5), in which variances constantly remain 1 and correlations change, and compared our results against those of [Wied et al., 2012] and [Aue et al., 2009].

| T | 1 | 2 | 3 | 4 | 5 | |

| (a) Our test | ||||||

| 200 | 0.01 | 0.04 | 0.70 | 0.70 | 0.04 | |

| 500 | 0.04 | 0.07 | 0.99 | 0.99 | 0.06 | |

| 1000 | 0.08 | 0.14 | 1 | 1 | 0.08 | |

| 2000 | 0.21 | 0.29 | 1 | 1 | 0.15 | |

| (b) Test of [Wied 2012] | ||||||

| 200 | 0.309 | 0.255 | 0.953 | 0.88 | 0.101 | |

| 500 | 0.255 | 0.488 | 0.996 | 0.989 | 0.207 | |

| 1000 | 0.83 | 0.733 | 0.998 | 0.998 | 0.422 | |

| 2000 | 0.967 | 0.928 | 1 | 0.999 | 0.75 | |

| (c) Test of [Aue 2009] | ||||||

| 200 | 0.24 | 0.16 | 0.97 | 0.84 | 0.08 | |

| 500 | 0.58 | 0.40 | 1 | 0.99 | 0.16 | |

| 1000 | 0.85 | 0.69 | 1 | 1 | 0.28 | |

| 2000 | 0.98 | 0.93 | 1 | 1 | 0.61 | |

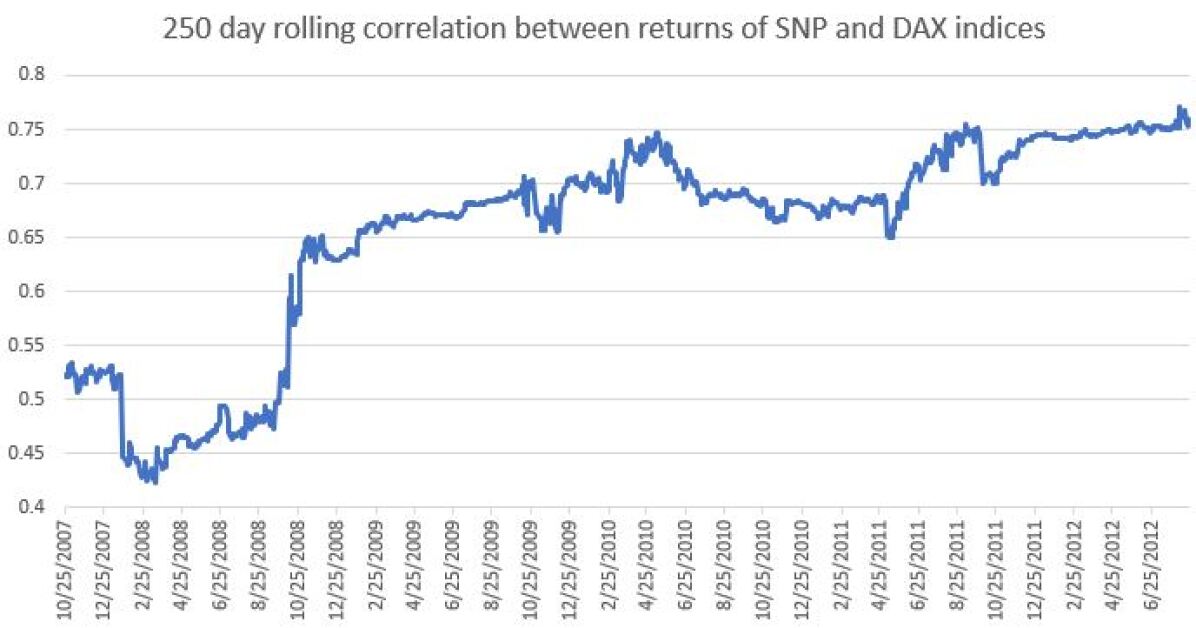

From Table 1, it is seen that, in general, the power of our test is lower compared to those of [Wied et al., 2012] and [Aue et al., 2009]. However, in particular, for cases 3 and 4, the power of our test is slightly higher - indicating that our test can detect large changes in the correlation structure more effectively. Further, it should be noted that a correlation change of about (0.3 - 0.35) is common during the times of financial crisis as indicated in Figure 3. So, while the power of our test is comparatively lower, our approach is simpler to explain, understand & implement, and still can be used to test the breakdown in correlation structure for real world scenarios.

5 Conclusions

In this paper, we have proposed a new fluctuation test for constant correlation matrix under a multivariate setting in which the change points need not be specified apriori. Our approach is more simplified because it allows us to work with more standard operations like eigen-decomposition and normal distributions against the pairwise comparison and Brownian bridges of [Wied et al., 2012] and [Wied, 2017]. Since we are dealing with only the largest eigenvalue, the power of our test is lower compared to the pairwise comparison of the entire correlation matrix of [Wied et al., 2012] and [Wied, 2017]. Nevertheless, our test is simpler in terms of understanding and practical application, and is effectively able to detect changes in correlation matrix in real world scenarios, as indicated in Section 3. Moreover, our method can be generalized to detect any changes in covariance matrix structure, as a complementary technique to [Aue et al., 2009]. One drawback of our test, which is also shared by [Wied et al., 2012] and [Wied, 2017], is the assumption of finite fourth moments and constant expectations and variances. Another drawback, which is shared by most of correlation based tests, is the low power when there are multiple change points in the duration under consideration, as illustrated in [Cabrieto et al., 2018]. Hence, it may be worthwhile to consider techniques like prefiltering and/or other transformations to overcome these drawbacks.

References

- [Sheldon Ross, 2014] Ross, Sheldon M (2014). Introduction to Probability Models. Academic Press , 16(3):353–367.

- [Brigo et al., 2007] Brigo, Damiano and Dalessandro, Antonio and Neugebauer, Matthias and Triki, Fares. (2007). A stochastic processes toolkit for risk management. SSRN 1109160

- [Anderson, 1963] Anderson, T. W. (1963). Asymptotic theory for principal component analysis. The Annals of Mathematical Statistics, 34(1):122–148.

- [Aue et al., 2009] Aue, A., Hörmann, S., Horváth, L., Reimherr, M., et al. (2009). Break detection in the covariance structure of multivariate time series models. The Annals of Statistics, 37(6B):4046–4087.

- [Cabrieto et al., 2018] Cabrieto, J., Tuerlinckx, F., Kuppens, P., Hunyadi, B., and Ceulemans, E. (2018). Testing for the presence of correlation changes in a multivariate time series: A permutation based approach. Scientific Reports, 8(1):769.

- [Forbes and Rigobon, 2002] Forbes, K. J. and Rigobon, R. (2002). No contagion, only interdependence: measuring stock market comovements. The Journal of Finance, 57(5):2223–2261.

- [Krishnan et al., 2009] Krishnan, C., Petkova, R., and Ritchken, P. (2009). Correlation risk. Journal of Empirical Finance, 16(3):353–367.

- [Weisstein, 2018] Weisstein, E. W. (2018). Cubic formula, from mathworld–a wolfram web resource. Accessed: 2018-03-11.

- [Wied, 2017] Wied, D. (2017). A nonparametric test for a constant correlation matrix. Econometric Reviews, 36(10):1157–1172.

- [Wied et al., 2012] Wied, D., Krämer, W., and Dehling, H. (2012). Testing for a change in correlation at an unknown point in time using an extended functional delta method. Econometric Theory, 28(3):570–589.