Abstract: This work extends the variance reduction method for the pricing of possibly path-dependent derivatives, which was developed in [Genin and Tankov, 2016] for exponential Lévy models, to affine stochastic volatility models [Keller-Ressel, 2011]. We begin by proving a pathwise large deviations principle for affine stochastic volatility models. We then apply a time-dependent Esscher transform to the affine process and use Varadhan’s Lemma, in the fashion of [Guasoni and Robertson, 2008] and [Robertson, 2010], to approximate the problem of finding the Esscher measure that minimises the variance of the Monte-Carlo estimator. We test the method on the Heston model with and without jumps to demonstrate the numerical efficiency of the method.

1. Introduction

The aim of this paper is to develop efficient importance sampling estimators for prices of path-dependent options in affine stochastic volatility (ASV) models of asset prices. To this end, we establish pathwise large deviation results for these models, which are of independent interest.

An ASV model, studied in [Keller-Ressel, 2011] is a two-dimensional affine process on with special properties, where models the logarithm of the stock price and its instantaneous variance. This class includes many well studied and widely used models such as Heston stochastic volatility model [Heston, 1993], the model of Bates [Bates, 1996], Barndorff-Nielsen stochastic volatility model [Barndorff-Nielsen and Shephard, 2001] and time-changed Lévy models with independent affine time change. European options in affine stochastic volatility models may be priced by Fourier transform, but for path-dependent options explicit formulas are in general not available and Monte Carlo is often the method of choice. At the same time, Monte Carlo simulation of such processes is difficult and time-consuming: the convergence rates of discretization schemes are often low due to the irregular nature of coefficients of the corresponding stochastic differential equations. To accelerate Monte Carlo simulation, it is thus important to develop efficient variance-reduction algorithms for these models.

In this paper, we therefore develop an importance sampling algorithm for ASV models. The importance sampling method is based on the following identity, valid for any probability measure , with respect to which is absolutely continuous. Let be a deterministic function of a random trajectory , then

This allows one to define the importance sampling estimator

where are i.i.d. sample trajectories of under the measure . For efficient variance reduction, one needs then to find a probability measure such that is easy to simulate under and the variance

is considerably smaller than the original variance .

In this paper, following the work of [Genin and Tankov, 2016] in the context of Lévy processes, we define the probability using the path-dependent Esscher transform,

where is the first component of the ASV model (the logarithm of stock price) and is a (deterministic) bounded signed measure on . The optimal choice of should minimize the variance of the estimator under ,

The computation of this variance is in general as difficult as the computation of the option price itself. Following [Dupuis and Wang, 2004, Glasserman et al., 1999, Guasoni and Robertson, 2008, Robertson, 2010] and more recently [Genin and Tankov, 2016], we propose to compute the variance reduction measure by minimizing the proxy for the variance computed using the theory of large deviations.

To this end, we establish a pathwise large deviation principle (LDP) for affine stochastic volatility models. A one dimensional LDP for as where is the first component of an ASV model has been proven in [Jacquier et al., 2013]. In this paper, we extend this result to the trajectorial setting, in the spirit of the pathwise LDP principles of [Léonard, 2000], but in a weaker topology.

The rest of the paper is structured as follows. In Section 2, we describe the model and recall certain useful properties of ASV processes. In Section 3, we recall some general results of large deviations theory. In Section 4, we prove a LDP for the trajectories of ASV processes. In Section 5, we develop the variance reduction method, using an asymptotically optimal change of measure obtained via the LDP shown in Section 4. In Section 6, we test the method numerically on several examples of options, some of which are path-dependent, in the Heston model with and without jumps.

2. Model description

In this paper, we model the price of the underlying asset of an option as , where we model as an affine stochastic volatility process. We recall, from [Keller-Ressel, 2011] and [Duffie et al., 2003], the definition and some properties of ASV models.

Definition 2.1.

An ASV model , is a stochastically continuous, time-homogeneous Markov process such that is a martingale and

| (2.1) |

for all .

Proposition 2.2.

The functions and satisfy generalized Riccati equations

| (2.2a) | |||||

| (2.2b) | |||||

where and have the Lévy-Khintchine forms

where ,

and satisfy the following conditions

-

•

are positive semi-definite 22-matrices where .

-

•

and .

-

•

and are Lévy measures on and .

In the rest of the paper, we assume that there exists such that , for the law of to depend on . Define the function

A sufficient condition for to be a martingale [Keller-Ressel, 2011, Corollary 2.7], which we assume to be satisfied in the sequel, is and .

In the following theorem, we compile several results of [Keller-Ressel, 2011] that describe the behaviour of the solution to eq. (2.2) as .

Theorem 2.3.

Assume that and .

-

•

There exists an interval , such that for each , eq. (2.2b) admits a unique stable equilibrium .

-

•

For , eq. (2.2b) admits at most one other equilibrium , which is unstable.

-

•

For , eq. (2.2b) does not have any equilibrium.

We denote the basin of attraction of the stable solution of eq. (2.2b) and , the domain of . We have that

-

•

is an interval such that .

-

•

For , and , we have

(2.3) -

•

For , and ,

(2.4) where .

-

•

For every , .

Definition 2.4.

A convex function with effective domain is essentially smooth if

-

i.

is non-empty;

-

ii.

is differentiable in ;

-

iii.

is steep, that is, for any sequence that converges to a point in the boundary of ,

In the rest of the paper, we shall make the following assumptions on the model.

Assumption 1.

The function satisfies the following properties.

-

(1)

There exists , such that .

-

(2)

is essentially smooth.

In [Jacquier et al., 2013], a set of sufficient conditions is provided for Assumption 1 to be verified:

Proposition 2.5 (Corollary 8 in [Jacquier et al., 2013]).

Let be an ASV model such that and are not identically 0 and and are strictly negative. If either of the following conditions holds

-

(i)

The Lévy measure of has exponential moments of all orders, F is steep and .

-

(ii)

is a diffusion,

then function is well defined, for every with effective domain . Moreover h is essentially smooth and .

We now discuss the form of the basin of attraction of the unique stable solution of (2.2b).

Lemma 2.6.

[Keller-Ressel, 2011, Lemma 2.2.]

-

(a)

and are proper closed convex functions on .

-

(b)

and are analytic in the interior of their effective domain.

-

(c)

Let be a one-dimensional affine subspace of . Then is either a strictly convex or an affine function. The same holds for .

-

(d)

If , then also for all . The same holds for .

Lemma 2.7.

Let be a convex function with either two zeros , or a single zero . In the latter case, we let . Assume that there exists such that . Then for every ,

Proof.

By convexity, for every such that ,

and therefore . Furthermore, for every ,

Let . If is continuous in , then and for every in , . If is discontinuous in however, then by convexity, for . ∎

Proposition 2.8.

3. Large deviations theory

In this section, we recall some useful classical results of the large deviations theory. We refer the reader to [Dembo and Zeitouni, 1998] for the proofs and for a broader overview of the theory.

Theorem 3.1 (Gärtner-Ellis).

Let be a family of random vectors in with associated measure . Assume that for each ,

as an extended real number. Assume also that 0 belongs to the interior of . Denoting

the following hold:

-

(a)

For any closed set ,

-

(b)

For any open set ,

where is the set of exposed points of , whose exposing hyperplane belongs to the interior of .

-

(c)

If is an essentially smooth, lower semi-continuous function, then satisfies a LDP with good rate function .

Definition 3.2.

A partially ordered set is called right-filtering if for every , there exists such that and .

Definition 3.3.

A projective system on a partially ordered right-filtering set is a family of Hausdorff topological spaces and continuous maps such that whenever .

Definition 3.4.

Let be a projective system on a partially ordered right-filtering set . The projective limit of , denoted , is the subset of topological spaces , consisting of all the elements for which whenever , equipped with the topology induced by . The projective limit of closed subsets are defined in the same way and denoted .

Remark 3.5.

The canonical projections of , i.e. the restrictions of the coordinate maps from to , are continuous.

Theorem 3.6 (Dawson-Gärtner).

Let be a projective system on a partially ordered right-filtering set and let be a family of probabilities on , such that for any , the Borel probability on satisfies the LDP with good rate function . Then satisfies the LDP with good rate function

Theorem 3.7 (Varadhan’s Lemma, version of [Guasoni and Robertson, 2008]).

Let be a family of -valued random variables, whose laws satisfy a LDP with rate function . If is a continuous function which satisfies

for some , then

4. Trajectorial large deviations for affine

stochastic volatility model

In this section, we prove a trajectorial LDP for when the time horizon is large. Define, for and , the scaling . We proceed by proving first a LDP for in finite dimension, that we extend, in a second step to the whole trajectory of .

4.1. Finite-dimensional LDP

Let , by convention , and define

for . We start by formulating our main technical assumption.

Assumption 2.

One of the following conditions is verified.

-

(1)

The interval support of is and .

-

(2)

For every , , i.e, the generalized Riccati equations have only one (stable) equilibrium.

The following Lemma gives an intuition on Assumption 2.

Lemma 4.1.

For every , .

Proof.

As a first step to apply Theorem 3.1, we prove the following result.

Theorem 4.2.

Proof.

Since Assumption 2 holds, then, by Lemma 4.1, for every . Assume first that for every . Using the Markov property and eq. (2.1), we obtain

Since and , eqs. (2.3) and (2.4) apply and

Using the fact that and for every , we can iterate the procedure to obtain

| (4.1) |

Assume now that there exists such that . Without loss of generality, we take the largest such . Following the same procedure, we find

Noting that explodes in finite time for then finishes the proof. ∎

We now proceed to the finite-dimensional large deviations result.

Theorem 4.3.

Let and as previously. Assuming that Assumption 2 holds, then satisfies a LDP on with good rate function

where .

Proof.

By Assumption 1(1), there exists such that , which implies that and therefore 0 is in the interior of . Theorem 4.2 implies that the limit

where , exists as an extended real number. Since, by Assumption 1(2), is essentially smooth and lower semi-continuous, then so is . Theorem 3.1 then applies and satisfies a LDP, on , with good rate function

Furthermore,

which finishes the proof. ∎

4.2. Infinite-dimensional LDP

4.2.1. Extension of the LDP

We now extend the LDP to the whole trajectory of on , the set of all functions from to that vanish at 0, by proving the following general lemma.

Lemma 4.4.

Assume that for any , the finite-dimensional process satisfies a large deviation property with good rate function . Then the family satisfies a large deviation property on equipped with the topology of pointwise convergence, with good rate function

Proof.

Let be the partially ordered right-filtering set

ordered by inclusion. We consider on the projective system defined by and the natural projection on shared times. The canonical projection from to is . Let be the probability measure generated by on . Then, by hypothesis, for any , satisfies a LDP with good rate function . The result is then given by Theorem 3.6. ∎

Theorem 4.5.

Assume that Assumption 2 holds, then satisfies a LDP on equipped with the topology of point-convergence, as , with good rate function

Proof.

The result is a direct application of Lemma 4.4. ∎

4.2.2. Calculation of the rate function

We finally calculate the rate function of Theorem 4.5.

Theorem 4.6.

The rate function of Theorem 4.5 is

where

is the derivative of the absolutely continuous part of , is the singular component of with respect to and is any non-negative, finite, regular, -valued Borel measure, with respect to which is absolutely continuous.

Proof.

By identifying with , we find for every ,

Note that the supremum can be taken indifferently on or on because the objective function depends on only on a finite set. Since we have assumed that there exists in , then if has infinite variation, we immediately find that . Assume therefore that has finite variation. We wish to show that

Notice that

To prove the other inequality, we use the following construction. Fix and let . Let also such that and define as

Then

where is the measure associated with . Hence

and

We will now use [Rockafellar, 1971, Thm. 5.] to obtain the result. Since has finite variation, the measure is regular. Using the notation of [Rockafellar, 1971], in our case the multifunction is the constant multifunction . Therefore is fully lower semi-continuous. Furthermore, since , the interior of is non-empty. The set is compact with no non-empty open sets of measure 0 and for every in the interior of , and open,

[Rockafellar, 1971, Thm. 5.] then implies that

where

is the derivative of the absolutely continuous part of , is the singular component of with respect to and is any non-negative, finite, regular, -valued Borel measure, with respect to which is absolutely continuous. ∎

Remark 4.7.

In particular, the proof of Theorem 4.6 shows that, if does not belong to , the set of trajectories with bounded variation, then .

5. Variance reduction

Denote the payoff of an option on . The price of an option is generally calculated as the expectation under a certain risk-neutral measure . For any equivalent measure , the price of the option can be written

The variance of is

whereas

We can therefore choose in order to reduce the variance of the random variable, whose expectation gives the price of the option.

A flexible class of measure changes introduced in [Genin and Tankov, 2016] is given by path dependent Esscher transform, that is the class of measures such that

where belongs to , the set of signed measures on . Denoting , the optimization problem writes

| (5.1) |

where

The optimization problem (5.1) cannot be solved explicitly. We therefore choose to solve the problem asymptotically using the two following lemmas. Denote the set of measures with support on a finite set of points. We first give a lemma that characterizes the behaviour of as , for as this will be sufficient for the cases that we will consider in Section 6 (see Prop. 5.5).

Lemma 5.1.

If Assumption 2 holds, then for any measure , such that for every , , we have

Proof.

Next, we give a result that characterizes the behaviour of the variance minimization problem (5.1) where has been replaced by as .

Lemma 5.2.

Let such that for every . Assume that the assumptions of Theorem 4.3 hold. Assume furthermore that is bounded from above by a constant and continuous on the set of functions , such that , with respect with to the pointwise convergence topology. Then

Proof.

First note that, by Lemma 5.1,

We therefore just need to prove that

Denote the function . Since is assumed to be continuous and has support on , is continuous. Let us show the integrability condition of Theorem 3.7. For every

Since for every , there exists such that remains in for every . Therefore Lemma 5.1 applies and

Theorem 3.7 then applies and yields the result. ∎

Definition 5.3.

Let . We say that is asymptotically optimal if it minimises

In general, is not easy to calculate explicitly. To solve this problem, we cite the following theorem of [Genin and Tankov, 2016].

Theorem 5.4.

Let be concave and assume that the set is non-empty and contains a constant element. Assume furthermore that is continuous on this set with respect to the topology of pointwise convergence, that is lower semi-continuous with open and bounded effective domain and that there exists a such that is complex-analytic on . Then

where

Furthermore, if minimises the left-hand side of the above equation, it also minimises the right-hand side.

We finally give a result for the case where depends on only through .

Proposition 5.5.

Let and let be a log-payoff depending on only through . Then for every such that , .

Proof.

Assume that is such that . Then there exists a set , such that . Fix . By definition, . Then

By letting tend to , one can therefore increase indefinitely . Therefore, . ∎

6. Numerical examples

In this section, we apply the variance reduction method to several examples. We first prove a result for options on the average value of the underlying over a finite set of points.

Proposition 6.1.

Let and consider an option with log-payoff

Then for any with support on ,

| (6.1) |

where we use the abuse of notation .

Proof.

In this case,

When the option is out or at the money, the log-payoff is . Assume that is such that and differentiate with respect to . We obtain

Therefore the that maximises satisfies

for every . Therefore

Inserting in the value of , we obtain the result. ∎

6.1. European and Asian put options in the Heston model

Consider the Heston model [Heston, 1993]

| (6.2) | ||||||

where are standard -Brownian motions. The Laplace transform of is

where satisfy the Riccati equations

| (6.3) | ||||||

for and

A standard calculation shows that the solution of the Riccati equations (6.3) is

| (6.4) | ||||

where and . Furthermore, for the Heston model, the function is given by

| (6.5) |

Remark 6.2.

The log-Laplace transform of the Heston model converges to the log-Laplace transform of an NIG process [Barndorff-Nielsen, 1997], which is complex-analytic on a strip around the real axis, thus allowing to apply Theorem 5.4.

The following proposition describes the effect of the time dependent Esscher transform on the dynamics of the Heston model.

Proposition 6.3.

Let and the measure given by

Under , the dynamics of the -Heston process becomes

| (6.6) | ||||||

where is 2-dimensional correlated -Brownian motion, , and and are defined iteratively as

and where, denoting ,

Proof.

Denote

Then

The dynamics of can then be expressed using Itō’s Lemma as

By Girsanov’s theorem,

is a 2-dimensional Brownian motion under the measure . Replacing in eq. (6.2) by gives the result. ∎

Remark 6.4.

Prop. 6.3 shows that the time-dependent Esscher transform changes a classical Heston process into a Heston process with time-inhomogeneous drift.

Remark 6.5.

Note that Assumption 2 is verified in the Heston model only when . Indeed, , where

while

However, since the actual variance reduction problem is itself unsolvable, our goal is to find a good candidate measure that we can test numerically. The fact that we do not have the full theory to justify it is therefore not problematic.

6.1.1. Numerical results for European put options

In this case, by Prop. 5.5 with and , has support on . Using the abuse of notation , we have

| (6.7) | ||||

In order to obtain , we therefore differentiate (6.7) with respect to and equate the derivative to 0 by dichotomy .

We simulate trajectories of the Heston model with parameters , , , and initial values and , under both , eq. (6.2), and , eq. (6.6), with and , using a standard Euler scheme with 200 discretization steps. For the -realisations , we calculate the European put price as

and for the -realisations , as

| (6.8) |

Each time, we compute the -standard deviation, the variance ratio and the adjusted variance ratio, i.e. the variance ratio divided by the ratio of simulation time. The latter measures the actual efficiency of the method, given the fact that simulating under the measure change takes in general slightly more time.

In Table 1, we fix the strike to the value and let the maturity vary from to , whereas in Tables 2 and 3, we fix maturity to and to , while we let the strike vary between and . We calculate each time the price, the standard error, the variance ratio adjusted and not adjusted by the ratio of simulation time.

| Price | Std. error | Var. ratio | Adj. ratio | Time, s | |

|---|---|---|---|---|---|

| 0.25 | 0.0395 | 3.72 | 2.46 | 2.14 | 20.2 |

| 0.5 | 0.0550 | 4.54 | 3.12 | 2.83 | 19.9 |

| 1 | 0.0780 | 5.59 | 3.92 | 3.66 | 19.5 |

| 2 | 0.111 | 7.20 | 4.21 | 3.89 | 19.7 |

| 3 | 0.134 | 8.48 | 4.19 | 3.79 | 19.8 |

| Price | Std. error | Var. ratio | Adj. ratio | Time, s | |

|---|---|---|---|---|---|

| 0.5 | 0.00014 | 7.65 | 26.6 | 24.5 | 18.4 |

| 0.75 | 0.00794 | 1.34 | 6.53 | 5.91 | 18.7 |

| 1 | 0.0773 | 5.60 | 3.96 | 3.65 | 18.5 |

| 1.25 | 0.261 | 8.62 | 4.20 | 3.78 | 18.9 |

| 1.5 | 0.502 | 7.92 | 5.84 | 5.36 | 18.6 |

| 1.75 | 0.749 | 6.84 | 8.45 | 7.29 | 19.7 |

| Price | Std. error | Var. ratio | Adj. ratio | Time, s | |

|---|---|---|---|---|---|

| 0.25 | 7.1 | 1.84 | 92.0 | 70.9 | 23.1 |

| 0.5 | 0.00418 | 6.05 | 16.1 | 16.0 | 20.0 |

| 0.75 | 0.0369 | 3.43 | 6.67 | 6.00 | 20.4 |

| 1 | 0.133 | 8.51 | 4.24 | 4.15 | 20.2 |

| 1.25 | 0.300 | 1.34 | 3.61 | 3.13 | 21.3 |

| 1.5 | 0.517 | 1.60 | 3.47 | 3.30 | 19.9 |

| 1.75 | 0.755 | 1.64 | 3.89 | 3.53 | 19.9 |

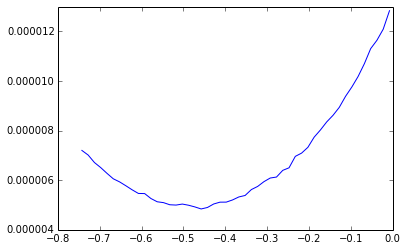

In all the cases, we can see that the variance ratio becomes very interesting when the option gets deeply out of the money and less significant, yet still very interesting, when the option is at or in the money. This corresponds to the natural behaviour of variance reduction techniques that involve measure changes, as the measure change is going to increase the probability of choosing a trajectory that is eventually going to enter the money. Note that the simulation time is only slightly larger when simulating with the measure change, while the time required for the optimization procedure is negligible compared with the simulation time. In Figure 6.1, we fix the maturity to and plot the empirical variance of the estimator (6.8) as a function of . Our method provides as asymptotically optimal measure change. We can therefore see that the asymptotically optimal is very close to the optimal one.

6.1.2. Numerical results for Asian put options

We now consider the case of a (discretized) Asian put option. Here, the log-payoff is

where . By Prop. 5.5, the support of is and we can denote . Using Prop. 6.1 and eq. (6.5), the function that we need to minimize is

or, alternatively, denoting ,

By differentiating with respect to , we obtain, for ,

| (6.9) | ||||

while, for , we have

| (6.10) | ||||

Finally, taking the exponential in eqs. (6.9) and (6.10), we obtain

Finally, define the real function that associates to

where and iteratively,

Equating to 0 by dichotomy then gives the asymptotically optimal measure.

Again, we simulate trajectories of the Heston model with parameters , , , and initial values and , under both , eq. (6.2), and , eq. (6.6), with and , using a standard Euler scheme with 200 discretization steps. For the -realisations , we calculate the Asian put price as

| (6.11) |

and for the -realisations , as

| (6.12) |

Again, each time, we compute the -standard deviation and the adjusted and non-adjusted variance ratios. In Table 4, we fix maturity to and let the strike vary between and .

| Price | Std. error | Var. ratio | Adj. ratio | Time, s | |

|---|---|---|---|---|---|

| 0.6 | 3.466 | 4.13 | 16.9 | 14.6 | 19.9 |

| 0.7 | 0.000562 | 2.60 | 5.77 | 4.77 | 21.1 |

| 0.8 | 0.00414 | 9.64 | 4.36 | 3.77 | 20.1 |

| 0.9 | 0.0185 | 0.00024 | 3.48 | 3.09 | 20.6 |

| 1 | 0.0558 | 0.00043 | 3.49 | 3.07 | 20.1 |

| 1.1 | 0.120 | 0.00057 | 3.69 | 3.20 | 20.1 |

| 1.2 | 0.206 | 0.00062 | 4.27 | 3.80 | 19.7 |

| 1.3 | 0.301 | 0.00059 | 5.30 | 4.41 | 21.0 |

The conclusion is the same as for the European put option. Indeed, the variance ratio explodes when the option moves away from the money. Due to the time-dependence of the measure change, the adjusted variance ratio is consistently around 13% below its non-adjusted version. The adjusted variance ratio remains however very interesting, with values above 3 around the money.

6.2. European put options in the Heston model with negative exponential jumps

We now consider the Heston model with negative exponential jumps

| (6.13) | ||||||

where are standard -Brownian motions and is an independent compound Poisson process with constant jump rate and jump distribution , i.e. the Lévy measure of is . The martingale condition on imposes . The Laplace transform of is

where satisfy the Riccati equations

| (6.14) | ||||||

for , where , and

Again, a standard calculation shows that the solution of the generalized Riccati equations (6.14) is

| (6.15) | ||||

where and . Furthermore, for the Heston model with negative jumps, the function is given by

| (6.16) |

Let us now study the effect of the Esscher transform on the dynamics of the Heston model with jumps.

Proposition 6.6.

Let be the measure given by

Under , the dynamics of the -Heston process with jumps becomes

| (6.17) | ||||||

where is 2-dimensional correlated -Brownian motion, and are given in (6.15),

and is a compound Poisson process with jump rate and jump distribution under .

Proof.

Denote

The dynamics of can then be expressed using Itō’s Lemma as

and Girsanov’s theorem then shows that

is a 2-dimensional Brownian motion under the measure . Replacing in eq. (6.2) by gives eq. (6.17). In order to finish the proof, it remains to show that the jump process has the desired distribution under . Let us calculate the -Laplace transform of :

By independence of the jumps,

where . Furthermore, is a standard Heston process without jumps. Therefore comparing (6.4) and (6.15), we find that

Using the fact that and

(see eq. (2.1) in [Keller-Ressel, 2011]), we finally obtain

which is indeed the Laplace transform of a compound Poisson process with jump rate and -distributed jumps. ∎

6.2.1. Numerical results for the European put option

Similarly to the case of the Heston model without jumps, denoting , we have

| (6.18) | ||||

and we obtain the asymptotically optimal by differentiating (6.18) with respect to and equating the derivative to 0 by dichotomy .

We simulate trajectories of the Heston model with jumps with parameters , , , , , and initial values and , under both , eq. (6.13), and , eq. (6.17), using a standard Euler scheme with 200 discretization steps. For the -realisations , we calculate the standard Monte-Carlo estimator of the European put price and for the -realisations , we use (6.8) where and are given in (6.15) and compute the same statistics as in the previous examples.

In Table 5, we fix the strike to the value and let the maturity vary from to , whereas in Tables 6 and 7, we fix the maturity to and to , while we let the strike vary between and .

| Price | Std. error | Var. ratio | Adj. ratio | Time, s | |

|---|---|---|---|---|---|

| 0.25 | 0.0945 | 9.96 | 3.28 | 3.00 | 23.6 |

| 0.5 | 0.147 | 1.28 | 3.20 | 2.99 | 24.5 |

| 1 | 0.215 | 1.61 | 2.95 | 2.77 | 24.7 |

| 2 | 0.309 | 2.04 | 2.61 | 2.43 | 24.7 |

| 3 | 0.374 | 2.30 | 2.40 | 2.20 | 25.0 |

| Price | Std. error | Var. ratio | Adj. ratio | Time, s | |

|---|---|---|---|---|---|

| 0.25 | 0.00606 | 7.83 | 11.6 | 10.4 | 25.8 |

| 0.5 | 0.0377 | 4.03 | 5.42 | 5.28 | 24.7 |

| 0.75 | 0.105 | 9.44 | 3.76 | 3.19 | 27.3 |

| 1 | 0.215 | 1.61 | 2.93 | 2.89 | 26.1 |

| 1.25 | 0.369 | 2.26 | 2.65 | 2.46 | 25.4 |

| 1.5 | 0.550 | 2.80 | 2.43 | 2.24 | 24.9 |

| 1.75 | 0.766 | 3.05 | 2.57 | 2.44 | 24.6 |

| Price | Std. error | Var. ratio | Adj. ratio | Time, s | |

|---|---|---|---|---|---|

| 0.25 | 0.0280 | 2.69 | 5.19 | 4.99 | 24.8 |

| 0.5 | 0.108 | 8.60 | 3.32 | 3.05 | 25.1 |

| 0.75 | 0.226 | 1.58 | 2.68 | 2.56 | 26.3 |

| 1 | 0.374 | 2.31 | 2.39 | 2.20 | 27.0 |

| 1.25 | 0.545 | 3.01 | 2.20 | 2.19 | 25.2 |

| 1.5 | 0.730 | 3.66 | 2.09 | 1.94 | 24.6 |

| 1.75 | 0.932 | 4.27 | 1.97 | 1.83 | 24.8 |

When adding negative jumps to the Heston model, one can see that the variance ratio diminishes. When the options are out of the money however it is still sufficiently important to make it interesting to use in applications. In Figure 6.2, we fix the maturity to and plot again the empirical variance of the estimator (6.8) as a function of for the Heston model with jumps. The method provides as asymptotically optimal measure change which is, as in the continuous case, very close to the optimal one.

References

- [Barndorff-Nielsen, 1997] Barndorff-Nielsen, O. E. (1997). Processes of normal inverse Gaussian type. Finance and Stochastics, 2(1):41–68.

- [Barndorff-Nielsen and Shephard, 2001] Barndorff-Nielsen, O. E. and Shephard, N. (2001). Non-Gaussian Ornstein–Uhlenbeck-based models and some of their uses in financial economics. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 63(2):167–241.

- [Bates, 1996] Bates, D. S. (1996). Jumps and stochastic volatility: Exchange rate processes implicit in Deutsche mark options. The Review of Financial Studies, 9(1):69–107.

- [Dembo and Zeitouni, 1998] Dembo, A. and Zeitouni, O. (1998). Large Deviations Techniques and Applications. Springer, Application of Mathematics, second edition.

- [Duffie et al., 2003] Duffie, D., Filipovic, D., and Schachermayer, W. (2003). Affine processes and applications in finance. The Annals of Applied Probability, 13(3):984–1053.

- [Dupuis and Wang, 2004] Dupuis, P. and Wang, H. (2004). Importance sampling, large deviations, and differential games. Stochastics: An International Journal of Probability and Stochastic Processes, 76(6):481–508.

- [Genin and Tankov, 2016] Genin, A. and Tankov, P. (2016). Optimal importance sampling for Lévy processes. Preprint, arXiv: 1608.04621.

- [Glasserman et al., 1999] Glasserman, P., Heidelberger, P., and Shahabuddin, P. (1999). Asymptotically optimal importance sampling and stratification for pricing path-dependent options. Mathematical Finance, 9(2):117–152.

- [Guasoni and Robertson, 2008] Guasoni, P. and Robertson, S. (2008). Optimal importance sampling with explicit formulas in continuous time. Finance and Stochastics, 12(1):1–19.

- [Heston, 1993] Heston, S. L. (1993). A closed-form solutions for options with stochastic volatility with applications to bond and currency options. Review of Financial Studies, 6(2):327–343.

- [Jacquier et al., 2013] Jacquier, A., Keller-Ressel, M., and Mijatović, A. (2013). Large deviations and stochastic volatility with jumps: asymptotic implied volatility for affine models. Stochastics: An International Journal of Probability and Stochastic Processes, 85(2):321–345.

- [Keller-Ressel, 2011] Keller-Ressel, M. (2011). Moment explosions and long-term behavior of affine stochastic volatility models. Mathematical Finance, 21(1):73–98.

- [Léonard, 2000] Léonard, C. (2000). Large deviations for Poisson random measures and processes with independent increments. Stochastic Processes and their Applications, 85(1):93–121.

- [Robertson, 2010] Robertson, S. (2010). Sample path large deviations and optimal importance sampling for stochastic volatility models. Stochastic Processes and their Applications, 120(1):66–83.

- [Rockafellar, 1971] Rockafellar, R. T. (1971). Integrals which are convex functionals. II. Pacific Journal of Mathematics, 39(2):439–469.