Optimal Dynamic Basis Trading

Abstract

We study the problem of dynamically trading a futures contract and its underlying asset under a stochastic basis model. The basis evolution is modeled by a stopped scaled Brownian bridge to account for non-convergence of the basis at maturity. The optimal trading strategies are determined from a utility maximization problem under hyperbolic absolute risk aversion (HARA) risk preferences. By analyzing the associated Hamilton-Jacobi-Bellman equation, we derive the exact conditions under which the equation admits a solution and solve the utility maximization explicitly. A series of numerical examples are provided to illustrate the optimal strategies and examine the effects of model parameters.

Keywords: futures stochastic basis cash and carry scaled Brownian bridge risk aversion

JEL Classification C41 G11 G12

1 Introduction

Basis trading, also known as cash-and-carry trading in the context of futures contracts, is a core strategy for many speculative traders who seek to profit from anticipated convergence of spot and futures prices. The practice usually involves taking a long position in the under-priced asset and a short position in the over-priced one, and closing the positions when convergence occurs. In reality, however, basis trading is far from a riskless arbitrage. Unexpected changes in market factors such as interest rate, cost of carry, or dividends can diminish profitability. Moreover, market frictions, such as transaction costs and collateral payments, can turn seemingly certain arbitrage opportunities into disastrous trades. It is also possible that the basis does not converge at maturity. This non-convergence phenomenon was commonly observed in the grains markets. As reported in Irwin et al. (2011), Adjemian et al. (2013), and Garcia et al. (2015), for most of 2005-2010 futures contracts expired up to 35% above the spot price. As a result, some cash-and-carry traders may choose to close their positions prior to maturity to limit risk exposure.

Early works on pricing of futures contracts, such as Cox et al. (1981) and Modest and Sundaresan (1983), established no-arbitrage relationships between the spot price and associated futures prices. Assuming imperfections, such as transaction cost, these relationships take the form of pricing bounds, which can be used for identifying profitable trades. Among related studies on basis trading, Brennan and Schwartz (1988) and Brennan and Schwartz (1990) assumed that the basis of an index futures follows a scaled Brownian bridge and that trading the assets is subject to position limits and transaction costs. They calculated the value of the embedded timing options to trade the basis, and used the option prices to devise open-hold-close strategies involving the index futures and the underlying index. Also under a Brownian bridge model, Dai et al. (2011) provided an alternative strategy and specification of transaction costs. Another related work by Liu and Longstaff (2004) assumed that the basis follows a scaled Brownian bridge and the investor is subject to a collateral constraint. They derived the closed-form strategy that maximizes the expected logarithmic utility of terminal wealth, and showed the optimality of taking smaller arbitrage positions well within the collateral constraint.

In the aforementioned studies on optimal basis trading, the market model contains arbitrage. Indeed, it is assumed that the basis, which is a tradable asset, converges to zero at a fixed future time. In this paper, we consider a different scenario where the basis does not vanish at maturity. More precisely, we model the stochastic basis by a scaled Brownian bridge that is stopped before its achieves convergence. Our proposed model is motivated by the market phenomenon of non-convergence as well as the possibility of traders closing their futures positions prior to maturity. It also has the added advantage that it generates an arbitrage-free futures market (see Proposition 2.5 below).

We consider a general class of risk preferences by using hyperbolic absolute risk aversion (HARA) utility functions which includes power (CRRA) and exponential (CARA) utilities. We exclude, however, the case of decreasing risk-tolerance functions and, in particular, the quadratic utility function. Among our findings, we derive in closed form the optimal dynamic basis trading strategy maximizing the expected utility of terminal wealth. In solving our portfolio optimization problem, the critical question of well-posedness arises. To that end, we find the exact conditions under which the maximum expected utility is finite. For the case where the expected utility explodes, we derive the critical investment horizon at which the explosion happens. See Section 3 for further details. Note that achieving infinite expected utility has been observed in the following contexts: infinite horizon portfolio optimization (Merton (1969)), optimal execution (Bulthuis et al. (2017)), and finite horizon optimal trading of assets with mean-reverting return (Kim and Omberg (1996);Korn and Kraft (2004)). The latter studies, respectively, have coined the terms “nirvana strategies” and “I-unstable” for investment strategies that yield infinite expected utility in finite investment horizon.

Our model is related to a number of studies in finance involving Brownian bridges. Applications include modeling the flow of information in the market. For example, Brody, Hughston, and Macrina (2008) used a Brownian bridge as the noise in the information about a future market event, and derived option pricing formulae based on this asset price dynamics and market information flow. Cartea, Jaimungal, and Kinzebulatov (2016) utilized a randomized Brownian bridge (rBb) to model the mid-price of an asset with a random end-point perceived by an informed trader, and determined the optimal placements of market and limit orders. Leung, Li, and Li (2018) also applied a rBb model to investigate the optimal timing to sell different option positions.

Basis trading involves trading a single futures contract along with its spot asset. A similar alternative strategy is to trade multiple futures with the spot but different maturities. For instance, Leung and Yan (2018, 2019) considered futures prices generated from the same two-factor stochastic spot model and optimize dynamic trading strategies. In optimal convergence trading, asset prices or their spreads are often modeled by a stationary mean-reverting process. See, for example, Kim and Omberg (1996), Korn and Kraft (2004), Mudchanatongsuk et al. (2008), Chiu and Wong (2011), Liu and Timmermann (2013), Tourin and Yan (2013), Cartea and Jaimungal (2016), Lee and Papanicolaou (2016), Leung and Li (2016), Kitapbayev and Leung (2018), and Cartea et al. (2018). In these studies, however, prices or spreads are not scheduled to converge at a future time. Using a scaled Brownian bridge, we can control the basis’s tendency to converge towards the expiration date.

The rest of the paper is organized as follows. In Section 2, we introduce our market model and formulate the dynamic basis trading problem. In Section 3, we solve the associated Hamilton-Jacobi-Bellman partial differential equation. Section 4 contains our results on the optimal basis trading strategy, along with a series of illustrative numerical examples. Section 5 concludes. Longer proofs are included in the Appendix.

2 Problem setup

We consider an investor who trades a riskless asset, a futures contract with maturity and its underlying asset , over a period . For simplicity, we assume that does not pay dividends and has no storage cost. We also assume that the interest rate is zero, by taking the riskless asset as the numeraire. Under these assumptions, the futures price, the forward price, and the spot price should be equal. In practice, however, market frictions and inefficiencies may render futures price different from the spot or forward price. As discussed above, the futures price may not even converge to the spot price at maturity.

Motivated by these market imperfections, we propose a stochastic model that incorporates the comovements of the futures and spot prices, and captures the tendency of the basis to approach zero but not necessarily vanish at maturity. In essence, the spot and futures prices are drive by correlated Brownian motions and the stochastic basis is represented by scaled Brownian bridge, as we will show in Lemma 2.2 below.

To describe our model, we assume that the volatility normalized111See Remark 2.1. futures price and the volatility normalized spot price satisfy

| (2.1) | ||||

| and | ||||

| (2.2) | ||||

| where is the log-value of the stochastic basis defined by | ||||

| (2.3) | ||||

Here, is a standard Brownian motion in a filtered probability space where is generated by the Brownian motion and satisfies the usual conditions. The parameters, and , with , represent the Sharpe ratios of and respectively (see Remark 2.1 below). As specified in (2.2), the futures price has the tendency to revert around . Indeed, if is significantly higher than , then becomes negative. Consequently, the drift of can also be negative, and thus driving the value of downward to be closer to . The opposite will hold if is significantly lower than . The speed of this mean reversion is reflected by the constant . On the other hand, the two prices need not coincide at maturity. The level of non-convergence is controlled by the parameter . A smaller means that at maturity and tend to be closer. In fact, if , and will be exactly the same. Lastly, we incorporate correlation between the two price processes through the parameter .

Remark 2.1.

Let satisfying

| (2.4) |

be the quoted price of an asset. The “volatility normalized price” of the asset is given by

| (2.5) |

such that the volatility of is 1.

Furthermore, let be the amount invested in the asset. The “volatility adjusted position” in asset is given by such that

| (2.6) |

In other words, when working with volatility normalized prices, volatility adjusted positions should be used. To find the $ positions, we only need to divide the volatility adjusted positions by volatility, i.e. .

For the rest of the article, we use the terms prices and positions in place of volatility normalized prices and volatility adjusted positions.

As we show in the following lemma, the price dynamics (2.1) and (2.2) imply that the stochastic basis is a scaled Brownian bridge that converges to zero at . This implies that and converge at , i.e. , -almost surely. However, since the futures contract expires at and is past maturity, such a convergence is not realized in the market. In a limiting case of our model where , the spot and future prices converge at and the market model admits arbitrage. In contrast, for any , the market is arbitrage-free. See Proposition 2.5 and Remark 2.6 below.

Lemma 2.2.

The stochastic basis satisfies

| (2.7) |

for . In particular, if we consider the solution of this SDE over , then , -almost surely.

Proof.

Remark 2.3.

As a corollary, we now describe the distribution of the basis .

Corollary 2.4.

Assume that is deterministic. Then, the basis is a Gauss-Markov process with mean function

| (2.10) | ||||

| and covariance function | ||||

| (2.11) | ||||

for all . Here, is given by (2.9).

Proof.

This result follows from direct calculations using (2.8). ∎∎

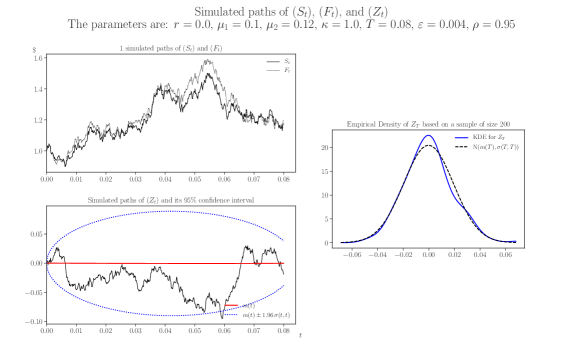

From Corollary 2.4, it follows that . Furthermore, as , we have and . Using Lemma 2.2 and its corollary, it is straightforward to devise a time-discretization scheme to simulate the paths of , , and , as shown in Figure 1. As a confirmation, we see the empirical density of based on 200 simulated paths closely matching with the theoretical density, i.e. .

Next, we prove that our market model is arbitrage-free. Let us first define the market price of risk function

| (2.12) |

for , where

| (2.13) |

Proposition 2.5.

Proof.

See Appendix A. ∎∎

Proposition 2.5 shows the importance of having . For , the market model (2.1)-(2.2) is not arbitrage-free. Indeed, setting in the proof of Lemma 2.2 yields that . Therefore, if there is a risk-neutral measure , then we must have

| (2.15) |

Remark 2.6.

We now discuss the dynamic trading problem faced by the investor. Let be the cash amount invested in , and the notional value222That is, the number of futures contracts held multiplied by the futures price. invested in , for . Define the volatility adjusted positions333See Remark 2.1. by , , where and are the volatilities of the spot and futures prices, respectively. Then, the trading wealth follows

| (2.16) | ||||

| (2.17) | ||||

| (2.18) |

for , and with .

Next, we define the set of admissible trading strategies.

Definition 2.7.

For constants , define the set as follows

| (2.19) |

We denote by the set of all -adapted processes, denoted by , such that

-

(i)

, -a.s.,

-

(ii)

-a.s. for all , where is given by (2.16),

-

(iii)

is uniformly bounded from below, -a.s.

Note that for , Condition (ii) becomes -a.s. for all , which makes Condition (iii) redundant. For , Condition (ii) is redundant since the corresponding utility imposes no constraint on the wealth process. Therefore, for , Condition (iii) is needed to exclude doubling strategies.

In order to maximize the expected utility of terminal wealth, the investor solves the stochastic control problem

| (2.20) |

where . Here, is a hyperbolic absolute risk aversion (HARA) utility function whose risk tolerance function admits the form:

| (2.21) |

We furthermore assume that, for ,

| (2.22) |

Note that any HARA utility, except the logarithmic utility (i.e. ), can be shifted by a constant such that (2.22) is satisfied. This result is trivial for (i.e. exponential utility). The following lemma makes precise this observation for . Hence, condition (2.22) results in no loss in generality.

Lemma 2.8.

Proof.

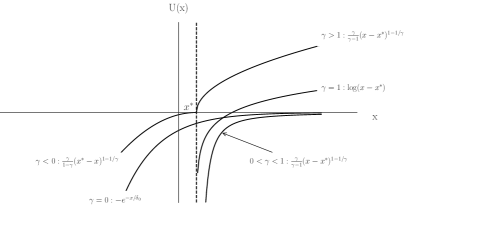

Figure 2 illustrates examples of HARA utility functions for different values of . Specifically, corresponds to power utilities, leads to the logarithmic utility, yields the exponential utility, and yields the quadratic utility. Note that we have excluded from our model the case of HARA utility functions with decreasing risk tolerance function, such as quadratic utility.

3 HJB equation

As we will show in Section 4, the value function in (2.20) coincides with the classical solution of the following terminal value problem on :

| (3.1) |

where the differential operator is given by

| (3.2) | ||||

for any and any function with continuous derivatives and .

3.1 Well-posedness Conditions

For the rest of this section, we derive the solution for the nonlinear Hamilton-Jacobi-Bellman (HJB) equation (3.1). As it turns out, this equation does not admit a solution for all parameter values. This leads us to determine and study the exact conditions under which (3.1) has a solution. To prepare for our results, we define the constant

| (3.3) |

Note that , and since we have assumed that and . We now identify the following cases:

-

(i)

For , (3.1) is “ill-posed” in the sense that it has a solution only if , where is given below.

-

(ii)

For , (3.1) is “well-posed” in the sense that it has a unique solution for all values of .

-

(iii)

For , (3.1) is “ill-posed” (resp. “well-posed”) if (resp. ). For , we have and the interval is empty.

These cases are derived from Theorem 3.3 below.

Achieving infinite expected utility (EU) has been observed in the context of infinite horizon portfolio choice problem (e.g. Merton (1969)), optimal execution (e.g. Bulthuis et al. (2017)), and finite horizon optimal trading of assets with mean-reverting returns (e.g. Kim and Omberg (1996) and Korn and Kraft (2004)). The last two studies, respectively, have coined the terms “nirvana strategies” and “I-unstable” for investment strategies that yield infinite expected utility over a finite horizon.

In reality, however, investors don’t achieve infinite EU; otherwise they would drive the prices out of equilibrium. This implies that either: (1) there is no investor with risk tolerance parameter that leads to infinite EU; (2) such an investor exists but the market parameters (that is, and ) are such that those investors don’t have enough time to achieve infinite EU (i.e. for all agents); or (3) market imperfections (such as transaction cost or parameter ambiguity) prevent investors from achieving infinite EU.

3.2 Value Function

Our solution to the HJB equation (3.1) will involve the solution of the following Riccati equation

| (3.4) |

There is an explicit solution to (3.4), as summarized in Lemma 3.1 below. To prepare for the result, we introduce the following notations. We define the “discriminant” as follows

| (3.5) |

Furthermore, the “escape time” is given by:

-

(i)

If , then

(3.6) -

(ii)

If and , then

(3.7) -

(iii)

If and , then

(3.8) -

(iv)

for all other values of .

The escape time plays a critical role in the Riccati equation (3.4).

Lemma 3.1.

The Riccati equation (3.4) has a solution only if . In particular, if , then and the solution is

| (3.9) |

If , then and the solution is

| (3.10) |

If , then .

The proof is by direct substitution, and thus omitted.

Remark 3.2.

Note that as , we have for cases (i)-(iii). This is consistent with the scenario where there is arbitrage in the limit .

Now, we present the value function in explicit form.

Theorem 3.3.

Proof.

See Appendix B. ∎

Next, we verify that the value function coincides with the solution of the HJB equation (3.1) from Theorem 3.3. We also identify the optimal trading strategy.

Theorem 3.4.

Proof.

See Appendix C. ∎

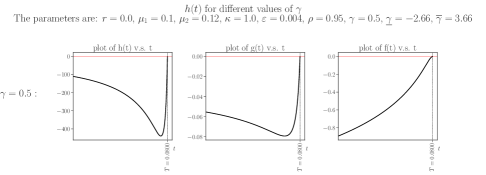

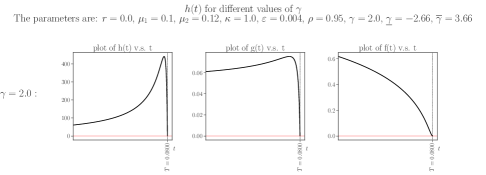

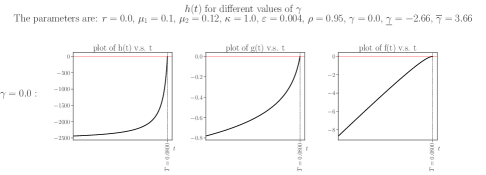

Figures 3 illustrates the behaviors of functions , , and under three well-posed scenarios. We have set and such that the critical risk tolerance value is . Each row of the figure shows the functions for different value of , namely , , and . Note that since , the values of in the interval are well-posed. In the exponential case (i.e. ), monotonically increases to zero. For the power cases (i.e. ), is not monotone and reaches a maximum of high value before reaching zero. For large values of (i.e. the left end on the x-axis), seems to flatten. In terms of behaviors, appears to have similar properties to , although the values and variations of is significantly less. In all three scenarios, moves monotonically to zero over time.

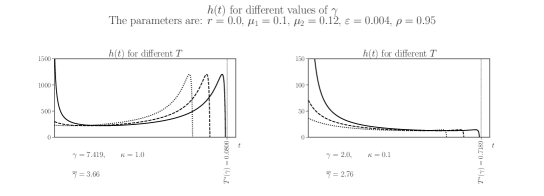

In Figure 4, we consider two ill-posed scenarios. Specifically, we plot over time for (the left panel) and and (the right panel). In each plot, is plotted for three choices of , which are, respectively, (dotted curve), (dashed curve), and (solid curve) of the escape time . As expected for these ill-posed cases, we see that , leading the expected utility to reach over a finite investment horizon.

4 Optimal basis trading strategy

Let us examine the optimal trading strategy in (3.16). Recall from Remark 2.1 that is the volatility adjusted position. The actual position value is given by , where and are the volatility of the spot and futures prices, respectively.

Our first observation is that is directly proportional to the risk-tolerance function , as has been observed in other studies such as Karatzas and Shreve (1998) and Zariphopoulou (2001). In other words, the larger the risk-tolerance, the larger the optimal positions in (3.16). If we consider the special case with , then it follows that , and the optimal strategy reduces to

| (4.1) |

This simple strategy does not depend on . This makes sense because, when , disappears in the SDE for (see (2.2)). One can loosely interpret as the Merton strategy. More generally, when , the incorporation of the scaled Brownian bridge in makes the optimal strategy dependent on the time varying functions and as well as the stochastic factor .

According to (3.16), for fixed values of and , and are affine functions of , with the slopes given by and respectively. The slope of this function has an interesting interpretation. Note that a positive log basis means that the spot is priced higher than the futures. To take advantage of the anticipated convergence, our strategy is to take a short position in and a long position in . The optimal strategy implies that for larger basis , the position in becomes more negative while the position in becomes more positive. Similarly, for negative values of (i.e. ), one expects to take a short position in and a long position in .

For to be a convergence trading strategy, we expect that and or, equivalently,

| (4.2) |

Let’s assume that , that is, the futures and spot prices are non-negatively correlated. Then, (4.2) is always satisfied near maturity, since . In other words, the optimal strategy always becomes a convergence trading strategy once we are close enough to maturity. It may also be the case that (4.2) is satisfied for all values of . One sufficient condition is (and ), since Lemma 3.5 yields that for all . On the other hand, it is also possible for (4.2) to be violated for some parameter values or for far enough from maturity. We show an example of such a case below.

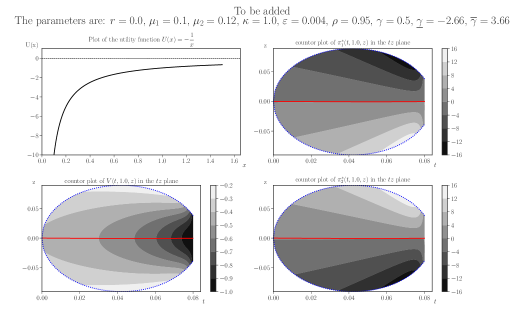

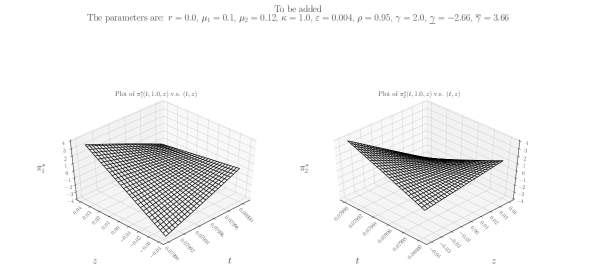

Figure 5 illustrates the optimal value function and optimal trading strategies for the HARA utility (i.e. ). Setting , we consider the contour plot of the value function for different values of . It is decreasing in and increasing as deviates from zero. This is intuitive since a longer time to maturity or larger basis implies more potential for making profits. The 95% confidence region of , i.e. , shows that has larger variance near the midpoint of the trading horizon.

The top and bottom right plot of Figure 5 illustrate the optimal positions and over values of in the 95% confidence region. Note that for fixed and and as , position sizes (i.e. , ) increase and then decrease. The reason for this behavior can be seen from the corresponding function in Figure 3, where reached a maximum before vanishing at . Furthermore, note that for fixed and , is decreasing in , while is increasing in . As mentioned above, this is because and (4.2) is satisfied.

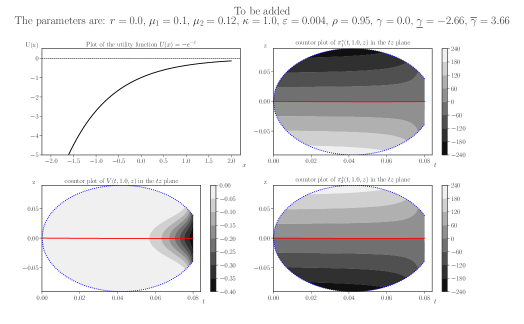

Figure 6 corresponds to the case with exponential utility (i.e. ). Note that the value function and optimal positions are much less sensitive to up till near maturity. Furthermore, the positions appear to change monotonically as time approaches maturity. This is in contrast to the power utility case where position sizes first peak then decrease towards maturity.

In the previous two examples with and , the optimal strategies implies convergence trading in that is decreasing and is increasing in . This was expected since and and (4.2) was satisfied.

Next, we consider a case where (4.2) does not hold for all values of . With the utility function (i.e. ), the chosen parameter values, and , imply that . Thus, does not satisfy (4.2) (see also Figure 3). From Figure 7, we observe that at time away from maturity (say, ), is increasing in while is decreasing. In particular, for large positive values of , meaning that the spot is higher priced than the futures, it is optimal to long and short . This is in contrast to a typical convergence trading strategy. Nevertheless, the optimal strategy from our model eventually becomes convergence trading as time approaches maturity.

To better understand the optimal trading strategy near maturity, we note that the mean reversion rate of the Brownian bridge, i.e. , is time varying and becomes much larger near maturity . Therefore, the force of mean reversion will quickly eliminate any deviation of the stochastic basis from its mean. As a result, convergence trading is optimal near maturity. However, further away from maturity, the mean reversion rate is much smaller, so any deviation of the stochastic basis from its mean would take longer to get corrected. As it turns out, for a sufficiently risk seeking investor (i.e. ), it is optimal to bet on the deviation from the mean not to get immediately corrected. The optimal position for this case is based on the expectation that the basis will diverge (or not immediately converge). Hence, the position is the opposite of a convergence trading.

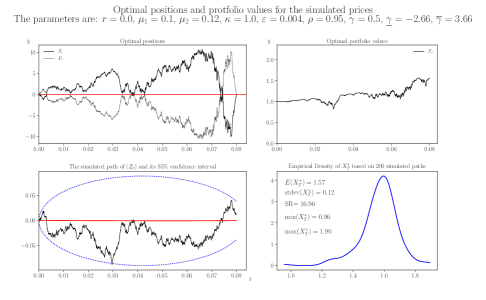

Figure 8 illustrates the optimal positions in and , along with the corresponding portfolio value, based on the simulated paths and parameters from Figure 1. In this well-posed scenario with (), the optimal positions take opposite signs and tend to move in opposite directions. Moreover, whenever the basis is negative, the position in is positive and position in is negative. The positions are reversed when is positive. Furthermore, the optimal positions fluctuate increasingly more rapidly and more sensitive to the basis near maturity.

In Figure 8 we also see the optimal portfolio value over time. Note that portfolio experience significant drawdowns as diverges from equilibrium. This is a common characteristic of convergence trading strategies. The bottom right plot of Figure 8 shows the empirical density of the optimal terminal wealth , based on 200 simulated paths, all of which started with the initial wealth . The estimated expected value of terminal wealth is , with an standard deviation of . Since the trading horizon is 20/250 = 0.08 year (i.e. one month), the annualized net expected return is and the annualized volatility is . This leads to a Sharpe ratio of for this simulated example.

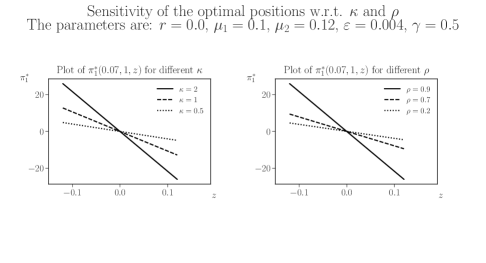

Turning to the value function, we show in Figure 9 its sensitivity with respect to and . For simplicity, we keep and fixed and show as a function of . All other parameters (including the utility function) are as in Figure 5. The value function tends to reach its minimum value at , and a higher means a higher value function in the figure. This is intuitive since a higher speed of mean reversion indicates higher profitability from trading the basis at any given level. On correlation increases, the expected utility improves in case of a large mispricing in the assets (i.e. large values of ) and it decreases when mispricing is small (i.e. for values near zero). This also makes sense. Note that by (2.7), the volatility of the basis is , which is decreasing in . Therefore, large correlation indicates less noise in the basis. If there is no mispricing, less noise means less probability of mispricing which lowers the profitability of basis trading. However, if there is a large mispricing, then less noise means that the mispricing will be corrected faster, which increases the profitability and the expected utility.

Figure 10 shows the sensitivity of the optimal spot position with respect to the parameters and . For different values of and , we see that is a decreasing function of . A higher mean-reversion rate or higher correlation makes more downward sloping in , which means that the investor will take a larger long (resp. short) position when is negative (resp. positive). The financial intuition is as follows. A higher means that the basis tends to converge to zero faster. This represents a more profitable trade, leading the investor to take a larger position in the basis. When the basis is negative, the spot price is below the futures price, so the optimal strategy is to long the spot. The opposite holds when the basis is positive. Increasing decreases the random fluctuations in the basis, which also implies that the basis will show a stronger tendency to converge. Hence, it is optimal to take a larger position.

5 Concluding Remarks

In summary, we have analyzed dynamic trading problem in which a risk-averse investor trades the stochastic basis to maximize expected utility. We describe the non-convergent basis process by a stopped scaled Brownian bridge. This leads us to solve analytically and numerically the associated HJB equation and illustrate the optimal trading strategies.

There are a number of directions for future research. In addition to basis trading, one can analyze other futures trading strategies, including futures rolling, and futures portfolios. Futures are also commonly used in many exchange-traded funds (ETFs) for tracking the spot price (see e.g. Leung and Ward (2015)). It would also be interesting to consider variations of our model. For example, in (2.1) and (2.2), one could interpret that the spot price is instantaneously leading the futures price in that the futures does not have any feedback on the spot. This is a question of price discovery, and we refer to the empirical studies, Chan (1992), Kawaller et al. (1987), and Stoll and Whaley (1990) for more background. It is possible to adapt our solution method by interchanging the leading roles of and , and more generally incorporate more sophisticated lead-lag effects between futures and spot prices into the trading problem.

References

- Adjemian et al. (2013) Adjemian, M. K., P. Garcia, S. Irwin, and A. Smith (2013). Non-convergence in domestic commodity futures markets: Causes, consequences, and remedies. US Department of Agriculture, Economic Research Service 115, 155381.

- Brennan and Schwartz (1988) Brennan, M. J. and E. S. Schwartz (1988). Optimal arbitrage strategies under basis variability. In M. Sarnat (Ed.), Essays in Financial Economics. North Holland.

- Brennan and Schwartz (1990) Brennan, M. J. and E. S. Schwartz (1990). Arbitrage in stock index futures. The Journal of Business 63(1), S7–S31.

- Brody et al. (2008) Brody, D. C., L. P. Hughston, and A. Macrina (2008). Information-based asset pricing. International Journal of Theoretical and Applied Finance 11(01), 107–142.

- Bulthuis et al. (2017) Bulthuis, B., J. Concha, T. Leung, and B. Ward (2017). Optimal execution of limit and market orders with trade director, speed limiter, and fill uncertainty. International Journal of Financial Engineering 4(2-3), 1750020.

- Cartea et al. (2018) Cartea, Á., L. Gan, and S. Jaimungal (2018). Trading cointegrated assets with price impact. Mathematical Finance, Forthcoming 2018, arXiv:1807.01428 [q-fin.TR].

- Cartea and Jaimungal (2016) Cartea, Á. and S. Jaimungal (2016). Algorithmic trading of co-integrated assets. International Journal of Theoretical and Applied Finance 19(06), 1650038.

- Cartea et al. (2016) Cartea, Á., S. Jaimungal, and D. Kinzebulatov (2016). Algorithmic trading with learning. International Journal of Theoretical and Applied Finance 19(4), 1650028.

- Chan (1992) Chan, K. (1992). A further analysis of the lead–lag relationship between the cash market and stock index futures market. The Review of Financial Studies 5(1), 123–152.

- Cheridito et al. (2005) Cheridito, P., D. Filipović, and M. Yor (2005). Equivalent and absolutely continuous measure changes for jump-diffusion processes. Ann. Appl. Probab. 15(3), 1713–1732.

- Chiu and Wong (2011) Chiu, M. and H. Wong (2011). Mean-variance portfolio selection of cointegrated assets. Journal of Economic Dynamics and Control 35, 1369–1385.

- Cox et al. (1981) Cox, J. C., J. F. Ingersoll, and S. A. Ross (1981). The relation between forward and futures price. Journal of Financial Economics 9(December), 321–346.

- Dai et al. (2011) Dai, M., Y. Zhong, and Y. K. Kwok (2011). Optimal arbitrage strategies on stock index futures under position limits. Journal of Futures markets 31(4), 394–406.

- Fleming and Soner (2006) Fleming, W. H. and H. M. Soner (2006). Controlled Markov Processes and Viscosity Solutions, Volume 25. springer New York.

- Garcia et al. (2015) Garcia, P., S. H. Irwin, and A. Smith (2015). Futures market failure? American Journal of Agricultural Economics 97(1), 40–64.

- Irwin et al. (2011) Irwin, S. H., P. Garcia, D. L. Good, and E. L. Kunda (2011). Spreads and non-convergence in chicago board of trade corn, soybean, and wheat futures: Are index funds to blame? Applied Economic Perspectives and Policy 33(1), 116–142.

- Karatzas and Shreve (1991) Karatzas, I. and S. Shreve (1991). Brownian Motion and Stochastic Calculus. Springer-Verlag.

- Karatzas and Shreve (1998) Karatzas, I. and S. Shreve (1998). Methods of Mathematical Finance, Volume 39. Springer.

- Kawaller et al. (1987) Kawaller, I. G., P. D. Koch, and T. W. Koch (1987). The temporal price relationship between S&P 500 futures and the S&P 500 index. The Journal of Finance 42(5), 1309–1329.

- Kim and Omberg (1996) Kim, S. and E. Omberg (1996). Dynamic nonmyopic portfolio behavior. The Review of Financial Studies 9(1), 141–161.

- Kitapbayev and Leung (2018) Kitapbayev, Y. and T. Leung (2018). Optimal mean-reverting spread trading: Nonlinear integral equation approach. Annals of Finance 13(2), 181–203.

- Korn and Kraft (2004) Korn, R. and H. Kraft (2004). On the stability of continuous-time portfolio problems with stochastic opportunity set. Mathematical Finance 14(3), 403–414.

- Lee and Papanicolaou (2016) Lee, S. and A. Papanicolaou (2016). Pairs trading of two assets with uncertainty in co-integration’s level of mean reversion. International Journal of Theoretical and Applied Finance 19(08), 1650054.

- Leung et al. (2018) Leung, T., J. Li, and X. Li (2018). Optimal timing to trade along a randomized Brownian bridge. International Journal of Financial Studies 6(3), 75.

- Leung and Li (2016) Leung, T. and X. Li (2016). Optimal Mean Reversion Trading: Mathematical Analysis And Practical Applications. World Scientific.

- Leung and Ward (2015) Leung, T. and B. Ward (2015). The golden target: Analyzing the tracking performance of leveraged gold ETFs. Studies in Economics and Finance 32(3), 278–297.

- Leung and Yan (2018) Leung, T. and R. Yan (2018). Optimal dynamic pairs trading of futures under a two-factor mean-reverting model. International Journal of Financial Engineering 5(3), 1850027.

- Leung and Yan (2019) Leung, T. and R. Yan (2019). A stochastic control approach to managed futures portfolios. International Journal of Financial Engineering 6(1), 1950005.

- Liu and Longstaff (2004) Liu, J. and F. A. Longstaff (2004). Losing money on arbitrage: Optimal dynamic portfolio choice in markets with arbitrage opportunities. The Review of Financial Studies 17(3), 611–641.

- Liu and Timmermann (2013) Liu, J. and A. Timmermann (2013). Optimal convergence trade strategies. Review of Financial Studies 26(4), 1048–1086.

- Merton (1969) Merton, R. C. (1969). Lifetime portfolio selection under uncertainty: The continuous-time case. Review of Economics and Statistics 51(3), 247–257.

- Modest and Sundaresan (1983) Modest, D. M. and M. Sundaresan (1983). The relationship between spot and futures prices in stock index futures markets: Some preliminary evidence. Journal of Futures Markets 3(1), 15–41.

- Mudchanatongsuk et al. (2008) Mudchanatongsuk, S., J. Primbs, and W. Wong (2008). Optimal pairs trading: a stochastic control approach. In Proceedings of the American Control Conference, Seattle, Washington, pp. 1035–1039.

- Stoll and Whaley (1990) Stoll, H. R. and R. E. Whaley (1990). The dynamics of stock index and stock index futures returns. Journal of Financial and Quantitative analysis 25(4), 441–468.

- Tourin and Yan (2013) Tourin, A. and R. Yan (2013). Dynamic pairs trading using the stochastic control approach. Journal of Economic Dynamics and Control 37(10), 1972–1981.

- Zariphopoulou (2001) Zariphopoulou, T. (2001). A solution approach to valuation with unhedgeable risks. Finance and stochastics 5(1), 61–82.

Appendix A Proof of Proposition 2.5

This proposition follows from existing results, such as Theorem 2.4 of Cheridito et al. (2005). For readers’ convenience, we provide our own proof in our notations.

| (A.1) |

Therefore, by Girsanov’s theorem, is a risk-neutral measure if given by (2.14) is a -martingale. It only remains to show that is a -martingale.

Define the processes as follows,

| (A.2) |

and note that is a 2-dimensional standard Brownian motion. By substituting with , , in (2.14) and noting (2.12), one obtains

| (A.3) |

where and , , are some appropriately defined constants.

Next, consider the (deterministic) time change

| (A.4) | ||||

| (A.5) |

and define . Note that strictly increases from 0 to as goes from 0 to . Let us also define as the inverse of .

Using Knight’s time-change theorem (see Theorem 3.4.13 on page 179 of Karatzas and Shreve (1991)), the processes defined by

| (A.6) |

are independent standard Brownian motions. Furthermore, from (2.8), it follows that

| (A.7) |

Consider the time-changed process and note that is a martingale if and only if is a martingale. By (A.3), (A.6), and (A.7), satisfies

| (A.8) |

where we have defined the functional

| (A.9) | ||||

| (A.10) |

for any continuous function . Note that,

-

(i)

is progressively measurable in the sense of Definition 3.5.15 on page 199 of Karatzas and Shreve (1991); and,

-

(ii)

for any , there exists a constant such that

(A.11) This follows from (A.9), since and and are continuous (and, thus, bounded) on and , respectively.

With conditions (i) and (ii) above, we now apply Corollary 3.5.16 on page 200 of Karatzas and Shreve (1991) to conclude that is a martingale. Hence, is also a martingale, as we set out to prove.∎

Appendix B Proof of Theorem 3.3

Applying the operator in (3.2) to the function in (3.1), we get

| (B.1) | ||||

| (B.2) | ||||

| (B.3) |

where we defined the constants

| (B.4) |

and matrix

| (B.5) |

Assume, for now, that , for , which will hold once we show that the solution is of the desired form (3.11). Then, it follows that, for ,

| (B.6) | ||||

| (B.7) |

and the HJB equation (3.1) becomes to the second-order nonlinear PDE

| (B.8) | ||||

for and with the terminal condition . Substituting the ansatz555This ansatz can be derived through the power transformation introduced by Zariphopoulou (2001). See, also, Kim and Omberg (1996), among others.

| (B.9) |

, in (B.8) leads to the following identity involving the unknown functions , , and ,

| (B.10) | |||

| (B.11) | |||

| (B.12) |

for all and . To obtain this equation, we have used the identity

| (B.13) |

which follows directly from (2.21) and (2.22). Furthermore, substituting (B.9) in the terminal condition yields . As a result, , , and are given by

| (B.14) | ||||

| (B.15) | ||||

| and | ||||

| (B.16) | ||||

Appendix C Proof of Theorem 3.4

Let be the solution of (3.1), given by Theorem 3.3. We prove the following two assertions:

-

(a)

For all , we have

(C.1) where is the terminal wealth generated by an admissible strategy .

-

(b)

There exists an admissible strategy such that the corresponding wealth process satisfies

(C.2)

As a consequence, (a) implies and (b) implies . Hence, if these assertions hold, we obtain as desired.

We consider two cases, namely, and .

Case 1 (): In this case, by Lemma 3.5, the function is negative. Therefore, which is of the form

| (C.3) |

is bounded in . Since has polynomial growth in , standard verification results such as Theorem 3.8.1 on page 135 of Fleming and Soner (2006) yield assertions (a) and (b) above. Furthermore, the optimal control is given by (B.6) which, in turn, yields (3.16).

Case 2 (): For these values of , Lemma 3.5 shows that is positive. Thus, , the solution of the HJB equation, has exponential growth in . For this case, we provide our own verification result by checking assertions (a) and (b) above.

To show (a), for all , define the stopping times

| (C.4) |

and note that , -almost surely. By Itô’s formula, we have

| (C.5) | ||||

where is given by (B.4). The first integral on the right side is non-positive because solves (3.1). Furthermore, by the definition of , the integrands of the second integral is uniformly bounded, therefore, taking the conditional expectation on both sides of (C.5) yields

| (C.6) |

Note that for , (2.22) yields that . Thus,

| (C.7) |

Finally, by letting , Fatou’s lemma yields that .

To show (b), define by (3.16), namely,

| (C.8) |

where, for ease of notation, we have defined

| (C.9) |

We need to show that and that (C.2) is satisfied.

To show admissibility of , we proceed as follows. By (2.16) and (C.8), the wealth process corresponding to satisfies

| (C.10) |

Since is a stochastic exponential, conditions (i)-(iii) in Definition 2.7 hold if the following integrability condition is satisfied

| (C.11) |

Since and are bounded on the interval , we have

| (C.12) |

for some positive constants , , and . Thus, (C.11) holds if , -almost surely. The latter conditions holds since, by Fubini’s theorem,

| (C.13) |

where and are bounded functions on given by (2.10) and (2.11) respectively. We have proved that .

It only remains to prove (C.2). Since satisfies (B.6), we have

| (C.14) |

for Therefore, by setting in the argument that yielded (C.6), we obtain

| (C.15) |

Next, we show that the process is a martingale. Once we show this, (C.2) follows from (C.15) by taking the limit as .

With a slight abuse of notation, let us define , . Set in (C.5) and use (C.14) to obtain

| (C.16) | ||||

| (C.17) | ||||

| (C.18) | ||||

| (C.19) | ||||

| (C.20) |

for , where we have defined and such that

| (C.21) |

Note, in particular, that and are bounded on since and are continuous on . We can then repeat the argument in the proof of Proposition 2.5 in Appendix A to show that, for the time change in (A.5), the time-changed processes is a martingale. Thus, is a martingale, as we set out to prove.

Appendix D Proof of Lemma 3.5

We first show that, for , for all . With , ODE (3.4) yields

| (D.1) |

Since , we must have in a left neighborhood of , say for some . For for all , we show that for all .

Assume otherwise, that is, for some . Then, it follows from (3.4) that

| (D.2) |

This implies that in a right neighborhood of , say , for some . Now, since the smooth function increases from to on the interval , there must be a point such that and . However, by (3.4),

| (D.3) |

which is a contradiction. Therefore, there cannot be such , as desired. The proof for the case with follows from a similar argument and is thus omitted.