On the approximation of Lévy driven Volterra processes and their integrals

Abstract

Volterra processes appear in several applications ranging from turbulence to energy finance where they are used in the modelling of e.g. temperatures and wind and the related financial derivatives. Volterra processes are in general non-semimartingales and a theory of integration with respect to such processes is in fact not standard. In this work we suggest to construct an approximating sequence of Lévy driven Volterra processes, by perturbation of the kernel function. In this way, one can obtain an approximating sequence of semimartingales.

Then we consider fractional integration with respect to Volterra processes as integrators and we study the corresponding approximations of the fractional integrals. We illustrate the approach presenting the specific study of the Gamma-Volterra processes. Examples and illustrations via simulation are given.

Keywords: Riemann-Liouville fractional integral, Volterra processes, fractional Brownian motion, ambit processes, generalized Lebesgue-Stieltjes integral, non-semimartingales.

1 Introduction

We consider Volterra type processes driven by Lévy noise , of the form:

| (1) |

where is a deterministic kernel. Such processes appear in many different applications including models for tumour growth, turbulence, and energy finance, see e.g. [6, 3, 4, 31]. Processes of type (1) belong to the family of ambit fields as presented e.g. in [2] and include, as particular cases, the Lévy fractional Brownian motion given by the Riemann-Liouville integral, see [22]. The fractional Brownian motion is represented (modulo a constant factor) by an integral of type (1) plus a suitable process with absolutely continuous trajectories, see [22, p. 424]. Compare also with the integral representation on with the Molchan-Golosov kernel, see e.g. [19]. For fractional Lévy processes we can refer e.g. to [23, 10, 9] and references therein.

In general Volterra processes are not semimartingales, see [7]. We recall that semimartingales constitute the largest class of integrators for a stochastic integration theory (Itô-type integration) which is well-suited for applications where the adaptedness or the predictability with respect to a given information flow plays an important role. This is the case, for example, in mathematical finance where one needs integration to define e.g. the central concept of the value process of a self financing portfolio. Also, the numerical methods are flourishing in the case of semimartingale models. Without means of being exhaustive, we can refer, e.g., to classical books [12, 20] and to more recent works that show that the area is in simmering activity [25, 32, 37, 38]. Processes of type (1) have interesting stylized features, like the non-trivial time correlation structure, that well suits several contexts of modelling, such as in renewable energies. In energy finance the use of non-semimartingale models is well motivated. See e.g. [3, section 3.3] for a discussion.

In this paper we propose to approximate (1) by the process

| (2) |

where , with , is a family of deterministic kernel functions approximating , i.e. as , in an appropriate sense. We are interested in the cases when guarantees that , is a semimartingale and we show that approximates in the sense of -convergence.

Approximations of this type were first introduced in [33] and [34], and then used in [17], but only in the case where is a fractional Brownian motion. Our result extends substantially this first study and moves beyond.

In fact, the core of the present paper deals with the generalized Lebesgue-Stieltjes integrals with respect to the processes (1) and (2) as integrators. This is a form of pathwise integration defined via the fractional derivatives. For a survey, new results and conditions for integration with respect to Volterra type processes as integrators see [14]. In this study we suggest sufficient conditions to ensure that, for a given integrand , the generalized Lebesgue-Stieltjes integrals with respect to and as integrators converge in :

| (3) |

We remark that, if is a semimartingale and is a predictable process (with respect to the same filtration), the generalized Lebesgue-Stieltjes integral corresponds to the Itô type integral. Hence, in the context of predictable integrands, the approximation (3) provides an approximation of a non-semimartingale by a semimartingale. We intend to exploit this feature in future research dealing with hedging in energy finance. Here we illustrate the use of the approximation in simulation with an example.

We illustrate the results in full detail in the case of

| (4) |

for , . In this case is, up to a constant, a Gamma kernel. For , the integral (4) is obtained as an appropriate stochastic modification of the Riemann-Liouville fractional integral in which the factor in the kernel has a dampening effect. The processes (4) appear explicitly in the modelling of turbulence and in the modelling of environmental risk factors in energy finance (e.g. wind), see [5, 36]. In the sequel we refer to (4) as Gamma-Volterra process. In view of the relevance of this family in applications, we shall detail the study of such processes.

The paper is organised as follows. The next section reviews knowledge about Volterra processes and introduces an approximation by perturbation of the kernel. Particularly interesting is the case when the Volterra process is not a semimartingale and it can be approximated by a semimartingale process. As illustration, the Lévy driven Gamma-Volterra processes are studied along with their approximations. Section 3 deals with fractional integration and it is divided in two parts. In the first part we revise general facts and then we provide conditions to guarantee when a Volterra process is an appropriate integrator. This includes cases when the Volterra process is not a semimartingale. Examples are provided. In the second part of the section, exploiting the approximation introduced before, we suggest an approximation of the integral with respect to a Volterra process. Examples and full detailed conditions are provided in the case of a Gamma-Volterra process. Finally, a numerical example is given as direct application and illustration of the technique proposed.

2 Volterra processes and a semimartingale

approximation

First of all we review the fundamental concepts to ensure the meaningful definition of in (1). We define the integration of a deterministic function with respect to the Lévy process as in [14] by the approach proposed in [35] and further developed in [26].

Let be a complete probability space and be a Lévy process with characteristic function represented in the following form (see e.g. [30]):

with

where

, and is a Lévy measure on , i.e. it is a -finite Borel measure satisfying

The triplet is called the characteristic triplet of the Lévy process .

From the increments of the Lévy process , we obtain the random measure on taking values in , see [26]. The random measure is still denoted by . For any s.t. , the random measure values are random variables with infinitely divisible distribution and Lévy-Khintchine characteristic function

Here denotes the Lebesgue measure on .

Definition 2.1.

-

(i)

Let be a real-valued simple function on , where the pairwise disjoint sets belong to a partition of . Then, for any , we set

-

(ii)

A measurable function is said to be -integrable (on ) if there exists a sequence of simple functions as in (i) such that

-

(a)

, -

-

(b)

for any , the corresponding sequence converges in probability as .

-

(a)

If is -integrable, the stochastic integral on is defined by

with convergence in probability.

The integral is well-defined, i.e. for any -integrable function

, the integral does not depend on the choice of approximating sequence .

Moreover, the integral is also infinitely divisible with explicit characteristic function, see [26, 35].

The following result characterizes the space of integrands. See e.g. Lemma 2.1 in [14].

Lemma 2.2.

-

(i)

For , any function is -integrable.

-

(ii)

For assume that satisfies and . Then any function is -integrable.

Hence for all , under the conditions of Lemma 2.2, we have that the integral (1) is well defined for -integrable functions on . The proper definition of is a standing assumption in this work.

Depending on the properties of the kernel function , the Volterra process may or may not be a semimartingale. The semimartingale property of various subclasses of Volterra type processes is studied in e.g. [7, 8, 9, 21]. Hereafter, we fix the natural filtration generated by the Lévy process with the characteristic triplet on and we state the necessary and sufficient conditions to guarantee that the Volterra process in (1) is a semimartingale. See [7], Theorem 3.1 and Corollary 3.5.

Theorem 2.3.

Assume that is of unbounded variation. Then is an -semimartingale if and only if , , is absolutely continuous on with a density such that

when , and satisfies

| (5) |

when .

Assume that is of bounded variation. Then is an -semimartingale if and only if it is of bounded variation, which is equivalent to requesting that is of bounded variation.

Example 2.4.

Semimartingale property of Gamma-Volterra processes. Consider the Gamma-Volterra process (4):

with . From direct application of the theorem above we see that if is a Brownian motion or a Lévy process with , then is a -semimartingale if and only if . If is a Lévy process with no Brownian component, i.e. , then is well-defined and an -semimartingale if and only if one of the following conditions is satisfied (see [7], Corollary 3.5):

-

(i)

,

-

(ii)

and ,

-

(iii)

and .

The following result is a moment estimate for the Lévy driven Volterra processes, see Theorem 2.2 and Remark 2.2 in [14]. This is obtained under the technical assumption that is symmetric. We shall make this assumption in our present work.

Theorem 2.5.

Let , be a Lévy process with symmetric Lévy measure . We have the following two statements:

-

(a)

For a Lévy process with characteristic triplet such that for some , we assume that for , . Then is integrable and we have the estimate:

-

(b)

For a Lévy process with characteristic triplet such that for some , we assume that for , . Then is integrable and we have the estimate:

The constants do not depend on .

Notice that, in the present work, all constants in the estimates are denoted by . Their dependence on the parameters can be explicitly given when relevant. Their specific form is deduced from the context.

Remark. Recall that a Lévy process with characteristic triplet is a square-integrable martingale if and only if, for some ,

Then, considering the assumptions of Theorem 2.5 in this case, if the Lévy process has symmetric Lévy measure and for some , this Lévy process is a square-integrable martingale with , . In this case we could also consider Itô stochastic integration of predictable stochastic processes and find estimates of the moments based on the Burkholder-Davis-Gundy and Bichteler-Jacod types inequalities. See e.g. Lemma 5.1 in [18]. However, we shall not consider such processes in the framework of the present work. We remark that other similar estimates can be found by means of Rosenthal inequalities in the case of Poisson stochastic integrals, which are optimal in the sense that an Itô isomorphism is obtained, see [16].

For later use, we consider the following result.

Lemma 2.6.

Let be a Lévy process with characteristic triplet , where is symmetric and for some , if , or some , if . Then , for all , and the integrals

are well defined. Assume that exists with convergence in and denote by the limit and the corresponding function defined -a.e. by a subsequence. Then the integral

is well-defined. Furthermore, exists with convergence in (and in probability) and .

Proof.

Since , by convergence, also , then the corresponding integrals and are well-defined by Lemma 2.2. We prove the last assertion. It is enough to show that the sequence admits a limit in .

Applying the estimates of Theorem 2.5 we can see that, for small enough,

Thus the sequence is Cauchy in . Analogously, we see that

∎

Hereafter we study an approximation for the Volterra process , derived by perturbation of the kernel function. Let , be a family of deterministic -integrable kernels and define the corresponding family of Volterra processes , by

| (6) |

Theorem 2.7.

Let , be a Lévy process with symmetric Lévy measure. Consider one of the following situations:

-

(a)

The Lévy process has characteristic triplet and for some .

-

(b)

The Lévy process has characteristic triplet and for some .

Then, for any , we have the convergence in :

| (7) |

whenever such that

| (8) |

If (8) is uniform on , then (7) would be uniform on as well.

Proof.

In the following example we specify under which assumptions we can approximate the Gamma-Volterra process in (4) with a semimartingale, using Theorem 2.7.

Example 2.8.

Approximation of Gamma-Volterra processes. Let , be the Gamma-Volterra process in (4) with driving noise , a Lévy process with the characteristic triplet , where is a symmetric measure such that , for some . Fix . From Lemma 2.2 we have that (4) is well defined whenever . That is

whenever . We shall consider two cases:

-

(a)

and , i.e. ;

-

(b)

;

Concerning the approximating process in (6), we define

Correspondingly, we have

These processes are well-defined and, applying Theorem 2.3, we can see that are semimartingales, since are absolutely continuous on and is bounded on for .

We can also see that since is bounded. Hereafter we give an estimate of this difference and we distinguish the cases in which is positive or negative.

(a) We consider the case and .

The kernel is singular at and continuously differentiable, strictly increasing and convex on the interval . Hence, we have the following inequality for :

| (9) |

This yields

where we have used the fact that, for and :

| (10) |

Moreover, also the following crude inequality holds for :

| (11) | ||||

Hence, we obtain the following estimate:

for the given parameters.

(b) Now assume .

The function is zero at and it is continuously differentiable on . For , we have that

We have to distinguish two cases. If , then we have

If , then

The estimates are uniform on .

3 Pathwise Volterra integrals and their approximation

Now that is well characterized, we proceed by reviewing stochastic integration with respect to as integrator.

Naturally, in the case when is a semimartingale and the integrand is predictable, integration can be carried out via Itô-type calculus with respect to the random measure generated by . See e.g. [11] and [13]. In [1] (see also [15]) a stochastic integral with respect to has been constructed by means of the Malliavin calculus with respect to the Brownian motion and the centered Poisson random measure. This approach does not consider the Lévy driving noise as a whole, but treats the Gaussian and the centered Poisson random measure separately, and it is well-set when the kernel is not degenerate at . Also [10] proposes a Skorohod-type integral based on the -transform for a pure jump centered .

In this paper we consider a pathwise-type of integration with respect to as introduced in [14] in the lines of [39, 41, 40]. This is based on fractional calculus, see [29] for a detailed background.

3.1 Generalized Lebesgue-Stieltjes integrals with respect to Volterra processes

First we recall some definitions from fractional calculus, that we are going to use to define the integral of our interest.

Elements of fractional calculus

For a deterministic real-valued function , the Riemann-Liouville left- and right-sided fractional integrals111In the definitions in [39, 41, 40] there is a term, originally used by Liouville. The interest in those papers is mostly about harmonic calculus, while in a different context we decided to omit such term. of order are defined by

and

respectively, if the integrals converge for a.a. . Here denotes the Gamma function. The fractional integrals above are well-defined for all if .

If and for and if , then the integration by parts

holds. This motivates the introduction of the fractional derivatives as a form of inverse operator to the fractional integral. For this we work with a class of functions for which these concepts are well defined. For , let be the set of functions for which there exists such that . It can be shown that the function is unique in (see [24] Lemma 1.1.2 and comments). Also, if , if and only if and there is -convergence for of the function

(where for ). The conditions are sufficient if . Analogously, set to be the set of functions for which there exists such that . For we have that if and only if and there is -convergence for of the function

Again the conditions are sufficient if .

Furthermore, for and all , the function coincides with the Riemann-Liouville left-sided fractional derivative defined as the inverse operator of . Namely, is equal to

Correspondingly, for , we have the right-sided fractional derivative

In this cases the Riemann-Liouville fractional derivatives admit the respective Weyl representations:

The convergence of the integrals is in , if , and it is pointwise , if . We recall that, for all , for all , the derivatives and exist and are in for .

Let . Assume that the limits

exist for and denote

Definition 3.1.

Assume that and for some , and . The generalized fractional Lebesgue-Stieltjes integral of with respect to is defined by

Naturally, the conditions and mean that and . Hence the integral on the right-hand side is well-defined. It can be shown that the definition of the integral does not depend on , see [39, Proposition 2.1].

Moreover, for , we have that if and only if and exists. Then the generalized Lebesgue-Stieltjes integral admits a simplified representation as

Motivated by the above considerations, the following definition can be given, see [14].

Definition 3.2.

Two real-valued measurable stochastic processes , , and , , are fractionally -connected for some and for some , if the generalized Lebesgue-Stieltjes integral

| (12) |

exists -

From fractional calculus we recall that the integral above exists and does not depend on whenever and - Here the random variables are well-defined, see Lemma 2.6. In general, we know that the integral above exists if and , - for some . Then the following definitions appear naturally.

On the time horizon , for and , define the sets of stochastic integrands :

and integrators :

It is easy to see that the couples , , and are fractionally -connected for all . Then we say that the elements in are the appropriate integrators, , for the elements in , , with the conventions that and .

Hereafter we formulate the concept of two processes being fractionally -connected in terms of expectations. This is a direct consequence of Theorem 2.5. We define new classes of integrands and integrator processes with conditions that are easier to verify and which are included in the previously given classes. We define the sets:

and

Again, we say that the elements in are the appropriate

integrators, , for the elements in , .

Remark. It is easy to see that for the couples , the generalized Lebesgue-Stieltjes integral (12) exists both - and in .

Remark: Relationship with other types of stochastic integration. The definition of generalised Lebesgue-Stieltjes integral (Definition 3.1) can be extended, see [41] Definition 4.4, which is motivated by Lemma 4.1 and Lemma 4.2 in the same reference. This leads to the Definition 4.7 of stochastic integral in [41], which also extends the forward integral introduced in [28] Section 1.

All these stochastic integrals coincide with the Itô integral whenever the integrator is a semimartingale, the integrand is an adapted càglàd process, and the convergences are uniformly on compacts in probability (ucp). See [28] Proposition 1.1, [41] Proposition 4.9, [40] Section 5. This result also applies to the stochastic integral of Definition 3.2 in the present paper. In fact two functionally -connected processes are integrable as per [41] Definition 4.7.

A Lévy driven Volterra process as integrator

We now review the case of Lévy driven Volterra processes (1) as integrators. The following result relies on the estimate of Theorem 2.5 (b). See [14] Section .

Theorem 3.3.

Let be a Volterra process where is a Lévy process with the characteristic triplet , for , and a symmetric Lévy measure such that for some with if or if . Moreover, for this value of , assume that for any and the following set of conditions for some :

Assumptions ()

-

(i)

,

-

(ii)

,

-

(iii)

,

-

(iv)

.

Then , so, is an appropriate -integrator for any with .

Example 3.4.

The Gamma-Volterra process as an appropriate -integrator. In this example, we find the conditions on the parameters depending on so that the Gamma-Volterra process in (4) is an appropriate -integrator. From Lemma 2.2 and Example 2.8 we already know that is well defined if and if with . We consider a Lévy driving noise with characteristic triplet . The case with is treated similarly, cf. Example 2.9.

Recall the set of conditions on the kernel function in Theorem 3.3. We go through the list, and find conditions on the parameters and in order for (i)-(iv) of () to be satisfied.

-

(i)

The innermost integral in (i) can be estimated by the following:

where the integral is well defined since . We calculate the outer integral of (i), and find an estimate:

where the integral is well defined when .

-

(ii)

We need to separate the cases in which is positive or negative.

For , by (10), we have that(13) Hence we can estimate the integral in (ii) as follows:

The integral above is finite for .

For we have that(14) Then we have the following estimate for the integral in (ii):

The innermost integral is finite as and increasing in . Then the estimate above is finite for .

-

(iii)

The innermost integrals of (i) and (iii) are the same with the only attention to be given to the range of integration, so:

which is well-defined as . The second layer of integrals is then dominated by

which is finite whenever . The outermost integral of (iii) is then also clearly finite.

-

(iv)

Similar to the study of (ii) here we also have to separate the cases and . Moreover, our estimates need to be sharper than before.

For , we go through the integral:

(15) by splitting the integration range in an opportune way. We start by considering

By application of (9) with in the place of , we observe that

Thus we have

This integral is finite when . Then, using (14), we consider

which is finite for . The last summand in (15) is given by

By using the same estimates as for , we get that is finite for .

For , as in case (b) in Example 2.8, we obtain the following inequality:

and again we have to distinguish two cases. If , then we have

Then the integral is finite for . If , we have

which is finite for and .

Summarising, the following conditions on the parameters are sufficient for the Gamma-Volterra process (4) to be a -integrator:

-

•

-

•

-

•

.

3.2 Approximation of integrals with Volterra drivers

We are now ready to study the approximation of integrals with respect to Volterra processes by integrals driven by semimartingales. Further on we will consider again the example of the Gamma-Volterra process in (4).

Theorem 3.5.

Let be a Lévy process with the characteristic triplet , for , and a symmetric measure such that for some with if or if . Let the kernel functions and belong to for any . Assume that and are well-defined and in and assume that also satisfy the set of conditions for some together with the following:

Assumptions (). For ,

Define the Volterra processes

and

Then, for any stochastic process where , we have the convergence

in of the generalised Lebesgue-Stieltjes integrals.

Proof.

In the given setting for the processes and , the generalised Lebesgue-Stieltjes integrals are well-defined - and in . See also Lemma 2.6 for the definition of , and ,. By linearity of the operators involved and the use of the Hölder inequality, we estimate the difference of the integrals as follows:

| (16) | ||||

Hence the statement is proved if

| (17) |

Define and

From , we can see that, if , the fractional derivative is well-defined and admits representation

| (18) | ||||

which can then be substituted into (17). Observe that, for , we have

Hence, from the moment estimates of Theorem 2.5, we obtain

| (19) |

which vanishes as , thanks to - and -. Similarly, we can see that - and - ensure the convergence

| (20) |

Naturally, (3.2)-(3.2) guarantee (17). To conclude the proof, we verify that . For , this is ensured when - and the processes

converges in , - for . We verify these two requirements. First we see that we have that from the estimates of Theorem 2.5. By dominated convergence we can see that converges to in .In fact, for all small, we have

-. and the bound (see (3.2)). By this the proof is complete. ∎

Example 3.6.

Approximation of the integrals with respect to Gamma-Volterra processes. For illustration, we consider the process (4) with , in the kernel function, that is . To treat the case , we need similar inequalities as in Example 3.4.

As before, we consider a Lévy driving noise with characteristic triplet with symmetric and such that for some . The parameters satisfy the conditions of Example 2.8 and Example 3.4. These guarantee the validity of assumptions . We now go through the requirements of with , .

-

(i)

Using the same approach and inequalities as in Example 2.8, we split the inner integral. Again we separate the cases depending on . Taking we obtain

The next layer of the integrals yields:

which converges to zero if .

The same estimate can be applied for . In this case we find the same condition as above. As far as the case is concerned, similar reasonings as in Example 2.8 can be done, leading to convergence if . These conditions are the same as in Example 3.4. -

(ii)

Consider . Observe that is negative and increasing, hence

Then we have

where we have applied the same argument as in Example 2.8 based on (9) and (11). Here we require that and .

With similar arguments, in the case it can be shown that the required conditions are , if , and , , if . These conditions are already guaranteed by those in Example 3.4. - (iii)

-

(iv)

Let . We split the integration range in disjoint intervals and study them separately, in a similar fashion as in Example 3.4:

By application of (9), (11) we obtain

which converges to if we require . The next summand is given by

where the last integral converges if . We proceed to the next summand:

Its convergence is given if . Then considering the last piece we get

If , we have convergence of the last integral.

For positive, with similar reasoning as above, we find that convergence is guaranteed when , , when , and , when .

Summarising, for the the driving Lévy process with characteristic triplet and symmetric measure such that , we have considered the integrals with and the integral with , see Definition 3.2. Then we have shown that there is convergence of the integrals in , according to Theorem 3.5, if one of the following conditions is satisfied:

-

•

-

•

-

•

.

We conclude this section with a numerical example of a Gamma-Volterra process as integrator driven by a pure jump Lévy process with infinite activity. The parameters are taken according to the sufficient conditions found in Example 3.4 and Example 3.6. We illustrate the use of the approximation result for simulation purposes. Approximating the non-semimartingale by the corresponding semimartingale as per Theorem 3.5, we can then exploit the connection of the fractional integral with the Itô integral that we have remarked earlier.

Example 3.7.

Numerical example of the approximation of an integral with Volterra driver. In light of Example 3.6, for illustration, set the parameters in (4) to be and , i.e.

and let be a symmetric tempered stable Lévy process with Lévy measure (). As illustration, choose , . Then we see that the -th moment of the Lévy measure is finite

since we can obtain the Gamma function by a change of variable and also .

From Example 2.4 we know that is not a semimartingale. From Example 3.4, taking , , we know that is an appropriate integrator for any , and that and satisfy the convergence conditions of Theorem 3.5, respectively. The fact that is a semimartingale is deduced from (5) in Theorem 2.3: For all ,

Thus from Example 3.6, for these values of the parameters, we have the convergence in .

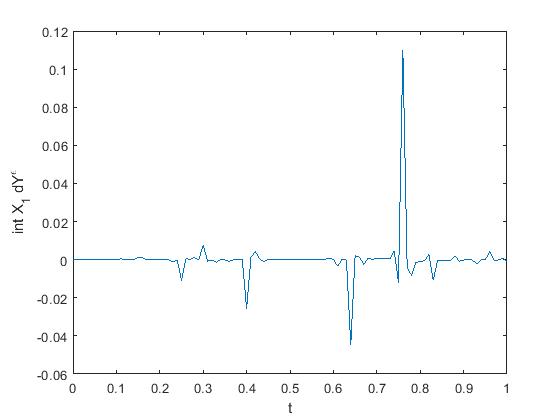

To complete the example, we consider two integrands. First we take . We see that , in fact

The second integrand is given by , where is a Brownian motion. In this case the fractional derivative is Gaussian and, to show that , we first find the second moment:

We see that , while

Similarly . Hence we find that

and .

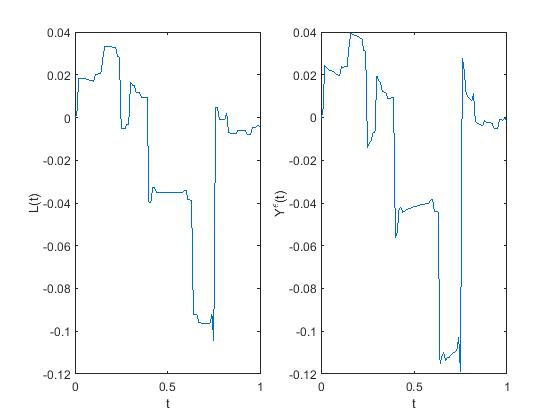

Figure 1, Figure 2 and Figure 3 present a simulation of the processes described above: , and , with and . For the simulation of a sample path of the tempered stable Lévy process in Figure 1 we used the series representation by Rosiński [27]. The simulation of the Volterra process is then obtained by means of a classical numerical integration with an Euler scheme, see e.g. [20], by using the sample path of .

Using the same approach we also simulated the integrals in the case of in Figure 2 and in Figure 3. In particular, since the integrands are clearly adapted and càglàd, the integral , , is well defined as an Itô integral. This is exploited in our simulation, which is again obtain by numerical integration, with the same value for . Theorem 3.5 will then guarantee that the simulations convergence in to the pathwise fractional integral , approximated in this way by Itô integrals.

4 Conclusion

In the framework of fractional integrals, we have studied an approximation of the fractional stochastic integral for non-semimartingale integrators by a sequence of integrals with semimartingale integrators . No filtration structure is needed on the integrand for the definition of the integral or for the convergence. However, in the case when is an adapted, càglàd process the integral agrees with the usual Itô-integral, thus can be approximated by a sequence of Itô-integrals. As illustration we have specialised our results to the case of Gamma-Volterra processes driven by Lévy processes, which is a family of models largely used in applications and of recent attention in energy finance and biological modelling. We have shown how the approximation procedures proposed is used for computational purposes by examples.

Acknowledgement. The research leading to these results is within the project STORM: Stochastics for Time-Space Risk Models, receiving funding from the Research Council of Norway (RCN). Project number: 274410.

References

- [1] O. E. Barndorff-Nielsen, F. E. Benth, J. Pedersen, and A. E. D. Veraart. On stochastic integration for volatility modulated Lévy-driven Volterra processes. Stochastic Process. Appl., 124(1):812–847, 2014.

- [2] O. E. Barndorff-Nielsen, F. E. Benth, and A. E. D. Veraart. Ambit processes and stochastic partial differential equations. In G. Di Nunno and B. Øksendal, editors, Advanced mathematical methods for finance, pages 35–74. Springer, Heidelberg, 2011.

- [3] O. E. Barndorff-Nielsen, F. E. Benth, and A. E. D. Veraart. Modelling energy spot prices by volatility modulated Lévy-driven Volterra processes. Bernoulli, 19(3):803–845, 2013.

- [4] O. E. Barndorff-Nielsen, F. E. Benth, and A. E. D. Veraart. Modelling electricity futures by ambit fields. Adv. in Appl. Probab., 46(3):719–745, 2014.

- [5] O. E. Barndorff-Nielsen and T.N. Thiele Centre for Applied Mathematics in Natural Science. Research Report: Notes on the Gamma Kernel. Number no. 3; no. 2012. 2012.

- [6] O. E. Barndorff-Nielsen and J. Schmiegel. Spatio-temporal modeling based on Lévy processes, and its applications to turbulence. Uspekhi Mat. Nauk, 59(1(355)):63–90, 2004.

- [7] A. Basse and J. Pedersen. Lévy driven moving averages and semi-martingales. Stochastic Process. Appl., 119(9):2970–2991, 2009.

- [8] A. Basse-O’Connor and J. Rosiński. On infinitely divisible semimartingales. Probab. Theory Related Fields, 164(1-2):133–163, 2016.

- [9] C. Bender, A. Lindner, and M. Schicks. Finite variation of fractional Lévy processes. J. Theoret. Probab., 25(2):594–612, 2012.

- [10] C. Bender and T. Marquardt. Stochastic calculus for convoluted Lévy processes. Bernoulli, 14(2):499–518, 2008.

- [11] K. Bichteler and J. Jacod. Random measures and stochastic integration. In Theory and application of random fields (Bangalore, 1982), volume 49 of Lect. Notes Control Inf. Sci., pages 1–18. Springer, Berlin, 1983.

- [12] N. Bouleau and D. Lépingle. Numerical methods for stochastic processes. John Wiley & Sons, Inc., New York, 1994

- [13] C. Chong and C. Klüppelberg. Integrability conditions for space-time stochastic integrals: theory and applications. Bernoulli, 21(4):2190– 2216, 2015.

- [14] G. Di Nunno, Y. Mishura, and K. Ralchenko. Fractional calculus and pathwise integration for Volterra processes driven by Lévy and martin- gale noise. Fract. Calc. Appl. Anal., 19(6):1356–1392, 2016.

- [15] G. Di Nunno and J. Vives. A Malliavin-Skorohod calculus in and for additive and Volterra-type processes. Stochastics, 89(1):142–170, 2017.

- [16] S. Dirksen. Itô isomorphisms for -valued Poisson stochastic integrals, Ann. Probab., 42 (6): 2595–2643, 2014.

- [17] N. T. Dung. Semimartingale approximation of fractional Brownian motion and its applications. Comput. Math. Appl., 61(7):1844–1854, 2011.

- [18] J. Jacod, T.G. Kurtz, , S, Méléard, and P. Protter.The approximate Euler method for Lévy driven stochastic differential equations, Ann. Inst. H. Poincaré Probab. Statist., 41 (3): 523–558, 2005.

- [19] C. Jost. On the connection between Molchan-Golosov and Mandelbrot-Van Ness representations of fractional Brownian motion, J. Integral Equations Appl., 20 (1): 93–119, 2008.

- [20] P.E. Kloeden and E. Platen. Numerical solution of stochastic differential equations, Springer-Verlag, Berlin, 1992.

- [21] F. B. Knight. Foundations of the prediction process, volume 1 of Oxford Studies in Probability. The Clarendon Press, Oxford University Press, New York, 1992. Oxford Science Publications.

- [22] B. B. Mandelbrot and J. W. Van Ness. Fractional Brownian motions, fractional noises and applications. SIAM Rev., 10:422–437, 1968.

- [23] T. Marquardt. Fractional Lévy processes with an application to long memory moving average processes. Bernoulli, 12(6):1099–1126, 2006.

- [24] Y.S. Mishura. Stochastic calculus for fractional Brownian motion and related processes, volume 1929 of Lecture Notes in Mathematics. Springer-Verlag, Berlin, 2008.

- [25] E. Platen and N. Bruti-Liberati. Numerical solution of stochastic differential equations with jumps in finance. Springer-Verlag, Berlin, 2010.

- [26] B. S. Rajput and J. Rosiński. Spectral representations of infinitely divisible processes. Probab. Theory Related Fields, 82(3):451–487, 1989.

- [27] Jan Rosiński. Tempering stable processes. Stochastic Process. Appl., 117(6):677–707, 2007.

- [28] F. Russo and P. Vallois. Elements of stochastic calculus via regularization. In Séminaire de Probabilités XL, volume 1899 of Lecture Notes in Math., pages 147–185. Springer, Berlin, 2007.

- [29] S. G. Samko, A. A. Kilbas, and O. I. Marichev. Fractional integrals and derivatives. Gordon and Breach Science Publishers, Yverdon, 1993.

- [30] K. Sato. Lévy processes and infinitely divisible distributions, volume 68 of Cambridge Studies in Advanced Mathematics. Cambridge University Press, Cambridge, 1999.

- [31] J. Schmiegel. Self-scaling tumor growth. Physica A: Statistical Mechanics and its Applications, 367(C):509–524, 2006.

- [32] Y. Song and H. Wang. Discretization error of stochastic iterated integrals. ArXiv, 1704.04894.

- [33] T. H. Thao. A note on fractional Brownian motion. Vietnam J. Math., 31(3):255–260, 2003.

- [34] T. H. Thao and T. T. Nguyen. Fractal Langevin equation. Vietnam J. Math., 30(1):89–96, 2002.

- [35] K. Urbanik and W. A. Woyczyński. A random integral and Orlicz spaces. Bull. Acad. Polon. Sci. Ser. Sci. Math. Astronom. Phys., 15:161–169, 1967.

- [36] T. von Kármán. Progress in the statistical theory of turbulence. J. Marine Research, 7:252–264, 1948.

- [37] H. Wang. The Euler scheme for a stochastic differential equation driven by pure jump semimartingales. J. Appl. Probab., 52(1):149–166, 2015.

- [38] L. Yan. Asymptotic error for the Milstein scheme for SDEs driven by continuous semimartingales. Ann. Appl. Probab., 15(4):2706–2738, 2005.

- [39] M. Zähle. Integration with respect to fractal functions and stochastic calculus. I. Probab. Theory Related Fields, 111(3):333–374, 1998.

- [40] M. Zähle. On the link between fractional and stochastic calculus. In Stochastic dynamics (Bremen, 1997), pages 305–325. Springer, New York, 1999.

- [41] M. Zähle. Integration with respect to fractal functions and stochastic calculus. II. Math. Nachr., 225:145–183, 2001.