Goodness-of-fit tests for Laplace, Gaussian and exponential power distributions based on -th power skewness and kurtosis

Abstract

Temperature data, like many other measurements in quantitative fields, are usually modeled using a normal distribution. However, some distributions can offer a better fit while avoiding underestimation of tail event probabilities. To this point, we extend Pearson’s notions of skewness and kurtosis to build a powerful family of goodness-of-fit tests based on Rao’s score for the exponential power distribution , including tests for normality and Laplacity when is set to 1 or 2. We find the asymptotic distribution of our test statistic, which is the sum of the squares of two -scores, under the null and under local alternatives. We also develop an innovative regression strategy to obtain -scores that are nearly independent and distributed as standard Gaussians, resulting in a distribution valid for any sample size (up to very high precision for ). The case leads to a powerful test of fit for the Laplace() distribution, whose empirical power is superior to all competitors in the literature, over a wide range of alternatives. Theoretical proofs in this case are particularly challenging and substantial. We applied our tests to three temperature datasets. The new tests are implemented in the R package PoweR.

keywords:

Asymmetric power distribution , Lagrange multiplier test , Local alternatives , Power analysis , Rao’s score test , Temperature dataMSC:

[2020]Primary: 62F03; Secondary: 62E20 , 62F12 , 60F05This manuscript was accepted for publication in Statistics (Taylor & Francis). This version may differ from the published version (doi:10.1080/02331888.2022.2144859) in typographic details.

1 Introduction

In many fields of application, the Gaussian distribution is the primary choice to model a symmetric dataset. However, further analysis using for example a QQ-plot often reveals more (or sometimes fewer) extreme values than expected in a Gaussian model. This is problematic because it can lead to a poor estimation of the probability of extreme events. The exponential power distribution , whose density function is proportional to , is then an interesting alternative thanks to its wide range of tails’ behaviour. In particular, the Laplace distribution (), with its heavier tails, is a popular alternative to the Gaussian distribution () for modelling observations that show a higher rate of extreme values. Goodness-of-fit tests for normality, Laplacity or in general for the with a fixed value of , are then necessary to assess the validity of the chosen model.

Our contribution in this paper is to propose a unified testing approach with a family of goodness-of-fit tests for the exponential power distribution with and unknown location and scale parameters and , including tests for the Laplace and Gaussian distributions if is set to 1 or 2, respectively. Specifically, we use Rao’s score test (Rao, 1948) – also known as Lagrange multiplier test – on the asymmetric power distribution (APD) introduced by Komunjer (2007). Asymptotically, we obtain tests that are equivalent to the Wald and likelihood ratio tests, which are the most powerful for small deviations. Since the APD family combines the wide range of exponential tail behaviours provided by the EPD family with different levels of asymmetry, the resulting tests are based on two asymptotically independent measures that we named ‘-th-power skewness’ and ‘-th-power kurtosis’, similar to the normality test of Jarque and Bera (1987) or the moment-based tests of Natarajan and Mudholkar (2004) for the inverse Gaussian.

We go further by adapting our asymptotic tests for all sample sizes and , using simulation and regression techniques. It is well known that skewed distributions are often associated with heavy tails for small samples. We therefore designed the ‘-th-power net kurtosis’ to replace the -th-power kurtosis, the former being virtually independent of the -th-power skewness for all sample sizes. This is a crucial step in building powerful tests. These two measures are then transformed into -scores, which are very close to being normally distributed under the null hypothesis and could be used as specific test statistics against symmetric and asymmetric alternatives, respectively. We obtain omnibus test statistics by adding the square of the two -scores, which is very close to being distributed under the null hypothesis. Theoretical results are also provided, showing that the asymptotic distribution of the omnibus test statistics is a chi-square with two degrees of freedom () under the null hypothesis and a noncentral under local alternatives. The proofs, given in the Supplementary Material B, are particularly challenging and substantial.

Our family of tests has characteristics that stand out in several respects. First, since our tests are built from two nearly independent components for all sample sizes, the amount of information in the test statistics is maximized. This results in powerful omnibus tests. In particular, in Desgagné et al. (2022), we performed a comprehensive empirical power comparison of 40 goodness-of-fit tests for the univariate Laplace distribution against 400 alternatives and our Laplace omnibus test performed best. Second, the distribution of our test statistics under the null hypothesis can be approximated very closely, for all sample sizes (up to very high precision for ), either by a for our omnibus tests or by the for the -scores. As a result, we obtain turnkey goodness-of-fit tests that allow accurate and easy calculation of critical values and p-values without the need to rely on simulated quantiles or tables, which can certainly facilitate their acceptance and implementation. Note that this is a rare feature in the Laplace test literature. Third, thanks to the -th-power skewness and net kurtosis – which extend Pearson’s notions of skewness and kurtosis –, the rejection of the null hypothesis is accompanied with a direct interpretation: the distribution can be skewed to the right or to the left, exhibit heavy or light tails. Fourth, when we know that the distribution of the random variable is symmetric, we can take advantage of this information to increase power. To achieve this, we propose to use the -score based on the -th-power net kurtosis as a test statistic against symmetric alternatives.

In this paper, we focus on applications to temperature data. The Gaussian distribution is used for example by Allen (1996) for human body temperatures, by Chamberlain et al. (1995) for ear temperatures measured using an infrared emission detection thermometer, by Issautier et al. (1998) for core electron temperatures, and by Pardo et al. (2017) for sea surface temperatures, while the Gaussian model is questioned by DeWitt and Friedman (1979) in the context of body temperatures of ectotherms and by Schoenau and Kehrig (1990) for heating or cooling degree days in buildings. In Section 4, we analyse a temperature dataset containing errors defined as the difference between observed ocean surface temperatures and forecasted values given by a geostatistical model (Gel et al., 2007). We show that the Laplace distribution, and more so the , is a better model than the Gaussian distribution. We also study the Gaussian and Laplace modelling of a large dataset () of domestic refrigerator temperatures collected as part of a study to help consumers reduce bacterial growth and ensure the quality and safety of food products stored at home for U.S. households (Kosa et al., 2007). We finally investigate a London temperature time series using a moving-average model with Gaussian and Laplace innovations (Piggott, 1980; Shea, 1987).

The remainder of the paper is structured as follows. In Section 2, we define reparametrized versions of the EPD and APD families, the null and alternative hypotheses of our tests, -th-power skewness, kurtosis and net kurtosis. In Section 3.1, we present our family of goodness-of-fit tests for the EPD. We establish the asymptotic test statistics and then adapt them for all sample sizes using simulation and regression techniques. Their asymptotic distributions under the null hypothesis are also given. In Section 3.2, we present the asymptotic distributions of the test statistics under local alternatives, which allows us to obtain asymptotic power curves. Specific cases of goodness-of-fit tests for Laplace and Gaussian distributions are presented in Section 3.3. In Section 4, as described above, we investigate Laplace, Gaussian and EPD modelling of three temperature datasets using our family of tests. Section 5 gathers the results of an extensive empirical power comparison of goodness-of-fit tests for the Laplace distributions. The conclusion follows in Section 6. All the detailed programming codes using the R software and all the proofs are given in the Supplementary Material.

2 Background and preliminaries

2.1 Family of asymmetric power distributions

The asymmetric power distribution (APD) introduced by Komunjer (2007) is a generalization of the exponential power distribution (EPD) (Kotz et al., 2001, p. 271), the latter also being known as the generalized error distribution or the generalized normal distribution (Nadarajah, 2005). The APD family is broader in that it combines the wide range of exponential tail behaviours provided by the symmetric EPD with different levels of asymmetry. Below we propose a modified version of the original APD density function defined in Komunjer (2007, Section 2) by modifying its original scaling through the change of variable and by adding location and scale parameters. In our context, is a fixed parameter chosen by the user.

Definition 2.1.

A random variable is said to be distributed if its density function is given by

| (1) |

where , is the asymmetry parameter, is the tail decay parameter, is the location parameter, is the scale parameter, ,

| (2) |

By integrating (1), one can easily verify that the cumulative distribution function (c.d.f.) is given by

| (3) |

which makes it possible to generate observations (see the proof in the Supplementary Material, Section B.1) by taking

| (4) |

|

2.2 The null and alternative hypotheses

We now consider particular cases of the which will form the null and alternative hypotheses of the tests. First, we define the distribution to be tested in the null hypothesis.

Definition 2.2.

A random variable is said to be distributed if its density function is given by

| (5) |

where , is the tail decay parameter, is the location parameter and is the scale parameter.

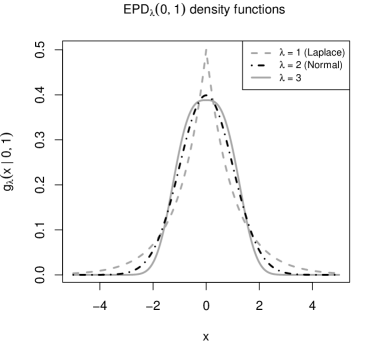

In particular, we obtain the distribution if and the distribution if , as illustrated in Figure 1.

We want to construct goodness-of-fit tests for specific , with a fixed value of . In particular, the values of and lead to tests for Laplace and Gaussian distributions. If the random sample is denoted by

| (6) |

then, for a fixed value of , the composite null hypothesis for all our tests is given by

| (7) |

The alternative hypothesis will depend on the type of test. Consider an omnibus test for the designed to detect all types of alternatives, whether asymmetrical or symmetrical with heavy or light tails. The alternative hypothesis is then given by

| (8) |

However, our strategy is to approximate as many existing distributions as possible by the large APD family. Therefore, we use this alternative hypothesis instead:

| (9) |

When specific information about the distribution of the random variable is known or assumed, we can take advantage of it to construct a more powerful directional test by narrowing the universe of the alternative hypothesis. Consider a directional test for the designed to detect asymmetric alternatives. For a fixed value of , the alternative hypothesis is then given by

| (10) |

Consider finally a directional test for the designed to detect symmetric alternatives. For a fixed value of , the alternative hypothesis is then given by

| (11) |

and the density function of the is given by

| (12) |

since (see Definition 2.1).

2.3 Other definitions and notation

Proposition 2.3.

For an i.i.d. sample and for a fixed value of , the maximum likelihood estimators of and for the (see Definition 2.2) are given by

| (13) |

and

| (14) |

Remark 2.4.

Following the usual convention, we define the median of an ordered sample as the central value if is odd and as the arithmetic mean of the two central values if is even. Also, when , has no explicit expression, however, the numerical calculation is simple.

Remark 2.5.

We prove in the Supplementary Material Section B.2 that and are strongly consistent, both under and .

Definition 2.6.

For an i.i.d. sample and for a fixed value of , the ‘-th-power skewness’ and the ‘-th-power kurtosis’ are, respectively, given by

| (15) |

where , and are the maximum likelihood estimators of and for the as given in Proposition 2.3, and we define .

Remark 2.7.

For any sample , note that as a direct consequence of Jensen’s inequality and the convexity of :

| (16) |

As their names suggest, the -th-power skewness and kurtosis are new measures of asymmetry and tail thickness for the data distribution. Our test statistics will be based on these two quantities. A positive (resp. negative) value of suggests that the distribution is right-skewed (resp. left-skewed), while a value close to 0 suggests that the distribution is symmetric. A large (resp. small) value of corresponds to a heavy-tailed (resp. light-tailed) distribution.

Definition 2.8.

For an i.i.d. sample and for a fixed value of , the ‘-th-power net kurtosis’ is given by

| (17) |

where and are given in Definition 2.6.

The -th-power net kurtosis will be used instead of the -th-power kurtosis in our test statistics to correct for dependence with the -th-power skewness for small to moderate sample sizes. A large (resp. small) value of corresponds to a heavy-tailed (resp. light-tailed) distribution, given the level of skewness. Note that in practice the only cases where we found the maximum function needed to bound a (slightly) negative value of in (17) were for nearly symmetric samples with extremely light tails ( and close to 0), and thus far from the null hypothesis.

Remark 2.9.

Analogously, for a random variable with an arbitrary distribution function , the -th-power skewness, -th-power kurtosis and -th-power net kurtosis can be defined, respectively, as

and

where , with , , and in general for , is the numerical solution to , which is unique for most known distributions. These measures, which represent the asymptotic version of their sample counterparts, can be useful in comparing the asymmetry and tail thickness of a distribution relative to the tested in . For symmetric distributions , we have and . For example, , , , , , and .

Notation. For , the gamma, digamma and trigamma functions are denoted respectively by

| (18) |

The chi-square distribution with 2 degrees of freedom is denoted by and its counterpart with the non-centrality parameter by . Convergence in distribution, in probability, and almost-surely, are denoted respectively by , , and , as . Furthermore, we note ‘ ’ for ‘approximately distributed as’.

3 Goodness-of-fit tests for the

In Section 3.1, we present our family of goodness-of-fit tests for the EPD and their asymptotic distributions under the null hypothesis. The asymptotic distributions under local alternatives are given in Section 3.2. Finally, the Laplace and Gaussian goodness-of-fit tests are presented in Section 3.3.

3.1 The test statistics and their distributions under the null hypothesis

We first use Rao’s score test on the APD family specified in . For the omnibus test, this consists in taking the -dimensional asymptotic test statistic

| (19) |

and replacing and with their maximum likelihood estimators and under . Only the first (resp. second) component of the vector in (19) is needed for the test against asymmetric (resp. symmetric) alternatives. The resulting test statistics are given in Definition 3.1. Their construction is detailed in the Supplementary Material B. These tests are only valid for very large sample sizes, but will be adapted below for all sample sizes. The case is not studied in this paper because the numerical solution to the equation in Proposition 2.3 is not unique, which makes the calculation of the maximum likelihood estimate of unstable due to multiple modes. Moreover, some proofs break down for (such as the proof of Proposition B.5, and thus the proof of Theorem 3.3) or would have to be significantly extended. Therefore, dealing with the case is not obvious and would require extensive additional research.

Definition 3.1.

Consider the tests of fit for the with a fixed value of . The statistic for the asymptotic directional test of fit against asymmetric alternatives is given by

| (20) |

while the statistic for the asymptotic directional test of fit against symmetric alternatives is given by

| (21) |

where and are respectively the sample -th-power skewness and -th-power kurtosis given in Definition 2.6, and are defined in (18). The statistic for the asymptotic omnibus test is given by

| (22) |

Remark 3.2.

The superscript symbol in Definition 3.1 indicates the asymptotic nature of the test statistics.

Theorem 3.3.

Under the null hypothesis, we have, as ,

| (23) |

Remark 3.4.

Theorem 3.3 contains our main theoretical result. The proof is presented in the Supplementary Material Section B.3. When and are known and fixed, this result follows by a standard application of the central limit theorem. Here the proof is rendered more difficult by the fact that and are replaced by their maximum likelihood estimators, and , which requires a control of the first-order derivatives of the score function when we expand the score function around and under . Nevertheless, controlling the derivatives is straightforward using ideas that go back to Lucien Le Cam on the uniform law of large numbers, see, e.g., Chapter 16 in Ferguson (1996). However, there is one exception, namely . In that case, one of the components of the first-order derivative matrix has misbehaving logarithmic summands. In its essential form, for , the problem reduces to showing that

| (24) |

Notice that blows up when is close to zero for . In more technical terms, the envelope of the class of functions is infinite in any small neighbourhood of , which means that standard uniform laws of large numbers cannot be applied, see, e.g., (van der Vaart and Wellner, 1996, Section 2.4). The saving grace is that while blows up at , it is still integrable locally at , and is mild enough at infinity to be dominated by the exponential tail of the Laplace distribution (i.e., the distribution). Under such conditions, it is to be expected that some form of uniform law of large numbers still holds, so that (24) is true (numerical simulations also confirm that intuition) and the aforementioned control on the first-order derivatives remains valid. In Lafaye de Micheaux and Ouimet (2018), a new uniform law of large numbers for summands that blow up was developed for this specific purpose. Using the main result in that paper, it can be shown that

| (25) |

so that the convergence in (24) holds not only in probability, but in fact in .

Theorem 3.3 gives us two independent normally distributed -scores representing asymptotic test statistics designed to detect asymmetric and symmetric alternatives, which can be combined into an omnibus test statistic converging to a distribution. As is often the case for small to moderate sample sizes, we observed that the distributions of Rao’s score test statistics and are not well approximated, under the null hypothesis, by their asymptotic distribution. Moreover, the independence of these two measures does not hold. To solve this problem, we generalize the approach adopted in Desgagné and Lafaye de Micheaux (2018). We address here the specific cases , but the approach would be the same for all . To increase precision, we optimized our approximations for , but they remain valid for smaller sample sizes.

The most important issue to address is the dependence between and , which increases as the sample size decreases and the value of increases (meaning lighter tails). A skewed distribution with a large value of is often also heavy-tailed with a large value of . This situation, at first sight complex, can fortunately be solved by using , the -th-power net kurtosis introduced in Definition 2.8. We find numerically that and are closely distributed as a normal and that the dependency between them is negligible, for all . The power of is inspired by an improvement of the Wilson-Hilferty cube root transformation that leads to approximate normality (see Hawkins and Wixley (1986)). Since we designed the -th-power net kurtosis to replace the -th-power kurtosis, the next step is to define an asymptotic -score denoted to replace . We found that the two -scores are asymptotically equivalent.

Definition 3.5.

Consider the test of fit for the with a fixed value of . A statistic equivalent to for the asymptotic directional test of fit against symmetric alternatives is given by

| (26) |

where is the -th-power net kurtosis given in Definition 2.8.

Proposition 3.6.

Under the null hypothesis, we have, as ,

| (27) |

| (28) |

The proof of Proposition 3.6 is given in the Supplementary Material Section B.5. Since the -scores and are affine transformations of and , they are also very close to being independent and normally distributed for all sample sizes. The final step is to adapt and to ensure that their expectations and variances are very close to 0 and 1 respectively, for all sample sizes , always under the null hypothesis. We can show that for all sample sizes under the null hypothesis, but we have to use simulation and regression techniques to approximate , and . Specifically, for , we fit the three following linear regression models with no intercept term:

| (29) |

| (30) |

where , and are estimated using 1,000,000 simulations for each value of , with . The values of and are arbitrary since , and are location-scale invariant. The dependent variables of the regressions are given by the ratio of the finite and asymptotic variances (or expectations), minus 1. The explanatory variables are given by , , and the coefficients are given by . The values , , , are chosen to maximize the value of their respective regressions. The quality of fit of the regressions is remarkable with values close to 1.

We present the resulting test statistics in Definition 3.7, with their asymptotic distributions is Proposition 3.8 and their approximate distributions for all sample sizes in Proposition 3.9.

Definition 3.7.

Consider the tests of fit for the with a fixed value of . The statistic for the directional test of fit against asymmetric alternatives, for all sample sizes, is given by

| (31) |

while the statistic for the directional test of fit against symmetric alternatives, for all sample sizes, is given by

| (32) |

where and are respectively the sample -th-power skewness and -th-power net kurtosis given in Definitions 2.6 and 2.8, are defined in (18) and the constants , are provided in Table 1 for . The statistic for the omnibus test, for all sample sizes, is given by

| (33) |

| (even ) | 1.06 | -1.856 | 1.01 | -0.422 | 0.92 | -1.950 | 2.3 | 39.349 |

|---|---|---|---|---|---|---|---|---|

| (odd ) | 1.03 | -0.281 | 0.86 | -0.198 | 1.04 | -3.827 | 1.0 | 0.000 |

| 0.99 | -0.952 | 0.99 | -0.637 | 0.55 | -3.488 | 0.5 | 2.434 | |

| 0.99 | -1.890 | 1.00 | -0.788 | 1.05 | -9.327 | 1.4 | 14.208 | |

| 0.99 | -2.981 | 0.99 | -0.844 | 1.10 | -23.104 | 1.3 | 30.028 | |

| 0.97 | -3.855 | 0.98 | -0.880 | 1.14 | -95.743 | 1.2 | 103.871 |

Proposition 3.8.

Under the null hypothesis, we have, as ,

| (34) |

| (35) |

The proof of Proposition 3.8 is given in the Supplementary Material Section B.6.

Proposition 3.9.

Under the null hypothesis, we have, for all sample sizes (up to very high precision for ),

| (36) |

|

|

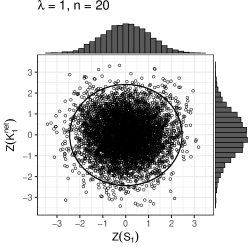

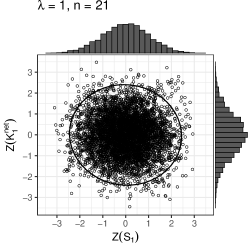

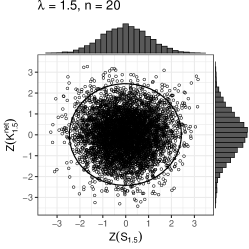

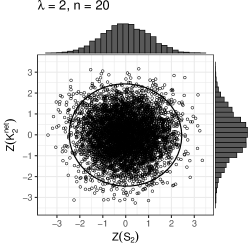

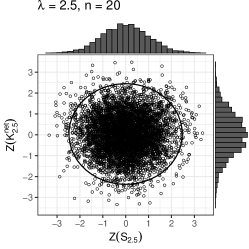

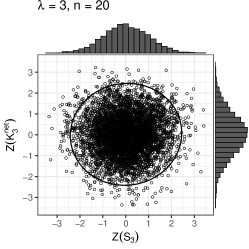

Proposition 3.8 states that the test statistics and are asymptotically equivalent to and , respectively, and therefore share the same asymptotic distributions. We combine them to obtain the omnibus test statistic , which is asymptotically distributed. Proposition 3.9 states that these asymptotic distributions are also valid approximations for all sample sizes, and this with high numerical precision when . We assessed the quality of the fit by performing a study of the empirical level (empirical power under the null hypothesis) of the statistic based on 1,000,000 simulations and on quantiles, for different sample sizes between 20 and 200, for and for significance levels . We found that the empirical and nominal levels are very close, with absolute differences less than 0.001. Furthermore, the and test statistics are plotted in Figure 2 for 5000 samples of size (or for the case of an odd sample size when ) generated under the null hypothesis, for values of . We observe that they behave like two independent standard Gaussian variables. The points outside the circle (which defines the critical region for a significance level of 5%) are relatively well distributed, as desired.

For the omnibus test, the null hypothesis that the observations come from the , with unknown and , is rejected for high values of the test statistic, specifically if the observed value of is greater than the chi-square quantile , at a significance level of . The p-value can be computed as , where is a distributed random variable. For the directional test against symmetric alternatives, is rejected if the observed test statistic is far from 0, specifically if or , where is the standard Gaussian quantile at a significance level of . The p-value can be computed as , where is a distributed random variable. We obtain the same conclusion for the directional test against asymmetric alternatives, replacing by .

If the null hypothesis is rejected, the cause can easily be identified. We observe that and are -scores of and , respectively. The further they deviate from 0, the more evidence there is for the rejection of the null hypothesis. A significant positive (resp. negative) value of suggests that the distribution is right-skewed (resp. left-skewed), while a value close to 0 suggests that the distribution is symmetric. A significant positive (resp. negative) value of suggests that the tails of the distribution are heavier (resp. lighter) than those of the , given the level of skewness.

3.2 Asymptotic distribution of the test statistics under local alternatives

We are interested in this section in calculating the asymptotic power of our tests, that is, the probability of correctly rejecting the null hypothesis when a specific alternative hypothesis is the true distribution, as . Since the asymptotic power of a well-designed test is equal to 1 for any fixed alternative different from the null hypothesis, we instead consider local alternatives (as was done by Falk et al. (2008) in the context of a Pareto distribution) that approach the as .

We then refine our general alternative hypothesis , , by a family of local alternatives, defined as

| (37) |

where are fixed (but arbitrary) for the omnibus test. We fix () for the test against asymmetric alternatives or () for the test against symmetric alternatives. The notation should be interpreted as any functions converging to 0 as . The constants and indicate the direction of the alternative relative to the specified in the null hypothesis. More precisely, (resp. ) represents a right-skewed (resp. left-skewed) alternative and (resp. ) results in an alternative with heavier (resp. lighter) tails.

Theorem 3.10.

Under the local alternatives , for fixed and , we have, as ,

| (38) |

where , are given in Definition 3.1 and is the noncentrality parameter of the distribution, with

| (39) |

The proof of Theorem 3.10 is presented in the Supplementary Material Section B.7. As a consequence, we obtain analogous convergence results for our test statistics adapted for small to moderate sample sizes.

Corollary 3.11.

The proof of Corollary 3.11 is given in Section B.9. Corollary 3.11 states that and , like and , are asymptotically equivalent also under local alternatives. We are therefore able to compute the asymptotic powers of our test statistics under local alternatives. For example, if the true distribution is for fixed values of , the asymptotic power of the omnibus test is given by , where is the quantile of the distribution at a significance level of and . If the true distribution is for a fixed value of , the asymptotic power of the test is given by , where is the quantile of the distribution at a significance level of and . We obtain similar results for the test . Note that the asymptotic powers are the same regardless of the sign of and by symmetry of the normal distribution.

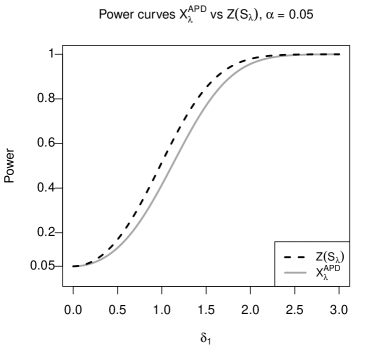

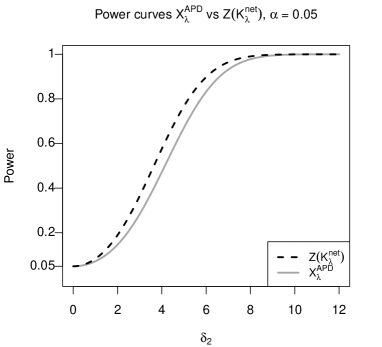

In Figure 3, the asymptotic power curves are shown under local alternatives for the case and a significance level of . In this case, the critical values are and . On the left graph, the power curves of and are compared under local alternatives, , for values of . We observe that the power of the directional test against asymmetric alternatives is uniformly higher than that of the omnibus test , as expected given the asymmetric family of alternatives. We also see that the power reaches its minimum at , where it is equal to the significance level , and gradually increases from 0.05 to 1 as moves away from 0, as expected. On the right graph, the power curves of and are compared under local alternatives, , for values of . We observe similar results.

|

3.3 Tests of fit for Laplace and Gaussian distributions

In this section, we summarize our previous results for the specific cases where is set to 1 or 2, namely the goodness-of-fit tests for Laplace and Gaussian distributions. We obtain simplified formulas which are worth presenting.

3.3.1 Tests of fit for the Laplace distribution

The omnibus test statistic for testing the null hypothesis

is given by

| (42) |

where (using Definition 3.7 with )

| (43) |

for an even sample size , and by

| (44) |

for an odd sample size , where the Euler-Mascheroni constant is given by

| (45) |

The first-power skewness and the first-power kurtosis (see Definition 2.6) are given by

| (46) |

where , while the first-power net kurtosis (see Definition 2.8) is given by

| (47) |

where the maximum likelihood estimators under (see Proposition 2.3) are given by

| (48) |

3.3.2 Tests of fit for the Gaussian distribution

The omnibus test statistic for testing the null hypothesis

is given by

| (50) |

where (using Definition 3.7 with , and )

| (51) |

| (52) |

where is the Euler-Mascheroni constant. The second-power skewness and the second-power kurtosis (see Definition 2.6) are given by

| (53) |

where , while the second-power net kurtosis (see Definition 2.8) is given by

| (54) |

where the maximum likelihood estimators under (see Proposition 2.3) are given by

| (55) |

4 Three applications to real temperature data

4.1 Prediction errors in geostatistical modelling of ocean surface temperatures

Mesoscale oceanography is the study of weather in the ocean at medium (‘meso’) scale. The most used mesoscale model MM5 (NCAR–Penn State Mesoscale Model Generation 5) enables one to make numerical ocean weather predictions. Gel et al. (2004) proposed a model to improve such predictions. Their model is the sum of two terms: one that corrects the forecasts for additive and multiplicative bias through spatio-temporal covariables, and one mean-zero stationary Gaussian spacetime stochastic process error term.

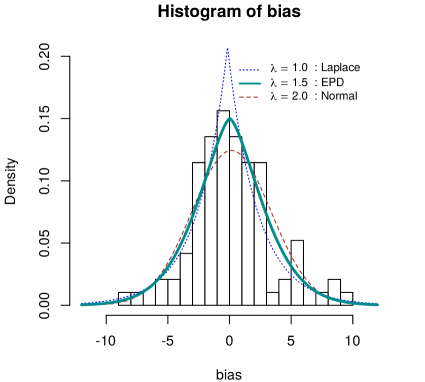

In that context, our first set of temperature data consists of prediction errors of 48-hour ahead MM5 forecasts of surface temperature measured at 96 locations in the US Pacific Northwest on 3-January-2000. The prediction error is the difference between the forecasted and observed surface temperature. This dataset is available as bias.rda in the R package lawstat (Gastwirth et al., 2019).

The histogram of this data (Figure 4) exhibits some heavier tails than the fitted density (dashed line), and a peak slightly lower than the one captured by the fitted Laplace() density (dotted line).

Consequently, we decided to fit an asymmetric EPD distribution with , a value between (Laplace) and (Normal). This leads to the density (bold line) which better captures the pattern of the histogram.

Of course, one can apply goodness-of-fit tests to confirm these findings. Gel et al. (2007) concluded to the non-normality of these data using the Shapiro-Wilks (), Jarque-Bera () and Bonett-Seier () tests and our omnibus normality test goes in the same direction (). In Table 2, we apply our tests for and , and we conclude that the is better than the normal and Laplace distributions fitted above, even if the Laplace also appears as a good fit.

| 1.0 | 1.5 | 2.0 | |

|---|---|---|---|

| 1.314 (0.189) | 1.457 (0.145) | 1.778 (0.075) | |

| -1.501 (0.133) | 0.700 (0.484) | 2.149 (0.032) | |

| 3.979 (0.137) | 2.612 (0.271) | 7.781 (0.020) |

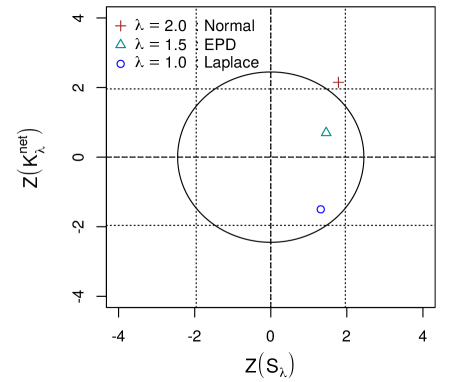

The information in Table 2 is also displayed graphically in Figure 5. Overall, the symbol is well within the circle whereas the symbols for the two other distributions are located closer to the circle at an angle of about which leads us to favour the former distribution.

From Figure 5, for the three models ( and ), the data are right-skewed with , though these results are not significant at the 5% level (all three symbols are located between the two vertical dotted lines with abscissa and ). We also see that the data have

-

1.

heavier tails than the Gaussian distribution (positive value of ; significant at the 5% level as indicated by the symbol above the upper horizontal dotted line);

-

2.

shorter tails than the Laplace distribution (negative value of ; non-significant since the symbol is between the two horizontal dotted lines);

-

3.

slightly heavier tails than the distribution (positive value of ; clearly non-significant with a symbol close to the origin).

Based on these results, one could extend the initial model of Gel et al. (2004) to use a non-Gaussian random field error term (see, e.g., Åberg and Podgórski (2011)). This would then allow for the estimation of probabilities of various weather scenarios by simulating or Laplace random fields for the errors.

4.2 Home refrigeration temperatures and food safety

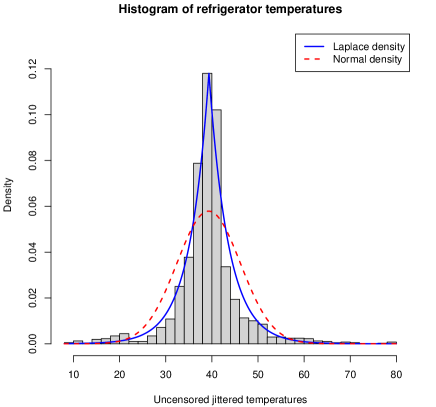

In this section, we analyse a dataset111Source: Q62 in XLS file at https://www.foodrisk.org/resources/sendFile/49 and see https://www.foodrisk.org/resources/sendFile/46 for a description of the format. containing refrigerator temperatures collected in a study aiming at helping consumers reduce bacterial growth and thus ensure the quality and safety of food products stored at home for U.S. households (Kosa et al., 2007). For convenience, we also provide a CSV version of this file, called refrig.csv, in the Supplementary Material A.3. This dataset was also analysed by Pouillot et al. (2010). In the original file, the data are encoded with integers in , corresponding to the temperatures (in degrees Fahrenheit) “more than F”, 58F, 56F, 54F, …, 24F, 22F, 20F, and “less than F”, respectively. In order to transform these grouped and censored data into uncensored continuous observations, we added to each one of the 20 grouped data an independent observation sampled from a . We also replaced the “less than F” and “more than F” censored values with random Laplace() observations on the intervals and , respectively, where and are the maximum likelihood estimates provided by Pouillot et al. (2010) using the censored data. An histogram of these uncensored jittered values is shown in Figure 6 together with the best fit obtained via a maximum likelihood approach, assuming a Laplace () or a Gaussian () distribution. The figure makes it clear that a Laplace distribution is more appropriate for these data than a normal distribution.

Of course, for such a large sample size, any goodness-of-fit test would almost certainly reject any a priori distributional assumption. In order to make the analysis more interesting, we considered the original (uncensored jittered) temperatures as the population from which we sampled at random and without replacement, times, a sub-sample of (moderate) size . For each such sub-sample (of size ) we computed the -value of our new test under both the null hypothesis that (i.e., a Laplace distribution) or under the null hypothesis that (i.e., a normal distribution). Numerical summaries of the -values for these two cases are given in Table 3. We also calculated that Laplacity was not rejected for 57.5% of the sub-samples, while Gaussianity was not rejected only for 2.5% of these sub-samples, for a significance level of 5%. Based on these results, one can safely assume that a Laplace distribution is more appropriate than a normal distribution for these data.

| Case | 1st Quart. | Median | Mean | 3rd Quart. |

|---|---|---|---|---|

| Laplace | 0.01412 | 0.07688 | 0.18661 | 0.27234 |

| Normal | 0.00000 | 0.00000 | 0.00629 | 0.00016 |

In order to steer clear of foodborne illnesses, the U.S. Food and Drug Administration recommends to “keep the refrigerator temperature at or below F”222Source: https://www.fda.gov/consumers/consumer-updates/are-you-storing-food-safely. Thanks to our parametric fit using a Laplace distribution, one can estimate the proportion of refrigerators having a temperature above this threshold to be (in the population of 2007 U.S. households). In comparison, this proportion under the Gaussian distribution is , reflecting the underestimation of the central values and the overestimation of the values in the “shoulders”.

4.3 London time series temperatures

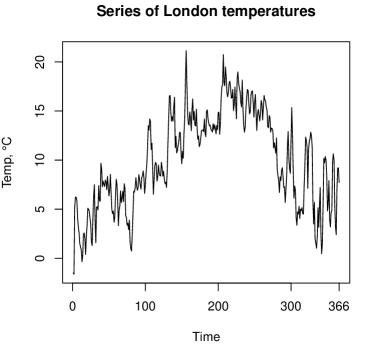

Shea (1987) proposed an algorithm for the computation of the exact likelihood of a multivariate time series and illustrated the methodology on a bivariate dataset of wind speed and temperature values. This data was originally studied by Piggott (1980) in an attempt to predict the residential consumption of gas in London. Here we revisit the task of building a univariate time series model for the daily temperature values , , represented in Figure 7.

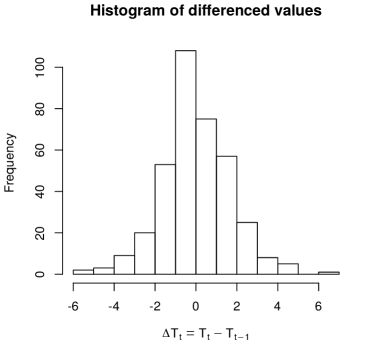

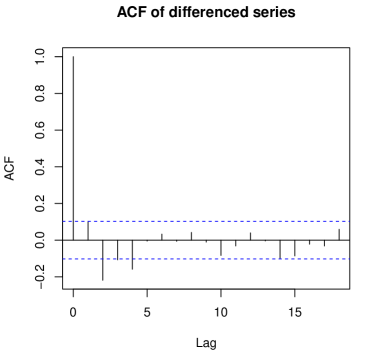

It is clear that this series is non-stationary, leading us to compute first order differences , (taking ), the histogram of which is shown in Figure 8 (left). An ACF plot (Figure 8; right) suggests that we use the model if a Gaussian distribution (with variance ) is assumed for the innovations (). This is often the case for temperatures as discussed in the previous example.

This is also confirmed by selecting the best model, in terms of AIC, among all models, , fitted on the centred values. (An AIC value of was found using Matlab; the coefficients of the fitted Gaussian model, without intercept, being , , and , with an estimated variance of and a log-likelihood of .) The exact same model was fitted by Shea (1987) and by Ducharme and Lafaye de Micheaux (2004).

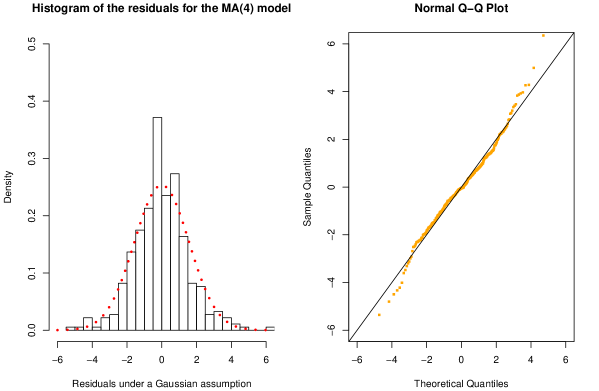

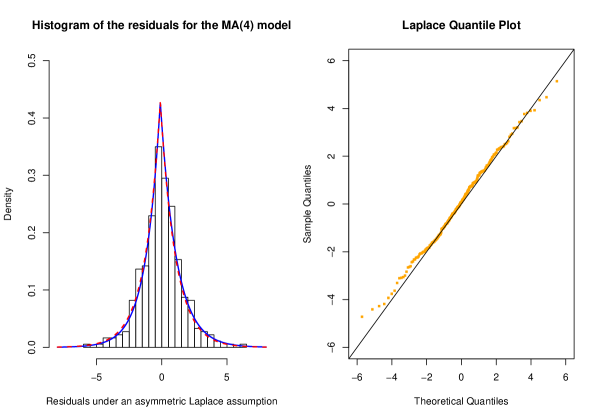

However, a look at the histogram of the residuals () of the fitted Gaussian MA(4) model, and at the associated QQ-plot in Figure 9, does not fully support the Gaussian assumption of the innovations. It is especially clear in the QQ-plot that the tails are heavier than those of a Gaussian distribution, while the histogram reveals that the middle peak is not adequately captured. This is confirmed by our new test of normality applied on these residuals (). Similar results are obtained if one uses the Jarque-Bera test () or the Duchesne et al. (2016) test ().

According to Lomnicki (1961), if the innovations are Gaussian, then the observations are also Gaussian, thanks to the central limit theorem. Therefore, we also applied our test of normality directly on the observations and obtained a -value of , which suggests that the observations, and hence the innovations, are not Gaussian. Consequently, it might not be such a good idea to fit an MA model with Gaussian innovations to these data. Now, even if non-Gaussian ARMA models are rather scarce in the literature (see Li and McLeod (1988); Lehr and Lii (1998); Ozaki and Iino (2001); Trindade et al. (2010) for the few references we could find), we believe this topic deserves more attention as illustrated below.

The histogram in Figure 9 (left) seems more peaky than the corresponding Gaussian density, with heavier tails. The statistic for the directional test of fit against symmetric alternatives is , which is statistically significant. There is a slight right asymmetry. The statistic for the directional test of fit against asymmetric alternatives is . Even though a linear combination of Laplace distributed random variables is not necessarily of Laplace type, the shape of the histogram suggests to fit an MA model using an distribution (asymmetric Laplace, AL) for the innovations. The best model (fitted using Matlab on the centred values and assuming an AL likelihood parametrized as in Trindade et al. (2010)), in terms of both AIC and parsimony, is also an model. The estimated coefficients are , , and , with an AIC of , a value much smaller than the AIC of 1380 we obtained when fitting an model with Gaussian innovations. The estimated values of the location and scale parameters of the distribution are respectively and . The estimated skewness parameter value is , quite close to 1, a value associated to perfect symmetry. A look at the histogram of the residuals (for this second model) and the associated QQ-plot (Figure 10) now favours an asymmetric Laplace assumption As we can see in Figure 10, a density curve of an (solid blue line) has been superimposed to the histogram of the residuals and the fit is good. We also added a symmetric Laplace (dashed red line) and we observe that it is practically identical, given that is close to 1, as mentioned above. Therefore, we applied our Laplacity test on the residuals of this model, and we do not reject the null hypothesis ().

To summarize, based on these results, there is a substantial support in favour of the model with asymmetric Laplace errors (AIC=1365; ) compared to the model with Gaussian errors (AIC=1380; ); see Burnham and Anderson (2004). One could also consider the more parsimonious model with asymmetric Laplace innovations (AIC=1380; ). The histogram of the residuals and the asymmetric Laplace QQ-plot for this model (not shown here) are very similar to the ones displayed in Figure 10.

5 Empirical power comparison

Empirical power comparison using Monte Carlo simulations is useful if done thoroughly, with a large number of tests and alternatives. Given the magnitude of this task, we focus our analysis on Laplace tests, or equivalently on tests with . Note that an empirical power comparison was performed in Desgagné and Lafaye de Micheaux (2018), where 13 of the best goodness-of-fit tests for the normal distribution () were compared against 85 alternatives for different sample sizes. One of these tests, denoted by , is an omnibus test also based on second-power skewness and kurtosis and practically equivalent to our test. Overall, three normality tests stood out as the most powerful, with the test in second place just behind the Chen and Shapiro (1995) test based on normalized spacings and ahead of the famous Shapiro and Wilk (1965) test.

In Desgagné et al. (2022), we performed a comprehensive empirical power comparison of 40 goodness-of-fit tests for the univariate Laplace distribution – including our new and tests – carried out using Monte Carlo simulations with sample sizes , significance levels , and 400 alternatives. The set of alternatives, formed of asymmetric and symmetric light/heavy-tailed distributions, consists of 20 specific cases of 20 submodels drawn from 11 main models. For each submodel, the 20 specific cases correspond to parameter values chosen to cover the entire power range.

We first identify in Table 4 the best omnibus tests against all 400 alternative distributions considered in the simulation study, whether symmetric/asymmetric light/heavy-tailed. The 10 most powerful tests (among the 40 candidates) are listed for each sample size and . As an interpretational aid, we define the “gap” as the difference between the maximum average power amongst the 40 tests and the average power of a given test. We obtained four such gaps for each test, one for each sample size. The “maximum gap” and “average gap” for a given test are defined as the maximum and the average of those 4 gaps. To complete Table 4, we have included the 10 best tests in terms of maximum and average gaps. We observe that the most powerful omnibus test, regardless of sample size, is our new test, with an average gap of 1.5% and a maximum gap of 3%. Note that the full name of the test abbreviations listed in Table 4 can be found in Table 2 in Desgagné et al. (2022).

| Wa | ||||||||||

| Power | 47.0 | 46.4 | 46.2 | 45.3 | 45.2 | 44.9 | 44.7 | 44.5 | 44.2 | 44.0 |

| Gap | - | 0.6 | 0.8 | 1.7 | 1.8 | 2.1 | 2.3 | 2.5 | 2.8 | 3.0 |

| LK | Wa | |||||||||

| Power | 63.7 | 62.6 | 62.3 | 60.8 | 60.4 | 60.4 | 60.1 | 59.0 | 58.9 | 58.8 |

| Gap | - | 1.1 | 1.4 | 2.8 | 3.2 | 3.3 | 3.5 | 4.7 | 4.7 | 4.8 |

| LK | Wa | Ku | ||||||||

| Power | 74.3 | 72.3 | 71.8 | 71.7 | 71.7 | 71.4 | 69.0 | 68.6 | 68.1 | 67.8 |

| Gap | - | 1.9 | 2.4 | 2.5 | 2.6 | 2.8 | 5.2 | 5.7 | 6.2 | 6.5 |

| Wa | LK | Ku | BS | |||||||

| Power | 81.8 | 80.7 | 80.3 | 79.5 | 79.1 | 78.0 | 77.3 | 77.1 | 76.8 | 76.8 |

| Gap | - | 1.1 | 1.5 | 2.3 | 2.7 | 3.8 | 4.5 | 4.7 | 5.0 | 5.0 |

| Max | Wa | LK | ||||||||

| Gap | 3.0 | 3.3 | 3.5 | 4.7 | 5.0 | 5.0 | 7.3 | 7.7 | 7.8 | 7.9 |

| Average | Wa | LK | Ku | |||||||

| Gap | 1.5 | 2.3 | 2.8 | 2.8 | 3.0 | 3.3 | 3.8 | 4.1 | 5.7 | 5.9 |

Similarly, we identify in Table 5 the best tests against the 240 symmetric alternative distributions (from the 12 symmetric submodels) considered in the simulation study, whether light or heavy-tailed. The 10 most powerful tests (among the 40 candidates) are listed by sample size and in terms of maximum and average gaps, for . We observe that our new test stands out as the best for sample sizes of , and also regardless of sample size, with an average gap of 1.0% (1st) and a maximum gap of 4.1% (2nd). Although directional tests designed specifically to detect symmetric alternatives are favoured here, our new omnibus test performs well with an average gap of 3.0% (4th) and a maximum gap of 4.0% (1st).

| Wa | Ku | |||||||||

| Power | 44.5 | 43.5 | 42.9 | 42.8 | 42.8 | 42.4 | 40.6 | 40.3 | 39.5 | 39.1 |

| Gap | - | 1.0 | 1.6 | 1.6 | 1.7 | 2.0 | 3.9 | 4.1 | 5.0 | 5.4 |

| Wa | GV | BS | ||||||||

| Power | 61.9 | 60.1 | 58.2 | 58.2 | 58.1 | 57.5 | 57.4 | 57.3 | 56.6 | 56.5 |

| Gap | - | 1.8 | 3.7 | 3.7 | 3.8 | 4.3 | 4.5 | 4.5 | 5.3 | 5.4 |

| GV | BS | Wa | LK | Ku | ||||||

| Power | 73.4 | 71.4 | 70.5 | 70.5 | 69.3 | 68.7 | 67.3 | 67.1 | 65.9 | 65.6 |

| Gap | - | 2.0 | 2.9 | 2.9 | 4.0 | 4.6 | 6.0 | 6.3 | 7.5 | 7.8 |

| BS | GV | Wa | LK | Ku | ||||||

| Power | 79.6 | 79.5 | 77.4 | 77.1 | 76.9 | 76.8 | 74.9 | 74.7 | 74.2 | 74.0 |

| Gap | - | 0.1 | 2.2 | 2.5 | 2.7 | 2.8 | 4.7 | 4.9 | 5.4 | 5.6 |

| Max | Wa | GV | BS | Ku | LK | |||||

| Gap | 4.0 | 4.1 | 4.6 | 5.0 | 6.0 | 6.0 | 6.3 | 7.6 | 7.8 | 7.8 |

| Average | Wa | BS | GV | Ku | LK | |||||

| Gap | 1.0 | 2.7 | 2.8 | 3.0 | 3.8 | 3.8 | 4.1 | 4.2 | 5.5 | 6.7 |

6 Conclusion

In this article, we introduced a family of goodness-of-fit tests for the distribution with , including tests for the Laplace and Gaussian distributions. We obtained directional tests of fit against asymmetric () and symmetric () alternatives, which we combined into an omnibus test (). These tests are based on interesting new moment-type statistics called ‘-th-power skewness’, ‘-th-power kurtosis’ and ‘-th-power net kurtosis’. The new tests are very powerful and can be used as diagnostics to understand which aspects of the null hypothesis are rejected. Their null distribution is well approximated by the well-known chi-square or Gaussian distributions, for all sample sizes (up to very high precision for ), which allow accurate and easy calculation of critical values and p-values without the need to rely on simulated quantiles. We applied these tests on three sets of real temperature data and were able to demonstrate that a Laplace distribution or an distribution is sometimes a better fit than a Gaussian distribution to model such measurements.

Funding

F. Ouimet was supported by postdoctoral fellowships from the Natural Sciences and Engineering Research Council of Canada (PDF) and the Fond québécois de la recherche – Nature et technologies (B3X supplement and B3XR). F. Ouimet is currently supported by a CRM-Simons postdoctoral fellowship from the Centre de recherches mathématiques and the Simons foundation.

Acknowledgements

We thank the anonymous referee for his/her comments. This research includes computations performed using the computational cluster Katana supported by Research Technology Services at UNSW Sydney. We thank the anonymous referee for his/her comments.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

References

- Åberg and Podgórski (2011) Åberg S, Podgórski K (2011). “A class of non-Gaussian second order random fields.” Extremes, 14(2), 187–222.

- Abramowitz and Stegun (1964) Abramowitz M, Stegun IA (1964). Handbook of mathematical functions with formulas, graphs, and mathematical tables, volume 55 of National Bureau of Standards Applied Mathematics Series. For sale by the Superintendent of Documents, U.S. Government Printing Office, Washington, D.C.

- Allen (1996) Allen LS (1996). “What’s normal? – Temperature, gender, and heart rate.” J. Educ. Stat., 4(2), 1–4.

- Burnham and Anderson (2004) Burnham KP, Anderson DR (2004). “Multimodel Inference: Understanding AIC and BIC in Model Selection.” Sociol. Methods Res., 33(2), 261–304.

- Chamberlain et al. (1995) Chamberlain JM, Terndrup TE, Alexander DT, Silverstone FA, Wolf-Klein G, O’Donnell R, Grandner J (1995). “Determination of normal ear temperature with an infrared emission detection thermometer.” Ann. Emerg. Med., 25(1), 15–20.

- Chen and Shapiro (1995) Chen L, Shapiro SS (1995). “An alernative test for normality based on normalized spacings.” J. Stat. Comput. Simul., 53(3-4), 269–287.

- Desgagné and Lafaye de Micheaux (2018) Desgagné A, Lafaye de Micheaux P (2018). “A powerful and interpretable alternative to the Jarque–Bera test of normality based on 2nd-power skewness and kurtosis, using the Rao’s score test on the APD family.” J. Appl. Stat., 45(13), 2307–2327.

- Desgagné et al. (2022) Desgagné A, Lafaye de Micheaux P, Ouimet F (2022). “A comprehensive empirical power comparison of univariate goodness-of-fit tests for the Laplace distribution.” Journal of Statistical Computation and Simulation, pp. 1–32.

- DeWitt and Friedman (1979) DeWitt CB, Friedman RM (1979). “Significance of skewness in ectotherm thermoregulation.” Am. Zool., 19(1), 195–209.

- Ducharme and Lafaye de Micheaux (2004) Ducharme GR, Lafaye de Micheaux P (2004). “Goodness-of-fit tests of normality for the innovations in ARMA models.” J. Time Ser. Anal., 25(3), 373–395.

- Duchesne et al. (2016) Duchesne P, Lafaye De Micheaux P, Tagne Tatsinkou J (2016). “Estimating the mean and its effects on Neyman smooth tests of normality for ARMA models.” Canad. J. Statist., 44(3), 241–270.

- Falk et al. (2008) Falk M, Guillou A, Toulemonde G (2008). “A LAN based Neyman smooth test for Pareto distributions.” J. Statist. Plann. Inference, 138(10), 2867–2886.

- Ferguson (1996) Ferguson TS (1996). A course in large sample theory. Texts in Statistical Science Series. Chapman & Hall, London.

- Gastwirth et al. (2019) Gastwirth JL, Gel YR, Wallace Hui WL, Lyubchich V, Miao W, Noguchi K (2019). lawstat: Tools for Biostatistics, Public Policy, and Law. R package version 3.3, URL https://CRAN.R-project.org/package=lawstat.

- Gel et al. (2004) Gel Y, Raftery AE, Gneiting T (2004). “Calibrated probabilistic mesoscale weather field forecasting: the geostatistical output perturbation method.” J. Amer. Statist. Assoc., 99(467), 575–583.

- Gel et al. (2007) Gel YR, Miao W, Gastwirth JL (2007). “Robust directed tests of normality against heavy-tailed alternatives.” Comput. Statist. Data Anal., 51(5), 2734–2746.

- Hawkins and Wixley (1986) Hawkins DM, Wixley RAJ (1986). “A note of the transformation of chi-squared variables to normality.” Amer. Statist., 40(4), 296–298.

- Issautier et al. (1998) Issautier K, Meyer-Vernet N, Moncuquet M, Hoang S (1998). “Solar wind radial and latitudinal structure: Electron density and core temperature from Ulysses thermal noise spectroscopy.” J. Geophys. Res. Space Phys., 103(A2), 1969–1979.

- Jarque and Bera (1987) Jarque CM, Bera AK (1987). “A test for normality of observations and regression residuals.” Internat. Statist. Rev., 55(2), 163–172.

- Karst and Polowy (1963) Karst OJ, Polowy H (1963). “Sampling properties of the median of a Laplace distribution.” Amer. Math. Monthly, 70, 628–636.

- Komunjer (2007) Komunjer I (2007). “Asymmetric power distribution: theory and applications to risk measurement.” J. Appl. Econometrics, 22(5), 891–921.

- Kosa et al. (2007) Kosa KM, Cates SC, Karns S, Godwin SL, Chambers D (2007). “Consumer home refrigeration practices: results of a web-based survey.” J. Food Prot., 70(7), 1640–1649.

- Kotz et al. (2001) Kotz S, Kozubowski TJ, Podgórski K (2001). The Laplace distribution and generalizations. Birkhäuser Boston, Inc., MA.

- Lafaye de Micheaux and Ouimet (2018) Lafaye de Micheaux P, Ouimet F (2018). “A uniform law of large numbers for functions of i.i.d. random variables that are translated by a consistent estimator.” Statist. Probab. Lett., 142, 109–117.

- Lehr and Lii (1998) Lehr ME, Lii KS (1998). “Maximum likelihood estimates of non-Gaussian ARMA models.” In Econometrics & Statistics Summer Symposia. University of California Berkeley.

- Li and McLeod (1988) Li WK, McLeod AI (1988). “ARMA modelling with non-Gaussian innovations.” J. Time Ser. Anal., 9(2), 155–168.

- Lomnicki (1961) Lomnicki ZA (1961). “Tests for departure from normality in the case of linear stochastic processes.” Metrika, 4, 37–62.

- Minc and Sathre (1964/65) Minc H, Sathre L (1964/65). “Some inequalities involving .” Proc. Edinburgh Math. Soc. (2), 14, 41–46.

- Nadarajah (2005) Nadarajah S (2005). “A generalized normal distribution.” J. Appl. Stat., 32(7), 685–694.

- Natarajan and Mudholkar (2004) Natarajan R, Mudholkar GS (2004). “Moment-based goodness-of-fit tests for the inverse Gaussian distribution.” Technometrics, 46(3), 339–347.

- Ozaki and Iino (2001) Ozaki T, Iino M (2001). “An innovation approach to non-Gaussian time series analysis.” J. Appl. Probab., 38(A), 78–92.

- Pardo et al. (2017) Pardo D, Jenouvrier S, Weimerskirch H, Barbraud C (2017). “Effect of extreme sea surface temperature events on the demography of an age-structured albatross population.” Philos. Trans. R. Soc. Lond., B, Biol. Sci., 372(1723), 1–10.

- Piggott (1980) Piggott JL (1980). “The use of Box-Jenkins modelling for the forecasting of daily gas demand.” In Paper presented to the Royal Statistical Society.

- Pouillot et al. (2010) Pouillot R, Lubran MB, Cates SC, Dennis S (2010). “Estimating parametric distributions of storage time and temperature of ready-to-eat foods for U.S. households.” J. Food Prot., 73(2), 312–321.

- Rao (1948) Rao RC (1948). “Large sample tests of statistical hypotheses concerning several parameters with applications to problems of estimation.” Proc. Cambridge Philos. Soc., 44, 50–57.

- Rubin and Rukhin (1983) Rubin H, Rukhin AL (1983). “Convergence rates of large deviations probabilities for point estimators.” Statist. Probab. Lett., 1(4), 197–202.

- Schoenau and Kehrig (1990) Schoenau GJ, Kehrig RA (1990). “Method for calculating degree-days to any base temperature.” Energy Build., 14(4), 299–302.

- Shapiro and Wilk (1965) Shapiro SS, Wilk MB (1965). “An analysis of variance test for normality: Complete samples.” Biometrika, 52, 591–611.

- Shea (1987) Shea BL (1987). “Estimation of multivariate time series.” J. Time Ser. Anal., 8(1), 95–109.

- Trindade et al. (2010) Trindade AA, Zhu Y, Andrews B (2010). “Time series models with asymmetric Laplace innovations.” J. Stat. Comput. Simul., 80(12), 1317–1333.

- van der Vaart (1998) van der Vaart AW (1998). Asymptotic statistics, volume 3 of Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, Cambridge.

- van der Vaart and Wellner (1996) van der Vaart AW, Wellner JA (1996). Weak convergence and empirical processes. Springer Series in Statistics. Springer-Verlag, New York. With applications to statistics.

Appendix A Supplementary material (R codes)

All the detailed programming codes using the R software are provided online at the address https://doi.org/doi:10.1080/02331888.2022.2144859 in two R files (A1 and A2). We also provide a CSV file (A3) of the dataset analysed in Section 4.2.

Appendix B Supplementary material (proofs)

In this section, we gather the proofs of the various results we stated in Sections 2 and 3 of the paper entitled “Goodness-of-Fit Tests for Laplace, Gaussian and Exponential Power Distributions Based on -th Power Skewness and Kurtosis”. Throughout, the convergence in law and in probability, under a given measure , will be denoted by and , respectively. A random term going to in -probability as will be denoted by . A random term bounded in -probability as will be denoted by .

B.1 Proof of Equation (3)

B.2 Proof of Remark 2.5

In Lemma B.1 below, we state a small adaptation of a well-known uniform law of large numbers due to Lucien Le Cam. We will use it several times for different proofs in this supplementary material, including the proof of the next lemma (Lemma B.2) regarding the strong consistency of the maximum likelihood estimators and , which we stated in Remark 2.5. The proof of Lemma B.1 follows the strategy described in Section 16 of Ferguson (1996). A small adaptation is needed to treat the case where the parameter space is not compact.

Lemma B.1.

Let be a sequence of i.i.d. random variables, and let be an estimator such that . For , let . Assume that is a measurable function and there exists such that

- (C.1)

-

For all , is continuous on ;

- (C.2)

-

There exists such that for all and .

If and , then

| (61) |

Proof of Lemma B.1.

Fix to a value for which and hold. By the triangle inequality, and since by assumption, we have

| (62) |

By applying a uniform law of large numbers on the compact set (Theorem 16 (a) in Ferguson (1996) with our assumptions and ), the first probability on the right-hand side of (B.2) is zero. By , and the dominated convergence theorem, we know that is continuous on . Since by hypothesis, the second probability on the right-hand side of (B.2) is also zero. ∎

We can now prove the strong consistency of the maximum likelihood estimators.

Lemma B.2.

Let and be defined as in Proposition 2.3. Assume that the observations are i.i.d. and distributed. Then

| (63) |

In other words, the above convergence holds under both and .

Proof of Lemma B.2.

By definition, for all , the estimator is determined by the equation

| (64) |

For any , is non-increasing when . From Theorem 2 and Remark 1 in Rubin and Rukhin (1983) (the proof is a simple application of Chernoff’s theorem), we get that, for any , the probabilities decay exponentially fast in (using the fact that and both hold). In particular, for any , the probabilities are summable in . Hence, by the Borel-Cantelli lemma, we have a.s.

Also, from Proposition 2.3, we have

| (65) |

If we denote and , then it is straightforward to verify that . From Lemma B.1, we deduce

| (66) |

This implies a.s. ∎

Remark B.3.

If is odd or if is even with , then we have the right-continuity of around , namely . Otherwise, if is even, we have more generally , and thus .

B.3 Proof of Theorem 3.3

For short, write

| (67) |

If , we define

| (68) | ||||

| (69) |

We can easily verify (using for example Wolfram Mathematica) that

| (70) |

where recall that denotes the digamma function, and for .

Using the notation in (68), we can write the Rao’s score statistic (see (6))

| (71) |

and the modified score statistic

| (72) |

Note that is location and scale invariant, or said otherwise, -invariant.

The first step of the proof of Theorem 3.3 consists in determining the asymptotic law of the vector

| (73) |

under (see Proposition B.4 below). The proof is a direct application of the central limit theorem. The second step consists in writing as a linear combination of the components of this vector plus a negligible term via a first-order Taylor expansion (see Proposition B.5). The estimation of the derivative part of the expansion is dealt with in Proposition B.6. Using these three propositions (which will be proved in Section B.4), we will then be able to deduce the asymptotic distribution of under .

Proposition B.4.

We have, as ,

| (74) |

where and are given in (70) and the covariance matrix is composed of , and , with

| (75) |

where and is the trigamma function.

Proposition B.5.

We have, as ,

| (76) |

where and .

Now, we study the term and rewrite (76).

Proposition B.6.

By combining Proposition B.4 and Proposition B.6, we see that

| (80) |

where the asymptotic covariance matrix is given by:

| (81) |

Given (70) and (72), we deduce from (80) and (B.3) that, as ,

| (82) |

Assuming that we have proofs for Propositions B.4, B.5 and B.6 (see Section B.4 below), this ends the proof of Theorem 3.3.

B.4 Proofs of Propositions B.4, B.5 and B.6 to complete the proof of Theorem 3.3

Proof of Proposition B.4.

The asymptotic normality in (74) is a direct consequence of the central limit theorem. Let and . In order to conclude the proof, we show below how to compute the covariances between , , and . Before that, we gather some facts. For any given , the density function of is

| (83) |

Recall the definitions of the gamma, digamma and trigamma functions (for ):

| (84) |

and some well-known properties they satisfy (see, e.g., (Abramowitz and Stegun, 1964, Chapter 6)):

| (85) | ||||

| (86) | ||||

| (87) | ||||

| (88) | ||||

| (89) |

Using these properties, we can easily verify that, for and ,

| (90) | ||||

| (91) | ||||

| (92) |

We obtain, for ,

| (93) | ||||

| (94) | ||||

| (95) |

By symmetry of the density with respect to 0 and anti-symmetry of the integrands, we have

| (96) |

If we define , we have . Here is how we compute the other covariances:

| (97) | ||||

| (98) | ||||

| (99) | ||||

| (100) | ||||

| (101) | ||||

| (102) |

This ends the proof. ∎

Proof of Proposition B.5.

We work under throughout this proof. Using the fundamental theorem of calculus to expand around , we have

| (103) |

where for .

From (71) and (70), we know that for all ,

| (104) |

where and

By the triangle inequality and Lemma B.1, we have, for all ,

| (105) | ||||

Since we already know from (78) (this will be proved below independently of Proposition B.5) that

| (106) |

we deduce from (103), (104), (105) and (106) that, for all ,

| (107) |

which is the statement we wanted to prove, see (76).

When , we have to be a bit more careful. Indeed, Lemma B.1 cannot be applied to in this case because the log term implies that, for any , for all , and thus (C.2) cannot be satisfied. Instead, we use Lemma B.7 below (again, this will be proved independently of Proposition B.5), which is a consequence of a uniform law of large numbers developed in Lafaye de Micheaux and Ouimet (2018) for summands that blow up. By using successively Jensen’s inequality, Fubini’s theorem, the triangle inequality and Lemma B.7, we have

| (108) | ||||

By Markov’s inequality, this yields, for ,

| (109) |

Putting (106) and (109) together into (103) proves the statement of the proposition when , assuming that Lemma B.7 is true. ∎

In order to conclude the proof of Proposition B.5, it remains to prove the following lemma.

Lemma B.7.

Let be a sequence of i.i.d. random variables such that , where , and . In particular, the density function of is given by

| (110) |

Define by

| (111) |

Let and be the sequences of maximum likelihood estimators found in Proposition 2.3 for :

| (112) |

The median is defined in Remark 2.4. For , let and . Then,

| (113) |

Proof of Lemma B.7.

Without loss of generality, assume that . Since and a.s., we have a.s. for any , which implies that the factors and in the function of can be ignored. Also, is symmetric, so . Combining these facts together, the supremum in (113) is bounded from above by

| (114) | ||||

where . By Lemma 3.1 in Lafaye de Micheaux and Ouimet (2018), we have .

It remains to prove that in (114). By the Cauchy-Schwarz inequality,

| (115) | ||||

Below, we show that is bounded and tends to zero as . We start with . Almost surely in , the function

| (116) |

is monotone and equal to zero at (by definition of , recall (64)). Therefore, almost surely in , the supremum of the square in is always attained at . We deduce that

| (117) |

by the strong law of large numbers and the bounded convergence theorem.

Now we show that is bounded. By successively using the inequality , the fact that always maximizes at one of the two end points on any closed sub-interval of , and the inequality for , we have

| (118) |

It remains to show that . Since is a mean of integrable terms (see (112)), we expect, at least heuristically (because of large deviations), that, as , its density function concentrates more and more around and decays exponentially faster and faster in the right tail. The specific form of the density function of is given in Equation (32) of Karst and Polowy (1963) and confirms the intuition. For large enough (depending on ), there exists small enough that, for all ,

| (119) | ||||

where and . This ends the proof. ∎

Proof of Proposition B.6.

We work under throughout this proof. Let , and . By the weak law of large numbers, the chain rule, integration by parts and , we have

| (120) | ||||

This proves (77). Now, we show the asymptotics of . By applying Theorem 5.23 in van der Vaart (1998) (we verify the technical conditions of the theorem below) with

| (121) |

(, recall Proposition 2.3 and the fact that by (69) yields

| (122) | ||||

This proves (78). Finally, since is by Proposition B.4, Equation (79) follows directly from Proposition B.5, (77) and (78).

For the convenience of the reader, we verify below the conditions of Theorem 5.23 in van der Vaart (1998), which allowed us to write the first equality in (122):

-

1.

For all , the function is measurable (this is obvious).

-

2.

For all (and thus for almost-all under the measure on induced by the distribution of ), the function is differentiable at , and the derivative at that point is

(123) -

3.

The function is measurable, and satisfies (this is easy to verify because the supremum is attained) and also

(124) This last equation is just a consequence of the mean value theorem and the fact that, for all , the function is uniformly continuous on the compact set .

-

4.

The map admits the following second order Taylor expansion at :

(125) where the matrix is finite, non-singular, symmetric (and even diagonal) by the proof of Proposition B.4. Indeed, whenever , the expansion easily holds true because integration by parts shows that and is uniformly continuous on . The only nontrivial case to verify is . In that case, we have , , and therefore

where the second integral on the third line was computed using Wolfram Mathematica.

-

5.

is trivially satisfied.

-

6.

since a.s. by Lemma B.2.

This ends the proof. ∎

B.5 Proof of Proposition 3.6

By applying a uniform law of large numbers, we can show the following preliminary result.

Lemma B.8.

Under and for , we have, as ,

| (126) |

so that

| (127) |

Proof of Lemma B.8.

For , and , let , ,

| (128) |

By Definition 2.6, note that

| (129) |

By the triangle inequality and Lemma B.1, we have, for all ,

| (130) | ||||

where, under ,

| (131) | ||||

by (94) with , and by the symmetry of the density with respect to and anti-symmetry of the function , respectively. This proves (126). The limit in (127) follows by applying the limits from (126) together in Definition 2.8 for . To obtain the positivity on the right-hand side of (127), Lemma 2 in Minc and Sathre (1964/65) shows that for all , so that for all ,

| (132) | ||||

This ends the proof of Lemma B.8. ∎

We are now ready to prove Proposition 3.6. Assume throughout, and denote

| (133) | ||||||

Using Definition 3.1 and Theorem 3.3, we can write

| (134) | ||||

where and as . Then, for any on the event

| (135) |

we have, as ,

By a second order Taylor expansion, we know that for all ,

| (136) |

where and . Hence, for and for any ,

| (137) |

for some constant that depends only on . Since as by Theorem 3.3, we conclude that

| (138) |

The last part of Proposition 3.6 follows directly using Slutsky’s theorem and Theorem 3.3.

We give here another proof of the asymptotic distribution of in the statement of Proposition 3.6. It suffices to prove that, as ,

| (139) |

Consider the vector-valued function

| (140) |

The positivity of the right-hand side in (127) implies that is differentiable in a small open set that contains the point . At that point, we have and

| (141) |

Now, by Equation (82) and the delta method, we get

| (142) |

which is exactly the statement (139).

B.6 Proof of Proposition 3.8

Assume throughout. We have

| (143) |

since for all values of in Table 3.1. Furthermore, we have

| (144) |

Since and , and since and for all values of in Table 3.1, we have

| (145) |

Also, note that (see Proposition 3.6) and thus by Slutsky’s theorem. Therefore, we have

| (146) |

Finally, the last convergence in distribution results follow directly from Proposition 3.6 and Slutsky’s theorem.

B.7 Proof of Theorem 3.10

The following proposition will be a crucial tool to prove the weak convergence of our modified score statistic under local alternatives. It is a consequence of the concept of contiguity, see, e.g., Section 6.2 in van der Vaart (1998).

Proposition B.9.

For any statistics taking values in ,

| (147) |

as .

As an immediate consequence, we obtain the same decomposition under that we found for the modified score statistic under in Proposition B.6.

Corollary B.10.

Let . Then, as ,

| (148) |

We now use Le Cam’s third lemma to prove the analogue of Proposition B.4 under . Our aim is to obtain the asymptotic distribution of the right-hand side of (148).

Proposition B.11.

By combining Corollary B.10 and Proposition B.11, we see that

| (150) |

where the expressions for , and are found in (75), and the covariance matrix was previously calculated in (B.3). Given (70) and (72), we deduce from (150) that, as ,

| (151) |

where

| (152) | ||||

Assuming that we have proofs for Propositions B.9 and B.11 (see Section B.8 below), this ends the proof of Theorem 3.10.

B.8 Proofs of Propositions B.9 and B.11 to complete the proof of Theorem 3.10

In order to establish our results under the local alternatives , we use Le Cam’s first and third lemma (see Lemma 6.4 and Example 6.7 of van der Vaart (1998)). The proof structure is inspired by the one presented in Section 4 of Falk et al. (2008).

Lemma B.12 (Le Cam’s first lemma).

Let and be sequences of probability measures on the measurable spaces . Then, the following statements are equivalent:

-

1.

, i.e., is contiguous with respect to .

-

2.

If along a subsequence, then .

-

3.

If along a subsequence, then .

-

4.

For any statistics : If , then .

Lemma B.13 (Le Cam’s third lemma).

Let and be sequences of probability measures on the measurable spaces , and let be a sequence of random vectors. Suppose that and

| (153) |

where is positive definite, and , then

| (154) |

Proof of Proposition B.9.

As suggested by a referee, this result can be proved using Lemma 7.6 of van der Vaart (1998) to establish the differentiability in quadratic mean of our density function under . Using Theorem 2 of van der Vaart (1998), this would imply a second order Taylor expansion akin to (158) along with the convergence of the first and second order terms as in (159) and (160). This would then yield (161) and the same argument using Le Cam’s first lemma (see below (161)) would finally give us the contiguity . This proof is shorter but has the downside of involving the concept of differentiability in quadratic mean, which may slightly obscure the relation between the statement of Proposition B.9 and the aforementioned contiguity for some readers.

Here is another straightforward (albeit lengthier) approach to the proof. We want to use Le Cam’s first lemma. Assume that our vector of observations is the identity function

| (155) |

where denotes the completion of the Borel -algebra , and where denotes the Lebesgue measure. On , define the probability measures

| (156) | ||||

where and . By construction, the law of under corresponds to the null hypothesis and the law under corresponds the alternative hypothesis . Since is positive on , the measures , and are equivalent on . From (156), we deduce that

| (157) |

where .

Using a second-order Taylor expansion around , we have, under ,

| (158) | ||||

where . From the convergence of the first two components in (74), we know that, as ,

| (159) |

For the second term on the right-hand side of (158), we want to apply a standard uniform law of large numbers (Lemma B.1). From the expression of in (1), we see that for each , the function satisfies:

- (C.1)

-

For all , is continuous on the compact ;

- (C.2)

-

There exists a finite polynomial such that for all (which implies that is integrable under ).

Take large enough that for all . By Jensen’s inequality and Lemma B.1 (under ), we deduce that

| (160) | ||||

By definition of the matrix in (74), note that (this can be seen by integrating by parts). Hence, (160) shows that the second term on the right-hand side of (158) is equal to . We deduce that

| (161) |

Take any random variable such that . The continuous mapping theorem and (161) imply that

| (162) |

By the definition of , we have . This shows in Lemma B.12 with and , which implies by . Define and note that by definition of . This shows in Lemma B.12 where the roles of and have been interchanged, which implies by . We conclude that the sequences and are mutually contiguous, which we denote by . The conclusion follows from . ∎

Proof of Proposition B.11.

From the expressions that we found for the two terms on the right-hand side of (158) in the proof of Proposition B.9, we have

| (163) |

where . By the central limit theorem (see the definition of in Proposition B.4), we obtain that, under ,

| (164) |

Then, by Le Cam’s third lemma,

| (165) |

This ends the proof. ∎

B.9 Proof of Corollary 3.11

Lemma B.14.

For , we have, as ,

| (166) |

so that

| (167) |

Then, we can apply the same second order Taylor expansion idea we used in the proof of Proposition B.5 (the proof is virtually identical so we omit the details) to prove that

| (168) |

Using the proof of Proposition 3.8 in Section B.6, in conjunction again with Proposition B.9, we also have

| (169) |

The last part of Corollary 3.11 follows directly using Slutsky’s theorem and Theorem 3.10.

References

References

- Abramowitz and Stegun (1964) Abramowitz M, Stegun IA (1964). Handbook of mathematical functions with formulas, graphs, and mathematical tables, volume 55 of National Bureau of Standards Applied Mathematics Series. For sale by the Superintendent of Documents, U.S. Government Printing Office, Washington, D.C.

- Falk et al. (2008) Falk M, Guillou A, Toulemonde G (2008). “A LAN based Neyman smooth test for Pareto distributions.” J. Statist. Plann. Inference, 138(10), 2867–2886.

- Ferguson (1996) Ferguson TS (1996). A course in large sample theory. Texts in Statistical Science Series. Chapman & Hall, London.

- Karst and Polowy (1963) Karst OJ, Polowy H (1963). “Sampling properties of the median of a Laplace distribution.” Amer. Math. Monthly, 70, 628–636.

- Lafaye de Micheaux and Ouimet (2018) Lafaye de Micheaux P, Ouimet F (2018). “A uniform law of large numbers for functions of i.i.d. random variables that are translated by a consistent estimator.” Statist. Probab. Lett., 142, 109–117.