Improving On-policy Learning with

Statistical Reward Accumulation

Abstract

Deep reinforcement learning has obtained significant breakthroughs in recent years. Most methods in deep-RL achieve good results via the maximization of the reward signal provided by the environment, typically in the form of discounted cumulative returns. Such reward signals represent the immediate feedback of a particular action performed by an agent. However, tasks with sparse reward signals are still challenging to on-policy methods. In this paper, we introduce an effective characterization of past reward statistics (which can be seen as long-term feedback signals) to supplement this immediate reward feedback. In particular, value functions are learned with multi-critics supervision, enabling complex value functions to be more easily approximated in on-policy learning, even when the reward signals are sparse. We also introduce a novel exploration mechanism called “hot-wiring” that can give a boost to seemingly trapped agents. We demonstrate the effectiveness of our advantage actor multi-critic (A2MC) method across the discrete domains in Atari games as well as continuous domains in the MuJoCo environments. A video demo is provided at https://youtu.be/zBmpf3Yz8tc.

1 Introduction

Advances in deep learning have mobilized the research community to adopt deep reinforcement learning (RL) agents for challenging control problems, typically in complex environments with raw sensory state-spaces. Breakthroughs by [10] show RL-agents can reach above-human performance in Atari 2600 games, and AlphaGo Zero [15] becomes the world champions on the game of Go. Still, training RL agents is non-trivial. Off-policy methods typically require days of training to obtain competitive performance, while on-policy methods could be trapped in local minima. Recent techniques featuring on-policy learning [9, 12, 21] have shown promising results in stabilizing the learning processes, enabling an agent to solve a variety of tasks in much less time. In particular, the state-of-the-art on-policy ACKTR agent by [21] shows improved sample efficiency with the help of Kronecker-factored (K-Fac) approximate curvature for natural gradient updates, resulting in stable and effective model updates towards a more promising direction.

However, tasks with sparse rewards remain challenging to on-policy methods. An agent could take massive amount of exploration before reaching non-zero rewards; and as the agent learns on-policy, the sparseness of reward feedback (receiving all-zero rewards from most actions performed by the agent) could be malicious and render an agent to falsely predict all states in an environment towards a value of zero. As there does not exist a universal criterion for measuring “task sparseness”, we show an ad-hoc metric in Figure 1 in an attempt to provide intuition. For example, we observe that the ACKTR agent is unable to receive sufficient non-zero immediate rewards that can provide instructive agent updates in Atari games “Freeway” and “Enduro”, resulting in failures when solving these two games. Moreover, if ACKTR gets drawn to and trapped in unfavorable states (as in games like Boxing and WizardOfWor), it could again take long hours of exploration before the agent can get out of the local minima. Such evidence shows that on-policy agent could indeed suffer from the insufficiencies of guidance provided by the exclusive immediate reward signals from the environment.

In this paper, we introduce an effective auxiliary reward signal in tasks with sparse rewards to remedy the deficiencies of learning purely from standard immediate reward feedbacks. As on-policy agents may take many explorations before reaching non-zero immediate rewards, we argue that we can leverage past reward statistics to provide more instructive feedbacks to agents in the same environment. To this end, we propose to characterize the past reward statistics in order to gauge the “long-term” performance of an agent (detailed in Section 4). After performing an action, an agent will receive a long-term reward signal describing its past performance upon this step, as well as the conventional immediate reward from the environment. To effectively characterize the long-term performance of the agent, we take into considerations both the crude amount of rewards and the volatility of rewards received in the past, where highly volatile distributions of long-term rewards are explicitly penalized. This enables complex value functions to be more easily approximated in multi-critics supervision. We find in practice that by explicitly penalizing highly volatile long-term rewards while maximizing the expectation of short-term rewards, the learning process and the overall performance are improved regarding both sample efficiency and final rewards. We further propose a “hot-wiring” exploration mechanism that can boost seemingly trapped agent in the earlier stage of learning. By leveraging the characterization of long/short-term reward statistics, our proposed advantage actor multi-critic model (A2MC) shows significantly improved performance on the Atari 2600 games and the MuJoCo tasks as compared to the state-of-the-art on-policy methods.

2 Related Work

The family of off-policy methods [19] may be less prone to failure in tasks with sparse rewards at the cost of large amount of explorations before performing agent updates. To tackle the challenge in tasks with rarely observed rewards, pseudo-rewards maximization is adopted in earlier works [6, 14]. Auxiliary vision tasks (e.g., learning pixel changes or network features) are adopted in the off-policy UNREAL agent [4] in order to facilitate learning better feature representations, particularly for sparse reward environments. Another direction of effort aims to design a better reward function for improving sample efficiency via experience replay. [1] enhances off-policy learning by re-producing informative reward in hindsight for sequences of actions that do not lead to success previously. The HRA approach [17] exploits domain knowledge to define a set of environment-specific rewards based on reward categories. In contrast to heuristically defining vision-related auxiliary tasks, our proposed on-policy A2MC agent learns from the characterization of intrinsic past reward statistics obtainable from any environment; and different from the hybrid architecture tailored specific to Ms. Pacman, our A2MC agent can generalize well to a variety of tasks without the need to engineer a decomposition of problem-specific environment rewards.

The multi-agent approaches [7, 8, 5] present another promising direction for learning. They propose to train multiple agents in parallel when solving a task, and to combine multiple action-value functions with a centralized action-value function. The multi-critics supervision in our proposed A2MC model can be seen as a form of joint-task or multi-task learning [16] for both long-term and short-term rewards.

Our empirical results based on learning the characterization of long/short-term reward statistics also echo the effectiveness of a recently proposed off-policy reinforcement learning framework [2] that features a distributional variant of Q-learning, wherein the value functions are learned to match the distribution of standard immediate returns. Also, [18] shows that applying experience replay to on-policy methods can further enhance learning stability. [11] proposes a variant of advantage function that provides both low-variance and low-bias gradient estimates. These works are orthogonal to our approach can potentially be combined with the proposed characterization of past reward statistics to further enhance learning performance.

3 Preliminary

Consider the standard reinforcement learning setting where an agent interacts with an environment over a number of discrete time step. At each time step , the agent receives an environment state , then executes an action based on policy . The environment produces reward and next state , according to which the agent gets feedback of its immediate action and will decide its next action . The process <>, typically considered as a Markov Decision Process, continues until a terminal state upon which the environment resets itself and produces a new episode. Under conventional settings, the return is calculated as the discounted summation of rewards accumulated from time step onwards . The goal of the agent is to maximize the expected return from each state while following policy . Each policy has a corresponding action-value function defined as . Similarly, each state under policy has a value function defined as: . In value-based approaches (e.g., Q-learning [10]), function approximator can be used to approximate the optimal action value function . This is conventionally learned by iteratively minimizing the below loss function:

| (1) |

where and is the next state following state .

In policy-based approaches (e.g., policy gradient methods), the optimal policy is approximated using the approximator . The policy approximator is then learned by gradient ascent on . The REINFORCE method [20] further incorporates a baseline to reduce the variance of the gradient estimator:

In actor-critic based approaches, the variance reduction further evolves into the advantage function in [9], where the action value is approximated by and is replaced by , deriving the advantage actor-critic architecture where actor-head and the critic-head share low-level features. The gradient update rule w.r.t. the action-head is . The gradient update w.r.t. the critic-head is: , where .

4 Characterization of Past Reward Statistics

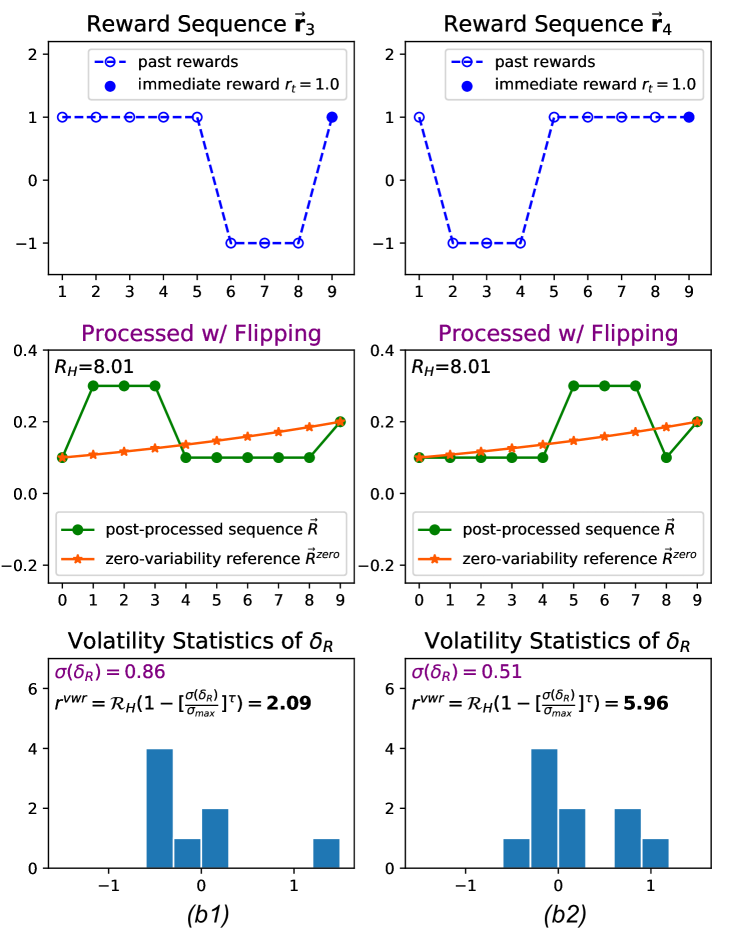

The conventional reward received from the environment at time step after an action is performed represents the immediate reward regarding this particular action. This “immediacy” could be interpreted as a short-term horizon of how the agent is doing, i.e., evaluating the agent via judging its actions by immediate rewards. We argue that the deficiencies of learning solely from immediate rewards mainly come from this limitation that the agent is learning from one single type of exclusive short-term feedback. As the goal of providing reward feedback to an agent is to inform the agent of its performance, we seek to find an auxiliary performance metric that can measure whether the agent is performing consistently well. Inspired by the formulation of Sharpe Ratio [13] in evaluating the long-term performance of fund performance and trading strategies, an effective characterization of historical reward statistics should take into account at least two factors, namely 1) how high the immediate reward is and 2) how varied past rewards were.

4.1 Variability-Weighted Reward

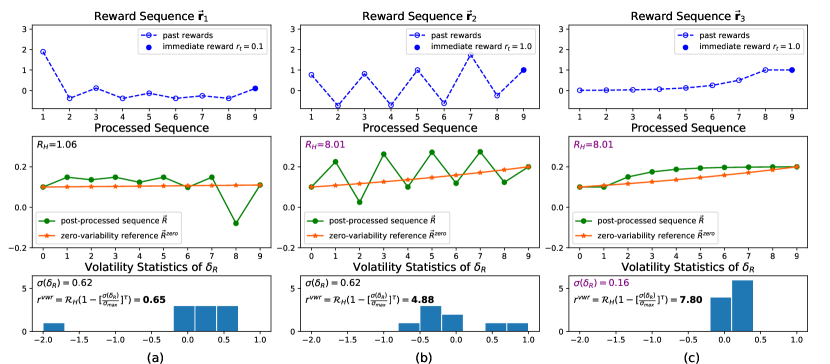

To this end, we follow insight behind [3] and define a variability-weighted characterization of rewards in the past. This is illustrated in Figure 2. In particular, we consider a historical sequence of rewards upon timestep (looking backward timesteps): . In order to evaluate how high and varied the reward sequence is, a few steps of pre-processing is applied, denoted as . In particular, we first derive the reward change at each timestep by extracting the first-order difference with :

| (2) |

Then we re-order the sequence by flipping 111By flipping, we further encourage recent stable rewards and penalize the volatility of recent past rewards. A concrete example is given in the Appendix A. with :

| (3) |

Next we append to the head of sequence and take the normalized cumulative sum to obtain post-processed reward sequence as:

| (4) |

Under such processing, is a reward sequence with , and . Therefore, the difference between and represents the immediate reward and the whole sequence reflects the volatility of past rewards. In Figure 2, three examples of processed sequence are presented in the second row with the corresponding raw rewards shown in the first row. We account for how high the immediate reward is by defining the average log total return as:

| (5) |

To account for how varied past rewards were, we first define a smooth zero-variability reference as: with , representing a smooth monotonic reference sequence from to . Then we define the reward differential as the differential reward versus its zero-variability reference as , whose statistics are sketched in the third row of Figure 2. With maximally allowed volatility as , the variability weights can be defined as:

| (6) |

where is the standard deviation and controls the rate to penalize highly volatile reward distribution. Finally we can derive the variability-weighted past reward indicator for the characterization of past reward statistics:

| (7) |

Example computed values of for the characterization of different reward statistics are shown in Figure 2.

4.2 Multi-Critic Architecture

A higher value of indicates better agent performance as the result of the historical sequence of actions. The same set of optimization procedures for conventional value function (i.e., via maximization of immediate reward signal ) update can be applied accordingly. The actual returns computed from both the “long-term” and “short-term” rewards are discounted by the same factor . In particular, for -step look-ahead approaches, we have:

| (8) |

| (9) |

Similar to the standard state value function , we further define as the value function w.r.t the variability-weighted reward . These value functions form multiple critics judging a given state . The gradients w.r.t. the critics then become:

| (10) |

We show the effectiveness of the proposed characterization of past reward statistics in advantage actor-critic frameworks. The two different value functions can share the same low-level feature representation, enabling a single agent to learn multiple critics as parameterized by .

5 Hot-Wire -Exploration

Being handed a game-stick, a human most likely would try out all the available buttons on it to see which particular button entails whatever actions on the game screen, hence receiving useful feedbacks. Inspired by this, we propose to hot-wire the agent to perform an identical sequence of randomly chosen actions in the N-step look-ahead during the initial stage (randomly pressing down a game-stick button for a while):

| (11) |

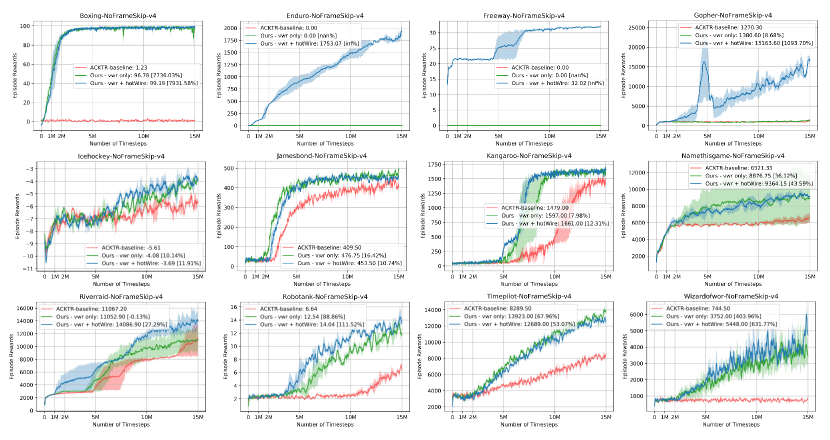

We show that by enabling the “hot-wiring” mechanism222hot-wire is triggered only when the agent is unable to receive meaningful rewards in an initial learning stage. The legend “vwr + hotWire” in Fig. 3 indicates that the mechanism is “enabled” but not “enforced”., a seemingly trapped agent can be boosted to learn to quickly solve problems where rewards can only be triggered by particular action sequences, as shown in games like “Robotank” and “WizardOfWor” in Figure 3.

The full algorithm, advantage actor multi-critic learning (A2MC), is shown in Algorithm 1 in the Appendix E.

6 Experiments

We use the same network architecture and natural gradient optimization method as in the ACKTR model [21]. We set , and in the computation of variability-weighted reward. For hot-wiring exploration, we choose and initial stage to be first of the total training period for all experiments. Other hyperparameters such as learning rate and gradient clipping remain the same as in the ACKTR model [21]. We first present results of evaluating the proposed A2MC model in two standard benchmarks, the discrete Atari experiments and the continuous MuJoCo domain. Then we show further ablation studies on the robustness of the hyper-parameters involved as well as evaluating the extensibility of the proposed long/short-term reward characterizations to other on-policy methods.

6.1 ATARI 2600 Games

We follow standard evaluation protocol to evaluate A2MC in a variety of Atari game environments (starting with 30 no-op actions). We train our models for 15 million timesteps for each game environment and score each game based on the average episode rewards obtained among the last 100 episodes as in [21]. The learning results on 12 Atari games are shown in Figure 3 where we also included an ablation experiment of A2MC without hot-wiring. We observe that on average A2MC improves upon ACKTR in terms of final performance under the same training budget. Our A2MC is able to consistently improve agent performance based on the proposed characterization of reward statistics, hence the agent is able to get out of local minima in less time (higher sample efficiency) compared to ACKTR. The complete learning results on all games are attached in the Appendix B.

We further expand the training budget and continue learning the games until 50 million timesteps as in [21]. As shown in Table 1, our A2MC model can solve games like “Boxing”, “Freeway” and “Enduro” that are challenging for the baseline ACKTR model. For a full picture of model performance in Atari games, A2MC has a human-level performance rate of (38 out of 51 games) in the Atari benchmarks, compared to reached by ACKTR. Individual game scores for all the Atari games are reported in the Appendix B.

| ACKTR | A2MC | ||||||

|---|---|---|---|---|---|---|---|

| Domain | Human Level | Rewards | Episode | Rewards | Episode | ||

| Asteroids | 47388.7 | 34171.0 | N/A | 830232.5 | 11314 | ||

| Beamrider | 5775.0 | 13581.4 | 3279 | 13564.3 | 3012 | ||

| Boxing | 12.1 | 1.5 | N/A | 99.1 | 158 | ||

| Breakout | 31.8 | 735.7 | 4097 | 411.4 | 3664 | ||

| Double Dunk | -16.4 | -0.5 | 742 | 21.3 | 544 | ||

| Enduro | 860.5 | 0.0 | N/A | 3492.2 | 730 | ||

| Freeway | 29.6 | 0.0 | N/A | 32.7 | 1058 | ||

| Pong | 9.3 | 20.9 | 904 | 19.4 | 804 | ||

| Q-bert | 13455.0 | 21500.3 | 6422 | 25229.0 | 7259 | ||

| Robotank | 11.9 | 16.5 | - | 25.7 | 4158 | ||

| Seaquest | 20182.0 | 1776.0 | N/A | 1798.6 | N/A | ||

| Space Invaders | 1652.0 | 19723.0 | 14696 | 11774.0 | 11064 | ||

| Wizard of Wor | 4756.5 | 702 | N/A | 7471.0 | 8119 | ||

6.2 Continuous Control

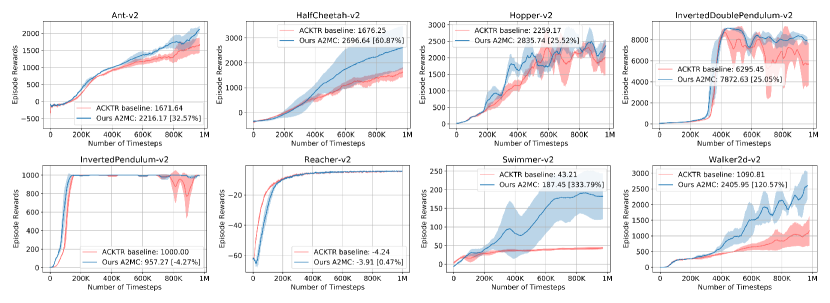

For the evaluations on continuous control tasks simulated in MuJoCo environment, we first follow [21] and tune a different set of hyper-parameters from Atari experiments. Specifically, all MuJoCo experiments are trained with a larger batch size of 2500. The results of eight MuJoCo environments trained for 1 million timesteps are shown in Figure 4. We observe that A2MC also performs well in all MuJoCo continuous control tasks. In particular, A2MC has obtained significant improvement as compared to ACKTR on the tasks of HalfCheetah, Swimmer and Walker2d (see Table 2).

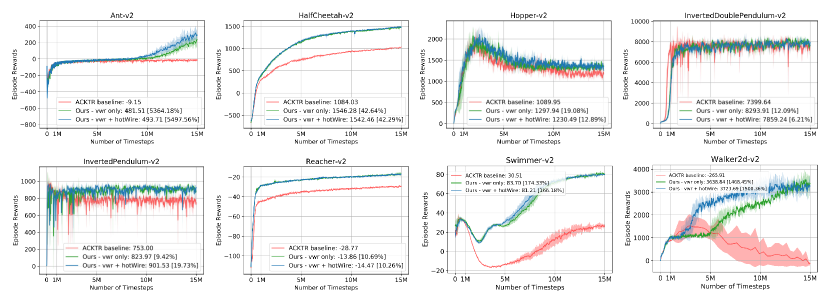

To test the robustness of A2MC, we perform another set of evaluations on MuJoCo tasks by keeping an identical set of hyper-parameters used in the Atari experiments. Figure 5 shows this ablation result. We observe that even under sub-optimal hyper-parameters, our A2MC model can still learn to solve the MuJoCo control tasks in the long run. Moreover, it is less prone to overfitting when compared to ACKTR under such “stress testing”. Additional hyper-parameter studies are shown in Appendix C.

We also evaluate a multi-critics variant of the proximal policy optimization (PPO) model on the MuJoCo tasks with our proposed long/short-term rewards. In particular, we observe that our proposed variability-weighted reward generalizes well with the vanilla PPO, and our multi-critics PPO variant (MC-PPO) shows more favorable performance, as shown in Table 2. Specifically, MC-PPO shows the best performance on Hopper and Walker-2d among all models under the 1-million timesteps training budget. Both of our multi-critics variants (A2MC and MC-PPO) have won 6 out of the 8 MuJoCo tasks with relative performance margins (percentages in parentheses) larger than (see Table 2).

| GAMES | ACKTR | Our A2MC | PPO | Our MC-PPO | |||||||||

| Ant | 1671.6 | 2216.1 | (32.5%) | 411.4 | ( 107.7) | ||||||||

| HalfCheetah | 1676.2 | 2696.6 | (60.8%) | 1433.7 | ( 83.9) | ||||||||

| Hopper | 2259.1 | 2835.7 | (25.5%) | 2055.8 | ( 274.6) | ||||||||

| InvertedDoublePendulum | 6295.4 | 7872.6 | (25.0%) | 4454.1 | ( 1098.1) | ||||||||

| InvertedPendulum | 1000.0 | 957.2 | (-4.2%) | 839.7 | ( 127.1) | ||||||||

| Reacher | -4.2 | -3.9 | (0.4%) | -5.47 | ( 0.3) | ||||||||

| Swimmer | 43.2 | 187.4 | (333.7%) | 79.1 | ( 31.2) | ||||||||

| Walker2d | 1090.8 | 2405.9 | (120.5%) | 2300.8 | ( 397.6) | ||||||||

| Win | Fair | Lose | N/A | 6 | 2 | 0 | N/A | 6 | 2 | 0 | |||||||||

7 Conclusion

In this work, we introduce an effective auxiliary reward signal to remedy the deficiencies of learning solely from the standard environment rewards. Our proposed characterization of past reward statistics results in improved learning and higher sample efficiencies for on-policy methods, especially in challenging tasks with sparse rewards. Experiments on both discrete tasks in Atari environment and MuJoCo continuous control tasks validate the effectiveness of utilizing the proposed long/short-term reward statistics for on-policy methods using multi-critic architectures. This suggests that expanding the form of reward feedbacks in reinforcement learning is a promising research direction.

References

- [1] M. Andrychowicz, F. Wolski, A. Ray, J. Schneider, R. Fong, P. Welinder, B. McGrew, J. Tobin, O. P. Abbeel, and W. Zaremba. Hindsight experience replay. In Advances in Neural Information Processing Systems, pages 5048–5058, 2017.

- [2] M. G. Bellemare, W. Dabney, and R. Munos. A distributional perspective on reinforcement learning. arXiv preprint arXiv:1707.06887, 2017.

- [3] K. Dowd. Adjusting for risk:: An improved sharpe ratio. International review of economics & finance, 9(3):209–222, 2000.

- [4] M. Jaderberg, V. Mnih, W. M. Czarnecki, T. Schaul, J. Z. Leibo, D. Silver, and K. Kavukcuoglu. Reinforcement learning with unsupervised auxiliary tasks. arXiv preprint arXiv:1611.05397, 2016.

- [5] J. Jin, C. Song, H. Li, K. Gai, J. Wang, and W. Zhang. Real-time bidding with multi-agent reinforcement learning in display advertising. arXiv preprint arXiv:1802.09756, 2018.

- [6] G. Konidaris and A. G. Barto. Skill discovery in continuous reinforcement learning domains using skill chaining. In Advances in neural information processing systems, pages 1015–1023, 2009.

- [7] M. Lanctot, V. Zambaldi, A. Gruslys, A. Lazaridou, J. Perolat, D. Silver, T. Graepel, et al. A unified game-theoretic approach to multiagent reinforcement learning. In Advances in Neural Information Processing Systems, pages 4193–4206, 2017.

- [8] R. Lowe, Y. Wu, A. Tamar, J. Harb, O. P. Abbeel, and I. Mordatch. Multi-agent actor-critic for mixed cooperative-competitive environments. In Advances in Neural Information Processing Systems, pages 6382–6393, 2017.

- [9] V. Mnih, A. P. Badia, M. Mirza, A. Graves, T. Lillicrap, T. Harley, D. Silver, and K. Kavukcuoglu. Asynchronous methods for deep reinforcement learning. In International Conference on Machine Learning, pages 1928–1937, 2016.

- [10] V. Mnih, K. Kavukcuoglu, D. Silver, A. A. Rusu, J. Veness, M. G. Bellemare, A. Graves, M. Riedmiller, A. K. Fidjeland, G. Ostrovski, et al. Human-level control through deep reinforcement learning. Nature, 518(7540):529, 2015.

- [11] J. Schulman, P. Moritz, S. Levine, M. Jordan, and P. Abbeel. High-dimensional continuous control using generalized advantage estimation. ICLR, 2016.

- [12] J. Schulman, F. Wolski, P. Dhariwal, A. Radford, and O. Klimov. Proximal policy optimization algorithms. arXiv preprint arXiv:1707.06347, 2017.

- [13] W. F. Sharpe. The sharpe ratio. Journal of portfolio management, 21(1):49–58, 1994.

- [14] D. Silver and K. Ciosek. Compositional planning using optimal option models. arXiv preprint arXiv:1206.6473, 2012.

- [15] D. Silver, J. Schrittwieser, K. Simonyan, I. Antonoglou, A. Huang, A. Guez, T. Hubert, L. Baker, M. Lai, A. Bolton, et al. Mastering the game of go without human knowledge. Nature, 550(7676):354, 2017.

- [16] Y. Teh, V. Bapst, W. M. Czarnecki, J. Quan, J. Kirkpatrick, R. Hadsell, N. Heess, and R. Pascanu. Distral: Robust multitask reinforcement learning. In Advances in Neural Information Processing Systems, pages 4499–4509, 2017.

- [17] H. Van Seijen, M. Fatemi, J. Romoff, R. Laroche, T. Barnes, and J. Tsang. Hybrid reward architecture for reinforcement learning. In NIPS, pages 5392–5402, 2017.

- [18] Z. Wang, V. Bapst, N. Heess, V. Mnih, R. Munos, K. Kavukcuoglu, and N. de Freitas. Sample efficient actor-critic with experience replay. arXiv preprint arXiv:1611.01224, 2016.

- [19] Z. Wang, T. Schaul, M. Hessel, H. Van Hasselt, M. Lanctot, and N. De Freitas. Dueling network architectures for deep reinforcement learning. arXiv preprint arXiv:1511.06581, 2015.

- [20] R. J. Williams. Simple statistical gradient-following algorithms for connectionist reinforcement learning. In Reinforcement Learning, pages 5–32. Springer, 1992.

- [21] Y. Wu, E. Mansimov, R. B. Grosse, S. Liao, and J. Ba. Scalable trust-region method for deep reinforcement learning using kronecker-factored approximation. In Advances in neural information processing systems, pages 5285–5294, 2017.

APPENDIX

Appendix A Effects of Flipping

While introducing the variability-weighted reward, a flipping operation is conducted in the pre-processing of the reward sequence as formulated in Eq. (3). In Figure 7 and 7, we construct 4 reward sequences to show that the flipping operation can further penalize the oscillation in the recent past rewards while encourage recent stable rewards. (a1, a2, b1, b2) share the same value of immediate reward at and thus the of all reward sequences are the same.

Therefore, the variability-weighted reward only depends on the volatility statistics of , i.e., how varied past rewards were.

Without flipping. In Figure 7, sequence (a1) and (a2) are mirror symmetrical to the -axis, and the only difference between them is that the recent past rewards () of (a2) are more stable than (a1). Intuitively, we want to encourage stable past rewards like (a2) while penalizing oscillation in (a1). As presented in the third row of Figure 7, the difference of (a1) and (a2) is less than 1 without flipping in the pre-processing.

With flipping. In Figure 7, (b1, b2) exactly have the same reward sequence as (a1, a2), respectively. However, flipping is performed as a step of pre-processing, largely increasing the gap (from less than 1 to nearly 4) between the two constructed sequences. Comparing (b1, b2) with (a1, a2) , the post-processed sequences (shown in green) become centrosymmetric to those without flipping. Specifically, the recent reward drops at are reflected as high values at the beginning of as shown in (b1), while oscillations long ago are transformed into high values at the end of as presented in (b2). When compared to the zero-variability reference (shown in orange), which is designed as an exponential function, the flipping leads to a higher variability for the former sequence while a lower variability for the latter one, enlarging the gap between those two sequences.

Appendix B Complete results in Atari 2600 Games

We show the learning curves for 15 million timesteps on all Atari games in Figure 9 and in Table 3 we show the complete results of training til 50 million timesteps. report the mean episode reward as in [21]. Entries with indicates approximated value as retrieved from learning figures published by [21]. Results from other models are taken from [21] and [10]. We show that A2MC has reached a human-level performance rate of (38 out of 51 games) as compared to reached by ACKTR. The relative performance margin of A2MC as compared to ACKTR is also shown.

| GAME | Human | DQN | DDQN | Prior. Duel | ACKTR | Our A2MC | (Margin) | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Alien | 7127.7 | 1620 | 3747.7 | 3941 | 3197.1 | 2986.3 | -6.6% | ||||||||||||

| Amidar | 1719.5 | 978 | 1793.3 | 2296.8 | 1059.4 | 2040.1 | 92.6% | ||||||||||||

| Assault | 742.0 | 4280.4 | 5393.2 | 11477 | 10777.7 | 9892.4 | -8.2% | ||||||||||||

| Asterix | 8503.3 | 4359 | 17356.5 | 375080 | 31583.0 | 32671.0 | 3.4% | ||||||||||||

| Asteroids | 47388.7 | 1364.5 | 734.7 | 1192.7 | 34171.6 | 828931.6 | 2325.8% | ||||||||||||

| Atlantis | 29028.1 | 279987 | 106056 | 395762 | 3433182.0 | 2886274.0 | -15.9% | ||||||||||||

| Bankheist | 753.1 | 455 | 1030.6 | 1503.1 | 1289.7 | 1290.6 | 0.1% | ||||||||||||

| Battlezone | 37187.5 | 29900 | 31700 | 35520 | 8910.0 | 10570.0 | 18.6% | ||||||||||||

| Beamrider | 16926.5 | 8627.5 | 13772.8 | 30276.5 | 13581.4 | 13715.6 | 1.0% | ||||||||||||

| Berzerk | 2630.4 | 585.6 | 1225.4 | 3409 | 927.2 | 974.0 | 5.0% | ||||||||||||

| Bowling | 160.7 | 50.4 | 68.1 | 46.7 | 24.3 | 31.6 | 30.0% | ||||||||||||

| Boxing | 12.1 | 88 | 91.6 | 98.9 | 1.5 | 93.5 | 6344.8% | ||||||||||||

| Breakout | 30.5 | 385.5 | 418.5 | 366 | 735.7 | 420.6 | -42.8% | ||||||||||||

| Centipede | 12017.0 | 4657.7 | 5409.4 | 7687.5 | 7125.3 | 12096.5 | 69.8% | ||||||||||||

| Choppercommand | 9882.0 | N/A | N/A | N/A | 8000 | 12149.0 | 42.5% | ||||||||||||

| Crazyclimber | 35829.4 | 110763 | 117282 | 162224 | 150444.0 | 152439.0 | 1.3% | ||||||||||||

| Demonattack | 1971.0 | 12149.4 | 58044.2 | 72878.6 | 274176.7 | 361807.1 | 32.0% | ||||||||||||

| Doubledunk | -16.4 | -6.6 | -5.5 | -12.5 | -0.5 | 20.6 | 3907.5% | ||||||||||||

| Enduro | 860.5 | 729 | 1211.8 | 2306.4 | 0.0 | 3550.6 | % | ||||||||||||

| Fishingderby | -38.7 | -4.9 | 15.5 | 41.3 | 33.7 | 38.4 | 13.9% | ||||||||||||

| Freeway | 29.6 | 30.8 | 33.3 | 33 | 0.0 | 32.7 | % | ||||||||||||

| Frostbite | 4335.0 | N/A | N/A | N/A | 280 | 293.7 | 5.1% | ||||||||||||

| Gopher | 2412.5 | 8777.4 | 14840.8 | 104368.2 | 47730.8 | 86101.4 | 80.4% | ||||||||||||

| Gravitar | 2672.0 | N/A | N/A | N/A | 300 | 995.0 | -2.9% | ||||||||||||

| Icehockey | 0.9 | -1.9 | -2.7 | -0.4 | -4.2 | -2.1 | 16.3% | ||||||||||||

| Jamesbond | 302.8 | 768.5 | 1358 | 812 | 490.0 | 545.0 | 11.2% | ||||||||||||

| Kangaroo | 3035.0 | 7259 | 12992 | 1792 | 3150.0 | 11269.0 | 257.7% | ||||||||||||

| Krull | 2665.5 | 8422.3 | 7920.5 | 10374.4 | 9686.9 | 10245.4 | 5.8% | ||||||||||||

| Kungfumaster | 22736.3 | 26059 | 29710 | 48375 | 34954.0 | 39773.0 | 13.8% | ||||||||||||

| Mspacman | 15693.0 | N/A | N/A | N/A | 3500 | 5006.1 | 34.5% | ||||||||||||

| Namethisgame | 4076.0 | N/A | N/A | N/A | 12500 | 12569.9 | 0.6% | ||||||||||||

| Phoenix | 7242.6 | 8485.2 | 12252.5 | 70324.3 | 133433.7 | 221288.3 | 65.8% | ||||||||||||

| Pitfall | 6463.7 | -286.1 | -29.9 | 0 | -1.1 | -2.5 | -0.3% | ||||||||||||

| Pong | 14.6 | 20.9 | 21 | 20.9 | 20.9 | 19.7 | -5.9% | ||||||||||||

| Privateeye | 69571.0 | N/A | N/A | N/A | 560 | 507.0 | -9.5% | ||||||||||||

| Qbert | 13455.0 | 13117.3 | 15088.5 | 18760.3 | 23151.5 | 24075.8 | 4.0% | ||||||||||||

| Riverraid | 17118.0 | 7377.6 | 14884.5 | 20607.6 | 17762.8 | 18671.9 | 5.1% | ||||||||||||

| Roadrunner | 7845.0 | 39544 | 44127 | 62151 | 53446.0 | 50071.0 | -6.3% | ||||||||||||

| Robotank | 11.9 | 63.9 | 65.1 | 27.5 | 16.5 | 26.5 | 60.5% | ||||||||||||

| Seaquest | 42054.7 | 5860.6 | 16452.7 | 931.6 | 1776.0 | 1805.6 | 1.7% | ||||||||||||

| Solaris | 12326.7 | 3482.8 | 3067.8 | 133.4 | 2368.6 | 2277.2 | -3.9% | ||||||||||||

| Spaceinvaders | 1668.7 | 1692.3 | 2525.5 | 15311.5 | 19723.0 | 13544.2 | -31.3% | ||||||||||||

| Stargunner | 10250.0 | 54282 | 60142 | 125117 | 82920.0 | 89616.0 | 8.1% | ||||||||||||

| Tennis | -8.9 | N/A | N/A | N/A | -12 | -4.7 | 20.4% | ||||||||||||

| Timepilot | 5229.2 | 4870 | 8339 | 7553 | 22286.0 | 21992.0 | -1.3% | ||||||||||||

| Tutankham | 167.6 | 68.1 | 218.4 | 245.9 | 314.3 | 193.7 | -38.4% | ||||||||||||

| Upndown | 11693.2 | 9989.9 | 22972.2 | 33879.1 | 436665.8 | 563659.3 | 29.1% | ||||||||||||

| Videopinball | 17667.9 | 196760.4 | 309941.9 | 479197 | 100496.0 | 127452.4 | 26.8% | ||||||||||||

| Wizardofwor | 4756.5 | 2704 | 7492 | 12352 | 702.0 | 7864.0 | 1020.2% | ||||||||||||

| YarsRevenge | 54576.9 | 18098.9 | 11712.6 | 69618.1 | 125169.0 | 143141.5 | 14.4% | ||||||||||||

| Zaxxon | 9173.3 | 5363 | 10163 | 13886 | 17448.0 | 19365.0 | 11.0% | ||||||||||||

|

N/A |

|

|

|

|

|

Appendix C Hyper-parameter Studies

The proposed variability-weighted reward mechanism considers the volatility of rewards by keeping a -step history of agent’s performance. The hyper-parameter is empirically chosen to be the same as the look-ahead parameter in standard on-policy methods, so as to keep the same period () in “T-step history” and “N-step forward”. And is chosen as the average of the observed volatility based on statistics in the history rewards of the ACKTR models. As parameter choices could be vital, we perform an additional ablation study shown below. The result shows that the performance of A2MC is robust across different parameters of choice and is not too sensitive to changes on either of the hyper-params.

| Games | ACKTR | A2MC w/ | T=20 | T=10 | T=10 | T=40 | T=40 |

|---|---|---|---|---|---|---|---|

| =1 | =1 | =2 | =1 | =2 | |||

| Boxing | 1.23 | 99.19 | 94.76 | 98.51 | 99.18 | 98.07 | |

| Jamesbond | 409.50 | 453.50 | 438.50 | 470.00 | 442.25 | 457.75 | |

| Wizard of Wor | 744.50 | 5448.00 | 5601.00 | 5363.50 | 2528.50 | 3287.50 |

Appendix D Extension to Multi-Critic PPO (MC-PPO)

The learning results of the proposed MC-PPO model on the MuJoCo tasks are shown in Figure 8. MC-PPO shows the best performance on Hopper and Walker-2d among all models under the 1-million timesteps training budget. Both of our multi-critics variants (A2MC and MC-PPO) have won 6 out of the 8 MuJoCo tasks with relative performance margins (percentages in parentheses) larger than .

Appendix E Algorithm

The learning algorithm of A2MC is shown in Algorithm 1.