and

t1Lukas Steinberger was supported by the Austrian Science Fund (FWF): P 28233-N32 and I 5484-N, the latter project is part of the Research Unit 5381 of the German Research Foundation. Part of this research was conducted while Lukas Steinberger was funded by the German Research Foundation (DFG): RO 3766/401.

t2Hannes Leeb was supported by the Austrian Science Fund (FWF): P 28233-N32 and P 26354-N26.

Conditional predictive inference for stable algorithms

Abstract

We investigate generically applicable and intuitively appealing prediction intervals based on -fold cross validation. We focus on the conditional coverage probability of the proposed intervals, given the observations in the training sample (hence, training conditional validity), and show that it is close to the nominal level, in an appropriate sense, provided that the underlying algorithm used for computing point predictions is sufficiently stable when feature-response pairs are omitted. Our results are based on a finite sample analysis of the empirical distribution function of -fold cross validation residuals and hold in non-parametric settings with only minimal assumptions on the error distribution. To illustrate our results, we also apply them to high-dimensional linear predictors, where we obtain uniform asymptotic training conditional validity as both sample size and dimension tend to infinity at the same rate and consistent parameter estimation typically fails. These results show that despite the serious problems of resampling procedures for inference on the unknown parameters (cf. Bickel and Freedman, 1983; Mammen, 1996; El Karoui and Purdom, 2018), cross validation methods can be successfully applied to obtain reliable predictive inference even in high dimensions and conditionally on the training data.

keywords:

[class=MSC]keywords:

1 Introduction

It is the fundamental task of (supervised) statistical learning, when given an i.i.d. training sample of feature-response pairs and an additional feature vector , to provide a point prediction for the corresponding unobserved response variable . In such a situation, a prediction interval that contains the unobserved response variable with a prescribed probability provides valuable additional information to the practitioner. In many applications a training sample is obtained only once and is subsequently used to repeatedly construct point and interval predictions as new measurements of feature vectors become available. In such a situation, it is desirable to control the conditional coverage probability of the prediction interval given the observations in the training sample, rather than the unconditional probability (the latter is controlled, for example, by procedures discussed in Vovk et al., 2005; Barber et al., 2021). We call this notion of validity of a prediction interval, where the conditional coverage probability given the training data is (approximately) controlled, training conditional validity (see also Vovk, 2013). Notice how this is markedly different from the notion of object conditional validity where the conditioning is on the new feature vector (cf. Foygel Barber et al., 2021).

We study a very simple method based on cross validation (CV) residuals, which is generic, in the sense that it can be constructed on top of any algorithm that produces a point predictor, and that yields asymptotic training conditionally valid prediction intervals provided the underlying point prediction algorithm is sufficiently stable. To illustrate the idea and keep notation simple, we begin with the case of -fold cross validation, that is, leave-one-out. For an i.i.d. training sample of size , consisting of -valued feature-response pairs, and an additional feature vector in , suppose that we have decided to use a prediction algorithm to produce a point prediction for the real unobserved response . If is the sample without the -th observation pair, compute leave-one-out residuals , . Finally, to obtain a prediction interval for , compute appropriate empirical quantiles and from the collection and report the leave-one-out prediction interval

In this paper we investigate the following conditional coverage probability given the training data, where the randomness comes only from the feature-response pair in the prediction period,

We investigate this probability in finite samples and in more specific asymptotic settings, including those where the dimension of the feature vectors increases at the same rate as sample size . We find that even in these challenging scenarios where both and are large, the conditional coverage probability of is typically close to the nominal level , that is, guarantees (approximate) training conditional validity, provided some regularity conditions on the data generating model and the predictor are satisfied. Note that the analogous procedure based on ordinary residuals instead of leave-one-out residuals would, in general, not be valid in such a large- scenario (cf. Bickel and Freedman, 1983). Extending these results to the general -fold cross-validation case relies on a generalization of a result by Bousquet and Elisseeff (2002) on the estimation of the test error of a learning algorithm by its empirical leave-one-out error, which might be of independent interest (see Lemma C.1 in the supplement).

Despite the remarkable simplicity of this method, and its apparent similarity to the Jackknife, we are not aware of any rigorous analysis of its statistical properties. Notable exceptions are Steinberger and Leeb (2016, 2021), which are precursors of this paper, and Barber et al. (2021); the latter will be discussed in Subsection 1.1.3. Our approach is similar, in spirit, to the methods proposed in Butler and Rothman (1980), Stine (1985), Schmoyer (1992), Olive (2007) and Politis (2013), in the sense that it relies on resampling and leave-one-out ideas for predictive inference. But the methods from these references, like most resampling procedures in the literature, are investigated only in the classical large sample asymptotic regime where the number of available explanatory variables is fixed. Prominent exceptions are Bickel and Freedman (1983), Mammen (1996) and, more recently, El Karoui and Purdom (2018). These articles draw mainly negative conclusions about resampling methods in high dimensions, arguing, for instance, that the famous residual bootstrap in linear regression, which relies on the consistent estimation of the true unknown error distribution, is unreliable when the number of variables in the model is not small compared to sample size. In contrast, we show that under mild conditions the leave-one-out prediction interval does not suffer from these problems because it relies on estimation of the conditional distribution of the prediction error instead of an estimator for the unconditional distribution of the error term . That the use of leave-one-out residuals leads to more reliable methods in high dimensions was also observed by El Karoui and Purdom (2018).

Our contribution is threefold. First, we show that the leave-one-out prediction interval (and its extension to -fold CV) is approximately training conditionally valid given the training sample , that is

The error term of the above approximation can be controlled in finite samples and asymptotically, provided that the employed prediction algorithm is sufficiently stable under the omission of feature-response pairs and that it has a bounded (in probability) estimation error as an estimator for the true unknown regression function. It is of paramount importance, however, to point out that we do not need to assume consistent estimability of the regression function and our leading examples are such that consistency fails.

Second, we show that the required stability and approximation properties are satisfied in many cases, including many linear predictors in high dimensional regression problems and even if the true model is not exactly linear. In particular, the proposed method is always valid if the employed predictor is consistent for the unknown regression function (or for an appropriate surrogate target), and is therefore applicable to complex data structures and methods such as non-parametric regression, LASSO prediction, random forests or deep learning (see Section 4).

Third, we discuss issues of interval length and find that in typical situations predictors with smaller mean squared prediction error lead to shorter prediction intervals. For ordinary least squares prediction, we also investigate the impact of the dimensionality of the regression problem on the interval length and discuss the relationship between the leave-one-out method and an obvious sample splitting technique. All our results hold uniformly over large classes of data generating processes and under weak assumptions on the unknown error distribution (e.g., the errors may be heavy tailed and non-symmetric, and the standardized design vectors may have dependent components and a non-spherical distribution).

Our work is greatly inspired by El Karoui et al. (2013) and Bean et al. (2013) (see also El Karoui, 2013, 2018), who investigate efficiency of general -estimators in linear regression when the number of regressors is of the same order of magnitude as sample size . In particular, the -estimators studied in these references provide one leading example of a class of linear predictors for which our construction of prediction intervals leads to training conditionally valid predictive inference even in high dimensions.

The remainder of the paper is organized as follows. In the following Subsection 1.1 we give a brief overview of alternative methods from the large body of literature on predictive inference in regression. Subsection 1.2 introduces the notation that is used throughout the paper. Sections 2 and 3 proceed along a general-to-specific scheme. We begin, in Subsection 2.1, by introducing the general cross validation method and the notion of training conditional validity and we relate this notion to estimation of the conditional prediction error distribution in Kolmogorov distance. In Subsection 2.2, we draw the connection between training conditional validity and algorithmic stability and present our main results which provide sufficient conditions for training conditional validity. In Section 3 we then show that these conditions can be verified in challenging statistical scenarios where regression function estimators and the bootstrap usually fail to be consistent. In particular, we consider linear predictors based on regularized -estimators and based on James-Stein-type estimators in a situation where the number of regressors is not small relative to sample size . We also take a closer look at the ordinary least squares estimator, because its simplicity allows for a rigorous analysis of the resulting interval length. In Section 4, we then also discuss the important case where the employed predictor is consistent (possibly for some pseudo target rather than the true regression function) and we provide examples on non-parametric regression, high-dimensional LASSO, random forests and deep neural networks. The case of consistency is an important test case for our method. Finally, we present the results of an extensive simulation study in Section 5. Further discussions and possible extensions of our results as well as most of the technical proofs are deferred to the supplementary material Steinberger and Leeb (2022).

1.1 Related work

In a fully parametric setting, predictive inference is essentially a special case of parametric inference (see, e.g., Cox and Hinkley, 1974, Subsection 7.5). Constructing valid prediction sets becomes much more challenging, however, if one is interested in a non-parametric setting. By non-parametric, we do not only mean that the regression function can not be indexed by a finite dimensional Euclidean space, but also that the random fluctuations about the conditional mean function can not be described by a parametric family of distributions.

1.1.1 Tolerance regions

A rather well researched and classical topic in the statistics literature is the construction of so called tolerance regions or tolerance limits, which are closely related to prediction regions. A tolerance region is a set valued estimate based on i.i.d. -variate data , , such that the probability of covering an independent copy is close to a prescribed confidence level. More precisely, a tolerance region is such that , and is called a -expectation tolerance region, if (cf. Krishnamoorthy and Mathew, 2009). The study of non-parametric tolerance regions goes back at least to Wilks (1941, 1942), Wald (1943) and Tukey (1947) (see Krishnamoorthy and Mathew, 2009, for an overview and further references) and is traditionally based on the theory of order statistics of i.i.d. data. These researchers already obtained multivariate distribution-free methods, that is, tolerance regions that achieve a certain type of validity in finite samples without imposing parametric assumptions. The connection to prediction regions is apparent: If , then a tolerance region for can be immediately used to obtain a prediction region for by setting . However, this is arguably not the most economical way of constructing a prediction region. In fact, the construction of a multivariate and possibly high-dimensional tolerance region appears to be a more ambitious goal than the construction of a prediction region for a univariate response variable. In particular, since estimation of the full density of – which could be used to compute an optimal highest density region – is usually not feasible if the dimension is non-negligible compared to sample size , one has to specify a shape for the tolerance region and it is not obvious which shapes are preferable in a non-parametric setting. For example, Bucchianico et al. (2001) provide results for smallest possible hyperrectangles and ellipsoids, but obtain only the classical large sample asymptotic results with fixed dimension. Chatterjee and Patra (1980) estimate the density non-parametrically, which fails in high dimensions. Li and Liu (2008) use a notion of data depth to avoid the specification of the shape, but the fully data driven method, again, is only shown to be valid asymptotically, with the dimension fixed. Finally, numerically computing the -cut of to obtain is computationally demanding and the result is sensitive to the shape of .

1.1.2 Conformal prediction

A strand of literature which has emerged from the early ideas of non-parametric tolerance regions, but which is more prominent within the machine learning community than the statistics community, is called conformal prediction (Vovk et al., 1999, 2005, 2009). Conformal prediction is a very flexible general framework for construction of prediction regions that can be used in conjunction with any learning algorithm. The general idea is to construct a pivotal -value to test based on the sample and , for each possible value of , and to invert the test to obtain a prediction region for , i.e., . The method was primarily designed for an on-line learning setup (cf. Vovk et al., 2009), but has recently been popularized in the statistics community by Lei et al. (2013); Lei et al. (2018) and Lei and Wasserman (2014), who study it as a batch method. Aside from their flexibility, conformal prediction methods have the advantage that they are valid in finite samples, in the sense that the unconditional coverage probability is no less than the nominal level , provided only that the feature-response pairs are exchangeable. On the other hand, their practical implementation is not so straight forward, because, for the test inversion, the -value has to be evaluated on a grid of possible values, which is especially tricky if the conformal prediction region is not an interval (see Chen et al., 2018; Lei, 2019, for further discussion of these issues). Moreover, it is not clear if the classical conformal methods can also provide training conditional validity. In Vovk (2012), a version of conformal prediction was presented that achieves also a certain type of (approximate) training conditional validity. However, the method relies on a sample splitting idea, which usually makes the prediction region unnecessarily wide (see Subsection 3.4 as well as Subsection A.2 in the supplement for further discussion of sample splitting techniques). A different version of conditional validity (conditioning on ), is discussed in Foygel Barber et al. (2021) (see also Remark A.3 in the supplement).

1.1.3 The jackknife+

Barber et al. (2021) recently proposed a modification of the leave-one-out method considered here. For the modified method, which they call jackknife+, they derived a finite-sample lower bound for the unconditional coverage probability, under the assumption that the feature-response pairs are exchangeable and without requiring that the prediction algorithm is stable. For a jackknife+ interval with nominal coverage probability , the lower bound is ; if the prediction algorithm is stable (under omission of a single feature-response pair), the lower bound moves closer towards (provided that the interval is slightly modified further). In simulations and data-examples, Barber et al. (2021) found that the jackknife+ performs essentially like the jackknife, i.e., like the method considered in this paper, unless the prediction algorithm is highly unstable; in the unstable case, jackknife+ outperforms jackknife. The use of an unstable prediction method is, of course, debatable, at least if the user is aware of the instability. The training conditional performance of the jackknife+ interval, that is, its coverage probability conditional on the training data, is yet to be analyzed.

1.2 Preliminaries and notation

For , let and be Borel measurable sets and let . For , , a realization of a training sample is denoted by , where is a feature-response pair. The realizations of feature-response pairs in the prediction period are denoted by . All the randomness we consider comes from drawing training samples and , and we assume that all feature-response pairs are drawn independently and identically distributed from some probability distribution belonging to a class of Borel probability measures on . By we denote the joint product measure of all occurring feature-response pairs with marginal distribution and we write for the corresponding expectation operator. Thus, strictly speaking, and can change their meaning from line to line if the number of feature-response pairs changes. We use expressions like , , , , etc., to denote integration only with respect to the indicated variables (or marginal distributions). By we denote a regular conditional distribution of given under . By , , we denote (a version of) the true unknown regression function, if it exists. We sometimes express the training data as , where and . Moreover, denotes the transpose of , and we write for the Moore-Penrose inverse of . Similarly, we write and for the corresponding leave-one-out quantities.

Next, we formally define the notion of a (learning) algorithm, of a predictor (or estimator) and of the cross validation residuals. For , write and consider a collection of measurable functions , . The collection is called a learning algorithm. For , let be a partition of and abbreviate , . For a vector , we set and , where denotes the reduced training sample where the observations with indices in have been excluded. We call a predictor or estimator and say that it, or the underlying learning algorithm, is symmetric if for every , for every choice of , every and every permutation of elements, .111Some of the predictors that appear in this paper happen to be symmetric, but symmetry is actually never imposed as a condition in our general theory. We mention this concept only because it can sometimes simplify things and also appears in the literature. Finally, we define -fold cross validation (-CV) residuals for and , by .

If is a real valued function on some domain , then . For , we also write , and , and let denote the smallest integer no less than . If is a cumulative distribution function, we write for the corresponding quantile function. We write , if the random quantities and are equal in distribution and the underlying probability spaces are clear from the context. By a slight abuse of notation, we also write if the random variable is distributed according to the probability law and, again, the underlying probability space is clear from the context.

For our asymptotic statements, we will also adopt the following array setup: Unless stated otherwise, all quantities introduced above are allowed to also depend on sample size . We consider sequences and of positive integers and a collection of data generating distributions , where is a probability measure on . We use symbols like , , , , etc., to emphasize dependence on . For a collection of measurable functions , we say that is -bounded in probability if , as , and write . If , as , for every , then we say that converges in -probability to zero and write . Similarly, we say that converges in -probability to , which is also assumed to be measurable, if . Since the probability measure will be chosen arbitrarily from some class of probability measures on , our asymptotic results will be uniform over the respective classes.

2 Main results

2.1 -CV prediction intervals and training conditional validity

For , we want to construct a prediction interval for , where and are measurable functions on , such that

| (2.1) |

is small uniformly over a class of data generating distributions for the feature-response pairs and . We can not expect the expression in (2.1) to be equal to zero for some fixed and a reasonably large class (see Remark A.1 in the supplement). Therefore, we are content with (2.1) being close to zero as , and possibly also , is large. A similar but slightly different notion of training conditional validity is studied by Vovk (2013), and is closely related to the conventional notion of a tolerance region for close to (cf. Krishnamoorthy and Mathew, 2009). However, these conventional definitions require only that the conditional coverage probability is no less than the prescribed confidence level , with high probability, whereas the requirement that (2.1) is small also excludes overly conservative procedures. Nevertheless, we also refer to our requirement in (2.1) as training conditional validity. Note that if (2.1) is small, then also

will be small. Hence, the prediction interval is then also approximately unconditionally valid, uniformly over .

If the conditional distribution function is continuous, then, for fixed, there is an optimal shortest but infeasible interval

| (2.2) |

in the set of all prediction intervals of the form which also satisfy

| (2.3) | ||||

| (2.4) |

Simply choose to be the largest -quantile of and to be the smallest -quantile of . This gives the user the flexibility to choose precisely what error probability of under- and over-prediction she is willing to accept. This also shows that what we are really interested in is the unknown conditional distribution of the prediction error . Thus, for , (2.1) is actually equal to zero (for ), at least if contains only probability distributions on for which is almost surely continuous.

We propose the following simple cross validation idea to approximate the optimal infeasible procedure: Consider the weighted empirical distribution function

| (2.5) |

of the -CV residuals , , where is the prediction of the learning algorithm at when all observations from the fold are removed from the training data . For , let denote the empirical -quantile. Then the -CV prediction interval is given by

| (2.6) |

The idea behind the -CV procedure is remarkably simple. To estimate the conditional distribution of the prediction error , i.e.,

| (2.7) |

we simply use the (weighted) empirical distribution of the -CV residuals , . Notice that is independent of , and is independent of , since , and thus has almost the same distribution as the prediction error, except that is calculated from observations less than . In many cases this difference turns out to be negligible if is large, even if is relatively large too, provided that is chosen to be sufficiently small. Note, however, that the -CV residuals are not independent, which leads to substantial technical challenges.

The following result shows that, indeed, a sufficient condition for asymptotic training conditional validity (2.1) of the -CV prediction interval in (2.6) is consistent estimation of in Kolmogorov distance.

Proposition 2.1.

Fix , a training sample , an arbitrary cumulative distribution function (possibly depending on ) and write for the size of the largest jump of . Define the interval

| (2.8) |

where . Let be as in (2.7).

-

i)

We have

-

ii)

If the cdf is continuous, then the prediction interval defined in (2.8) satisfies

Remark 2.2.

Note that the inequalities of Proposition 2.1 are purely algebraic statements for a fixed training set . Also note that the coverage probability is a version of the conditional probability .

Proof of Proposition 2.1.

By virtue of Proposition 2.1, most of what follows will be concerned with the analysis of . We are particularly interested in situations where, for a fixed , does not concentrate around with high probability but remains random (cf. Remark A.2 in the supplement). In such cases, the unconditional distribution function of the prediction error , the empirical distribution function of the ordinary residuals and the true error distribution function need not be close to one another, because may not contain enough information about the true regression function (see, for instance, Bickel and Freedman, 1983; Bean et al., 2013, for a linear regression example where )222It turns out, however, at least in the linear model and for appropriate estimators of , that the conditional distribution of the prediction error does concentrate at its mean, i.e., the unconditional distribution, even if and are of the same order of magnitude (cf. Subsection 3.3 and Lemma C.9 in the proof of Theorem 3.4).. Nevertheless, we will see that even in such a challenging scenario, it is often possible to consistently estimate the conditional distribution of , given the training sample , by the (weighted) empirical distribution of the -CV residuals.

2.2 The role of algorithmic stability

In this section we present general results that relate the uniform estimation error to a measure of stability of the underlying predictor . For our first result, sample size and dimension are fixed. We only need the following condition on the data generating distribution.

-

(C1)

The conditional distribution has a Lebesgue density .

Notice that, although the training data , , are assumed to be realizations of i.i.d. random vectors, Condition (C1) allows to model heteroskedasticity, because the conditional variance of the response given is allowed to depend on the value of the feature vector . Building on terminology from Bousquet and Elisseeff (2002) (see also Devroye and Wagner, 1979), we use the following probabilistic notion to quantify algorithmic stability, which is adjusted to the general case of -fold cross validation and which depends on the true data generating distribution on .

Definition 2.3.

The -stability coefficient of the predictor is defined as

The stability coefficient measures the average change of the prediction of as the observations of each of the -folds are removed in turn for training. A highly stable algorithm has small stability coefficient. In the extreme case of an algorithm that does not even make use of the training data at all, we have . Since the feature-response pairs are assumed to be i.i.d. under , it is easy to see that in case of equal fold sizes , , a symmetric predictor has stability coefficient . Also note that a predictor with can not depend on the training data in a non-trivial way (cf. Lemma D.6 in the supplement). We are now in the position to state our main result on the estimation of by . To that end, we adopt the triangular array setup described in Subsection 1.2.

Theorem 2.4.

For , let and be positive integers, with as , and let be a data generating distribution on , with , , that satisfies (C1). Furthermore, suppose that there exists a scaling constant and a measurable function , such that the following hold true:

| (2.10) | ||||

| (2.11) | ||||

| (2.12) | ||||

| (2.13) |

Then, the (weighted) empirical cdf of the -fold cross validation residuals satisfies

Moreover, for , the -fold cross validation interval is asymptotically training conditionally valid, i.e.,

| (2.14) |

Remark 2.5 (Uniform training conditional validity).

For each , let and be as in Thorem 2.4, and let be a class of probability measures on . If Theorem 2.4 applies for any sequence , , then the -fold cross validation interval is uniformly asymptotically training conditionally valid, i.e., the left-hand-side of (2.14) converges to zero even when taking the supremum over all .

In Theorem 2.4, one should think of the scaling constant and the function as the error variance and the regression function in a non-linear regression model , with additive error that is independent of and has variance . However, they can be taken as appropriate pseudo parameters if needed. Also notice that Condition (C1) allows for a heteroskedastic error term. Theorem 2.4 is actually a simple consequence of the following finite sample bound.

Theorem 2.6.

Fix positive finite constants and a measurable function . If Condition (C1) holds, then

where is the stability coefficient of the predictor .

Proof of Theorem 2.4.

Theorem 2.6 provides an upper bound on the risk of estimating the conditional prediction error distribution by the (weighted) empirical distribution of the cross validation residuals . The upper bound crucially relies on the properties of the chosen estimator for the (pseudo) regression function . If the sample size is sufficiently large and if the estimator is sufficiently stable and has a moderate estimation error, then the parameters can be chosen such that the upper bound is small. This is what we do in Theorem 2.4. It is important to note that Theorem 2.4 and Theorem 2.6 are informative also in case the estimator is not consistent for , as is often the case when . The bound of Theorem 2.6 also exhibits an interesting trade-off between the -stability of and the magnitude of its estimation error. More stable estimators are allowed to be less accurate whereas less stable estimators need to achieve higher accuracy in order to be as reliable for predictive inference purposes as a more stable algorithm.

Theorem 2.4 and Theorem 2.6 show that the -CV prediction interval in (2.6) is approximately uniformly training conditionally valid, i.e., has the property that (2.1) is uniformly small at least for large , provided that the underlying estimator has two essential properties: First, the -stability coefficient of the estimator must be (uniformly) small if is large, as in (2.13). This is an intuitively appealing assumption since otherwise the -CV residuals may not be well suited to estimate the distribution of the prediction error . Second, the scaled estimation error at the new observation must be -bounded (cf. (2.12) with ). This is used to guarantee that the conditional distribution of the prediction error given the training data is tight in an appropriate sense (cf. Lemma C.5(ii) in the supplement), so that a pointwise bound on can be turned into a uniform bound. In the following sections we demonstrate that these two conditions on the estimator are satisfied in several different contexts. From now on, as in Theorem 2.4, we will take on an asymptotic point of view.

3 Linear prediction with many variables

In this section we investigate a scenario in which both consistent parameter estimation as well as bootstrap consistency fail (cf. Bickel and Freedman, 1983; El Karoui and Purdom, 2018), but the -CV prediction interval is still asymptotically uniformly training conditionally valid. See Section 4 for a discussion of scenarios where consistent parameter estimation is possible. For simplicity, in this section we consider only the leave-one-out case, that is, . For , we fix a sequence of positive integers , such that as and for all . In case , this type of ‘large , large ’ asymptotics has the advantage that certain finite sample features of the problem are preserved in the limit, while offering a workable simplification. It turns out that conclusions drawn from this type of asymptotic analyses often provide remarkably accurate descriptions of finite sample phenomena.

We work with linear predictors of the form for various estimators . Suppose the second moment matrix exists. Then the conditions (2.13) and (2.12) can be verified as follows: For ,

where, for the second inequality, we have used the conditional Markov inequality along with independence of and under , and denotes the estimator based on the reduced training sample . Thus (2.13) follows if

| (3.1) | ||||

| (3.2) |

Notice that (3.1) coincides with (2.10). By a similar argument, we find that (2.12) with follows if

| (3.3) |

for some vectors , and (2.11) can be expressed as

| (3.4) |

3.1 Regularized -estimators

An important class of linear predictors for which our theory on the leave-one-out prediction interval applies are those based on regularized -estimators investigated by El Karoui (2018) in the challenging scenario where is not close to zero (see also El Karoui et al., 2013; Bean et al., 2013; El Karoui, 2013). For a given convex loss function and a fixed tuning parameter (both not depending on ), consider the estimator

| (3.5) |

In a remarkable tour de force, El Karoui (2018) studied the estimation error as , in a linear model , allowing for heavy tailed errors (including the Cauchy distribution) and non-spherical design (see Subsection 2.1 in El Karoui, 2018, for details on the technical assumptions). In particular, the author shows that converges in probability to a deterministic positive and finite quantity and characterizes the limit through a system of non-linear equations. On the way to this result, El Karoui (2018, Theorem 3.9 together with Lemma 3.5 and the ensuing discussion) also establishes the stability property in probability. Thus, under the assumptions maintained in that reference, (3.2), (3.3) and (3.4) hold, and the leave-one-out prediction interval based on the linear predictor is asymptotically training conditionally valid, provided that also the boundedness condition (3.1) is satisfied. Finally, we note that a detailed assessment of the predictive performance of in dependence on requires a highly non-trivial analysis of . For the asymptotic validity of the leave-one-out prediction interval, however, all the information needed on is that it is finite.

3.2 James-Stein type estimators

Another important example is the class of linear predictors based on James-Stein type estimators defined below. Here, we can allow for the class of data generating processes defined in Condition (C2) below. The feature-response pairs are realizations of a non-Gaussian random design non-linear homoskedastic regression model with regression function and error variance . Moreover, the feature vectors are allowed to have a complex geometric structure, in the sense that the standardized design vector is not necessarily concentrated on a sphere of radius , as would be the case if in Condition (C2) was supported on (see, e.g., Subsection 3.2 in El Karoui, 2010 and Subsection 2.3.1 in El Karoui, 2018 for further discussion of this point).

-

(C2)

Fix finite constants and and probability measures and on , such that has mean zero, unit variance and finite fourth moment, and .

For every , the class consists of all probability measures on , such that the following hold:

-

(a)

The -marginal distribution of is given by

where are i.i.d. according to , is independent of the and is the unique symmetric positive definite square root of a positive definite covariance matrix .

-

(b)

The conditional distribution of the response given the regressors is

where is independent of and has mean zero, unit variance and fourth moment bounded by , where is some measurable regression function with and .

-

(a)

The model in (C2) is non-parametric, because the regression function is unrestricted, up to being centered, and the independent error distribution is arbitrary, up to the requirements , and .

To predict the value of from and a training sample with , generated from , we consider linear predictors , where is a James-Stein-type estimator given by

for a tuning parameter . Here , . The corresponding leave-one-out estimator is defined equivalently, but with and replaced by and . Note that the leave-one-out equivalent of is given by

The ordinary least squares estimator belongs to the class of James-Stein estimators. In particular, , because, with , we have if, and only if, , and the latter clearly implies .

Using James-Stein type estimators for prediction is motivated, e.g., by the optimality results of Dicker (2013) and the discussion in Huber and Leeb (2013). The next result shows that in the model (C2) with and if the deviation from a linear model is not too severe, the James-Stein-type estimators are sufficiently stable and their estimation errors are uniformly bounded in probability, just as required in (3.2) and (3.3).

Theorem 3.1.

For every , let as in Condition (C2) and suppose that under , the error term in (C2) has a Lebesgue density. Define to be the minimizer of over . If , for all , and

| (3.6) |

then the positive part James-Stein estimator satisfies (3.3), i.e.,

If, in addition, , then (3.2) is also satisfied, i.e., for every ,

Remark 3.2.

Under the assumptions of Theorem 3.1, uniform asymptotic training conditional validity of the leave-one-out prediction interval follows, provided that, in addition, the errors in Condition (C2) have uniformly bounded densities so that (3.1) holds. To see this, note that (3.2) and (3.3) are conclusions of the theorem, that uniformly bounded fourth moment of the error implies -uniform boundedness, such that (3.4) is a consequence of assumption (3.6).

Remark 3.3.

The last statement of Theorem 3.1 can also be established for the case but would require a different proof strategy. Since this case is statistically less interesting we omit it for the sake of brevity.

3.3 Ordinary least squares and interval length

We investigate the special case of the ordinary least squares predictor in some more detail, because here also the length

of the leave-one-out prediction interval (cf. (2.6) with ) admits a reasonably simple asymptotic characterization. We consider a class which is a subset of the one of Condition (C2), with the additional assumption that the regression function is linear and that the error distribution is fixed (up to arbitrary scaling).

-

(C3)

Fix a finite constant and probability measures , and on , such that and have mean zero, unit variance and finite fourth moment, and .

For every , the class consists of all probability measures on , such that the following hold:

-

(a)

The -marginal distribution of is given by

where are i.i.d. according to , is independent of the and is the unique symmetric positive definite square root of a positive definite covariance matrix .

-

(b)

The conditional distribution of the response given the regressors is

where is independent of , and where and .

-

(a)

Note that under (C3), the distributions , and are fixed, so that is a parametric model indexed by , and . However, these parameters may depend on sample size , and the dimension of and of may increase with . Subsequently, we aim at uniformity in these parameters.

Theorem 3.4.

Fix . For every , let with as in (C3). If then the scaled empirical -quantile of the leave-one-out residuals based on the OLS estimator converges in -probability to the corresponding -quantile of the asymptotic distribution of the scaled prediction error . The latter is equal in distribution to

where and are defined as follows: , , and are independent, and is non-random.

The same statement holds also for , provided that, in addition, has a continuous and strictly increasing cdf and as .

Here, the function defined on has the following properties: For any as in (C3), if, and only if, . If , then .

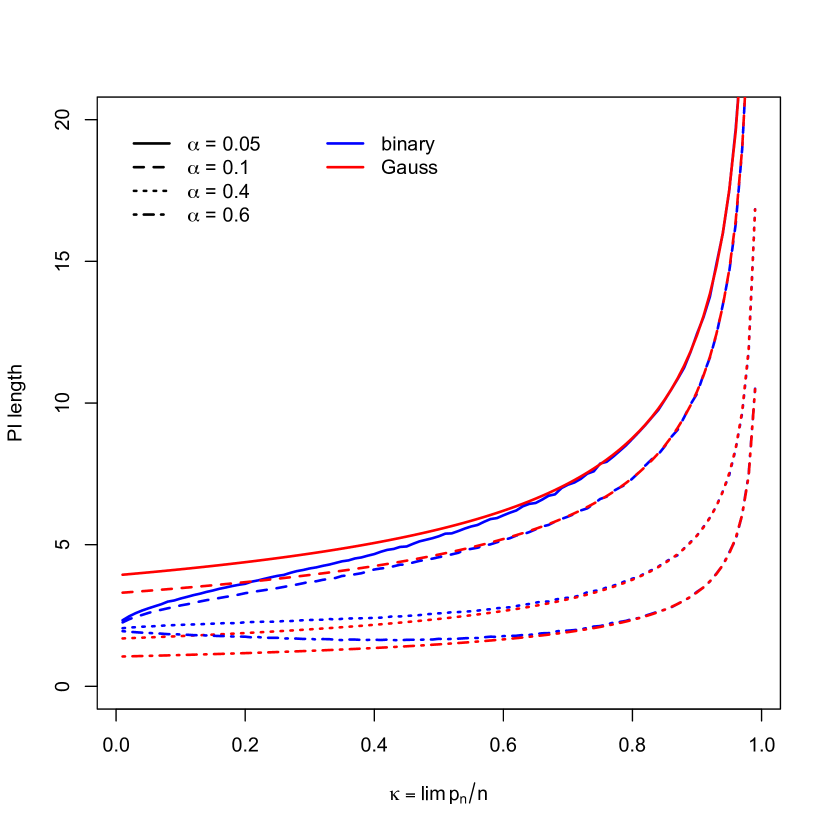

Theorem 3.4 shows how the length of the leave-one-out prediction interval for the OLS predictor depends (asymptotically) on , and . For simplicity, let and consider an equal tailed interval, i.e., . Figure 1 shows asymptotic interval lengths as functions of for different values of error level in the cases and . For a wide range of values (), the interval length is almost constant. However, for high dimensional problems () the interval length increases dramatically, as expected, because here the asymptotic estimation error explodes. We also get an idea about the impact of the error distribution, on which the practitioner has no handle. In particular, for large error levels () we even observe a non-monotonic dependence of the interval length on , which seems rather counterintuitive. This results from the non-monotonicity of , where denotes convolution. This non-monotonicity may only occur if the error distribution is not log-concave (e.g., the blue curve for in Figure 1; cf. the discussion in Subsection A.1 of the supplement). Finally, for large values of , and thus, for large values of , the error distribution has little effect on the interval length, because in that case the term dominates the distribution of .

The result of Theorem 3.4 can be intuitively understood as follows. If the true model is linear and satisfies (C3) then the scaled prediction error under , is distributed as

and for large, is approximately non-random, so that , where is a random unit vector that is independent of . Thus, if is large and satisfies the Lyapounov condition , then (see Lemma C.9(ii) in the supplement). This effect of additional Gaussian noise in the prediction error was also observed by El Karoui (2013); El Karoui et al. (2013); El Karoui and Purdom (2018); El Karoui (2018). Note that the conditions and need not be satisfied by a given estimator . However, the former condition is always satisfied by the robust -estimators

considered in El Karoui (2018, 2013) and under the model assumptions in that reference (cf. Subsection 3.1). Here, is an appropriate convex loss function. The Lyapounov condition is also satisfied by , provided that the standardized design vectors follow an orthogonally invariant distribution, because then one easily sees that under (C3)

where and is uniformly distributed on the unit sphere and independent of . Therefore, , in probability, for , as . However, the Lyapounov property is not satisfied, e.g., by the James-Stein estimators (cf. Lemma D.5 in the supplement). If the mentioned conditions are not satisfied, much more complicated limiting distributions of the prediction error than the one of Theorem 3.4 may arise.

3.4 Sample splitting

An obvious alternative to the -fold cross validation prediction interval (2.6) is to use a sample splitting method as follows. Decide on a fraction and use only a number of observation pairs , , , to compute an estimate . Now use the remaining observations to compute residuals , . Since, conditionally on the observations corresponding to , these residuals are i.i.d. and distributed as , constructing a prediction interval of the form for is now equivalent to constructing a tolerance interval for based on i.i.d. observations with the same distribution. One can now simply use appropriate empirical quantiles and from the sample splitting residuals (see also Subsection A.2 in the supplement). Such a procedure is suggested and studied, e.g., by Vovk (2012) and Lei et al. (2018). Notice, however, that this prediction interval is not centered at the more accurate point predictor that is computed from the full sample of size .

In order to formally study the length of this sample splitting interval we restrict to the case of OLS estimation, i.e., , where is the OLS estimator based on the sample corresponding to . Note that in this case, the estimator will not be unique if , so one usually requires . Now, in view of Theorem 3.4, the empirical quantiles of the residuals , , converge (unconditionally) to the quantiles of , where now is the non-random limit of . In particular, if degenerates to , then , where . Thus, we can read off the asymptotic interval length of the sample splitting procedure from Figure 1 by simply adjusting the value of to . For instance, in the binary error case with , if and we use sample splitting with , then and the asymptotic length of the leave-one-out prediction interval is about , while the asymptotic length of the sample splitting interval is about , so almost twice as wide.

4 Asymptotically degenerate (non-random) estimators

Another important class of problems, where the conditions (2.12) and (2.13) of Subsection 2.2 are satisfied, are those where the estimator (and those computed without the observations in the -th fold ) asymptotically degenerates to some non-random function which need not be the true regression function . We point out that in the scenario considered in this section, the naive approach that tries to estimate the true unknown distribution of the errors in the additive error model (C2) based on the ordinary residuals is often successful (asymptotically) for constructing training conditionally valid prediction intervals, provided that consistent estimation of is possible. This less challenging but more classical setting of asymptotically non-random predictors is an important test case for the CV method. We still consider asymptotic results where the number of explanatory variables and the number of folds can grow with sample size . Thus, we consider sequences and , and a sequence of probability measures, where is supported on . Moreover, we have to slightly extend the usual definition of uniform consistency of an estimator sequence to cover also the estimates omitting the -th fold and to allow the possibility of an asymptotically non-vanishing bias.

Definition 4.1 (Uniform Asymptotic Degeneracy (UAD)).

For every , let , let be a probability measure on and let . We say that a sequence of predictors is uniformly asymptotically degenerate (UAD) with respect to and relative to , if there exists measurable functions , such that for every ,

| (4.1) | |||

| (4.2) |

In the classical case of consistent estimation, the function would be the true unknown regression function and the constant can be thought of as the error variance , if it exists, or can be chosen equal to .

It is convenient and common practice to choose the -folds of approximately the same size. We consider the following convention: In case , choose all folds of equal size and otherwise choose and and . With this convention, the left hand side of (4.2) can be written as

irrespective of whether is symmetric or not. Hence, (4.2) follows if

| (4.3) |

Thus, under this construction it actually suffices to verify (4.1) and (4.3) to establish UAD. Furthermore, in many cases (4.3) will even be equivalent to (4.1), provided that is growing sufficiently fast with .

It is easy to see that if is UAD with respect to and relative to and if (C1) holds, then the sequence of stability constants satisfies (2.13), i.e.,

provided that . Simply use the inequality , for . Also note that is the sup-norm of the conditional density of the scaled error term given .

In the remainder of this subsection we list a number of examples where the UAD property of holds. Therefore (assuming (C1) and the boundedness conditions of Theorem 2.4) also asymptotic training conditional validity of the -CV prediction interval follows. We emphasize that the conditions on the statistical model , that are imposed in the subsequent examples, are taken from the respective reference and we do not claim that they are minimal.

Example 4.2 (Non-parametric regression estimation).

Consider a constant sequence of dimension parameters . For positive finite constants and , let denote the class of probability distributions on such that and whose corresponding regression function is -Lipschitz, i.e., for all . Györfi et al. (2002, Chapter 7) show that if is either an appropriate kernel estimate, a partitioning estimate or a nearest-neighbor estimate, all with fully data driven choice of tuning parameter, then, if ,

for every . Thus (4.1) holds with and , and under the (approximate) equal fold size construction mentioned above, (4.3) also holds provided , because here is constant, and UAD follows.

Example 4.3 (Deep neural networks).

Schmidt-Hieber (2020) considers a nonparametric regression model similar to (C2), but with and . The distribution of the regressors is supported on but is otherwise unrestricted. He assumes a smooth compositional structure for the true unknown regression function, that is, , where

, , , , , , for , , is the set of Hölder functions on with Hölder-exponent and Hölder norm bounded by , and it is implicitly assumed that depends only on of its possible input variables. Consider a predictor that is obtained by empirical risk minimization over a certain class of -bounded (i.e., ) ReLU networks with layers where the -th layer has output dimension , and , and which have bounded and -sparse network parameters. If the tuning parameters and are chosen appropriately, and if, in particular, the network depth is logarithmically growing with , Schmidt-Hieber (2020, Corollary 1) shows that

where does not depend on (but on ),

and . Thus, (4.1) and (4.2) are satisfied with and , provided that , where is the number of observed feature-response pairs excluding the ones in the largest fold.

Example 4.4 (Random forests).

Scornet et al. (2015) consider an additive regression model similar to (C2), but with , the uniform distribution on and additive regression function

where the are continuous. A random forest predictor is trained in the following way: Each tree is grown by first randomly subsampling a number of feature-response pairs from the training set and then growing a tree according to the CART-split criterion (see Scornet et al., 2015, Section 2, for details). The tree growing process is terminated when a number of leaves is reached. In this way, random regression trees are grown, each of which predicts by averaging all the whose features belong to the leaf containing . Scornet et al. (2015) study the idealized predictor obtained from averaging these predictions and letting . They show that if in such a way that , we have for every fixed data generating distribution as above,

Thus (4.1) holds, and under the (approximate) equal fold size construction mentioned above, (4.3) also holds provided , because here is constant.

Example 4.5 (High-dimensional linear regression with the LASSO).

Consider a non-decreasing sequence of positive real numbers and a sequence of dimension parameters such that as . For a positive finite constant , let denote the class of probability distributions on , such that under , the pair has the following properties:

-

•

, almost surely.

-

•

Conditional on , is distributed as , for some and .

-

•

The parameters and satisfy .

In particular, we have . Chatterjee (2013, Theorem 1) shows that any estimate which minimizes

satisfies

for every and if . Clearly, here the estimate excluding the data from the first fold has the same asymptotic property, provided that , with . Thus, under the (approximate) equal fold size construction, UAD holds. Note that in this example, consistent estimation of the parameters and would require additional assumptions on the distribution of the feature vector (so called ‘compatibility conditions’, see Bühlmann and van de Geer, 2011), and therefore, it is not immediately clear whether the usual Gaussian prediction interval, based on estimates and and a Gaussian quantile, is asymptotically valid in the present setting. Furthermore, the result of Chatterjee (2013) can be extended also to the non-Gaussian case, where the usual Gaussian prediction interval certainly fails.

Example 4.6 (Ridge regression with many variables).

A qualitatively different parameter space is considered in Lopes (2015), who shows uniform consistency of ridge regularized estimators in a linear model under a boundedness assumption on the regression parameter and a specific decay rate of eigenvalues of .

Example 4.7 (Misspecified regression estimation).

A classical strand of literature on the asymptotics of Maximum-Likelihood under misspecification has established various conditions under which the MLE is not consistent for the true unknown parameter, but for a pseudo parameter that corresponds to the projection of the true data generating distribution onto the maintained working model. See, for example, Huber (1967), White (1980b, a) or Fahrmeir (1990). A common pseudo target in random design regression is the minimizer of .

5 Numerical results

We conduct an extensive simulation study to assess the quality of our theoretical approximations in a small sample situation. For our numerical experiments we closely follow the setup of Barber et al. (2021). We compute prediction intervals with nominal coverage probability of using i.i.d. training samples of different sizes and explanatory variables. Each data point is generated as

We also generate test data points from the same distribution. The true coefficient vector is drawn once for each parameter configuration as for a uniform random unit vector in and is then fixed throughout the Monte Carlo iterations. Instead of the least squares estimator (or the minimum norm interpolator in case ) studied in the simulation section 7.1 of Barber et al. (2021), which was exemplified to be unstable in the present regime of and results in anti-conservative performance, we here investigate the LASSO as our prediction algorithm. For simplicity and reproducibility we take the default implementation of the LASSO in the R-package glmnet (Friedman et al., 2010) with data driven choice of tuning parameter determined by -fold cross validation333cv.glmnet(x=X, y=Y, family=”gaussian”, intercept=FALSE, nfolds=5, alpha=1) in glmnet version 4.1-2..

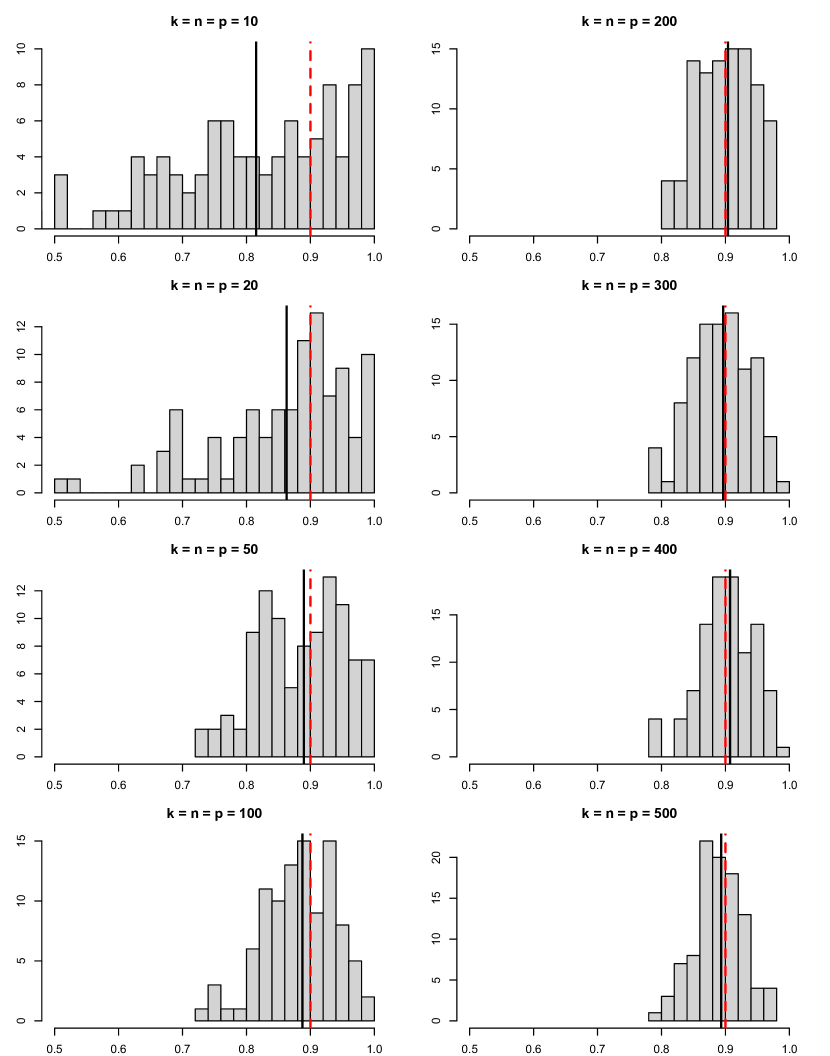

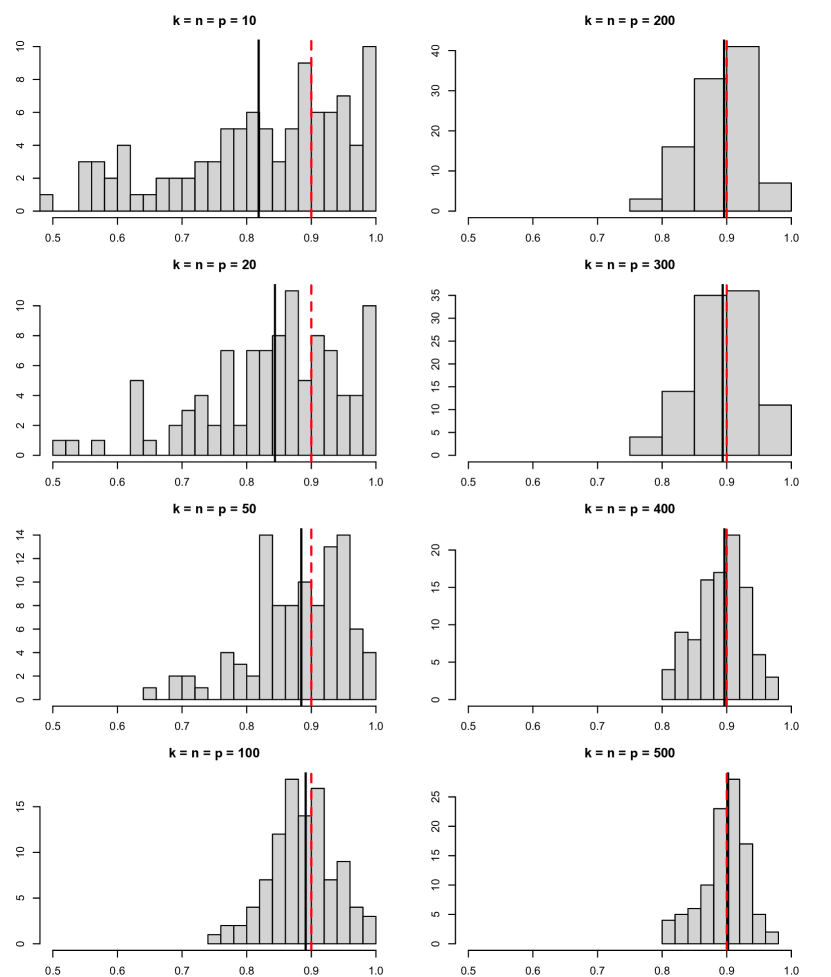

First, we try to experimentally confirm our theoretical prediction that the cross-validation prediction intervals are asymptotically training conditionally valid even in scenarios where no consistent parameter estimation is possible. For simplicity, we consider only leave-one-out cross validation (). Recall that in the challenging scenario where , stability of the OLS predictor fails. Notice also that the condition for consistency of the LASSO predictor of Example 4.5 is not satisfied in the current setup. For each , using the test data points, we compute the empirical probability of coverage. For one fixed training sample , this gives us a Monte Carlo estimate of the conditional coverage probability . In Figure 2 we show histograms of these Monte Carlo estimates, their sample means (black solid lines) and the nominal coverage level (red dashed lines). For small samples we observe an anti-conservative bias as well as a considerable variability in the true conditional coverage probabilities, both of which are reduced as sample size increases, even though increases as well.

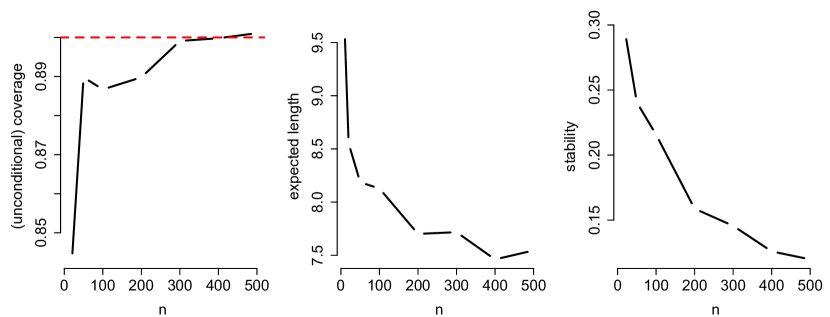

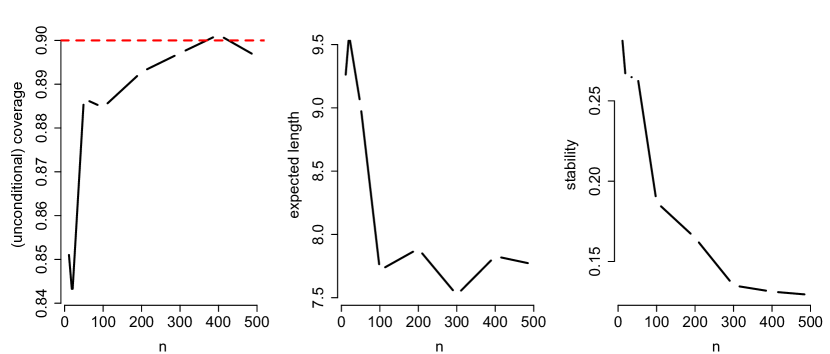

In Figure 3 we show average coverage (i.e., Monte Carlo estimates of the unconditional coverage probabilities ), average length (i.e., Monte Carlo estimates of the expected length) and a Monte Carlo estimate of the stability coefficient (cf. Definition 2.3) as functions of (here, still, ). We estimate the stability of the predictor on a given training sample , by

where , are the regressors in the test set, and then average over the Monte Carlo samples to approximate . As we already saw in Figure 2 (black bold vertical lines), Figure 3 also shows that the unconditional coverage probabilities increase towards the nominal level with increasing and . Simultaneously, the expected interval lengths and the stability coefficients decrease with increasing . Notice that a feasible but trivial prediction (or tolerance) interval for in the present scenario is , with , which has length . This is well outperformed by the leave-one-out prediction interval even in small samples. For reference, the oracle prediction interval for which uses knowledge of the true coefficient vector , has length .

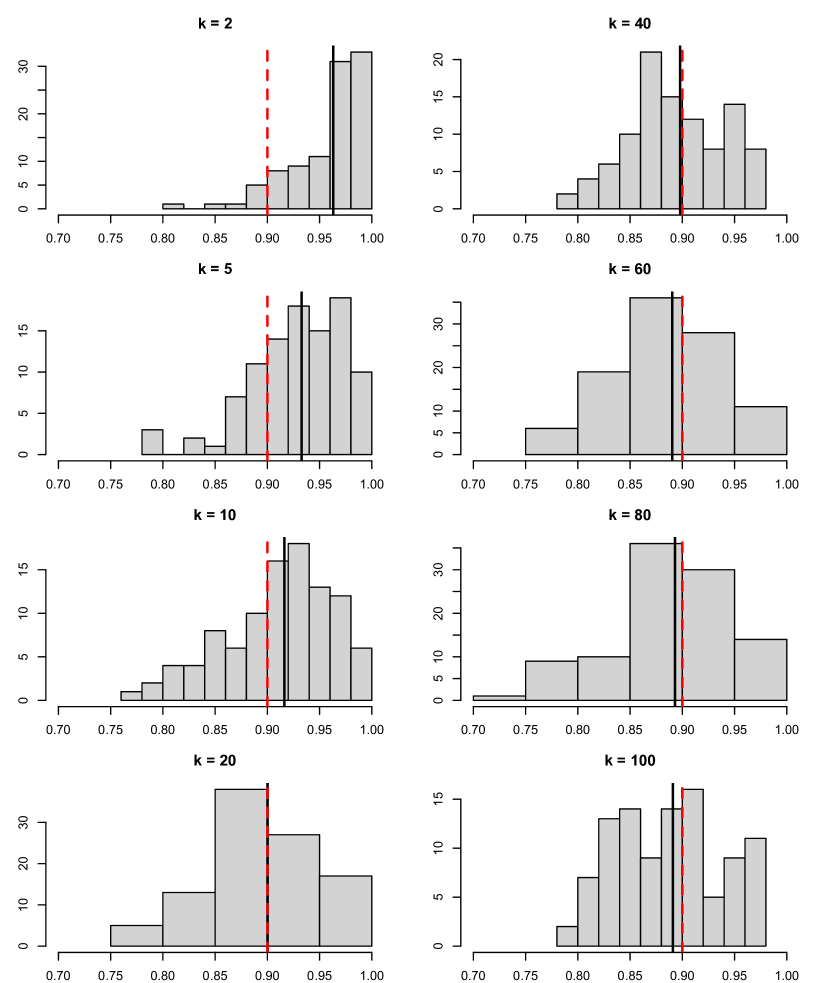

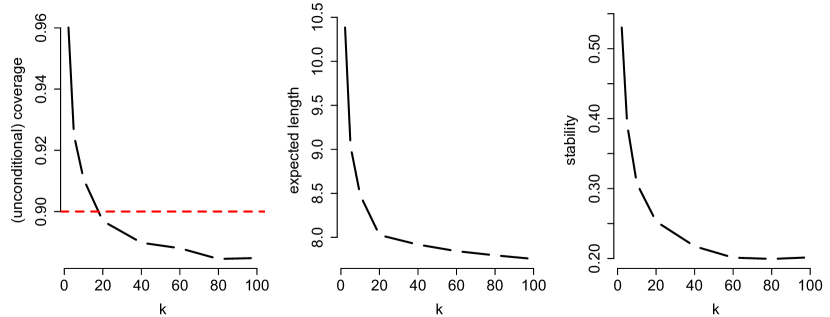

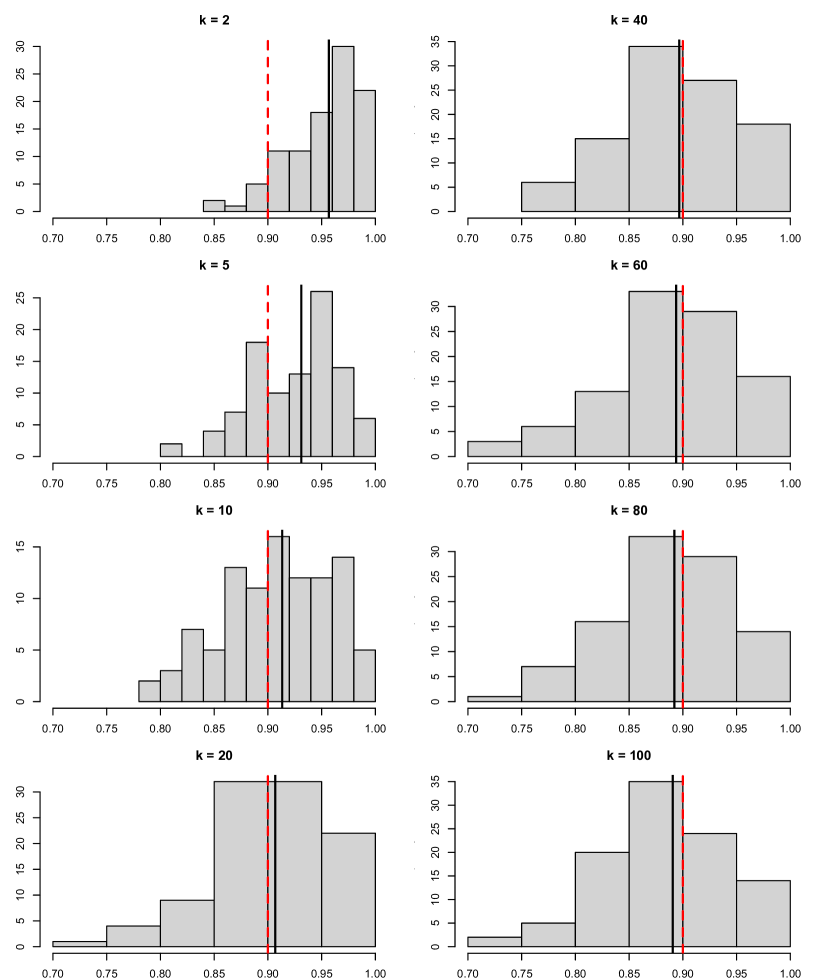

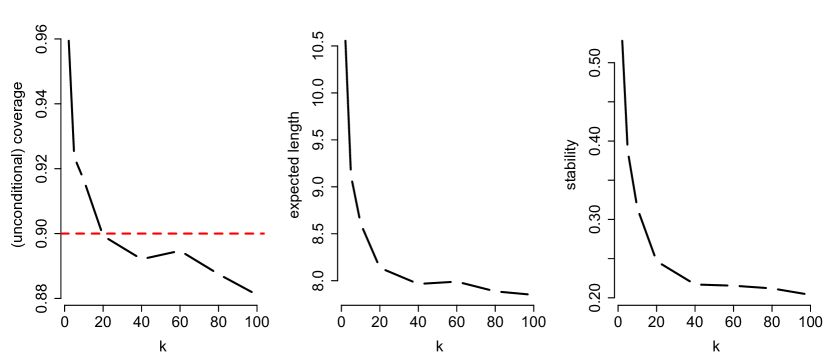

Next, we investigate the impact of the number of folds on the -CV prediction interval. We compute (2.6) for a range of from up to sample size . In Figure 4 we plot histograms of conditional coverage probabilities for different values of , in the case . We find that for small values of , most training samples produce conservative prediction intervals, whereas for larger the conditional coverages are more symmetrically spread around the nominal level with a slight anti-conservative bias (as was already observed in Figure 2). The number of folds does not seem to have a strong impact on the spread of theses conditional probabilities. The conservative behavior for small can be explained in a similar way as for the case of sample splitting (cf. Subsection 3.4 and Subsections A.1 and A.2 in the supplement). In a nutshell, if is small, then , , will be based on much fewer observations than and will thus be less accurate for prediction, leading to residuals that will have much larger variance than the true prediction error . Hence, the resulting prediction interval will be too wide. This reasoning is also supported by Figure 5.

From Figure 5 we learn that coverage probabilities, expected interval lengths and stability all decrease with increasing in a quite similar fashion. This was to be expected for the stability, because for nearly equal fold sizes, the number of observations in each fold decreases as increases, which means that, on average, will decrease for each , as the two predictors are computed on nearly the same observations. We also see in Figure 5 that apparently for smaller values of below , the -CV prediction interval is too wide, as we observe both, large interval lengths as well as over-coverage (cf. the discussion in the previous paragraph). On the other hand, there does not seem to be any practical reason to choose substantially larger than , as there is no benefit in terms of validity or interval length for increasing the number of folds above that threshold. However, keep in mind that the runtime of the -CV prediction interval increases (roughly) linearly in (cf. Remark A.5 in the supplement).

Finally, we repeated the simulations for heteroskedastic generated as

For comparability we have chosen the conditional variance of such that in order to achieve , as in the homoskedastic case. The resulting plots are very similar to those of the homoskedastic case and are deferred to Section B in the supplement. For heteroskedastic data we observe slightly larger spread of conditional probabilities around the nominal level, slightly wider intervals and slightly slower asymptotic convergence of average (unconditional) coverage to the nominal level.

Acknowledgements

The authors thank the participants of the “ISOR Research Seminar in Statistics and Econometrics” at the University of Vienna for discussion of an early version of the paper. In particular, we want to thank Benedikt M. Pötscher and David Preinerstorfer for valuable comments. We are also grateful to three anonymous referees and an associate editor for their constructive feedback to improve the paper.

References

- Aven (1985) Aven, T. (1985). Upper (lower) bounds on the mean of the maximum (minimum) of a number of random variables. J. Appl. Probab. 22(3), 723–728.

- Bai and Silverstein (2010) Bai, Z. and J. W. Silverstein (2010). Spectral Analysis of Large Dimensional Random Matrices (2nd ed.). Springer Series in Statistics. New York: Springer.

- Bai and Yin (1993) Bai, Z. D. and Y. Q. Yin (1993). Limit of the smallest eigenvalue of a large dimensional sample covariance matrix. Ann. Probab. 21(3), 1275–1294.

- Barber et al. (2021) Barber, R. F., E. J. Candes, A. Ramdas, and R. J. Tibshirani (2021). Predictive inference with the jackknife+. Ann. Statist. 49(1), 486–507.

- Bean et al. (2013) Bean, D., P. J. Bickel, N. El Karoui, and B. Yu (2013). Optimal m-estimation in high-dimensional regression. Proc. Natl. Acad. Sci. USA 110(36), 14563–14568.

- Bickel and Freedman (1983) Bickel, P. J. and D. A. Freedman (1983). Bootstrapping regression models with many parameters. In P. Bickel, K. Doksum, and J. Hodges (Eds.), A Festschrift for Erich L. Lehmann, pp. 28–48. Wadsworth Inc.

- Billingsley (1995) Billingsley, P. (1995). Probability and Measure (3rd ed.). New York: Wiley.

- Bousquet and Elisseeff (2002) Bousquet, O. and A. Elisseeff (2002). Stability and generalization. J. Mach. Learn. Res. 2, 499–526.

- Bucchianico et al. (2001) Bucchianico, A. D., J. H. J. Einmahl, and N. A. Mushkudiani (2001). Smallest nonparametric tolerance regions. Ann. Statist. 29(5), 1320–1343.

- Bühlmann and van de Geer (2011) Bühlmann, P. and S. van de Geer (2011). Statistics for High-dimensional Data. Berlin: Springer.

- Butler and Rothman (1980) Butler, R. and E. D. Rothman (1980). Predictive intervals based on reuse of the sample. J. Amer. Statist. Assoc. 75(372), 881–889.

- Chatterjee (2013) Chatterjee, S. (2013). Assumptionless consistency of the lasso. arXiv preprint arXiv:1303.5817.

- Chatterjee and Patra (1980) Chatterjee, S. K. and N. K. Patra (1980). Asymptotically minimal multivariate tolerance sets. Calcutta Statist. Assoc. Bull. 29(1-2), 73–94.

- Chen et al. (2018) Chen, W., K.-J. Chun, and R. F. Barber (2018). Discretized conformal prediction for efficient distribution-free inference. Stat 7(1), e173.

- Cox and Hinkley (1974) Cox, D. R. and D. V. Hinkley (1974). Theoretical Statistics. London: Chapman and Hall.

- Devroye and Wagner (1979) Devroye, L. and T. J. Wagner (1979). Distribution-free inequalities for the deleted and holdout error estimates. IEEE Trans. Inform. Theory 25(2), 202–207.

- Dicker (2012) Dicker, L. (2012). Optimal estimation and prediction for dense signals in high-dimensional linear models. arXiv:1203.4572.

- Dicker (2013) Dicker, L. H. (2013). Optimal equivariant prediction for high-dimensional linear models with arbitrary predictor covariance. Electron. J. Stat. 7, 1806–1834.

- El Karoui (2010) El Karoui, N. (2010). The spectrum of kernel random matrices. Ann. Statist. 38(1), 1–50.

- El Karoui (2013) El Karoui, N. (2013). Asymptotic behavior of unregularized and ridge-regularized high-dimensional robust regression estimators: rigorous results. arXiv preprint arXiv:1311.2445.

- El Karoui (2018) El Karoui, N. (2018). On the impact of predictor geometry on the performance on high-dimensional ridge-regularized generalized robust regression estimators. Probab. Theory Relat. Fields 170(1-2), 95–175.

- El Karoui et al. (2013) El Karoui, N., D. Bean, P. J. Bickel, C. Lim, and B. Yu (2013). On robust regression with high-dimensional predictors. Proc. Natl. Acad. Sci. USA 110(36), 14557–14562.

- El Karoui and Purdom (2018) El Karoui, N. and E. Purdom (2018). Can we trust the bootstrap in high-dimensions? the case of linear models. J. Mach. Learn. Res. 19(1), 170–235.

- Fahrmeir (1990) Fahrmeir, L. (1990). Maximum likelihood estimation in misspecified generalized linear models. Statistics 21(4), 487–502.

- Foygel Barber et al. (2021) Foygel Barber, R., E. J. Candes, A. Ramdas, and R. J. Tibshirani (2021). The limits of distribution-free conditional predictive inference. Information and Inference: A Journal of the IMA 10(2), 455–482.

- Friedman et al. (2010) Friedman, J., T. Hastie, and R. Tibshirani (2010). Regularization paths for generalized linear models via coordinate descent. Journal of Statistical Software 33(1), 1–22.

- Györfi et al. (2002) Györfi, L., M. Kohler, A. Krzyżak, and H. Walk (2002). A Distribution-Free Theory of Nonparametric Regression. Springer Series in Statistics. New York: Springer.

- Huber and Leeb (2013) Huber, N. and H. Leeb (2013). Shrinkage estimators for prediction out-of-sample: Conditional performance. Commun. Statist. - Theory Methods 42(7), 1246–1264.

- Huber (1967) Huber, P. J. (1967). The behavior of maximum likelihood estimates under nonstandard conditions. Proceedings of the Fifth Berkeley Symposium on Mathematical Statistics and Probability 1, 221–233.

- Krishnamoorthy and Mathew (2009) Krishnamoorthy, K. and T. Mathew (2009). Statistical Tolerance Regions: Theory, Applications, and Computation. Wiley Series in Probability and Statistics. Hoboken, New Jersey: Wiley.

- Lei (2019) Lei, J. (2019). Fast exact conformalization of the lasso using piecewise linear homotopy. Biometrika 106(4), 749–764.

- Lei et al. (2018) Lei, J., M. G’Sell, A. Rinaldo, R. J. Tibshirani, and L. Wasserman (2018). Distribution-free predictive inference for regression. J. Amer. Statist. Assoc. 113(523), 1094–1111.

- Lei et al. (2013) Lei, J., J. Robins, and L. Wasserman (2013). Distribution-free prediction sets. J. Amer. Statist. Assoc. 108(501), 278–287.

- Lei and Wasserman (2014) Lei, J. and L. Wasserman (2014). Distribution-free prediction bands for non-parametric regression. J. Roy. Statist. Soc. Ser. B 76, 71–96.

- Lewis and Thompson (1981) Lewis, T. and J. W. Thompson (1981). Dispersive distributions, and the connection between dispersivity and strong unimodality. J. Appl. Probab. 18(1), 76–90.

- Li and Liu (2008) Li, J. and R. Y. Liu (2008). Multivariate spacings based on data depth: I. construction of nonparametric multivariate tolerance regions. Ann. Statist. 36(3), 1299–1323.

- Lopes (2015) Lopes, M. E. (2015). Some Inference Problems in High-Dimensional Linear Models. Ph. D. thesis, UC Berkeley.

- Mammen (1996) Mammen, E. (1996). Empirical process of residuals for high-dimensional linear models. Ann. Statist. 24(1), 307–335.

- Massart (1990) Massart, P. (1990). The tight constant in the Dvoretzky-Kiefer-Wolfowitz inequality. Ann. Probab. 18(3), 1269–1283.

- Olive (2007) Olive, D. J. (2007). Prediction intervals for regression models. Comput. Statist. Data Anal. 51(6), 3115–3122.

- Politis (2013) Politis, D. N. (2013). Model-free model-fitting and predictive distributions. Test 22(2), 183–221.

- Romano et al. (2019) Romano, Y., E. Patterson, and E. Candes (2019). Conformalized quantile regression. Adv. Neural Inf. Process. Syst. 32.

- Schmidt-Hieber (2020) Schmidt-Hieber, J. (2020). Nonparametric regression using deep neural networks with relu activation function. Ann. Statist. 48(4), 1875–1897.

- Schmoyer (1992) Schmoyer, R. L. (1992). Asymptotically valid prediction intervals for linear models. Technometrics 34(4), 399–408.

- Scornet et al. (2015) Scornet, E., G. Biau, and J.-P. Vert (2015). Consistency of random forests. Ann. Statist. 43(4), 1716–1741.

- Steinberger and Leeb (2016) Steinberger, L. and H. Leeb (2016). Leave-one-out prediction intervals in linear regression models with many variables. arXiv preprint arXiv:1602.05801.

- Steinberger and Leeb (2021) Steinberger, L. and H. Leeb (2021). Conditional predictive inference for high-dimensional stable algorithms. arXiv preprint arXiv:1809.01412.

- Steinberger and Leeb (2022) Steinberger, L. and H. Leeb (2022). Supplement to “Conditional predictive inference for stable algorithms”.

- Stine (1985) Stine, R. A. (1985). Bootstrap prediction intervals for regression. J. Amer. Statist. Assoc. 80(392), 1026–1031.

- Tukey (1947) Tukey, J. W. (1947). Non-parametric estimation ii. statistically equivalent blocks and tolerance regions – the continuous case. Ann. Math. Statist. 18(4), 529–539.

- van der Vaart (2007) van der Vaart, A. W. (2007). Asymptotic Statistics (8th ed.). Cambridge Series in Statistical and Probabilistic Mathematics. New York: Cambridge University Press.

- Vovk (2012) Vovk, V. (2012). Conditional validity of inductive conformal predictors. In Asian conference on machine learning, pp. 475–490.

- Vovk (2013) Vovk, V. (2013). Conditional validity of inductive conformal predictors. Machine Learning 92(2), 349–376.

- Vovk et al. (1999) Vovk, V., A. Gammerman, and C. Saunders (1999). Machine-learning applications of algorithmic randomness. In I. Bratko and S. Dzeroski (Eds.), Proceedings of the Sixteenth International Conference on Machine Learning, ICML ’99, pp. 444–453. Morgan Kaufmann Publishers Inc.

- Vovk et al. (2005) Vovk, V., A. Gammerman, and G. Shafer (2005). Algorithmic Learning in a Random World. New York: Springer.

- Vovk et al. (2009) Vovk, V., I. Nouretdinov, and A. Gammerman (2009). On-line predictive linear regression. Ann. Statist. 37(3), 1566–1590.

- Wald (1943) Wald, A. (1943). An extension of Wilks’ method for setting tolerance limits. Ann. Math. Statist. 14(1), 45–55.

- White (1980a) White, H. (1980a). A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity. Econometrica 48(4), 817–838.

- White (1980b) White, H. (1980b). Using least squares to approximate unknown regression functions. Internat. Econom. Rev. 21(1), 149–170.

- Wilks (1941) Wilks, S. S. (1941). Determination of sample sizes for setting tolerance limits. Ann. Math. Statist. 12(1), 91–96.

- Wilks (1942) Wilks, S. S. (1942). Statistical prediction with special reference to the problem of tolerance limits. Ann. Math. Statist. 13(4), 400–409.

Appendix A Discussion and further remarks

In this section we collect several further thoughts on the -CV prediction intervals. We discuss some properties of the proposed method that we have established above but which we believe hold in much higher generality. We also draw some further connections to other methods such as sample splitting, tolerance regions and prediction regions based on non-parametric density estimation, and we provide further intuition. Finally, we sketch possible extensions and open problems.

A.1 Predictor efficiency and interval length

Recall that if and are such that

is continuous, the optimal infeasible interval

in (2.2) is the shortest interval of the form such that (2.3) and (2.4) are satisfied. In this infeasible scenario and for given error probabilities , the only way in which the data analyst can influence the length of is via the choice of predictor . This choice clearly affects the conditional distribution of the prediction error and, thus, potentially its inter-quantile-range , which is the length of the infeasible prediction interval. Since we only care about minimizing the inter-quantile-range of the conditional distribution , for the rest of this subsection we consider the training data to be fixed and non-random. Thus, the predictor is also non-random. Now we would like to use a predictor such that the prediction error has short inter-quantile-range. For simplicity, assume that , where the error term has mean zero and is independent of the features . Therefore, the prediction error is given by

i.e., the sum of the estimation error and the innovation . Following Lewis and Thompson (1981), we say that a continuous univariate distribution is more dispersed than if, and only if, any two quantiles of are further apart than the corresponding quantiles of . Now we note that minimizing the inter-quantile-range of the prediction error is, in general, not equivalent to minimizing the inter-quantile-range of , because of the effect of the error term . However, if the distribution of the error term has a log-concave density, then the distribution of is more dispersed than that of , if, and only if, is more dispersed than (see Theorem 8 of Lewis and Thompson, 1981). Thus, under log-concave error distributions, the interval length of is directly related to the prediction accuracy of the point predictor in use. These considerations naturally carry over to the feasible analog defined in (2.6). In Subsection 3.3, in the special case of a linear model and ordinary-least-squares prediction, we have discussed the issue of interval length in some more detail and provided a rigorous description of the asymptotic interval length in a high-dimensional regime. This sheds more light on the connection between the length of and the estimation error . However, the lessons learned from the linear model appear to be valid in a much more general situation. In particular, we see that, at least for log-concave error distributions, the lengths of -CV prediction intervals can potentially be used to evaluate the relative efficiency of competing predictors.

A.2 The case of a naive predictor and sample splitting

Next, we discuss the important special case where we naively decide to work with a predictor , , that does not depend on the training data at all.444Note that this covers, in particular, the case where we do not even use, or do not have available, the feature vectors , i.e., . In this case, a prediction interval for that is only based on is more commonly referred to as a tolerance interval. In this case, the predictor and its -fold CV analogs all coincide and the (-CV) residuals for , are actually independent and identically distributed according to the non-random distribution and is their empirical distribution function. Therefore, by Proposition 2.1 and the Dvoretzky-Kiefer-Wolfowitz (DKW) inequality (Massart, 1990), if is continuous, we get for every that

Integrating this tail probability also yields

We also point out that in the present case where the predictor does not depend on , the problem of constructing a prediction interval for can actually be reduced to finding a non-parametric univariate tolerance interval for based on the i.i.d. copies . For this problem classical solutions are available, based on the theory of order statistics of i.i.d. data (cf. Krishnamoorthy and Mathew, 2009, Chapter 8). Unfortunately, the problem changes dramatically, once we try to learn the true regression function from the training data and use to predict , because then the -CV residuals are no longer independent and the conditional distribution function of the prediction error given is random. Thus, in the general case we can not expect to obtain equally powerful and elegant results as above and we can not resort to the theory of order statistics of i.i.d. data. In particular, we note that the bound of Theorem 2.6 is still somewhat sub-optimal in this trivial case where the estimator does not depend on the training sample . In that case, , but the derived bound still depends on the distribution of the estimation error , even though in that case the alternative bound obtained above by the DKW inequality does no longer involve the estimation error. It is an open problem to establish a concentration inequality for analogous to the DKW inequality but in the general case of dependent -CV residuals and random .

The discussion of the previous paragraph also applies to the case where the predictor was obtained as an estimator for , but from another independent training sample of i.i.d. copies of . This situation can be seen as a sample splitting method, where of the overall observations are used to compute the point predictor and the remaining observations in are used as a validation set to estimate the conditional distribution of the prediction error given (and ), from the (conditionally on ) i.i.d. residuals , . Such a procedure is discussed, for instance, by Lei et al. (2018) and Vovk (2012). Note that under the assumptions of the previous paragraph, such a method is asymptotically training conditionally valid if the size of the validation set diverges to infinity. However, this method uses only of the available observation pairs for prediction, such that the point predictor based on is not as efficient as the analogous predictor based on the full sample . This typically results in a larger prediction interval than necessary, because then the conditional distribution of the prediction error is usually more dispersed than that of . See also the discussion in Subsections 3.4 and A.1.

A.3 Further remarks

Remark A.1 (On exact training conditional validity).

Suppose that the class contains at least the data generating distributions and , where for

that is, the feature variables in and the response are i.i.d. . Further, suppose that we decide to predict by some linear predictor for some estimator . We shall show that for every , it is impossible to construct a prediction interval of the form based on a finite sample and , such that (2.1) is equal to zero.

Proof.

If (2.1) is equal to zero, then for both and -almost all samples , where is the -fold product measure of ,

Since , we must have , almost surely, and it is easy to see that the function

is continuous and strictly decreasing, provided that , and thus, for such and , is invertible. Therefore, for and for -almost all samples (equivalently, for Lebesgue almost all ), we have

In other words, there exists , such that , a contradiction. ∎

Remark A.2.

Consistent estimation of the true regression function from an i.i.d. sample of size is usually not possible if the dimension of is non-negligible compared to , even if is very regular and the error is homoskedastic and has rapidly decaying tails. For example, in a Gaussian linear model where the only unknown parameter is the -vector of regression coefficients, it is impossible to consistently estimate the conditional mean , unless or strong assumptions are imposed on the parameter space (cf. Dicker, 2012).

Remark A.3.

A natural approach for constructing non-parametric prediction sets is to estimate the conditional density of given (if it exists), because, as can be easily shown, a highest density region of the conditional density of given provides the smallest (in terms of Lebesgue measure) prediction region for that controls the conditional coverage probability given , i.e., that satisfies

| (A.1) |