Robust estimations for the tail index of Weibull-type distribution111Financial support from the National Natural Science Foundation of China grant (11604375), and Chinese Government Scholarship (201708505031), are gratefully acknowledged.

Abstract

Based on suitable left-truncated or censored data, two flexible classes of -estimations of Weibull tail coefficient are proposed with two additional parameters bounding the impact of extreme contamination. Asymptotic normality with -rate of convergence is obtained. Its robustness is discussed via its asymptotic relative efficiency and influence function. It is further demonstrated by a small scale of simulations and an empirical study on CRIX.

Keywords: robust; Weibull tail coefficient; influence function; asymptotic relative efficiency; CRIX

JEL Classification: C13, G10, G31

Mathematics Subject Classification (2010): 60G70, 62G32, 91B28

1 Introduction

The estimation of tail quantities plays an important role in extreme value statistics. One challenging problem is to select extreme sample fraction to balance the asymptotic variance and bias. Meanwhile, this requires a large and ideal sample from the underlying distribution. Indeed, in practical data analysis, it is not unusual to encounter outliers or mis-specifications of the underlying model which may have a considerable impact on the estimation results. A typical treatment is then required for instance by down-weighting its influence on the estimation in various standards, see e.g., Basu et al. (1998), Beran and Schell (2012), Vandewalle et al. (2004, 2007), Goegebeur et al. (2015); Liu and Tang (2010).

Given the wide applications of Weibull-type distributions and little studies on its robust estimations, this paper shall address this issue concerning its tail quantities. Let be an independent and identically distributed sequence from parent satisfying

| (1.1) |

where is the so-called Weibull tail coefficient (WTC) and is a slowly varying function at infinity, i.e., (cf. Bingham et al. (1987))

Prominent instances of Weibull-type distributions of are Gaussian (), gamma, Logistic and exponential () and extended Weibull (any ) distributions (cf. Gardes and Girard (2008)). As an important subgroup of light-tailed distributions, Weibull-type distributions are of great use in hydrology, meteorology, environmental and actuarial science, to name but a few (cf. Beirlant and Teugels (1992); Hashorva and Weng (2014); Dȩbicki and Hashorva (2018); Arendarczyk and Dȩbicki (2011)). Meanwhile, the WTC governs the tail behavior of , and the larger the WTC is, the faster the tail of decays. Dedicated estimations of WTC have thus been proposed and most of them are based on an asymptotically vanishing sample fraction of high quantiles, which asymptotic normality is achieved under certain second-order condition specifying the rate of convergence of to 1, see e.g., Girard (2004), Gardes and Girard (2008), Goegebeur et al. (2010), Asimit et al. (2010). Indeed, most data-sets from applied-oriented fields are relative large and with certain deviations from the pre-supposed model. For instance, it occurs with the slowly varying function (where ) in the left part of the distributions. To the best of our knowledge, it is new to investigate the robust Weibull tail estimations when only a small sample is available.

Inspired by the theory of robust inference in Huber (1964), we propose two classes of robust estimations of WTC. Denote for given

| (1.2) |

Clearly, we have is the score function of

| (1.3) |

Please note that is not monotone and thus one cannot directly weaken the effect of outliers by bounding score function . On the other hand, most interest of risk management lies principally in the extreme large risks. This motivates us to consider some tailored according to certain left-truncated/censored Weibull distributions with the same Weibull tail coefficient under considerations. Namely, we set below with specified by (1.2) and

| (1.4) |

which properties are stated as below.

Lemma 1.1.

Let and . Then is strictly increasing, and is the score function of . Moreover, is strictly increasing provided that .

Basically, both and are certain modifications of via its valued interval and domain region. Now, we are ready to state our -estimations of Weibull tail coefficient using the -estimation process based on the alternative samples ’s and ’s respectively from and where ’s is a random sample from . Set below and is a set of distributions with support in .

Definition 1.1.

Let and be given by (1.3) and (1.4), respectively. Define the psi-function as

| (1.5) | |||||

Then the functional as the solution of the equation

is called huberized Weibull tail -functional corresponding to . The corresponding -estimator , the solution of the equation

is the huberized Weibull tail -estimator of . If further , then define the psi-function with and

| (1.6) | |||||

Then the functional as the solution of the equation

is called huberized Weibull tail -functional corresponding to . The corresponding -estimator , the solution of the equation

is the huberized -estimator of the Weibull tail coefficient .

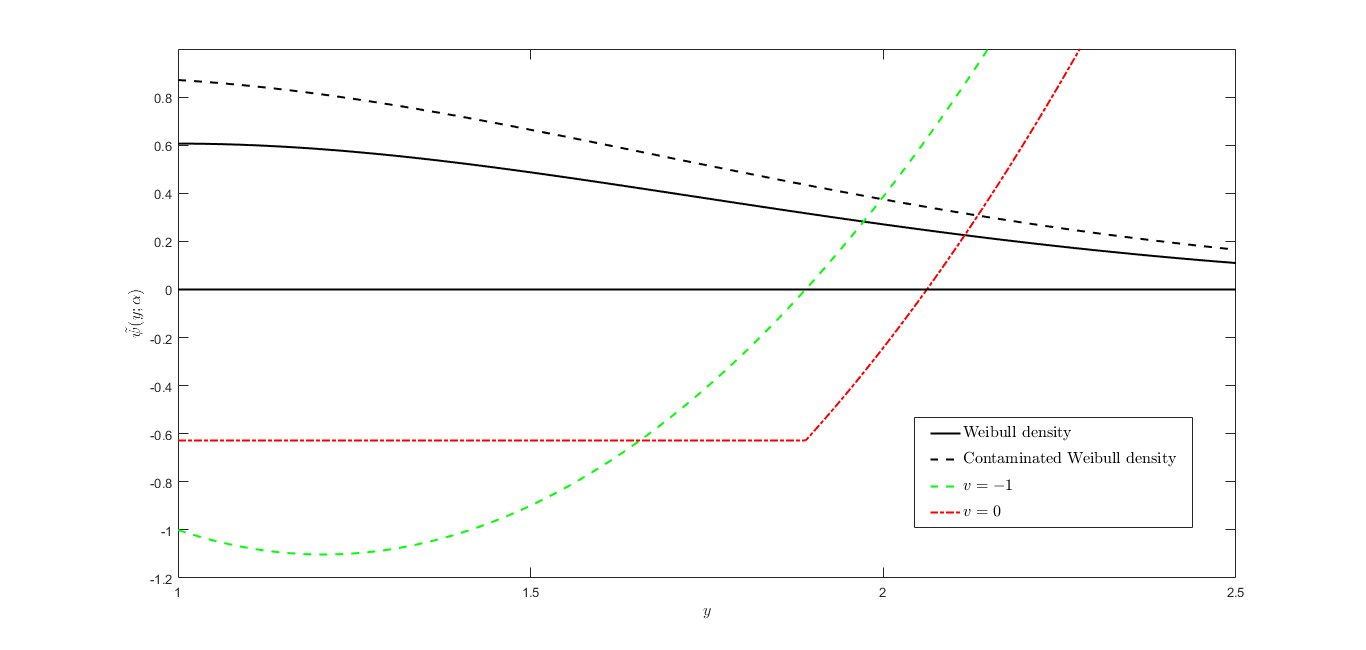

Figure 1 illustrates the lower huberization by comparing the score function of (recall Lemma 1.1) with . We see that the contaminated Weibull density by Gamma (see (3.1) below for its definition) has almost the same shape as the pre-supposed Weibull one in the right tail, and therefore lower-huberized psi-function can restrict the influence of all observations below instead of removing them completely. On the other hand, for all , the is shifted downwards for the consistency purpose. One may similarly analyze the function.

The paper principally investigates the asymptotic behavior of the proposed new classes of -estimations of Weibull tail coefficient. Details are as follows.

In Section 2, we consider Weibull distributions in Theorems 2.1 and 2.2 and establish its asymptotic normality of the -estimations and with -rate of convergence, which is rather faster than that of most classical Weibull tail estimations such as the Hill-type estimation, see Theorem 2 in Girard (2004). Generally, we study related asymptotic properties in Theorems 2.3 and 2.4 when the underlying risk follows Weibull-type distributions specified in (1.1). Some bounded asymptotic bias may appear due to its deviations from the Weibull distributions.

In Section 3, using asymptotically relative efficiency (AEFF) and influence function (IF), we investigate the robustness (Theorem 3.1) and the bias, which are further related to the choices of flexible parameters and . These results are useful, especially when the practical regulators in risk management consider the trade-off between the robustness and consistency.

In Section 4, a small scale of Monte Carlo simulations and an empirical study concerning the CRIX proposed by Trimborn and Härdle (2016) are carried out. We see that both -estimations are robust and perform very well even for small samples, in comparisons with the classical maximum likelihood estimations and Hill-type estimations of the Weibull tail coefficient. We expect the results would be beneficial to both financial practitioners and theoretical experts in risk management and extreme value statistics.

The rest of the paper is organized as follows. Main results are given in Section 2 followed with a section dedicated to the robust analysis. Sections 4 and 5 are devoted to a small scale of Monte Carlo simulations and an empirical studies on CRIX. All proofs of the results are postulated to Section 6.

2 Asymptotic results

Throughout this section, we keep the same notation as in Introduction and write further and for the convergence in probability and in distribution, respectively. All the limits are taken as unless otherwise stated.

Theorem 2.1.

Let be a random sample from . Denote by , and by the solution of

Then and

| (2.1) |

where, with

Remark 2.1.

Theorem 2.2.

Let be a random sample from and . Denote by with , and by the solution of

Then and

where, with

Remark 2.2.

(i) The difference between and is that is not the score function of , the distribution of the censored risk at point , where is needed to ensure the monotonicity of and , see details in (6) with .

(ii) The proposed -estimations are principally based on suitable left-truncated and censored data, which are commonly used in survival analysis, see e.g., Kundu et al. (2017). Moreover, both consistency and robustness are obtained since we bound the psi-functions to weaken the influence of the extreme outliers for the exact Weibull models.

In what follows, we consider generally the Weibull-type risks and investigate asymptotic properties of the proposed -estimations.

Theorem 2.3.

Let be a random sample from . Suppose that there is a unique solution of Then , the solution of

converges in probability to . If further and hold in a neighbourhood of , then

| (2.2) |

where

Theorem 2.4.

Let be a random sample from and . Suppose that there is a unique solution of Then , the solution of

converges in probability to . If further and hold in a neighbourhood of , then

| (2.3) |

where

3 Robustness

A simple criterion for choosing and in the -estimations is the trade-off between the efficiency loss (that one is willing to put up with when data are generated by a Weibull distribution), and its asymptotic bias (when the underlying distribution deviates from the ideal Weibull distribution). We study below the relative asymptotic efficiency (AEFF) in Theorem 3.1, and then analyze its influence function. Both quantities are some functions of the flexible parameters and , which enable the risk regulators to balance the robustness and consistency.

As stated in Remark 2.1, the -estimation with reduces to the maximum likelihood estimation of . Therefore, a straightforward application of Theorems 2.1 and 2.2 leads to the following theorem.

Theorem 3.1.

Figure 2 illustrates the effect of on the relative asymptotic efficiency of and (compared to the MLE ). For smaller , the relative asymptotic effective loss of is rather smaller than that of . While for larger , both are asymptotically the same.

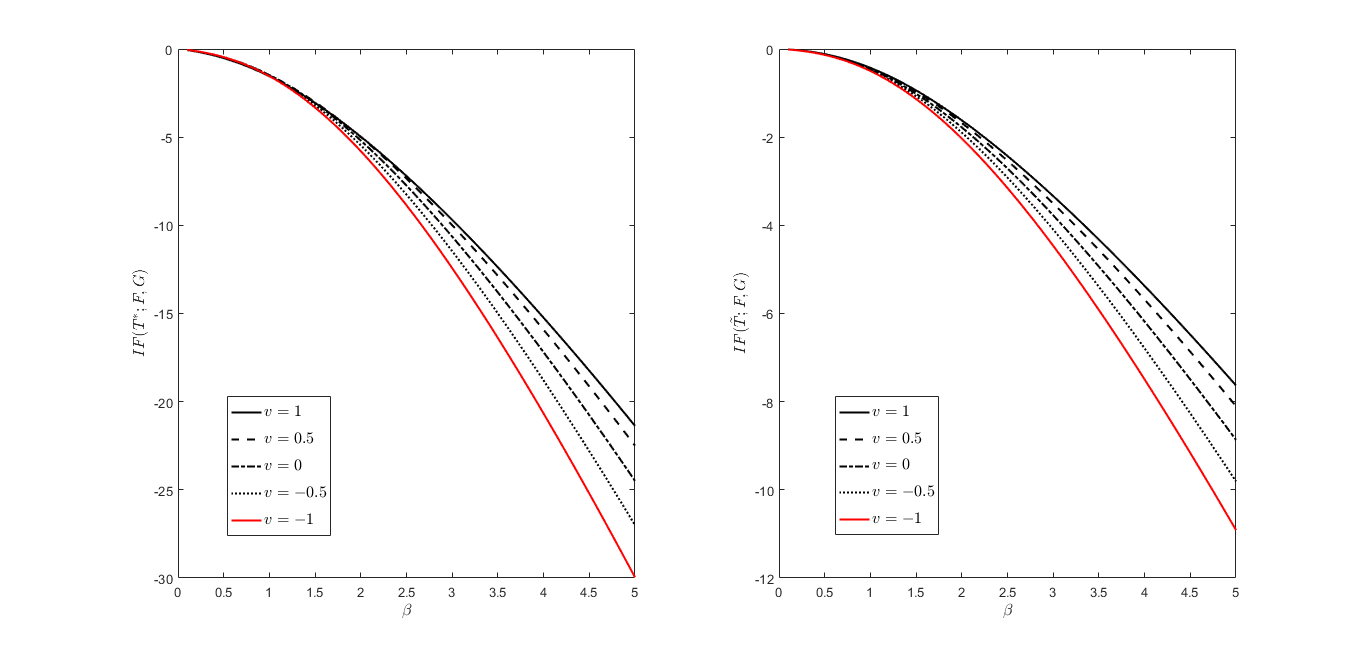

The influence function approach, known also as the “infinitesimal approach”, is generally employed to quantify robustness. Recall that the influence function describes the effect of some functional for in an infinitesimal -contamination neighbourhood , is defined by

We have

In Figure 3, we take with scale parameter and shape parameter , which is a Weibull-type distribution with . Its density function is given by

| (3.1) |

We see that, the absolute values of the influence functions of both -estimations and are increasing in , and decreasing with . In other words, with increasing huberization and light-tail contamination, one gets the reduction of sensitivity to deviations from the Weibull model.

4 Simulations

In this section, we carry out a simulation study to illustrate the small sample behavior of -estimations and compared to the maximum likelihood estimation and the classical Hill-type estimation of the Weibull tail coefficient given by (cf. Girard (2004))

| (4.1) |

To analyze the robustness of the -estimations, we generate samples of size and 100 from Weibull distribution contaminated by Gamma distribution with contamination level , i.e., the underlying risk follows

In the simulations, we take and . Table 1 lists the average estimations , the sample variance and the ratio of mean squared error (MSE) of MLE, Hill-type estimation to that of and with , i.e., is given by

| (4.2) |

Here, we use alternatively given by (since the traditional optimal choice of in Girard (2004) is not available for small samples)

The last column of Table 1 is the relative proportion of for which , denoted by , is given by

The describes the percent that the Hill-type estimation outperforms the estimation .

| * | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (0.3, 1, 1) | 30 | 0.9217 | 0.8255 | 1.0006 | 1.0005 | 0.0072 | 0.0451 | 0.0018 | 0.0015 | 68.6811 | 8.7774 | 8.3678 | 0.00 |

| 50 | 0.8609 | 0.8435 | 1.0022 | 1.0061 | 0.0068 | 0.0289 | 0.0014 | 0.0015 | 23.1288 | 14.3407 | 13.4344 | 0.00 | |

| 80 | 0.8274 | 0.8326 | 1.0083 | 1.0075 | 0.0041 | 0.0176 | 0.0013 | 0.0016 | 9.7485 | 19.5972 | 19.2393 | 0.00 | |

| 100 | 0.8161 | 0.8368 | 1.0147 | 1.0119 | 0.0030 | 0.0148 | 0.0018 | 0.0015 | 6.2607 | 20.8143 | 20.0842 | 0.00 | |

| (0.1, 1, 1) | 30 | 0.9885 | 0.9343 | 0.9942 | 0.9940 | 0.0007 | 0.0469 | 0.0007 | 0.0006 | 5.7287 | 1.2283 | 1.0561 | 0.00 |

| 50 | 0.9834 | 0.9252 | 0.9949 | 0.9952 | 0.0009 | 0.0269 | 0.0007 | 0.0006 | 3.6407 | 1.8194 | 1.8000 | 0.00 | |

| 80 | 0.9776 | 0.9407 | 0.9962 | 0.9953 | 0.0009 | 0.0189 | 0.0005 | 0.0006 | 1.0006 | 2.5849 | 2.3829 | 0.00 | |

| 100 | 0.9735 | 0.9302 | 0.9964 | 0.9961 | 0.0010 | 0.0130 | 0.0005 | 0.0005 | 0.7138 | 3.2549 | 2.9623 | 0.15 | |

| (0.3, 1, 2) | 30 | 1.2382 | 1.6039 | 1.9960 | 1.9919 | 0.0687 | 0.2408 | 0.0056 | 0.0050 | 74.7362 | 147.2932 | 126.8653 | 0.00 |

| 50 | 1.1347 | 1.6443 | 2.0015 | 1.9963 | 0.0268 | 0.1576 | 0.0045 | 0.0042 | 22.7834 | 158.1670 | 165.1127 | 0.00 | |

| 80 | 1.0851 | 1.6853 | 2.0050 | 2.0039 | 0.0127 | 0.1219 | 0.0039 | 0.0038 | 7.8035 | 197.7217 | 180.3746 | 0.00 | |

| 100 | 1.0731 | 1.6709 | 2.0081 | 2.0073 | 0.0085 | 0.0883 | 0.0042 | 0.0038 | 5.1102 | 223.2889 | 186.3996 | 0.00 | |

| (0.1, 1, 2) | 30 | 1.9245 | 1.8399 | 1.9903 | 1.9859 | 0.0169 | 0.2025 | 0.0026 | 0.0024 | 4.8833 | 9.3566 | 8.4148 | 0.00 |

| 50 | 1.8459 | 1.8506 | 1.9900 | 1.9888 | 0.0239 | 0.1223 | 0.0022 | 0.0021 | 3.1233 | 21.4576 | 18.4649 | 0.00 | |

| 80 | 1.7654 | 1.8392 | 1.9873 | 1.9895 | 0.0228 | 0.0754 | 0.0017 | 0.0017 | 3.0758 | 39.6547 | 35.4584 | 0.00 | |

| 100 | 1.7249 | 1.8681 | 1.9898 | 1.9906 | 0.0190 | 0.0660 | 0.0018 | 0.0018 | 1.9142 | 43.1656 | 45.1557 | 0.00 | |

| (0.3, 2, 1) | 30 | 0.9466 | 0.8640 | 0.9974 | 0.9987 | 0.0047 | 0.0429 | 0.0016 | 0.0021 | 82.5558 | 4.6014 | 3.5335 | 0.00 |

| 50 | 0.9061 | 0.8881 | 0.9955 | 0.9965 | 0.0051 | 0.0298 | 0.0015 | 0.0013 | 22.7834 | 12.7013 | 10.1286 | 0.00 | |

| 80 | 0.8729 | 0.8848 | 0.9944 | 0.9955 | 0.0036 | 0.0172 | 0.0012 | 0.0010 | 3.2990 | 16.1109 | 16.0286 | 0.00 | |

| 100 | 0.8562 | 0.8938 | 0.9970 | 0.9978 | 0.0029 | 0.0152 | 0.0011 | 0.0011 | 1.7146 | 19.8407 | 18.1323 | 0.00 | |

| (0.1, 2, 1) | 30 | 0.9880 | 0.9223 | 0.9953 | 0.9956 | 0.0005 | 0.2773 | 0.0483 | 0.0011 | 5.1904 | 0.8848 | 0.7232 | 0.00 |

| 50 | 0.9852 | 0.9557 | 0.9941 | 0.9952 | 0.0007 | 0.1438 | 0.0261 | 0.0006 | 3.4681 | 1.2380 | 1.1071 | 0.00 | |

| 80 | 0.9808 | 0.9452 | 0.9940 | 0.9942 | 0.0008 | 0.1775 | 0.0165 | 0.0005 | 0.9524 | 2.0353 | 1.6522 | 0.10 | |

| 100 | 0.9762 | 0.9560 | 0.9927 | 0.9939 | 0.0009 | 0.0444 | 0.0148 | 0.0006 | 0.8589 | 2.3773 | 2.2494 | 0.12 | |

| (0.3, 2, 2) | 30 | 1.3019 | 1.6018 | 1.9855 | 1.9853 | 0.0583 | 0.2434 | 0.0030 | 0.0026 | 85.6893 | 153.3920 | 159.4866 | 0.00 |

| 50 | 1.2012 | 1.6589 | 1.9850 | 1.9850 | 0.0228 | 0.1209 | 0.0024 | 0.0021 | 14.7957 | 260.7202 | 270.0256 | 0.00 | |

| 80 | 1.1570 | 1.6701 | 1.9844 | 1.9838 | 0.0099 | 1.1006 | 0.0018 | 0.0017 | 2.5650 | 348.1278 | 345.6587 | 0.00 | |

| 100 | 1.1484 | 1.6771 | 1.9832 | 1.9830 | 0.0069 | 0.0712 | 0.0017 | 0.0017 | 1.4158 | 386.5744 | 370.8852 | 0.00 | |

| (0.1, 2, 2) | 30 | 1.9238 | 1.8054 | 1.9885 | 1.9870 | 0.0161 | 0.1763 | 0.0027 | 0.0032 | 4.3161 | 5.8439 | 6.3442 | 0.00 |

| 50 | 1.8519 | 1.8637 | 1.9886 | 1.9850 | 0.0212 | 0.1201 | 0.0031 | 0.0023 | 3.9388 | 17.6548 | 16.9291 | 0.00 | |

| 80 | 1.7646 | 1.8565 | 1.9869 | 1.9849 | 0.0200 | 0.0696 | 0.0017 | 0.0019 | 1.2588 | 37.7912 | 36.6744 | 0.00 | |

| 100 | 1.7402 | 1.8839 | 1.9849 | 1.9843 | 0.0181 | 0.0756 | 0.0017 | 0.0017 | 0.9791 | 47.8601 | 44.6477 | 0.05 | |

| (0.3, 0.5, 1) | 30 | 0.9320 | 0.7989 | 1.0056 | 1.0065 | 0.0048 | 0.0565 | 0.0012 | 0.0014 | 7.2497 | 7.7231 | 6.7977 | 0.00 |

| 50 | 0.8912 | 0.8250 | 1.0116 | 1.0096 | 0.0051 | 0.0468 | 0.0012 | 0.0013 | 8.8465 | 12.2309 | 10.2765 | 0.00 | |

| 80 | 0.8565 | 0.8130 | 1.0185 | 1.0188 | 0.0034 | 0.0261 | 0.0013 | 0.0012 | 2.8355 | 15.4294 | 14.8902 | 0.00 | |

| 100 | 0.8463 | 0.8368 | 1.0218 | 1.0232 | 0.0024 | 0.0252 | 0.0011 | 0.0012 | 1.3175 | 17.0045 | 16.5285 | 0.00 | |

| (0.1, 0.5, 1) | 30 | 0.9874 | 0.8848 | 0.9968 | 0.9943 | 0.0005 | 0.0428 | 0.0006 | 0.0006 | 5.3788 | 1.2157 | 1.0236 | 0.00 |

| 50 | 0.9853 | 0.9136 | 0.9972 | 0.9952 | 0.0005 | 0.0295 | 0.0005 | 0.0005 | 3.8457 | 1.5111 | 1.4974 | 0.00 | |

| 80 | 0.9799 | 0.9193 | 0.9977 | 0.9975 | 0.0006 | 0.0181 | 0.0004 | 0.0005 | 1.9436 | 2.3528 | 1.9708 | 0.00 | |

| 100 | 0.9783 | 0.9165 | 0.9991 | 0.9989 | 0.0006 | 0.0143 | 0.0005 | 0.0004 | 0.9241 | 2.2865 | 2.1840 | 0.10 | |

| (0.3, 0.5, 2) | 30 | 1.3277 | 1.5964 | 2.0065 | 1.8144 | 0.0713 | 0.2504 | 0.0052 | 0.0004 | 61.5168 | 111.5918 | 15.1011 | 0.00 |

| 50 | 1.2141 | 1.6243 | 2.0185 | 1.8083 | 0.0373 | 0.1607 | 0.0049 | 0.0003 | 31.3754 | 129.6489 | 17.7850 | 0.00 | |

| 80 | 1.1618 | 1.6596 | 2.0357 | 1.8042 | 0.0147 | 0.1047 | 0.0046 | 0.0002 | 13.2211 | 128.0530 | 18.8915 | 0.00 | |

| 100 | 1.1486 | 1.6707 | 2.0386 | 1.8035 | 0.0125 | 0.0974 | 0.0047 | 0.0002 | 4.5564 | 118.1708 | 19.1617 | 0.00 | |

| (0.1, 0.5, 2) | 30 | 1.9443 | 1.8589 | 1.9900 | 1.8040 | 0.0093 | 0.2091 | 0.0020 | 0.0005 | 8.5329 | 6.7537 | 0.3454 | 0.00 |

| 50 | 1.8936 | 1.8745 | 1.9935 | 1.7963 | 0.1316 | 0.6520 | 0.0020 | 0.0003 | 4.9060 | 12.6372 | 0.5832 | 0.00 | |

| 80 | 1.8329 | 1.8271 | 1.9958 | 1.7937 | 0.0720 | 0.6408 | 0.0018 | 0.0002 | 1.3524 | 22.1326 | 0.9232 | 0.00 | |

| 100 | 1.8125 | 1.8538 | 2.0024 | 1.7930 | 0.0670 | 2.8163 | 0.0017 | 0.0002 | 0.9561 | 26.7188 | 1.0363 | 0.08 |

We conclude from Table 1 that

(i) The bias of the proposed -estimations is smaller than that of Hill-type estimation and MLE estimation (see columns 2–5 for details).

(ii) The sample variance of our estimations is very close to zero. Note by passing that even with the optimal choice of , the of Hill-type estimations is still relatively larger than the other (see columns 6–9 for details).

(iii) Since the ratios of MSE satisfy , we see that the best rank estimation is , which coincides with the analysis of the relative efficiency (see columns 10–12 and Figure 2).

(iiii) outperforms Hill-type estimators for almost all ’s. For , does not exceed in most cases which means that there is a set with at most = 8 of such that the Hill-type estimators would outperform . Similar argument holds for . Hence, the -estimations perform better even for small samples.

5 Empirical Study

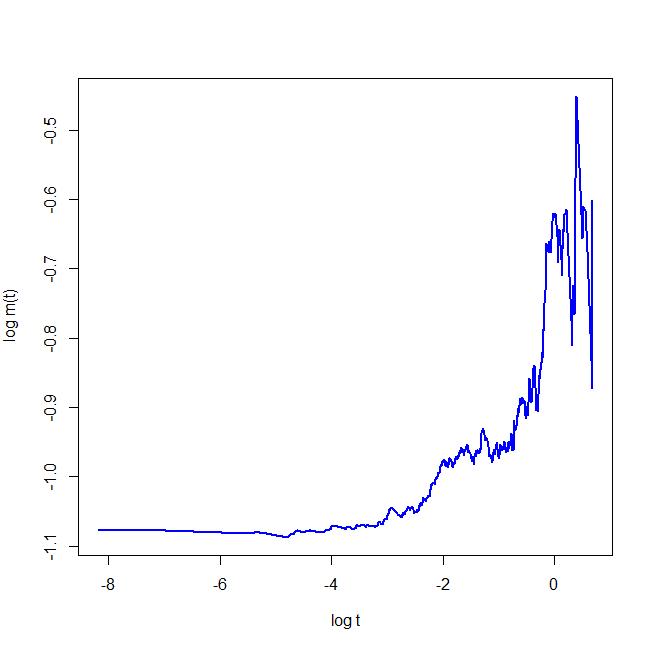

The CRIX, a market index (benchmark), is designed by Trimborn and Härdle (2016). It enables each interested party to study the performance of the crypto market as a whole or single crypto market, and therefore attracts increasing attention of risk managers and regulators. We select the daily CRIX index during 31 July 2014–1 January 2018 (available on crix.berlin) and take all positive log returns of CRIX multiplied by 15 to obtain a moderate amount of sample of size around 35–50 greater than 1 for the -estimation (recall scaled risks keep the same tail decay feature) as the original data sequence .

In Figure 4 we employ the empirical mean excess function from extreme value theory to analyze its tail feature (set below as the indicator function)

where ’s are the scaled daily log returns of CRIX. We see that the log mean excess function behaves linearly for large threshold, indicating the Weibull tail feature of the data-set (cf. Dierckx et al. (2009)).

Therefore, we illustrate the robustness of the proposed -estimations and with as the confidence interval via MLE, and using the real data-set and compare it with the Hill-type estimations given by (4.1). Specifically, we consider the same contamination distribution and contamination level , . Besides, the sample fraction involved in the Hill-type estimations, is chosen via the bootstrap and maximum likelihood method as follows.

| (5.1) |

where is the average of Hill-type estimations based on bootstrap samples, and is the maximum likelihood estimation of the shape parameter of Weibull distribution (see (1.1) for its definition). Due to the unknown Weibull tail coefficient , we use alternatively the relative deviation of at contamination level to , denoted by to study the relative robustness. Specifically,

| (5.2) |

where and stand for the -estimations and Hill-type estimations with optimal choice of as in (5.1), accordingly.

From Table 2, we draw the following conclusions: (i) As expected, the proposed -estimations are not sensitive to the contaminations, since the relative deviations of -estimations are almost zero. Conversely, both Hill-type estimations with optimal choices of sample fraction have obvious deviations from no contamination to small contamination ( for ). (ii) The Hill-type estimation , with average value around 0.67, underestimates the to some extent since the averages of the other three estimations are closer to 0.80.

| 0.00 | 0.7711 | 0.7932 | 0.9202 | 0.9359 | 0.0072 | 0.0055 | 0.1277 | 0.2601 |

| 0.05 | 0.7783 | 0.7987 | 0.7925 | 0.6758 | 0.0056 | 0.0060 | 0.0084 | 0.0246 |

| 0.10 | 0.7839 | 0.8047 | 0.8009 | 0.6512 | 0.0002 | 0.0005 | 0.0038 | 0.0028 |

| 0.15 | 0.7841 | 0.8052 | 0.8047 | 0.6484 | 0.0026 | 0.0144 | 0.0258 | 0.0172 |

| 0.20 | 0.7867 | 0.8196 | 0.8305 | 0.6312 | 0.0093 | 0.0117 | 0.0560 | 0.0094 |

| 0.25 | 0.7960 | 0.8313 | 0.7745 | 0.6406 | 0.0046 | 0.0186 | 0.0168 | 0.0075 |

| 0.30 | 0.8006 | 0.8499 | 0.7577 | 0.6331 | 0.0046 | 0.0092 | 0.0038 | 0.0089 |

| 0.35 | 0.7960 | 0.8407 | 0.7539 | 0.6420 | 0.0120 | 0.0084 | 0.0168 | 0.0049 |

| 0.40 | 0.8080 | 0.8491 | 0.7707 | 0.6371 | 0.0008 | 0.0096 | 0.0370 | 0.0029 |

| 0.45 | 0.8072 | 0.8587 | 0.7337 | 0.6400 | 0.0069 | 0.0052 | 0.0208 | 0.0096 |

| 0.50 | 0.8003 | 0.8639 | 0.7545 | 0.6304 | - | - | - | - |

6 Proofs

Proof of Lemma 1.1.

Firstly, we show that is strictly increasing. Indeed, is twice differentiable and

| (6.1) |

which imply that is a convex function with a unique minimum where . Therefore, we have exists and the unique solution and thus is strictly increasing. Noting further for given that is strictly decreasing in , we have is strictly increasing in with since .

Secondly, note that . It follows by some elementary calculations that is the score function of . Moreover, in view of (6.1), the minimizer of is decreasing in . This together with the fact that implies that is strictly increasing. ∎

Proof of Theorem 2.1.

It follows by (1.5) that is strictly increasing and continuous in . Hence it suffices to show that

has an isolated root . We have

| (6.2) |

Next, it follows by a change of variable and integration by parts that

Hence, and

| (6.3) |

since is strictly increasing over and

Consequently, the consistency of is obtained.

Next, we show the asymptotic normality of . Set below (recall given in (6))

Since

is finite in a neighbourhood of and continuous at . It follows thus by Theorem A, p. 251 in Serfling (1980) that is asymptotically normal distributed.

Furthermore, we have by (6.3)

Hence, the asymptotic variance of is given by

Please note that . We complete the proof of Theorem 2.1. ∎

Proof of Theorem 2.2.

Similar arguments of Theorem 2.1 apply with and replaced by and , respectively. First we show the consistency of . It follows by (1.6) that is strictly increasing and continuous in . Hence it suffices to show that

has an isolated root . We have

| (6.4) |

Next, it follows by a change of variable and integration by parts that

| (6.5) |

where in the second equality we use . Hence, and

| (6.6) |

since is strictly increasing over and

Consequently, the consistency of is obtained.

Next, we show the asymptotic normality of . Set below (recall given by (6))

Since

is finite in a neighbourhood of and continuous at , it follows by Theorem A, p. 251 in Serfling (1980) that is asymptotically normal distributed.

Furthermore, we have by (6.6)

Hence, the asymptotic variance is given by

We complete the proof of Theorem 2.2. ∎

Proof of Theorem 2.3.

The result follows by analogous arguments as in the proof of Theorem 2.1. Since is strictly increasing and contionuous in , the assumptions of Theorem 2.3 are sufficient for the consistency and asymptotic normality of . Using further Lemma 7.2.1A and Theorem A (see p. 249 and 251 therein) by Serfling (1980), we complete the proof of Theorem 2.3. ∎

Proof of Theorem 2.4.

The result follows by analogous arguments as in the proof of Theorem 2.2. Since is strictly increasing and continuous in , the assumptions of Theorem 2.4 are sufficient for the consistency and asymptotic normality of . Using further Lemma 7.2.1A and Theorem A (see p. 249 and 251 therein) by Serfling (1980), we complete the proof of Theorem 2.4. ∎

Acknowledgments. The authors would like to thank the referee for hisher important suggestions which significantly improve this contribution.

References

- [1]

- Arendarczyk and Dȩbicki [2011] Arendarczyk, M. and Dȩbicki, K. [2011]. Asymptotics of supremum distribution of a gaussian process over a weibullian time, Bernoulli 17: 194–210.

- Asimit et al. [2010] Asimit, A. V., Li, D. and Peng, L. [2010]. Pitfalls in using weibull tailed distributions, Journal of Statistical Planning and Inference 140(7): 2018–2024.

- Basu et al. [1998] Basu, A., Harris, I. R., Hjort, N. L. and Jones, M. C. [1998]. Robust and efficient estimation by minimising a density power divergence, Biometrika 85(3): 549–559.

- Beirlant and Teugels [1992] Beirlant, J. and Teugels, J. L. [1992]. Modeling large claims in non-life insurance, Insurance: Mathematics and Economics 11(1): 17–29.

- Beran and Schell [2012] Beran, J. and Schell, D. [2012]. On robust tail index estimation, Comput. Statist. Data Anal. 56(11): 3430–3443.

- Bingham et al. [1987] Bingham, N., Goldie, C. and Teugels, J. [1987]. Regular variation, Vol. 27 of Encyclopedia of Mathematics and its Applications, Cambridge University Press, Cambridge.

- Dȩbicki and Hashorva [2018] Dȩbicki, Krzysztof, J. F. and Hashorva, E. [2018]. Extremes of randomly scaled gumbel risks, Journal of Mathematical Analysis and Applications 458(1): 30–42.

- Dierckx et al. [2009] Dierckx, G., Beirlant, J., De Waal, D. and Guillou, A. [2009]. A new estimation method for Weibull-type tails based on the mean excess function, Journal of Statistical Planning and Inference 139(6): 1905–1920.

- Gardes and Girard [2008] Gardes, L. and Girard, S. [2008]. Estimation of the weibull tail-coefficient with linear combination of upper order statistics, Journal of Statistical Planning and Inference 138(5): 1416–1427.

- Girard [2004] Girard, S. [2004]. A Hill type estimator of the Weibull tail-coefficient, Communications in Statistics-Theory and Methods 33(2): 205–234.

- Goegebeur et al. [2010] Goegebeur, Y., Beirlant, J. and De Wet, T. [2010]. Generalized kernel estimators for the Weibull-tail coefficient, Communications in Statistics –Theory and Methods 39(20): 3695–3716.

- Goegebeur et al. [2015] Goegebeur, Y., Guillou, A. and Rietsch, T. [2015]. Robust conditional weibull-type estimation, Annals of the Institute of Statistical Mathematics 67(3): 479–514.

- Hashorva and Weng [2014] Hashorva, E. and Weng, Z. [2014]. Tail asymptotic of weibull-type risks, Statistics 48(5): 1155–1165.

- Huber [1964] Huber, P. [1964]. Robust estimation of a location parameter, The Annals of Mathematical Statistics 35(1): 73–101.

- Kundu et al. [2017] Kundu, D., Mitra, D. and Ganguly, A. [2017]. Analysis of left truncated and right censored competing risks data, Computational Statistics and Data Analysis 108: 12–26.

- Liu and Tang [2010] Liu, Y. and Tang, Q. [2010]. The subexponential product convolution of two weibull-type distributions, Journal of the Australian Mathematical Society 89(2): 277–288.

- Serfling [1980] Serfling, R. J. [1980]. Approximation theorems of mathematical statistics, John Wiley & Sons, New York.

- Trimborn and Härdle [2016] Trimborn, S. and Härdle, W. K. [2016]. CRIX an Index for Blockchain Based Currencies, Vol. SFB 649 Discussion Paper 2016-2021, Berlin: Economic Risk.

- Vandewalle et al. [2007] Vandewalle, B., Beirlant, J., Christmann, A. and Hubert, M. [2007]. A robust estimator for the tail index of Pareto-type distributions, Computational Statistics & Data Analysis 51(12): 6252–6268.

- Vandewalle et al. [2004] Vandewalle, B., Beirlant, J. and Hubert, M. [2004]. A robust estimator of the tail index based on an exponential regression model, Theory and applications of recent robust methods, Springer, pp. 367–376.