Shrinkage for Covariance Estimation: Asymptotics, Confidence Intervals, Bounds and Applications in Sensor Monitoring and Finance

Ansgar Steland

Institute of Statistics,

RWTH Aachen University,

Aachen, Germany

Email: steland@stochastik.rwth-aachen.de

Abstract

When shrinking a covariance matrix towards (a multiple) of the identity matrix, the trace of the covariance matrix arises naturally as the optimal scaling factor for the identity target. The trace also appears in other context, for example when measuring the size of a matrix or the amount of uncertainty. Of particular interest is the case when the dimension of the covariance matrix is large. Then the problem arises that the sample covariance matrix is singular if the dimension is larger than the sample size. Another issue is that usually the estimation has to based on correlated time series data. We study the estimation of the trace functional allowing for a high-dimensional time series model, where the dimension is allowed to grow with the sample size - without any constraint. Based on a recent result, we investigate a confidence interval for the trace, which also allows us to propose lower and upper bounds for the shrinkage covariance estimator as well as bounds for the variance of projections. In addition, we provide a novel result dealing with shrinkage towards a diagonal target.

We investigate the accuracy of the confidence interval by a simulation study, which indicates good performance, and analyze three stock market data sets to illustrate the proposed bounds, where the dimension (number of stocks) ranges between and . Especially, we apply the results to portfolio optimization and determine bounds for the risk associated to the variance-minimizing portfolio.

Keywords: Central limit theorem, high-dimensional statistics, finance, shrinkage, strong approximation, portfolio risk, risk, time series.

1 Introduction

In diverse fields such as finance, natural science or medicine the analysis of high-dimensional time series data is of increasing importance. In the next section, we consider data from financial markets and sensor arrays, for instance consisting of photocells (solar cells), as motivating examples for high-dimensional data. Here the number of time series, the dimension , can be much larger than the sample size . Then standard assumptions such as fixed and , the classical low-dimensional setting, or , as in random matrix theory, [6], are not justifiable. Even when , so that - theoretically - the covariance matrix may have nice properties such as invertability, it is recommended to regularize the sample covariance matrix when is large. A commonly used method is shrinkage as studied in depth by [17], [18] and for weakly dependent time series in [20], among others. Here the trace functional of the sample covariance matrix arises as a basic ingredient for shrinkage. The trace also arises in other settings, e.g. as the trace norm to measure the size of a nonnegative definite matrix , or when measuring the total information. For the latter application, recall that the variance of a zero mean random variable with finite second moment is a natural measure of the uncertainty of and a canonical measure of its precision is . For random variables it is natural to consider the total variance defined as the sum of their variances. These applications motivate us to study estimators for the trace and, especially, their statistical evaluation in terms of variance estimators and confidence intervals, lower and upper bounds; the problem of regularized covariance estimation solved by (linear) shrinkage represents our key application.

We study variance estimators and a related easy-to-use confidence interval for the trace of a covariance matrix, when estimating the latter by time series data. By [16], the estimator is asymptotically normal and the variance estimator turns out to be consistent under a high-dimensional framework, which even allows that the dimension grows in an arbitrary way, as . Indeed, the results of [16], which are based on [15], and those of the present paper do not require any condition on the dimension and the sample size such as , contrary to results using random matrix theory.

These results allow us to construct an easy-to-calculate confidence interval, which in turn allows us to make inference and to quantify the uncertainty associated to the proposed estimator in a statistically sound way. The results also suggest novel lower and upper data-based bounds for the shrinkage covariance estimator, and these bounds in turn yield lower and upper data-based bounds for the variance of a projection of the -dimensional observed vector onto a projection vector. We evaluate the confidence interval by its real coverage probability and examine its accuracy by a simulation study for high dimensions. Here we consider settings where the dimension is up to times larger than the length of the time series.

Going beyond the identity target for shrinkage covariance estimation, this paper also contributes new asymptotic results when shrinking towards a diagonal matrix. Concretely, we consider case of a diagonal target corresponding to uncorrelated coordinates. Then the shrinkage covariance estimator strengthens the diagonal of the sample covariance matrix. Our results deal with a strong approximation by a Gaussian random diagonal matrix. Again, the result holds true without any constraint on the dimension.

The paper is organized as follows. Motivating applications to finance and sensor monitoring, which also lead to the assumed high-dimensional model framework, are discussed in Section 2. In Section 3, we review the trace functional and discuss its role for shrinkage estimation. Section 4 provides the details about the proposed variance estimator and the asymptotic large sample approximations. Especially, Section 4.3 reviews the estimator proposed and studied in [15] based on the work of [16] and discusses the proposed confidence interval. A new result about the diagonal shrinkage target is provided in Section 4.4. Simulations and the application to financial stock market data are presented in Section 5. Our application especially covers portfolio optimization as one of the most important problems related to investment. As well known, the strategy of the portfolio selection process heavily determines the risk associated to the portfolio return. Here we follow the classical approach to measure risk by the variance and consider the variance-minimizing portfolio calculated from a shrinkage covariance estimator. Our results provide in a natural way lower and upper bounds for the portfolio risk. We illustrate their application by analyzing three data sets of stock market log returns.

2 Motivating example and assumptions

Let us consider the following motivating examples.

2.1 High-dimensional sensor monitoring

Suppose a source signal is monitored by a large number of sensors. The source is assumed to be given by independent zero mean noise with possibly heterogenous (finite) variances,

for constants , . Here we write for a random variable and constants and , if follows an arbitrary distribution with mean and existing variance .

The above model implies that the information present in the source signal is coded in the variances . The source is in a homogeneous or stable state, if it emits a signal with constant variance. Let us consider the testing problem given by the null hypothesis of homogeneity,

The source signal is i.i.d., , for all .

If the source emits a signal with a non-constant variance, we may say that it is in an unstable state. This can be formulated, for instance, by the alternative hypothesis

are independent with variances satisfying for ,

where . Note that represents the complement of within the assumed class of distributions for with independent, zero mean coordinates under moment conditions specified later. Depending on the specific application, certain patterns may be of interest, of course, and demand for specialized procedures, but this issue is beyond the scope of this paper. Let us, however, briefly discuss a less specific situation frequently studied, namely when a change-point occurs where the uncertainty of the signal changes: If at a certain time instant, say , the variance changes to another value, is called change-point and we are led to a change-point alternative,

, for .

Let us now assume that the source is monitored by sensors which deliver to a central data center a flow of possibly correlated discrete measurements in the form of a time series. Denote by the real-valued measurement of the th sensor received at time , . We want to allow for sensor arrays which are possibly spread over a large area and therefore receive the source signal at different time points. Further, we have in mind sensors which aggregate the input over a certain time frame, such as capacitors, Geiger counters to detect and measure radiation or the photocells of a camera sensor. Therefore, let us make the following assumption about the data-processing mechanism of the sensors:

-

•

The sensor receives the source signal with a delay , such that (instead of ) influences :

-

•

Previous observations , , affect the sensor, but they are damped by weights

This model can also be justified by assuming that the source signal may be disturbed and reflected, e.g. at buildings etc., such that at a certain location we cannot receive but only a mixture of that current signal value and past observations.

These realistic assumptions call for the well known concept of a linear filter providing the output, such that a natural model taking into account the above facts is to assume that the time series available for statistical analyses follow a linear process,

| (2.1) |

Lastly, it is worth mentioning that sensor devices frequently do not output raw data but apply signal processing algorithms, e.g. low and/or high pass filters, which also result in outputs following (2.1), even if one can observe at time . For example, image sensors use built-in signal processing to reduce noise, enhance contrast or, for automotive applications, detect lanes, see [11]. For body sensor networks in health monitoring 3D acceleration signals need to be filtered to maximize the signal-to-noise ratio. [21] develop and study a 3D sensor with a built-in Butterworth low-pass filter with waveform delay correction.

2.2 Financial time series

Linear time series are also a common approach to model econometric and financial data such as log return series of assets defined as

where denotes the time price of a share. Although the serial correlations of the daily log returns of a single asset are usually quite small or negligible, the cross correlations between different assets are relevant and are used to reduce investment risk by proper diversification. Hence, models such as (2.1) for series of daily log returns are justifiable. Extensions to factor models are preferable; they are subject of current research and will be published elsewhere.

Instead of analyzing marginal moments, analyzing conditional variances of log returns by means of GARCH models and their extensions has become quite popular, and we shall briefly review such models to clarify and discuss the differences to the class of models studied in the present paper.

Recall that is called a GARCH()-process, see [3], [9] and [14], if it is a martingale difference sequence with respect to the natural filtration , and if there exist constants such that the conditional variance satisfies the equations

For conditions on the parameters ensuring existence of a solution we refer to [9], see also [14, Theorem 3.7.6]. Such GARCH processes show volatility clusters which is one of the reasons of their success in financial modelling. Putting and substituting the by it follows that the squares can be written as

where , if and if , and are the innovations. This equation shows that the squares of a GARCH() process follow an ARMA()-process with respect to the innovations . The GARCH approach can therefore be interpreted as an approach which analyzes the conditional mean of the second moments by an ARMA model, i.e. as a (linear) function of the information set . Various extensions, such as the exponential GARCH etc., have been studied, which consider different models for the conditional variance in terms of the information set.

Consider now a zero mean -dimensional time series and let and , where now . Multivariate extensions of the GARCH approach model the matrix of the conditional second moments, , as a function of the information set . For example, the so-called vec representation considers the model

for coefficient matrices , see [8] and [9]. Here the vector-half operator stacks the elements of the lower triangular part of a matrix . Whereas this model is designed to analyze the conditional variances and covariances of the coordinates of , which determine the marginal second moments, modelling the centered squares by (2.1), such that

| (2.2) |

models the dependence structure of the squares and implies the model

for their covariance matrix, where

with for . We may write

with . Therefore, in this model hypotheses dealing with inhomogeneity of , , may be a consequence of a change in the variances , or result from a change of the coefficients summarized in the vectors .

2.3 Assumptions

The theoretical results used below and motivated above assume model (2.1) and require the following conditions.

Assumption 1: The innovations have finite absolute moments of the order .

Assumption 2: The coefficients satisfy the decay condition

| (2.3) |

for some . This condition is weak enough to allow for ARMA() models,

where is a lag polynomial of order and a lag polyonmial of order . It is worth mentioning that also seasonal ARMA models with seasons are covered, where the observations , , of season follows an ARMA() process,

for lag polynomials and , see e.g. [4] for details.

3 The trace functional and shrinkage

Let be the covariance matrix of a zero mean random vector of dimension . Recall that the trace of is defined as the sum of the diagonal,

The related average,

is called scaled trace. Observe that it assigns the value to the identity matrix, , whereas , if the dimension tends to infinity. The trace resp. scaled trace arises naturally in the form of a scaling factor when shrinking the true covariance matrix towards the identity matrix under the Frobenius norm, see [17] and [18], which represents the simplistic model of uncorrelated, homogenous coordinates.

Denote by the set of matrices and denote by the subset of covariance matrices of dimension . Equip with the inner product

which induces the Frobenius matrix norm , . Then becomes a separable Hilbert space of dimension . The orthogonal projector, , onto the one-dimensional linear subspace

associated to a single matrix is given by

Clearly, is the optimal element from which minimizes the distance

between and the subspace : is the element from to approximate best. It follows that for the optimal approximation of by a multiple of the identity matrix is given by

This is the optimal target for shrinking: If one wants to ’mix in’ a regular matrix, then one should use . The shrunken covariance matrix with respect to a shrinkage weight , also called mixing parameter or shrinkage intensity, is now defined by the convex combination

To summarize, the optimal shrinkage target is given by where the optimal scaling factor is called shrinkage scale.

Provided we have a (consistent) estimator of , we can estimate the shrunken covariance matrix by the shrinkage covariance estimator

| (3.1) |

where

is the usual sample covariance matrix. Whatever the shrinkage weight, the shrinkage covariance estimator has several appealing properties: Whereas is singular if , the shrinkage estimator is always positive definite and thus invertible. From a practical and computational point of view, it has the benefit that it is fast to compute. We shall, however, see that its statistical evaluation by a variance estimator is computationally more demanding. As shown in [17] and [18], the shrinkage estimator has further optimality properties, whose discussion goes beyond the scope of this brief review. For extensions of those studies to weakly dependent time series see [20]. There it is also shown how one can select the shrinkage weight in an optimal way, if there is no other guidance.

4 Nonparametric estimation of the scaled trace

In practice, one has to estimate the shrinkage target , i.e. we have to estimate the scaled trace of . Let us assume that for each coordinate of the vector a time series of length ,

is available for estimation. Put , . The canonical nonparametric estimator for is the sample moment

which suggests the plug-in estimator

Obviously, we have the relationship

The scaled trace is now estimated by

4.1 Variance estimation: uncorrelated case

If the time series , , are independent and if is fixed, then the statistical evaluation of the uncertainty associated with the estimator , on which we shall focus in the sequel, is greatly simplified, since then

| (4.1) |

and we may estimate this expression by estimating the variances , . Let us first stick to that case. Suppose that all time series are strictly stationary with finite absolute moments of the order for some . Then a straightforward calculation shows that

where

is the lag autocovariance of the squared time series. The canonical sample autocovariance estimates

where , lead to the Bartlett-type long-run variance estimator

Here are weights satisfying the usual conditions,

-

(i)

for some constant and

-

(ii)

, as , for all .

Starting with [13] and [1] conditions under which such estimators are consistent are well known. Essentially, one has to require that the lag truncation sequence satisfies and . For a result on almost sure convergence under weak conditions we refer to [2]. Since the estimator (4.1) sums up a finite number of such estimators, the consistency easily carries over.

4.2 Variance estimation: correlated case

In the sequel, we want to relax two crucial conditions made above: We will now consider correlated time series and allow that the dimension depends on and may grow with : . Our exposition follows [16]. But if the time series are correlated, then, in general, formula (4.1) no longer applies. Instead we have

In what follows, we assume that . A direct calculation reveals the long-run variance structure

where

are the lag cross-covariances of the squares. They can be estimated by

Now we can estimate the covariances by the long-run variance estimators

| (4.2) |

for , where is a sequence of lag truncation constants. Eventually, we are led to the estimator

4.3 Asymptotics for the trace estimator

In [16] the asymptotics of the estimator has been studied in depth. Let us briefly review these results.

Theorem 4.1.

Suppose (2.1) and Assumptions 1 and 2 hold. Then the scaled trace norm is asymptotically normal in the sense that, provided the probability space is rich enough to carry an additional uniformly distributed random variable, there exists a Gaussian random variable

such that

| (4.3) |

as , a.s.. Further, the estimator for is -consistent, i.e.

as , if the lag truncation sequences satisfies

as .

Based on the above result one may propose the confidence interval

where denotes the -quantile of the standard normal distribution, i.e. for , where denotes the distribution function of the standard normal distribution.

For the shrinkage estimator , see (3.1), the above result allows us to calculate lower and upper bounds: A lower bound is given by

and an upper bound by

Observe that these bounds differ only on the diagonal. From a statistical point of view, they provide the justifiable minimal and maximal amount of strengthening of the diagonal of the sample covariance matrix.

Suppose now that we estimate the variance

of the projection onto a projection vector with uniformly bounded -norm using the shrinkage covariance estimator

Estimating using the above lower and upper bounds, we obtain the lower bound

| (4.4) |

and the upper bound

| (4.5) |

Here or if one considers only one of those bounds.

Remark 4.1.

The normal approximation (4.3) holds true under weaker conditions. In particular, the coefficients of the time series may depend on and are only required to satisfy the weaker decay condition

| (4.6) |

for some , and the innovations are only required to have finite absolute moments of the order for some , see [16, Theorem 2.3].

4.4 Shrinking towards a diagonal matrix

Let us now study the more general situation to shrink the covariance matrix towards the diagonal matrix. Here we consider the -dimensional subspace

which is spanned by the orthonormal matrices , where are the unit vectors of and for a vector . Here and in the sequel we write for the matrix whose diagonal is given by and all other elements are zero. Further, for a square matrix we write for the (main) diagonal represented as a column vector and let

The orthogonal projection onto is given by

Consequently, the optimal shrinkage target is

We estimate by

where denote the elements on the diagonal of the sample covariance matrix . The corresponding shrinkage covariance estimator is given by

The following new result provides the asymptotics of . Recall that

is the th diagonal element of , , and observe that

Theorem 4.2.

Assume model (2.1) with coefficients satisfying the decay condition (4.6). Let and be two sequences of weighting vectors with and

Then one can redefine the vector time series on a new probability space, together with a -dimensional Gaussian random vector with covariance structure given by

such that there exist constants and with

as , a.s.. Under the additional assumption we may therefore conclude that

as well as

| (4.7) |

as , a.s..

5 Simulations and application to financial data

5.1 Simulation study

We conducted simulations, in order to study the accuracy of the confidence interval

for the scaled trace in terms of its coverage probability. Of primary interest is the case that the dimension of the vector time series is of the order of the sample size or even larger. For there are covariances which need to be estimated to calculate the estimator . These computations can, however, be easily parallelized.

Vector time series of dimension were simulated following a family of autoregressive processes of order ,

where , , . The weights were chosen as

with lag truncation constant . The nominal coverage probability was chosen as . The true value of the scaled trace norm of the corresponding true covariance matrix was estimated by a simulation using runs. Then the coverage probability was estimated by Monte Carlo simulations. The simulations were carried out using R and the doParallel and foreach packages for parallel computations.

Table 1 provides the simulated coverage probabilities for sample sizes and dimensions . As our theoretical results do not require a constraint on the dimension such as convergence of to a constant between and , we simulate all resulting combinations. The nominal coverage probability is . It can be seen that the coverage is good, if the sample size is not too small; especially, the coverage gets better if increases. It is remarkable that, according to the simulation results, the accuracy is quite uniform in the dimension, even when the dimension is much larger than the sample size as in the case and .

| 0.885 | 0.897 | 0.884 | 0.900 | 0.902 | |

| 0.917 | 0.915 | 0.916 | 0.921 | 0.917 | |

| 0.932 | 0.935 | 0.930 | 0.913 | 0.932 |

5.2 Application to asset returns

We applied the proposed methods to three data sets, in order to illustrate their potential benefit in practice. The first one, NYSE, is a standard data set of asset returns from the New York stock exchange used by [7], [10] and others. The NYSE data set includes daily closing prices of stocks over a 22-year period from July 3rd, 1962 to December 31th, 1984. The second one, TSE, consists of returns of stocks of the Toronto stock exchange for the 5-year period from January 4th, 1994 to December 31st, 1998. The last data set consists of 470 stocks of the SP500 over the 5-year period from February 8th, 2013 to February 7th, 2018.

In a first experiment, we estimated nonparametrically the dimensional covariance matrix of the associated log returns for the first log returns of the NYSE data set. [18] proposed an estimator of the (optimal) shrinkage weight leading to the estimate ; for the other data sets the estimates are larger. Hence, in all analyses we use the weight . In this way we keep the regularization at a moderate level and can mask out effects due to the estimation error with respect to . Further, this also allows better comparisions across the data sets and subsamples.

How does the condition number, defined as the ratio of the largest eigenvalue and the smallest one, improves by shrinking? The following figures provide some insights. When using only the last log returns of the NYSE data set, the condition number of the sample covariance matrix is . Shrinking substantially improves the condition number by more than a factor of to . For the TSE stock data with stocks, the condition number decreases from to . Lastly, for the SP500 data from 2013-2018 the condition number for the -dimensional covariance matrix decreases from to .

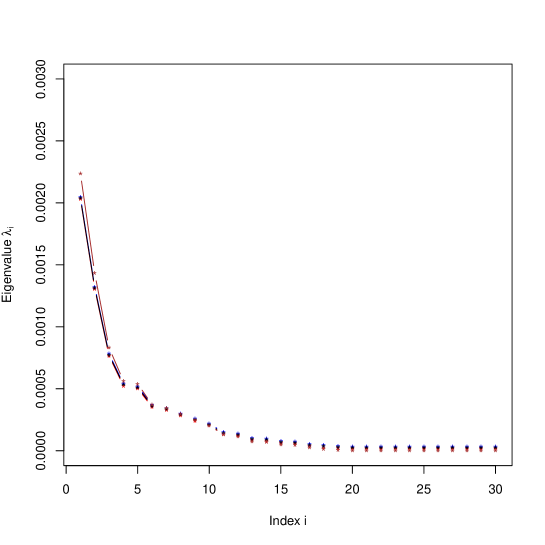

For a confidence level of the lower and upper bounds for the shrinkage covariance matrix were calculated. We report the eigenvalues as an informative summary statistic. Figure 1 shows the eigenvalues of the sample covariance matrix , the shrinkage estimator and of the lower and upper bounds for the NYSE data. One can see that the eigenvalues of the lower (upper) bound are always smaller (larger) than eigenvalues of the shrinkage estimator. However, note that the corresponding intervals can not be interpreted as confidence intervals.

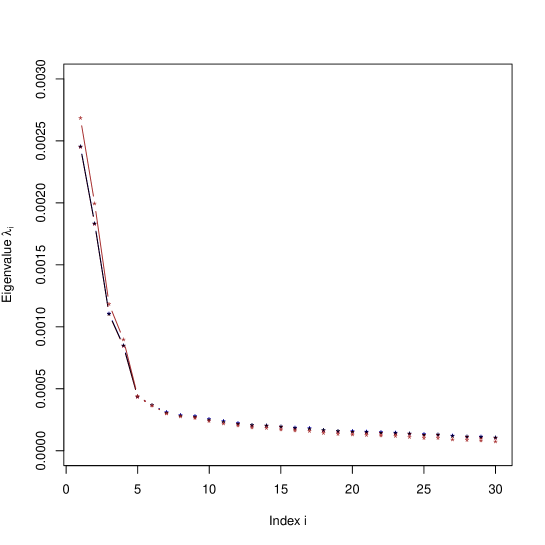

As a comparison, Figure 2 provides the eigenvalues of the sample covariance matrix and the shrinkage estimator when using the full data set of trading days.

In addition to the above analysis, we applied the proposed lower and upper bounds to portfolio optimization. Recall that the classical approach to porfolio optimization is to minimize the portfolio variance under the constraint and, optionally, constrained on a specified mean portfolio return. Here and in what follows, we focus on the variance-minimizing portfolio, called minimum variance portfolio, which minimized the variance under the constraint ,

where is the true covariance matrix of daily log returns. If there are no short sales in the optimal portfolio, its -norm is . For real markets, this condition usually does not hold true. Then we need to assume that . This can be guaranteed by adding an appropriate penalty term to the optimization problem as, e.g., in [5], which often leads to -sparse portfolios, i.e. one holds only positions in a subset of the available stocks. Nevertheless, we stay with the variance-minimizing portfolio in our analysis, which holds (long or short) positions in all assets, so that all covariances between the asset log returns are relevant to calculate the variance estimator . For -constrained portfolios holding positions only in a subset of the assets one can presumably expect tighter bounds for the portfolio risk than reported here for the variance-minimizing portfolio.

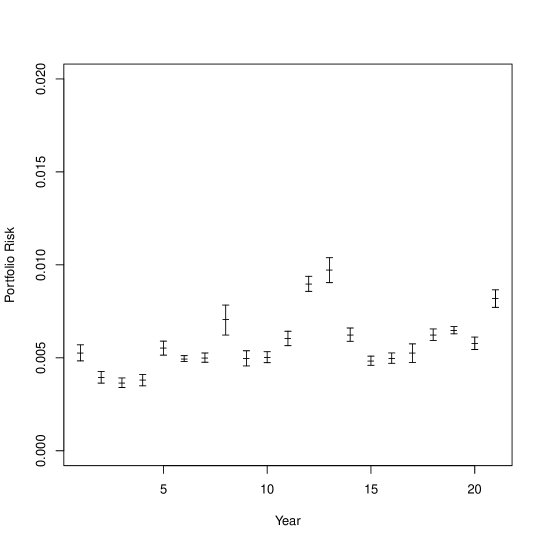

The whole data set was split in subsamples of returns corresponding to one year. For each year the optimal portfolio , its associated estimated risk and the lower and upper bounds

for were calculated, cf. (4.4) and (4.5). If the expression under the square root is negative, then it is set to .

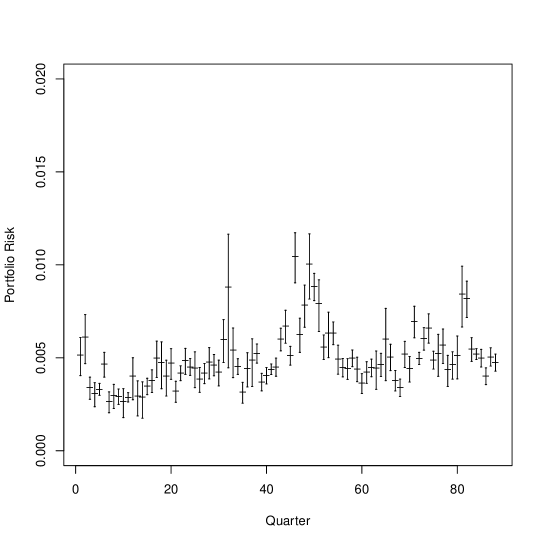

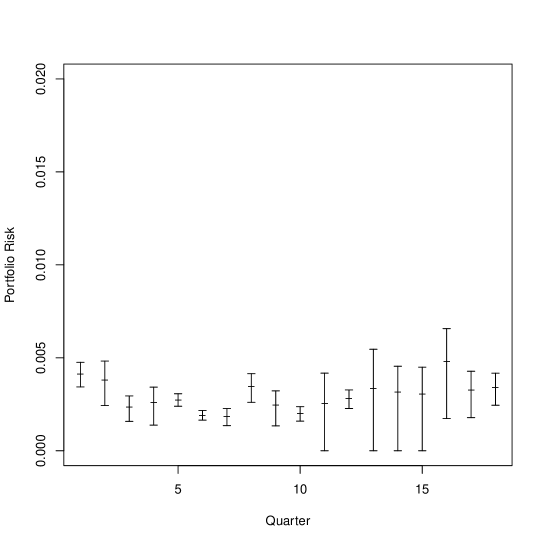

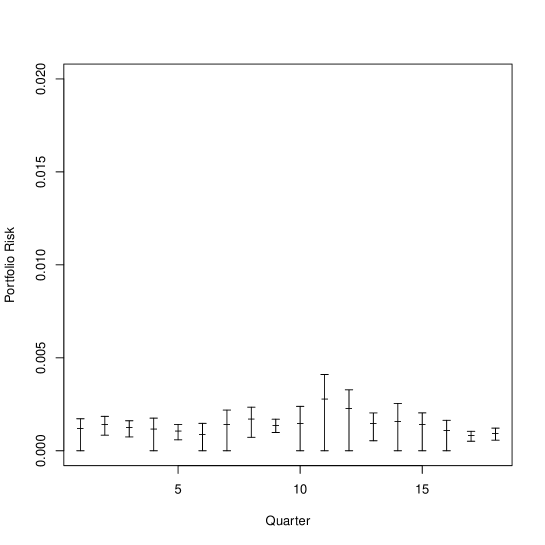

Figure 3 shows the result for the NYSE data set. This analysis was repeated on a quarterly basis based on trading days. The result is shown in Figure 4. One can observe that the bounds are less tight due to the smaller sample size available for estimation which increases the statistical estimation error.

For the TSE data set where the corresponding results on a quarterly basis are shown in Figure 5. Here the covariance matrix is estimated based on log returns, such that .

Lastly, for the SP500 data set for the period from February 2013 to February 2018, Figure 5 shows the corresponding portfolio risks and their bounds on a quarterly basis. Here return vectors are used to estimate the -dimensional covariance matrix and the associated risks of the variance-minimizing portfolio.

Acknowledgments

This work was supported by a grant from Deutsche Forschungsgemeinschaft, grant STE 1034/11-1. Comments from anonymous reviewers are appreciated.

References

- [1] Andrews D. W. K. (1991). Heteroscedasticity and autocorrelation consistent covariance matrix estimation. Econometrica, 69(3), 817-858.

- [2] Berkes I., L. Horváth, P. Kokoszka and Q. Shao. Almost sure convergence of the Bartlett estimator. Periodica Mathematica Hungaria, 51, 1, 11-25.

- [3] Bollerslev T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31, 307-327.

- [4] Brockwell P. J. and Davis R. A. (2006). Time Series: Theory and Methods, Springer Series in Statistics, New York.

- [5] Brodie J., Daubechies I., De Mol C., Giannone D. and Lorris I. (2009). Sparse and stable Markowitz portfolios, Proc. Natl. Acad. Sci. USA, 106, 12267-12272.

- [6] Bai Z. and Silverstein J.W. (2010). Spectral analysis of large dimensional random matrices. 2nd ed., Springer, New York.

- [7] Cover T. M. (1991). Universal Portfolios. Mathematical Finance, 1, 1–29.

- [8] Engle R.F. and Kroner K.F. (1995). Multivariate simultaneous generalized ARCH. Econometric Theory, 11, 1, 122-150.

- [9] Francq C. and Zakoian J.M. (2010). GARCH Models - Structure, Statistical Inference and Financial Applications, Wiley, Chichester.

- [10] Györfi L., Lugosi G. and Udina F. (2006). Nonparametric kernel-based sequential investment strategies. Mathematical Finance, 16, 2, 337-357.

- [11] Hsiao, P.Y., Cheng, H.C., Huang, S.S. and Fu, L.C. (2009). CMOS image sensor with a built-in lane detector. Sensors, 9, 1722-1737.

- [12] Michael A. Kouritzin (1995). Strong approximation for cross-covariances of linear variables with long-range dependence. Stochastic Processes and Their Applications, 60(2), 343-353.

- [13] Newey W. and West, K. D. (1987). A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix. Econometrica, 55(3), 703-708.

- [14] Steland A. (2012). Financial Statistics and Mathematical Finance - Methods, Models and Applications, Wiley, Chichester.

- [15] Steland, A. and von Sachs, R. (2017a). Large sample approximations for variance-covariance matrices of high-dimensional time series. Bernoulli, 23 (4A), 2299-2329.

- [16] Steland, A. and von Sachs, R. (2017b). Asymptotics for high-dimensional covariance matrices and quadratic forms with applications to the trace functional and shrinkage. Stochastic Processes and Their Applications, to appear, arXiv:1711.01835

- [17] Ledoit, O. and Wolf, M. (2003). Improved estimation of the covariance matrix of stock returns with an application to portfolio selection. Journal of Empirical Finance, 10, 603-621.

- [18] Ledoit, O. and Wolf, M. (2004). A well-conditioned estimator for large-dimensional covariance matrices. Journal of Multivariate Analysis, 88, 365-411.

- [19] Philipp, W. (1986). A note on the almost sure approximation of weakly dependent random variables. Monatshefte Mathematik, 102(3), 227-236.

- [20] Sancetta, A. (2008). Sample covariance shrinkage for high dimensional dependent data. Journal of Multivariate Analysis, 99(5), 949-967.

- [21] Wang, W.Z., Guo, Y.W., Huang, B.Y., Zhao, G.R, Liu, B.Q. and Wang, L. Analysis of filtering methods for 3D acceleration signals in body sensor network. International Symposium on Bioelectronics and Bioinformations, 2011, Shuzu, China.

Appendix A Proof of Theorem 4.2

We give a sketch of the proof. We apply [16, Theorem 2.3], which generalizes [15] and is based on techniques of [12] and [19]. [16, Theorem 2.3] is applied with , where denotes the th unit vector of the Euclidean space , and . Basically, the result asserts that, on a new probability space, one can approximate the partial sums

by a Brownian motion, and here the number of such bilinear forms ( in our case) given by pairs of weighting vectors, may grow to . Using the notation and definitions of Secton 2.3 of [16], we obtain

By [16, Theorem 2.3] we may redefine the above processes, on a new probability space together with a Gaussian random vector with and covariances given by

where satisfy

by Lemma 2.1 and Theorem 2.2 of [16] (there the quantities are denoted by ), such that the strong approximation

as , a.s., holds true. But this immediately yields

as , a.s.. Now both assertions follow, because