Chen, Kuhn, and Wiesemann

Data-Driven Chance Constrained Programs over Wasserstein Balls

Data-Driven Chance Constrained Programs

over Wasserstein Balls

Zhi Chen

\AFFCollege of Business, City University of Hong Kong, Kowloon Tong, Hong Kong,

zhi.chen@cityu.edu.hk

\AUTHORDaniel Kuhn

\AFFRisk Analytics and Optimization Chair, École Polytechnique Fédérale de Lausanne, Lausanne, Switzerland,

daniel.kuhn@epfl.ch

\AUTHORWolfram Wiesemann

\AFFImperial College Business School, Imperial College London, London, United Kingdom,

ww@imperial.ac.uk

\ABSTRACTWe provide an exact deterministic reformulation for data-driven chance constrained programs over Wasserstein balls. For individual chance constraints as well as joint chance constraints with right-hand side uncertainty, our reformulation amounts to a mixed-integer conic program. In the special case of a Wasserstein ball with the -norm or the -norm, the cone is the nonnegative orthant, and the chance constrained program can be reformulated as a mixed-integer linear program. Our reformulation compares favourably to several state-of-the-art data-driven optimization schemes in our numerical experiments.

Distributionally robust optimization; ambiguous chance constraints; Wasserstein distance.

1 Introduction

Distributionally robust optimization is a powerful modeling paradigm for optimization under uncertainty, where the distribution of the uncertain problem parameters is itself uncertain, and where the performance of a decision is assessed in view of the worst-case distribution from a prescribed ambiguity set. The earlier literature on distributionally robust optimization has focused on moment ambiguity sets which contain all distributions that obey certain (standard or generalized) moment conditions; see, e.g., Delage and Ye (2010), Goh and Sim (2010) and Wiesemann et al. (2014). Pflug and Wozabal (2007) were the first to propose an ambiguity set of the form of a ball in the space of distributions with respect to the celebrated Wasserstein, Kanthorovich or optimal transport distance. The type-1 Wasserstein distance between two distributions and on , equipped with a general norm , is defined as the minimal transportation cost of moving to under the premise that the cost of moving a Dirac point mass from to amounts to . Mathematically, this implies that

where , and represents the set of all distributions on with marginals and . The Wasserstein ambiguity set is then defined as a ball of radius with respect to the Wasserstein distance, centered at a prescribed reference distribution :

| (1) |

One can think of the Wasserstein radius as a budget on the transportation cost. Indeed, any member distribution in can be obtained by rearranging the reference distribution at a transportation cost of at most . If only a finite training dataset is available, a natural choice for is the empirical distribution , which represents the uniform distribution on the training samples. Throughout the paper, we will assume that is the empirical distribution.

While it has been recognized early on that Wasserstein ambiguity sets offer many conceptual advantages (e.g., their member distributions do not need to be absolutely continuous with respect to and, if properly calibrated, they constitute confidence regions for the unknown true data-generating distribution), it was believed that they almost invariably lead to hard global optimization problems. Recently, Mohajerin Esfahani and Kuhn (2018) and Zhao and Guan (2018) discovered that many interesting distributionally robust optimization problems over Wasserstein ambiguity sets can actually be reformulated as tractable convex programs—provided that is discrete and that the problem’s objective function satisfies certain convexity properties. These reformulations have subsequently been generalized to Polish spaces and non-discrete reference distributions by Blanchet and Murthy (2019) and Gao and Kleywegt (2016). Since then, distributionally robust optimization models over Wasserstein ambiguity sets have been proposed for many applications, including transportation (Carlsson et al. 2018) and machine learning (Blanchet et al. 2019, Gao et al. 2017, Shafieezadeh-Abadeh et al. 2019 and Sinha et al. 2017).

In this paper we study distributionally robust chance constrained programs of the form

| (2) |

where the goal is to find a decision from within a compact polyhedron that minimizes a linear cost function and ensures that the exogenous random vector falls within a decision-dependent safety set with high probability under every distribution . Since the reference distribution in (2) is the empirical distribution over the training dataset , we refer to (2) as a data-driven chance constrained program.

To date, the literature on data-driven chance constraints has focused primarily on variants of problem (2) where the Wasserstein ambiguity set is replaced with an ambiguity set that contains all distributions close to the empirical distribution with respect to a -divergence (such as the Kullback-Leibler divergence or the -distance):

where is the divergence function. Hu and Hong (2013) show that a distributionally robust chance constrained program over a Kullback-Leibler ambiguity set reduces to a classical chance constrained progam over the reference distribution and an adjusted risk threshold . While this result holds for any reference distribution, -divergence ambiguity sets only contain distributions that are absolutely continuous with respect to , that is, any distribution in only assigns positive probability to those measurable subsets for which . This is undesirable for problems with a large dimension and/or few training data, where it is unlikely that every possible value of has been observed in . This shortcoming is addressed by Jiang and Guan (2016, 2018), who replace the reference distribution with a Kernel density estimator.

Despite their tremendous success and widespread adoption in recent years, the use of -divergences can lead to undesirable side effects in some applications: they compare distributions on a “scenario-by-scenario” basis and thus do not consider the possibility of noisy measurements (Gao and Kleywegt 2016), and they generically fail to be probability metrics as they typically violate symmetry as well as the triangle inequality. Moreover, as we show next, -divergence ambiguity sets may be overly optimistic when only few training samples are available.

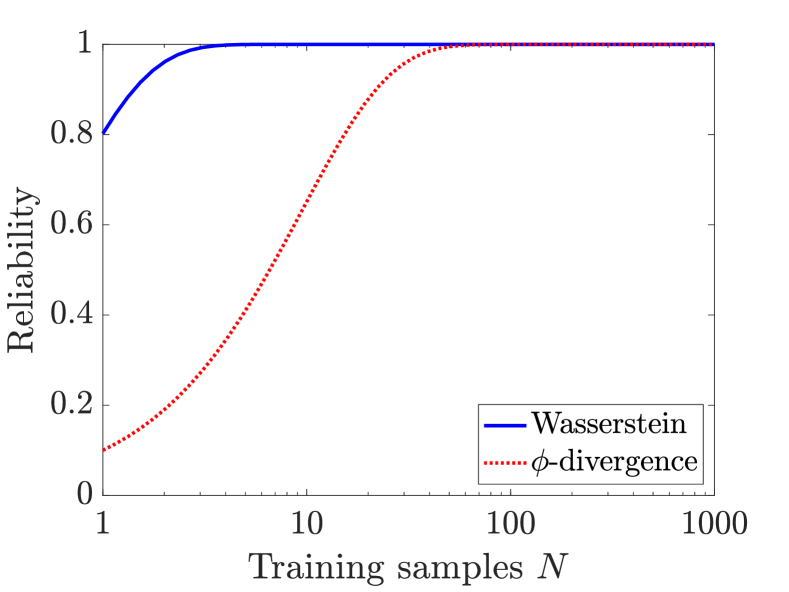

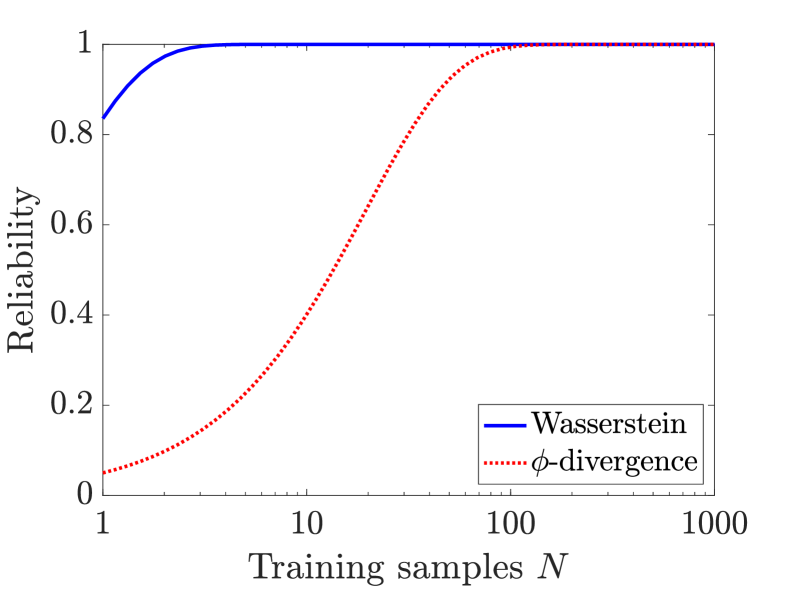

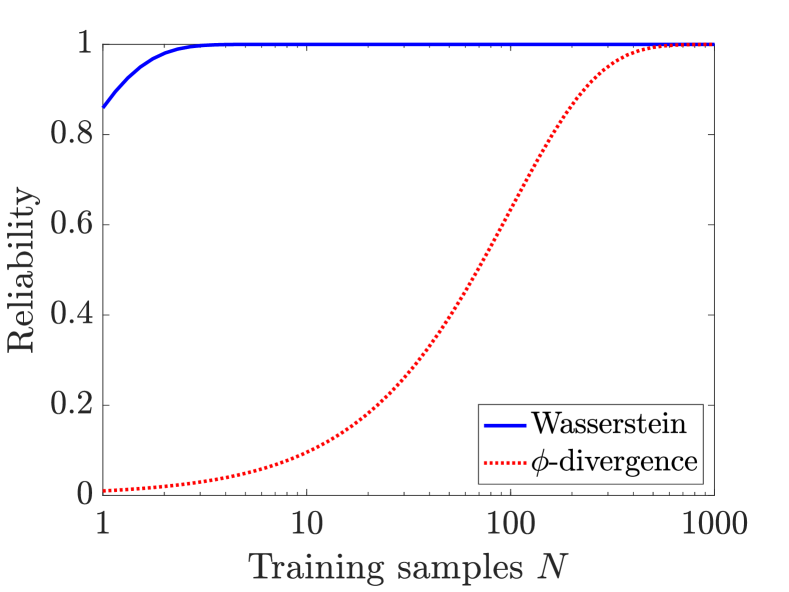

Motivating Example. Consider the arguably simplest instance of the data-driven optimization problem (2), which estimates the worst-case value-at-risk of a scalar random variable at level from a limited set of i.i.d. training samples of under the unknown data-generating distribution that are summarized by the empirical distribution at the centre of the Wasserstein ball . To avoid technicalities, we assume that is atomless. In addition, with and we define a distribution

to be used subsequently. Here, denotes the -th order statistic of the training samples .

The reliability of the aforementioned worst-case value-at-risk, that is, the probability that it weakly exceeds the unknown true value-at-risk , can be bounded from below by

where is the -fold product of that generates . The first inequality holds since is contained in . The first equality holds since by construction of , and the last inequality is due to a standard concentration inequality for empirical quantiles (see, e.g., Theorem 2.3.2 of Serfling 2009).

If we replace the Wasserstein ambiguity set with the ambiguity of any -divergence, on the other hand, then we can bound the reliability from above by

Here, the first inequality holds since all distributions in share a common support with , and the second inequality follows from the definition of . We highlight that this probability bound holds for every radius of the -divergence ball .

Figure 1 compares the worst-case reliability offered by the Wasserstein ambiguity set with the best-case reliability of the -divergence ambiguity set for a uniform distribution over the interval . We observe that in low-sample regimes, -divergence ambiguity sets may underestimate the true VaR with high probability.

To our best knowledge, the paper of Xie and Ahmed (2020) is the only previous work on data-driven chance constraints over Wasserstein ambiguity sets. The authors study the special class of covering problems, where the feasible region satisfies for every . This problem class encompasses, among others, portfolio optimization problems without budgetary restrictions and lot-sizing problems in the absence of setup costs. The authors prove that the resulting individual chance constrained program is NP-hard. They also demonstrate that two popular approximation schemes, the CVaR approximation as well as the scenario approximation, can perform arbitrarily poorly for classical individual chance constraints, that is, when the Wasserstein radius is . Based on this insight, the authors propose a bicriteria approximation scheme for covering problems with classical as well as distributionally robust individual chance constraints over moment and Wasserstein ambiguity sets. This bicriteria approximation scheme determines solutions that trade off a higher risk threshold in the chance constraint with a smaller optimality gap . This is achieved by solving a tractable convex relaxation of the chance constrained problem (using, e.g., a Markovian or Bernstein generator) and subsequently scaling the solution to this relaxation so that it becomes feasible for the chance constraint with the higher risk threshold . By design, the performance guarantee of the bicriteria approximation scheme becomes weaker (and eventually trivial) as the selected risk threshold approaches the risk threshold of the original problem formulation.

In this paper, we study distributionally robust chance constrained programs over the Wasserstein ambiguity set (1). We derive deterministic reformulations for individual chance constrained programs, where for affine functions and , as well as for joint chance constrained programs with right-hand side uncertainty, where for and an affine function . Our reformulations are mixed-integer conic programs that reduce to mixed-integer linear programs when the norm on is the -norm or the -norm.

While preparing this paper for publication, we became aware of the independent work by Xie (2019), which derives similar reformulations for distributionally individual and joint chance constraints over Wasserstein ambiguity sets. In contrast to our work, however, Xie (2019) assumes that each safety condition , , in the joint chance constraint depends on a subvector of , and that these subvectors are pairwise disjoint for different safety conditions. In other words, different safety conditions of the joint chance constraints studied by Xie (2019) must depend on different random variables. Furthermore, the reformulations of Xie (2019) are derived via duality theory, whereas our reformulations directly leverage the structural insights into the worst-case distributions. This enables us to keep our reformulations largely independent of the selected ground metric for the Wasserstein ball, which opens up possibilities to incorporate other cost functions in our definition of the Wasserstein distance. Since the initial submission of this paper, our exact reformulation for data-driven chance constrained program over Wasserstein balls has been further studied and tightened; see, for instance, Ho-Nguyen et al. (2020, 2021), Shen and Jiang (2021) and Zhang and Dong (2021). Along with these theoretical extensions, our reformulation has also been applied in several domains, including risk sharing in finance (Chen and Xie 2021), network design for humanitarian operations (Jiang et al. 2021) and optimal power flows in energy systems (Arrigo et al. 2022).

Notation. We use boldface uppercase and lowercase letters to denote matrices and vectors, respectively. Special vectors of appropriate dimensions include and , which respectively correspond to the zero vector and the vector of all ones. We denote by the dual norm of a general norm . We use the shorthand to represent the set of all integers up to . Given a (possibly fractional) real number , we define the partial sum of the first values in as . Random vectors are denoted by tilde signs (e.g., ), while their realizations are denoted by the same symbols without tildes (e.g., ). Given a random vector governed by a distribution , a measurable loss function and a risk threshold , the value-at-risk (VaR) of at level is defined as .

2 Exact Reformulation of Data-Driven Chance Constraints

Section 2.1 reviews a previously established result on the quantification of uncertainty over Wasserstein balls. We use this result to derive an exact reformulation of generic data-driven chance constrained programs in Section 2.2. We finally specialize this generic reformulation to the subclasses of data-driven individual chance constrained programs as well as data-driven joint chance constrained programs with right-hand side uncertainty in Sections 2.3 and 2.4, respectively.

2.1 Uncertainty Quantification over Wasserstein Balls

Consider an open safety set , and denote by its closed complement. The uncertainty quantification problem

| (3) |

computes the worst (largest) probability of the system under consideration being unsafe, which is the case whenever the random vector attains a value in the unsafe set . Throughout the rest of the paper, we exclude trivial special cases and assume that and .

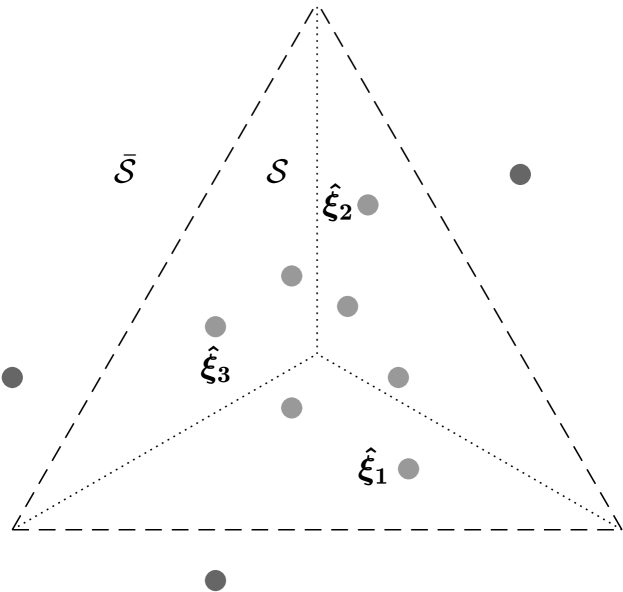

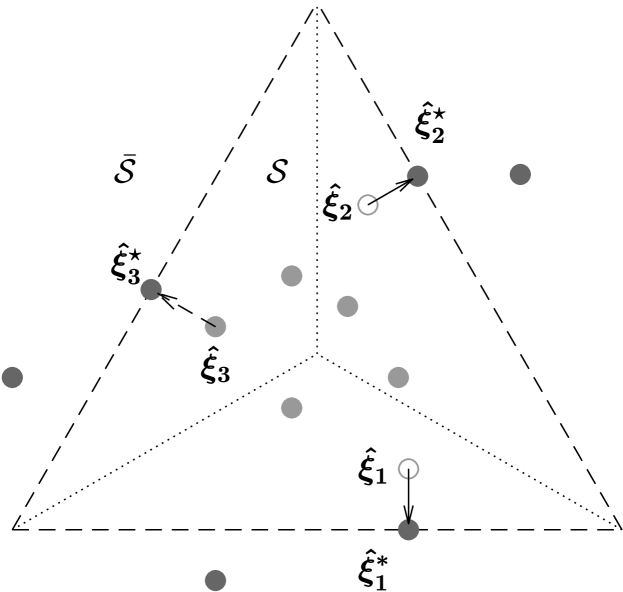

To solve the uncertainty quantification problem (3), denote by the distance of the data point of the empirical distribution to the unsafe set . This distance is based on a norm , which we keep generic at this stage. Without loss of generality, we assume that the data points are ordered in increasing distance to , that is, for all . We also assume that (that is, the data point is unsafe) if and only if , where if for all . Finally, we denote by an unsafe point that is closest to the data point , , in terms of the distance .

Blanchet and Murthy (2019) as well as Gao and Kleywegt (2016) have characterized the solution to the uncertainty quantification problem (3) in closed form. To keep our paper self-contained, we reproduce their findings without proof in Theorem 2.1 below.

Theorem 2.1

Let . The uncertainty quantification problem (3) is solved by a worst-case distribution that is characterized as follows:

-

(i)

If , then for

-

(ii)

If , then for

where .

Intuitively speaking, the worst-case distribution in Theorem 2.1 transports the training dataset to the unsafe set in a greedy fashion, see Figure 2. The data points are already unsafe and hence do not need to be transported. The subsequent data points are closest to the unsafe set and are thus transported from to . Due to the limited transportation budget , the data point is only partially transported. The safe samples , finally, are too far away from the unsafe set and are thus left unchanged. Note that the distribution characterized in Theorem 2.1 may not be the only distribution that solves problem (3).

2.2 Reformulation of Generic Chance Constraints

We now develop deterministic reformulations for the distributionally robust chance constrained program (2). To this end, we focus on the ambiguous chance constraint

| (4) |

For any fixed decision , we let be an arbitrary open safety set, and we denote by its closed complement, which comprises all unsafe scenarios. Every fixed training dataset then induces a (decision-dependent) permutation of that orders the training samples in increasing distance to the unsafe set, that is,

We first show that a fixed decision satisfies the ambiguous chance constraint (4) over the Wasserstein ambiguity set (1) if and only if the partial sum of the smallest transportation distances to the unsafe set multiplied by the mass of a training sample exceeds .

Theorem 2.2

The left-hand side of (5) can be interpreted as the minimum cost of moving a fraction of the training samples to the unsafe set. If this cost exceeds the prescribed transportation budget , then no distribution in the Wasserstein ambiguity set can assign the unsafe set a probability of more than , which means that the distributionally robust chance constraint (4) is satisfied.

Proof of Theorem 2.2. From Theorem 2.1 we know that the worst-case distribution is an optimal solution (not necessarily unique) to the maximization problem embedded in the left-hand side of the ambiguous chance constraint (4). We thus conclude that the constraint (4) is satisfied if and only if for defined in the statement of that theorem.

In case (i) of Theorem 2.1, the ambiguous chance constraint (4) is violated since while by assumption. At the same time, since , we have . If this inequality is strict, then (5) is violated as desired since . If the inequality is satisfied as an equality, on the other hand, we know that since by assumption and for all by construction of the re-ordering . Thus, since by assumption, we have and equation (5) is violated as desired.

In case (ii) of Theorem 2.1, we have with as well as . We claim that is the optimal value of the bivariate mixed-integer optimization problem

| (6) |

Indeed, the solution is feasible in (6) by definition of and . Moreover, we have for any other feasible solution that satisfies and . Assume now that the optimal solution to (6) would satisfy . Any such solution would violate the first constraint since by definition of while . Similarly, any solution with cannot be optimal in (6) since while .

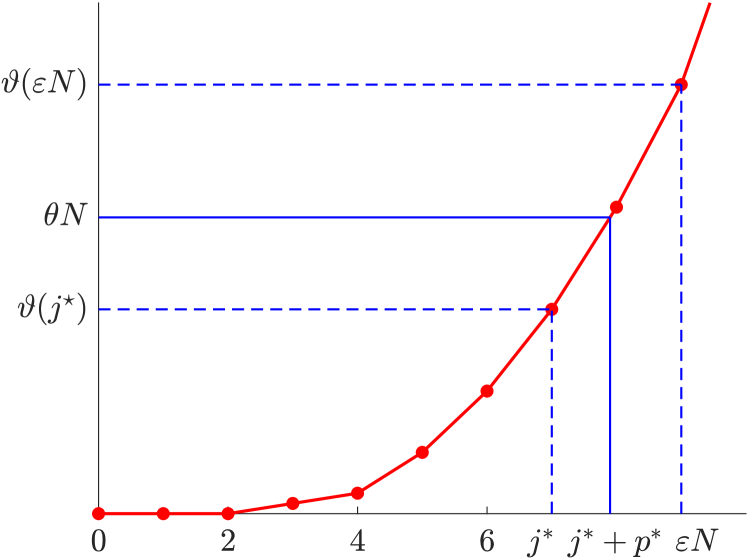

We can re-express problem (6) as the univariate discrete optimization problem

Using our definition of partial sums, we observe that this problem is equivalent to

By construction, the mapping , , is continuous and monotonically nondecreasing. It therefore affords the right inverse that satisfies for all . Figure 3 visualizes the relationship between and . We thus conclude that the ambiguous chance constraint (4) is satisfied if and only if

where the last equivalence follows from , which holds because for , as well as the fact that is monotonically nondecreasing. By definition, the right-hand side of the last equivalence holds if and only if (5) in the statement of the theorem is satisfied. \Halmos

Remark 2.3

We emphasize that the inequality (5) fails to be equivalent to the ambiguous chance constraint (4) when , in which case the Wasserstein ball collapses to the singleton set . To see this, suppose that for all and for all , where . If , then the chance constraint (4) is violated because

while the inequality (5) holds trivially because .

Theorem 2.2 establishes that a decision satisfies the ambiguous chance constraint (4) if and only if the sum of the smallest distances of the training samples to the unsafe set weakly exceeds . This result is of computational interest because the sum of the smallest out of real numbers is concave in those real numbers (while being convex in ). This reveals that the constraint (5) is convex in the decision-dependent distances . In the remainder we develop an efficient reformulation of this convex constraint that does not require an enumeration of all possible sums of different distances between the training samples and the unsafe set. This reformulation is based on the following auxiliary lemma.

Lemma 2.4

For any , the sum of the smallest out of real numbers coincides with the optimal value of the linear program

Proof of Lemma 2.4. By definition, the sum of the smallest elements of the set corresponds to the optimal value of the (manifestly feasible) linear program

The claim now follows from strong linear programming duality. \Halmos

Armed with Theorem 2.2 and Lemma 2.4, we are now ready to reformulate the chance constrained program (2) as a deterministic optimization problem.

Theorem 2.5

The chance constrained program (2) is equivalent to

| (7) |

Proof of Theorem 2.5. The claim follows immediately by using Theorem 2.2 to reformulate the chance constraint (4) as the inequality (5), using Lemma 2.4 to express the left-hand side of (5) as a linear maximization problem and substituting the resulting constraint back into (2). \Halmos

We emphasize that the reformulation offered by Theorem 2.5 is independent of the selected ground metric . In the remainder, we assume that the ground metric is based on a norm .

2.3 Reformulation of Individual Chance Constraints

Assume now that problem (2) accommodates an individual chance constraint defined through the safety set . Individual chance constrained programs have been studied, among others, in network design (Wang 2007), vehicle routing (Gounaris et al. 2013, Ghosal and Wiesemann 2020) and portfolio optimization (Rujeerapaiboon et al. 2016, Dert and Oldenkamp 2000). By Lemma A.1 in the appendix, we have

where we adopt the convention that , and thus Theorem 2.5 allows us to reformulate problem (7) as the deterministic optimization problem

| (8) |

Unfortunately, problem (8) fails to be convex as its constraints involve fractions of convex functions. Below we show, however, that problem (8) can be reformulated as a mixed integer conic program.

Proposition 2.6

Assume that for all . For the safety set , problem (2) is equivalent to the mixed integer conic program

| (9) |

where is a suitably large (but finite) positive constant.

Proof of Proposition 2.6. We already know that the chance constrained program (2) is equivalent to the non-convex optimization problem (8). A complicating feature of this problem is the appearance of the maximum operator in the second constraint group, which evaluates the positive part of . To eliminate this maximum operator, for each we introduce a binary variable , and we re-express the member of the second constraint group via the two auxiliary constraints

| (10) |

Note that at optimality we have if is negative and otherwise. Intuitively, thus activates the less restrictive one of the two auxiliary constraints in (10). Next, we apply the variable substitutions and , which is admissible because for all . This change of variables yields the postulated reformulation (9).

To see that a finite value of is sufficient for our reformulation to be exact, we show that the expression as well as the values of and , , in (10) can all be bounded without affecting the optimal value of problem (9). This is clear for the fraction as is compact and the denominator is non-zero for all . Moreover, is nonnegative as otherwise the first constraint in (9) would be violated. For any fixed values of and , an optimal value of , , is given by . Since is bounded, it thus remains to show that can be bounded from above. Indeed, for sufficiently large (but finite) , the slope of on the left-hand side of the first constraint in (9) is . Since , we thus conclude that this constraint is violated for large values of . \Halmos

Remark 2.7

The condition that for all does not restrict the generality of our formulation. Indeed, if an optimal solution to problem (9) satisfies , then solves problem (2) since our argument in the proof of Proposition 2.6 applies to even if for some . Assume now that an optimal solution to problem (9) satisfies . In that case, the ambiguous chance constraint in problem (2) requires that . If that is the case for , it is optimal in problem (2). If, finally, an optimal solution to problem (9) satisfies and , then one would ideally like to solve a variant of problem (9) that includes the additional constraint

| (11) |

This variant of problem (9) can be solved by solving versions of problem (9), where each version includes exactly one of the constraints , , , or . One readily verifies that the solution that attains the least objective value amongst these versions of problem (9) is an optimal solution to problem (9) with the added constraint (11).

Remark 2.8

Remark 2.9

The deterministic reformulation (9) is remarkably parsimonious. For an -dimensional feasible region and an empirical distribution with data points, our reformulation (9) has binary variables, continuous decisions as well as constraints (excluding those that describe ). In comparison, a classical chance constrained formulation, which is tantamount to setting the Wasserstein radius to in problem (2), has binary variables, continuous decisions as well as constraints. Thus, adding distributional robustness only requires an additional continuous decisions as well as further constraints.

Remark 2.10

The deterministic reformulation (9) requires the specification of a sufficiently large constant , which can typically be determined by an investigation of the structure of problem (9). Alternatively, many commercial solver packages allow to directly specify the following reformulation of problem (9) via the use of piecewise linear constraints:

This formulation has the advantage that it does not require the specification of the constant .

2.4 Reformulation of Joint Chance Constraints with Right-Hand Side Uncertainty

Assume next that problem (2) accommodates a joint chance constraint defined through the safety set , in which the uncertainty affects only the right-hand sides of the safety conditions. Without loss of generality, we may assume that for all . Indeed, if , then the safety condition in the chance constraint becomes independent of the uncertainty and can thus be absorbed in . Joint chance constrained programs with right-hand side uncertainty have been proposed, among others, for problems in transportation (Luedtke et al. 2010), lot-sizing (Beraldi and Ruszczyński 2002, Küçükyavuz 2012), unit commitment (Yanagisawa and Osogami 2013) and project management (Wiesemann et al. 2012).

Observe that the complement of the safety set is now representable as , where is a closed halfspace for every . By Lemma A.1 in the appendix we have

| (12) |

With this closed-form expression for the distance to the unsafe set, we can reformulate problem (2) as a mixed integer conic program.

Proposition 2.11

For the safety set , where for all , the chance constrained program (2) is equivalent to the mixed integer conic program

| (13) |

where is a suitably large (but finite) positive constant.

Proof of Proposition 2.11. By Theorem 2.5, the chance constrained program (2) is equivalent to (7). Using (12), the member of the second constraint group in (7) can be reformulated as

To eliminate the maximum operator, we introduce a binary variable to re-express the above constraint as

A similar argument as in the proof of Proposition 2.6 shows that a finite value of is sufficient for our reformulation to be exact. \Halmos

Similar to Remark 2.10 in the previous section, many commercial solvers allow to directly specify a reformulation of problem (13) that replaces the constant with piecewise linear constraints.

Remark 2.12

The deterministic reformulation (13) has binary variables, continuous decisions as well as constraints (excluding those that describe ). In comparison, the corresponding classical chance constrained formulation has binary variables, continuous decisions as well as constraints. Thus, adding distributional robustness requires an additional continuous decisions as well as further (linear) constraints.

3 Numerical Experiments

We compare our exact reformulation of the ambiguous chance constrained program (2) with the bicriteria approximation scheme of Xie and Ahmed (2020) on a portfolio optimization problem in Section 3.1 as well as with a classical (non-ambiguous) chance constrained formulation and a Kernel density estimator based version of the ambiguous chance constrained program over a -divergence ambiguity set on a transportation problem in Section 3.2. Our goal is to investigate the computational scalability of our reformulation as well as its out-of-sample performance in a data-driven setting. All results were produced on an Intel Xeon 2.66GHz processor with 8GB memory in single-core mode using CPLEX 12.8. Following Remark 2.10, we avoid the specification of the constant in our ambiguous chance constrained program through the use of piecewise linear constraints.

3.1 Portfolio Optimization

We consider a portfolio optimization problem studied by Xie and Ahmed (2020). The problem asks for the minimum-cost portfolio investment into assets with random returns that exceeds a pre-specified target return with high probability . The problem can be cast as the following instance of the ambiguous chance constrained program (2):

| (14) |

We compare our exact reformulation of problem (14) with the -bicriteria approximation scheme of Xie and Ahmed (2020), which produces solutions that satisfy the ambiguous chance constraint in (14) with probability , , and whose costs are guaranteed to exceed the optimal costs in (14) by a factor of at most . Since the bicriteria approximation scheme can readily utilize support information for the random vector , we replace the ambiguity set with in their approach. Contrary to the experiments conducted by Xie and Ahmed (2020), we set . This is to the disadvantage of their approach, as it does not provide any approximation guarantees in that case, but it allows us to compare the resulting portfolios as they provide the same return guarantees. For the performance of the bicriteria approximation scheme with , we refer to Section 6.2 of Xie and Ahmed (2020).

In our numerical experiments, we consider a similar setting as Xie and Ahmed (2020). We set , and choose the cost coefficients uniformly at random from . Each asset return is governed by a uniform distribution on , and we assume that training samples are available. We use the -norm Wasserstein ambiguity set, which implies that our exact reformulation of problem (14) is a mixed-integer second-order cone program, and set the Wasserstein radius to . The risk threshold is set to .

| Ratio of objective values | Ratio of runtimes | |||||

| 5% | 50% | 95% | 5% | 50% | 95% | |

| 1.6 | 2.4 | 3.2 | 5.2 | 8.3 | 10.8 | |

| 1.9 | 2.9 | 5.0 | 4.9 | 7.7 | 10.6 | |

| 2.3 | 2.8 | 3.5 | 3.8 | 4.9 | 7.2 | |

| 1.0 | 1.1 | 1.3 | 7.3 | 10.9 | 13.0 | |

| 1.5 | 2.3 | 3.1 | 7.1 | 9.7 | 13.3 | |

| 2.1 | 2.7 | 3.9 | 4.2 | 6.2 | 10.1 | |

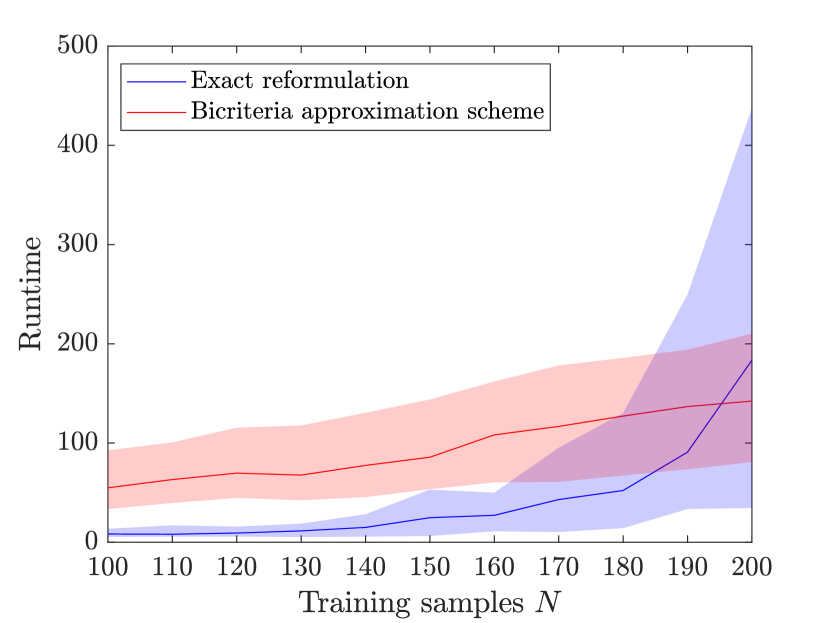

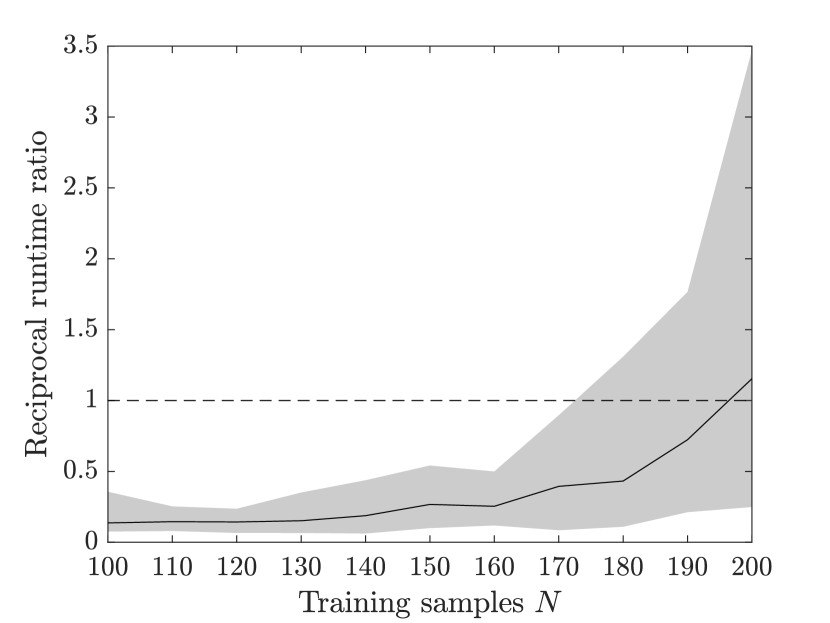

Table 1 compares the objective values and runtimes of our exact reformulation and the bicriteria approximation scheme for various combinations of the risk threshold and Wasserstein radius . The table shows that despite incorporating additional support information, the bicriteria approximation scheme determines solutions whose costs significantly exceed those of the solutions found by our exact reformulation. Perhaps more surprisingly, the bicriteria approximation scheme is also computationally more expensive. As Figure 4 shows, however, this is an artifact of the small sample size employed in the experiments of Xie and Ahmed (2020), and the bicriteria approximation scheme is faster than our exact reformulation for larger samples sizes.

3.2 Transportation

We consider a probabilistic transportation problem studied by Luedtke et al. (2010) and Yanagisawa and Osogami (2013). The problem asks for the cost-optimal distribution of a single good from a set of factories to a set of distribution centers . Each factory has an individual production capacity , and each distribution center faces a random aggregate customer demand . The cost of shipping one unit of the good from factory to distribution center is denoted by . We aim to find a transportation plan that minimizes the shipping costs, respects the production capacity of each factory and satisfies the demand at each distribution center with high probability. The problem can be cast as the following instance of problem (2):

| (15) |

Here, denotes the quantity shipped from factory to distribution center . Problem (15) is an ambiguous joint chance constrained program with right-hand side uncertainty. Since each safety condition in (15) contains a single random variable with coefficient on the right-hand side, our exact reformulation reduces to the same mixed-integer linear program for any norm .

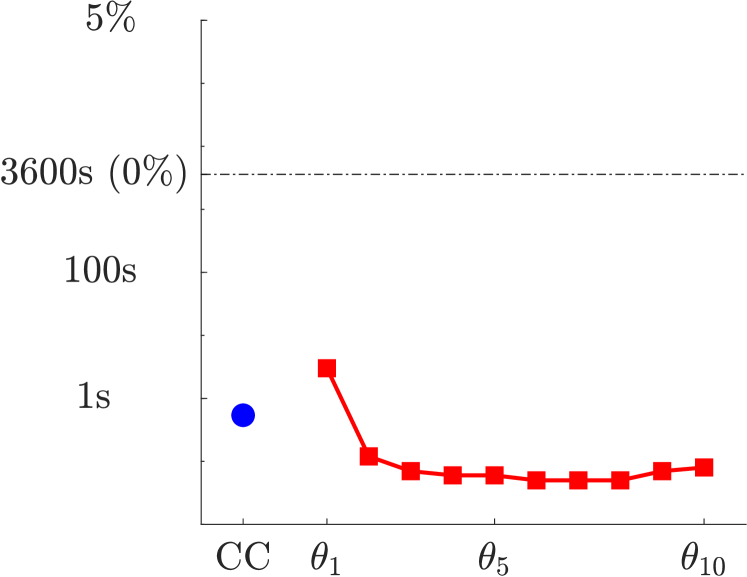

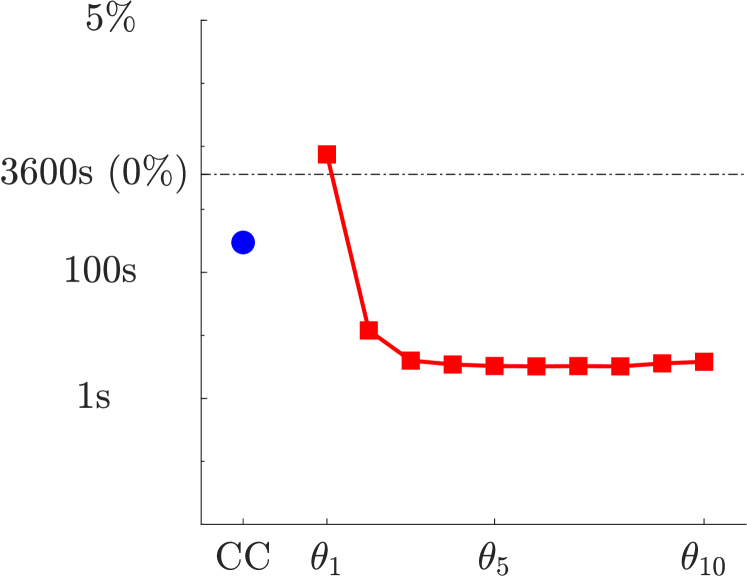

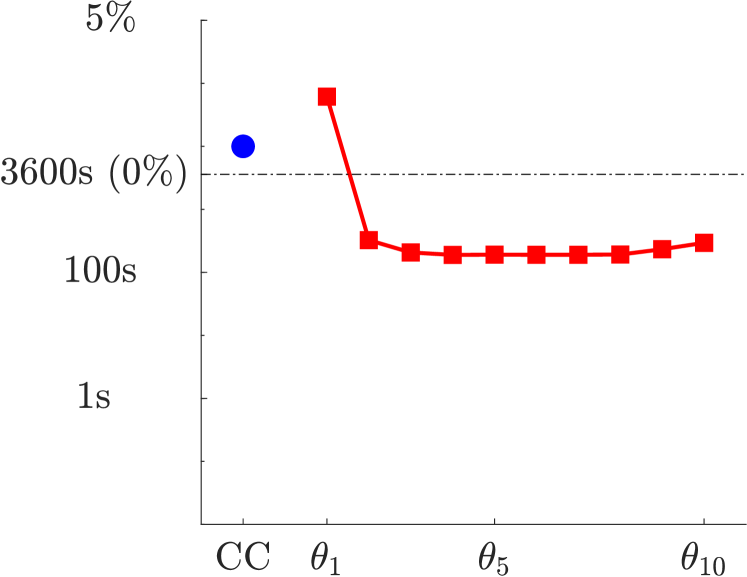

In our first experiment, we investigate the scalability of the exact reformulation of problem (15) that is offered by Proposition 2.11. To this end, we generate random test instances with factories and distribution centers that are located uniformly at random on the Euclidean plane . We identify the transportation costs with the Euclidean distances between the factories and distribution centers. The demand vector is described by , or samples from a uniform distribution that is supported on , where the expected demand at distribution center is picked uniformly at random from the interval . The capacity of each factory is chosen uniformly at random, and the capacities are subsequently scaled so that the factories can jointly produce up to of the maximum cumulative demand. For each instance, we choose ascending Wasserstein radii uniformly so that and is the smallest radius for which the corresponding instance of problem (15) becomes infeasible. We fix .

Tables 2–4 and Figure 5 compare the runtimes of our ambiguous chance constrained program with those of the classical chance constrained formulation of problem (15),

| (16) |

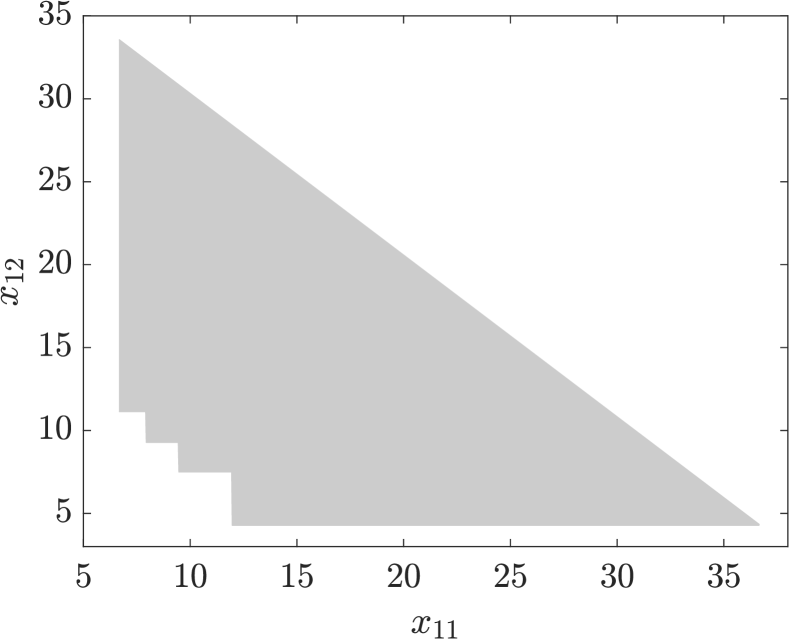

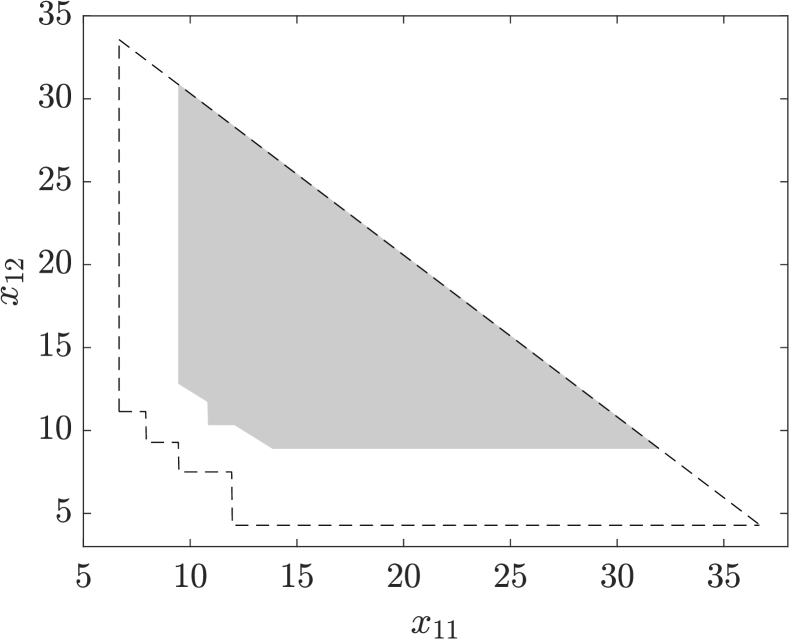

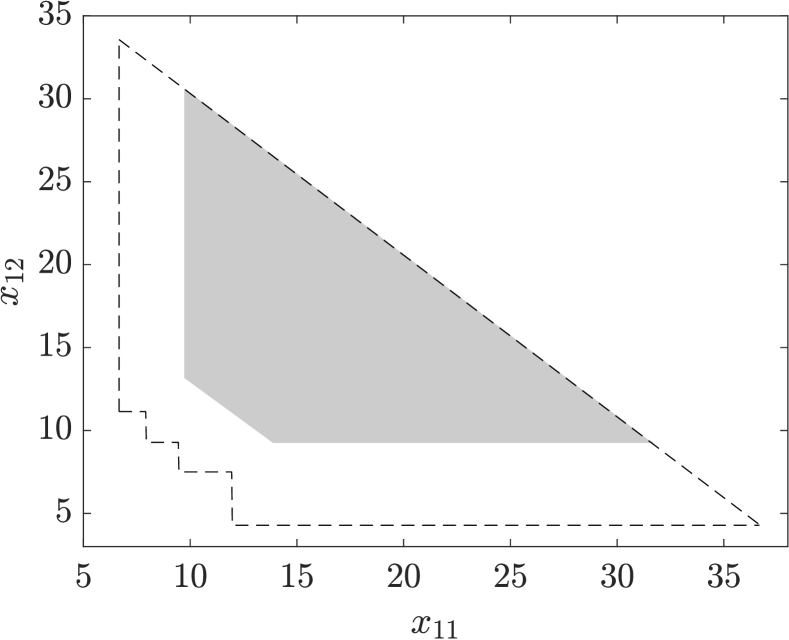

where is a sufficiently large positive constant. The results show that for the smallest Wasserstein radius , the ambiguous chance constrained program (15) is—as expected—more difficult to solve than the corresponding classical chance constrained program (16). Interestingly, the ambiguous chance constrained program becomes considerably easier to solve than the classical chance constrained program for the larger Wasserstein radii . This surprising result is explained in Figure 6, which shows that the feasible region of the ambiguous chance constrained program tends to convexify as the Wasserstein radius increases. In fact, one can show that the set of vectors that are feasible in the deterministic reformulation of problem (15) shrinks monotonically with . Since it is the presence of these binary vectors that causes the non-convexity of problem (15), one can expect the problem to become better behaved as increases.

|

CC | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10 | 0.5 | 3.0 | 0.1 | ||||||||||

| 20 | 4.0 | 9.7 | 0.2 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | |||||

| 30 | 7.3 | 13.1 | 0.3 | 0.2 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.2 | ||

| 40 | 11.2 | 19.3 | 0.4 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.3 | ||

| 50 | 15.8 | 166.5 | 0.3 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.3 | 0.3 |

|

CC | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10 | 16.3 | 166.4 | 4.7 | 2.0 | 1.5 | 1.4 | 1.4 | 1.4 | 1.4 | 1.5 | 1.8 | ||

| 20 | 93.6 | 1910.8 | 8.1 | 2.9 | 2.5 | 2.5 | 2.4 | 2.4 | 2.4 | 2.7 | 2.8 | ||

| 30 | 298.3 | 12.0 | 4.0 | 3.5 | 3.3 | 3.2 | 3.3 | 3.2 | 3.6 | 3.8 | |||

| 40 | 664.2 | 16.0 | 5.1 | 4.7 | 4.5 | 4.5 | 4.5 | 4.4 | 4.8 | 5.1 | |||

| 50 | 1,293.2 | 20.3 | 6.5 | 5.6 | 5.5 | 5.4 | 5.4 | 5.4 | 5.7 | 6.2 |

|

CC | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10 | 94.6 | 85.6 | 48.5 | 44.8 | 44.0 | 42.5 | 43.3 | 43.0 | 52.0 | 77.0 | |||

| 20 | 874.2 | 143.9 | 90.5 | 76.3 | 75.6 | 72.8 | 72.5 | 73.2 | 85.7 | 112.4 | |||

| 30 | 213.8 | 126.4 | 113.0 | 109.5 | 108.9 | 108.8 | 110.3 | 125.4 | 165.1 | ||||

| 40 | 286.8 | 168.2 | 154.2 | 149.1 | 149.3 | 151.7 | 152.1 | 182.8 | 231.5 | ||||

| 50 | 324.6 | 207.0 | 189.3 | 190.9 | 190.0 | 190.4 | 191.8 | 233.0 | 294.4 |

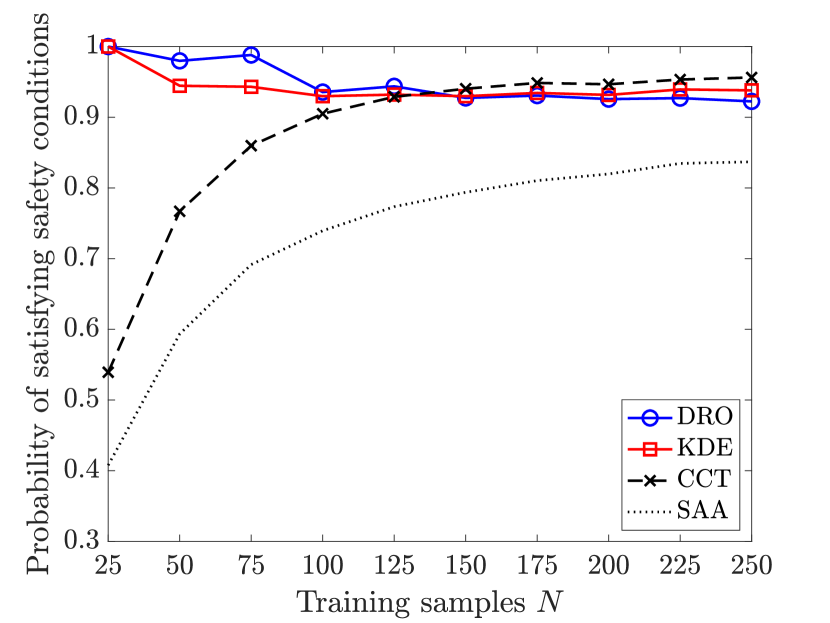

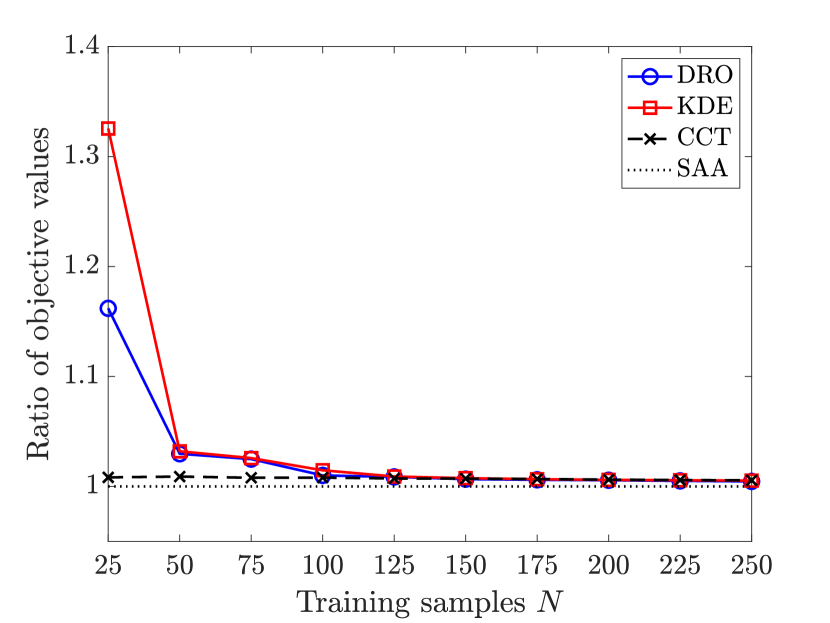

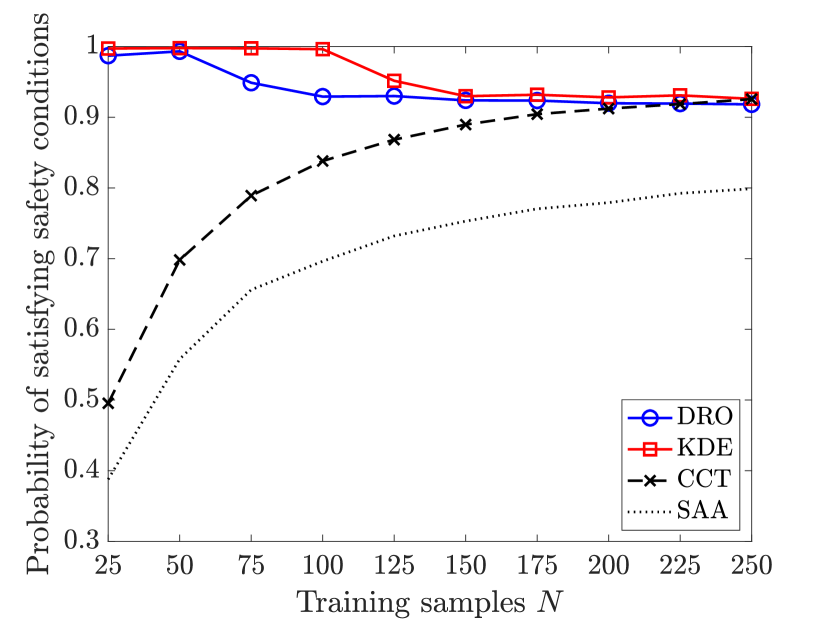

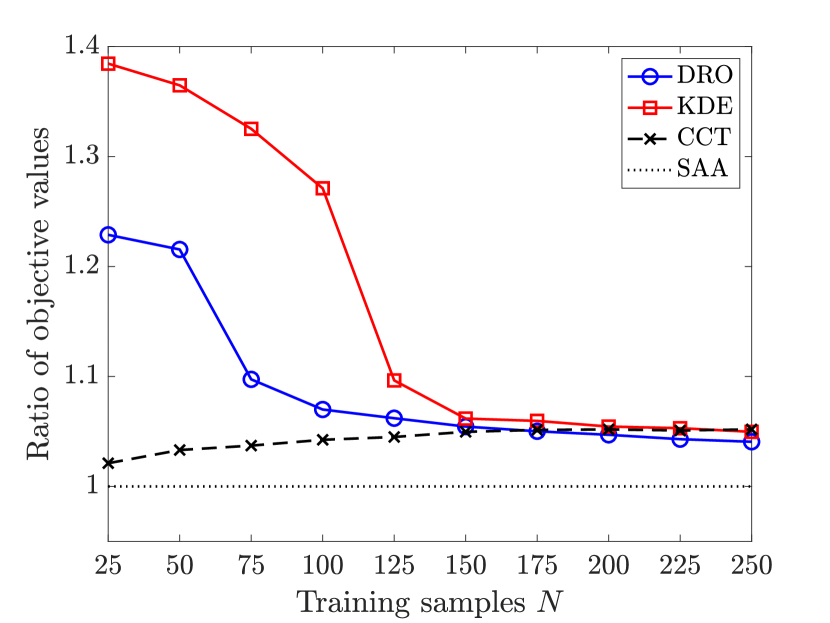

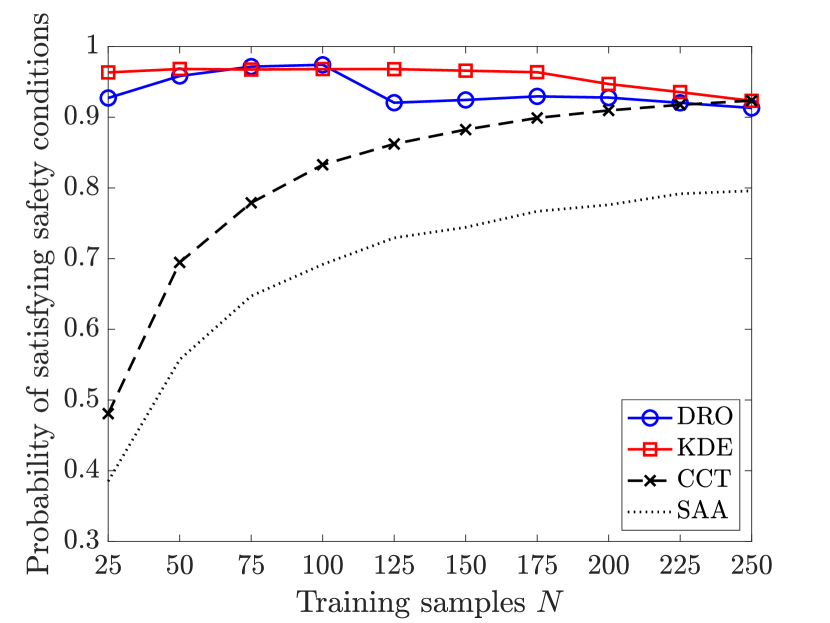

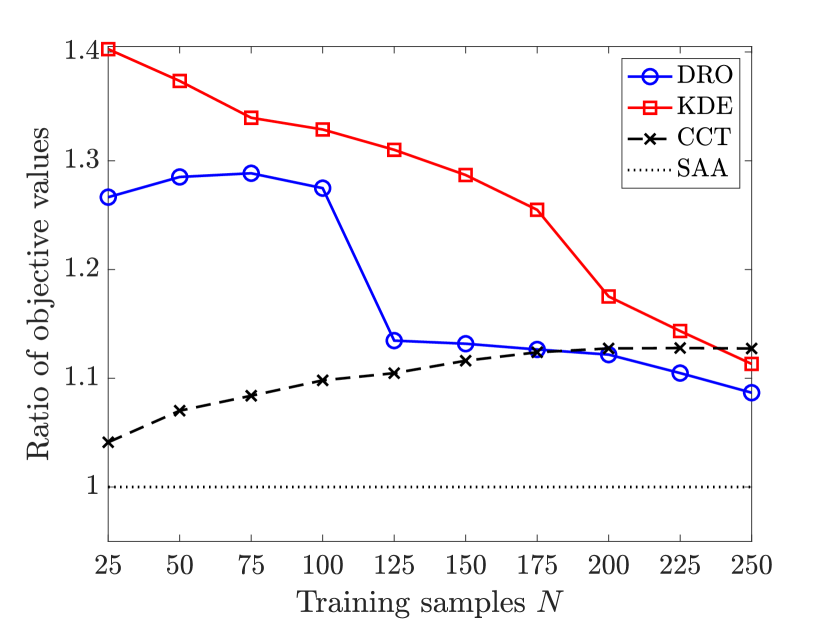

We next compare the out-of-sample performance of our ambiguous chance constrained program (15), where the risk threshold and the Wasserstein radius are selected using a -fold cross-validation on the training dataset (‘DRO’), with (i) the classical chance constrained program (16), where the risk threshold is fixed to (‘SAA’), (ii) a variant of the classical chance constrained program (16), where the risk threshold is selected using a -fold cross-validation on the training dataset (‘CCT’), as well as (iii) a Kernel density estimator based version of the ambiguous chance constrained program over a -divergence ambiguity set, where the risk threshold and the bandwidth of the Gaussian kernel are selected using a -fold cross-validation on the training dataset (‘KDE’; see Jiang and Guan 2016). We note that CCT can be regarded as a cross-validated version of the ‘best data-driven reformulation’ proposed by Lam (2019). We generate random problem instances with factories, distribution centers and , , …, training samples. In all experiments, the expected demand at distribution center is picked uniformly at random from the interval , whereas the actual demands follow a uniform distribution that is supported on (Figure 7), a normal distribution with mean and covariance matrix (Figure 8) or an exponential distribution where each distribution center faces a demand , where follows an exponential distribution with parameter (Figure 9). In all cases, the demands are truncated to the non-negative real line. Our results indicate that the classical chance constrained program (16) generates solutions that significantly violate the chance constraint, even if we select the risk threshold out-of-sample. The two ambiguous chance constrained formulations, on the other hand, achieve the desired risk threshold, often at a modest increase in transportation costs. While our approach and the -divergence ambiguity set perform similarly, our formulation appears to result in lower transportation costs, especially when data is scarce.

Acknowledgments

The authors are grateful to the review team for constructive comments that led to substantial improvements of the paper. The authors gratefully acknowledge financial support from the ECS grant 9048191, the SNSF grant BSCGI0157733 and the EPSRC grant EP/N020030/1.

References

- Arrigo et al. (2022) Arrigo, Adriano, Christos Ordoudis, Jalal Kazempour, Zacharie De Grève, Jean-François Toubeau, François Vallée. 2022. Wasserstein distributionally robust chance-constrained optimization for energy and reserve dispatch: an exact and physically-bounded formulation. European Journal of Operational Research 296(1) 304–322.

- Ben-Tal and Nemirovski (2001) Ben-Tal, Aharon, Arkadi Nemirovski. 2001. Lectures on modern convex optimization: analysis, algorithms, and engineering applications. SIAM.

- Beraldi and Ruszczyński (2002) Beraldi, Patrizia, Andrzej Ruszczyński. 2002. A branch and bound method for stochastic integer problems under probabilistic constraints. Optimization Methods and Software 17(3) 359–382.

- Blanchet et al. (2019) Blanchet, Jose, Yang Kang, Karthyek Murthy. 2019. Robust Wasserstein profile inference and applications to machine learning. Journal of Applied Probability 56(3) 830–857.

- Blanchet and Murthy (2019) Blanchet, Jose, Karthyek Murthy. 2019. Quantifying distributional model risk via optimal transport. Mathematics of Operations Research 44(2) 565–600.

- Carlsson et al. (2018) Carlsson, John Gunnar, Mehdi Behroozi, Kresimir Mihic. 2018. Wasserstein distance and the distributionally robust TSP. Operations Research 66(6) 1603–1624.

- Chen and Xie (2021) Chen, Zhi, Weijun Xie. 2021. Sharing the value-at-risk under distributional ambiguity. Mathematical Finance 31(1) 531–559.

- Delage and Ye (2010) Delage, Erick, Yinyu Ye. 2010. Distributionally robust optimization under moment uncertainty with application to data-driven problems. Operations Research 58(3) 595–612.

- Dert and Oldenkamp (2000) Dert, Cees, Bart Oldenkamp. 2000. Optimal guaranteed return portfolios and the casino effect. Operations Research 48(5) 768–775.

- Gao et al. (2017) Gao, Rui, Xi Chen, Anton J Kleywegt. 2017. Distributional robustness and regularization in statistical learning. arXiv preprint arXiv:1712.06050.

- Gao and Kleywegt (2016) Gao, Rui, Anton J Kleywegt. 2016. Distributionally robust stochastic optimization with Wasserstein distance. arXiv preprint arXiv:1604.02199.

- Ghosal and Wiesemann (2020) Ghosal, Shubhechyya, Wolfram Wiesemann. 2020. The distributionally robust chance-constrained vehicle routing problem. Operations Research 68(3) 716–732.

- Goh and Sim (2010) Goh, Joel, Melvyn Sim. 2010. Distributionally robust optimization and its tractable approximations. Operations Research 58(4) 902–917.

- Gounaris et al. (2013) Gounaris, Chrysanthos E, Wolfram Wiesemann, Christodoulos A Floudas. 2013. The robust capacitated vehicle routing problem under demand uncertainty. Operations Research 61(3) 677–693.

- Ho-Nguyen et al. (2020) Ho-Nguyen, Nam, Fatma Kılınç-Karzan, Simge Küçükyavuz, Dabeen Lee. 2020. Strong formulations for distributionally robust chance-constrained programs with left-hand side uncertainty under Wasserstein ambiguity. arXiv preprint arXiv:2007.06750.

- Ho-Nguyen et al. (2021) Ho-Nguyen, Nam, Fatma Kılınç-Karzan, Simge Küçükyavuz, Dabeen Lee. 2021. Distributionally robust chance-constrained programs with right-hand side uncertainty under Wasserstein ambiguity. Mathematical Programming 1–32.

- Hu and Hong (2013) Hu, Zhaolin, Jeff Hong. 2013. Kullback-Leibler divergence constrained distributionally robust optimization. Available at Optimization Online.

- Jiang and Guan (2016) Jiang, Ruiwei, Yongpei Guan. 2016. Data-driven chance constrained stochastic program. Mathematical Programming 158(1-2) 291–327.

- Jiang and Guan (2018) Jiang, Ruiwei, Yongpei Guan. 2018. Risk-averse two-stage stochastic program with distributional ambiguity. Operations Research 66(5) 1390–1405.

- Jiang et al. (2021) Jiang, Zhenlong, Ran Ji, Sasha Dong. 2021. A distributionally robust chance-constrained model for humanitarian relief network design. Available at SSRN 3929286.

- Küçükyavuz (2012) Küçükyavuz, Simge. 2012. On mixing sets arising in chance-constrained programming. Mathematical programming 132(1-2) 31–56.

- Lam (2019) Lam, Henry. 2019. Recovering best statistical guarantees via the empirical divergence-based distributionally robust optimization. Operations Research 67 1090–1105.

- Luedtke et al. (2010) Luedtke, James, Shabbir Ahmed, George L Nemhauser. 2010. An integer programming approach for linear programs with probabilistic constraints. Mathematical Programming 122(2) 247–272.

- Mohajerin Esfahani and Kuhn (2018) Mohajerin Esfahani, Peyman, Daniel Kuhn. 2018. Data-driven distributionally robust optimization using the Wasserstein metric: performance guarantees and tractable reformulations. Mathematical Programming 171(1-2) 1–52.

- Pflug and Wozabal (2007) Pflug, Georg, David Wozabal. 2007. Ambiguity in portfolio selection. Quantitative Finance 7(4) 435–442.

- Rujeerapaiboon et al. (2016) Rujeerapaiboon, Napat, Daniel Kuhn, Wolfram Wiesemann. 2016. Robust growth-optimal portfolios. Management Science 62(7) 2090–2109.

- Serfling (2009) Serfling, Robert J. 2009. Approximation theorems of mathematical statistics, vol. 162. John Wiley & Sons.

- Shafieezadeh-Abadeh et al. (2019) Shafieezadeh-Abadeh, Soroosh, Daniel Kuhn, Peyman Mohajerin Esfahani. 2019. Regularization via mass transportation. Journal of Machine Learning Research 20(103) 1–68.

- Shen and Jiang (2021) Shen, Haoming, Ruiwei Jiang. 2021. Convex chance-constrained programs with Wasserstein ambiguity. arXiv preprint arXiv:2111.02486.

- Sinha et al. (2017) Sinha, Aman, Hongseok Namkoong, John Duchi. 2017. Certifiable distributional robustness with principled adversarial training. arXiv preprint arXiv:1710.10571.

- Wang (2007) Wang, Jiamin. 2007. The -reliable median on a network with discrete probabilistic demand weights. Operations Research 55(5) 966–975.

- Wiesemann et al. (2012) Wiesemann, Wolfram, Daniel Kuhn, Berç Rustem. 2012. Multi-resource allocation in stochastic project scheduling. Annals of Operations Research 193(1) 193–220.

- Wiesemann et al. (2014) Wiesemann, Wolfram, Daniel Kuhn, Melvyn Sim. 2014. Distributionally robust convex optimization. Operations Research 62(6) 1358–1376.

- Xie (2019) Xie, Weijun. 2019. On distributionally robust chance constrained programs with Wasserstein distance. Mathematical Programming 1–41.

- Xie and Ahmed (2020) Xie, Weijun, Shabbir Ahmed. 2020. Bicriteria approximation of chance-constrained covering problems. Operations Research 68(2) 516–533.

- Yanagisawa and Osogami (2013) Yanagisawa, H., T. Osogami. 2013. Improved integer programming approaches for chance-constrained stochastic programming. Proceedings of the 23rd International Joint Conference on Artificial Intelligence. 2938–2944.

- Zhang and Dong (2021) Zhang, Yiling, Jin Dong. 2021. Building load control using distributionally robust chance-constrained programs with right-hand side uncertainty and the risk-adjustable variants. arXiv preprint arXiv:2104.11312.

- Zhao and Guan (2018) Zhao, Chaoyue, Yongpei Guan. 2018. Data-driven risk-averse stochastic optimization with Wasserstein metric. Operations Research Letters 46(2) 262–267.

Appendix A Distance to a Union of Halfspaces

The distance of a point to a closed set with respect to a norm is defined as

Note that the minimum is always attained. In the following, we derive a closed-form expression for the distance of a point to the union of finitely many closed halfspaces.

Lemma A.1

Let be a closed halfspace for each . If denotes the union of all halfspaces, then the distance of a point to is given by

Proof of Lemma A.1. We first prove the assertion for , in which case . We thus have

where the second equality follows from strong conic duality, which holds because the primal minimization problem is strictly feasible. Similarly, for we find

where the second equality follows from the first part of the proof. \Halmos