drmac@math.hr (Z. Drmač), mezic@engr.ucsb.edu (I. Mezić), mohrr@aimdyn.com (R. Mohr)

Data driven Koopman spectral analysis in Vandermonde–Cauchy form via the DFT: numerical method and theoretical insights

Abstract

The goals and contributions of this paper are twofold. It provides a new computational tool for data driven Koopman spectral analysis by taking up the formidable challenge to develop a numerically robust algorithm by following the natural formulation via the Krylov decomposition with the Frobenius companion matrix, and by using its eigenvectors explicitly – these are defined as the inverse of the notoriously ill–conditioned Vandermonde matrix. The key step to curb ill–conditioning is the discrete Fourier transform of the snapshots; in the new representation, the Vandermonde matrix is transformed into a generalized Cauchy matrix, which then allows accurate computation by specially tailored algorithms of numerical linear algebra. The second goal is to shed light on the connection between the formulas for optimal reconstruction weights when reconstructing snapshots using subsets of the computed Koopman modes. It is shown how using a certain weaker form of generalized inverses leads to explicit reconstruction formulas that match the abstract results from Koopman spectral theory, in particular the Generalized Laplace Analysis.

keywords:

Dynamic Mode Decomposition, Koopman operator, Krylov subspaces, proper orthogonal decomposition, Rayleigh-Ritz approximation, Vandermonde matrix, Discrete Fourier Transform, Cauchy matrix, Generalized Laplace Analysis15A12, 15A23, 65F35, 65L05, 65M20, 65M22, 93A15, 93A30, 93B18, 93B40, 93B60, 93C05, 93C10, 93C15, 93C20, 93C57

1 Introduction

Dynamic Mode Decomposition is a data driven spectral analysis technique for a time series. For a sequence of snapshot vectors in , assumed driven by a linear operator , , the goal is to represent the snapshots in terms of the computed eigenvectors and eigenvalues of . Such a representation of the data sequence provides an insight into the evolution of the underlying dynamics, in particular on dynamically relevant spatial structures (eigenvectors) and amplitudes and frequencies of their evolution (encoded in the corresponding eigenvalues) – it can be considered a finite dimensional realization of the Koopman spectral analysis, corresponding to the Koopman operator associated with the dynamics under study [1]. This important theoretical connection with the Koopman operator and the ergodic theory, and the availability of numerical algorithm [34] make the DMD a tool of trade in computational study of complex phenomena in fluid dynamics, see e.g. [31], [41]. A peculiarity of the data driven setting is that direct access to the operator is not available, thus an approximate representation of is achieved using solely the snapshot vectors whose number is usually much smaller than the dimension of the domain of .

In this paper, we revisit the natural formulation of finite dimensional Koopman spectral analysis in terms of Krylov bases and the Frobenius companion matrix. In this formulation, reviewed in §2.1 below, a spectral approximation of is obtained by the Rayleigh–Ritz extraction using the primitive Krylov basis . This means that the Rayleigh quotient of is the Frobenius companion matrix, whose eigenvector matrix is the inverse of the Vandermonde matrix , parametrized by its eigenvalues . The DMD (Koopman) modes, that is, the Ritz vectors , are then computed as . Then, from we readily have for .

Unfortunately, Vandermonde matrices can have extremely high conditions numbers, so a straight-forward implementation of this algebraically elegant scheme can lead to inaccurate results in finite precision computation. Most other DMD-variants bypass this issue by computing an orthonormal basis from the snaphshots using a truncated singular value decomposition [34, 33, 38]. We note that the original formulation of DMD was based on the SVD ([34], reviewed in Algorithm 1 in this paper), whereas the first connection between DMD and Koopman operator theory was formulated in terms of the companion matrix [32]. In Rowley et al. [32], though, there was no consideration of the deep numerical issues related to working with Vandermonde matrices which has likely contributed to the prevalence of the SVD-based variants of DMD. There is, however, a certain intrinsic elegance in the decomposition of the snapshots in terms of the spectral structure of the companion matrix in addition to a stronger connection to Generalized Laplace Analysis (GLA) theory [27, 26] of Koopman operator theory than the SVD-based DMD variants have.

Following this natural formulation, we present a DMD algorithm capable of numerically robust computing without resorting to the singular value decomposition of . We do this by leveraging high accuracy numerical linear algebra techniques to curb the potential ill-conditioning of the Vandermonde matrix. The key step is to transform the snapshot matrix by the discrete Fourier transform (DFT) – this induces a similarity of the companion matrix, and transforms its eigenvector matrix into the inverse of a generalized Cauchy matrix, which then allows accurate computation by specially tailored algorithms. This will be achieved using the techniques introduced in [10], [9]. We present the details of our formulation in section 3. Numerical example presented in section 4, where the spectral condition number of is above , illustrates the potential of the proposed method.

While the full collection of DMD modes and eigenvalues gives insight into the intrinsic physics, in many applications a reduced-order model is required. Thus reconstructions of the snapshots using a subset of the modes (selected using some criteria that we do not address here) is desired. We take up the subject of optimal reconstruction of the snapshots in section 5. The problem of computing optimal reconstruction weights is formulated in terms of reflexive g-inverses (see [30]), which are somewhat weaker than the more well-known Moore-Penrose pseudo-inverse. It is this set of results that is closely linked with Generalized Laplace Analysis (GLA). We compare formulas for the optimal reconstruction weights, derived in section 5, with reconstruction formulas given by GLA theory in section 6. Whereas the GLA reconstruction formulas have the form of a (finite) ergodic average, the optimal reconstruction formulas can be formulated as a non-uniformly weighted (finite) ergodic average which reduces to the GLA version for unitary spectrum. It is also interesting to note that while the reconstruction formulas from section 5 optimally reconstruct (by definition) any finite set of snapshots, they are not asymptotically consistent in the sense that they do not recover the correct expansion of the observable in terms of eigenvectors in the limit of infinite data. On the other hand, while the GLA reconstruction formulas are sub-optimal (for general operators possessing non-unitary spectrum) for any finite set of snapshots, they are asymptotically consistent, recovering the correct expansion in the limit. We also show that the least squares problem, solved via the g-reflexive inverses defined on a tensor product of coefficient spaces, is equivalent to an eigenvector-adapted hermitian form in state space.

2 Preliminaries

In this section, we set the scene and review results relevant for the later development. We assume that the data vectors are generated by a matrix via for some given initial . As a technical simplification, a generic case is assumed, i.e. that is diagonalizable, and that its Ritz values with respect to the subspaces spanned by the snapshots are simple. We can think of the snapshots as being generated by e.g. black–boxed numerical software for solving a partial differential equation with initial condition , or e.g. as vectorized images of flames in combustion chamber, taken by a high-speed camera. The goal is to represent the snapshots of the underlying dynamics using the (approximate) eigenvectors and eigenvalues of .

2.1 Spectral analysis using Krylov basis

The data driven framework leaves little room to maneuver; hence we resort to the classical Rayleigh-Ritz approximations from the Krylov subspaces spanned by the snapshots. Let be the column partitioned matrix . The columns of span the Krylov subpsace . Without loss of generality, we assume that is of full rank. The action of on can be represented as

| (1) |

where the ’s are the -basis coefficients of the orthogonal projection of onto , and, with , is orthogonal to ; . Hence , where is the Moore–Penrose generalized inverse of . Thus, the Frobenius companion matrix is the matrix representation of the Rayleigh quotient in the basis formed by the columns of . In practical computation, the coefficients of are obtained from the solution of the least squares problem .

The spectral decomposition of has beautiful structure. Assume for simplicity that the eigenvalues , , are algebraically simple. It is easily checked that the rows of are the left eigenvectors of , so the columns of are the (right) eigenvectors of ; they are essentially unique. Hence, the spectral decomposition of reads

| (2) |

Proposition 2.1.

The columns of are the Ritz vectors, with the corresponding Ritz values . For a Ritz pair , the residual is given by

| (3) |

Proof 2.2.

It holds that , where for the last row of we can use the formulas from [39] to obtain

Hence, for a particular Ritz pair we have

| (4) |

2.1.1 Modal representation of the snapshots

Once the Ritz pairs have provided useful spectral information on , we would like to analyze the snapshots in terms of spectral data. To that end, write

| (5) |

and, with the column partition of , define

| (6) |

Then, from the first relation in (5), we have

| (7) |

and from the last column in the second relation in (5) we have

| (8) |

It is important to note that the decompositions (or reconstructions) (7, 8) are by definition attached to the Ritz pairs of , formed using the spectral decomposition (2) of the matrix representation of . If is close to being an -invariant subspace, then , i.e. the decompositions (7, 8) are approximately in terms of the eigenpairs of .

Remark 2.3.

Note that , , and that

Of course, we can replace each term with (thus redefining and ) without affecting the decompositions (7, 8), but this normalization to real ’s seems reasonable if we interpret those numbers as amplitudes. Further, the amplitudes and the scalings of the Ritz vectors can be done in some other appropriate norm instead of in . However if we pursued the computation of modes from more than one initial condition, the complex form of the amplitudes would be enforced by the requirement that modes are independent of initial conditions [25].

2.2 On computing the eigenvalues of

Since the spectral decomposition (2) of is given explicitly from its eigenvalues, it remains to compute the ’s efficiently and in a numerically robust way. Computing the eigenvalues of is equivalent to finding the zeros of its characteristic polynomial , but this is only an elegant theoretical connection that has limited value in practical computation. In fact, the most robust polynomial root finding procedure is based on solving the matrix eigenvalue problem, while taking the structure of the companion matrix into account. For an excellent mathematical elucidation we refer to [17], [29].

From the software point of view, if we want truly high performance, both in terms of numerical robustness and run time efficiency, using an eigenvalue method for general matrices (such as e.g. eig() in Matlab) is not the best choice. Namely, in that case the eigenvalues are extracted from the Schur form with the backward error that is small in the sense that is of the order of the machine roundoff , but is not a companion matrix and there is no information on the size of the backward error in the coefficients . Further, the computation requires memory space and flops.

Proper method for this case is the one that preserves the structure of the companion matrix and for which the computed eigenvalues correspond exactly to the eigenvalues of a companion matrix with coefficients , where is small. Note that backward stability in terms of the coefficients is proper framework for assessing the numerical accuracy as the coefficients are the results from previous computation – solving the least squares problem . The desired complexity is in memory space and in flop count.

Two methods that satisfy the above requirements are presented in [5], [2] and they should be used in high performance software implementations. Particularly interesting is the unitary–plus–rank one formulation

| (9) |

which has been exploited in [5] to construct an efficient implicit QR iterations process that requires memory and flops. This splitting, when plugged into (1), provides the following intersting form of the Krylov decomposition.

Proof 2.5.

Note that , where .

An important remark is in order.

Remark 2.6.

If the eigenvalues ’s of are computed as ’s with small backward error in the vector of the coefficients , then is (assuming that all ’s are algebraically simple) the exact eigenvector matrix of the companion matrix defined by , where is small. To appreciate this fact more, consider the general case. If we compute the eigenvectors of a general square matrix , then the accuracy depends on the condition number of the eigenvectors and on the gap between an eigenvalue and it neighbors in the spectrum. More precisely, if is a simple eigenvalue of a diagonalizable , with unit eigenvector , then with appropriate nonsingular and , is diagonal. If is an eigenpair of , then, under some additional assumptions,

So, for instance, if a group of eigenvalues is tightly clustered, then their corresponding eigenvectors are extremely sensitive and difficult to compute numerically. Here we can set , where is the residual. For more details ee e.g. [8], [35, Ch. V.,§2], [7, §3.2.2].

2.3 Computation with Vandermonde matrices

The natural representation of the evolving dynamics by the Krylov decomposition (1) and the simple and elegant snapshots’ decompositions (7, 8) have not lead to a numerical scheme that can be used in practical computations. The reason is in numerical difficulties when computing the matrix of the Ritz vectors, due to potentially extremely high condition number of the Vandermonde matrix .

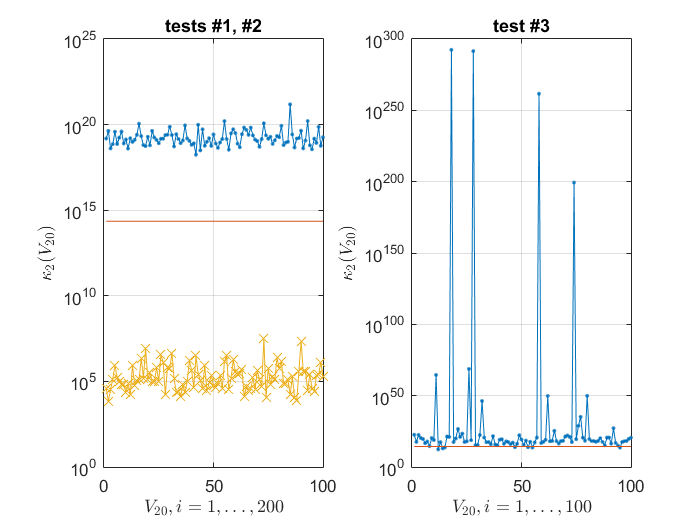

And indeed, the Vandermonde matrices can be arbitrarily badly ill-conditioned [28]. More precisely, the condition number will depend on the distribution of the eigenvalues and it can be as small as one and it can grow with the dimension as fast as for harmonically distributed ’s, see Gautschi [19], [18]. For example, any real Vadermonde matrix has condition number greater than . As an illustration, we show on Figure 1 the values of on three sets, each containing matrices. Recall that the classical upper bound on the relative error in the solution of linear systems is , so that implies no accuracy whatsoever.

On the other hand, if the ’s are the th roots of unity, then is the unitary Discrete Fourier Tranformation (DFT) matrix with . In fact, if the ’s are on the unit circle, then is, under some additional assumptions (e.g. that the nodes are not tightly clustered), usually moderate [3], [4]. If the underlying operator is nearly unitary then the ’s will be close to the unit circle and is usually well conditioned. Further, it is well-known that the condition number can be reduced by scaling and this opens a possibility for accurate reconstruction, at least in those cases when scaling sufficiently reduces the condition number.

With an unlucky distribution of the nodes, a Vandermonde matrix can be extremely ill-conditioned even for small dimensions, e.g. if is small, then both matrices

can be turned into singular ones by small changes, so their condition numbers are . Furthermore, the rows as well as the columns of both and above are nearly equilibrated (nearly of same , or norm) so that the condition number cannot be improved by diagonal scalings.

In certain cases, accurate computation is possible independent of the condition number. The Björck-Pereyra algorithm [6] can solve the Vandermonde system to high accuracy if the ’s are real, of same sign and increasingly ordered, see [22]. It is the distribution of the signs that determines whether a catastrophic cancellation can occur and in our case, unfortunately, we cannot rely on such a constellation of the Ritz values as the ’s are in general complex numbers. Our main goal in this work is to provide a numerically robust implementation of the snapshot reconstruction scheme outlined in §2.1, that is independent of the distribution of the Ritz values .

2.4 Reconstruction using Schmid’s DMD – an alternative to working with Vandermonde matrices

To alleviate numerical difficulties caused by the inherent ill-conditioning of the matrix and of the eigenvalues of the companion matrix, Schmid [34] proposed using, instead of the companion matrix , the Rayleigh quotient , where is the SVD of . More precisely, the SVD is used to determine a numerical rank of , and then the Rayleigh quotient is , where the columns of are the leading left singular vectors of . The resulting scheme, designated as DMD (Dynamic Mode Decomposition) and outlined in Algorithm 1 below, has become a tool of trade in computational fluid dynamics.

-

•

that define a sequence of snapshots pairs . (Tacit assumption is that is large and that .)

In this way, the matrix of the Ritz vectors and the amplitudes for the representation of the snapshot are computed without having to invert Vandermonde matrix. The two approaches are algebraically equivalent, and in the following proposition we provide the details.

Proof 2.8.

Let , with , . Since

we have , and Further, since is assumed simple, and are collinear and thus, is collinear with . Note that

Since , it holds with some ,

and the corresponding Ritz vector then reads

Hence, , , and we seek reconstruction in the form

| (12) |

Note that such a decomposition exists by (7), and (12) is just a way of expressing it in terms of Algorithm 1. If we equate the first columns on both sides in the above relation, then solving for the ’s and using (7) yields111Note that .

| (13) |

In terms of the quantities computed by Schmid’s method, the representations (7, 8) hold with instead of . As discussed in Remark 2.3, we can scale by and replace with .

If Algorithm 1 uses , then is a Rayleigh quotient of , and the columns of are not the same Ritz vectors as in from (6). For more details on this connection, we refer to [12].

Remark 2.9.

In the framework of the Schmid’s DMD, the amplitudes are usually determined by the formula (13). Since (see line 6. in Algorithm 1) and , instead of applying the pseudoinverse of the explicitly computed , we use more the more efficient formula

| (14) |

Recall that we assume that all ’s are mutually distinct, so is of full rank. Since it can be ill-conditioned, we can use the (possibly truncated) SVD of and determine the ’s as least squares solution. In the case of numerical rank deficiency in , we can choose/prefer sparse solution (instead of the least norm).

Remark 2.10.

Recently, in [12], we proposed a new computational scheme – Refined Rayleigh Ritz Data Driven Modal Decomposition. It follows the DMD scheme, but it further allows data driven refinement of the Ritz vectors and computable data driven residuals.

3 Numerical algorithm for computing

There is certain intrinsic elegance in the snapshots reconstructions (7, 8) based on the spectral structure of the companion matrix (2). Unfortunately, the potentially high condition number of precludes exploiting it in numerical computations. Indeed, even in relatively simple examples we can encounter as high as , or higher. If is computed in the standard double precision arithmetic with the roundoff , the classical perturbation theory estimates the relative error in the computed result essentially as222Up to an factor that is polynomial in the dimensions of the problem. (e.g. ), thus rendering the output as entirely wrong and useless. The Shmid’s DMD provides an alternative path that avoids , as outlined in §2.4.

We now explore another way to curb ill-conditioning, based on the methods of numerical linear algebra [10], [9], [11]. Our starting point, based on the state of the art in numerical linear algebra, is that accurate computation with notoriously ill-conditioned Vandermonde matrices may be possible despite high classical condition number.

3.1 A review of accurate computation with Vandermonde matrices

For the reader’s convenience, we briefly describe the two main components of computational schemes capable of performing linear algebra operations with accurately in standard floating point arithmetic.

First, the Discrete Fourier Transform (DFT) of a Vandermonde matrix is a generalized Cauchy matrix parametrized by the ’s (the original parameters that define ) and the th roots of unity. In our setting, DFT is an allowable and actually meaningfully interpretable transformation, and the result obtained by using the auxiliary Cauchy matrix are easily back substituted into the original formulation. The details are given in §3.1.1.

Secondly, in the framework of [10], [9], accurate computation with generalized Cauchy matrix is possible (e.g. LDU decomposition, SVD) independent of its condition number.

3.1.1 Discrete Fourier Transform of

Let denote the Discrete Fourier Transform (DFT) matrix, , where , . Now, recall that DFT transforms Vandermonde into Cauchy matrices as follows (see [9]):

| (15) |

In other words, where and are diagonal, and is a Cauchy matrix. Note, in addition, that is unitary.

To avoid singularity (i.e. an expression of the form ) if in (15) some ’s equals an -th root of unity we proceed as follows. If for some index , write and replace (15) with the equivalent formula for the -th row

| (16) |

If is a subsequence of , and if is an submatrix of consisting of the rows with indices , then (15, 16) trivially hold for the entries of .

Note that the matrices , , are given implicitly by the parameters (eigenvalues, available on input) and the -th roots of unity , (easily computed to any desired precision and e.g. tabulated in a preprocessing phase of the computation), so that the DFT is not done by actually running an FFT. It suffices to make a note that the ’s and the roots of unity are the parameters that define as in (15, 16).

Remark 3.1.

It is interesting to see how this transformation fits the framework of the Krylov decomposition (1). Post-multiply (1) with to obtain

| (17) |

and then, using (15), and

| (18) | |||||

| (19) |

If we think of each row as a time trajectory of the corresponding observable, then represents its image in the frequency domain, and (18, 19) is the corresponding Krylov decomposition.

3.1.2 Rank revealing (LDU) decomposition of

Applying the DFT to in order to avoid the ill–conditioning of may seem a futile effort – since is unitary, . Further, Cauchy matrices are also notoriously ill-conditioned, so, in essence, we have traded one badly conditioned structure to another one.

Example 3.2.

The best known example of ill–conditioned Cauchy matrix is the Hilbert matrix, . For instance, the condition number of the Hilbert matrix satisfies . Ill-conditioning is not always obvious in the sizes of its entries – the entries of the Hilbert matrix range from to . Moreover, in Matlab, cond(hilb(100)) returns ans=4.622567959141155e+19. One should keep in mind that the matrix condition number is a matrix function with its own condition number. By a result of Higham [21], condition number of the condition number is the condition number itself, meaning that our computed condition number, if it is above (in Matlab, 1/eps=4.503599627370496e+15), it might be entirely wrongly computed. This may lead to an underestimate of extra precision needed to handle the ill–conditioning.

Although we have not changed the condition number, we have changed the representation of the data, which will allow more accurate computation. The key numerical advantage of this change of variables is in the fact that for any two diagonal matrices , and any Cauchy matrix , the pivoted LDU decomposition

| (20) |

can be computed by a specially tailored algorithm so that all entries of , , , even the tiniest ones, are computed to nearly machine precision accuracy, no matter how high is the condition number of . More precisely, if , and are the computed matrices, then, for all ,

| (21) |

where is the pivoted LDU decomposition that is computed exactly from the stored parameters. Essentially, if we take the stored (in the machine memory) eigenvalues and the roots of unity as our initial data, the first errors committed in the floating point LDU decomposition (20) are the entry-wise small forward errors (21). This is achieved by avoiding subtractions of intermediate results and using clever updates of the Schur complements, see [9].

Moreover, as a consequence of pivoting, the matrix (lower triangular with unit diagonal) and the matrix (upper triangular with unit diagonal) are well conditioned. All ill-conditioning is conspicuously exposed on the diagonal of . For instance, in the case of the Hilbert matrix from Example 3.2, and .

3.2 Cauchy matrix based reconstruction (in the frequency domain)

We now revise the relation (5), and write as . This mere insertion of the identity between and allows a natural interpretation: the time trajectories of the observables (the rows of ) have been mapped to the frequency domain, and the inverse Vandermonde matrix of the eigenvectors of has been changed with the inverse of the generalized Cauchy matrix (the eigenvectors of ); see Remark 3.1.

Following §3.1.2, compute the LDU decomposition with complete pivoting , and then apply through backward and forward substitutions,

| (22) |

The implementation of this formula depends on a particular software tool. For the reader’s convenience, in Algorithm 3 we show a simple Matlab version,333Note that we have adapted post-multiplication by to the Matlab’s definition of the functions fft(), ifft(). where the function Vand_DFT_LDU() computes the decomposition (20).

This is obviously more complicated than “backslashing” in Matlab (i.e. ) and not as efficient as the fast Vandermonde inversion techniques such as the Björck-Pereyra type algorithms that solve single Vandermonde system with complexity. But, Algorithm 3, when combined with Algorithm 2, provides superior accuracy, independent of the distribution of the ’s.

Besides ill–conditioning, one general difficulty with Vandermonde matrices is that the powers may spread, in absolute value, hundreds of orders of magnitude and that underflows and overflows may cause irreparable exceptions in machine arithmetic. An interesting salient feature of the transformation (15) is that the powers of are changed into where the only powers are those of the primitive th root of unity ; the powers of are extracted in the form on the diagonal of the scaling matrix , where they can be kept until the very end of the computation. Namely, since our goal is to compute and its column norms, we can rephrase the previous formulas as

and compute by using the LDU of , instead of (20), and the forward and backward substitutions analogously to (22). The diagonal entries of will then be assimilated as multiplicative factors in the computation of , see (6). (Analogously, we can write and invert via its pivoted LDU, but this makes not a big difference since is unitary.) This modification can be easily implemented by minor modifications in Algorithm 3 and 2; we omit the details for the sake of brevity.

3.2.1 SVD based reconstruction. Regularization

Furthermore, based on the decomposition (20), computed to high accuracy (21), we can compute accurate SVD of the product , , which gives an accurate SVD of , For details of the algorithm we refer to [14], [10], [9], [15], [16].

Now, instead of computing as a solution of linear system of equation, with the inverse , we change the framework into a regularized LS solution. Let be filter factors, and

| (23) |

For instance, the commonly used regularization is

| (24) |

Then we use the approximation

| (25) |

The key is that we have an accurate SVD even with extremely large , and that with the tuning parameter we can control the influence of the smallest singular values. This may be important in the case of noisy data – an issue not considered in this paper.

4 Numerical example: a case study

To illustrate the preceding discussion, we use the simulation data of a 2D model obtained by depth averaging the Navier–Stokes equations for a shear flow in a thin layer of electrolyte suspended on a thin lubricating layer of a dielectric fluid; see [37], [36] for more detailed description of the experimental setup and numerical simulations.444We thank Michael Schatz, Balachandra Suri, Roman Grigoriev and Logan Kageorge from the Georgia Institute of Technology for providing us with the data.

The (scalar) vorticity field data consists of snapshots of dimensions ; in this particular example , . The tensor is matricized into matrix , and is of dimensions .

The computational schemes are tested with respect to reconstruction potential as follows: for a given snapshot , the representation (7) is truncated by taking given number of modes with absolutely largest amplitudes (abbreviated as dominant modes). We note that, in general, selecting most appropriate modes is a separate nontrivial problem, not considered here.

4.1 Ill-conditioning of and diagonal scalings

In the first experiment, we illustrate the problem caused by high condition number of , and also the effects of simple diagonal scalings. More precisely, we attempt reconstruction of the snapshots as outlined in §2.1.1, using the modes computed by

-

1.

inversion of the Vandermonde matrix by the backslash operator in Matlab ;

-

2.

inversion of the row scaled Vandermonde matrix by the backslash operator in Matlab: , , where ;

-

3.

inversion of the column scaled Vandermonde matrix by the backslash operator in Matlab: , , where .

We choose the scaling in the norm, i.e. . The relevant condition numbers, estimated using the Matlab’s function cond() are as follows

| (26) |

We can also scale in or norm, with similar effect as in (26). (It is known that this scaling that equilibrates the columns, or rows, is nearly optimal in the class of all diagonal scalings, see [40].) This is instructive; we see that the condition number of can indeed be high, much higher than , and that certain diagonal scaling may reduce it enough to allow sufficiently accurate computations in machine working precision (here assumed to sixteen decimal digits).

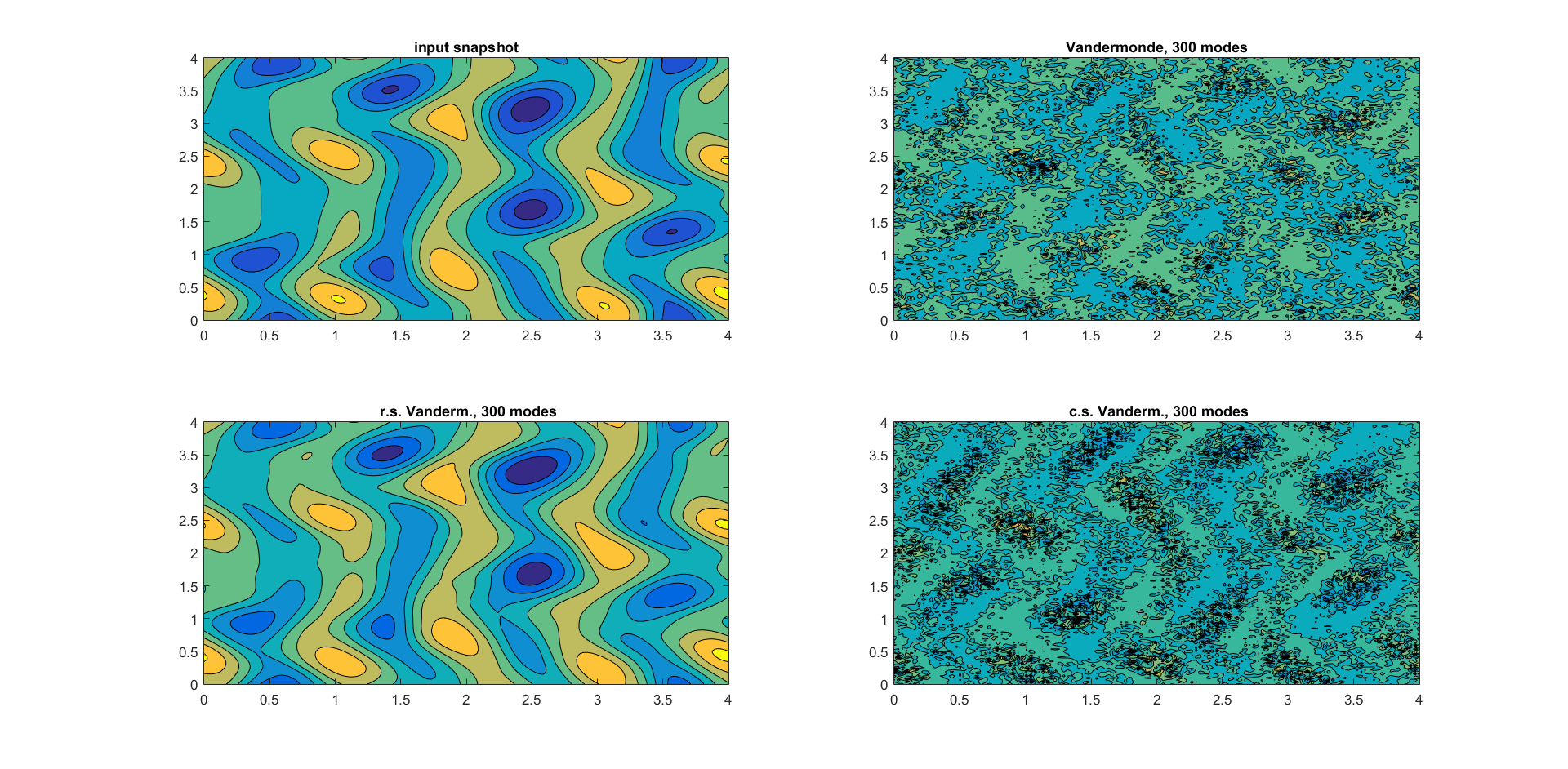

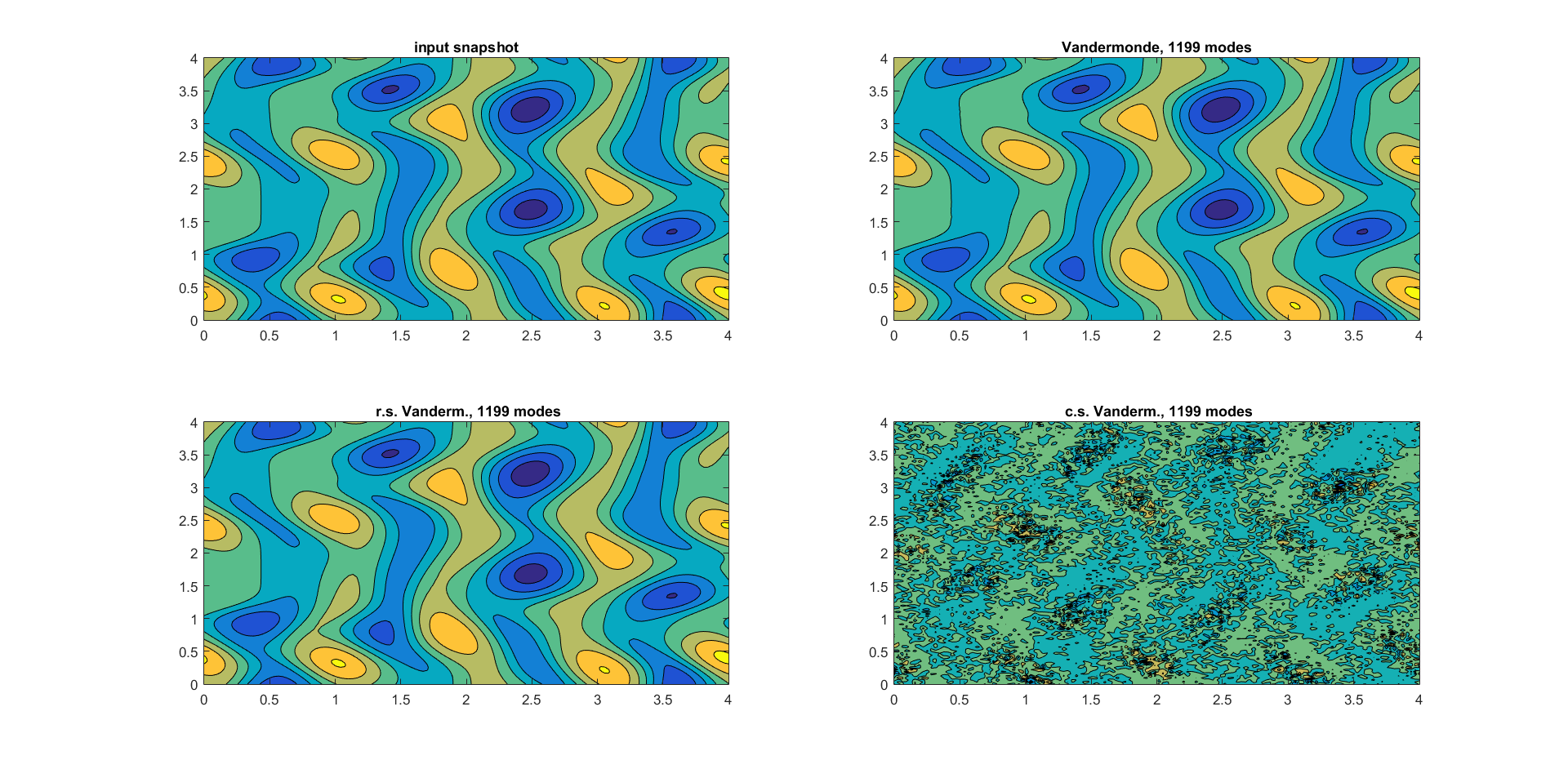

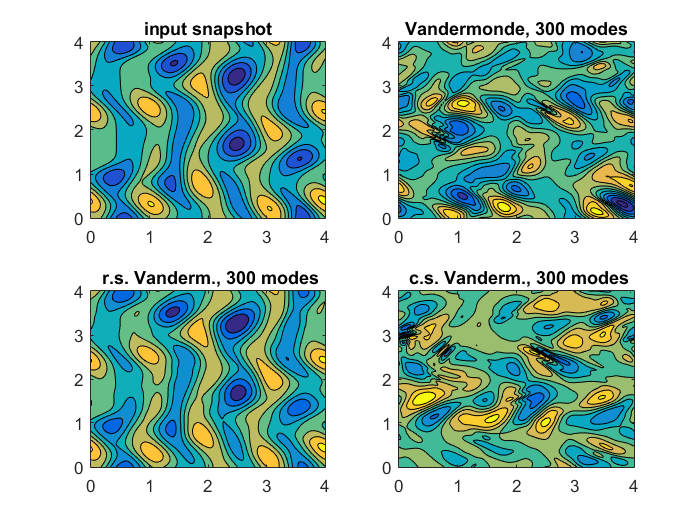

In Figure 3, we display reconstruction results for , using dominant modes. The snapshots are visualized using the contour plots over the 2D domain. The results are consistent with (26) – with the condition number above we do not expect any reasonable accuracy.

The key for the success of row scaling of is that in this case the distribution of the Ritz values is such that it allows improvement of the condition number by row scaling. Although this will not be the case in general, it provides a good case study example for numerical analysts. It should be noted that () is just a different scaling of the eigenvectors of (Ritz vectors of ), that is compensated by the corresponding scaling of the amplitudes; this scaling is as an allowable transformation – an invariant of the representation.

On the other hand, the column scaling of did not reduce the condition number enough to ensure accurate inversion, although the reduction was by more than fifty orders of magnitude. Also, this scaling is not interpretable as an invariant of the reconstruction; note that it rescales the snapshots.

It is interesting that in the case of taking all or almost all modes, the reconstruction by simply backslashing provides perfect reconstruction, see Figure 4. (This can be explained by the fact that even an inaccurate solution of a linear system of equations may have small residual.)

For an analysis of optimally selected real nodes and the potential improvement of the condition number of Vandermonde matrices by scaling we refer to [20] with a caveat – our nodes are complex and we have no luxury of selecting them. Our ultimate goal is to develop accurate computation (to the extent deemed possible by the perturbation theory) of independent of the distribution of the ’s and independent of the range of their moduli, including the case of .

4.2 Comparing Björck-Pereyera, DMD and DFT based reconstruction

Next, we do reconstruction using the following three methods:

-

1.

companion matrix formulation with the Björck-Pereyera method [6] for Vandermonde systems. Although forward stable in the special case of real and ordered ’s, this method may be very sensitive in the case of general complex ’s and relatively large dimension .

-

2.

companion matrix formulation with the DFT and inversion of the Cauchy matrix, as described in §3. Since and in (15) are unitary, Algorithm 3 solves linear system with the matrix of condition number bigger than . No additional scaling is used; we want to check the claim that such high condition number cannot spoil the result.

-

3.

Schmid’s DMD method as described in §2.4. Here we expect good reconstruction results, provided it is feasible for given data and the parameters. The SVD is not truncated because the spectral condition number of is approximately (, ).

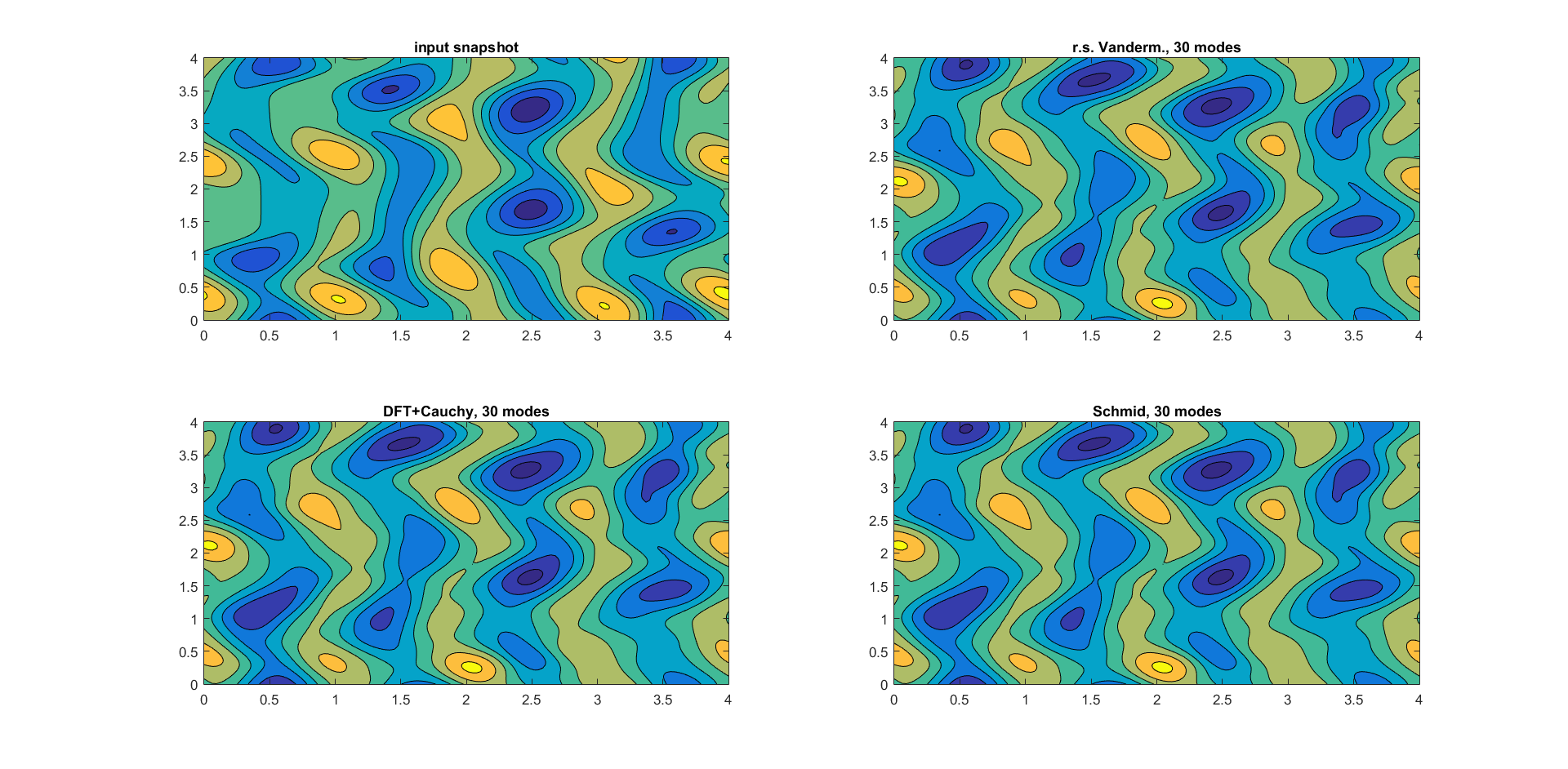

The reconstruction results for , shown on Figure 5, indicate that row scaled based computation, as well as DFT based and the Schmids’ DMD are capable of reconstructing the snapshots with relatively small number of dominant modes.

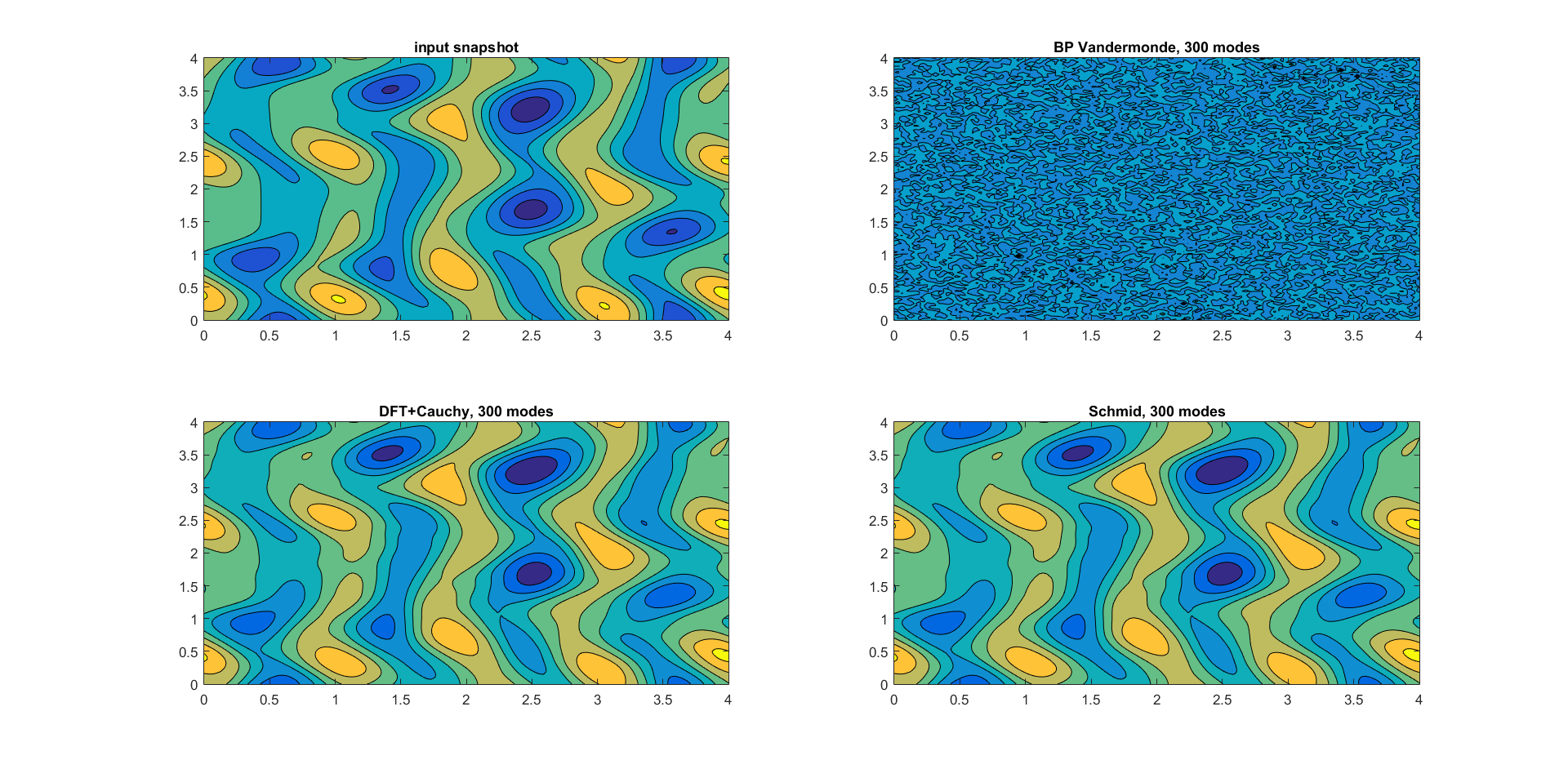

The Björck-Pereyera method was not successful, and increasing the number of modes brings no improvement, see Figure 6.

Increasing the number of modes in the reconstruction further may or may not not bring improvement, as seen in Figure 7. Ar first, it may come as a surprise that the SVD based DMD starts failing after taking more and more nodes. On the other hand, we must take into account that the left singular vectors of the matrix as well as the eigenvectors of the Rayleigh quotient (lines 1. and 5. in the DMD Algorithm 1) may be computed inaccurately as their sensitivity depends on the condition numbers of and (line 4.) and the gaps in the singular values and the eigenvalues, respectively.

Remark 4.1.

The result shown in Figure 7, showing unsuccessful reconstruction by the SVD based DMD starting at mode seems surprising. On the other hand, in DMD, the modes are computed from the product of the left singular vector matrix of the snapshots and the eigenvectors of the Rayleigh quotient; both sets of vectors are sensitive to small gaps in the spectrum and may not be computed to high accuracy; recall Remark 2.6. For the sensitivity of the singular vectors see [24].

4.3 Reconstruction in the QR compressed space

An efficient method of reducing the dimension of the ambient space is the QR–compressed scheme [12, §5.2.1], which reduces to via the QR factorization of . We briefly review the main idea; for more details and the general case of non-sequential data and we refer the reader to [12].

In the QR factorization

| (27) |

where is upper triangular, it holds that . (Clearly, if and only if is of full column rank.) Hence, we can reparametrize the data, and work in the new representation in the basis defined by the columns of . To that end, set , , . Then

| (28) |

and, in the basis of the columns of , we can identify , , i.e. we can think of and as snapshots in an dimensional space.

Further, the coefficients of the companion matrix are computed as

where the explicit use of assumes the full rank case. Numerically, we would solve the LS problem by an appropriate method (including refinement).

In this representation, if we set , and if we have a computed reconstruction , then , with the error . Hence we can run the entire process (including the initial DMD) in the basis , and switch to the original representation at the very end. Since the factorization (27) is available in high performance software implementations, the overall procedure is more efficient in particular in the cases when .

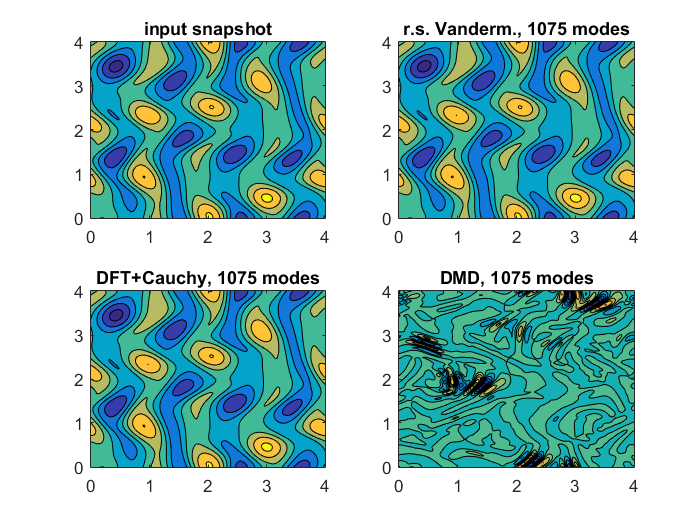

Let us now from try this scheme using the test data from §4.1 and §4.2. As expected, the compressed scheme computes considerably faster. The numerical results are similar, with some minor variations. To illustrate, we again reconstruct and .

The results shown in Figure 8, when compared to Figure 3, seem to indicate that pure Vandermonde inversion, while still performing poorly, shows some improvement. This is probably due to the fact that the Vandermonde inverse is applied to a triangular matrix; we omit the discussion for the sake of brevity. (The DMD and the DFT+Cauchy algorithms produced results similar to the ones in Figure 5.)

With the snapshot (see Figure 7), the QR compressed DMD started failing at the number of dominant modes; the DFT+Cauchy method performed well, as before.

5 Snapshot reconstruction: theoretical insights

It is desirable to have a representation analogous to (12), but with smaller number of eigenmodes and with as small as possible representation error. Suppose that we use modes, , and that the Ritz pairs are so enumerated that the selected ones are . We do not specify how the pairs have been computed – the ’s can be the Ritz vectors or e.g. the refined Ritz vectors [12]. The selection of the particular pairs can be guided e.g. by the sparsity promoting DMD [23]. Wanted are the coefficients that minimize the least squares error over all snapshots:

| (29) |

If we set , , , , and then the objective (29) can be written as

| (30) |

If we compute the economy size (tall) QR factorization and define projected snapshots , then the LS problem can be compactly written as

| (31) |

The normal equations approach [23] allows efficient computation of due to the particular structure of . Recently, [13] proposed a corrected semi-normal solution and a QR factorization based method.

In this section, our interests are of theoretical nature. We explore other choices of the pseudo–inverse based solution, different from the Moore–Penrose solution , in an attempt to establish a connection between the numerical linear algebra framework and the GLA.

5.1 Minimization in a –induced norm

The reflexive g–inverse [30, Definition 2.4] of ,

allows interesting explicit formulas that reveal a relation to the GLA [27, 26]. Indeed, if we define , then:

| (32) | |||||

| (33) | |||||

| (34) | |||||

| (35) |

Although this does not minimize (30), nor (31), it follows from the theory of generalized inverses that it does have some interesting properties.

Remark 5.1.

Recall that, by definition, satisfies

| (36) |

In fact, since , we have in general that , so .

Proposition 5.2.

Let , , and let . Then is the minimum –norm solution of the weighted least squares problem

| (37) |

Proof 5.3.

The matrix is obviously positive definite and is well defined norm. The claim is a direct corollary of [30, Theorem 3.3], because one can easily establish that

The claim can be derived also by brute force calculation. Since

is the Cholesky factorization and , we have

| (38) | |||||

| (39) |

However, the framework of the theory of matrix generalized inverses gives deeper insights.

Remark 5.4.

If (e.g. if is normal, and we compute an orthonormal set of Ritz vectors), then is diagonal and unitary and .

5.2 LS reconstruction in the frequency domain

We now repeat the reconstruction procedure, but in the frequency domain, following the methodology of §3. That is, instead of time observable trajectories sampled at time-equidistant points (the rows of ) we have their DFT transforms, i.e. , as the raw input. We assume that the eigenvalues are simple and are enumerated so that the selected ones are ; the QR factorization of the selected modes is .

If we post-multiply the expression in (30) by the unitary DFT matrix , the objective becomes

| (40) |

where is the DFT of the submatrix of . Because of the structure of , we distinguish two cases.

5.2.1 Case 1:

If none of the ’s equals an th root of unity, then (see (15))

where denotes an submatrix from the relation (15). In particular, , , and is unitary diagonal matrix. Introduce column partition

| (41) |

Let , . Then

If we set , then, using the reflexive g–inverse as before,

Hence, the components of the LS solution via the reflexive g–inverse are

Remark 5.5.

It remains an interesting open question whether these formulas have an appropriate interpretation in a wider context. Also, its ingredients such as or the harmonic mean of squared distances from to the th roots of unity may be of interest.

5.2.2 Case 2:

We now consider the case when some of the ’s are among the th roots of unity. Here we recall (16), i.e. if then the th row of reads

We set , and for . Hence, if e.g. , are the only two eigenvalues that match some th root of unity, we have the following version of the partition (41):

As an illustration of the reconstruction by the product when two of the ’s are among the roots of unity, consider the following schematic representation of (5.2.1) with , :

Here and are roots of unity and thus () and () participate in the representation of only and , respectively. That is, if , then participates in the reconstruction of only one transformed snapshot, namely .

6 Reconstructions based on GLA theory

We now wish to compare and contrast our above calculations to the Generalize Laplace Analysis (GLA) theorem [27, 26] adapted to this matrix setting. The GLA theorem is a theoretical result for a Koopman operator acting on infinite dimensional function spaces which constructs projections of functions onto Koopman eigenfunctions via ergodic-type averages. The classical formulation begins with merely knowing the spectrum of and constructs projections onto the eigenspaces using infinite-time averages.

6.1 Matrix GLA

We call an eigenvalue of a dominant eigenvalue if for all other eigenvalues , . We call strictly dominant if for all , .

Proposition 6.1 (Matrix GLA).

Let be a dominant eigenvalue and the (skew) projection onto . Then for any

| (43) |

Remark 6.2.

If we let , the above average is .

This is easily shown by expanding in the eigenvector basis. The above sum is then composed of -terms of the form . Since is a dominant eigenvalue, then for any , the term converges to 0. Projections onto another eigenspace requires subtracting off from all projections corresponding to all eigenvalues strictly dominating the one of interest and then running the above average for the new vector.

Remark 6.3.

The GLA is an inherently infinitary result. A straight forward application using finite data quickly leads to numerical instability.

The projection operators are skew projections along the other eigenvectors of . We can define a weighted inner product in which these spectral projections become orthogonal. Let be the normalized eigenvectors of and let be the QR decomposition of . Let and and define the hermitian form

| (44) |

Since is full rank, this form is nondegenerate and defines an inner product. Noting that is just it can easily be shown that which implies that the projections are orthogonal projections with respect to this inner product.

We can formulate a “coordinate” version of the GLA theorem. Since we know the eigenvectors, we can reduce the infinitary result to a finitary one.

Proposition 6.4.

Let and define , where is the diagonal matrix of eigenvalues of . Then

| (45) |

Proof 6.5.

Since exists,

By definition . This gives the equivalent formulations.

6.2 GLA formulas for reconstruction weights

As in section 5, we wish to reconstruct the evolution with a smaller number of Ritz vectors , . Given that the matrix version of the GLA (prop. 6.4) gives the exact reconstruction weights, we would like to investigate how well GLA reconstructs the weights without full knowledge of the eigenvectors. Since the GLA gives a skew projection onto the eigenfunctions rather than an orthogonal one, the reconstructed weights will not be optimal in minimizing the error’s 2-norm.

The objective is to find such that

| (46) |

In general, it will not be possible to perfectly reconstruct the data. Define for , the functionals

First consider the case of a particular . We look for that reconstructs exactly; i.e., the satsifying

| (47) |

Write . The QR-decomposition of this matrix is written as , where , and . The pseudo inverse of is

| (48) |

Let and such that ; and . Now,

| (49) | ||||

| (50) |

Thus is minimized with the choice . Component-wise this is

| (51) |

It is unlikely that will be the minimizer for every and is therefore unlikely to be a minimizer for . However, Jensen’s inequality will allow us to construct an which does better than the average of the error’s induced by each . Let and define the probability measure as . Define the random vectors as . Then since is a convex function, Jensen’s inequality gives us

| (52) |

In other words,

| (53) |

We can rewrite as

| (54) |

Compare this formula with (45) in Proposition 6.4. This is a GLA formula, except now we can only project onto the eigenfunctions we have. We call the components of this vector the GLA reconstruction weights . This can be written in a form similar to (eq. (35)):

| (55) |

6.2.1 Optimal reconstruction formula as a generalized ergodic average.

Using a reflexive g-inverse, we recall formula (35) giving the optimal reconstruction weights using ;

| (35 revisited) |

In the case of unimodular spectrum, the weights given via the reflexive g-inverse reduce exactly to the GLA weights.

Proposition 6.6.

When the spectrum of lies on the unit circle, .

Proof 6.7.

For with , we have . Then for each ,

When we do not have unimodular spectrum, we can interpret the optimal reconstruction weights as the result of a weighted GLA average. Indeed, the formula for each component can be manipulated as follows:

| (56) | ||||

| (57) |

Define

| (58) |

Then and . Then, for each component , we have the (non-uniformly) weighted average

| (59) |

Let us define the set of diagonal matrices as

| (60) |

Then, the optimal reconstruction weights are given by the weighted GLA formula

| (61) |

Remark 6.8.

Compare this with the formula for (eq. (55)), where the weight matrix for the GLA formula is the uniform weight matrix .

6.2.2 Distance between GLA weights and optimal reconstruction weights.

We have two expressions for reconstructing snapshots using eigenfunctions, namely (35) and (55). We have already shown that when the spectrum is on the unit circle that these formulas are equivalent. In the case when the spectrum is not contained in the unit circle, the question of their equivalence remains. Clearly, for any fixed number of snapshots, these formulas give different weights. What about the limit of trying to reconstruct an increasing number of snapshots still only using eigenfunctions? If we write and for the optimal and GLA weights reconstructing snapshots, does as ?

In general, the answer is no. We consider the simple case when with eigenvectors , where and is not orthogonal to either of the other eigenvectors. We also assume that the associated eigenvalues satisfy . The evolution satisfies

| (62) |

We reconstruct with . In this case, the term in the weights’ formulas is

| (63) |

For , define we have

where and . Note that is summable

| (64) |

We can define the limit of the optimal weights as

| (65) |

Clearly, since exponentially fast in , for large enough, we have that and . Since exponentially fast in , then for all large enough, and . Let be the largest integer such that . Then

| (66) |

Since and we can vary , , and (subject to the above assumptions on the last two), it is clear that we can find signals such that as .

What is interesting is that in the limit ; i.e., is asymptotically correct, or a consistent estimator in statistical language. To see this, fix and let be such that for . Then

| (67) |

For all large enough, we have for each , .

It is interesting that while each gives the optimal reconstruction of snapshots (i.e., it is an efficient estimator in statistical language), these weights are not asymptotically correct, whereas the GLA weights are sub-optimal for any finite , but are asymptotically correct.

| Estimator | Consistent/Asymptotically Correct | Efficient/Optimal |

|---|---|---|

| no | yes | |

| yes | no |

Remark 6.9.

The reason that GLA weights were asymptotically correct is due to the fact eigenvalues associated with the reconstruction vectors dominated the eigenvalue of the unresolved eigenvector. This lead the signal to converge exponentially fast to the correct weight . This result will continue to hold if . However, the result will be false, if any eigenvalue of an unresolved eigenvector has a larger modulus than the reconstruction eigenvalues; i.e., if for or 2.

6.2.3 Eigenvector-adapted hermitian forms and reflexive g-inverses.

The weight matrix in Proposition 5.2 and the minimizer can be recovered from a hermitian form on which is adapted to the eigenvector basis. This gives a connection with the abstract GLA theorem [27] in which appropriate spaces of observables for the Koopman operator were constructed by adapting the norm in order to orthogonalize the principal eigenfunctions and their products.

Let be the eigenvectors of . These are not necessarily orthogonal with respect to the standard inner product, . We can construct a weighted hermitian form in which the first eigenvectors are orthogonal. Let be the QR decomposition of , where , , and is unitary. Define the matrix as

| (68) |

and define the bilinear form as

| (69) |

Proposition 6.10.

Let and . Then

-

(a)

and

-

(b)

.

Proof 6.11.

For , . Then

| (70) |

Write . Then since ,

| (71) |

With this inner product, for each , is the orthogonal projection onto . It is easy to see that is a positive, semidefinite hermitian form. It is also nondegenerate; for any , if for all , then . Therefore the hermitian form generates a norm .

Remark 6.12.

When the first eigenfunctions are orthonormal, the -norm reduces to the canonical norm on the space. Indeed, if are orthonormal, then the QR-decomposition satisfies where is unitary. Then for any

Since is unitary, which gives the result .

We reformulate (46) using this -norm.

| (72) |

We write each as

| (73) |

where . Using Proposition 6.10,

| (74) | ||||

| (75) | ||||

| (76) |

Using definition (68) of and noting that and , we have

and therefore

| (77) | ||||

| (78) |

Defining

| (79) |

The coefficient vector that solves (72) is

| (80) |

Noting that and expanding the above formula for , we recover formula (35) for the optimal reconstruction weights; i.e., .

7 Conclusions

We have presented a new variant of the Dynamic Mode Decomposition that follows the natural formulation in terms of Krylov bases. Using high accuracy numerical linear algebra techniques we were able to curb the ill-conditioning of the companion matrix’s associated Vandermonde matrix allowing us to invert it and find the DMD modes. In addition to the inherent elegance in terms of the companion matrix formulation of DMD, our methods have a close connection to Koopman operator theory, explicitly comparing our methods with the result coming from Generalized Laplace Analysis theory. Furthermore, our methods can be incorporated in a meta-algorithm which reconstructs data snapshots. There exists other formulas for the optimal reconstruction of the snapshots from the DMD modes. Within these algorithms, there is a hierarchy of methods which trade accuracy for faster speed/lower complexity. Our methods can be regarded as the last line of defense; one requires a very accurate result despite very poor condition numbers. We take up this line of enquiry in a companion paper to this one.

References

- [1] H. Arbabi and I. Mezić. Ergodic theory, dynamic mode decomposition, and computation of spectral properties of the koopman operator. SIAM Journal on Applied Dynamical Systems, 16(4):2096–2126, 2017.

- [2] J. Aurentz, T. Mach, R. Vandebril, and D. Watkins. Fast and backward stable computation of roots of polynomials. SIAM Journal on Matrix Analysis and Applications, 36(3):942–973, 2015.

- [3] F. S. V. Bazán. Conditioning of rectangular Vandermonde matrices with nodes in the unit disk. SIAM Journal on Matrix Analysis and Applications, 21(2):679–693, 2000.

- [4] L. Berman and A. Feuer. On perfect conditioning of Vandermonde matrices on the unit circle. Electronic Journal of Linear Algebra, 16:157–161, 2007.

- [5] D.A. Bini, P. Boito, Y. Eidelman, L. Gemignani, and I. Gohberg. A fast implicit QR eigenvalue algorithm for companion matrices. Linear Algebra and its Applications, 432(8):2006 – 2031, 2010. Special issue devoted to the 15th ILAS Conference at Cancun, Mexico, June 16-20, 2008.

- [6] Å. Björck and V. Pereyra. Solution of Vandermonde systems of equations. Mathematics of Computation, 24:893–903, 1970.

- [7] Å. Björck. Numerical Methods in Matrix Computations. Springer, 2015.

- [8] S C. Eisenstat and Ilse Ipsen. Relative perturbation results for eigenvalues and eigenvectors of diagonalisable matrices. BIT Numerical Mathematics, 38:502–509, 09 1998.

- [9] J. Demmel. Accurate singular value decompositions of structured matrices. SIAM J. Matrix Anal. Appl., 21(2):562–580, 1999.

- [10] J. Demmel, M. Gu, S. Eisenstat, I. Slapničar, K. Veselić, and Z. Drmač. Computing the singular value decomposition with high relative accuracy. Lin. Alg. Appl., 299:21–80, 1999.

- [11] J. Demmel and P. Koev. Accurate SVDs of polynomial Vandermonde matrices involving orthonormal polynomials. Linear Algebra and Its Applications, 417:382–396, 2006.

- [12] Z. Drmač, I. Mezić, and R. Mohr. Data driven modal decompositions: analysis and enhancements. SIAM Journal on Scientific Computing, 40(4):A2253–A2285, 2018.

- [13] Z. Drmač, I. Mezić, and R. Mohr. On least squares problem with certain Khatri–Rao structure with applications to DMD. ArXiv e-prints, August 2018.

- [14] Z. Drmač. Accurate computation of the product induced singular value decomposition with applications. SIAM J. Numer. Anal., 35(5):1969–1994, 1998.

- [15] Z. Drmač and K. Veselić. New fast and accurate Jacobi SVD algorithm: I. SIAM J. Matrix Anal. Appl., 29(4):1322–1342, 2008.

- [16] Z. Drmač and K. Veselić. New fast and accurate Jacobi SVD algorithm: II. SIAM J. Matrix Anal. Appl., 29(4):1343–1362, 2008.

- [17] A. Edelman and H. Murakami. Polynomial roots from companion mtrix eigenvalues. Mathematics of Computation, 64(210):763–776, 1995.

- [18] W. Gautschi. How (un)stable are Vandermonde systems? In R. Wong, editor, Asymptotic and computational analysis (Lecture Notes Pure Appl. Math. 124), pages 193–210. CRC Press, 1990.

- [19] Walter Gautschi. Optimally conditioned Vandermonde matrices. Numerische Mathematik, 24(1):1–12, Feb 1975.

- [20] Walter Gautschi. Optimally scaled and optimally conditioned Vandermonde and Vandermonde-like matrices. BIT Numerical Mathematics, 51(1):103–125, 2011.

- [21] Desmond J. Higham. Condition numbers and their condition numbers. Linear Algebra and its Applications, 214:193 – 213, 1995.

- [22] N. J. Higham. Error analysis of the Björck-Pereyra algorithms for solving Vandermonde systems. Numerische Mathematik, 50:613–632, 1987.

- [23] M. R. Jovanović, P. J. Schmid, and J. W. Nichols. Sparsity-promoting dynamic mode decomposition. Phys. Fluids, 26(2):024103 (22 pages), 2014.

- [24] R. Li. Relative perturbation theory: II. eigenspace and singular subspace variations. SIAM Journal on Matrix Analysis and Applications, 20(2):471–492, 1998.

- [25] Igor Mezić. Spectral properties of dynamical systems, model reduction and decompositions. Nonlinear Dynamics, 41(1-3):309–325, 2005.

- [26] Igor Mezić. Analysis of Fluid Flows via Spectral Properties of the Koopman Operator. Annual Review of Fluid Mechanics, 45(1):357–378, January 2013.

- [27] R. Mohr and I. Mezić. Construction of eigenfunctions for scalar-type operators via Laplace averages with connections to the Koopman operator. ArXiv e-prints, March 2014. arXiv:1403.6559 [math.SP].

- [28] Victor Y. Pan. How bad are Vandermonde matrices? SIAM Journal on Matrix Analysis and Applications, 37(2):676–694, 2016.

- [29] Victor Y. Pan and Ai-Long Zheng. New progress in real and complex polynomial root-finding. Computers & Mathematics with Applications, 61(5):1305 – 1334, 2011.

- [30] C. Radhakrishna Rao and Sujit Kumar Mitra. Generalized inverse of a matrix and its applications. In Proceedings of the Sixth Berkeley Symposium on Mathematical Statistics and Probability, Volume 1: Theory of Statistics, pages 601–620, Berkeley, Calif., 1972. University of California Press.

- [31] Clarence W Rowley, Igor Mezić, Shervin Bagheri, Philipp Schlatter, and Dan S Henningson. Spectral analysis of nonlinear flows. Journal of fluid mechanics, 641:115–127, 2009.

- [32] Clarence W Rowley, Igor Mezić, Shervin Bagheri, Philipp Schlatter, and Dan S Henningson. Spectral analysis of nonlinear flows. Journal of Fluid Mechanics, 641:115–127, 2009.

- [33] P. J. Schmid, L. Li, M. P. Juniper, and O. Pust. Applications of the dynamic mode decomposition. Theoretical and Computational Fluid Dynamics, 25(1):249–259, 2011.

- [34] Peter J. Schmid. Dynamic mode decomposition of numerical and experimental data. Journal of Fluid Mechanics, 656:5–28, 008 2010.

- [35] G. W. Stewart and Ji-Guang Sun. Matrix Perturbation Theory. Academic Press, 1990.

- [36] B. Suri, J. Tithof, R. Mitchell, R. O. Grigoriev, and M. F. Schatz. Velocity profile in a two-layer Kolmogorov-like flow. Physics of Fluids, 26(5):053601, May 2014.

- [37] Jeffrey Tithof, Balachandra Suri, Ravi Kumar Pallantla, Roman O. Grigoriev, and Michael F. Schatz. Bifurcations in a quasi-two-dimensional kolmogorov-like flow. Journal of Fluid Mechanics, 828:837–866, 2017.

- [38] Jonathan H. Tu, Clarence W. Rowley, Dirk M. Luchtenburg, Steven L. Brunton, and J. Nathan Kutz. On dynamic mode decomposition: Theory and applications. Journal of Computational Dynamics, 1(2):391–421, 2014. arXiv:1312.0041 [math.NA].

- [39] L. R. Turner. Inverse of the Vandermonde matrix with applications. NASA Technical Note D–3547, Lewis Research Center, Cleveland, Ohio, August 1966.

- [40] A. van der Sluis. Condition numbers and equilibration of matrices. Numerische Mathematik, 14:14–23, 1969.

- [41] Matthew O. Williams, Ioannis G. Kevrekidis, and Clarence W. Rowley. A data–driven approximation of the Koopman operator: Extending dynamic mode decomposition. Journal of Nonlinear Science, 25(6):1307–1346, 2015.