On Model Selection Criteria for Climate Change Impact Studies111Corresponding Author: Dalia Ghanem, dghanem@ucdavis.edu. The authors are grateful to Felix Pretis, Zack Miller, Ariel Ortiz-Bobea and Glenn Rudebusch for helpful comments and suggestions. We also thank participants at the World Congress of the Econometric Society 2020 and the Climate Econometrics Virtual Seminar. Xiaomeng Cui acknowledges financial support from the National Natural Science Foundation of China (71903070) and the 111 Project of China (B18026).

Abstract

Climate change impact studies inform policymakers on the estimated damages of future climate change on economic, health and other outcomes.

In most studies, an annual outcome variable is observed, e.g. agricultural yield, along with a higher-frequency regressor, e.g. daily temperature.

Applied researchers then face a problem of selecting a model to characterize the nonlinear relationship between the outcome and the high-frequency regressor to make a policy recommendation based on the model-implied damage function.

We show that existing model selection criteria are only suitable for the policy objective if one of the models under consideration nests the true model.

If all models are seen as imperfect approximations to the true nonlinear relationship, the model that performs well in the normal climate conditions is not guaranteed to perform well at the projected climate that is different from the historical norm.

We therefore propose a new criterion, the proximity-weighted mean-squared error (PWMSE), that directly targets precision of the damage function at the projected future climate.

To make this criterion feasible, we assign higher weights to prior years that can serve as weather analogs to the projected future climate when evaluating competing models using the PWMSE.

We show that our approach selects the best approximate regression model that has the smallest weighted error of predicted impacts for a projected future climate.

A simulation study and an application revisiting the impact of climate change on agricultural production illustrate the empirical relevance of our theoretical analysis.

Keywords: mixed frequency data, Monte Carlo cross-validation, information criteria, aggregation

1 Introduction

Using panel data, impacts of climate change have been extensively studied on aggregate economic productivity [Hsiang, 2010, Dell et al., 2012, Burke et al., 2015], micro-level productivity and economic returns [Deryugina and Hsiang, 2017, Zhang et al., 2018, Addoum et al., 2020, Somanathan et al., 2021], agricultural profits and crop production [Deschênes and Greenstone, 2007, Schlenker and Roberts, 2009, Burke and Emerick, 2016, Aragón et al., 2021, Cui, 2020], energy consumption [Li et al., 2019, Auffhammer et al., 2017, Wenz et al., 2017], migration and labor allocation [Feng et al., 2010, Mueller et al., 2014, Jessoe et al., 2018, Cattaneo and Peri, 2016], human capital [Graff Zivin et al., 2018, Garg et al., 2020, Park et al., 2020], health and mortality [Deschênes and Greenstone, 2011, Barreca et al., 2016, Burke et al., 2018, Heutel et al., 2021], and conflicts [Hsiang et al., 2011, 2013, Harari and Ferrara, 2018].

Researchers typically consider multiple models in their analysis of the relationship between the outcome and temperature, the so-called damage or response function. This function not only informs policy design regarding climate adaptation in specific sectors and locations, but they also serve as empirical foundations for quantifying the social cost of carbon and influence decision-making on mitigating and adapting climate change at the regional and global scale [Dell et al., 2014, Diaz and Moore, 2017, Ricke et al., 2018]. This paper formalizes the model selection problem in climate change impact studies given the policy objective, evaluates the suitability of existing criteria and proposes a new criterion that directly targets the policy objective by incorporating the information about the projected future climate.

In typical empirical climate change impact studies, for , , we observe an outcome and a regressor , which is observed at a higher frequency . Practitioners tend to present results for a set of models , where each model uses different summary statistics of the higher-frequency weather variable as a model of the response function, , of the outcome to the high-frequency regressor time series, .666 Among the most commonly used summary statistics of temperature are the annual average [e.g., Dell et al., 2012], various degree day measures [e.g., Burke and Emerick, 2016], seasonal averages [e.g., Mendelsohn et al., 1994] as well as temperature bins [e.g., Deschênes and Greenstone, 2011]. To capture nonlinearities in the annual average temperature, a quadratic function has also been employed [e.g., Burke et al., 2015]. For a given , specifies a linear-in-parameter model,

| (1) |

Here, is known up to a finite-dimensional parameter, is a fixed effect and constitutes idiosyncratic shocks.777In practice, additional covariates, year fixed effects and flexible time trends are included. To simplify our presentation, we do not include these additional features. However, our analysis extends in a straightforward manner to accommodating them as we illustrate in our empirical applications.

Our first contribution is to formalize the model selection problem and policy objective in the climate change impacts literature. To do so, we first provide a review of recent work published in leading economics journals with a focus on modeling the response function between an outcome and temperature. Building on the review, we characterize the class of models in the empirical literature, define nested, non-nested overlapping and strictly non-nested models as well as formalize the policy objective of climate projections. Suppose that the outcome is given by the true model, ,

| (2) |

where is the true response function. The policy objective is to forecast the impact of the projected change in climate in period for each location , , where is the projected climate in a future period . With the formal expression of the policy objective, we proceed to define the ideal mean-squared error (MSE) target for this policy problem, specifically

| (3) |

which is the mean of squared errors in predicting the climate change impact using the model .

We begin our analysis with an assessment of the suitability of the existing consistent model selection criteria, such as Monte Carlo cross-validation (MCCV) and Generalized Information Criteria (GICs), in our context. We extend results from the classical literature on MCCV and GICs [Shao, 1993, 1997, Vuong, 1989, Sin and White, 1996] to the mixed-frequency panel data setting in the climate change impacts literature. We show that MCCV with a vanishing training-to-full sample ratio, BIC, and the criteria proposed in Sin and White [1996] are model selection consistent if one of the models under consideration nests the true model.888Let denote the true model and denote the model selected by criterion , a criterion is said to be model selection consistent if as sample size grows. For additional discussion, see Sections 3.1 and C.2. In contrast, only the criteria proposed in Sin and White [1996] are consistent if all models are misspecified.999This property is referred to as pseudo-model selection consistency in Sin and White [1996]. We provide a definition and related discussions in Section C.2. An interesting byproduct of this analysis is that we find that in the context of mixed-frequency panel data BIC can be pseudo-inconsistent in nested model selection problems when all models under consideration are misspecified, whereas in standard nonlinear model selection problems prior literature establishes that BIC is pseudo-inconsistent in non-nested model selection problems [Sin and White, 1996, Hong and Preston, 2012]. We formally discuss this issue in Online Appendix E. Since consistent model selection criteria select the true model (or the most parsimonious model that nests it) with probability approaching one if such a model is under consideration, they would asymptotically achieve the ideal MSE in Eq. (3). While it is plausible for empirical researchers to correctly specify the model for outcomes with a clear and well-studied physical relationship with weather, there is a wide range of economic outcomes of interest for which this would not be plausible.

If none of the models under consideration nest the true model, consistent model selection criteria are not guaranteed to select models that perform well in terms of the ideal MSE target for the policy objective given in (3). We therefore proceed to propose an alternative criterion suitable for the policy objective that treats all models as potentially misspecified. Building on our formal definition of the policy objective, we propose a new criterion that accounts for the projected change in the weather distribution in the (infeasible) ideal MSE target in (3) and incorporates the information about the future climate in the evaluation. The criterion we propose is based on a proximity-weighted mean of the squared errors (PWMSE) in predicting the impact of the projected change in climate between year relative to prior years available in the data for ,

| (4) |

The weighting function in the PWMSE is designed to give higher weight to prior years in the sample that are more similar to the projected future climate at . The weighting function therefore ensures that the selected model performs well in terms of predicting the impacts of projected climate change from to in line with the policy objective. To estimate the PWMSE, we propose a resampling procedure and show that the model that minimizes the estimated PWMSE minimizes the population PWMSE with probability approaching one as the sample size grows. We demonstrate numerically that the simulated ideal MSE target is minimized by the true model as well as models that nest it in our simulation examples.

We conduct a simulation study to examine the finite-sample performance of the MCCV, GIC and PWMSE criteria. Our simulations demonstrate that, when the true model is under consideration, all model selection criteria select the true model with high probabilities. However, when all candidate models are misspecified, the PWMSE is more likely to select the model that minimizes the simulated ideal MSE target since it incorporates the information about the future forecasts in the evaluation. Since the PWMSE requires practitioners to specify the weighting function, we also examine the finite-sample performance of the PWMSE with different choices for the weighting function and provide guidance to practitioners on this choice in Online Appendix F.

To illustrate the empirical relevance of our results, we compare the behavior of existing criteria and our proposed PWMSE in the context of an application revisiting the relationship between temperature and agricultural yield. In this application, while different criteria select different models, the associated damage functions are qualitatively similar — rising temperature becomes detrimental at high temperatures. Consistent with our theoretical predictions, the Sin and White [1996] criteria (SW) choose the most parsimonious among those models. Our proposed criteria of PWMSE, which incorporates the HadCM3-B1 climate projection in the weighting function, selects a less parsimonious model that provides flexible estimates of the nonlinear relationship consistent with the agronomic literature. Although the models selected by the SW and PWMSE criteria result in qualitatively similar damage functions, the quantitative differences between their predicted outcomes matter for policy arrangements on adaptation toward the specific future climate projected by HadCM3-B1. This application highlights the value of the PWMSE criterion in terms of ensuring that the selected model targets the policy objective for a given climate change projection.

Implications for practice. This paper has practical implications for the use of model selection criteria in climate change impact studies. We show that the existing model selection criteria, although useful, have important limitations in their application to climate change impact studies. The usefulness of consistent model selection criteria is limited to the case when the true model is nested in one of the models under consideration. While this is plausible in applications where the relationship between temperature and the outcome of interest is well-studied, such as for agricultural outcomes, it is restrictive for many other economic outcomes of interest. Therefore, the PWMSE serves as a useful addition to the existing criteria as it ensures improved performance for the policy objective of climate change projections. We emphasize, however, that rather than reporting the results of a particular model selection criterion, applied researchers should report the results of the different model selection criteria we consider, MCCV, GIC and PWMSE. The reasoning behind this recommendation stems from the fact that if the true response function is nested in one or more of the models under consideration, then the different model selection criteria should select models that have similar response functions, albeit different numbers of parameters, which is consistent with our theoretical and simulation analysis. The usefulness of reporting the different criteria in interpreting the empirical results is also clearly illustrated in our empirical application. We elaborate on these practical implications in Section 3.4 and illustrate these insights in the context of our empirical application in Section 4.

Related literature. This paper builds on the literature on the asymptotic properties of model selection criteria [e.g. Claeskens and Hjort, 2008, Arlot and Celisse, 2010]. We build on the literature on the asymptotic behavior of MCCVs in linear models [Shao, 1993, 1997] as well as nonlinear model selection based on GICs [Sin and White, 1996, Hong and Preston, 2012]. The latter strand of the literature builds on the seminal work in Vuong [1989] which shows that the convergence rate of the quasi-likelihood ratio depends on whether the models under consideration are nested or not.101010Recent work in this literature develops approaches to uniformly valid testing and post-selection inference for non-nested models [Shi, 2015, Schennach and Wilhelm, 2017, Liao and Shi, 2020].

The analysis of model selection consistency in the context of the mixed-frequency panel data models is of independent interest and relates to an important body of work on aggregation in mixed-frequency time series. While the goal in this literature is starkly different from the climate change impacts literature, both share a common theme which is the need to aggregate regressors due to the mixed-frequency nature of the empirical setting. There is a large body of work in the mixed-frequency time series literature providing different aggregation schemes [Andreou and Ghysels, 2006, Ghysels et al., 2006, 2007, Chambers, 2016, Miller, 2016, 2018].111111We point to some interesting connections between notions of misspecification bias in this paper and the literature on aggregation in cointegration models [Chambers, 2003, 2011, Chambers and McCrorie, 2007, Miller, 2014, 2016] in Online Appendix E. One promising direction for future work that complements existing work on specification testing [Andreou et al., 2010, Groenvik and Rho, 2018, Kvedaras and Zemlys, 2012, Miller, 2018, Liu and Rho, 2019] is to adopt the proposed model selection framework to examine the aggregation problem in mixed-frequency time series from the perspective of optimal selection of an approximate model.

The PWMSE criterion proposed in this paper has some apparent similarity with analog forecasting procedures (as proposed in Lorenz [1969]) used in short-term climate forecasting. The analog forecasting uses past trajectories of the weather with initial conditions that approximately match the current conditions. Such approach is based on the fact that the climate systems follow deterministic differential equations that are time-invariant. So any two solutions for such systems with close initial conditions remain close to each other at least for a short time. The PWMSE criterion selects the model that performs best on average for past observations that resemble the future projected climate. Despite sharing this common feature, the goals of the two methods are different: the analog forecasting seeks to forecast the climate using past patterns, while PWMSE-minimizing model forecasts a nonlinear impact of the future weather that is taken as given.

The remainder of the paper is organized as follows. Section 2 provides the policy motivation behind the present paper, summarizes current empirical practice, and formalizes the model selection problem and policy objective. Section 3 evaluates the suitability of existing criteria for the policy objective of climate change projections and introduces the PWMSE criterion. Section 4 illustrates the empirical relevance of our theoretical analysis in the context of an empirical application revisiting the relationship between temperature and agricultural yields.

2 Why Model Selection in Climate Change Impact Studies?

Panel estimates of climate change impacts have served as critical inputs for policy making on climate change mitigation and adaptation. In this section, we first briefly introduce the rationale behind the existing empirical studies and review existing methods in recent work. We then formalize the model selection problem and the policy objective in this context, which also provides a foundation for understanding the behavior of existing criteria as well as the rationale behind our proposed PWMSE criteria in Section 3.

2.1 Damage functions as policy parameters

Designing cost-effective policy on climate change mitigation and adaptation requires a precise and thorough understanding on how the key climatic factor (e.g., temperature) affects human society. In responding to this mission, extensive efforts have been made to properly estimate the economic damage functions, which characterize the quantitative relationship between certain economic outcomes and climatic factors, especially temperature.

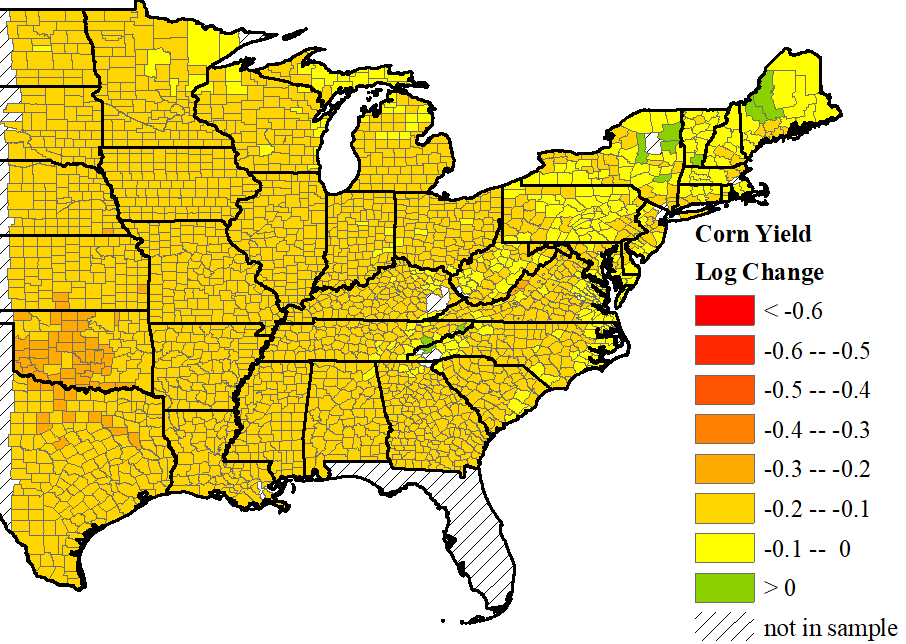

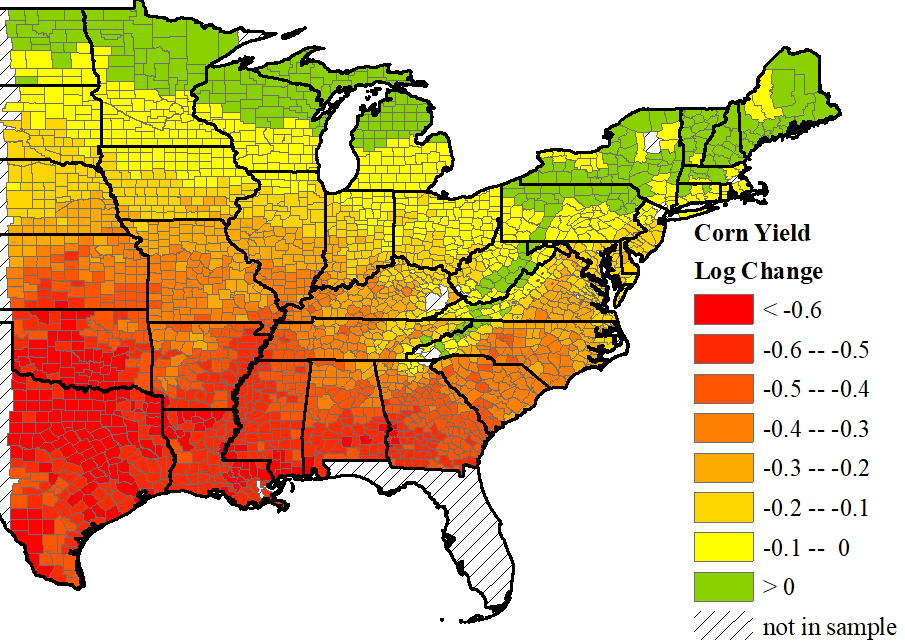

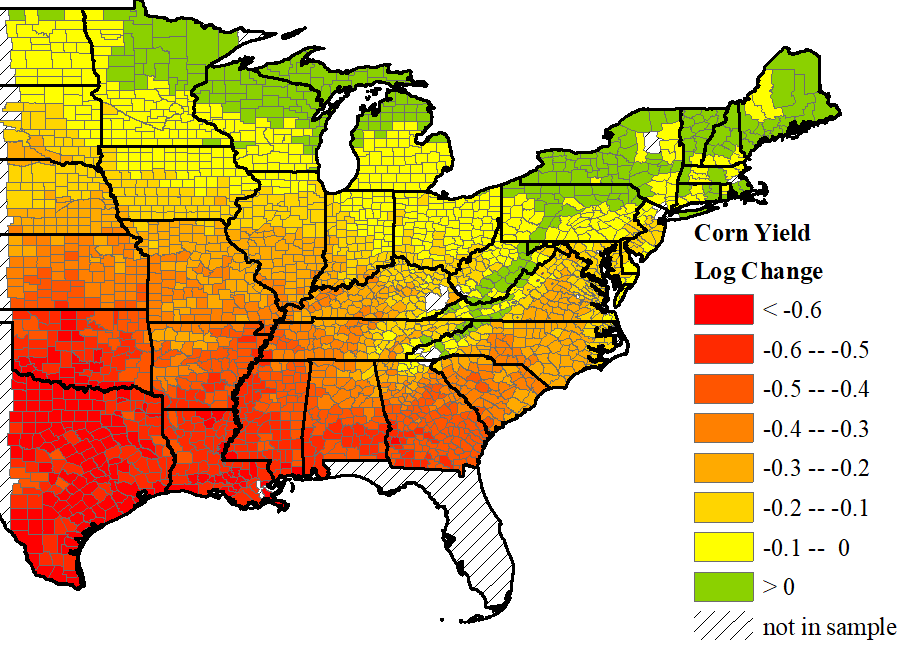

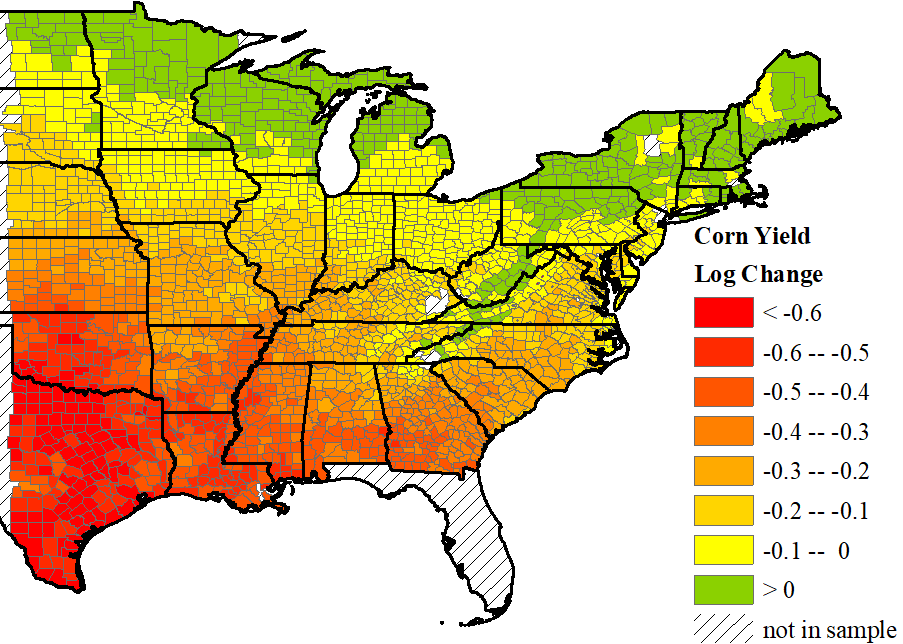

The estimated damage functions serve two purposes. From a micro perspective, they help improve the design of regulatory and adaptation policies that target specific contexts. Using agricultural production as an example, Figure 1 shows sharply contrasted warming implications on corn yields in the United States under two distinct but reasonable damage functions. Both panels reflect predicted warming-induced yield losses by 2050 under future temperatures projected by the HadCM3-B1 model. Panel A relies on a damage function empirically estimated based on a specification of monthly average temperatures, while Panel B relies on that of linear spline with an endogenously determined knot.121212We describe the precise steps for obtaining these estimates and projections in Section 4. It is clear that the chosen damage function would directly influence policy arrangements on where and how corn production needs to be adapted to mitigate potential losses under future warming.

| A. Monthly averages | B. One-knot linear spline |

|---|---|

|

|

Notes: The county-level log changes in corn yields are obtained by applying different empirically estimated damage functions to the temperature of 2050 projected under HadCM3-B1. The damage functions are estimated based on monthly average temperatures in panel A and linear spline with one endogenously determined knot in panel B.

The policy relevance of damage functions is not restricted to policies targeting specific outcomes and sectors. From a macro perspective, the cost-benefit evaluation of a host of domestic policies as well as international agreements is directly influenced by the estimated social cost of carbon (SCC). Improving this estimate hinges on those damage functions as critical inputs [National Academies of Sciences, Engineering, and Medicine, 2017]. This point is epitomized in Moore et al. [2017] as they show that the SCC is doubled by simply updating the damage functions of agriculture with the most recent empirical estimates in the FUND model.131313The FUND model is a widely used integrated assessment model (IAM) developed by Richard Tol and David Anthoff. See more details at: http://www.fund-model.org.

2.2 Current Empirical Practice

The empirical studies for pinning down the damage functions typically rely on panel data with large and relatively small . For example, the empiricist may observe some economic outcomes at the county level for more than a thousand counties, and the outcomes are observed annually over a period of a few decades. This practice was first initiated in the seminal work of Deschênes and Greenstone [2007] on identifying temperature impacts on agriculture, it then became popular and widely adopted in understanding climatic impacts on many dimensions of human society.

In this empirical literature, researchers commonly use a panel fixed effects model where, conceptually, the location fixed effects control for impacts of the time-invariant factors like county characteristics.141414To the best of our knowledge, there are no studies in this literature relying on random effects models. With this setup, identifying the damage function would mostly rely on year-to-year within-county variation in weather that is arguably exogenous.151515The literature has acknowledged that this year-to-year weather variation is different from long-run climate change, but utilizing the arguably exogenous weather variation for pinning down damage functions is still regarded as highly useful for policy purposes [Auffhammer, 2018]. This empirical approach rests on the validity of the strict exogeneity assumption. To focus our attention on the model selection problem in this literature, we therefore maintain this assumption here.

A critical component in these econometric examinations is to estimate the particularly damaging effects associated with high temperatures, commonly referred to as the nonlinear temperature effects. With raw temperature data observed at a higher frequency than that for the panel regressions, identifying this nonlinearity would require the empiricist to first summarize the high-frequency regressor data in certain ways such that the variables with summarized temperature information can support estimating nonlinear temperature effects.

| Article | Journal | Temperature Models Considered | ||||||

|---|---|---|---|---|---|---|---|---|

| mean | max | degree | bins | poly- | splines | heat | ||

| temp. | temp. | days | nomials | index | ||||

| Levinson [2016] | AER | ✓ | ||||||

| Barreca et al. [2016] | JPE | ✓ | ||||||

| Somanathan et al. [2021] | JPE | ✓ | ✓ | ✓ | ||||

| Busse et al. [2015] | QJE | ✓ | ✓ | |||||

| Heyes and Saberian [2019] | AEJ-App | ✓ | ✓ | ✓ | ||||

| Colmer [2021] | AEJ-App | ✓ | ✓ | ✓ | ||||

| LoPalo [Forthcoming] | AEJ-App | ✓ | ||||||

| Burke and Emerick [2016] | AEJ-Pol | ✓ | ||||||

| Park et al. [2020] | AEJ-Pol | ✓ | ✓ | |||||

| Aragón et al. [2021] | AEJ-Pol | ✓ | ✓ | |||||

| Cohen and Dechezleprêtre [Forthcoming] | AEJ-Pol | ✓ | ||||||

| Liu et al. [Forthcoming] | AEJ-Pol | ✓ | ||||||

| Anderson et al. [2017] | EJ | ✓ | ||||||

| Jessoe et al. [2018] | EJ | ✓ | ✓ | |||||

| Jagnani et al. [2021] | EJ | ✓ | ✓ | |||||

| Adhvaryu et al. [2020] | REStat | ✓ | ✓ | |||||

| Heutel et al. [2021] | REStat | ✓ | ||||||

| Novan et al. [Forthcoming] | REStat | ✓ | ✓ | |||||

| Notes: This survey covers empirical studies on the Top 5 journals, AEJs, EJ, and REStat since 2015. We focus on studies for which identifying the response function to temperatures is of critical importance. The temperature models are broadly categorized. Within each model category, the specific formulation of the model still varies across different articles. Formal definitions of these models are provided in Online Appendix B. | ||||||||

There is no consensus or best practice on how to implement this process. Empiricists usually make decisions on how they summarize high-frequency temperature information to eventually obtain the estimates on the nonlinearity. In Table 1, we summarize temperature models considered in recent empirical studies in leading economics journals, including the “Top 5” journals, American Economic Journals (AEJ), Economic Journal (EJ), and Review of Economics and Statistics (REStat). We limit our attention to the studies for which identifying the response function to temperature fluctuations is of critical importance for the research question.161616Under this criterion, this survey does not include articles where response to temperature is only a first-stage or temperatures are simply considered as control variables.

The chosen models vary across different studies, and none of the listed empirical studies adopt a selection rule for determining which model should be used to inform policy.171717While not included this review, we note that the influential study in Schlenker and Roberts [2009], which we revisit in Section 4, relies on Monte Carlo cross-validation to select between the models under consideration. Even though many studies favor the use of degree days and bins, the specific ways of constructing these variables as well as the critical thresholds involved are determined by the empiricists.181818We note one exception in Burke and Emerick [2016] where the authors rely on in-sample fits (i.e., ) to determine the whole-number cutoff degree for separating growing and heat degree days. It is important to note, however, that the revealed nonlinearity (or the absence of it) obtained from the econometric estimation is shaped or at least indirectly influenced by the decision made on how to summarize the high-frequency regressor data, as we have illustrated in Figure 1. If empiricists improperly summarize the information and adopt a poorly specified model, they could potentially reach biased conclusions on climate change impacts.

In the following subsection, we make precise definitions and formalize the model selection problem and policy objective for these empirical studies on identifying climate change impacts.

2.3 Formalizing the Model Selection Problem and Policy Objective

2.3.1 Class of Models in Empirical Practice

In the setting of climate change impact studies, researchers observe an annual outcome and a vector of regressors observed at a higher frequency, such as daily or hourly, . In this mixed-frequency panel data setting, the models considered in the literature as presented in Section 2.2 are fixed effects models that differ in terms of the response functions used to model the relationship between the outcome, , and the high-frequency regressor time series, . For a given model , the outcome equation is thus given by the following

| (5) |

While control variables and additional fixed effects can be included, we omit them in our analysis to simplify the exposition and to focus our analysis on the main issue we consider here which is the potential misspecification of the response function.

The class of response functions considered in the empirical literature can be formally represented as follows,

| (6) | ||||

| (7) |

where is a vector of linear and/or nonlinear transformations of the high-frequency regressor, , and is a vector of -specific weights. Once the weighted transformations of are aggregated over , the transformation is applied to them. For the purposes of this paper, we assume that , and are finite, such that .

While the class of models considered in the literature preserves linearity in the parameters and separability between observables and unobservables, it can allow for nonlinearities in the high-frequency regressor. To show this, we provide a few examples to illustrate the different roles played by , and . The annual mean model, where , can be obtained by letting , , and , where . The quadratic in annual mean model, where , relies on the same and as the annual mean model, but uses a second-order polynomial function , such that . To obtain the quarterly mean model, we set ,

and is the identity function. For , denotes the subset of indices that are in the quarter and denotes the cardinality for a set . Finally, the model with temperature bins, where , can be obtained by setting

, is the identity function and is a set of intervals. In Online Appendix B, we also provide formal definitions for other commonly used models in the literature, such as degree days, polynomials, splines, etc.

2.3.2 Defining Nested and Non-nested Models

Since all models considered rely on different aggregated transformations of the same underlying high-frequency regressor, the models are likely to be overlapping as defined below. However, we would like to differentiate between different cases of overlapping models. Assume without loss of generality . Let denote a realization of . For a fixed realization , the realizations of and are given by and , respectively. Let denote the parameter space of and the element of .

We next provide formal definitions for when two models, and , are nested, non-nested overlapping or strictly non-nested. In the following, let denote a -dimensional column vector of zeros.

Definition 1.

-

(i)

is nested in iff for all and , where and is a non-random matrix with full row rank,

-

(ii)

and are non-nested, overlapping iff does not nest , but for all and some and ,

-

(iii)

and are strictly non-nested iff they are not nested and for all , and .

Note that according to (i), a model contains another if the regressors in the latter can be expressed as a linear combination of the regressors in the former. This is different from the typical linear regression framework where a model contains another if the regressors in the latter are a subset of the regressors in the former, i.e. the elements in can only be zero or one. We illustrate the above definitions with the following example.

Example 1.

(Annual Mean, Quarterly Mean, Quadratic in Annual Mean and Temperature Bin Models)

Let denote the annual mean model, with outcome equation

| (8) |

where . The quarterly mean model uses instead the quarterly means of as regressors. In the quarterly mean model, Then prescribes the outcome equation

| (9) |

Note that for all , where

| (11) | ||||

Hence, is nested in .

The quadratic in annual mean model, , uses as regressors. Even though the quadratic in annual mean and the quarterly mean models are not nested, if and for , with , then both models yield the annual mean model given . Hence, they are overlapping, non-nested.

To complete the example, note that annual mean model is both non-nested and non-overlapping with the temperature bin model with regressor as long as has continuous support. Indeed, one can construct multiple examples of elementary events such that the number of the days with positive values being equal, but the annual average being different and vice versa. Thus the only overlapping submodel of and is an empty model.

2.3.3 Policy Objective: Climate Change Projections

Consider a set of locations , for which we observe an annual outcome and daily temperature time series over time periods, .191919Note that our setting can allow for a vector of high-frequency regressors, but to fix ideas and to remain consistent with the policy question, we motivate this section with as the temperture time series. We would like to forecast the impact of climate change on the outcome between period and . The location is projected to experience the daily weather time series in periods ahead, . In this setting, is obtained from a forecast model of a specific projection for a given climate change scenario.202020We note that uncertainties exist in forecasting future climate and the forecasts may vary across different projections even for the same climate change scenario. We restrict our attention to the case that the policy maker is interested in the impact of climate forecasted by a specific projection.

Our goal is to predict the impact of this change in climate on an outcome of interest. One of the unique features of this policy objective is that the goal of the prediction exercise here is a causal parameter. As a result, to make progress here, we have to define a true model that generates the outcome. For the purposes of this paper, we assume that the outcome, , is given by the following model, ,

| (12) |

Similar to the models imposed in the literature, imposes separability between unobservables and observables. As a result, the potential source of misspecification of a given model would stem from the misspecification of the true response function, .

Assuming strict exogeneity, , which imposes the mean independence of not only of but also , we can formally define the object of interest for each location

| (13) |

Let us define as the support of . Our object of interest is a functional of and

| (14) |

We are therefore interested in estimating the function with the highest precision in a specific set of values that correspond to the support of and , respectively.

In practice, researchers and policymakers do not know the true functional form of , they rely on a set of models to estimate the impact of projected climate change. The question that arises here is what criterion policymakers should use to choose between the different models and their implied projections. For instance, in Figure 1, how should a policymaker decide between the two models considered which give substantially different climate change projections and therefore have very different policy implications? We tackle this question in the following section, evaluating the usefulness of existing criteria and proposing a new criterion tailored to the policy objective in climate change impact studies. We then illustrate the empirical relevance of our theoretical analysis in the context of the empirical application that corresponds to Figure 1.

3 Model Selection Criteria for Climate Change Impact Studies

Given the policy objective of climate change projections, an ideal criterion to choose between a set of models under consideration would be to minimize the following mean-squared error (MSE) criterion,

| (15) |

This MSE criterion is based on the error of predicting the impact of the projected climate change from to . A challenge here, as in other forecasting problems, is of course that this ideal target is infeasible. Given the use of MCCV in practice, we first examine the asymptotic properties of this criterion as well as GICs (Section 3.1). Since our theoretical analysis of these existing criteria underscores the importance of at least one of the models in the set nesting for these criteria to minimize the ideal MSE target in (15), we proceed to propose a class of alternative criteria that minimize feasible counterparts of the ideal target whether or not the models under consideration are correctly specified (Section 3.2).

In the following, we consider asymptotics that let while holding fixed. Given the observational nature of the panel data under consideration in this setting, we do not restrict the conditional mean of given , but maintain the strict exogoneity assumption, . As a result, we focus our attention on fixed effects (FE) estimators that rely on the within-group transformation.212121Our results can be extended to the first-difference estimator in a straightforward manner. For a random variable , (in particular, ) and .

3.1 Asymptotic Properties of Existing Model Selection Criteria

In this section, we consider two classes of model selection criteria, MCCV and GIC, and discuss the conditions under which these criteria are suitable for our policy objective. To maintain a simple exposition in this section, we relegate all formal conditions and statements to Online Appendix C and provide a summary of the implications of these results for our setting here.

MCCV is a very popular method in practice, because it directly measures out-of-sample prediction error and seems “model-free”. It has been used in Schlenker and Roberts [2009] to justify their model selection choice. To formally introduce it, let and . Given observations , to compute the MCCV mean squared error, we randomly draw a collection of subsets of with size (test sample size). For a given choice of , the model selected by MCCV minimizes the following out-of-sample MSE criteria among a set of models ,

| (16) |

Here is an vector that vertically stacks for all and , where denotes the within-demeaned version of and is the estimator of the parameter vector of using the training data set , where denotes a set in and denotes the complement of , i.e. the remaining subsets in the collection after removing subset .

GICs have been shown to be closely related to MCCV criteria in the classical variable selection problem with cross-sectional data in Shao [1997]. Unlike MCCV, however, GICs can be estimated using the original sample without any resampling. Given a penalty level , the model selected by GIC among a set of models minimizes the following criterion

| (17) |

where and

For a formal derivation of the concentrated likelihood , see Appendix C.2.

When examining the asymptotic behavior of MCCV and GICs, there are two properties that have been examined in the literature, model selection efficiency (optimality) as well as model selection consistency [e.g., Shao, 1993, 1997, Claeskens and Hjort, 2008].222222See Yang [2005], for an interesting analysis that poses the question of whether these two objectives can be combined and points to a clear trade-off between the two objectives.

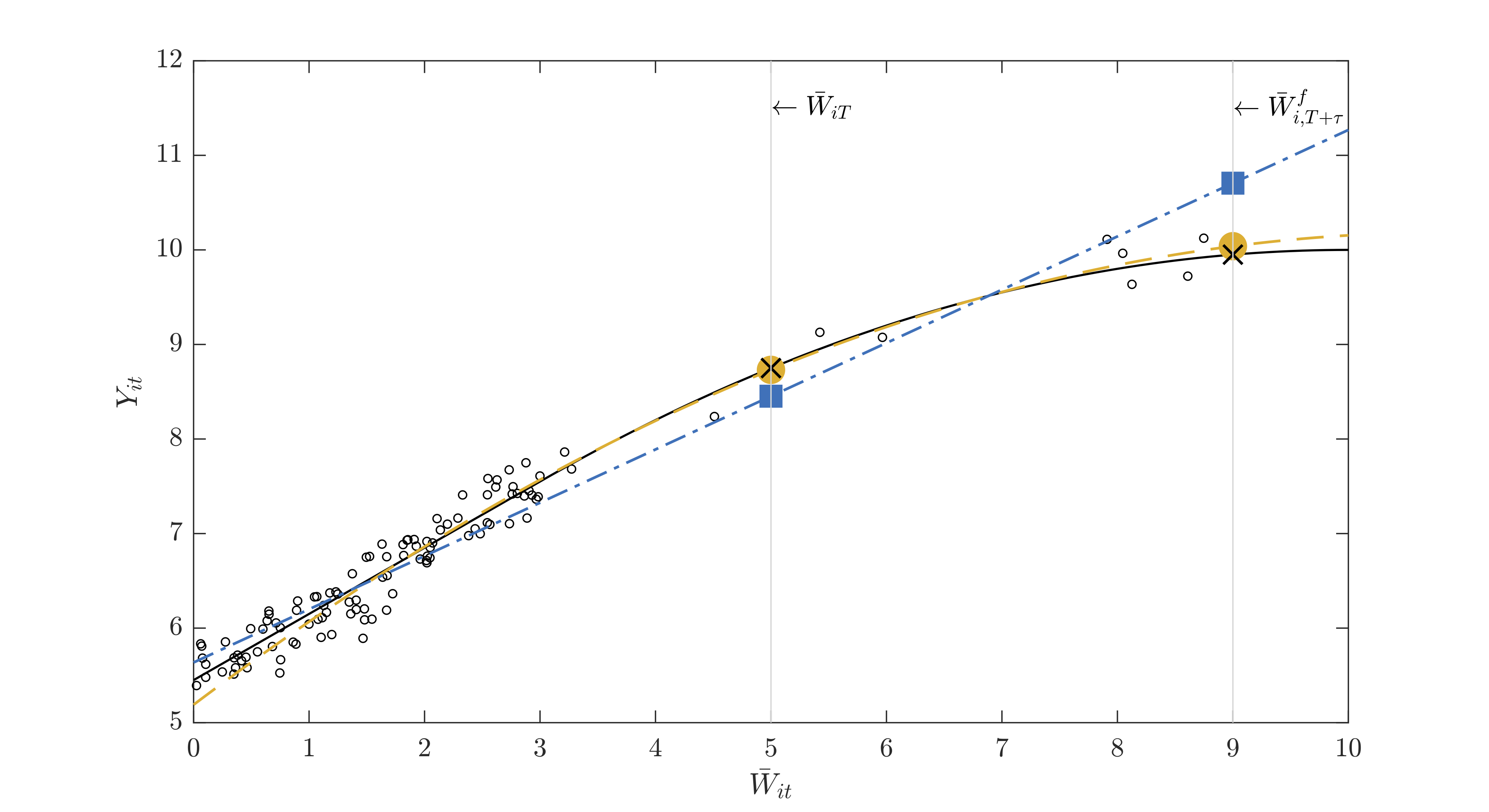

Notes: The black solid line corresponds to the true model (nonlinear in ); blue dot-dashed line corresponds to the best approximating model that minimizes the in-sample MSE (linear in ), the gold dashed line corresponds to the best approximating model that minimizes the impact MSE (quadratic in ). The small black circles correspond to a random sample of for a given .

A model selection criterion is said to be efficient [Shao, 1997, Claeskens and Hjort, 2008] if the ratio of the mean squared error (MSE) of the model selected by these criteria and the theoretical minimizer among those under consideration will converge in probability to one. Formally, a criterion is said to be model selection efficient in our context relying on FE estimators, if the following ratio converges to one

| (18) |

where is the model selected by the criterion , is the theoretical minimizer of the loss function, integrates over all random quantities except for ,

Among MCCV and GIC criteria, leave-one-out cross-validation (MCCV with ) and AIC (GIC with ) are model selection efficient [Shao, 1997]. While such criteria select models that minimize the MSE of the within-group transformed outcome, they are not guaranteed to perform well for the ideal target for climate change projections in (15). The MSE of the within-group transformed outcome and the ideal target in (15) can in fact result in substantially different best approximate models, even in settings where the true response function depends only on a scalar . To illustrate this point, consider the prediction of the impact of projected climate change for a unit illustrated in Figure 2. In this graphical illustration, both linear and quadratic in models are misspecified, but the quadratic model predicts the impact of the projected change from to better. To see this, compare the gold circles with the blue squares, noting that the black crosses correspond to the true impact. In this diagram, most observations are far away from the projected climate and lie in the domain where the true impact function is linear. As a result, minimizing the MSE in levels results in a linear-in- model, which has a larger bias at the projected climate. This example provides an intuition for why model selection efficiency relying on the MSE in levels, and therefore AIC and leave-one-out cross-validation, are not guaranteed to minimize our ideal target.

Consistent model selection can be suitable for the policy objective of climate change projections under certain conditions. Specifically, if one of the models under consideration nests the true model, a consistent model selection criterion chooses with probability approaching one asymptotically, as . As a result, consistent model selection criteria minimize the ideal target in (15) and particularly attain zero by selecting with probability one asymptotically. As a result, we provide conditions on the tuning parameter choices for the MCCV and GIC that ensure consistent model selection in Online Appendix C. These results extend Shao [1993] and Sin and White [1996] to the mixed-frequency panel data setting we examine. We specifically show that MCCV with vanishing training-to-full sample ratios () and the GIC criteria proposed in Sin and White [1996] (e.g. GIC with as well as BIC (GIC with ) are model selection consistent and will choose the true model or the most parsimonious model that nests it with probability approaching one as , assuming that such a model is contained in the set under consideration. Otherwise, the criteria proposed in Sin and White [1996] are pseudo-consistent, i.e. consistent under misspecification, in the sense that they minimize the Kullback-Leibler divergence. The problem, however, is that minimizing the Kullback-Leibler divergence does not guarantee that we minimize the ideal target in (15).

In sum, this section underscores that the suitablity of consistent model selection criteria for the policy objective of climate change projections is limited to cases where at least one model under consideration nests the true model. While this is possible in applications where the scientific literature can characterize the physical relationship between temperature and the outcome, the literature on climate change impacts examines a variety of economic outcomes for which the relationship with temperature is difficult to fully characterize. When all models are misspecified, some of the existing criteria minimize the MSE of the within-group transformed outcome, whereas others minimize the Kullback-Leibler divergence. Neither of these two targets ensures that the selected model would perform well in terms of the ideal target in (15). As a result, we next propose the PWMSE that seeks to mimic the ideal target.

3.2 Targeting the MSE of Projected Climate Change Impacts

In this section, we propose a new MSE criterion that targets the prediction of climate change impacts directly for a given climate projection , which we refer to as proximity-weighted MSE (PWMSE). We then propose an MCCV procedure to estimate the PWMSE and show that the model minimizing the estimated PWMSE is asymptotically minimizing its population analogue.

To provide an intuition for this criterion, let us re-examine Figure 2. Recall that in this example, minimizing the MSE of the levels of the outcome would not lead us to choose the best approximate model at . Now consider an alternative approach where instead of relying on the within-group transformation, we use within-differences between and prior years , but only use prior years with weather “close” to for model selection. This approach would guarantee that we choose the better approximate model, quadratic in . This insight guides the formulation of the PWMSE. Note that under strict exogeneity and additional regularity conditions, minimizing the ideal MSE target in (15) is equivalent to minimizing

| (19) |

where and is limit of the cross-sectional average of expectations that accounts for heterogeneity in distributions over space (see Condition 1.5 below for a formal definition). Since the second term in (19) does not depend on , we can select the model based on the first term.

In practice, the problem, as with other forecasting settings, is that we do not observe . The standard approach in forecasting would be to mimic the -step-ahead forecasting in the following way,

| (20) |

This approach is not suitable in our setting since climate change implies that the distribution of weather is strongly persistent and possibly non-stationary. As a result, this criterion targets precision of the functional approximation of under the past as opposed to the projected future climate. For example, if in the past the climate was on average more moderate, while the projected climate is relatively hot, the above criterion will give relatively higher weight to moderate climates. Moreover, there is no guarantee that the projected changes in the climate will follow a linear trend that would make changes between and comparable to changes between and . Finally, this criterion can be infeasible in this setting, since tends to be close to or greater than 1 in practice.

We suggest the following criterion that relies on a weighting function that gives higher weights to historical years with climates that are more similar to the projected climate and thereby mimics the ideal target more closely,

| (21) |

where is a weighting function that gives higher weight to prior years with similar weather to the projected weather. The PWMSE can provide a good approximation to the ideal target in (15), if for each there exists a year in the sample that resembles the corresponding projected climate. The two criteria trivially coincide if and for all . Intuitively, the weighting function ensures that the selected model provides improved prediction of climate change impacts for years with climates that resemble the corresponding projected climate, .

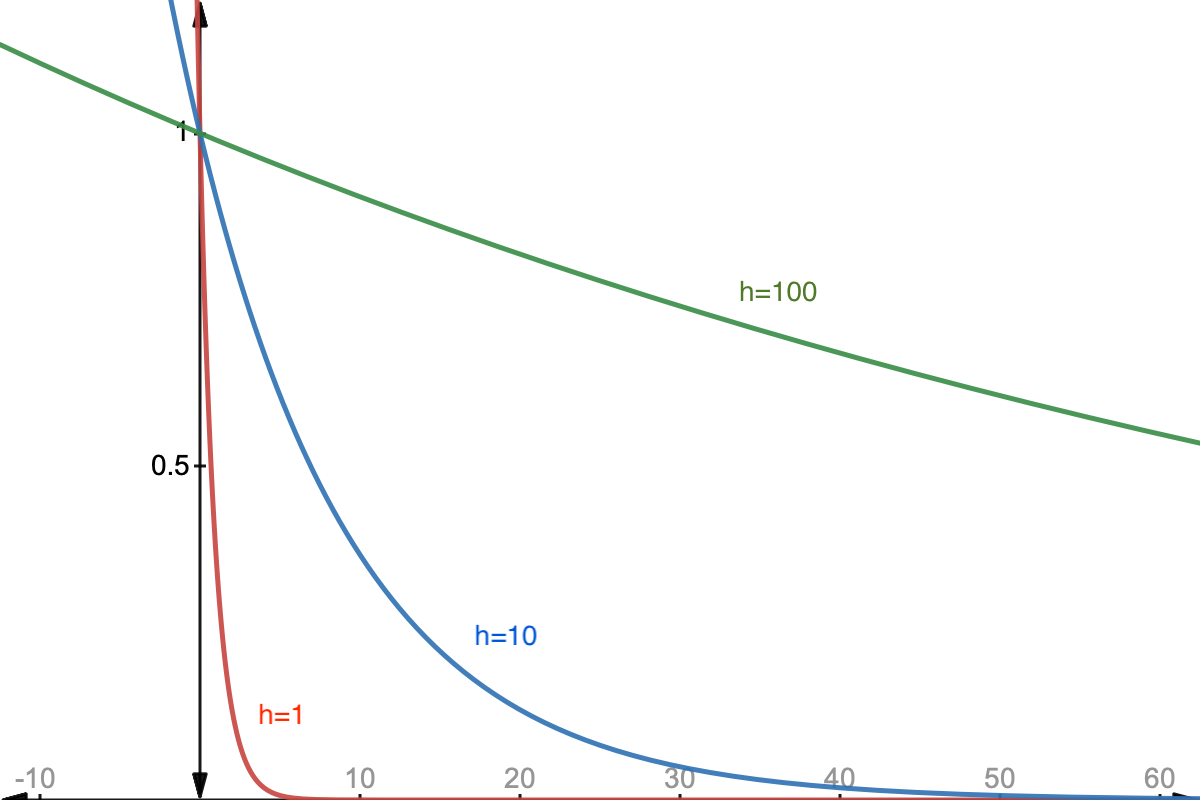

In practice, the weighting function is a user-specified component in the PWMSE criterion. The function should be non-negative, bounded, and decrease with the distance between and the target . A natural choice for the weighting function is the following:

which decays exponentially as the distance between and grows as measured by the norm, .

The choice of the norm should be guided by what aspects of the projected climate the researcher or policymaker would like to mimic. In the simulation section, we consider norms of the difference in annual and monthly mean temperature with a moderate level of the tuning parameter . We also examine the impact of other different norms as well as the choice of the tuning parameter in additional simulations in Online Appendix F.1, and we provide guidance for practitioners on the choice of norms and the tuning parameter in Online Appendix F.2.

In order to estimate the PWMSE in practice, we propose the following MCCV procedure,

-

1.

For each randomly split individuals into a training sample of size and a testing sample of size . Use training sample to estimate and use the testing sample to compute the out-of-sample MSE,

(22) where .

-

2.

Repeat Step 1 times and compute the average (for variance reduction purposes),

(23)

Next, we show that the model that minimizes minimizes with probability one as . Before we proceed to the proposition, we introduce the required conditions.

Condition 1 (Consistency of FE).

The following conditions hold:

-

1.

for all and .

-

2.

are (stochastically) independent across .

-

3.

There exist constants and such that for all , , and the following moment conditions hold

(24) where .

-

4.

is uniformly positive definite for all and .

-

5.

The following limits exist for all , , , and

(25) (26) where .

Condition 1 provides the set of sufficient conditions for the consistency of the to be established in Proposition 1. It includes the conditions required for the almost sure consistency of the FE estimator for misspesified models in the case of independent, heterogeneously distributed observations. They are analogous to sufficient conditions for the consistency of the OLS estimator in White [2014, Exercise 3.14] but have two subtle differences, Eq. (24) and Condition 1.5, which we explain below.

Condition 1.1 is an augmented version of the strict exogeneity assumption that includes the projected climate . Augementation is required to make sure that the weights are not correlated with the scores when establishing consistency of .232323 In principle, one can imagine that the economic variables in a location may have effect on the weather projections for that location through the anthropogenic climate feedback, which would invalidate Condition 1.1. However, this feedback is typically modeled only through the total global human influence and does not include direct impact of the local economic activity, which can be seen from the descriptions on general circulation models [Teixeira et al., 2014]. As a result, any dependence of the mean of on future projections can be assumed negligible.

The cross-sectional independence assumption (Condition 1.2) is imposed on both regressors and residuals. It is one of the sufficient conditions for the consistency of and the application of the uniform law of large numbers to the PWMSE. Remark 1 below discusses that one can accommodate arbitrary dependence between the regressors across in the presence of heterogeneity in the distribution under the assumption of bounded support. Independence of across (unconditional or conditional on the regressors) can be replaced by a weak-dependence assumption across . This would, however, invalidate certain standard inference procedures, including cluster-robust standard errors for FE estimators. Finally, we emphasize that Condition 1.2 allows for arbitrary serial correlation and does not restrict the dependence of across . Therefore, the outcome may be spatially correlated under Condition 1.2 through fixed effects .

Condition 1.3 is a sufficient condition for the applicability of Markov’s law of large numbers that results in the almost sure consistency of and for all . It is a rather mild moment restriction that is commonly assumed. The difference with the standard conditions for consistency (Exercise 3.14 in White [2014]) is the moment restriction on given in (24). It is required for the consistency of the PWMSE criterion.

Similar to the conventional OLS setup, Condition 1.4 (no multicollinearity in approximate models) is required for the consistency of the FE estimator .

Finally, Condition 1.5 ensures the existence of a well-defined limit of the FE estimator in case of misspecified models (it is redundant for correctly specified models). This condition also requires the existence of limits for the weighted averages of the means which is an important step to establish consistency of the PWMSE criterion. In the cases of spatially distributed data, this condition would be satisfied if the corresponding mean functions considered as a function of continuous coordinates are Lebesgue integrable, in which case the limits on the right-hand side expression coincides with integrals over the geographic domain with weights equal to the spatial intensity of the observations.242424It is a direct corollary of Theorem 5.24 and Corollary 5.41 in Kallenberg et al. [2017], as long as the spatial point process of weather measurement locations is stationary and ergodic.

Remark 1.

Note that the independence of across is essentially without loss of generality. One can apply the theory in presence of arbitrary dependence of weather measurements across as long as have bounded support, which is a realistic assumption in the case of the geophysical variables. In this case, one can interpret the independence of across as independence conditional on and moments (24) in conditional expectation sense with the same conditioning. Bounded support for would immediately imply a conditional expectation version of (24). One should keep in mind, however, that the regression coefficients and the notion of the best approximate model would depend on a particular draw of the spatial weather distribution. ∎

Proposition 1.

Consider a finite class of models . Suppose that Condition 1 holds, and , as holding fixed, and the split into training and validation samples is uniform and random. Then, the model that minimizes also minimizes in the class of models with probability 1 as the sample size grows.

The proof is provided in Appendix A. If the model with minimal error is unique, Proposition 1 implies that selects that model as the training and validation sample sizes grow. Otherwise, is guaranteed to select one of the models that minimize with probability 1 as the training and validation sample sizes grow.

The feasible criterion is only an approximate version of the ideal criterion (19) — if all of the historical data do not have any resemblance to the future climate, the criterion will fail at selecting a model that can perform well in terms of the ideal target. In such an unfortunate occasion, however, none of the existing alternative methods would perform better since they are not using any information about the distribution of the future weather, unless one of the models under consideration nests the true model. That is, in the absence of historical observations analogous to the future climate, the only practical solution would be to make sure that one of the models under consideration is correctly specified and rely on a consistent model selection procedure.252525Alternatively, one can impose the random effects assumption on and consider comparing model damage function predictions across locations and time (instead of time only). This approach can be used if the forecasts of the weather are very different from the historical data. For example, a climate projection may predict that London becomes as hot as Cairo is now. If there is no historical analog of Cairo-type weather for London, then under the random effect assumption one can use Cairo’s observations as analog for future London climate in PWMSE computation. We leave this extension for future work.

3.3 Simulation Study

We design a simulation study to illustrate the finite-sample performance of the MCCV, GIC and PWMSE criteria. We consider three DGPs of an outcome-temperature relationship: (i) the annual mean model (), (ii) the quadratic in annual mean model (), and (iii) the quarterly mean model (), and we evaluate the performance of each model selection criterion for selecting among a broader set of models.

The following functions generate the outcome for the three DGPs we consider which correspond to the examples we provide in Example 1:

-

•

Annual Mean (): ,

-

•

Quadratic in Annual Mean (): ,

-

•

Quarterly Mean (): ,

For each of the DGPs, we use a random sample of counties from the National Climatic Data Center (NCDC) temperature dataset for the years 1968-1977 as for and , where . For each simulation replication, we generate , where . The idiosyncratic shocks are generated as a bivariate mixture normal that is heteroskedastic and serially correlated as follows. Let , where and , with

| (47) |

For each DGP, we consider different subsets of the following set of models:

-

•

Annual Mean (): ,

-

•

Bi-annual Mean (): ,

-

•

Quarterly Mean (): ,

-

•

Monthly Mean (): ,

-

•

Quadratic in Annual Mean (): ,

-

•

10∘F Bins (): .

Since the ideal target in (15) involves future climate, we use the year of 1997 as the future period, twenty years after the last period of the 1968-1977 sample (i.e., ). In addition, we also consider other future climates by treating 1992 and 2002 as alternative future periods (i.e., ), respectively. Data for these three years come from the same county-level NCDC temperature dataset.

Given the importance of the pseudo-true parameter values as well as our ideal target evaluated at these values in our theoretical analysis, we simulate these quantities for models , , , , , and using simulation replications using the sample of all counties in our dataset () to ensure that our simulated quantities are as close as possible to their population analogues.

Table 2 presents simulated pseudo-true parameter values .262626We compute these values by taking the simulation mean of the estimated coefficients using the entire NCDC sample for each model across 2,000 simulations. We also simulate the ideal target for our sample for , where . The results indicate that the ideal target is minimized when the model being considered is the DGP (true model). However, we note that the simulated ideal target is very close to that of the true model for models that nest it. In Appendix Table A1, we also report the ideal targets calculated for and , respectively. The results are qualitatively similar.

We use the same random sample of counties from the full NCDC sample of 3,074 counties and use the temperature data for these counties between 1968-77 as our high-frequency regressor in all the simulation designs. The outcome variable is generated using the DGP in question. All regression models are implemented on the generated data and the eight model selection criteria presented below are calculated for each model:

-

•

MCCV ()

-

-

(MCCV with fixed training-to-full sample ratios, hereinafter MCCV-),

-

-

(MCCV with vanishing training-to-full sample ratios, hereinafter MCCV-Shao);

-

-

-

•

, where ,

-

-

(AIC),

-

-

(BIC),

-

-

(SW1),

-

-

(SW2);

-

-

-

•

PWMSE with weights specified as

-

-

norm of monthly differences with the tuning parameter (PWMSE1),

-

-

norm of yearly differences with the tuning parameter (PWMSE2).272727For formal definitions of these norms, see Section F.1.

-

-

The simulation probabilities (proportions) of selecting a particular model using each of the criteria are computed using 500 simulation replications.282828For the Monte Carlo cross-validation procedure of PWMSE as described in Online Appendix 3.2, we use and within each simulation.

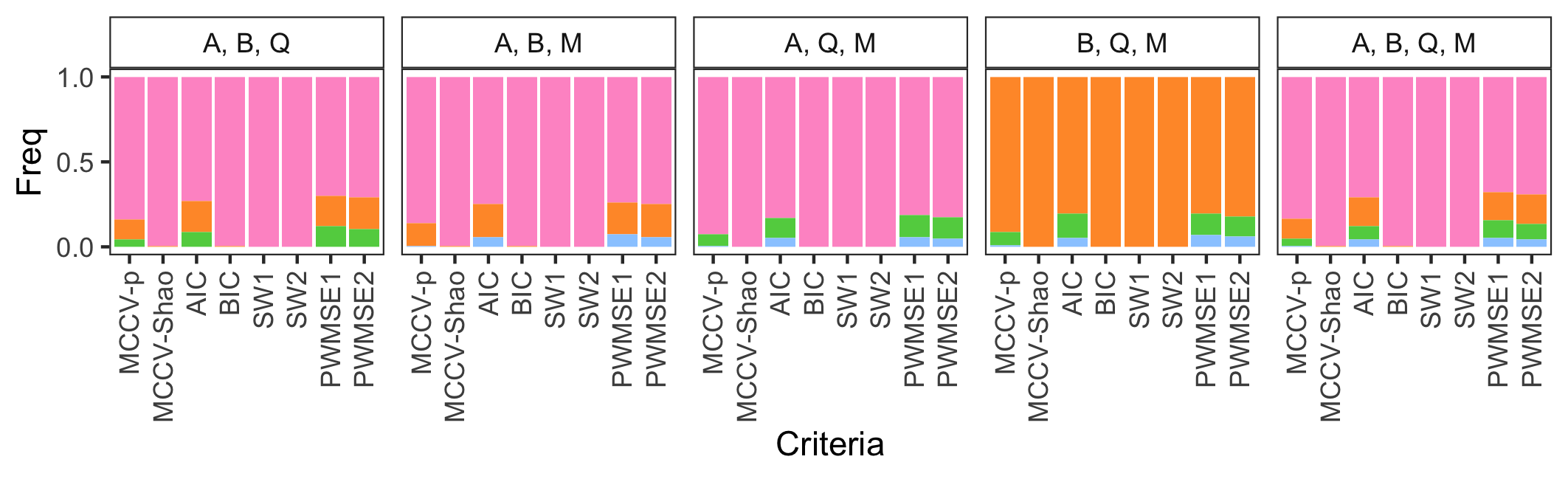

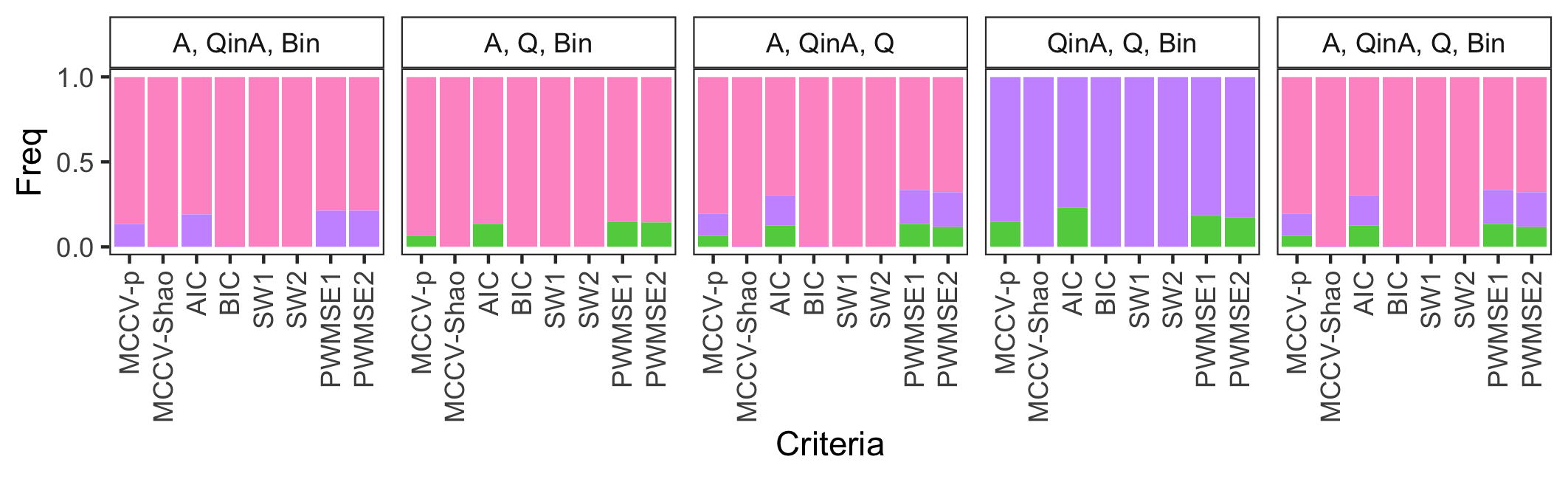

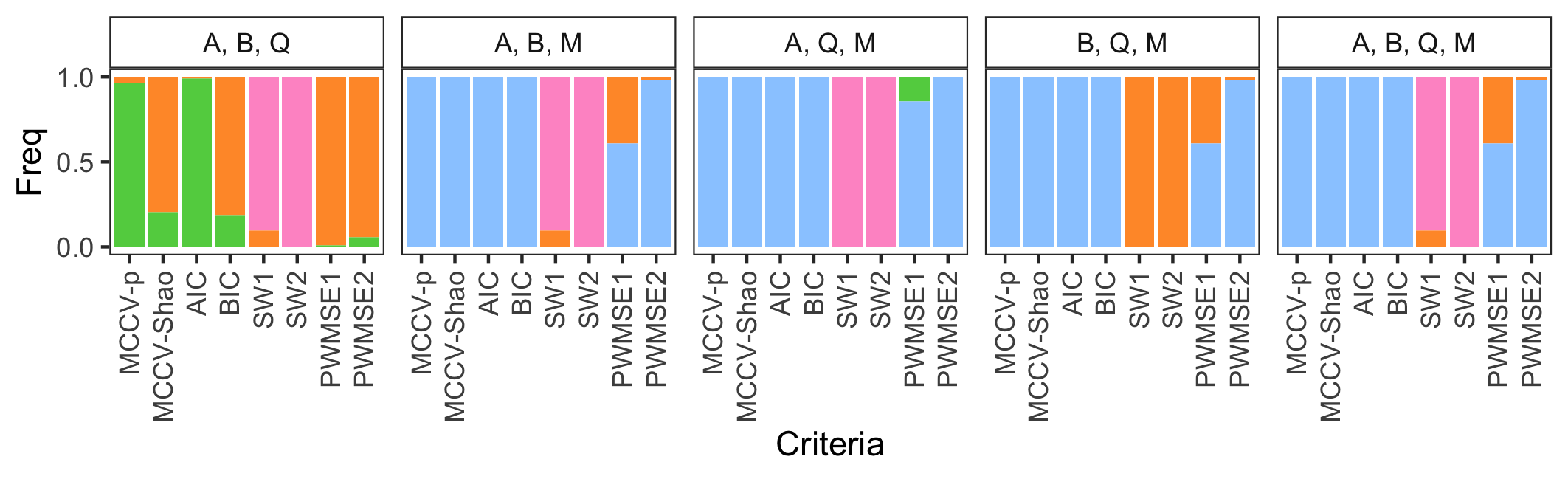

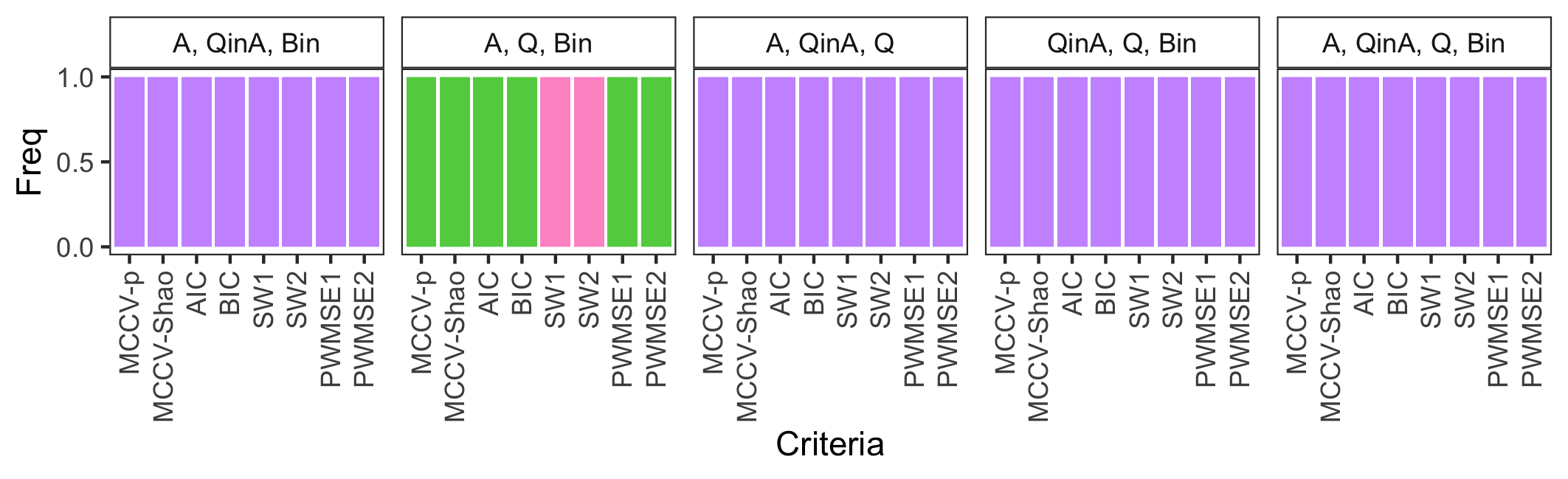

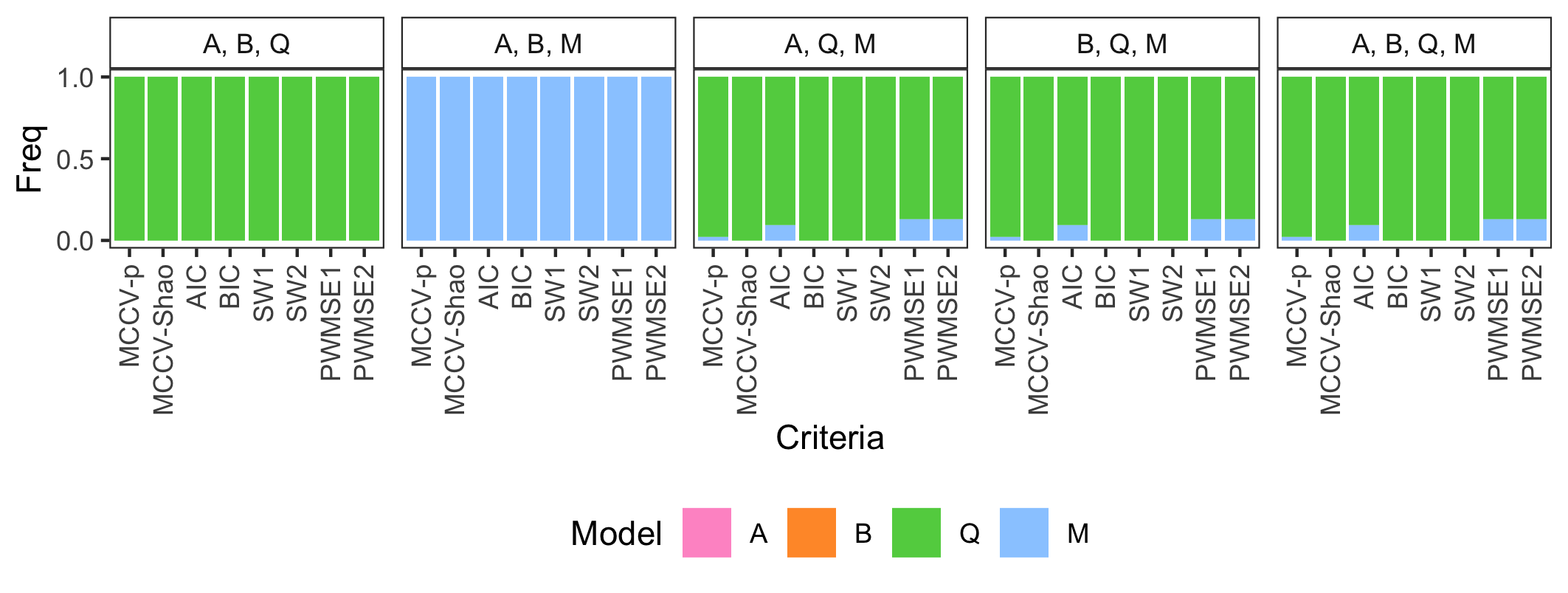

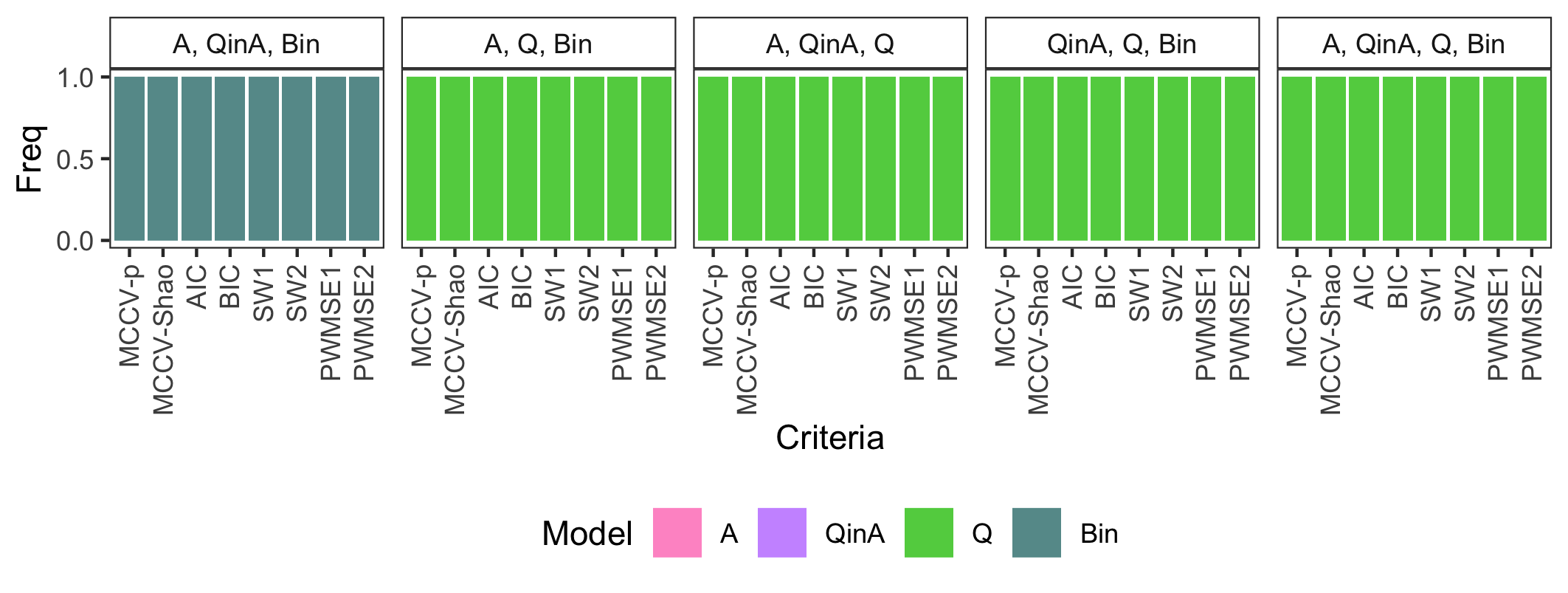

Figure 3 presents the simulation results for . The figure is arranged in three rows with each corresponding to a specific DGP (i.e., , , ). Within each row, we consider two groups of comparisons: (i) across nested models (i.e., , , , ), and (ii) across possibly non-nested models (i.e., , , , ). Within the nested/non-nested models, we compare across all the four models as well as all combinations of every three out of the four models, which allows us to make systematic evaluations when the true model is included or excluded in the set of candidate models. Within each panel, each bar corresponds to a specific model selection criterion, and the height of a colored bar indicates the simulation proportion of a model being selected.

The results illustrate that, when the true DGP is in the set of models under consideration, all model selection criteria select the true model with high simulation probabilities. The MCCV with vanishing training-to-full sample ratios, BIC and the SW criteria select it with simulation probability approaching one, while AIC, MCCV with fixed training-to-full sample ratios, and the two PWMSE criteria show a non-zero probability to choose the less parsimonious model that nests the true DGP in certain circumstances.

When all models under consideration are misspecified, however, different criteria tend to select different models. This difference is most evident in the results for DGP. In particular, the SW criteria tend to select the most parsimonious model, while the PWMSE is more likely to select the model that corresponds to the smallest value of the ideal target. This can be seen when considering the set of models . Referring to Table 2, under DGP, is the most parsimonious model but is the misspecified model that corresponds to the smallest value of the ideal target.292929Note that BIC exhibits pseudo-inconsistency in this context, selecting and , unlike the pseudo-consistent SW criteria which select with probability equal to 1. We provide a formal explanation of the behavior of BIC in nested, misspecified model selection problems in Online Appendix E.

We note that here we only report results considering the future period of and our PWMSE formations are based on two weight specifications. We present a set of extended simulation results under different future climates as well as using PWMSE with weights formed based on different combinations of the norms and tuning parameters. We make detailed discussions of these additional results in Online Appendix F.1.

3.4 Implications for Practice

The theoretical and simulation results have several implications for the use of model selection criteria in climate change impact studies. When the true model is considered in a set of models, all criteria we have discussed above tend to select the true model with high probabilities. In particular, MCCV with vanishing training-to-full sample ratios, BIC, and the SW criteria select it with probability approaching one as sample size grows. This illustrates the usefulness of the existing criteria in the context where the scientific literature can guide the applied researchers on the underlying relationship between climatic factors and the economic outcome of interest.

When all models being considered are misspecified, which is likely for many outcomes of interest in practice, different model selection criteria may favor different models. This issue is particularly concerning when the policy objective is to understand climatic impacts under a specific future climate projection. The existing model selection criteria do not incorporate the projected future climate into model selection and therefore would choose the same model regardless of the climate projection in question. By contrast, the PWMSE chooses the best approximate model for a given climate projection. Consistent with our theoretical predictions, the advantage from the PWMSE relative to existing criteria is greater when all models under consideration are misspecified. Given the importance of the choice of the weighting function when using the PWMSE in practice, we provide detailed guidance in Online Appendix F.2 on the choice of the norm and tuning parameter.

Finally, we recommend that practitioners report the results of the different criteria we consider, including the PWMSE. As we illustrate in the next section, comparing the models selected by the different criteria can aid practitioners in interpreting their empirical results.

4 Empirical Application: Temperature and Crop Yields

In this section, we illustrate the model selection criteria we examine in a classic context of the empirical literature — identifying nonlinear temperature effects on crop yields. The agronomic studies have documented that the accumulation of heat is only beneficial to crop growth over certain ranges of the temperature and becomes detrimental otherwise [Ritchie and Nesmith, 1991]. Previous statistical analyses also find evidence of nonlinearity in crop yield response to temperature under different estimation specifications [e.g., Schlenker and Roberts, 2009, Burke and Emerick, 2016, Gammans et al., 2017]. However, the qualitative similarity of nonlinearity does not diminish the importance of exploring the quantitative difference between alternative specifications, especially considering that nuances in the estimation results could be substantially magnified when it comes to projecting future climate impacts.

In this empirical application, we consider different specifications of temperature variables in the following model,

where represents corn yield (bushels/acre) in county in crop year . The response function is a linear function of regressors constructed from the daily temperature time series over the growing season .303030Previous studies have shown the importance of considering within-season temperature variation in modeling the response of crop yields since the seminal work in Schlenker et al. [2006] and Schlenker and Roberts [2009]. represents growing-season total precipitation, and characterize state-level quadratic trends, represents county fixed effect and is the error term.

We consider the following set of temperature specifications: (a) reference model with no temperature variables, (b) monthly average temperatures, (c) 1∘C daily temperature bins, (d) 3∘C step function, (e) degree days in the fashion of Schlenker et al. [2006] (SHF degree days, hereafter), (f) piecewise linear function with one knot, and (g) piecewise linear function with two knots. Models (a)-(f) are model candidates considered in Schlenker and Roberts [2009], and model (g) is a more flexible variant of (f).313131Model (c) uses bins constructed based on daily average temperatures, while (d) further utilizes diurnal variation in temperature by employing a sinusoidal interpolation between daily maximum and minimum temperatures before forming relevant bins. All the models above only consider growing-season temperatures. The two piecewise linear specifications rely on knots selected by minimizing MSE.323232We present the smallest ten MSEs in Appendix Table A3. Although the specifications considered here are not exhaustive, we believe they are sufficiently rich to illustrate the differentiated performances among different model selection criteria.

We obtain county-level corn yield data covering 1950-2015 from USDA Quick Stats. The source of historical weather information is the PRISM dataset, which provides spatially gridded daily data at 4km-by-4km resolution. We follow the data managing procedure in Schlenker and Roberts [2009] and obtain county-level daily temperature and precipitation over 1950-2015. Based on the merged county-level data, we first conduct estimation using an unbalanced panel of all available observations. This unbalanced sample contains 2,278 counties with a total of 120,995 observations. The estimation results, as reported in Appendix Table A4, are in line with previous findings.333333We also report the SNR for each model, and these ratios are mostly close to 0.40. When calculating, we consider all weather variables as the signal component, and we obtain the SNRs by projecting out all the time trends and fixed effects. We also implement the estimation based on a balanced panel of 679 counties in the core region of the corn belt, with a total of 44,814 observations. The estimation results, presented in Appendix Table A5, are qualitatively similar.

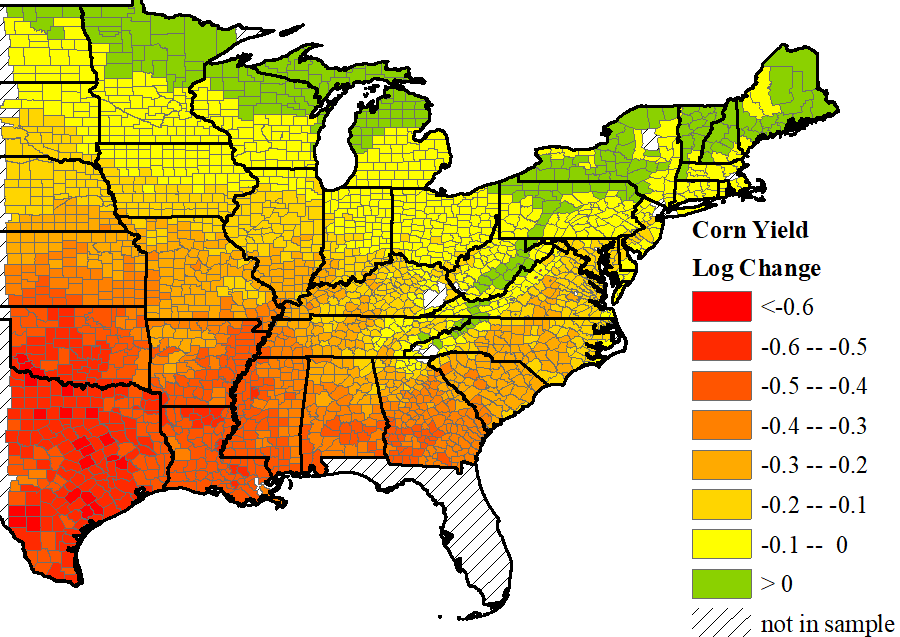

We illustrate the different projection results based on these empirical estimates in the mid-century. Specifically, we recalculate all relevant temperature variables for the 2050 climate at the county level using projected climate data from the HadCM3-B1 model. We then calculate the predicted changes in these temperature variables at the county level by differencing their 2050 values with their 2015 counterparts, and form predicted changes in log yields by applying different sets of the empirical estimates. The predicted changes in log yields based on different models are mapped in Figure 4.

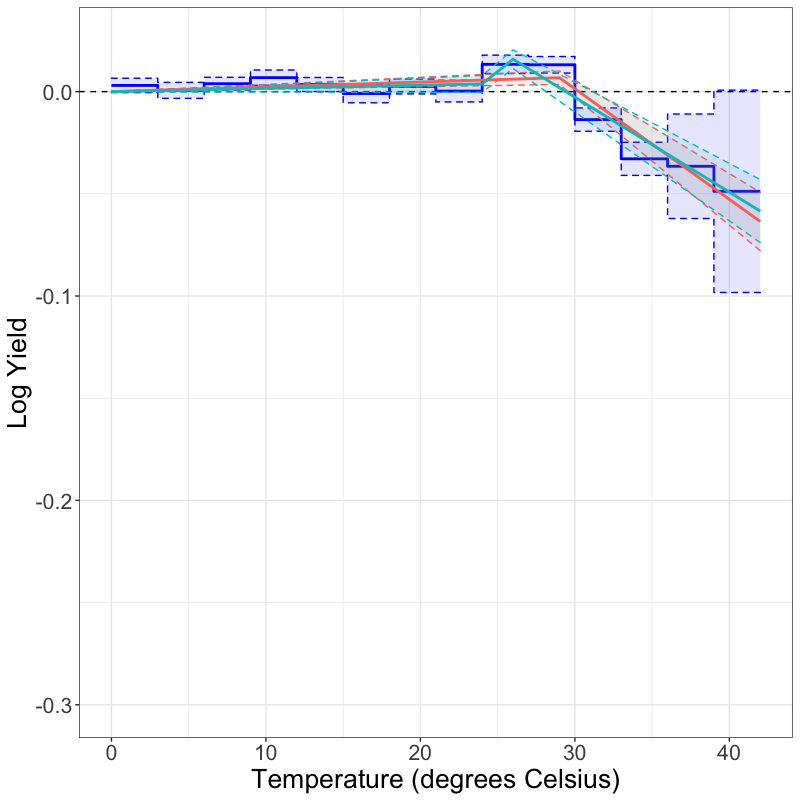

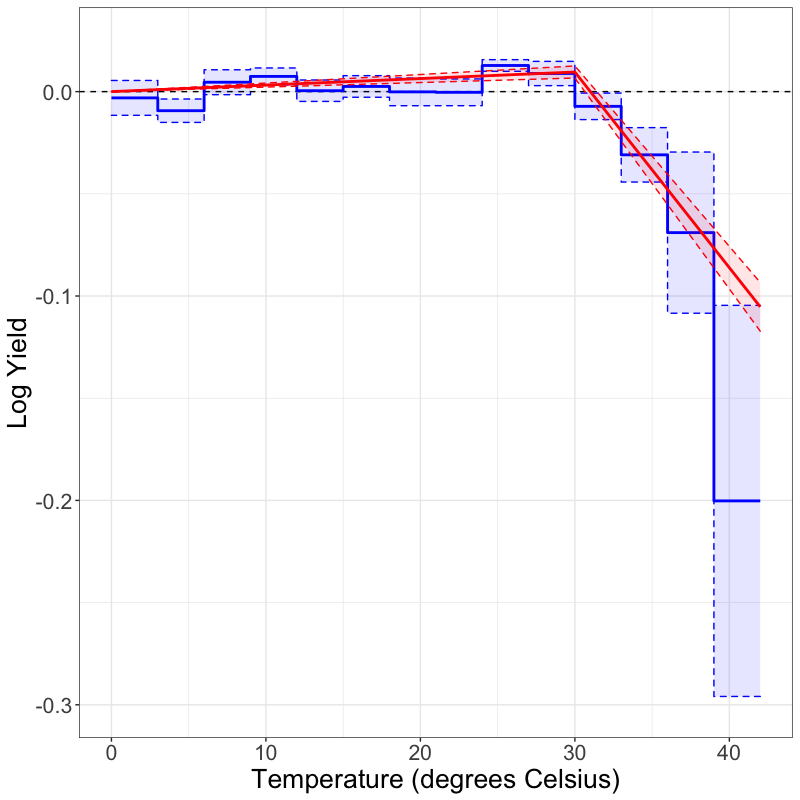

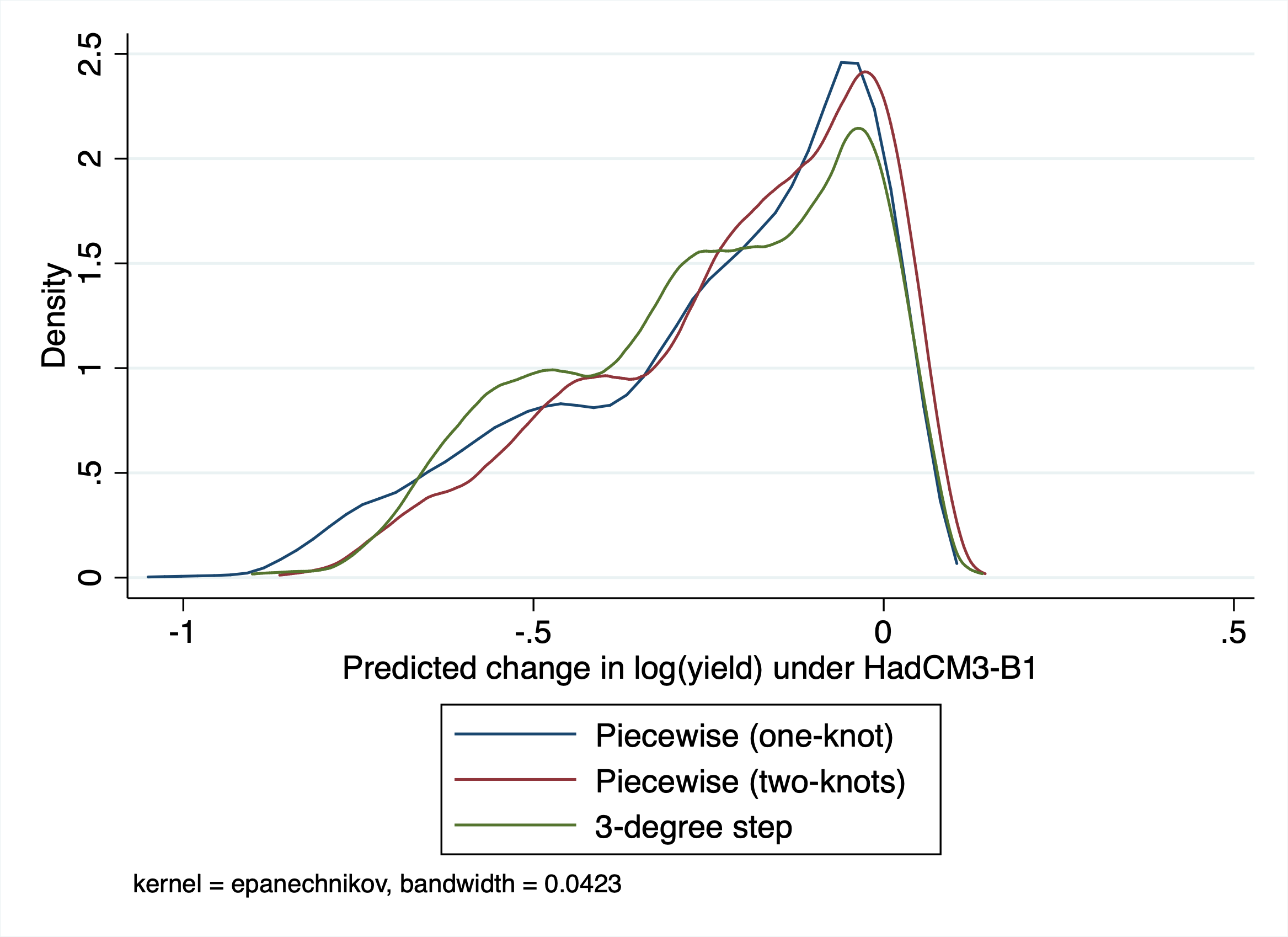

As for model selection, we first apply the existing model selection criteria, including the two MCCV and the four GICs. Table 3 shows that, evaluated on the unbalanced panel, AIC and BIC select the 3∘C step function, the two cross-validation procedures and SW1 select the two-knot piecewise function (knots at 24∘C and 26∘C), and SW2 selects the one-knot piecewise linear function (knot at 29∘C). When evaluated on the balanced panel, both AIC and BIC still select the 3∘C step function, while the two SW criteria and the two MCCV procedures all choose the one-knot piecewise function for which the MSE-minimizing knot is at 30∘C. We visualize these selected nonlinear temperature response functions in Figure 5. Although the nonlinear patterns are qualitatively similar for these selected models, those piecewise models selected by MCCV and SW criteria are more parsimonious while the step function selected by AIC and BIC is more complex.

As we discussed earlier, none of the criteria above are specifically tailored for the policy objective of better understanding potential future impacts of climate change. Therefore, we apply our proposed PWMSE criteria that incorporate projected future climatic conditions to the seven candidate models with . Since the finest temporal resolution of our HadCM3-B1 projection data is at the monthly level, we consider the norms based on monthly and annual differences when forming weights. In Table 4, we present the PWMSE for each model evaluated with different weights for the unbalanced panel and the balanced panel, respectively. Specifically, we consider the case with no weight specified, and the cases with weights based on the and norms of annual and monthly temperatures (i.e., M1, M2, Y1, and Y2, respectively), scaled by , respectively. For the unbalanced panel, the PWMSEs are minimized by the model of 3∘C step function except for the cases of where the selected model is degree days in the fashion of Schlenker et al. [2006] (i.e., SHF degree days).343434The SHF degree days include three variables: the growing degree days (GDD), the square of GDD, and the square-root of heat degree days (HDD). GDD accumulates degree-by-days in the range of 8-32∘C and HDD accumulates degree-by-days above 34∘C. But we note that setting in this unbalanced panel exercise may have assigned much higher weights to some of the historical observations that correspond to less frequent growing counties on the peripheral regions of the corn belt. For the balanced panel, the model of 3∘C step function delivers the lowest PWMSE regardless of how we specify the weights.

Compared with the models selected by the SW criteria, the PWMSE criterion selects models that result in a qualitatively similar damage function, as we illustrated visually in Figure 5. We also note that the piecewise functions selected by the SW criteria deliver PWMSEs that are only slightly larger than those of the 3∘C step function. These similarities may reflect that both models are fairly close approximations of the underlying DGP, especially considering that they deliver damage functions that are consistent qualitatively with agronomic predictions.

The models selected by the SW criteria are more parsimonious compared with those selected by the PWMSE criterion. This result is consistent with our theoretical discussion and simulation illustration. Nevertheless, we highlight that only the PWMSE criterion takes the projected future climate into account directly through specifying the weights, while the SW criteria only depend on the historical observations. Our results indicate that the larger model of the 3∘C step function provides higher flexibility that potentially improves the projection-specific prediction for the policy objective of climate change projection. This tailored model selection has quantitative implications since the predicted outcomes under HadCM3-B1, although similar in their spatial gradient, have noticeable differences in their extents of yield reductions across the piecewise and 3∘C step functions, as illustrated in Appendix Figure A5. These quantitative differences matter for the policy arrangements of investment activities and adaptation efforts that target specific areas toward a given future climate projection.

5 Conclusion

This paper formalizes the model selection problem as well as the policy target faced by applied researchers and policymakers interested in examining climate change impacts on outcomes of interest. Building on this crucial first step, the paper first provides conditions under which existing criteria, specifically MCCV and GICs, are appropriate for the policy objective. We show that consistent model selection criteria are suitable if at least one of the models under consideration nests the truth. Since this requirement is restrictive for economic outcomes for which the relationship with temperature is not well understood, we propose a proximity-weighted MSE criterion that targets the MSE of projected climate change impacts directly. We illustrate that these criteria choose models that minimize the ideal target with high probability in a simulation analysis. We demonstrate the empirical relevance of our theoretical analysis in the context of an application on climate change projection of agricultural yields.

While this paper constitutes an important first step toward principled model selection in this policy-relevant empirical context, there are several interesting directions for future research. In light of recent work on exogeneity in climate econometrics [Pretis, 2021], developing methods that relax the strict exogeneity assumption is an important direction for future work. More flexible procedures to estimate the response functions would also be a good substitute to the model selection approach taken in this literature. Furthermore, allowing for possible nonlinearities between regressors and fixed effects is another important departure from the setup in this paper. Finally, providing valid post-selection inference for the aforementioned methods constitutes a priority for future work.

Appendix A Proof of Proposition 1

The proof proceeds in 5 steps.

Step 1 (Auxiliary Limits). Consider any subsample out of cross-sectional units of growing size . Under Conditions 1.2 and 1.3, one can apply Propositions 3.9 and Corollary 3.9 (Markov’s law of large numbers) from White [2014] to show that the following sums converge to 0 almost surely,

| (48) | |||

| (49) | |||

| (50) |

where for each (indices domains are ; and ).

Step 2 (Consistency of FE estimator). Consider the FE estimator for a subsample with split index for the model that determines ,

| (51) |

(As before, the true regressors can be chosen equal to even if the true model does not admit finite linear index representation.)

Under Condition 1, the corresponding population analog exists. Since the split is taken at random, the limit coincides with the full sample limit,

| (52) |

By Step 1, the law of large numbers implies as for each and under consideration. As a result, one can define the approximate damage function as .

Step 3 (Uniform LLN for PWMSE). Consider the PWMSE estimate based on a single sample split ,

| (53) |

and its component for an individual time period ,

| (54) |

Let be any compact subset of that contains as an interior point. By Step 2, with probability 1 as grows.

For each , consider an empirical process indexed by a vector .

| (55) |

where operator notation is used to define an empirical process indexed by . This process can be rewritten as

| (56) | ||||

| (57) | ||||

| (58) |

By Step 1, the LLN applies for each of the coefficient matrices above. Since the index set for the empirical process is a compact set in a finite-dimensional Euclidean space,

| (59) |

It implies for each as

| (60) |

where

| (61) | |||

| (62) | |||

| (63) | |||

| (64) |

Step 4 (Conditional Expectation of PWMSE). This component can be rewritten as

| (65) | |||

| (66) | |||

| (67) |

The term (65) can be further decomposed as follows,

| (68) | |||

| (69) | |||

| (70) | |||

| (71) |

The conditional expectation of the cross-product term (71) is given by

| (72) | |||

| (73) | |||

| (74) |

where the last equality follows from the independence of the training and validation samples. In addition, under strict exogeneity (Condition 1.1), we obtain the following,

| (75) | ||||

| (76) |

Summarizing the previous steps,

| (77) | ||||

| (78) | ||||

| (79) | ||||

| (80) | ||||

| (81) | ||||

| (82) |

where . The last term in the displayed formula above does not depend on so it will not affect the model selection.

Step 5 (Using continuous mapping theorem). As a result of equation (60) and Step 4, the model that minimizes as also minimizes with probability 1 the following expression

| (83) |

where and

by the continuous mapping theorem. Since by Step 2 , the model selected by also minimizes with probability 1 as the sample size grows. ∎

References

- Addoum et al. [2020] J. M. Addoum, D. T. Ng, and A. Ortiz-Bobea. Temperature shocks and establishment sales. The Review of Financial Studies, 33(3):1331–1366, 2020.

- Adhvaryu et al. [2020] A. Adhvaryu, N. Kala, and A. Nyshadham. The light and the heat: Productivity co-benefits of energy-saving technology. Review of Economics and Statistics, 102(4):779–792, 2020.

- Anderson et al. [2017] R. W. Anderson, N. D. Johnson, and M. Koyama. Jewish persecutions and weather shocks: 1100–1800. The Economic Journal, 127(602):924–958, 2017.

- Andreou and Ghysels [2006] E. Andreou and E. Ghysels. Sampling frequency and window length trade-offs in data-driven volatility estimation: appraising the accuracy of asymptotic approximations. In D. Terrell and T. B. Fomby, editors, Econometric Analysis of Financial and Economic Time Series, Advances in Econometrics, Volume 20 Part 1, pages 155–181. Emerald Group Publishing Limited, 2006.

- Andreou et al. [2010] E. Andreou, E. Ghysels, and A. Kourtellos. Regression models with mixed sampling frequencies. J. Econometrics, 158(2):246–261, 2010. ISSN 0304-4076. doi: 10.1016/j.jeconom.2010.01.004. URL http://dx.doi.org/10.1016/j.jeconom.2010.01.004.

- Aragón et al. [2021] F. M. Aragón, F. Oteiza, and J. P. Rud. Climate change and agriculture: Subsistence farmers’ response to extreme heat. American Economic Journal: Economic Policy, 13(1):1–35, 2021.

- Arellano [2003] M. Arellano. Panel Data Econometrics. Oxford: Oxford University Press, 2003.

- Arlot and Celisse [2010] S. Arlot and A. Celisse. A survey of cross-validation procedures for model selection. Statistics Surveys, 4:40–79, 2010. doi: 10.1214/09-SS054.

- Auffhammer [2018] M. Auffhammer. Quantifying economic damages from climate change. Journal of Economic Perspectives, 32(4):33–52, 2018.

- Auffhammer et al. [2017] M. Auffhammer, P. Baylis, and C. H. Hausman. Climate change is projected to have severe impacts on the frequency and intensity of peak electricity demand across the united states. Proceedings of the National Academy of Sciences, 114(8):1886–1891, 2017.