Reflected maxmin copulas and modeling quadrant subindependence

Tomaž Košir,

Faculty of Mathematics and Physics, University of Ljubljana, Slovenia

Department of Mathematics, Institute of Mathematics, Physics, and Mechanics, Ljubljana, Slovenia111The authors acknowledge the financial support from the Slovenian Research Agency (research core funding No. P1-0222, and research funding No. L1-6722).

E-mail address:tomaz.kosir@fmf.uni-lj.si

Matjaž Omladič,

Department of Mathematics, Institute of Mathematics, Physics, and Mechanics, Ljubljana, Slovenia1

E-mail address:matjaz@omladic.net

Abstract

Copula models have become popular in different applications, including modeling shocks, in view of their ability to describe better the dependence concepts in stochastic systems. The class of maxmin copulas was recently introduced by Omladič and Ružić [21]. It extends the well known classes of Marshall-Olkin and Marshall copulas by allowing the external shocks to have different effects on the two components of the system. By a reflection (flip) in one of the variables we introduce a new class of bivariate copulas called reflected maxmin (RMM) copulas. We explore their properties and show that symmetric RMM copulas relate to general RMM copulas similarly as semilinear copulas relate to Marshall copulas. We transfer that relation also to maxmin copulas. We also characterize possible diagonal functions of symmetric RMM copulas.

Dependence concepts play a crucial role in multivariate statistical literature since it was recognized that the independence assumption cannot conveniently describe the behavior of a stochastic system. Since then, different attempts have been made in order to provide more flexible methods to describe the variety of dependence-types that may occur in practice. Copula models have become popular in different applications in view of their ability to describe the relationships among random variables in a flexible way. To this end, several families of copulas have been introduced, motivated by special needs from the scientific practice (cf. [9, 11, 20]).

Consider, for instance, the case when one wants to build a stochastic model for describing the dependence among

two (or more) lifetimes, i.e. positive random variables. In engineering applications, joint models of lifetimes may serve to estimate the expected lifetime of a system composed by several components. In a related situation like portfolio credit risk, instead, the lifetimes may have the interpretation of time-to-default of firms, or generally financial entities, while a stochastic model may estimate the price/risk of a related derivative contract (e.g. CDO). In both cases, it is of interest to estimate the probability of the occurrence of a joint default. The generation of convenient statistical distributions for modeling such situations originated from the seminal paper by Marshall and Olkin [18], for an up-to-date review see [2]. They consider the case of a 2-component system (which may be easily extended to more components) whose behavior is described by the continuous random variables (=r.v.’s) and distributed according to a continuous distribution function for . Furthermore for each consider the random variable with probability distribution function , that can be interpreted as a shock that effects only the -th component of the system, i.e., the idiosyncratic shock. In addition, consider an r.v. with probability distribution function that can be interpreted as an (exogenous) shock that affects the stochastic behavior of both system components. The life-times of components in this model (which is basically the Marshall model, somewhat more general than the Marshall-Olkin model [18, 17] – see also [4] for the description of a general framework) are linked with the shocks via and .

In a recent paper Omladič and Ružić [21] extend results of Marshall and Olkin, cf. also [8], by introducing a new class of copulas. A simple model where these copulas occur naturally is a two-component system similar to the above in which we assume that the first of the two components has a recovery option. This assumption affects the linkages substantially. As a matter of fact, we get and . The authors of [21] develop the resulting copula of this model again in a closed form and call it the maxmin copula. Various interpretations of this model can be found in [8], since it is possible in many practical situations that the common exogenous shock will produce different effects on different system components. For instance, we may think of and as r.v.’s representing the respective wealth of two groups of people, and the exogenous shock is interpreted as an event that is beneficial to the first group and detrimental to the second one. Analogously, and can be thought as a short and a long investment, respectively, while is beneficial only to one of the types of investment.

Maxmin copulas have some properties that are appealing in various contexts related to fuzzy set theory and multicriteria decision making. It includes nonsymmetric copulas that are used for instance as more general fuzzy connectives [1, 6]. Its associated measure may have a singular part, a fact of potential use in various copula-based integrals (see [14, 15]). As we shall show in what follows the main idea for maxmin copulas is reflected to probabilistic extensions of semilinear copulas, so it might be worth while to study possible analogues to their extensions to various classes of constructions (cf. [12, 13]).

In a seminal paper Durante et al. [6] introduce semilinear copulas and give a surprising relation between these copulas and Marshall’s copulas. The idea of these copulas is roughly that, given a diagonal section , they extend linearly across the two triangles. More precisely,

where convention is adopted, is called (lower) semilinear copula. The authors of [6] observe that every symmetric Marshall copula is actually semilinear and moreover [6, Proposition 8], for every Marshall copula there exist semilinear copulas and such that, for all ,

In Section 2 we shortly review the maxmin copulas, introduce the reflected maxmin (RMM) copulas, and give some properties of this class of copulas. Section 3 is devoted primarily to the singularity and absolute continuity of RMM copulas. In Section 4 we give a statistical interpretation of this class of copulas, and in Section 5 we study the properties of the diagonals of symmetric RMM copulas.

2 Maxmin copulas revisited

A maxmin copula has two generating functions that satisfy the following properties:

(F1)

, and ,

(F2)

are nondecreasing,

(F3)

the associated functions and defined by

are nonincreasing. Here, if .

Given and with the above properties the maxmin copula is then defined by (cf. [21])

where the latter equality holds if and .

In order to make the role of the generating functions and more symmetric we apply the following transformation to the class of maxmin copulas. If is a maxmin copula, then we introduce the copula

This is a copula of a random vector where is strictly increasing on the range of and is strictly decreasing on the range of (cf. [20, Theorem 2.4.4]). A general approach to symmetries of copulas is given in [9, Section 1.7.3]. A simple calculation then gives that

where . Here and in the sequel we are using the notation “” for the transformation only in the case when is a maxmin copula and the flip is performed on the second variable. Observe that notation is used in this place in [9] thus pointing out that this is a reflection in the second variable, while reflection in the first variable is denoted by . We will point out the fact that copula is obtained from the maxmin copula via the above reflection by terming it reflected maxmin copula, or RMM copula for short; we will also use abbreviation SRMM copulas for the symmetric reflected maxmin copulas. Note that the same reflection sends reflected maxmin copula back to the maxmin copula.

From Properties (F1)–(F3) of the generating functions and it follows that

Also if for some , then for all . Similarly, if

for some then for all . We write

and

for . In addition we define

(2)

and similarly for . Hence and .

1 Lemma.

Suppose , and correspond to maxmin copula as defined above. Then the following holds:

(G1)

, , ,

(G2)

the functions and are nondecreasing on .

(G3)

the functions and are nonincreasing on .

Proof: In this proof we use the properties of generators and of found in [21]. Recall that and to get property (G1) right away. Property (G2) follows by (Fc) and (Fd) of [21]. (G3): Recall that is nonincreasing, so that is also nonincreasing. Finally, the function

is nondecreasing on by [21, Lemma 3]. So, is nonincreasing on .

As noted in [21, p. 117] the functions and are continuous on , the function is not necessarily continuous at 0, and the function is not necessarily continuous at 1.

Comment. Observe that Condition (G3) allows for a very simple geometric interpretation: The angle between the vectors and is nonincreasing.

Definition. Given the functions which satisfy Properties (G1)–(G3) of Lemma 1, we define a reflected maxmin copula by the following rule

(3)

Note that we can rewrite as follows

(4)

It follows by Lemma 1 that we can associate to every maxmin copula a corresponding RMM copula. The next lemma shows the converse of this fact.

2 Lemma.

Suppose the functions , and satisfy properties (G1)–(G3) of Lemma 1. Then the functions

satisfy properties (F1)–(F3) and is a maxmin copula.

Proof.

Property (F1) is straightforward. Now, since for all , property (G2) implies that is nondecreasing. Similarly, is nondecreasing by (G2), so that

for any such that . So, . Hence, is nondecreasing and (F2) is proved as well.

To show (F3) recall first that for all so that function is nonincreasing since function is nonincreasing by (G3). Next, consider

and recall that the function is nonincreasing by property (G3) implying that is nondecreasing and therefore is nonincreasing. So, is nonincreasing on as desired and (F3) holds. (Observe that here, one may want to consider the possibility of existence of a such that as a special case.)

Using this fact we show in the next theorem immediately that defined by (3) or equivalently (4) is a copula. But, before we do that, let us pause for a few comments. First, the copulas defined by these two formulas remind us of a class of copulas introduced in [22]. Copulas of this type also appeared in [5, Proposition 3.2]. As a matter of fact the authors of [22] study there copulas of the form . Since we allow that for some , our copulas extend a subclass of those. Moreover, our copulas may be viewed as perturbations of the product copula . General perturbations of copulas were studied in [3] and [19], where a subclass of what we call reflected maxmin copulas were considered (cf. [19, §3]). Formula (3) can also be related to the formula in [7, Theorem 7.1] with maximum replaced by minimum; we believe that similarity is more than just coincidental. An extension of our copulas in aggregation context may bring us to more general generating functions on one hand and possibly to more general class of bivariate functions (that are currently copulas), i.e. to quasi-copulas.

3 Theorem.

Let and satisfy (G1)–(G3), then is a copula. For and we have

and

Proof.

By Lemma 2 the functions and satisfy conditions (F1)–(F3) so that is a maxmin copula by definition. So

Observe that the product copula is an RMM copula for . Also, the Fréchet-Hoeffding lower bound is an RMM copula if we take

Actually, these are the lower and upper bound for the whole class of RMM copulas.

4 Lemma.

If is an RMM copula then

Proof: This is a straightforward consequence of the definition since for some .

By the properties of generating functions of maxmin copulas it follows that and are continuous on , but they need not be continuous at .

If we take then the RMM copula is symmetric, so that it is an SRMM copula. We write

Note that by Lemma 4 every RMM copula is negatively quadrant dependent (cf. [20]). This fact might encourage us to call the kind of copulas equivalently to be quadrant subindependent.

The diagonal section of an RMM copula is of the form

Since , it follows that for all .

5 Proposition.

If a copula is simultaneously an RMM copula and a semilinear copula, then it is equal to the product copula.

Proof: This is immediate by the fact that a semilinear copula is PQD by [6, Corollary 5] and an RMM copula is NQD by Lemma 4.

So, RMM copulas seem to have a complementary position to the semilinear copulas. Note also that RMM copulas cannot be obtained from semilinear copulas via reflections (also called flipping transformations).

RMM copulas may have additional asymmetries. The symmetry (or exchangeability) property may be too restrictive, as discussed in [10]. Here we have pointed out some properties of the symmetric RMM copulas that are not shared by the whole class of RMM copulas. Some more will be given in Section 5.

3 Some specific properties of RMM copulas

In this section we will consider primarily the singularity and absolute continuity of RMM copulas. Here is some notation to start with. For an RMM copula we introduce the stand of (just for the sake of this paper). It is denoted by and defined as the closure of the set

It is also the closure of the set

The closure of the complement of will be called the zero set of and denoted by ; clearly

Here are some examples of RMM copulas with or without singular component in addition to for which we already know that it is fully singular RMM copula.

6 Example.

There are families of RMM copulas that are absolutely continuous.

Proof.

The functions

for satisfy conditions (G1)–(G3). The corresponding two-parameter family of RMM copulas has the densities

as a straightforward computation reveals. The desired conclusion then follows by [9, 20]. Note that is nonzero everywhere on . Observe also that if we replace by some such that , the copula remains unchanged. So, the generators of an RMM copula are not uniquely determined by it (cf. the remark at the end of this section).

7 Example.

There is a class of SRMM copulas that belongs to the class of EFGM (Eyraud-Farlie-Gumbel-Morgenstern222Here we are following the notiation of [9, Section 6.3]) copulas.

Proof.

Let be a class of SRMM copulas generated by for . Then

are EFGM copulas (see [9, p. 193]). They are absolutely continuous with density .

8 Example.

There are families of RMM copulas that have both a nontrivial absolutely continuous component and a singular component.

Proof.

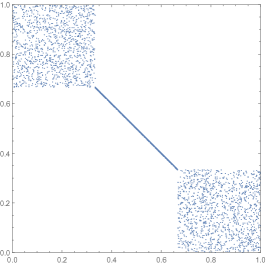

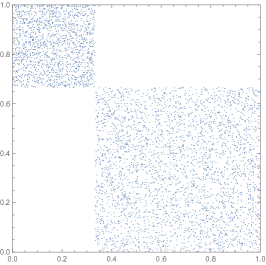

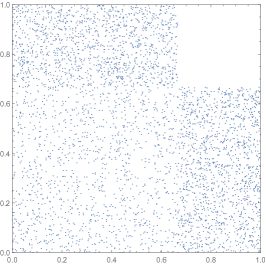

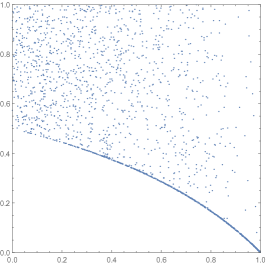

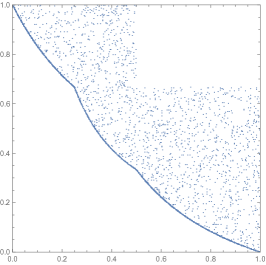

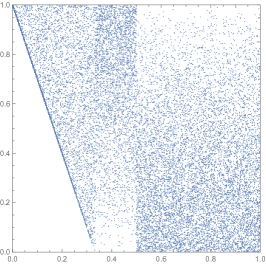

We give three examples of the kind with slightly different properties.

(a) Functions

for , satisfy conditions (G1)–(G3). Each copula of the corresponding two-parameter family of RMM copulas has the density

as seen via a straightforward computation. So, copula under consideration has both the continuous component and the singular component if . The latter is distributed uniformly along the segment

(5)

as it is immediately checked. In the limit we obtain copula .

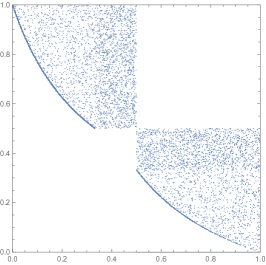

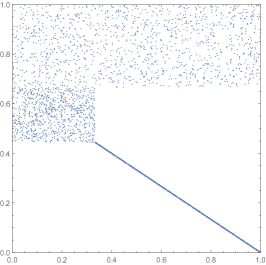

(b) A one-parameter family of SRMM copulas is given by the function

for , satisfying conditions (G1)–(G3). After performing a direct computation we obtain that the integral of the density function of these copulas over equals to . The singular component is distributed along the two arcs

(6)

and we can verify quickly that the mass of each arc equals .

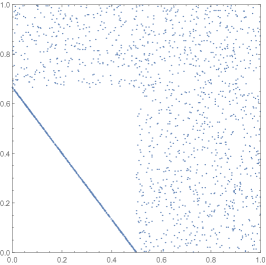

(c) The functions

for satisfy conditions (G1)–(G3). Each copula of the corresponding one-parameter family of RMM copulas has the density whose integral over the unit square is equal to . A painless computation shows that the singular mass is distributed along the arc

(7)

To be able to show the differences of Examples 8 let us first recall the notation for the level set of a copula

for any . For the level set is defined differently (see [20, 9]), i.e.

if this intersection is nonempty, or

if .

So, in the case of RMM copulas all of the level sets are curves given by equations

It is not always possible to give an explicit equation of either the form or for set as it is seen for of the family of copulas presented in Example 8(b). There is the union of arcs given by (6) and segments

Also, level curves for small of the same example are not convex functions.

Now, among copulas of Example 8 with nontrivial singular component there are those, whose singular component is only a part of the boundary of their stand. This happens, say, in Example 8(a) with , where the singular component is given by Formula (5); and also in Example 8(b). On the other hand, the copulas presented in Example 8(c) have their singular components distributed along the entire level set expressed by (7); and the same is true for copula . Among the absolutely continuous copulas there are those with density nonzero everywhere on the unit square as is the case for copulas of Example 6, and those whose density have parts where it is identically equal to zero as in Example 8(a) with .

Scatterplots of some of the copulas from Example 8 are presented in Figure 1. In the first row of the figure, there are three copulas from 8(a), i.e. those for , , , and , respectively. The first one has a nontrivial singular part, while the other two are absolutely continuous. In the second row, there are copulas from 8(b) for , and 8(c) for and , respectively.

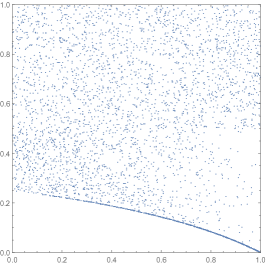

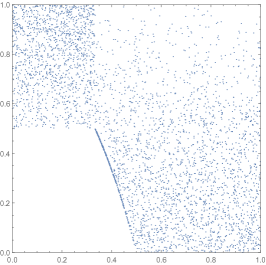

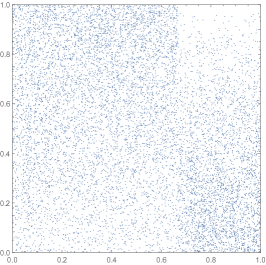

Figure 2: Some more reflected maxmin copulas

We include some more scatterplots of RMM copulas in Figure 2. The generators of the copulas in the first row are respectively equal to

and

The second generator of all copulas in the second row equals , while the first one equals respectively

and

Next, we give some regularity properties of the functions and consequently of the reflected maxmin copula.

9 Proposition.

For a given reflected maxmin copula we have:

(a)

and are differentiable a.e. (w.r. to Lebesgue measure) on , and and .

(b)

is partially differentiable a.e. (w.r. to Lebesgue measure) w.r. to and the partial derivative is no greater that .

(c)

is partially differentiable a.e. (w.r. to Lebesgue measure) w.r. to and the partial derivative is no greater that .

Proof.

(a) Since is a continuous and nondecreasing function it is firstly differentiable almost everywhere (w.r. to the Lebesgues measure) and secondly a.e. So, a.e. since a.e.

(b) By part (a) the function is differentiable a.e. so that the function is differentiable for every with respect to a.e. Consequently, the corresponding partial derivative exists a.e. with respect to the Lebesgue measure on . Clearly

for all and a.e. w.r. to . Now, using the fact that this expression is no greater than for all and a.e. w.r. to .

(c) The proof is obtained by exchanging the roles of and in the proof of part (b).

It is time to present the main results of the section. Some of these are adopted from those presented in [22] where copulas of the form

(8)

are considered. However, since we allow to be negative and use the truncation in this case, we need to reformulate their results. We include some of the proofs for the benefit of the reader. Let us point out that some extensions of the results of [22] on copulas of the form (8) are also given in [5] and in [9, Section 1.6]. Also, in the results on absolute continuity of the functions and , and consequently , the reader will be assumed familiar with definitions and properties of such functions as given in [16, Section 7.3].

10 Lemma.

Suppose that functions and satisfy conditions (G1)–(G3). Then:

(a)

For any both functions are absolutely continuous on the interval .

(b)

For every pair the product is absolutely continuous on .

(c)

For every pair the difference is absolutely continuous on .

Proof.

(a)

By Lemma 1 and the definition following it, is a copula and has the -increasing property. It follows easily for any points and with (implying that for all combinations of indices that

(9)

Here we may choose with no loss. As a matter of fact, we may then choose satisfying conditions (G1)–(G3) in relations (9) in an arbitrary manner. In particular, we may choose non-trivial, so that it contains a point at which its value is strictly positive, so that it is increasing at some points smaller than and decreasing at some points greater than by the fact that . So, we may find the points such that

(Observe that we may assume in the first case that by property (G2).) So, we are developing respectively relation (9) into the two relations given below:

and is absolutely continuous by [22, Lemma 2.1]. These arguments with the role of and reversed yield being absolutely continuous. (b) follows by (a) and (c) is an easy consequence of (b).

11 Corollary.

An RMM copula is absolutely continuous on all rectangles and for .

Proof.

This follows immediately by Lemma 10 and the fact that is identically on .

For a function defined on we introduce

12 Lemma.

Suppose that functions and satisfy conditions (G1)–(G3). Let be such that

(a)

, then , respectively

(b)

, and and are not both negative, then .

In particular, for all .

Proof.

(a) Condition (G2) clearly implies that , implying , and similarly for , so that

provided that the derivatives are not both negative. Otherwise the claim follows by Proposition 9(a). Case (b) goes similarly.

13 Theorem.

Suppose that is an RMM copula. Then it is absolutely continuous in the interior of the stand of and in the interior of the zero set . Therefore, it may be singular only along the boundary .

Proof.

By Lemma 10 and Corollary 11 the functions and are absolutely continuous on all the rectangles in the interior of the stand , and also on all the rectangles in the interior of the zero set . Therefore, the density function

for any rectangle in either the interior of or of . Consequently, the copula may be singular only on .

14 Proposition.

For an RMM copula the density of its absolutely continuous part is given by (10). The mass of its singular part is given by

Here we write shorter and . As before denotes the Lebesque measure.

15 Proposition.

The only fully singular RMM copula is the Fréchet-Hoeffding lower bound .

Proof.

Let be a fully singular RMM copula. So, the mass of its singular part is equal to 1 and by (10) we have

(11)

for almost all . (Here we have implicitly used the fact that by Lemma 10 functions are absolutely continuous on the interval and therefore their derivatives exist almost everywhere.)

Now, if or for almost all , then (since by (G1) ) contradicting (11). So, there exist such that and implying that the set

is nonempty. We want to show that contains almost all of . Towards a contradiction, assume this is not the case; then there is a subset of positive Lebesgue measure contained in . Using (11) as above we choose a point in this set such that and . In addition choose and observe that either or . Because of and this is contradicting (11).

Finally, Proposition 9 together with (9) tells us that and for almost all and consequently for almost all . So,

yielding the desired conclusion.

The above results on RMM copulas imply the following result for the maxmin copulas.

16 Corollary.

Let be a maxmin copula. Then the singular component of is included in the curve . The only fully singular maxmin copula is the Fréchet-Hoeffding upper bound .

Proof.

A short computation reveals that the curve defined by corresponds, when translated back to maxmin copulas, to the curve . Also, when we perform one flip on the Fréchet-Hoeffding lower bound , we get the Fréchet-Hoeffding upper bound and the corollary follows by Proposition 15.

Remark. It turns out that two pairs of generators and that generate the same RMM copula (distinct from the product copula) differ only by a multiplicative constant: and for some . In particular, the generator of an SRMM copula is uniquely determined by the copula.

We will omit the proof of these facts not to lengthen this paper too much.

4 Statistical aspects of RMM and SRMM copulas

In this section we need the difference

and the corresponding quotient of differences

for a given RMM copula . Note that difference is always nonnegative and measures the “dependent” part of . In particular, it is identically equal to zero if and only if and models an independence. Of course, the quotient is well-defined only if the denominator is non-zero.

Given an SRMM copula we want to find the generator or equivalently in closed form, at least for for which is nonzero, to be defined precisely in a moment. (The question of finding one of the two generators of an RMM copula is of the same complexity, as we believe.) Given a continuous nonnegative function on the interval such that (G1)–(G3) hold, the SRMM copula generated by is defined as

Note that this infimum is actually a minimum by continuity of and consequently of . Now, if are large enough we get by the fact that is nonincreasing and the diagonal of the copula defined by (12) is positive for large enough. Denote and observe that for all we have that is nonnegative (or equivalently ) since is nonincreasing. For the same reason it holds for every that even more . So, the value of the expression

exists as a quotient of two strictly positive numbers and is independent of . Replace in this equation first by to get

Then, replace by an arbitrary to get the formula (after recalling from the definition of that and consequently )

(13)

Here, is arbitrary but chosen so that both differences in the numerator and the denominator of this quotient are positive. Observe that the quotient is independent of .

17 Theorem.

An RMM copula , generated by generators of two SRMM copulas and , is given in closed form by

Proof: In order to get this formula we use formula (13) twice. In the first factor we replace by , while in the second one we replace by , by , and by .

Observe that this formula is independent of the choice of and provided that in both quotients the numerators and denominators are nonzero (and, of course we can always choose them so.)

18 Theorem.

Suppose that is an RMM copula, and and are univariate d.f.’s. Furthermore, let be a bivariate d.f. Then there exist three independent random variables , and such that is the joint distribution function of the random pair , where the d.f. of is the survival d.f. corresponding to , and

This follows directly from our definition and [21, Lemma 7]. We now want to combine all the results of this section together with Formula (13) for inverted marginal d.f. Observe in particular that when with the point translates into .

19 Theorem.

Suppose that is a maxmiin copula, and and are univariate d.f.’s. Furthermore, let be a bivariate d.f. Then there exist three independent random variables , and such that is the joint distribution function of random pair , where

Moreover, there exist two SRMM copulas and such that

5 Diagonals of symmetric reflected maxmin copulas

One wants to determine which diagonal functions that satisfy on are possible diagonal sections of RMM copulas. We say that a function is a diagonal function if it satisfies the following conditions:

(D1)

,

(D2)

for all ,

(D3)

is nondecreasing,

(D4)

is 2-Lipshitz: for all .

A function is a diagonal function if and only if it is the diagonal section of a copula [20, pp. 84-85]. We denote the set of all diagonal functions by .

20 Proposition.

Suppose is a diagonal section of an RMM copula . Then is nondecreasing.

Proof: We have that

By Lemma 1 (property (G3), and combined with (G1)) the functions and are nonincreasing and nonnegative, so that their product is also nonincreasing. Hence, the function is nondecreasing and proposition follows.

We can say somewhat more about the diagonal sections in case of the symmetric RMM’s.

21 Proposition.

Suppose is a diagonal section of an SRMM copula . Then is nondecreasing.

Proof: Since we have , i.e.

(14)

By Lemma 1 (property (G2)) it follows that the function is nondecreasing. Then, is nondecreasing by an easy observation based on Equation (14).

We denote by the set of all diagonal sections that satisfy conditions of Propositions 20 and 21, i.e.

Observe that the functions , and are related via Equations

(15)

and

(16)

where we used the standing assumption for all that holds for diagonal sections of reflected maxmin copulas. From relations (15) and (16) it follows directly that is nondecreasing if and only if is nonincreasing on . Using this fact we get an equivalent definition of

22 Theorem.

A function is a diagonal section of an SRMM copula if and only if . Moreover, if for , where , then is the diagonal section of the SRMM copula .

Proof: Suppose first that is the diagonal section of the SRMM copula . Then by Propositions 20 and 21.

Conversely, if then , and are nondecreasing. Define and observe first that it is well-defined. Indeed, , is nondecreasing on , and . Next observe that

and

Since and are nondecreasing it follows easily that is nondecreasing and is nonincreasing. Recall that to conclude that all the properties (G1)–(G3) hold and is a generator of an SRMM copula with the diagonal .

23 Example.

An SRMM copula is not uniquely determined by its diagonal section in general.

Proof: The diagonal of the Fréchet-Hoeffding lower bound equals

It belongs to . We already know that for

Observe also that is not equal to the function corresponding to by Theorem 22. This is equal to and the corresponding copula is equal to

Actually, for any function such that for all and such that and are nondecreasing and nonincreasing, respectively, we have that the diagonal of is equal to . Observe that the copula is equal to the reflected ordinal sum of two copies of with respect to the partition (see [9, Section 3.8]).

24 Corollary.

If is such that for all then for is the unique SRMM copula with the diagonal section equal to .

Proof: By Theorem 22 we know that is such that the diagonal section of is equal to . Suppose that is an SRMM copula such that its diagonal is equal to . Then and since , we have that for all . But then for all .

25 Example.

There exists a diagonal section of a copula satisfying for all such that is nondecreasing and is not.

Proof: Let be given by

It is easy to verify that is a continuous function that satisfies conditions (D1)–(D4) together with for all . Then

is nondecreasing while

is not.

For any diagonal section denote by the largest such that . This means that for and for . Since is the lower bound for all copulas it follows that . In the following theorem we give the lower and the upper bound for SRMM copulas with a given diagonal section .

26 Theorem.

Suppose that is such that and write

Then and are SRMM copulas with diagonal section , and if is any SRMM copula with diagonal section , then

Proof: The fact that is an SRMM copula follows by Theorem 22. To see that the same is true for we have to modify slightly the proof of that theorem. We first observe that and then introduce

As in the proof of Theorem 22 we see that the function is nondecreasing on and clearly it is also nondecreasing on . Since , and so , it is nondecreasing on .

Next, we consider the function

for . This function is clearly nonincreasing on and we can see, similarly to the proof of Theorem 22, that it is nonincreasing on . Since it is nonincreasing on . So, satisfies conditions (G1)–(G3) and it is a generator of an SRMM copula.

Now, suppose is an SRMM copula with diagonal section . So, . On we have so that

(17)

For we have . The fact that is nondecreasing on implies on so that

This theorem implies, in particular, that the SRMM copula is uniquely determined by the diagonal section for .

We will now show by a counterexample that the statement of Proposition 21 fails if SRMM coupula is replaced by a general RMM copula.

27 Example.

There exists an RMM copula such that for its diagonal function is not nondecreasing.

Proof: It is not hard to see that functions

satisfy conditions (G1)–(G3). Thus, they are generating functions of the RMM copula . The diagonal section of this copula equals

Then is equal to

Since

it follows that is not nondecreasing.

Acknowledgements.

The authors are thankful to Fabrizio Durante for some useful comments to a previous version of this paper. We are also grateful to an anonymous referee for helping us improve some parts of the paper especially in Section 3. We want to thank to our colleague Blaž Mojškerc who helped us with the figures.

References

[1] L. Běhounek, U. Bodenhofer, P. Cintula, S. Saminger-Platz, P. Sarkoci, Graded dominance and related graded properties of fuzzy connectives, Fuzzy Sets and Systems, 262 (2015), 78–101.

[2] U. Cherubini, F. Durante, S. Mulinacci, (eds.), Marshall–Olkin Distributions – Advances in Theory and Applications, Springer Proceedings in Mathematics & Statistics, Springer International Publishing, 2015.

[3] F. Durante, J. Fernández Sánchez, M. Úbeda Flores, Bivariate copulas generated by perturbarion, Fuzzy Sets and Systems, 228 (2013), 137–144.

[4] F. Durante, S. Girard, G. Mazo, Marshall–Olkin type copulas generated by a global shock, J. Comput. Appl. Math., 296 (2016), 638–648.

[5] F. Durante, P. Jaworski, A new characterization of bivariate copulas, Comm. in Stats. Theory and Methods, 39 (2010), 2901–2912.

[6] F. Durante, A. Kolesarová, R. Mesiar, C. Sempi, Semilinear copulas, Fuzzy Sets and Systems, 159 (2008), 63–76.

[7] F. Durante, R. Mesiar, P. L. Papini, C. Sempi, 2-Increasing binary aggregation operators, Information Sciences, 177 (2007), 111–129.

[8] F. Durante, M. Omladič, L. Oražem, N. Ružić, Shock models with dependence and asymmetric linkages, Fuzzy Sets and Systems, 323 (2017), 152–168.

[9] F. Durante, C. Sempi, Principles of Copula Theory, CRC/Chapman & Hall, Boca Raton (2015).

[10] C. Genest, J. Nešlehová, Assessing and Modeling Asymmetry in Bivariate Continuous Data, In: P. Jaworski, F. Durante, W.K. Härdle, (eds.), Copulae in Mathematical and Quantitative Finance, Lecture Notes in Statistics, Springer Berlin Heidelberg, (2013), 152–16891–114.

[11] H. Joe, Dependence Modeling with Copulas, Chapman & Hall/CRC, London (2014).

[12] T. Jwaid, B. De Baets, H. De Meyer, Ortholinear and paralinear semi-copulas, Fuzzy Sets and Systems, 252 (2014), 76–98.

[13] T. Jwaid, B. De Baets, H. De Meyer, Semiquadratic copulas based on horizontal and vertical interpolation, Fuzzy Sets and Systems, 264 (2015), 3–21.

[14] E. P. Klement, J. Li, R. Mesiar, E. Pap, Integrals based on monotone set functions, Fuzzy Sets and Systems, 281 (2015), 3–21.

[15] E. P. Klement, R. Mesiar, F. Spizzichino, A. Stupňanová, Universal integrals based on copulas, Fuzzy Optim. Decis. Mak., 13, No. 3, (2014), 273–286.

[16] S. Łojasiewicz, An introduction to the theory of real functions, John Wiley (1988).

[17] A. W. Marshall, Copulas, marginals, and joint distributions, in: L. Rüschendorf, B. Schweitzer, M. D. Taylor (eds.), Distributions with Fixed Marginals and Related Topics in LMS, Lecture Notes – Monograph Series, vol. 28, 1996, 213–222.

[18] A. W. Marshall, I. Olkin, A multivariate exzponential distributions, J. Amer. Stat. Assoc., 62, (1967), 30–44.

[19] R. Mesiar, M. Komorníková, J. Komorník, Perturbation of bivariate copulas, Fuzzy Sets and Systems, 268 (2015), 127–140.

[20] R. B. Nelsen, An introduction to copulas, 2nd edition, Springer-Verlag, New York (2006).

[21] M. Omladič, N. Ružić, Shock models with recovery option via the maxmin copulas, Fuzzy Sets and Systems, 284 (2016), 113–128.

[22] J. A. Rodríguez-Lallena, M. Úbeda-Flores, A new class of bivariate copulas, Stat. & Probab. Lett., 66 (2004), 315–325.