A Unified Framework for Robust Modelling of Financial Markets in discrete time

Abstract.

We unify and establish equivalence between the pathwise and the quasi-sure approaches to robust modelling of financial markets in discrete time. In particular, we prove a Fundamental Theorem of Asset Pricing and a Superhedging Theorem, which encompass the formulations of (Bouchard and Nutz,, 2015) and (Burzoni et al., 2019a, ). In bringing the two streams of literature together, we also examine and relate their many different notions of arbitrage. We also clarify the relation between robust and classical -specific results. Furthermore, we prove when a superhedging property w.r.t. the set of martingale measures supported on a set of paths may be extended to a pathwise superhedging on without changing the superhedging price.

1. Introduction

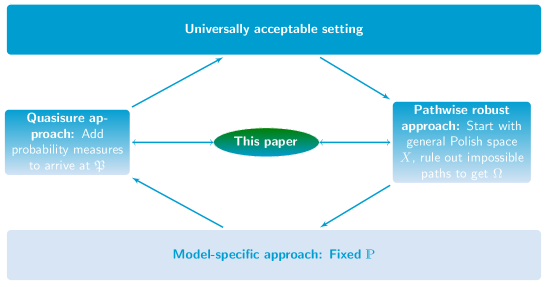

Mathematical models of financial markets are of great significance in economics and finance and have played a key role in the theory of pricing and hedging of derivatives and of risk management. Classical models, going back to (Samuelson,, 1965) and (Black and Scholes,, 1973) in continuous time, specify a fixed probability measure to describe the asset price dynamics. They led to a powerful theory of complete, and later incomplete, financial markets. The original models have undergone a myriad of variations including, amongst others, local and stochastic volatility models and have been widely applied. However, they also faced important criticism for ignoring the issue of model uncertainty, particularly so in the wake of the 2007/08 financial crisis. Consequently, inspired by the theoretical developments going back to (Knight,, 1921), new modelling approaches emerged which aim to address this fundamental issue. These can be broadly divided into two streams based on the so-called quasi-sure and pathwise approaches respectively.

The quasi-sure approach introduces a set of priors representing possible market scenarios. These priors can be very different and typically contains measures which are mutually singular. This presents significant mathematical challenges and led to the theory of quasi-sure stochastic analysis (see, e.g., (Peng,, 2004; Denis and Martini,, 2006)). In discrete time, this framework was abstracted in (Bouchard and Nutz,, 2015), which we call the quasi-sure formulation in the rest of this paper. By varying the set of probability measures between the “extreme” cases of one fixed probability measure, , and that of considering all probability measures, , this formulation allows for widely different specifications of market dynamics. The quasi-sure approach has been employed to consider model uncertainty along market frictions and other related problems, see e.g. (Bayraktar and Zhou,, 2017; Bayraktar and Zhang,, 2016). The pathwise approach addresses Knightian uncertainty in market modelling by describing the set of market scenarios in absence of a probability measure or any similar relative weighting of such scenarios. It is also referred to as the pointwise, or by , approach and it bears similarity to the way central banks carry out stress tests using scenario generators. In discrete time a suitable theory was obtained in (Burzoni et al., 2019a, ), based on earlier developments in (Burzoni et al.,, 2017, 2016). The methodology builds on the notion of prediction sets introduced in (Mykland et al.,, 2003) and used in continuous time in (Hou and Obłój,, 2018). The particular case of including all scenarios is often referred to as the model-independent framework and was pioneered in (Davis and Hobson,, 2007) and (Acciaio et al.,, 2016). From here, a further model specification is carried out by including additional assumptions, which represent the different agents’ beliefs. In this manner paths deemed impossible by all agents are eliminated. The remaining set of paths is then called the prediction set, or the model.

Both approaches, the quasi-sure and the pathwise, allow thus to interpolate between the two ends of the modelling spectrum, as identified by (Merton,, 1973): the model-independent and the model-specific settings (see Figure 1). In doing so, they allow to capture how their outputs change in function of adding or removing modelling assumptions, thus allowing to quantify the impact and risk that a given set of assumptions bear on the problem at hand, see (Cont,, 2006).

Both approaches were successful in developing suitable notions of arbitrage and extending the core results from the classical -a.s. setting to their more general context. In particular, in both approaches, it is possible to establish a Fundamental Theorem of Asset pricing of the form

and a Superhedging Theorem of the form

Our main contribution is to unify these two approaches to model uncertainty. We show that, under mild technical assumptions, the pathwise and quasi-sure Fundamental Theorems of Asset Pricing and Superhedging Dualities can be inferred from one another and are thus equivalent. Our statements follow a meta-structure outlined below:

Metatheorem.

Suppose we are in the quasi-sure setting with a given set of priors . Then, there exists a suitable selection of scenarios such that the pathwise result for implies the quasi-sure result for .

Conversely, suppose we are given a selection of scenarios . Then, there is a set of priors such that the quasi-sure result for implies the pathwise result for .

Establishing such equivalence allows us to gain significant additional insights into the core objects in both approaches, as well as clarify links to the classical model-specific setting. In particular, when transposing the results from the pointwise to the quasi-sure setup, the key technical analytic product structure assumption in Bouchard and Nutz, (2015), see Definition 2.1 below, is deduced naturally from the analyticity of the set of scenarios in (Burzoni et al., 2019a, ). When establishing the Superhedging Theorem, we not only show that the pathwise superhedging price of is equal to the quasi-sure one, but we also show that both are equal to the model-specific -superhedging price, where depends on the setting, i.e., on or equivalently on , but also on the payoff . Finally, the key implication in the proof of the robust Fundamental Theorem of Asset Pricing, i.e., (5) (1) in Theorem 2.7 below, is obtained by carefully constructing a suitable which does not admit an arbitrage in the classical sense and hence admits an equivalent martingale measure.

Furthermore, we survey and relate the concepts of arbitrage used in both approaches. We provide an extensive list of arbitrage notions introduced and used across the literature on robust finance and establish clear relations between them. We also investigate in detail the notion of pathwise superhedging. As noted in (Burzoni et al.,, 2017), the pathwise superhedging duality does not hold for general claims when superhedging on a general set is required. Instead, one has to consider hedging on a smaller “efficient” set (defined as the largest set supported by martingale measures and contained in ) to retain the pricing-hedging duality. We clarify when this is necessary and when one can extend the superhedging duality from to . Intuitively, since there are arbitrage opportunities on , one could try to superhedge the claim on without any additional cost by implementing an arbitrage strategy. We provide a number of counterexamples to show this idea is not feasible in general and link this to measurability constraints on arbitrage strategies, which were also encountered in (Burzoni et al.,, 2016). We then show that the above-mentioned intuition is only true for essentially uniformly continuous under certain regularity conditions on .

The rest of the paper is organised as follows. Section 2 contains the main results. First, in Section 2.1, we introduce the general setup in which we work. We discuss different notions of (robust) arbitrage in Section 2.2. Then, in Section 2.3, we establish our version of the robust Fundamental Theorem of Asset Pricing which unifies the quasi-sure and pathwise perspectives. And in Section 2.4, we state a robust Superhedging Theorem. Section 3 presents complementary results on extending the superhedging duality from to without additional cost and on relations between two strong notions of pathwise arbitrage. Finally, Section 4 contains technical results and most of the proofs. In particular, we give the proofs of Theorems 2.6 and 2.7 in Section 4.1 and of Theorem 2.9 in Section 4.2.

2. Unified Framework for Robust Modelling of Financial Markets

2.1. Trading strategies and pricing measures

We use notation similar to (Bouchard and Nutz,, 2015) and work in their setting, so we only recall the main objects of interest here and refer to (Bouchard and Nutz,, 2015) and (Bertsekas and Shreve,, 1978, Chapter 7) for technical details. Let and be a Polish space. We define for the Cartesian product and define , with the convention that is a singleton. We denote by the Borel sets on , by the set of probability measures on and define the function which projects to the -th coordinate, i.e., .

Next we specify the financial market. Let , an arbitrary filtration and let be Borel-measurable, , and adapted.

All prices are given in units of a numeraire, , which itself is thus normalised, , .

Trading strategies are defined as the set of -predictable -valued processes. All trading is frictionless and self-financing. Given , we denote

with representing the cashflow at time from trading using . Above, and throughout, is a row vector, is a column vector and denotes either a scalar or a column vector . We let denote the vector of payoffs of the statically traded assets , where is some index set. For notational convenience, we often identify with the set of its elements. We assume that each is Borel-measurable. When there are no statically traded assets we write . These assets, which we think of as options, can only be bought or sold at time zero (without loss of generality at zero cost) and are held until maturity . A trading position can only hold finitely many of these assets, the space of sequences of reals indexed by with only finitely many non-zero elements, and generates the payoff at time T. We call a pair a semistatic trading strategy. The class of such strategies is denoted . For technical reasons we also introduce the level sets of , which are denoted by

for and , where .

Finally, we denote by the natural filtration generated by and let be the universal completion of , . Furthermore we write for and often consider as a subspace of .

Within this setup, the literature on robust pricing and hedging adopts two approaches to model an agent’s beliefs. One stream is scenario-based and proceeds by specifying a prediction set , which describes the possible price trajectories. The other stream proceeds by specifying a set of probability measures , which determines the set of negligible outcomes.

We refer to the latter as the quasi-sure approach, while the former is usually called the pathwise, or pointwise, approach. In both cases, the model specification may depend on the agent’s market information as well as on her specific modelling assumptions. Changing the sets or can be seen as a natural way to interpolate between different beliefs. One of the principal aims of this paper is to show that both model approaches are equivalent in terms of corresponding FTAPs and Superhedging prices.

In order to aggregate trading strategies on different level sets in a measurable way, we always assume in this paper that is analytic and has the following structure:

Definition 2.1.

A set is said to satisfy the Analytic Product Structure condition (APS), if

where the sets are nonempty, convex and

is analytic.

This structure facilitates a dynamic programming principle and allows to essentially paste together one-step results in order to establish their multistep counterparts.

In order to formulate a Fundamental Theorem of Asset pricing we need to define the dual objects to trading strategies: the pricing (martingale) measures. Given a set of measures , following (Bouchard and Nutz,, 2015), we define

which, in the model-specific case , is simply the familiar set of all martingale measures equivalent to . Within the pathwise approach, for a set and a filtration , we define

where denotes the finitely supported Borel probability measures on . As a general convention, in this paper we interpret the above sub- and super-scripts as restrictions on the sets of measures. When we drop some of them it is to indicate that these conditions are not imposed, e.g., denotes all -martingale measures supported on . Next let

with the same convention regarding sub- and super-scripts as above. We also define

and is the power set of if .

Remark 2.2.

Note that holds. All these filtrations generate the same martingale measures on calibrated to , which we denote by .

For , thus denotes the collection of its null sets. Likewise, given a family , the collection of its polar sets if given by . We say that a property holds -q.s. if it holds outside a -polar set.

2.2. Notions of Arbitrage

One of the most important underlying concepts in financial mathematics is the absence of arbitrage. In the literature on robust pricing and hedging many notions of arbitrage have been proposed to date. We present these here together in a unified manned and discuss their relative dependencies. To complement the picture, we establish some novel technical results. These are postponed to Section 3.2.

Definition 2.3.

Fix a filtration , a set , a set of subsets of and a set . Recall that semistatic admissible trading strategies are given by .

-

1pA()

A One-Point Arbitrage (see (Riedel,, 2015)) is a strategy such that on with strict inequality for some .

-

OA()

An Open Arbitrage (see (Riedel,, 2015)) is a strategy such that on with strict inequality for some open subset of .

-

SA()

A Strong Arbitrage (see (Acciaio et al.,, 2016)) is a strategy such that on .

-

USA()

A Uniformly Strong Arbitrage (see (Davis and Hobson,, 2007)) is a strategy such that on for some .

-

A()

A -quasi-sure Arbitrage (see (Bouchard and Nutz,, 2015)) is a strategy such that holds and for some . If a -quasi-sure Arbitrage is called a -arbitrage and is denoted A().

-

CA()

A Classical Arbitrage in (see (Davis and Hobson,, 2007)) is a family of strategies such that, for all , is a -arbitrage.

-

WA()

A Weak Arbitrage (see (Blanchard and Carassus,, 2019)) is a strategy which is a -arbitrage for some .

-

IntA()

An Interior Arbitrage (see (Bayraktar et al.,, 2014)) is a sequence of strategies such that is a -quasi-sure Arbitrage relative to option payoffs given by for all large enough.

- WFLVR()

-

locA()

A -local -quasi-sure Arbitrage (see (Bartl,, 2019)) is a strategy such that -q.s. (where and ) and there exists such that .

-

A()

An Arbitrage de la Classe (see (Burzoni et al.,, 2016)) is a strategy such that on and for some .

When we want to stress the role of the filtration we include it as an argument, e.g., we write, e.g., SA(). When the filtration is not specified it is implicitly taken to be . We use a prefix N to indicate a negation of any of the above notions, e.g., we say that “NA() holds” when there does not exist a -quasi-sure arbitrage strategy, likewise NUSA() denotes the absence of a uniformly strong arbitrage on , etc.

Lemma 2.4.

The following relations hold:

-

(1)

-

(2)

-

(3)

-

(4)

-

(5)

.

-

(6)

when then

for some .

Proof.

Items (1)-(4) are immediate. Assertion (6) follows from (Bouchard and Nutz,, 2015, Lemma 4.6, p.842). For a strategy satisfying

we have, for any ,

where . Absence of IntA implies that there exists such that for any strategy as above we have

so that and absence of A follows so (5) holds. ∎

USA() was first discussed in (Davis and Hobson,, 2007), see also (Cox and Obłój,, 2011) and (Cox et al.,, 2016) for a definition of USA() and WFLVR(), where . Note that if we take in the definition of and replace the pathwise inequalities by their -a.s. counterparts for some fixed , we recover a discrete version of the condition of (Delbaen and Schachermayer,, 1994).

SA(() was used in (Acciaio et al.,, 2016) in the canonical setup. We refer to (Burzoni et al., 2019a, , Theorem 3) for a general FTAP connecting the notion of Strong and Uniformly Strong Arbitrage under the condition that there exists an option with a strictly convex super-linear payoff in the market. See also (Bartl et al.,, 2017) for an equivalence result under marginal constraints. In Section 3.2 we discuss the connection between SA() and USA() without the above assumptions.

A() is a unifying concept since

1pA(), OA(), SA(), USA() and A() can all be seen as special cases of A, see (Burzoni et al.,, 2016, Section 4.6) for a detailed discussion. It was first defined in (Burzoni et al.,, 2016) in a pathwise setting, see in particular the pathwise Fundamental Theorem of Asset pricing in (Burzoni et al.,, 2016, Theorem 2 & Section 4). This extends the results obtained in (Riedel,, 2015) who introduced 1pA() and OA(). OA() is furthermore defined in the setup of (Dolinsky and Soner,, 2014).

A was introduced in the quasi-sure setting of (Bouchard and Nutz,, 2015), where they prove a quasi-sure Fundamental Theorem of Asset pricing and Superhedging Theorem. From Lemma 2.4 above we see that the crucial distinction between and is the aggregation of arbitrage strategies, which poses a fundamental technical difficulty overcome in Bouchard and Nutz, (2015) by the specific (APS) structure of . We also note that was actually referred to as weak arbitrage in (Davis and Hobson,, 2007).

The notion of interior arbitrage was introduced, and called a robust arbitrage, by Bayraktar et al., (2014) in the context of transaction costs. Absence of is equivalent to absence of A() not only at the current prices of statically traded options but also under all, sufficiently small, perturbations of their prices. This notion was also used in (Hou and Obłój,, 2018, Assumption 3.1). It is equivalent to saying that the prices of the options are strictly inside the region of their -q.s. no-arbitrage prices, thus avoiding the delicate issue of boundary classification. In general, does not imply . To see this, take for some and . Then there is no -q.s. arbitrage, while for every we have and thus holds.

Throughout the remainder of this paper, unless otherwise stated, we take , i.e., we have a finite with statically traded options.

2.3. Robust Fundamental Theorem of Asset Pricing

The first Fundamental Theorem of Asset Pricing characterises absence of arbitrage in terms of existence of martingale (pricing) measures. In the classical discrete-time setting, this refers to the notion of -arbitrage. However, in a robust setting, there are many possible notions of arbitrage one can consider. If we adopt a strong notion of arbitrage, its absence should be equivalent to a weak statement, e.g., . This is often done in the pathwise literature, see (Burzoni et al., 2019a, ), and leads to a robust (multi-prior) version of the familiar Dalang-Morton-Willinger theorem.

Theorem 2.5 (Robust DMW Theorem).

Let be a set of probability measures satisfying (APS). Then there exists a universally measurable set of scenarios with for all and a filtration with , such that the following are equivalent:

-

(1)

.

-

(2)

for some .

-

(3)

.

-

(4)

.

-

(5)

NSA() holds.

Conversely, for an analytic set there exists a set satisfying (APS) such that for all there exists with and such that (1)-(5) are equivalent.

The above result follows from Theorem 2.7 below by setting . To see its opposite twin we should adopt a weak notion of arbitrage, its absence thus being equivalent to a strong statement, e.g., for all there exists such that . This route is most often taken in the quasi-sure literature, see (Bouchard and Nutz,, 2015), and leads to the following version of the robust FTAP.

Theorem 2.6.

Let be a set of probability measures satisfying (APS). Then there exists an analytic set of scenarios with for all , such that the following are equivalent:

-

(1)

holds and -q.s.

-

(2)

For all there exists such that .

-

(3)

NA( holds.

Conversely, if is an analytic set, then there exists a set of probability measures satisfying (APS) such that for all there exists with and such that the following are equivalent:

-

(1)

holds and .

-

(2)

For all there exists such that .

-

(3)

NA holds.

Our proof of this theorem, given in Section 4.1, does not rely on the proof of (3) (2) given in (Bouchard and Nutz,, 2015). Instead we give pathwise arguments. In particular, given such that we explicitly construct a quasi-sure Arbitrage strategy using the Universal Arbitrage Aggregator of (Burzoni et al., 2019a, ). This strengthens the results of Theorem 2.7 below. Indeed, using the fact that satisfies (APS), it is possible to select for each such that . Necessarily the support of each is then concentrated on .

Finally, we give our main abstract result, which establishes a pathwise and probabilistic characterisation of the absence of Arbitrage de la Classe . Its proof is presented in Section 4.1. As noted above, Arbitrage de la Classe allows to consider many notions of arbitrage at once. Accordingly, the main result below implies Theorem 2.5 and can be strengthened to imply Theorem 2.6 as will be seen in Section 4.

Theorem 2.7.

Assume that satisfies (APS) and is such that

| (2.1) |

Then there exists a co-analytic set of scenarios such that for all and a filtration with , such that the following are equivalent:

-

(1)

For all with there exists such that .

-

(2)

For all with there exists with .

-

(3)

For all with there exists such that .

-

(4)

.

-

(5)

There is no Arbitrage de la Classe in on .

Conversely, for an analytic set there exists a set satisfying (APS), such that for all there exists with and such that (1)-(5) are equivalent.

Remark 2.8.

Condition (2.1) was first stated in (Burzoni et al.,, 2016, Cor. 4.30 and the discussion thereafter). It turns out that for the proof of Theorem 2.7 a weaker condition is sufficient: we only need the properties

| (2.2) |

and

| (2.3) |

to hold, where we refer to Section 4.1 for a formal definition of . Conditions (2.2) and (2.3) are compatibility conditions on , and . Indeed, they assert that the (likely uncountable) union of “inefficient” subsets of (modulo -polar sets), stays an “inefficient” subset (modulo -polar sets). If this condition is not satisfied for some arbitrary and , then there is no reason why a set for which (2) holds should exist. Take for example a collection having densities and a set of singletons in . Then for any and any so the only which could satisfy (2) is the empty set. We note that when then (2.2) is always satisfied and (2.3) is satisfied as soon as is separable. However, in general, conditions (2.2) and (2.3) may be hard to verify, which is why we provide (2.1) as an easier sufficient condition. Lastly, we remark that it is not straightforward to show that corresponding to satisfies (2.3), which is why we give a direct proof of Theorem 2.6 in Section 4.

We note that the set can in general not be assumed to be analytic. The implications follow directly from the definitions. Apart from measurability considerations regarding , the equivalence of (3), (4) and (5) essentially follows from (Burzoni et al.,, 2016). Furthermore, given an analytic set , we will simply define as all the finitely supported probability measures on . The analyticity of then implies (APS) of . We then also have and equivalence of (1) and (3)-(5) follows from (Burzoni et al., 2019a, ). In this context, the essential connection we make is the combination of pathwise and quasi-sure criteria as stated in (2): for every , the pathwise efficient subset is required to be “seen” by at least one measure in the set .

For a given , the set in Theorem 2.7 can be explicitly constructed as the concatenation of the quasi-sure supports of . The main difficulty of the proof is then to show the implication , where one needs to establish existence of martingale measures , which are compatible with and in the sense of (1). This, modulo measurable selection arguments, is achieved by finding an element such that zero is in the relative interior of the support of . Indeed, let us explain the main idea of the proof of based on the following example: assume , , and the set is given by the grey polyhydron in Figure 2. Assume that the support of for a given measure is given by the blue dot (see Figure 2). Then as , we can find three additional points in , such that zero is in the relative interior of the convex hull of the four points. By definition of , the three additional points are in the support of some measures in , which we call in . As is convex, it follows that

is an element of as well, as visualised in Figure 3. Since zero is in the relative interior of the support of , one can now use results from (Rokhlin,, 2008) to find a martingale measure , in particular .

Note that this argument fundamentally relies on the convexity of . The analytic product structure assumption then grants suitable measurability for the concatenation procedure in the multiperiod case.

2.4. Robust Superhedging Theorem

In this section we focus on the key result which characterises superhedging prices: the pricing-hedging duality, or the Superhedging Theorem. As before, we compare pathwise and quasi-sure superhedging approaches as extensions of the classical model-specific result, see (Föllmer and Schied,, 2011, Chapter 5, Theorem 5.30).

For a set we denote the pathwise superhedging price on by

and denote the -q.s. superhedging price by

Take an analytic set such that for all we have . Using the Superhedging Theorems of (Bouchard and Nutz,, 2015) and (Burzoni et al., 2019a, ) it is immediate that the following relationships hold for all upper semianalytic :

The above inequality is strict in general. An easy way to see this is to take , , and , where denotes the Lebesgue measure on . Then and the pathwise superhedging price is equal to , while the quasi-sure superhedging price is equal to zero. In fact, to link the super-hedging and pathwise formulations, we have to choose a specific set which depends not only on but also on . We determine this set by reducing to superhedging under a fixed measure as stated in the following theorem:

Theorem 2.9.

Let be a set of probability measures satisfying (APS). Assume NA holds and let be upper semianalytic. Then there exists a measure and an -measurable set with for all , such that

Conversely, let be an analytic subset of with and let be upper semianalytic. For any set , which satisfies (APS) and , we have

In both cases, the value, if finite, is attained by a superhedging strategy .

The proof of this result is postponed to Section 4.2. In particular, Theorem 2.9 lets us interpret robust superhedging prices as classical superreplication prices under an “extremal” measure . Determining such measures is not straightforward in general. In a one-period case and for a continuous , we can use the arguments in the proof of Lemma 4.10 to see that any measure which attains the one-step quasisure support can be chosen. To extend this result to the multiperiod-case, certain continuity properties of the maps have to be guaranteed: we refer to (Carassus et al.,, 2019, Prop. 3.7) for a sufficient condition.

3. Complementary results on superhedging and arbitrage

3.1. Extension of Pathwise Superhedging from to

The preceding results show that quasi-sure and pathwise superhedging are essentially equivalent. As -q.s. superhedging strategies might be difficult to compute and implement in practice, it might be preferable to work on a prediction set using pathwise arguments. Given that determining is computationally expensive as well, the quantity of interest is then the superhedging price on and not on seen in the duality results in Section 2.4. Thus, we would like to find sufficient conditions under which the superhedging strategy associated with can be extended to without any additional cost. The intuition is that as describes non-efficient beliefs, we should be able to superhedge on this set implementing an arbitrage strategy. It turns out that this intuition is not true in general. Indeed, we run into problems regarding measurability of these arbitrage strategies, which means that this procedure only works in special cases.

To simplify the analysis, throughout this section only, we assume that and is continuous. The latter is satisfied, e.g., when is the coordinate mapping, i.e., . In order to give some intuition and to identify necessary conditions for the sets , and the function we first give two counterexamples:

Example 3.1.

Let , and . We set and . Then and trivially

Thus we have to assume that in the remainder of this section. We also note that here SA() holds whilst USA() does not, see Section 3.2.

Example 3.2.

Let , and and . We set and . In particular, is not a closed set. Note that . Now, introduce the claim

It is easy to see that and any trading strategy with is a superhedging strategy. We now claim that we cannot extend superhedging to with initial capital zero. For this we show that even for initial capital one, there exist no superreplication strategies on . Indeed for this we would need

which is equivalent to

As , this means if is arbitrarily close to 0 and is sufficiently large. Even if we look at for some positive , then taking arbitrarily large still leads to non-existence of superhedging strategies. In conclusion we will only consider compact sets in the rest of this section, on which “arbitrage strategies are effective for superhedging” in a sense defined below. Furthermore, modifying the function on in the above example, we can easily construct situations, in which for discontinuous payoffs . In conclusion we will also assume that is continuous in this section.

We can also modify this example so that the is closed and there is no attainment of superreplication strategies for . We stress that this is a fundamental difference to the case , where attainment is always given (see Theorem 2.9). Namely, take with the other elements unchanged. Note that did not change. Repeating the arguments above and looking at and we find

for .

As we have seen in the examples above, in general it is necessary to assume that , is continuous and that is compact as well as “well suited for superhedging by arbitrage strategies”. We first address the second point and show continuity of the one-step superhedging prices , which are defined via a dynamic programming approach:

Definition 3.3.

For a Borel-measurable we define the one-step superhedging prices

where .

A sufficient condition for continuity of was identified in (Carassus et al.,, 2019) and relies on the following assumption:

Assumption 3.4.

The sets and the sets are compact for all and all . Furthermore, for all , the correspondence is uniformly continuous from to the subsets of endowed with the Hausdorff distance, and where .

We refer to (Carassus et al.,, 2019, Section 3) for a discussion and examples of sets satisfying Assumption 3.4. The following lemma now follows from a direct application of (Carassus et al.,, 2019, Proposition 3.5):

Lemma 3.5.

Let be continuous. Under Assumption 3.4 the one-step superhedging prices are continuous for all .

Secondly, Example 3.2 also shows, that it is important to identify the subset of , on which “arbitrage strategies are ineffective for superhedging” in the following sense:

Definition 3.6.

We denote by the orthogonal projection of onto the linear subspace spanned by and define the set as the collection of all , for which is not an element of .

For an illustration of the set see Figure 4. We now state an assumption ensuring compatibility of and :

Assumption 3.7.

For each level set the following is true: if a sequence of points converges to a point , then necessarily .

Alas, it turns out that while Assumptions 3.4 and 3.7 are sufficient to establish the equality for , it is not so for . It is linked with the notion of standard separators introduced in (Burzoni et al., 2019a, ), which are measurable selectors of pointwise arbitrage strategies. We refer the reader to (Burzoni et al., 2019a, , Proof of Lemma 1) and the discussion therein for a detailed definition. Here we formulate an example, in which the existence of two standard separators together with the measurability constraint on implies :

Example 3.8.

Let , and . We set and

Then and using the notation of (Burzoni et al., 2019a, , Proof of Lemma 1) the standard separators are given by and . Next we define

We note that for we have . So in particular to hedge on we need initial capital and any hedging strategy satisfies for . For any such strategy to also superhedge on with initial capital , has to satisfy in particular

so as . Lastly extending superhedging g on gives the constraint

Taking gives , a contradiction. Thus we will assume that all one-point arbitrages can be reduced to a single standard separator.

Note that Example 3.8 can be easily altered to make compact by adding additional points. For clarity of exposition we have refrained from doing this but we conclude that Assumptions 3.4 and 3.7 are not sufficient for . We have to add a last assumption, which guarantees measurability of the corresponding Universal Arbitrage Aggregator. Intuitively it states, that locally, i.e., for every and every , there exists at most one arbitragable direction of the evolution of assets , so that the first standard separator is already the Universal Arbitrage Aggregator:

Assumption 3.9.

For all and we have , where is the Universal Arbitrage Aggregator of (Burzoni et al., 2019a, ) for the set .

Theorem 3.10.

Suppose that and is continuous for all . For an analytic satisfying Assumptions 3.4, 3.7 and 3.9 the Superhedging Duality of (Burzoni et al., 2019a, ) extends from to for all continuous , i.e., we have

Proof.

As before, we prove the claim by backward induction over . Let us now fix . We assume and , otherwise the claim is trivial. We first look at the case, where is an element of , i.e., there exists such that . Note that by Assumption 3.9 the standard separator is orthogonal to . By definition of the superhedging price on there exists an -measurable strategy such that

where we can assume without loss of generality that . Now we fix and the corresponding orthogonal projection. Let . As is uniformly continuous on , we can use (Vanderbei,, 1997, Theorem 1) (in connection with Tietze’s extension theorem to extend the domain to a convex set) in order to find such that

where is chosen such that for all we have whenever . Note that is orthogonal to and

Next we use the assumption that is bounded and has no points of convergence in outside the set . In particular the continuous functions and are bounded on . There exists such that for all with we still have

By assumption there exists such that for all with . Define and . Now we note that

for all . This concludes the proof. ∎

3.2. Comparison of Strong and Uniformly Strong Arbitrage

We take now a closer look at the notions and and establish their equivalence in specific market setups. Clearly every Uniformly Strong Arbitrage is a Strong Arbitrage. In general the opposite assertion is not true: take for example , , , , then every is a Strong Arbitrage, but there do not exist any Uniformly Strong Arbitrages. This simple example can be generalised: a one-period market in the canonical setting with and an open convex set such that and admits a Strong Arbitrage but exhibits no Uniformly Strong Arbitrages. On the level of superhedging prices a Uniformly Strong Arbitrage on corresponds to . For a financial market which exhibits a Strong Arbitrage but no uniformly Strong Arbitrages, the Pricing-Hedging duality cannot hold (as there are no martingale measures supported on ) but . In conclusion, the difference between Uniformly Strong Arbitrage and Strong Arbitrage can be seen as a property describing the boundary of the prediction set and thus manifests itself in the boundary behaviour of the superhedging functional

As it is an upper semicontinuous function, it takes the value zero on the boundary of , while its lower semicontinuous version takes the value . Nevertheless the two notions agree in specific cases, which we now explore.

We assume the canonical setting , and set for all . In this section we allow for countably many statically traded options, , but only of European type, , with real-valued continuous payoffs and a common maturity . We write for simplicity.

We fix a closed subset and recall that martingale measures on calibrated to are denoted by . We define and

denote by the space of real-valued continuous functions such that

Finally, we define the calibrated supermartingale measures as

The following theorem can be seen as a unification of (Acciaio et al.,, 2016, Theorem 1.3), (Cox and Obłój,, 2011, Prop. 2.2, p.6) and (Bartl et al.,, 2017, Cor. 4.6). We also refer to (Burzoni et al., 2019a, , Thm. 3), who extend (Acciaio et al.,, 2016, Thm. 1.3) under the assumption and to (Burzoni et al., 2019b, , Thm. C.5) for a general discussion in the case . In contrast to the work of Acciaio et al., (2016), we do not need to assume the existence of a convex superlinear payoff , which might be artificial in some settings, but explicitly enforce tightness of martingale measures through the condition.

Theorem 3.11.

The following hold:

-

(1)

SA .

-

(2)

Assume , no short-selling in any of the assets and

for all . Then

-

(3)

As in (2) assume that . Furthermore assume that for every sequence with , there exists a sequence of trading strategies, a constant and a sequence such that

-

•

and

-

•

on for all ,

-

•

for all .

Then

but in general does not imply .

-

•

Remark 3.12.

-

(1)

The case is covered in (Bouchard and Nutz,, 2015; Burzoni et al., 2019a, )), while the case is not. The basic idea in both works is to inductively construct a martingale measure calibrated to a finite number of options.

-

(2)

Contrary to the case (see (Burzoni et al., 2019a, , proof of Theorem 1, p.1050)), the set might not necessarily contain any finitely supported martingale measures.

-

(3)

An example showing that does not imply is given in (Cox and Obłój,, 2011, Prop. 2.2).

-

(4)

A special but important case of (3) is and , where . In this case we can set , for all , where is the th unit vector and note that

and

in particular all three conditions in (3) are satisfied.

Proof.

For simplicity of exposition we only give the proof for . This conveys the important ideas, while the multiperiod case extends these via a dynamic programming approach and can found in (Wiesel,, 2020).

Regarding (1), clearly , so we show . Let be a Strong Arbitrage. We show that it is actually a Uniformly Strong Arbitrage. For we denote by the -norm of and define the compact set . Then, as is continuous and positive on a compact set , there exists such that

Scaling suitably we can without loss of generality assume take . Let be the row unit vector in . Then

| (3.1) |

Furthermore on we have

Now we show (2). Clearly the relation holds and by (1) also . Further, readily implies since otherwise if then, by Fatou’s lemma,

a contradiction. Next we show following closely the argument in (Acciaio et al.,, 2016, proof of Prop. 2.3 and Theorem 1.3, pp. 240-242). We denote by the subset of all non-negative sequences in . We define the set

Note that is convex and non-empty. Furthermore denote the positive cone of by

By we have . An application of Hahn-Banach theorem yields existence of a positive measure such that

We now aim to show that the normalised measure given by

is an element of . For this let us first assume that . Then

as is positive, which is a contradiction. As , we conclude

Furthermore

and thus follows.

Lastly we show (3). For this we follow the same construction as in (2). In particular redefining

we note that again by we have . Thus all that is left to show is . Let us assume towards a contradiction and take such that

| (3.2) |

Then by symmetry of and the same reasoning as in (2) we have

| (3.3) |

| (3.4) |

Note that for a sequence with

for all we need to have by no WFLVR() that , so the LHS of (3.4) is equal to zero, a contradiction. ∎

4. Technical results and proofs

4.1. Proof of Theorems 2.6 and 2.7

We start with the following technical observation:

Proposition 4.1.

Let be analytic. Then the FTAP of (Bouchard and Nutz,, 2015) implies:

Proof.

Set . To apply the FTAP of (Bouchard and Nutz,, 2015) we only need to show that has analytic graph: we therefore fix and consider the Borel measurable function

and note that the image is analytic, since is analytic and the image of an analytic set under a Borel measurable map as well as the Cartesian product of analytic sets is analytic (see (Bertsekas and Shreve,, 1978, Prop. 7.38 & 7.40, p. 165)). Next we consider the continuous function

Note that

is analytic and as projections of analytic sets are analytic

is analytic as well. Let denote the simplex. Since the functions

and

are continuous, it follows that graph is analytic.

Take now and such that . By the FTAP of (Bouchard and Nutz,, 2015) there exists such that for some , for all and . In particular and .

Lastly assume that and fix such that for some . We can find such that for . Then and for , i.e., .

∎

We now give a complete proof of the quasi-sure FTAP in (Bouchard and Nutz,, 2015) using results from (Burzoni et al., 2019a, ). We first look at the case and start with an auxiliary lemma:

Lemma 4.2.

Let and be analytic. Then the conditional standard separator of (Burzoni et al., 2019a, ) denoted by is -measurable.

Proof.

We shortly recall arguments from (Burzoni et al., 2019a, )[proof of Lemma 1]: let us define the multifunction

Then is an -measurable multifunction. Indeed, for open we have

As is Borel measurable . Also as intersections, projections and preimages of analytic sets are analytic (see (Bertsekas and Shreve,, 1978, Prop. 7.35 & Prop. 7.40)), we find that is analytic and in particular -measurable. Let be the unit sphere in , then by preservation of measurability also the multifunction

is -measurable and closed-valued. Let be its -measurable Castaing representation. The conditional standard separator is then defined as

∎

Remark 4.3.

We recall that this separator has the property that it aggregates all one-dimensional One-point Arbitrages on in the sense that

for every measurable selector of .

Proof of Theorem 2.6 for .

We start by proving the first part of Theorem 2.6, i.e., we are given a set of measures satisfying and we need to construct such that (1)-(3) are equivalent. We define for

Then is closed valued and for all and all . Evidently

Also it follows from (Bouchard and Nutz,, 2015, Lemma 4.3, page 840), that is analytically measurable. We quickly repeat their argument: let us define

Then is Borel measurable. Next we consider

Since its graph is analytic, it follows that for open

is analytic as is Borel.

We also note that for the function is continuous, so is Borel and

is analytic. Now we define

Then

is analytic and by Fubini’s theorem holds for all . We now set

which is again analytic and for all .

Having defined we can now begin to prove equivalence of (1)-(3). If (2) holds then (3) follows immediately by a contradiction argument,

so we now show the more involved implications and . Let us start with the proof of : we assume that there exists such that . We want to find and such that -q.s and . For this we take and assume that

Let us now fix . Denote by the -measurable standard separator of Lemma 4.2. Now we define for each the push-forward of as

where . We note that by definition

holds for all . With a slight abuse of notation we recall the set

from (Burzoni et al., 2019a, , proof of Lemma 1, Step 1) and note that for all

follows. Clearly the set is open in , thus by definition of there is a such that

or there are no One-point Arbitrages on . To finish the proof of we need to select in a measurable way and this follows by standard arguments: Define the correspondence by

This function has analytic graph by arguments in (Nutz,, 2016, proof of Lemma 3.4, p.11), so we can employ the Jankov-von-Neumann theorem (cf. (Bertsekas and Shreve,, 1978, Proposition 7.49, page 182)) to find a universally measurable kernel

such that for all and on . Then also the kernel

is universally measurable. Defining , which is the product measure formed from the restriction of to and gives . This proves by backward induction.

Lastly we show : let us assume for all . Note that by the arguments given in the proof of this means that

is a -polar set, so in particular for all and -q.e. . Here denotes the relative interior of the convex hull of . Let be fixed. We define for an arbitrary and the support of conditioned on as

Using selection arguments which are explained below, we can now find measurable selectors such that

and fulfil the following property: define

for and every . Then for we have

where denotes the relative interior of the convex hull of .

We note that since is convex, we have for and by definition holds. Now it follows from (Rokhlin,, 2008, Theorem 1, page 1), that there exists a martingale measure equivalent to . The fact that implies , which shows the claim.

We now present the measurable selection argument: we fix . Note that for all we conclude by definition of , which implies by (Bonnice and Reay,, 1969, Theorem D, p.1) that there exist , which might not be pairwise distinct, s.t.

Note that is universally measurable. We define the correspondence by

Note that for open we have

Since is Borel measurable, we conclude that is weakly measurable. Let us denote by the unit sphere in . By preservation of measurability (cf. (Rockafellar and Wets,, 2009, Exercise 14.12, page 653)) it follows that the correspondence

is weakly measurable. Then also the correspondence

is weakly measurable and closed-valued. Let be a countable base of . The set

is Borel measurable. Note that for an arbitrary convex set the relationship

holds. Let

Then from the above arguments it follows that is Borel and in particular the set-valued mapping

has analytic graph. We can now employ the Jankov-von-Neumann theorem (cf. (Bertsekas and Shreve,, 1978), Proposition 7.49, page 182) to find universally measurable kernels such that for every we have and

This concludes the proof of .

The second part of Theorem 2.6 follows immediately from Proposition 4.1.

∎

Before continuing the proof of Theorem 2.6 let us first give a short remark on the measurability of the arbitrage strategies involved in the proof of above:

Remark 4.4.

By the FTAP of (Burzoni et al., 2019a, ) there exists a filtration with such that there is no Strong Arbitrage in on . More concretely there exists an - and thus -measurable arbitrage aggregator . So in particular if for some , then is an -measurable -q.s arbitrage. In general the inclusion does not hold. This is why we need to construct a new -measurable arbitrage strategy, which captures the arbitrages essential for . More generally, in this paper we manage to avoid using projectively measurable sets, which were essential for the arguments in (Burzoni et al., 2019a, ). In fact, all our trading strategies are universally measurable without invoking the axiom of projective determinacy.

Furthermore, we hope that by constructing an explicit arbitrage strategy in the proof of we can clarify the proof of (Burzoni et al.,, 2016), Theorem 4.23, pp. 42-46 (in particular (Burzoni et al.,, 2016)[A.3]) by offering a similar to the above (but much simpler) reasoning for the case . Introducing a measurable separator it is apparent that in (Burzoni et al.,, 2016, p.44) can always be chosen equal to one in our setting. Also the resulting strategy therein can be chosen universally measurable.

To prove the first part of Theorem 2.6 for the case we recall the following notion from (Burzoni et al., 2019a, ):

Definition 4.5 ((Burzoni et al., 2019a, ), Def. 4).

A pathspace partition scheme of is a collection of trading strategies , and arbitrage aggregators for some such that

-

(1)

the vectors , are linearly independent,

-

(2)

for any

where , ,

-

(3)

for any , is an Arbitrage Aggregator for ,

-

(4)

if , then either or for any linearly independent from there does not exist such that

Definition 4.6 ((Burzoni et al., 2019a, ), Def. 5).

A pathspace partition scheme is successful if .

We quote the following results:

Lemma 4.7 ((Burzoni et al., 2019a, ), Lemma 5).

For any , . Moreover, if is successful, then .

Lemma 4.8 ((Burzoni et al., 2019a, ), Proof of Theorem 1 for ).

A pathspace partition scheme is successful if and only if .

We now complete the first part of the proof of Theorem 2.6 for the case :

Proof of Theorem 2.6 for .

The existence of and No Strong Arbitrage in on , follow exactly as before. We now argue that holds in the spirit of (Bouchard and Nutz,, 2015, Theorem 5.1, p. 850), by induction over the number of options available for static trading. In particular we can assume without loss of generality that there exists a random variable such that for all and consider the set in order to avoid integrability issues. So let us assume there are traded options , for which holds. We introduce an additional option and assume for all . Then clearly for all and by the induction hypothesis there is no arbitrage in the market with options available for static trading. Let . Then by exactly the same arguments as in (Bouchard and Nutz,, 2015, proof of Theorem 5.1(a)) we can use convexity of and Theorem 2.9 to find a measure , such that and , so (2) holds.

Lastly it remains to show . Let us thus assume there exists such that . We want to find and such that -q.s and .

We use the properties of a pathspace partition scheme recalled above. We define

where . If then we select the strategy which satisfies on . We note that for all by definition of and , so that for some . If , then for all , for some , so we can argue as in the proof of Proposition 2.6 for using a standard separator and measurable selection of a measure in .

As before, the second part of Theorem 2.6 follows immediately from Proposition 4.1. This concludes the proof.

∎

Proof of Theorem 2.7.

We recall the analytic set from the proof of Theorem 2.6 for and the sets from (2.1). Now we define

We claim that (2.1) implies that

Indeed, clearly . Now assume towards a contradiction that there exists

In particular for some such that . By By (2.1) there exists such that and . This implies and thus shows the claim.

Let us now first assume that and set

| (4.1) |

By assumption we have for all . By definition of the operation

follows. To see the above equality, take a martingale measure and assume that . As we conclude that . Since any calibrated martingale measure supported on a subset of is in this leads to a contradiction to the definition of . Also, is the intersection of two analytic sets, so we conclude that is analytic. Lastly, by definition of we conclude -q.s..

The implications (1) (2) (3) (4) (5) follow directly from the definition. Thus we only need to show (5) (1). Let us fix such that . No Arbitrage de la Classe on implies that . From (4.1) we thus conclude that for some . As -q.s. this implies . Using a construction similar to the proof of Proposition 2.6 for the case , we can find a measure such that and 0 is in the interior of the conditional support of . By (Rokhlin,, 2008, Theorem 1), we conclude that there exists a martingale measure equivalent to , in particular . The case can now be treated similarly: indeed, we define as in the proof of Theorem 2.6 for , but now including the statically traded options in the definition of the quasi-sure support and follow the same arguments as above. This concludes the proof. ∎

4.2. Proof of Theorem 2.9

We first show that the quasi-sure superhedging theorem of (Bouchard and Nutz,, 2015) implies the second part of Theorem 2.9.

Proposition 4.9.

Let be an analytic subset of and . Let the set satisfy (APS) and Then and for an upper semianalytic function

| (4.2) |

Proof.

That and have the same polar sets follows by the definition of and (Burzoni et al., 2019a, , Lemma 2). We now show (4.2): consider

Note that there is no -q.s. arbitrage iff there is no -q.s arbitrage.

We now show that is analytic if is analytic.

Recall the set from Lemma 5.4 of (Burzoni et al.,, 2017), page 13 defined by

where and . (Burzoni et al.,, 2017) show that the set

is analytic, where . Note that

is analytic and the projection of the above set to the first coordinate is exactly , which shows that is analytic. We note has analytic graph by exactly the same argument as in the proof of Proposition 4.1 replacing by . The result now follows from the Superhedging Theorem of (Bouchard and Nutz,, 2015) and the definition of . ∎

We now show that the classical -a.s. one-step superhedging duality can be deduced by means of pathwise reasoning:

Lemma 4.10.

Let and be -measurable. Let and fix such that NA holds for the one-period model . Then

Proof.

As is -measurable, by (Bertsekas and Shreve,, 1978, Lemma 7.27, p.173) there exists a Borel-measurable function such that for -a.e. . Assume first that is continuous. Define . Then as NA holds and thus by (Burzoni et al., 2019a, , Theorem 2) and continuity of as well as

If is Borel-measurable, then by Lusin’s theorem (see (Cohn,, 2013, Theorem 7.4.3, p.227)) there exists an increasing sequence of compact sets such that , and is continuous. In particular there exists such that for all we have . By the above argument

| (4.3) | ||||

holds for . The claim now follows by taking suprema in on both sides of (4.3):

∎

Using this one-step duality result under fixed and (APS) of we now prove the first part of Theorem 2.9, which is restated in the following proposition:

Proposition 4.11.

Let NA hold and let be upper semianalytic. Then there exists a measure and an -measurable set with for all , such that

Proof.

We note that by NA and Theorem 2.6 the difference is -polar. We first take . Recall the definition of the one-step functionals given in (Bouchard and Nutz,, 2015, Lemma 4.10, p. 846)

By (APS) and upper semianalyticity of g, every is upper semianalytic. We show recursively that for every and for -q.e. there exists a measure such that NA holds and

Note that by measurable selection arguments and construction of we conclude that for -q.e. the properties NA and hold for all . We now fix and such that NA and for all holds. Note that there exists a sequence such that for all and

We see from the proof of Theorem 2.6 for in Section 4.1 that under NA() and for a fixed , we can always find such that and NA() holds. Thus we can assume without loss of generality that NA holds for all . Define as well as and note that NA as well as NA hold for all . Furthermore

where the last equality follows from Lemma 4.10. Define

Clearly . Now assume towards a contradiction that the inequality is strict and set . Furthermore note that for a sequence of compact sets such that we have

where

Choose large enough, such that Denote by the closed set of such that

Then for every there exists such that

Note that there exists a countable sequence , which is dense in . In particular for every such that

there exists such that

Set now and note that for all large enough

Taking we have in particular

a contradiction. Thus

As a natural universally measurable candidate for a superhedging strategy is the right derivative where is the superhedging price for the Borel-measurable stock , instead of . This is a pointwise limit of differences of upper seminanalytic functions and thus universally measurable. For such that this quantity does not exist, we set . Furthermore in order to show that the map can be chosen to be universally measurable we first note that in (Bouchard and Nutz,, 2015, Lemma 4.8, p.843) the set

is analytic. Thus we can apply the Jankov-von-Neumann selection theorem (see (Bertsekas and Shreve,, 1978, Proposition 7.50, p.184)) to find -optimisers for and the claim follows. The case can be handled by induction as in the proof of Theorem 2.6 for .

In conclusion we have found a strategy such that

We now define

This concludes the proof. ∎

Remark 4.12.

By NA Proposition 4.11 implies for

where we define

In particular for every there exists such that . A similar result was obtained by (Burzoni et al., 2019b, ) in a more general setup. Aggregating the martingale measures corresponding to all (and thus to all -polar sets) to achieve a result comparable to (Bouchard and Nutz,, 2015) in a setup without using (APS) of remains an open problem.

Data Availability Statement: Data sharing is not applicable to this article as no new data were created or analyzed in this study.

References

- Acciaio et al., (2016) Acciaio, B., Beiglböck, M., Penkner, F., and Schachermayer, W. (2016). A model-free version of the Fundamental Theorem of Asset Pricing and the Super-replication Theorem. Math. Finance, 26(2):233–251.

- Bartl, (2019) Bartl, D. (2019). Exponential utility maximization under model uncertainty for unbounded endowments. Ann. Appl. Probab., 29(1):577–612.

- Bartl et al., (2017) Bartl, D., Cheridito, P., Kupper, M., Tangpi, L., et al. (2017). Duality for increasing convex functionals with countably many marginal constraints. Banach Journal of Mathematical Analysis, 11(1):72–89.

- Bayraktar and Zhang, (2016) Bayraktar, E. and Zhang, Y. (2016). Fundamental theorem of asset pricing under transaction costs and model uncertainty. Math. Oper. Res., 41(3):1039–1054.

- Bayraktar et al., (2014) Bayraktar, E., Zhang, Y., and Zhou, Z. (2014). A note on the fundamental theorem of asset pricing under model uncertainty. Risks, 2(4):425–433.

- Bayraktar and Zhou, (2017) Bayraktar, E. and Zhou, Z. (2017). On arbitrage and duality under model uncertainty and portfolio constraints. Math. Finance, 27(4):988–2012.

- Bertsekas and Shreve, (1978) Bertsekas, D. and Shreve, S. (1978). Stochastic optimal control: The discrete time case, volume 23. Academic Press New York.

- Black and Scholes, (1973) Black, F. and Scholes, M. (1973). The pricing of options and corporate liabilities. J. Political Econ., pages 637–654.

- Blanchard and Carassus, (2019) Blanchard, R. and Carassus, L. (2019). No-arbitrage with multiple-priors in discrete time. arXiv preprint arXiv:1904.08780.

- Bonnice and Reay, (1969) Bonnice, W. and Reay, J. (1969). Relative interiors of convex hulls. Proc. Am. Math. Soc., 20(1):246–250.

- Bouchard and Nutz, (2015) Bouchard, B. and Nutz, M. (2015). Arbitrage and duality in nondominated discrete-time models. Ann. Appl. Probab., 25:823–859.

- (12) Burzoni, M., Fritelli, M., Hou, Z., Maggis, M., and Obłój, J. (2019a). Pointwise arbitrage pricing theory in discrete time. Math. Oper. Res.

- Burzoni et al., (2016) Burzoni, M., Frittelli, M., and Maggis, M. (2016). Universal arbitrage aggregator in discrete-time markets under uncertainty. Finance Stoch., 20(1):1–50.

- Burzoni et al., (2017) Burzoni, M., Frittelli, M., and Maggis, M. (2017). Model-free superhedging duality. Ann. Appl. Probab., 27(3):1452–1477.

- (15) Burzoni, M., Riedel, F., and Soner, H. (2019b). Viability and arbitrage under Knightian uncertainty. arXiv preprint arXiv:1707.03335.

- Carassus et al., (2019) Carassus, L., Obłój, J., and Wiesel, J. (2019). The robust superreplication problem: A dynamic approach. SIAM J. Financial Math. to appear.

- Cohn, (2013) Cohn, D. (2013). Measure theory. Springer.

- Cont, (2006) Cont, R. (2006). Model uncertainty and its impact on pricing derivative instruments. Math. Finance, 16(3):519–547.

- Cox et al., (2016) Cox, A., Hou, Z., and Oblój, J. (2016). Robust pricing and hedging under trading restrictions and the emergence of local martingale models. Finance Stoch., 20(3):669–704.

- Cox and Obłój, (2011) Cox, A. and Obłój, J. (2011). Robust pricing and hedging of double no-touch options. Finance Stoch., 15(3):573–605.

- Davis and Hobson, (2007) Davis, M. and Hobson, D. (2007). The range of traded option prices. Math. Finance, 17(1):1–14.

- Delbaen and Schachermayer, (1994) Delbaen, F. and Schachermayer, W. (1994). A general version of the fundamental theorem of asset pricing. Mathematische Annalen, 300(1):463–520.

- Denis and Martini, (2006) Denis, L. and Martini, C. (2006). A theoretical framework for the pricing of contingent claims in the presence of model uncertainty. Ann. Appl. Probab., 16(2):827–852.

- Dolinsky and Soner, (2014) Dolinsky, Y. and Soner, H. (2014). Robust hedging with proportional transaction costs. Finance and Stochastics, 18(2):327–347.

- Föllmer and Schied, (2011) Föllmer, H. and Schied, A. (2011). Stochastic Finance: An Introduction in Discrete Time. Walter de Gruyter.

- Hou and Obłój, (2018) Hou, Z. and Obłój, J. (2018). On robust pricing–hedging duality in continuous time. Finance Stoch., 22(3):511–567.

- Knight, (1921) Knight, F. (1921). Risk, uncertainty and profit. Boston: Houghton Mifflin.

- Merton, (1973) Merton, R. C. (1973). Rational theory of option pricing. Bell J. Econ. Manage. Sci., 4(1):141–183.

- Mykland et al., (2003) Mykland, P. et al. (2003). Financial options and statistical prediction intervals. Ann. Statist., 31(5):1413–1438.

- Nutz, (2016) Nutz, M. (2016). Utility maximization under model uncertainty in discrete time. Math. Finance, 26(2):252–268.

- Peng, (2004) Peng, S. (2004). Nonlinear expectations, nonlinear evaluations and risk measures. In Stochastic methods in finance, pages 165–253. Springer.

- Riedel, (2015) Riedel, F. (2015). Financial economics without probabilistic prior assumptions. Decisions in Economics and Finance, 38(1):75–91.

- Rockafellar and Wets, (2009) Rockafellar, R. and Wets, R. (2009). Variational Analysis, volume 317. Springer Berlin.

- Rokhlin, (2008) Rokhlin, D. (2008). A proof of the Dalang-Morton-Willinger theorem. arXiv preprint arXiv:0804.3308.

- Samuelson, (1965) Samuelson, P. (1965). Rational theory of warrant pricing. Ind. Manag. Rev.(pre-1986), 6(2):13.

- Vanderbei, (1997) Vanderbei, R. (1997). Uniform continuity is almost Lipschitz continuity. Technical report, SOR-91-11, Statistics and Operations Research Series.

- Wiesel, (2020) Wiesel, J. (2020). Time-consistent data driven approach to robust pricing and hedging. DPhil thesis.