Estimation in a Generalization of Bivariate Probit Models with Dummy Endogenous Regressors††thanks: The authors thank Jason Abrevaya, Xiaohong Chen, Stephen Donald, Brendan Kline, Ed Vytlacil, and Haiqing Xu for valuable discussions. An earlier version of this paper has been circulated under the title “Sensitivity Analysis in Triangular Systems of Equations with Binary Endogenous Variables.”

This Draft: March 4, 2019)

Abstract

The purpose of this paper is to provide guidelines for empirical researchers

who use a class of bivariate threshold crossing models with dummy

endogenous variables. A common practice employed by the researchers

is the specification of the joint distribution of the unobservables

as a bivariate normal distribution, which results in a bivariate

probit model. To address the problem of misspecification in this

practice, we propose an easy-to-implement semiparametric estimation

framework with parametric copula and nonparametric marginal distributions.

We establish asymptotic theory, including root- normality, for

the sieve maximum likelihood estimators that can be used to conduct

inference on the individual structural parameters and the average

treatment effect (ATE). In order to show the practical relevance of

the proposed framework, we conduct a sensitivity analysis via extensive

Monte Carlo simulation exercises. The results suggest that the estimates

of the parameters, especially the ATE, are sensitive to parametric

specification, while semiparametric estimation exhibits robustness

to underlying data generating processes. We then provide an empirical

illustration where we estimate the effect of health insurance on doctor

visits. In this paper, we also show that the absence of excluded instruments

may result in identification failure, in contrast to what some practitioners

believe.

Keywords: Triangular threshold crossing model, bivariate probit model, dummy endogenous regressors, binary response, copula, exclusion restriction, sensitivity analysis.

JEL Classification Numbers: C14, C35, C36.

1 Introduction

The purpose of this paper is to provide guidelines for empirical researchers who use a class of bivariate threshold crossing models with dummy endogenous variables. This class of models is typically written as follows. With the binary outcome and the observed binary endogenous treatment , we consider

| (1.1) |

where denotes a vector of exogenous regressors that determine both and , and denotes a vector of exogenous regressors that directly affect , but not (i.e., instruments for ). Since does not appear in the equation for , this model forms a triangular model, as a special case of a simultaneous equations model, with the binary endogenous variables. In this paper, we investigate the consequences of the common practices employed by empirical researchers who use this class of models. As an important part of this investigation, we conduct a sensitivity analysis on the specification of the joint distribution of the unobservables . This is the component of the model that practitioners have the least knowledge about, and thus typically impose a parametric assumption. To address the problem of misspecification, we propose a semiparametric estimation framework with parametric copula and nonparametric marginal distributions. The semiparametric specification is an attempt to ensure robustness while achieving point identification and efficient estimation.

The parametric class of models (1.1) includes the bivariate probit model, in which the joint distribution of is assumed to be a bivariate normal distribution. This model has been widely used in empirical research, including the works of Evans and Schwab (1995), Neal (1997), Goldman et al. (2001), Altonji et al. (2005), Bhattacharya et al. (2006), Rhine et al. (2006) and Marra and Radice (2011) to name a just few. The distributional assumption in this model, however, is made out of convenience or convention, and is hardly justified by underlying economic theory and thus susceptible to misspecification. With binary endogenous regressors, the objects of interest in model (1.1) are the mean treatment parameters, in addition to the individual structural parameters. Because the outcome variable is also binary, the mean treatment parameters such as the average treatment effect (ATE) are expressed as the differential between the marginal distributions of . Therefore, the problem of misspecification when estimating these treatment parameters can be even more severe than that when estimating individual parameters.

To one extreme, a nonparametric joint distribution of can be used in a bivariate threshold crossing model, as in Shaikh and Vytlacil (2011). Their results, however, suggest that the ATE is only partially identified in this fully flexible setting. Instead of sacrificing point identification, we impose a parametric assumption on the dependence structure between the unobservables using copula functions that are known up to a scalar parameter. At the same time, in order to ensure robustness, we allow the marginal distribution of (and ), which is involved in the calculation of the ATE, to be unspecified. Our class of models encompasses both parametric and semiparametric models with parametric copula and either parametric or nonparametric marginal distributions. This broad range of models allows us to conduct a sensitivity analysis on the specification of the joint distribution of .

The identification of the individual parameters and the ATE in this class of models is established in Han and Vytlacil (2017, hereafter, HV17). They show that when the copula function for satisfies a certain stochastic ordering, identification is achieved in both parametric and semiparametric models under an exclusion restriction and mild support conditions. Building on these results, we consider estimation and inference in the same setting. For the semiparametric class of models (1.1) with parametric copula and nonparametric marginal distributions, the likelihood contains infinite-dimensional parameters (i.e., the unknown marginal distributions). To estimate this model, we consider the sieve maximum likelihood (ML) estimation method for the finite- and infinite-dimensional parameters of the model, as well as their functionals. The estimation of the parametric model, on the other hand, is within the standard ML framework.

The contributions of this paper can be summarized as follows. Through these contributions, this paper is intended to provide a guideline to empirical researchers. First, we establish the asymptotic theory for the sieve ML estimators in a class of semiparametric copula-based models. This result can be used to conduct inference on the functionals of the finite- and infinite-dimensional parameters, such as inference on the individual structural parameters and the ATE. We show that the sieve ML estimators are consistent and that their smooth functionals are root- asymptotically normal.

Second, in order to show the practical relevance of the theoretical results for empirical researchers, we conduct a sensitivity analysis via extensive Monte Carlo simulation exercises. We find that the parametric ML estimates, especially those for the ATE, can be highly sensitive to the misspecification of the marginal distributions of the unobservables. On the other hand, the sieve ML estimates perform well in terms of the mean squared error (MSE) as they are robust to the underlying data generating process. Moreover, their performance is comparable to that of the parametric estimates under a correct specification. We also show that copula misspecification does not have a substantial effect in estimation, as long as the true copula is within the stochastic ordering class of the identification. As copula misspecification is a problem common to both parametric and semiparametric models considered in this paper, our sensitivity analysis suggests that a semiparametric consideration may be more preferable in estimation and inference.

Third, we provide an empirical illustration of the sieve estimation and the sensitivity analysis of this paper. We estimate the effect of health insurance on decisions to visit doctors using the the Medical Expenditure Panel Survey data combined with the National Compensation Survey data by matching industry types. We compare the estimates of parametric and semiparametric bivariate threshold crossing models with the Gaussian copula. We show that the estimates differ, especially so for the estimated ATE’s, which suggest the misspecification of the marginal distribution of the unobservables, consistent with the simulation results. In other words, the estimates of the bivariate probit model can be misleading in this example.

Fourth, we formally show that identification may fail without the exclusion restriction, in contrast to the findings of Wilde (2000). The bivariate probit model is sometimes used in applied work without instruments (e.g., White and Wolaver (2003) and Rhine et al. (2006)). We show, however, that this restriction is not only sufficient but also necessary for identification in parametric and semiparametric models when there is a single binary exogenous variable common to both equations. We also show that under joint normality of the unobservables, the parameters are, at best, weakly identified when there are common (and possibly continuous) exogenous variables. 111HV17 only show the sufficiency of this restriction for identification. Mourifié and Méango (2014) show the necessity of the restriction, but their argument does not exploit all information available in the model; see Section 2.2 of the present paper for further details. We also note that another source of identification failure is the absence of restrictions on the dependence structure of the unobservables, as mentioned above.

The sieve estimation method is a useful nonparametric estimation framework that allows for a flexible specification, while guaranteeing the tractability of the estimation problem; see Chen (2007) for a survey of sieve estimation in semi-nonparametric models. The estimation method is also easy to implement in practice. The sieve ML estimation has been used in various contexts: Chen et al. (2006, hereafter, CFT06) consider the sieve estimation of semiparametric multivariate distributions that are modeled using parametric copulas; Bierens (2008) applies the estimation method to the mixed proportional hazard model; and Hu and Schennach (2008) and Chen et al. (2009) use the method to estimate nonparametric models with non-classical measurement errors. The asymptotic theory developed in this paper is based on the results established in the sieve extremum estimation literature (e.g., CFT06; Chen (2007); Bierens (2014)). A semiparametric version of bivariate threshold crossing models is also considered in Marra and Radice (2011) and Ieva et al. (2014). In contrast to our setting, however, they introduce flexibility for the index function of the threshold, and not for the distribution of the unobservables.

The remainder of this paper is organized as follows. The next section reviews the identification results of HV17, and then discusses the lack of identification in the absence of exclusion restrictions and in the absence of restrictions on the dependence structure of the unobservables. Section 3 introduces the sieve ML estimation framework for the semiparametric class of models defined in (1.1), and Section 4 establishes the large sample theory for the sieve ML estimators. The sensitivity analysis is conducted in Section 5 by investigating the finite sample performance of the parametric ML and sieve ML estimates under various specifications. Section 6 presents the empirical example, and Section 7 concludes.

2 Identification and Failure of Identification

2.1 Identification Results in Han and Vytlacil (2017)

We first summarize the identification results in HV17. In model (1.1), let and , and conformably, let , , and .

Assumption 1.

and satisfy that , where “” denotes statistical independence.

Assumption 2.

does not lie in a proper linear subspace of a.s.222A proper linear subspace of is a linear subspace with a dimension strictly less than . The assumption is that if is a proper linear subspace of , then .

Assumption 3.

There exists a copula function such that the joint distribution of satisfies , where and are the marginal distributions of and , respectively, that are strictly increasing and absolutely continuous with respect to Lebesgue measure.333 Sklar’s theorem (e.g., Nelsen (1999)) guarantees the existence of such a copula, which is, in fact, unique because and are continuous.

Assumption 4.

As scale and location normalizations, and .

A model with alternative scale and location normalizations, and , can be viewed as a reparametrized version of the model with the normalizations given in Assumption 4; see, for example, the reparametrization (2.1) below. For and , write a one-to-one map (by Assumption 3) as

| (2.1) |

Take and , for some , where is the conditional support of , given . Then, by Assumption 1, model (1.1) implies that the fitted probabilities are written as

| (2.2) |

where for . The equation (2.2) serves as the basis for the identification and estimation of the model. Depending upon whether one is willing to impose an additional assumption on the dependence structure of the unobservables via , the underlying parameters of the model are either point identified or partially identified.

We first consider point identification. The results for point identification can be found in HV17, which we adapt here given Assumption 4. The additional dependence structure can be characterized in terms of the stochastic ordering of the copula parametrized with a scalar parameter.

Definition 2.1 (Strictly More SI or Less SD).

Let and be conditional copulas, for which and are either increasing or decreasing in for all . Such copulas are referred to as stochastically increasing (SI) or stochastically decreasing (SD), respectively. Then, is strictly more SI (or less SD) than if is strictly increasing in ,444Note that is increasing in by definition. which is denoted as .

This ordering is equivalent to having a ranking in terms of the first order stochastic dominance. Let and . When is strictly more SI (less SD) than is, then increases even more than does as increases.555In the statistics literature, the SI dependence ordering is also referred to as the (strictly) “more regression dependent” or “more monotone regression dependent” ordering; see Joe (1997) for details.

Assumption 5.

The copula in Assumption 3 satisfies with a scalar dependence parameter , is twice differentiable in , and , and satisfies

| (2.3) |

The meaning of the last part of this assumption is that the copula is ordered in in the sense of the stochastic ordering defined above. This requirement defines the class of copulas that we allow for identification. Many well-known copulas satisfy (2.3): the normal copula, Plackett copula, Frank copula, Clayton copula, among many others; see HV17 for the full list of copulas and their expressions. Under these assumptions, we first discuss the identification in a fully parametric model.

Assumption 6.

and are known up to means and variances .

Given this assumption, and , where and are the distributions of and , respectively. Define

Theorem 2.2.

The proof of this theorem is a minor modification of the proof of Theorem 5.1 in HV17.

Although the parametric structure on the copula is necessary for the point identification of the parameters, HV17 show that the parametric assumption for and are not necessary. In addition, if we make a large support assumption, we can also identify the nonparametric marginal distributions and .

Assumption 7.

(i) The distributions of (for ) and (for ) are absolutely continuous with respect to Lebesgue measure; (ii) There exists at least one element in such that its support conditional on is and and , where, without loss of generality, we let .

Theorem 2.3.

An interesting function of the underlying parameters that are point identified under the parametric and semiparametric distributional assumptions is the conditional ATE:

| (2.4) |

2.2 Extension of Han and Vytlacil (2017): Identification under Conditional Independence

The identification analysis of Han and Vytlacil (2017) relies on the full independence assumption (Assumption 1) for . The analysis, however, can be easily extended to a case where conditional independence is alternatively assumed. Since this is a more empirically relevant situation, we explore this case in detail here. In the empirical section below, we impose the conditional independence. Let be a vector of (potentially endogenous) covariates in .

Assumption 1′.

and satisfy that .

Similarly, we modify Assumptions 2–3, 5–7 accordingly. Then the following theorems immediately hold by applying the same proof strategies as in Theorems 2.2 and 2.3. Let be the conditional copula, and , and be the conditional distributions.

Theorem 2.4.

In model (1.1), suppose Assumptions 1′ and 4 hold. Also, suppose Assumption 2 holds conditional on , and Assumptions 3, 5–6 hold with , , and instead, for all . Then, are point identified in an open and convex parameter space if (i) is a nonzero vector, and (ii) does not lie in a proper linear subspace of a.s. conditional on .

Theorem 2.5.

In model (1.1), suppose Assumptions 1′ and 4 hold. Also, suppose Assumptions 2 and 7(i) hold conditional on , and Assumptions 3 and 5 hold with , , and instead, for all . Then are point identified in an open and convex parameter space if (i) is a nonzero vector; and (ii) does not lie in a proper linear subspace of a.s. In addition, if Assumption 7(ii) holds conditional on , and are identified up to additive constants for all .

2.3 The Failures of Identification

In this section, we discuss two sources of identification failure in the class of models (1.1): the absence of exclusion restrictions and the absence of restrictions on the dependence structure of the unobservables .

2.3.1 No Exclusion Restrictions

There are empirical works where (1.1) is used without excluded instruments; see, e.g., White and Wolaver (2003) and Rhine et al. (2006). Identification in these papers relies on the results of Wilde (2000), who provides an identification argument by counting the number of equations and unknowns in the system. Here, we show that this argument is insufficient for identification. We show that without the excluded instruments (i.e., when ), the structural parameters are not identified, even with a full parametric specification of the joint distribution (Assumptions 5 and 6). The existence of common exogenous covariates in both equations is not very helpful for identification in a sense that becomes clear below.

Before considering the lack of identification in a general case with possibly continuous in , we start the analysis with binary . Mourifié and Méango (2014) show the lack of identification when there is no excluded instrument in a bivariate probit model with binary . They, however, only provide a numerical counter-example. Moreover, their analysis does not consider the full set of observed fitted probabilities, and hence possibly neglects information that could have contributed to the identification. Here, we provide an analytical counter-example in a more general parametric class of model (1.1) that nests the bivariate probit model. We show that are not identified, even if the full set of probabilities are used. Note that the reduced-form parameters are always identified from the equation for , and as a normalization using scalar .

Theorem 2.6.

In showing this lack-of-identification result, we find a counter-example where the copula density induced by is symmetric around and , and the density induced by is symmetric. Note that the bivariate normal distribution, namely, the normal copula with normal marginals, satisfies these symmetry properties. That is, in the bivariate probit model with a common binary exogenous covariate and no excluded instruments, the structural parameters are not identified.

The proof of Theorem 2.6 proceeds as follows. Under Assumption 4, let

Then, we have

where . We want to show that, given which are identified from the reduced-form equation, there are two distinct sets of parameter values and (with ) that generate the same observed fitted probabilities and for all under some choices of and . The detailed proof can be found in the online appendix.

One might argue that the lack of identification in Theorem 2.6 is due to the limited variation of . Although this is a plausible conjecture, this does not seem to be the case in the model considered here.666In fact, in Heckman (1979)’s sample selection model under normality, although identification fails with binary exogenous covariates in the absence of the exclusion restriction, it is well known that identification is achieved with continuous covariates by exploiting the nonlinearity of the model (Vella (1998)). We now consider a general case with possibly continuous , and discuss what can be said about the existence of two distinct sets of that generate the same observed data. To this end, define

Then,

Similar to the proof strategy for the binary case, we want to show that, given , there are two distinct sets of parameter values and that generate the same observed fitted probabilities for all and under some choices of and .

Let for all and for some . Also, choose and some . For , we want to show that there exists such that, for ,

| (2.5) | ||||

| (2.6) |

for all , where

| (2.7) |

The question is whether we find and such that (2.5)–(2.7) hold simultaneously. First, note that, since , we have and hence by the assumption that there is no linear subspace in the space of . Now, choose to be a normal copula and choose and . Then, using arguments similar to those of the binary case (found in the online appendix), we obtain

| (2.8) |

and . Then, (2.7) can be rewritten as

| (2.9) |

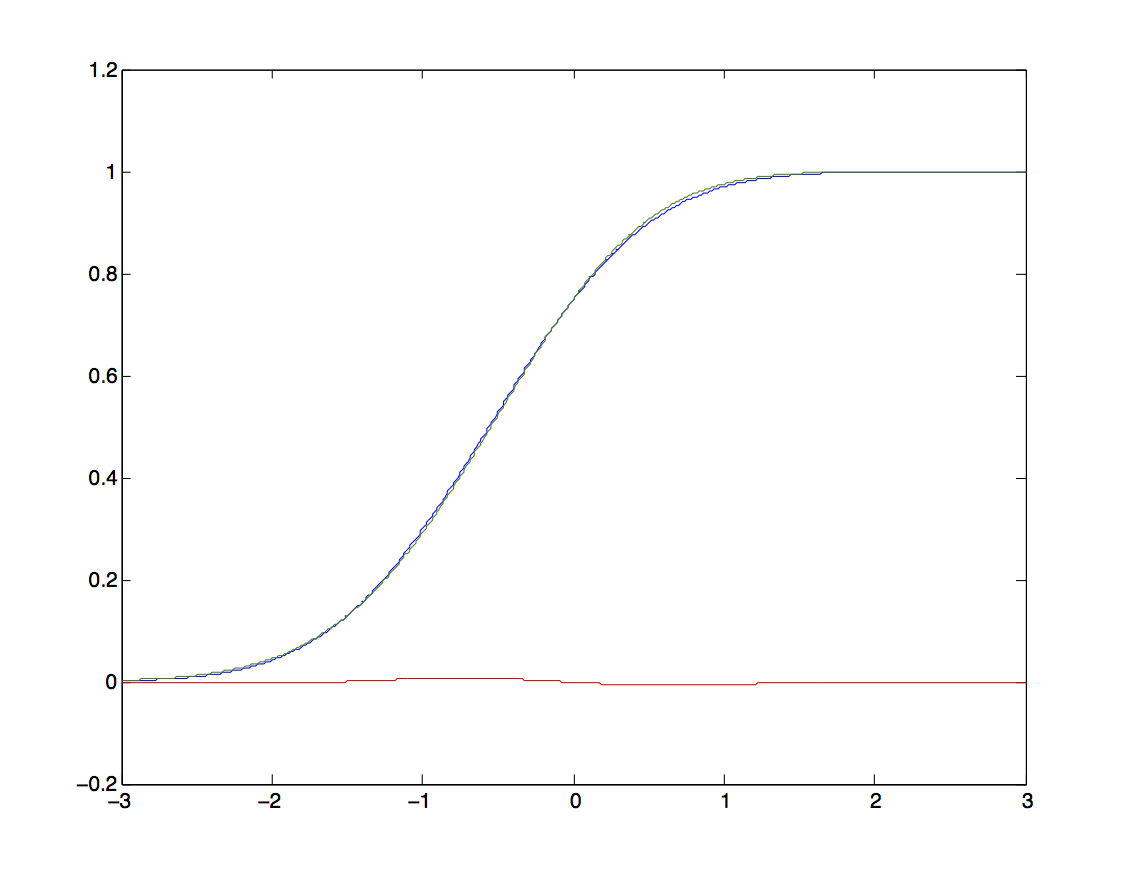

The complication here is to ensure that this equation is satisfied for all . Note that (2.8) and (2.9) are consistent with the definition of a distribution function of a continuous r.v.: , , and is strictly increasing. We can then numerically show that a distribution function that is close to a normal distribution satisfies the conditions with a particular choice of ; see Figure 1.

Although no formal derivation of the counterexample is given, this result suggests the following:

-

(i)

In the bivariate probit model with continuous common exogenous covariates and no excluded instruments, the parameters will be, at best, weakly identified;

-

(ii)

This also implies that, in the semiparametric model considered in Theorem 2.3, the structural parameters and the marginal distributions are not identified without an exclusion restriction, even if has large support.

2.3.2 No Restrictions on Dependence Structures

When the restriction imposed on (i.e., Assumption 5) is completely relaxed, the underlying parameters of model (1.1) may fail to be identified, regardless of whether the exclusion restriction holds. That is, a structure describing how the unobservables are dependent on each other is necessary for identification. This is closely related to the results in the literature that the treatment parameters (which are lower dimensional functions of the individual parameters) in triangular models similar to (1.1) are only partially identified without distributional assumptions; see Bhattacharya et al. (2008), Chiburis (2010), Shaikh and Vytlacil (2011), and Mourifié (2015).

Suppose Assumptions 1–4 hold. Then the model becomes a semiparametric threshold crossing model in that the joint distribution is completely unspecified. Then, as a special case of Shaikh and Vytlacil (2011), one can easily derive bounds for the ATE . The sharpness of these bounds is shown in their paper under a rectangular support assumption for , which is, in turn, relaxed in Mourifié (2015). In addition, using Assumption 6, one can also derive bounds for the individual parameters and , as shown in Chiburis (2010). When there are no excluded instruments in the model, Chiburis (2010) shows that the bounds on the ATE do not improve on the bounds of Manski (1990), whose argument applies to the individual parameters.

3 Sieve and Parametric ML Estimations

Based on the identification results, we now consider estimation. Let denote the vector of the structural individual parameters. Let and be the density functions associated with the distribution functions and , respectively, of the unobservables. Then, is the set of parameters in the semiparametric version of the model. The model becomes fully parametric, once the infinite-dimensional parameters and are fully characterized by some finite-dimensional parameters, i.e., and for and . This yields to be the set of parameters in the parametric version of the model. For either case, the parameter of the model is denoted as for convenience. That is, in the semiparametric model and in the parametric model. For the rest of this paper, we explicitly express to be the true parameter value for . This applies to all the other parameter expressions.

Let be the parameter space for . For the parametric model, the spaces for the finite-dimensional parameters and are denoted as and , respectively. Then, the parameter space for becomes a Cartesian product of , , and , i.e., , in the parametric model.777For example, if one imposes Assumption 6, then and . For the semiparametric model, we consider the following function spaces as the spaces for and :

| (3.1) |

where and is a space of functions, which we specify later. Then, the parameter space of can be written as in the semiparametric model. Note that the function spaces and contain functions that are nonnegative.

We adopt the ML method to estimate the parameters in the model. Let be the random sample. For both parametric and semiparametric models with corresponding , we define the conditional density function of conditional on as

where abbreviates the right hand side expression that equates in (2.2). Then, the log of density becomes

| (3.2) |

where . Consequently, the log-likelihood function can be written as .

Now, the ML estimator of in the parametric model is defined as

| (3.3) |

For the semiparametric model, let and be appropriate sieve spaces for and , respectively, and let and be the sieve approximations of and on their sieve spaces and , respectively. Then, we define the sieve ML estimator of in the semiparametric model as follows:

| (3.4) |

where is the sieve space for .

With the parameter spaces and in (3.1), we are interested in a class of “smooth” univariate square root density functions. Specifically, we assume that and belong to the class of p-smooth functions and we restrict our attention to linear sieve spaces for and .888The definition of -smooth functions can be found in Chen (2007, p.5570) or CFT06 (p.1230). We give the formal definition of -smooth functions in Section 4. In this case, the choice of sieve spaces for and depends on the supports of and . If the supports are bounded, then one can use the polynomial sieve, trigonometric sieve, or cosine sieve. When the supports are unbounded, then we can use the Hermite polynomial sieve or the spline wavelet sieve.

In this paper, we implicitly assume that the copula function is correctly specified. As mentioned earlier, using a parametric copula may lead to model misspecification. It is well known that when the model is misspecified, the ML estimator converges to a pseudo-true value which minimizes the Kullback-Leibler (KL) divergence (e.g., White (1982)). This result applies to a semiparametric model (e.g., Chen and Fan (2006a) and Chen and Fan (2006b)) as in our semiparametric case. We, however, do not investigate the asymptotic properties of the sieve estimators under copula misspecification, as it is beyond the scope of this paper. Instead, later in simulation, we investigate how the copula misspecification affects the performance of estimators.999For related issues of copula misspecification, refer to, e.g., Chen and Fan (2006a) and Liao and Shi (2017). In particular, Chen and Fan (2006a) propose a test procedure for model selection that is based on the test of Vuong (1989). Liao and Shi (2017) extend Vuong’s test to cases where models contain infinite-dimensional parameters and propose a uniformly asymptotically valid Vuong test for semi/non-parametric models. Their setting encompasses those models that can be estimated by the sieve ML as a special case.

4 Asymptotic Theory for Sieve ML Estimators

In this section, we provide the asymptotic theory for the sieve ML estimator of in the semiparametric model. This theory will be useful for practitioners to conduct inference. The asymptotic theory for the ML estimator of in the parametric model is relatively standard and can be found in, e.g., Newey and McFadden (1994). The theory establishes that the parametric ML estimator is consistent, asymptotically normal, and efficient under some regularity conditions. To investigate the asymptotic properties of the sieve ML estimator, we slightly modify our model as follows.

Let ) be a strictly increasing function mapping from to . We further assume that is differentiable and that its derivative is bounded away from zero on . Then, without loss of generality (e.g., Bierens (2014)), we consider the following transformation of and as:

| (4.1) |

where and are unknown distribution functions on . For , we can choose the standard normal distribution function or the logistic distribution function. Since we assume that the distribution functions of and admit density functions, we require that and be differentiable, and write their derivatives as and , respectively. For each , let for some function space . With this modification, we redefine the parameter as . Note that, using the transformation of the distribution functions in equation (4.1), the unknown infinite-dimensional parameters are defined on a bounded domain. In the online appendix, we show that the transformation does not affect the identification result.

We redefine the parameter space to facilitate developing the asymptotic theory. The identification requires that the space of the finite-dimensional parameter be open and convex (see Theorems 2.2 and 2.3), and thus cannot be compact. We introduce an “optimization space” that contains the true parameter and consider it as the parameter space of . Formally, we restrict the parameter space for estimation in the following way.

Assumption 8.

There exists a compact and convex subset such that , where is the interior of the set .

With the optimization space, we define the parameter space as , and the corresponding sieve space is denoted by . Then, the sieve ML estimator in equation (3.4) is also redefined as follows:

| (4.2) |

4.1 Consistency of the Sieve ML Estimators

We begin by showing the consistency of the sieve ML estimator. Since the parameter involves both finite- and infinite-dimensional objects, we establish the consistency of the sieve ML estimators with respect to a pseudo distance function on .101010It is important to choose appropriate norms to ensure the compactness of the original parameter space, as compactness plays a key role in establishing the asymptotic theory. Since the parameter space is infinite-dimensional, it may be compact under certain norms but not under other norms. An infinite-dimensional space that is closed and bounded is not necessarily compact, and thus it is more demanding to show that the parameter space is compact under certain norms. To overcome this difficulty, we take the approach introduced by Gallant and Nychka (1987), which uses two norms to obtain the consistency. Their idea is to use the strong norm to define the parameter space as a ball, and then to ensure the compactness of the parameter space using the consistency norm. In our setting, the Hölder norm is the strong norm and is the consistency norm. Related to this issue, Freyberger and Masten (2015) recently extend the idea to more cases and present compactness results for several parameter spaces. All of the norms and the definitions of function spaces in this paper are provided in the online appendix.

We present the following assumptions, under which the sieve ML estimator in equation (4.2) is consistent with respect to the pseudo-metric .

Assumption 9.

There exists a measurable function such that for all and for all , , with and .

Assumption 10.

is a random sample, with .

Assumption 11.

(i) , with and some ; (ii) where , with being defined as in (i) and being a Hölder ball with radius ; (iii) the density functions and are bounded away from zero on .

Assumption 12.

(i) , where and as ; (ii) for all , we have , and there exists a sequence such that as .

Assumption 13.

For , let and . The derivatives and are uniformly bounded for all .

Assumption 9 guarantees that the log-likelihood function is well defined for all and that . Assumption 10 restricts the data generating process (DGP), and assumes the existence of moments of the data. Assumption 11 defines the parameter space and implies that the infinite-dimensional parameters are in some smooth class called a Hölder class. Note that conditions (i) and (ii) in Assumption 11 together imply that and belong to , where .111111See the online appendix for details. Thus, we may assume that and belong to a Hölder ball with smoothness under Assumption 11.121212These conditions implicitly define the strong norm (Hölder norm). The condition that and are the same can be relaxed, but it is imposed for simplicity. The first part of Assumption 12 restricts our choice of sieve spaces for and to linear sieve spaces with order . This can be relaxed so that the choice of is different for and . The latter part of Assumption 12 requires that the sieve space be chosen appropriately so that the unknown parameters can be well-approximated. Because the unknown infinite-dimensional parameters belong to a Hölder ball and are defined on bounded supports, we can choose the polynomial sieve, trigonometric sieve, cosine sieve, or spline sieve.131313Refer to Chen (2007) or CFT06 for details on the choice of sieve spaces. For example, if we choose the polynomial sieve or the spline sieve, then one can show that (e.g., Lorentz (1966)). Assumption 13 imposes the boundedness of the derivatives of the copula function.

The following theorem demonstrates that under the above assumptions, the sieve estimator is consistent with respect to the pseudo metric, .

4.2 Convergence Rates

In this section, we derive the convergence rate of the sieve ML estimator. The convergence rate provides information on how fast the estimator converges to the true parameter value. Heuristically, the faster the convergence rate, the larger the effective sample size is for estimation. The next theorem demonstrates the convergence rate of the sieve ML estimator with respect to the -norm .

Theorem 4.2.

The former convergence rate is standard in the literature, where the first term corresponds to variance, which increases in , and the second term corresponds to the approximation error , which decreases in . The choice of yields the optimal convergence rate, which is slower than the parametric rate (). Note that this rate increases with the degree of smoothness, .

4.3 Asymptotic Normality of Smooth Functionals

We now establish the asymptotic normality of smooth functionals. The parameters in our model contains both finite- and infinite-dimensional parameters, and many objects of interest are written as functionals of both types of the parameters. The results of this section can be used to calculate the standard error of the estimate of a functional of interest (including the individual finite-dimensional parameters), or to conduct inference (i.e., testing hypotheses and constructing confidence intervals) based on normal approximation.

Before proceeding, we strengthen the smoothness condition in Assumption 5. Let denote the second-order partial derivative of a copula function with respect to and , for .

Assumption 14.

The copula function is twice continuously differentiable with respect to and , and its first- and second- order partial derivatives are well defined in a neighborhood of .

Let be the linear span of . For , define the directional derivative of at the direction as

| (4.3) |

where , , and are given by equations (B.4)–(B.6) in the online appendix. If we denote the closed linear span of under the Fisher norm by , then is a Hilbert space.

Let be a functional. For any , we write

provided the right hand side limit is well defined. The following assumption characterizes the smoothness of the functional .

Assumption 15.

The following conditions hold:

(i) there exist constants and a small such that for any with ,

(ii) For any , is continuously differentiable in around , and

Assumption 15 defines a smooth functional and guarantees the existence of such that for all and . Here, we call the Riesz representer for the functional .

The next assumption requires that the Riesz representer be well approximated over the sieve space and that it converges at a rate with respect to the Fisher norm.

Assumption 16.

There exists such that .

The following proposition states that the plug-in sieve ML estimator of is -asymptotically normally distributed under certain conditions. The technical conditions (Assumptions 17, 18 and 19) can be found in the online appendix.

It is worth noting that, although the parameter contains an infinite-dimensional object (i.e., the marginal distributions of and ), the sieve plug-in estimator is -estimable due to the fact that is a smooth functional.

4.3.1 Example 1: Asymptotic Normality for the Finite-Dimensional Parameter

The finite-dimensional parameter is a special case of the smooth functionals. Here, we demonstrate the asymptotic normality of the sieve estimator of the finite-dimensional parameter .

Theorem 4.3.

The covariance matrix in (4.4) needs to be estimated. To do so, CFT06 adopt the covariance estimation method proposed by Ai and Chen (2003). Since an infinite-dimensional optimization is involved in calculating , we provide a sieve estimator of . The sieve spaces for and can be the same as those for and , respectively. As in Ai and Chen (2003), we first estimate efficient score functions by solving the following minimization problem: for all ,

Let for given and compute

to obtain a consistent estimator of . We now summarize this result as follows:

Theorem 4.4.

Suppose that assumptions in Theorem 4.3 hold. Then, .

The proof of the theorem can be found in Theorem 5.1 in Ai and Chen (2003).

4.3.2 Example 2: Asymptotic Normality for the Conditional ATE

We now consider the conditional ATE, . From Proposition 4.1, we provide the asymptotic normality of the sieve plug-in estimator of the conditional ATE:

4.4 Weighted Bootstrap

The asymptotic variances characterized in the previous subsection can be estimated using the sieve methods. In practice, estimating asymptotic variances may be sensitive to the choice of the number of sieve approximation terms. Furthermore, when the dimension of is large, it is relatively cumbersome to estimate the asymptotic variance of the sieve estimator for the finite-dimensional parameter. In this subsection, we briefly discuss the weighted bootstrap as an alternative procedure.

For general semiparametric M-estimation, Ma and Kosorok (2005) and Cheng and Huang (2010) provide the validity of the weighted bootstrap for finite-dimensional parameters in a class of semiparametric models that includes our model. Related to these results, Chen and Pouzo (2009) provide the bootstrap validity in semiparametric conditional moment models. We do not pursue to prove the bootstrap validity in this paper, as these references sufficiently address it. In our empirical exercise, we use the weighted bootstrap scheme proposed in these papers to obtain the standard errors of the estimated functionals of interest. Let be a smooth functional of interest and be the number of bootstrap iterations. The weighted bootstrap is carried out as follows:

-

1.

For each , let be a random sample generated from a positive random variable such that , , and is independent of .141414Note that the condition on the variance of can be relaxed. In our empirical example, we use .

-

2.

For each bootstrap iteration , define be a bootstrap estimate of :

where . Obtain the bootstrap estimate of the functional of interest by using and denote it by .

-

3.

The bootstrap standard error of is given by , where .

One may use the bootstrap standard errors to construct confidence intervals, and such confidence intervals rely on the normal approximation. As an alternative to the normal approximation, one can use percentile confidence intervals. For a small , a percent percentile confidence interval for a functional is constructed as follows:

where is the -th quantile of bootstrap estimates . We suggest that practitioners use the percentile confidence intervals rather than the confidence intervals with the bootstrap standard errors.

5 Monte Carlo Simulation and Sensitivity Analysis

In this section, we conduct a sensitivity analysis via Monte Carlo simulation exercises to provide guidance for empirical researchers. To this end, we investigate the finite sample performance of the sieve ML estimators of the finite-dimensional parameter and the ATE. We compare them with the performance of the parametric ML estimators under various DGPs and model specifications, and illustrate how the parametric estimators of and the ATE suffer from misspecification of the marginal distribution of . Note that the ATE involves and the marginal of .

5.1 Simulation Design

We compare the performance of the parametric and semiparametric estimators when the marginal distributions are misspecified in the parametric models. To calculate the parametric estimators, we specify the parametric models with normal distributions for the marginals of and , owing to their popularity. For the DGPs, we consider two marginals of and : the standard normal distribution (to reflect correct specification) and a mixture of normal distributions (to reflect misspecification).

The DGPs are as follows:

where , , and . Here, and are normal or a mixture of normal.151515For the mixture of normal distributions, and are generated from for appropriate , so that the mean is zero and the variance is one. For , we consider the Gaussian, Frank, Clayton, and Gumbel copulas, which satisfy the identifying assumption (Assumption 5). The dependence structure between and is characterized by a one-dimensional parameter in all copulas considered, but the interpretation of the dependence parameter differs across the copulas. To resolve this issue, we report the Spearman’s corresponding to the estimated dependence parameter in each copula specification. We estimate the models with several values of to examine whether the performance of the estimators varies with the degree of dependence. Although we assume that the copula is correctly specified, economic theory does not provide a justification for the choice of copula. In this simulation study, we also examine the effect of copula misspecification on the performance of the estimators.161616Misspecification problems in copula-based models have been documented using Monte Carlo simulations in the statistic literature (e.g., Kim et al. (2007a, b); Lawless and Yilmaz (2011)). In particular, Lawless and Yilmaz (2011) compare the performance of the parametric and semiparametric ML estimators in a copula-based model and show that the semiparametric two-step method outperforms the parametric estimation method when the copula function is misspecified.

We impose a restriction that has no constant for the location normalization, and fix and to -1 for the scale normalization. We use these normalizations in both parametric and semiparametric models, and it allows us to easily compare the performance of the parametric and semiparametric estimators. We consider two sample sizes, 500 and 1000, and all results are obtained from 2000 Monte Carlo replications. As a performance measure of the estimators, we consider the root mean squared errors (RMSEs) in our simulation.

5.2 Estimation of Parametric and Semiparametric Models

The parametric models can be estimated by the standard ML method. Since bivariate probit models are commonly used in practice, we specify the model using the Gaussian copula and normal marginals. In addition to that, we also try different copulas and normal marginals.171717Such an estimation method in related parameteric models can be found in Marra and Radice (2011). The R package (GJRM) used in their paper can be used to estimate our parametric model as well.

Consider semiparametric models. Recall that we assume that . Therefore, for each , we approximate to

| (5.1) |

where is the set of approximating functions for , and is the number of approximating functions. The approximation in (5.1) guarantees that by construction. We take the space of the polynomials as the sieve space for and . The orders of the polynomials ( and ) are set to be proportional to . To incorporate the specification given in (4.1), we choose the standard normal distribution function for .

5.3 Simulation Results

We begin by examining the simulation results under correct specification (i.e., the true marginal distributions and the specified marginal distributions are both normal). Table 1 shows the simulation results for . We find that the ML estimators of and the ATE perform well in the parametric models, with negligible biases and small variances.181818The ATE is evaluated at the mean of . The performance of the sieve ML estimators of and the ATE in the semiparametric models is as good as that in the parametric models, even with this moderate sample size.

Now, we consider the cases where the marginal distributions are misspecified in the parametric models. Table 2 considers the case where the true marginal distributions are a mixture of normal distributions, but the researcher specifies them as normal distributions. In this table, the RMSEs of the parametric ML estimators are larger than those of the sieve ML estimators. This implies that the parametric ML estimators suffer from misspecification while the sieve ML estimators do not. Moreover, the parametric estimators of the ATE are substantially distorted under this misspecification, presumably because the ATE is a function of the misspecified distribution of . Note that the poor performance of the parametric estimators is attributed not only to large bias, but also large variance. For instance, the bias of the parametric estimator of the ATE with the Gaussian copula is 0.1377, which is about eight times larger than that of the corresponding sieve estimator. These biases of the parametric estimators of the ATE are substantial in that they do not disappear with the increased sample size.191919We provide simulation results with a larger sample size (), and they can be found in the online appendix. Therefore, the simulation results demonstrate that when the marginal distributions are misspecified, the sieve estimators outperform the parametric estimators in terms of the RMSE. The online appendix also contains simulation results for the cases where both the copula and the marginal distributions are misspecified. The results show that, even under copula misspecification, the sieve ML estimators remain to outperform the parametric counterparts when the marginal distributions are misspecified.

Overall, the simulation results suggest that researchers are recommended to use the semiparametric models and the sieve ML estimation proposed in this paper when they are concerned about model misspecification. The following is the summary of the main findings from our simulation study:

-

(i)

When the model is correctly specified, the performance of the sieve ML estimators is comparable to that of the parametric ML estimators.

-

(ii)

When the marginal distributions are misspecified, the sieve ML estimation is recommended in order to improve the performance.

-

(iii)

The semiparametric ML estimators performs better than the parametric ML estimators under both copula and marginal misspecification. Therefore, the semiparametric models are preferred to the parametric models in such cases.

-

(iv)

Especially for the ATE, whenever the marginal distributions are misspecified, the parametric ML estimates can be significantly distorted.

We provide additional simulation results in the online appendix, where we consider (a) a larger sample size, (b) both copula and marginal misspecification, (c) different degrees of dependence, (d) marginal density functions of heavy tails, and (e) the coverage probabilities of bootstrap confidence intervals. Here is the summary. Across various simulation designs ((a)–(c)), our main findings remain the same. When the marginal distributions are believed to have fat tails, we recommend practitioners to use the transformation function that has fat tails. Lastly, the percentile bootstrap works well with the coverage probabilities close to its nominal level.

6 Empirical Example

In this section, we illustrate in an application the practical relevance of the theoretical results developed in this paper. It is widely recognized that health insurance coverage can be an important factor for patients’ decisions for making medical visits. At the same time, having insurances is endogenously determined by individual’s health status and socioeconomic characteristics. In our empirical application, we analyze how health insurance coverage affects an individual’s decision to visit a doctor. In this example, is a binary outcome variable indicating whether an individual visited a doctor’s office, and is the endogenous treatment variable that indicates whether an individual has her own private insurance.

We use the 2010 wave of the Medical Expenditure Panel Survey (MEPS) as our main data source. We focus on all the visits happened in January, 2010. We restrict the sample to contain individuals with age between 25 and 64, and exclude individuals who have retained any kinds of federal or state insurance in 2010. For , we consider two instrumental variables that are used in Zimmer (2018)—the number of employees in the firm at which the individual works and a dummy variable that indicates whether a firm has multiple locations. These variables reflect how big the firm is, and the underlying rationale for using these variables as instruments is as follows: the bigger the firm is, the more likely it provides fringe benefits including health insurance. Therefore, it is likely that these instruments affect insurance status. We can argue, however, that they do not have direct effects on decisions to visit doctors.202020Note that it is difficult to justify these instruments for individuals who are either self-employed or unemployed. To avoid this issue, we exclude those individuals from our analysis. We assume that these variables are exogenous conditional on covariates. For additional covariates , we include age, gender, years of education, family size (the number of family members), income, region, race, marital status, subjective physical and mental health status evaluations, and whether living in a metropolitan statistical area. For the exogenous variable in our model, we use information about the provision of paid sick leave, which is separately collected from the National Compensation Survey published by the U.S. Bureau of Labor Statistics. We match the information for various industries with the primary dataset we use. Conditional on the covariates listed above, we assume that the number of sick leave days and leave benefits are exogenous, by the same argument as for the instruments. Since and are assumed to be exogenous only conditional on , we rely on Assumption 1′ instead of Assumption 1 for identification.

Since we include various control variables, one may concern that the resulting estimators are imprecise with a moderate sample size. It is worth emphasizing, however, that our semiparametric estimators do not suffer from the curse of dimensionality as theoretically shown in Section 4. This is because of the parametric index structure in our model. Moreover, we do not attempt to estimate the distributions of the unobservables conditional on these covariates, but only estimate the marginal distributions.

Table 3 summarizes the variables used in estimation and shows their summary statistics. While of individuals had private health insurances in January 2010, only of them visited doctors during the period. We use two variables for the pay sick leave provision (i.e., )—within each industry, the percentage of workers who are provided with paid sick leave benefits and the percentage of workers who are provided with a fixed number of days for sick leave per year. The summary statistics for these two variables show that there are sufficient variations across individuals in different industries. Note that all the continuous variables are standardized in order to ensure stability in estimation.212121That is, for a continuous random variable , define , where and are the sample average and standard deviation of , respectively.

Before estimating the parametric and semiparametric models, we run a first-stage OLS regression of on , , and to see if the excluded instruments are weak. The -statistic value is , and thus we assume that the instruments are strong.222222The -statistic in the first-stage linear regression may not be the best indicator for detecting weak instruments in nonlinear models. Han and McCloskey (2019) develop inference methods that are robust to weak identification for a class of nonlinear models, and consider bivariate probit models as one of the leading examples. For the normalization of the parametric model, we you the convention— and . On the other hand, for the semiparametric model, we impose the normalization used in our simulation studies—i.e. we exclude the constant terms and the coefficients on are fixed to be corresponding parametric estimates. We choose the Gaussian copula to capture the dependence structure between and . In both models, the standard errors are obtained by the bootstrap procedure (Section 4.4), where the bootstrap weights are generated from the exponential distribution with the parameter value .

Tables 4 and 5 present the estimation results for the selection equation and the outcome equation, respectively. Between the parametric and semiparametric models, the magnitude and significance of the estimates differs, although, overall, the signs of the estimates are similar. Table 6 shows the ATE estimates evaluated at various values of , as well as the estimates of the copula parameter . The parametric estimate of is statistically significant under level, whereas the semiparametric estimate is not. We can find that the parametric estimates of the ATE are different from the corresponding semiparametric estimates. For example, the parametric ATE estimate evaluated at the quantile of is about , which means that having private insurance increases the probability of visiting doctors by . On the other hand, the corresponding semiparametric estimate shows that the effect is . The discrepancy in the ATE estimates between the parametric and semiparametric models suggests the possible misspecification of the marginals, which is consistent with the premise of this paper.

7 Conclusions

In this paper, we propose semiparametric estimation and inference methods for generalized bivariate probit models. Specifically, we develop the asymptotic theory for the sieve ML estimators of semiparametric copula-based triangular systems with binary endogenous variables. We show that the sieve ML estimators are consistent and that their smooth functionals are -asymptotically normal under some regularity conditions. This semiparametric estimation approach allows for flexibility in the models and thus provides robustness in estimation and inference.

We conduct a sensitivity analysis to examine how sensitive the estimation results are to model specifications. The results show that, overall, the semiparametric sieve ML estimators perform well in terms of both bias and variance. When the marginal distributions are misspecified, the sieve ML estimators substantially outperform the parametric ML estimators and the latter exhibit substantial bias. In particular, we find that the parametric estimates of the parameters involving the misspecified marginal distributions, such as the ATE, are highly misleading. When the model is correctly specified, we find that the performance of the sieve ML estimators is comparable to that of the parametric ones. When the copula is also misspecified, the distortion of the parametric estimates under misspecification of the marginals can become even more severe, whereas the semiparametric estimates do not seem to be affected by this misspecification as long as the copula of the true DGP is within the stochastic ordering class. A related and interesting question is how the results would change if the data are not generated from this class of copulas.

We also formally show that the exclusion restriction is not only sufficient, but is also necessary for identification. Without the exclusion restriction, the model parameters are not identified or, under the normality assumption, are, at best, weakly identified. Some empirical studies ignore the exclusion restriction when estimating the model, and our non-identification result provides a caveat for practitioners.

References

- Ai and Chen (2003) Ai, C. and X. Chen (2003). Efficient estimation of models with conditional moment restrictions containing unknown functions. Econometrica 71(6), 1795–1843.

- Altonji et al. (2005) Altonji, J. G., T. E. Elder, and C. R. Taber (2005). An evaluation of instrumental variable strategies for estimating the effects of catholic schooling. Journal of Human Resources 40(4), 791–821.

- Bhattacharya et al. (2006) Bhattacharya, J., D. Goldman, and D. McCaffrey (2006). Estimating probit models with self-selected treatments. Statistics in Medicine 25(3), 389–413.

- Bhattacharya et al. (2008) Bhattacharya, J., A. M. Shaikh, and E. Vytlacil (2008). Treatment effect bounds under monotonicity assumptions: An application to swan-ganz catheterization. The American Economic Review 98(2), 351–356.

- Bierens (2008) Bierens, H. J. (2008). Semi-nonparametric interval-censored mixed proportional hazard models: Identification and consistency results. Econometric Theory 24(3), 749–794.

- Bierens (2014) Bierens, H. J. (2014). Consistency and asymptotic normality of sieve ml estimators under low-level conditions. Econometric Theory 30(5), 1021–1076.

- Chen (2007) Chen, X. (2007). Large sample sieve estimation of semi-nonparametric models. Handbook of Econometrics 6B, 5549–5632.

- Chen and Fan (2006a) Chen, X. and Y. Fan (2006a). Estimation and model selection of semiparametric copula-based multivariate dynamic models under copula misspecification. Journal of Econometrics 135(1), 125–154.

- Chen and Fan (2006b) Chen, X. and Y. Fan (2006b). Estimation of copula-based semiparametric time series models. Journal of Econometrics 130(2), 307–335.

- Chen et al. (2006) Chen, X., Y. Fan, and V. Tsyrennikov (2006). Efficient estimation of semiparametric multivariate copula models. Journal of the American Statistical Association 101(475), 1228–1240.

- Chen et al. (2009) Chen, X., Y. Hu, and A. Lewbel (2009). Nonparametric identification and estimation of nonclassical errors-in-variables models without additional information. Statistica Sinica, 949–968.

- Chen and Pouzo (2009) Chen, X. and D. Pouzo (2009). Efficient estimation of semiparametric conditional moment models with possibly nonsmooth residuals. Journal of Econometrics 152(1), 46–60.

- Chen and Shen (1998) Chen, X. and X. Shen (1998). Sieve extremum estimates for weakly dependent data. Econometrica 66(2), 289–314.

- Cheng and Huang (2010) Cheng, G. and J. Z. Huang (2010). Bootstrap consistency for general semiparametric M-estimation. The Annals of Statistics 38(5), 2884–2915.

- Chiburis (2010) Chiburis, R. (2010). Semiparametric bounds on treatment effects. Journal of Econometrics 159(2), 267–275.

- Evans and Schwab (1995) Evans, W. N. and R. M. Schwab (1995). Finishing high school and starting college: Do catholic schools make a difference? The Quarterly Journal of Economics 110(4), 941–974.

- Freyberger and Masten (2015) Freyberger, J. and M. Masten (2015). Compactness of infinite dimensional parameter spaces. Technical report, cemmap working paper, Centre for Microdata Methods and Practice.

- Gallant and Nychka (1987) Gallant, A. R. and D. W. Nychka (1987). Semi-nonparametric maximum likelihood estimation. Econometrica 55(2), 363–390.

- Goldman et al. (2001) Goldman, D., J. Bhattacharya, D. Mccaffrey, N. Duan, A. Leibowitz, G. Joyce, and S. Morton (2001). Effect of Insurance on Mortality in an HIV-Positive Population in Care. Journal of the American Statistical Association 96(455).

- Han and McCloskey (2019) Han, S. and A. McCloskey (2019). Estimation and inference with a (nearly) singular Jacobian. Quantitative Economics (Forthcoming).

- Han and Vytlacil (2017) Han, S. and E. Vytlacil (2017). Identification in a generalization of bivariate probit models with dummy endogenous regressors. Journal of Econometrics 199(1), 63–73.

- Heckman (1979) Heckman, J. J. (1979). Sample selection bias as a specification error. Econometrica 47(1), 153–162.

- Hu and Schennach (2008) Hu, Y. and S. M. Schennach (2008). Instrumental variable treatment of nonclassical measurement error models. Econometrica 76(1), 195–216.

- Ieva et al. (2014) Ieva, F., G. Marra, A. M. Paganoni, and R. Radice (2014). A semiparametric bivariate probit model for joint modeling of outcomes in stemi patients. Computational and Mathematical Methods in Medicine 2014.

- Joe (1997) Joe, H. (1997). Multivariate Models and Multivariate Dependence Concepts. Chapman & Hall/CRC Monographs on Statistics & Applied Probability. Taylor & Francis.

- Kim et al. (2007a) Kim, G., M. J. Silvapulle, and P. Silvapulle (2007a). Comparison of semiparametric and parametric methods for estimating copulas. Computational Statistics & Data Analysis 51(6), 2836–2850.

- Kim et al. (2007b) Kim, G., M. J. Silvapulle, and P. Silvapulle (2007b). Semiparametric estimation of the error distribution in multivariate regression using copulas. Australian & New Zealand Journal of Statistics 49(3), 321–336.

- Lawless and Yilmaz (2011) Lawless, J. F. and Y. E. Yilmaz (2011). Comparison of semiparametric maximum likelihood estimation and two-stage semiparametric estimation in copula models. Computational Statistics & Data Analysis 55(7), 2446–2455.

- Liao and Shi (2017) Liao, Z. and X. Shi (2017). A uniform model selection test for semi/nonparametric models. Working paper.

- Lorentz (1966) Lorentz, G. (1966). Approximation of functions. Holt, Rinehart and Winston New York.

- Ma and Kosorok (2005) Ma, S. and M. R. Kosorok (2005). Robust semiparametric M-estimation and the weighted bootstrap. Journal of Multivariate Analysis 96(1), 190–217.

- Marra and Radice (2011) Marra, G. and R. Radice (2011). Estimation of a semiparametric recursive bivariate probit model in the presence of endogeneity. Canadian Journal of Statistics 39(2), 259–279.

- Mourifié (2015) Mourifié, I. (2015). Sharp bounds on treatment effects in a binary triangular system. Journal of Econometrics 187(1), 74–81.

- Mourifié and Méango (2014) Mourifié, I. and R. Méango (2014). A note on the identification in two equations probit model with dummy endogenous regressor. Economics Letters 125(3), 360–363.

- Neal (1997) Neal, D. A. (1997). The effects of catholic secondary schooling on educational achievement. Journal of Labor Economics 15(1), 98–123.

- Nelsen (1999) Nelsen, R. B. (1999). An introduction to copulas. Springer Verlag.

- Newey and McFadden (1994) Newey, W. K. and D. McFadden (1994). Large sample estimation and hypothesis testing. Handbook of Econometrics 4, 2111–2245.

- Rhine et al. (2006) Rhine, S. L., W. H. Greene, and M. Toussaint-Comeau (2006). The importance of check-cashing businesses to the unbanked: Racial/ethnic differences. Review of Economics and Statistics 88(1), 146–157.

- Shaikh and Vytlacil (2011) Shaikh, A. M. and E. J. Vytlacil (2011). Partial identification in triangular systems of equations with binary dependent variables. Econometrica 79(3), 949–955.

- van de Geer (2000) van de Geer, S. A. (2000). Empirical Processes in M-estimation, Volume 6. Cambridge university press.

- van der Vaart and Wellner (1996) van der Vaart, A. and J. Wellner (1996). Weak convergence and empirical processes. Springer, New York.

- Vella (1998) Vella, F. (1998). Models with sample selection bias: A survey. Journal of Human Resources 33(1), 127–169.

- Vuong (1989) Vuong, Q. H. (1989). Likelihood ratio tests for model selection and non-nested hypotheses. Econometrica 57(2), 307–333.

- White (1982) White, H. (1982). Maximum likelihood estimation of misspecified models. Econometrica 50(1), 1–25.

- White and Wolaver (2003) White, N. E. and A. M. Wolaver (2003). Occupation choice, information, and migration. The Review of Regional Studies 33(2), 142.

- Wilde (2000) Wilde, J. (2000). Identification of multiple equation probit models with endogenous dummy regressors. Economics Letters 69(3), 309–312.

- Zimmer (2018) Zimmer, D. (2018). Using copulas to estimate the coefficient of a binary endogenous regressor in a Poisson regression: Application to the effect of insurance on doctor visits. Health Economics 27(3), 545–556.

| Parametric Estimation, Gaussian Copula | Semiparametric Estimation, Gaussian Copula | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| True Values | 0.8000 | 1.1000 | 0.5000 | 0.3643 | True Values | 0.8000 | 1.1000 | 0.5000 | 0.3643 |

| Estimate | 0.8074 | 1.1469 | 0.4956 | 0.3657 | Estimate | 0.8070 | 1.1577 | 0.5037 | 0.3584 |

| S.D | 0.0934 | 0.3954 | 0.1537 | 0.0897 | S.D | 0.0940 | 0.4141 | 0.1528 | 0.0935 |

| Bias | 0.0074 | 0.0469 | -0.0044 | 0.0014 | Bias | 0.0070 | 0.0577 | 0.0038 | -0.0060 |

| RMSE | 0.0936 | 0.3982 | 0.1537 | 0.0897 | RMSE | 0.0943 | 0.4181 | 0.1528 | 0.0937 |

| Parametric Estimation, Frank Copula | Semiparametric Estimation, Frank Copula | ||||||||

| True Values | 0.8000 | 1.1000 | 0.5000 | 0.3643 | True Values | 0.8000 | 1.1000 | 0.5000 | 0.3643 |

| Estimate | 0.8027 | 1.1450 | 0.4909 | 0.3681 | Estimate | 0.8028 | 1.1556 | 0.4981 | 0.3598 |

| S.D | 0.0936 | 0.3379 | 0.1310 | 0.0781 | S.D | 0.0943 | 0.3588 | 0.1314 | 0.0829 |

| Bias | 0.0027 | 0.0450 | -0.0091 | 0.0037 | Bias | 0.0028 | 0.0556 | -0.0019 | -0.0045 |

| RMSE | 0.0936 | 0.3409 | 0.1313 | 0.0781 | RMSE | 0.0944 | 0.3631 | 0.1314 | 0.0830 |

| Parametric Estimation, Clayton Copula | Semiparametric Estimation, Clayton Copula | ||||||||

| True Values | 0.8000 | 1.1000 | 0.5000 | 0.3643 | True Values | 0.8000 | 1.1000 | 0.5000 | 0.3643 |

| Estimate | 0.8024 | 1.1083 | 0.5075 | 0.3598 | Estimate | 0.8027 | 1.1275 | 0.5140 | 0.3504 |

| S.D | 0.0942 | 0.3371 | 0.1368 | 0.0791 | S.D | 0.0935 | 0.3719 | 0.1354 | 0.0816 |

| Bias | 0.0024 | 0.0083 | 0.0075 | -0.0045 | Bias | 0.0027 | 0.0275 | 0.0139 | -0.0139 |

| RMSE | 0.0942 | 0.3372 | 0.1370 | 0.0792 | RMSE | 0.0936 | 0.3729 | 0.1361 | 0.0828 |

| Parametric Estimation, Gumbel Copula | Semiparametric Estimation, Gumbel Copula | ||||||||

| True Values | 0.8000 | 1.1000 | 0.5000 | 0.3643 | True Values | 0.8000 | 1.1000 | 0.5000 | 0.3643 |

| Estimate | 0.8026 | 1.1339 | 0.5060 | 0.3605 | Estimate | 0.8035 | 1.1564 | 0.5102 | 0.3562 |

| S.D | 0.0974 | 0.4002 | 0.1488 | 0.0894 | S.D | 0.0994 | 0.4300 | 0.1535 | 0.0978 |

| Bias | 0.0026 | 0.0339 | 0.0060 | -0.0038 | Bias | 0.0035 | 0.0564 | 0.0102 | -0.0081 |

| RMSE | 0.0974 | 0.4016 | 0.1489 | 0.0895 | RMSE | 0.0995 | 0.4337 | 0.1539 | 0.0981 |

| Parametric Estimation, Gaussian Copula | Semiparametric Estimation, Gaussian Copula | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| True Values | 0.8000 | 1.1000 | 0.5000 | 0.1066 | True Values | 0.8000 | 1.1000 | 0.5000 | 0.1066 |

| Estimate | 0.7994 | 1.0925 | 0.4496 | 0.2443 | Estimate | 0.8562 | 1.2696 | 0.4895 | 0.1241 |

| S.D | 0.1281 | 0.6285 | 0.1651 | 0.1129 | S.D | 0.1113 | 0.3728 | 0.1059 | 0.0653 |

| Bias | -0.0006 | -0.0075 | -0.0504 | 0.1377 | Bias | 0.0562 | 0.1696 | -0.0105 | 0.0174 |

| RMSE | 0.1281 | 0.6285 | 0.1726 | 0.1780 | RMSE | 0.1247 | 0.4096 | 0.1064 | 0.0675 |

| Parametric Estimation, Frank Copula | Semiparametric Estimation, Frank Copula | ||||||||

| True Values | 0.8000 | 1.1000 | 0.5000 | 0.1066 | True Values | 0.8000 | 1.1000 | 0.5000 | 0.1066 |

| Estimate | 0.8056 | 1.3088 | 0.3976 | 0.2894 | Estimate | 0.8377 | 1.2541 | 0.4829 | 0.1276 |

| S.D | 0.1272 | 0.5093 | 0.1221 | 0.0883 | S.D | 0.1141 | 0.3564 | 0.0963 | 0.0689 |

| Bias | 0.0056 | 0.2088 | -0.1024 | 0.1827 | Bias | 0.0377 | 0.1541 | -0.0171 | 0.0210 |

| RMSE | 0.1273 | 0.5504 | 0.1594 | 0.2030 | RMSE | 0.1202 | 0.3883 | 0.0978 | 0.0720 |

| Parametric Estimation, Clayton Copula | Semiparametric Estimation, Clayton Copula | ||||||||

| True Values | 0.8000 | 1.1000 | 0.5000 | 0.1066 | True Values | 0.8000 | 1.1000 | 0.5000 | 0.1066 |

| Estimate | 0.8099 | 1.1439 | 0.4236 | 0.2555 | Estimate | 0.8441 | 1.2234 | 0.4948 | 0.1192 |

| S.D | 0.1309 | 0.5236 | 0.1412 | 0.0913 | S.D | 0.1134 | 0.3611 | 0.0999 | 0.0611 |

| Bias | 0.0099 | 0.0439 | -0.0764 | 0.1488 | Bias | 0.0441 | 0.1234 | -0.0053 | 0.0126 |

| RMSE | 0.1312 | 0.5254 | 0.1605 | 0.1746 | RMSE | 0.1217 | 0.3816 | 0.1001 | 0.0624 |

| Parametric Estimation, Gumbel Copula | Semiparametric Estimation, Gumbel Copula | ||||||||

| True Values | 0.8000 | 1.1000 | 0.5000 | 0.1066 | True Values | 0.8000 | 1.1000 | 0.5000 | 0.1066 |

| Estimate | 0.7892 | 1.0326 | 0.4650 | 0.2373 | Estimate | 0.8484 | 1.2692 | 0.4900 | 0.1259 |

| S.D | 0.1333 | 0.5297 | 0.1338 | 0.0986 | S.D | 0.1142 | 0.3646 | 0.0986 | 0.0645 |

| Bias | -0.0108 | -0.0674 | -0.0350 | 0.1307 | Bias | 0.0484 | 0.1692 | -0.0099 | 0.0193 |

| RMSE | 0.1337 | 0.5340 | 0.1383 | 0.1637 | RMSE | 0.1241 | 0.4019 | 0.0991 | 0.0673 |

| Variable | Mean | S.D | Min | Max | |

| Whether or not visit doctors | 0.182 | 0.386 | 0 | 1 | |

| Whether or not have insurance | 0.657 | 0.475 | 0 | 1 | |

| Age | 42.591 | 10.574 | 25 | 64 | |

| Years of education | 13.433 | 2.892 | 0 | 17 | |

| Income (hourly) | 20.094 | 11.990 | 0.4 | 73.08 | |

| Family size | 2.932 | 1.595 | 1 | 14 | |

| Living in MSA | 0.868 | 0.338 | 0 | 1 | |

| Male | 0.500 | 0.500 | 0 | 1 | |

| Region: NorthEast | 0.141 | 0.348 | 0 | 1 | |

| Region: MidWest | 0.226 | 0.418 | 0 | 1 | |

| Region: South | 0.369 | 0.483 | 0 | 1 | |

| Region: West | 0.264 | 0.441 | 0 | 1 | |

| Race: White | 0.739 | 0.439 | 0 | 1 | |

| Race: Black | 0.170 | 0.376 | 0 | 1 | |

| Race: Minority | 0.010 | 0.099 | 0 | 1 | |

| Race: Asian | 0.081 | 0.273 | 0 | 1 | |

| Ever married | 0.782 | 0.413 | 0 | 1 | |

| Physical health below Good | 0.095 | 0.293 | 0 | 1 | |

| Mental health below Good | 0.036 | 0.186 | 0 | 1 | |

| Number of employees | 149.385 | 182.662 | 1 | 500 | |

| Firm has multiple locations | 0.682 | 0.466 | 0 | 1 | |

| sick 32 | 68.317 | 17.402 | 42 | 91 | |

| sick 34 | 70.463 | 3.633 | 67 | 77 | |

| Number of observations = 7,555 | |||||

: The original variables for these variables are coded into 5 groups - Excellent, Very Good, Good, Fair, and Poor. These variables show how much portion of individuals in the sample considers their physical/mental health is below Good (i.e. Fair or Poor).

| Parametric | Semiparametric | |

|---|---|---|

| age | 0.130*** | 0.077*** |

| (0.018) | (0.038) | |

| years of education | 0.190*** | 0.098** |

| (0.018) | (0.044) | |

| family size | -0.120*** | -0.041* |

| (0.017) | (0.023) | |

| income | 0.268*** | 0.416*** |

| (0.028) | (0.089) | |

| male | 0.193*** | 0.062 |

| (0.036) | (0.039) | |

| Living in MSA | -0.090* | -0.040 |

| (0.047) | (0.056) | |

| Ever married | -0.112*** | -0.048 |

| (0.043) | (0.050) | |

| Physical health very good | 0.001 | -0.024 |

| (0.050) | (0.042) | |

| Physical health good | 0.009 | -0.011 |

| (0.053) | (0.043) | |

| Physical health fair | -0.097 | -0.066 |

| (0.071) | (0.060) | |

| Physical health poor | 0.080 | 0.039 |

| (0.155) | (0.126) | |

| Mental health very good | 0.004 | -0.016 |

| (0.043) | (0.043) | |

| Mental health good | -0.031 | -0.029 |

| (0.049) | (0.038) | |

| Mental health fair | -0.009 | -0.041 |

| (0.095) | (0.067) | |

| Mental health poor | 0.135 | 0.113 |

| (0.287) | (0.399) | |

| Days for sick leave (T32) | 0.119*** | 0.094*** |

| (0.020) | (0.025) | |

| Days for sick leave (T34) | 0.113*** | 0.113 |

| (0.019) | (N/A) | |

| Number of employees | 0.228*** | 0.231** |

| (0.020) | (0.116) | |

| Firm has multiple locations | 0.374*** | 0.173*** |

| (0.034) | (0.067) | |

| Region and Race Dummies | Yes | Yes |

| Number of Observations | 7,555 | 7,555 |

| Standard errors in parentheses, * , ** , *** . | ||

-

•

indicates that the variable is standardized.

-

•

The coefficient on T34 in the semiparametric model is fixed for normalization.

-

•

Gaussian copula is used.

| Parametric | Semiparametric | |

|---|---|---|

| Treatment () | 0.493*** | 0.368** |

| (0.168) | (0.183) | |

| age | 0.055*** | 0.059 |

| (0.020) | (0.047) | |

| years of education | 0.142*** | 0.126* |

| (0.028) | (0.066) | |

| family size | -0.055*** | -0.052* |

| (0.021) | (0.030) | |

| income | 0.018 | 0.031 |

| (0.026) | (0.068) | |

| male | -0.398*** | -0.373** |

| (0.037) | (0.169) | |

| Living in MSA | 0.063 | 0.040 |

| (0.052) | (0.061) | |

| Ever married | 0.188*** | 0.179** |

| (0.049) | (0.084) | |

| Physical health very good | 0.227*** | 0.201** |

| (0.056) | (0.084) | |

| Physical health good | 0.395*** | 0.356*** |

| (0.059) | (0.130) | |

| Physical health fair | 0.691*** | 0.644*** |

| (0.077) | (0.224) | |

| Physical health poor | 0.978*** | 0.959* |

| (0.163) | (0.492) | |

| Mental health very good | -0.033 | -0.040 |

| (0.048) | (0.057) | |

| Mental health good | -0.066 | -0.064 |

| (0.053) | (0.064) | |

| Mental health fair | 0.042 | 0.053 |

| (0.105) | (0.154) | |

| Mental health poor | 0.300 | 0.186 |

| (0.297) | (0.320) | |

| Days for sick leave (T32) | -0.026 | -0.023 |

| (0.026) | (0.027) | |

| Days for sick leave (T34) | -0.049** | -0.049 |

| (0.025) | (N/A) | |

| Region and Race Dummies | Yes | Yes |

| Number of Observations | 7,555 | 7,555 |

| Standard errors in parentheses, * , ** , *** . | ||

-

•

indicates that the variable is standardized.

-

•

The coefficient on T34 in the semiparametric model is fixed for normalization.

-

•

Gaussian copula is used.

| Parametric | Semiparametric | |

|---|---|---|

| ATE at the mean | 0.114*** | 0.100** |

| (0.037) | (0.048) | |

| ATE at 50% quantile | 0.129*** | 0.104* |

| (0.045) | (0.054) | |

| ATE at 25% quantile | 0.121** | 0.104 |

| (0.050) | (0.058) | |

| ATE at 75% quantile | 0.139*** | 0.105* |

| (0.043) | (0.056) | |

| Spearman’s | -0.200** | -0.154 |

| (0.105) | (0.134) | |

| Number of Observations | 7,555 | 7,555 |

| Standard errors in parentheses, * , ** , *** . | ||

Online Appendix

Appendix A Proofs of Results in Section 2

A.1 Proof of Theorem 2.6

Recall

and

where . Again, we want to show that, given which are identified from the reduced-form equation, there are two distinct sets of parameter values and (with ) that generate the same observed fitted probabilities and for all . In showing this, the following lemma is useful:

Lemma A.1.

Assumption 5 implies that, for any and ,

| (A.1) |

The proof of this lemma can be found below.

Now fix . First, consider the fitted probability . Given and , note that, for ,232323The inequality here and other inequalities implied from this (e.g., , and etc.) are assumed only for concreteness. there exists a solution such that

| (A.2) | ||||

| (A.3) | ||||

and note that by Assumption 5 and a variant of Lemma A.1, we have that . Here, and result in the same observed probability . Now consider the fitted probability . Choose . Also let only for simplicity, which is relaxed later. Then there exists a solution such that

| (A.4) | ||||

| (A.5) | ||||

and note that by Assumption 5 and Lemma A.1. Then, by letting , and satisfy . Lastly, note that and , and so and above will also result in the same values of and .

It is tempting to have a parallel argument for , , , and , but there is a complication. Although other parameters are not, and are common in both sets of probabilities. Therefore, we proceed as follows. First, consider . Given and the above choice of , note that there exists a solution such that

| (A.6) | ||||

| (A.7) | ||||

and similarly as before, we have . Here, and result in the same observed probability . Now consider . Recall and . Then there exists a solution such that

| (A.8) | ||||