Inconsistency of diagonal scaling under high-dimensional limit: a replica approach

Abstract

In this note, we claim that diagonal scaling of a sample covariance matrix is asymptotically inconsistent if the ratio of the dimension to the sample size converges to a positive constant, where population is assumed to be Gaussian with a spike covariance model. Our non-rigorous proof relies on the replica method developed in statistical physics. In contrast to similar results known in literature on principal component analysis, the strong inconsistency is not observed. Numerical experiments support the derived formulas.

1 Main results

Let be independent and identically distributed according to the -dimensional Gaussian distribution with mean vector and covariance matrix . Denote the (uncentered) sample covariance matrix by . We assume , which implies that is positive definite with probability one, unless otherwise stated.

Let be the set of positive numbers. By a diagonal scaling theorem established by [7], there exists a unique vector such that

| (1) |

where and . In other words, all row sums of the scaled matrix are unity. Refer to [11] for an application of this fact to a rating method of multivariate quantitative data.

Let be the population counterpart of , which means , . If is fixed and , a standard argument of asymptotic statistics shows that converges almost surely to the true parameter because converges to . However, if is getting large as well as , then the limiting behavior of is not obvious. We are interested in the behavior of if converges to some as .

In principal component analysis, this type of high-dimensional asymptotics is deeply investigated. In particular, the angle between the first eigenvectors of and converges to a non-zero value. Furthermore, the limit becomes if is less than a threshold. We call these phenomena inconsistency and strong inconsistency, respectively. The fact is found by [1, 2] in literature of statistical physics and then mathematically proved by [4, 8, 10].

We obtain similar conclusions for the diagonal-scaling problem, at least numerically, as follows. First consider the simplest case , the identity matrix of order . It is easy to see that for this case. The following claim is derived in Section 2 with the help of the replica method in statistical physics.

Claim 1.

Let . Suppose that converges to some as . Then we have

| (2) |

The right hand side falls within .

The quantity is the cosine of the angle between and , referred to as the cosine similarity. It follows from (2) that the cosine similarity does not converge to and hence is inconsistent. In contrast to principal component analysis, is never strongly inconsistent. This is not a direct consequence of positivity of and . For example, the angle between two positive vectors and in converges to as .

Next consider a spike covariance model given by

| (3) |

where is a positive constant meaning the signal-to-noise ratio. It is easy to see that . The following claim is also derived in Section 2.

Claim 2.

Assume the spike covariance model (3) with . Suppose that converges to some as . Then we have

| (4) |

where is the unique minimizing point of a convex function

| (5) |

and

| (6) |

Let us consider extreme cases , and . As , the quantity expectedly converges to the right hand side of (2). For the other two extreme cases, converges to 1. This consequence is natural since means that the signal is infinitely large compared to the noise, and corresponds to the classical limit. The proof of these statements is given in Appendix B.

As a final remark, we consider what happens if . In this case, the equation (1) may not have a solution, depending on . If , a result of geometric probability [3, 13] implies that (1) admits a solution with probability

| (7) |

See Appendix C for more details. As , the probability converges to 0 if and 1 if . This may be seen as a phase transition phenomenon.

The rest of the paper is as follows. In Section 2, we derive the two claims using the replica method. In Section 3, we perform numerical experiments for validating the formulas as well as studying the cases that is not a spike covariance model. Section 4 concludes with open problems. Proofs are given in Appendices.

2 Non-rigorous proof based on the replica method

We derive the claims stated in the preceding section using the replica method. We will put the replica symmetry assumption and exchange integral and limits without justification. The outline is similar to the case of principal component analysis (e.g. Chapter 3 of [12]).

2.1 The saddle point equation

Let be the solution of (1). Then is the unique minimizer of a strictly convex function

| (8) |

We call the Hamiltonian. Define the partition function by

The free energy density is defined by

In order to obtain the macroscopic variables appearing in Claim 1 and 2, we calculate

| (9) |

where denotes the expectation with respect to .

The replica method first calculates for positive integers and then formally applies an identity

| (10) |

as if is a real number. We will also put the replica symmetry assumption and exchange integration and limits without justification.

In the following, we assume the spike covariance model (3) including the case . We use abbreviation for vectors . Recall that as .

Proof of all lemmas is given in Appendix A.

Lemma 1.

Let be a positive integer. Then we have

| (11) |

where ,

| (12) |

and the function is defined by

| (13) |

The quantities in Eq. (12) are macroscopic variables of interest. By applying the Fourier inversion and saddle point approximation to (11), we obtain the following lemma.

Lemma 2.

Let be a positive integer. Then we have

| (14) |

up to an additional constant, where

| (15) |

and is given in (13) after is replaced with .

Since the optimization problem (14) is not easy to solve, we put the replica symmetry assumption: suppose that the extremal point satisfies

where , and

where . Under these assumptions, the optimal is also written as .

Lemma 3.

Under the replica symmetry, we have

and

where is the unique positive root of the quadratic equation

| (16) |

Our goal is to calculate in (9). Using the replica trick (10) and exchanging limits, we have

We scale the variables as

according to [12]. Then the free variables are and .

After some calculation, we obtain the following equation. See Appendix for details.

Lemma 4.

Under the assumptions mentioned above, we have

Furthermore, we formally exchange the supremum and infimum, and then rescale the variables as

| (17) |

Then

Denote the objective function by

Finally, the stationary conditions are

| (18) | ||||

| (19) | ||||

| (20) | ||||

| (21) |

2.2 Derivation of Claim 1 and Claim 2

First, assume . Then it is immediate from (19), (18), (21) and (20) in this order that

Hence we obtain

This implies Claim 1.

Next, consider the case . By Eq. (18),

Substituting it to (19) yields

| (22) |

Therefore is written in terms of as

| (23) |

From Eq. (21), we have

and

| (24) |

Now we obtain the expression of in terms of . Finally, substitute them into to obtain

This function is well defined and strictly convex whenever and since a function is convex if . The minimizer of exists since as and .

Now Claim 2 follows.

3 Numerical experiments

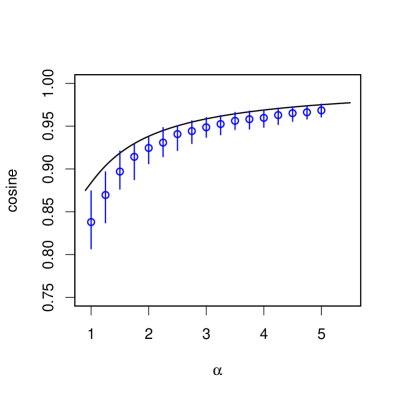

We numerically compute the cosine similarity between and under various conditions. Denote the ratio by for simplicity.

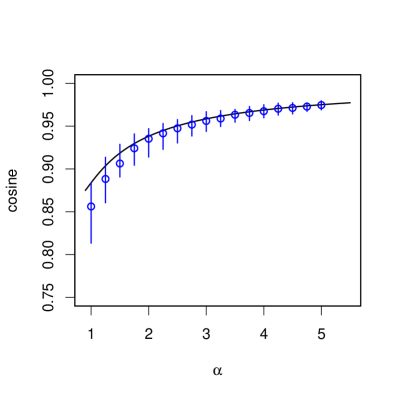

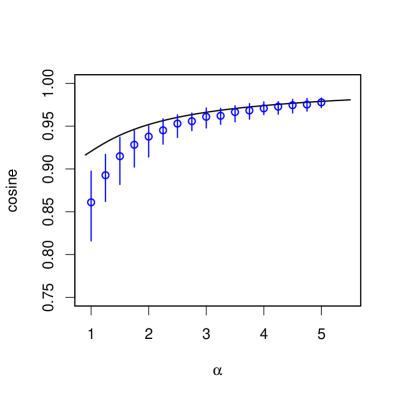

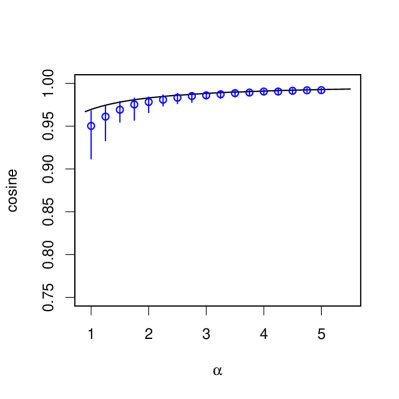

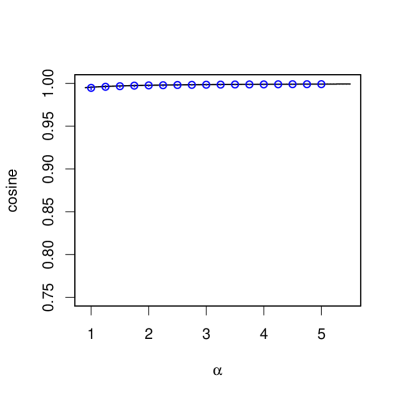

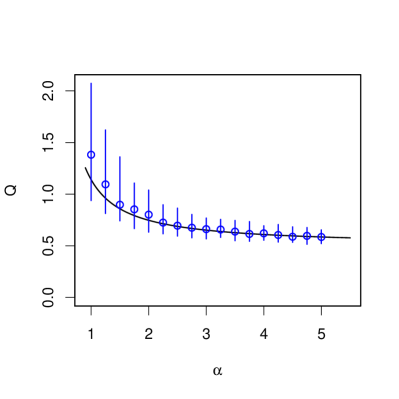

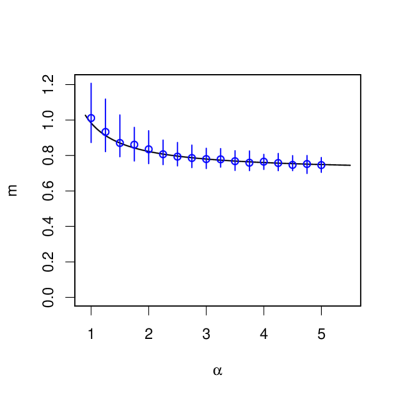

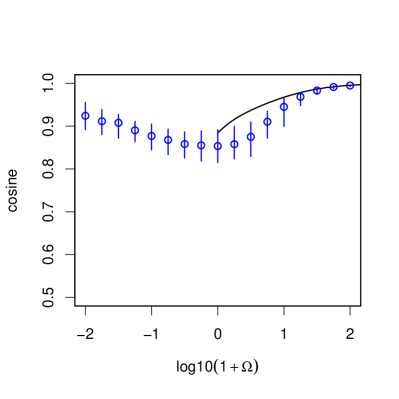

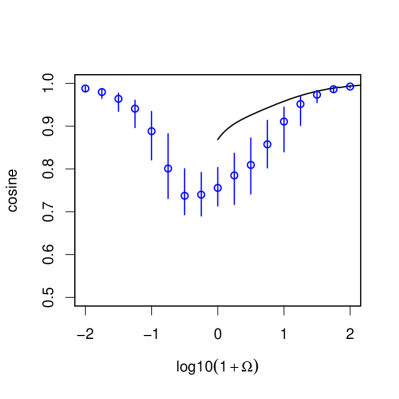

Figure 1 shows the -profile of the cosine similarity under the Gaussian spike model (3) for and . The number of simulation is 100 for each set of parameters. Although we see that the simulated values are close to the theoretical curve, there are some gaps for small if and . The gap is not so large if we focus on the other macroscopic variables and . See Figure 2. Note that the cosine similarity is equal to .

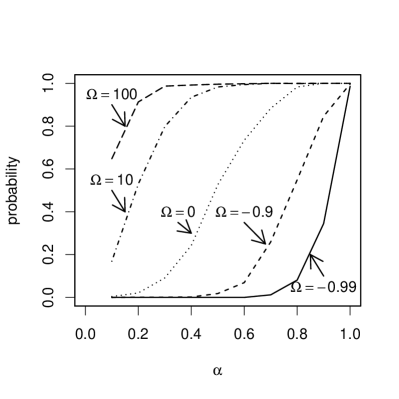

We assumed at the beginning of the paper to make the sample covariance matrix positive definite. However, the equation (1) can admit a solution even if is not positive definite. In fact, the solution exists if and only if is strictly copositive [7], meaning that for any non-negative vector . Figure 3 shows the probability that is strictly copositive for various and . Note that the spike covariance model (3) is positive definite even for . The probability tends to 1 as if is greater than a threshold. The threshold is lower if is larger. If , the result is consistent with the formula (7).

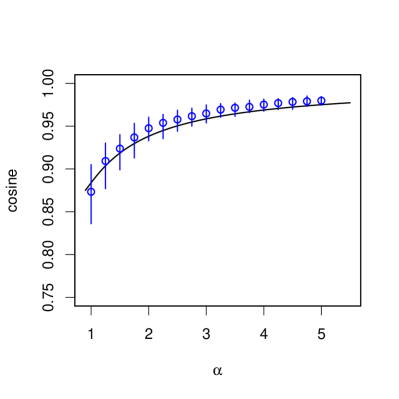

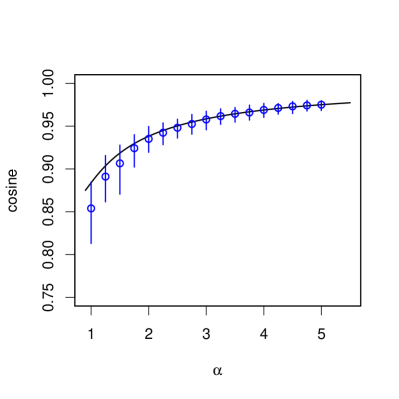

In Figure 4, we plot the cosine similarity as a function of for and . It is observed that the similarity increases as tends to . This phenomenon is expected since the diagonal scaling problem (1) is essentially the same as that of the inverse matrix. More precisely, if solves , then it also satisfies .

We examine other covariance models

| (25) |

where is a fixed matrix with properties and , is a random rotation matrix of order and is a positive vector in given below. Note that becomes the identity matrix if . We define the power-law model by

| (26) |

and the stepwise model by

| (27) |

where the proportional constant is determined to impose . Figure 5 shows the cosine similarity under these models. We generated a random rotation matrix in (25) each time when is sampled. The replica solution (2) for the identity covariance matrix is surprisingly well fitted for the two cases.

Figure 6 shows the cosine similarity when the Gaussian distribution is replaced with the standardized -distribution with 3 degrees of freedom. The similarity is slightly smaller than the Gaussian case but the difference is not drastic.

4 Discussion

In this paper, we analytically and numerically investigated the diagonal scaling problem (1) under the limit . In particular, it is claimed that the angle between the estimated vector and the true vector does not converge to zero. The replica solution fits the numerical experiments except for small , as observed in Figure 1. The difference may be caused by the replica symmetry breaking (e.g. [9]). We have to fill the gap and rigorously prove the claims. It is worth mentioning that the behavior of was relatively stable with respect to change of probabilistic assumptions, as seen in Figure 5 and Figure 6. On the other hand, it may be possible to consistently estimate under some sparsity assumptions, as discussed for principal component analysis in [5].

We could not establish analytical expressions for the cases . The formula in Claim 2 is not extrapolated to the region. Formulas for are needed as well. How to deal with the case of , called the high-dimensional low sample size data, is highly non-trivial for the diagonal scaling problem. Refer to [6, 14] for this direction on principal component analysis.

Finally, although we focused only on convergence of the cosine similarity, the limit distribution of like the Marchenko–Pastur law are also of interest.

Acknowledgments

This study was supported by Kakenhi Grant Numbers JP17K00044 and JP26108003.

References

- [1] Biehl, M. and Mietzner, A. (1993). Statistical mechanics of unsupervised learning, Europhys. Let., 24 (5), 421–426.

- [2] Biehl, M. and Mietzner, A. (1994). Statistical mechanics of unsupervised structure recognition, J. Phys. A: Math. Gen., 27, 1885–1897.

- [3] Cover, T. M. and Efron, B. (1967). Geometrical probability and random points on a hypersphere, Ann. Math. Statist., 38, 213–220.

- [4] Johnstone, I. M. and Lu, A. Y. (2004). Sparse principal components analysis, Technical Report, Stanford University, Dept. of Statistics, arxiv:0901.4392.

- [5] Johnstone, I. M. and Lu, A. Y. (2009). On consistency and sparsity for principal components analysis in high dimensions, J. Amer. Statist. Assoc., 104, 682–703.

- [6] Jung, S. and Marron, J. S. (2009). PCA consistency in high-dimension, low sample size context, Ann. Statist., 37, 4104–4130.

- [7] Marshall, A. W. and Olkin, I. (1968). Scaling of matrices to achieve specified row and column sums. Numer. Math., 12, 83–90.

- [8] Nadler, B. (2008). Finite sample approximation results for principal component analysis: a matrix perturbation approach, Ann. Statist., 36 (6), 2791–2817.

- [9] Nishimori, H. (2001). Statistical Physics of Spin Glasses and Information Processing: An Introduction, Oxford University Press.

- [10] Paul, D. (2007). Asymptotics of sample eigenstructure for a large dimensional spiked covariance model, Statistica Sinica, 17, 1617–1642.

- [11] Sei, T. (2016). An objective general index for multivariate ordered data, J. Multivariate Anal., 147, 247–264.

- [12] Watanabe, S., Nagao, T., Kabashima, Y., Tanaka, T. and Nakajima, S. (2014). Mathematical Science of Random Matrices (in Japanese), Morikita Publishing.

- [13] Wendel, J. G. (1962). A problem in geometric probability, Math. Scandinavica, 11, 109–111.

- [14] Yata, K. and Aoshima, M. (2009). PCA consistency for non-Gaussian data in high-dimension, low sample size context, Comm. Statist. Theory Methods, 38, 2634–2652.

Appendix

Appendix A Proof of lemmas

Proof of Lemma 1.

By definition of the partition function, we have

The simultaneous distribution of is the -dimensional Gaussian distribution with mean zero and covariance matrix

Recall that and . The expectation we need is

Hence

which completes the proof. ∎

Proof of Lemma 2.

We formally use Dirac’s delta function and its Fourier representation, but it will be justified by Schwartz’ distribution theory. Define and as functions of , whereas and denote free variables. Then

where is a constant depending only on and . The innermost integral is

Therefore

Finally, by using the saddle point approximation, we obtain (14) and (15). ∎

Proof of Lemma 3.

Proof of Lemma 4.

Appendix B Limiting behavior as , and

First consider the case for fixed in Claim 2. The objective function in (5) is asymptotically written as

as . Hence the minimizer converges to . The variable is

Next consider the case for fixed . We show that both and converge to 1. Since the objective function is asymptotically

as , the stationary condition is

Solving this equation, we obtain

By (24), we have

Finally, consider the case for fixed . We show and converge to 1. The objective function converges to

The stationary condition is

which has the unique positive solution . Furthermore, .

Appendix C Proof of Eq. (7)

We calculate the probability of the event that is strictly copositive (see Section 3 for the definition). Denote the data matrix by

Then . The following are equivalent to each other.

-

(a)

is strictly copositive

-

(b)

There is not a non-negative non-zero vector such that .

-

(c)

generates a proper convex cone in .

As stated in [3], the probability of the event (c) is given by Eq. (7) if ’s are independent and the distribution of each is symmetric with respect to the origin. This result is due to [13] and related to Schläfli’s theorem, which states that hyperplanes in general position in divide into regions.

|

|

| (a) . | (b) . |

|

|

| (c) . | (d) . |

|

|

|

|

| (a) . | (b) . |

|

|

| (a) . | (b) . |

|

|

| (a) The power-law model. | (b) The stepwise model. |

|