Latent Agents in Networks:

Estimation and Targeting

Baris Ata \AFFUniversity of Chicago, Booth School of Business, \EMAILbaris.ata@chicagobooth.edu \AUTHORAlexandre Belloni \AFFDuke University, The Fuqua School of Business, \EMAILabn5@duke.edu \AUTHOROzan Candogan \AFFUniversity of Chicago, Booth School of Business, \EMAILozan.candogan@chicagobooth.edu

We consider a network of agents. Associated with each agent are her covariate and outcome. Agents influence each other’s outcomes according to a certain connection/influence structure. A subset of the agents participate on a platform, and hence, are observable to it. The rest are not observable to the platform and are called the latent agents. The platform does not know the influence structure of the observable or the latent parts of the network. It only observes the data on past covariates and decisions of the observable agents. Observable agents influence each other both directly and indirectly through the influence they exert on the latent agents.

We investigate how the platform can estimate the dependence of the observable agents’ outcomes on their covariates, taking the latent agents into account. First, we show that this relationship can be succinctly captured by a matrix and provide an algorithm for estimating it under a suitable approximate sparsity condition using historical data of covariates and outcomes for the observable agents. We also obtain convergence rates for the proposed estimator despite the high dimensionality that allows more agents than observations. Second, we show that the approximate sparsity condition holds under the standard conditions used in the literature. Hence, our results apply to a large class of networks. Finally, we apply our results to two practical settings: targeted advertising and promotional pricing. We show that by using the available historical data with our estimator, it is possible to obtain asymptotically optimal advertising/pricing decisions, despite the presence of latent agents.

1 Introduction

Network effects are relevant in many social and economic settings. Recent literature has empirically characterized the strength of these effects in a wide variety of domains ranging from consumption to risk sharing and from education to crime (see, e.g., Calvó-Armengol et al. (2009), Bramoullé et al. (2009), Patacchini and Zenou (2012b), Fletcher (2012), Blume et al. (2015), De Paula (2017), Patacchini et al. (2017), Angelucci et al. (2018), De Giorgi et al. (2020)). A different strand of the literature complemented this line of work by shedding light on how information on the network structure can be used to improve decision making. For instance, motivated by the prevalence of online social networks, Candogan et al. (2012), Belloni et al. (2016), Bimpikis et al. (2016) and Zhou and Chen (2016) have focused on understanding how a seller can use the available social network information to target agents in the social network with improved pricing/seeding/marketing decisions.

The first line of research often assumes that historical data on all of the agents in the network are readily available. The second line of research makes a stronger assumption and assumes that the decision maker fully knows the underlying network/influence structure. These informational assumptions can be too strong in practice. This paper asks the following fundamental questions: (i) How can network effects be estimated in the absence of data on some agents? (ii) How can a decision maker leverage such estimates to improve her targeting decisions?

1.1 Estimating Network Effects in the Presence of Latent Agents

First, we focus on the estimation question. Specifically, Section 2 presents a social network model, where the agents’ outcomes depend linearly on their neighbors’ outcomes, as well as their (agent-specific) covariates. The underlying network is weighted, and the entries of the associated (weighted) adjacency matrix capture how much the outcomes of agents influence each other. Historical data on a subset of the agents, hereafter referred to as observable agents, are available. The remaining agents in the network are called the latent agents. A priori there is no information on the latent agents; e.g., neither their influence on the observable agents, nor the number of latent agents is known. Crucially, the latent agents still influence (and are influenced by) the observable ones. However, influence structure among observable agents is also unknown.

Our first contribution is to provide an algorithm to estimate the relationship between the observable agents’ outcomes and covariates (Section 3). In our model, this relationship is linear and is captured by a matrix which is closely related to the underlying network structure. Specifically, this matrix is a sub-block (corresponding to the observable agents) of the inverse of the matrix given by the difference of a diagonal matrix and the (weighted) adjacency matrix. We investigate how to estimate this matrix, whose th row captures the change in the outcome of agent due to changes in the covariates of this agent and the remaining agents.

Social networks often involve a large number of agents that are sparsely connected.111See, e.g., Ugander et al. (2011), who report that in May 2011, the Facebook graph consisted of 721 million active nodes, and users had on average 190 Facebook friends. Consequently, our problem is a high-dimensional estimation problem. A natural way to deal with this high dimensionality and obtain efficient estimators is to exploit the underlying sparsity. That being said, even when the underlying network is sparse, the aforementioned matrix need not be sparse (since it is given by the inverse of a matrix related to the structure of the network; see Section 3).

We get around this difficulty by using a notion of approximate sparsity for this matrix (see Definition 3.1). Intuitively, this sparsity notion posits that even though the matrix is not sparse, it admits a sparse approximation. Under the approximate sparsity assumption, we provide an estimator for this matrix, and characterize its convergence rates in matrix and -norms. Controlling the estimation errors in both matrix norms is methodologically challenging, but needed in our setting. This is because, for many decision problems where the payoff of the decision maker depends on the underlying network structure, using estimators with small errors in both norms enables constructing near-optimal policies (see the relevant discussion in Section 1.2). Such guarantees are not possible for estimators that control errors only in one or the other norm. From the statistical perspective this amounts to controlling errors not only within each model (that captures the dependence of the outcome of a single agent on all covariates – which is standard) but also across linear models. Achieving this necessitates leveraging a different approximate sparsity condition that encodes sparsity across linear models, and using thresholded estimators after de-biasing. We also provide distributional limits for our estimator that allow for constructing valid confidence intervals.

It is not a priori clear when the aforementioned approximate sparsity condition holds. Our second contribution is to provide conditions on the network structure and edge weights that ensure that this condition is satisfied (Section 5). Using ideas from the theory of banded matrices, approximation theory, spectral theory, and Banach algebras of matrices and their off-diagonal decay properties, we establish that our approximate sparsity assumption holds for large classes of networks under (diagonal dominance) assumptions that are standard in the social networks literature. For such classes of networks, we prove that our estimators yield small approximation errors even when the number of observations scales logarithmically with the number of observable agents, thereby making these estimators suitable for large networks.

1.2 Applications: Improving Targeting Decisions

Our third contribution (Section 4) is to illustrate how the estimation framework can improve targeting decisions of a decision maker. We focus on two applications: targeted advertising and pricing. In both applications, agents consume a divisible product that exhibits positive network externalities. Due to the presence of network externalities, each agent’s consumption decision depends on those of her neighbors in the underlying social network. Hence, an ad shown or a discount offered to an agent impacts the consumption decision of not only this agent, but also those of her neighbors (as well as their neighbors and so on).

A subset of these agents (observable ones) purchase the product from an online seller who offers it through a social networking platform. While the online seller does not know how much agents influence each other, she has historical data on the targeting/consumption decisions for the observable agents. We investigate how this seller should target these agents with ads or discounts to maximize her payoff, which depends on the sales to observable agents.

The targeting question here is partly motivated by firms that offer targeted prices/ads through online social networks. For instance, prominent social networking platforms such as Facebook allow retailers to target individuals who previously shopped with them via ads through their “Custom Audiences” (see, Facebook for Business (2020a)). Moreover, these ads can take the form of “Offer Ads”, where the targeted individuals receive unique promo codes (see Facebook for Business (2020b) and Facebook for Business (2020c)). This type of “custom audience” targeting is not unique to Facebook, and it is common to all major social networking platforms (see, e.g., Instagram Business (2016), Twitter Business (2020)).

Consider the customers who shopped with an online seller in the past (i.e., the “custom audience”). The seller can target them with informative ads (which help increase sales, as in our advertising application) or promo codes (which correspond to price discounts in our pricing application). These individuals correspond to the observable agents in our model. Any agent who is not in the custom audience is latent. These agents can correspond to other participants of the social networking platform, or agents who do not participate in such platforms but still influence others through offline channels.222These cases are mathematically equivalent. For sake of exposition, when we present our results in Section 4, we frame the problem through the latter case. For products that exhibit network externalities (e.g., fashion items), the optimal targeting decisions (advertising intensities and/or discounts involving promo codes) depend on the underlying network structure. This information is not readily available to the online seller. That said, information on whether/how the targeted individuals engage with ads (e.g., whether the individual uses the “unique code” and what they purchase with it – see Facebook for Business (2020c)) is available. In the context of our model, this means that data on past targeting decisions as well as outcomes are available. Note that advertising a product may increase the consumption of observable agents, but it may also increase the latent agents’ incentives to obtain similar products (possibly through alternative channels/sellers) due to the presence of network externalities. The latter effect could in turn incentivize other observable agents to consume more. How should the seller optimize her advertising/pricing decisions for the observable agents?

We show that the seller can use the available historical data to estimate network effects, and construct targeting decisions that would be optimal if the network effects were precisely captured by the estimated quantities. Leveraging the convergence rates of our estimator in matrix and -norms, we show that the constructed targeting decisions are asymptotically optimal in the sense that the ratio of the payoff under these to the optimal payoff that would be achieved if the seller knew the underlying influence structure, converges to one as the number of samples increases. Once again, we show that if the number of observations is at least logarithmic in the number of observable agents, then a small payoff gap can be guaranteed and we provide a precise characterization of this gap in terms of a measure of approximate sparsity. These results indicate that even with the limited amount of available data, the seller can exploit approximate sparsity to construct targeting decisions that are near-optimal.

To the best of our knowledge, the proposed network setting with latent agents is new. Collectively, our results shed light on how in such settings the mapping between the covariates and outcomes of the observable agents can be estimated, and how such estimates can be used to construct approximately optimal targeting decisions.

1.3 Related Literature

Our paper is closely related to the literature on identification and estimation of network effects, and targeting. The application we cover in Section 4.2 also relates to the pricing literature.

Identification and estimation of peer effects:

There is a growing body of literature on identification and estimation of peer effects, where it is often assumed that observations on outcomes and covariates of all agents are available (e.g., Sacerdote 2001, Calvó-Armengol et al. 2009, Epple and Romano 2011). The canonical model is the linear specification presented in Manski (1993), which is similar to the one considered in the present paper (although Manski (1993) considers additional covariates). Manski (1993) points out an identification issue for the estimation of peer effects (the reflection problem): it is not possible to disentangle the endogenous effects (which are given by the average decisions of individuals in a group) and the exogenous (contextual) effects (which are given by the average of the covariates of individuals in the group). Bramoullé et al. (2009) and Blume et al. (2015) show that when the underlying network lacks a regular structure this identification problem disappears. In the present paper, we assume that an agent’s outcome is impacted by the outcomes of her neighbors rather than their covariates. Hence, the exogenous effects do not play a role, and the aforementioned identification issue is not relevant.

Manresa (2013) and Rose (2017) consider the identification and estimation of peer effects when the network is sparse. These papers rely on panel data, and leverage lasso or instrumental variable approaches (e.g., due to Gautier and Tsybakov 2014) to the estimation problem. A relevant recent survey of De Paula et al. (2015) discusses the estimation of the network structure via penalization methods like lasso, SCAD, and others. In the presence of latent agents the underlying aggregate influence structure among observable agents is no longer sparse (see Section 3). Moreover, as opposed to estimating the influence structure, our focus is on estimating the inverse of a matrix related to it (which also is not sparse). Hence, the results from this line of literature are not readily applicable. It is also worth mentioning that the methodology in these papers can be used to obtain estimators that yield small estimation errors for each row of the matrices of interest. However, in this paper our estimator yields small estimation errors simultaneously for both rows and columns, which is essential for ensuring asymptotic optimality in the subsequent decision problems.

Decision making with incomplete network information:

A relevant stream of the social networks literature assumes that as opposed to knowing the precise network structure, a decision maker has access to some summary statistics about the network; e.g., she knows the degree distribution in the network, which partially reflects the extent of externalities. In such a setting, each agent’s degree might be modeled as her private information and the decision maker’s challenge is to elicit the relevant information and decide on how to optimally target agents using this information. The literature provides various mechanisms for eliciting agents’ private information and optimizing targeting decisions in the context of pricing, advertising, or product referrals (e.g., Hartline et al. 2008, Campbell 2013, Galeotti et al. 2010, Lobel et al. 2015, Zhang and Chen 2016). By contrast, we assume that past data on individual outcomes are available for some (observable) agents, and shed light on how the available data can be employed to better understand the underlying influence structure and improve targeting decisions.

Learning and pricing problems:

There is also a related literature on the question of learning optimal prices through dynamic price experimentation, which is of interest even in the absence of social interactions (e.g., Harrison et al. 2012, Keskin and Zeevi 2014, Besbes and Zeevi 2015). This literature assumes that a parameter of the underlying demand system is unknown, and develops price experimentation policies that do not have a large performance gap relative to the optimal policy derived in a setting where the underlying demand system is fully known. Similarly, in our application in Section 4.2 the demand system is not fully known, since the underlying network is not known. On the other hand, due to network externalities, the seller now finds it optimal to price differentiate agents. Thus, the seller needs to learn an optimal price vector as opposed to a single price, which leads to a more complex learning problem. Although it is beyond the scope of the present work, it would be interesting to study how this dynamic price experimentation can be done in a way that minimizes the long-run performance gap in the seller’s profits measured over the entire experimentation horizon.

2 Model and Preliminaries

We consider a social network with a set of agents and a set of connections among agents . We represent the social network with a directed graph , where and respectively correspond to nodes and edges. In the social network, the set of agents who are connected to agent are referred to as the neighbors of , denoted by .

Each agent is associated with an outcome (), which linearly depends on an agent-specific covariate () as well as the outcomes of her neighbors. Specifically, we denote the outcome of agent at time by

| (1) |

Here is an agent-specific intercept term, and denotes an (idiosyncratic) shock for agent at time , which impacts her outcome but is not observable to the researcher. The term denotes an agent-specific scaling factor (which will be set equal to in one of our applications, and its effect will be estimated in the other one; see Section 4). We assume that have zero mean, and are independent over time, but are possibly correlated across agents. Each edge is associated with a weight that captures how much the outcome of influences that of agent ( if agents and are not connected, i.e., ). Unless otherwise noted, we do not require the weights to be symmetric; i.e., in general . Intuitively this allows an agent to influence her neighbors more than she is influenced by them. Until Section 4, we also allow the weights to be positive or negative. We refer to the set of weights as the influence structure in .

We assume that a subset of the agents participate in an online platform. These correspond to the observable agents in our model, and we assume that data on past covariates and outcomes of these agents are available. By contrast, no such information about the remaining (latent) agents is available. We denote the set of latent agents by , and assume that and .

For a given set of parameters , we denote the associated column vector by , e.g., respectively stand for , , and . For any vector , we represent its entries corresponding to observable and latent nodes by and respectively, i.e., .333For any column vectors , we denote by the column concatenation, and by the row concatenation if they are the same size. We similarly denote row/column concatenation for matrices. Similarly, for any matrix , we express the blocks corresponding to observable and latent components as follows:

We denote by the th row of , by its th column. We use to denote a vector of ones.

In our applications in Section 4, the covariates associated with the latent agents are identical and constant over time (e.g., as they represent the advertising intensity/price discounts through the online platform; which are equal to zero for the agents that are not on the platform). Motivated by this, and to simplify the exposition, we let for all and , where is a constant. We emphasize that our estimation results hold under weaker conditions (e.g. it suffices to have, ). We revisit this point in Remark 3.7.

Let denote a diagonal matrix whose th diagonal entry is given by , and let denote a matrix whose th entry is . Let be such that

Throughout the paper we index the entries of matrices and (as well as other network-related matrices) by the nodes of the underlying network.

Using matrix notation, and rearranging terms in (1), we obtain the following relationship among the outcomes and covariates:

| (2) |

We next focus on observable agents and restate this relationship more explicitly for these agents. To this end, we introduce the following matrices:

| (3) |

and also the following vectors:

| (4) |

Lemma 2.1

In period , the observable agents’ outcomes are given by

| (5) |

The preceding discussion implicitly assumes the invertability of , its sub-block , as well as . This is a mild condition that will be imposed in the remainder of our analysis. We also assume that the maximum absolute row and column sums of (equivalently the and norms of this matrix) are bounded. It is worth noting that in our applications, we will focus on settings where satisfies some diagonal dominance condition (see Assumption 4), which readily implies all of these assumptions (see Section 4 and Lemmas LABEL:lem:MInv, LABEL:lem:matBounds). Finally, we conduct our analysis under the assumption that the parameters as well as the covariates are bounded, i.e., , , and for all and , and some constants .

Lemma 2.1 suggests that the entries of capture how changes in the covariates of the observable agents impact their outcomes. Intuitively, the components and of , respectively represent the direct influence of observable agents’ outcomes on each other and their indirect influence through the latent agents. We refer to as the aggregate externality structure among observable agents.

In our applications in Section 4, the covariates will correspond to prices offered for a product that exhibits network externatilites or advertising intensity for this product; and the outcome will capture the agents’ purchase quantities. We will investigate how the decision maker should set these covariates to maximize an objective of interest, e.g., expected revenues or sales. Lemma 2.1 suggests that knowing is critical for deciding how to target observable agents so as to maximize the aforementioned objectives. We will focus on a setting where the decision maker does not know , but has historical information on the past covariates and outcomes. The crucial questions are whether using the aforementioned data the matrix can be estimated and whether any such estimates can be used for improving pricing/advertising decisions.

Linear models have a long history of facilitating empirical research in various fields. As such, linear models similar to (1) are prevalent in the network estimation literature. Topa and Zenou (2015) provides an overview of research on social networks and their role in shaping behavior and economic outcomes. In particular, the authors discuss local-aggregate and local-average network models, which have a similar structure to ours and assume that the outcome of each agent depends linearly on the outcomes of other agents as well as some covariates. The difference between these model is in the specification of edge weights. The first class of models assume that all edges have identical weights, whereas the second one scales down the edge weights adjacent to each node by the degree of that node. Our model allows for more general influence weights among agents than identical weights or degree-scaled weights. Topa and Zenou (2015) summarizes various papers that use these models and highlight applications in education Calvó-Armengol et al. (2009), De Giorgi et al. (2010), Lin (2010), Bifulco et al. (2011), Boucher et al. (2014), Patacchini et al. (2017), crime Patacchini and Zenou (2012b), Liu et al. (2012), Lindquist and Zenou (2014), labor Patacchini and Zenou (2012a), consumption De Giorgi et al. (2020), smoking Fletcher (2010), Bisin et al. (2011), alcohol consumption Fletcher (2012), and risk sharing Angelucci et al. (2018). More recent applications of these models in other domains, e.g., R&D networks, have also appeared in the literature (e.g., see König et al. (2019)). De Paula (2017) also highlights the prevalence of linear models and argues that “The canonical representation for the joint determination of outcomes mediated by social interactions builds on the linear specification”.

This literature has largely assumed away the presence of latent agents, despite their prevalence in network data. The next section provides a framework for estimating network effects (summarized through the matrix) in the presence of latent agents, by focusing on the linear model in (1). In doing so, we assume that aside from past covariates/outcomes of observable agents, no additional information is available. In particular, we do not assume the knowledge of the underlying network structure (or the parameters), the set of latent agents (or its cardinality), parameters , or taste shocks .

Remark 2.2 (Identification issues)

Observe that in the absence of latent agents , and hence its estimate readily reveals the dependence of outcomes on covariates (by (2)). However, when there are latent agents it is not possible to identify , and hence we restrict attention to estimation of . To see this, consider a network with latent agents, where the mapping between outcomes and covariates is as in Lemma 2.1. Note that another network, which has no latent agents and admits an influence structure for for all observable agents, exhibits the same relationship between covariates and outcomes. Thus, either network could explain covariate/outcome observations, and it is not possible to identify the true matrix.

3 An Estimator for Large Networks

This section focuses on the estimation of the matrix from panel data on the observable agents, , where . We are particularly interested in large networks, where the number of observable agents can exceed the number of periods observed in the data. The linear specification in Lemma 2.1 can be exploited for the estimation of provided that covariates and taste shocks (similarly ) are orthogonal. That is,

| (6) |

To estimate the coefficients of interest (and in particular, the entries of and ) we use the moment condition (6) with an -regularization procedure (which results in a variant of the Dantzig selector; see Candès and Tao (2007), Belloni et al. (2017b)). The use of the -penalty is often motivated by big data applications where underlying models involve many different variables, yet the available sample size is substantially smaller. Estimation in such settings becomes possible only if a relatively small number of variables matter, i.e., if the underlying coefficient vector is sparse. Employing -penalty guarantees the sparsity of the estimator, and allows for estimating the relevant coefficients.

The number of entries of the matrix is large ( – and hence scales quadratically with the number of observable agents), which naturally results in a high-dimensional estimation setting. Yet, this matrix is not necessarily sparse even if the underlying influence structure is sparse (i.e., has a small number of nonzero entries). In fact, as we establish in Lemma LABEL:lem:MInv of Appendix 14.1, if the network is (strongly) connected (and satisfies an additional assumption imposed in our applications), then all entries of as well as are nonzero. There are two effects that contribute to this nonsparsity. First, even if the underlying influence matrix is sparse, the related matrices obtained after a matrix inversion operation (such as as well as ) are not sparse. Second, in the presence of latent agents, the aggregate externality structure is not sparse (due to the term ).

To tackle this issue, in Section 3.1, we introduce an “approximate sparsity” condition on . In Section 3.2, we provide our estimation algorithm for , and in Section 3.3, we obtain rates of convergence for our algorithm under the approximate sparsity condition. We revisit this condition in Section 5 and establish that it holds for a large class of networks and influence structures. Hence, the results of this section are applicable to those general settings.

To facilitate the analysis, we next introduce additional notation. We use to denote the cumulative density function of the standard normal distribution. We define , and index the entries of vectors in and by the elements of and respectively. For instance, is equal to if , and is equal to otherwise, where . We denote by with an indicator variable that takes the value one if and zero otherwise. We denote by (for ) the norm of a vector , i.e., (with the convention ). Similarly, for a matrix , denotes the induced matrix -norm, i.e., . Observe that for we get the maximum absolute row sum (), and for we get the maximum absolute column sum () of the relevant matrix.

3.1 Approximate Sparsity

Before we proceed with the details of our estimation approach, we formalize our approximate sparsity notion.

Definition 3.1

We say that a matrix is -sparse if it has at most nonzero entries in each row and column. Moreover, we say that the matrix admits an -sparse approximation if there exists an -sparse matrix such that

Motivated by Definition 3.1, we say that a network admits an -sparse approximation if the associated matrix does so. A given network can admit different sparse approximations with different parameters . There is a clear trade-off between such approximations: more sparse approximations will lead to higher approximation errors. To achieve the best tradeoff in the estimation, it may be appropriate to consider less/more sparse approximations (i.e., larger/smaller ) depending on the number of available observations. In what follows, we focus on -sparse approximation of networks, when there are observations . We provide the convergence rates of our estimator (in various norms) in terms of and .

3.2 The Estimation Algorithm

-

Input. The data and the thresholds .

-

Initialize. , , and .

-

Step 1. Compute an initial estimate by solving the following optimization problem:

(7) -

Step 2. For the design matrix , compute a debiasing matrix by solving

(8) -

Step 3. Compute

(9) -

Step 4. Compute the thresholded estimator

Terminate and return , respectively as the estimates of and .

Our estimator is presented in Algorithm 1. This algorithm builds on different ideas in the high-dimensional statistics literature. It can be viewed as a thresholded bias-corrected Dantzig selector estimator whose penalty parameter is pivotal.444That is, it does not depend on unknown quantities such as the variance of the noise. Under (approximate) sparsity assumptions, high-dimensional models are estimable with the introduction of regularization (in this case the -penalty). However, the regularization requires carefully setting penalty parameters and typically yields estimators that are consistent but not asymptotically normal. Algorithm 1 addresses both issues through the use of self-normalized moderate deviation theory.

Step 1 of the algorithm obtains a preliminary estimate of based on a pivotal version of the Dantzig selector estimator; see Candès and Tao (2007), Bickel et al. (2009), Belloni et al. (2017b). This preliminary estimate is not necessarily asymptotically normal, which necessitates the subsequent debiasing step (Step 3).

Step 2 of the algorithm solves an auxiliary regularized estimation problem (again with pivotal choices of the penalty parameter) to compute a pseudo-inverse of the (empirical) covariance matrix (which is rank-deficient due to the high dimensionality). The variant used in Algorithm 1 is similar to the formulations in Javanmard and Montanari (2014) and Zhu and Bradic (2016) but involves significant differences. First, in addition to handling the network setting, the specific form of (8) used here is new. Notably, the optimization formulation in (8) is always feasible (unlike the corresponding problem in Javanmard and Montanari (2014)). Second, it exploits self-normalization to achieve pivotal choices of the penalty parameter . Third, we use a new objective function and minimize a function of the average (empirical) fourth moment of . Leveraging the optimality of in (8), this novel criterion leads to bounds on the higher order empirical moments of , where . As we shall see in the next section, such bounds in turn allow us to achieve desired rates of convergence for a rich class of data-generating processes where it is not required for (i) shocks to be Gaussian, and (ii) to converge to .555It is worth pointing out that if is known, then its inverse can readily be used in place of thereby simplifying the estimator. Our estimator works even in the absence of this information.

Step 3 uses the pseudo-inverse of computed in Step 2 to reduce the bias in the preliminary estimator obtained in Step 1, and leads to the debiased estimator . (This can be seen as a Newton step from .) In the high-dimensional case such ideas have recently been used by different authors with different variants and assumptions; see, e.g., Belloni et al. (2014), Zhang and Zhang (2014), Van de Geer et al. (2014), Javanmard and Montanari (2014), Belloni et al. (2015a). Similar ideas can be traced back to Neyman and Scott (1965) and Neyman (1979) in the fixed dimensional case with the use of the so-called orthogonal moment conditions to reduce the impact of estimation errors of nuisance parameters.

Finally, Step 4 thresholds the intermediate estimator to obtain . The motivation to consider such a thresholded estimator is somewhat subtle, and has to do with the convergence rates that can be obtained by different estimators. Intuitively, our approximate sparsity notion encodes sparsity across a collection of linear models (each of which captures the dependence of the outcome of a single agent on the covariates). It turns out that under such sparsity assumptions (and an appropriate choice of thresholds), the thresholded estimator enjoys good rates of convergence for both the rows and columns of (see Theorem 3.2), thereby allowing us to control errors not only within each model (rows of ), but also across models (columns of ). This, in turn, ensures consistency of the estimates in the matrix -norm. Such guarantees do not hold for the intermediate estimators obtained in Algorithm 1. For instance, it can be seen that Step 1 of the proposed Algorithm 1, as well as the lasso estimator and its variants, decouple over the rows of , and they can be used to obtain convergence rates for the estimation of rows of . However, since is not necessarily symmetric, in the high-dimensional setting we consider, such estimates do not provide meaningful guarantees for column estimates of . Similarly, it can be shown that the estimator obtained in Step 3 has good rates of convergence in the maximum entry-wise error but it need not be a consistent estimator of in matrix -norm (or the -norm).

The importance of achieving good rates of convergence for both the rows and columns is justified in Section 4. In that section, we show that in decision problems where the payoff of the decision maker naturally depends on the network structure, the optimal decisions and payoffs depend both on and . Thus, controlling the estimation errors for both the rows and columns of is important for constructing approximately (and asymptotically) optimal decisions. Indeed, we leverage our approach and bounds on row and column errors to obtain asymptotically optimal targeting decisions for the applications studied in Section 4.

3.3 Convergence Rates

In order to provide the convergence rates of our algorithm, we require the underlying covariate and error processes to be “well-behaved.” In particular, we impose the following assumption: {assumption} Suppose that the network admits an -sparse approximation. Let be constants such that , and let be parameters satisfying . The following conditions hold:

-

i.

The observed data are i.i.d. random vectors that satisfy (5). Moreover, the shock term satisfies for every .

-

ii.

For every we have , , .

-

iii.

The matrix is such that

Moreover, . Finally, we assume that the eigenvalues of are upper bounded by a constant.

-

iv.

We have , , and .

Assumption 3.3i. states that the shock term is a zero mean conditional on the covariates in period . Assumptions 3.3ii. and iii. are mild moment conditions on the shocks and covariates. For example, conditional on covariates, we require the shocks’ fourth moments to be bounded from above, and their second moments to be bounded from below. Similarly, the eigenvalues of matrices constructed from expectations of outerproducts of covariate vectors are well-behaved. Such moment conditions readily hold for sub-Gaussian and subexponential distributions as well as more heavy-tailed distributions. These assumptions are commonly employed in high-dimensional statistics, with a general covariate/observation structure, and are adapted to our setting (see, e.g., Bickel et al. (2009), Belloni et al. (2017b, a)). Assumption 3.3iv. imposes requirements on how the number of agents and the sample size can relate. In particular, we allow for a high-dimensional setting where .

We proceed with our first result on the estimator provided in Algorithm 1.

Theorem 3.2

Under Assumption 3.3 with probability at least the following statements hold:

-

i.

Uniformly over we have

where .

-

ii.

If and for all , then the thresholded estimator satisfies

for some constants .

The first part of Theorem 3.2 provides an (approximate) linear representation of the (intermediate) estimator of Step 3. With high probability the estimation error is a zero-mean term plus an approximation error , which vanishes provided that (since by Assumption 3.3). This result is key to establishing the relevant rates of convergence (Theorem 3.3 below) and also a distributional limit that allows the construction of valid confidence intervals (Theorem 12.1 in the Appendix). Therefore we will build substantially on Theorem 3.2i. in what follows.

The second part of Theorem 3.2 pertains to the thresholded estimator. It states that if the thresholds are chosen to be sufficiently larger than the entry-wise estimation errors (at the end of Step 3), the thresholded estimator will achieve good rates of convergence both for the rows and for the columns of . To see why the thresholded estimator enjoys good rates of convergence, first observe that Assumption 3.3 guarantees that can be approximated well with a matrix that has a small number of nonzero entries in each row/column. Fix a row, and let denote the entries in this row that take nonzero values in this approximation. Suppose thresholds that satisfy the conditions of the theorem are available, and consider the errors the thresholded estimator makes in the entries that belong to vs. . Since has small cardinality, it can be shown that the absolute sum of the errors for the elements in cannot be large. Similarly, due to approximate sparsity, many entries of that belong to are already small. Thus, the definition of the threshold implies that only a small fraction of the corresponding entries of are above the threshold, and the total error the thresholded estimator incurs for these entries is also small. The remaining entries in are below the threshold, and take the value of zero in the thresholded estimator. Approximate sparsity ensures that the corresponding entries of are also small, and hence the total error due to these entries is small. These observations can be leveraged to uniformly bound the -norm error in each row of . A similar argument also bounds the errors in the columns of , and combining these the desirable convergence rates in the theorem, in terms of matrix and norms, can be obtained. Without thresholding, the last error component would in general be large, and it would not be possible to provide similar guarantees in these matrix norms.

Of course, the choice of thresholds is key for this result. We deliberately state the second part of Theorem 3.2 to allow for different choices of thresholds. A particular choice of can be obtained using analytic bounds, based on self-normalized moderate deviation theory, that are slightly conservative but computationally trivial, or using a bootstrap procedure that exploits the correlation structure and still allows for , but is computationally more demanding and requires stronger conditions. For concreteness we provide the results based on the self-normalization ideas in Theorem 3.3 and refer the interested reader to Theorem 12.1 in the Appendix for the result associated with the bootstrap procedure. Theorem 3.3 is based on the following thresholds:

| (10) |

where .

Theorem 3.3

Suppose that Assumption 3.3 holds. Then, with probability at least the intermediate estimator based on Algorithm 1 satisfies

for some constant . Moreover, suppose that . Then the thresholds in (10), with probability at least , yield

| (11) |

for some constant . Finally, with probability the thresholded estimator based on these thresholds satisfies

| (12) |

| (13) |

for some constant .

Theorem 3.3 implies that Algorithm 1 provides consistent estimates of the entries of , uniformly over all entries. Having estimates of the entries of is valuable for understanding the impact of the covariate of an agent on another agent’s outcome (accounting for the network externalities through latent agents). Moreover, under the approximate sparsity assumptions that imply that (see Section 5), Theorem 3.3 also shows that there is a suitable choice of thresholding parameters that allows for the estimator to have desirable rates of convergence for the rows and columns. The proposed thresholds are derived using self-normalized moderate deviation theory. This allows us to handle non-Gaussian shocks as well as the high dimensionality of the estimand matrix.

Remark 3.4 (Bootstrap-based thresholds)

Theorem 3.3 constructs thresholds using self-normalized moderate deviation theory and the union bound, i.e., a Bonferroni correction. In some cases this could be conservative and it is of interest to pursue a less conservative choice. To accomplish this one needs to account for the correlation structure. Under stronger regularity conditions, this can be done through the use of a multiplier bootstrap procedure conditional on the data. In particular, for each define

where , are i.i.d. standard normal random variables independent of the data. The associated critical value we are interested in is

which can be computed by simulation (by redrawing the Gaussian multipliers). Then the thresholds can be set . Such a bootstrap procedure also leads to the construction of simultaneous confidence intervals. We refer the interested reader to Section 12 in the Appendix for a more detailed discussion. In this appendix, using recent central limit theorems for high-dimensional vectors (where is allowed; see, e.g., Chernozhukov et al. (2014b, 2013a)), the validity of this procedure is established. \Halmos

Remark 3.5 (Time dependence)

In this work we focus on the impact of latent agents on the remaining agents and throughout the paper we assume i.i.d. observations. The key technical tools we rely on, namely, self-normalized moderate deviation theory and high-dimensional central limit theorems, have been derived under this assumption. However, recent works have been generalizing these tools to allow for time dependence as well; see Chen et al. (2016) for results of self-normalized moderate deviation theory and Chernozhukov et al. (2013b), Zhang and Cheng (2014), Zhang et al. (2017), Belloni and Oliveira (2018) for high-dimensional central limit theorems under various types of dependence. Therefore it is plausible that most of these tools can be extended to allow for time dependence under more stringent conditions both on the moments and on the growth of and relative to . Although it is beyond the scope of the present work we view this endeavor as a potentially interesting future research direction. \Halmos

Remark 3.6 (Handling endogeneity)

In some applications it is of interest to also allow for endogenous covariates, i.e., . In such cases it is well known that the moment condition (6) no longer holds and in turn the proposed procedure does not lead to consistent estimates of the matrix . Nonetheless the tools proposed here can still be useful when suitable instrumental variables are available; i.e., for each , we observe a random vector such that and is full rank and well-behaved. These instruments yield a similar moment condition

| (14) |

and Algorithm 1 can be adjusted accordingly. This generalization is of interest as it allows for covering a different set of applications. However, its analysis poses interesting technical challenges. The analysis of that new estimator would combine the analysis developed here and the analysis of high-dimensional linear instrumental variables developed in Belloni et al. (2017a). This is being pursued in a companion work Ata et al. (2020). \Halmos

Remark 3.7 (Variation in Covariates for Latent Agents)

In this paper, we consider the case in which the covariates that the latent agents are exposed to are fixed. As discussed in Section 4, this is natural in the advertising/pricing applications we focus on. That said, our results could be obtained under weaker conditions. Specifically, suppose that the covariates of the latent agents evolve with respect to a stochastic process . Then, we can use a similar characterization to Lemma 2.1 to express observable agents’ outcome as , where (analogous to (4)) and

An inspection of the proofs reveals that it suffices to have for the arguments (and the results of this section) to go through (after replacing with ). For example, this is achieved if the variation in is introduced in a randomized experiment, which is possible in many online platforms. In observational studies, additional considerations may be needed to justify this condition, since it imposes a restriction on the relation between and , e.g., . When such a condition does not hold, it becomes a source of endogeneity, in which case the comments in Remark 3.6 become relevant. \Halmos

4 Applications

In this section, we study applications of our estimation framework to targeted advertising (Section 4.1) and pricing (Section 4.2) problems. In both cases, we focus on settings where agents in a social network consume a divisible product that exhibits positive network externalities, which are of a local nature. The edge weights summarize these externalities, and in particular captures how much the consumption of an agent influences her neighbor . A subset of the agents are observable, e.g., they participate in an online platform, which makes data on their past decisions available. An advertiser/seller decides on agent-specific advertisement levels/prices for the product to influence (observable) agents’ purchase decisions. Her payoff depends on the induced sales. We establish that using the estimation framework of the previous section with historical data on observable agents, near optimal advertisement levels/prices can be obtained.

In our applications, the relationship between the agents’ outcomes and covariates take the form presented in Section 2. We conduct our analysis under the following assumption: {assumption} There exists some such that for each , we have and . This assumption guarantees that the matrix is strictly row and column diagonally dominant. Here, is a parameter that captures how large the diagonal entries are relative to off-diagonal entries. The positivity of this parameter implies that the eigenvalues of are bounded away from zero. Recall that our earlier analysis assumed the boundedness of the absolute row/column sums of . This condition is also readily implied by Assumption 4 (see Lemma LABEL:lem:matBounds). Qualitatively, Assumption 4 implies that the network externality that an agent exerts on the rest of the network (or vice versa) is not too large.666Variants of this assumption have appeared in pricing in social networks literature to ensure that equilibrium solutions are interior and induced pricing problems are concave. See e.g., Ballester et al. (2006), Candogan et al. (2012), Fainmesser and Galeotti (2015), Zhou and Chen (2015).

4.1 Targeted advertising

We first focus on the problem of an advertiser who advertises a product that exhibits network externalities through an online (social networking) platform. Specifically, we study a model where the consumption of agent is given by

| (15) |

Here, captures network externalities. The agent-specific parameter represents agent ’s affinity for the product which captures her (mean) consumption in the absence of any network or advertising effects. The parameter represents exposure level of agent to ads on the online platform. The coefficient captures how responsive customer is to advertising on the platform. In different settings it has been documented that advertising exhibits diminishing marginal returns (see, e.g., Lilien et al. (1995, p. 267) and Manchanda et al. (2006)). Consistently with this is a concave advertising response function that captures how advertising translates into additional consumption. More concretely, for our analysis in this section we assume (but we emphasize that this is for the ease of exposition and the analysis and results can be extended to other concave response functions). Finally, represent zero-mean shocks to agents’ consumption decisions.

As before, we assume that the parameters of the model are bounded, and in particular we require that , and . Here the positive lower bound on is imposed to rule out settings in which advertising has no impact on consumption, since in this case the advertising problem becomes trivial. We also make the following assumption, which ensures that all agents’ consumptions in (15) are nonnegative: {assumption} for all .

We assume that unit ad exposure on the platform can be achieved at a cost of . Only a subset of all of the agents participate in the online platform. The advertiser targets these agents with different ad exposure levels . For a latent agent , we set (since latent agents do not participate in the platform, and hence cannot be exposed to ads there). The cost of choosing exposure levels to the advertiser is given by .

Note that advertising the product on the platform leads to an increase in observable agents’ consumptions through two different channels. The first one is the direct effect of advertising, which motivates the observable agents to consume more. Through network externalities this triggers latent agents to consume more, which then leads to a further (indirect) increase in the consumptions of observable agents.

Let denote the consumption levels of the observable agents under exposure levels . We assume that the advertiser enjoys a unit payoff for each unit consumed by the observable agents. Her objective is to maximize total consumption by these agents minus the cost of advertising. Specifically, for given the expected total payoff of the advertiser is given by:

It is more convenient to formulate the problem of the advertiser after a change of variables: . With some abuse of terminology in what follows we refer to as the advertising intensity for agent . After this change of variables, the dependence of agents’ consumptions on advertising intensities takes the following form:

| (16) |

Slightly abusing the earlier notation, we denote by the consumption levels of observable agents under advertising intensities , and restate the induced payoffs as follows:

| (17) |

Note that this payoff form is consistent with the convex quadratic cost assumptions used in the advertising literature, e.g., see Slade (1995), Dubé and Manchanda (2005). The problem of the advertiser is to choose advertising intensities for to maximize her expected payoffs.777The results of this section go through if is allowed to be unbounded.

We assume that the advertiser does not know the influence structure , or the parameters . Thus, it is not possible to directly solve for the advertising intensities that maximize (17). However, we assume that the advertiser has historical data on past consumption/advertising levels for observable agents. In the remainder of this subsection, we argue that near-optimal advertising levels can be obtained by first estimating the underlying parameters using the available data, and then using these estimates to construct the advertising levels.

To this end, we first map the model introduced in this section back to the model introduced in Section 2, by setting for , , and , where is the identity matrix. We rearrange the terms in (16) and restate it (by using matrix notation and making time dependence explicit) as follows:

| (18) |

Here is a diagonal matrix whose diagonal entries are given by for (and zero for the remaining agents). This equation is almost identical to (2), the only difference being the matrix. Thus, an analogous result to Lemma 2.1 holds, and yields:

| (19) |

where is a row-scaled version of , i.e., , and we redefine as

| (20) |

since for . The remaining variables are defined as in (3) and (4). Note that since , it follows that satisfies the approximate sparsity conditions introduced in Section 3 if and only if does so. This observation together with the fact that (19) has the same form as in (2.1), implies that the algorithm of Section 3 can be used to estimate and , achieving the error rates provided in Theorems 3.2 and 3.3 for a given approximately sparse network.

Using this notation in (17), the expected payoff of the advertiser for advertising intensities can be more explicitly expressed as:

Let denote the advertising intensities that maximize the advertiser’s expected payoff, i.e., solves:

| (21) |

Observe that the payoff function is concave in and . Thus, if the constraints are not binding, the optimal advertising intensities are given by

| (22) |

Suppose that the advertiser chooses advertising levels instead of . Her payoff loss from using the former advertising levels can be measured as follows:

| (23) |

Here, the numerator gives the absolute payoff difference under the optimal decisions and advertising intensities . The denominator is the payoff under optimal decisions. The ratio measures the payoff loss from using prices .

We next show that the advertiser can approximately maximize her payoff by first using our estimator to estimate and then computing the optimal based on this estimate using (22).

Theorem 4.1

This result relies on bounding the loss in the advertiser’s payoff due to using solution as opposed to in terms of . When the gap between and its estimate is small with respect to the -norm, we show that the latter quantity is also small. Theorem 3.2 implies that the aforementioned gap is small with respect to the and -norms, which in turn enables bounding the errors with respect to the -norm. Leveraging this observation, we obtain the bound in Theorem 4.1.

This result implies that when the number of samples is at least logarithmic in the number of observable agents, for approximately sparse networks (e.g., those discussed in Section 5), small payoff loss can be guaranteed. Moreover, the targeting decisions our approach yield are asymptotically optimal, i.e., as the number of samples goes to infinity goes to zero.

4.2 Obtaining Approximately Optimal Prices

We next study the problem of a seller who offers targeted promotional prices for a product that exhibits network externalities. We start by explicitly defining agents’ payoffs.

The payoff function of agent has the same structure every period, and consists of an individual consumption term, a network externality term, and a payment term. Suppose that in period , agent consumes units of the product at unit price , and the remaining agents consume units of the product. Then, the payoff of agent is given by888It is standard to provide microfoundation for linear econometric models of the type we introduced in Section 2 using quadratic payoff functions (see, e.g., Calvó-Armengol et al. (2009), Blume et al. (2015), Topa and Zenou (2015)). In a similar spirit, the payoff function provided here offers a microfoundation for the econometric model studied in the remainder of this section.

| (25) |

The first term in the payoff function determines the value the agent derives from her own consumption of the product. We assume that so that this term is concave, and agents’ marginal payoffs are decreasing in their own consumption. We also assume that , for all and some . Here denotes an (idiosyncratic) taste shock for agent at time , which impacts her marginal value and consumption. As before we assume that have zero mean, and are independent over time, but are possibly correlated across agents. Note that if there are no taste shocks (i.e., for all ), the payoffs reduce to those considered in Candogan et al. (2012). The term captures the positive externality that the consumption of her neighbors imposes on agent . The positive externality increases with the consumption () of agent , as well as with that of her neighbors in the underlying network ( for such that ). The last term captures the cost incurred by agent for consuming units of the product at unit price .

In every period, given a vector of prices , each agent chooses the consumption level that maximizes her payoff. Since agents’ payoffs depend on each other’s consumption decisions, the consumption levels are determined at a corresponding consumption equilibrium:

Definition 4.2 (Consumption equilibrium)

For a given vector of prices , a vector is a consumption equilibrium in period if, for all ,

| (26) |

Note that a consumption equilibrium corresponds to the Nash equilibrium of the normal form game with a set of agents , a strategy set for each agent , and payoffs given as in (25).999This equilibrium concept implicitly assumes that agents know the underlying network structure, and each other’s payoff functions (including taste shocks, and prices). That being said, in order to determine her optimal consumption level in (26), agent needs to observe only her neighbors’ consumption levels. Moreover, it can be shown that for any set of prices/taste shocks, the induced game among agents is supermodular, and agents’ best-responses converge to a consumption equilibrium (see, e.g., Candogan et al. 2012).

Hereafter, we denote by the (lowest) prices available to the agents in period , and by the induced equilibrium consumption levels.101010Here, we assume that the agents choose their consumption levels in a period, based only on the prices offered in that period. Prices/consumption could vary over time due to a variety of factors ranging from inventory imbalances to seasonality. The former corresponds to the covariates and the latter the outcomes in the abstract setting discussed in Section 2. If in a consumption equilibrium agents’ consumption amounts are strictly positive, then by the first-order optimality conditions in (25), it can be seen that in period the equilibrium consumption levels are given as in (2) after letting (and ), for all . Hence, each agent’s consumption depends linearly on the price offered to her, as well as to the other agents.

A subset of agents participate in an online (social networking) platform, and a seller (hereafter the platform seller), offers targeted promotional prices to these agents. The platform seller has access to historical data on the past prices as well as the consumption decisions of these (observable) agents. Both observable and latent agents can purchase the product at price from a different channel (hereafter outside sellers), and this price is public knowledge. This constitutes an outside option for the observable agents. We assume that the prices offered by the platform seller to observable agents are nonnegative and weakly lower than . If this were not the case, then agent would prefer to purchase the product from the outside sellers. Hence, a revenue-maximizing platform always finds it optimal to offer prices weakly lower than . Thus, for any , we ignore the outside option , and focus only on the price offered by the platform. We assume that the outside option is not time varying (see Remark 4.5), whereas the prices offered by the platform to the observable agents possibly are. In other words, is such that for and for .

We conduct our analysis under the following assumption: {assumption} The outside option is such that for all and . Note that this assumption requires negative shocks to be bounded, but allows for unbounded positive shocks. If no agent consumes the product, the marginal utility of agent is given by . Since for every , is weakly lower than , this assumption ensures that the marginal utilities are positive for any realization of taste shocks. As formally established in Lemma 13.1 (Appendix 13) this implies that all agents consume positive amounts of the product. Hence this assumption plays a similar role to Assumption 4.1 in the previous section, and ensures the linear dependence of agents’ outcomes on their covariates (as in (2)).

Since agents’ consumption decisions are expressed as in (2), the dependence of the consumption decisions of observable agents on the prices offered to them can be given as in Lemma 2.1. A central question we investigate is how the platform seller should offer targeted price discounts to maximize her expected revenues. If the network were known (and recalling that the platform seller sells only to the observable agents), we would focus on the following optimization problem:

| (27) | ||||

where the expectation is taken over taste shocks. The constraint reflects that each agent consumes the payoff-maximizing amount, given the prices and the remaining agents’ consumption levels. The optimal price vector for problem (27) is denoted by .

It was established in Candogan et al. (2012) that when all agents are observable, the optimal prices set by the platform seller are independent of the network structure, whenever the underlying influence structure is symmetric (and for all ). Interestingly, in Appendix 13 we show that this is no longer the case when there are latent agents. In this case, the platform seller finds it optimal to increase the prices offered to observable agents, proportional to how much they are influenced by the “central” latent agents. Intuitively, this is the case since such observable agents have a strong incentive to consume the product (due to the positive influence of the latent agents on them), and the platform seller can improve her profits by charging higher prices to those agents. We detail and formally discuss these points in Appendix 13.

Following a similar approach to the previous section, we denote the consumption levels of the observable agents in the consumption equilibrium induced by some price vector by . We denote the corresponding expected revenues by , i.e., . If the platform seller uses price vector instead of , we capture the induced revenue loss as in (23).

Recall that the prices used by the platform seller are nonnegative and less than . For a given vector of prices , we denote by the vector obtained by capping these prices at and projecting them to nonnegative reals, i.e., for all . Using this notation we now state the main result of this section.

Theorem 4.3

Intuitively, if constitutes a good estimate of , then we can exploit this approximation to (solve (27) and) construct approximately optimal prices. Theorem 4.3 formalizes this intuition. In particular, this result establishes that a seller can leverage the algorithm of the previous section to estimate , and compute prices as in (28) using these estimates. Moreover, it is possible to quantify the revenue loss from using these approximately optimal prices as opposed to the optimal prices. Our theorem sheds light on how this loss diminishes as a function of the number of available observations. In settings where the underlying influence structure is approximately sparse (with small and ), our approach is particularly powerful, and guarantees small revenue loss and prices that are asymptotically optimal.

Remark 4.4 (Choosing prices adaptively)

Here, we do not model the platform seller as an entity that strategically experiments with prices over time to choose the prices that should be offered to different agents. Instead, we assume that there is historical data on the prices used in the past and the induced consumption, and we explore how such data might be leveraged to design future prices. There is a corresponding online decision problem where the platform has no historical data but adaptively learns optimal prices. Since the network is large the possible externality structures are rich, and this naturally induces an online decision problem in the high-dimensional regime. This is a growing area of research (see, e.g., Bastani and Bayati (2020)), and applications of similar ideas to network pricing problems remain to be interesting research directions. Note that in our setting the mapping () from the prices to the induced consumption is not sparse, which makes the learning problem challenging. Under approximate sparsity assumptions similar to ours (which are satisfied by various networks as discussed in Section 5), we suspect that it may be possible to develop online learning algorithms with desirable guarantees as well. \halmos

Remark 4.5 (Static outside price)

In this section, we assumed that the price of the product through the alternative channel is fixed at , and the prices offered through the platform are weakly lower. Fixed outside price (that is independent of the price offered through the platform) is natural in some settings. For instance, some manufacturers employ minimum advertised pricing or resale price maintenance policies (see, e.g., Elzinga and Mills (2008), Israeli et al. (2016), Bazhanov et al. (2019)), where authorized resellers are effectively restricted to offering the product at the manufacturer suggested retail price (or a price close to it). The products are often not discounted when purchased directly through the manufacturer (or authorized resellers), though other sellers can still offer the product with some discounts. Viewing the outside sellers as the manufacturer/authorized resellers, while the platform seller as a 3rd party seller yields the structure in our model.

More interestingly, such prices could also emerge as equilibrium prices in natural settings. For instance, suppose that the outside sellers have access to the real-time information on the prices used on the network, and best respond to these prices. This can be modeled as a Bertrand competition (with network externalities) among the platform seller and the outside sellers, e.g., brick and mortar stores. Many online retailers have lower operating costs, as they do not incur costs due to running brick and mortar stores. Let us assume lower marginal cost for the platform seller, and, higher (and identical) ones for the outside sellers. At the induced equilibrium (i) the prices of the outside sellers would be equal to their marginal costs, and (ii) the platform seller’s prices would be lower, consistently with our model. \halmos

Remark 4.6 (Alternative approaches for approximately optimal prices)

An alternative approach for constructing approximately optimal prices involves first estimating (as opposed to ), and then using the prices that would be optimal if were equal to this estimate (see Lemma 13.5 for the dependence of on ). However, estimating presents similar challenges to those of estimating . First, note that in the presence of latent agents the matrix is not sparse in general. To see this, note on the one hand that the consumption of observable agents has direct influence on the consumption of their observable neighbors, which can be represented by a sparse matrix when the underlying network is sparse. On the other hand, observable agents also influence other observable agents indirectly through the influence they exert on the latent agents (who in turn influence other observable agents). This latter influence structure is not sparse in general. Hence, the matrix that captures the aggregate influence that the observable agents exert on each other need not be sparse. Second, to construct approximately optimal prices through the estimates of the matrix, it is necessary to obtain small estimation errors for both rows and columns. When estimating , this was accomplished by our algorithm in Section 3. We explore how ideas such as approximate sparsity can be exploited to obtain estimators for the aggregate influence structure with desirable guarantees on row/column errors in our companion paper Ata et al. (2020). \halmos

Remark 4.7 (Relaxing the assumptions)

In this and the previous section, we assumed that externalities are positive, i.e., , and required that the parameter is not small (through Assumptions 4.1 and 4.2). These assumptions were made to ensure the nonnegativity of the induced consumption levels, and hence the linear dependence of outcomes on the covariates. It is worth highlighting that weaker assumptions that ensure such linearity are sufficient for the results to go through. For instance, limited negative externalities (together with bounded covariates) can be allowed. \halmos

4.3 Numerical Example

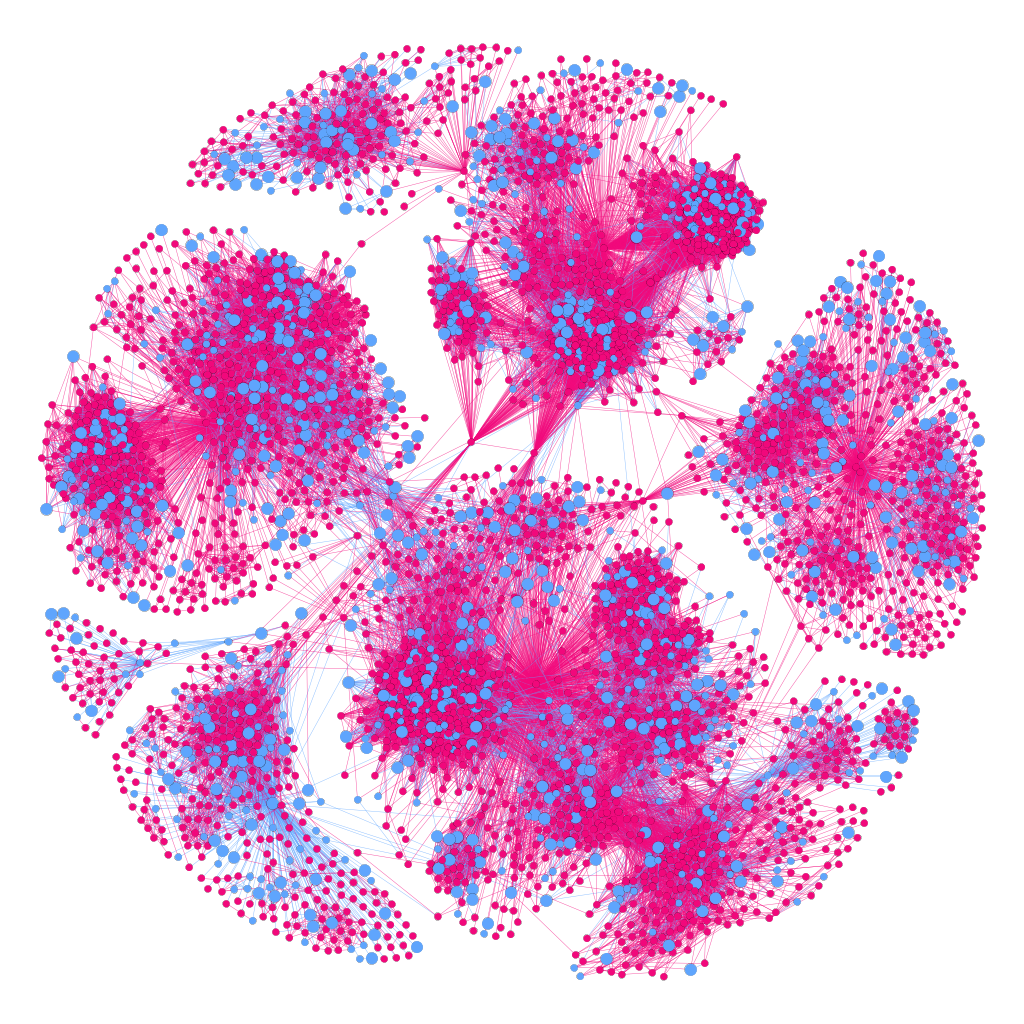

In this section we illustrate our applications by focusing on a nontrivial network structure. Specifically, we focus on an induced subnetwork of the Facebook network, provided by Leskovec and Krevl (2014). The subnetwork consists of 4,039 nodes (agents) and 88,234 edges. The degrees of the agents (which vary between 1 and 1,045) and the connection structure are quite heterogeneous, as can be seen from Figure 1.

We focus on the advertising application (where for all ) and assume that the edge weights are given by for some parameter . We set this parameter equal to , and note that in this case Assumption 4 does not hold. In particular, due to the large degrees of some nodes, for many rows (or columns) of the absolute sum of off-diagonal entries exceeds . Our objective is to illustrate the applicability and the performance of our estimator even in settings where some assumptions made for our asymptotic results no longer hold. We uniformly at random choose nodes, and assume that they are observable while the remaining nodes are latent (see Figure 1). We assume that and for all agents, and we assume that these parameters as well as the network structure are unknown to the advertiser.

We assume that samples of advertising decisions/outcomes, denoted by are available for observable agents. For , we draw each independently from , while we set for . Similarly, the taste shocks are also independent (from each other and ), and drawn from . As before, we assume that the problem of the advertiser is to choose advertising intensities to maximize . For our numerical studies we assume that .

We do not restrict the maximum advertising intensity, i.e., we set . Let be the optimal solution to (21). We observe that this vector has strictly positive entries and is given as in (22). Recall that gives the advertising intensities that maximize the payoff of the advertiser, if the parameters of the underlying system were known. Since she does not know these parameters, we assume that the advertiser follows the approach discussed in Section 4.1. In particular, she uses the available data to obtain an estimate of , and then constructs as in Theorem 4.1 using these estimates.

To estimate , we apply Algorithm 1 with three standard modifications (see, e.g., Tibshirani (1996)) which boost performance when small number of samples are available. In particular, (i) we use demeaned and standardized covariates, (ii) we do not penalize the intercept, and (iii) we cross validate some model parameters. We detail these modifications next.

Let , and . We compute these quantities and construct the demeaned and scaled covariates (hereafter we use the prefix to denote quantities associated with the demeaned/scaled system). Note that using these variables (19) can be rewritten as:

| (29) |

where

| (30) |

and is a diagonal matrix with diagonal entries . We use Algorithm 1 to estimate the linear system in (29) as opposed to the one in (19). That is, we use the algorithm with input , and obtain the estimates (and ) of (and ). Then we “rescale” these estimates (using the equations in (30) that relate and to the parameters , , of the model) to obtain estimates of and . More precisely, we set and . We choose the threshold parameters through bootstrapping as described in Remark 2 (and Appendix 12; using the quantile parameter ). Though, we verify that the alternative choice of these parameters in (10) also gives similar results.

Second, in Step 1 of the algorithm, we modify the first constraint for . Specifically, in this case we replace the aforementioned constraint with . That is, when , we replace the quantity on the right hand side with zero. This allows us to treat the intercept in our linear system differently, and reduce the errors in its estimation in Step 1.

Third, in Step 1 as opposed to using the parameter given in the algorithm, we identify it via cross-validation (and use the cross-validated parameter value ). Our asymptotic results are robust to the exact choice of this parameter (e.g., a different constant could be used as opposed to in its definition in Algorithm 1 while still yielding same asymptotic guarantees), however, different parameter values can lead to different finite sample performance. We optimize it via cross-validation (over a grid of 100 values containing the value provided in the algorithm). Note that other parameters of the algorithm (such as ) can also be optimized using cross-validation, but we do not explore this here, since even without cross validating those parameters we obtain good performance from our estimators.

For the setting described here, we see that despite having access to a small number of samples, the advertiser can achieve a payoff that is very close to the optimal. Specifically, we obtain that , . These in turn imply that . That is, using the available data a targeting structure that is within of the optimal can be achieved. Without estimating the parameters of the underlying system it is not clear how to set the advertising intensities. It is also worth noting that in this example not advertising at all yields substantially lower aggregate consumption (e.g., about 1500 units vs. more than 60000 units with optimal advertising) and payoff to the advertiser.

5 Examples of Approximately Sparse Networks

The results in Section 3 rely on approximate sparsity of . The rates of convergence of the proposed estimators (in Theorem 3.2 and Theorem 3.3) are particularly useful if there exists a sparse approximation to with a few nonzero entries in each row/column that leads to small approximation errors, i.e., if we can set the maximum number of nonzero elements in each row and column () so that and the approximation error are small. In this section, we establish that this indeed is the case for many classes of networks.

Throughout the section we impose Assumption 4, and analyze different classes of networks. We start with two special cases: (i) -banded networks and (ii) matrices that exhibit polynomial off-diagonal decay of connection strength. Then, we consider a fairly general class of networks, where we require agents’ neighborhoods not to grow too fast. For all these cases, we establish -sparsity of the matrix, and provide results on convergence rates when Algorithm 1 is employed. The proofs of the results in this section can be found in Appendix 11.

5.1 -Banded Networks

A matrix is -banded if its nonzero entries are at most entries away from its diagonal, i.e., for . Motivated by this definition, we say that a network is -banded if for some permutation , its adjacency matrix satisfies

| (31) |

In other words, for an -banded network a permutation of rows/columns of the corresponding matrices and are -banded (e.g., consider the matrix such that for all ). This definition captures cases where nodes are embedded at the integer points on the real line, and they have only “local” connections, i.e., connections with nodes to the left and nodes to the right.111111We emphasize that in our context the nodes that correspond to observable agents need not be consecutive integers on the real line. Nevertheless, it can be seen that if the underlying network is -banded, then the induced subgraph of observable (similarly latent) agents is also -banded.

It is known that if is an -banded matrix, then exhibits “exponential decay” (see Demko et al. (1984)), where the rate of decay is characterized in terms of the singular values of . That is, as we get away from the diagonal the magnitude of the entries decays exponentially. We next adapt this result to our setting and obtain an exponential decay result on the inverse of . In this subsection, we discuss our results, using the shorthand notation and .

Lemma 5.1

Suppose that the underlying network is -banded. Then, for any we have

| (32) |

Similarly, for , .

This result suggests a natural -sparse approximation for : since entries of decay (exponentially) in for any , for an -sparse approximation of these matrices we just focus on for which is small. In particular, let be a matrix, such that for we have

| (33) |

Observe that has at most nonzero elements in each row and column by construction. Our next result establishes that yields a sparse approximation of .

Lemma 5.2