appendAppendix References

Improved Methods for Moment Restriction Models with Marginally Incompatible Data Combination and an Application to Two-sample Instrumental Variable Estimation

Heng Shu & Zhiqiang Tan111 Heng Shu is with JPMorgan Chase, New York, NY 10017 and Zhiqiang Tan is Professor, Department of Statistics, Rutgers University, Piscataway, NJ 08854 (E-mail: ztan@stat.rutgers.edu). An earlier version of this work was completed as part of the PhD thesis of Heng Shu at Rutgers University.

Abstract.

Combining information from multiple samples is often needed in biomedical and economic studies, but the differences between these samples must be appropriately taken into account in the analysis of the combined data. We study estimation for moment restriction models with data combination from two samples under an ignorablility-type assumption but allowing for different marginal distributions of common variables between the two samples. Suppose that an outcome regression model and a propensity score model are specified. By leveraging the semiparametric efficiency theory, we derive an augmented inverse probability weighted (AIPW) estimator that is locally efficient and doubly robust with respect to the outcome regression and propensity score models. Furthermore, we develop calibrated regression and likelihood estimators that are not only locally efficient and doubly robust, but also intrinsically efficient in achieving smaller variances than the AIPW estimator when the propensity score model is correctly specified but the outcome regression model may be misspecified. As an important application, we study the two-sample instrumental variable problem and derive the corresponding estimators while allowing for incompatible distributions of common variables between the two samples. Finally, we provide a simulation study and an econometric application on public housing projects to demonstrate the superior performance of our improved estimators.

Key words and phrases.

Data Combination; Double robustness; Inverse probability weighting; Intrinsic efficiency; Local efficiency; Moment restriction models; Two-sample instrument variable estimation.

1 Introduction

Typically, empirical studies in biomedical and social sciences involve drawing inferences regarding a population. However, there are various situations where information need to be combined from two or more samples possibly for different populations from the target (e.g., Ridder & Moffitt 2007). For example, a single sample may not contain all the relevant variables, or some variables in the sample may be measured with errors. Even if all the relevant variables are collected from one sample, the sample size may be too small to achieve accurate estimation.

Suppose that two random samples are obtained: a primary sample from the target population and an auxiliary sample from another population possibly different from the target population. The primary sample provides the measurements of variables , and the auxiliary sample contains measurements of variables . That is, the variable is only available from the primary data, only from the auxiliary data, and from both data. We distinguish two different settings:

-

(I)

The parameter of interest can be defined through a set of moment restrictions in , without involving , under the primary population (Chen et al. 2008).

-

(II)

The parameter can also be defined through moment restrictions that are separable in and in under the primary population as studied in Graham et al. (2016).

Setting (I) is more basic than (II) because the inferential difficulty mainly lies in the lack of primary data on jointly. On the other hand, setting (I) can be subsumed under (II) with degenerate restrictions in . A special case of such settings is estimation of average treatment effects on the treated (ATT) (Hahn 1998). Identification of the parameter can be achieved provided that the conditional distributions of given are the same under the primary and auxiliary populations. The marginal distributions of may, however, differ between the two populations.

The foregoing setting (I), with only involved but not , is called the “verify-out-of-sample” case in Chen et al. (2008), because the auxiliary sample is obtained independently of the primary sample such that no individual units are linked between the two samples. This setting differs from missing-data and causal inference problems which are studied in Robins et al. (1994) and Tan (2010a, 2011) among others and called the “verify-in-sample” case in Chen et al. (2008) because the auxiliary sample is a subset of the primary sample by design or by happenstance. A particular example of the latter setting is estimation of average treatment effects in the overall population (ATE) (e.g., Hahn, 1998; Imbens, 2004). The current setting should also be contrasted with the analysis of linked data, where common units are linked between different samples by probabilistic record linkage (e.g., Lahiri & Larsen 2005).

A large body of works have been done on statistical theory and methods for estimation in moment restriction models with auxiliary data in the “verify-out-of-sample” case, in addition to the “verify-in-sample” case. The semiparametric efficiency bounds are studied by Hahn (1998) for ATT estimation, by Chen et al. (2008) for moment restriction models with only involved in setting (I), and by Graham et al. (2016) for moment restriction models that are separable in and in setting (II). Moreover, asymptotically globally efficient estimators are proposed in these cases by Hahn (1998), Hirano et al. (2003), and Chen et al. (2008) among others, using nonparametric series/sieve estimation on the propensity score (PS) or the outcome regression (OR) function. But the smoothness conditions typically assumed for such methods can be problematic in many practical situations with a high-dimensional vector of common variables (e.g., Robins & Ritov 1997). Recently, Graham et al. (2016) proposed a locally efficient and doubly robust method with separable moment restrictions, using parametric PS and OR models. But methods achieving local efficiency and double robustness alone may still suffer from large variances due to inverse probability weighting. Such a phenomenon is known in the “verify-in-sample” case of missing-data problems (Kang & Schafer 2007), and can be seen to motivate various recent methodological development (e.g., Tan 2010a; Cao et al. 2009).

We develop improved methods for moment restriction models with data combination and make three contributions. First, we derive augmented inverse probability weighted (AIPW) estimators in setting (I), by using efficient influence functions as estimating functions with the true outcome regression function and propensity score replaced by their fitted values. The idea of constructing estimating equations from influence functions (including efficient influence functions) is widely known, at least for missing-data problems in the “verify-in-sample” case (e.g., Tsiatis 2006; Graham 2011). But our application of this idea to the “verify-out-of-sample” case seems new and reveals subtle properties associated with the fact that the semiparametric efficient bounds vary under a nonparametric model, a correctly specified propensity score model, or known propensity scores in the “verify-in-sample” case, instead of staying the same in the “verify-out-of-sample” case (Hahn 1998; Chen et al. 2008).

On one hand, we show that the AIPW estimator based on the efficient influence function calculated under the nonparametric model is locally nonparametric efficient (i.e., achieves the nonparametric variance bound if both the OR and PS models are correctly specified), and doubly robust (i.e., remains consistent if either the OR model or the PS model is correctly specified). This AIPW estimator is simpler and more flexible than the related estimator of Graham et al. (2016), which is shown to be locally efficient and doubly robust only under the restrictions that the PS model is logistic regression, the OR model is linear, and all the regressors of the OR model are included in the linear span of those of the PS model.222For Theorem 4 of Graham et al. (2016), it should be added to condition (b) that each component of is contained in the linear span of . Some of the restrictions for the method of Graham et al. (2016) can potentially be relaxed. For example, the fitted values from a nonlinear OR model can be included as regressors in an augmented logistic PS model similarly as used in our estimators in Section 2.3. But our calibrated estimators are designed to achieve desirable properties beyond local efficiency and double robustness as seen from the subsequent discussion. On the other hand, we find that the AIPW estimator based on the efficient influence function calculated with known propensity score is locally semiparametric efficient (i.e., achieves the semiparametric variance bound calculated under the PS model used if both the OR and PS models are correctly specified), but generally not doubly robust.

Second, we propose in setting (I) calibrated regression and likelihood estimators which are not only locally efficient and doubly robust, but also intrinsically efficient (i.e., asymptotically more efficient than the corresponding locally efficient and doubly robust AIPW estimator when the PS model is correctly specified but the OR model may be misspecified). Such improved estimators have been obtained in the “verify-in-sample” case of missing-data problems (e.g., Tan 2006, 2010a, 2010b; Cao et al. 2009). But due to the aforementioned difference between the locally nonparametric and semiparametric efficient AIPW estimators, a direct application of existing techniques would not yield an estimator with the desired properties in the “verify-out-of-sample” setting. We introduce a new idea to overcome this difficulty and develop estimators of the desired properties, by working with an augmented propensity score model which includes the fitted outcome regression functions as additional regressors.

Third, our theory and methods from setting (I) can be applied and extended to setting (II). As a concrete application, we study two-sample instrumental variable estimation and derive the improved estimators in setting (II). The two-sample instrumental variable (TSIV) estimator (Angrist & Krueger 1992) is generally consistent only when the marginal distributions of the common variables are the same in the two samples or, equivalently, the propensity score for selection into the samples is a constant in . The two-sample two-stage least squares (TS2SLS) estimator (Bjorklund & Jantti 1997) is consistent if either the propensity score is a constant in or the linear regression in the first stage is correctly specified. In contrast, our calibrated estimators are doubly robust, i.e., remain consistent if either a general OR model or a general PS model is correctly specified. Moreover, our estimators tend to achieve smaller variances than related doubly robust AIPW estimators when the PS model is correctly specified but the OR model may be misspecified. We present a simulation study and an econometric application on public housing projects, to demonstrate the advantage of our estimators compared with existing estimators.

2 Moment restriction models with auxiliary data

Throughout this section, consider setting (I) described in the Introduction, where we are interested in the estimation of parameters through the moment conditions

| (1) |

where denotes the expectation under a primary population, is a vector of known functions, and is a vector of unknown parameters. Suppose that are defined on an i.i.d. sample of size from the primary population, but are missing and only are observed. For a remedy, suppose that additional data are obtained on an i.i.d. sample of size from an auxiliary population, possibly different from the primary population. To draw valid inference about , we need to combine the data from the primary population and the data from the auxiliary population.

For technical convenience, we make the following assumption:

-

(A1)

The sample sizes are determined from binomial sampling: the combined set of units are independently drawn from either the primary or the auxiliary population with a fixed probability . As a result, converges in probability to a finite constant in as .

With some additional work (not pursued here), it is possible to adapt our methods and results to other sampling schemes with non-random . Under Assumption (A1), the combined set of variables are i.i.d. realizations from a mixture distribution , where is an indicator variable, equal to either 1 or 0 if the th unit is drawn from the primary or the auxiliary population. The combined set of observed data are

The moment conditions (1) can be represented as

| (2) |

where denotes the expectation with respect to the mixture distribution . This setup is exactly the “verify-out-of-sample” case in Chen et al. (2008). Because are not jointly observed given (primary population), we need borrow information from jointly observed given (auxiliary population).

To achieve identification of by information-borrowing from the auxiliary data, there are two basic assumptions needed (e.g., Chen et al. 2008). The first assumption is that the conditional distributions of given are the same under the primary and auxiliary populations, that is,

-

(A2)

and are conditionally independent given .

Assumption (A2) is similar to the unconfoundedness for controls for identification of ATT (e.g., Imbens 2004). The marginal distributions of are, however, allowed to differ between the primary and auxiliary populations. The second assumption is that the support of the common variable in the primary population is contained within that in the auxiliary population, that is,

-

(A3)

.

Assumption (A3) allows that is 0 for some values , i.e., subjects with certain -values will always be in the auxiliary population, because information from those subjects is not needed for inference about in the primary population. Nevertheless, Assumption (A3) will be strengthened in our asymptotic theory such that for all , where is a constant. See Condition (C5) and the associated discussion preceding Proposition 1.

2.1 Modeling approaches for estimation

There are two types of working/assisting models typically postulated for estimation of in (2), focusing on either the relationship between and or between and , similarly to those for estimation in missing-data problems (e.g., Kang & Schafer 2007; Tan 2006, 2010a). The two approaches roughly correspond to conditional expectation projection or inverse probability weighting in Chen et al. (2008).

The first approach is to build a (parametric) regression model for the outcome regression (OR) function, , such that for any value ,

| (3) |

where is a vector of known functions and is a vector of unknown parameters. In general, this model can be derived from a conditional density (not just mean) model of given , , by the relationship . In special cases as discussed in Section 4.2.1, model (3) can be directly induced from a conditional mean model of given . Let be an estimator of from the auxiliary sample (i.e., ), and denote by the fitted outcome regression function. Define as an estimator of that solves the equation

| (4) |

If OR model (3) is correctly specified for each possible value (not just the true ), for example, a conditional density model is correctly specified, then is a consistent estimator of under standard regularity conditions. See Conditions (C1), (C4), and (C6) in Supplementary Material.

The other approach is to build a (parametric) regression model for the propensity score (PS), , such that (Rosenbaum & Rubin 1983)

| (5) |

where is an inverse link function, is a vector of known functions including 1, and is a vector of unknown parameters. The score function of is:

Typically, a logistic regression model is used:

Denote by the maximum likelihood estimator (MLE) of that solves , which in the case of logistic regression reduces to

| (6) |

where denotes the sample average over the merged sample. For convenience, write the fitted propensity score as . Similarly as inverse probability weighting (IPW) for the estimation of ATT (e.g., Imbens 2004), an IPW estimator for is defined as a solution to

| (7) |

If PS model (5) is correctly specified, then is consistent under standard regularity conditions. See Conditions (C2), (C4), (C5), and (C7) in Supplementary Material. However, because the fitted propensity score is used for inverse weighting in Eq. (7), can be very sensitive to possible misspecification of model (5).

2.2 AIPW estimators

As discussed in Section 2.1, the consistency of depends on the correct specification of OR model (3), and the consistency of depends on the correct specification of PS model (5). We exploit semiparametric theory to derive locally efficient and doubly robust estimators of in the form of augmented IPW (AIPW), using both OR model (3) and PS model (5). Understanding of these estimators will be important for our development of improved estimation in Section 2.3.

In Supplementary Material, Proposition S1 restates the semiparametric efficiency results from Chen et al. (2008) for estimation of under (2) in three settings:

-

(i)

the propensity score is unknown with no parametric restriction;

-

(ii)

the propensity score is assumed to belong to a parametric family ;

-

(iii)

the propensity score is known.

The efficient influence functions are denoted by , , and , and their variances (i.e., semiparametric efficiency bounds) are denoted by , , and . It holds, in general with strict inequalities, that , which is in contrast with other missing-data problems such as Robins et al. (1994) and the “verify-in-sample” case in Chen et al. (2008), where .

Two estimator of can be derived by directly taking the efficient influence functions as estimating functions, with the unknown true functions and replaced by the fitted values and . The first estimator, denoted by , is based on and defined as a solution to

| (8) |

The second estimator, denoted by , is based on or equivalently based on and defined as a solution to

| (9) |

Proposition 1 shows that both estimators possess local efficiency but of different types,333Local efficiency means attaining the efficiency bound under a semiparametric model when some additional modeling restrictions (not part of the model) are satisfied. Thus there are different types of local efficiency, depending on what model and additional restrictions are involved. and only is doubly robust. For clarity, the semiparametric efficiency bound under the nonparametric PS model is hereafter called the nonparametric efficiency bound. See, for example, Newey (1990), Robins & Rotnitzky (2001), and Tsiatis (2006) for general discussions on local efficiency and double robustness.

We briefly describe regularity conditions for the asymptotic results below. See Appendix II in Supplementary Material for details. To match the Supplementary Material, the numbering of the conditions is not consecutive here.

-

(C1)

For a constant , it holds that . If OR model (3) is correctly specified, then .

-

(C2)

For a constant , it holds that . If PS model (5) is correctly specified, then .

-

(C4)

The vector of estimating functions satisfies regularity conditions to ensure -convergence of the estimator of that solves if, hypothetically, were jointly observed given .

-

(C5)

There exists a constant such that for all . We assume that is bounded away from 1, to avoid “irregular identification” for inverse weighting (Khan & Tamer 2010). Moreover, we assume that is nonzero (but possibly close to 0), to simplify technical arguments; otherwise, some components of would be in PS model (5).

-

(C7)–(C8) Partial derivative matrices of and are uniformly integrable in neighborhoods of , , and .

Proposition 1

In addition to Assumptions (A1)–(A2), suppose that Conditions (C1), (C2), (C4), (C5), (C7), and (C8) are satisfied, allowing for possible model misspecification (e.g., \citealtappendWhite1982). Then the following results hold.

- (i)

- (ii)

For both estimators and , the estimating equations (8) and (9) can be expressed in the following AIPW form with the choice or respectively:

| (10) |

Setting leads to the IPW estimator . By local semiparametric efficiency in Proposition 1(ii), achieves the minimum asymptotic variance among all regular estimators under PS model (5), including AIPW estimators like as solutions to (10) over possible choices of , when both PS model (5) and OR model (3) are correctly specified. However, is not doubly robust, and is doubly robust. This situation should be contrasted with other missing-data problems such as the “verify-in-sample” case where nonparametric and semiparametric efficiency bounds are the same, and there exists an AIPW estimator that is locally nonparametric and semiparametric efficient and doubly robust simultaneously (e.g., Robins et al. 1994; Tan 2006, 2010a). These differences present new challenges in our development of improved estimation; see the discussion after Proposition 2.

2.3 Improved estimation

We develop improved estimators of under moment conditions (2) which are not only doubly robust and locally nonparametric efficient, but also intrinsically efficient: as long as PS model (5) is correctly specified, these estimators will attain the smallest asymptotic variance among a class of AIPW estimators including but with replaced by the fitted value from an augmented propensity score model as defined later in (11). The new estimators are then similar to in achieving local nonparametric efficiency and double robustness, but often achieve smaller variances than when PS model (5) is correctly specified but the OR model is misspecified.

2.3.1 Calibrated regression estimator

We derive regression estimators for , similar to the regression estimators of ATE in Tan (2006), but with an important new idea as follows. For simplicity, assume that PS model (5) is logistic regression. With additional technical complexity, the approach can be extended when PS model (5) is non-logistic regression similarly as discussed in Shu & Tan (2018). Consider an augmented PS model

| (11) |

where and is a vector of unknown coefficients for additional regressors . Let be the MLE of and , depending on through . This dependency on is suppressed for convenience in the notation. A consequence of including the additional regressors is that, by Eq. (6), we have the two equations,

| (12) | |||

| (13) |

For augmented PS model (11), there may be linear dependency in the variables , . In this case, the regressors should be redefined to remove redundancy.

We define the regression estimator as a solution to

| (14) |

with and , where

and are defined as follows,

The dependency of , , and on through is suppressed in the notation. To compute , the equations (12)–(13) and (14) can be solved jointly by alternating Newton-Raphson iterations to update and , as in Tan (2010b). The computation can be simplified in special cases, as discussed in Section 4.2.2.

The variables in are included to achieve different properties. First, is included in to ensure efficiency gains over the ratio estimator. Second, is included in to achieve double robustness and local nonparametric efficiency, as later seen from Eq. (16). Finally, is included to account for the variation of to achieve intrinsic efficiency as described in Proposition 2 below. The variables in corresponding to are exactly the scores for the augmented PS model (11). The subvector can be removed to reduce the dimension of , with little sacrifice or even improvement in finite samples.

We impose the following regularity conditions in addition to those described earlier for Proposition 1. See Appendix II in Supplementary Material for details.

-

(C3)

For in a neighborhood of and some constants , it holds that . If PS model (5) is correctly specified, then .

-

(C6)

There exists a constant such that for all and .

-

(C9)

Partial derivative matrices of are uniformly integrable in neighborhoods of for .

Assumption (C6) is similar to (C5), whereas (C9) is similar to (C8). In particular, if PS model (5) is correctly specified, then (C6) is equivalent to (C5). If PS model (5) is misspecified, then (C6) requires that the limit propensity score under the augmented PS model (11) is bounded away from 1 for .

Proposition 2

Suppose that Assumptions (A1)–(A2) and Conditions (C1)–(C9) are satisifed, and PS model (5) is logistic regression. Then the following results hold.

- (i)

- (ii)

-

(iii)

is intrinsically efficient: if model (5) is correctly specified, then it achieves the lowest asymptotic variance among the class of estimators of that are solutions to estimating equations of the form

(15) where is a matrix of constants.

In the following, we provide several remarks to discuss Proposition 2.

Double robustness. We explain why the use of the augmented propensity score is important for to achieve double robustness, in addition to the fact that is included in . If the OR model (3) is correctly specified, then, as shown in the proof of Proposition 2 in Supplementary Material, is asymptotically equivalent, up to , to a solution of the equation

| (16) |

mainly because is included in . By the use of the augmented PS model, Eq. (13) holds and hence Eq. (16) is identical to the equation

| (17) |

which has exactly the same form as Eq. (8) but with replaced by the augmented propensity score . Let be a solution of Eq. (17). Then is doubly robust similarly as based on by Proposition 1. Therefore, is consistent when OR model (3) is correctly specified even if the PS model (5) is misspecified.

Local efficiency. The asymptotic equivalence between and discussed above under OR model (3) also implies that when model (3) is correctly specified, is locally nonparametric efficient, similarly as and . It should be noted that is generally not locally semiparametric efficient in terms of PS model (5), but locally semiparametri efficient in terms of PS model (11): achieves the semiparametric efficiency bounded calculated under model (11), not under model (5), when both model (3) and model (5) are correctly specified. In fact, when PS model (5) holds, the efficiency bound under model (11) coincides with the nonparametric efficiency bound , because can be shown to be included in the score function of model (11). On the other hand, with replaced by throughout would be locally semiparametric efficient with respect to original PS model (5), but generally not doubly robust, similarly as .

Intrinsic efficiency. The regression coefficient is constructed by the approach of Tan (2006), for to achieve intrinsic efficiency beyond local nonparametric efficiency and double robustness. In fact, we did not apply , the classical estimator of the optimal choice in minimizing the asymptotic variance of (15). The estimator , which solves the equation , is asymptotically equivalent to the first order to when the PS model is correctly specified. But , unlike , is generally inconsistent for , when OR model is correctly specified and PS model may be misspecified. The particular form of can also be derived through empirical efficiency maximization (Rubin & van der Laan 2008; Tan 2008) and design-optimal regression estimation for survey calibration (Tan 2013). See further discussion related to calibration estimation after Proposition 3.

The advantage of achieving intrinsic efficiency can be seen as follows. Let and, as done before, be a solution to Eq. (7) for and Eq. (8) for respectively, with replaced by . Moreover, consider an extension of the auxiliary-to-study tilting (AST) estimator in Graham et al. (2016) under our general setting using the augmented PS model (11) as mentioned in Introduction. Let be a solution to , where , is the MLE of for model (11), and is chosen such that . Then and can be shown to be doubly robust and locally nonparametric efficient.

Corollary 1

The concept of intrinsic efficiency was introduced in related works on missing-data and causal inference problems (Tan, 2006, 2010a, 2010b), and is useful for comparing various estimators that are all shown to be doubly robust and locally efficient when both OR and PS models are involved. Roughly speaking, intrinsic efficiency indicates that an estimator achieves the smallest possible asymptotic variance among a class of AIPW-type estimators, such as (15), using the same fitted OR function as long as the PS model is correctly specified. It is tempting, but remains an open question, to formulate a similar property in terms of a correctly specified OR model and construct estimators with the desired property. See Tan (2007) for a discussion about different characteristics of PS and OR approaches related to DR estimation.

2.3.2 Calibrated likelihood estimator

A practical limitation of the regression estimator is that it may take some outlying values due to large inverse weights in both terms and . In this section, we derive a likelihood estimator of which is doubly robust, locally nonparametrically efficient and intrinsically efficient similarly to the regression estimator , but tends to be less sensitive to large weights than the regression estimator.

We take two steps to derive a likelihood estimator achieving all the desirable properties. First, we derive a locally nonparametric efficient, intrinsically efficient, but non-doubly robust estimator of by the approach of empirical likelihood using estimating equations (Owen 2001; Qin & Lawless 1994) or equivalently the approach of nonparametric likelihood (Tan 2006, 2010a). Specifically, our approach is to maximize the log empirical likelihood subject to the constraints

| (18) |

where is a nonnegative weight assigned to for with . Let be the weights obtained from the maximization. The empirical likelihood estimator of , , is defined as a solution to

| (19) |

where is the fitted value of under model (11) as in Section 2.3.1. In the just-identified setting with and of the same dimension, this approach is equivalent to maximizing the empirical likelihood subject to (18) and (19) together. In Supplementary Material, we show that Eq. (19) can also be expressed as

| (20) |

where and is a maximizer of the function

subject to if and if for . Setting the gradient of to zero shows that is a solution to

| (21) |

The estimator can be shown to be intrinsically efficient among the class of estimators (15) and locally nonparametric efficient, but generally not doubly robust. Next we introduce the following modified likelihood estimator, to achieve double robustness but without affecting the first-order asymptotic behavior.

Partition as and accordingly as . Define , where are obtained from , and is a maximizer of the function

subject to if for . Setting the gradient of to 0 shows that is a solution to

| (22) |

The resulting estimator of , , is defined as a solution to

| (23) |

where is also involved in and , although this dependency is suppressed in the notation. To compute , the equations (12)–(13), (21)–(22), and (23) can be solved by alternating Newton-Raphson iterations. See Section 4.2.2 for simplification in special cases. The estimator has several desirable properties as follows.

Proposition 3

The double robustness of holds mainly for two reasons. First, we have by Eq. (22) with included in . Second, we have by Eq. (13) for the augmented PS model (11). Combining the two equations indicates that , which can be easily shown to imply that remains consistent when OR model (3) is correctly specified even if the PS model (5) is misspecified.

The doubly robust estimators and can be regarded as calibrated regression and likelihood estimators, with an important connection to calibration estimation using auxiliary information in survey sampling (Deville & Sarndal 1992; Tan 2013). In fact, the estimating equations (14) and (23) can be expressed as , where the (possibly negative) weights are determined to satisfy the calibration equation

| (24) |

For the likelihood estimator , by Eq. (22). For the regression estimator , it can be shown by direct calculation that , where . However, the associated weights for may be negative, whereas the weights for are always nonnegative by construction. As a result, tends to perform better (less likely yield outlying values) than , especially with possible PS model misspecification. It remains an interesting but challenging topic to provide further theoretical analysis of performances of and in the presence of model misspecification.

3 Data combination

Consider setting (II) described in the Introduction, where another variable in addition to is observed from the primary data. The moment restriction model of interest is postulated in a separable form as

| (25) |

where is a vector of known functions of only whereas is a vector of known functions of only. The expectation can be directly estimated as simple sample averages from the primary data. For estimation of , the main challenge is then to estimate using both the primary and secondary data, which is exactly the problem addressed in Section 2.

Similarly as in Section 2, we assume that the sample sizes are determined from binomial sampling. The combined set of observed data are

| (26) |

where is an indicator variable, equal to either 1 or 0 if the th unit is in the primary or auxiliary sample. The moment conditions (25) can be represented by

| (27) |

Various statistical problems can be studied in the above setup of data combination as discussed by Graham et al. (2016) and references therein.

The methods and theory developed in setting (I) for moment restriction models with auxiliary data can be adopted and extended to setting (II). An AIPW estimator for in (27) can be defined as a solution to equation similar to (9),

| (28) |

where is a fitted propensity score using model (5) as before, and is a fitted outcome regression function using model (3), with replaced by . A calibrated regression estimator can be defined as a solution to

| (29) |

and a calibrated likelihood estimator defined as a solution to

| (30) |

where is defined as in (14), and defined as in (22), with replaced by throughout, including the newly defined in augmented PS model (11). Similarly as in Section 2, the estimators , , and can be shown to be doubly robust and locally nonparametric efficient. Moreover, and are expected to yield smaller variances than and the doubly robust estimator in Graham et al. (2016) when the propensity score model is correctly specified. In general, and do not achieve intrinsic efficiency or the theoretical guarantee as in Corollary 1, mainly due to the inefficiency of in (29) and (30), which, however, tends to be of less concern than the variability from the second term. It is possible to construct calibrated estimators of differently to achieve intrinsic efficiency, as shown in Shu & Tan (2018) for ATT estimation. But such estimators are more complex than above and may not be preferable in the case where and are multi-dimensional, due to finite-sample consideration. See the end of Section 4.2.2 for related discussion.

4 Two-sample instrumental variable estimation

A typical problem in econometrics involves estimating regression coefficients in a linear regression model with endogeneity,

| (31) |

where is a response variable, is a scalar, endogenous variable possibly correlated with the error term , and is a vector of exogenous variables uncorrelated with . Suppose that there exists a scalar instrument variable (IV) that is correlated with but uncorrelated with . Extension to multiple endogenous variables and instruments is possible, but would be technically more complex. Let and . Given an i.i.d. sample from the primary population, the conventional IV estimator of is , where, as before, denotes the sample average. This estimator is identical to the two-stage least squares (2SLS) estimator, defined as , where and .

Recently, two-sample instrumental variable estimation has been proposed to deal with the situation where only and (but not ) are observed in one primary sample, and only and (but not ) are observed in another auxiliary sample (Klevmarken 1982; Angrist & Krueger 1992; Inoue & Solon 2010). In the notation of Section 3, the two samples can be combined and represented as (26). The moment conditions corresponding to IV estimation,

| (32) |

can be put in the form (27), where and with . In the remainder of this section, we discuss existing methods in Section 4.1, and then develop improved methods in Section 4.2.

4.1 Existing methods

For two-sample instrumental variable estimation, Angrist & Krueger (1992) used the following estimator mimicking the form of :

Alternatively, another estimator motivated by two-stage least squares is defined as (e.g., Bjorklund & Jantti 1997)

where and for . As emphasized in Inoue & Solon (2010), the two estimators and are different from each other in the two-sample case, even though IV and 2SLS estimation are equivalent in the standard one-sample case.

The estimators and have been shown to be consistent provided that the two samples are drawn from the same population, i.e., the propensity score is a constant (Angrist & Krueger 1992; Inoue & Solon 2010). This assumption is much more restrictive than (A2), which allows that the marginal distributions of differ between the primary and auxiliary populations or, equivalently, the propensity score is a nonconstant function of . Under Assumption (A2), and generally become inconsistent. An interesting exception noticed by Inoue & Solon (2010) is that , but not , remains consistent if a linear regression model of given holds even when the two samples are differentially stratified on . Therefore, is doubly robust (i.e., remains consistent) if either a constant PS model is correct or a linear regression model of given is correct. See Khawand & Lin (2015) and Choi et al. (2017) for more recent works, both under the assumption of compatible moments of common variables between the two samples.

4.2 Improved methods

We discuss how the improved methods developed in Section 2 for moment restriction models can be applied for estimating in the two-sample instrumental variable problem. The application is facilitated by the fact that from the moment conditions (32) can be represented in a closed form as , where , , and . Then and are both vectors, and is a matrix, where is the dimension of . Similar ideas can be followed when the parameter of interest is only implicitly defined through moment conditions (27), but will not be further pursued here.

Because are measured in the primary data indicated by , the conditional means and can be directly estimated by and . These estimators and are consistent, free of modeling assumptions. On the other hand, can be estimated from a moment restriction model (2), by defining , where is a vector of unknown parameters. For any estimator , the resulting estimator of is

| (33) |

The remaining task is then to estimate . Because of the use of the model-free estimators and , consistency of is directly determined by that of , but efficiency properties can be subtle. See the discussion at the end of Section 4.2.2.

4.2.1 Model-based and AIPW estimators

First, simple estimators of can be derived, depending on either an outcome regression model or a propensity score model. Suppose that a PS model (5) is specified, and the fitted propensity score is obtained by maximum likelihood. The IPW estimating equation (7) yields the estimator

which is consistent when PS model (5) is correctly specified. Noticing that , consider a regression model for ,

| (34) |

where is an inverse link function, is a vector of known functions including 1, and is a vector of unknown parameters. Let be the least-squares estimate of from the auxiliary sample (i.e., ), and let . Substituting the fitted value into Eq. (4) yields the OR estimator

which is consistent when OR model (34) is correctly specified. The resulting estimator from Eq. (33) can be seen as a solution to the equation

It can be easily shown that reduces to in the special case where model (34) is a linear regression model of on , i.e., . In general, the two estimators and are different from each other.

Similarly, substituting and into Eq. (8) for leads to the AIPW estimator

By Proposition 1, the estimator is doubly robust, i.e., remains consistent if either PS model (5) or OR model (34) is correctly specified, and is locally nonparametric efficient, i.e., achieves the nonparametric efficiency bound for when both PS model (5) and OR model (34) are correctly specified.

4.2.2 Calibrated regression and likelihood estimators

We apply the calibrated regression estimator and likelihood estimator to estimates , with and . As in Section 2.3, assume that an augmented logistic PS model (11) is used, and the fitted propensity score is obtained by maximum likelihood.

The computation can be further simplified. First, the additional regressors in the augmented PS model (11) can be simplified as by dropping the term, because already includes a constant. Similarly, the vector in can be simplified as by removing the term . Then is redefined with , , and . Therefore, and are independent of . As mentioned in Section 2.3.1, can also be removed from for finite-sample considerations.

Substituting these definitions into Eq. (14) yields the regression estimator

| (35) |

where , , , and . But Eq. (35) can be further simplified to

because . The first equality can be shown by direct calculation using the fact that is a component of because is included as a component of . The second equality holds by the score equation (6) because a constant is included in .

Substituting into Eq. (23) yields the likelihood estimator

| (36) |

where the second equality holds due to Eq. (22) with included in and to by the score equation (12).

By Propositions 2 and 3, the estimators and are not only doubly robust and locally nonparametric efficient similarly as , but also intrinsically efficient within a class of estimators as solutions to Eq. (15), including the estimators and but with replaced by .

Finally, we examine statistical properties for the resulting estimators of , denoted by , , or by Eq. (33). The estimators and are only based on sample averages and hence are fully robust (consistent without modeling assumptions) and nonparametrically efficient (achieving the nonparametric efficiency bounds), as shown in Shu & Tan (2018) in the context of ATT estimation. As a result, the estimators , , and are doubly robust, i.e., remain consistent if either PS model (5) or OR model (34) is correctly specified, and are locally nonparametric efficient, i.e., achieve the nonparametric efficiency bound for when both PS model (5) and OR model (34) are correctly specified. On the other hand, and do not generally inherit the intrinsic efficiency of and , because and are not intrinsically efficient. Although it is possible to derive regression and likelihood estimators of and to achieve double robustness and intrinsic efficiency, such estimators are no longer fully robust and, more importantly, may not perform well in small or moderate samples because they would depend on augmentation of PS model (5) with additional regressors as many as the dimensions, and of and . Nevertheless, by the intrinsic efficiency of and , the estimators and are still often more efficient than when PS model (5) is correctly specified but OR model (34) is misspecified, as demonstrated in our simulation studies.

5 Simulation study

We conducted a simulation study to compare various estimators for two-sample IV estimation as discussed in Section 4. For the primary population, suppose that the response variable is defined as

the endogenous variable is defined as

| (37) |

where are mutually independent and marginally distributed as , and are distributed independently of as

In the notation of Section 4, the instrumental variable is , the vector of exogenous variables is , and hence . For the auxiliary population, suppose that is also defined by Eq. (37), but are mutually independent and marginally distributed as .

For each simulation, we generated an i.i.d. sample of size and recorded only from the primary population, and generated an i.i.d. sample of size and recorded only from the auxiliary population. The two samples are then merged into one, and an indicator variable is introduced, equal to 1 or 0 for the primary or auxiliary sample respectively. By direct calculation based on the density ratio of between the two samples, the true propensity score is

See the Supplmentary Material for simulation results where the coefficient of the instrument in Eq. (37) is smaller, or , corresponding to a weaker instrument, or where the primary and auxiliary data sizes are reversed: and . The relative performances of the estimates of are similar as discussed below.

|

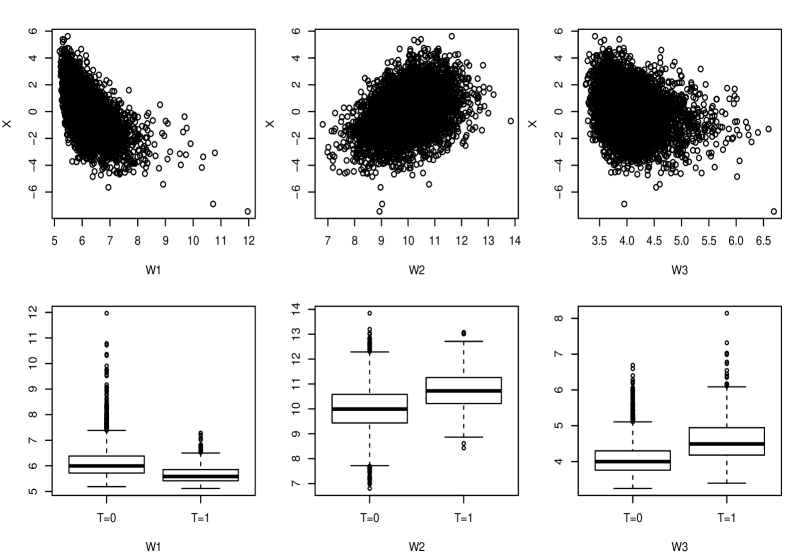

To investigate possible model misspecification similarly as in Kang & Schafer (2007), we define the transformed variables

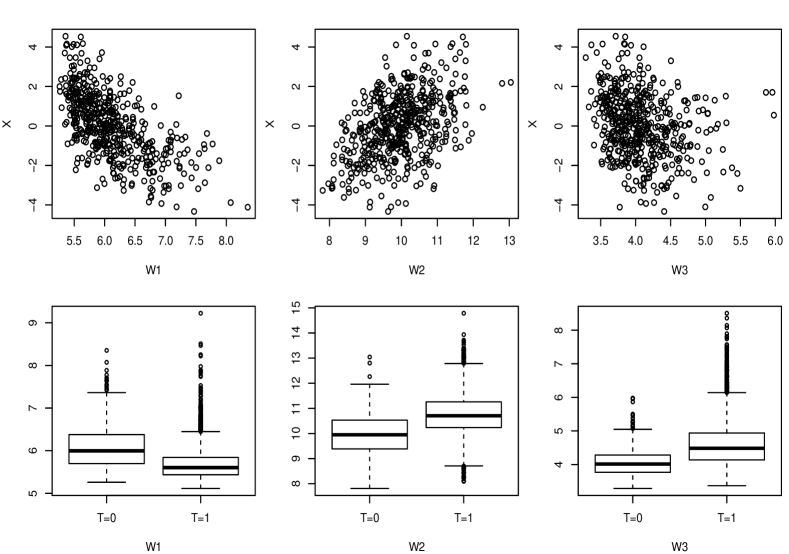

We constructed the OR model (34) with the identity link and set to either or , corresponding to a correct and misspecified OR model respectively. Similarly, we constructed the PS model (5) with the logistic link and set to or , corresponding to a correct and misspecified PS model respectively. Figure 1 shows the scatterplots of versus the transformed variables in the auxiliary data and the boxplots of between the two samples. From these plots, the OR model and PS models based on the transformed variables seem to be reasonable from the usual viewpoint of data analysis, even though they are misspecified.

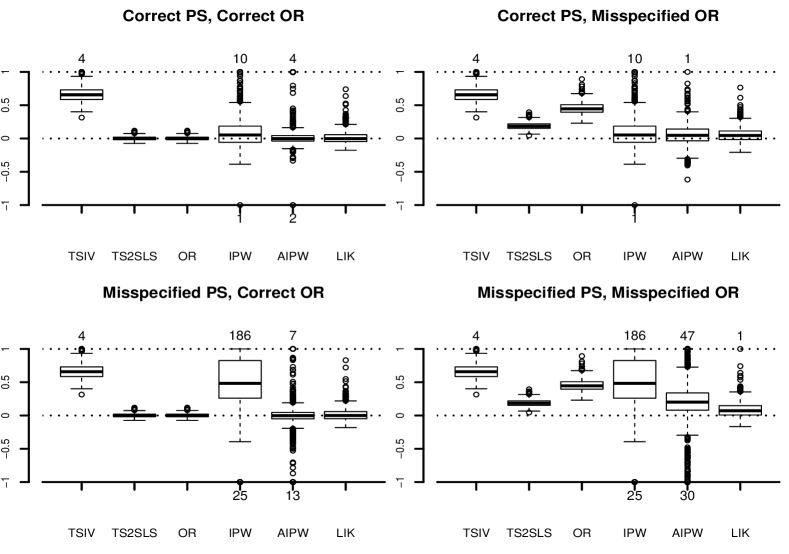

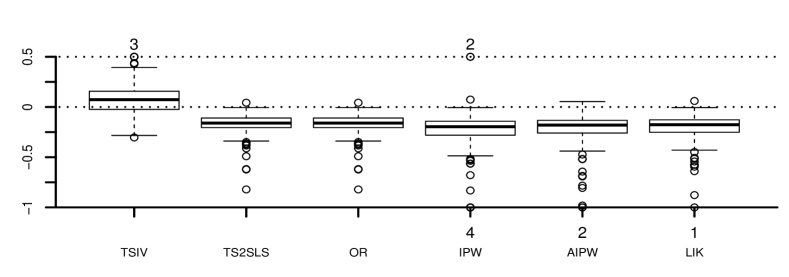

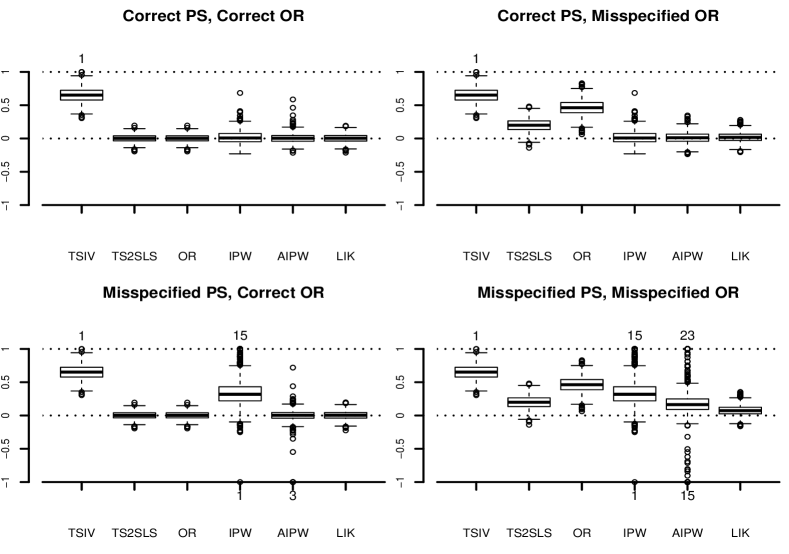

Table 1 summarizes the results based on 1000 repeated simulations for various estimates of for two-sample IV estimation under four scenarios of OR and PS model specification. Figure 2 shows the boxplots of the differences between the estimates of and the true value . The realizations of each estimator are censored within the range of the -axis, and the number of realizations that lie outside the range are marked next to the lower or the upper limit of -axis for each estimator.

| TSIV | TS2SLS | OR | IPW | AIPW | LIK | |

|---|---|---|---|---|---|---|

| Correct PS, Correct OR | 0.66330 | 0.00119 | 0.00138 | 0.09151 | 0.01079 | 0.01514 |

| (0.10858) | (0.02886) | (0.02891) | (0.42858) | (0.15080) | (0.09404) | |

| Correct PS, Misspecified OR | 0.66330 | 0.18837 | 0.45569 | 0.09151 | 0.05283 | 0.05582 |

| (0.10858) | (0.05056) | (0.08390) | (0.42858) | (0.16045) | (0.10712) | |

| Misspecified PS, Correct OR | 0.66330 | 0.00119 | 0.00138 | 0.63761 | -0.01244 | 0.01656 |

| (0.10858) | (0.02886) | (0.02891) | (2.19874) | (0.42315) | (0.09916) | |

| Misspecified PS, Misspecified OR | 0.66330 | 0.18837 | 0.45569 | 0.63761 | 0.04598 | 0.08604 |

| (0.10858) | (0.05056) | (0.08390) | (2.19874) | (3.26092) | (0.11847) |

The estimators of are taken from , , and in Eq. (33) where is set to , , , and with removed from (see Sections 4.2.1-4.2.2). The results for the estimator of based on are less satisfactory than based on and hence not shown. Each cell gives the empirical bias (upper) and standard deviation (lower) of the point estimator, from 1000 Monte Carlo samples.

|

The following remarks be drawn on the comparisons of various estimators.

-

•

The TSIV estimator (Angrist & Krueger 1992) does not depend on the PS model or OR model used, but it yields dramatic biases in all the four scenarios, because the common variables are distributed differently between the two samples. As discussed in Section 4.1, the TSIV estimator is generally consistent only when the two samples are drawn from the same population.

-

•

The TS2SLS and OR estimators are equivalent because as discussed in Section 4.2.1, and both are approximately unbiased, when OR model is correctly specified. On the other hand, these two estimators differ from each other, and both become biased, when OR model is misspecified.

-

•

The IPW estimator is approximately unbiased only when PS model is correctly specified and it has very large variances whether PS model is correctly specified or misspecified. Such a performance is typical of simple IPW estimators.

-

•

The AIPW estimator and LIK estimator are doubly robust: they are approximately unbiased when either PS model or OR model is correctly specified. As implied by local efficiency, the two estimators have similar variances to each other when both PS model and OR model are correctly specified. However, when PS model is correctly specified but OR model is misspecified, the LIK estimator has a smaller variance than AIPW by a factor about , due to intrinsic efficiency of the calibrated likelihood estimator used for estimating , the central quantity in two-sample IV estimation.

-

•

The LIK estimator also has a much smaller variance than AIPW, which yields a considerable number of outlying values, when the OR model is correctly specified but PS model is misspecified, although the two estimators are approximately unbiased in this scenario. This comparison shows that the LIK estimator can be less sensitive than AIPW to misspecification of the PS model.

6 Reassessing public housing projects

In order to improve the quality of housing and prospects of children in poor families, the US federal government has provided substantial housing assistance such as public housing projects to low-income families since 1937. However, public dissatisfaction with public housing projects remained high, largely in response to the rising cost of public housing and the high rates of crime, unemployment and school failure among public housing residents. But there was little evidence, beyond newspaper accounts, on the negative impact of public housing on children. In this context, Currie & Yelowitz (2000) investigated the effects of participation in public housing projects on the living quality and children’s educational attainment, using two-sample IV analysis which combines information from different data sources.

Currie & Yelowitz (2000) restricted the analysis to families with exactly two children under 18 in the household, for reasons as discussed later related to the validity of the instrumental variable used. To study the effects of project participation on various outcomes, the linear regression model (31) can be expressed as

| (38) |

where PROJ is project participation (), defined as 1 if a family lived in a housing project or 0 otherwise, and EXOG includes exogenous explanatory variables () such as the household head’s gender, age, race, education, marital status and the number of boys in the family and so on. The OUTCOME variable can be a measure of housing quality (overcrowding or housing density) or children’s educational attainment (grade repetition). For simplicity, we take “overcrowdedness” as the outcome of interest (), which is defined as if a family had two or less living/bedrooms and otherwise. See the Supplementary Materials for the results with housing density as the outcome. An important aspect of model (38) is that PROJ is considered an endogenous variable, possibly correlated with the error term , due to unobserved factors affecting both project participation and outcomes. In fact, families are eligible in projects if they had incomes at or below 50% of the area median. They may be more likely to live in substandard housing and their children may be more likely to experience negative outcomes, even if not participating in projects.

To control for the endogeneity, Currie & Yelowitz (2000) identified sex composition as an instrument () for project participation, defined as 1 if a family had a boy and a girl and 0 if two boys or two girls. Under the Department of Housing and Urban Development (HUD) rules, boys and girls cannot be required to share one bedroom except very young children. As a result, a family with two boys or two girls would be eligible for a two-bedroom apartment, whereas a family with a boy and a girl would be eligible for a three-bedroom apartment. In order for sex composition to be a valid instrument, it should influence project participation , but have no direct effect on the outcome, overcrowding, except through . To abstract from any effects due to the number of children, Currie & Yelowitz (2000) restricted the analysis to families with exactly two children under 18. In this case, families with a boy and a girl should be more likely to participate in projects, by the benefit of an extra room. On the other hand, Currie & Yelowitz (2000) pointed out that there was little reason to expect sex composition would affect overcrowding at least as they defined. In fact, families with two children of opposite sex would probably seek a change from two to three bedrooms, but not a change from one () to two () bedrooms.

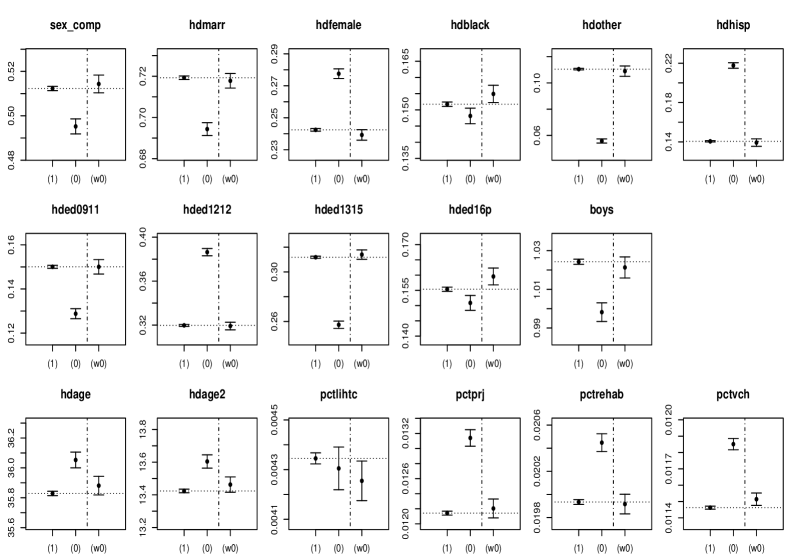

|

Label “(1)” or “(0)” denotes, respectively, the simple sample means from the Census or CPS data, and “(w0)” denotes the inverse probability weighed means from the CPS data.

Currie & Yelowitz (2000) showed that living in projects is associated with poorer outcomes, using data from the Survey of Income and Program Participation (SIPP). But they found that the SIPP sample is too small to yield reliable estimates using standard IV methods. Therefore, Currie & Yelowitz (2000) used the two-sample IV method to combine information from 1990 Census data and 1990 to 1995 waves of the March Current Population Survey (CPS). The Census data of size are the primary data, which contain the outcome for overcrowding, the instrumental variable for sex composition, and exogenous explanatory variables as seen from Table 4 of Currie & Yelowitz (2000). The CPS data of size are the auxiliary data, which contain the dummy variable for housing project participation and defined exactly the same as in Census data.

Figure 3 shows the simple sample means with error bars (one standard error) for all the common variables from the Census and CPS samples. The binary variables in the first two rows include information about the household head’s marital status, gender, race, education (“hdmarr”,“hdfemale”,“hdblack”, etc.). The continuous variable in the third row include the age of household head (“hdage”) and its squared value “hdage2”, the percentage of households in projects or other subsidized housing (“pctprj”), and so on. Except “hdblack”, “hded16p” and “pctlihtc”, all the variables have significantly different means at 5% level between the two samples. Therefore, the two samples are representative of different populations. In this situation, the TSIV estimator in Angrist & Krueger (1992) is generally biased, as discussed in Section 4.1 and illustrated in the simulation study.

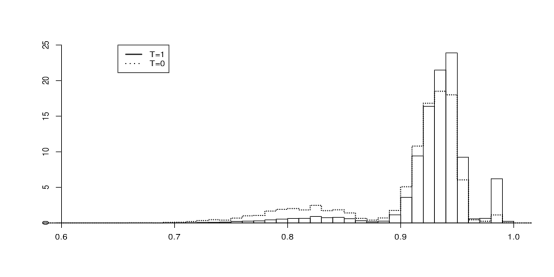

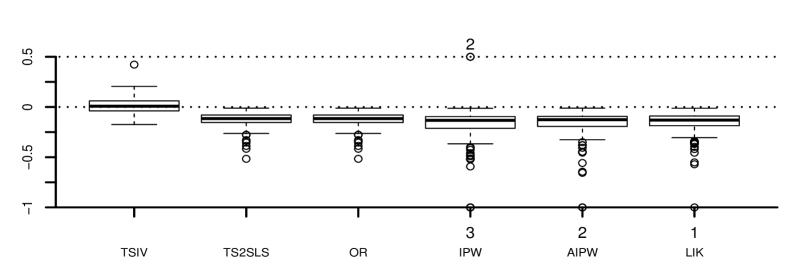

We apply the six estimators as studied in Section 5 to estimate in model (38). The OR model (34) is specified with the identity link and regressors . The PS model (5) is specified with the logistic link and including 1, the main effects , and the interaction hdother:hdhisp. Initially, the PS model with only the main effects is fitted, and covariate balance is examined by comparing the sample means from Census data and inverse probability weighted means from CPS data (Rosenbaum & Rubin 1984). The interaction term is then added to improve covariate balance as shown in Figure 3. Figure 4 presents the histograms of the fitted propensity scores separately for the two samples. As is consistent with Figure 3, the fitted propensity scores vary noticeably, about , indicating that the two samples are likely to be drawn from different populations.

|

Table 2 presents the point estimates of , the analytical and bootstrap standard errors, and 95% bootstrap confidence intervals. Bootstrap is performed by drawing bootstrap samples separately from the Census and CPS data in our two-sample setting. Figure 5 shows the boxplots of the six estimators of from 200 bootstrap samples. Similarly as in Figure 2, the number of realizations that lie outside the range of -axis are marked next to the lower or the upper limit of -axis for each estimator.

We obtain the same TS2SLS point estimate as Currie & Yelowitz (2000), , showing the households in public housing projects are less likely to be overcrowded. Because , the OR estimate is identical to TS2SLS as discussed in Section 4.2.1. Our bootstrap standard error is somewhat larger than the analytical standard error reported in Currie & Yelowitz (2000). The 95% bootstrap percentile confidence interval still falls to the left of 0, confirming that the effect of housing projects is likely to be positive in reducing overcrowdedness.

The TSIV estimate is positive with 95% confidence interval covering 0. But this result is probably biased as discussed above. Compared with the TS2SLS results, the IPW and AIPW estimates are associated with much larger standard errors, more serious outlying values, and wider confidence intervals. The LIK point estimate is between the TS2SLS and IPW/AIPW estimates, with bootstrap standard error also between the corresponding standard errors. The 95% bootstrap confidence interval from LIK, however, still falls to the left of 0, indicating that participation in housing projects could alleviate the overcrowdedness of households. This result agrees with that from TS2SLS, but can be seen to be more robust, allowing that either the linear regression in the first stage of TS2SLS is valid or the propensity score model is correctly specified for capturing differences between the two samples.

| TSIV | TS2SLS | OR | IPW | AIPW | LIK | |

|---|---|---|---|---|---|---|

| Point | 0.06900 | -0.15949 | -0.15949 | -0.20437 | -0.18821 | -0.18289 |

| SE | 0.12834 | — | 0.06241 | 0.11430 | 0.09785 | 0.09494 |

| boot.SE | 0.15408 | 0.10138 | 0.10138 | 3.57790 | 5.17650 | 0.18207 |

| boot.CI | (-0.220,0.394) | (-0.384,-0.049) | (-0.384,-0.049) | (-0.683,-0.033) | (-0.694,-0.043) | (-0.575,-0.043) |

Each column gives the point estimate (upper), the analytical and bootstrap (boot) standard errors (middle), and 95% bootstrap percentile confidence interval (lower) from 200 bootstrap samples. For comparison, the TS2SLS estimate is reported as , with analytical standard error , in Currie & Yelowitz (2000).

|

7 Conclusion

Combining information from two or more samples is important to various biomedical and economic studies. However, these samples may often differ in the marginal distributions of the common variables. Such differences need to be appropriately accounted for in order to draw valid and accurate inferences from the combined data.

We develop various estimators with improved statistical properties for moment restriction models with data combination from two samples, provided that the distributions of the missing data given the common variables are the same between the two samples. As a concrete application, we study the two-sample instrumental variable problem. The simulation study and reanalysis of public housing projects demonstrate the advantage of our estimators compared with existing estimators.

References

- Angrist & Krueger (1992) Angrist, J. D. and Krueger, A. B. (1992). The effect of age at school entry on educational attainment: An application of instrumental variables with moments from two samples. Journal of the American Statistical Association, 87:328–336.

- Bjorklund & Jantti (1997) Bjorklund, A. and Jantti, M. (1997). Intergenerational income mobility in sweden compared to the united states. American Economic Review, 87:1009–1018.

- Cao et al. (2009) Cao, W., Tsiatis, A. A., and Davidian, M. (2009). Improving efficiency and robustness of the doubly robust estimator for a population mean with incomplete data. Biometrika, 96:723–734.

- Chen et al. (2008) Chen, X., Hong, H., and Tarozzi, A. (2008). Semiparametric efficiency in GMM models with auxiliary data. The Annals of Statistics, 36:808–843.

- Choi et al. (2017) Choi, J., Gu, J., and Shen, S. (2017). Weak-instrument robust inference for two-sample instrumental variables regression. working paper.

- Currie & Yelowitz (2000) Currie, J. and Yelowitz, A. (2000). Are public housing projects good for kids? Journal of Public Economics, 75:99–124.

- Deville & Sarndal (1992) Deville, J.-C. and Sarndal, C.-E. (1992). Calibration estimators in survey sampling. Journal of the American Statistical Association, 87:376–382.

- Graham (2011) Graham, B. S. (2011). Efficiency bounds for missing data models with semiparametric restrictions. Econometrika, 79:437–452.

- Graham et al. (2016) Graham, B. S., de Xavier Pinto, C. C., and Egel, D. (2016). Efficient estimation of data combination models by the method of auxiliary-to-study tilting (AST). Journal of Business and Economic Statistics, 34:288–301.

- Hahn (1998) Hahn, J. (1998). On the role of the propensity score in efficient semiparametric estimation of average treatment effects. Econometrica, 66:315–331.

- Hirano et al. (2003) Hirano, K., Imbens, G. W., and Ridder, G. (2003). Efficient estimation of average treatment effects using the estimated propensity score. Econometrica, 71:1161–1189.

- Imbens (2004) Imbens, G. W. (2004). Nonparametric estimation of average treatment effects under exogeneity: A review. Review of Economics and Statistics, 86:4–29.

- Inoue & Solon (2010) Inoue, A. and Solon, G. (2010). Two-sample instrumental variables estimators. The Review of Economics and Statistics, 92:557–561.

- Kang & Schafer (2007) Kang, J. D. Y. and Schafer, J. L. (2007). Demystifying double robustness: A comparison of alternative strategies for estimating a population mean from incomplete data (with discussions). Statistical Science, 22:523–539.

- Khan & Tamer (2010) Khan, S. and Tamer, E. (2010). Irregular identificatin, support conditions, and inverse weight estimation. Econometrika, 78:2021–2042.

- Khawand & Lin (2015) Khawand, C. and Lin, W. (2015). Finite sample properties and empirical applicability of two-sample two-stage least squares. working paper.

- Klevmarken (1982) Klevmarken, W. A. (1982). Missing variables and two-stage least-squares estimation from more than one data set. Business and Economic Statistics Section, pages 156–161.

- Lahiri & Larsen (2005) Lahiri, P. and Larsen, M. D. (2005). Regression analysis with linked data. Journal of the American Statistical Association, 100:222–230.

- Newey (1990) Newey, W. K. (1990). Semiparametric efficiency bounds. Journal of Applied Econometrics, 5:99–135.

- Owen (2001) Owen, A. B. (2001). Empirical Likelihood. Chapman & Hall/CRC.

- Qin & Lawless (1994) Qin, J. and Lawless, J. (1994). Empirical likelihood and general estimating equations. The Annals of Statistics, 22:300–325.

- Ridder & Moffitt (2007) Ridder, G. and Moffitt, R. (2007). The econometrics of data combination. In Handbook of Econometrics (Vol 6B). North-Holland, New York.

- Robins & Ritov (1997) Robins, J. M. and Ritov, Y. (1997). Toward a curse of dimensionality appropriate (CODA) asymptotic theory for semi-parametric models. Statistics in Medicine, 16:285–319.

- Robins & Rotnitzky (2001) Robins, J. M. and Rotnitzky, A. (2001). Comment on the Bickel and Kwon article, ‘Inference for semiparametric models: Some questions and an answer’. Statistica Sinica, 11:920–936.

- Robins et al. (1994) Robins, J. M., Rotnitzky, A., and Zhao, L. P. (1994). Estimation of regression coefficients when some regressors are not always observed. Journal of the American Statistical Association, 89:846–866.

- Rosenbaum & Rubin (1983) Rosenbaum, P. R. and Rubin, D. B. (1983). The central role of the propensity score in observational studies for causal effects. Biometrika, 70:41–55.

- Rosenbaum & Rubin (1984) Rosenbaum, P. R. and Rubin, D. B. (1984). Reducing bias in observational studies using subclassification on the propensity score. Journal of the American Statistical Association, 79:516–524.

- Rubin & van der Laan (2008) Rubin, D. B. and van der Laan, M. J. (2008). Empirical efficiency maximization: Improved locally efficient covariate adjustment in randomized experiments and survival analysis. International Journal of Biostatistics, 4:1557–4679.

- Shu & Tan (2018) Shu, H. and Tan, Z. (2018). Improved estimation of average treatment effects on the treated: Local efficiency, double robustness, and beyond. arXiv:1808.01408.

- Tan (2006) Tan, Z. (2006). A distributonal approach for causal inference using propensity score. Journal of the American Statistical Association, 101:1619–1637.

- Tan (2007) Tan, Z. (2007). Comment: Understanding OR, PS and DR. Statistical Science, 22:560–568.

- Tan (2008) Tan, Z. (2008). Improved local efficiency and double robustness, comment on ‘empirical efficiency maximization: Improved locally efficient covariate adjustment in randomized experiments and survival analysis’ by Rubin and van der Laan. International Journal of Biostatistics, 4:Article 10.

- Tan (2010a) Tan, Z. (2010a). Bounded, efficient and doubly robust estimation with inverse weighting. Biometrika, 97:661–682.

- Tan (2010b) Tan, Z. (2010b). Nonparametric likelihood and doubly robust estimating equations for marginal and nested structural models. Can. J. Stat., 38:609–632.

- Tan (2011) Tan, Z. (2011). Efficient restricted estimators for conditional mean models with missing data. Biometrika, 98:663–684.

- Tan (2013) Tan, Z. (2013). Simple design-efficient calibration estimators for rejective and high-entropy sampling. Biometrika, 100:399–415.

- Tsiatis (2006) Tsiatis, A. A. (2006). Semiparametric Theory and Missing Data. Springer Series in Statistics. Springer.

Supplementary Material

for “Improved Methods for Moment Restriction Models with Marginally

Incompatible Data Combination and an Application to Two-sample

Instrumental Variable Estimation” by Shu & Tan

I Review of semiparametric theory

Proposition S1 restates the efficient influence functions from \citeappendChen2008 for estimation of under moment conditions (2) in three different settings.

Proposition S1 (\citealtappendChen2008)

Let , , and

where and . Under Assumptions (A1)–(A3),111It is originally assumed in \citeappendChen2008 that for all . However, the proofs in \citeappendChen2008 can be seen to still hold even when is 0 for some values , because only subjects with are inversely weighted by . the efficient influence function for estimation of is as follows.

-

(i)

The efficient influence function is

where .

-

(ii)

If the propensity score is known, then the efficient influence function is

where .

-

(iii)

If the propensity score is unknown but assumed to belong to a parametric family , then the efficient influence function is

where .

For two random vectors and , , i.e., the linear projection of onto .

As discussed in \citetappendChen2008, the semiparametric efficiency bounds satisfy , with strict inequalities holding in general, where , , and are respectively the variances of , , and . This ordering of efficiency bounds agrees with the usual comparison that the efficiency bound under a more restrictive model is no greater than under a less restrictive model. But this relationship between the efficiency bounds, , differs from the situation where the efficiency bounds remain the same when the propensity score is unknown, or assumed in a parametric family, or known, in various other missing-data problems (e.g., \citealtappendRobins1994, Tsiatis2006), such as the “verify-in-sample” case in \citeappendChen2008. This difference is related to the fact that the propensity score is ancillary for estimation of ATE, but not ancillary for estimation of ATT (\citealtappendHahn1998).

II Technical details

II.1 Preparation

Throughout, we make the following assumptions regarding the estimators for OR model (3), for PS model (5), and for augmented PS model (11), allowing for possible model misspecification (e.g., \citealtappendWhite1982).

-

(C1)

Assume that converges to a constant such that . Write . If model (3) is correctly specified, then . In general, and may differ from each other.

-

(C2)

Assume that converges to a constant such that

where , and the matrix is nonsingular. Write . If model (5) is correctly specified, then and . In general, and may differ from each other.

- (C3)

In addition, we assume that the following regularity conditions hold (e.g., \citealtappendRobins1994, Appendix B).

-

(C4)

Assumptions 1–2 in \citeappendNewey_Smith2004 hold for the vector of estimating functions .

-

(C5)

There exists a constant such that for all .

-

(C6)

There exists a constant such that for all and .

-

(C7)

There exists a neighborhood of such that , where for any matrix with element .

-

(C8)

There exists a neighborhood of such that and .

-

(C9)

There exists a neighborhood of such that and , where and .

II.2 Proof of Proposition 1

For convenience, write , , , , , , and .

First, we show the double robustness of . If PS model (5) is correctly specified, then and

and hence the left hand side of Eq. (8) is

This implies that is a consistent estimator of similarly as . If OR model (3) is correctly specified, then and

and hence the left hand side of Eq. (8) is

This implies that is a consistent estimator of similarly as .

Second, we prove the local nonparametric efficiency of . If OR model (3) and PS model (5) are correctly specified, then by Slutsky Theorem, the left hand side of Eq. (8) is

By a Taylor expansion for about , we have

and hence

| (S1) |

Therefore, achieves the nonparametric variance bound when both PS model and OR model are correctly specified.

Third, we prove the local semiparametric efficiency of . By similar arguments as in the derivation of Eq. (S1), when OR model (3) and PS model (5) are correctly specified, we have

| (S2) |

By a Taylor expansion for about , we have

Combining the preceding two expansions shows that achieves the semiparametric variance bound when both OR and PS model are correctly specified.

II.3 Proof of Proposition 2

First, it is straightforward to show that , where and , , , and are defined as , , , and respectively but with and in place of and throughout.

Second, we show the local nonparametric efficiency and double robustness of . By the discussion in Section 2.3.1, it suffices to show that if OR model (3) is correctly specified, then is asymptotically equivalent, up to , to the solution of Eq. (16). By construction, is a linear combination of variables in , i.e., for some constant vector . Then also holds for the same vector . If OR model (3) is correctly specified, then and . By direct calculation, we have

and hence the left hand side of Eq. (14) is asymptotically equivalent, to the first order, to the left hand side of Eq. (16).

Third, we show the intrinsic efficiency of among the class of estimators, denoted by , that are solutions to (15). By similar arguments as in the derivation of Eqs. (S1) and (S2), when PS model (5) is correctly specified, we have

where is fixed at the true in , , and . By applying Lemma 1 in \citetappendShu2015 with replaced by , by , and by , we have

Inside above, the first term is uncorrelated with the second term , which is independent of . Moreover, the first term can be expressed as for some constant vector , because each variable in is a linear combination of variables in by construction. By combining these two facts, the asymptotic variance of is minimized when is equal to

But to make equal to , it suffices to set , because is uncorrelated with and hence . If PS model (5) is correctly specified, then . Therefore, is intrinsically efficient among the class of estimators .

II.4 Proof of Corollary 1

The comparison follows from Proposition 2 directly for , which falls in the class (15) with . The estimating equation (17) for can be rewritten as

which is of the form (15) for some suitable , because both and are included in . For the estimator , if PS model (5) is correctly specified, then converges to 0 in probability and hence

by a Taylor expansion of . Moreover, a Taylor expansion of the estimating equation for gives

Therefore, if PS model (5) is correctly specified, then is, up to , a solution to estimating equations of the form (15) for some suitable . The conclusion then follows from Proposition 2.

II.5 Derivation of empirical likelihood estimates

By standard calculation (\citealtappendQinlawless1994), the empirical likelihood estimate of subject to constraints (18) is

where is a maximizer of the function

Write , , and for . By direct calculation, can be reexpressed as

which equals up to an additive constant. Therefore, is a maximizer of .

II.6 Proof of Proposition 3

We need only to show that if PS model (5) is correctly specified, then is asymptotically equivalent, to the first order, to . If PS model (5) is correctly specified, the left hand side of Eq. (23) can be approximated as

by a Taylor expansion for about and the fact that , similarly as in the asymptotic expansion of the calibrated likelihood estimator in \citetappendTan2010. Moreover, if PS model (5) is correctly specified, then converges to in probability and

by a Taylor expansion for about , similarly as in the asymptotic expansion of the non-calibrated likelihood estimator in \citetappendTan2010. The desired result for then follows from the preceding the expansions.

III Additional simulation results

We present additional simulation results in the setup of Section 5, but with Eq. (37) modified to

or modified to

That is, the coefficient of the instrument is set to or . The correlation between and the instrument is , , or respectively in the case of IV coefficient 1, , or , corresponding to an increasingly weaker instrument.

Table S1 and Figure S1 summarize the results in the case of IV coefficient , and Table S2 and Figure S2 summarize the results in the case of IV coefficient , similarly as Table 1 and Figure 2 in the case of IV coefficient . All estimators lead to larger standard errors when the coefficient (or strength) of the instrument decreases. But the relative performances of these estimators in the case of IV coefficient or are similar to those in the case of IV coefficient .

| TSIV | TS2SLS | OR | IPW | AIPW | LIK | |

|---|---|---|---|---|---|---|

| Correct PS, Correct OR | 0.70214 | 0.00177 | 0.00206 | 0.08849 | 0.07985 | 0.02405 |

| (0.12170) | (0.03621) | (0.03629) | (0.46412) | (1.74026) | (0.13319) | |

| Correct PS, Misspecified OR | 0.70214 | 0.13775 | 0.48176 | 0.08849 | 0.06736 | 0.07169 |

| (0.12170) | (0.05393) | (0.10262) | (0.46412) | (0.20352) | (0.14197) | |

| Misspecified PS, Correct OR | 0.70214 | 0.00177 | 0.00206 | -0.48397 | 0.01444 | 0.02720 |

| (0.12170) | (0.03621) | (0.03629) | (33.07874) | (0.46850) | (0.14907) | |

| Misspecified PS, Misspecified OR | 0.70214 | 0.13775 | 0.48176 | -0.48397 | 0.16885 | 0.13498 |

| (0.12170) | (0.05393) | (0.10262) | (33.07874) | (2.12672) | (0.19056) |

The estimators of are taken from , , and in Eq. (33) where is set to , , , and with removed from . Each cell gives the empirical bias (upper) and standard deviation (lower) of the point estimator, from 1000 Monte Carlo samples.

|

| TSIV | TS2SLS | OR | IPW | AIPW | LIK | |

|---|---|---|---|---|---|---|

| Correct PS, Correct OR | 0.76775 | 0.00300 | 0.00353 | 0.03036 | -0.01200 | 0.02697 |

| (0.14729) | (0.04866) | (0.04884) | (2.40077) | (3.51675) | (0.40818) | |

| Correct PS, Misspecified OR | 0.76775 | 0.04516 | 0.53005 | 0.03036 | 0.55899 | 0.10943 |

| (0.14729) | (0.05885) | (0.14107) | (2.40077) | (18.90818) | (0.34001) | |

| Misspecified PS, Correct OR | 0.76775 | 0.00300 | 0.00353 | -4.37817 | -0.00123 | 0.03718 |

| (0.14729) | (0.04866) | (0.04884) | (156.98569) | (1.38405) | (0.27388) | |

| Misspecified PS, Misspecified OR | 0.76775 | 0.04516 | 0.53005 | -4.37817 | 0.63544 | 0.21258 |

| (0.14729) | (0.05885) | (0.14107) | (156.98569) | (9.17403) | (0.68056) |

The estimators of are taken from , , and in Eq. (33) where is set to , , , and with removed from . Each cell gives the empirical bias (upper) and standard deviation (lower) of the point estimator, from 1000 Monte Carlo samples.

|

We present additional simulation results with the primary and auxiliary data sizes and . The true propensity score is

Figures S3 and S4 and Table S3 correspond to Figures 1 and 2 and Table 1 respectively.

The TS2SLS and OR estimators have larger variances, whereas the IPW, AIPW, and LIK estimators have smaller variances, than in the case of and , because the variability of IPW based estimators is affected mainly by the auxiliary data size. Nevertheless, the relative performances of the estimates of are qualitatively the same as in the case of and .

|

| TSIV | TS2SLS | OR | IPW | AIPW | LIK | |

|---|---|---|---|---|---|---|

| Correct PS, Correct OR | 0.65155 | 0.00235 | 0.00235 | 0.01568 | 0.00526 | 0.00410 |

| (0.11001) | (0.05461) | (0.05462) | (0.09699) | (0.06781) | (0.06109) | |

| Correct PS, Misspecified OR | 0.65155 | 0.19988 | 0.46434 | 0.01568 | 0.01274 | 0.01849 |

| (0.11001) | (0.09562) | (0.11383) | (0.09699) | (0.08382) | (0.07263) | |

| Misspecified PS, Correct OR | 0.65155 | 0.00235 | 0.00235 | 0.46519 | -0.03335 | 0.00441 |

| (0.11001) | (0.05461) | (0.05462) | (2.41001) | (0.97861) | (0.06182) | |

| Misspecified PS, Misspecified OR | 0.65155 | 0.19988 | 0.46434 | 0.46519 | 0.19439 | 0.07495 |

| (0.11001) | (0.09562) | (0.11383) | (2.41001) | (1.10682) | (0.07773) |