Randomized sketch descent methods for non-separable linearly constrained optimization

Abstract

In this paper we consider large-scale smooth optimization problems with multiple linear coupled constraints. Due to the non-separability of the constraints, arbitrary random sketching would not be guaranteed to work. Thus, we first investigate necessary and sufficient conditions for the sketch sampling to have well-defined algorithms. Based on these sampling conditions we developed new sketch descent methods for solving general smooth linearly constrained problems, in particular, random sketch descent and accelerated random sketch descent methods. From our knowledge, this is the first convergence analysis of random sketch descent algorithms for optimization problems with multiple non-separable linear constraints. For the general case, when the objective function is smooth and non-convex, we prove for the non-accelerated variant sublinear rate in expectation for an appropriate optimality measure. In the smooth convex case, we derive for both algorithms, non-accelerated and accelerated random sketch descent, sublinear convergence rates in the expected values of the objective function. Additionally, if the objective function satisfies a strong convexity type condition, both algorithms converge linearly in expectation. In special cases, where complexity bounds are known for some particular sketching algorithms, such as coordinate descent methods for optimization problems with a single linear coupled constraint, our theory recovers the best-known bounds. We also show that when random sketch is sketching the coordinate directions randomly produces better results than the fixed selection rule. Finally, we present some numerical examples to illustrate the performances of our new algorithms.

1 Introduction

During the last decade first order methods, that eventually utilize also some curvature information, have become the methods of choice for solving optimization problems of large sizes arising in all areas of human endeavor where data is available, including machine learning [21, 27, 31], portfolio optimization [17, 6], internet and multi-agent systems [10], resource allocation [18, 40] and image processing [39]. These large-scale problems are often highly structured (e.g., sparsity in data, separability in objective function, convexity) and it is important for any optimization method to take advantage of the underlying structure. It turns out that gradient-based algorithms can really benefit from the structure of the optimization models arising in these recent applications [5, 22].

Why random sketch descent methods? The optimization problem we consider in this paper has the following features: the size of data is very large so that usual methods based on whole gradient/Hessian computations are prohibitive; moreover the constraints are coupled. In this case, an appropriate way to approach these problems is through sketch descent methods due to their low memory requirements and low per-iteration computational cost. Sketching is a very general framework that covers as a particular case the (block) coordinate descent methods [15] when the sketch matrix is given by sampling columns of the identity matrix. Sketching was used, with a big success, to either decrease the computation burden when evaluating the gradient in first order methods [22] or to avoid solving the full Newton direction in second order methods [24]. Another crucial advantage of sketching is that for structured problems it keeps the computation cost low, while preserving the amount of data brought from RAM to CPU as for full gradient or Newton methods, and consequently allows for better CPUs utilization on modern multi-core machines. Moreover, in many situations general sketching keeps the per-iteration running-time almost unchanged when compared to the particular sketching of the identity matrix (i.e. comparable to coordinate descent settings). This, however, leads to a smaller number of iterations needed to achieve the desired quality of the solution as observed e.g. in [25].

In second order methods sketching was used to either decrease the computation cost when evaluating the full Hessian or to avoid solving the full Newton direction. In [24, 3] a Newton sketch algorithm was proposed for unconstrained self-concordant minimization, which performs an approximate Newton step, wherein each iteration only a sub-sampled Hessian is used. This procedure significantly reduces the computation cost, and still guarantees superlinear convergence for self-concordant objective functions. In [25], a random sketch method was used to minimize a smooth function which admits a non-separable quadratic upper-bound. In each iteration a block of coordinates was chosen and a subproblem involving a random principal submatrix of the Hessian of the quadratic approximation was solved to obtain an improving direction.

In first order methods particular sketching was used, by choosing as sketch matrix (block) columns of the identity matrix, in order to avoid computation of the full gradient, leading to coordinate descent framework. The main differences in all variants of coordinate descent methods consist in the criterion of choosing at each iteration the coordinate over which we minimize the objective function and the complexity of this choice. Two classical criteria used often in these algorithms are the cyclic and the greedy coordinate search, which significantly differs by the amount of computations required to choose the appropriate index. For cyclic coordinate search estimates on the rate of convergence were given recently in [2, 8, 32], while for the greedy coordinate search (e.g. Gauss-Southwell rule) the convergence rates were given in [35, 15]. Another approach is based on random choice rule, where the coordinate search is random. Complexity results on random coordinate descent methods for smooth convex objective functions were obtained in [22, 18]. The extension to composite convex objective functions was given e.g. in [27, 19, 14, 21, 28]. These methods are inherently serial. Recently, accelerated [5, 4], parallel [19, 29, 34], asynchronous [13] and distributed implementations [33, 16] of coordinate descent methods were also analyzed. Let us note that the idea of sketching or sub-sampling was also successfully applied in various other settings, including [37, 30, 7].

Related work. However, most of the aforementioned sketch descent methods assume essentially unconstrained problems, which at best allow separable constraints. In contrast, in this paper we consider sketch descent methods for general smooth problems with linear coupled constraints. Particular sketching-based algorithms, such as greedy coordinate descent schemes, for solving linearly constrained optimization problems were investigated in [35, 15], while more recently in [1] a greedy coordinate descent method is developed for minimizing a smooth function subject to a single linear equality constraint and additional bound constraints on the decision variables. Random coordinate descent methods that choose at least 2 coordinates at each iteration have been also proposed recently for solving convex problems with a single linear coupled constraint in [18, 21, 20]. In all these papers, detailed convergence analysis is provided for both, convex and non-convex settings. Motivated by the work in [20] several recent papers have tried to extended the random coordinate descent settings to multiple linear coupled constraints [6, 21, 26]. In particular, in [26] an extension of the 2-random coordinate descent method from [20] has been analyzed, however under very conservative assumptions, such as full rank condition on each block of the matrix describing the linear constraints. In [6] a particular sketch descent method is proposed, where the sketch matrices specify arbitrary subspaces that need to generate the kernel of the matrix describing the coupled constraints. However, in the large-scale context and for general linear constraints it is very difficult to generate such sketch matrices. Another strand of this literature develops and analysis center-free gradient methods [40], augmented Lagrangian based methods [9] or Newton methods [38].

Our approach and contribution. Our approach introduces general sketch descent algorithms for solving large-scale smooth optimization problems with multiple linear coupled constraints. Since we have non-separable constraints in the problem formulation, a random sketch descent scheme needs to consider new sampling rules for choosing the coordinates. We first investigate conditions on the sketching of the coordinates over which we minimize at each iteration in order to have well-defined algorithms. Based on these conditions we develop new random sketch descent methods for solving our linearly constrained convex problem, in particular, random sketch descent and accelerated random sketch descent methods. However, unlike existing methods such as coordinate descent, our algorithms are capable of utilizing curvature information, which leads to striking improvements in both theory and practice.

Our contribution. To this end, our main contribution can be summarized as follows:

(i) Since we deal with optimization problems having non-separable constraints we need to design sketch descent schemes based on new sampling rules for choosing the sketch matrix. We derive necessary and sufficient conditions on the sketching of the coordinates over which we minimize at each iteration in order to have well-defined algorithms. To our knowledge, this is the first complete work on random sketch descent type algorithms for problems with more than one linear constraint. Our theoretical results consist of new optimization algorithms, accompanied with global convergence guarantees to solve a wide class of non-separable optimization problems.

(ii) In particular, we propose a random sketch descent algorithm for solving such general optimization problems. For the general case, when the objective function is smooth and non-convex, we prove sublinear rate in expectation for an appropriate optimality measure. In the smooth convex case we obtain in expectation an -accurate solution in at most iterations, while for strongly convex functions the method converges linearly.

(iii) We also propose an accelerated random sketch descent algorithm. From our knowledge, this is the first analysis of an accelerated variant for optimization problems with non-separable linear constraints. In the smooth convex case we obtain in expectation an -accurate solution in at most iterations. For strongly convex functions the new random sketch descent method converges linearly.

Let us emphasize the following points of our contribution. First, our sampling strategies are for multiple linear constraints and thus very different from the existing methods designed only for one linear constraint. Second, our (accelerated) sketch descent schemes are the first designed for this class of problems. Thirdly, our non-accelerated sketch descent algorithm covers as special cases some methods designed for problems with a single linear constraint and coordinate sketch. In these special cases, where convergence bounds are known, our theory recovers the best known bounds. We also illustrate, that for some problems, random sketching of the coordinates produces better results than deterministic selection of them. Finally, our theory can be used to further develop other methods such as Newton-type schemes.

Paper organization. The rest of this paper is organized as follows. Section 2 presents necessary and sufficient conditions for the sampling of the sketch matrix. Sections 3 provides a full convergence analysis of the random sketch descent method, while Section 4 extends this convergence analysis to an accelerated variant. In Section 5 we show the benefits of general sketching over fixed selection of coordinates.

1.1 Problem formulation

We consider the following large-scale general smooth optimization problem with multiple linear coupled constraints:

| (1) |

where is a general differentiable function and , with , is such that the feasible set is nonempty. The last condition is satisfied if e.g. has full row rank. The simplest case is when , that is we have a single linear constraint as considered in [1, 18, 21, 20]. Note that we do not necessarily impose to be a convex function. From the optimality conditions for our optimization problem (1) we have that is a stationary point if there exists some such that:

However, if is convex, then any satisfying the previous optimality conditions is a global optimum for optimization problem (1). Let us define the set of these points. Therefore, is a stationary (optimal) point if it is feasible and satisfies the condition:

1.2 Motivation

We present below several important applications from which the interest for problems of type (1) stems.

1.2.1 Page ranking

This problem has many applications in google ranking, network control, data analysis [10, 22, 18]. For a given graph let be its incidence matrix, which is sparse. Define , where denotes the vector with all entries equal to . Since , i.e. the matrix is column stochastic, the goal is to determine a vector such that: and . This problem can be written directly in optimization form:

which is a particular case of our optimization problem (1) with and sparse matrix.

1.2.2 Machine learning

Consider the optimization problem associated with the loss minimization of linear predictors without regularization for a training data set containing observations [31]:

Here is some loss function, e.g. SVM , logistic regression , ridge regression , regression with the absolute value and support vector regression for some predefined insensitivity parameter . Moreover, in classification the labels , while in regression . Further, let denote the Fenchel conjugate of . Then the dual of this problem becomes:

where . Clearly, this problem fits into our model (1), with representing the number of features, the number of training data, and the objective function is separable.

1.2.3 Portfolio optimization

In the basic Markowitz portfolio selection model [17], see also [6] for related formulations, one assumes a set of assets, each with expected returns , and a covariance matrix , where is the covariance between returns of assets and . The goal is to allocate a portion of the budget into different assets, i.e. represents a portion of the wealth to be invested into asset , leading to the first constraint: . Then, the expected return (profit) is and the variance of the portfolio can be computed as . The investor seeks to minimize risk (variance) and maximize the expected return, which is usually formulates as maximizing profit while limiting the risk or minimizing risk while requiring given expected return. The later formulation can be written as:

which clearly fits again into our optimization model (1) with . We can further assume that each asset belongs exactly to one class , e.g. financials, health care, industrials, etc. The investor would like to diversify its portfolio in such a way that the net allocation in class is : for all , where if asset is in class and otherwise. One can observer that in this case we get a similar problem as above, but with additional linear constraints ().

2 Random sketching

It is important to note that stochasticity enters in our algorithmic framework through a user-defined distribution describing an ensemble of random matrices (also called sketch matrices). We assume that , in fact we usually require and note that can also be random (i.e. the can return matrices with different ). Our schemes and the underlying convergence theory support virtually all thinkable distributions. The choice of the distribution should ideally depend on the problem itself, as it will affect the convergence speed. However, for now we leave such considerations aside. The basic idea of our algorithmic framework consists of a given feasible , a sample sketch matrix and a basic update of the form:

| (2) |

where the requirement ensures that the new point will remain feasible. Clearly, one can choose a distribution which will not guarantee convergence to stationary/optimal point. Therefore, we need to impose some minimal necessary conditions for such a scheme to be well-defined. In particular, in order to avoid trivial updates, we need to choose such that the homogeneous linear system admits also nontrivial solutions, that is we require:

| (3) |

Moreover, since for any feasible an optimal solution satisfies , it is necessary to require that with our distribution we can generate :

| (4) |

Note that the geometric conditions (3)-(4) are only necessary for a sketch descent type scheme to be well-defined. However, for a discrete probability distribution, having e.g. the property that for all , condition (4) is also sufficient. In Section 2.3 (see Assumption 3) we will provide sufficient conditions for a general probability distribution in order to obtain well-defined algorithms based on such sketching. Below we provide several examples of distributions satisfying our geometric conditions (3)-(4).

2.1 Example 1 (finite case)

Let us consider a finite (or even countable) probability distribution . Further, let be a particular solution of the linear system . For example, if denotes the pseudo-inverse of the matrix , then we can take . Moreover, by the properties of the pseudo-inverse, is a projection matrix onto , that is . Therefore, any solution of the linear system can be written as:

for any . Thus, we may consider a finite (the extension to countable case is straightforward) set of matrices endowed with a probability distribution for all and condition (4) requires that the span of the image spaces of contains or is equal to :

| (5) |

In particular, we have several choices for the sampling for a finite distribution:

-

1.

If one can compute a basis for , then we can take as random sketch matrix any block of elements of this basis endowed with some probability (for the case the matrix represents a single element of this basis generating ). This sampling was also considered in [6]. Clearly, in this particular case condition (3) and condition (4) or equivalently (5) hold since .

-

2.

However, for a general matrix it is difficult to compute a basis of . A simple alternative is to consider then any -tuple , with , and the corresponding random sketch matrix , where denotes the th column of the identity matrix , with some probability distribution over the set of -tuples in . It is clear that for this choice condition (3) and condition (4) or equivalently (5) also hold. For the particular case when we have a single linear coupled constraint, i.e. , we can take random matrices also considered e.g. in [18]. This particular sketch matrix based on sampling columns of the identity matrix leads to coordinate descent framework. However, the other examples (including those from Section 2.2) show that our sketching framework is more general than coordinate descent.

-

3.

Instead of working with the matrix , as considered previously, we can take any orthogonal or full rank matrix having the columns and thus forming a basis of . Then, we can consider tuples , with , and the corresponding random sketch matrix , with some probability distribution over the set of -tuples in . It is clear that for this choice of the random sketch matrices the condition (3) and condition (4) or equivalently (5) still hold.

2.2 Example 2 (infinite case)

Let us now consider a continuous (uncountable) probability distribution . We can consider in this case two simple sampling strategies:

-

1.

If one can sample easily a random matrix such that , then we can choose one or several columns from this matrix as a sketch matrix . In this case .

-

2.

Alternatively, we can sample random full rank matrices in and then define to be random columns. Furthermore, since it is known that random Gaussian matrices are full rank almost surely, then we can define to be a random Gaussian matrix. Similarly, we can consider random uniform matrices and define e.g. .

A sufficient condition for a well-defined sampling in the infinite case is to ensure that in expectation one can move in any direction in . Considering the general update rule (2), we see that if we sample , then our update can be only for some . Now, we also have a condition, that we want to stay in the , and therefore cannot be anything, but has to be chosen such that . Now, this restricts the set of possible ’s to be such that:

for some . Recall, that we allow to be also random, hence to derive the sufficient condition we need to have some quantity with dimension independent on . Note that each can be represented as for some (possibly non-unique) . Therefore, we see that if is sampled, then we can move in the direction:

hence, we have the ability to move in . Now, the condition to be able to move in can be expressed as requiring that on expectation we can move anywhere in :

| (6) |

provided that the expectation exists and is finite. Note, that this condition must hold also for a discrete probability distribution, however the condition (4) is more intuitive in the discrete case. In the next section we provide algebraic sufficient conditions on the sampling for a general probability distribution in order to obtain well-defined algorithms.

2.3 Sufficient conditions for sketching

It is well known that in order to derive any reasonable convergence guarantees for a minimization scheme we need to impose some smoothness property on the objective function. Therefore, throughout the paper we consider the following blanket assumption on the smoothness of :

Assumption 1.

For any feasible there exists a positive semidefinite matrix such that is positive definite on and the following inequality holds:

| (7) |

Note that for a general (possibly non-convex) differentiable function the smoothness inequality (7) does not imply that the objective function has Lipschitz continuous gradient, so our assumption is less conservative than requiring Lipchitz gradient assumption. However, when is convex the condition (7) is equivalent with Lipschitz continuity of the gradient of on [23]. In particular, if for some Lipschitz constant we recover the usual definition of Lipschitz continuity of the gradient for the class of convex functions. Our sketching methods derived below are based on (7) and therefore they have the capacity to utilize curvature information. In particular, if the objective function is quadratic, our methods can be interpreted as novel extensions to more general optimization models of the recently introduced iterative Hessian sketch method for minimizing self-concordant objective functions [24]. The reader should also note that we can further relax the condition (7) and require smoothness of with respect to any image space generated by the random matrix . More precisely, it is sufficient to assume that for any sample there exists a positive semidefinite matrix such that is positive definite on and the following inequality holds:

Note that if for all we recover the relation (7). For simplicity of the exposition in the sequel we assume (7) to be valid, although all our convergence results can be also extended under previous smoothness condition given in terms of .

From the above discussion it is clear that the direction in our basic update (2) needs to be in the kernel of matrix . However, it is well known that the projection onto is given by the projection matrix:

Clearly, we have . Let us further define the matrix:

| (8) |

The matrix has some important properties that we will derive below since they are useful for algorithm development. First we observe that:

Lemma 2.

For any probability distribution the matrix is symmetric (), positive semidefinite (), and for any we have , that is . Moreover, the following identity holds .

Proof.

It is clear that is positive semidefinite matrix since is assumed positive semidefinite. It is well-known that for any given matrix its pseudo-inverse satisfies and . Now, for the first statement given the expression of it is sufficient to prove that for . However, if then there exists such that and consequently we have:

where in the last equality we used the first property of pseudo-inverse . For the second part of the lemma we use the expression of and the second property of the pseudo-inverse applied to the matrix , that is:

which concludes our statements. ∎

Now, since the random matrix is positive semidefinite, then we can define its expected value, which is also a symmetric positive semidefinite matrix:

| (9) |

In the sequel we also consider the following assumption on the expectation matrix :

Assumption 3.

We assume that the distribution is chosen such that has a finite mean, that is the matrix is well defined, and positive definite (notation ) on .

As we will see below, Assumption 3 is a sufficient condition on the probability distribution in order to ensure convergence of our algorithms that will be defined in the sequel. To our knowledge this algebraic characterization of the probability distribution defining the sketch matrices for problems with multiple non-separable linear constraints seems to be new.

Note that the necessary condition (3) holds provided that . Indeed, from Lemma (2) we have for all and . Therefore, we get that and we know that . Let , , then there exists unique and such that . Moreover, we have , i.e. , which implies that . Thus, and . From the last relation, we get:

Moreover, from the definition of the symmetric matrix we have , which combined with the previous relation leads to:

and consequently proving that the condition (3) holds provided that . Moreover, we can show that the necessary condition (4) holds if satisfies Assumption 3:

Lemma 4.

Proof.

Note that Assumption 3 holds, i.e. on , if and only if on . Moreover, for any non-zero , we have , that is . In conclusion, we get . But, , from which we can conclude (4).

For the second part we use again Lemma (2): for all . This means that . The other inclusion follows by reducing to absurd. Assume that there exists such that , or equivalently for some . However, note that on if and only if on , which contradicts our assumption. In conclusion, the second statement holds. Finally, it is well-known that is an orthogonal projector onto and the rest follows from standard algebraic arguments. ∎

The primal-dual ”norms”. Since the matrix is positive semidefinite, matrix is also positive semidefinite. Moreover, from Lemma 2 we conclude that . In the sequel we assume that such that is a positive definite matrix on and consequently on (see Assumption 3). Then, we can define a norm induced by the matrix on or even . This norm will be used subsequently for measuring distances in the subspace . More precisely, we define the primal norm induced by the positive semidefinite matrix as:

Note that for all (see Lemma 2) and for all . On the subspace we introduce the extended dual norm:

Using the definition of conjugate norms, the Cauchy-Schwartz inequality holds:

| (10) |

Lemma 5.

Under Assumption 3 the primal and dual norms have the following expressions:

| (11) |

Proof.

Let us consider any . Then, the dual norm can be computed for any as follows:

We obtain an extended dual norm that is well defined on the subspace :

| (12) |

The eigenvalue decomposition of the positive semidefinite matrix can be written as , where are its positive eigenvalues and the columns of orthogonal matrix are the corresponding eigenvectors, generating and generating . Then, we have:

where are the nonzero eigenvalues of symmetric matrix . From (12) it follows that our newly defined dual norm has the following closed form:

where denotes the pseudoinverse of matrix . ∎

The following example shows that the 2-coordinate sampling proposed in [20] (in the presence of a single linear constraint ) is just a special case of the sketching analyzed in this paper:

Example 6.

Let us consider the following optimization problem:

In this case, assuming that each scalar function has Lipschitz continuous gradient, then . Moreover, we can take any random pair of coordinates with and consider the particular sketch matrix . Note that, for simplicity, we focus here on Lipschitz dependent probabilities for choosing the pair , that is with . Following basic derivations we get:

| (13) |

Clearly, on and thus Assumption 3 holds. Similarly, we can compute explicitly and for the fixed selection of the pair of coordinates with .

3 Random Sketch Descent (RSD ) algorithm

For the large-scale optimization problem (1) methods which scale cubically, or even quadratically, with the problem size is already out of the question; instead, linear scaling of the computational costs per-iteration is desired. Clearly, optimization problem (1) can be solved using projected first order methods, such as gradient or accelerated gradient, both algorithms having comparable cost per iteration [23]. In particular, both methods require the computation of the full gradient and finding the optimal solution of a subproblem with quadratic objective over the subspace :

| (14) |

For example, for the projected gradient method since we assume positive definite on (see Assumption 1), then the previous subproblem has a unique solution leading to the following gradient iteration:

| (15) |

where is obtained by replacing in the definition of the matrix . However, for very large even the first iteration is not computable, since the cost of computing is cubic in the problem dimension (i.e. of order operations) for a dense matrix . Moreover, since usually is a dense matrix regardless of the matrix being dense or spare, the cost of the subsequent iterations is quadratic in the problem size (i.e. ). Therefore, the development of new optimization algorithms that target linear cost per iteration and nearly dimension-independent convergence rate is needed. These properties can be achieved using the sketch descent framework. In particular, let us assume that the initial iterate is a feasible point, i.e. . Then, the first algorithm we propose, Random Sketch Descent (RSD ) algorithm, chooses at each iteration a random sketch matrix according to the probability distribution and find a new direction solving a simple subproblem (see Algorithm 1 below).

Let us explain the update rule of our algorithm RSD . Note that the new direction in the update of RSD is computed from a subproblem with quadratic objective over the subspace that it is simpler than subproblem (14) corresponding to the full gradient:

We observe that from the feasibility condition we can compute as:

for some . Then, the constrains will not be violated. Now, let’s plug this into the objective function of the subproblem, to obtain an unconstrained problem in :

Then, from the first order optimality conditions we obtain that:

and hence we can define as

In conclusion we obtain the following update rule for our RSD algorithm:

| (16) |

After iterations of the RSD algorithm, we generate a random output , which depends on the observed implementation of the random variable:

Let us define the expected value of the objective function w.r.t. :

Next, we compute the decrease of the objective function after one random step:

| (17) |

Then, we obtain the following strict decrease for the objective function in the conditional expectation:

| (18) |

provided that is not optimal. This holds since we assume that on and since any feasible satisfying is optimal for the original problem. Therefore, RSD algorithm belongs to the class of descent methods.

3.1 Computation cost per-iteration for RSD

It is easy to observe that if the cost of updating the gradient is negligible, then the cost per iteration in RSD is given by the computational effort of finding the solution of the subproblem. The sketch sampling can be completely dense (e.g. Gaussian random matrix) or can be extremely sparse (e.g. a few columns of the identity matrix).

Case 1: dense sketch matrix . In this case, since we assume (in fact we usually choose of order or even smaller), then the computational cost per-iteration in the update (16) is linear in (more precisely of order ) plus the cost of computing the matrix . Clearly, if is also a dense matrix, then the cost of computing the matrix is quadratic in . However, it can be reduced substantially, that is the cost of computing this matrix depends linearly on , when e.g. we have available a decomposition of the matrix as , with and , or is sparse.

Case 2: sparse sketch matrix . For simplicity, we can assume that is chosen as few columns of the identity matrix and thus obtaining a coordinate descent type method. In this case, the cost per-iteration of RSD is independent of the problem size . For example, the cost of computing is , while the cost of computing is .

In conclusion, in all situations the iteration (16) of RSD is much computationally cheaper (at least one order of magnitude) than the iteration (15) corresponding to the full gradient. Based on the decrease of the objective function (18) we can derive different convergence rates for our algorithm RSD depending on the assumptions imposed on the objective function .

3.2 Convergence rate: smooth case

We derive in this section the convergence rate of the sequence generated by the RSD algorithm when the objective function is only smooth (Assumption 1). Recall that in the non-convex settings a feasible is a stationary point for optimization problem (1) if . On the other hand, for any feasible we have the unique decomposition of :

It is clear that if a feasible satisfies , then such an is a stationary point for (1). In conclusion, a good measure of optimality for a feasible is described in terms of . The theorem below provides a convergence rate for the sequence generated by RSD in terms of this optimality measure:

Theorem 7.

Proof.

Taking expectation over the entire history in (18) we get:

| (20) |

Summing the previous relation and using that is bounded from below we further get:

Using the unique decomposition for all and since , then we obtain . Therefore, taking the limit as we obtain the asymptotic convergence . Moreover, since on and we also get:

which concludes our statement. ∎

3.3 Convergence rate: smooth convex case

In order to estimate the rate of convergence of our algorithm when the objective function is smooth and convex, we introduce the following distance that takes into account that our algorithm is a descent method:

| (21) |

which measures the size of the sublevel set of given by . We assume that this distance is finite for the initial iterate . In the next theorem we prove sublinear convergence in expected value of the objective function for the smooth convex case:

Theorem 8.

Proof.

Recall that all our iterates are feasible, i.e. . From convexity of and the definition of the norm on the subspace , we get:

Since the previous chain of inequalities hold for any optimal point , we get further:

Combining this inequality with (18), we obtain:

or equivalently

Taking the expectation of both sides of this inequality in and denoting leads to:

Dividing both sides of this inequality with and taking into account that (see (18)), we obtain:

Adding these inequalities from we get the following inequalities , from which we obtain the desired statement. ∎

3.4 Convergence rate: smooth strongly convex case

In addition to the smoothness assumption, we now assume that the function is strongly convex with respect to the extended norm with strong convexity parameter on the subspace :

Assumption 9.

We assume that the objective function is strongly convex on the subspace , that is there exists a parameter satisfying the following inequality:

| (23) |

Note that if is strongly convex function everywhere in , that is there exists a positive definite matrix such that:

| (24) |

then using the definition of the dual norm (see Lemma 5) we have that (23) also holds for some satisfying:

Since for all (see Lemma 2), then also for all . In conclusion, the matrix inequality holds automatically on for any constant , and consequently we can define as the largest positive constant satisfying everywhere on the matrix inequality:

This shows that Assumption 9 is less restrictive than requiring strong convexity for everywhere in as in (24). Next, we prove that the strong convexity parameter is bounded from above:

Lemma 10.

Proof.

By the Lipschitz continuous gradient inequality (see Assumption 1) and the strong convexity inequality (see Assumptions 9) we have that on (or equivalently on ). Since for all (see Lemma 2), then also for all . In conclusion, the matrix inequality holds automatically on . Therefore, we get the following matrix inequality valid on :

Pre- and post-multiplying the previous matrix inequality with leads to:

or equivalently

Using the basic properties of the pseudo-inverse we obtain:

Therefore, if we denote by , then we get that and thus for any eigenvalue of it holds that or equivalently . It remains to show that . For this, we recall that according to Lemma 2 we know that . By utilizing the fact that is symmetric and positive-definite, we can notice that

Therefore, all the eigenvalues of belongs to the set . Further, by the definition of in (9) and using the convexity of the function on the set of positive semidefinite matrices, we have:

which completes our proof. ∎

We now derive a linear convergence estimate for our algorithm RSD under this additional strong convexity assumption on the subspace :

Theorem 11.

Proof.

Given , taking the conditional expectation in (18) over the random matrix leads to the following inequality:

| (27) |

On the other hand, consider the minimization of the right hand side in (23) over , and denote its optimal solution. Using the definition of the dual norm in the subspace , one can see that satisfies the following optimality conditions:

Combining these optimality conditions with the well-known property of the pseudo-inverse, that is , we get that the optimal value of this minimization problem has the following expression:

Therefore, minimizing both sides of inequality (23) over , we have:

| (28) |

and for we get:

Combining the inequality (27) with the previous one, and taking expectation in on both sides, we arrive at the statement of the theorem. ∎

Remark 12.

From the proof of Theorem 11 it follows that we can further relax the strong convexity assumption, that is instead of (23) it is sufficient to require (28) to hold on . The reader should note that an inequality of the form (28) is known in the optimization literature as the Polyak-Lojasiewicz (PL) condition (see e.g. [11] for a recent exposition), and the proof above shows that algorithm RSD converges linearly for smooth convex functions satisfying only the PL condition. Since functions satisfying the PL inequality need not be convex, linear convergence of RSD method to the global optimum extends beyond the realm of convex functions. More precisely, is is easy to see that the convergence result of Theorem 7 can be strengthen, that is we can prove linear convergence in the expected values of the objective function for the iterates of algorithm RSD provided that additionally the PL type condition (28) holds (we just need to combine the inequalities (20) and (28)).

Note that in special cases, where complexity bounds are known for RSD , such as optimization problems with a single linear coupled constraint, our theory recovers the best known bounds (see e.g. the convergence analysis in [6, 20]). For example, in the smooth convex case choosing for the sketch matrix at least columns of the identity matrix, then combining (6) with Theorem 8 we recover the convergence rate of coordinate descent algorithm from [20, Theorem 4.1] for the problem with a separable objective function and a single linear constraint. Similarly, for the strongly convex case our convergence analysis recovers [20, Theorem 4.2]. In conclusion, to our knowledge, this is the first complete convergence analysis of a general random sketch descent algorithm, for which coordinate descent method is a particular case, for solving optimization problems with multiple linear coupled constraints.

4 Accelerated random sketch descent algorithm

For the accelerated variant of Algorithm RSD let us first define the following constant:

| (29) |

Let us now consider any constant parameter . The Accelerated Random Sketch Descent (A-RSD ) scheme is depicted in Algorithm 2:

4.1 Computation cost per-iteration for A-RSD

It is easy to observe that the computational cost for updating the sequence is comparable to the one corresponding to RSD algorithm. Therefore, the conclusions regarding the cost per-iteration from Section 3.1 corresponding to RSD are also valid here. Note that the accelerated variant also requires updating two additional sequences and , which requires computations with full vectors in . However, for structured optimization problems we can avoid the addition of full vectors in and still keep the cost per-iteration of A-RSD comparable to that of RSD . More precisely, we can efficiently implement the updates of A-RSD algorithm without full-dimensional vector operations when the sketch matrix is sparse and when we can efficiently compute:

Note that gradient evaluation in such points is computationally easy when has a special structure, e.g. of the form , where is a sparse matrix [5]. Objective functions of this form includes many generalized linear models, such as logistic regression, least squares, etc. In Appendix A we provide efficient implementations of the updates of A-RSD for these settings.

4.2 Basic properties of A-RSD

Before deriving convergence rates for A-RSD we analyze some basic properties of this algorithm. First, we prove that the newly introduced constant is bounded, thus finite:

Proof.

EXAMPLE 6 cont. For the optimization problem considered in Example 6 we can easily compute a good upper approximation for :

where we used that . This relation shows that and consequently it is related to a global Lipschiz type constant for the gradient of .

For simplicity of the exposition let us also denote:

From the updates of A-RSD we can also show a descent property for the conditional expectation . Indeed, from our updates and Assumption 1 we have:

Taking now the conditional expectation with respect to random choice and using that (see Lemma 2) we obtain:

| (30) |

Moreover, the sequences and satisfies , and , and consequently also . Moreover, since (see Lemma 4), then is a projection matrix onto , that is for all , and thus the following holds:

| (31) |

For any optimal point let us also define the sequence:

| (32) |

Based on the previous discussion, we can show the following descent property for the sequence of Algorithm A-RSD that holds also for the case :

Lemma 14.

Proof.

Using the definition of we have:

where in the last inequality we used the convexity of the norm and the fact that . Taking now the conditional expectation with respect to we get:

Rearranging the terms, we get:

Note that the previous derivations also hold without Assumption 9, that is we use the strong convexity inequality (23) with . Using now the convexity of the function and that , we further get:

which concludes our statement. ∎

Based on the previous descent property we can derive different convergence rates for our algorithm A-RSD depending on the assumptions imposed on the objective function .

4.3 Convergence rate: smooth convex case

In this section we prove the sublinear convergence rate for A-RSD (Algorithm 2) for some choices of the sequences , and . In particular, the next lemma shows the behavior of defined as follows:

Lemma 15.

Let be a sequence defined recursively as and be the largest solution of the second order equation:

| (34) |

Then, satisfies the following inequality:

| (35) |

Proof.

First, we observe that is a non-decreasing sequence. Indeed, the largest root of (34) is given by:

| (36) |

Next, we have:

| (37) |

which implies that

This concludes our proof. ∎

From (35) it follows that for all . Now, we are ready to prove the sublinear convergence of A-RSD :

Theorem 16.

Proof.

In the smooth convex case we can use Lemma 14 (i.e. descent relation (33)) by setting , i.e. we have:

| (38) |

Note that and hence the last term in (38) vanishes. Thus, we further obtain:

| (39) |

Moreover, since , then:

| (40) |

Plugging (40) into (39) and dividing both sides by we obtain:

| (41) |

Now, it reminds to note that satisfy (34) and consequently:

Taking now the expectation over the entire history in the previous recursion and unrolling it, we get:

Since we have the second order equation for all , we get our statement. ∎

4.4 Convergence rate: smooth strongly convex case

We are now ready to state the linear convergence rate for A-RSD (Algorithm 2).

Theorem 17.

Proof.

| RSD | A-RSD | |

|---|---|---|

| smooth convex | ||

| smooth strong convex |

Table 1 summarizes the convergence rates in of RSD and A-RSD algorithms for smooth (strongly) convex objective functions (we assumed for simplicity that ). We observe from this table that we have obtained the typical convergence rates for these two methods, in particular, A-RSD converges with one order of magnitude faster than RSD , see [22] for more details. It is important to note that in this work we provide the first analysis of an accelerated random sketch descent (A-RSD ) algorithm for optimization problems with multiple non-separable linear constraints.

5 Illustrative numerical experiments

In this section we provide several numerical examples showing the benefits of random sketching and the performances of our new algorithms.

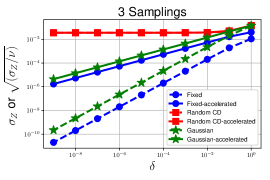

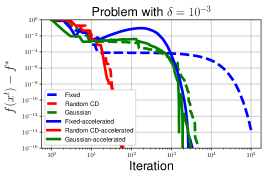

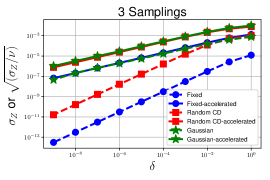

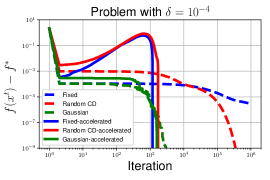

Experiment #1: A pre-fixed coordinate sampling can be a disaster. Recently, in [36] it has been shown for linear systems that Gauss-Seidel algorithm with randomly sampled coordinates substantially outperforms Gauss-Seidel with any fixed partitioning of the coordinates that are chosen ahead of time. Motivated by this finding, we also analyze the behavior of RSD and A-RSD algorithms for fixed coordinate sketch, random coordinate sketch and Gaussian sketch. We build two challenging problems. One problem has a particular structure with a single linear constraint. The second example is easier, and it involves a random matrix, but the linear constraints make the problem more challenging. The first problem is to minimize the following convex optimization problem parameterized by :

| (42) |

We consider three different choices for , fixed partition of the coordinates, random partition of the coordinates, and a Gaussian random sketch:

where we recall that denotes the th column of the identity matrix and is normally distributed random variable with mean and variance . We use the same sketching also for the second problem, where and is a rank deficient random matrix, and . In this case we denote to be a set of orthogonal eigenvectors of , such that corresponds to the largest eigenvalue and is the eigenvector which corresponds to the smallest eigenvalue. We have chosen and . The optimal solution for both problems is with .

In Figure 1 top row, we show the results for the first problem and in the second row we show the results for the second problem. On the left, we show the important quantities or which characterize the convergence rates of the two algorithms in the strongly convex case (see Table 1). In the right column we show the typical evolution of . One can observe that for the first problem, the random sampling is the best both in practice, whereas the other two samplings are suffering. The main reason is that for this problem, the most important sketch matrix is which is selected more often by the random sketching than the other two sketching strategies. For the second test problem the best sketching is the Gaussian sketch. Therefore, empirically this experiment shows that both algorithms, RSD and A-RSD , based on random sketching provides speedups compared to the fixed partitioning counterpart.

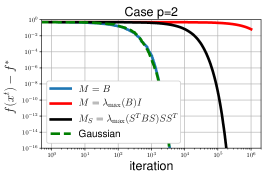

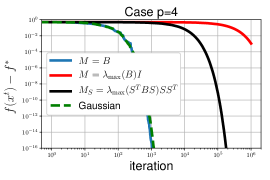

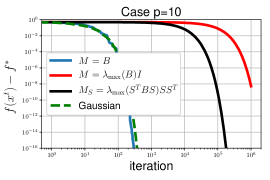

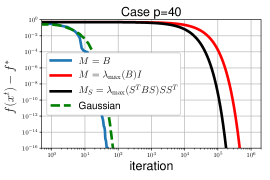

Experiment #2: The effect of a quadratic upper-bound in convergence speed. In this experiment, we investigate the benefit of using the full matrix in (7) as compared to just using a scaled diagonal upper-bound as considered e.g. in [6, 18]. Consider the following convex optimization problem parameterized by :

| (43) |

We compare the speed of Algorithm RSD when the random matrix is chosen uniformly at random as columns of the identity matrix and consider three choices for the matrix : , and . We also implement RSD for the Gaussian sketch and . From Figure 2 one can observe that if we set , then increasing will decrease the number of iterations needed to achieve the desired accuracy with the best rate. We can also observe that Gaussian sketch or coordinate descent sketch have a similar behavior for the case .

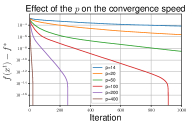

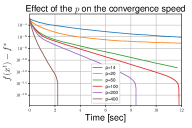

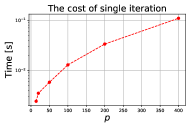

Experiment #3: Portfolio optimization with specified industry allocation. In Section 1.2.3 we have described the basic Markowitz portfolio selection model [17]. We have also described a variant of the basic model which assumes that investor also decide how much net wealth would be allocated in different asset classes (e.g. Financials, Health Care, Industrials, etc). When we have asset classes, then the problem of minimizing the risk with all the desired constraints will lead to linear constraints. In Figure 3 we show the performance of the RSD algorithm with the sketch matrix chosen random Gaussian. We considered real data from the index S&P500 which contains 500 assets split across asset classes. The s and were estimated from the historical data. In the left plot we show the evolution of error for various sizes of as a function of iterations and in the middle plot we put on x-axis the computational time. We can observe that increasing leads to significantly decrease of number of iterations and also faster convergence in terms of wall-clock time. Note also that as is becoming larger, the per-iteration computational cost increases moderately (see the right plot).

Acknowledgements

The work of Ion Necoara was supported by the Executive Agency for Higher Education, Research and Innovation Funding (UEFISCDI), Romania, under PNIII-P4-PCE-2016-0731, project ScaleFreeNet, no. 39/2017. The work of Martin Takáč was partially supported by the U.S. National Science Foundation, under award numbers NSF:CCF:1618717, NSF:CMMI:1663256 and NSF:CCF:1740796.

References

- [1] Amir Beck. The 2-coordinate descent method for solving double-sided simplex constrained minimization problems. Journal of Optimization Theory and Applications, 162(3):892–919, 2014.

- [2] Amir Beck and Luba Tetruashvili. On the convergence of block coordinate descent type methods. SIAM journal on Optimization, 23(4):2037–2060, 2013.

- [3] Albert S Berahas, Raghu Bollapragada, and Jorge Nocedal. An investigation of newton-sketch and subsampled newton methods. arXiv:1705.06211, 2017.

- [4] Olivier Fercoq, Zheng Qu, Peter Richtárik, and Martin Takáč. Fast distributed coordinate descent for non-strongly convex losses. In Machine Learning for Signal Processing (MLSP), 2014 IEEE International Workshop on, pages 1–6. IEEE, 2014.

- [5] Olivier Fercoq and Peter Richtárik. Accelerated, parallel, and proximal coordinate descent. SIAM Journal on Optimization, 25(4):1997–2023, 2015.

- [6] Rafael Frongillo and Mark D Reid. Convergence analysis of prediction markets via randomized subspace descent. In Advances in Neural Information Processing Systems, pages 3034–3042, 2015.

- [7] Robert M Gower, Peter Richtárik, and Francis Bach. Stochastic quasi-gradient methods: Variance reduction via jacobian sketching. arXiv:1805.02632, 2018.

- [8] Mert Gurbuzbalaban, Asuman Ozdaglar, Pablo A Parrilo, and Nuri Vanli. When cyclic coordinate descent outperforms randomized coordinate descent. In Advances in Neural Information Processing Systems, pages 6999–7007, 2017.

- [9] Mingyi Hong and Zhi-Quan Luo. On the linear convergence of the alternating direction method of multipliers. Mathematical Programming, 162(1-2):165–199, 2017.

- [10] Hideaki Ishii, Roberto Tempo, and Er-Wei Bai. A web aggregation approach for distributed randomized pagerank algorithms. IEEE Transactions on Automatic Control, 57(11):2703–2717, 2012.

- [11] Hamed Karimi, Julie Nutini, and Mark Schmidt. Linear convergence of gradient and proximal-gradient methods under the polyak-łojasiewicz condition. In Joint European Conference on Machine Learning and Knowledge Discovery in Databases, pages 795–811. Springer, 2016.

- [12] Yin Tat Lee and Aaron Sidford. Efficient accelerated coordinate descent methods and faster algorithms for solving linear systems. arXiv:1305.1922, 2013.

- [13] Ji Liu and Stephen J Wright. Asynchronous stochastic coordinate descent: Parallelism and convergence properties. SIAM Journal on Optimization, 25(1):351–376, 2015.

- [14] Zhaosong Lu and Lin Xiao. On the complexity analysis of randomized block-coordinate descent methods. Mathematical Programming, 152(1-2):615–642, 2015.

- [15] Zhi-Quan Luo and Paul Tseng. Error bounds and convergence analysis of feasible descent methods: a general approach. Annals of Operations Research, 46(1):157–178, 1993.

- [16] Jakub Mareček, Peter Richtárik, and Martin Takáč. Distributed block coordinate descent for minimizing partially separable functions. In Numerical Analysis and Optimization, pages 261–288. Springer, 2015.

- [17] Harry Markowitz. Portfolio selection. The journal of finance, 7(1):77–91, 1952.

- [18] Ion Necoara. Random coordinate descent algorithms for multi-agent convex optimization over networks. IEEE Transactions on Automatic Control, 58(8):2001–2012, 2013.

- [19] Ion Necoara and Dragos Clipici. Parallel random coordinate descent method for composite minimization: Convergence analysis and error bounds. SIAM Journal on Optimization, 26(1):197–226, 2016.

- [20] Ion Necoara, Yurii Nesterov, and François Glineur. Random block coordinate descent methods for linearly constrained optimization over networks. Journal of Optimization Theory and Applications, 173(1):227–254, 2017.

- [21] Ion Necoara and Andrei Patrascu. A random coordinate descent algorithm for optimization problems with composite objective function and linear coupled constraints. Computational Optimization and Applications, 57(2):307–337, 2014.

- [22] Yu Nesterov. Efficiency of coordinate descent methods on huge-scale optimization problems. SIAM Journal on Optimization, 22(2):341–362, 2012.

- [23] Yurii Nesterov. Introductory lectures on convex optimization: A basic course, volume 87. Springer Science & Business Media, 2013.

- [24] Mert Pilanci and Martin J Wainwright. Newton sketch: A near linear-time optimization algorithm with linear-quadratic convergence. SIAM Journal on Optimization, 27(1):205–245, 2017.

- [25] Zheng Qu, Peter Richtárik, Martin Takáč, and Olivier Fercoq. SDNA: stochastic dual newton ascent for empirical risk minimization. In International Conference on Machine Learning, pages 1823–1832, 2016.

- [26] Sashank Reddi, Ahmed Hefny, Carlton Downey, Avinava Dubey, and Suvrit Sra. Large-scale randomized-coordinate descent methods with non-separable linear constraints. arXiv:1409.2617, 2014.

- [27] Peter Richtárik and Martin Takáč. Iteration complexity of randomized block-coordinate descent methods for minimizing a composite function. Mathematical Programming, 144(1-2):1–38, 2014.

- [28] Peter Richtárik and Martin Takáč. On optimal probabilities in stochastic coordinate descent methods. Optimization Letters, 10(6):1233–1243, 2016.

- [29] Peter Richtárik and Martin Takáč. Parallel coordinate descent methods for big data optimization. Mathematical Programming, 156(1-2):433–484, 2016.

- [30] Peter Richtárik and Martin Takáč. Stochastic reformulations of linear systems: algorithms and convergence theory. arXiv:1706.01108, 2017.

- [31] Shai Shalev-Shwartz and Tong Zhang. Stochastic dual coordinate ascent methods for regularized loss minimization. Journal of Machine Learning Research, 14(Feb):567–599, 2013.

- [32] Ruoyu Sun and Yinyu Ye. Worst-case complexity of cyclic coordinate descent: gap with randomized version. arXiv:1604.07130, 2016.

- [33] Martin Takáč, Peter Richtárik, and Nathan Srebro. Distributed mini-batch SDCA. arXiv:1507.08322, 2015.

- [34] Rachael Tappenden, Martin Takáč, and Peter Richtárik. On the complexity of parallel coordinate descent. Optimization Methods and Software, 33(2):372–395, 2018.

- [35] Paul Tseng and Sangwoon Yun. Block-coordinate gradient descent method for linearly constrained nonsmooth separable optimization. Journal of optimization theory and applications, 140(3):513, 2009.

- [36] Stephen Tu, Shivaram Venkataraman, Ashia C Wilson, Alex Gittens, Michael I Jordan, and Benjamin Recht. Breaking locality accelerates block gauss-seidel. arXiv:1701.03863, 2017.

- [37] Jialei Wang, Jason D Lee, Mehrdad Mahdavi, Mladen Kolar, and Nathan Srebro. Sketching meets random projection in the dual: A provable recovery algorithm for big and high-dimensional data. Electronic Journal of Statistics, 11(2):4896–4944, 2017.

- [38] Ermin Wei, Asuman Ozdaglar, and Ali Jadbabaie. A distributed newton method for network utility maximization–i: Algorithm. IEEE Transactions on Automatic Control, 58(9):2162–2175, 2013.

- [39] Stephen J Wright. Accelerated block-coordinate relaxation for regularized optimization. SIAM Journal on Optimization, 22(1):159–186, 2012.

- [40] Lin Xiao and Stephen Boyd. Optimal scaling of a gradient method for distributed resource allocation. Journal of optimization theory and applications, 129(3):469–488, 2006.

Appendix A

In this appendix we discuss how to implement the A-RSD updates without full-dimensional vector operations. Recall that we assume the following settings: the sketch matrix is sparse and we can efficiently evaluate . First we derive an efficient implementation of A-RSD iterations for strongly convex objective functions and then a simplified implementation for the convex case. Following a similar approach as in the coordinate descent work proposed in [12] for solving linear systems and further extended in [5] for accelerated coordinate descent method with separable composite problems we note that:

Hence, we obtain the following recursion:

| (44) |

with

Now, our goal is to maintain two sequences such that: . Therefore, it has to hold that

and therefore we require

In order to make this computationally efficient, it is sufficient to define recursively as:

and to obtain the following update rule

which is a sparse update provided that is a sparse vector. However, when the sketch matrix is sparse the vector is sparse as well and consequently is also a sparse vector (see Example 6 where for the corresponding vector has only two non-zero entries). The final algorithm is depicted in Algorithm 3 below.

Simplified Convex Case. In the case of non-strongly convex objective function, the implementation can be significantly simplified using the fact that for all . Then, we have:

| (45) |

and

Therefore, we obtain the following recursion:

| (46) |

with

Now, we see that the update of given by (45) is sparse if is sparse. Further, we want to express . Then, from (46) we have:

Therefore, if we define , this will simplify to:

It follows that the update of is also sparse if is sparse. Next, we can easily compute (however, this shouldn’t be formed during the run of the algorithm). Finally, it is sufficient to note that , and we can choose . The final algorithm is given in Algorithm 4 below.