appendAppendix References

Improved Estimation of Average Treatment Effects on the Treated: Local Efficiency, Double Robustness, and Beyond

Heng Shu & Zhiqiang Tan111Heng Shu is with JPMorgan Chase, New York, NY 10017 and Zhiqiang Tan is Professor, Department of Statistics, Rutgers University, Piscataway, NJ 08854 (E-mail: ztan@stat.rutgers.edu). An earlier version of this work was completed as part of the PhD thesis of Heng Shu at Rutgers University.

Abstract.

Estimation of average treatment effects on the treated (ATT) is an important topic of causal inference in econometrics and statistics. This problem seems to be often treated as a simple modification or extension of that of estimating overall average treatment effects (ATE). However, the propensity score is no longer ancillary for estimation of ATT, in contrast with estimation of ATE. In this article, we review semiparametric theory for estimation of ATT and the use of efficient influence functions to derive augmented inverse probability weighted (AIPW) estimators that are locally efficient and doubly robust. Moreover, we discuss improved estimation over AIPW by developing calibrated regression and likelihood estimators that are not only locally efficient and doubly robust, but also intrinsically efficient in achieving smaller variances than AIPW estimators when a propensity score model is correctly specified but an outcome regression model may be misspecified. Finally, we present two simulation studies and an econometric application to demonstrate the advantage of the proposed methods when compared with existing methods.

Key words and phrases.

Average treatment effect; Average treatment effect on the treated; Causal inference; Double robustness; Inverse probability weighting; Intrinsic efficiency; Local efficiency; Semiparametric estimation.

1 Introduction

A central problem in various social and behavioral studies is to evaluate average effects of treatments and actions ceteris paribus (with all other things being equal). Such problems can be addressed by introducing potential outcomes that would be observed for each subject under different treatments (Neyman 1923; Rubin 1974). Average causal effects are then defined as statistical comparisons (e.g., mean differences) of potential outcomes over a population or subpopulation. Two causal parameters commonly studied are the average treatment effect (ATE) and the average treatment effect on the treated (ATT). The ATE is defined as the mean difference of two potential outcomes under the active treatment and the control over the entire population, whereas ATT is defined as the mean difference of two potential outcomes over the subpopulation of individuals who received the active treatment. As argued by Heckman & Robb (1985) and Heckman et al. (1997) in the context of evaluating training programs, the ATT answers the question “How much did persons participating in the programme benefit compared to what they would have experienced without participating in the programme?” The ATT is relevant in making forecasts when the same selection rule operates in the future as has operated in the past.

Drawing inferences about ATE and ATT is challenging because, in reality, all but one potential outcome are missing for each subject. Nevertheless, under unconfoundedness (i.e., exogeneity) and overlap assumptions, the ATE and ATT are point identifiable from observed data (e.g., Imbens 2004). There is an extensive collection of theory and methods developed for statistical estimation of ATE and ATT under exogeneity. Let be an observed outcome, a treatment indicator, and a vector of covariates. Semiparametric efficiency bounds for estimation of both ATE and ATT are obtained by Hahn (1998), and can be seen as special cases of semiparametric theory in Robins et al. (1994) and Chen et al. (2008) for moment restriction models with missing data. Asymptotically globally efficient estimators for ATE and ATT are studied by Hahn (1998), Hirano et al. (2003), and Chen et al. (2008) among others, using nonparametric series/sieve estimation on the propensity score, , or the outcome regression function, , or both. But various smoothness conditions are assumed for such methods and can sometimes be problematic with a high-dimensional covariate vector (Robins & Ritov 1997).

Alternatively, various methods are developed by using parametric working models on the propensity score or the outcome regression function or both, to achieve desirable properties such as local efficiency, double robustness, and beyond. This line of research has been well pursued for estimation of ATE (e.g., Robins et al. 1994; Tan 2006, 2010; Cao et al. 2009). See also Kang & Schafer (2007) and its discussion. For an estimator of ATE, double robustness means that the estimator remains consistent if either the propensity score model or the outcome regression model is correctly specified. Local efficiency means that if both the propensity score model and the outcome regression model are correctly specified, then the estimator achieves the semiparametric efficiency bound, which is the same whether the propensity score is known, paramtrically modeled, or completely unknown due to the ancillarity of the propensity score for estimation of ATE (Hahn 1998). To our knowledge, there seems to be limited work explicitly dealing with locally efficient and doubly robust estimation of ATT (e.g., Graham et al. 2016; Zhao & Percival 2017).

There are two possible reasons why ATT estimation has been studied much less extensively than ATE estimation. On one hand, ATT can often be estimated by a simple modification or extension of estimators of ATE. On the other hand, semiparametric theory for estimation of ATT is complicated by the fact that the propensity score is no longer ancillary (Hahn 1998). The purpose of this article is twofold: (i) we review semiparametric theory for ATT estimation and the use of efficient influence functions to derive augmented inverse probability weighted (AIPW) estimators of ATT, and (ii) we discuss the extension of related techniques for improved estimation of ATE (Tan 2006, 2010; Cao et al. 2009) to develop calibrated estimators of ATT that achieve desirable properties beyond local efficiency and double robustness. Demonstration of these ideas can also facilitate their applications to other missing-data problems, for example, data combination discussed in Graham et al. (2016).

There are several interesting phenomena clarified from our work, all different from familiar results for estimation of ATE. First, there are two AIPW estimators achieving local efficiency of different types. If the propensity score and outcome regression models are correctly specified, the first estimator achieves the semiparametric efficiency bound, , calculated when the propensity score is unknown, whereas the second estimator achieves the semiparametric efficiency bound, , calculated under the parametric propensity score model used. These two estimators are then referred to as locally nonparametric or, respectively, semiparametric efficient.

Second, the locally nonparametric efficient estimator AIPW of ATT is doubly robust, but the locally semiparametric efficient AIPW estimator is generally not. Therefore, it is the efficient influence function calculated under the nonparametric model (i.e., when the propensity score as well as the outcome regression function is unknown) that leads to doubly robust estimation. Incidentally, it can be shown that the doubly robust estimators of ATT in Graham et al. (2016) and Zhao & Percival (2017) are also locally nonparametric efficient.

Third, due to the discrepancy between the locally nonparametric and semiparametric AIPW estimators, a direct application of the techniques in Tan (2006, 2010) and Cao et al. (2009) would fail to yield an improved estimator of ATT that is not only doubly robust and locally nonparametric efficient, but also intrinsically efficient in achieving smaller variances than AIPW estimators when the propensity score model is correctly specified but the outcome regression model may be misspecified. We show that such improved estimators can still be developed by introducing a simple idea, namely, working with an augmented propensity score model which includes the fitted outcome regression functions as additional regressors.

To illustrate the advantage of the improved estimators, we present two simulation studies and an econometric application related to LaLonde (1986) and subsequent analyses (e.g., Dehejia & Wahba 2002; Smith & Todd 2005a). In contrast with these previous works, we compare the performance of different methods by examining not only the effect or bias estimates (where the experimental treatment or, respectively, control group is compared with a non-experimental comparison group), but also how well the differences between the effect and bias estimates agree with the benchmark estimate (where the experimental control and treatment groups are compared). The latter comparisons are relevant even if the non-experimental group might inherently differ from the cohort on which the experiment was conducted.

2 Setup

To introduce the setup, suppose that a simple random sample of subjects is available from a population under study. The observed data consist of independent and identically distributed observations of , where is an outcome variable, is a dichotomous treatment variable ( if treated or otherwise), and is a vector of measured covariates. In the potential outcomes framework for causal inference (Neyman 1923; Rubin 1974), two potential outcomes are defined to indicate what would be the response under treatment 0 or 1 respectively. By consistency, the observed outcome is assumed to be either or , depending on whether or . Two causal parameters commonly of interest are the average treatment effect (ATE), defined as with , and the average treatment effect on the treated (ATT), defined as with . In this article, we are concerned with estimation of the ATT. See, for example, Imbens (2004) for a review and Tan (2006, 2010) for related works on estimation of ATE.

While the parameter is directly identifiable as , a fundamental difficulty in identification of is that is missing for treated subjects with . Nevertheless, it is known (e.g., Imbens 2004) that the and hence ATT are identifiable from observed data under the two assumptions:

-

(A1)

Unconfoundedness for controls: , i.e., and are conditionally independent given ;

-

(A2)

Weak overlap: for all .

Assumption (A2) allows that is 0 for some values , i.e., subjects with certain covariate values will always take treatment 0.

By the fact that , a consistent, nonparametric estimator of is , where and are the sizes of treated and untreated groups respectively in the sample. However, modeling (or dimension-reduction) assumptions, in addition to (A1)–(A2), are, in general, needed to obtain consistent estimation of and ATT from finite samples with high-dimensional . There are broadly two modelling approaches as follows (e.g., Tan 2007).

One approach is to build a (parametric) regression model for the outcome regression (OR) function, :

| (1) |

where is an inverse link function, is a vector of known functions of including 1, and is a vector of unknown parameters. For or 1, let be the maximum quasi-likelihood estimate of , and let . If model (1) is correctly specified for or 1, then a consistent estimator for is . The ATT can be estimated by . In the special case where is the identity link and parallel regression functions are assumed for the two treatment groups, i.e., with excluding 1, the ATT can be directly estimated as .

An alternative approach is to build a (parametric) regression model for the propensity score (PS) (Rosenbaum & Rubin 1983), :

| (2) |

where is an inverse link function, is a vector of known functions including 1, and is a vector of unknown parameters. The score function for is

Typically, logistic regression is used: , and the score function is . Let be the maximum likelihood estimator (MLE) of and , satisfying the score equation , which for logistic regression reduces to

| (3) |

where denotes a sample average, for example, . Then and ATT can be estimated by matching, stratification, or weighting on the fitted propensity score (e.g., Imbens 2004). We focus on inverse probability weighting (IPW), which is central to rigorous theory of statistical estimation in missing-data problems (e.g., Tsiatis 2006). Two standard IPW estimators for are (e.g., McCaffrey et al. 2004; Abadie 2005)

The estimator of ATT based on and is then

If model (2) is correctly specified, then the IPW estimators are consistent. However, if model (2) is misspecified or even mildly so, these estimators can perform poorly, especially due to the instability of inverse weighting to fitted propensity scores near 1 for some untreated subjects (e.g., Kang & Schafer 2007).

3 Semiparametric theory and AIPW estimation

For consistency, the estimator requires a correctly specified OR model (1) for , whereas and require a correctly specified PS model (2). Alternatively, it is desirable to develop estimators of and ATT using both OR model (1) and PS model (2) to gain efficiency and robustness, similarly as in estimation of ATE. We review semiparametric theory and derive locally efficient and doubly robust estimators of and ATT in the form of augmented IPW (AIPW). Understanding of these estimators facilitates our development of improved estimators in Section 4.

First, Proposition 1 restates the efficient influence functions for estimation of under three different settings, based on Hahn (1998) and Chen et al. (2008).

Proposition 1 (Hahn 1998; Chen et al. 2008)

Let and define

The efficient influence function for estimation of is as follows, depending on assumptions on the propensity score.

-

(i)

The efficient influence function is

-

(ii)

If the propensity score is known, then the efficient influence function is

-

(iii)

If the propensity score is unknown but assumed to belong to a correctly specified parametric family , then the efficient influence function is

where for two random vectors and , , i.e., the linear projection of onto .

As discussed in Hahn (1998) and Chen et al. (2008), the semiparamtric efficiency bounds satisfy the following order: , with strict inequalities holding in general, where , , and are respectively the variances of , , and . In fact, the efficient influence functions , , and can all be expressed as the following functional with suitable choices of :

| (4) |

The minimum variance of over possible choices of is exactly , corresponding to the choice .

This ordering of efficiency bounds agrees with the usual comparison that the efficiency bound under a more restrictive model is no greater than under a less restrictive model. But this relationship differs from the result that the semiparametric efficiency bounds for estimation of are the same whether under the nonparametric model for , or under a parametric model for , or with exact knowledge of . Conceptually, these differences reflect the fact the propensity score is ancillary for estimation of ATE, but not ancillary for estimation of ATT (Hahn 1998).

We now derive two estimators of that depend on both fitted outcome regression function and fitted propensity score , by directly taking the efficient influence functions in Proposition 1 as estimating functions, with and in place of the unknown truth and . Proposition 2 shows that only one estimator is doubly robust, whereas both estimators possess local efficiency but of different types according to the semiparametric efficiency bounds achieved when the OR and PS models are correctly specified. For clarity, the semiparametric efficiency bound under the nonparametric model is hereafter referred to as the nonparametric efficiency bound. See, for example, Newey (1990), Robins & Rotnitzky (2001), and Tsiatis (2006) for general discussions on local efficiency and double robustness.

Proposition 2

Under suitable regularity conditions (see Appendix I in the Supplementary Material), the following results hold.

- (i)

-

(ii)

Define an estimator of as

For logistic PS model (2), can be equivalently expressed as

because by Eq. (3) with including 1. Then is locally semiparametric efficient: it achieves the semiparametric efficiency bound when both model (1) for and model (2) are correctly specified. But is, generally, not doubly robust.

The estimators and, for a logistic PS model, belong to the following class of AIPW estimators, with the choice or respectively:

which are defined by directly taking (4) as the estimating function with the fitted propensity score in place of the unknown truth . Setting leads to the simple estimator . Although related estimators of may be implicit in previous works (e.g., Stoczynski & Wooldridge 2014) and the idea of constructing estimators from influence functions is generally known (e.g., Tsiatis 2006), our application of this idea to derive the estimators and for seems new and sheds light on subtle differences between the two estimators as discussed below. Such differences lead to new challenges to be addressed in our development of improved estimators in Section 4; see the remarks after Proposition 5.

By local semiparametric efficiency, the estimator , but not , achieves the minimum asymptotic variance among all regular estimators under PS model (2), including AIPW estimators over possible choices of , when both model (1) for and model (2) are correctly specified. However, is not doubly robust, and is doubly robust. This situation differs from the case where among the class of AIPW estimators of , the estimator

is doubly robust, i.e., consistent when either OR model (1) for or PS model (2) is correctly specified, and locally semiparamtric and nonparametric efficient, i.e., achieving the minimum asymptotic variance among all regular estimators under parametric PS model (2) and, respectively, under the nonparametric model when model (1) for and model (2) are correctly specified. As discussed after Proposition 1, the semiparametric efficient bound for estimation of under a parametric PS model coincides with that under the nonparametric model.

Next, we restate the efficient influence functions in Proposition 3 for estimation of , based on Hahn (1998) and Chen et al. (2008). Similarly as for estimation of , the efficiency bounds satisfy , with strict inequalities in general.

Proposition 3 (Hahn 1998; Chen et al. 2008)

The efficient influence function for estimation of is as follows, depending on assumptions on the propensity score.

-

(i)

The efficient influence function is

-

(ii)

If the propensity score is known, then the efficient influence function is

-

(iii)

If the propensity score is unknown but assumed to belong to a correctly specified parametric family , then the efficient influence function is

The estimator is always consistent and has the efficient influence function . Therefore, is fully robust to model misspecification, and globally nonparametric efficient. Alternatively, taking as an estimating function with and in place of and gives an estimator of that is locally semiparametric efficient, but not doubly robust.

Proposition 4

Under suitable regularity conditions (see Appendix I in the Supplementary Material), the following results hold.

- (i)

- (ii)

Finally, for estimation of ATT , the efficient influence function is the difference of the efficient influence functions for estimation of and under each of the three settings in Propositions 1 and 3. Combining the estimators of and in Propositions 2 and 4 leads to the following results.

Corollary 1

Under suitable regularity conditions (see Appendix I in the Supplementary Material), the following results hold.

- (i)

- (ii)

4 Improved estimation

We develop estimators of that are not only locally nonparametric efficient and doubly robust, but also intrinsically efficient: when the PS model (2) is correctly specified but the OR model (1) for may be misspecified, these estimators achieve at least as small asymptotic variances among a class of AIPW estimators, including but only with replaced by the fitted value from a slightly augmented PS model as defined later in (5). The new estimators are then similar to , in being consistent when either the PS model or the OR model is correctly specified and achieving the nonparametric efficiency bound when both models are correctly specified, but often achieve smaller variances over when the PS model is correctly specified but the OR model is misspecified.

Similarly, we develop estimators of ATT that are not only locally nonparametric efficient and doubly robust, but also often provide efficiency gains over when the PS model is correctly specified but the OR model is misspecified.

Before proceeding, we point out that although, by symmetry, it also seems desirable to construct estimators of or ATT that are not only locally nonparametric efficient and doubly robust, but also achieve efficiency gains approximately over or when the OR model is correctly specified but the PS model is misspecified, such estimators have not been obtained so far.

4.1 Regression estimators

We derive regression estimators for and ATT to achieve the desired properties, similarly to regression estimators for ATE (Tan 2006) but with an important new idea as follows. For simplicity, assume in Sections 4.1–4.2 that PS model (2) is logistic regression. See Appendix I.6 for an extension when PS model (2) is non-logistic regression. Consider an augmented logistic PS model

| (5) |

where , are estimates of from OR model (1), and are unknown coefficients for additional regressors and . Let be the MLE of and . An important consequence of including the additional regressors is that, by Eq. (3), we have, in addition to ,

| (6) |

For the augmented PS model, there may be linear redundancy in the variables, , , , in which case the regressors need to be redefined accordingly. In particular, consider the following condition:

-

(L)

is a linear combination of variables in for ,

which is satisfied when all variables in are included as components of , and is the identity link corresponding to linear regression in (1). If Condition (L) holds, then the augmented model (5) reduces to (2) and hence subsequently. Otherwise, and generally differ from each other.

With the fitted value from the augmented PS model (5), we define the regression estimator of as

where with

and are defined with a constant matrix such that the variables in are linearly independent, and

where is the vector of nonconstant variables in , because is already a component of in . For example, if Condition (L) holds for or 1, then should be specified such that one variable is removed from the vector in .

The variables in are included for the following considerations. The variables and are included in and respectively to achieve double robustness and local nonparametric efficiency, as later seen from Eq. (8). Moreover, the variables in , in addition to , are included to accommodate the variation of for achieving intrinsic efficiency, as later described in Proposition 5. The corresponding variables in or are exactly the scores for the augmented PS model (5). Finally, is included in and to ensure efficiency gains over the ratio estimator under a correctly specified PS model, as discussed after Corollary 2.

The name “regression estimator” is adopted from the literatures of survey sampling (Cochran 1977) and Monte Carlo integration (Hammersley & Handscomb 1964), and should be distinguished from the estimator based on outcome regression in Section 2. The idea is to exploit the fact that if the PS model is correct, then asymptotically has mean (to be estimated) and mean 0 (known). That is, serves as auxiliary variables (in the terminology of survey sampling) or control variates (in that of Monte Carlo integration). The effect of variance reduction using regression estimators can be seen from in the following results.

Proposition 5

Under suitable regularity conditions (see Appendix I in the Supplementary Material), the estimator for has the following properties for .

- (i)

- (ii)

-

(iii)

is intrinsically efficient: if model (2) is correctly specified, then it achieves the lowest asymptotic variance among the class of estimators

(7) where is an arbitrary vector of constants.

Corollary 2

The estimator for ATT has the following properties.

- (i)

- (ii)

-

(iii)

is intrinsically efficient: if model (2) is correctly specified, then it achieves the lowest asymptotic variance among the class of estimators

where is an arbitrary vector of constants.

Double robustness. We point out that the use of augmented propensity scores is crucial for to be doubly robust, in particular, to be consistent under a correctly specified OR model but a misspecified PS model. [It is possible, for example, under Condition (L) that reduces to .] If the OR model (1) for or 1 is correctly specified, then, as shown in the Appendix I.3, the vector converges to a constant vector such that

| (8) |

because is a linear combination of variables in and is a linear combination of those in . By Eq. (6) for the augmented PS model, is identical to for , which is doubly robust similarly as by Propsition 2, or to for , which is fully robust. Therefore, is consistent when the OR model (1) for the corresponding is correctly specified. This result would not hold when were defined with in place of .

Local efficiency. For or 1, the estimator is locally nonparametric efficient, similarly as or . In addition, is generally not locally semiparametric efficient with respect to PS model (2), but locally semiparametric efficient with respect to PS model (5): achieves the semiparametric efficiency bounded calculated under model (5), when both model (1) and model (2) are correctly specified. In fact, when model (2) holds, the efficiency bound under model (5) coincides with the nonparametric efficiency bound , because is a linear combination of the score function, which contains under model (5) as shown in Appendix I. On the other hand, with replaced by throughout would be locally semiparametric efficient with respect to the original PS model (2), but generally not doubly robust, similarly as .

Intrinsic efficiency. A classical estimator of the optimal choice of in minimizing the asymptotic variance of (7) is , which differs from in a subtle manner. It can be shown that the corresponding estimator, , for is asymptotically equivalent to the first order to when the PS model is correctly specified. But , unlike , is generally inconsistent for , even when the OR model is correctly specified and the PS model may be misspecified. The particular form of , although seems ad hoc in the above definition, can also be derived through empirical efficiency maximization (Rubin & van der Laan 2008; Tan 2008) and design-optimal regression estimation for survey calibration (Tan 2013). See further discussion related to calibration estimation after Proposition 6.

The advantage of achieving intrinsic efficiency is shown by the following comparison, where , , and, as discussed below (8), , are obtained from , , and with replaced by .

Corollary 3

A technical complication of using augmented propensity scores is that may not, in general, be intrinsically efficient, when compared to the class of estimators (7) with replaced by in and . [Nevertheless, such intrinsic efficiency holds in the special case with , where the OR model (1) for is linear regression with all variables in also included in .] Particularly, if the PS model (2) is correctly specified, then may not be as efficient as based on even though is proven to be asymptotically at least as efficient as based on and, when the OR model (1) for is also correctly specified, asymptotically equivalent to and . However, the increase in the asymptotic variance of over that of is usually small, caused by the use of a slightly augmented PS model (5). The estimator may still often achieve efficiency gains over when the PS model is correctly specified but the OR model is misspecified, as shown in our simulation studies.

4.2 Likelihood estimators

A practical limitation of the regression estimators as well as AIPW estimators is that they may lie outside either the sample or the population range of observed outcomes. For example, may take values outside the interval for binary outcomes. Such behavior may occur due to the presence of fitted propensity scores near 1 or, equivalently, large inverse probability weights among the untreated. In this section, we derive likelihood estimators for that are not only doubly robust, locally nonparametric efficient, and intrinsically efficient similarly to the regression estimators, but also sample-bounded in falling within the range of . These likelihood estimators are therefore much less sensitive to large weights than the regression and AIPW estimators.

There are two steps in constructing the desired likelihood estimators, similarly as for ATE estimation in Tan (2010) but using the fitted propensity scores from augmented PS model (5). First, we derive intrinsically efficient, but non-doubly robust, likelihood estimators by the approach of empirical likelihood (Owen 2001) taking and as asymptotically unbiased estimating functions or, equivalently, the approach of nonparametric likelihood (Tan 2006, 2010). Specifically, our approach is to maximize the log empirical likelihood, , subject to the constraints

where is a nonnegative weight assigned to for with . We show in the Appendix I.4 that the resulting estimates of and are

where and is a maximizer of the function

subject to if and if for . Setting the gradient of to zero shows that is a solution to

| (9) |

Because is a linear combination of variables in , it follows from Eq. (9) that the two denominators, and , in the definitions of and are equal to each other.

The estimator can be shown to be intrinsically efficient among the class of estimators (7) and locally nonparametric efficient, but generally not doubly robust. We introduce the following modified likelihood estimators, to achieve double robustness but without affecting the first-order asymptotic behavior.

For or 1, partition as for a constant matrix and accordingly as , where or if or 1, and consists of the elements of excluding . Moreover, write or 1, or , and or respectively for or 1. Define , where and are obtained from , and is a maximizer of the function

subject to if for . Setting the gradient of to 0 shows that is a solution to

| (10) |

For , the resulting estimator of is

where the second equation holds due to Eq. (10) with included in and , and by the score equation for model (5). The likelihood estimator has several desirable properties as follows.

Proposition 6

The sample-boundedness of holds because if for and by Eq. (10). The double robustness of follows mainly for two reasons: by Eq. (10) with included in , and by Eq. (6) for the augmented PS model (5).

Eq. (10), which underlies both sample-boundedness and double robustness as discussed above, can be connected to calibration estimation using auxiliary information in survey sampling (Deville & Sarndal 1992; Tan 2013). In fact, the inverse weighted average of is matched (or calibrated) with the simple sample average of . This is equivalent to saying that if is replaced by , then the numerator in the definition of yields exactly . A similar property holds for : if is replaced by , then the numerator in the definition of yields exactly . By this relationship, and can be referred to as calibrated regression and likelihood estimators.

5 Extensions and comparisons

To possibly enhance numerical stability and finite-sample performance, we suggest the following versions of and with simplifications of and :

-

(i)

Consider an augmented logistic PS model in place of (5):

(11) where is included as an offset, and and are unknown coefficients. Let be the MLE of , and redefine . In contrast with (5), this model (11) is meaningful even when the original model (2) is non-logistic regression or is obtained by non-maximum likelihood estimation, for example, penalized estimation.

-

(ii)

Redefine , that is, with removed. Then is defined by projection of on a lower-dimensional vector , and is defined by solving a lower-dimensional optimization problem. The dimension reduction may improve numerical stability and finite-sample performance of and .

For concreteness, the resulting estimators and are denoted by and respectively. These simplified estimators can be shown to remain locally nonparametric efficient and doubly robust as in Propositions 5 and 6; they are generally not intrinsically efficient, but are expected to asymptotically nearly as efficient as and when the PS model (2) is correctly specified. Informally, and would be intrinsically efficient if were replaced, in model (11) and the definition of , by with the limit of in probability.

While can be removed from for dimension reduction, we point out that can be extended to include additional functions of for achieving calibration on those variables in addition to . Specifically, let be a vector of known but possibly data-dependent functions of including 1, for example, in the OR model (1) for . Redefine the augmented PS model (11) as

| (12) |

where and are unknown coefficients, and or is the vector of nonconstant variables in or respectively. Redefine with the MLE of for model (12), and redefine with for . Then Eq. (10) in conjunction with the score equation for model (11) leads to calibration equations

| (13) | |||

| (14) |

By the discussion after (8), the resulting estimators and are doubly robust and locally nonparametric efficient under the following condition:

-

(R)

is a linear combination of for .

This condition is satisfied when all variables in including 1 are contained in , and is the identity link in the OR model (1).

In the rest of this section, we compare our calibrated methods and several related methods for estimating ATT, including Qin & Zhang (2008), Hainmueller (2012), Imai & Ratkovic (2014), and Graham et al. (2016). The estimators of in Qin & Zhang (2008) and Graham et al. (2016) are in the form

where are derived such that, similarly to (13)–(14),

Qin & Zhang (2008) studied asymptotic behavior of their estimator under a correctly specified PS model, but did not investigate local efficiency or double robustness or address how should be specified to gain efficiency or robustness over non-augmented IPW estimators. For our current setting, Graham et al. (2016) showed that their estimator of is locally semiparametric efficient with respect to PS model (2) under Condition (R), and doubly robust under the following condition:

- (R+)

These results can be related to our results as follows.

-

(i)

Similarly as discussed after Proposition 5, the semiparametric efficiency bound with respect to model (2) coincides with the nonparametric efficiency bound when model (2) is logistic regression and is a linear combination of . Therefore, under Condition R+, the estimator of Graham et al. (2016) is doubly robust and locally both nonparametric and semiparamtric efficient (see Proposition 2).

-

(ii)

If Condition (R+) holds, then Condition (L) holds and hence reduces to . In this case, our estimators and , while using directly, are not only doubly robust and locally nonparametric efficient, but also intrinsically efficient among the class of estimator (7) with the same as . The estimator of Graham et al. (2016) can be shown to be asymptotically equivalent, to the first order, to some estimator in class (7) under a correctly specified PS model (2). Therefore, under Condition (R+), our estimators are proved to be asymptotically at least as efficient as the estimator of Graham et al. (2016) when the PS model (2) is correctly specified but the OR model (1) is misspecified.

- (iii)

If PS model (2) is logistic regression, then the methods of Hainmueller (2012) and Imai & Ratkovic (2014) seem to use the same estimator of ,

where and is determined from the balancing equation similar to Eq. (13)–(14),

| (15) |

Eq. (15) differs from balancing equations used for ATE estimation in Imai & Ratkovic (2014). The two expressions of follow from the fact that by Eq. (15) with including a constant. That is, can be seen as standard IPW estimators: , where is substituted for with the MLE . Under Condition (L), the estimator can be shown to be doubly robust and locally nonparametric efficient (Zhao & Percival 2017). However, is not intrinsically efficient and hence, similarly to the estimator of Graham et al. (2016), not as efficient as our estimators and when the PS model (2) is correctly specified but the OR model (1) is misspecified.

6 Simulation studies

We conducted two simulation studies to compare the proposed and existing estimators. We present in Appendix II the results under the simulation settings of Kang & Schafer (2007) and McCaffrey et al. (2007). Here we present the results under the simulation settings of Qin & Zhang (2008) and Graham et al. (2016).

The simulation setting of Qin & Zhang (2008) is originally designed in the context of difference-in-differences estimation, but can be equivalently recast for estimation of ATT as shown in Graham et al. (2016). Specifically, suppose that the covariate vector, , is generated as

The true propensity score is generated as a logistic regression function

where , , or , corresponding to increasing selection bias into treatment. The potential outcomes are generated (regardless of for exogenity) as

where and are set in two possible ways:

-

(i)

LIN-OR: , ,

-

(ii)

QUA-OR: , .

It is easily shown that the true value of ATT is always 2, because the regression functions and are parallel to each other.

For estimation of ATT, consider an outcome regression model (1) with the identity link and the regressor vector or , corresponding to a linear or quadratic OR model. Under the LIN-OR setting, the linear or quadratic OR model is, respectively, correctly specified or misspecified. Under the QUA-OR setting, both of the OR models are misspecified, but the quadratic OR model is misspecified to a lesser degree. Similarly, consider a propensity score model (2) with the logistic link and the regressor vector or , corresponding to a logistic linear or quadratic PS model, which is, respectively, correctly specified or misspecified.

We implemented the following estimators of ATT:

-

•

(OR) ;

-

•

(IPW) , (IPW.ratio) ;

-

•

(AIPW) ;

-

•

(LIK) , (LIK2) ;

-

•

(HIR) , (AIPW.HIR) .

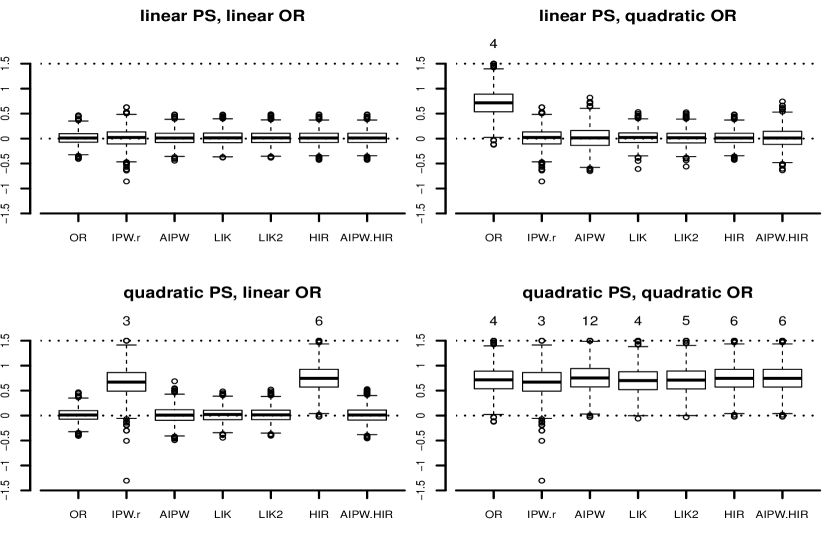

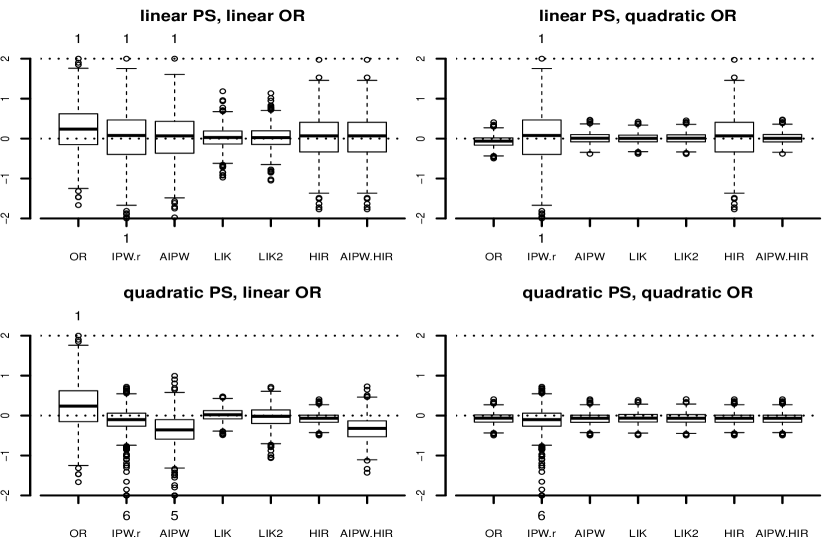

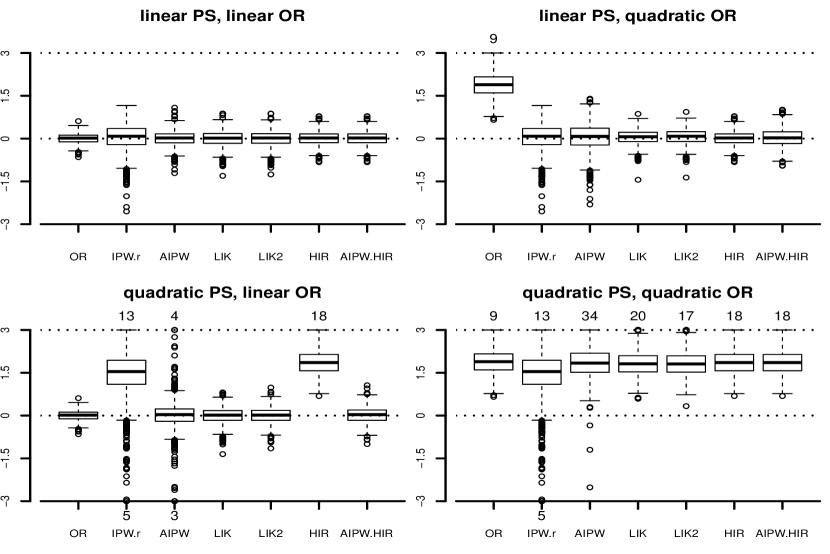

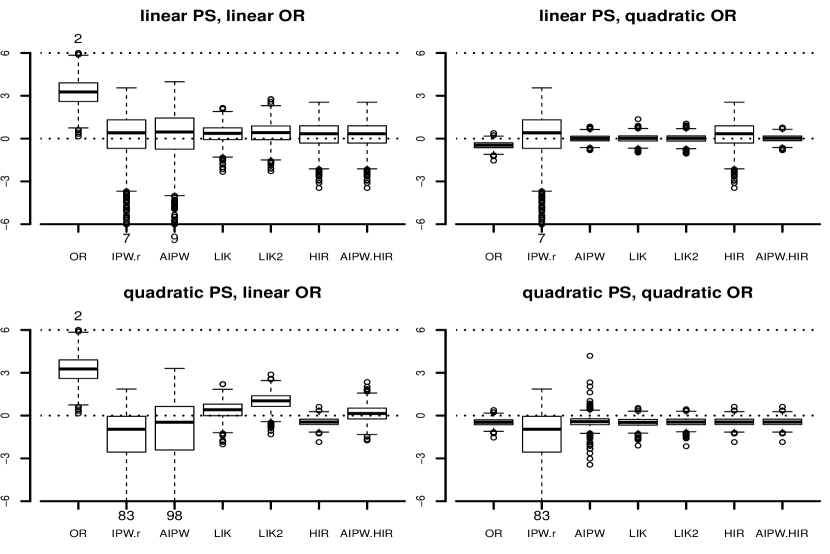

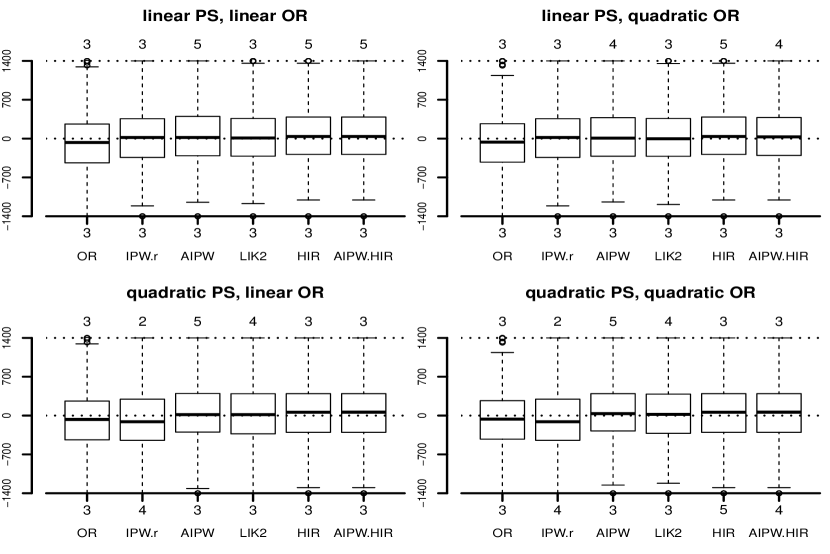

Table 1 and Figures 2-2 present the results for these estimators, from Monte Carlo samples of size , under the PS setting with moderate selection bias, . In addition, results are reproduced under the same setting for two estimators in Qin & Zhang (2008) and Graham et al. (2016). See the Appendix II for the results under the other two PS settings.

The following remarks can be drawn on the comparisons of various estimators. First, the OR estimator is approximately unbiased only when the OR model used is correctly specified (i.e., linear OR model under LIN-OR setting).

Second, the IPW and IPW.ratio estimators are approximately unbiased only when the PS model used is correctly specified (i.e., linear PS model), but they have large variances with noticeably outlying values.

| Models | OR | IPW.r | AIPW | LIK | LIK2 | HIR | AIPW.HIR | EL | AST |

|---|---|---|---|---|---|---|---|---|---|

| Data generated under LIN-OR setting | |||||||||

| linear PS, | 0.0120 | 0.0147 | 0.0125 | 0.0118 | 0.0120 | 0.0123 | 0.0123 | 0.0031 | -0.0065 |

| linear OR | (0.0175) | (0.0358) | (0.0201) | (0.0209) | (0.0208) | (0.0200) | (0.0200) | (0.0275) | (0.0261) |

| linear PS, | 0.7170 | 0.0147 | 0.0139 | 0.0168 | 0.0132 | 0.0123 | 0.0122 | -0.0009 | -0.0039 |

| quadratic OR | (0.0767) | (0.0358) | (0.0500) | (0.0221) | (0.0225) | (0.0200) | (0.0431) | (0.0306) | (0.0371) |

| quadratic PS, | 0.0120 | 0.6655 | 0.0106 | 0.0125 | 0.0105 | 0.7501 | 0.0114 | ||

| linear OR | (0.0175) | (0.0878) | (0.0269) | (0.0212) | (0.0221) | (0.0756) | (0.0244) | ||

| quadratic PS, | 0.7170 | 0.6655 | 0.7644 | 0.7023 | 0.7120 | 0.7501 | 0.7501 | ||

| quadratic OR | (0.0767) | (0.0878) | (0.0828) | (0.0746) | (0.0746) | (0.0756) | (0.0756) | ||

| Data generated under QUA-OR setting | |||||||||

| linear PS, | 0.7028 | 0.0414 | 0.0500 | 0.0471 | 0.0522 | 0.0553 | 0.0553 | 0.0477 | 0.0787 |

| linear OR | (0.4176) | (0.6407) | (0.5201) | (0.0796) | (0.0946) | (0.3683) | (0.3683) | (0.1227) | (0.3620) |

| linear PS, | -0.1473 | 0.0414 | 0.0142 | 0.0120 | 0.0138 | 0.0553 | 0.0144 | 0.0028 | 0.0078 |

| quadratic OR | (0.0238) | (0.6407) | (0.0216) | (0.0224) | (0.0221) | (0.3683) | (0.0223) | (0.0309) | (0.0218) |

| quadratic PS, | 0.7028 | -0.4155 | -0.6468 | 0.0549 | 0.1256 | -0.1554 | -0.4657 | ||

| linear OR | (0.4176) | (0.6381) | (0.6286) | (0.0485) | (0.1044) | (0.0249) | (0.1021) | ||

| quadratic PS, | -0.1473 | -0.4155 | -0.1599 | -0.1465 | -0.1493 | -0.1554 | -0.1554 | ||

| quadratic OR | (0.0238) | (0.6381) | (0.0263) | (0.0272) | (0.0258) | (0.0249) | (0.0249) | ||

Third, the HIR estimator is approximately unbiased when the PS model is correctly specified, but becomes biased when the PS model is misspecified and even when the OR model is correctly specified (for example, quadratic PS model and linear OR model under LIN-OR setting). The HIR estimator is not doubly robust, because Condition L is not satisfied in this situation.

Fourth, the four estimators, AIPW, LIK, LIK2, and AIPW.HIR are doubly robust: they are approximately unbiased when either the PS model is correctly specified (i.e., linear PS model) or the OR model is correctly specified (i.e., linear OR model under LIN-OR setting). In accordance with local efficiency, these estimators have similar variances to each other when both the PS and OR models are correctly specified. But LIK and LIK2 have smaller variances, sometimes substantially so, than AIPW and AIPW.HIR estimators when the PS model is correctly specified but the OR model is misspecified. For example, for linear PS model and linear OR model under QUA-OR setting, the variance of LIK is smaller than that of AIPW by a factor of and that of AIPW.HIR by a factor of . Such differences are supported by our theoretical results on intrinsic efficiency.

|

|

Fifth, in contrast with AIPW and AIPW.HIR, the LIK estimator appears to be approximately unbiased when the quadratic PS model and linear OR model are used under the QUA-OR setting (hence both PS and OR models are misspecified). This behavior is not indicated by general theory, but can be explained by the fact that even though the PS model (2) is misspecified, the augmented PS model (5) happens to be correctly specified in this case: provide exactly the correct regressors up to linear transformation.

Finally, we compare our likelihood estimators with the estimators in Qin & Zhang (2008) and Graham et al. (2016) when the PS model is correctly specified (i.e., linear PS model). Results for a misspecified PS model were not available in these previous simulation studies. Similarly as in the comparisons with AIPW and AIPW.HIR, our likelihood estimators have smaller variances than those in Qin & Zhang and Graham et al. when the PS model is correctly specified but the OR model is misspecified. For example, for linear PS model and linear OR model under QUA-OR setting, the variance of LIK is smaller than that of Qin & Zhang by a factor of and that of Graham et al. by a factor of . Another interesting observation is that when the OR model is also correctly specified or approximately so, our likelihood estimators and Graham et al. have similar variances, but smaller than that of Qin & Zhang estimator, indicating a lack of local efficiency for the latter estimator. For example, the factor of efficiency gain is for linear PS model and quadratic OR model under the QUA-OR setting.

7 Analysis of LaLonde data

NSW (“National Supported Work Demonstration”) is a randomized job training program implemented in 1970s to provide work experience for individuals who had economic and social disadvantages. The randomized experiment provides benchmark estimates of average treatment effects. To study econometric methods for program evaluation with non-experimental data, LaLonde (1986) constructed an observational study by replacing the data from the experimental control group with survey data from either Current Population Survey (CPS) or the Panel Study of Income Dynamics (PSID). The question of interest is how well the experimental benchmark estimates of average treatment effects can be recovered by econometric methods when applied to such composite observational studies. LaLonde (1986) showed that many commonly used methods failed to replicate the experimental results.

Analysis of LaLonde’s composite data has since been extensively discussed in the evaluation and causal inference literature. Dehejia & Wahba (1999, 2002) obtained effect estimates that have low biases from the experimental benchmark, while applying propensity score matching methods to a particular subsample of LaLonde’s original data. Smith & Todd (2005a) raised the criticism that the propensity score matching estimates are highly sensitive to both the analysis sample used and the specification of propensity score models. They calculated direct estimates of the bias by applying matching to the experimental control group and a non-experimental comparison group (either CPS or PSID), whereas LaLonde and Dehejia & Wahba calculated the bias by applying matching to the experimental treatment group and a non-experimental comparison group and then comparing the resulting estimate to the experimental benchmark. See Diamond & Sekhon (2013), Hainmueller (2012), and Imai & Ratkovic (2014), among others, for more recent analyses.

We investigate the performances of the proposed and existing estimators for analyzing LaLonde’s original composite data. Specifically, we apply various estimators of ATT as listed in Section 6 in the following analyses:

-

•

Analysis (i): NSW experimental treatment group is combined with either CPS or PSID non-experimental comparison group for effect estimation or, equivalently, for bias estimation by subtracting the experimental benchmark from all effect estimates;

-

•

Analysis (ii): NSW experimental control group is combined with either CPS or PSID non-experimental comparison group for bias estimation.

For each application, we consider two possible PS models and two possible OR models, as specified in Table 3. The quadratic PS model differs, only by a few terms, from the PS model obtained in an iterative model-building approach by Dehejia & Wahba (2002) for analyzing NSWCPS or NSWPSID composite data.

For propensity score estimation, we use either the experimental treatment group in (i) or experimental control group in (ii) as treated observations () and the non-experimental comparison group as untreated observations (). This strategy is in line with LaLonde (1986) and Dehejia & Wahba (1999, 2002), but differs from Smith & Todd (2005a) and Imai & Ratkovic (2014). In the latter articles, both the experimental treatment and control groups are used as treated observations () when estimating propensity scores, but then either the experimental treatment or control group is used in, respectively, effect or bias estimation. This scheme does not mimic the practical situation of econometric analysis where a single dataset is used, and may not even be desirable as discussed in Dehejia (2005b).

Before turning to our results, we provide some remarks to explain how the relative performances of estimators will be assessed from such empirical results. First, as discussed in Dehejia (2005a) in response to Smith & Todd (2005a), applications of propensity score methods should involve searching for a propensity score model that leads to balance of covariates between treatment groups. The approach suggested in Rosenbaum & Rubin (1984) and Dehejia & Wahba (1999, 2002) is conceptually useful but leaves open the issue of how PS models can actually be built to achieve covariate balance. Alternatively, simple PS models such as in Table 3 may often be used in applied research. Second, Smith & Todd (2005b) presented additional analyses in response to Dehejia (2005a) to argue that the low-bias matching estimates in Dehejia & Wahba (1999, 2002) are sensitive not only in regard to the sample and propensity score specification as shown in Smith & Todd (2005a), but also, among other factors, to whether the propensity score and subsequently the bias are estimated using the experimental treatment or control group, as in Analyses (i) and (ii) described above. Third, a criterion typically used in previous analyses of LaLonde data is that the bias estimates should be close to 0 for a good method. But the true bias can be 0 only when the exogeneity assumption (A1) holds on the composite sample, i.e., potential outcomes are influenced by the measured covariates in the experimental sample in the same way as in the comparison sample (CPS or PSID). Nevertheless, the difference between the two bias estimates from Analyses (i) and (ii), as examined in Smith & Todd (2005b), can be shown to be 0 (up to random variation) even when the exogeneity assumption (A1) fails on the composite sample. See Appendix I.7 for details. By all the preceding considerations, we will assess the relative performances of estimators mainly in terms of how close the two bias estimates from Analyses (i) and (ii) are to each other, depending on PS and OR models used.

| Name | Regressors in PS model or in OR model |

|---|---|

| Linear | |

| Quadratic |

Note: The variables are defined as in Table 2 of Dehejia & Wahba (2002). The PS model is with logistic link. The OR model is with identity link.

| OR | IPW.ratio | AIPW | LIK2 | HIR | AIPW.HIR | ||

| Linear PS, Linear OR | Treatment Effect | -1690 | 901 | 1109 | 555 | 475 | 475 |

| (650) | (781) | (852) | (616) | (598) | (598) | ||

| Evaluation Bias | -2941 | -6 | 337 | -211 | -118 | -118 | |

| (636) | (764) | (815) | (523) | (496) | (496) | ||

| Difference | 1251 | 907 | 772 | 765 | 594 | 594 | |

| (590) | (669) | (757) | (563) | (549) | (549) | ||

| Linear PS, Quadratic OR | Treatment Effect | -1577 | 901 | 613 | 378 | 475 | 441 |

| (803) | (781) | (729) | (613) | (598) | (601) | ||

| Evaluation Bias | -2674 | -6 | -7 | -365 | -118 | -177 | |

| (807) | (764) | (653) | (529) | (496) | (501) | ||

| Difference | 1096 | 907 | 620 | 743 | 594 | 618 | |

| (610) | (669) | (641) | (560) | (549) | (553) | ||

| Quadratic PS, Linear OR | Treatment Effect | -1690 | 901 | 1216 | 573 | 393 | 477 |

| (650) | (799) | (896) | (623) | (606) | (601) | ||

| Evaluation Bias | -2941 | -9 | 451 | -236 | -254 | -142 | |

| (636) | (791) | (862) | (537) | (505) | (498) | ||

| Difference | 1251 | 910 | 765 | 809 | 647 | 618 | |

| (590) | (685) | (804) | (560) | (556) | (547) | ||

| Quadratic PS, Quadratic OR | Treatment Effect | -1577 | 901 | 571 | 332 | 393 | 393 |

| (803) | (799) | (742) | (618) | (606) | (606) | ||

| Evaluation Bias | -2674 | -9 | -27 | -429 | -254 | -254 | |

| (807) | (791) | (666) | (531) | (505) | (505) | ||

| Difference | 1096 | 910 | 598 | 761 | 647 | 647 | |

| (610) | (685) | (651) | (560) | (556) | (556) |

Note: In the upper rows are the bootstrap means, and in the brackets are the corresponding bootstrap standard errors. Treatment Effect is obtained from Analysis (i), and Evaluation Bias from Analysis (ii). The difference is to be compared with the experimental benchmark $886 with standard error $488. To tackle numerical non-convergence when computing estimates during bootstrapping, the following procedure is used. We performed Principle Component Analysis to the regressors from the composite data, NSW (treatmentcontrol) PSID, and dropped principle components whose sample variances are less than of the component with the largest sample variance. Then we resampled the entire composite dataset and conducted Analyses (i) and (ii) on each bootstrap sample.

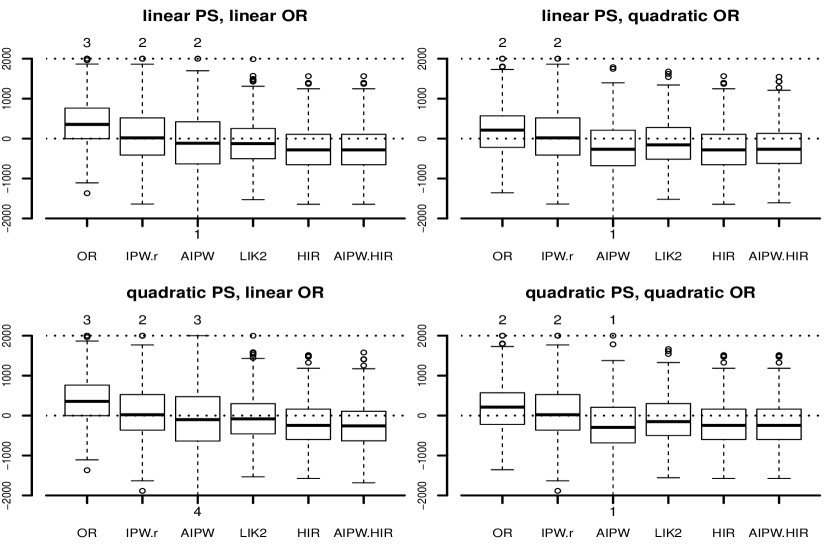

Table 3 and Figure 3 present the results from Analyses (i) and (ii) for various estimators as listed in Section 6, based on 500 bootstrap samples of the NSWPSID composite data. See the Appendix III for the results on the NSWCPS composite data, where the relative performances of estimators are more similar to each other than on the NSWPSID composite data.

Among all estimators studied, the IPW.ratio estimator yields point estimates of effect closest to the experimental benchmark $886 and estimates of bias closest to 0 from Analyses (i) and (ii), using either the linear or quadratic PS model. But the bootstrap variances for IPW.ratio are among the highest for all estimators studied. Although such point estimates of effect are much closer to the experimental benchmark than various previously obtained estimates on LaLonde NSWPSID data (e.g., Diamond & Sekhon 2013; Imai & Ratkovic 2014), these results may not present real evidence for any advantage of IPW.ratio for reasons discussed above.

In terms of how close the difference between effect and bias estimates is to the experimental benchmark (i.e., how close the two bias estimates are close to each other) from Analyses (i) and (ii), the estimators IPW.ratio, AIPW, and LIK2 yield the most accurate point estimates among all estimators studied, regardless of PS and OR models used. But the bootstrap variances for LIK2 are much smaller than those of IPW.rato and AIPW. As explained above, these results present strong evidence for the advantage of the proposed estimator LIK2.

|

8 Conclusion

We study the problem of estimating ATTs from observational data and make the following contributions. In spite of non-ancillarity of the propensity score, we show how efficient influence functions from semiparametric theory can be harnessed to derive AIPW estimators that are locally efficient and doubly robust. Furthermore, we develop calibrated regression and likelihood estimators that achieve desirable properties in efficiency and boundedness beyond local efficiency and double robustness. From two simulation studies and reanalysis of LaLonde (1986) data, the proposed methods perform overall the best compared with various existing methods.

The ideas developed in this article can be extended in various directions. For example, it is interesting to consider marginal and nested structural models for ATTs in subpopulations, i.e., with some selected covariates , and develop calibrated regression and likelihood estimators. Moreover, as seen from Graham et al. (2016), estimation of ATT can be put in a broader class of data combination problems. The methods developed here can be extended in that direction.

References

- Abadie (2005) Abadie, A. (2005). Semiparametric difference-in-differences estimators. Review of Economic Studies, 72:1–19.

- Cao et al. (2009) Cao, W., Tsiatis, A. A., and Davidian, M. (2009). Improving efficiency and robustness of the doubly robust estimator for a population mean with incomplete data. Biometrika, 96:723–734.

- Chen et al. (2008) Chen, X., Hong, H., and Tarozzi, A. (2008). Semiparametric efficiency in GMM models with auxiliary data. The Annals of Statistics, 36:808–843.

- Cochran (1977) Cochran, W. G. (1977). Sampling Techniques. John Wiley & Sons, 3 edition.

- Dehejia (2005a) Dehejia, R. (2005a). Practical propensity score matching: A reply to Smith and Todd. Journal of Econometrics, 125:355–364.

- Dehejia (2005b) Dehejia, R. (2005b). Does matching overcome LaLonde’s critique of nonexperimental estimators? A postscript. Manuscript.

- Dehejia & Wahba (1999) Dehejia, R. and Wahba, S. (1999). Causal effects in nonexperimental studies: Reevaluating the evaluation of training programs. Journal of the American Statistical Association, 94:1053–1062.

- Dehejia & Wahba (2002) Dehejia, R. and Wahba, S. (2002). Propensity score-matching methods for nonexperimental causal studies. The Review of Economics and Statistics, 84:151–161.

- Deville & Sarndal (1992) Deville, J.-C. and Sarndal, C.-E. (1992). Calibration estimators in survey sampling. Journal of the American Statistical Association, 87:376–382.

- Diamond & Sekhon (2013) Diamond, A. and Sekhon, J. S. (2013). Genetic matching for estimating causal effects: A general multivariate matching method for achieving balance in observational studies. The Review of Economics and Statistics, 95:932–945.

- Graham et al. (2016) Graham, B. S., de Xavier Pinto, C. C., and Egel, D. (2016). Efficient estimation of data combination models by the method of auxiliary-to-study tilting (AST). Journal of Business and Economic Statistics, 34:288–301.

- Hahn (1998) Hahn, J. (1998). On the role of the propensity score in efficient semiparametric estimation of average treatment effects. Econometrica, 66:315–331.

- Hainmueller (2012) Hainmueller, J. (2012). Entropy balancing for causal effects: A multivariate reweighting method to produce balanced samples in observational studies. Political Analysis, 20:25–46.

- Hammersley & Handscomb (1964) Hammersley, J. M. and Handscomb, D. C. (1964). Monte Carlo Methods. Methuen.

- Heckman et al. (1997) Heckman, J. J., LaLonde, R. J., and Smith, J. A. (1997). Matching as an econometric evaluation estimator: Evidence from evaluating a job training program. Review of Economic Studies, 64:605–654.

- Heckman & Robb (1985) Heckman, J. J. and Robb, R. (1985). Alternative methods for evaluating the impact of interventions. In Heckman, J. J. and Singer, B., editors, Longitudinal Analysis of Labor Market Data, pages 156–246. Cambridge University Press, New York.

- Hirano et al. (2003) Hirano, K., Imbens, G. W., and Ridder, G. (2003). Efficient estimation of average treatment effects using the estimated propensity score. Econometrica, 71:1161–1189.

- Imai & Ratkovic (2014) Imai, K. and Ratkovic, M. (2014). Covariate balancing propensity score. Journal of the Royal Statistical Society, 76:243–263.

- Imbens (2004) Imbens, G. W. (2004). Nonparametric estimation of average treatment effects under exogeneity: A review. Review of Economics and Statistics, 86:4–29.

- Kang & Schafer (2007) Kang, J. D. Y. and Schafer, J. L. (2007). Demystifying double robustness: a comparison of alternative strategies for estimating a population mean from incomplete data (with discussions). Statistical Science, 22:523–539.

- LaLonde (1986) LaLonde, R. J. (1986). Evaluating the econometric evaluations of training programs with experimental data. The American Economic Review, 76:604–620.

- McCaffrey et al. (2004) McCaffrey, D. F., Ridgeway, G., and Morral, A. R. (2004). Propensity score estimation with boosted regression for evaluating causal effects in observational studies. Psychological Methods, 9:403–425.

- McCaffrey et al. (2007) McCaffrey, D. F., Ridgeway, G., and Morral, A. R. (2007). Comment: Demystifying double robustness: A comparison of alternative strategies for estimating a population mean from incomplete data. Statistical Science, 22:540–543.

- Newey (1990) Newey, W. K. (1990). Semiparametric efficiency bounds. Journal of Applied Econometrics, 5:99–135.

- Neyman (1923) Neyman, J. (1923). On the application of probability theory to agricultural experiments: Essay on principles, Section 9. Statistical Science, 5:465–472.

- Owen (2001) Owen, A. B. (2001). Empirical Likelihood. Chapman & Hall/CRC.

- Qin & Zhang (2008) Qin, J. and Zhang, B. (2008). Empirical-likelihood-based difference-in-differences estimators. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 70:329–349.

- Robins & Ritov (1997) Robins, J. M. and Ritov, Y. (1997). Toward a curse of dimensionality appropriate (CODA) asymptotic theory for semi-parametric models. Statistics in Medicine, 16:285–319.

- Robins & Rotnitzky (2001) Robins, J. M. and Rotnitzky, A. (2001). Comment on the Bickel and Kwon article, ‘Inference for semiparametric models: Some questions and an answer’. Statistica Sinica, 11:920–936.

- Robins et al. (1994) Robins, J. M., Rotnitzky, A., and Zhao, L. P. (1994). Estimation of regression coefficients when some regressors are not always observed. Journal of the American Statistical Association, 89:846–866.

- Rosenbaum & Rubin (1983) Rosenbaum, P. R. and Rubin, D. B. (1983). The central role of the propensity score in observational studies for causal effects. Biometrika, 70:41–55.

- Rosenbaum & Rubin (1984) Rosenbaum, P. R. and Rubin, D. B. (1984). Reducing bias in observational studies using subclassification on the propensity score. Journal of the American Statistical Association, 79:516–524.

- Rubin (1974) Rubin, D. B. (1974). Estimating causal effects of treatments in randomized and nonrandomized studies. Journal of Educational Statistics, 66:688–701.

- Rubin & van der Laan (2008) Rubin, D. B. and van der Laan, M. J. (2008). Empirical efficiency maximization: Improved locally efficient covariate adjustment in randomized experiments and survival analysis. International Journal of Biostatistics, 4:1557–4679.

- Smith & Todd (2005a) Smith, J. and Todd, P. (2005a). Does matching overcome lalonde’s critique of nonexperimental estimators? Journal of Econometrics, 125:305–353.

- Smith & Todd (2005b) Smith, J. and Todd, P. (2005b). Rejoinder. Journal of Econometrics, 125:365–375.

- Stoczynski & Wooldridge (2014) Stoczynski, T. and Wooldridge, J. (2014). A general double robustness result for estimating average treatment effects. IZA Discussion Paper. No. 8084.

- Tan (2006) Tan, Z. (2006). A distributonal approach for causal inference using propensity score. Journal of the American Statistical Association, 101:1619–1637.

- Tan (2007) Tan, Z. (2007). Comment: Understanding or, ps and dr. Statistical Science, 22:560–568.

- Tan (2008) Tan, Z. (2008). Improved local efficiency and double robustness, comment on ‘empirical efficiency maximization: Improved locally efficient covariate adjustment in randomized experiments and survival analysis’ by Rubin and van der Laan. International Journal of Biostatistics, 4:Article 10.

- Tan (2010) Tan, Z. (2010). Bounded, efficient and doubly robust estimation with inverse weighting. Biometrika, 97:661–682.

- Tan (2013) Tan, Z. (2013). Simple design-efficient calibration estimators for rejective and high-entropy sampling. Biometrika, 100:399–415.

- Tsiatis (2006) Tsiatis, A. A. (2006). Semiparametric Theory and Missing Data. Springer Series in Statistics. Springer.

- Zhao & Percival (2017) Zhao, Q. and Percival, D. (2017). Entropy balancing is doubly robust. Journal of Causal Inference, 5:20160010.

Supplementary Material

for “Improved Estimation of Average Treatment Effects on the Treated:

Local Efficiency, Double Robustness, and Beyond” by Shu & Tan

I Technical details

I.1 Preparation

Throughout, we make the following assumptions regarding the estimators for OR model (1), for PS model (2), and for augmented PS model (5), allowing for possible model misspecification (e.g., \citealtappendWhite1982).

-

(C1)

Assume that converges to a constant such that for . Write . If model (1) is correctly specified, then . In general, and may differ from each other.

-

(C2)

Assume that converges to a constant such that

where , and the matrix is nonsingular. Write . If model (2) is correctly specified, then and . In general, and may differ from each other.

- (C3)

In addition, we assume that the following regularity conditions hold (e.g., \citealtappendRobins1994, Appendix B).

-

(C4)

and for .

-

(C5)

There exists such that and for all .

-

(C6)

There exists a neighborhood of such that for , where for any matrix with element .

-

(C7)

There exists a neighborhood of such that and .

-

(C8)

There exists a neighborhood of such that and , with .

We provide the following lemma on asymptotic expansions of AIPW estimators.

Lemma 1

Assume that . If the PS model (2) is correctly specified, then the following results hold.

-

(i)

admits the asymptotic expansion,

where .

-

(ii)

Define . Then admits the asymptotic expansion,

where .

Proof of Lemma 1. By direct calculation and Slutsky theorem, we have

By a Taylor expansion for about and direct calculation, we have

By similar arguments, we have

Combining the preceding three expansions gives the desired expansion for . Similarly, the expansion for can be shown.

I.2 Proofs of Propositions 2 & 4

First, we show the local nonparametric efficiency of . If both model (1) for and model (2) are correctly specified, then by Slutsky theorem,

The leading term can be reexpressed as

and, by Slutsky theorem, approximated by

which gives the desired result. Alternatively, the result follows from Lemma 1(i) with and the fact that and hence .

Second, we show the double robustness of . If PS model (2) is correctly specified, then and hence

On the other hand, can be reexpressed as

If OR model (1) for is correctly specified, then and hence

Third, we show the local semiparametric efficiency of . If both model (1) for and model (2) are correctly specified, then

by direct calculation and Slutsky theorem. Applying, to the above, Lemma 1(i) with replaced by and yields

The desired results follows because by direct calculation, and the variable is uncorrelated with the score and hence .

I.3 Proof of Proposition 5

First, it is straightforward to show that , where and , , , and are defined as , , , and respectively but with and in place of and throughout.

Second, we show the local nonparametric efficiency and double robustness of . By the discussion in Section 4.1, it suffices to show that if the OR model (1) for or 1 is correctly specified, then asymptotic expansion (8) holds for the corresponding . By construction, is a linear combination of , that is, for some constant vector . Then also holds for the same vector . If model (1) for holds, then and hence . By direct calculation, we have

and hence asymptotic expansion (8) holds for . Similarly, because is a linear combination of , it can be shown that if the OR model (1) for is correctly specified, then expansion (8) holds for .

Third, we show the intrinsic efficiency of among the class of estimators (7) for , denoted by . By direct calculation and Slutsky theorem, we have

If PS model (2) is correctly specified, then applying, to the above, Lemma 1(i) with replaced by and yields

where and is decomposed as because is contained in . The first term inside above, , is uncorrelated with the second term, , which is independent of . Moreover, the first term can be expressed as for some constant vector , because, by construction, each variable in is a linear combination of varibles in . By combining these two facts, we see that the asymptotic variance of is achieved when is equal to

But to make equal to , it suffices to set , because is uncorrelated with and hence . If PS model (2) is correctly specified, then . Therefore, is intrinsically efficient among the class of estimators .

Finally, we show the intrinsic efficiency of among the class of estimators (7) for , denoted by . By direct calculation and Slutsky theorem, we have

If PS model (2) is correctly specified, then applying, to the above, Lemma 1(i) with replaced by and yields

where . The intrinsic efficiency of can be similarly obtained as above for the intrinsic efficiency of .

I.4 Derivation of empirical likelihood estimates

The empirical likelihood estimate of is , where are obtained from the constrained maximization problem:

| subject to |

By standard calculation (\citealtappendQinlawless1994), we have

where is a maximizer of the function

Write , , and for . By direct calculation, can be reexpressed as

which equals up to an additive constant. Therefore, is a maximizer of . The desired expressions for and hold because, by direct calculation,

where for .

I.5 Proof of Corollary 3

The simple estimator based on falls in the class (7) for , with . The ratio estimator does not directly fall in the class (7), but can be shown to be asymptotically equivalent to the first order, under a correctly specified PS model, to , which falls in class (7) for becauase is a linear combination of the variables, and , in . The estimator falls in the class (7) for because is a linear combination of the variables, and , included in . The comparison then follows from Proposition 5.

I.6 Proof of Proposition 6

We need only to show that if model (2) is correctly specified, then is asymptotically equivalent, to the first order, to for . By direct calculation and Slutsky theorem, we have

If model (2) is correctly specified, then

by a Taylor expansion for about and the fact that , similarly as in the asymptotic expansion of the calibrated likelihood estimator in \citetappendTan2010. Moreover, if model (2) is correctly specified, then converges to in probability and

by a Taylor expansion for about , similarly as in the asymptotic expansion of the non-calibrated likelihood estimator in \citetappendTan2010. The desired result for then follows from the preceding expansions. Similarly, the result for can be shown.

I.7 Extension with non-logistic PS model

We discuss an extension of the regression and likelihood estimators and when the PS model (2) is non-logistic regression. Consider an augmented PS model

where , , and is the derivative of . For logistic regression, reduces to a constant 1. Let be the estimates of solving the estimating equations

Let , and define the estimators and same as before, except that is defined with

Particularly, to establish intrinsic efficiency, it can be shown that if PS model (2) is correctly specified, then the estimates are asymptotically equivalent to the first order to the MLE of from the following “model,”

where . That is, the random variation in , , and does not affect the asymptotic behavior of to the first order. The proofs of Propositions 5 and 6 can be completed similarly as before.

I.8 Violation of the exogeneity assumption

We present large-sample limits for estimators of ATT when the exogeneity assumption (A1) may be violated, i.e., and may not be conditionally independent given . Similar results are known for estimators of ATE under possible violation of exogeneity assumptions (e.g., \citealtappendRobins1999; \citealtappendTan2006). We mainly use these results to justify how various estimators are compared in our analysis of LaLonde data in Section 7, although the results can be broadly used.

Suppose that the exogeneity ssumption (A1) may be violated. The following results can be shown by similar calculations as under Assumption (A1).

- (i)

-

(ii)

If the PS model (2) is correctly specified, then , , , and converge in probability as to .

In the context of LaLonde analysis, let be the indicator for the NSW cohort, i.e., for the NSW treatment group in Analysis (i) or NSW control group in Analysis (ii) and for the comparison group, and let be the indicator for job training, i.e., for the NSW treatment group and for the NSW control group and the comparison group. Define as the potential outcome that would be observed if an individual was selected into NSW cohort and assigned to treatment, as the potential outcome that would be observed if an individual was selected into NSW cohort and assigned to control, and as the potential outcome that would be observed if an individual was selected into the comparison cohort and hence no job training. It is not necessary that , which would rule out any placebo effect such that earnings could be affected by merely participating in the NSW experiment. The exogeneity assumption (A1), , means that the NSW and comparison cohorts would have similar distributions of of earnings, at each covariate level , if both placed in the comparison cohort and not assigned to job training. This assumption is implicitly made in all previous studies starting from \citeappendLaLonde1986, but can potentially be violated.

Because the NSW treatment and control groups are randomized, the difference

is the experimental benchmark. For Analysis (i) with NSW treatment group combined with a comparison group, a valid ATT estimator should be close to , and the corresponding bias be close to

where . For Analysis (ii) with NSW control group combined with a comparison group, a valid ATT estimator should be close to

Therefore, the two bias estimates separately from Analyses (i) and (ii) should be close to each other for a good method, even when the exogeneity assumption (A1) is violated. This relationship forms the basis in our assessment of relative performances of various estimators of ATT in Section 7.

II Additional simulation results

II.1 Qin–Zhang simulation

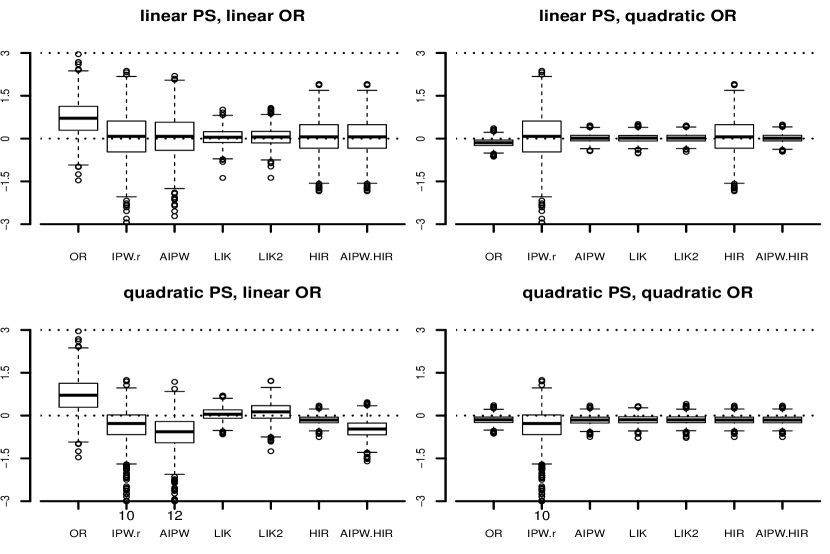

Table S1 and Figures S2-S2 present the results from Monte Carlo samples of size , under the PS setting with small selection bias, . Table S2 and Figures S3-S4 present the results from Monte Carlo samples of size , under the PS setting with large selection bias, .

The relative performances of the estimators under study are similar to those under the PS setting with large selection bias, . In particular, efficiency gains of the calibrated likelihood estimators over the doubly robust estimators, AIPW and AIPW.HIR, remain considerable across these settings, when the PS model is correctly specified but the OR model is misspecified.

| Models | OR | IPW.r | AIPW | LIK | LIK2 | HIR | AIPW.HIR | EL | AST |

|---|---|---|---|---|---|---|---|---|---|

| Data generated under LIN-OR setting | |||||||||

| linear PS, | 0.0070 | 0.0076 | 0.0069 | 0.0062 | 0.0066 | 0.0069 | 0.0069 | 0.0038 | -0.0004 |

| linear OR | (0.0147) | (0.0200) | (0.0153) | (0.0157) | (0.0156) | (0.0153) | (0.0153) | (0.0204) | (0.0154) |

| linear PS, | 0.3551 | 0.0076 | 0.0032 | 0.0072 | 0.0040 | 0.0069 | 0.0032 | 0.0040 | -0.0083 |

| quadratic OR | (0.0562) | (0.0200) | (0.0320) | (0.0163) | (0.0185) | (0.0153) | (0.0312) | (0.0241) | (0.0285) |

| quadratic PS, | 0.0070 | 0.3488 | 0.0062 | 0.0072 | 0.0070 | 0.3687 | 0.0063 | ||

| linear OR | (0.0147) | (0.0553) | (0.0176) | (0.0160) | (0.0167) | (0.0557) | (0.0171) | ||

| quadratic PS, | 0.3551 | 0.3488 | 0.3721 | 0.3428 | 0.3516 | 0.3687 | 0.3687 | ||

| quadratic OR | (0.0562) | (0.0553) | (0.0576) | (0.0544) | (0.0541) | (0.0557) | (0.0557) | ||

| Data generated under QUA-OR setting | |||||||||

| linear PS, | 0.2235 | 0.0275 | 0.0291 | 0.0233 | 0.0249 | 0.0302 | 0.0302 | 0.0347 | 0.0009 |

| linear OR | (0.3152) | (0.4034) | (0.3335) | (0.0647) | (0.0730) | (0.2999) | (0.2999) | (0.1561) | (0.3050) |

| linear PS, | -0.0690 | 0.0275 | 0.0094 | 0.0071 | 0.0084 | 0.0302 | 0.0094 | 0.0029 | -0.0011 |

| quadratic OR | (0.0190) | (0.4034) | (0.0173) | (0.0162) | (0.0170) | (0.2999) | (0.0178) | (0.0226) | (0.0168) |

| quadratic PS, | 0.2235 | -0.1398 | -0.3619 | 0.0214 | -0.0387 | -0.0731 | -0.3250 | ||

| linear OR | (0.3152) | (0.1555) | (0.1949) | (0.0241) | (0.0635) | (0.0191) | (0.0906) | ||

| quadratic PS, | -0.0690 | -0.1398 | -0.0742 | -0.0672 | -0.0698 | -0.0731 | -0.0731 | ||

| quadratic OR | (0.0190) | (0.1555) | (0.0193) | (0.0198) | (0.0195) | (0.0191) | (0.0191) | ||

|

|

| Models | OR | IPW.r | AIPW | LIK | LIK2 | HIR | AIPW.HIR | EL | AST |

|---|---|---|---|---|---|---|---|---|---|

| Data generated under LIN-OR setting | |||||||||

| linear PS, | 0.0089 | 0.0323 | 0.0107 | 0.0009 | 0.0030 | 0.0109 | 0.0109 | 0.0051 | 0.0024 |

| linear OR | (0.0280) | (0.2078) | (0.0608) | (0.0733) | (0.0698) | (0.0547) | (0.0547) | (0.0900) | (0.0537) |

| linear PS, | 1.8926 | 0.0323 | 0.0471 | 0.0527 | 0.0665 | 0.0109 | 0.0294 | -0.0089 | 0.0244 |

| quadratic OR | (0.1748) | (0.2078) | (0.2414) | (0.0642) | (0.0663) | (0.0547) | (0.0998) | (0.1103) | (0.1015) |

| quadratic PS, | 0.0089 | 1.3964 | 0.0262 | 0.0026 | 0.0059 | 1.8722 | 0.0169 | ||

| linear OR | (0.0280) | (0.9500) | (0.3731) | (0.0739) | (0.0770) | (0.1931) | (0.0731) | ||

| quadratic PS, | 1.8926 | 1.3964 | 1.8918 | 1.8529 | 1.8459 | 1.8722 | 1.8722 | ||

| quadratic OR | (0.1748) | (0.9500) | (0.4227) | (0.2195) | (0.2220) | (0.1931) | (0.1931) | ||

| Data generated under QUA-OR setting | |||||||||

| linear PS, | 3.2822 | 0.1296 | 0.1560 | 0.3212 | 0.3819 | 0.2428 | 0.2428 | 0.1969 | 0.1943 |

| linear OR | (0.9469) | (3.0404) | (3.7185) | (0.4148) | (0.5712) | (0.9017) | (0.9017) | (0.2647) | (0.7010) |

| linear PS, | -0.4663 | 0.1296 | 0.0077 | 0.0091 | 0.0061 | 0.2428 | 0.0156 | 0.0075 | 0.0095 |

| quadratic OR | (0.0593) | (3.0404) | (0.0657) | (0.0796) | (0.0798) | (0.9017) | (0.0603) | (0.1026) | (0.0549) |

| quadratic PS, | 3.2822 | -1.9909 | -1.9277 | 0.3801 | 0.9864 | -0.4403 | 0.1483 | ||

| linear OR | (0.9469) | (13.0100) | (34.4996) | (0.3366) | (0.3682) | (0.0742) | (0.3204) | ||

| quadratic PS, | -0.4663 | -1.9909 | -0.4319 | -0.4754 | -0.4449 | -0.4403 | -0.4403 | ||

| quadratic OR | (0.0593) | (13.0100) | (0.1954) | (0.0918) | (0.0858) | (0.0742) | (0.0742) | ||

|

|

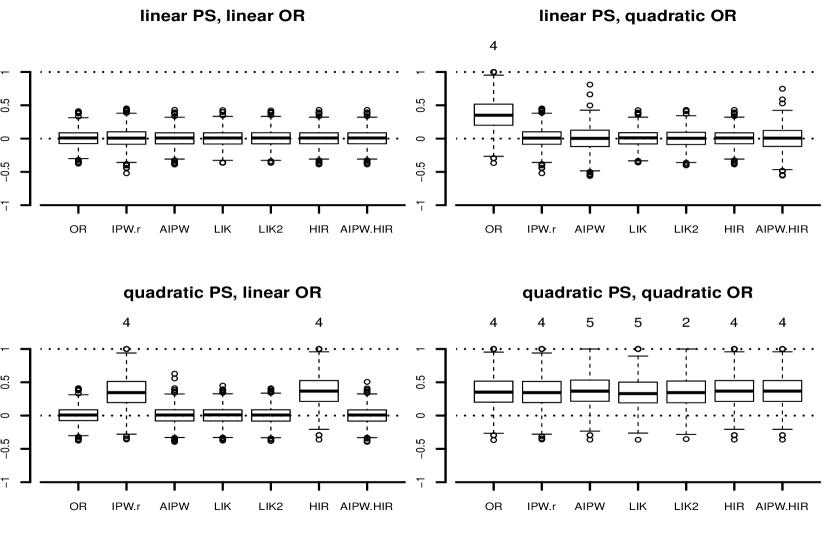

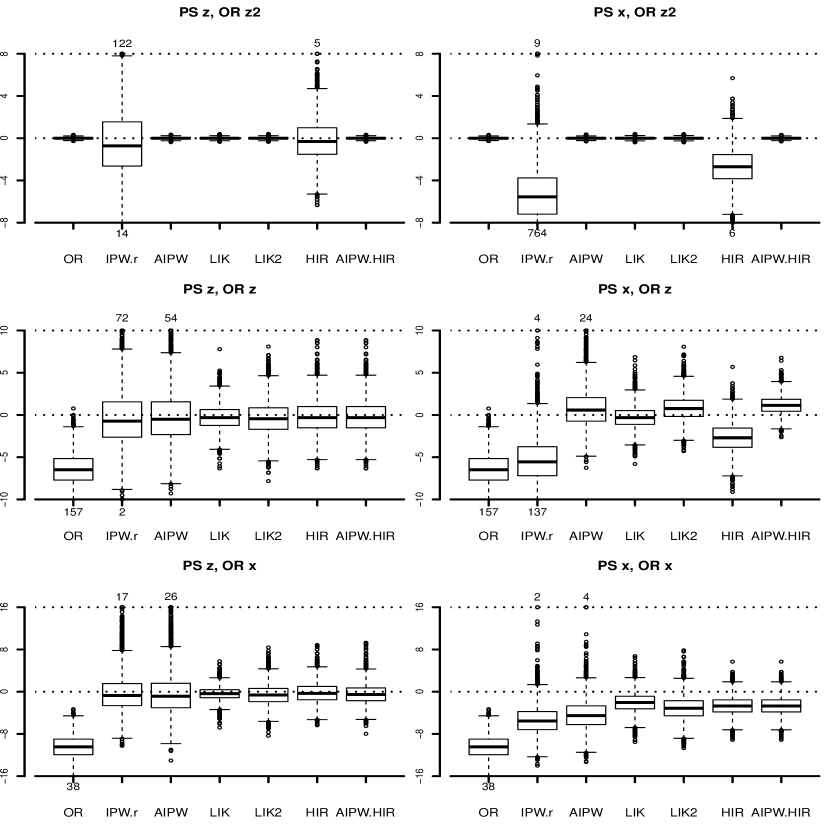

II.2 Kang–Schafer simulation

In addition to the simulation study with the design of \citetappendQin2008, we also conducted a simulation study with the design of \citetappendKS2007 and a modified design defined in \citetappendMcCaffrey2007.